the it spending report - bus.umich.edu · the it spending report ... may be used to forecast the...

TRANSCRIPT

The

IT SpendingReportTM

November 2001

www.emarketer.com

This report is the property of eMarketer, Inc. and is protected under both the United States Copyright Act and by contract.Section 106 of the Copyright Act gives copyright owners the exclusive rights of reproduction, adaptation, publication,performance and display of protected works.

Accordingly, any use, copying, distribution, modification, or republishing of this report beyond that expressly permitted byyour license agreement is prohibited. Violations of the Copyright Act can be both civilly and criminally prosecuted andeMarketer will take all steps necessary to protect its rights under both the Copyright Act and your contract.

If you are outside of the United States: copyrighted United States works, including the attached report, are protected underinternational treaties. Additionally, by contract, you have agreed to be bound by United States law.

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

3

The IT Spending Report

Table of Contents 3

Methodology 7

The eMarketer Methodology: Making Sense of the Numbers 8

The eMarketer Difference 8

What Benefits Do eMarketer Reports Provide? 9

I Worldwide IT Spending 11

A. Introduction 12

B. Worldwide IT Spending Forecasts 12

C. Worldwide IT Spending Growth Rates 18

D. Worldwide IT Spending by Category 21

Telecommunications Spending 25

Hardware Spending 27

Software Spending 32

IT Services Spending 36

E-Business/Internet Technology Spending 42

II North America 47

A. North American IT Spending Forecasts 48

B. Impact of the September 11th Terrorist Attacks 52

C. IT Budgeting in North America 55

D. Information Technology’s Place in the US Economy 56

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

4

The IT Spending Report

III Europe 61

A. European IT Spending Forecasts 62

B. IT Spending Growth Rates in Europe 67

C. IT Budgeting in Europe 70

IV Asia-Pacific 73

A. Asia-Pacific IT Spending Forecasts 74

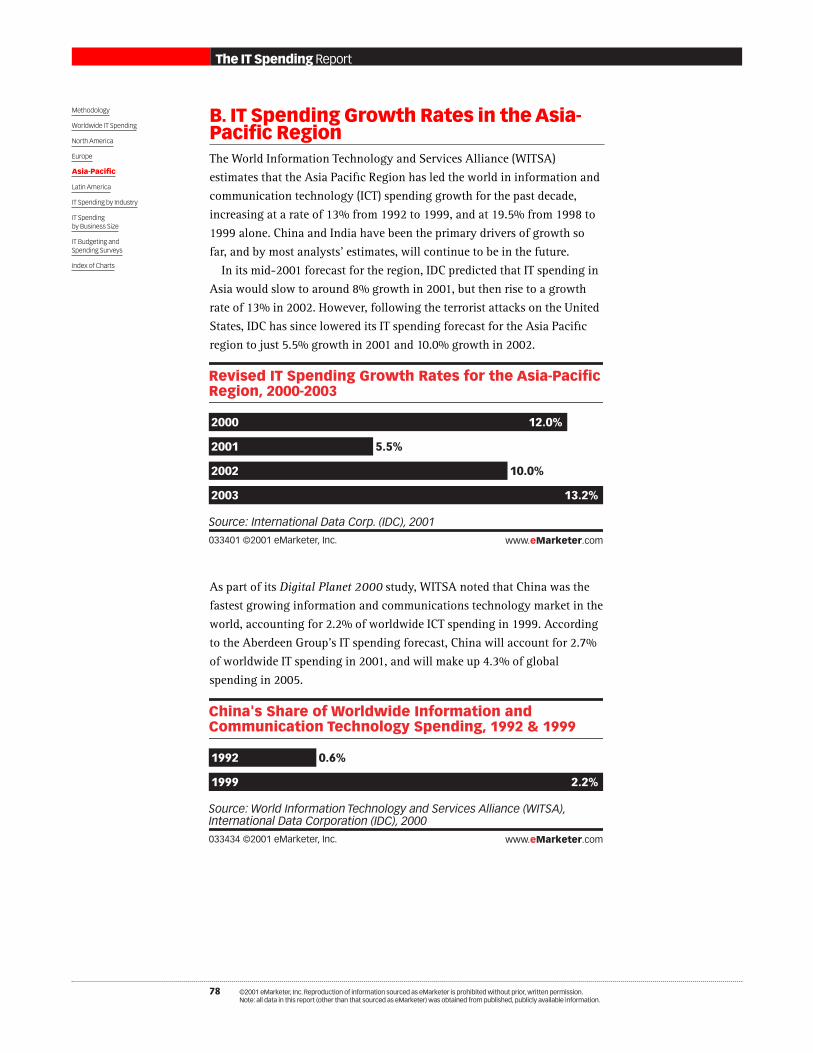

B. IT Spending Growth Rates in the Asia-Pacific Region 78

C. IT Budgeting in the Asia-Pacific Region 82

V Latin America 85

A. Latin American IT Spending Forecasts 86

B. IT Spending Growth Rates in Latin America 88

VI IT Spending by Industry 89

VII IT Spending by Business Size 101

VIII IT Budgeting and Spending Surveys 111

A. IT Budgeting and the ROI Focus 112

B. E-Business and IT Spending 120

C. Anticipating the Recovery in IT Spending 125

Index of Charts 135

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

5

The IT Spending Report

November 2001

Welcome to eMarketer

Dear Reader,

The IT Spending ReportTM is the first eMarketer report to focus upon the major trends and spendingprojections for information technology goods and services throughout the world.

Along with its companion reports, the Telecommunications Spending ReportTM and the PC MarketReportTM, the IT Spending ReportTM provides readers with top-level data and comparative estimatesabout leading technology markets. Coverage of regional, national and industry-specific IT spending isincluded, as well as IT spending by business size.

And unique to eMarketer’s analysis, these reports also include extensive survey sections, whichprovide insight that covers the current thinking among technology users, as well as data on the latesttrends in technology spending.

As an entire package, the IT Spending SeriesTM is a useful tool for those decision-makers who have aninterest in monitoring the current and future performance of technology spending in the world today.

If you have any questions or comments concerning eMarketer or any of the material in this report,please call, fax or e-mail us.

Sincerely,Steve ButlerSenior Analyst

Steve ButlerSenior Analyst, [email protected]

eMarketer, inc.821 BroadwayNew York, NY 10003T: 212.677.6300F: 212.777.1172

Reuse of information in this document, without prior authorization,is prohibited. If you would like to license this report for yourorganization, please contact David Iankelevich [email protected], or 212.763.6037.

Written by Steve Butler

Also contributing to this report:Yael Marmon, researcherAndrew Raff, researcherTracy Tang, researcherMarius Meland, editorAllison Smith, senior editorDana Hill, production artistTerry King, production artistJames Ku, production

Methodology 7

I Worldwide IT Spending

II North America

III Europe

IV Asia-Pacific

V Latin America

VI IT Spending by Industry

VII IT Spending by Business Size

VIII IT Budgeting and Spending Surveys

Index of Charts

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

7

The IT Spending Report

The eMarketer Methodology: MakingSense of the NumberseMarketer’s approach to market research is founded on a philosophy ofaggregating data from as many different sources as possible. Why? Becausethere is no such thing as a perfect research study and no single researchsource can have all the answers. Moreover, a careful evaluation andweighting of multiple sources will inevitably yield a more accurate picturethan any single source could possibly provide.

The eMarketer DifferenceeMarketer does not conduct primary research. Neither a research firm nor aconsultancy, eMarketer has no testing technique to defend, no research biasand no client contracts to protect.

eMarketer prepares each market report using a four-step process ofaggregating, filtering, organizing and analyzing data from leading researchsources worldwide.

Accessing information from the internet as well as a library ofelectronically-filed research reports, surveys and studies, the eMarketerresearch team first compiles publicly available e-business data fromhundreds of research sources. This information is filtered and organizedand then presented in the form of easy-to-read tables, charts and graphs.

To develop each report, eMarketer’s analysts evaluate the aggregateddata and conduct further research to understand the numbers behind thenumbers. Next, they provide concise analysis around the information tohelp make sense of the conflicting numbers and trends.

“I think eMarketer reports are extremely useful andset the highest standards for high quality,objective compilation of often wildly disparatesources of data. I rely on eMarketer’s researchreports as a solid and trusted source.”— Professor Donna L. Hoffman, Co-Director, eLab, Vanderbilt University

www.eMarketer.com©2001 eMarketer, Inc.

Analyze

Aggregate

Filter

Organize

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

8

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

What Benefits Do eMarketer Reports Provide?There are many benefits associated with eMarketer’s aggregation approachto research. The evaluation and presentation of multiple sources means that:

■ The information is more objective than that provided by any singleresearch source. eMarketer has no bias towards any particular internettechnology, e-business trend or market segment.

■ The information is more comprehensive — each set of findings reflectsthe collected wisdom of the leading research firms, consultancies andindustry analysts.

■ The information is all in one place, making it easy to locate, evaluateand compare. eMarketer reports assemble all the different data pointsand accompanying expert opinions into one easy-to-follow referencedocument.

■ The information is neatly organized and clearly presented to savepeople time and help them make better, faster and more informedbusiness decisions.

eMarketer reports also serve as a convenient guidebook or roadmap toother research sources for those wanting more drill-down or “how-to”information on a given topic of interest.

“When I need the latest trends and stats on e-business, I turn to eMarketer. eMarketer cutsthrough the hype and turns an overabundance ofdata into concise information that is sound anddependable.”— Mark Selleck, Business Unit Executive, DISU e-business Solutions, IBM

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

9

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

IMethodology

I Worldwide IT Spending 11

A. Introduction 12

B. Worldwide IT Spending Forecasts 12

C.Worldwide IT Spending Growth Rates 18

D. Worldwide IT Spending by Category 21

II North America

III Europe

IV Asia-Pacific

V Latin America

VI IT Spending by Industry

VII IT Spending by Business Size

VIII IT Budgeting and Spending Surveys

Index of Charts

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

11

The IT Spending Report

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

12

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

A. IntroductionThe year 2001 has seen much uncertainty since companies began to pullback on their IT spending. Leading technology vendors claim that poorvisibility prevents them from forecasting future sales, while economistsand Wall Street analysts are trying – with poor results - to call a bottom ofthe economic slowdown in the United States.

Following the September 11th terrorist attacks on America, thiseconomic uncertainty has been exacerbated, with increased talk of apossible worldwide recession. The best that most analysts have been able todo is offer multiple scenarios for economic recovery, which by extensionmay be used to forecast the recovery in technology spending.

In this report, we include several surveys that attempt to gauge the ITspending climate over the short term and going into 2002. But it isimportant to underscore the point that IT spending is best consideredwithin the context of the long term.

The next three to ten years will see an extraordinary build-out ofinformation and telecommunications infrastructure that will truly move usinto the new, information-based economy. The deployment of e-businesssystems has only just begun, and the conclusion of the excessive dot comera will provide us with a clearer, more realistic view of what is to come.

Comparative estimates for IT spending, along with a variety of surveydata, will help readers put the technology landscape in perspective, andgain a better sense of the major trends that are shaping the New Economy.By using this information, decision-makers will be able to develop theirown strategies for both the short- and long-term.

B.Worldwide IT Spending ForecastsAccording to the World Information Technology and Services Alliance(WITSA), worldwide information and communication technology (ICT)spending will reach $3 trillion by 2003. As of 2000, the organizationestimated that ICT spending accounted for 6.6% percent of global GDP, and9% of US GDP.

Worldwide Information and CommunicationTechnology Spending, 1999 & 2003 (in billions)

1999 $2,100.00

2003 $3,000.00

Source: World Information Technology and Services Alliance (WITSA), International Data Corporation (IDC), 2000

033436 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

13

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

New Zealand has the highest rate of ICT spending as a percent of nationalGDP, at 10.5%. It is followed by the United Kingdom, Sweden, the UnitedStates, Australia, Colombia, Canada, the Czech Republic, Hong Kong, andSingapore.

According to WITSA, the United States, Japan and Germany are theleading markets for ICT spending on an absolute basis. Other countries inthe top ten include the United Kingdom, France, Italy, Canada, China,Brazil and Australia. Since 1997, China had moved to eighth on the list, upfrom the tenth spot between Brazil and Australia.

Collectively, the top ten countries’ ICT spending accounts for 80% of theworld total, while the bottom ten countries’ spending accounts for less than1% of the global ICT market.

As for the top ten countries for ICT spending on a per capita basis,Switzerland and Japan lead the United States, which is followed byDenmark, Singapore, Sweden, Norway, the Netherlands, the UnitedKingdom, and Australia.

Top Three Countries for Information andCommunication Technology Spending, 1999 (inbillions)

US $762

Japan $362

Germany $139

Source: World Information Technology and Services Alliance (WITSA), International Data Corporation (IDC), 2000

033435 ©2001 eMarketer, Inc. www.eMarketer.com

Top Three Countries for Information andCommunication Technology Spending, 1999 (spendingper capita)Switzerland $3,335

Japan $2,854

United States $2,792

Source: World Information Technology and Services Alliance (WITSA), International Data Corporation (IDC), 2000

033448 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

14

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

As might be expected, comparative estimates for the size of worldwideinformation technology spending vary by research firm or forecaster. Inmost cases, definitional differences account for disagreements between ITspending estimates, while differences over forecast growth rates oftenresult in discrepancies as well.

Since Gartner Dataquest includes the telecommunications market in itsIT spending forecast, the firm has put forward one of the largest estimatesfor the size of worldwide IT spending, predicting that the global market willgrow to almost $4.31 trillion by 2005. This latest revision to Gartner’sworldwide spending forecast was released in July of 2001.

Compared with Gartner’s $2.74 trillion estimate for the size of IT spendingin 2001, both the Aberdeen Group’s and Computer Economics’ estimatesare much lower, at $1.210 trillion and $1.185 trillion respectively.

Worldwide IT Spending Forecast, 1999-2005 (inbillions)

1999 $2,144.7

2000 $2,443.8

2001 $2,745.6

2002 $3,088.3

2003 $3,441.9

2004 $3,842.5

2005 $4,308.9

Source: Gartner Dataquest, July 2001

033760 ©2001 eMarketer, Inc. www.eMarketer.com

Worldwide IT Spending Forecast, 2001-2005 (inbillions)

2001 $1,210.80

2002 $1,324.15

2003 $1,452.17

2004 $1,591.40

2005 $1,746.83

Source: Aberdeen Group, 2001

033404 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

15

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

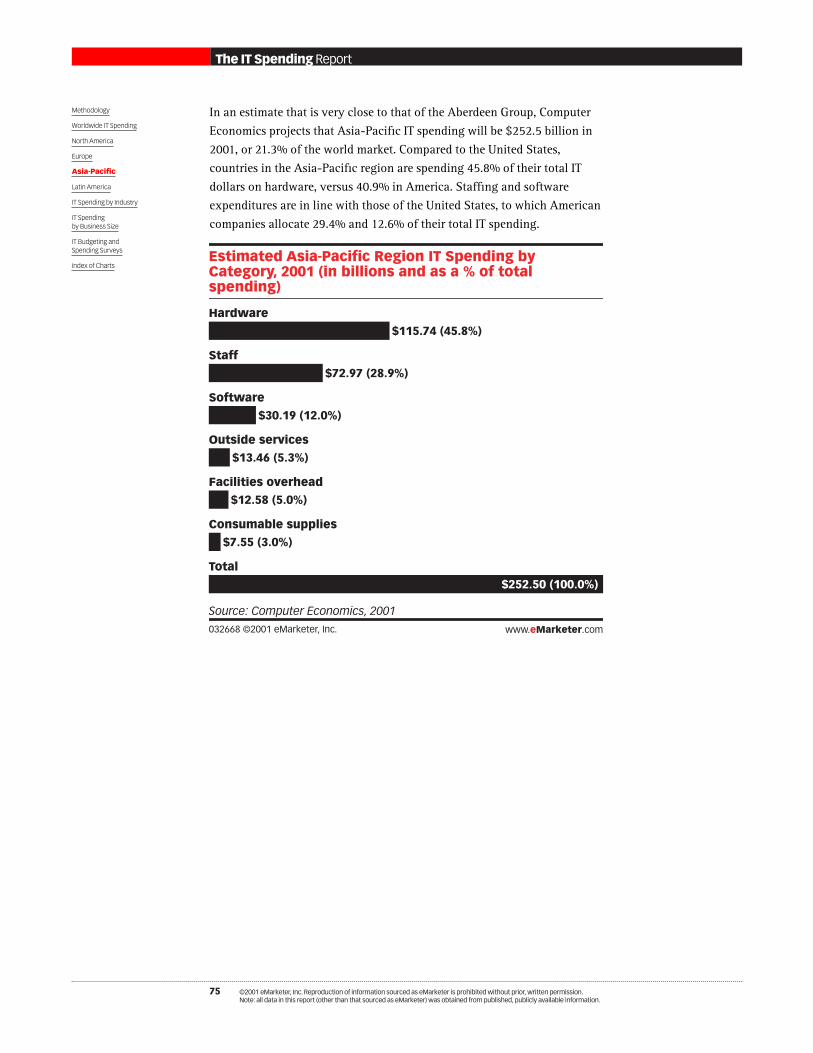

In its comprehensive study of IT spending on a country-by-country basis,the Aberdeen Group estimates that the North American market accounts for40.6% global spending, followed by Western Europe at 24.5% and the Asia-Pacific region at 20.8%.

Breaking out worldwide IT spending by region, Computer Economicsestimates that the United States will account for 44.4% of global ITspending in 2001, while Europe is second with 25.9% of the global market,followed by the Asia-Pacific region and Latin America.

Worldwide IT Spending, by Region, 2001 (in billions)

North America

$492.29

Western Europe

$297.11

Asia/Pacific

$251.96

Latin America

$67.80

Middle East and North Africa

$23.25

Sub-Saharan Africa

$7.55

Rest of World

$70.83

Total

$1,210.80

Source: Aberdeen Group, May 2001

030027 ©2001 eMarketer, Inc. www.eMarketer.com

For Information

Technology Spending

forecasts broken down by

country, coverage of 73

countries is available from

the Aberdeen Study in the

eStat DatabaseEstimated Worldwide IT Spending, by Region, 2001 (inbillions and as a % of total spending)

US $525.66 (44.4%)

Europe $306.40 (25.9%)

Asia Pacific $252.50 (21.3%)

Latin America $44.45 (3.7%)

Rest of world $56.24 (4.7%)

Total $1,185.24 (100.0%)

Source: Computer Economics, 2001

032622 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

16

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Finally, a fourth comparative estimate by IDC forecasts that worldwide ITspending will reach $1.27 trillion by 2003, growing at a compound annualgrowth rate of 10.1% between 2000 and 2003. The fastest growing region isexpected to be the developing countries of the Asia-Pacific region,followed by Eastern Europe and the Middle East/Africa. IDC includesJapan, Australia, New Zealand, Hong Kong and Singapore among themature economies within the Asia-Pacific region, while Indonesia,Malaysia, South Korea, Thailand, Taiwan and India are listed as developingeconomies.

Worldwide IT Spending, by Region, 2000 & 2003 (inbillions)

North America

$443.68

$580.89

Western Europe

$283.30

$386.22

Asia Pacific (Mature)

$128.88

$154.91

Asia Pacific (Developing)

$37.55

$63.23

Latin America

$30.00

$42.19

Eastern Europe/Middle East & Africa

$26.51

$40.21

Total

$949.90

$1,267.64

2000 2003

Source: International Data Corporation (IDC), 2000

032962 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

17

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

As per IDC’s calculations, the United States and Canada will account for45.8% of worldwide IT spending in 2003. Western Europe follows at 30.5%,while the advanced economies of the Asia Pacific region will account for12.2% of the global market for IT goods and services. The developingregions of the world will naturally be gaining market share at the expenseof the more mature IT markets over the next several years.

According to the Information Technology Association of America, theUnited States alone accounts for almost 35% of worldwide information andcommunications technology (ICT) spending.

Worldwide IT Spending, by Region, 2000 & 2003 (as a% of world total)

North America

46.7%

45.8%

Western Europe

29.8%

30.5%

Asia Pacific (Mature)

13.6%

12.2%

Asia Pacific (Developing)

4.0%

5.0%

Latin America

3.2%

3.3%

Eastern Europe/Middle East & Africa

2.8%

3.2%

2000 2003

Source: International Data Corporation (IDC), 2000

032963 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

18

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

C.Worldwide IT Spending Growth RatesThe World Information Technology and Services Alliance (WITSA)estimates that US ICT spending grew at a compound annual growth rate of7.8% from 1992 to 1999, compared to a worldwide figure of 7.5% and aCAGR of 5.2% among G-8 countries for that same period. The sharpestgrowth in ICT spending was found in the Asia-Pacific region, whichexperienced a CAGR of 13.3%. It was closely followed by Latin America at13%, while Western Europe lagged farthest behind with a CAGR of 6.2%.

WITSA has gone on to list what it believes are the key drivers of growth inworldwide ICT spending. These continue to be the build-out of the internetand related telecommunications infrastructure, the adoption of e-businesstechnologies such as e-commerce or supply chain management softwaresystems, and the emergence of new ICT markets in countries such as China,India and Brazil.

Historical data reveal that the growth rate for IT spending correlates verystrongly with growth rates in GDP. During the last US recession in 1991, forexample, IT spending growth declined from 8.9% the previous year to a lowof 4.2%, while the US GDP contracted by 0.5%, down from a growth rate of1.8% for the previous year. By the following year, however, the USeconomy rebounded to a growth rate of 3.1% while IT spending recoveredto 9.0%.

Worldwide Information and CommunicationTechnology Spending Growth, 1992-1999

US 7.8%

Worldwide 7.5%

G-8 countries 5.2%

Source: World Information Technology and Services Alliance (WITSA), International Data Corporation (IDC), 2000

033437 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

19

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

A similar pattern occurred among countries in the Asia-Pacific regionduring the 1998 currency crisis there, and most analysts expect to see thisrepeated with global IT spending during the current economic slowdown inthe United States.

But just as it is difficult to pre-determine the exact timing of a bottomand recovery within the overall economy, so too has it been difficult toforecast the timing of a bottom and recovery in technology spending.Nonetheless, as more information has become available, most leadingresearch firms have continued to adjust their IT spending forecastsaccording to their best read on the economy, as well as the business climatein general.

For example, after conducting a global survey of 589 companies duringthe second quarter of 2001, Gartner found that on average, respondentsplanned to increase their IT spending at a rate of 21.5% in 2001. Theresearch firm was careful to note, however, that it expects IT capitalspending will decrease during 2001. It is only when operating expenses andoutsourced services are included as a part of IT budgets, that the result willbe overall growth in IT spending.

As the year has progressed, most forecasts have become much lessoptimistic. Following its own read of economic trends, IDC noted in itsmid-2001 report that worldwide IT spending could be reduced by as muchas $150 billion through 2003. The research firm went on to indicate that asignificant $50 billion portion of that reduced spending would beaccounted for by a slowdown in IT spending in Europe.

8.9%

9.0%

11.9%

16.1% 16.5%

13.0%

10.5%

9.4%

11.1%

Historical US GDP and IT Spending Growth Rates,1989-2000

1989

3.5%

6.7%

1990

1.8%

1991

-0.5%

4.2%

1992

3.1%

1993

2.7%

1994

4.0%

1995

2.7%

1996

3.6%

1997

4.4%

1998

4.4%

1999

4.2%

2000

5.0%

15

0

GDP IT spending

Source: International Data Corporation (IDC), September 2001

032701 ©2001 eMarketer, Inc. www.eMarketer.com

9.0%

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

20

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

And as might be expected, an increasingly pessimistic outlook began totake shape by the end of the third quarter, as the possibility of a USrecession became more likely. IDC issued a forecast revision on October11th, projecting that worldwide IT spending would see just 2.4% growth in2001, and reach 6.1% growth in 2002.

Similarly, a September 2001 forecast revision by Merrill Lynch projectedthat worldwide IT spending will grow at a rate of just 2.6% in 2001, and4.6% in 2002. At about the same time, another downward revision wasissued by Credit Suisse First Boston as well, forecasting IT spending torange between 0% and 5% growth in 2002.

Revised Worldwide IT Spending Growth Rates,2000-2003

2000

10.0%

2001

2.4%

2002

6.1%

2003

10.5%

6

10

Note: revised 11 October 2001Source: International Data Corporation (IDC), October 11, 2001

033400 ©2001 eMarketer, Inc. www.eMarketer.com

Worldwide IT Spending Growth, 2001 & 2002

2001 2.6%

2002 4.6%

Source: Merrill Lynch, 2001

033438 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

21

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

And finally, after examining the results of its 33-country IT spendingsurvey in October, the Meta Group has determined that non-US businesseshave increased their IT spending by 6% in 2001. The research firm has goneon to predict that spending growth will remain flat in 2002, while ITspending in the United States will contract for the first time, by 2%.

D.Worldwide IT Spending by CategoryIn an IT spending forecast published in 2000, research firm Gartner hasestimated that hardware spending as a portion of total IT spending was19.8% that year, but is expected to drop to 17.4% by 2003. By comparison,communications equipment spending continues to hold the greatest shareof the overall IT market at 49.2% in 2001, but will fall to a 47.5% shareover the next two years.

IT services spending accounts for 23.5% of total spending in 2001,according to Gartner’s forecast, while software takes an 8.5% share. Theselatter two categories are expected to take an increasingly greater portion ofthe worldwide IT market, accounting for 25.5% and 9.6% of total ITspending by 2003.

Worldwide IT Spending, by Category, 1999-2003 (inbillions)

1999 2000 2001 2002 2003

Hardware $415.5 $463.4 $501.2 $537.2 $572.5

Software $159.3 $187.6 $225.4 $264.1 $315.8

Communications $1,081.3 $1,196.4 $1,313.6 $1,431.5 $1,560.6

Services $475.0 $541.3 $625.4 $726.2 $839.0

Total $2,131.1 $2,338.7 $2,665.6 $2,959.0 $3,287.9

Source: Gartner Group, October 2000

033564 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

22

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

In another comparative estimate that breaks down worldwide IT spendingfor 2001, Computer Economics has found that hardware represents thelargest category at 43.2% of IT spending, followed by personnel and thensoftware at 30.0% and 11.6% of total expenditures on IT.

Taking an even more comprehensive look at technology spending thatincludes the revenues of semiconductor manufacturers and electronicsdistribution, investment bank UBS Warburg estimates that global ITspending will reach $1.7 trillion in 2001. Communications equipmentmakes up the greatest share at 26.6% of total spending, followed byenterprise hardware and consumer electronics at 15.5% and 12.4%respectively.

Estimated Worldwide IT Spending, by Category, 2001(in billions and as a % of total spending)

Hardware

$512.01 (43.2%)

Staff

$356.08 (30.0%)

Software

$137.39 (11.6%)

Outside services

$88.53 (7.5%)

Facilities overhead

$50.61 (4.3%)

Consumable supplies

$40.61 (3.4%)

Total

$1,185.24 (100.0%)

Source: Computer Economics, 2001

032619 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

23

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

UBS Warburg’s projections for IT spending growth by category show thatsemiconductor manufacturers have been hardest hit by the downturn.Overall IT spending is projected to contract by 5% for this year, comparedto an estimated 16% rate of growth in 2000. Software and IT servicesspending are expected to show the most positive growth rates.

Estimated Worldwide IT Revenues, by Category, 2001(in billions)Communications equipment $451.89

Enterprise hardware $263.51

Consumer electronics $210.78

PCs & peripherals $182.16

Semiconductors $168.19

Software $110.48

Components $91.19

IT services $90.07

Electronic manufacturers’ services $57.59

Semi equipment $45.52

Electronics distribution $29.10

Total $1,700.47

Source: UBS Warburg, 2001

032971 ©2001 eMarketer, Inc. www.eMarketer.com

Estimated Worldwide IT Revenue Growth, byCategory, 2001IT services 14%

Software 14%

Electronics distribution 13%

Electronics manufacturers’ services 5%

Enterprise hardware -3%

PCs and peripherals -3%

Communications equipment -8%

Components -9%

Consumer electronics -10%

Semi equipment -12%

Semiconductors -15%

Source: UBS Warburg, 2001

032972 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

24

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

The investment bank is projecting a recovery by next year however, withan overall growth rate for IT revenues of 6% in 2002. Software and ITservices are once again set to lead the way.

Estimated Worldwide IT Revenue Growth, byCategory, 2002Software 15%

IT services 12%

Semiconductors 10%

Electronic manufacturers’ services 10%

Consumer electronics 8%

PCs and peripherals 6%

Components 6%

Electronic distribution 5%

Enterprise hardware 5%

Communications equipment 2%

Semi equipment -4%

Source: UBS Warburg, 2001

032973 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

25

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

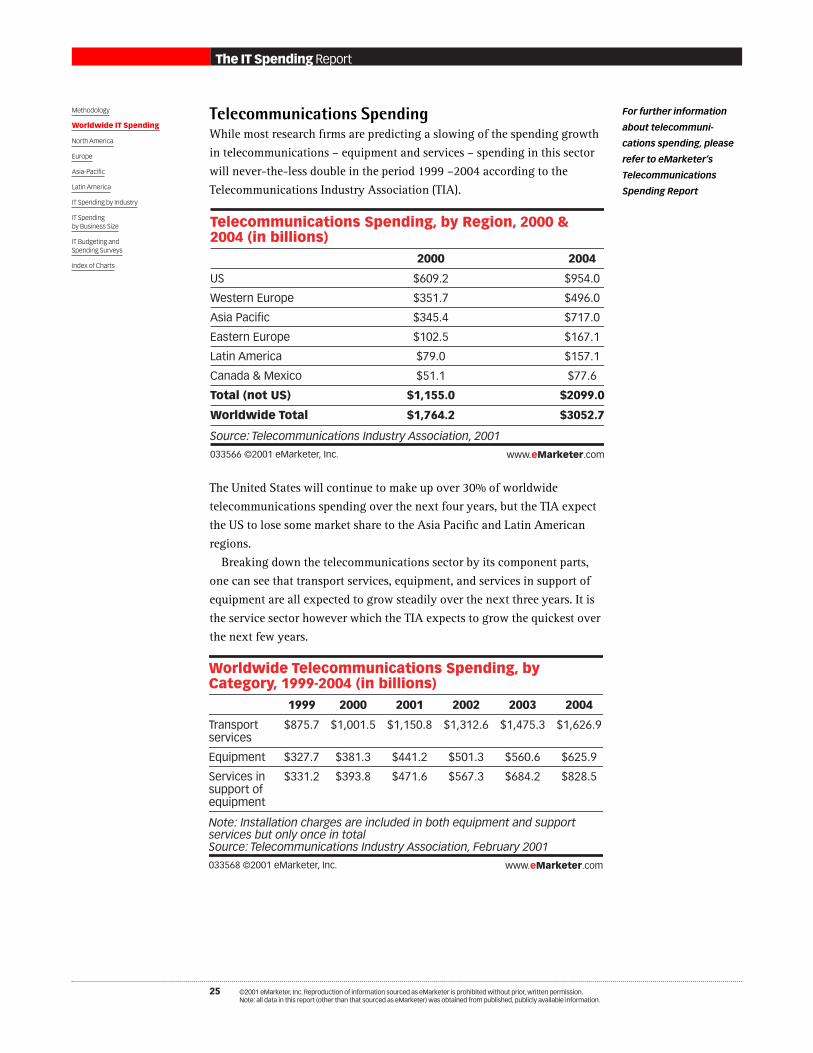

Telecommunications SpendingWhile most research firms are predicting a slowing of the spending growthin telecommunications – equipment and services – spending in this sectorwill never-the-less double in the period 1999 –2004 according to theTelecommunications Industry Association (TIA).

The United States will continue to make up over 30% of worldwidetelecommunications spending over the next four years, but the TIA expectthe US to lose some market share to the Asia Pacific and Latin Americanregions.

Breaking down the telecommunications sector by its component parts,one can see that transport services, equipment, and services in support ofequipment are all expected to grow steadily over the next three years. It isthe service sector however which the TIA expects to grow the quickest overthe next few years.

Telecommunications Spending, by Region, 2000 &2004 (in billions)

2000 2004

US $609.2 $954.0

Western Europe $351.7 $496.0

Asia Pacific $345.4 $717.0

Eastern Europe $102.5 $167.1

Latin America $79.0 $157.1

Canada & Mexico $51.1 $77.6

Total (not US) $1,155.0 $2099.0

Worldwide Total $1,764.2 $3052.7

Source: Telecommunications Industry Association, 2001

033566 ©2001 eMarketer, Inc. www.eMarketer.com

Worldwide Telecommunications Spending, byCategory, 1999-2004 (in billions)

1999 2000 2001 2002 2003 2004

Transportservices

$875.7 $1,001.5 $1,150.8 $1,312.6 $1,475.3 $1,626.9

Equipment $327.7 $381.3 $441.2 $501.3 $560.6 $625.9

Services insupport ofequipment

$331.2 $393.8 $471.6 $567.3 $684.2 $828.5

Note: Installation charges are included in both equipment and supportservices but only once in totalSource: Telecommunications Industry Association, February 2001

033568 ©2001 eMarketer, Inc. www.eMarketer.com

For further information

about telecommuni-

cations spending, please

refer to eMarketer’s

Telecommunications

Spending Report

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

26

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Putting the US market aside for the moment reveals that within theinternational sector, wireless services are expected to be the fastest growingtelecommunications spending category above all others, rising to over$600 billion in 2004 from $153 billion in 1999. This of course wouldcoincide with the deployment of next-generation wireless networks, whichare being rolled out globally over the next three to five years. Other areasof significant spending include the enterprise equipment sector andtelecommunications support services.

Among those leaders in the telecommunications equipment space, Ciscoremains by far the largest in terms of market capitalization. Share prices forall of these companies have been hit hard over the past several months,following the headier days of the late 1990’s and 2000. But despite theirrecent troubles with short-term visibility, these firms will continue to play acritical role during the long-term build-out of telecommunicationsinfrastructure over the next five to ten years.

Top 10 Communications Equipment Companies, byMarket Capitalization, September 7, 2001 (in billions)

Cisco Systems

$105.91

Qualcomm Inc.

$41.29

Motorola Inc.

$39.35

NEC Corp.

$20.79

Fujitsu

$20.27

Lucent Technologies

$20.11

Nortel Networks

$19.39

Corning Inc.

$10.40

JDS Uniphase Corp.

$8.77

Mitsubishi Electric

$8.04

Source: UBS Warburg, 2001

032974 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

27

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Hardware SpendingResearch from Global Industry Analysts forecasts that worldwide ITequipment spending will increase at a CAGR of 6.43% between 1999 and2005. The United States, Japan, and Germany are the world’s three largestand most mature markets, while the strongest growth rates are expected tooccur in the Asia-Pacific region (excluding Japan) and Latin America.These latter two markets are projected to see CAGR’s of 11.68% and 9.94%over the 1999-2005 period.

Global Industry Analysts breaks down IT equipment spending into threeseparate categories, of which computer equipment holds a 63.6% share.Telecommunications equipment and then business equipment account forthe remaining 24.8% and 11.6% of the market.

In another look at the hardware market, Gartner has estimated thatbusiness spending on PC’s and servers grew 8% during 2000, down from12% growth in 1999. By comparison, UBS Warburg estimates thatworldwide hardware spending increased 12% in 1999, but will slow to agrowth rate of just 7% in 2001. The best growth year for hardwarespending, according to the investment bank, was in 1995 when sales grew30% over the previous year.

Breakdown of Worldwide IT Equipment Spending, byCategory, 1999 (in billions)

Computer equipment $626.51 (63.6%)

Telecom equipment $244.57 (24.8%)

Business equipment $114.31 (11.6%)

Total $985.39 (100.0%)

Source: Global Industry Analysts, 2001

032993 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

28

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

But now that the hardware market has matured in regions such as NorthAmerica and Europe, PC and server manufacturers are pinning their hopeson growth in the Asia-Pacific region and Latin America. China and SouthKorea represent two of the most promising markets over the short term,while India will be a significant market over the longer-term, according toUBS Warburg.

As for the current share of the PC market by unit demand, UBS Warburgestimates that the United States accounts for 42% of the worldwide marketin 2001, ahead of Western Europe which has a 26% market share, andJapan which purchases 10% of PC units. The remaining countries in theAsia-Pacific region hold a 13% market share, while Latin America’s portionof the worldwide PC market is 4%.

With desktop PC’s reaching high penetration rates among householdsand businesses in developed countries, manufacturers are turning to laptopand handheld computing devices as alternate high growth areas. IDCpredicts that portable PC’s will experience a CAGR of 20.9% in the numberof units shipped between 1999 and 2004, compared with a CAGR of 14.2%for desktop PC’s during that same period.

According to Global Industry Analysts, the server market is led by fivecompanies, which together hold a 77% share of worldwide sales in 2000.Compaq is the leader with a 27% market share, followed by IBM and DellComputer, which each held 17% and 15% of the market. Hewlett Packardand Sun Microsystems rounded out the top five, with an 11% and 7% shareeach. The overall market for servers grew at a rate of 14% in 2000.

Salomon Smith Barney and IDC have a different view of the worldwideserver market in 2001, however, placing IBM on top with a 24.1% marketshare, followed by Compaq and Sun Microsystems accounting for 17.0%and 15.9% of global server sales. Taken together, the top five companieshold 78.4% of the total market for servers.

Worldwide PC Market Revenue Forecast, by Region,2001 (in billions)

United States $68.4

Western Europe $44.9

Japan $21.4

Asia/Pacific $18.1

Rest of World $27.3

Total $180.1

Source: UBS Warburg, 2001

033083 ©2001 eMarketer, Inc. www.eMarketer.com

For further information

about the PC industry and

markets, please refer to

eMarketer’s PC Market

Report

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

29

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Top 10 Server Vendors, by Revenues, 2001 (in billionsand as a % of market share)

IBM

$14.81 (24.1%)

Compaq

$10.45 (17.0%)

Sun Microsystems

$9.77 (15.9%)

Hewlett-Packard

$9.18 (14.9%)

Dell Computer

$4.02 (6.5%)

Fujitsu

$2.13 (3.5%)

Siemens

$1.10 (1.8%)

NEC

$1.07 (1.7%)

Hitachi

$0.98 (1.6%)

SGI

$0.77 (1.3%)

Source: International Data Corporation (IDC), Salomon Smith Barney, 2001

033439 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

30

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Focusing upon the enterprise hardware market, UBS Warburg has selectedthe top ten vendors by their market capitalization as of September 7th,2001. Not unexpectedly, IBM is by far the largest company, followed byHewlett-Packard and Sun Microsystems.

Defined by their core product offerings and placed in a separate category,UBS Warburg has ranked the leading PC and peripherals manufacturers bymarket capitalization as of September 7th.

Top 10 Enterprise Hardware Equipment Companies,by Market Capitalization, September 7, 2001 (inbillions)

IBM Corp.

$178.69

Hewlett-Packard

$37.33

Sun Microsystems Inc.

$35.24

EMC Corp.

$32.64

Hitachi

$25.17

Secom Co. Ltd.

$11.17

Brocade Communications Systems

$5.21

Network Appliance Inc.

$3.86

NCR Corp.

$3.64

Unisys Corp.

$3.52

Source: UBS Warburg, 2001

032985 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

31

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

In a separate ranking of desktop PC vendors by market share in 2000,Salomon Smith Barney places Compaq Computer at the top with 13% ofthe worldwide market, followed by Dell Computer at 11.1% and Hewlett-Packard at 8.8% market share.

Top 10 PC and Peripherals Manufacturers, by MarketCapitalization, September 7, 2001 (in billions)

Dell Computer

$56.49

Canon

$27.60

Compaq Computer Corp.

$18.84

Pitney Bowes Inc.

$10.94

Ricoh Company Ltd.

$10.73

Xerox Corp.

$6.20

Lexmark International Group Inc.

$6.10

Apple Computer Inc.

$5.97

Quanta

$4.95

CDW Computer Centers Inc.

$3.52

Source: UBS Warburg, 2001

032986 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

32

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

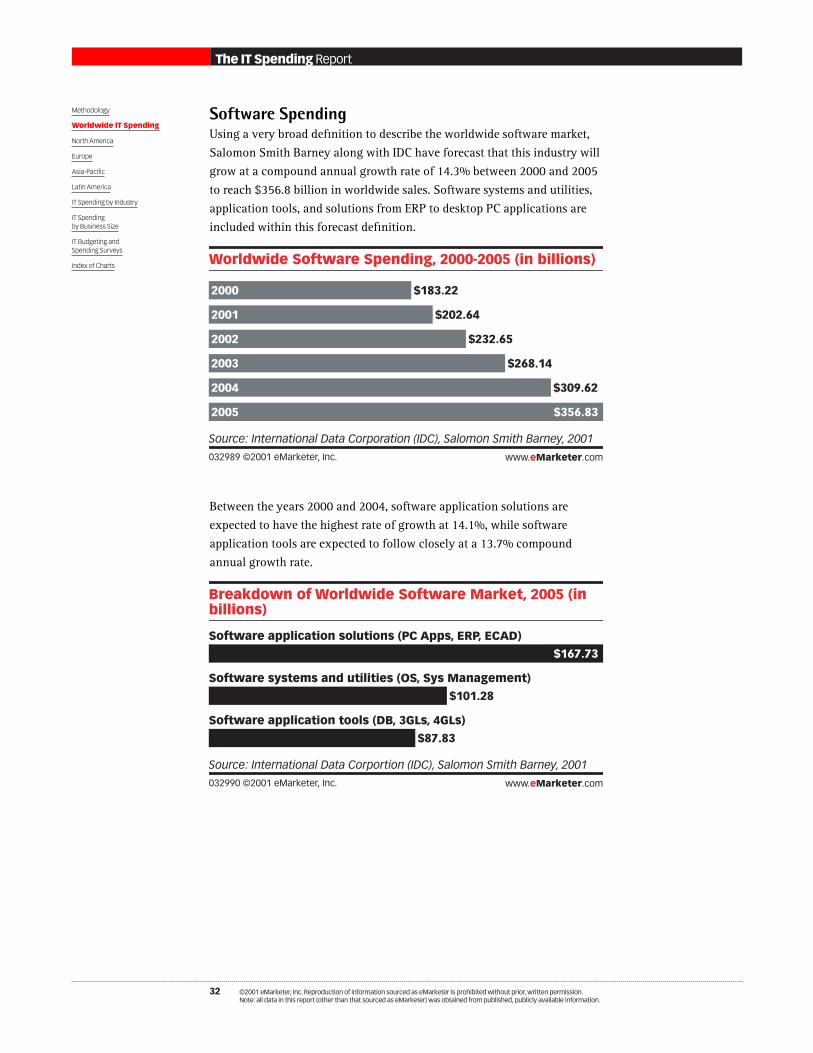

Software SpendingUsing a very broad definition to describe the worldwide software market,Salomon Smith Barney along with IDC have forecast that this industry willgrow at a compound annual growth rate of 14.3% between 2000 and 2005to reach $356.8 billion in worldwide sales. Software systems and utilities,application tools, and solutions from ERP to desktop PC applications areincluded within this forecast definition.

Between the years 2000 and 2004, software application solutions areexpected to have the highest rate of growth at 14.1%, while softwareapplication tools are expected to follow closely at a 13.7% compoundannual growth rate.

Worldwide Software Spending, 2000-2005 (in billions)

2000 $183.22

2001 $202.64

2002 $232.65

2003 $268.14

2004 $309.62

2005 $356.83

Source: International Data Corporation (IDC), Salomon Smith Barney, 2001

032989 ©2001 eMarketer, Inc. www.eMarketer.com

Breakdown of Worldwide Software Market, 2005 (inbillions)

Software application solutions (PC Apps, ERP, ECAD)

$167.73

Software systems and utilities (OS, Sys Management)

$101.28

Software application tools (DB, 3GLs, 4GLs)

$87.83

Source: International Data Corportion (IDC), Salomon Smith Barney, 2001

032990 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

33

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

In the Global Industry Analysts’ forecast for worldwide software sales, theapplications market is also expected to see the strongest increase, growingat an average annual growth rate of 21.4% between 1999 and 2005. Bycomparison, software infrastructure sales are set to grow at an averageannual rate of 17.1%, while software tools are forecast to have a 12.6%average annual growth rate.

In its historical analysis of corporate software spending, IDC has found thatsoftware accounted for 20% of total business IT spending between theyears 1995 and 2000. Software solutions formed the largest market at $110billion in aggregate sales over that period. As a category, software salesgrew at a CAGR of 18% between 1995 and 2000, compared to an estimated10% to 11% CAGR for total corporate IT spending during the same time.

Worldwide Software Market, by Category, 2000-2005(in billions)

2000 2001 2002 2003 2004 2005

Applications $78.4 $90.1 $106.5 $129.7 $164.9 $220.4

Infrastructure $50.2 $57.2 $66.2 $77.7 $93.2 $114.6

Tools $39.2 $44.4 $50.1 $56.1 $63.1 $71.2

Total $167.8 $191.7 $222.8 $263.5 $321.2 $406.2

Source: Global Industry Analysts, 2001

033080 ©2001 eMarketer, Inc. www.eMarketer.com

Worldwide Software Market, by Category andPlatform, 2001 (in billions)

Host Desktop Client/server Internet Total

Applications $13.2 $35.1 $35.0 $6.8 $90.1

Infrastructure $16.2 $10.8 $19.0 $11.2 $57.2

Tools $10.8 $5.8 $19.1 $8.7 $44.4

Source: Global Industry Analysts, 2001

033081 ©2001 eMarketer, Inc. www.eMarketer.com

Breakdown of Aggregate Worldwide CorporateSoftware Spending, by Category, 1995-2000 (inbillions)

Solutions $101.0

System/utilities $39.0

Application tools $37.0

Total $177.0

Source: International Data Corporation (IDC), 2001

033147 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

34

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

A narrower forecast from AMR Research indicates that the market forenterprise software will grow at a compound annual growth rate of 15%over the next four years, led by strong sales growth in Asia and LatinAmerica. North America will form the largest market, accounting for 44%of sales by 2004, while Europe is projected to take a 36% market share,followed by Asia at 12% of worldwide software sales. Latin America isforecast to account for 6% of enterprise software sales.

Within the enterprise software market, supply chain management (SCM)and e-commerce applications are projected by AMR Research to have evenhigher growth rates, at CAGR’s of 54% and 79% respectively.

According to most industry observers, whenever there has been adownturn in technology spending, software spending typically lagshardware and other IT categories by six to nine months. In anticipation of adecline in software sales, Morgan Stanley noted that through the first halfof 2001 annualized software spending was off only 5%, compared with adecline of 31% for the wider IT industry.

A similar warning of an approaching decline in software sales was issuedby Gartner Dataquest in late September of 2001, as the research firm notedthat new software sales had grown at a rate of 6% during the first half ofthe year. Gartner went on to forecast that total worldwide sales for the yearwould top off at 7% growth, well below the 18% growth rate of theprevious year.

Among those industries expected to reduce their software spending themost were airlines, travel, automobiles, insurance, and consumer PCvendors, according to Gartner. Business-to-consumer e-commerceapplications were also expected to see a drop-off in sales, asimplementation or upgrades of online retailing applications have becomeless urgent following the dot com boom.

Salomon Smith Barney has put together the following list of leadingsoftware companies with the help of data from IDC. Microsoft, IBM andOracle are the largest vendors, holding a 23.4% market share between thethree of them. The software industry is rather diverse compared to othersegments of the IT industry, in which as much as 80% of the total market isconcentrated among the top five players.

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

35

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Top 15 Software Companies, by Revenues, 2000 (inbillions and as a % of market share)

Microsoft

$19.46 (11.1%)

IBM

$13.66 (7.8%)

Oracle

$7.89 (4.5%)

Computer Associates

$7.34 (4.2%)

SAP AG

$3.34 (1.9%)

Hewlett-Packard

$3.25 (1.9%)

Sun Microsystems

$1.79 (1.0%)

Fujitsu

$1.77 (1.0%)

BMC Software

$1.70 (1.0%)

Hitachi

$1.58 (0.9%)

Siebel Systems

$1.31 (0.7%)

Peoplesoft

$1.19 (0.7%)

Siemens

$1.16 (0.7%)

Adobe

$1.13 (0.6%)

Veritas

$1.13 (0.6%)

Source: International Data Corporation (IDC), Salomon Smith Barney, 2001

032988 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

36

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

IT Services SpendingIn May of 2001, the Gartner Group revised its forecast for the size of theworldwide IT services market, which the research firm had initiallyestimated was $541.3 billion in 2000. The May revision now finds that ITservices spending had reached $665 billion in 2000, and is set to grow to$1.4 trillion by 2005. Gartner estimates that the market grew at a rate of9.7% in 2000, and will grow by 12.5% in 2001.

North America accounts for the largest share of IT services spending, at$345 billion in 2000. This 52% share is expected to remain constantthrough 2005, when North American spending will reach $712 billion.

Breaking down the IT services market, Gartner has found that the largestsegment is represented by development and integration services, which isprojected to reach $368.5 billion in revenues by 2005. Much of theanticipated growth in this area is expected to come from the need to linkbusinesses’ internal legacy systems and software to new e-businesssoftware, and to the external systems of their trading partners.

Worldwide Information Technology ServicesSpending, 2000 & 2005 (in billions)

2000 $665

2005 $1,400

Source: Gartner Group, 2001

031270 ©2001 eMarketer, Inc. www.eMarketer.com

Worldwide Technology Development & IntergrationServices Spending, 2000 & 2005 (in billions)

2000 $169.4

2005 $368.5

Source: Gartner Group, 2001

031271 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

37

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

The next largest segment is business process management services, whichby Gartner’s definition includes outsourcing services. This market isforecast to reach $345.5 billion by 2005.

Compared to Gartner’s forecasts, IDC has estimated that worldwide spendingon IT services will grow at a compound annual growth rate of 12% from2000 to 2005, to reach $700 billion. In 2001, the United States represents a47% share of the world market according to IDC, while Western Europe hasa 29% share, and Japan accounts for 12% of global spending.

Worldwide Technolgy Business Process ManagementServices Spending, 2000 & 2005 (in billions)

2000 $148.2

2005 $345.5

Source: Gartner Group, 2001

031272 ©2001 eMarketer, Inc. www.eMarketer.com

Breakdown of Worldwide IT Services Market, byRegion, 2001 (in billions)

United States $206.9

Western Europe $127.5

Japan $53.2

Rest of world $52.5

Total $440.1

Source: International Data Corp. (IDC), 2001

031342 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

38

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Similar to the Gartner Group, IDC expects the United States’ share of theworldwide IT services market to remain constant over the next severalyears, rising marginally to 48% by 2005. The market share for WesternEurope and Japan is expected to see modest declines to 27.4% and 10.7%,as other regions of the world increase their IT services spending.

Breakdown of Worldwide IT Services Market, 2005 (inbillions)

US $335.0

Western Europe $192.4

Japan $75.2

Rest of World $97.7

Total $700.3

Source: International Data Corp. (IDC), 2001

031343 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

39

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

The entire IT services market is forecast to grow at a compound annualgrowth rate of 12% between 2000 and 2005, with 11% growth in 2001. TheAsia-Pacific region is expected to be the fastest-growing market, increasingat a CAGR of 23% through the next five years.

Breaking down the IT services market by spending category, IDC expectssystems integration services to be a $142 billion market by 2005.

Breakdown of Worldwide IT Services Market, byService, 2001

Hardware and support

21%

Systems integration

18%

Processing services

18%

IS outsourcing

15%

Network integration and management

10%

Application development and outsourcing

7%

IT training and education

6%

IT consulting

5%

Source: International Data Corp. (IDC), 2001

031344 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

40

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Compared to other segments within the technology industry, the worldwideIT services market is highly fragmented. According to Gartner Dataquest,there are more than 15,000 services companies operating in the UnitedStates alone. The top 400 IT services vendors account for less than 50% oftotal market revenues, while the top 10 account for less than 20% ofrevenues. IBM leads the way, bringing in almost $33.2 billion in servicesrevenues in 2000 as it grew to hold a 5% market share.

Top 10 Worldwide IT Services Vendors, by RevenueEstimates, 1999 & 2000 (in billions)

1999Revenue

2000Revenue

2000 MarketShare

IBM $32.16 $33.15 5.0%

EDS $18.62 $19.22 2.9%

Fujitsu $12.57 $13.30 2.0%

Computer Sciences Corp. (CSC) $9.20 $10.45 1.6%

Accenture $9.12 $10.00 1.5%

Cap Gemini Ernst & Young $8.16 $7.77 1.1%

Xerox $8.05 $7.72 1.1%

Hewlett-Packard $6.16 $7.29 1.1%

Compaq $7.06 $6.70 1.1%

NTT Data $5.71 $6.69 1.1%

Others $490.18 $543.59 81.6%

Total Market $606.98 $665.87 100.1%

Source: Gartner Dataquest, 2001

032694 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

41

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Investment bank UBS Warburg has compiled its list of leading IT servicescompanies by selecting those businesses whose core focus is uponinformation technology services. When ranked according to marketcapitalization, EDS comes out on top, followed closely by Wipro, Sungardand CSC.

Top 10 IT Services Companies, by MarketCapitalization, September 7, 2001 (in billions)

Electronic Data Services Corp.

$27.77

Wipro Ltd.

$7.41

Sungard Data Systems Inc.

$6.71

Computer Sciences Corp.

$6.31

DST Systems Inc.

$6.08

Infosys Technologies Ltd.

$4.80

Affiliated Computer Svcs. Inc.

$4.19

CGI Group Inc.

$2.02

Datacraft Asia Ltd.

$1.70

HCL Technologies

$1.40

Source: UBS Warburg, 2001

032987 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

42

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

E-Business/Internet Technology SpendingAlthough not traditionally broken out as a segment of IT spending, there isa significant interest in the portion of technology spending that isdedicated to e-business or internet-related initiatives. Many companieshave begun to dedicate significant portions of their IT budgets to suchprojects, and several researchers are now considering the contribution thate-business initiatives are making to overall IT spending growth.

However, e-business spending forecasts do vary considerably, due in partto the fact that it is almost impossible for technology vendors to break outtheir product sales by intended customer use. Furthermore, sometechnologies may have multiple uses that make it difficult to define them asinternet-specific. And finally, definitional differences between forecastsresult in different projections, as some researchers include just hardware,software and telecommunications equipment, while others include servicesas well.

In one of the earlier attempts to isolate and forecast internet-relatedspending, UK-based research firm Frost & Sullivan has estimated thatspending on technology used specifically for internet initiatives reached$40 billion in 1999, and will grow to $80 billion by 2004.

According to research firm Strategy Analytics, worldwide spending ondedicated hardware, software and services that were targeted at e-businessgrew at a rate of 73% and totaled $36 billion during the year 2000. Butfollowing the extraordinary burst of spending that year, Strategy Analyticsestimates that e-business spending will fall by 12.5% in 2001, withbusinesses spending just $31 billion by the end of this year.

Estimated Worldwide Spending on InternetTechnologies, 1999 & 2004 (in billions)

1999 $40.00

2004 $80.00

Source: Frost & Sullivan, 2000

033440 ©2001 eMarketer, Inc. www.eMarketer.com

Worldwide IT Spending on Dedicated E-BusinessTechnology, 2000 & 2001 (in billions)

2000 $36.00

2001 $31.00

Source: Strategy Analytics, 2001

032698 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

43

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Another estimate by Cahner’s In-Stat has put the figure for IT spending oninternet initiatives by US businesses at $80 billion in 2000. By Cahner’sdefinition, internet spending includes technology, software and services forinternet-specific projects. Total spending is expected to reach $197 billionin the United States alone by 2004.

After conducting an extensive global survey of e-business spending in 27countries, IDC has estimated that aggregate worldwide spending on e-business projects will exceed $5 trillion over the next four years, between2001 and 2004. Leading the way on the global stage will be the UnitedStates, followed by Japan and the United Kingdom.

Estimated Spending on Internet-Specific Initiatives byUS Businesses, 2000 & 2004 (in billions)

2000 $80.0

2004 $197.0

Source: Cahners In-Stat, 2001

033398 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

44

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

The research firm has gone on to point out that online trading initiativesand integration costs will be the primary expenditures behind future e-business investment.

Top 10 Countries' Aggregate Spending on E-BusinessTechnology, 2001-2004 (in billions)

US

$2,397.60

Japan

$361.80

UK

$285.80

France

$285.80

Germany

$228.61

Canada

$193.89

Italy

$77.41

Spain

$76.11

Australia

$67.85

Sweden

$67.85

Source: International Data Corporation (IDC), 2001

033592 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

45

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Through the end of 2001, it is estimated that American companies will havealready spent $495.6 billion over the past several years, with Germanyfollowing as an early adopter, having spent $73.97 billion by then. Chinahas already invested a considerable amount in e-business technologyaccording to IDC, while Japan is off to a slow start, although it is expectedto be a leader through the long term.

Top 10 Countries' Aggregate Spending on E-BusinessTechnology by Year-End , 2001 (in billions)

US

$495.68

Germany

$73.97

UK

$65.72

France

$53.98

Canada

$30.62

Italy

$26.35

China

$19.81

Japan

$19.81

Netherlands

$17.38

Australia

$16.89

Source: International Data Corporation (IDC), 2001

033397 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

46

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

Investment bank Salomon Smith Barney has broken out the leaders in theentry- or appliance-server market – vendors of those servers that areprimarily used as web servers or for network access purposes and webcaching. Note that this is only a small portion of the web hardware market.

As an indication of the leaders in the e-business software market, IDC hasbroken out the $2.2 billion market for Java application server software, byleading vendor. This software is typically used on high-end servers thathandle e-commerce and other website transactions. In 2000, BEA Systemswas the leader with an 18% market share, followed by IBM at 15% and Sunand Oracle, each with an approximate 8% share.

Leading Vendors in the Entry Server Market*, byRevenues, 2001 (in billions and as a % of marketshare)

Sun Microsystems

$4.86 (44.4%)

Hewlett-Packard

$2.08 (18.9%)

IBM

$1.49 (13.6%)

Compaq

$1.20 (10.9%)

Fujitsu

$0.25 (2.2%)

NCR

$0.08 (0.7%)

Data General

$0.05 (0.5%)

NEC

$0.01 (0.1%)

Others

$0.92 (8.4%)

Total

$10.94 (99.8%)

Note: *including PCsSource: International Data Corporation (IDC), Salomon Smith Barney, 2001

033441 ©2001 eMarketer, Inc. www.eMarketer.com

IIMethodology

I Worldwide IT Spending

II North America 47

A. North America IT Spending forecasts 48

B. Impact of the September 11th Terrorist Atttacks 52

C. IT Budgeting in North America 55

D. Information Technology’s Place in the US Economy 56

III Europe

IV Asia-Pacific

V Latin America

VI IT Spending by Industry

VII IT Spending by Business Size

VIII IT Budgeting and Spending Surveys

Index of Charts

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

47

The IT Spending Report

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

48

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

A. North American IT Spending ForecastsThe Aberdeen Group has forecast that North American IT spending willgrow from $492.29 billion in 2001 to $681.78 billion by 2005.

A comparative estimate by Global Industry Analysts forecasts NorthAmerican IT spending on the equipment market alone will be $521.86billion in 2001 and $656.03 billion by 2005. Growth in the US market isexpected to be 8.04% in 2001, down from 9.38% in 2000. In 2002, ITequipment spending is forecast to grow 7.0% in the United States.

IT Spending Forecast for North America, 2001-2005 (inbillions)

2001

$30.29

$462.00

2002

$32.66

$501.27

2003

$35.27

$545.13

2004

$38.27

$590.10

2005

$41.52

$640.26

Canada US

Source: Aberdeen Group, May 20001

030030 ©2001 eMarketer, Inc. www.eMarketer.com

©2001 eMarketer, Inc. Reproduction of information sourced as eMarketer is prohibited without prior, written permission.Note: all data in this report (other than that sourced as eMarketer) was obtained from published, publicly available information.

49

The IT Spending Report

Methodology

Worldwide IT Spending

North America

Europe

Asia-Pacific

Latin America

IT Spending by Industry

IT Spendingby Business Size

IT Budgeting andSpending Surveys

Index of Charts

In 2001, Canada’s share of North American IT spending was 6.15% of thetotal market, according to the Aberdeen Group’s forecast. By comparison,Global Industry Analysts’ estimate for the IT equipment market placesCanada’s share at 6.88%. The research firm has gone on to predict thatCanada will experience a growth rate of 4.98% in IT equipment spending in2002, down from a rate of 5.76% in 2001.