the military lending act: compliance challenges and … · •borrower grants creditor right to...

TRANSCRIPT

1 Proprietary & Confidential | BuckleySandler LLP, 2016

Legal Counsel to the Financial Services Industry

The Military Lending Act: Compliance Challenges and Best Practices

Benjamin K. Olson

Sasha Leonhardt

March 23, 2016

2 Proprietary & Confidential | BuckleySandler LLP, 2016

Background and Purpose

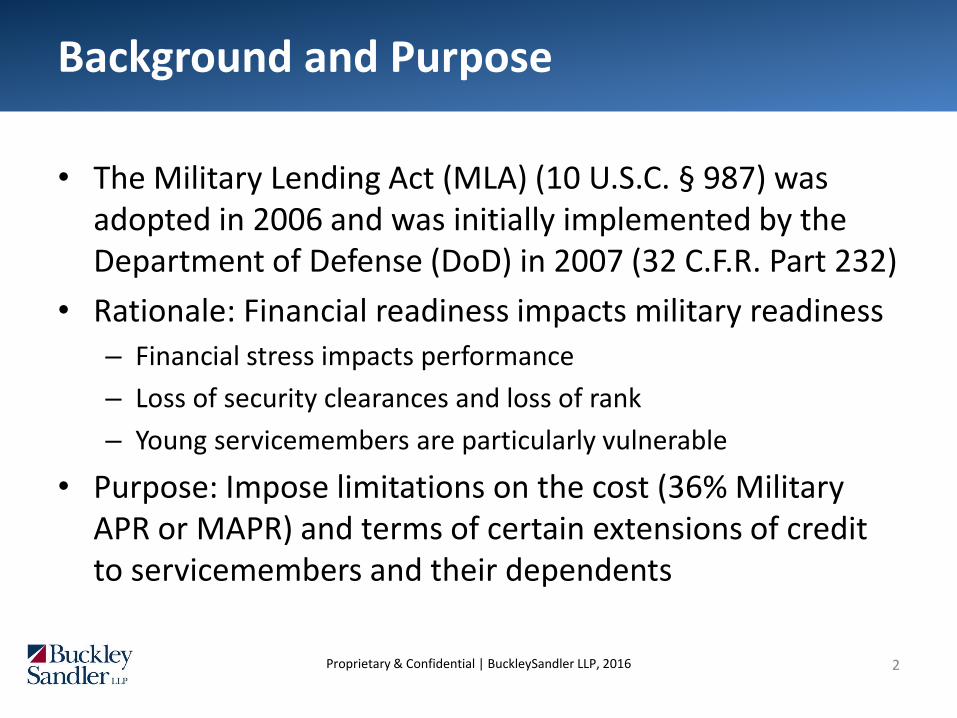

• The Military Lending Act (MLA) (10 U.S.C. § 987) was adopted in 2006 and was initially implemented by the Department of Defense (DoD) in 2007 (32 C.F.R. Part 232)

• Rationale: Financial readiness impacts military readiness

– Financial stress impacts performance

– Loss of security clearances and loss of rank

– Young servicemembers are particularly vulnerable

• Purpose: Impose limitations on the cost (36% Military APR or MAPR) and terms of certain extensions of credit to servicemembers and their dependents

3 Proprietary & Confidential | BuckleySandler LLP, 2016

Original MLA Rule (2007)

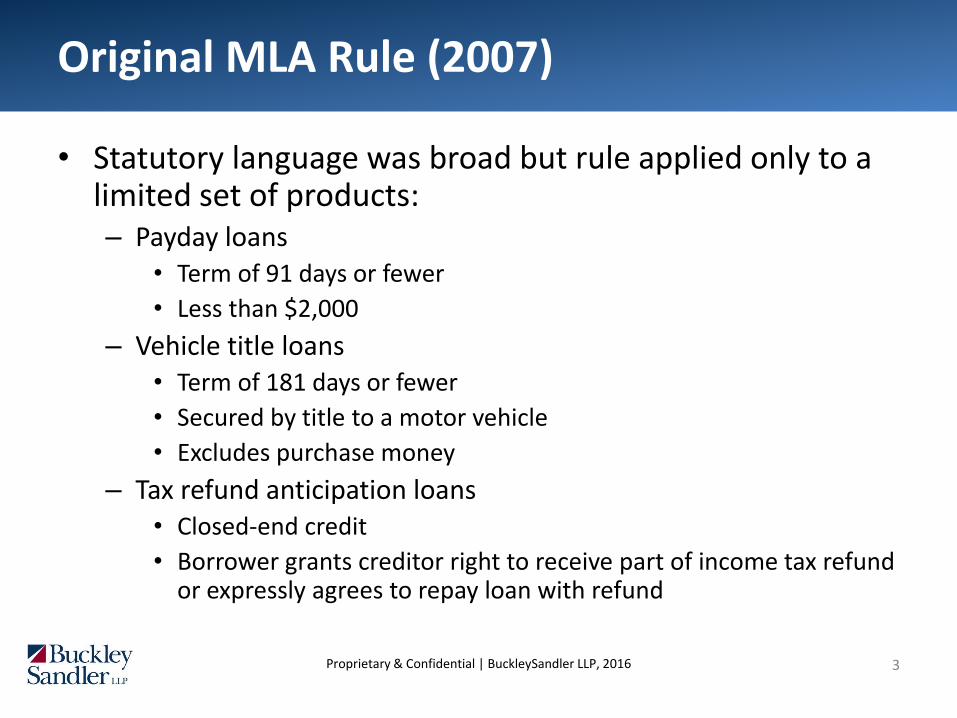

• Statutory language was broad but rule applied only to a limited set of products: – Payday loans

• Term of 91 days or fewer

• Less than $2,000

– Vehicle title loans • Term of 181 days or fewer

• Secured by title to a motor vehicle

• Excludes purchase money

– Tax refund anticipation loans • Closed-end credit

• Borrower grants creditor right to receive part of income tax refund or expressly agrees to repay loan with refund

4 Proprietary & Confidential | BuckleySandler LLP, 2016

Recent DoD Rulemaking

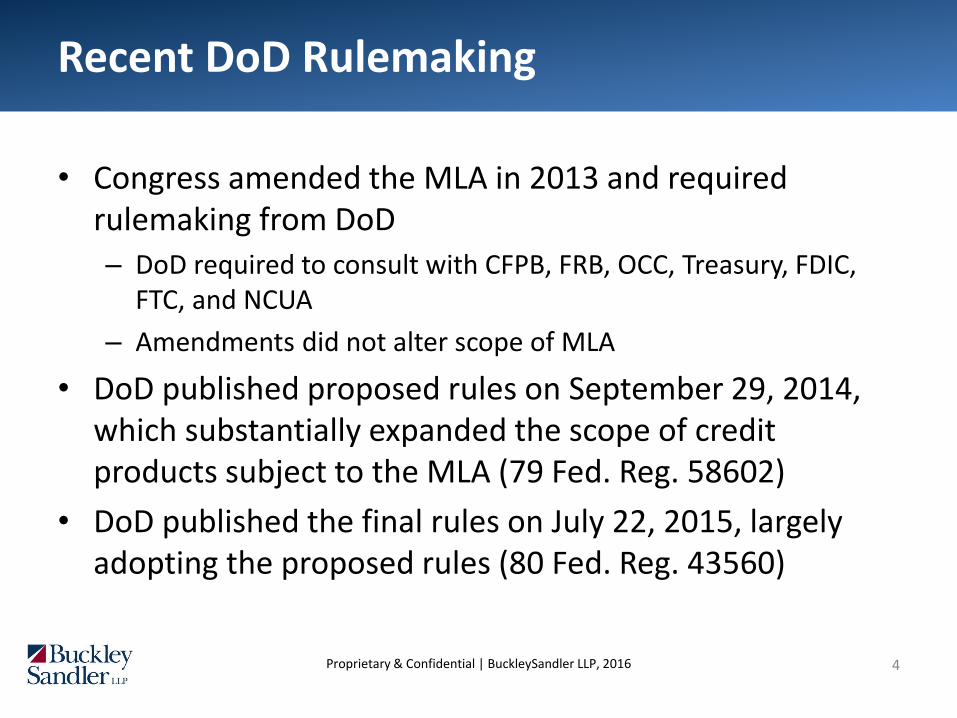

• Congress amended the MLA in 2013 and required rulemaking from DoD

– DoD required to consult with CFPB, FRB, OCC, Treasury, FDIC, FTC, and NCUA

– Amendments did not alter scope of MLA

• DoD published proposed rules on September 29, 2014, which substantially expanded the scope of credit products subject to the MLA (79 Fed. Reg. 58602)

• DoD published the final rules on July 22, 2015, largely adopting the proposed rules (80 Fed. Reg. 43560)

5 Proprietary & Confidential | BuckleySandler LLP, 2016

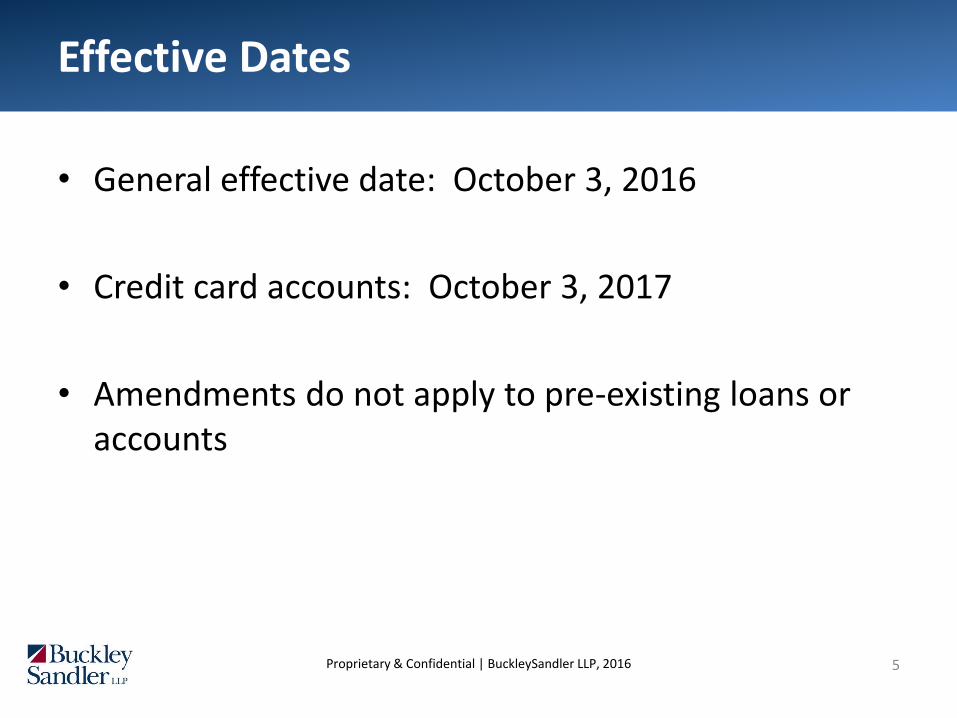

Effective Dates

• General effective date: October 3, 2016

• Credit card accounts: October 3, 2017

• Amendments do not apply to pre-existing loans or accounts

6 Proprietary & Confidential | BuckleySandler LLP, 2016

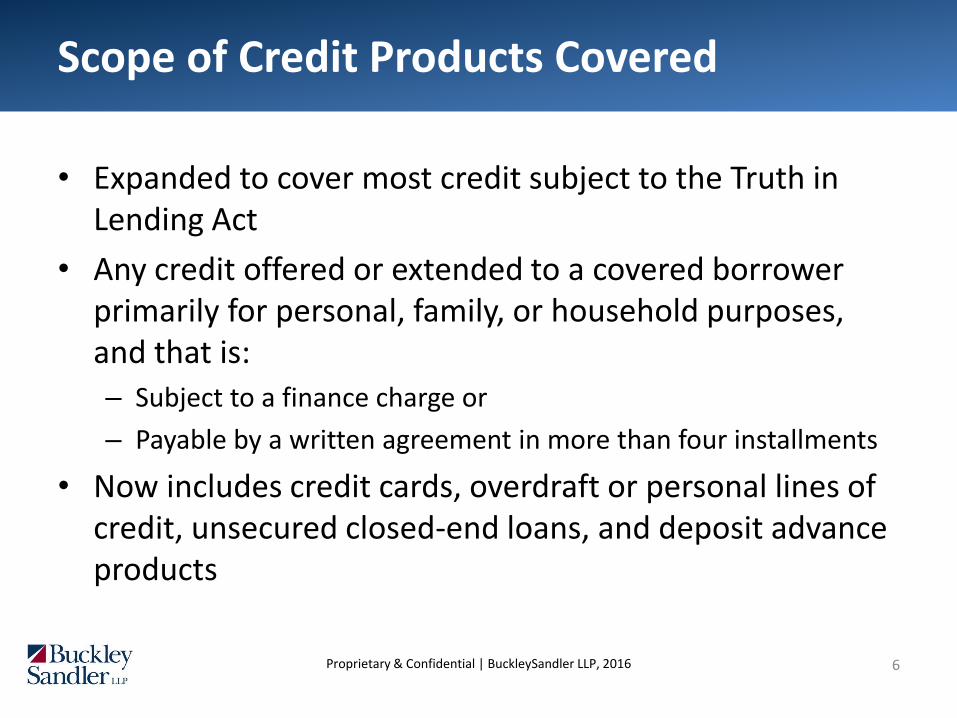

Scope of Credit Products Covered

• Expanded to cover most credit subject to the Truth in Lending Act

• Any credit offered or extended to a covered borrower primarily for personal, family, or household purposes, and that is:

– Subject to a finance charge or

– Payable by a written agreement in more than four installments

• Now includes credit cards, overdraft or personal lines of credit, unsecured closed-end loans, and deposit advance products

7 Proprietary & Confidential | BuckleySandler LLP, 2016

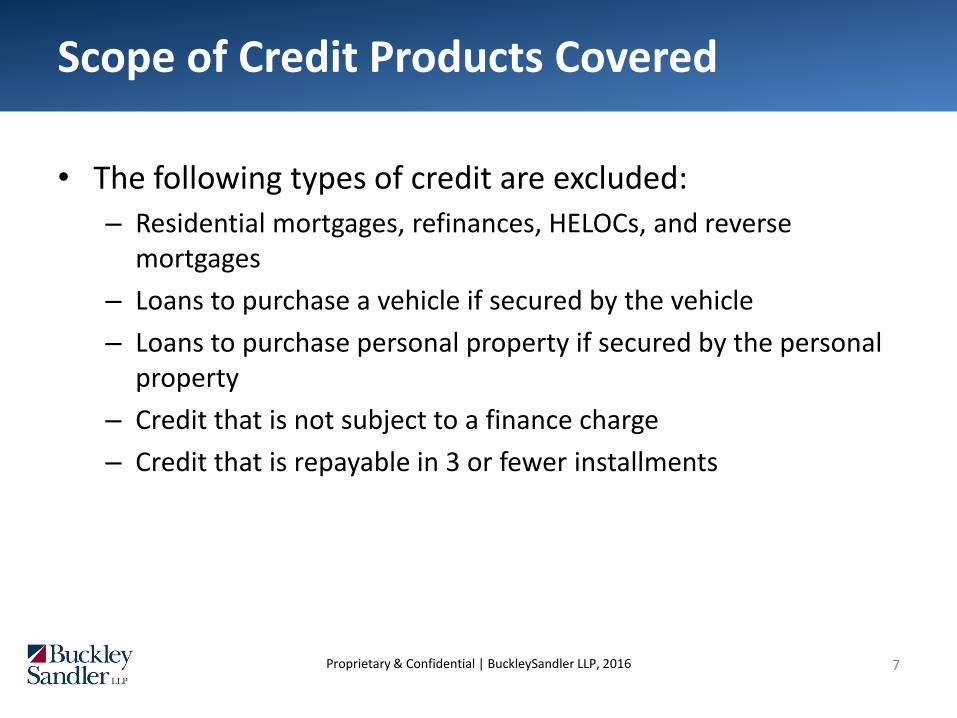

Scope of Credit Products Covered

• The following types of credit are excluded:

– Residential mortgages, refinances, HELOCs, and reverse mortgages

– Loans to purchase a vehicle if secured by the vehicle

– Loans to purchase personal property if secured by the personal property

– Credit that is not subject to a finance charge

– Credit that is repayable in 3 or fewer installments

8 Proprietary & Confidential | BuckleySandler LLP, 2016

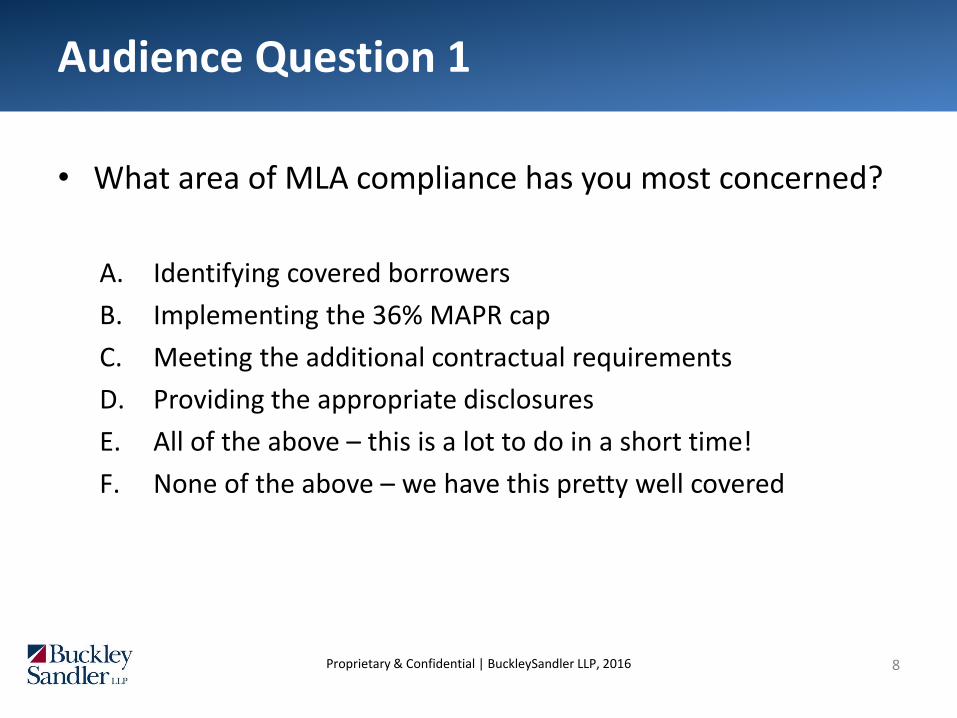

Audience Question 1

• What area of MLA compliance has you most concerned?

A. Identifying covered borrowers

B. Implementing the 36% MAPR cap

C. Meeting the additional contractual requirements

D. Providing the appropriate disclosures

E. All of the above – this is a lot to do in a short time!

F. None of the above – we have this pretty well covered

9 Proprietary & Confidential | BuckleySandler LLP, 2016

Who Counts as a Covered Borrower?

• Covered Borrowers: Active duty servicemembers and their dependents

• Dependents include, but are not limited to: – Spouse

– A child under 21 (or 23 in certain circumstances)

– A parent or parent-in-law who is dependent on the covered member for over ½ of their support and residing in the covered member’s household

– Certain persons over whom the covered member has legal custody

• The protections cease when the consumer is no longer a covered borrower

10 Proprietary & Confidential | BuckleySandler LLP, 2016

How Do You Know Who is a Covered Borrower?

• 2007 rule allowed credit applicants to self-certify whether or not they are covered borrower – Limited safe harbor if borrower certifies not on active duty – Only applies if creditor does not otherwise determine that borrower is

eligible for MLA protection

• 2013 rule allows for self-certification, but removes any safe harbor protection from this

• Instead, DoD determined that a database-focused safe harbor would be better for both borrowers and creditors – Provides creditors “a degree of certainty” – Dynamic between creditors and borrowers has led to misuses of

borrower self-certification statement – Safe harbor relieves servicemembers and dependents from making

any statement regarding covered borrower status

11 Proprietary & Confidential | BuckleySandler LLP, 2016

How Do You Know Who is a Covered Borrower?

• Revised regulations provide a safe harbor if the creditor assesses the consumer’s status using one of the following methods:

– Information obtained directly or indirectly from the DoD’s DMDC database

– Direct connection to the DMDC database

– Verifying the status using a “statement, code, or similar indicator” contained in a consumer report obtained from a nationwide consumer reporting agency

• Creditor must retain results from safe harbor check in its files

12 Proprietary & Confidential | BuckleySandler LLP, 2016

How Do You Know Who is a Covered Borrower?

• The creditor only needs to undertake the covered borrower check once

• However, the check must occur at the time: – The consumer initiates the transaction (or within 30 days

before)

– The consumer applies to establish the account (or within 30 days before)

– The creditor develops or processes, with respect to a consumer, a firm offer of credit that (among the specific criteria used by the creditor for the offer) includes the status of the consumer as a covered borrower, provided the consumer responds within 60 days after the creditor makes the offer

13 Proprietary & Confidential | BuckleySandler LLP, 2016

How Do You Know Who is a Covered Borrower?

• Safe harbor output is “legally conclusive”

• Creditors are prohibited from using the MLA database for any sort of “lookback” review

– Prevents additional traffic on DMDC systems

– Prevents any post-hoc challenge of MLA eligibility

• DoD considered—and affirmatively dismissed—any actual knowledge exemption from the safe harbor

14 Proprietary & Confidential | BuckleySandler LLP, 2016

Audience Question 2

• What method are you planning to use to identify covered borrowers?

A. DMDC’s MLA website database

B. DMDC’s MLA direct connection database

C. Credit bureau reports

D. Borrower self-identification

E. Unsure at this time

15 Proprietary & Confidential | BuckleySandler LLP, 2016

Substantive Protections: MAPR

• MAPR: Military Annual Percentage Rate

– The MAPR cannot exceed 36% on a closed-end loan or in any billing cycle for open-end credit

– Creditors must develop systems for calculating the MAPR, which is calculated consistent with the APR in Regulation Z (though for open-end transactions, the MAPR is calculated like the “effective APR”)

– The MAPR includes finance charges, credit insurance premiums, debt suspension fees, ancillary product fees, and certain application and participation fees, among other things (but excludes late fees and other default charges)

16 Proprietary & Confidential | BuckleySandler LLP, 2016

Substantive Protections: MAPR

• MAPR Compliance Challenges

– “Ancillary products” undefined

– For open-end credit, ancillary products or transaction fees can quickly cause MAPR to exceed 36%

– Because MAPR ≠ APR, calculation must be done through new method that does not parallel Regulation Z—systems issues

– No balance during a billing cycle no fee or charge except participation fee for open-ended credit less than $100 per year

17 Proprietary & Confidential | BuckleySandler LLP, 2016

Substantive Protections: MAPR

• Special MAPR Rules for Credit Cards:

– For certain credit card accounts, the MAPR excludes “bona fide” fees, provided they are “reasonable for that type of fee”

– To be reasonable, the fee must be compared to fees “typically imposed by other creditors for the same or a substantially similar product or service”

– Higher fee than other creditors may be reasonable “depending on other factors relating to the credit card account”

– Consider credit limit in effect, services/perks available as part of the card account, or other factors

18 Proprietary & Confidential | BuckleySandler LLP, 2016

Substantive Protections: MAPR

• Special MAPR Rules for Credit Cards:

– Issuers cannot exclude as a bona fide fee from Card MAPR the following fees: (i) credit insurance premiums, (ii) fees for debt cancellation or debt suspension, or (iii) fees for ancillary products

– Safe Harbor: A “bona fide” fee is reasonable if it is less than or equal to the average amount charged by 5 or more issuers with $3B or more in outstanding loans over the preceding 3 years

19 Proprietary & Confidential | BuckleySandler LLP, 2016

Additional Substantive Protections

• For certain non-depository creditors, roll-overs and vehicle title loans are prohibited

• Covered borrower cannot be required to waive legal recourse under any state or federal law (including the Servicemembers Civil Relief Act)

• Covered borrower cannot be required to submit to arbitration

20 Proprietary & Confidential | BuckleySandler LLP, 2016

Additional Substantive Protections

• Creditor may not impose “onerous” or “unreasonable” notice requirements

• The covered borrower cannot be required to establish an allotment to repay the obligation

• Prepayment penalties and restrictions on prepayment are prohibited

21 Proprietary & Confidential | BuckleySandler LLP, 2016

Additional Substantive Protections

• Creditor violates MLA rule if it “uses a check or other method of access to a deposit, savings, or other financial account maintained by the covered borrower,” except that the credit may, unless otherwise prohibited by law:

– Require an electronic fund transfer to repay a consumer credit transaction

– Require direct deposit of the consumer’s salary as a condition eligibility for consumer credit

– Take a security interest in funds deposited after the extension of credit in an account established in connection with the consumer credit transaction

22 Proprietary & Confidential | BuckleySandler LLP, 2016

Audience Question 3

• How are you planning to ensure that covered borrowers receive appropriate contracts/account agreements?

A. Creating different contracts for covered borrowers and non-covered borrowers

B. Having a check-box approach to identify whether an individual is a covered borrower

C. Providing the MLA’s protections to all borrowers, regardless of covered status

D. Unsure at this time

23 Proprietary & Confidential | BuckleySandler LLP, 2016

Disclosure Requirements

• Creditor must provide certain disclosures “before or at the time the borrower becomes obligated or establishes an account” 1. Statement of the MAPR

2. Applicable Regulation Z disclosures

3. A clear description of the payment obligation

• No exception for telephone transactions

• MAPR statement and description of payment obligation must be provided orally and in writing in a form the consumer may keep

24 Proprietary & Confidential | BuckleySandler LLP, 2016

Oral Disclosures

• Oral disclosures may be provided to the covered borrower orally:

– In person; or

– Through a toll-free telephone number included on the application form or in a separate written disclosure

25 Proprietary & Confidential | BuckleySandler LLP, 2016

MAPR Statement

• Creditor does not need to disclose the MAPR itself

• Creditor does not need to describe the total dollar amount of all charges in the MAPR

• Model statement provided, which may be included in the agreement:

Federal law provides important protections to members of the Armed Forces and their dependents relating to extensions of consumer credit. In general, the cost of consumer credit to a member of the Armed Forces and his or her dependent may not exceed an annual percentage rate of 36 percent. This rate must include, as applicable to the credit transaction or account: The costs associated with credit insurance premiums; fees for ancillary products sold in connection with the credit transaction; any application fee charged (other than certain application fees for specified credit transactions or accounts); and any participation fee charged (other than certain participation fees for a credit card account).

26 Proprietary & Confidential | BuckleySandler LLP, 2016

Disclosure Requirements

• Creditor must also provide a “clear description of the payment obligation of the covered borrower”

• Closed-end credit: Regulation Z payment schedule

– For example: “As estimated, your loan has [59] regularly scheduled monthly payments of $[300] starting [April 15, 2016] and a final payment of $[340] due on [March 15, 2021].”

• Open-end credit: Regulation Z account-opening disclosure

27 Proprietary & Confidential | BuckleySandler LLP, 2016

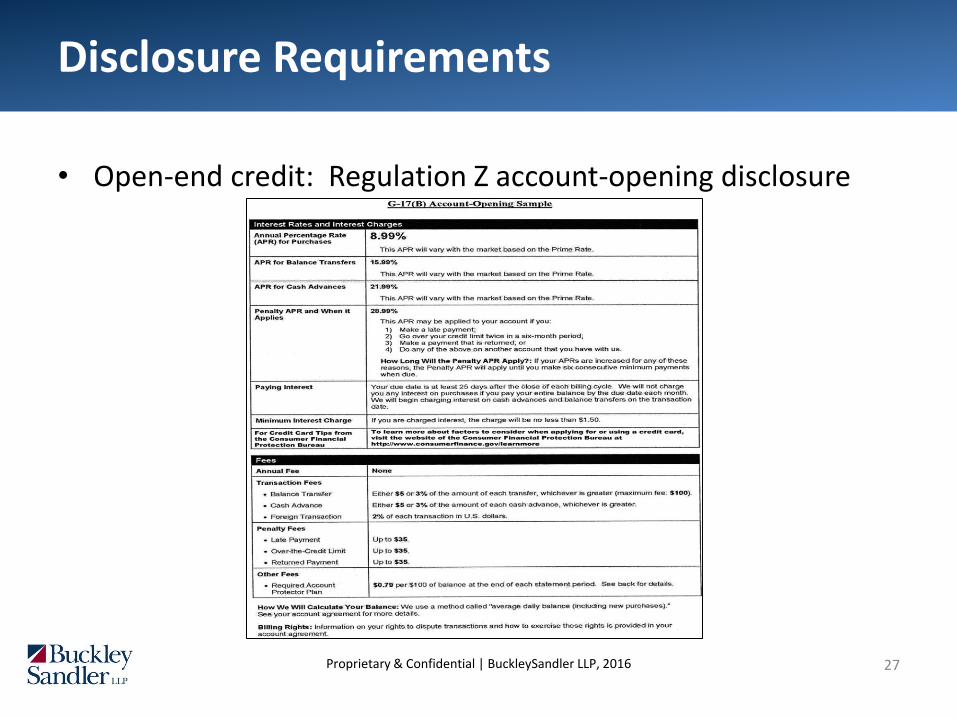

Disclosure Requirements

• Open-end credit: Regulation Z account-opening disclosure

28 Proprietary & Confidential | BuckleySandler LLP, 2016

Penalties and Enforcement

• Significant potential penalties

– Fine or one year in prison, or both, for knowing violations

– Credit agreement void at inception

– Civil liability for the greater of actual damages or $500

• Plus punitive damages (no cap)

• Plus costs and attorney’s fees

– Equitable relief

29 Proprietary & Confidential | BuckleySandler LLP, 2016

Contract Voidance

“Any credit agreement, promissory note, or other contract with a covered borrower that fails to comply with 10 U.S.C. 987 as implemented by this part or which contains one or more provisions prohibited under 10 U.S.C. 987 as implemented by this part is void from the inception of the contract.”

• Compliance Questions:

– Inclusion of arbitration provision that applies only to non-covered borrowers

– Inclusion of erroneous Regulation Z disclosures or MAPR statement in agreement

– Late delivery of agreement containing disclosures

30 Proprietary & Confidential | BuckleySandler LLP, 2016

Penalties and Enforcement

• Enforcement risk

– Significant attention on new MLA Regulations

– CFPB has clear interest in MLA compliance

• CFPB’s own comment letter on MLA Regulations

• Holly Petraeus’s blog posts on the CFPB website

• CFPB examination guidance on Military Lending Act (September 2013)

• CFPB enforcement action against Cash America for extending payday loans to servicemembers and their families in violation of the act (November 2013)

31 Proprietary & Confidential | BuckleySandler LLP, 2016

Penalties and Enforcement

• Potential defenses – No civil liability if creditor shows by a preponderance of evidence that

the violation was a bona fide error • Clerical error • Calculation error • Computer malfunction/programming error • Printing error

– Does not include error of legal judgment

• Statute of limitations is earlier of – Two years after date plaintiff discovers the violation, or – Five years after violation occurs

• If a plaintiff’s action against a creditor is brought in bad faith, the plaintiff is liable for defendant’s reasonable attorney’s fees

32 Proprietary & Confidential | BuckleySandler LLP, 2016

Additional Compliance Challenges

• Vendor management

• Point-of-sale credit contracts

• Employee training

• Underwriting

• Covered borrower communication

33 Proprietary & Confidential | BuckleySandler LLP, 2016

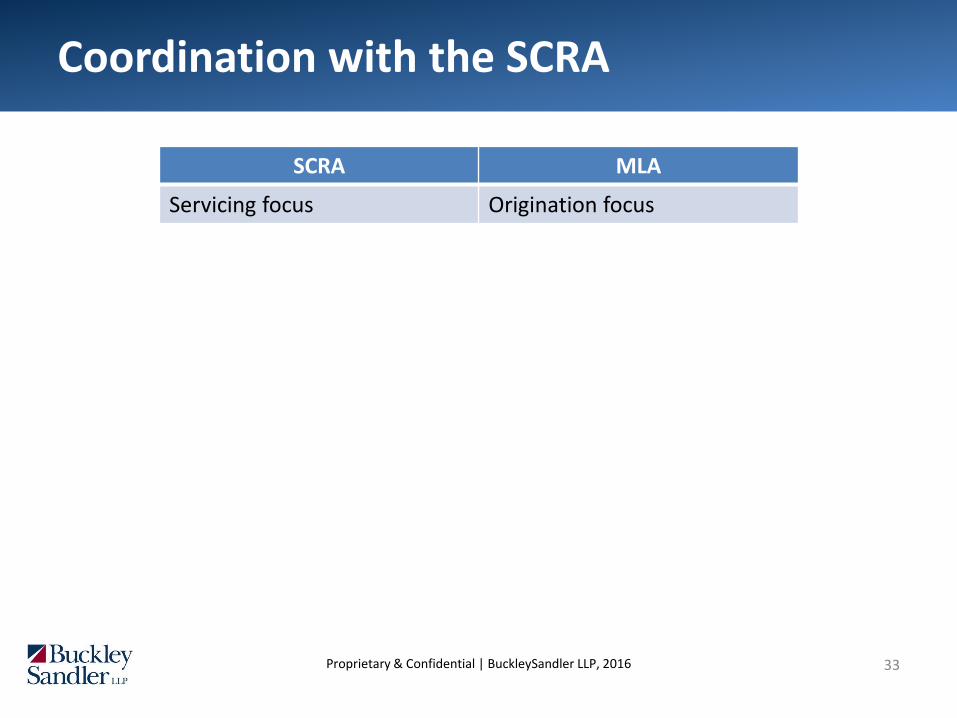

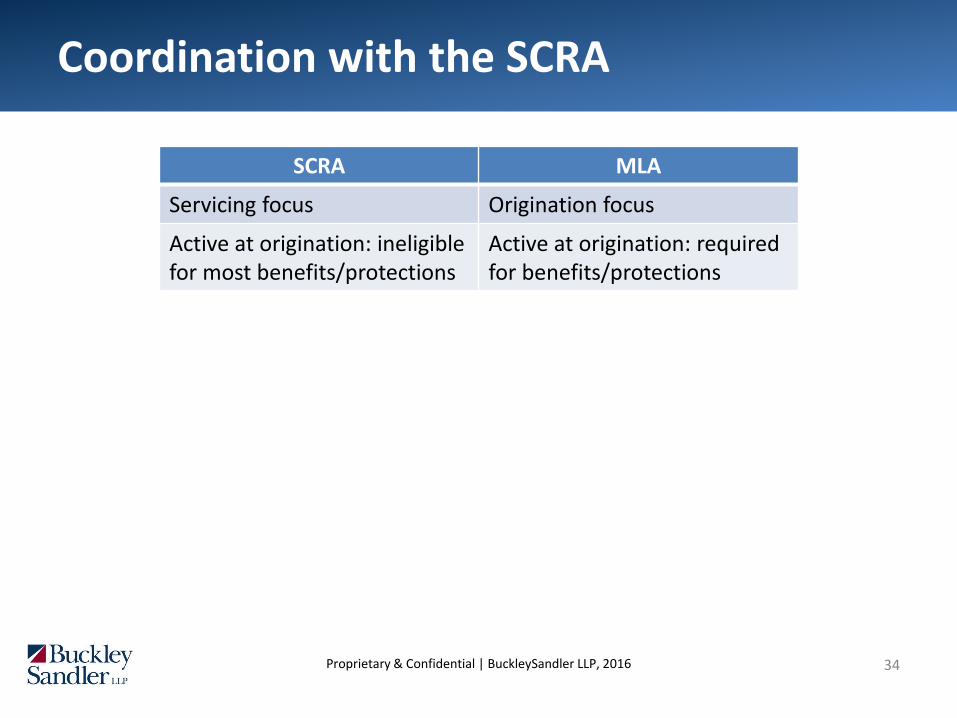

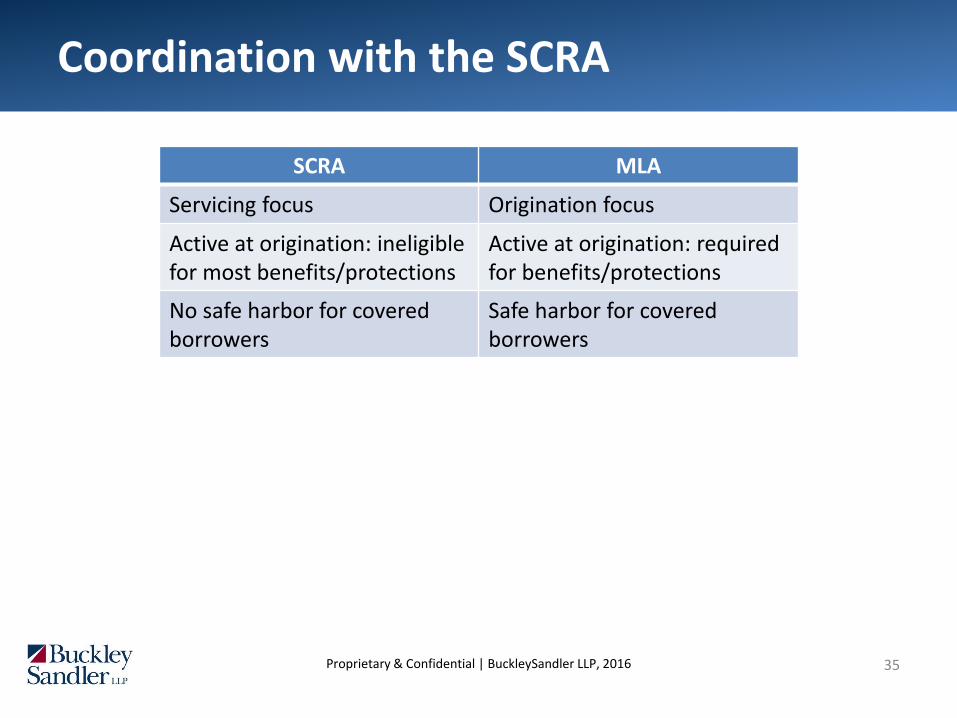

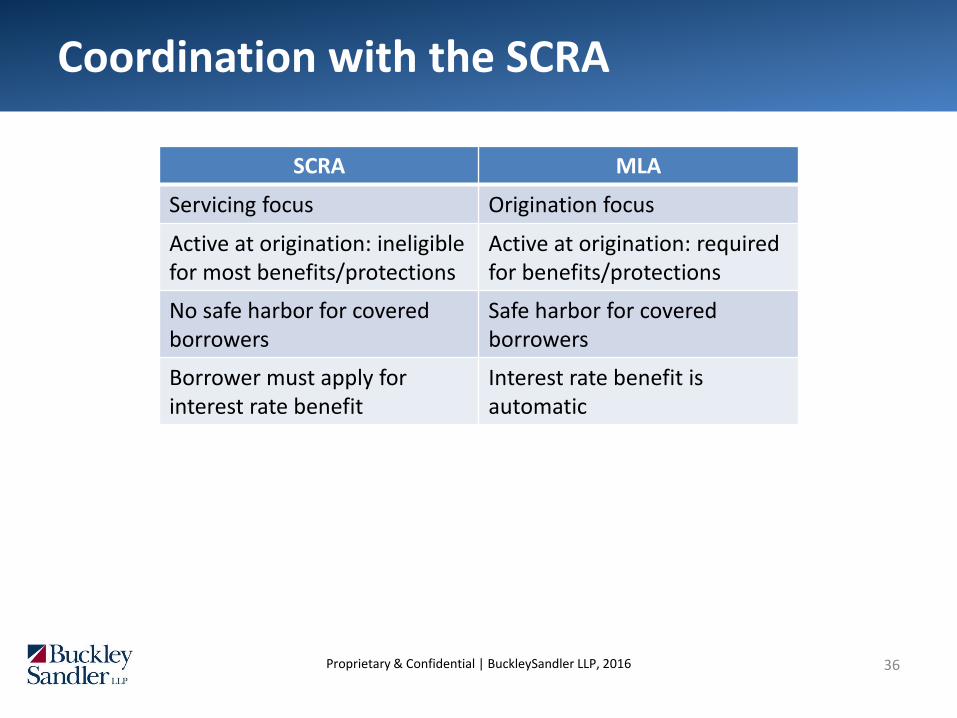

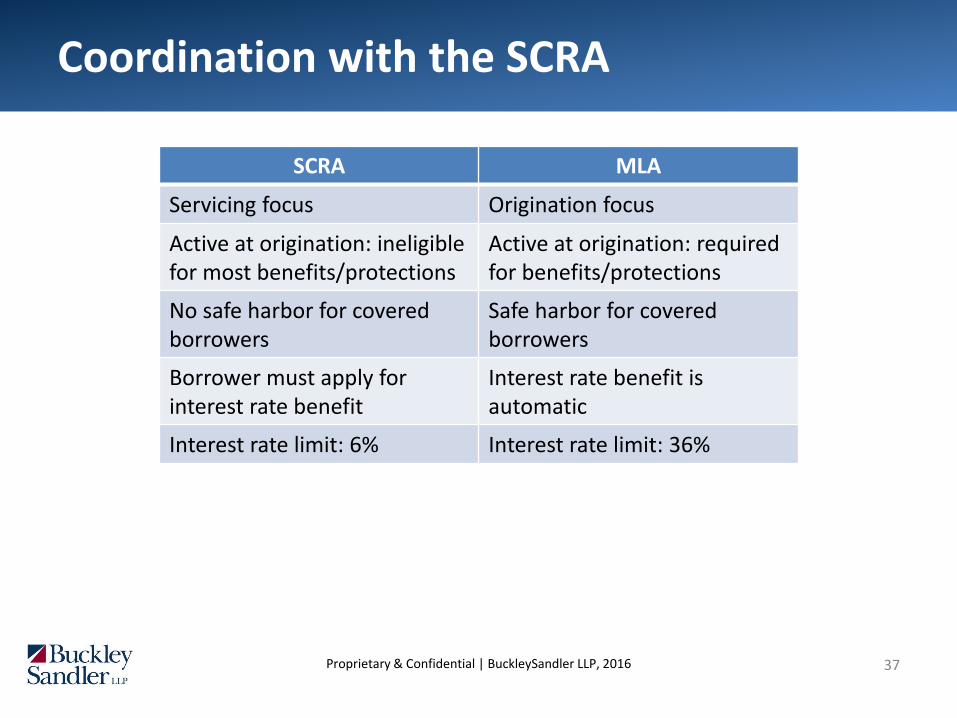

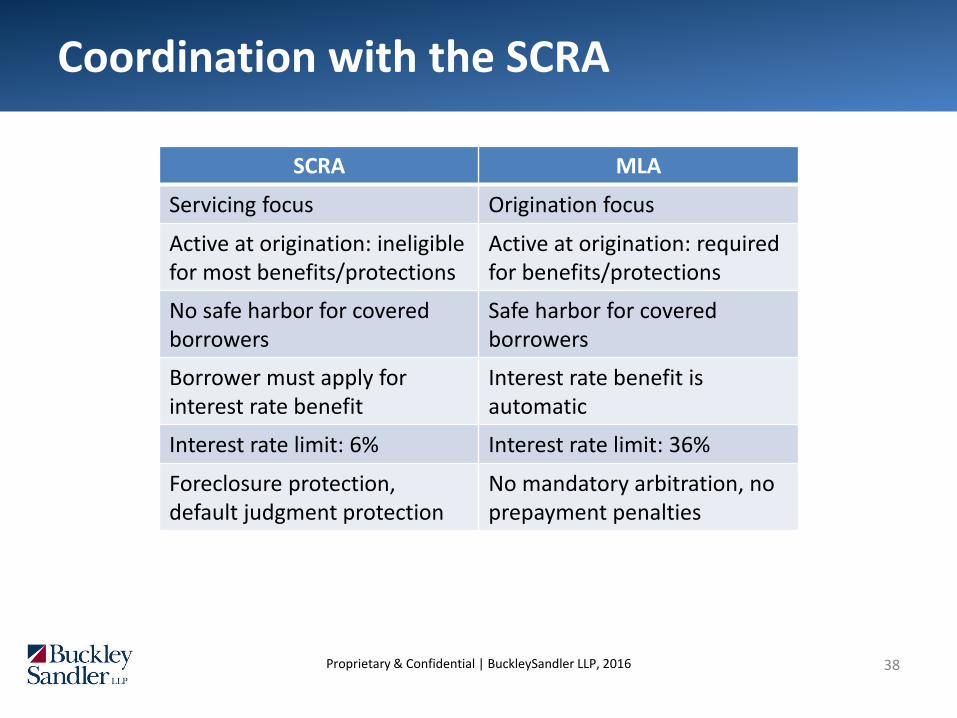

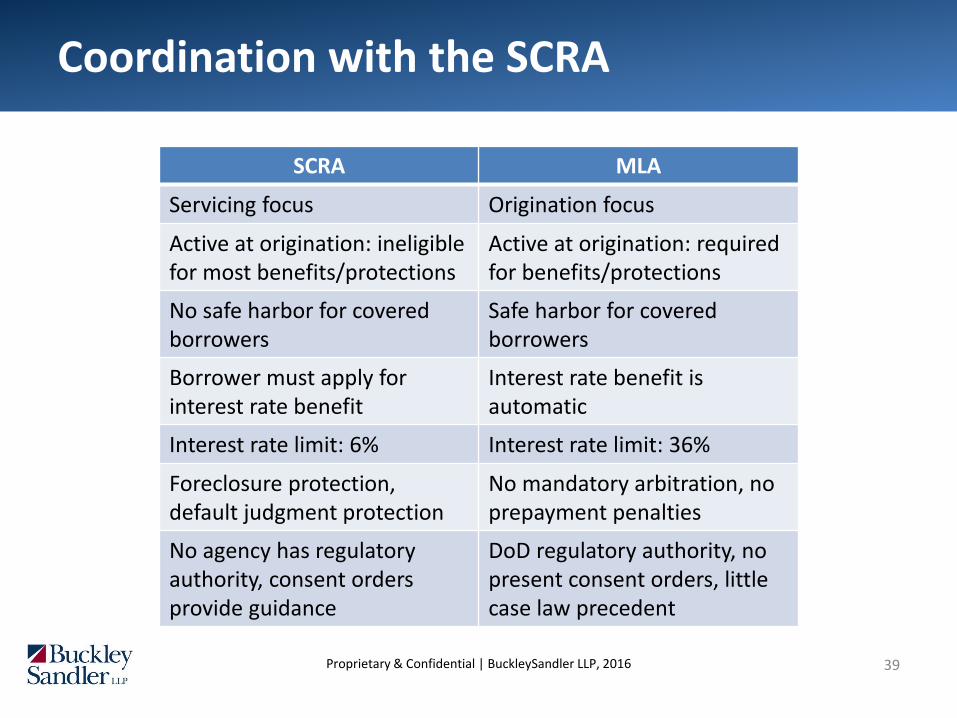

Coordination with the SCRA

SCRA MLA

Servicing focus Origination focus

34 Proprietary & Confidential | BuckleySandler LLP, 2016

Coordination with the SCRA

SCRA MLA

Servicing focus Origination focus

Active at origination: ineligible for most benefits/protections

Active at origination: required for benefits/protections

35 Proprietary & Confidential | BuckleySandler LLP, 2016

Coordination with the SCRA

SCRA MLA

Servicing focus Origination focus

Active at origination: ineligible for most benefits/protections

Active at origination: required for benefits/protections

No safe harbor for covered borrowers

Safe harbor for covered borrowers

36 Proprietary & Confidential | BuckleySandler LLP, 2016

Coordination with the SCRA

SCRA MLA

Servicing focus Origination focus

Active at origination: ineligible for most benefits/protections

Active at origination: required for benefits/protections

No safe harbor for covered borrowers

Safe harbor for covered borrowers

Borrower must apply for interest rate benefit

Interest rate benefit is automatic

37 Proprietary & Confidential | BuckleySandler LLP, 2016

Coordination with the SCRA

SCRA MLA

Servicing focus Origination focus

Active at origination: ineligible for most benefits/protections

Active at origination: required for benefits/protections

No safe harbor for covered borrowers

Safe harbor for covered borrowers

Borrower must apply for interest rate benefit

Interest rate benefit is automatic

Interest rate limit: 6% Interest rate limit: 36%

38 Proprietary & Confidential | BuckleySandler LLP, 2016

Coordination with the SCRA

SCRA MLA

Servicing focus Origination focus

Active at origination: ineligible for most benefits/protections

Active at origination: required for benefits/protections

No safe harbor for covered borrowers

Safe harbor for covered borrowers

Borrower must apply for interest rate benefit

Interest rate benefit is automatic

Interest rate limit: 6% Interest rate limit: 36%

Foreclosure protection, default judgment protection

No mandatory arbitration, no prepayment penalties

39 Proprietary & Confidential | BuckleySandler LLP, 2016

Coordination with the SCRA

SCRA MLA

Servicing focus Origination focus

Active at origination: ineligible for most benefits/protections

Active at origination: required for benefits/protections

No safe harbor for covered borrowers

Safe harbor for covered borrowers

Borrower must apply for interest rate benefit

Interest rate benefit is automatic

Interest rate limit: 6% Interest rate limit: 36%

Foreclosure protection, default judgment protection

No mandatory arbitration, no prepayment penalties

No agency has regulatory authority, consent orders provide guidance

DoD regulatory authority, no present consent orders, little case law precedent

40 Proprietary & Confidential | BuckleySandler LLP, 2016

Questions?

Benjamin K. Olson Partner

202.349.7924 [email protected]

Sasha Leonhardt Associate

202.349.7971 [email protected]

buckleysandler.com | infobytesblog.com