the means: to change places for the better. - wordpress.com · feasibility study report date:...

TRANSCRIPT

A BUSINESS IMPROVEMENT DISTRICT FOR NEWPORT?

FEASIBILITY STUDY REPORT

Date: 25/5/2014

Prepared by: Peter Williams, Tom Evans and Becky Chantry

The means: to change places for the better.

Executive summary ................................................................................................................................. 3

1.0 Introduction & methodology............................................................................................................. 5

1.1 The project brief ............................................................................................................................ 5

1.2 Methodology ................................................................................................................................. 5

2.0 Results of the business interviews .................................................................................................... 7

2.1 Business Health ............................................................................................................................. 9

2.2 Top issues for businesses in Newport city centre ....................................................................... 11

2.2.1 Vacant premises ................................................................................................................... 11

2.2.3 Perception of crime .............................................................................................................. 12

2.2.4 Levels of marketing and promotion ..................................................................................... 12

2.2.5 Cleanliness ............................................................................................................................ 12

2.3 Improvements to the city centre ................................................................................................ 13

2.3.1 Parking .................................................................................................................................. 14

2.3.2 Anti-social behaviour ............................................................................................................ 14

2.3.3 Increase promotional activity ............................................................................................... 14

2.3.4 Improvments to shop fronts ................................................................................................ 14

2.4 Issues in the Kingsway Centre vs. the rest of Newport city centre ............................................. 15

2.5 Reactions to concept of a BID for Newport ................................................................................ 16

2.5.1 BID concept support ............................................................................................................. 16

2.5.2 Targeting spending ............................................................................................................... 17

What should the focus of a BID in Newport City Centre be? ........................................................ 17

4.0 Potential BID levy outturn ............................................................................................................... 25

4.1 The UK Average BID & Newport .................................................................................................. 25

4.2 Potential levy income .................................................................................................................. 26

4.3 Levy rates by BID area ................................................................................................................. 27

4.4 Top ten hereditaments and potential levy payers ..................................................................... 30

5.0 Feasiblity matrix .............................................................................................................................. 31

6.0 Conclusions and recommendations for phase two ......................................................................... 34

6.1 Suggested themes for BID programme ....................................................................................... 34

6.2 Recommendations and next steps .............................................................................................. 36

EXECUTIVE SUMMARY

In November 2013 The means was commissioned by Newport Unlimited and the Chamber of Trade to

conduct a feasibility study to explore the potential of developing a Business Improvement District (BID)

in Newport City Centre. This was preceded by an initial scoping study, which was conducted between

May and July 2013. In total, one hundred and four businesses were interviewed across the centre,

including those based on Commercial Street, Bridge Street, Cambrian Road, Charles Street, High

Street, John Frost Square, the Kingsway Centre, Stow Hill, Upper Dock Street, Llanarth Street, Docks

Way and Newport Market. These surveys aimed to test business reactions to the concept of a BID and

capture issues in the city centre and the best ways to tackle them.

In addition to business interviews, a Symposium event was held as part of the scoping study at which

businesses discussed in themed groups the potential BID and its priorities.

Overall, the survey results demonstrated that business health in the city centre was varied. For

example, a similar number of businesses reported that their turnover had declined over the past

12months as reported that their businesses had improved.

The results also highlighted the following key points:

A significant number of businesses identified vacant premises, perception of crime, parking

(cost and availability) and marketing of the centre as being the most important issues.

Results were broken down between the primary retail area and other areas of the city centre

but there was generally consensus on the top issues.

In terms of measures for improving the area, the majority of businesses identified providing

easier and cheaper parking, reducing anti-social behaviour and increasing promotional activity

as key areas for action.

When asked directly about their views about the BID concept in principle, 74% of respondents

were positive and 23% unsure. Only 8% were negative.

Based on the above evidence, this report therefore concludes that Newport City Centre should move

toward a BID ballot either at the end of 2014 or early in 2015.

The report recommends that the BID programme be based on four themes:

Accessibility & Attractiveness

Safety & Welcome

Marketing & Events

Future Newport: City Centre Strategy & Advocacy

It is recommended that the proposed BID’s programme of improvements complement the services and

projects of reNewport, The Newport Business Development Task Force, the local authority and local

cultural, civic and community groups. Areas of collaboration could include cultural activities, digital

high street projects and health/sporting initiatives.

1.0 INTRODUCTION & METHODOLOGY

1.1 The project brief

The means was initially commissioned by Newport Unlimited, with Newport Chamber of Trade, to

complete a scoping study in May 2013. This was followed by a further commission, in November

2013, to carry out a feasibility study into the development of a BID in Newport City Centre.

The appointment followed the initiation of an exploration into the opportunities presented by the BID

mechanism by a core of local businesses in late 2012. Two public meetings were held in 2013 and a

Steering Group was then formed to lead further investigations, engage with other traders and review

business sentiments.

This study represents a significant step in the work to explore the option of a BID in Newport City

Centre, and to ascertain whether a BID would be an effective mechanism to address current issues

and seize new opportunities.

1.2 Methodology

The feasibility study focused on gathering opinions on issues that were important to businesses in

Newport City Centre and views on measures to improve trading conditions. The study also aimed to

raise awareness and gauge levels of support among businesses for a Business Improvement District.

1.2.1 Business consultation: scoping & feasibility

The business consultation was conducted in both feasibility and scoping phases where interviews took

place on a face-to face basis at individual business premises. Where possible the most senior

member of staff was interviewed, which in most cases was the store manager/ owner or a company

director. During the interview, whilst being asked general questions to determine business issues and

trends, the concept of a BID was introduced. A full list of the businesses consulted as well as a copy

of the questionnaire used can be found in the appendices. The result of the business interviews can

be found in Section 2.

1.2.2 Symposium

The symposium event, organised as part of the scoping exercise, helped to inform this study. The

event was hosted on the evening of the 27th June 2013 at Breeze Bar, Cambrian Road Newport. The

event provided an opportunity to pool thinking around what the main issues for businesses in Newport

City Centre were, what was currently being done, what else could be done to improve the viability &

vitality of the centre and what role a BID might play.

Following a lively and constructive group discussion session, a member from each group provided

feedback to all attendees to highlight key areas they had identified. From this event the following key

issues and common themes emerged:

Tackle negativity about Newport & promote its individuality – Strategy & PR campaign

Address the issue of empty shops – attract new businesses & introduce meanwhile projects

Utilize the creative sector & develop distinctive cultural events

Improve parking locations & introduce parking promotions

Tackle anti-social behaviour & improve co-ordination of initiatives/services

Further details regarding the event, along with outcomes, can be found in the appendices.

2.0 RESULTS OF THE BUSINESS INTERVIEWS

The means conducted a total of 104 interviews over a six month period, which aimed to gather a cross

section of businesses views. The interviews were designed to ascertain;

1) The nature of the business and its current health

2) The individual’s view of the key issues facing Newport City Centre and possible measures to

improve trading conditions

3) Reaction to the idea in principle of a Business Improvement District.

It was relatively easy to meet and have a face-to-face discussion with the businesses across Newport

City Centre. Senior decision maker (managers or owners) were generally in attendance or readily at

hand, and happy to take the time away from their duties to complete the survey. With chain or

franchise retailers the situation was similar. However some managers found it difficult to engage fully

because they felt they weren’t empowered to do so. Office-based businesses and top levy payers

required a meeting to be set up in advance but were also relatively easy to engage.

Within the sample, 60% of businesses were franchises whilst 40% were classed as independent.

Q1. Business type: Independent or part of a wider group?

Graph 1: Breakdown of businesses by sector

Business interviews covered a broad spread of sectors, shown as follows:

Graph 2: Breakdown of businesses by type

These were grouped into four basic sectors to help simplify comparisons.

Retail: Non Food Retail, Food (butchers etc.), convenience stores, Fashion Retail and

Newsagents.

Hospitality: Restaurants, hotels, bars, cafes and pubs.

Services: Community Facilities, Motor Trade, Leisure, Other Services and Professional

Services (estate agents, banks etc.).

Other in Newport includes charities, housing associations and libraries.

4% 17%

6%

11%

21%

13%

3%

4%

0%

1%

8%

2% 5% 5%

Q2. Nature/type of business

Food/Grocer

Small Household goods

Large Household goods

Restaurant

Fashion/retail

Professional

Other Service

Pub

Community Facilities

Motor related

Leisure

Newsagent

Graph 3: Breakdown of businesses by group types

2.1 Business Health

A number of questions were asked to determine business health. These included whether turnover

had grown, declined or remained stable, what plans the business had for the next 12 months and

whether there were plans to recruit anymore personnel.

Graph 4: Business performance in 2012/13

This pie chart shows that different businesses have had a variety of experiences in terms of trading

conditions. When asked to comment further, many businesses said that footfall has decreased since

stores had vacated the centre and many attributed the decline to online shopping and competition

from out of town shopping destinations, such as Spytty Park, and Cwmbran.

59% 23%

12% 6%

Business sector

Retail

Services

Hospitality

Other

35%

26%

39%

Q3. How is your business performing?

Improved

Remained the same

Declined

Graph 5: Business optimism

The majority of businesses identified that within the next 12 months they thought that the businesses

would remain the same. A small number, 17%, identify the potential for expansion, but very few

businesses planned to leave the centre.

Graph 6: Recruitment plans

With regards to recruitment, the majority of businesses were not planning to hire more staff at the time

interviews took place. Nevertheless, around a quarter of those interviewed said that they were

planning to recruit, indicating a positive outlook amongst a section of the business community.

17%

80%

3%

Q4. What are your plans for the next 12 months?

Expand

Stay the same

Leave the centre

26%

65%

9%

Q5.Do you have any plans to recruit any more personnel?

Yes

No

Maybe

2.2 Top issues for businesses in Newport city centre

Businesses were presented with a list of issues and asked whether they believed them to be a

significant issue, minor issue or not a problem.

Graph 7: Issues in Newport City Centre

2.2.1 Vacant premises

The biggest issue for Newport City Centre appears to be vacant premises. 90% of respondents

described this as a significant issue, whilst a mere 3% identified this as not being an issue. This

appears to be a significant problem for the city centre, which has higher vacancy rates than the

national average.

Many businesses represented in the sample expressed an urgency to fill the empty shops with start-

ups and provide rates relief in order to help them do so. Charity stores appeared to be an unfavorable

way of filling empty units.

2.2.2 Parking

As with many urban centers across the UK, parking appeared to be a significant problem for traders,

especially in terms of cost and location. Over 70% identified this as an issue, with 60% highlighting it

as a big issue. In their comments respondents referred to Cwmbran and Spytty Park’s free parking.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q6.How much of an issue is the following?

Big issue Small Issue Not an issue

2.2.3 Perception of crime

Over 80% identified perception of crime to be an issue, with 58% saying that is a big issue. Many

respondents described anti-social behaviour as a significant problem.

2.2.4 Levels of marketing and promotion

Marketing of the centre was also recognised as a big issue by many businesses interviewed. 48% of

respondents highlighted this as a big issue, whilst a further 20% said this was a small issue. Many

traders noted that the city centre needs to be promoted more effectively, similar to the ways in which

Cwmbran and Cardiff’s St David’s Centre are marketed.

2.2.5 Cleanliness

Across the city centre respondents provided different views on the cleanliness of streets and pubic

spaces. Those businesses interviewed towards the north of the centre, around the market, and

towards the lower end of Commercial Street identified cleanliness as a big issue. Chewing gum on

the streets, ‘grot spots’ and cleanliness towards the rear of shop units were identified as significant

problems.

2.3 Improvements to the city centre

Following on from the discussion around issues in the city centre, businesses were presented with a

list of measures and asked whether they felt each would help improve the centre ‘a lot’, ‘a little’ or ‘not

at all’. Additional time was also allocated to discussing other issues that the business felt would

enhance the trading environment.

Graph 8: Measures to improve Newport City Centre

0

10

20

30

40

50

60

70

80

90

100

Q7. How much would the following improve the centre?

A lot A little Not at all

2.3.1 Parking

Those interviewed felt that making improvements to the centre’s parking provision, both in terms of

ease and cost, would significantly improve trading conditions. This was noted by over 80% of

respondents who felt that measures in this area would help a lot and a little. Many traders compared

the cost of parking to other nearby retail areas, such as Cwmbran and Spytty, and noted that there

was not a level playing field.

2.3.2 Anti-social behaviour

Over 90% of businesses consulted thought that reducing anti-social behavior would either improve the

center a lot or a little. The type of behavior identified appeared to range from street drinking and

swearing to shoplifting and fighting.

2.3.3 Increase promotional activity

Promotional activity, including events, was identified as an effective way to improve trading conditions

and to celebrate what the area had to offer. A number of those interviewed felt that the city had

developed a bad image and that there was a lot of work to be done to change perceptions. Many of

those businesses interviewed noted that when events do occur in city centre they are not informed of

them in advance.

2.3.4 Improvments to shop fronts

80% of respondents identified improvements to shop-fronts as a way to advance the city centre.

Enhancing the look of empty units was highlighted as a solution to improving the appearance of the

area and making it more appealing to visitors.

2.4 Issues in the Kingsway Centre vs. the rest of Newport city centre

Since the Kingsway Centre has its own level of service, being within a managed shopping centre that

provides services such as security and marketing, it is important to briefly look at whether business

views here varied from those in other city centre areas.

During discussions with business representatives based in the Kingsway Centre the following trends

emerged:

Issues-

Ease of parking appeared to be less of an issue in the Kingsway Centre due its 2 hour free car

parking offer.

Security was identified as only a small issue, as they have security guards who regularly visit

and engage well with businesses. Consequently perception of crime is also lower.

Like the rest of Newport city centre, empty shops were identified as the most significant issue

for businesses

Signage appeared to be more significant problem for those based in the Kingsway Centre.

Many respondents said that construction work outside the centre and the relocation of the bus

station made the shopping centre difficult to find.

Improvements-

Filling empty premises and reducing rates were seen as key improvements.

More businesses in the Kingsway Centre wanted to advance business networking than

elsewhere in the city centre.

It was felt that promoting the city centre as a whole would be beneficial as it would drive up

footfall.

Although there are differences in opinion amongst those businesses consulted in the Kingsway Centre

compared to those outside, these are relatively minor and a general consensus exists between all

businesses regarding increasing footfall and creating a thriving commercial district. Since the

Kingsway Centre respondents felt that they already receive a degree of service, however, it could be

suggested that they be charged a smaller levy than those in the rest of the city centre who do not pay

such a service charge.

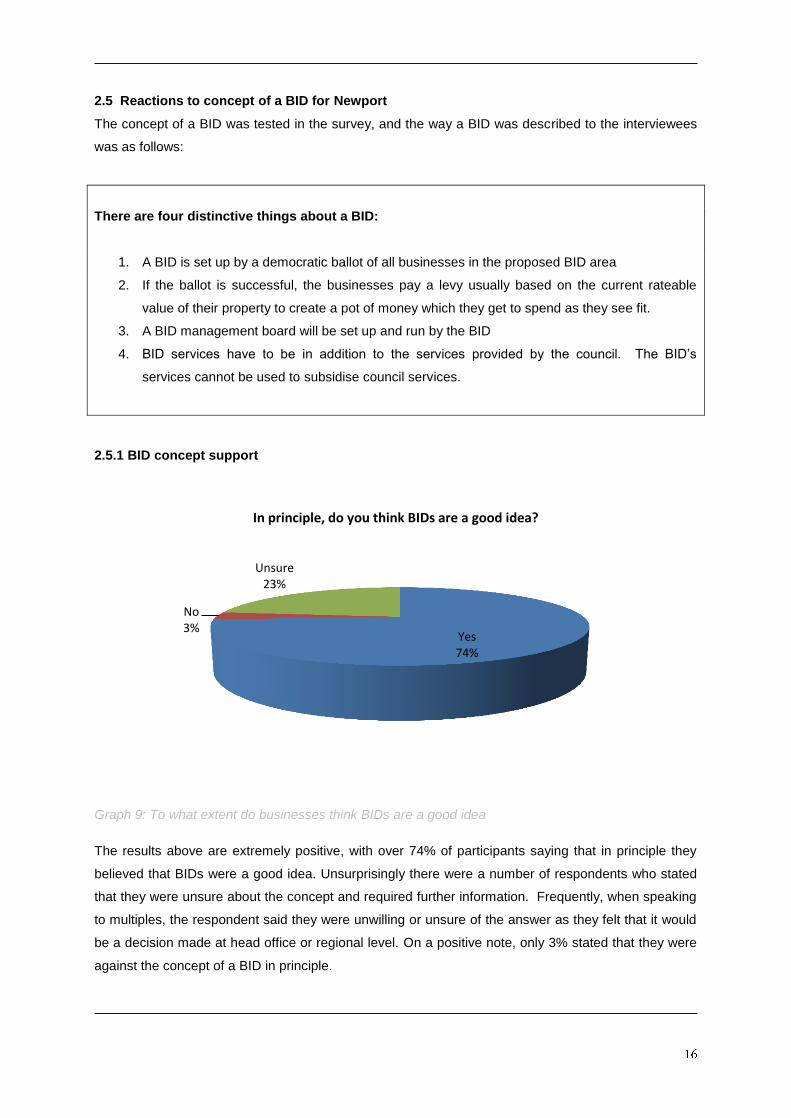

2.5 Reactions to concept of a BID for Newport

The concept of a BID was tested in the survey, and the way a BID was described to the interviewees

was as follows:

There are four distinctive things about a BID:

1. A BID is set up by a democratic ballot of all businesses in the proposed BID area

2. If the ballot is successful, the businesses pay a levy usually based on the current rateable

value of their property to create a pot of money which they get to spend as they see fit.

3. A BID management board will be set up and run by the BID

4. BID services have to be in addition to the services provided by the council. The BID’s

services cannot be used to subsidise council services.

2.5.1 BID concept support

Graph 9: To what extent do businesses think BIDs are a good idea

The results above are extremely positive, with over 74% of participants saying that in principle they

believed that BIDs were a good idea. Unsurprisingly there were a number of respondents who stated

that they were unsure about the concept and required further information. Frequently, when speaking

to multiples, the respondent said they were unwilling or unsure of the answer as they felt that it would

be a decision made at head office or regional level. On a positive note, only 3% stated that they were

against the concept of a BID in principle.

Yes 74%

No 3%

Unsure 23%

In principle, do you think BIDs are a good idea?

2.5.2 Targeting spending

After respondents began to understand the concept and the types of services a BID might deliver, they

were asked to suggest priorities for such a body if one was formed in Newport City Centre. The

budgets from Merthyr Tydfil and Swansea BIDs were used to show respondents what type of revenue

different size centres in Wales can raise from a BID levy.

The world cloud below shows the ideas suggested by respondents for targeting spending. The most

popular suggestions were enticing new businesses, parking, events and promotions, reducing anti-

social behavior and empty shops projects.

What should the focus of a BID in Newport City Centre be?

Image 1: Focus of a BID in Newport Word Cloud

3.0 Characteristics of Newport’s central areas

3.1 Area description

For the purposes of the feasibility study, the central areas of Newport were divided up into the

following main areas: The Core City Centre, Docks Way, Goldtops, Commercial Road, Clarence Place

and Corporation Road:

The City Centre Core: this is the main commercial area stretching from the railway station in

the North to George Street in the South and from the banks of the River Usk to Ivor Street and

Stow Hill. The area contains a number of retail units, featuring national chains, independent

businesses, professional services, cafes, bars and an indoor market. It is also home to a

campus of the University of South Wales and the Council’s Information Station. The area has

suffered a well-publicised decline to the retail core in recent years and the loss of a number of

key businesses, including a Marks & Spencer store.

Docks Way: A new development area, which runs along the River Usk to the South East of

the core city centre area. This is now home to The Passport Office, Magistrates Court and

Newport City Homes. The area also contains two supermarkets, Lidl and Asda, as well as a

couple of independent businesses.

Goldtops: This area is north of the railway station and runs from Devon Place and Godfrey

Road to Goldtops. Many offices are located in this area, together with the Council’s Civic

Centre and health care providers such as dentists.

Commercial Road: A secondary shopping area which runs south of the core central area. It

is home to a range of independent and ethnic businesses and forms the commercial centre of

the Pill area. It also features a number of community facilities, bars and cafes, along with the

central police station.

Clarence Place & Corporation Road: located on the eastern banks of the River Usk, Clarence

Place and Corporation Road is home to Rodney Parade, the stadium for the city’s football and

rugby teams, as well as a number of restaurants and pubs. The area is seeing a number of

residential units being constructed along the waterfront.

3.2 Newport City Centre – Options for the BID area

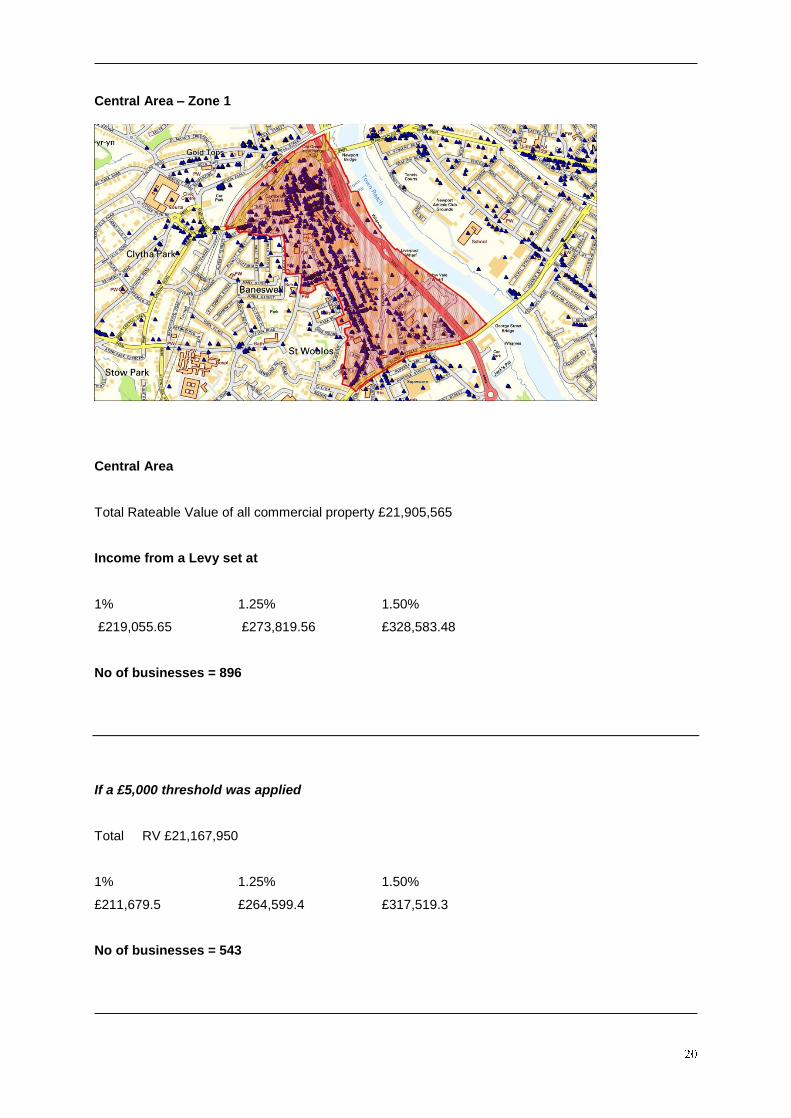

Central Area – Zone 1

Central Area

Total Rateable Value of all commercial property £21,905,565

Income from a Levy set at

1% 1.25% 1.50%

£219,055.65 £273,819.56 £328,583.48

No of businesses = 896

If a £5,000 threshold was applied

Total RV £21,167,950

1% 1.25% 1.50%

£211,679.5 £264,599.4 £317,519.3

No of businesses = 543

Corporation Road – Zone 2

Corporation Road

Total Rateable Value of all commercial property £2,220,145

Income from a Levy set at

1% 1.25% 1.50%

£22,201.45 £27,751.81 £33,302.18

No of businesses = 142

If a £5,000 threshold was applied

Total RV £2,074,550.00

Levy

1% 1.25% 1.50%

£20,745.50 £25,931.88 £31,118.25

No of businesses = 75

Docks Way – Zone 3

Docks Way

Total Rateable Value of all commercial property £3,604,823

Income from a Levy set at

1% 1.25% 1.50%

£36,048.23 £45,060.29 £54,072.35

No of businesses = 63

If a £5,000 threshold was applied

Total RV £3,533,800

Levy

1% 1.25% 1.50%

£35,338.00 £44,172.50 £53,007.00

No of businesses = 28

Gold Tops – Zone 4

Gold Tops

Total Rateable Value of all commercial property £2,423,415

Income from a Levy set at

1% 1.25% 1.50%

£24,234.15 £30,292.69 £36,351.23

No of businesses = 109

If a £5,000 threshold was applied

Total RV £2,340,500

Levy

1% 1.25% 1.50%

£23,405.00 £29,256.25 £35,107.50

No of businesses = 72

Commercial Road (Pill) – Zone 5

Commercial Road (Pill)

Total Rateable Value of all commercial property £378,590

Income from a Levy set at

1% 1.25% 1.50%

£3,785.90 £4,732.38 £5,678.85

No of businesses =102

If a £5,000 threshold was applied

Total RV £201,350

Levy

1% 1.25% 1.50%

£2,013.50 £2,516.88 £3,020.25

No of businesses = 22

4.0 Potential BID levy outturn

4.1 The UK Average BID & Newport

According to the 2013 National BIDs Survey, produced by British BIDs, the outturn raised by the

smallest annual levy income is £22,400 at London’s New Addington BID. The largest annual levy

income is £2,814,000 at London’s New West End Company.

The means maintains a model of the UK Average BID. At the 9th April the model shows the following

outcomes. This illustrates that the average BID levy in the UK is 1.4% and average levy outturn is

£365,000:

Image 2: The means UK Average BID model

It is proposed that Newport will follow the UK average with a levy rate between 1 and 1.5%. This will

raise an annual total levy income slightly lower than the UK average which, dependent on the levy

percent, will collect in the region of £250,000 per annum.

4.2 Potential levy income

The tables below set out the potential levy income for Newport City Centre when different levy rates

and rateable value thresholds are applied. In most BID areas some form of threshold is applied,

partly to ensure that the costs of collecting the levy from smaller businesses does not exceed the levy

they pay, but also to keep the number of BID businesses down to a level with which the BID board and

team can reasonably communicate. The ratings threshold in Merthyr Tydfil, for example, was set at

£5,000.

Table 1: BID LEVY OUTTURN BY ZONE – No threshold

Zone Total levy at 1% Total levy at 1.25% Total levy at 1.5%

Zone 1 – Central Core £219,055.65 £273,819.56 £328,583.48

Zone 2 – Corporation

Road

£22,201.45 £27,751.81 £33,302.18

Zone 3 – Docks Way £36,048.23 £45,060.29 £54,072.35

Zone 4 – Goldtops £24,234.15 £30,292.69 £36,351.23

Zone 5 – Commercial

Road

£3,785.90 £4,732.38 £5,678.85

Total £305,325.38 £381,656.73 £457,988.09

Number of businesses: 1312

Table 2: Levy Outturns – £5,000 threshold

Zone Total levy at 1% Total levy at 1.25% Total levy at 1.5%

Zone 1 – Central Core £211,679.5 £264,599.4 £317,519.3

Zone 2 – Corporation

Road

£20,745.50 £25,931.88 £31,118.25

Zone 3 – Docks Way £35,338.00 £44,172.50 £53,007.00

Zone 4 – Goldtops £23,405.00 £29,256.25 £35,107.50

Zone 5 – Commercial

Road

£2,013.50 £2,516.88 £3,020.25

Total £293,181.50 £366,476.91 £439,772.30

Number of businesses: 740

4.3 Levy rates by BID area

In addition to setting the levy rate and threshold, there are a number of other options to consider in

setting up a BID most importantly the definition of the area which could be any combination of the

zones identified above.

The existence of a service charge is another consideration. The Kingsway Centre currently provides a

number of services to its tenants paid for through their service charge that in other areas could be

considered core BID activities. This is likely to be the same for the new Friars Walk development.

One option would therefore be to reduce the levy rate by say10-20% for those businesses located in

serviced shopping centres. .

The table below sets out the potential levy outturn in the case of the six different options – each with a

£5,000 rateable value threshold:

Option 1: All Zones

Option 2: Zone 1

Option 3: Zones 1,2,3,4

Option 4: Zones 1&2

Option 5: Zones 1&3

Option 6: Zones 1&4

Option 7: Zones 1&5

Option 8; Zones 1, 2 & 3

Option 9: Zones 1, 2&4

It should be noted that in light of the new developments taking place in the city centre, notably Friars

Walk and the Admiral offices, the BID would likely see an increase in funding from additional

hereditaments in future years.

Table 3: BID LEVY OUTTURN BY OPTION – HEREDITAMENTS ABOVE £5,000 RV THRESHOLD

Option Total number of

hereditaments

Total Levy outturn

@1%

Total levy outturn at

1.25%

Option 1: All Zones 740 £293,181.50 £366,476.91

Option 2: Zone 1 543 £211,679.50 £264,599.40

Option 3: Zones 1,2,3,4 718 £291,168.00 £363,960.03

Option 4: Zones 1&2 618 £232,425.00 £290,531.28

Option 5: Zones 1&3 571 £247,017.50 £308,771.90

Option 6: Zones 1&4 615 £235,084.50 £293,855.65

Option 7: Zones 1&5 565 £213,693.00 £267,116.28

Option 8; Zones 1,2 & 3 646 £267,763.00 £334,703.78

Option 9: Zones 1,2&4 690 £255,830.00 £319,787.53

Recommended option =

The British Retail Consortium has stated that ‘any levy in excess of 1% of rateable value will be

extremely unlikely to deliver comparable benefits and is therefore unjustified’. However, the national

average BID levy is 1.4%, and our experience in other centres shows that retailers will pay a slightly

higher levy if they feel that it is justified by the proposed programme, and can either improve their

sales or mitigate a decline in sales. In Merthyr Tydfil, for examples, the levy rate was set at 1.35%.

Considering trading condition in Newport City Centre and the potential services that a BID might

deliver, we would recommend a levy rate of 1.25% be considered by the BID board.

We are not at this stage proposing that the levy should be ‘capped’ for any of the larger payers. This

position may change if, for example any large occupiers make capping a condition of their support for

the BID.)

4.4 Top ten hereditaments and potential levy payers

The top ten hereditaments across the 5 zones are as follows:

Table 4: TOP TEN HEREDITAMENTS WITH BID LEVY

Business

ASDA STORES LTD

NEWPORT CITY COUNCIL

UNIVERSITY OF SOUTH WALES

BURLINGTON CAP (old Marks & Spencer building)

BRITISH HOME STORES LTD

BOOTS THE CHEMISTS LTD

COURT SERVICE AGENCY

NEWPORT CITY HOMES HOUSING

UK PASSPORT AGENCY WALES

CASTLE LEISURE LTD

5.0 Feasiblity matrix

In order to compare and contrast these five BID areas as objectively as possible, The means used its

own feasibility matrix. The criteria for assessment can be defined as follows:

Sustainability

Is the revenue generated from the levy in proportion to (or in excess of) the revenue required to

service the area in question?

Viability

Can the levy be set at a reasonable level and still generate adequate funds for the BID? At this point it

has not been possible to estimate the cost of running a BID against, say, the square metreage of each

area. In Newport City Centre, a further consideration is whether the area concerned includes

development which is likely to come into use during the first BID term and therefore be an addition

source of BID levy income.

Marketability

What is the likelihood of winning a BID referendum? The costs of marketing the BID and running the

referendum need to be in reasonable proportion to the eventual levy outturn. There needs to be an

adequate number of businesses which will directly benefit from the BID. There also needs to be some

indication that some of the larger businesses, at least, are in favour.

Do ability

Can BID services complement (or ‘join up’ with) existing services in such a way as to make a

significant difference? Typical considerations:

Is there a ‘gateway’ area that can be improved?

Are there streets which can be improved?

Is there a landmark visitor attraction or major commercial estate which can be

better serviced?

Each of these criteria are scored out of 5 (5 being the highest) in the table below.

Option Sustainable Viable Marketable Doable Total Score

Zone1 A good levy outturn and a

clearly defined area. Major

new developments are

taking place here and it is

the focus of major

economic revival efforts.

4

Yes. The area has a good

number and size of

hereditaments to enable a

rate of 1.25% to be

achievable.

4

There is strong support

for the BID concept in this

area and the core issues

are clear and relevant to

all businesses here. A

concerted marketing effort

would be needed to

demonstrate benefits of

the proposed BID,

especially to those

hereditaments with large

RVs.

4

New regeneration and

economic development

efforts could be

complemented by the BID

programme. There are

also a number of gateways

which could be enhanced

and a focus on changing

perceptions and creating a

more welcoming

environment would deliver

clear benefits.

4

16

Zone 2 Low Levy outturn. Small

hereditaments and major

service requirements would

result in revenue being

significantly stretched

2

A levy rate of 1.25% for

all hereditaments over

£5,000 RV would not

generate adequate funds

2

A fragmented area with a

range of, manly small,

businesses. The

exception is Rodney

Parade, which could

benefit from a range of

BID services. The area

as a whole, however, has

limited marketability.

There are number of

residential developments

taking place in the area and

a major attraction in

Rodney Parade, but little in

terms of commercial

development.

3

10

Option Sustainable Viable Marketable Doable Total Score

3

Zone 3 An adequate levy outturn. A

number of commercial and

residential developments

have recently taken place

in the area.

3

A levy rate of 1.25% for all

hereditaments over

£5,000 RV would

generate acceptable

funds for the area.

4

A range of businesses

operate in the area, which

is fairly fragmented.

Would need to show

benefits in terms of

employees and the

environment.

3

A potentially difficult area to

service in terms of layout

and varying quality of sub

areas.

2

12

Zone 4 A lower levy outturn. Mostly

small office occupiers and

the Council’s civic centre.

2

Limited revenue, but

easier area to service

would make it a viable

option.

3

Would need to

demonstrate benefits to

small office based

businesses. .

3

A very different

environment to the rest of

the city centre and would

require a distinct range of

services.

2

10

Zones 5 Low Levy outturn. Small

hereditaments and major

service requirements would

result in revenue being

significantly stretched.

1

Unlikely to be able to

support 1.25% rate unless

this zone forms part of a

wider BID area.

1

A significant area with a

large number of small

businesses.

2

Relatively simple, linear

area, to service. A focus for

regeneration efforts for the

past 15 years.

3

7

6.0 Conclusions and recommendations for phase two

6.1 Suggested themes for BID programme

The results of the survey and ideas from businesses at the symposium event, as reported in Section

2, suggest that the BID programme could be formed of the following four theme areas:

1. Creating a more accessible & attractive city centre

This theme would focus on improving access to the centre and creating a more attractive

environment. It would include services such as:

Working with the local authority to develop an effective parking strategy that would

make access the city centre by car easier and more affordable

Enhancing gateways, such as those at car parks, the bus station, train station and

the lower end of Commercial Street.

Providing a deep clean service to “grot spots” and at other key locations and

attractions.

2. Making the city centre safer & more welcoming

This theme would focus on a number of services to make the city centre experience more

pleasant for those that work, live and visit there. It would include services such as:

A uniformed street ranger scheme, to meet and greet, help prevent crime against

property and anti-social behaviour and pick up on issues to fix in the public realm

A taxi marshal service to create a better nighttime experience

Creating a welcome pack for new businesses and those working in the city centre

Strengthening pub-watch and shop-watch type activity

Support and boost the Newport Business Against Crime Partnersgip

3. Marketing & Events

This theme would focus on changing perceptions, building on the opportunities provided by

new city centre developments and creating more reasons for people to visit the centre.

Services could include:

A programme of events that builds on existing activities, such as the food festival.

A loyalty card to encourage those working and living locally to spend more in the city

centre.

A marketing campaign that focuses on Newport’s distinctive assets and new

developments with a view to changing perceptions.

Actively marketing the centre to potential new businesses

4. Future Newport: Advocacy & Strategy

There is an obvious issue in the city centre with regards to vacant units. New developments

provide a great opportunity, but also bring with them the threat of creating further voids in

traditional shopping areas, such as Commercial Street. During the survey, businesses also

highlighted the need for better communication between the council and the business

community. This theme would look at mechanisms to attract new businesses, support

existing businesses and work with the local council to develop a vision for a sustainable and

thriving trading environment. Initiatives under this theme could include:

Developing a nighttime and evening economy strategy that builds on the research already

carried out in this area and opportunities presented by the leisure aspect of the Friars

Walk development.

Proving support to businesses through mentoring, facilitating access to grants, providing

training opportunities, organising collective purchasing and holding workshops on key

business issues.

Creating an empty shop project that aims to open up the use of empty units for new

activities.

Working with the Newport Food Festival Partnership to create a better food and beverage

offer across the centre all year round.

Looking at opportunities to build on Newport’s sporting facilities/events and bring the

benefits to the city centre

Digital Economy

Complement efforts in turning Newport into a ‘Super-Connected City’ and the focus on

digital innovation of the reNewport, business development task force. Projects might

include working with the proposed Innovation Company and digital businesses in the city

to attract funding and deliver ‘digital high street’ projects.

Cultural Activities

Newport has a rich and distinctive heritage and a vibrant art and music scene. It is also

home to a growing number of groups and organisations that are passionate about the city

and active in providing a growing cultural offer. A BID could work closely with such

organisations, including the local university, and capitalise on the city’s rich cultural assets

to change perceptions and create a vibrant centre that people want to visit.

6.2 Recommendations and next steps

Recommendation 1: In light of all available evidence, it is recommended that the Newport BID

Steering Group moves towards a BID ballot for Newport City Centre.

FOR a BID ballot AGAINST a BID ballot

• There is strength of support within

the town centre, with 74% of

businesses indicating that they

support the BID concept in-

principle

• There is strong leadership from

both the BID Steering Group and

the Chamber of Trade, with good

support from the Local Authority.

• There are a series of physical

developments and regeneration

efforts taking place in the centre,

which a programme of services

could complement – especially in

terms of marketing, safety and

accessibility.

• In the vast majority of cases, the

BID levy remains a relatively

small sum for individual

businesses and should be

portrayed as such.

• There are a number of small

businesses that may not feel they

have the funds available for the

BID levy in the current climate.

They have no influence over

many of their costs – such as

business rates – but they do have

power over the BID levy. (A

threshold may help to address

this.)

• There are a number of national

chain retailers who may not make

their voting decision locally.

• The condition of the city centre

and competition from other

centres such as Cwmbran and

Spytty Park presents a serious

challenge for a BID, especially in

terms of evidencing ways to drive

up footfall and making serious

improvements to trading

conditions.

Recommendation 2: Focus immediate effort on engagement, particularly with the key potential

large levy payers

To build a strong foundation on which a successful BID ballot could be achieved, the next couple of

months should see the development of more and deeper relationships with local businesses and in

particular those who would be the largest potential levy payers.

Recommendation 3: It is recommended that the BID area is composed of Zone 1, the core

centre area

This area covers the main commercial district, including the primary retail area and nighttime

economy district. It is suggested that in the first term, the BID focus on this central area and deliver

targeted services that will make a real difference to the trading environment. Critically this area

includes the new developments of Friars Walk and the Admiral offices. If a first BID term is achieved,

the area could then be extended at a renewal ballot. The other areas considered - Goldtops,

Commercial Road, Docks Way and Clarence Place and Corporation Road – would either require an

extended range of services or would not bring in sufficient funding through the BID levy to justify a

sufficient level of service. Including them in the BID area would spreads resources too thinly and risk

diluting a strong programme of improvements that business would find worthy of supporting at a BID

ballot.

The proposed Business Club will allow businesses, particularly at the top end of Commercial Road, in

Clarence Place or in Docks Way, to participate in some BID services.

Recommendation 4: It is recommended that the levy rate is set at 1.25% of rateable value for

all area except the serviced shopping centres, where a 1% rate should be applied.

The average UK BID levy is 1.4%. Although there is increasing downward pressure on BID levies

(partly due to the success of BIDs in raising funds from other sources), a 1.25% levy is justified in

Newport because of the current condition of the city centre and the services required to make a real

difference.

Kingsway Centre tenants already pay for a number of services that are ‘BID like’ as part of their

service charge and it is likely that future tenants of Friars Walk would pay a similar charge. It is,

therefore, recommended that a lower levy rate be applied in these locations. Whether this rate is 1%

or slightly higher may depend on whether higher cost BID services, such as street rangers, are

provided to centre tenants or not.

Recommendation 5: It is recommended that the rateable value threshold is set at £5,000 and

that there is no ‘cap’.

With respect to the threshold, the £5,000 figure makes sufficient downward impact on the number of

hereditaments, with the least possible impact on the levy outturn.

With respect to the ‘cap’, there are no hereditaments that are significantly higher than any of the

others. In addition, the levy outturn is required if the whole range of services set out above can be

provided. It would therefore be inadvisable to further reduce it.

Recommendation 6: It is recommended that the would-be BID creates a ‘Business Club’-type

mechanism.

This would allow businesses excluded by the £5,000 levy threshold, or by being outside the BID area,

to benefit from some BID services (such as business networking, collective purchasing, promotions

and mentoring) by making an annual voluntary payment. The amount may vary according to the size

of business and/or individual requirements. Similar schemes have worked well for BIDs in other

areas and have crucially helped to maintain a sense of a cohesive business community. The

beneficiaries would include a number of the smaller independent retailers and local attractions for

whom promotion would be important.

Recommendation 7: It is recommended that an intensive BID campaign be delivered that

includes a series of ‘pilot projects’.

From previous experience, we have found that face to face contact with the vast majority of

businesses is a key part of a successful BID campaign. It is recommended that a CRM database be

developed and all businesses within the proposed area offered a meeting at their premises. In

addition, a series of pilot projects should be organised to demonstrate the type of services that a BID

could deliver and the benefits to city centre businesses. A BID HQ has already been opened in the

city centre and this should be used as a base for activities.

A more detailed timetable for the BID campaign can be found in the appendices, but can be

summarised as follows:

Table 14: TIMESCALE FOR BID BALLOT (SUMMARY)

Timescale Stage

BID Start Date 1st April 2015

Billing Period & Company set up March 2015

Ballot Period November 2014

or February 2015

BID Proposal Published/BID event 28th August

Initiation of pilot projects, illustrating

what the BID can achieve

June-November

BID Business Plan signed off End July 2014

BID Campaign begins June 2014

Appendices – see separate document

www.themeans.co.uk

Swyddfa Cymru Unit 3, West End Yard, 21-25 West End, Llanelli, Sir Gâr / Carmarthenshire,

SA15 3DN London Office

81 Southwark Street, London, SE1 0HX Phone / Ffôn: +44 (0)20 7261 1010 Phone / Ffôn: +44 (0)1554 780170

The means: to change places for the better.