the journal and source documents lesson 3: harmonized sales tax (hst)

TRANSCRIPT

The Journal and Source DocumentsThe Journal and Source Documents

Lesson 3Lesson 3: Harmonized Sales Tax (HST): Harmonized Sales Tax (HST)

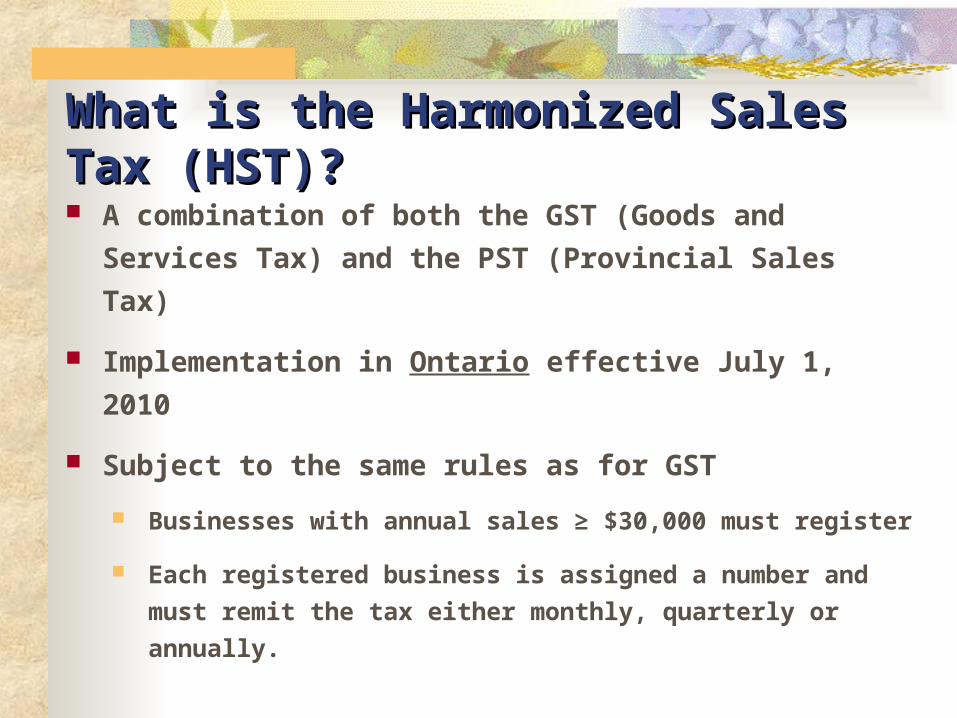

What is the Harmonized Sales Tax (HST)?What is the Harmonized Sales Tax (HST)?

A combination of both the GST (Goods and

Services Tax) and the PST (Provincial Sales Tax)

Implementation in Ontario effective July 1, 2010

Subject to the same rules as for GST

Businesses with annual sales ≥ $30,000 must register

Each registered business is assigned a number and

must remit the tax either monthly, quarterly or

annually.

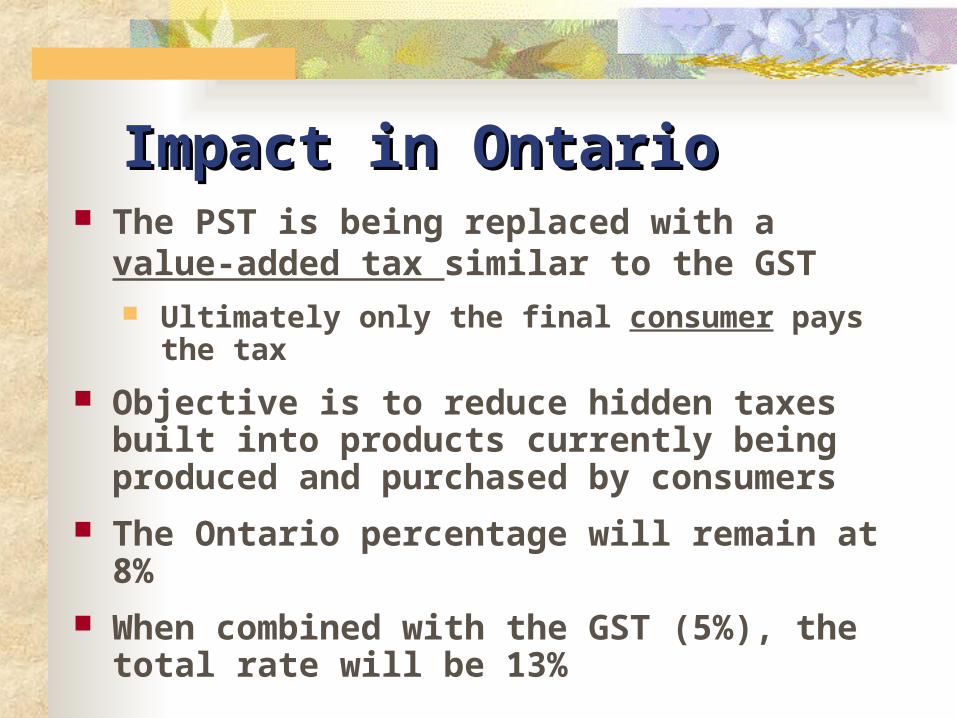

Impact in OntarioImpact in Ontario The PST is being replaced with a

value-added tax similar to the GST Ultimately only the final consumer pays the tax

Objective is to reduce hidden taxes built into products currently being produced and purchased by consumers

The Ontario percentage will remain at 8%

When combined with the GST (5%), the total rate will be 13%

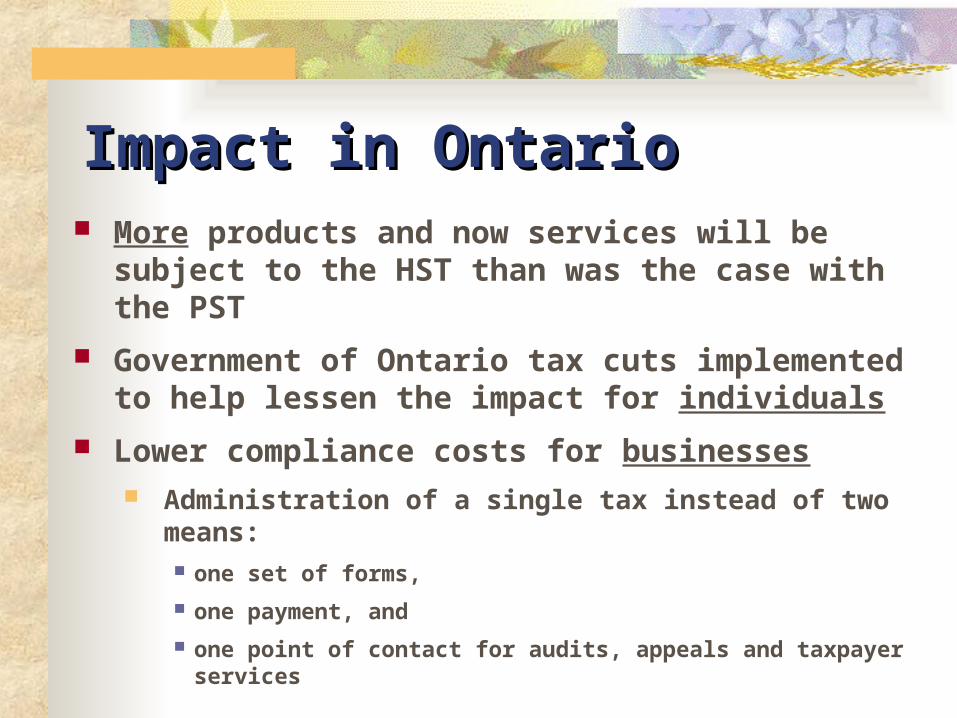

Impact in OntarioImpact in Ontario More products and now services will be subject to

the HST than was the case with the PST

Government of Ontario tax cuts implemented to help lessen the impact for individuals

Lower compliance costs for businesses Administration of a single tax instead of two means:

one set of forms,

one payment, and

one point of contact for audits, appeals and taxpayer services

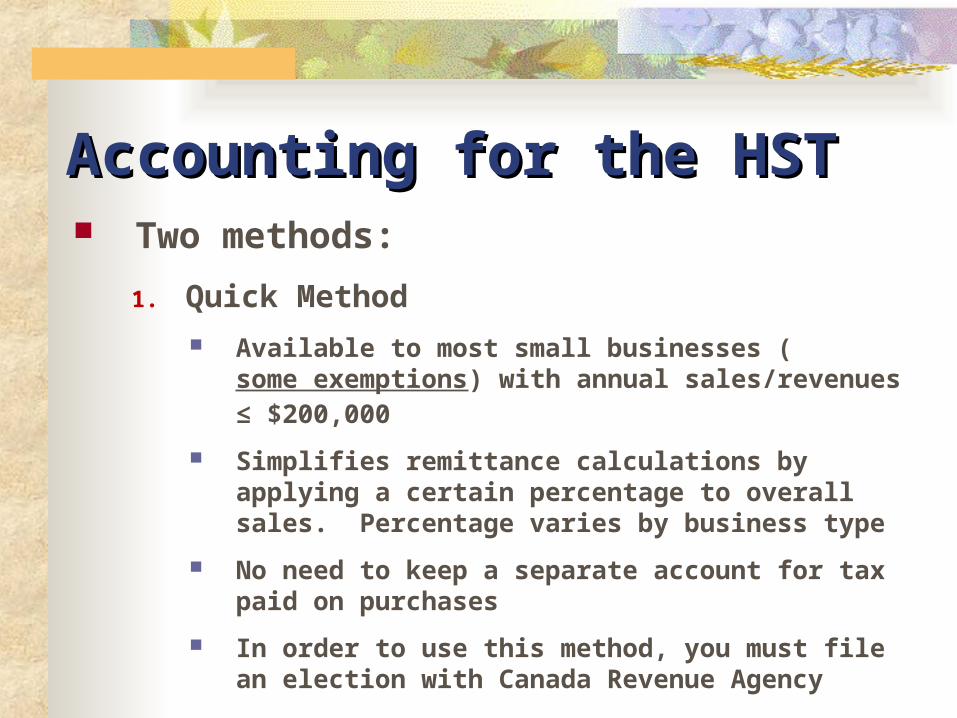

Accounting for the HSTAccounting for the HST Two methods:

1. Quick Method

Available to most small businesses (some exemptions) with annual sales/revenues ≤ $200,000

Simplifies remittance calculations by applying a certain percentage to overall sales. Percentage varies by business type

No need to keep a separate account for tax paid on purchases

In order to use this method, you must file an election with Canada Revenue Agency

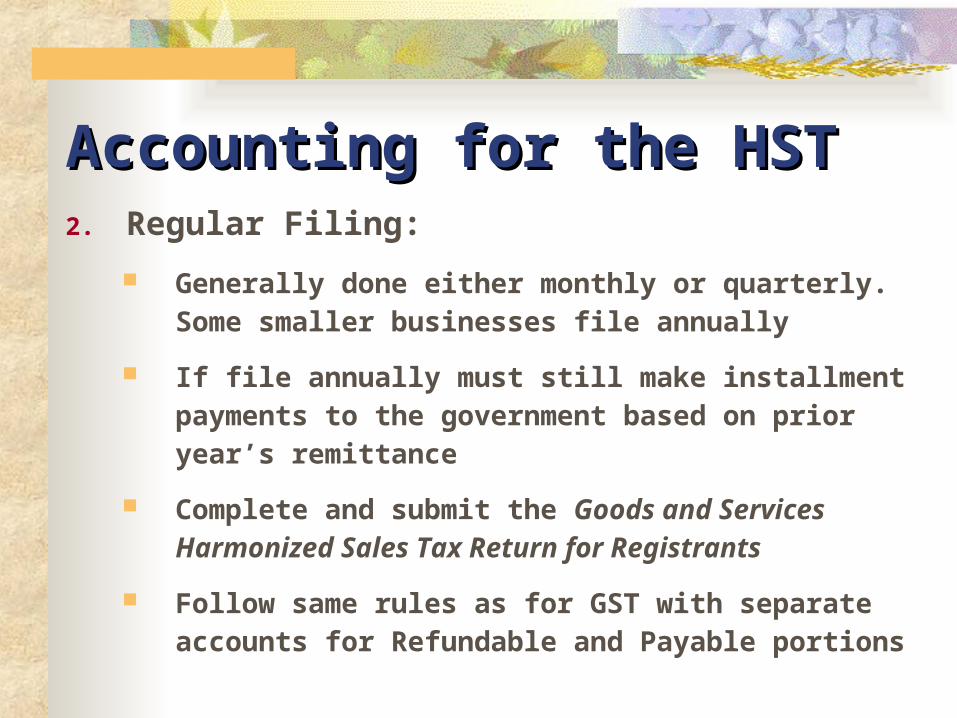

Accounting for the HSTAccounting for the HST2. Regular Filing:

Generally done either monthly or quarterly. Some smaller businesses file annually

If file annually must still make installment payments to the government based on prior year’s remittance

Complete and submit the Goods and Services Harmonized Sales Tax Return for Registrants

Follow same rules as for GST with separate accounts for Refundable and Payable portions

Accounting for the HSTAccounting for the HST Can claim rebate (Input Tax Credit – ITC) for the

amount of HST paid on items purchased for business purposes

In effect, costs of purchases will increase but rebate/ITC claimed

Note that the increased short term cost may cause some cash flowcash flow issues for smaller businesses

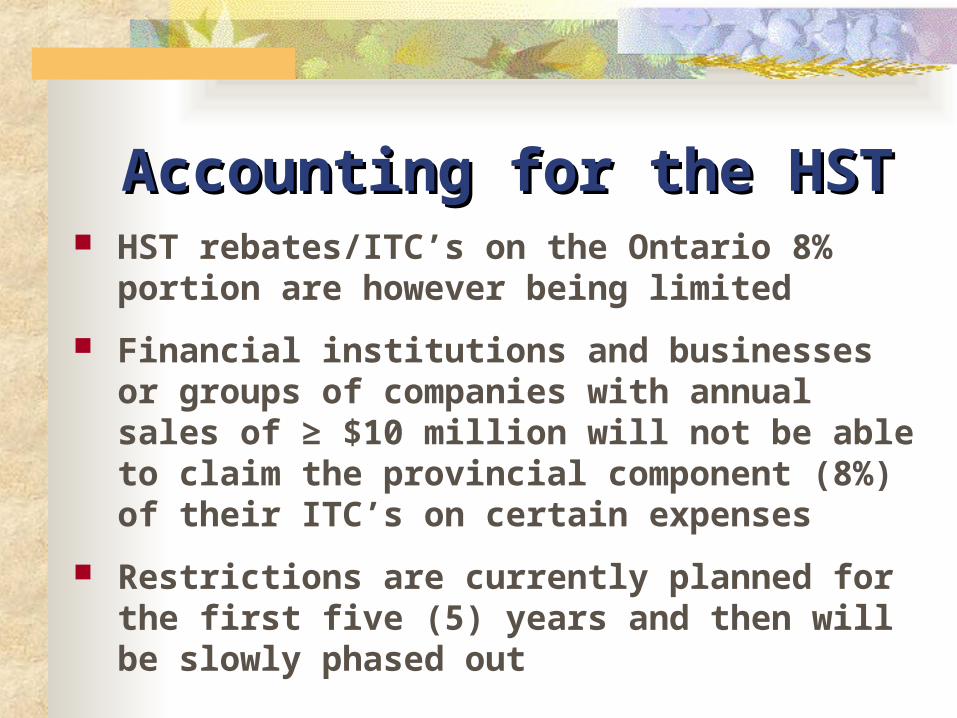

Accounting for the HSTAccounting for the HST HST rebates/ITC’s on the Ontario 8% portion

are however being limited

Financial institutions and businesses or groups of companies with annual sales of ≥ $10 million will not be able to claim the provincial component (8%) of their ITC’s on certain expenses

Restrictions are currently planned for the first five (5) years and then will be slowly phased out

Two Parts to the HSTTwo Parts to the HST

1. SALES and the HST

The tax is added to the customer’s invoice,

collected from the customer, and remitted

(sent) to the government. The sale can only take place one of two

ways:

1. Pay now (Bank)

2. Pay Later (Accounts Receivable)

Two Parts to the HSTTwo Parts to the HST2. PURCHASES and the HST

All businesses are entitled to recover the GST portion (5%) charged by their suppliers.

Most businesses are entitled to recover the PST portion (8%) charged by their suppliers. (See previous restrictions discussed)

For teaching purposes we will always assume that the PST is recoverable by businesses.

Businesses have to pay the tax to the supplier, but are entitled to recover this tax from the government.

The purchases can only take place one of two ways:

1. Pay now (Bank)

2. Pay Later (Accounts Payable)

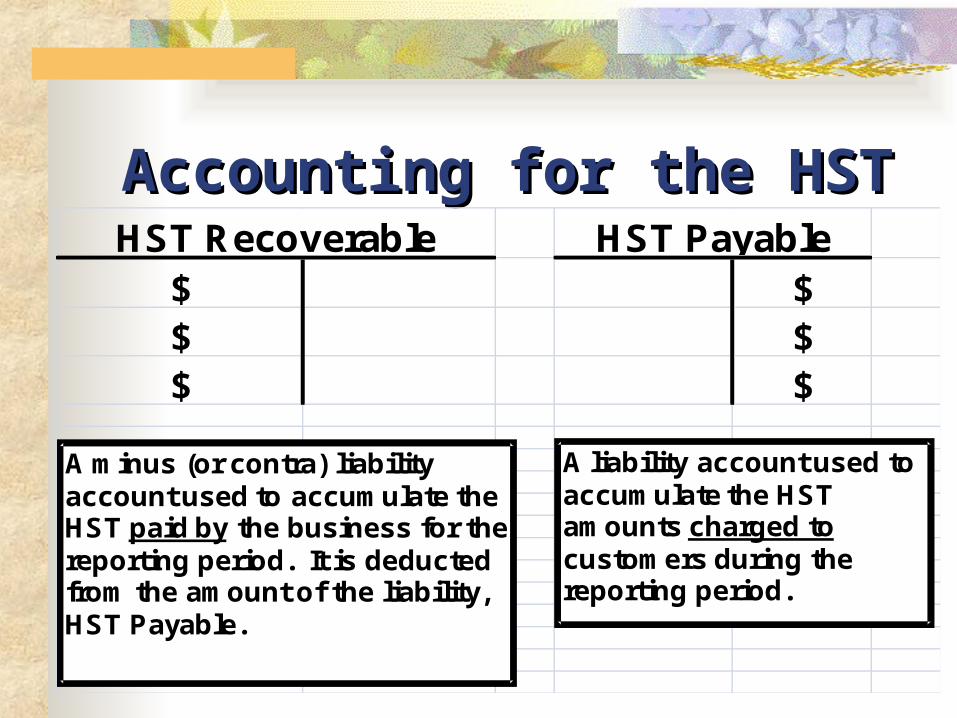

Accounting for the HSTAccounting for the HST There are two accounts for HST in the

ledger:

HST Recoverable, and

HST Payable

Accounting for the HSTAccounting for the HST

$ $$ $$ $

HST Recoverable HST Payable

A minus (or contra) liability account used to accumulate the HST paid by the business for the reporting period. It is deducted from the amount of the liability, HST Payable.

A liability account used to accumulate the HST amounts charged tocustomers during the reporting period.

Accounting for the HSTAccounting for the HST

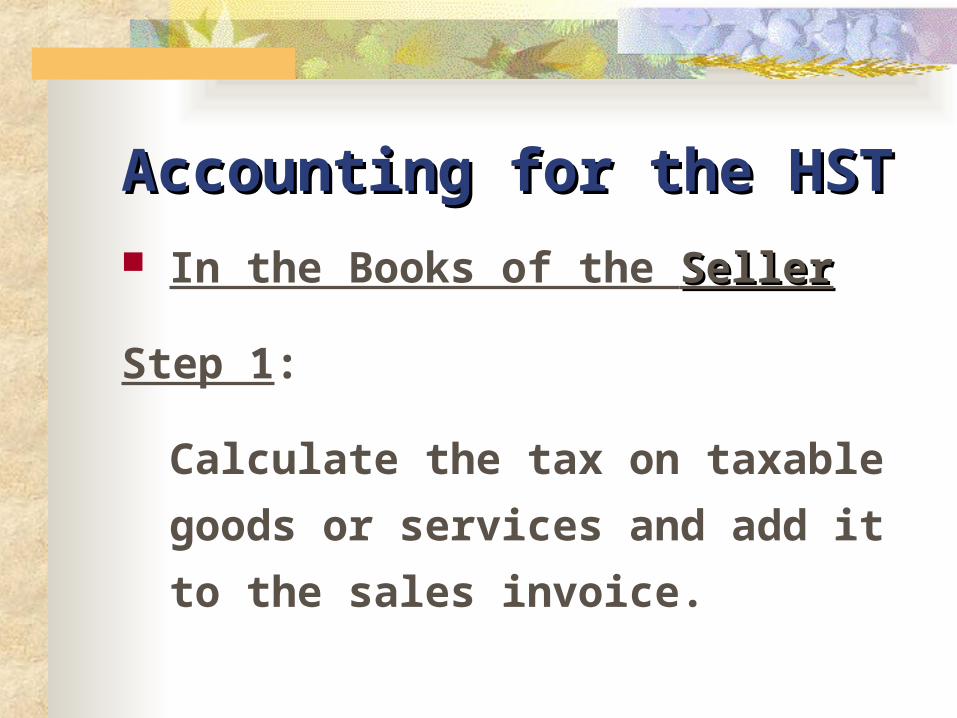

In the Books of the SellerSeller

Step 1:

Calculate the tax on taxable goods or

services and add it to the sales invoice.

HST Number

HST

SPARKLES CLEANERS123 Any StreetAny Town, ONA1B 2C3 Invoice: 777

Phone: (123) 456-7890 FAX: (123) 456-0987

To: ABC Bank987 Any StreetAny Town, ONB2C 3D4

For: Cleaning and maintenance 1,800$ services for September 20--

Total 2,034$

HST #: R007512392 TERMS: Net 30 Date: Sept. 25, 20--

HST (13%) 234

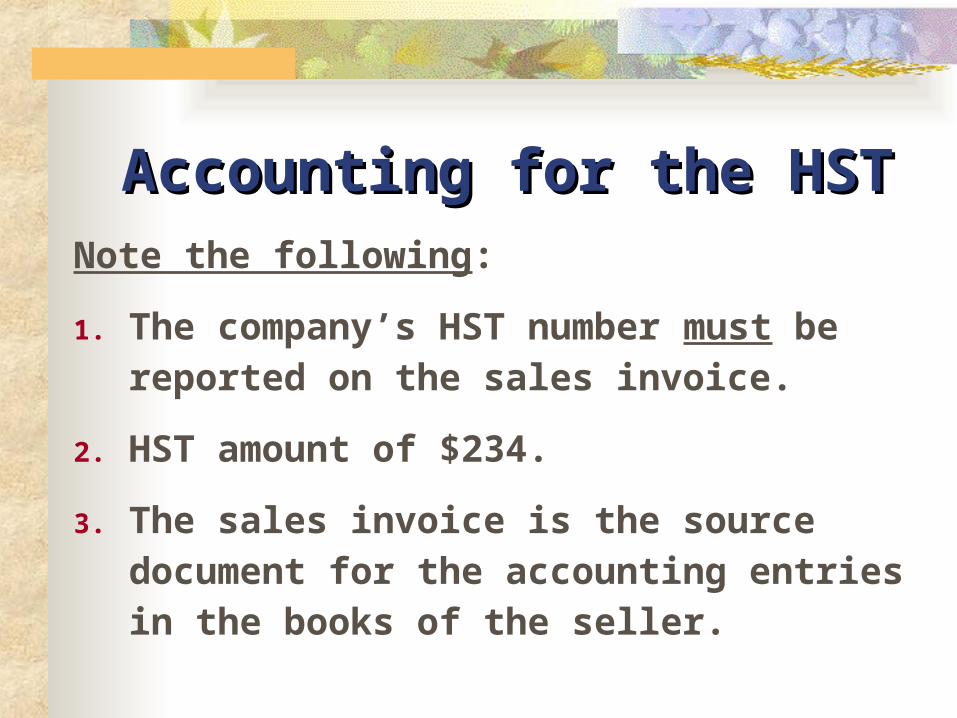

Accounting for the HSTAccounting for the HSTNote the following:

1. The company’s HST number must be reported on the sales invoice.

2. HST amount of $234.

3. The sales invoice is the source document for the accounting entries in the books of the seller.

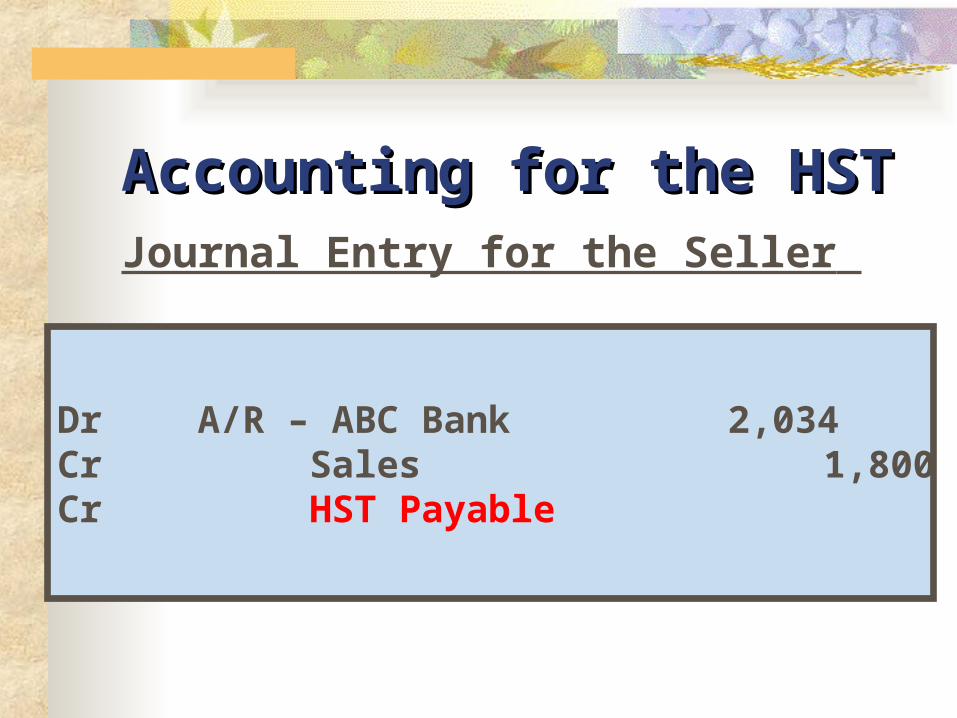

Accounting for the HSTAccounting for the HSTJournal Entry for the Seller

Dr A/R – ABC Bank 2,034Cr Sales 1,800Cr HST Payable 234

Accounting for the HSTAccounting for the HST

In the Books of the Purchaser

Sparkles Cleaners is not just the seller of services.

In some instances it is the purchasing company

receiving the sales invoices of other companies.

In the hands of a purchaser, these are

purchase invoices.

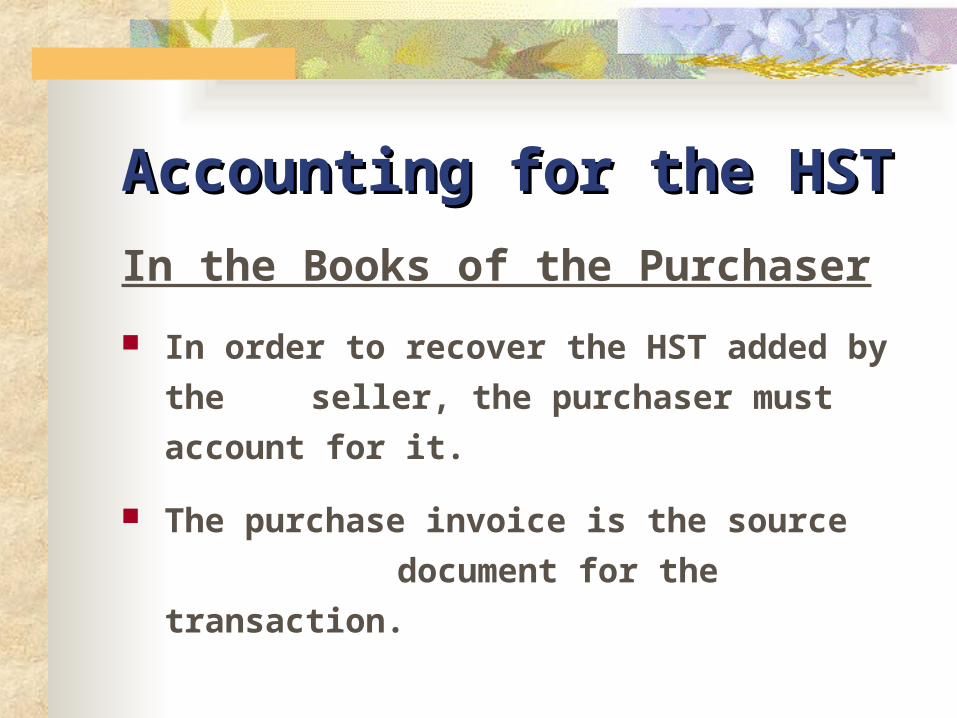

Accounting for the HSTAccounting for the HST

In the Books of the Purchaser

In order to recover the HST added by the

seller, the purchaser must account for it.

The purchase invoice is the source

document for the transaction.

THE SUPPLY HOUSEBox 2000 INVOICE Sometown, Ontario NUMBER N7S 5R6

Phone: 234-5678 Fax: 234-5686

Sparkles Cleaners123 Any StreetAny Town, ONA1B 2C3

For 20 pkg computer printing paper @ $30 each $600.00

HST (13%) $78.00Total $678.00

HST No. 113956554 Terms Net 60 Date: March 24, 20--

To

257

Accounting for the HSTAccounting for the HSTIn the Books of the Purchaser (Sparkles Cleaners):

Dr Office Supplies 600.00Dr HST Recoverable 78.00Cr A/P – The Supply House 678.00

Remitting the HSTRemitting the HST Most businesses are required to file

monthly and must remit the net tax

owed within one month following the

end of their reporting period.

Refer to the example on the next slide:

Remitting the HSTRemitting the HST

Calculate the difference:

HST Payable – HST Recoverable

$2,309.65 - $1,567.90

= $741.75 (owed toowed to the government)

Note:

If this is a negative amount, the company will receive a refundrefund cheque from the Federal government.

1,567.90 2,309.65 HST Recoverable HST Payable

Remitting the HSTRemitting the HSTMake the Journal Entry

Dr HST Payable 2 309.65Cr HST Recoverable 1 567.90Cr Bank 741.75

HST on the Balance SheetHST on the Balance Sheet The smaller account balance is subtracted from the

larger.

If the difference is a CREDITCREDIT, it is shown in the Liabilities section.

If the difference is a DEBITDEBIT, it may be shown in the Assets section.

However, most computer-generated balance sheets, will show a debit balance as a negative number in the liabilities section.

HST on the Balance SheetHST on the Balance Sheet

LiabilitiesAccounts Payable 4,572$ HST Payable 875$ Less HST Recoverable 468 407 Bank Loan 6,275 Total Liabilities 11,254$

Any Company

April 30, 20--Balance Sheet (Partial Only)