the most successful regional aircraft programs in history

TRANSCRIPT

The most successfulRegional Aircraft programs in history.

Regional Aircraft … The Way Forward

Presented by Mike LewisSeptember 26, 2006

2

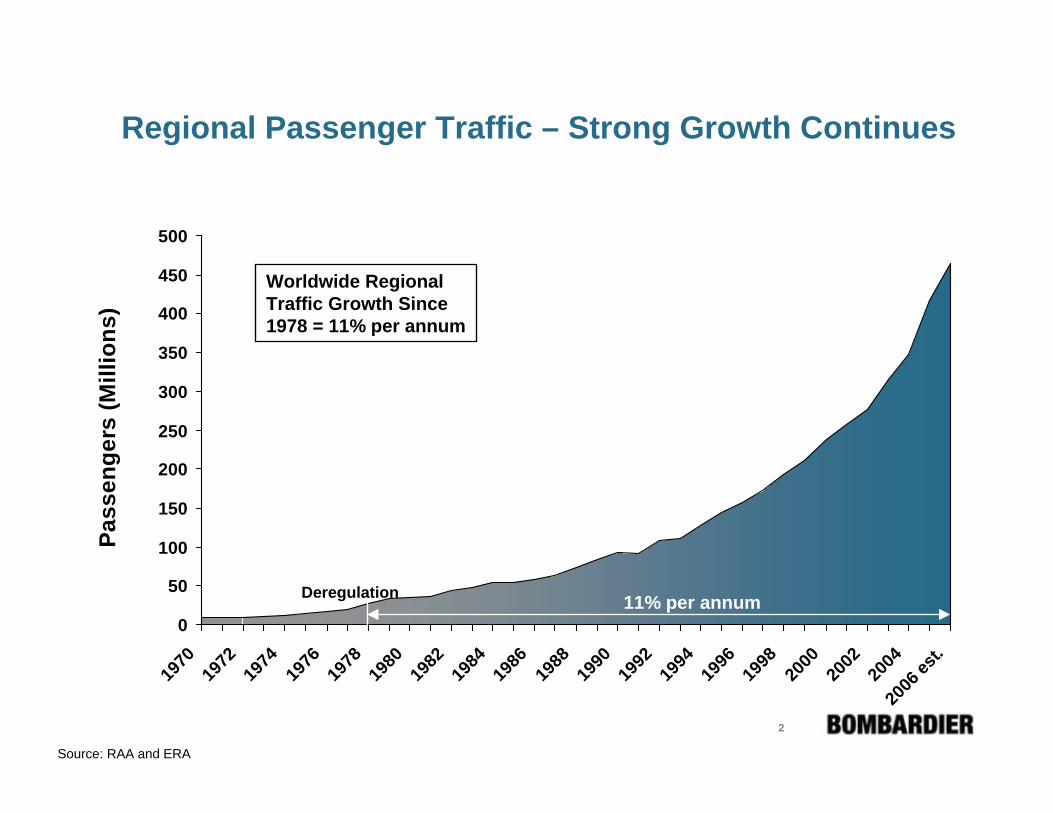

Regional Passenger Traffic – Strong Growth Continues

0

50

100

150

200

250

300

350

400

450

500

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

est.

Pass

enge

rs (M

illio

ns)

11% per annum

Worldwide Regional Traffic Growth Since 1978 = 11% per annum

Deregulation

Source: RAA and ERA

3

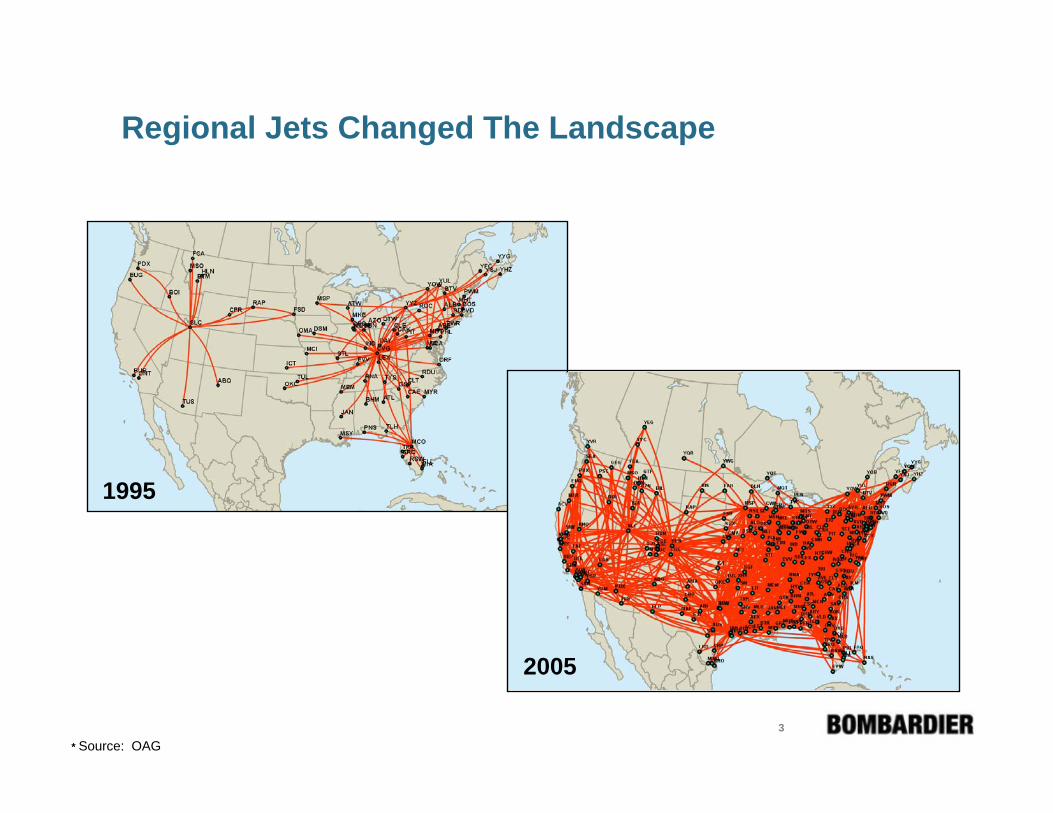

1995

* Source: OAG

2005

Regional Jets Changed The Landscape

4

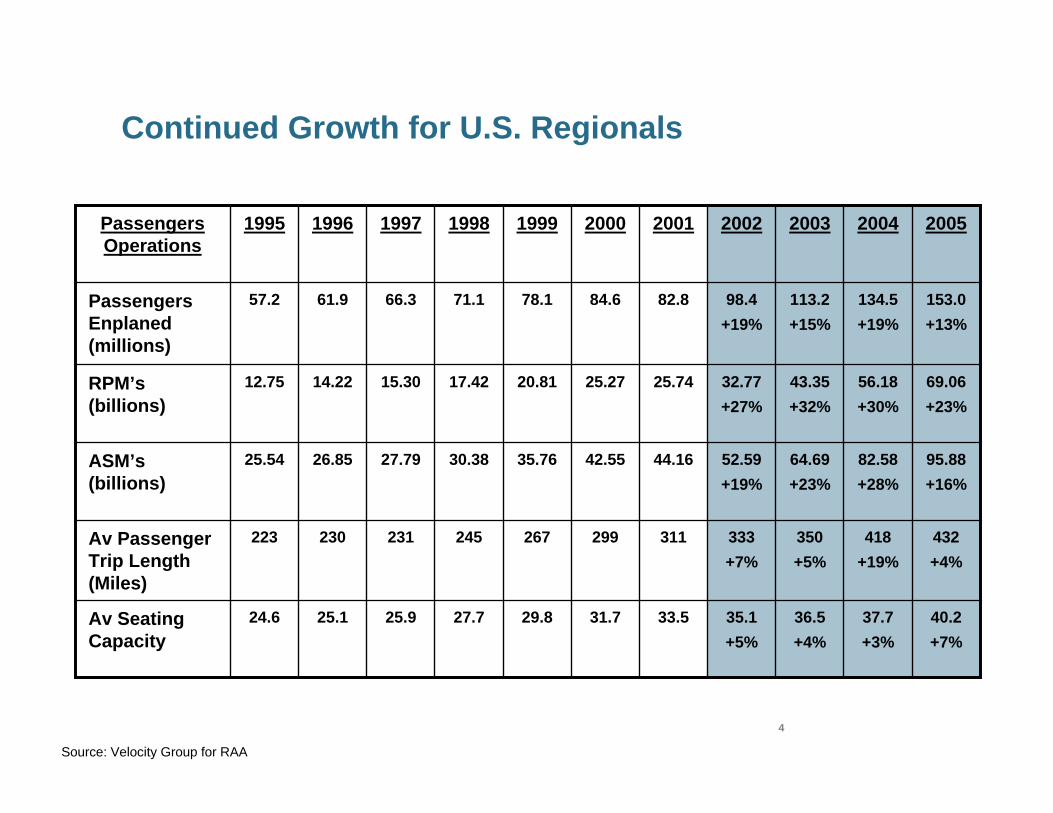

Continued Growth for U.S. Regionals

40.2+7%

432+4%

95.88+16%

69.06+23%

153.0+13%

2005

35.1+5%

333+7%

52.59+19%

32.77+27%

98.4+19%

2002

36.5+4%

350+5%

64.69+23%

43.35+32%

113.2+15%

2003

37.7+3%

33.531.729.827.725.925.124.6Av Seating Capacity

418+19%

311299267245231230223Av Passenger Trip Length (Miles)

25.54

12.75

57.2

1995

26.85

14.22

61.9

1996

27.79

15.30

66.3

1997

30.38

17.42

71.1

1998

82.58+28%

44.1642.5535.76ASM’s(billions)

56.18+30%

25.7425.2720.81RPM’s(billions)

134.5+19%

82.884.678.1Passengers Enplaned (millions)

2004200120001999Passengers Operations

Source: Velocity Group for RAA

5

50-seat Regional Jets are an integral part of airlines’ networks

Source: OAG

0

500

1,000

1,500

2,000

2,500

3,000

3,500

20 30 50 70 90 110

130

150

170

190

210

230

250

270

290

310

330

350

370

390

410

430

450+

20002005

Average Seats per Departure

No. of Markets

Worldwide Scheduled Non-stop Markets by Average Seats Offered

• No sign of significant fleet withdrawal

• Short term surplus aircraft are expected to go back into the system

6

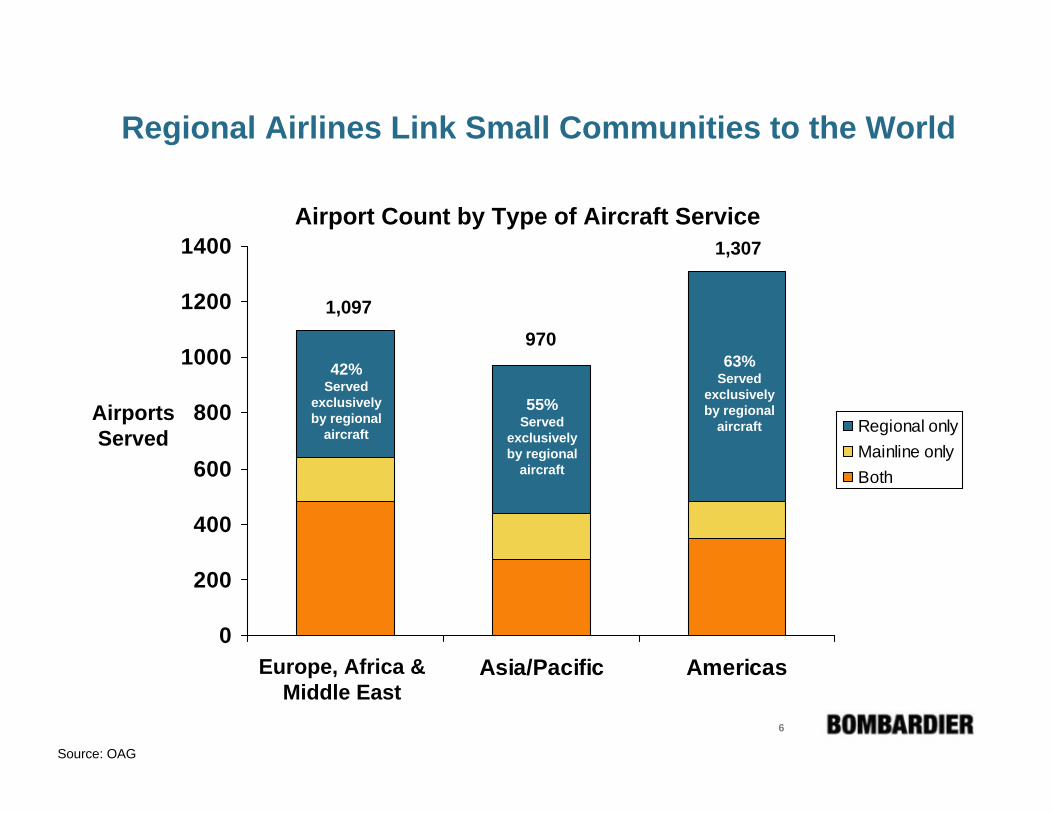

Regional Airlines Link Small Communities to the World

0

200

400

600

800

1000

1200

1400

Eurpoe, Africa &Middle East

Asia/Pacific Americas

Regional onlyMainline onlyBoth

1,097

1,307

Source: OAG

Airports Served

Airport Count by Type of Aircraft Service

97042%

Served exclusively by regional

aircraft

55%Served

exclusively by regional

aircraft

63%Served

exclusively by regional

aircraft

Europe, Africa &Middle East

7

Regional Airlines and Low Cost Carriers Are Part of the Same Market Dynamic

91%83% 84%

76% 71% 66% 61% 59% 57%

7% 9%11% 13% 16%

19% 20% 21%

3% 10% 7% 14% 16% 18% 20% 21% 22%5%

1980 1985 1990 1995 2000 2002 2003 2004 2005

Network Regionals Low Cost

Historical Distribution of U.S. Domestic Passenger Enplanements

Source: Velocity Group for RAA

8

Airline Challenges are Intensifying

4.0¢

8.3¢

1978 1983 1988 1993 1998 2003

55¢

163¢

1995 1997 1999 2001 2003 2005

Source: ATA, cents per US gallon US carrier average yield in 1978 cents

Increasing cost of jet fuel

Decreasing passenger yield

9.3¢

12.1¢

8.6¢ 8.2¢

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Network carrier

Low cost carrier

US DOT Form 41

Diverging CASM gap

9

6¢

8¢

10¢

12¢

14¢

16¢

$0 $5 $10 $15 $20 $25

As Major Carriers Drop Their Small NarrowbodiesThey Outsource the Routes to Regional Partners

Aircraft Unit Cost Comparison (500 nm Sector)

Cos

t per

sea

t-mile

(US¢

)

Cost per mile (US$)

Low Fare Carriers

Regional Carriers

Assumptions: US operating environment and fuel price @ $1.80 per US gallon

Outsourced Routes

Network Carriers110 Seaters

130 Seaters

150 Seaters

50 Seaters

70 Seaters

90 Seaters

2005 US Domestic Yield Curve

180 Seaters

10

The Capacity Growth and Outsourcing Trends Are Evident in Reported Figures

16.2% 16.8% 18.1% 19.6% 20.0% 22.4%

35.3

35.9

36.4

36.8

37.5

38.0

2000 2001 2002 2003 2004 2005

83.8% 83.2% 81.9% 80.4% 80.0% 77.6%

170.9

172.0

173.0 173.2

174.1

174.8

2000 2001 2002 2003 2004 2005

Regional Aircraft Market Share and Average Seat Capacity

Mainline Aircraft Market Share and Average Seat Capacity

Average seats per departureTotal seats offered

Source: OAG, US & Europe data ONLY

11

Industry Instability Will Continue Until Segmentation Share Equilibrium Is Reached

Networks will match their operating costs to the premium the passenger is willing to pay:

Restructure - labor- productivity- schedule- distribution- simplification

Route Transfer to Regional Partners- scope- cost

Operating Costs Are The Key

Network Carriers57%

Network Carriers33%

Regional Airlines

21%

Low Cost Carriers

22%

Regional Airlines

33%

Low Cost Carriers

33%

Today EquilibriumN

etw

ork

Car

riers

Where Will It End Up ?

12

Market Pressures Are Favoring Larger Regional Aircraft

Driving Factors

Lower YieldsHigher Fuel PricesRelaxed Pilot Scope ClausesRoute Transfers from Mainline

13

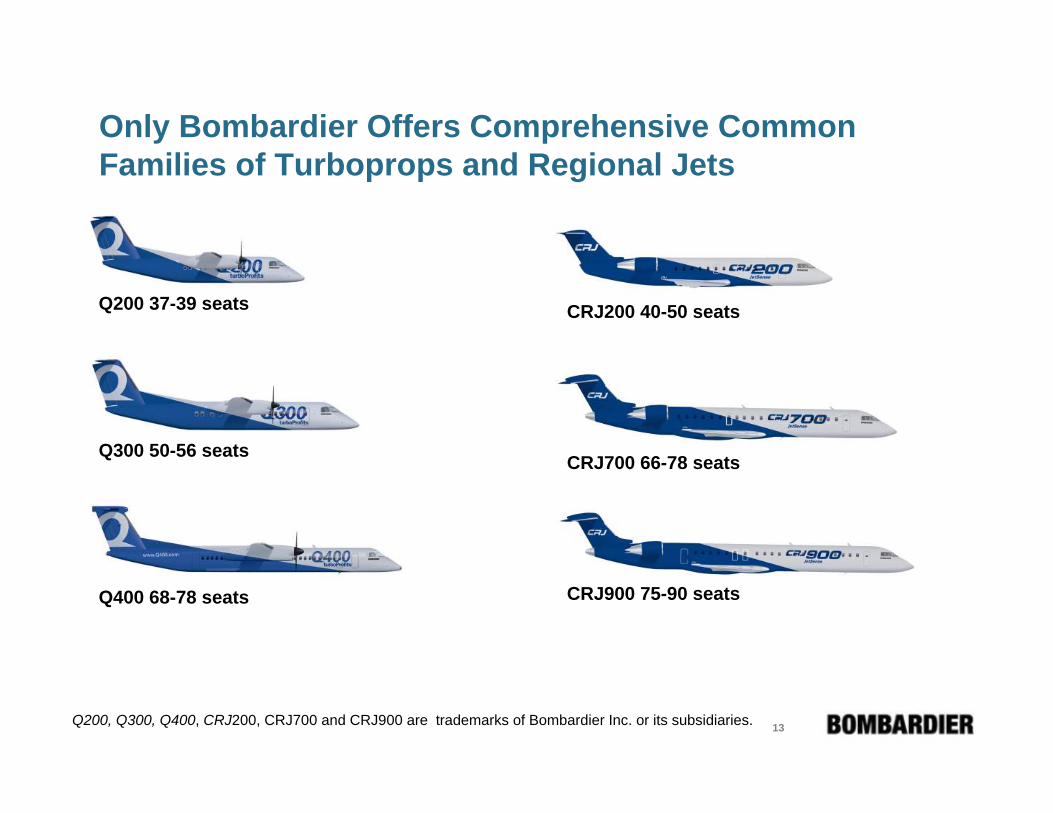

Only Bombardier Offers Comprehensive Common Families of Turboprops and Regional Jets

Q200, Q300, Q400, CRJ200, CRJ700 and CRJ900 are trademarks of Bombardier Inc. or its subsidiaries.

Q200 37-39 seats

Q300 50-56 seats

Q400 68-78 seats

CRJ200 40-50 seats

CRJ700 66-78 seats

CRJ900 75-90 seats

14

Bombardier Has Lead the Market Over Five yearsGross Orders in the 20-99 Seat Regional Market

72%

51%58% 60%

50%42%

28%

49%42% 40%

50%58%

2001 2002 2003 2004 2005 2006 Ytd

Bombardier Others

Note: Data includes order conversions between programs. Does not include corporate shuttle aircraft.

At September 27, 2006

15

Regional Jet Market & Programs

16

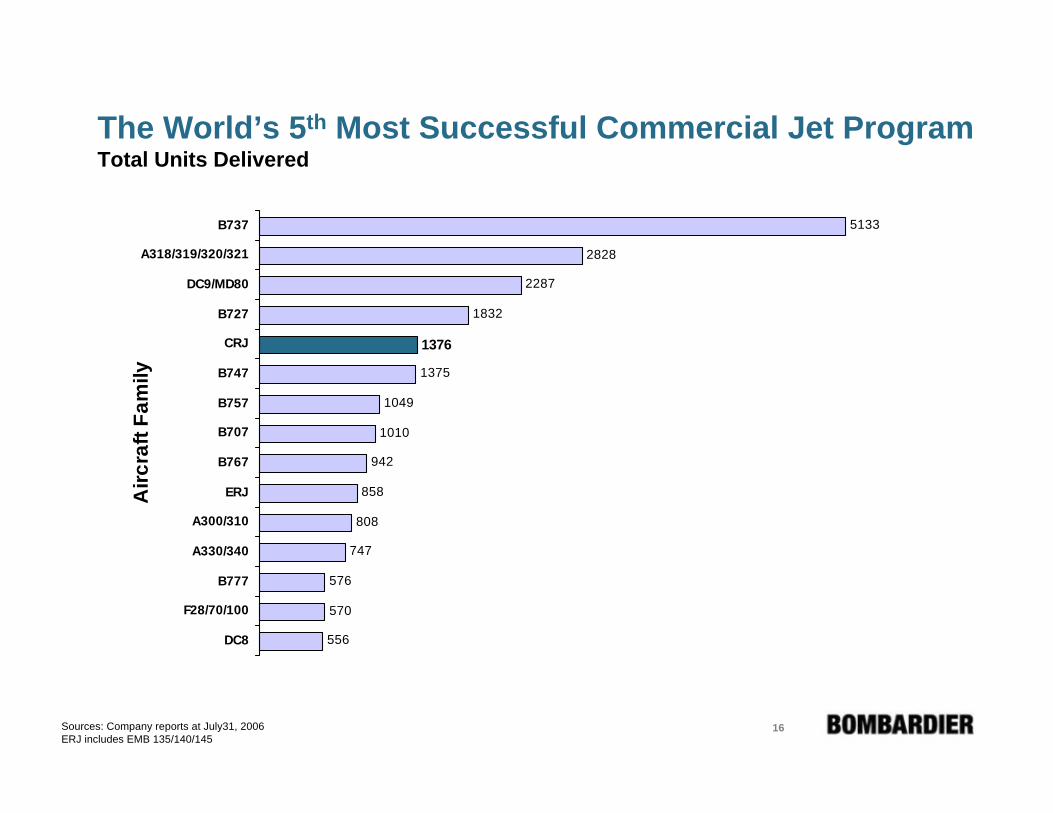

556

570

576

747

808

858

942

1010

1049

1832

2287

2828

5133

1376

1375

DC8

F28/70/100

B777

A330/340

A300/310

ERJ

B767

B707

B757

B747

CRJ

B727

DC9/MD80

A318/319/320/321

B737

Airc

raft

Fam

ilyThe World’s 5th Most Successful Commercial Jet ProgramTotal Units Delivered

Sources: Company reports at July31, 2006ERJ includes EMB 135/140/145

17

45 Customers Worldwide

Diverse Customer Base for the CRJ Series

18

Bombardier CRJ Series Sales StatusAs of July 31, 2006

29255284CRJ700*

731,3761,449Total

4359102CRJ900

01515CRJ705

11,0471,048CRJ100/200/440*

BacklogDelivered Aircraft

Firm Aircraft

* Includes Corporate variants of the CRJ (Orders and deliveries include 26 CRJ200 and seven CRJ700.)

19

CRJ100/200/440 Fleet At a Glance Fleet

Aircraft in Service * 948Parked Aircraft * 94Operators in Service 28 Regional operators

12 Business operators

Reliability - as of June 2006 (excludes business operators)

Dispatch Reliability 99.0%Scheduled Completion 99.6%

Utilization - as of June 2006 (excludes business operators)

Cumulative Hours 13,426,555Cumulative Cycles 11,582,651

High Time Aircraft - (in service)

Hours 32,019 SN 7030 (SkyWest)

Cycles 29,458 SN 7011 (Comair)

* Commercial Aviation Value Report August 2006

20

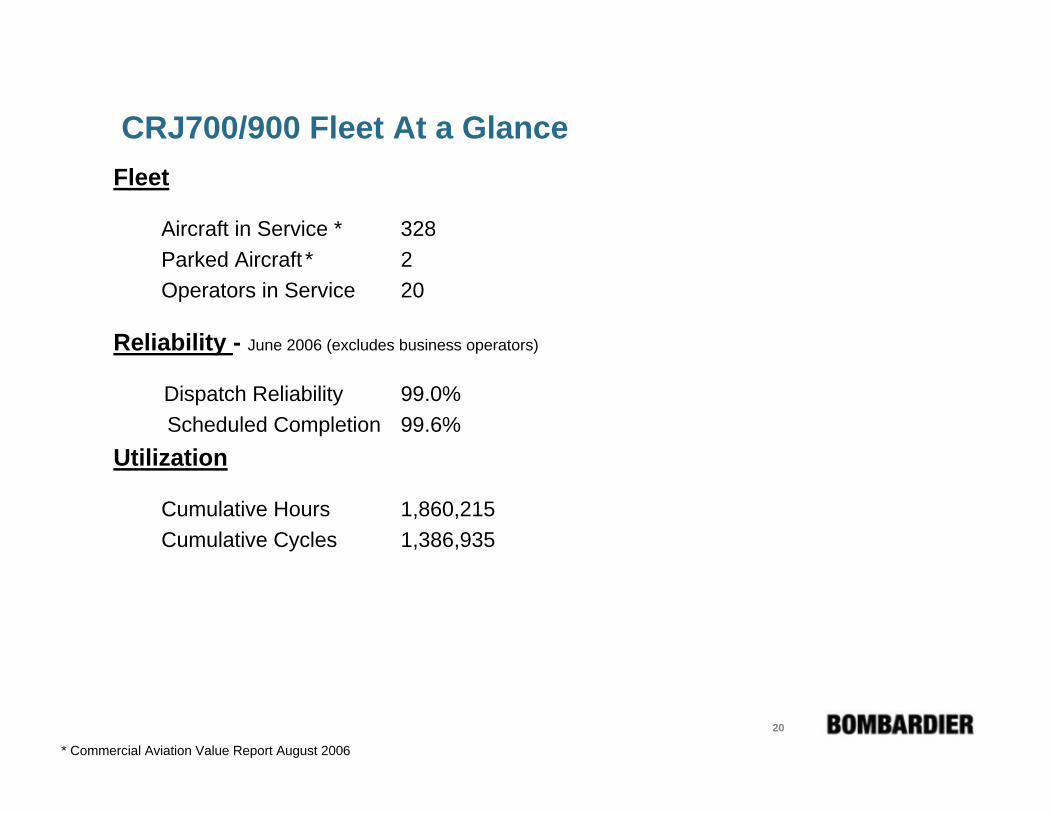

CRJ700/900 Fleet At a Glance Fleet

Aircraft in Service * 328Parked Aircraft * 2Operators in Service 20

Reliability - June 2006 (excludes business operators)

Dispatch Reliability 99.0%Scheduled Completion 99.6%

Utilization

Cumulative Hours 1,860,215Cumulative Cycles 1,386,935

* Commercial Aviation Value Report August 2006

21

Large RJs Compete Effectively With Narrowbodies on a Cost Per Seat Basis

500 nm Sector Operating Cost per Seat-Mile Comparison

Major CarriersRegional Carriers

TOC

DOC

Assumptions: US operating environment and fuel price @ $1.80 per US gallon

TOC

DOC

13.6¢

11.3¢

9.7¢8.9¢

15.0¢

13.7¢

12.1¢

10.5¢

8.2¢ 7.8¢7.2¢

6.5¢6.6¢7.1¢8.1¢

9.1¢

CRJ200 CRJ700 CRJ900 CRJ900X 100-SeatJet

130-SeatJet

150-SeatJet

180-SeatJet

22

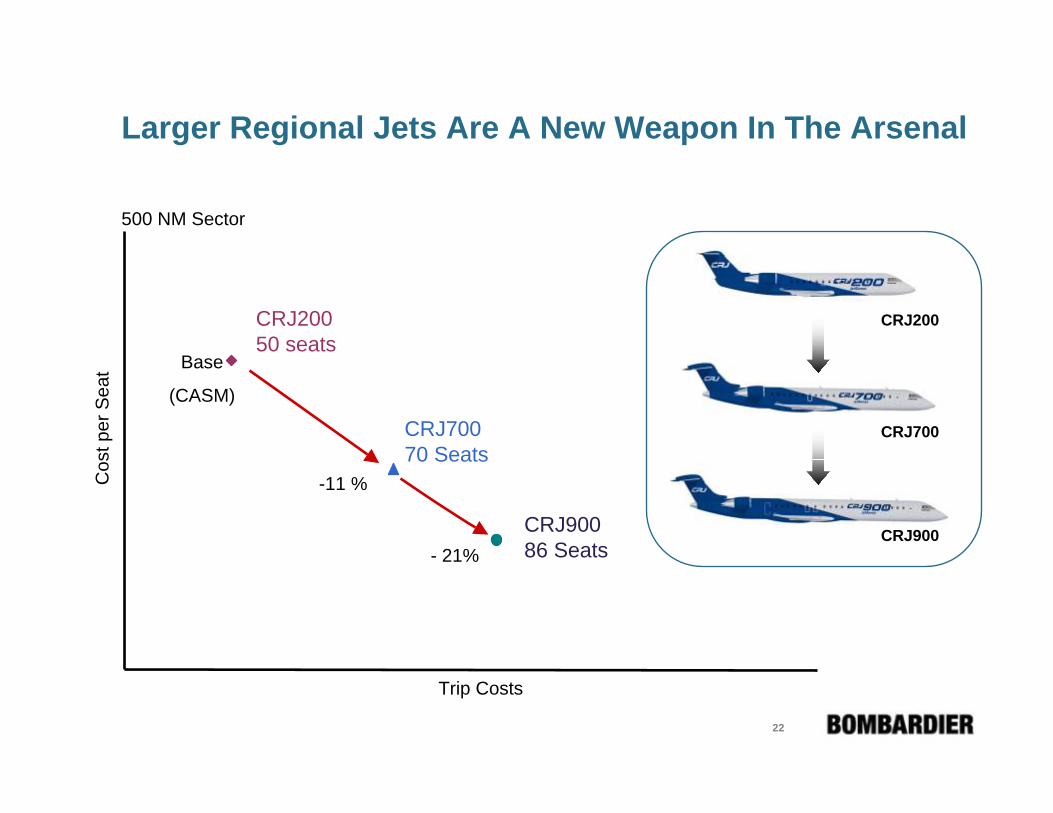

Larger Regional Jets Are A New Weapon In The Arsenal

Trip Costs

Cos

t per

Sea

t

CRJ20050 seats

CRJ70070 Seats

CRJ90086 Seats

-11 %

- 21%CRJ900

CRJ700

CRJ200

500 NM Sector

Base

(CASM)

23

The CRJ900 Continues to Gain Momentum

Over 100 firm orders in the past 30 months

24

Turboprop Market & Programs

25

Bombardier Q Series Dash 8 Sales StatusAs of July 31, 2006

496100Q200

82749831Total

60125185Q400

18229247Q300

0299299Q100

BacklogDelivered Aircraft

Firm Aircraft

26

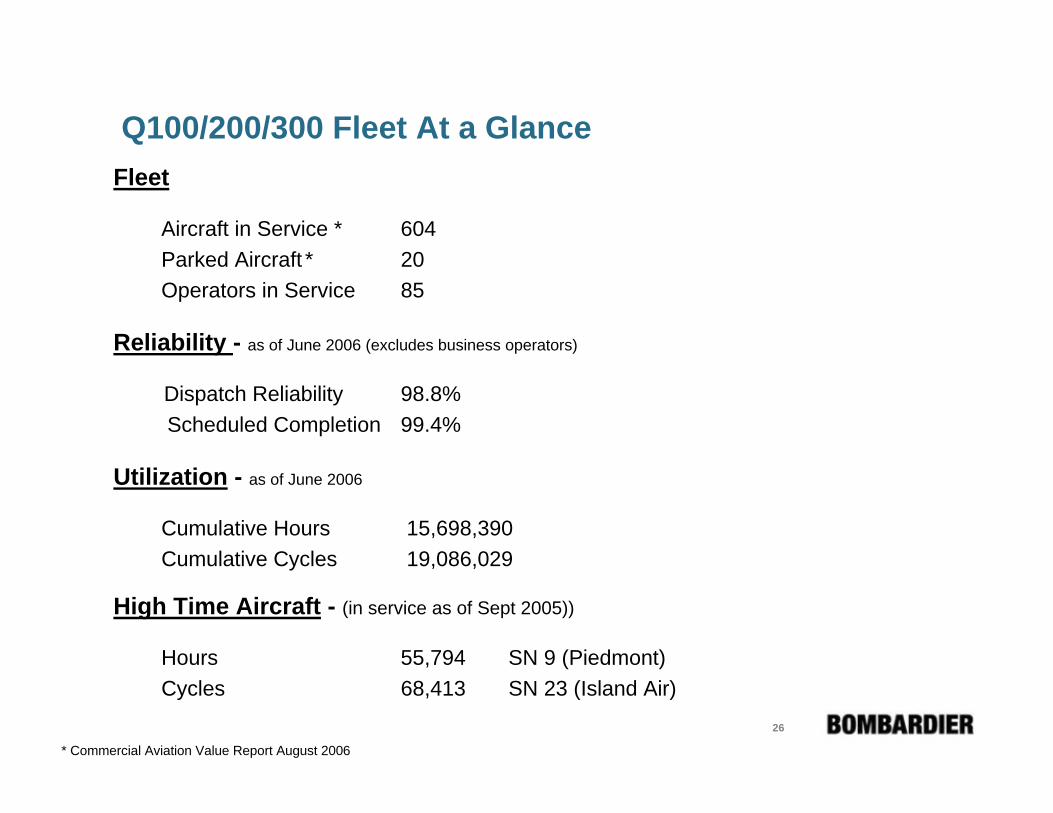

Q100/200/300 Fleet At a GlanceFleet

Aircraft in Service * 604Parked Aircraft * 20Operators in Service 85

Reliability - as of June 2006 (excludes business operators)

Dispatch Reliability 98.8%Scheduled Completion 99.4%

Utilization - as of June 2006

Cumulative Hours 15,698,390Cumulative Cycles 19,086,029

High Time Aircraft - (in service as of Sept 2005))

Hours 55,794 SN 9 (Piedmont)Cycles 68,413 SN 23 (Island Air)

* Commercial Aviation Value Report August 2006

27

Q400 Fleet At a Glance Fleet

Aircraft in Service* 125Parked Aircraft * 0Operators in Service 16

Reliability - as of July 2006 (excludes business operators)

Dispatch Reliability 98.7%Scheduled Completion 99.6%

Utilization - as of July 2006 (excludes business operators)

Cumulative Hours 819,102Cumulative Cycles 914,585

* Commercial Aviation Value Report August 2006

28

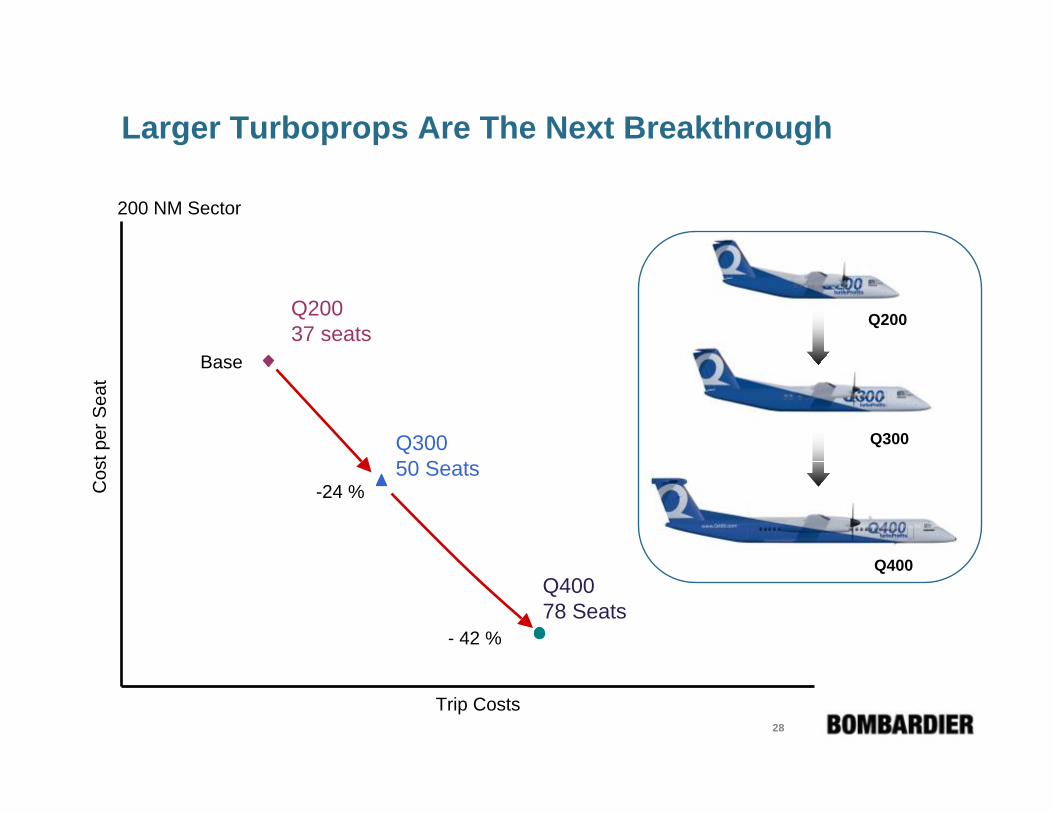

Larger Turboprops Are The Next Breakthrough

Trip Costs

Cos

t per

Sea

t

Q20037 seats

Q30050 Seats

Q40078 Seats

-24 %

- 42 %

Q200

Q300

Q400

200 NM Sector

Base

29

The Q400 Continues to Gain Ground Around The World

Over 90 firm orders in the past 30 months … including our latest Customers

Luxair South African Express

Porter Airlines Tassili Airlines

Frontier Airlines

30

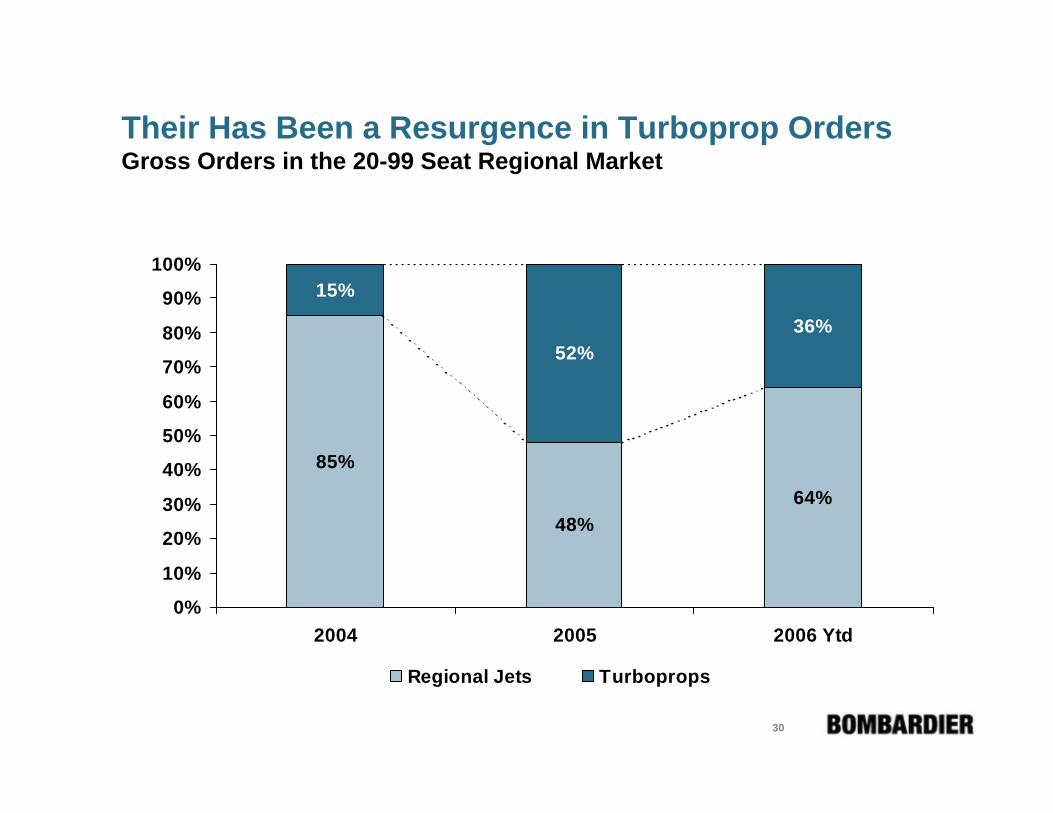

Their Has Been a Resurgence in Turboprop OrdersGross Orders in the 20-99 Seat Regional Market

85%

48%64%

15%

52%36%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 Ytd

Regional Jets Turboprops

31

Market Pressures Are Favoring Larger Regional Aircraft

Driving Factors

Lower YieldsHigher Fuel PricesRelaxed Pilot Scope ClausesRoute Transfers from Mainline

32

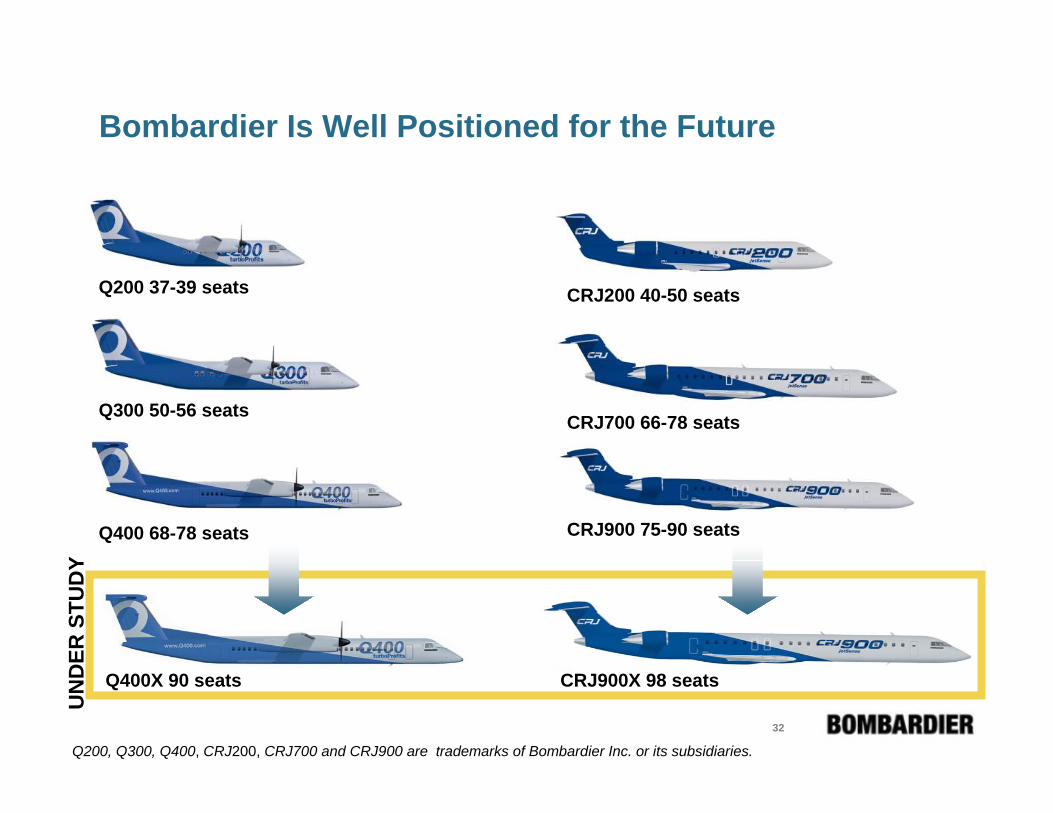

Bombardier Is Well Positioned for the Future

Q200 37-39 seats

Q300 50-56 seats

Q400 68-78 seats

CRJ200 40-50 seats

CRJ700 66-78 seats

CRJ900 75-90 seats

Q200, Q300, Q400, CRJ200, CRJ700 and CRJ900 are trademarks of Bombardier Inc. or its subsidiaries.

CRJ900X 98 seatsQ400X 90 seats

UN

DER

STU

DY

33

Regional Aircraft Strategy Going Forward

Capitalize on surging turboprop volume and forecasted “next wave” of large CRJ orders to strengthen our backlog

Aggressively pursue cost reduction initiatives including lean manufacturing, supply base rationalization and low cost manufacturing strategies

Continue to capitalize on our strong platforms and introduce new derivatives to meet market needs

34

Information contained in this document is proprietary to Bombardier Inc., Bombardier Aerospace, Regional Aircraft (“Bombardier”). This document must not be reproduced or shared with, or distributed to, any third party in whole or in part without Bombardier’s prior written consent.

This document is submitted for informational purposes only; is not part of any proposal; and creates no contractual commitment. Bombardier provides the information contained in this document on an ‘as is, where is’ basis and makes no representation or warranty of any kind regarding the applicability or reliability of any of such information with respect to any use whatsoever to be made of it by the recipient.

Any information of a technical nature contained in this document may contain inaccuracies and is subject to change and should never be relied upon for operational use.

Disclaimer