the marketpulse with quarterly executive letter · during the third quarter, the economy grew 2.7...

TRANSCRIPT

With Quarterly Executive Letter

Volume 1, Issue 12

December 2012

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

ii

December 12, 2012

Gathering Steam

We launched The MarketPulse last January on an upbeat note. At that time, our Chief Economist Mark Fleming

wrote that both “the broad economy and the housing market are moving toward positive growth in 2012.” Now,

almost a year later, we see continued signs of economic improvement. And while not yet fully recovered, the

housing market gathered steam through the summer and into the fourth quarter. But will it heat up enough to

help power the general economic engine in the year ahead?

Improved fundamentals

CoreLogic® data demonstrate that home prices are stabilizing in response to improved market fundamentals

like reduced inventories and improved buyer demand. Notably, 2012 was the first year of significant price

appreciation since 2006. Year-to-date, the CoreLogic Home Price Index is up 8 percent nationally—

welcome news for borrowers, especially those saddled with negative equity.

Government efforts, too, seem to be making some difference. The Federal Reserve held the federal funds rate

target at zero this year. Continued low interest rates boosted refinancing opportunities for many homeowners,

thus benefiting the balance sheets of those who could qualify. For other borrowers, struggling to pay their

mortgages, the Home Affordable Modification Program helped reduce their monthly payment to a sustainable

level. The Federal Reserve also continued to use non-traditional monetary tools, such as quantitative easing.

As part of implementing a third round of this easing last summer, the government renewed its commitment to

purchase mortgage securities. In turn, these purchases helped keep interest rates low.

With credit remaining tight, one of the more vexing problems facing policymakers has been finding ways to

help borrowers who lack sufficient equity to qualify for a traditional refinance gain access at lower interest

rates. The expanded Home Affordable Refinance Program—HARP 2.0—gave more borrowers this access

in 2012. Since 2009, HARP programs have helped more than 1.5 million borrowers refinance under more

favorable terms.

Lenders and investors have also allowed more homeowners to pursue short sales as an alternative to foreclosure.

The continuing downward trend in both delinquency rates and foreclosures as well as a gradual clearing of the

shadow inventory are signs of stabilization in the housing market. While we’re still far from pre-crisis levels, the

trend is firmly in the right direction.

Beyond these factors, we are encouraged by strengthening consumer confidence, the mending of consumer

credit, increasing household formation and greater home affordability. Taken together, we see a brightening

outlook for mortgage production in the coming year.

From the CEO

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

iii

Building confidence

Despite this promise, the emerging recovery, in our view, is still a fragile one. Ongoing uncertainty in the overall

business climate brings into question whether the economy can fire on all cylinders. The lack of a workable plan

to resolve the fiscal cliff so close to deadline has impacted the confidence of business leaders. The ongoing,

unresolved problems related to the European debt crisis also weigh down confidence.

In the lead article in this month’s issue of The MarketPulse, our economists share their observations on the

difference between economic uncertainty and risk. We strongly believe, in the face of such an uncertain

environment, the best way to increase your confidence level when making decisions and taking action is access

to the right information at the right time. It is at the center of smart business planning and can help your teams

not only manage business uncertainty but also mitigate risk. At CoreLogic, we are prepared to work with you to

deliver expert analysis and innovative, tailored solutions that can help you capitalize on growth opportunities,

even in challenging markets.

On behalf of the entire CoreLogic team, best wishes for a happy holiday season. We look forward to the year

ahead and collaborating with you toward your ongoing business success.

Sincerely,

Anand Nallathambi

President and CEO

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

iv

The MarketPulse – Volume 1, Issue 12

The Authors

Anand K. NallathambiPresident and Chief Executive Officer

Anand K. Nallathambi is the president and chief executive officer of CoreLogic, a leading provider of consumer, financial and property information, analytics and services to business and government. Nallathambi is responsible for all aspects of the CoreLogic business.

Dr. Mark Fleming Chief Economist

Dr. Mark Fleming is the chief economist for CoreLogic. He leads the economics team responsible for analysis, commentary, and forecasting trends in the real estate and mortgage markets.

Sam KhaterDeputy Chief Economist

Sam Khater is deputy chief economist for CoreLogic. He is responsible for providing in-depth economic, mortgage market and real estate analysis.

Aurora BristorSenior Research Analyst

Aurora Bristor is a senior research analyst for CoreLogic in the Office of the Chief Economist. She develops and delivers mortgage market and real estate analytics in support of CoreLogic and the CoreLogic Academic Research Council.

Table of ContentsFrom the CEO ............................................................... ii

The Authors ................................................................... iv

Media Contacts ........................................................... iv

The MarketPulse...........................................................1

Economic Risk Versus Uncertainty.........................1

Impact of Residential Investment on Economic Growth ...................................................1

Recessions and the Residential Investment Cycle .....................................................1

Moving Toward Regulatory Certainty ............2

Follow the Money: Investing in Single-Family Rentals .................................................3

Rental Income Isn’t Just for Investors ............3

Trends in Rental Income for Owners, Tenants and Free Riders ...........................................3

It’s Good to Be an Investor In Single-Family Rental Properties .......................4

Follow the Money ...................................................5

Multifamily Rentals Rise Above the Flood ........6

In the News .....................................................................6

National Summary October 2012 .....................7

Largest 25 CBSA Summary October 2012 ...........................................................7

State Summary October 2012 ...........................8

Home Prices .............................................................9

Mortgage Performance ...................................... 10

Home Sales .............................................................. 11

Variable Descriptions .......................................... 12Media ContactsFor real estate industry and trade media:

Bill Campbell [email protected] (212) 995.8057 (office) (917) 328.6539 (mobile)

For general news media:

Lori Guyton [email protected] (901) 277.6066

The MarketPulse

1© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

n “Risk, Uncertainty and Profit,” the economist Frank Knight distinguishes between economic risk and uncertainty.

Economic risk occurs when potential outcomes are unknown, but have well defined probability distributions. Uncertainty occurs when the outcomes are completely unknown and unquantifiable.

Over the past year, the current economic and regulatory landscape facing real estate and the mortgage markets has been characterized as uncertain. The conclusion of the recent election cycle provided some clarification, since we now know regulators are likely to pursue similar policies to the ones they’ve pursued over the last two years. The road to economic certainty is also aided by a strong comeback in residential investment. This is important because, while historically residential investment has averaged only 5 percent of GDP, its contribution to GDP growth during expansions is much higher.

Impact of Residential Investment on Economic Growth

Over the last four quarters, residential investment has added 0.3 percentage

points to GDP. While the level is low, it is contributing 12 percent of the overall low GDP growth rate. This is on par with how residential investment contributed in prior recoveries immediately after recession. It took a full two years, but residential investment is now providing the post-recession boost it normally does.

During the third quarter, the economy grew 2.7 percent, up from 1.3 percent in the second quarter. Growth in the third quarter, if not revised downward, is in line with an expected long-run trend level of about 2.5 percent. While there were some anomalies in the third-quarter report which reveal that growth is not as strong as it appears on the surface, one thing is certain: The real estate cycle is now contributing to economic growth. This is good news because residential investment is the most important cyclical component of the economy.

Recessions and the Residential Investment Cycle

Since 1970, there have been six recessions. In each of the four quarters prior to those recessions, growth averaged 3 percent. However, while economic growth was

Economic Risk Versus UncertaintyBy Sam Khater and Mark Fleming

Housing Statistics (October 2012)

HPI YOY Chg . . . . . . . . . . . . . . .6.3%

HPI YOY Chg XD . . . . . . . . . . .5.8%

NegEq Share (Q2 2012) . . . .22.3%

Shadow Inventory (07/2012) . . .2.3m

Distressed Discount. . . . . . . .34.7%

New Sales (ths, ann.) . . . . . . . . . 270

Existing Sales (ths, ann.) . . . . 2,715

Average Sales Price . . . . . . $234,990

HPI SFC Peak-to-Current. . . -26.9%

Foreclosure Inventory Peak-to-Current . . . . . . . . . . -15.8%

Volume 1, Issue 12

December 12th, 2012

Data as of October 2012

I

Cont...

FIGURE 1. BORROWER WILLINGNESS COMMANDS A PREMIUM

660

680

700

720

740

760

780

Jan

-00

Jul-

00

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Weighted Average Credit Score at Origination

Fig 1 borrower willingness commands a premium 120612

Change in YOY PricesChange in YOY REO Share

Source: CoreLogic July 2012

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

2

The MarketPulse – Volume 1, Issue 12

positive prior to the recession, residential investment was already flashing a warning sign and subtracting 0.2 percentage points from growth. Then, during the recession, residential investment was responsible for nearly two-thirds (0.9 percentage points) of the average overall decline of 1.4 percent per quarter. In the four quarters after the recession, residential investment contributed 13 percent (0.6 percentage points) of the overall economic growth of 4.2 percent.

The pattern was different during the most recent recession (Q4 2007 to Q2 2009). The collapse in residential investment preceded the start of the recession earlier than in prior recessions. Residential investment began to subtract from GDP growth in Q1 2006, a full seven quarters before the recession began. Moreover, during the four quarters prior to the beginning of the recession, residential investment was subtracting a full percentage point of growth from GDP. This is similar to the magnitude of movement during prior recessions—but in this case it was prior to the recession’s start. Residential investment remained weak after the recession ended during Q2 2009, contributing only 0.1 percentage points to GDP.

Moving Toward Regulatory Certainty

On the horizon are regulatory policies that require further clarification. “Qualified mortgage” and “qualified residential mortgage” will become the standards for the “credit box” within which mortgage originations

will be defined and provide regulatory preference. Two of the most important and frequently discussed dimensions of the “credit box” are credit scores and debt-to-income (DTI) ratios. The two together provide insight into a borrower’s willingness and capacity to pay.

Weighted average credit scores (Figure 1), using CoreLogic loan servicing data1, show modestly improving scores as home prices were rising in the middle of the decade. This trend may have been driven by the increased pace of refinancing, particularly prevalent

in sub-prime loans, causing successful loan repayment to “inflate” credit scores. The sudden shift to a higher credit score requirement can be seen in late 2008. Since that time, average origination credit scores have trended between 740 and 760, significantly higher than the pre-crisis average of approximately 700. Lenders today are requiring borrowers

to show a greater willingness to pay their mortgage.

Weighted average DTI ratios (Figure 2) showed a rising trend in the first half of the decade as home prices rose. Capacity to pay, and arguably the sustainability of that

capacity, was increasingly at risk. Weighted average DTIs peaked in late 2007 at more than 40, but declined quickly in late 2008 back to 2002 levels. Since that time, weighted average origination DTIs have exhibited some volatility caused by the recent refinance boomlets. They are currently in the low 30s, consistent with DTIs coming out of the refinance boom at the beginning of the 2000s. Lenders today are requiring a level of capacity and sustainability roughly in line with traditional underwriting practices prior to the housing boom.

The economy is continuing to recover, and residential investment is once again pulling its weight—as it has coming out of prior recessions. Lenders have returned to more sustainable loan products, but remain cautious in extending credit to only the most qualified borrowers. Overall market uncertainty can be reduced further through reduced mortgage risk, investment driven economic recovery and clarity on housing policies, leading to more sustainable profits and outcomes for real estate and housing finance.

“The real estate cycle is now

contributing to economic growth.

This is good news because residential

investment is the most important

cyclical component of the economy.”

End.

Footnote

1 The loan servicing data covers more than 80 percent of all first lien mortgages in the U.S. representing all types of mortgages.

FIGURE 2. CAPACITy RETURNS TO SUSTAINABLE LEVELS

30

32

34

36

38

40

42

Jan

-00

Jul-

00

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Weighted Average Debt-to-Income Ratio at Origination

Fig 2 capacity returns to sustainable levels 121112

Change in YOY PricesChange in YOY REO Share

Source: CoreLogic July 2012

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

3

The MarketPulse – Volume 1, Issue 12

Follow the Money: Investing in Single-Family RentalsBy Sam Khater

Footnote

2 It excludes rental income by corporations or entities.

Cont...

ore than three years into the economic recovery, incomes continue to stagnate. As of

September 2012, per capita disposable income increased only 1 percent from a year earlier. While there are many factors behind both the short-term and long-term stagnation in incomes, there are some segments of personal income that are rapidly rising.

Rental income of residential properties, defined as gross rents for homeowners and renters minus the associated costs of financing and other expenses, increased 12 percent from September 2011. This growth shows no signs of slowing down. Since reaching a trough of $120 billion in February 2007, rental income has nearly quadrupled to $470 billion as of September 2012 (Figure 1).

The rapid growth in rental income is a byproduct of fundamental shifts in the housing market, driven by a large increase in affordability and rising rents, which created a large increase in rental incomes. This article explores the rapid growth of rental income in more detail to gain a finer understanding of the profitability of the single-family residential investor rental market.

Rental Income Isn’t Just for Investors

While there are a variety of home price indicators for residential real estate transactions that span several decades, there are few monthly sources of rent

or rental income data. The closest metric is produced by the Bureau of Economic Analysis (BEA) as part of the personal income data released every month. Personal income entails many categories of income well beyond the layman’s definition. It includes wages, salaries, employer contributions, rents, dividends, interest, proprietor income and transfers2. By far the largest category is wages and salaries, which account for nearly two-thirds of all income. The fastest growing primary income category over the last 12 months has been rental income. Rental income only accounts for 4 percent of overall income, but over the last year it has accounted for 10 percent of the income growth through September, and in early 2012 it accounted for nearly one-fifth of all income growth.

While some of the rise in rental income has been driven by higher

rents and the rise in the number of

renters, much of the rise has nothing

to do with the rental market, but the

owner-occupied market. This is due to

the definition of rental income, which

is not just the rental income investors

receive from renting single family

or multifamily properties, but also

the imputed rental income from the

flow of services to homeowners. Put

differently, homeowners are treated

as if they were in the rental business

and they leased the property back to

themselves. Homeowner rental income

accounts for about 70 percent of total

rental income, while investor single-

family and multifamily rental income

account for the remaining 30 percent.

Trends in Rental Income for Owners, Tenants and Free Riders

Rental income growth averaged an

annualized rate of 23 percent during

the five years ending in 2011, but

M

FIGURE 1. LAND VS. LABOR — LAND IS THE BETTER DEALPercent Change in Income Segment from a year Ago

-40%

-20%

0%

20%

40%

60%

80%

Jan

-00

Aug

-00

Mar

-01

Oct

-01

May

-02

Dec

-02

Jul-

03

Feb

-04

Sep

-04

Ap

r-0

5

No

v-0

5

Jun

-06

Jan

-07

Aug

-07

Mar

-08

Oct

-08

May

-09

Dec

-09

Jul-

10

Feb

-11

Sep

-11

Ap

r-12

Rental Income Overall Income

Khater: fig 1 land vs labor 120612

Source: CoreLogic September 2012

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

4

The MarketPulse – Volume 1, Issue 12

there are wide disparities by tenure.

Homeowner rental income rose at

an annualized rate of 28 percent,

compared to 15 percent a year for

investor rental income. In the first

half of the 2000s, homeowner rental

income fell from a high of $162 billion

to a low of $66 billion. Over that

same time period, investor rental

income typically ranged from $60 to

$70 billion. Homeowner rental income

in 2011 was $257 billion, and investor

rental income was $126 billion.

Both segments are exhibiting rapid

growth, but the overall rise in

rental income is driven more by the

increase in homeowner rental income

(Figure 2). The reason for the rapid

rise in homeowner rental income is

that homeowner costs have declined

since 2008. Consequently, homeowner

rental income, which is defined as gross

equivalent rents minus the acquisition

and financing costs, soared.

Moreover, the rise in delinquencies

and foreclosures, in which millions of

homeowners received the monetary

benefit of living in a home but were

in default and not paying for it (i.e., homeowner “free riding”), provided a boost to rental income. Free-rider rental income was estimated to be $27 billion dollars in 2011. The combination of these two factors has driven up overall rental incomes dramatically over the last two years.

It’s Good to Be an Investor In Single-Family Rental Properties

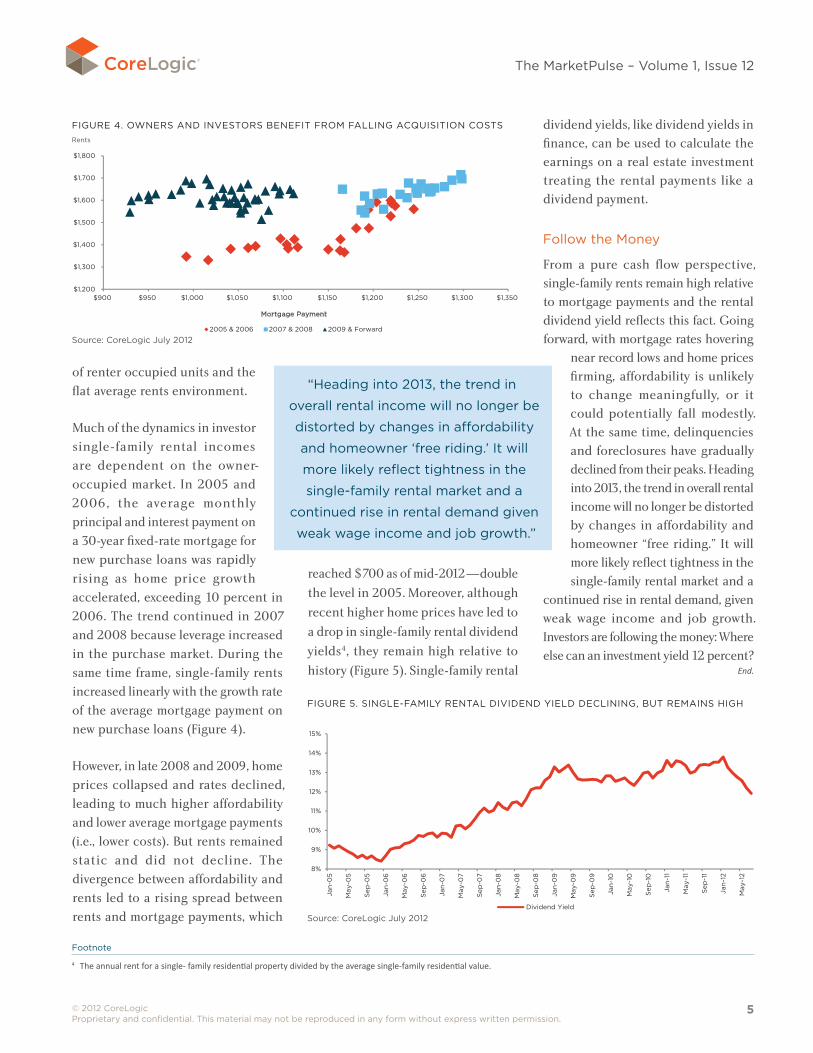

To the best of our knowledge, the BEA publicly released data does not distinguish between single-family and multifamily rental income. In order to estimate investor single-family rental income trends, CoreLogic combines

Census, BEA, and CoreLogic single-family rental data (as a proxy for national rents)3. Investor single-family rental income remained flat between 2005 and 2007 (Figure 3).

At first, this may seem odd because both single-family rents and the number of single-family rentals were rapidly rising, leading to higher aggregate gross rents for investors. However, rental income is measured on a net basis. Therefore, the rapid rise in home prices in 2005 (and early 2006) led to higher financing costs and offset the higher investor gross rents, resulting in a flat trend in investor single-family rental incomes.

Affordability conditions reversed during the housing bust between 2008 and 2011, and investor rental incomes soared because home prices and mortgage rates fell, resulting in a drop in financing costs. Meanwhile, investors’ aggregate gross rents continued to rise due to an increased demand for single-family rental units. In 2012, the rise in single-family rental income began to moderate, primarily due to the slowdown in the growth rate

Cont...

FIGURE 2. OWNERS, INVESTORS AND FREE RIDERSRental Income by Segment, $Billions

0

50

100

150

200

250

300

350

400

450

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

2010

2011

Investor Homeowner Homeowner Free Riding

Khater: fig 2 owners, investors, free riders 120612

Source: CoreLogic 2011

Footnote

3 Census data was used to estimate stocks of single-family rentals and CoreLogic and BEA data were used to calculate gross rents and investor single-family rental income estimates to be consistent with BEA’s approach for rental income calculations.

FIGURE 3. IT'S GOOD TO BE A LANDLORDAggregate Single-Family Investor Rents, $Billions

0

10

20

30

40

50

60

70

80

2005 2006 2007 2008 2009 2010 2011 Q2 2012

Khater: fig 3 its good to be landlord 120612

Source: CoreLogic Q2 2012

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

5

The MarketPulse – Volume 1, Issue 12

of renter occupied units and the

flat average rents environment.

Much of the dynamics in investor

single-family rental incomes

are dependent on the owner-

occupied market. In 2005 and

2006, the average monthly

principal and interest payment on

a 30-year fixed-rate mortgage for

new purchase loans was rapidly

rising as home price growth

accelerated, exceeding 10 percent in

2006. The trend continued in 2007

and 2008 because leverage increased

in the purchase market. During the

same time frame, single-family rents

increased linearly with the growth rate

of the average mortgage payment on

new purchase loans (Figure 4).

However, in late 2008 and 2009, home

prices collapsed and rates declined,

leading to much higher affordability

and lower average mortgage payments

(i.e., lower costs). But rents remained

static and did not decline. The

divergence between affordability and

rents led to a rising spread between

rents and mortgage payments, which

reached $700 as of mid-2012—double

the level in 2005. Moreover, although

recent higher home prices have led to

a drop in single-family rental dividend

yields4, they remain high relative to

history (Figure 5). Single-family rental

dividend yields, like dividend yields in finance, can be used to calculate the earnings on a real estate investment treating the rental payments like a dividend payment.

Follow the Money

From a pure cash flow perspective, single-family rents remain high relative to mortgage payments and the rental dividend yield reflects this fact. Going forward, with mortgage rates hovering

near record lows and home prices firming, affordability is unlikely to change meaningfully, or it could potentially fall modestly. At the same time, delinquencies and foreclosures have gradually declined from their peaks. Heading into 2013, the trend in overall rental income will no longer be distorted by changes in affordability and homeowner “free riding.” It will more likely reflect tightness in the single-family rental market and a

continued rise in rental demand, given weak wage income and job growth. Investors are following the money: Where else can an investment yield 12 percent?

End.

FIGURE 4. OWNERS AND INVESTORS BENEFIT FROM FALLING ACQUISITION COSTSRents

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

$1,800

$900 $950 $1,000 $1,050 $1,100 $1,150 $1,200 $1,250 $1,300 $1,350

Mortgage Payment

2005 & 2006 2007 & 2008 2009 & Forward

Khater: fig 4 owners and investors benefit 120612

Source: CoreLogic July 2012

FIGURE 5. SINGLE-FAMILy RENTAL DIVIDEND yIELD DECLINING, BUT REMAINS HIGH

8%

9%

10%

11%

12%

13%

14%

15%

Jan

-05

May

-05

Sep

-05

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Dividend Yield

Khater: fig 5 single family rental dividend yield 120612

Source: CoreLogic July 2012

“Heading into 2013, the trend in

overall rental income will no longer be

distorted by changes in affordability

and homeowner ‘free riding.’ It will

more likely reflect tightness in the

single-family rental market and a

continued rise in rental demand given

weak wage income and job growth.”

Footnote

4 The annual rent for a single- family residential property divided by the average single-family residential value.

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

6

The MarketPulse – Volume 1, Issue 12

Multifamily Rentals Rise Above the Flood By Aurora Bristor

In a housing market of underwater mortgages just beginning to dry out, multifamily rents are still floating

high. Multifamily rents dropped year-over-year in 2008 and 2009 with the rest of the economy, but recovered faster and stronger than single-family rents. While neither rental class dropped as significantly as the bursting housing bubble, the single-family rental market is more of a draw to foreclosed homeowners who brought their volatile circumstances to market.

January 2010 was the first year-over-year decline in pre-foreclosure filings, keeping more homeowners out of the single-family rental market. At the same time, as shown in the chart on page six of the November issue of The MarketPulse (“Flooding the Residential Rental Market”), the flow of properties

into the single-family rental market was negative year-over-year. This tightening helped spur the single-family rental turnaround seen in the chart, though contracted rents did not turn positive until early 2011. The CoreLogic Home

Price Index (HPI®) has been listing year-over-year housing price gains since early 2012. However, the multifamily rental market has been rising steadily since early 2010, leading the housing recovery in duration and strength.

National Mortgage Professional Magazine, December 6Foreclosures Still Part of Market LandscapeThe number of homes lost to foreclosure continued to decline in October, but the overall levels of foreclosure remain uncomfortably high.

Fox Business, December 4Home prices dip in September after string of gains: CoreLogicHome prices posted their biggest annual jump in more than six years in October in a sign the housing sector continues to recover, data analysis firm CoreLogic said on Tuesday.

Business Insider, December 4CoreLogic: Home Prices Are Growing At Their Fastest Rate In 6 YearsNational home prices including that of distressed homes, climbed 6.3 percent year-over-year in October, rising for the eighth straight month, according to the latest data from CoreLogic. This is the biggest increase since June 2006.

USA Today, December 3Cheaper homes see accelerating price gainsLower-priced homes, which fell the most in price during the housing bust, are showing more zip as the housing market strengthens.

HousingWire, December 3Foreclosures drop 17% in October: CoreLogicWhen America was in more normal times pre-housing crisis, foreclosures averaged about 21,000 completed actions per month between the years 2000 and 2006.

Orange County Register, December 2CEO: Housing recovery becoming a rallyIn the 2½ years since CoreLogic broke away from parent company First American Financial Corp., the real estate data giant has refocused on its core business.

In the News

RENT INCREASESyear-Over-year Change

-6%

-4%

-2%

0%

2%

4%

6%

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-10

Jul-

10

Oct

-10

Jan

-11

Ap

r-11

Jul-

11

Oct

-11

Jan

-12

Ap

r-12

Jul-

12

Multifamily Rents Single-Family Rents

COTM rental increases 121112

Source: CoreLogic September 2012

End.

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

7

The MarketPulse – Volume 1, Issue 12

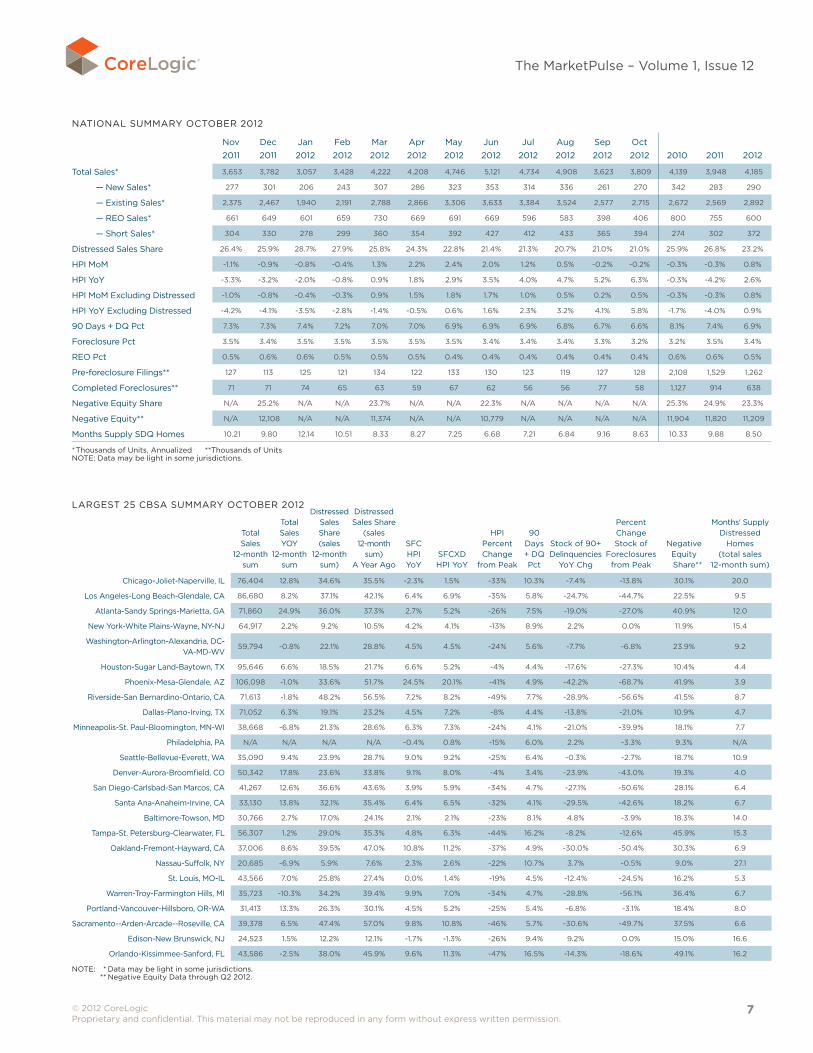

NATIONAL SUMMARy OCTOBER 2012

Nov 2011

Dec 2011

Jan 2012

Feb 2012

Mar 2012

Apr 2012

May 2012

Jun 2012

Jul 2012

Aug 2012

Sep 2012

Oct 2012 2010 2011 2012

Total Sales* 3,653 3,782 3,057 3,428 4,222 4,208 4,746 5,121 4,734 4,908 3,623 3,809 4,139 3,948 4,185

— New Sales* 277 301 206 243 307 286 323 353 314 336 261 270 342 283 290

— Existing Sales* 2,375 2,467 1,940 2,191 2,788 2,866 3,306 3,633 3,384 3,524 2,577 2,715 2,672 2,569 2,892

— REO Sales* 661 649 601 659 730 669 691 669 596 583 398 406 800 755 600

— Short Sales* 304 330 278 299 360 354 392 427 412 433 365 394 274 302 372

Distressed Sales Share 26.4% 25.9% 28.7% 27.9% 25.8% 24.3% 22.8% 21.4% 21.3% 20.7% 21.0% 21.0% 25.9% 26.8% 23.2%

HPI MoM -1.1% -0.9% -0.8% -0.4% 1.3% 2.2% 2.4% 2.0% 1.2% 0.5% -0.2% -0.2% -0.3% -0.3% 0.8%

HPI yoy -3.3% -3.2% -2.0% -0.8% 0.9% 1.8% 2.9% 3.5% 4.0% 4.7% 5.2% 6.3% -0.3% -4.2% 2.6%

HPI MoM Excluding Distressed -1.0% -0.8% -0.4% -0.3% 0.9% 1.5% 1.8% 1.7% 1.0% 0.5% 0.2% 0.5% -0.3% -0.3% 0.8%

HPI yoy Excluding Distressed -4.2% -4.1% -3.5% -2.8% -1.4% -0.5% 0.6% 1.6% 2.3% 3.2% 4.1% 5.8% -1.7% -4.0% 0.9%

90 Days + DQ Pct 7.3% 7.3% 7.4% 7.2% 7.0% 7.0% 6.9% 6.9% 6.9% 6.8% 6.7% 6.6% 8.1% 7.4% 6.9%

Foreclosure Pct 3.5% 3.4% 3.5% 3.5% 3.5% 3.5% 3.5% 3.4% 3.4% 3.4% 3.3% 3.2% 3.2% 3.5% 3.4%

REO Pct 0.5% 0.6% 0.6% 0.5% 0.5% 0.5% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% 0.6% 0.6% 0.5%

Pre-foreclosure Filings** 127 113 125 121 134 122 133 130 123 119 127 128 2,108 1,529 1,262

Completed Foreclosures** 71 71 74 65 63 59 67 62 56 56 77 58 1,127 914 638

Negative Equity Share N/A 25.2% N/A N/A 23.7% N/A N/A 22.3% N/A N/A N/A N/A 25.3% 24.9% 23.3%

Negative Equity** N/A 12,108 N/A N/A 11,374 N/A N/A 10,779 N/A N/A N/A N/A 11,904 11,820 11,209

Months Supply SDQ Homes 10.21 9.80 12.14 10.51 8.33 8.27 7.25 6.68 7.21 6.84 9.16 8.63 10.33 9.88 8.50

* Thousands of Units, Annualized **Thousands of Units NOTE: Data may be light in some jurisdictions.

LARGEST 25 CBSA SUMMARy OCTOBER 2012

Total Sales

12-month sum

Total Sales yOy

12-month sum

Distressed Sales Share (sales

12-month sum)

Distressed Sales Share

(sales 12-month

sum) A year Ago

SFC HPI yoy

SFCXD HPI yoy

HPI Percent Change

from Peak

90 Days + DQ Pct

Stock of 90+ Delinquencies

yoy Chg

Percent Change Stock of

Foreclosures from Peak

Negative Equity

Share**

Months' Supply Distressed

Homes (total sales

12-month sum)

Chicago-Joliet-Naperville, IL 76,404 12.8% 34.6% 35.5% -2.3% 1.5% -33% 10.3% -7.4% -13.8% 30.1% 20.0

Los Angeles-Long Beach-Glendale, CA 86,680 8.2% 37.1% 42.1% 6.4% 6.9% -35% 5.8% -24.7% -44.7% 22.5% 9.5

Atlanta-Sandy Springs-Marietta, GA 71,860 24.9% 36.0% 37.3% 2.7% 5.2% -26% 7.5% -19.0% -27.0% 40.9% 12.0

New york-White Plains-Wayne, Ny-NJ 64,917 2.2% 9.2% 10.5% 4.2% 4.1% -13% 8.9% 2.2% 0.0% 11.9% 15.4

Washington-Arlington-Alexandria, DC-VA-MD-WV

59,794 -0.8% 22.1% 28.8% 4.5% 4.5% -24% 5.6% -7.7% -6.8% 23.9% 9.2

Houston-Sugar Land-Baytown, TX 95,646 6.6% 18.5% 21.7% 6.6% 5.2% -4% 4.4% -17.6% -27.3% 10.4% 4.4

Phoenix-Mesa-Glendale, AZ 106,098 -1.0% 33.6% 51.7% 24.5% 20.1% -41% 4.9% -42.2% -68.7% 41.9% 3.9

Riverside-San Bernardino-Ontario, CA 71,613 -1.8% 48.2% 56.5% 7.2% 8.2% -49% 7.7% -28.9% -56.6% 41.5% 8.7

Dallas-Plano-Irving, TX 71,052 6.3% 19.1% 23.2% 4.5% 7.2% -8% 4.4% -13.8% -21.0% 10.9% 4.7

Minneapolis-St. Paul-Bloomington, MN-WI 38,668 -6.8% 21.3% 28.6% 6.3% 7.3% -24% 4.1% -21.0% -39.9% 18.1% 7.7

Philadelphia, PA N/A N/A N/A N/A -0.4% 0.8% -15% 6.0% 2.2% -3.3% 9.3% N/A

Seattle-Bellevue-Everett, WA 35,090 9.4% 23.9% 28.7% 9.0% 9.2% -25% 6.4% -0.3% -2.7% 18.7% 10.9

Denver-Aurora-Broomfield, CO 50,342 17.8% 23.6% 33.8% 9.1% 8.0% -4% 3.4% -23.9% -43.0% 19.3% 4.0

San Diego-Carlsbad-San Marcos, CA 41,267 12.6% 36.6% 43.6% 3.9% 5.9% -34% 4.7% -27.1% -50.6% 28.1% 6.4

Santa Ana-Anaheim-Irvine, CA 33,130 13.8% 32.1% 35.4% 6.4% 6.5% -32% 4.1% -29.5% -42.6% 18.2% 6.7

Baltimore-Towson, MD 30,766 2.7% 17.0% 24.1% 2.1% 2.1% -23% 8.1% 4.8% -3.9% 18.3% 14.0

Tampa-St. Petersburg-Clearwater, FL 56,307 1.2% 29.0% 35.3% 4.8% 6.3% -44% 16.2% -8.2% -12.6% 45.9% 15.3

Oakland-Fremont-Hayward, CA 37,006 8.6% 39.5% 47.0% 10.8% 11.2% -37% 4.9% -30.0% -50.4% 30.3% 6.9

Nassau-Suffolk, Ny 20,685 -6.9% 5.9% 7.6% 2.3% 2.6% -22% 10.7% 3.7% -0.5% 9.0% 27.1

St. Louis, MO-IL 43,566 7.0% 25.8% 27.4% 0.0% 1.4% -19% 4.5% -12.4% -24.5% 16.2% 5.3

Warren-Troy-Farmington Hills, MI 35,723 -10.3% 34.2% 39.4% 9.9% 7.0% -34% 4.7% -28.8% -56.1% 36.4% 6.7

Portland-Vancouver-Hillsboro, OR-WA 31,413 13.3% 26.3% 30.1% 4.5% 5.2% -25% 5.4% -6.8% -3.1% 18.4% 8.0

Sacramento--Arden-Arcade--Roseville, CA 39,378 6.5% 47.4% 57.0% 9.8% 10.8% -46% 5.7% -30.6% -49.7% 37.5% 6.6

Edison-New Brunswick, NJ 24,523 1.5% 12.2% 12.1% -1.7% -1.3% -26% 9.4% 9.2% 0.0% 15.0% 16.6

Orlando-Kissimmee-Sanford, FL 43,586 -2.5% 38.0% 45.9% 9.6% 11.3% -47% 16.5% -14.3% -18.6% 49.1% 16.2

NOTE: * Data may be light in some jurisdictions. ** Negative Equity Data through Q2 2012.

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

8

The MarketPulse – Volume 1, Issue 12

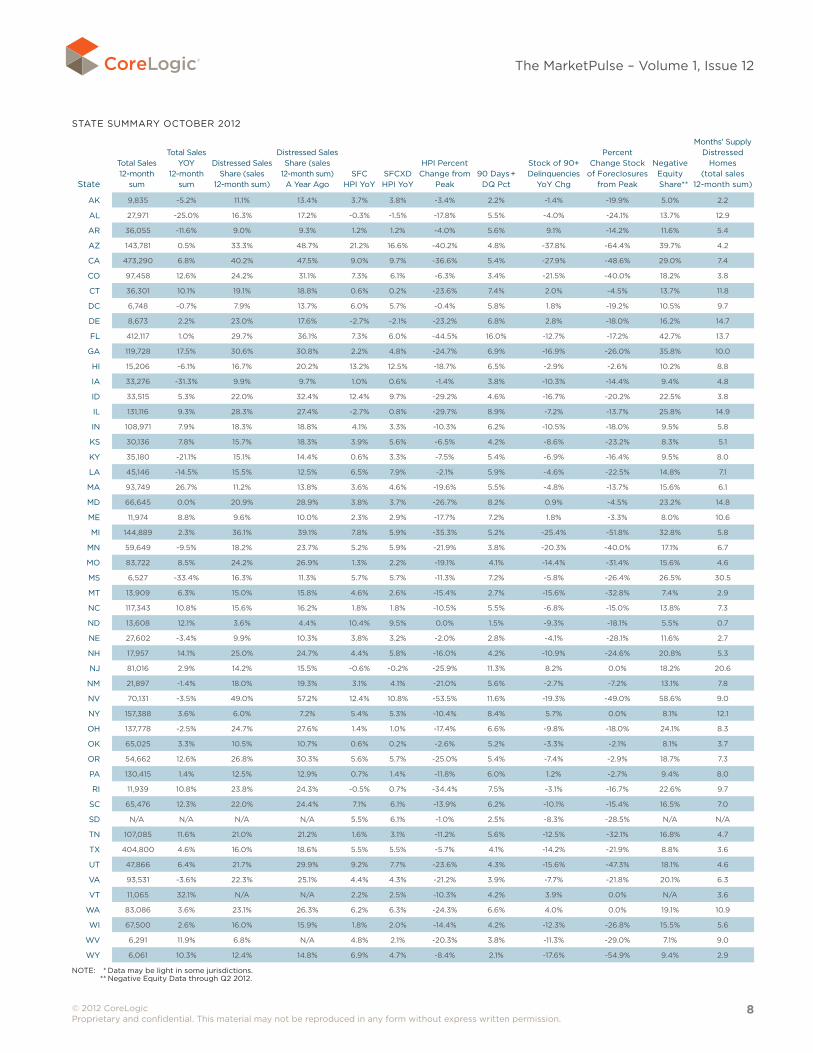

STATE SUMMARy OCTOBER 2012

State

Total Sales 12-month

sum

Total Sales yOy

12-month sum

Distressed Sales Share (sales

12-month sum)

Distressed Sales Share (sales

12-month sum) A year Ago

SFC HPI yoy

SFCXD HPI yoy

HPI Percent Change from

Peak90 Days +

DQ Pct

Stock of 90+ Delinquencies

yoy Chg

Percent Change Stock

of Foreclosures from Peak

Negative Equity

Share**

Months' Supply Distressed

Homes (total sales

12-month sum)

AK 9,835 -5.2% 11.1% 13.4% 3.7% 3.8% -3.4% 2.2% -1.4% -19.9% 5.0% 2.2

AL 27,971 -25.0% 16.3% 17.2% -0.3% -1.5% -17.8% 5.5% -4.0% -24.1% 13.7% 12.9

AR 36,055 -11.6% 9.0% 9.3% 1.2% 1.2% -4.0% 5.6% 9.1% -14.2% 11.6% 5.4

AZ 143,781 0.5% 33.3% 48.7% 21.2% 16.6% -40.2% 4.8% -37.8% -64.4% 39.7% 4.2

CA 473,290 6.8% 40.2% 47.5% 9.0% 9.7% -36.6% 5.4% -27.9% -48.6% 29.0% 7.4

CO 97,458 12.6% 24.2% 31.1% 7.3% 6.1% -6.3% 3.4% -21.5% -40.0% 18.2% 3.8

CT 36,301 10.1% 19.1% 18.8% 0.6% 0.2% -23.6% 7.4% 2.0% -4.5% 13.7% 11.8

DC 6,748 -0.7% 7.9% 13.7% 6.0% 5.7% -0.4% 5.8% 1.8% -19.2% 10.5% 9.7

DE 8,673 2.2% 23.0% 17.6% -2.7% -2.1% -23.2% 6.8% 2.8% -18.0% 16.2% 14.7

FL 412,117 1.0% 29.7% 36.1% 7.3% 6.0% -44.5% 16.0% -12.7% -17.2% 42.7% 13.7

GA 119,728 17.5% 30.6% 30.8% 2.2% 4.8% -24.7% 6.9% -16.9% -26.0% 35.8% 10.0

HI 15,206 -6.1% 16.7% 20.2% 13.2% 12.5% -18.7% 6.5% -2.9% -2.6% 10.2% 8.8

IA 33,276 -31.3% 9.9% 9.7% 1.0% 0.6% -1.4% 3.8% -10.3% -14.4% 9.4% 4.8

ID 33,515 5.3% 22.0% 32.4% 12.4% 9.7% -29.2% 4.6% -16.7% -20.2% 22.5% 3.8

IL 131,116 9.3% 28.3% 27.4% -2.7% 0.8% -29.7% 8.9% -7.2% -13.7% 25.8% 14.9

IN 108,971 7.9% 18.3% 18.8% 4.1% 3.3% -10.3% 6.2% -10.5% -18.0% 9.5% 5.8

KS 30,136 7.8% 15.7% 18.3% 3.9% 5.6% -6.5% 4.2% -8.6% -23.2% 8.3% 5.1

Ky 35,180 -21.1% 15.1% 14.4% 0.6% 3.3% -7.5% 5.4% -6.9% -16.4% 9.5% 8.0

LA 45,146 -14.5% 15.5% 12.5% 6.5% 7.9% -2.1% 5.9% -4.6% -22.5% 14.8% 7.1

MA 93,749 26.7% 11.2% 13.8% 3.6% 4.6% -19.6% 5.5% -4.8% -13.7% 15.6% 6.1

MD 66,645 0.0% 20.9% 28.9% 3.8% 3.7% -26.7% 8.2% 0.9% -4.5% 23.2% 14.8

ME 11,974 8.8% 9.6% 10.0% 2.3% 2.9% -17.7% 7.2% 1.8% -3.3% 8.0% 10.6

MI 144,889 2.3% 36.1% 39.1% 7.8% 5.9% -35.3% 5.2% -25.4% -51.8% 32.8% 5.8

MN 59,649 -9.5% 18.2% 23.7% 5.2% 5.9% -21.9% 3.8% -20.3% -40.0% 17.1% 6.7

MO 83,722 8.5% 24.2% 26.9% 1.3% 2.2% -19.1% 4.1% -14.4% -31.4% 15.6% 4.6

MS 6,527 -33.4% 16.3% 11.3% 5.7% 5.7% -11.3% 7.2% -5.8% -26.4% 26.5% 30.5

MT 13,909 6.3% 15.0% 15.8% 4.6% 2.6% -15.4% 2.7% -15.6% -32.8% 7.4% 2.9

NC 117,343 10.8% 15.6% 16.2% 1.8% 1.8% -10.5% 5.5% -6.8% -15.0% 13.8% 7.3

ND 13,608 12.1% 3.6% 4.4% 10.4% 9.5% 0.0% 1.5% -9.3% -18.1% 5.5% 0.7

NE 27,602 -3.4% 9.9% 10.3% 3.8% 3.2% -2.0% 2.8% -4.1% -28.1% 11.6% 2.7

NH 17,957 14.1% 25.0% 24.7% 4.4% 5.8% -16.0% 4.2% -10.9% -24.6% 20.8% 5.3

NJ 81,016 2.9% 14.2% 15.5% -0.6% -0.2% -25.9% 11.3% 8.2% 0.0% 18.2% 20.6

NM 21,897 -1.4% 18.0% 19.3% 3.1% 4.1% -21.0% 5.6% -2.7% -7.2% 13.1% 7.8

NV 70,131 -3.5% 49.0% 57.2% 12.4% 10.8% -53.5% 11.6% -19.3% -49.0% 58.6% 9.0

Ny 157,388 3.6% 6.0% 7.2% 5.4% 5.3% -10.4% 8.4% 5.7% 0.0% 8.1% 12.1

OH 137,778 -2.5% 24.7% 27.6% 1.4% 1.0% -17.4% 6.6% -9.8% -18.0% 24.1% 8.3

OK 65,025 3.3% 10.5% 10.7% 0.6% 0.2% -2.6% 5.2% -3.3% -2.1% 8.1% 3.7

OR 54,662 12.6% 26.8% 30.3% 5.6% 5.7% -25.0% 5.4% -7.4% -2.9% 18.7% 7.3

PA 130,415 1.4% 12.5% 12.9% 0.7% 1.4% -11.8% 6.0% 1.2% -2.7% 9.4% 8.0

RI 11,939 10.8% 23.8% 24.3% -0.5% 0.7% -34.4% 7.5% -3.1% -16.7% 22.6% 9.7

SC 65,476 12.3% 22.0% 24.4% 7.1% 6.1% -13.9% 6.2% -10.1% -15.4% 16.5% 7.0

SD N/A N/A N/A N/A 5.5% 6.1% -1.0% 2.5% -8.3% -28.5% N/A N/A

TN 107,085 11.6% 21.0% 21.2% 1.6% 3.1% -11.2% 5.6% -12.5% -32.1% 16.8% 4.7

TX 404,800 4.6% 16.0% 18.6% 5.5% 5.5% -5.7% 4.1% -14.2% -21.9% 8.8% 3.6

UT 47,866 6.4% 21.7% 29.9% 9.2% 7.7% -23.6% 4.3% -15.6% -47.3% 18.1% 4.6

VA 93,531 -3.6% 22.3% 25.1% 4.4% 4.3% -21.2% 3.9% -7.7% -21.8% 20.1% 6.3

VT 11,065 32.1% N/A N/A 2.2% 2.5% -10.3% 4.2% 3.9% 0.0% N/A 3.6

WA 83,086 3.6% 23.1% 26.3% 6.2% 6.3% -24.3% 6.6% 4.0% 0.0% 19.1% 10.9

WI 67,500 2.6% 16.0% 15.9% 1.8% 2.0% -14.4% 4.2% -12.3% -26.8% 15.5% 5.6

WV 6,291 11.9% 6.8% N/A 4.8% 2.1% -20.3% 3.8% -11.3% -29.0% 7.1% 9.0

Wy 6,061 10.3% 12.4% 14.8% 6.9% 4.7% -8.4% 2.1% -17.6% -54.9% 9.4% 2.9

NOTE: * Data may be light in some jurisdictions. ** Negative Equity Data through Q2 2012.

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

9

The MarketPulse – Volume 1, Issue 12

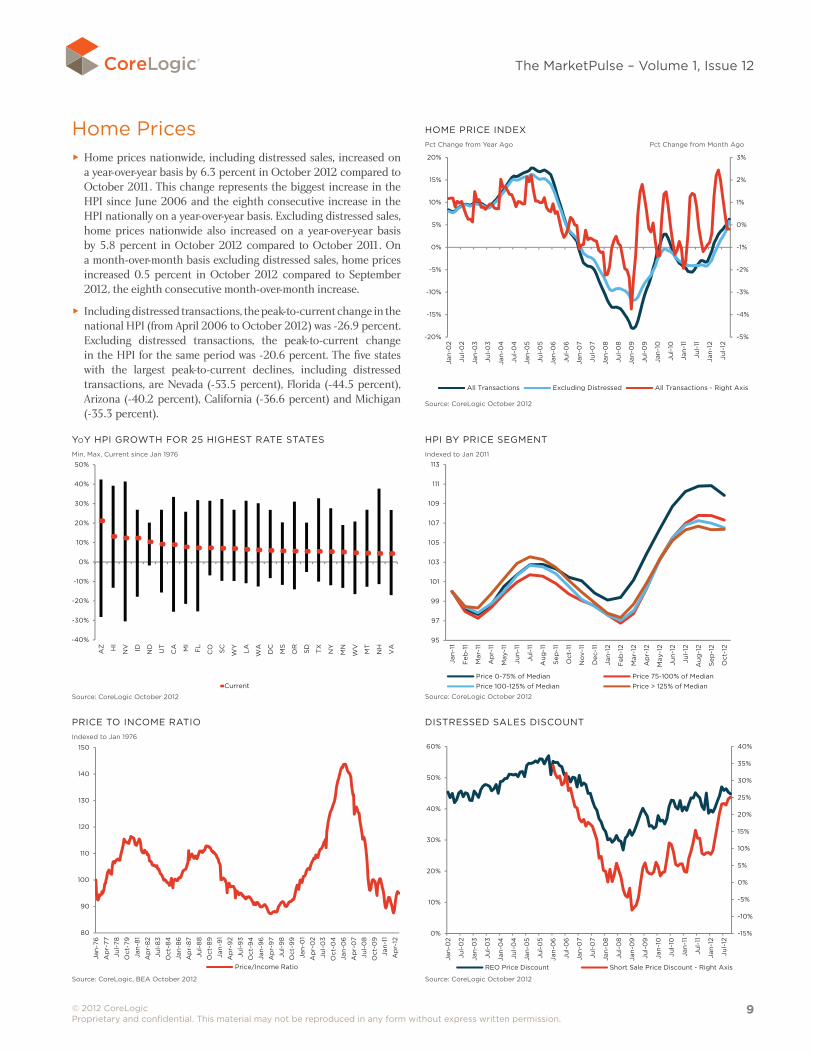

Home Prices ► Home prices nationwide, including distressed sales, increased on a year-over-year basis by 6.3 percent in October 2012 compared to October 2011. This change represents the biggest increase in the HPI since June 2006 and the eighth consecutive increase in the HPI nationally on a year-over-year basis. Excluding distressed sales, home prices nationwide also increased on a year-over-year basis by 5.8 percent in October 2012 compared to October 2011. On a month-over-month basis excluding distressed sales, home prices increased 0.5 percent in October 2012 compared to September 2012, the eighth consecutive month-over-month increase.

► Including distressed transactions, the peak-to-current change in the national HPI (from April 2006 to October 2012) was -26.9 percent. Excluding distressed transactions, the peak-to-current change in the HPI for the same period was -20.6 percent. The five states with the largest peak-to-current declines, including distressed transactions, are Nevada (-53.5 percent), Florida (-44.5 percent), Arizona (-40.2 percent), California (-36.6 percent) and Michigan (-35.3 percent).

yoy HPI GROWTH FOR 25 HIGHEST RATE STATES Min, Max, Current since Jan 1976

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

AZ HI

NV ID ND

UT

CA MI

FL

CO SC

WY

LA

WA

DC

MS

OR

SD TX

NY

MN

WV

MT

NH

VA

Current

2.6x3.57 5pt gothamPrices: yoy hpi growth for 25 lowest rate states oct 2012

Source: CoreLogic October 2012

HPI By PRICE SEGMENT Indexed to Jan 2011

95

97

99

101

103

105

107

109

111

113

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

May

-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

Price 0-75% of Median Price 75-100% of MedianPrice 100-125% of Median Price > 125% of Median

2.6x3.57 5pt gothamPrices: hpi by price segment oct 2012

Source: CoreLogic October 2012

HOME PRICE INDEXPct Change from year Ago Pct Change from Month Ago

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

All Transactions Excluding Distressed All Transactions - Right Axis

2.75x3.66 5pt gotham bookPrices: home price index oct 2012

Source: CoreLogic October 2012

PRICE TO INCOME RATIO Indexed to Jan 1976

80

90

100

110

120

130

140

150

Jan

-76

Ap

r-77

Jul-

78

Oct

-79

Jan

-81

Ap

r-8

2

Jul-

83

Oct

-84

Jan

-86

Ap

r-8

7

Jul-

88

Oct

-89

Jan

-91

Ap

r-9

2

Jul-

93

Oct

-94

Jan

-96

Ap

r-9

7

Jul-

98

Oct

-99

Jan

-01

Ap

r-0

2

Jul-

03

Oct

-04

Jan

-06

Ap

r-0

7

Jul-

08

Oct

-09

Jan

-11

Ap

r-12

Price/Income Ratio

2.49x3.39Prices: price to income ratio oct 2012

Source: CoreLogic, BEA October 2012

DISTRESSED SALES DISCOUNT

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0%

10%

20%

30%

40%

50%

60%

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

REO Price Discount Short Sale Price Discount - Right Axis

2.49x3.39Prices: distressed sales discount oct 2012

Source: CoreLogic October 2012

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

10

The MarketPulse – Volume 1, Issue 12

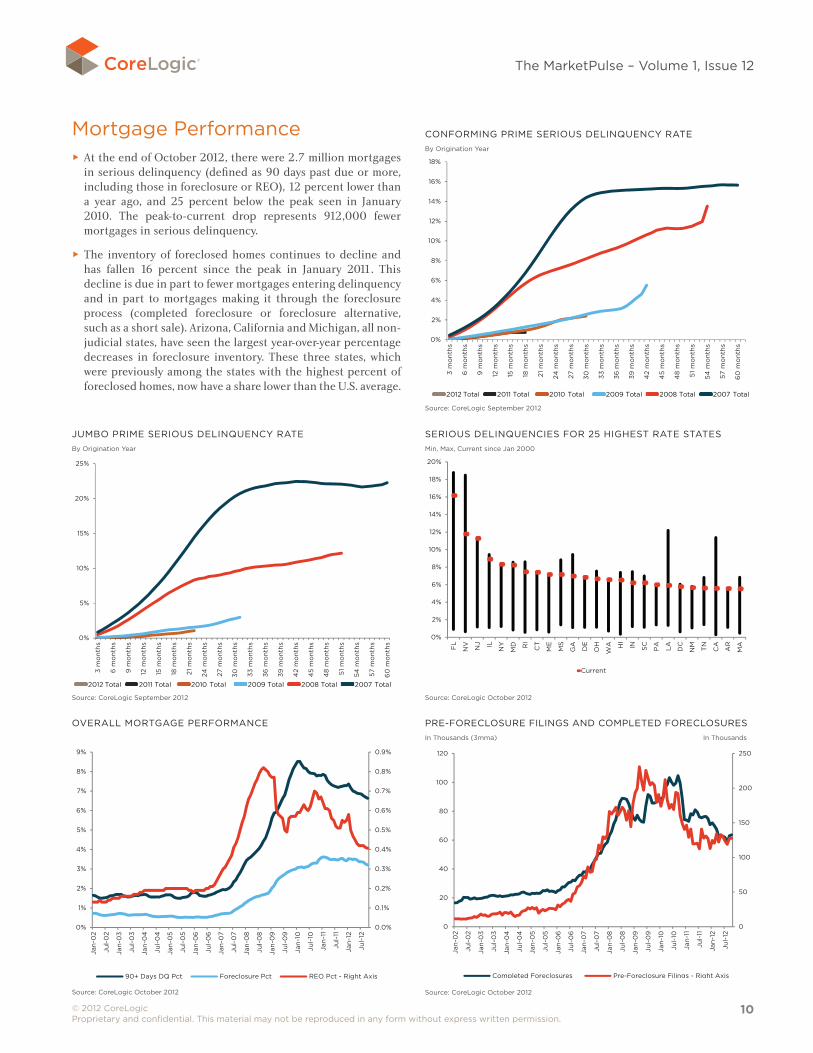

Mortgage Performance ► At the end of October 2012, there were 2.7 million mortgages in serious delinquency (defined as 90 days past due or more, including those in foreclosure or REO), 12 percent lower than a year ago, and 25 percent below the peak seen in January 2010. The peak-to-current drop represents 912,000 fewer mortgages in serious delinquency.

► The inventory of foreclosed homes continues to decline and has fallen 16 percent since the peak in January 2011. This decline is due in part to fewer mortgages entering delinquency and in part to mortgages making it through the foreclosure process (completed foreclosure or foreclosure alternative, such as a short sale). Arizona, California and Michigan, all non-judicial states, have seen the largest year-over-year percentage decreases in foreclosure inventory. These three states, which were previously among the states with the highest percent of foreclosed homes, now have a share lower than the U.S. average.

CONFORMING PRIME SERIOUS DELINQUENCy RATEBy Origination year

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

3 m

on

ths

6 m

ont

hs

9 m

ont

hs

12 m

ont

hs

15 m

ont

hs

18 m

on

ths

21 m

ont

hs

24 m

ont

hs

27 m

ont

hs

30 m

ont

hs

33 m

on

ths

36 m

ont

hs

39 m

ont

hs

42

mo

nths

45

mo

nths

48

mo

nths

51 m

ont

hs

54 m

ont

hs

57 m

ont

hs

60

mo

nths

2012 Total 2011 Total 2010 Total

2009 Total 2008 Total 2007 Total

3.08x3.45Performance: conforming prime serious del rate sep 2012

Source: CoreLogic September 2012

2012 Total 2011 Total 2010 Total 2009 Total 2008 Total 2007 Total

JUMBO PRIME SERIOUS DELINQUENCy RATEBy Origination year

0%

5%

10%

15%

20%

25%

3 m

on

ths

6 m

ont

hs

9 m

ont

hs

12 m

ont

hs

15 m

ont

hs

18 m

on

ths

21 m

ont

hs

24 m

ont

hs

27 m

ont

hs

30 m

ont

hs

33 m

on

ths

36 m

ont

hs

39 m

ont

hs

42

mo

nths

45

mo

nths

48

mo

nths

51 m

ont

hs

54 m

ont

hs

57 m

ont

hs

60

mo

nths

2012 Total 2011 Total 2010 Total

2009 Total 2008 Total 2007 Total

3.1x3.42Performance: jumbo prime serious del rate oct 2012

Source: CoreLogic September 2012

2012 Total 2011 Total 2010 Total 2009 Total 2008 Total 2007 Total

SERIOUS DELINQUENCIES FOR 25 HIGHEST RATE STATESMin, Max, Current since Jan 2000

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%F

L

NV NJ IL NY

MD RI

CT

ME

MS

GA

DE

OH

WA HI

IN SC

PA

LA

DC

NM TN

CA

AR

MA

Current

2.5x3.57Performance: serious del for 25 highest rate states oct 2012

Source: CoreLogic October 2012

OVERALL MORTGAGE PERFORMANCE

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

90+ Days DQ Pct Foreclosure Pct REO Pct - Right Axis

2.53x3.42Performance: overall mortgage performance oct 2012

Source: CoreLogic October 2012

PRE-FORECLOSURE FILINGS AND COMPLETED FORECLOSURESIn Thousands (3mma) In Thousands

0

50

100

150

200

250

0

20

40

60

80

100

120

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Completed Foreclosures Pre-Foreclosure Filings - Right Axis

2.69x3.45Performance: pre foreclosure filings and completed

foreclosures oct 2012

Source: CoreLogic October 2012

© 2012 CoreLogic Proprietary and confidential. This material may not be reproduced in any form without express written permission.

11

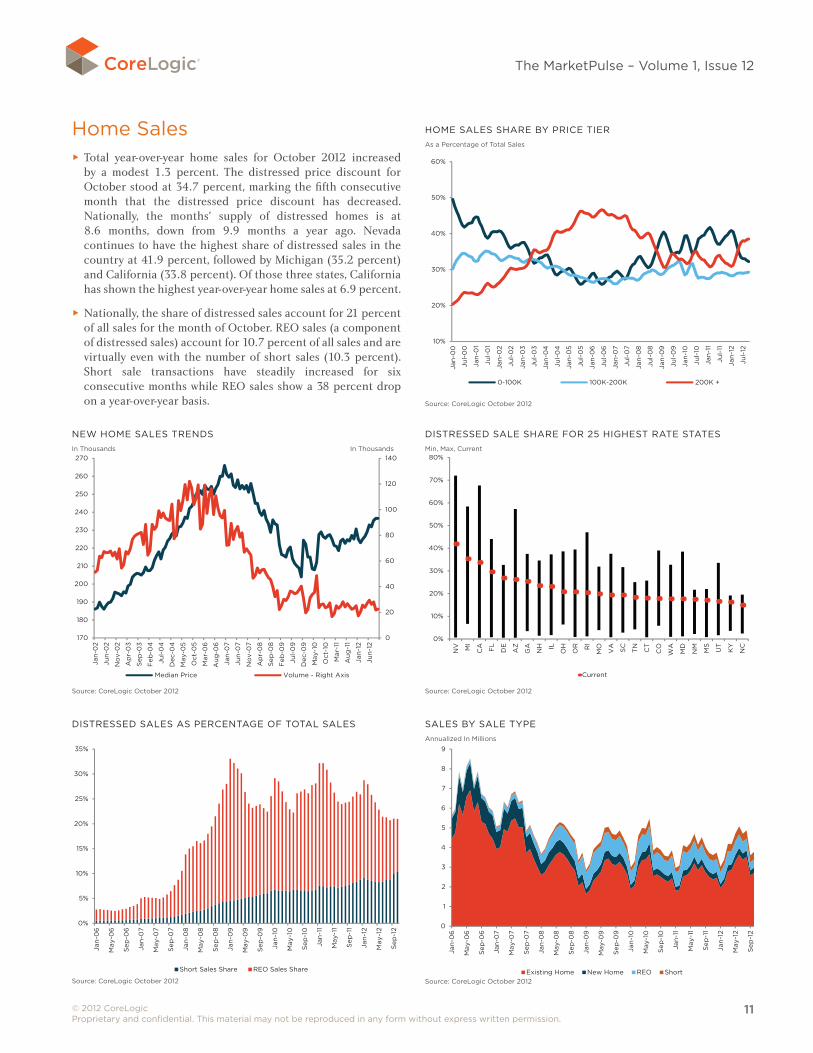

The MarketPulse – Volume 1, Issue 12

Home Sales ► Total year-over-year home sales for October 2012 increased by a modest 1.3 percent. The distressed price discount for October stood at 34.7 percent, marking the fifth consecutive month that the distressed price discount has decreased. Nationally, the months' supply of distressed homes is at 8.6 months, down from 9.9 months a year ago. Nevada continues to have the highest share of distressed sales in the country at 41.9 percent, followed by Michigan (35.2 percent) and California (33.8 percent). Of those three states, California has shown the highest year-over-year home sales at 6.9 percent.

► Nationally, the share of distressed sales account for 21 percent of all sales for the month of October. REO sales (a component of distressed sales) account for 10.7 percent of all sales and are virtually even with the number of short sales (10.3 percent). Short sale transactions have steadily increased for six consecutive months while REO sales show a 38 percent drop on a year-over-year basis.

HOME SALES SHARE By PRICE TIERAs a Percentage of Total Sales

10%

20%

30%

40%

50%

60%

Jan

-00

Jul-

00

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

0-100K 100K-200K 200K +

2.46x3.43Sales: home sales vol by price tier oct 2012

Source: CoreLogic October 2012

NEW HOME SALES TRENDSIn Thousands In Thousands

0

20

40

60

80

100

120

140

170

180

190

200

210

220

230

240

250

260

270

Jan

-02

Jun

-02

No

v-0

2

Ap

r-0

3

Sep

-03

Feb

-04

Jul-

04

Dec

-04

May

-05

Oct

-05

Mar

-06

Aug

-06

Jan

-07

Jun

-07

No

v-0

7

Ap

r-0

8

Sep

-08

Feb

-09

Jul-

09

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug

-11

Jan

-12

Jun

-12

Median Price Volume - Right Axis

2.65x3.62Sales: new home sales trends oct 2012

Feb

-12

Source: CoreLogic October 2012

DISTRESSED SALE SHARE FOR 25 HIGHEST RATE STATESMin, Max, Current

0%

10%

20%

30%

40%

50%

60%

70%

80%N

V MI

CA FL

DE

AZ

GA

NH IL

OH

OR RI

MO

VA SC

TN CT

CO

WA

MD

NM

MS

UT

KY

NC

Current

2.33x3.48Sales: distressed sale share for 25 highest rate states oct 2012

Source: CoreLogic October 2012

DISTRESSED SALES AS PERCENTAGE OF TOTAL SALES

0%

5%

10%

15%

20%

25%

30%

35%

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Short Sales Share REO Sales Share

2.62x3.64Sales: distressed sales as % of total sales oct 2012

Source: CoreLogic October 2012

SALES By SALE TyPEAnnualized In Millions

2.65x3.61Sales: sales by sale type oct 2012

0

1

2

3

4

5

6

7

8

9

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Existing Home New Home REO ShortSource: CoreLogic October 2012

corelogic.com

© 2012 CoreLogic, Inc. All rights reserved.

CoreLogic, the CoreLogic logo, and HPI are trademarks of CoreLogic, Inc. and/or its subsidiaries.

17-MKTPLSEQTR-1212-00

Source: CoreLogicThe data provided is for use only by the primary recipient or the primary recipient's publication or broadcast. This data may not be re-sold, republished or licensed to any other source, including publications and sources owned by the primary recipient's parent company without prior written permission from CoreLogic. Any CoreLogic data used for publication or broadcast, in whole or in part, must be sourced as coming from CoreLogic, a data and analytics company. For use with broadcast or web content, the citation must directly accompany first reference of the data. If the data is illustrated with maps, charts, graphs or other visual elements, the CoreLogic logo must be included on screen or website. For questions, analysis or interpretation of the data, contact CoreLogic at [email protected]. Data provided may not be modified without the prior written permission of CoreLogic. Do not use the data in any unlawful manner. This data is compiled from public records, contributory databases and proprietary analytics, and its accuracy is dependent upon these sources.

FOR MORE INFORMATION PLEASE CALL 1-415-536-3500The MarketPulse is a newsletter published by CoreLogic, Inc. ("CoreLogic"). This information is made available for informational purposes only and is not intended to provide specific commercial, financial or investment advice. CoreLogic disclaims all express or implied representations, warranties and guaranties, including implied warranties of merchantability, fitness for a particular purpose, title, or non-infringement. Neither CoreLogic nor its licensors make any representations, warranties or guaranties as to the quality, reliability, suitability, truth, accuracy, timeliness or completeness of the information contained in this newsletter. CoreLogic shall not be held responsible for any errors, inaccuracies, omissions or losses resulting directly or indirectly from your reliance on the information contained in this newsletter.

This newsletter contains links to third-party websites that are not controlled by CoreLogic. CoreLogic is not responsible for the content of third-party websites. The use of third-party website and its content is governed by the terms and conditions set forth on the third-party’s site and CoreLogic assumes no responsibility for your use of or activities on the site.

VARIABLE DESCRIPTIONS

Variable Definition

Total Sales The total number of all home-sale transactions during the month.

New Sales The total number of newly constructed residential housing units sold during the month.

Existing SalesThe number of previously constructed homes that were sold to an unaffiliated third party. DOES NOT INCLUDE REO AND SHORT SALES.

REO Sales Number of bank-owned properties that were sold to an unaffiliated third party.

Short SalesThe number of short sales. A short sale is a sale of real estate in which the sale proceeds fall short of the balance owed on the property's loan.

Distressed Sales Share The percentage of the total sales that were a distressed sale (REO or short sale).

HPI MoM Percent increase or decrease in HPI single family combined series over a month ago.

HPI yoy Percent increase or decrease in HPI single family combined series over a year ago.

HPI MoM Excluding Distressed Percent increase or decrease in HPI single family combined excluding distressed series over a month ago.

HPI yoy Excluding Distressed Percent increase or decrease in HPI single family combined excluding distressed series over a year ago.

90 Days + DQ Pct The percentage of the overall loan count that are 90 or more days delinquent as of the reporting period. This percentage includes loans that are in foreclosure or REO.

Foreclosure Pct The percentage of the overall loan count that is currently in foreclosure as of the reporting period.

REO Pct The count of loans in REO as a percentage of the overall count of loans for the reporting period.

Pre-foreclosure FilingsThe number of mortgages where the lender has initiated foreclosure proceedings and it has been made known through public notice (NOD).

Completed ForeclosuresA completed foreclosure occurs when a property is auctioned and results in either the purchase of the home at auction or the property is taken by the lender as part of their Real Estate Owned (REO) inventory.

Negative Equity ShareThe percentage of mortgages in negative equity. The denominator for the negative equity percent is based on the number of mortgages from the public record.

Negative EquityThe number of mortgages in negative equity. Negative equity is calculated as the difference between the current value of the property and the estimated unpaid principal balance. If the mortgage debt is greater than the current value, the property is considered to be in a negative equity position.

Months' Supply Distressed HomesThe number of months it would take to sell all homes currently in distress of 90 days past due or more based on the current sales pace.

Total Sales yoy Change 12-month sum Percent increase or decrease in current 12 months of total sales over prior 12 months of total sales.

Price/Income Ratio CoreLogic HPI divided by Nominal Personal Income provided by the Bureau of Economic Analysis.