the indian media & entertainment industry 2015 (revision1)

TRANSCRIPT

The Indian Media &

Entertainment Industry

2015

Presentation by

Trends & Analysis - Past, Present & Future

Source: FICCI-KPMG Report 2015

The Indian M&E Industry

The Indian Media & Entertainment Industry includes

Television, Film, Print, Radio, Music, Digital Media, Animation, Gaming,

Events & Live Media, Out-of-home & other ancillary media.

• Valued at over US$

16.2bn (1,02,600Cr INR)

which is 0.9% of the

global M&E industry

(estimated at US$ 1.8tn)

• Its growth (11.7%) is

nearly double the growth

of the global M&E industry

(at 6.1%)

• High-volume, low-value.

580 587652

728

821

918

1026

1160

1330

1532

1740

1964

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

INR

Billio

ns

11.7%

13.9%

Source: FICCI-KPMG Report 2015

Indian M&E Industry – % Breakdown

TV to grow from 46% to 50% market-share by 2019.

Film is expected to drop from 12% in 2008 to 10% in 2018.

Digital is expected double its share of the M&E market in the next 5 years.

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

42% 44% 46% 45% 45% 45% 46% 47% 47% 48% 49% 50%

30%30%

30% 29% 27% 26% 26% 25% 23% 22% 21% 20%

18% 15% 13% 13% 14% 14% 12% 12% 12% 11% 11% 10%

1% 1% 2%2% 2% 2%

2%2% 2%

2% 2% 2%

1% 1% 1%1% 1% 1%

1%1% 1%

1% 1% 1%

3% 2% 2%2% 2% 2%

2%2% 2%

2% 2% 2%

3% 3% 4%4% 4% 4%

4%4% 4%

5% 5% 5%

1% 1% 2% 2% 2% 2%2%

2% 2%2% 2% 2%

1% 1% 2% 2% 3% 3% 4% 5% 6% 8% 8% 8%

TV Print Motion Picture Radio Music OOH Animation & VFX Gaming Digital

Source: FICCI-KPMG Report 2015

The Indian Film Industry

• Largest in the world by

films released theatrically

or tickets sold (over 1,400

films released & over

3.25bn tickets sold)

• 2014 was a year of

introspection when the

‘star-backed’ films

performed average and

the ‘script-backed’ films

did great, marking a

coming of age of

Bollywood.

1913-2000 2000-2004 2004-2010 2010-2014

Production Analog Analog Analog Analog & Digital

Post-Production Analog Digital Digital Digital

Distribution Analog Analog Analog & Digital Analog & Digital

The Digital-isation of the Industry

105

8983

93

113

125 126

136

156

171

186

204

0

50

100

150

200

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

INR

Billio

ns

Film

0.9%

10%

Source: FICCI-KPMG Report 2015

The Indian Film Industry =

‘Bollywood’While‘Bollywood’ is a generally used term to define the Indian Film industry,

Hindi films accounted for only 16% of the 1,400+ films that released.

The South Indian Film industry accounts for almost 50% of the films

Language No of Films

Hindi 234

Tamil 210

Telugu 218

Kannada 157

Malayalam 108

Bengali 139

Marathi 122

Gujrati 67

Bhojpuri 84

Punjabi 9

Others 78

Total 1,426

Source: FICCI-KPMG Report 2015

Film Revenues Breakdown

Domestic Revenues have always accounted for over 90% of the Indian Film

industry’s revenues. The trend is expected to strengthen against International

revenues. This is THE double-edged sword for the industry.

Proving the digital

medium’s

dominance, Ancillary

revenues as a % of

total film revenue

will increase 1.5x

over the next 5

years.

Home Video, like in

the rest of the world,

is dying out fast. 0%

20%

40%

60%

80%

100%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

74% 74% 76% 75% 74% 73% 73% 72% 72% 71%

8% 7% 7% 7% 7% 7% 7% 7% 7% 7%

10% 11% 11% 12% 12% 11% 11% 11% 11% 11%

5% 5% 5% 6% 7% 8% 8% 9% 10% 11%

IN

R B

illio

ns

Film Revenues % Breakdown

Domestic Theatrical Overseas Theatrical Home Video Cable & Satellite Rights Ancillary Revenues

Source: FICCI-KPMG Report 2015

Film – Revenue Split

When you pay Rs 100 for a movie ticket, what is the split?

• Gross – 100% (Rs 100)

• Entertainment Tax – 30% (Rs 30)

• Exhibitor – 50% of balance 70% (Rs 35)

• Distributor – 50% of balance 70% (Rs 35)

• Lead Producer(s) – depends on what deal they have made with

distributor – Outright / MG / Commission

• Co-producer(s) – Last in First out.

• Talent – actors / director – points!

Source: FICCI-KPMG Report 2015

Exhibition needs to grow!

• India has one of the lowest screen

densities among global film markets

• Urgent & rapid infrastructure growth in

multiplex screens is needed

• Since the Box office is not as robust as

other countries, government

intervention is needed by way of SOPs.

125

85 82

61 57

26

137

0

20

40

60

80

100

120

140

Screens/Million

1 1.11.4

1.6 1.61.5

2

2.7

3.5

4.7

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2010 2011 2012 2013 2014

Billio

n $

Domestic Box Office Size

India China

1,000 1,250 1,470 1,650 1,750

6,256

9,200

13,118

18,195

22,000

-

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013 2014

Multiplex Screens

India China

Source: FICCI-KPMG Report 2015

Industry = Value x Volume

No of screens that a film plays in

has grown radically over the past

decade, curbing piracy and

augmenting theatrical revenues

239

127

95

56

0

50

100

150

200

250

300

High EndMultiplex

Multiplex Single Screen Low End SingleScreen

Ticket Rates (INR)

500

1000

3000

4500

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

1994 - HumAapke Hain Koun

2009 - 3 Idiots 2012 - Ek ThaTiger

2013 - Dhoom 3

No of Screens

Average ticket prices of

multiplexes are 3-4 times that of

single screen theatres.

Source: FICCI-KPMG Report 2015

The Indian Film Industry - Key points

• Realisation of the value of Film education. Scale needed. Urgently.

• Script-backed v/s Star-backed.

• Hollywood films account for less than 10% of the Indian Film industry.

• Over-reliance on Domestic Theatrical revenues for mid-range films.

• Increased in-film advertising – Tourism & products

• Increased no of domestic prints – 5000

• Increased no of overseas prints – 2000

• Share of Revenue from first week is highly critical (ranges from 55-

75% of box office collections)

• The industry lacks a globally merchandisable home-grown IP brand.

Source: FICCI-KPMG Report 2015

The Indian Television Industry

• The most consistently

performing sector of the

Indian M&E Industry.

• It is, presently, nearly 4

times the size of the Indian

Film industry and is the

largest employer in the M&E

space.

• India overtook the US in

2014 as the 2nd largest TV-

owning market in the world

(168 million TV households

– 82% penetration).

The potential: The Indian average subscription rate is

US$5-6 per month per TV for Cable TV / DTH against

US$40-100 in evolved markets like US / UK / Europe.

241 257297

329370

417

475

543

631

739

855

975

0

100

200

300

400

500

600

700

800

900

1000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

INR

Billio

ns

TV

13.8%

15.5%

Source: FICCI-KPMG Report 2015

TV Connectivity – A Digital blitz

With digitisation

primarily

successful for

Phase 1 & 2

(over 95%) and

the rest of the

country

underway on

the same path,

digital STBs

and DTH

connections are

the way of the

future. 0

20

40

60

80

100

120

140

160

180

200

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

6574 69 68 70

55

27

5 5 5

5

6 19 2529

45

67

85 90 94

28

31

3437

4048 61 72

7476

8

8

9

9

10

1111

1212

12

Subscribers

Analog Cable Digital Cable DTH Other Digital

Source: FICCI-KPMG Report 2015

TV Connectivity – A Digital blitz

TV households, C&S penetration & ARPUs are all expected to grow

over the next 5 years, enabling distribution-led growth in TV

161 168

196

80%

82%

90%

0

50

100

150

200

250

74%

76%

78%

80%

82%

84%

86%

88%

90%

92%

2013 2014 2019

TV Households (Millions) C&S penetration

175

196

225

248

273

301

200

220

242

266

292

322

150

170

190

210

230

250

270

290

310

330

350

2014 2015 2016 2017 2018 2019

ARPUs

Digital Cable DTH

Source: FICCI-KPMG Report 2015

TV Channels galore!

• Channel growth over

the past 14 years has

been significant. On

an average, India has

added 3.2 channels

per month for the

past 14 years.

• India has more than

400 news channels.

• Channel

differentiation is

weak.

0

100

200

300

400

500

600

700

800

1991 1995 2000 2005 2010 2014

5

55

130

263

550

800

No of Channels

Source: FICCI-KPMG Report 2015

GEC – GRP v/s Profitability

Low GRP High GRP

Low

Profitability

High

Profitability

Long running soaps

Low-cost game /

performance based

reality shows

Mythological series

Recently released movies

Celebrity-based shows

Why do we see what we see on TV?

How do funds available for content creation get allocated between building a viewer

base and then en-cashing on the base?

Source: FICCI-KPMG Report 2015

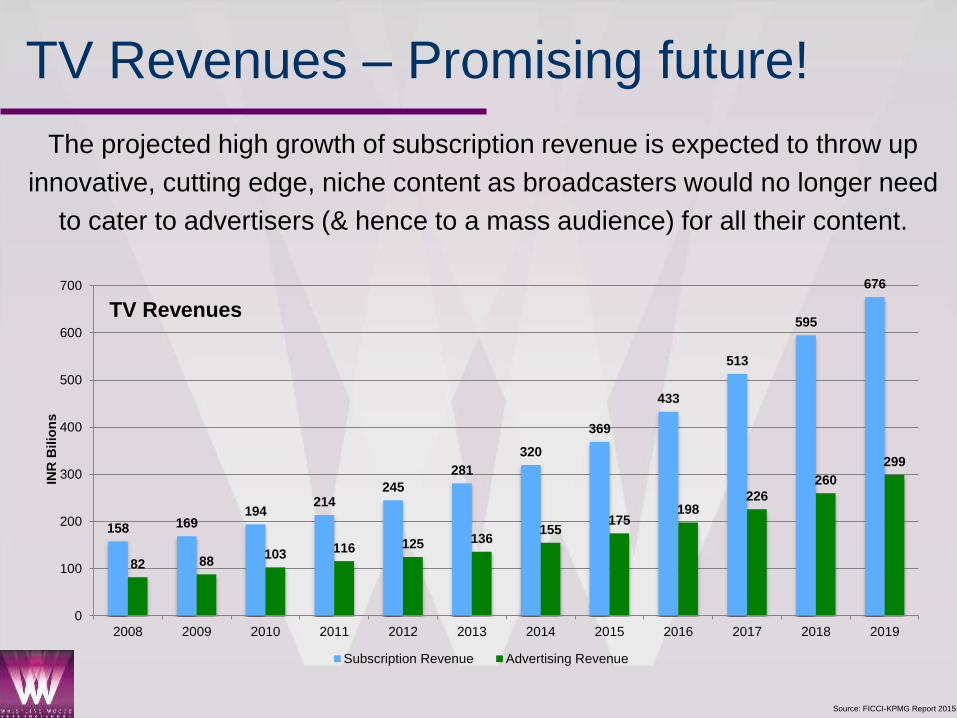

TV Revenues – Promising future!

The projected high growth of subscription revenue is expected to throw up

innovative, cutting edge, niche content as broadcasters would no longer need

to cater to advertisers (& hence to a mass audience) for all their content.

158 169194

214245

281

320

369

433

513

595

676

82 88103 116 125 136

155175

198226

260

299

0

100

200

300

400

500

600

700

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

INR

Bilio

ns

TV Revenues

Subscription Revenue Advertising Revenue

Source: FICCI-KPMG Report 2015

TV Revenue Sharing – A concern!

Of an amount collected of INR 320 billion, ONLY INR 75 billion is reaching

the broadcasters, which is less than 25%. Ideally, it should be in reverse with

only 25-30% being retained by the LCOs, MSOs. However, underreporting of

subscribers, carriage fees & lack of digitisation is the reason for this.

245281

320369

433

513

595

676

57 69 75 90 114 145 174 201

23%25%

23%24%

26%

28%29% 30%

0%

5%

10%

15%

20%

25%

30%

35%

0

100

200

300

400

500

600

700

800

2012 2013 2014 2015 2016 2017 2018 2019

INR

Billio

ns

Subscription Revenue

Paid by Consumers Recd by Broadcasters %

Source: FICCI-KPMG Report 2015

Viewership & Ad-Revenue

Disparity between viewership & Ad Revenue is stark, esp. in the case of English

content. English News has 0.1% viewership but gets a whopping 5.2% of the Ad

Revenue. Similarly, English Entertainment has 1.1% of the viewership but 4.5% of the

Ad Revenue pie. It reflects the SEC & spending capacity of its audience. Regional TV

is heavily discounted in pricing on account of the nature / SEC of its audience.

Source: FICCI-KPMG Report 2015

Indian Animation picks up

• Broadcasters are willing to pay

double for good quality Indian

Animated content as compared to

daily soaps / Hindi general

entertainment content, even though

this segment gets only 7.3% of the

viewership, as compared to 31.1%

for Hindi GECs.

• Also the fact that this segment

continues to be under-indexed, with

only 3.8% ad-revenue share doesn’t

bother broadcasters as this content

has long-tail revenue

• It offers repeat viewing value, multi-

language dubbing value and

merchandising value.

Source: FICCI-KPMG Report 2015

Hindi GEC Fiction content changing. Slowly.

• GECs have finally embraced the

tele-series format with season-

based programming

• The value:volume ratio is reversed

in such programming as compared

to the daily / weekly soaps.

• For the past 20-odd years, the

content has largely mirrored

American programming of the 70s-

80s, with our soaps comparable to

content like the Bold & The

Beautiful, Santa Barbara, Dallas,

etc.

Source: FICCI-KPMG Report 2015

TV – Key Points

• Digitisation – increased revenue for the broadcaster, should lead to

more investment in content (& hence better quality content)

• Global proliferation of Indian-origin content is increasing, albeit for

the Indian diaspora only. This is THE BIG opportunity.

• Indian animation on TV is starting to matter.

• Hindi GECs are exploring new content programming & a changed

value:volume mix in revenue models.

• Lack of quality viewership measurement systems is an issue.

Hopefully, digitisation should resolve this.

Source: FICCI-KPMG Report 2015

Focus: Digital

INR Billions

Digital is expected to triple in industry size in the next 5 years.

Source: FICCI-KPMG Report 2015

The Digital Business – A BLITZ of growth!

• India has the lowest net penetration

among all developing countries and

much lower than the developed ones.

• Despite that, India has more internet

users than the US.

• Increasing cellphone penetration, large

number of low-cost smartphones fuels

this growth.

0

100

200

300

400

500

600

2014 2015 2016 2017 2018 2019

20 22 25 27 30 32

210

273

337

402

469

528

Milio

ns o

f U

sers

Internet Users

Wired Wireless

19%

53%

46%

60%

87%90%

86%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

India Brazil China Russia USA UK Japan

Internet Penetration

0

50

100

150

200

250

300

350

400

450

500

2014 2015 2016 2017 2018 2019

173

232

286

342

399

457

116

188

249

299

369

435

Millio

ns o

f U

sers

Net on Mobile

Net on Mobile Smartphones

21%

Source: FICCI-KPMG Report 2015

Telecom Base – Volume galore!

The overall tele-

density in India was

81.83

Urban tele-density

was 153.45 and

rural teledensity was

49.94

As of December 2015

Telecom Service Providers

Active subscribers

Bharti Airtel 243,289,404

Vodafone 193.600,085

IDEA 171,912,608

Reliance 100,890,431

Aircel 85,632,249

BSNL 82,507,640

Tata 60,727,856

Telenor 50,702,396

Sistema 8,006,814

Videocon 6,958,178

MTNL 3,614,439

Quadrant 3,047,100TOTAL 1,010,889,200

Source: FICCI-KPMG Report 2015

TV v/s Digital

Digital is the medium

for the future.

The web user base is expected to

grow at an incredible 18% annual

growth rate over the next 5 years as

compared to 3% of TV.

AD Spend on Digital platforms is

growing at four times the rate of TV.

825857

886913

938 960

281

348

420

494

570

640

0

100

200

300

400

500

600

700

800

900

1000

2014 2015 2016 2017 2018 2019

Millio

ns o

f U

sers

TV Internet

18%

38.354.8

72.498.6

116.1135.4

5.2

7.7

11.6

16.8

22.1

27.1

0

20

40

60

80

100

120

140

160

180

2014 2015 2016 2017 2018 2019

INR

Billio

ns

Digital Advertising Growth

Web Mobile

30.16%

Source: FICCI-KPMG Report 2015

Digital – Key Points

• The Digital platforms of web, mobile & web-connected smart TVs

are the future.

• Content consumption modes & patterns are already starting to

change with a large number of sub-18-yr-olds are switching to

YouTube to find their new ‘stars’

• YouTube is taking the Indian market very seriously and has set up

a ‘YouTube space’ in India, in partnership with Whistling Woods

International

• YouTube has ‘approved’ a credit-based semester-long training

course for ‘Content Creation, Audience Development &

Monetisation for digital platforms’ developed by Whistling Woods.

Source: FICCI-KPMG Report 2015

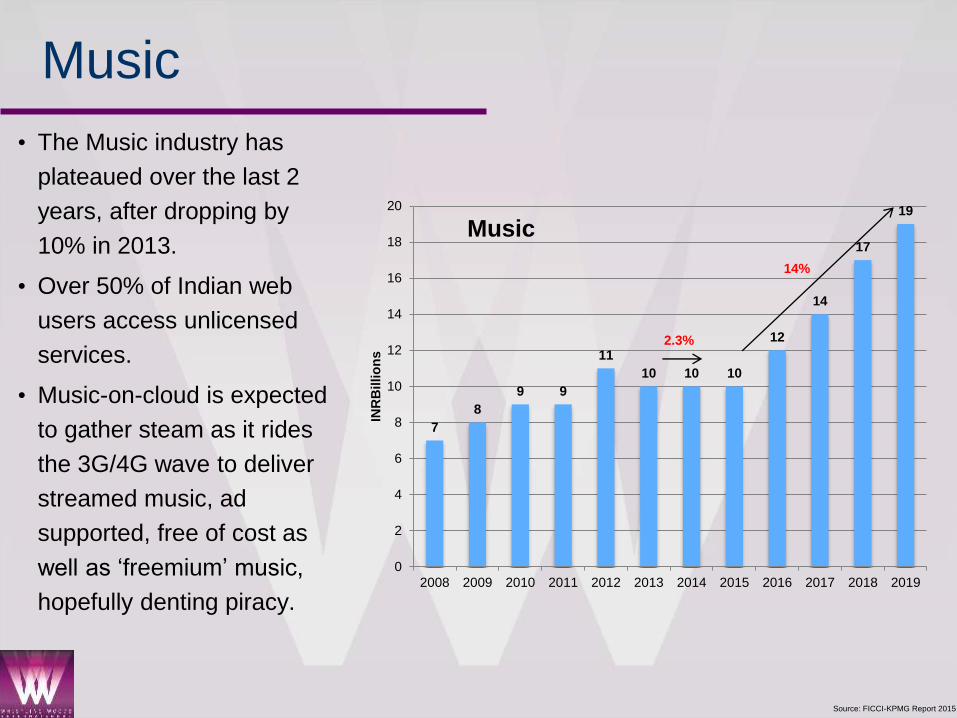

Music

• The Music industry has

plateaued over the last 2

years, after dropping by

10% in 2013.

• Over 50% of Indian web

users access unlicensed

services.

• Music-on-cloud is expected

to gather steam as it rides

the 3G/4G wave to deliver

streamed music, ad

supported, free of cost as

well as ‘freemium’ music,

hopefully denting piracy.

7

8

9 9

11

10 10 10

12

14

17

19

0

2

4

6

8

10

12

14

16

18

20

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

INR

Billio

ns

Music

14%

2.3%

Source: FICCI-KPMG Report 2015

Music - Consumption

• The consumption % reversed

from 2009 to 2014 between

physical & digital.

• Bollywood fuels over 80% of

the Music industry

• Indian non-Bollywood music

(Indie / pop / rock / regional) is

struggling, with only Religious

& Indian Classical music

managing to survive.

• Hardly ANY innovation in

Music, since AR Rahman.

• Hardly any proper music

schools

58%

33%

6%3%

20%

55%

15%

10%

0%

10%

20%

30%

40%

50%

60%

70%

Physical Digital TV & Radio PublicPerformance

Music Consumptionby Source

2009

2014

81.0%

10.0%

4.0%2.2% 2.8%Music Consumption

by Genre

Bollywood

International

South Indian

Punjabi

Others

Source: FICCI-KPMG Report 2015

Gaming

• Grew over 20%, on the back of

mobile gaming.

• With 960 mn+ users & a young

population, India is one of the

fastest growing mobile gaming

markets in the world

7 810

1315

19

24

28

32

35

40

46

0

5

10

15

20

25

30

35

40

45

50

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

INR

Billio

ns

Gaming14.3%

46% 49% 51% 52% 55% 57%

39% 35% 32% 30% 28% 26%

15% 16% 17% 18% 18% 17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2015 2016 2017 2018 2019

Mobile Console PC & Online

22.4%

Source: FICCI-KPMG Report 2015

Radio

• Small industry size, primarily

on account of restriction of

content by the government (no

news radio, talk radio allowed)

• Hence every FM radio station

sounds the same.

• The growth in 2014 has been

built around increased ad-ex

by e-commerce, real estate

and retail.

• The shift to radio is as it is a

cost-effective advertising

vehicle, as compared to TV.

8 810 11

1315

17

2022

27

33

40

0

5

10

15

20

25

30

35

40

45

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

INR

Billio

ns

Radio18.1%

17.6%

21266

401

1232

12 98167

431

0

200

400

600

800

1000

1200

1400

Phase 1 (1990s) Phase 2 (2006-07)

Phase 3 - 1(2015)

Phase 3 - 2(2015-16)

Licences available Cities

Source: FICCI-KPMG Report 2015

Animation, VFX & Post-Production

• The industry has shown decent

growth, on the back of VFX / post-

prodn, not Animation.

• Increased consumption of VFX &

digital post production in Film & TV.

• Lack of original IP creation is a major

reason of the stagnation of the

Animation industry.

18 2024

3135

4045

51

59

69

81

96

0

10

20

30

40

50

60

70

80

90

100

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

INR

Billio

ns

Animation & VFX16.3%

13.1%

1 1

2 2

4

6

1

4

1

5

3 3

0

1

2

3

4

5

6

7

1992 2000 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Animated Films Released Theatrically

Source: FICCI-KPMG Report 2015

Animation, VFX & Post-Production

The industry has split with itself, with the Animation industry tanking and

the VFX / post-prodn growing.

From a 60:40 ratio in 2010, the industry reaches a 80:20 ratio in 2019.

26% 23% 22% 20% 18% 16% 15% 14% 13% 12%

16%

14%13%

12%11%

11%10% 9% 9% 8%

19%

20% 22% 23%25% 27% 29% 30% 32% 34%

38%44% 44% 45% 45% 46% 46% 46% 46% 46%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Animation Services Animation Product Creation VFX Post-Prodn

Source: FICCI-KPMG Report 2015

Animation on Indian Screens

Only 3 out of the top-10 characters on Indian TV are of Indian origin!

Source: FICCI-KPMG Report 2015

Jobs in M&E

• By 2022, as per the NSDC, the

Media & Entertainment industry

would be requiring 12.9 lakh

skilled professionals, over 80% of

these in the Film & TV vertical.

• The media industry as a whole still

lacks sufficient world-class

training facilities to enable

professionalism and best

practices.

• Significant government-

intervention and private

investments will be needed to

correct this imbalance

1.60 2.40

4.40

1.40

2.80

6.40

0.60 0.70

1.30

0.20 0.30 0.40 0.20 0.30 0.40

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

2014 2017 2022

EmploymentGrowth

Film

TV

Radio

Animation,VFX, Gaming

Source: FICCI-KPMG Report 2015

What are the pain-points of the Indian M&E Industry?

• Lack of original Intellectual Property creation leading to lack of a globally

merchandisable brand.

• M&E Education & Training

o Of the 4 lakh people employed, nearly 75% involved in content creation have

no formal training.

o Very few world-class Film & Media institutes with a combined output of

approx 500 graduates a year, with 200 of them being from a single institute.

• Innovation – we are followers, not leaders when it comes to formats or

technical / narrative innovation.

• Piracy - Affects every sector of the industry & causes nearly 35%

revenue reduction

Source: FICCI-KPMG Report 2015

The Great Opportunities in M&E

• Digital – with an increasing youth population who are open to new

platforms and new content ideas, the next generation of Indian

consumers are ready and waiting for content for the digital

platforms.

• In the M&E industry, building volume is hard. India already has the

volume. We now need to build value to each unit of the already

existing volume. This is done by enhancing quality. The best way to

build quality is be educating & training the industry.