the light commercial vehicle surge in europe – when · pdf filethe light commercial...

TRANSCRIPT

The Light Commercial Vehicle Surgein Europe – When Will the Tide Break?

Grischa Meyer

Market Analyst, Light Commercial Vehicles

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 2

• Focus: Light Commercial Vehicles (LCVs) up to 6t GVW

• Defining the LCV Sector by Segment

• The Notion of ‛Light Trucks’

• Global Segment Sales Trends of LCVs

• Western Europe Segment Perspective of the LCV Sector

• What Are the Market Drivers in Western Europe?

• When Will the Tide Break?

• Questions

Presentation Outline

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 3

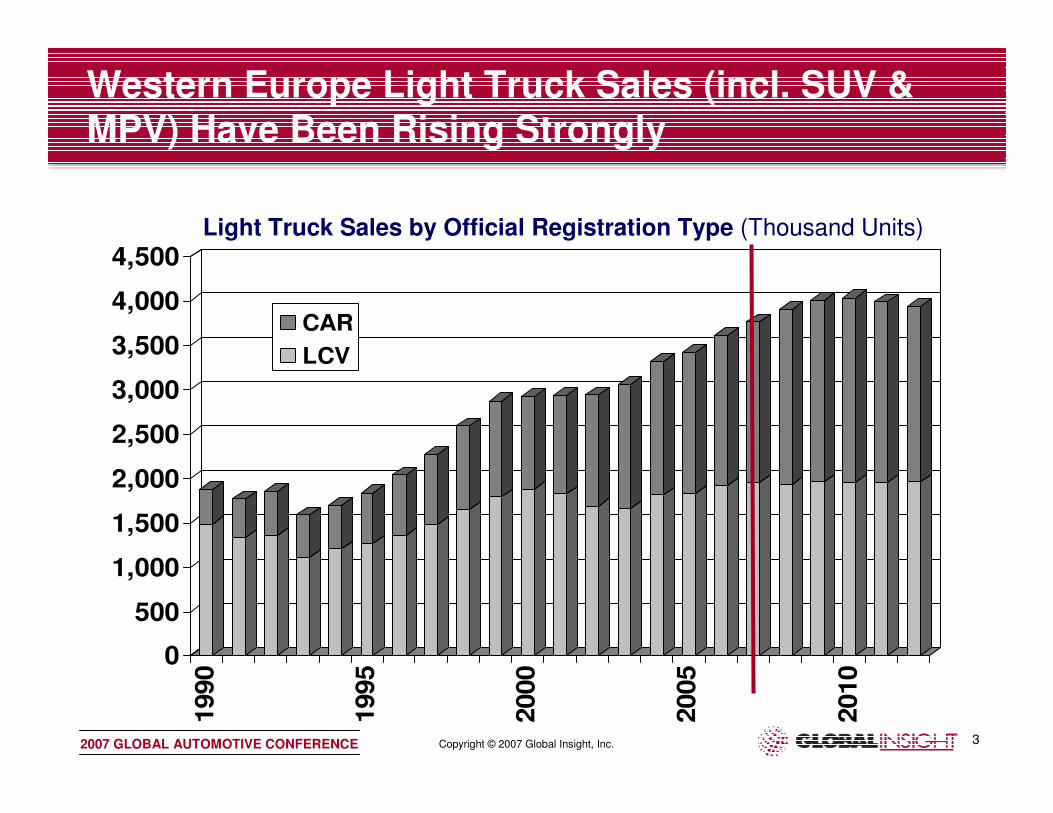

Western Europe Light Truck Sales (incl. SUV & MPV) Have Been Rising Strongly

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1990

1995

2000

2005

2010

CAR

LCV

Light Truck Sales by Official Registration Type (Thousand Units)

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 4

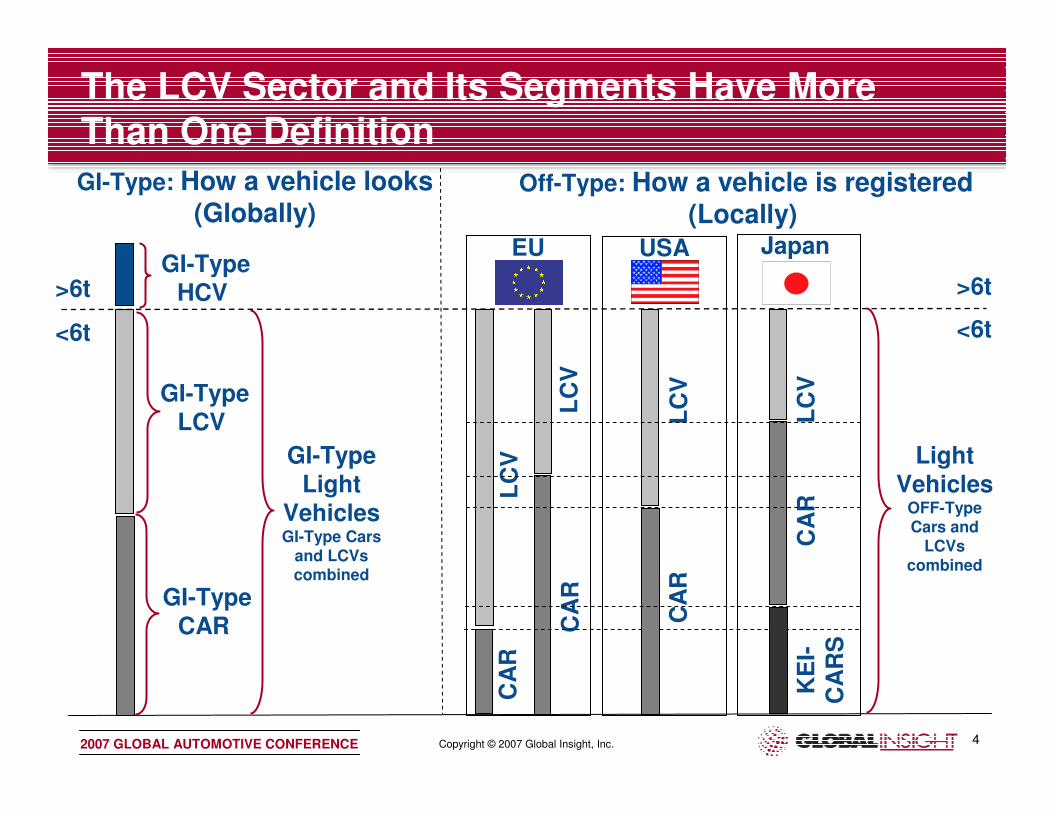

The LCV Sector and Its Segments Have More Than One Definition

GI-Type HCV

GI-Type Light

VehiclesGI-Type Cars

and LCVs combined

GI-Type: How a vehicle looks (Globally)

GI-Type LCV

GI-Type CAR

Off-Type: How a vehicle is registered (Locally)

<6t

>6t

<6t

>6t

Light Vehicles

OFF-Type Cars and

LCVs combined

EU USA Japan

CA

RL

CV

CA

RL

CV

CA

RL

CV

LC

VC

AR

KE

I-C

AR

S

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 5

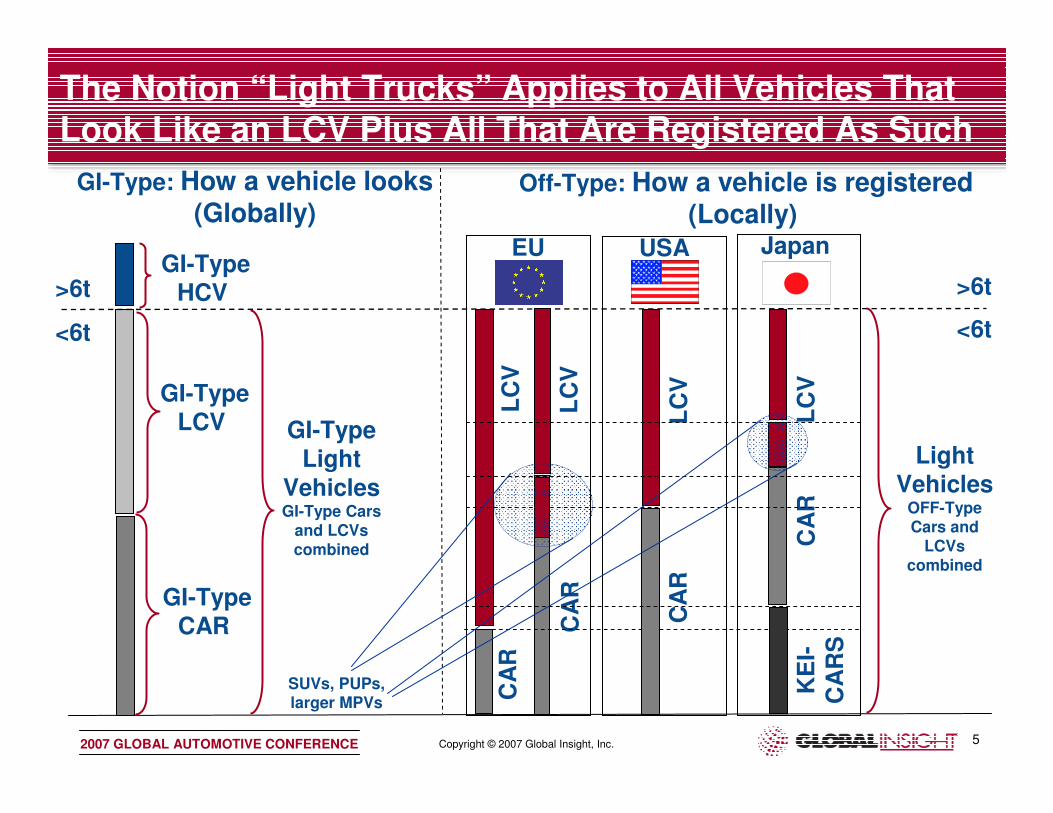

The Notion “Light Trucks” Applies to All Vehicles That Look Like an LCV Plus All That Are Registered As Such

GI-Type HCV

GI-Type Light

VehiclesGI-Type Cars

and LCVs combined

GI-Type LCV

GI-Type CAR

<6t

>6t

<6t

>6t

Light Vehicles

OFF-Type Cars and

LCVs combined

EU USA Japan

CA

RL

CV

CA

RL

CV

CA

RL

CV

LC

VC

AR

KE

I-C

AR

S

SUVs, PUPs, larger MPVs

GI-Type: How a vehicle looks (Globally)

Off-Type: How a vehicle is registered (Locally)

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 6

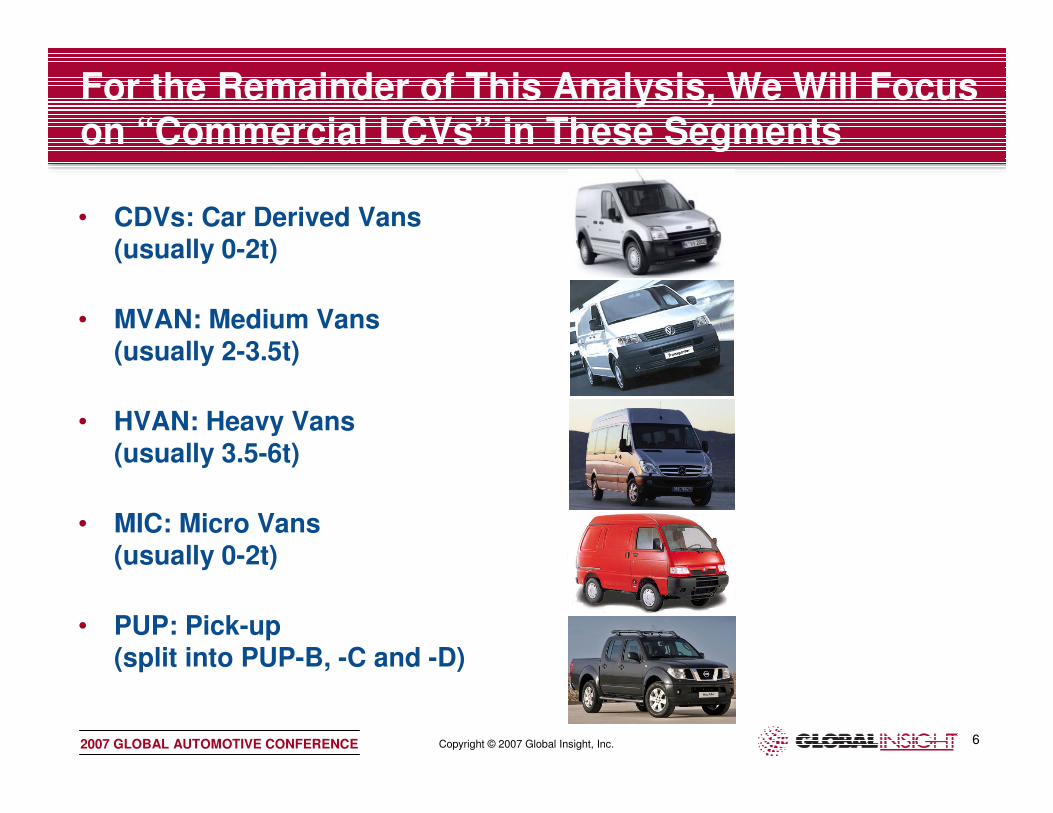

• CDVs: Car Derived Vans (usually 0-2t)

• MVAN: Medium Vans (usually 2-3.5t)

• HVAN: Heavy Vans(usually 3.5-6t)

• MIC: Micro Vans(usually 0-2t)

• PUP: Pick-up(split into PUP-B, -C and -D)

For the Remainder of This Analysis, We Will Focus on “Commercial LCVs” in These Segments

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 7

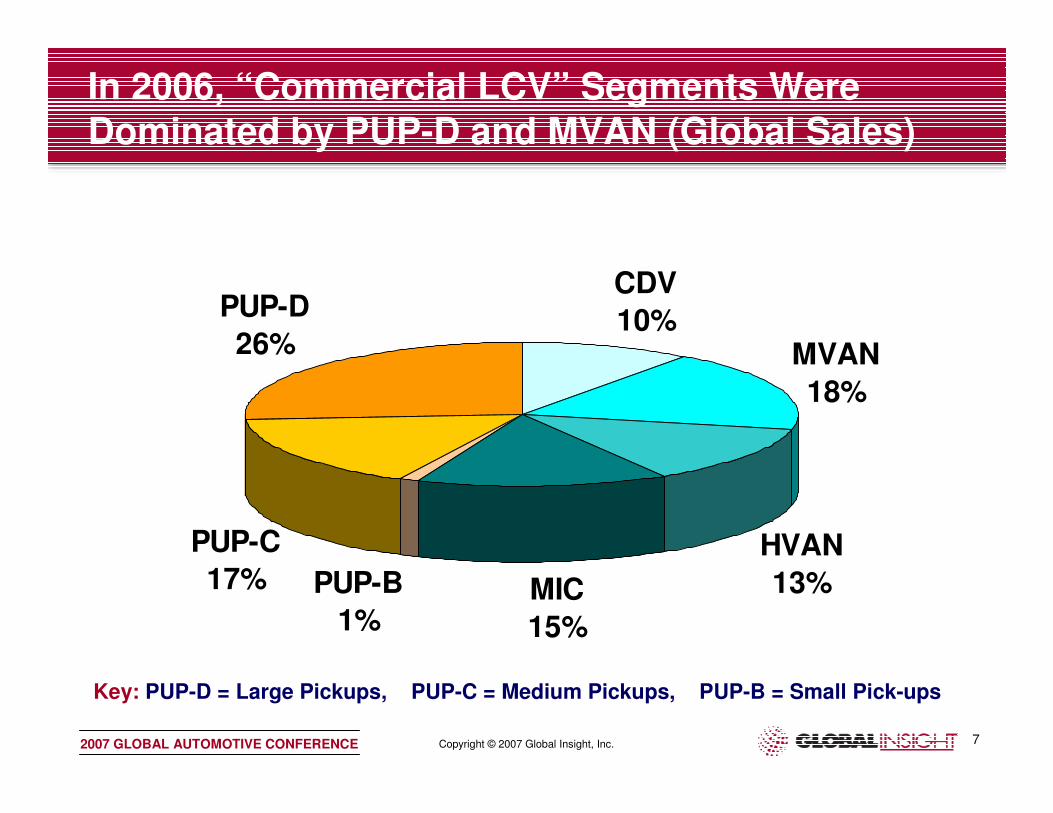

CDV

10%MVAN

18%

HVAN

13%MIC

15%

PUP-B

1%

PUP-C

17%

PUP-D

26%

Key: PUP-D = Large Pickups, PUP-C = Medium Pickups, PUP-B = Small Pick-ups

In 2006, “Commercial LCV” Segments Were Dominated by PUP-D and MVAN (Global Sales)

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 8

0

500

1 000

1 500

2 000

PUP-C CDV MVAN

0

500

1 000

1 500

2 000

MVAN CDV PUP-C

0

500

1 000

1 500

2 000

PUP-C PUP-B CDV

0

500

1 000

1 500

2 000

MVAN CDV PUP-B

0

500

1 000

1 500

2 000

MIC HVAN PUP-C

0

500

1,000

1,500

2,000

2,500

3,000

PUP-D PUP-C HVAN

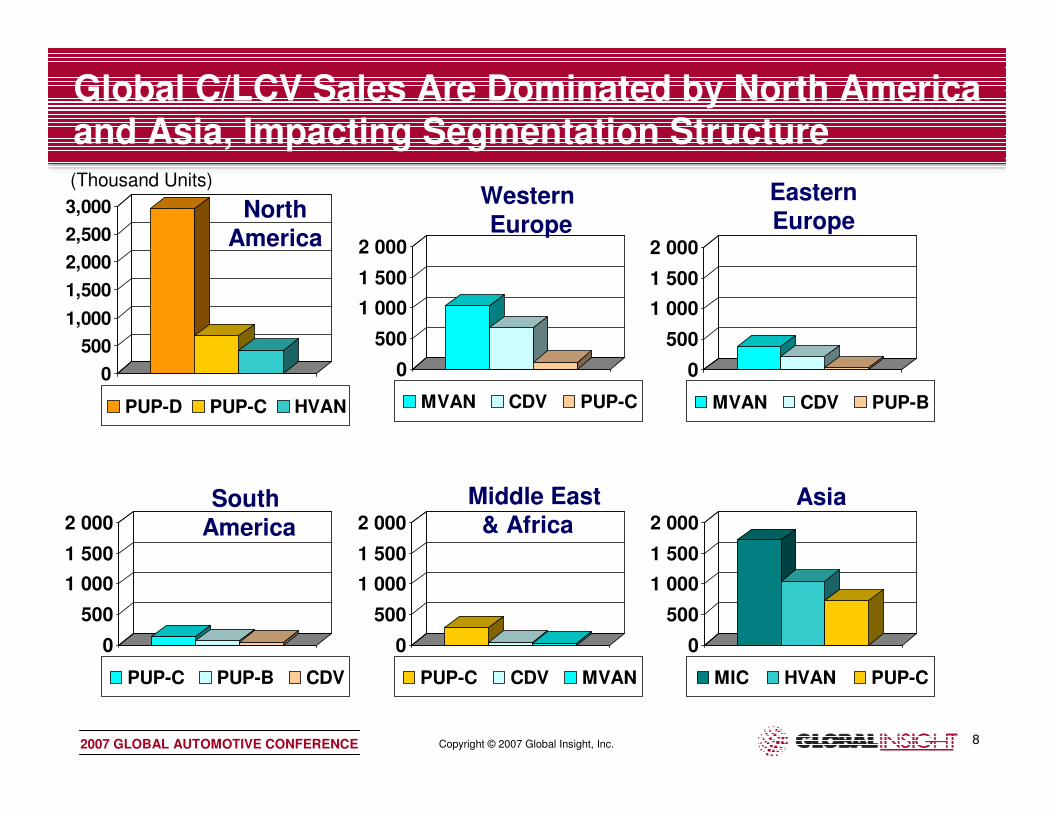

NorthAmerica

South

America

Western

Europe

EasternEurope

Middle East& Africa

Global C/LCV Sales Are Dominated by North America and Asia, Impacting Segmentation Structure

Asia

(Thousand Units)

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 9

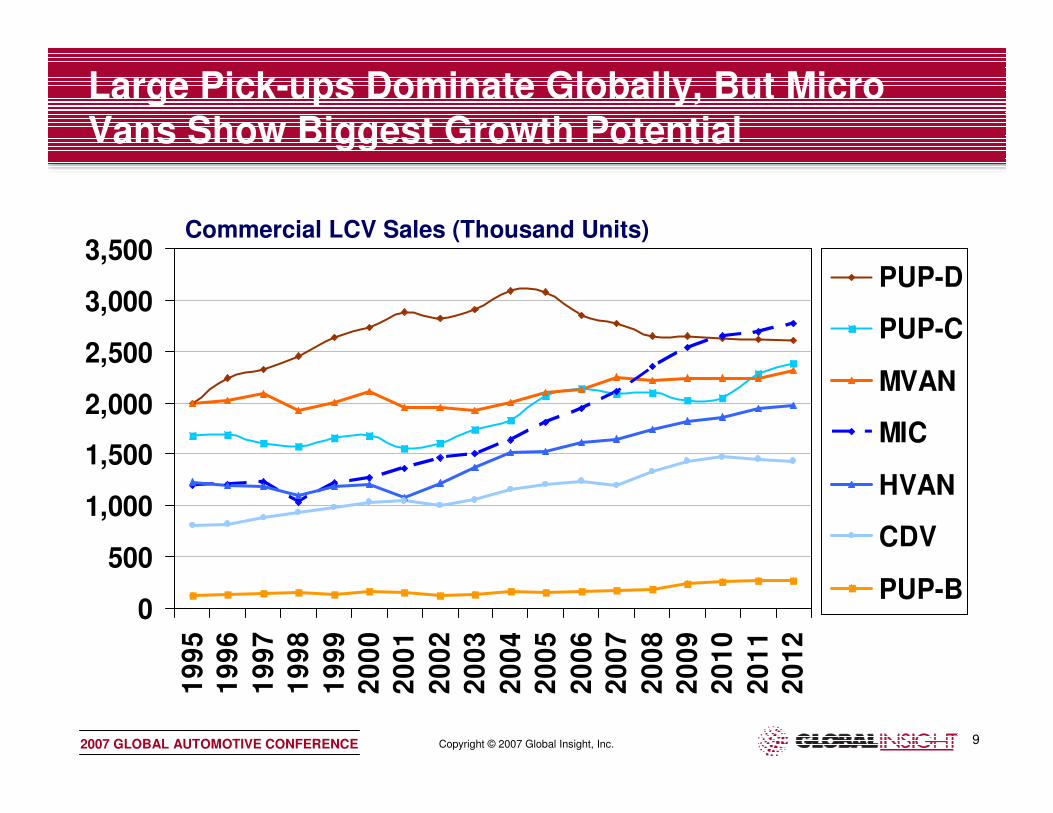

Large Pick-ups Dominate Globally, But Micro Vans Show Biggest Growth Potential

0

500

1,000

1,500

2,000

2,500

3,000

3,500

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

PUP-D

PUP-C

MVAN

MIC

HVAN

CDV

PUP-B

Commercial LCV Sales (Thousand Units)

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 10

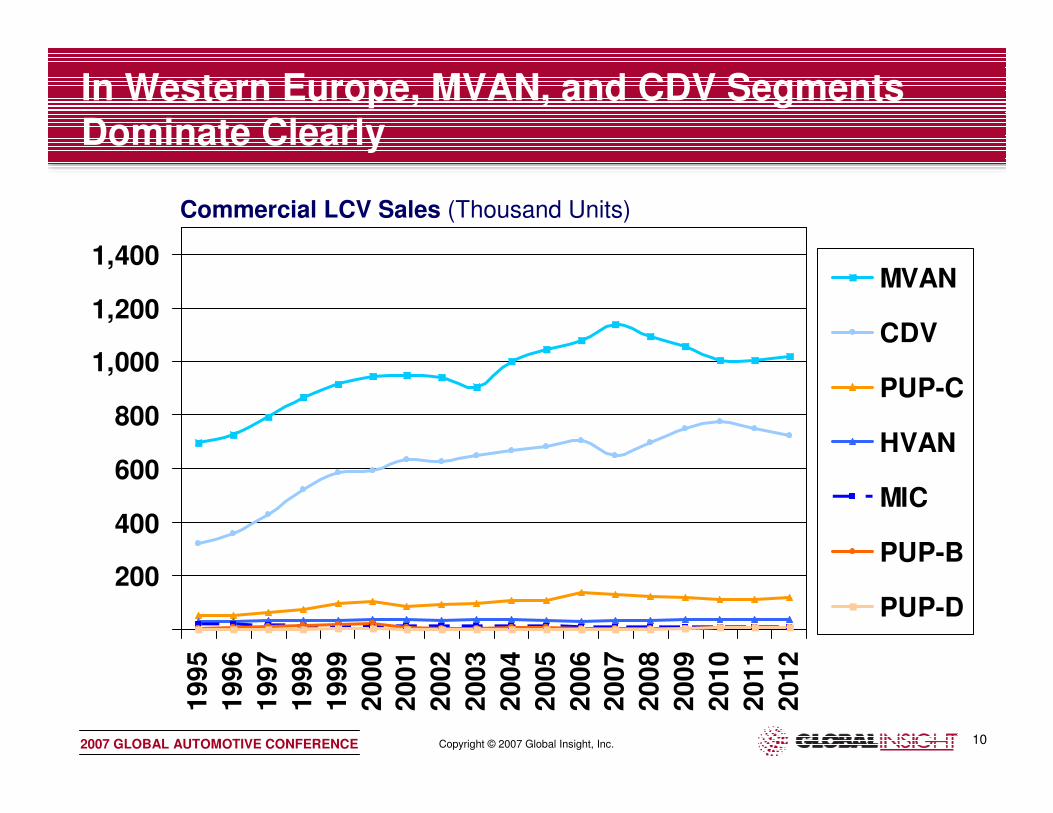

In Western Europe, MVAN, and CDV Segments Dominate Clearly

200

400

600

800

1,000

1,200

1,400

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

MVAN

CDV

PUP-C

HVAN

MIC

PUP-B

PUP-D

Commercial LCV Sales (Thousand Units)

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 11

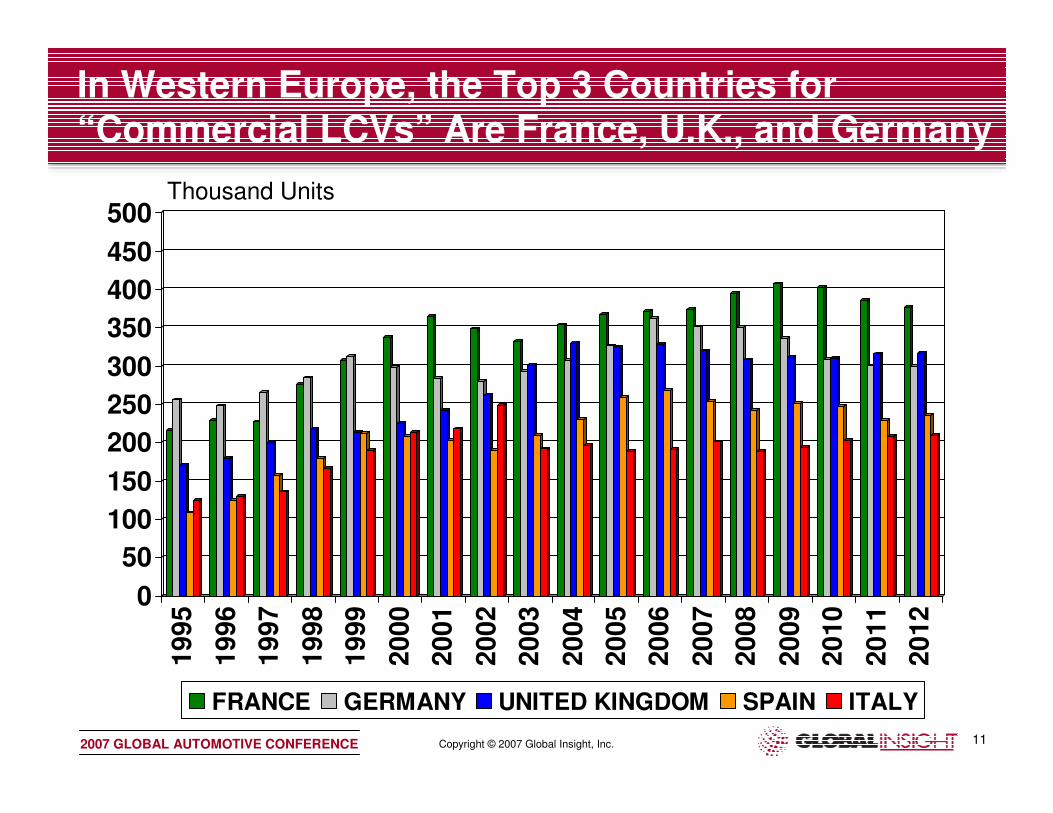

In Western Europe, the Top 3 Countries for “Commercial LCVs” Are France, U.K., and Germany

0

50

100

150

200

250

300

350

400

450

5001

995

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

FRANCE GERMANY UNITED KINGDOM SPAIN ITALY

Thousand Units

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 12

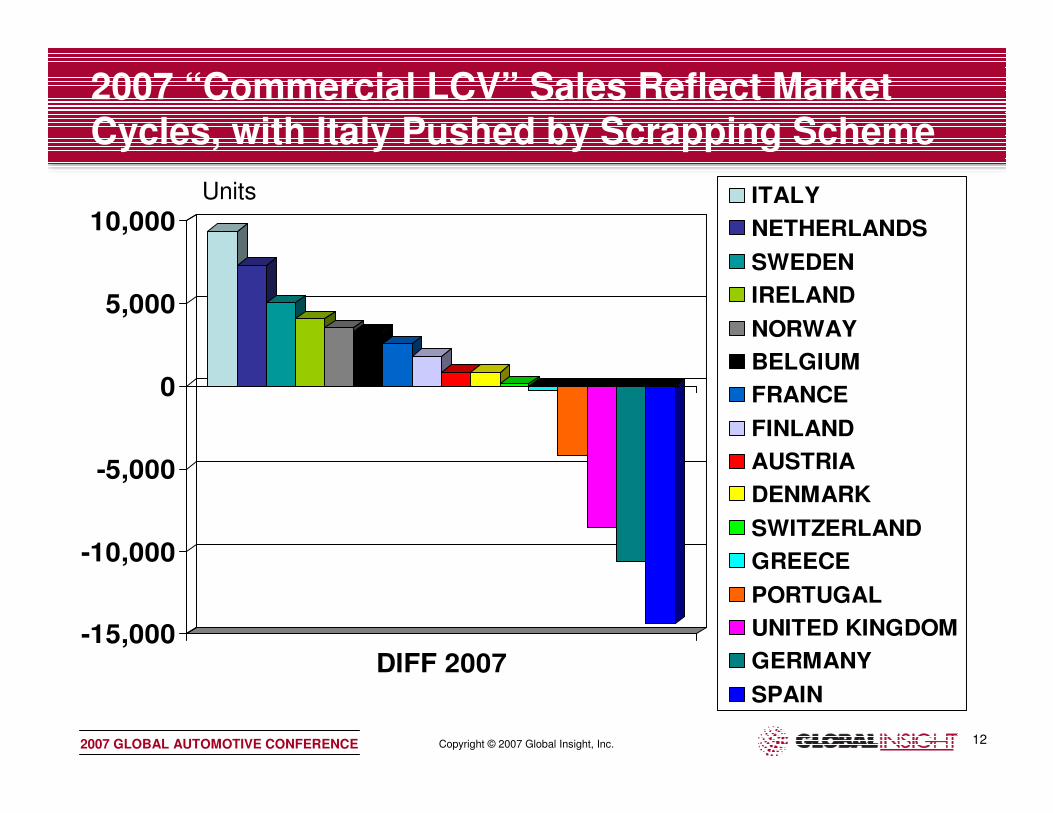

2007 “Commercial LCV” Sales Reflect Market Cycles, with Italy Pushed by Scrapping Scheme

-15,000

-10,000

-5,000

0

5,000

10,000

DIFF 2007

ITALY

NETHERLANDS

SWEDEN

IRELAND

NORWAY

BELGIUM

FRANCE

FINLAND

AUSTRIA

DENMARK

SWITZERLAND

GREECE

PORTUGAL

UNITED KINGDOM

GERMANY

SPAIN

Units

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 13

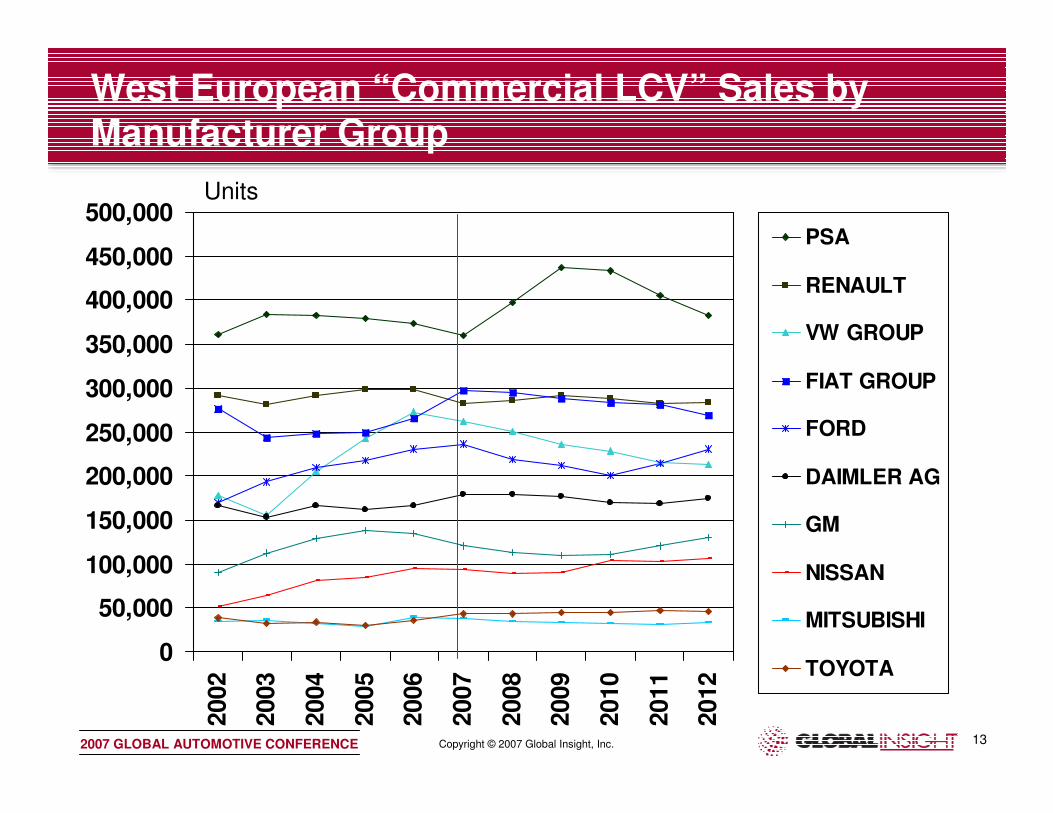

West European “Commercial LCV” Sales by

Manufacturer Group

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,0002002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

PSA

RENAULT

VW GROUP

FIAT GROUP

FORD

DAIMLER AG

GM

NISSAN

MITSUBISHI

TOYOTA

Units

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 14

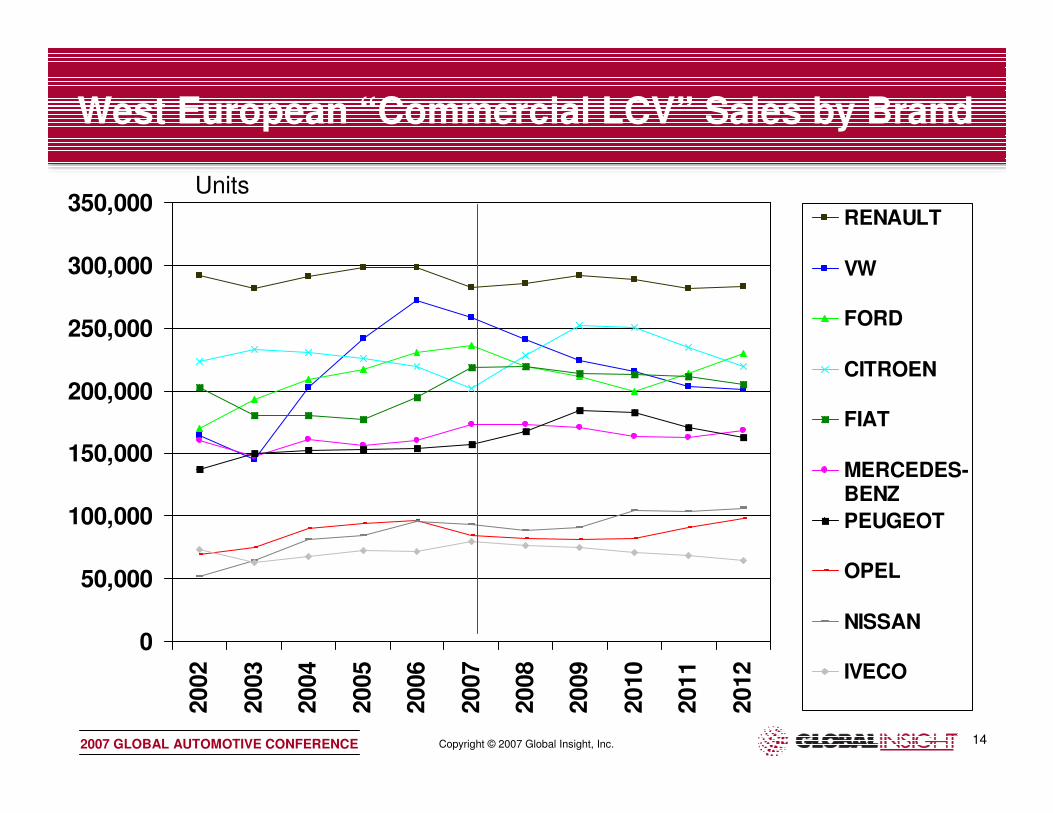

West European “Commercial LCV” Sales by Brand

0

50,000

100,000

150,000

200,000

250,000

300,000

350,0002002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

RENAULT

VW

FORD

CITROEN

FIAT

MERCEDES-BENZ

PEUGEOT

OPEL

NISSAN

IVECO

Units

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 15

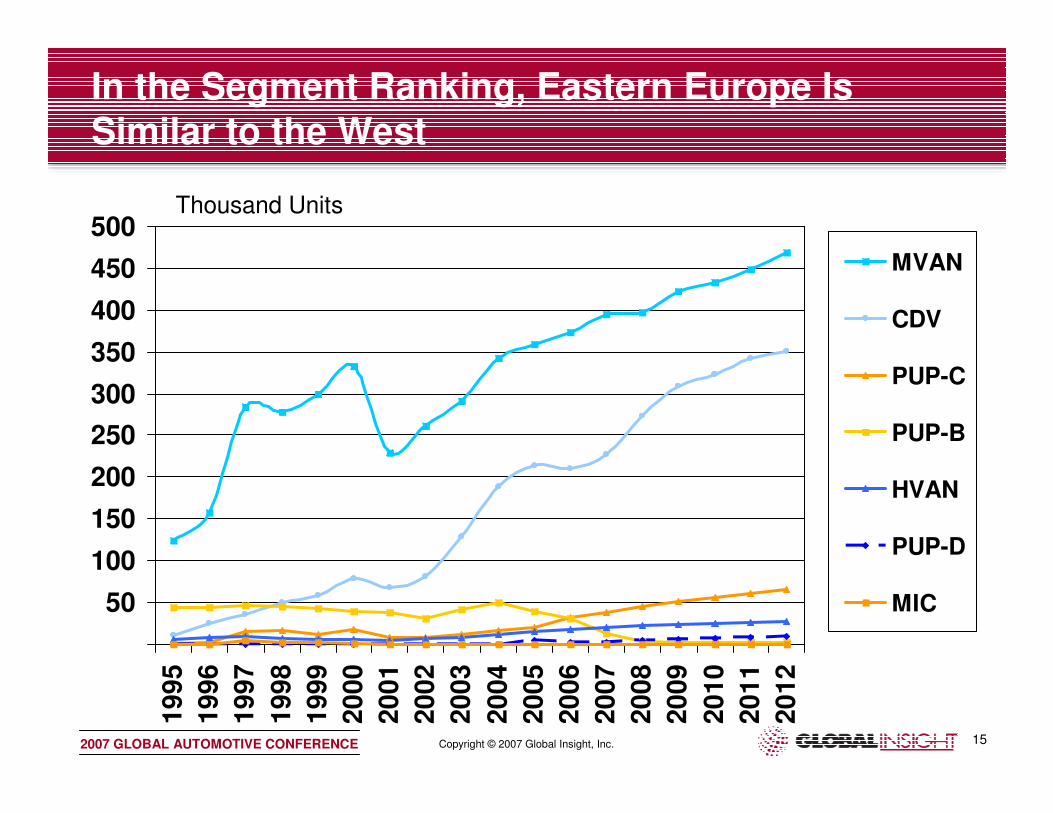

In the Segment Ranking, Eastern Europe Is Similar to the West

50

100

150

200

250

300

350

400

450

500

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

MVAN

CDV

PUP-C

PUP-B

HVAN

PUP-D

MIC

Thousand Units

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 16

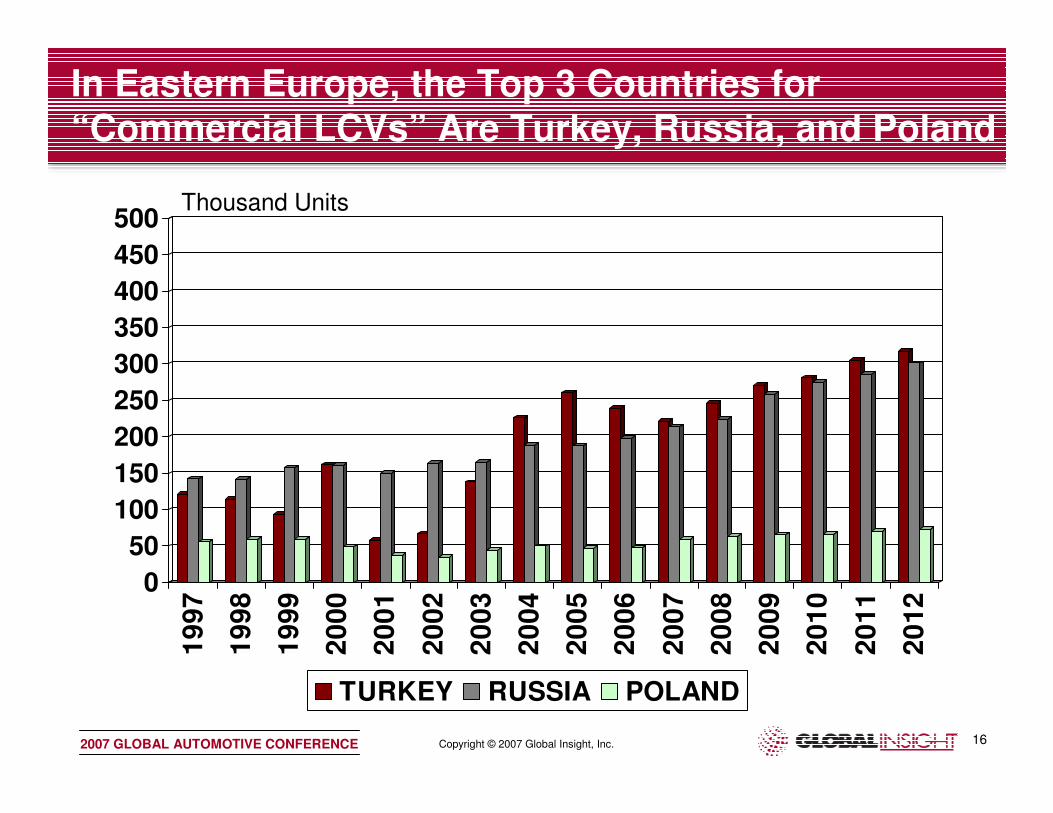

In Eastern Europe, the Top 3 Countries for “Commercial LCVs” Are Turkey, Russia, and Poland

0

50

100

150

200

250

300

350

400

450

5001

99

7

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

TURKEY RUSSIA POLAND

Thousand Units

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 17

• Short Term– (+) replacement of leading MVAN models

– (+) confidence indices are rising again since mid-2005

– (+) deep-grounded parc renewal due to imminent legislation

– (~) deteriorating economic growth in France and Spain

– (~) 99/00 transaction replacement demand cycle fades out

– (~) historically high fuel prices and tax burden

• Medium and Long Term – (-) Overall stagnating demand due to completely built-up car parc

– (+) Ongoing parc renewal before Euro-5 legislation

– (-) Technological pressure due to CO2 limitation regulations

“Commercial) LCV” sales are forecast to grow by just 1.6% in 2007

Car Substitutes are expected to expand by 8.6% in 2007

Total Light Truck forecast to grow by 4.1%

What Are the Market Drivers in the West European “Commercial LCV” Market?

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 18

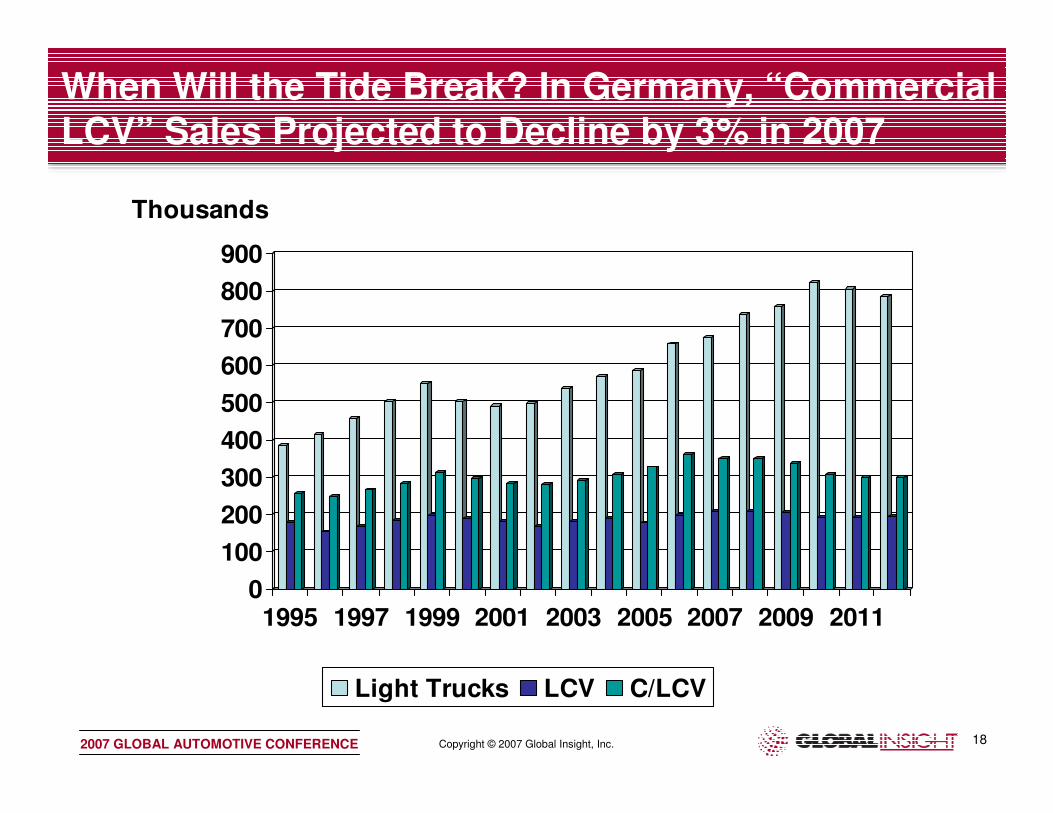

When Will the Tide Break? In Germany, “Commercial LCV” Sales Projected to Decline by 3% in 2007

0

100

200

300

400

500

600

700

800

900

Thousands

1995 1997 1999 2001 2003 2005 2007 2009 2011

Light Trucks LCV C/LCV

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 19

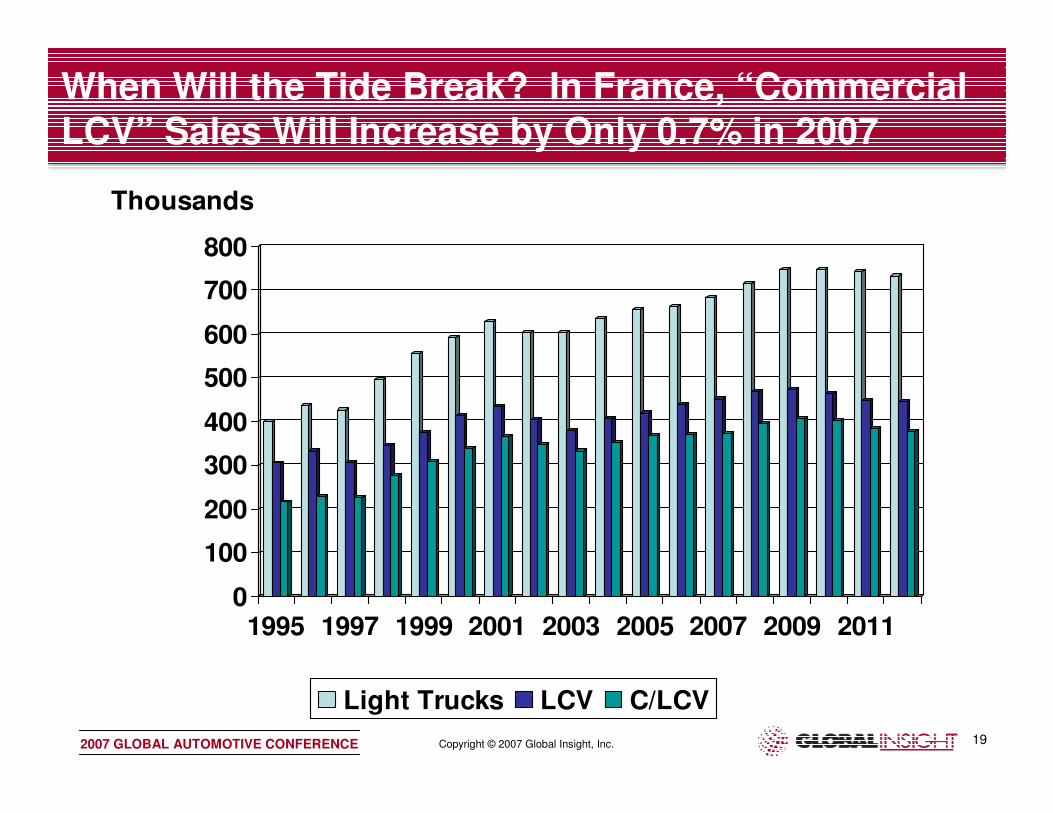

When Will the Tide Break? In France, “Commercial LCV” Sales Will Increase by Only 0.7% in 2007

0

100

200

300

400

500

600

700

800

Thousands

1995 1997 1999 2001 2003 2005 2007 2009 2011

Light Trucks LCV C/LCV

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 20

0

100

200

300

400

500

600

700

Thousands

1995 1997 1999 2001 2003 2005 2007 2009 2011

Light Trucks LCV C/LCV

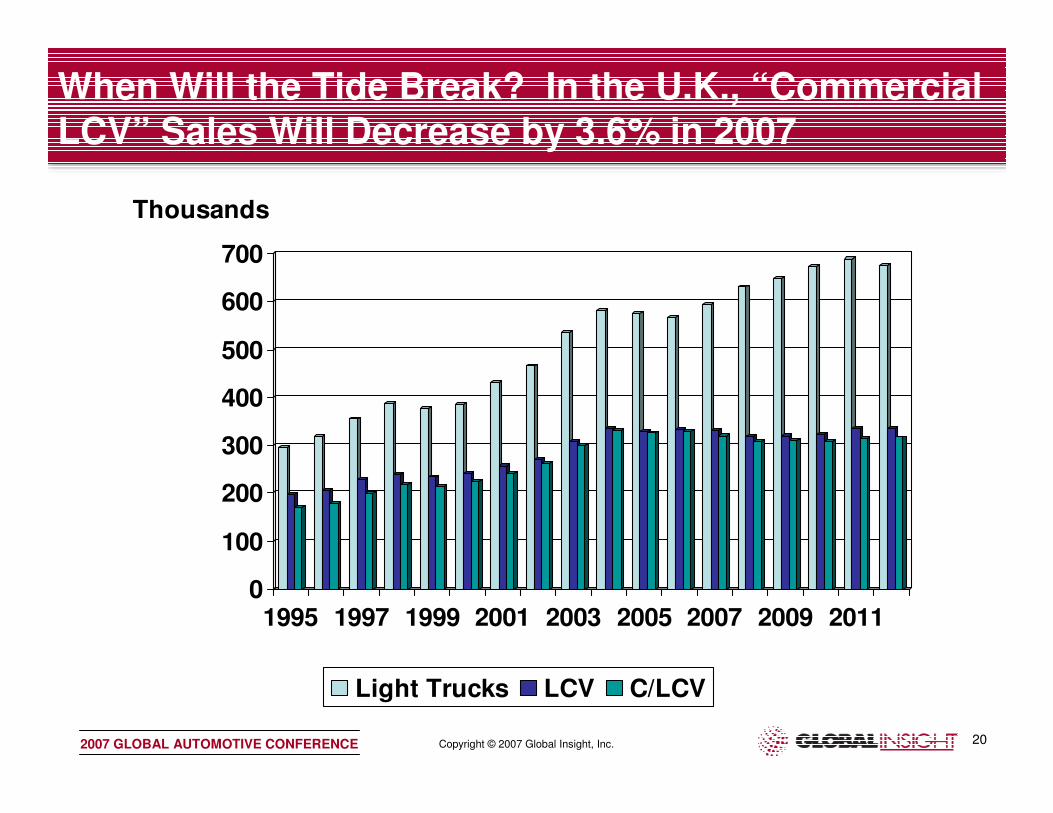

When Will the Tide Break? In the U.K., “Commercial LCV” Sales Will Decrease by 3.6% in 2007

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 21

0

100

200

300

400

500

600

Thousands

1995 1997 1999 2001 2003 2005 2007 2009 2011

Light Trucks LCV C/LCV

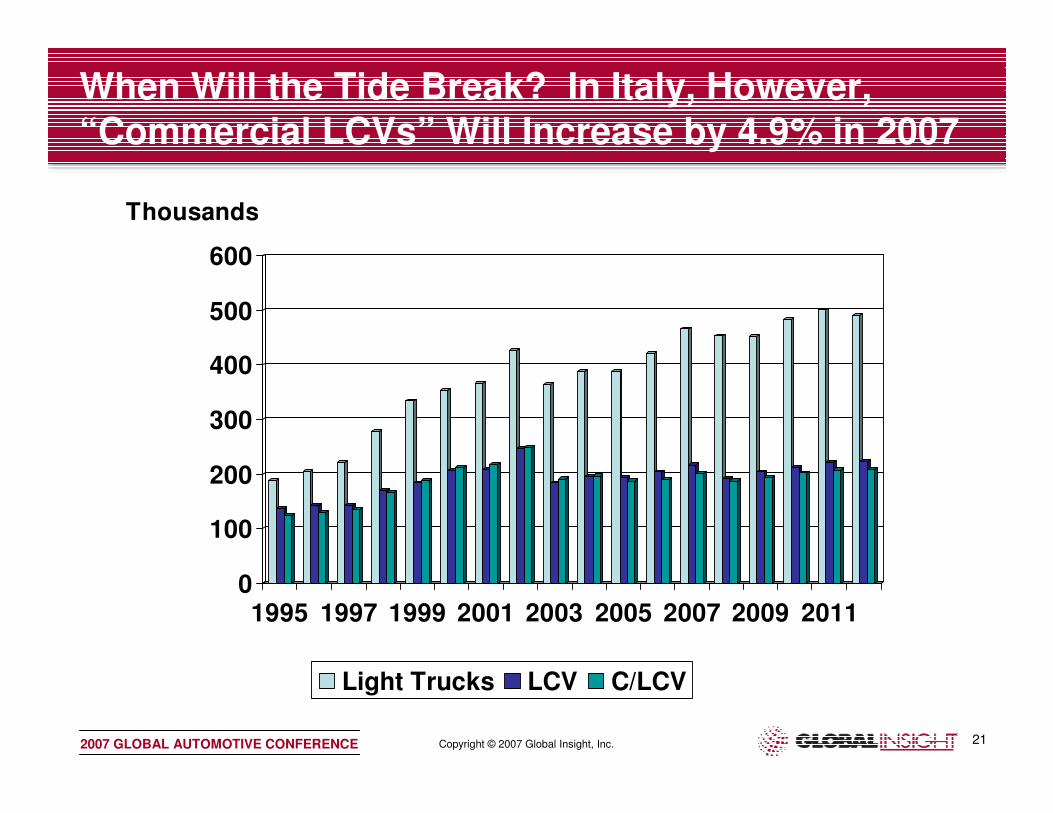

When Will the Tide Break? In Italy, However, “Commercial LCVs” Will Increase by 4.9% in 2007

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 22

0

50

100

150

200

250

300

350

400

450

500

Thousands

1995 1997 1999 2001 2003 2005 2007 2009 2011

Light Trucks LCV C/LCV

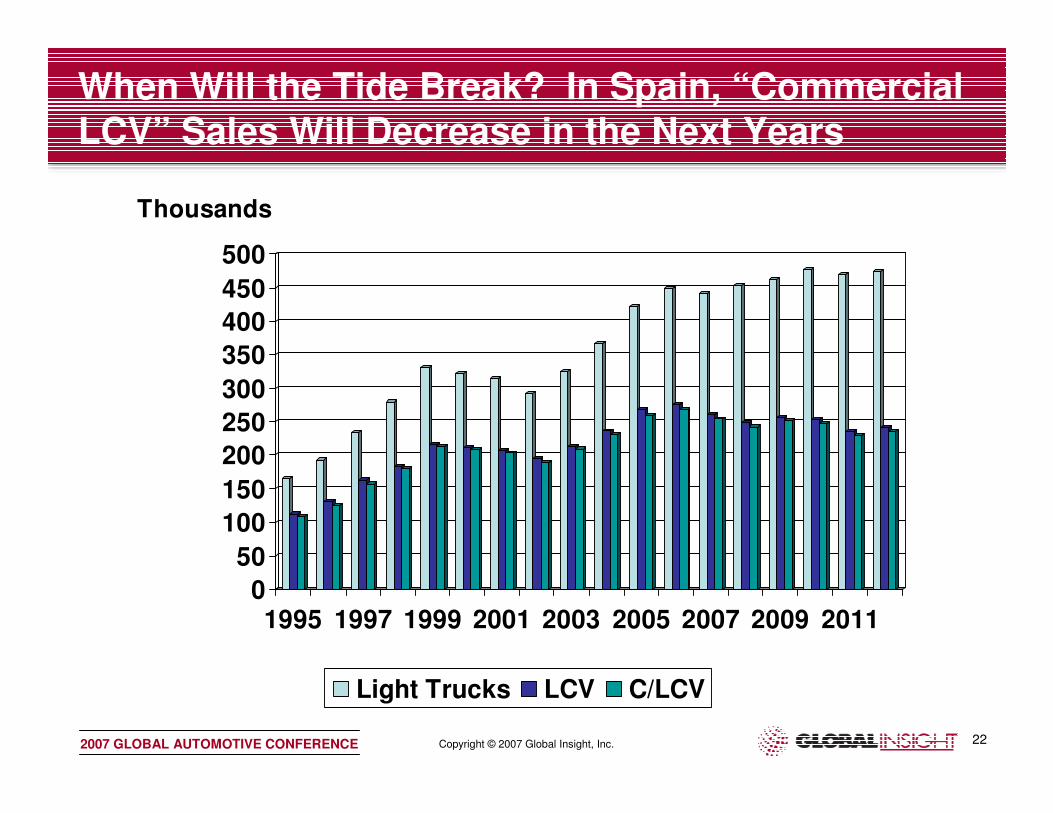

When Will the Tide Break? In Spain, “Commercial LCV” Sales Will Decrease in the Next Years

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 23

• Segment – West European OEMs should think again:

– Micro Vans (MIC) might be worth taking another look at, especially for West European OEMs looking at Asia

– Heavy Vans (HVANs) will be growing, still with many coming from the Light Duty Truck range (3.5 – 7.5t GVW)

– Medium Pick-ups (PUP-C) is also an interesting growth opportunity mostly outside Europe, Thailand is important

– Large Pick-ups (PUP-D) is the segment to enter in the United States

• As market leaders show, it pays off to leverage:

– Home base competitive advantage

– Localised production

– Partnering and co-operation

– Manufacturing and distribution synergies

What Does This Mean for West European OEMs?

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 25

APPENDIX

Applicable Segment Definitions

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 26

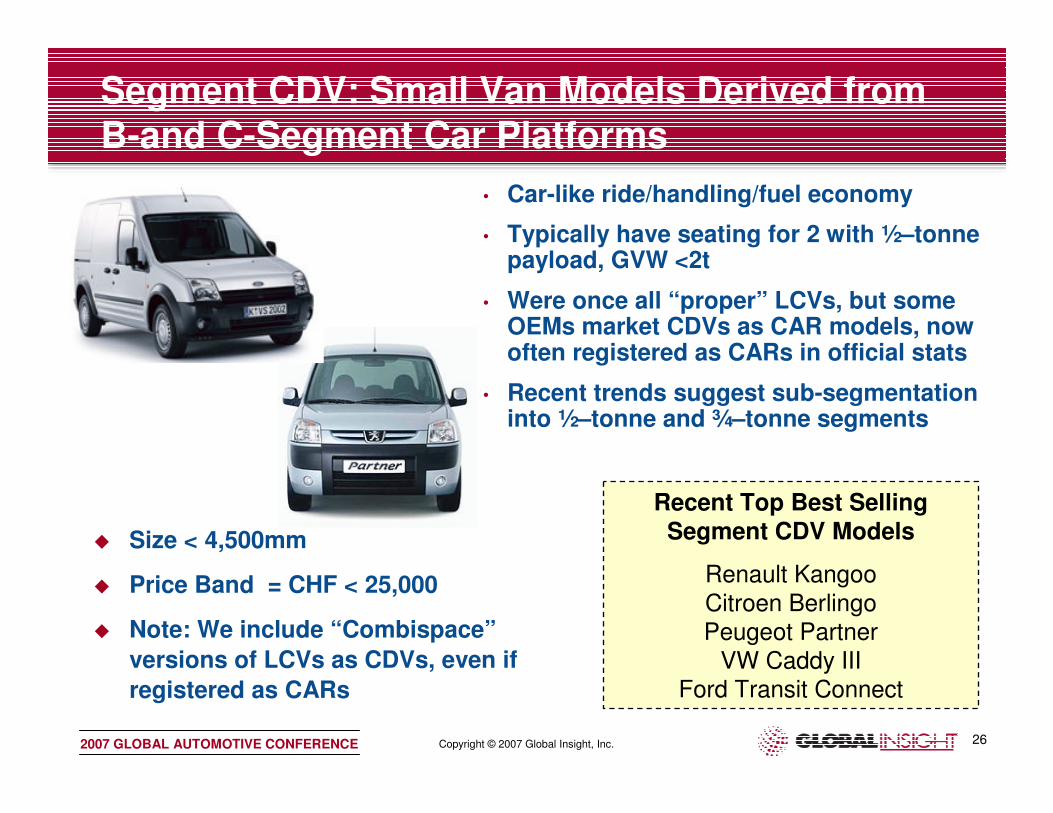

Recent Top Best Selling

Segment CDV Models

Renault Kangoo

Citroen BerlingoPeugeot Partner

VW Caddy IIIFord Transit Connect

• Car-like ride/handling/fuel economy

• Typically have seating for 2 with ½–tonne payload, GVW <2t

• Were once all “proper” LCVs, but someOEMs market CDVs as CAR models, now often registered as CARs in official stats

• Recent trends suggest sub-segmentation into ½–tonne and ¾–tonne segments

� Size < 4,500mm

� Price Band = CHF < 25,000

� Note: We include “Combispace”

versions of LCVs as CDVs, even if

registered as CARs

Segment CDV: Small Van Models Derived from B-and C-Segment Car Platforms

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 27

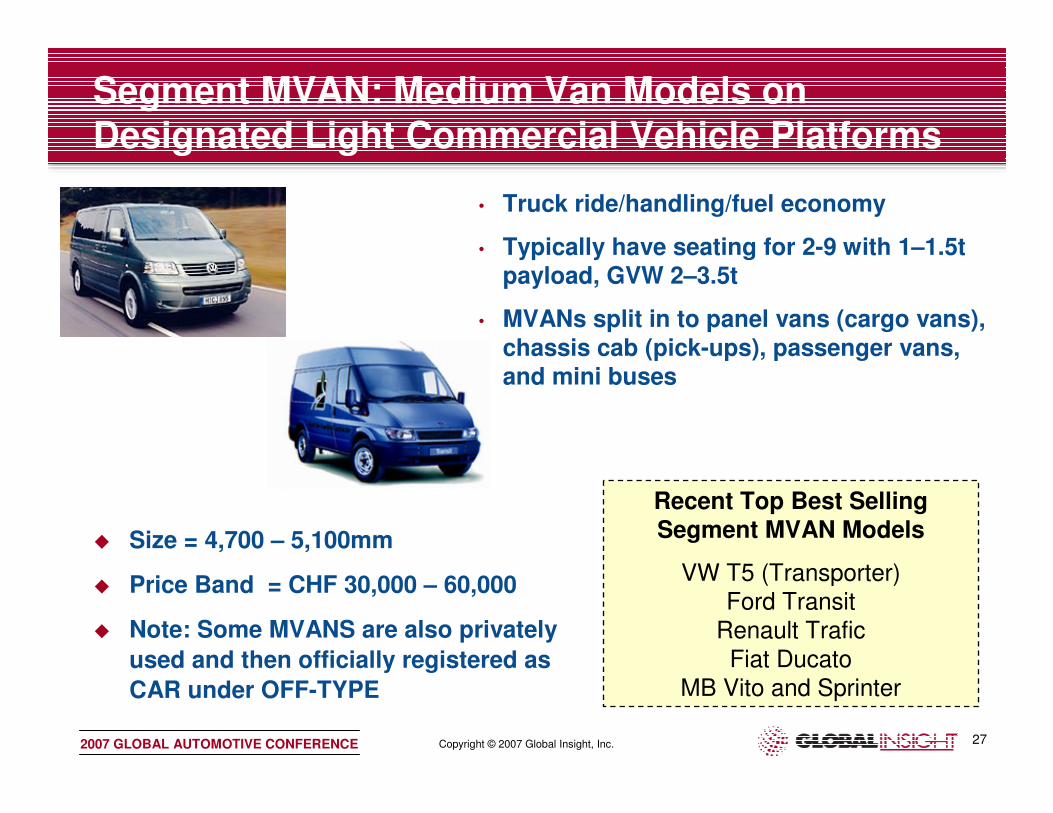

Segment MVAN: Medium Van Models on Designated Light Commercial Vehicle Platforms

Recent Top Best Selling Segment MVAN Models

VW T5 (Transporter)

Ford TransitRenault Trafic

Fiat DucatoMB Vito and Sprinter

• Truck ride/handling/fuel economy

• Typically have seating for 2-9 with 1–1.5t payload, GVW 2–3.5t

• MVANs split in to panel vans (cargo vans),

chassis cab (pick-ups), passenger vans, and mini buses

� Size = 4,700 – 5,100mm

� Price Band = CHF 30,000 – 60,000

� Note: Some MVANS are also privately

used and then officially registered as

CAR under OFF-TYPE

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 28

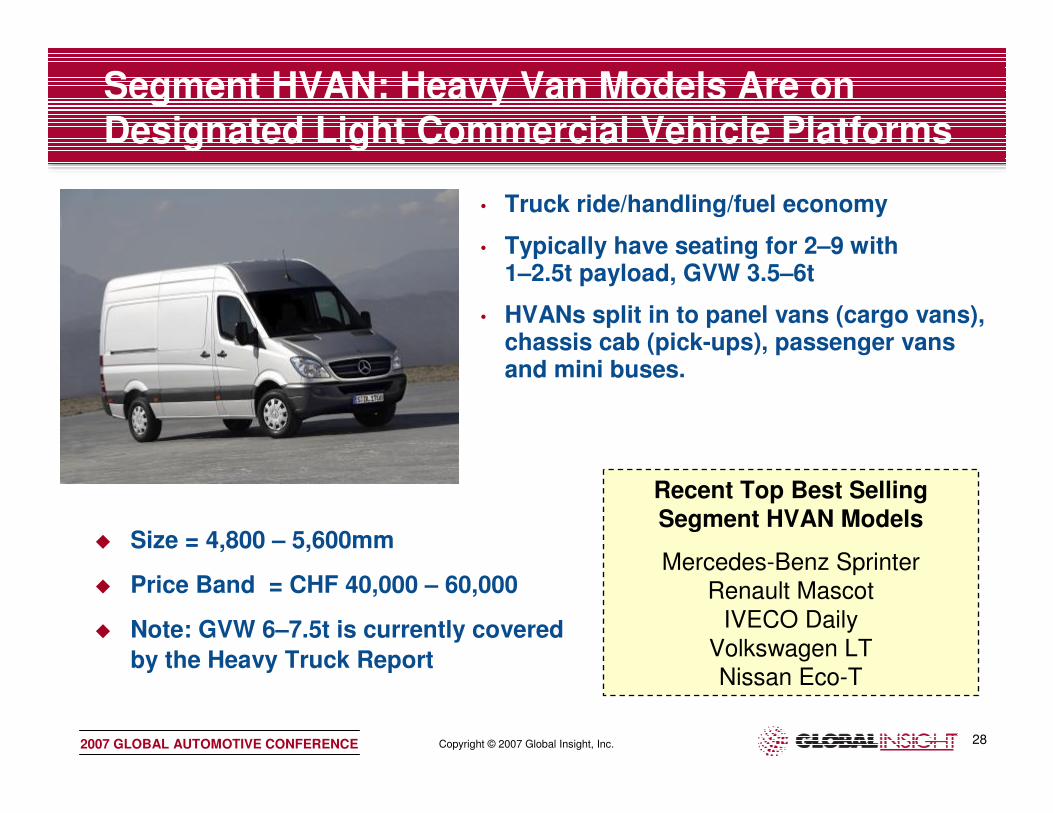

Segment HVAN: Heavy Van Models Are on Designated Light Commercial Vehicle Platforms

Recent Top Best Selling Segment HVAN Models

Mercedes-Benz Sprinter

Renault Mascot

IVECO DailyVolkswagen LTNissan Eco-T

• Truck ride/handling/fuel economy

• Typically have seating for 2–9 with 1–2.5t payload, GVW 3.5–6t

• HVANs split in to panel vans (cargo vans), chassis cab (pick-ups), passenger vans and mini buses.

� Size = 4,800 – 5,600mm

� Price Band = CHF 40,000 – 60,000

� Note: GVW 6–7.5t is currently covered

by the Heavy Truck Report

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 29

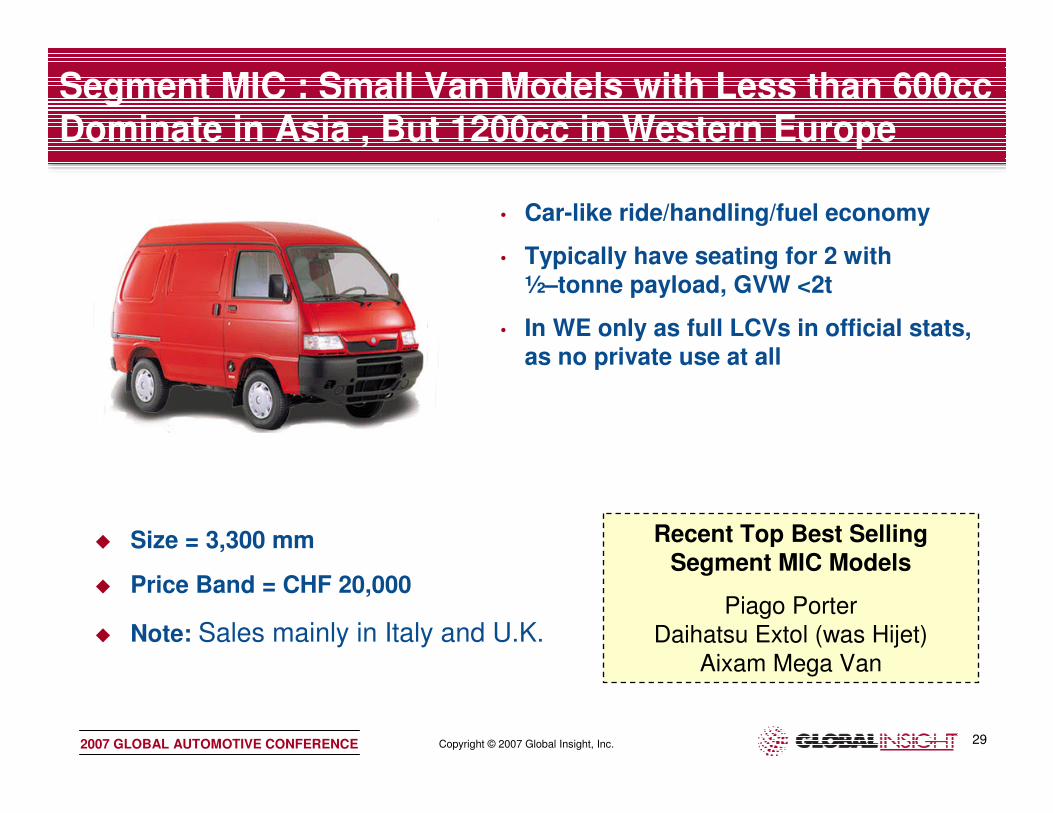

Segment MIC : Small Van Models with Less than 600cc Dominate in Asia , But 1200cc in Western Europe

Recent Top Best Selling Segment MIC Models

Piago PorterDaihatsu Extol (was Hijet)

Aixam Mega Van

• Car-like ride/handling/fuel economy

• Typically have seating for 2 with½–tonne payload, GVW <2t

• In WE only as full LCVs in official stats, as no private use at all

� Size = 3,300 mm

� Price Band = CHF 20,000

� Note: Sales mainly in Italy and U.K.

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 30

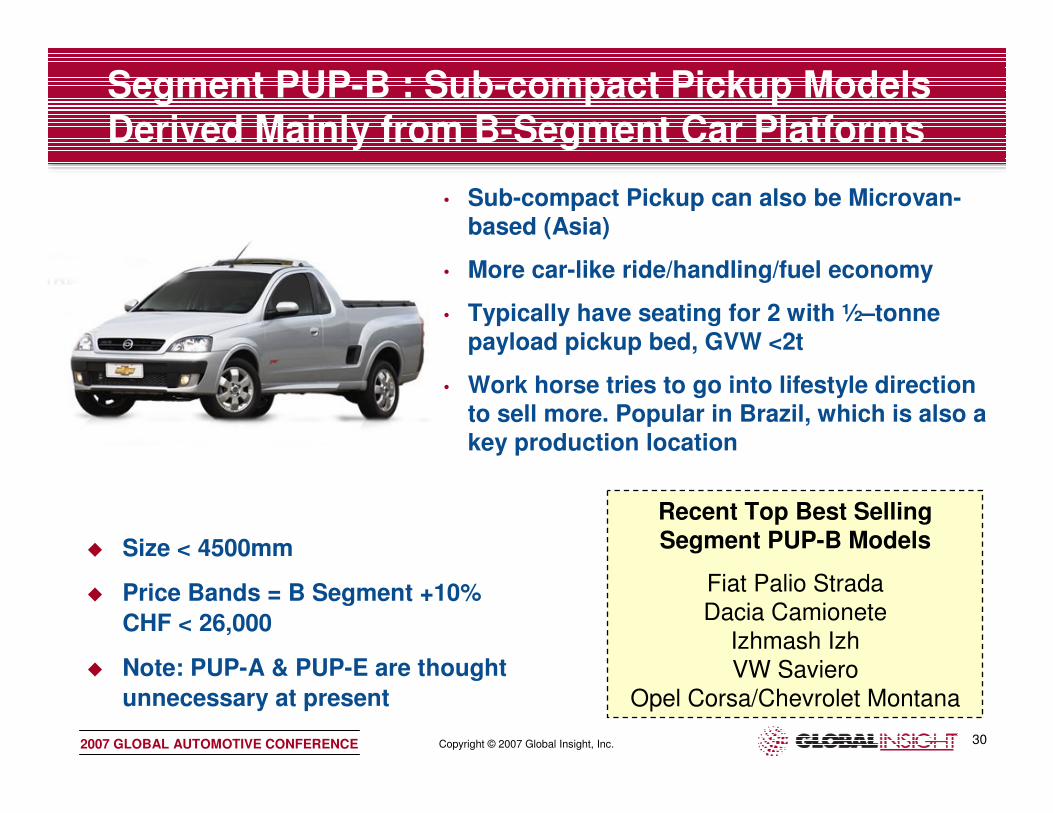

Segment PUP-B : Sub-compact Pickup Models Derived Mainly from B-Segment Car Platforms

Recent Top Best Selling Segment PUP-B Models

Fiat Palio Strada

Dacia CamioneteIzhmash Izh

VW SavieroOpel Corsa/Chevrolet Montana

• Sub-compact Pickup can also be Microvan-based (Asia)

• More car-like ride/handling/fuel economy

• Typically have seating for 2 with ½–tonne payload pickup bed, GVW <2t

• Work horse tries to go into lifestyle direction to sell more. Popular in Brazil, which is also a key production location

� Size < 4500mm

� Price Bands = B Segment +10%

CHF < 26,000

� Note: PUP-A & PUP-E are thought

unnecessary at present

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 31

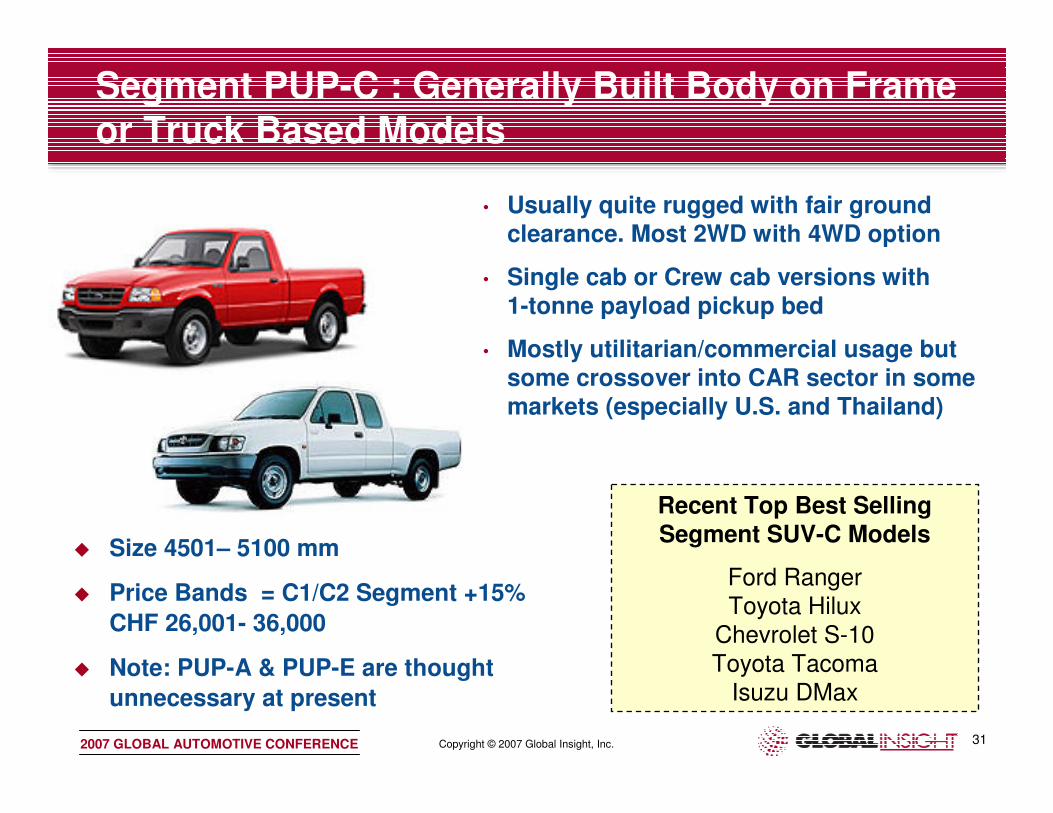

Segment PUP-C : Generally Built Body on Frame or Truck Based Models

Recent Top Best Selling Segment SUV-C Models

Ford Ranger

Toyota HiluxChevrolet S-10

Toyota TacomaIsuzu DMax

� Size 4501– 5100 mm

� Price Bands = C1/C2 Segment +15%

CHF 26,001- 36,000

� Note: PUP-A & PUP-E are thought

unnecessary at present

• Usually quite rugged with fair ground clearance. Most 2WD with 4WD option

• Single cab or Crew cab versions with1-tonne payload pickup bed

• Mostly utilitarian/commercial usage but some crossover into CAR sector in some markets (especially U.S. and Thailand)

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 32

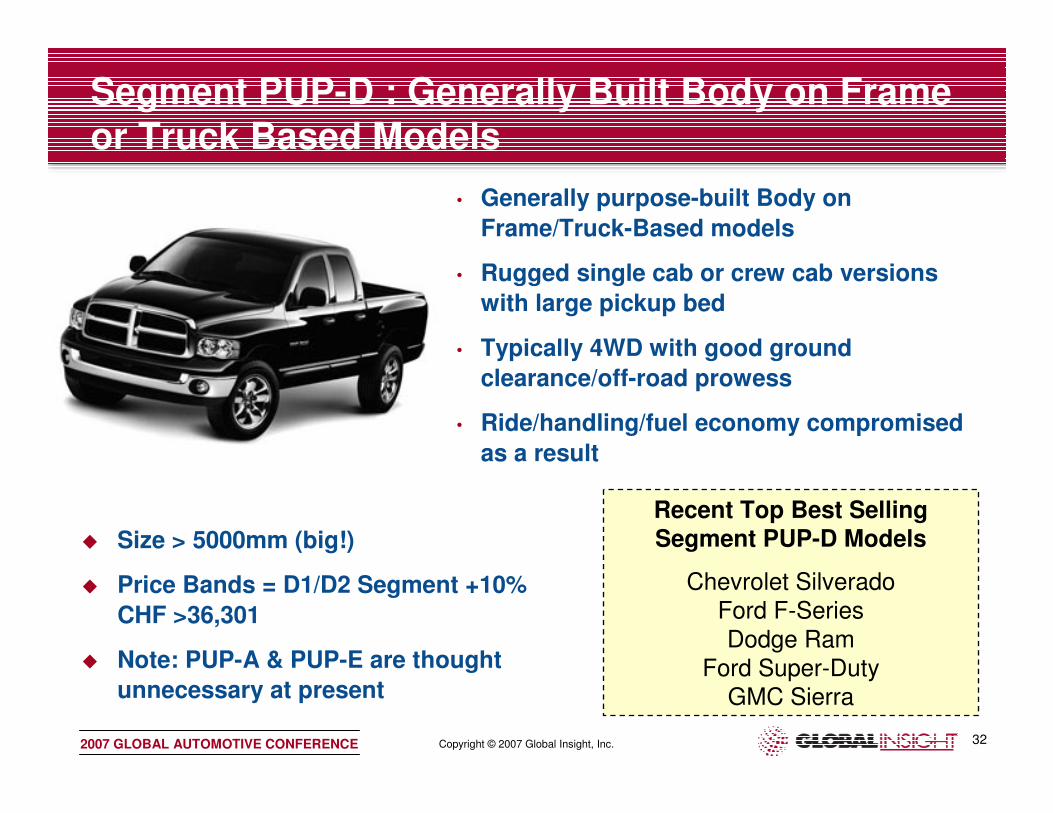

Segment PUP-D : Generally Built Body on Frame or Truck Based Models

Recent Top Best Selling Segment PUP-D Models

Chevrolet Silverado

Ford F-Series

Dodge Ram

Ford Super-DutyGMC Sierra

• Generally purpose-built Body on

Frame/Truck-Based models

• Rugged single cab or crew cab versions

with large pickup bed

• Typically 4WD with good ground

clearance/off-road prowess

• Ride/handling/fuel economy compromised

as a result

� Size > 5000mm (big!)

� Price Bands = D1/D2 Segment +10%

CHF >36,301

� Note: PUP-A & PUP-E are thought

unnecessary at present