the nbfc liquidity situation: analysis and insights nbfc liquidity situation.pdf · vehicle loans...

TRANSCRIPT

The NBFC Liquidity Situation:Analysis and Insights

J u l y 2 0 1 9

Table of Contents

• Quantum of debt raised

• Sources of debt

• Products providing liquidity

• Cost of funds

• Potential factors impacting liquidity

• Vivriti Capital clients’ view

• Outlook

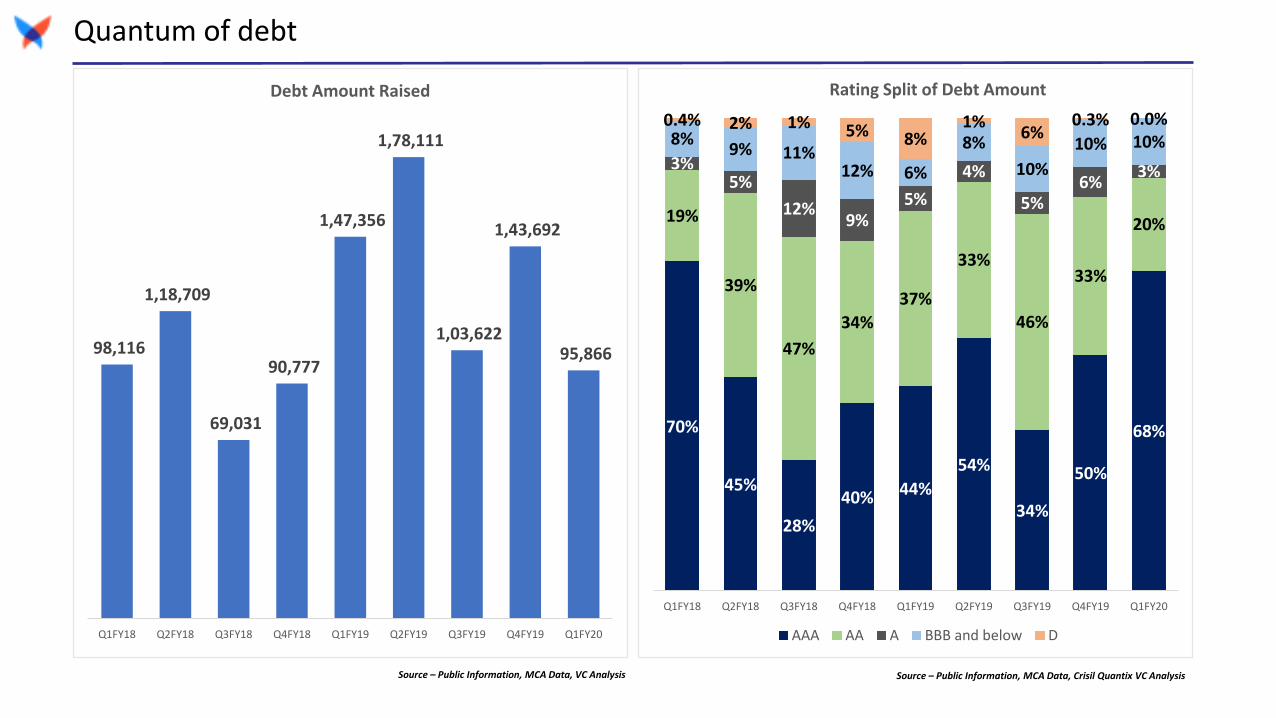

Quantum of debt

Quantum of debt

98,116

1,18,709

69,031

90,777

1,47,356

1,78,111

1,03,622

1,43,692

95,866

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q2FY19 Q3FY19 Q4FY19 Q1FY20

Debt Amount Raised

70%

45%

28%

40% 44%

54%

34%

50%

68%

19%

39%

47%

34%

37%

33%

46%

33%

20%

3%5%

12%9%

5%

4%

5%6%

3%

8%9% 11%

12% 6%

8%

10%

10% 10%0.4% 2% 1% 5% 8%

1%6%

0.3% 0.0%

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q2FY19 Q3FY19 Q4FY19 Q1FY20

Rating Split of Debt Amount

AAA AA A BBB and below D

Source – Public Information, MCA Data, VC Analysis Source – Public Information, MCA Data, Crisil Quantix VC Analysis

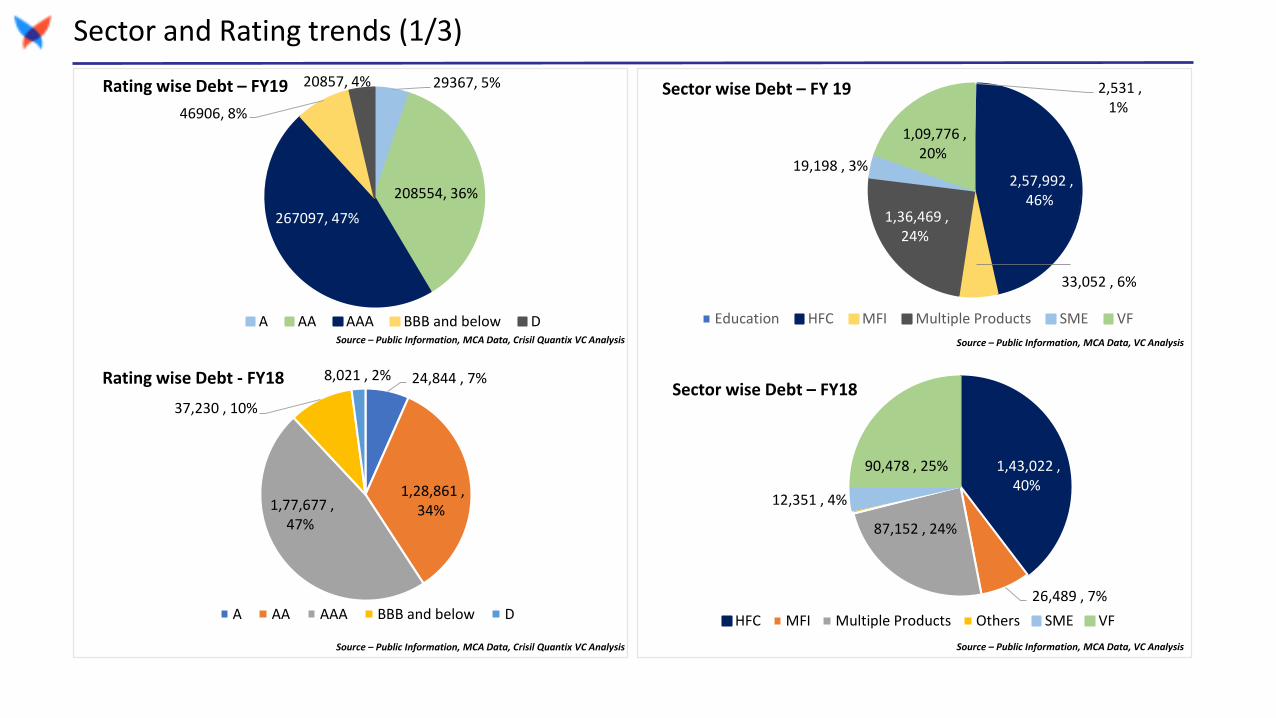

Sector and Rating trends (1/3)

29367, 5%

208554, 36%

267097, 47%

46906, 8%

20857, 4%Rating wise Debt – FY19

A AA AAA BBB and below D

24,844 , 7%

1,28,861 , 34%1,77,677 ,

47%

37,230 , 10%

8,021 , 2%Rating wise Debt - FY18

A AA AAA BBB and below D

2,531 , 1%

2,57,992 , 46%

33,052 , 6%

1,36,469 , 24%

19,198 , 3%

1,09,776 , 20%

Sector wise Debt – FY 19

Education HFC MFI Multiple Products SME VF

1,43,022 , 40%

26,489 , 7%

87,152 , 24%

12,351 , 4%

90,478 , 25%

Sector wise Debt – FY18

HFC MFI Multiple Products Others SME VF

Source – Public Information, MCA Data, Crisil Quantix VC Analysis

Source – Public Information, MCA Data, Crisil Quantix VC Analysis Source – Public Information, MCA Data, VC Analysis

Source – Public Information, MCA Data, VC Analysis

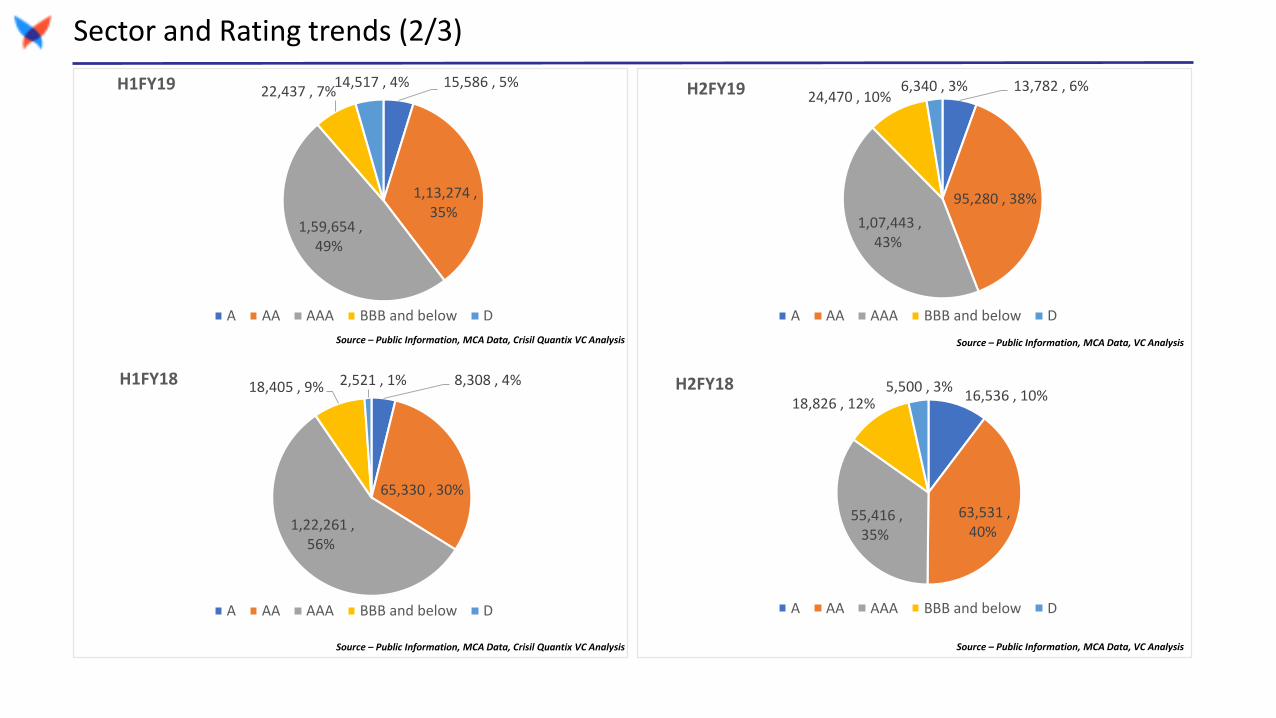

Sector and Rating trends (2/3)

15,586 , 5%

1,13,274 , 35%

1,59,654 , 49%

22,437 , 7%14,517 , 4%H1FY19

A AA AAA BBB and below D

8,308 , 4%

65,330 , 30%

1,22,261 , 56%

18,405 , 9% 2,521 , 1%H1FY18

A AA AAA BBB and below D

13,782 , 6%

95,280 , 38%

1,07,443 , 43%

24,470 , 10%6,340 , 3%H2FY19

A AA AAA BBB and below D

16,536 , 10%

63,531 , 40%

55,416 , 35%

18,826 , 12%5,500 , 3%H2FY18

A AA AAA BBB and below D

Source – Public Information, MCA Data, Crisil Quantix VC Analysis

Source – Public Information, MCA Data, Crisil Quantix VC Analysis Source – Public Information, MCA Data, VC Analysis

Source – Public Information, MCA Data, VC Analysis

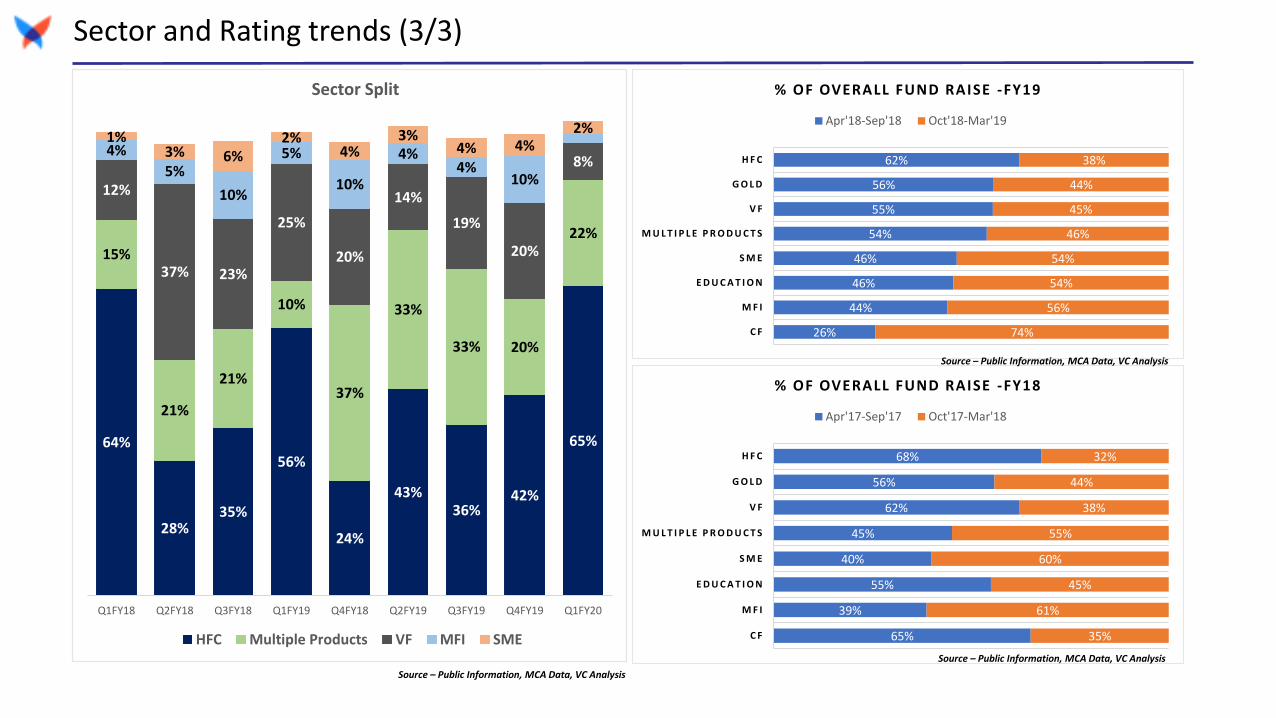

Sector and Rating trends (3/3)

64%

28%35%

56%

24%

43%36%

42%

65%

15%

21%

21%

10%

37%

33%

33% 20%

22%

12%

37% 23%

25%

20%

14%

19%

20%

8%4%

5%

10%

5%

10%

4%4%

10%

1%3% 6%

2%4%

3%4% 4%

2%

Q1FY18 Q2FY18 Q3FY18 Q1FY19 Q4FY18 Q2FY19 Q3FY19 Q4FY19 Q1FY20

Sector Split

HFC Multiple Products VF MFI SME

Source – Public Information, MCA Data, VC Analysis

26%

44%

46%

46%

54%

55%

56%

62%

74%

56%

54%

54%

46%

45%

44%

38%

C F

M F I

E D U C A T I O N

S M E

M U L T I P L E P R O D U C T S

V F

G O L D

H F C

% OF OVERALL FUND RAISE -FY19

Apr'18-Sep'18 Oct'18-Mar'19

65%

39%

55%

40%

45%

62%

56%

68%

35%

61%

45%

60%

55%

38%

44%

32%

C F

M F I

E D U C A T I O N

S M E

M U L T I P L E P R O D U C T S

V F

G O L D

H F C

% OF OVERALL FUND RAISE -FY18

Apr'17-Sep'17 Oct'17-Mar'18

Source – Public Information, MCA Data, VC Analysis

Source – Public Information, MCA Data, VC Analysis

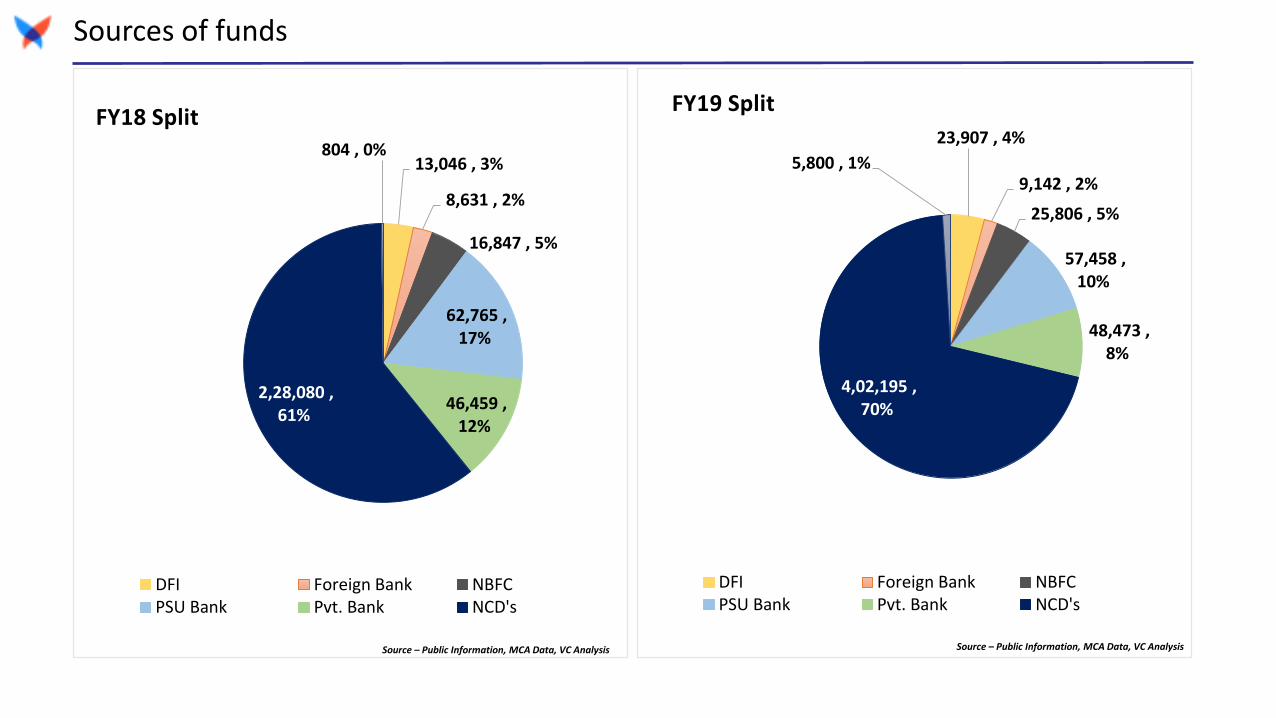

Sources of funds

Sources of funds

13,046 , 3%

8,631 , 2%

16,847 , 5%

62,765 , 17%

46,459 , 12%

2,28,080 , 61%

804 , 0%

FY18 Split

DFI Foreign Bank NBFCPSU Bank Pvt. Bank NCD's

23,907 , 4%

9,142 , 2%

25,806 , 5%

57,458 , 10%

48,473 , 8%

4,02,195 , 70%

5,800 , 1%

FY19 Split

DFI Foreign Bank NBFCPSU Bank Pvt. Bank NCD's

Source – Public Information, MCA Data, VC Analysis Source – Public Information, MCA Data, VC Analysis

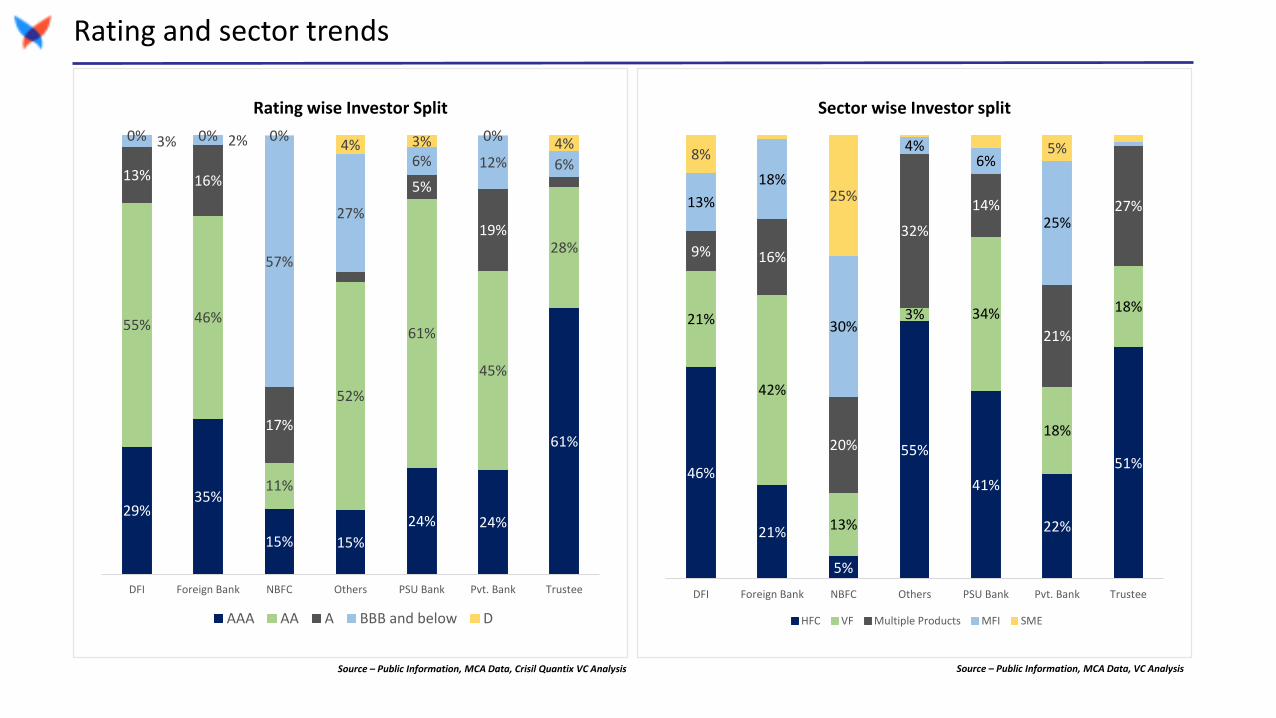

Rating and sector trends

29%35%

15% 15%

24% 24%

61%

55% 46%

11%

52%

61%

45%

28%

13% 16%

17%

2%

5%

19%

2%

3% 2%

57%

27%

6% 12% 6%

0% 0% 0%4% 3% 0% 4%

DFI Foreign Bank NBFC Others PSU Bank Pvt. Bank Trustee

Rating wise Investor Split

AAA AA A BBB and below D

46%

21%

5%

55%

41%

22%

51%

21%

42%

13%

3% 34%

18%

18%

9% 16%

20%

32%

14%

21%

27%13%

18%

30%

4%6%

25%

8%

25%

5%

DFI Foreign Bank NBFC Others PSU Bank Pvt. Bank Trustee

Sector wise Investor split

HFC VF Multiple Products MFI SME

Source – Public Information, MCA Data, VC AnalysisSource – Public Information, MCA Data, Crisil Quantix VC Analysis

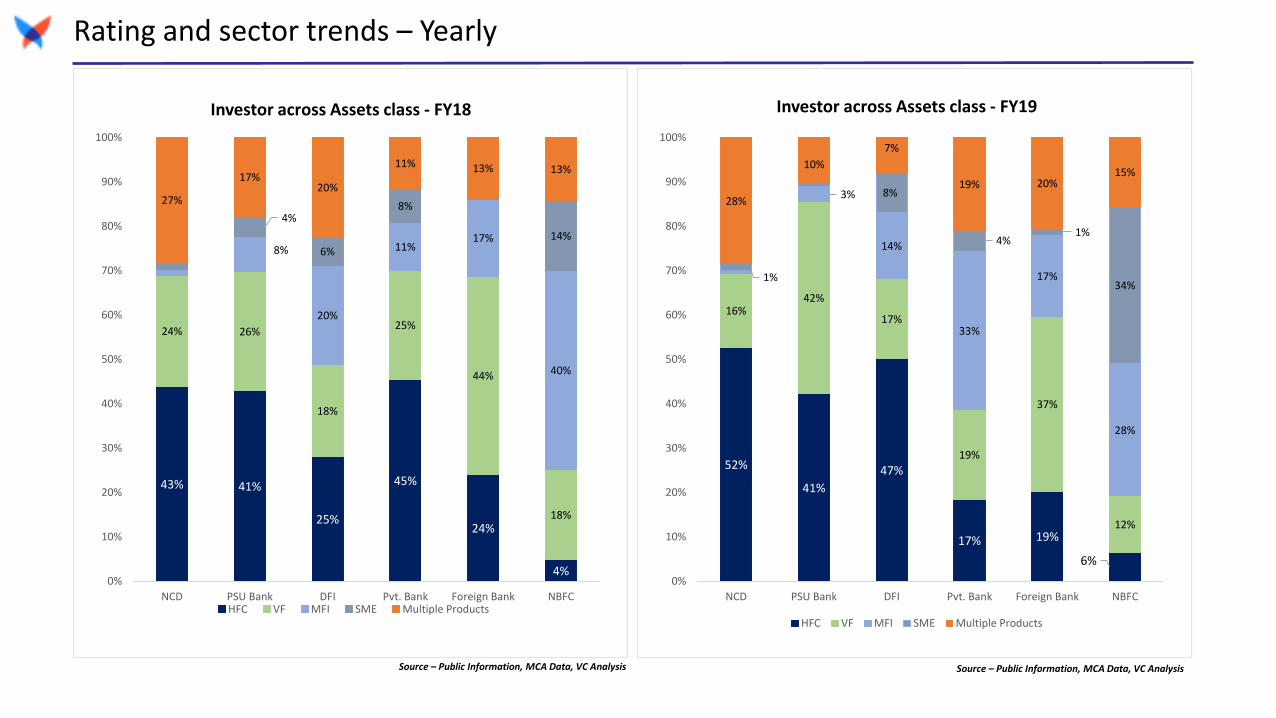

Rating and sector trends – Yearly

43% 41%

25%

45%

24%

4%

24% 26%

18%

25%

44%

18%

8%

20%

11%17%

40%

4%

6%

8%

14%

27%

17%20%

11% 13% 13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

NCD PSU Bank DFI Pvt. Bank Foreign Bank NBFC

Investor across Assets class - FY18

HFC VF MFI SME Multiple Products

52%

41%

47%

17% 19%

6%

16%42%

17%

19%

37%

12%

1%

3%

14%

33%

17%

28%

8%

4%1%

34%

28%

10%

7%

19% 20%15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

NCD PSU Bank DFI Pvt. Bank Foreign Bank NBFC

Investor across Assets class - FY19

HFC VF MFI SME Multiple Products

Source – Public Information, MCA Data, VC AnalysisSource – Public Information, MCA Data, VC Analysis

Products providing liquidity

70%2%

17%

5%

1%2%

3%

FY 2018- ABS Issuances- Sector Split

Vehicle loans

Housing loans

Micro loans

Loan against property(LAP)

Small business loans

Tractor loans

Others*

Source – Rating Agencies Market Estimate

Structured Finance : Sector Wise Split: Aggregate Market TrendsABS Issuances: Sector Split

Direct Assignment Issuances: Sector Split

14%

54%

10%

18%

2% 2%

FY 2018- DA Issuances- Sector Split

Vehicle loans

Housing loans

Micro loans

LAP

Small business loans

Tractor loans

Others*

Source – Rating Agencies Market Estimate

• Vehicle loans receivables-backed securitizationtransactions are dominating ABS issuances bothin FY 18 and FY 19.

• Microfinance loans were second highestcontributor to the overall ABS issuances; owingto improved asset quality on postdemonetization originated portfolio

• The direct assignment issuances continues to bedominated by housing finance companies-constituting more than 50% of total issuancevolumes.

• Housing finance issuances continue to dominateDA issuances on account of following reasonsdue to low risk perception of asset class

• Microfinance issuances on account of improvedasset quality has shown considerableimprovement in issuance volumes for this FY

• Vehicle finance issuances due to favorable tenorare quite popular in ABS market; however thevolatility of PAR of the underlying makes itunattractive under direct assignment route

13

49%

6%

16%

5%

4%

2%

17%

1%

FY 2019- ABS Issuances- Sector Split

Vehicle Loans

Housing Loans

Micro Loans

Loan Against Property(LAP)Small Business Loans

Tractor Loans

Lease Rentals

Others*

Source – Rating Agencies Market Estimate

11%

52%

14%

16%

1%

6%

FY 2019- DA Issuances- Sector Split

Vehicle Loans

Housing Loans

Micro Loans

LAP

Small Business Loans

Tractor Loans

Others

Source – Rating Agencies Market Estimate

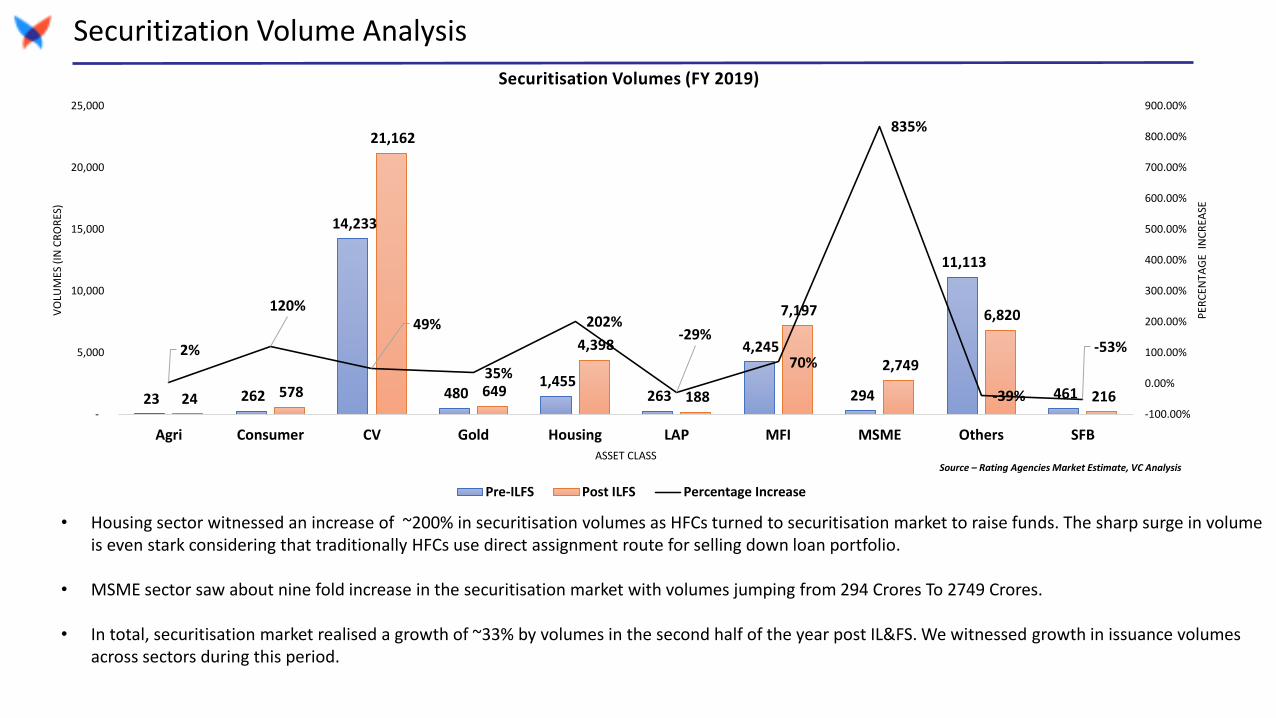

Securitization Volume Analysis

• Housing sector witnessed an increase of ~200% in securitisation volumes as HFCs turned to securitisation market to raise funds. The sharp surge in volume is even stark considering that traditionally HFCs use direct assignment route for selling down loan portfolio.

• MSME sector saw about nine fold increase in the securitisation market with volumes jumping from 294 Crores To 2749 Crores.

• In total, securitisation market realised a growth of ~33% by volumes in the second half of the year post IL&FS. We witnessed growth in issuance volumes across sectors during this period.

23 262

14,233

480 1,455

263

4,245

294

11,113

461 24 578

21,162

649

4,398

188

7,197

2,749

6,820

216

2%

120%49%

35%

202%-29%

70%

835%

-39%

-53%

-100.00%

0.00%

100.00%

200.00%

300.00%

400.00%

500.00%

600.00%

700.00%

800.00%

900.00%

-

5,000

10,000

15,000

20,000

25,000

Agri Consumer CV Gold Housing LAP MFI MSME Others SFB

PER

CEN

TAG

E IN

CR

EASE

VO

LUM

ES (

IN C

RO

RES

)

ASSET CLASS

Securitisation Volumes (FY 2019)

Pre-ILFS Post ILFS Percentage Increase

Source – Rating Agencies Market Estimate, VC Analysis

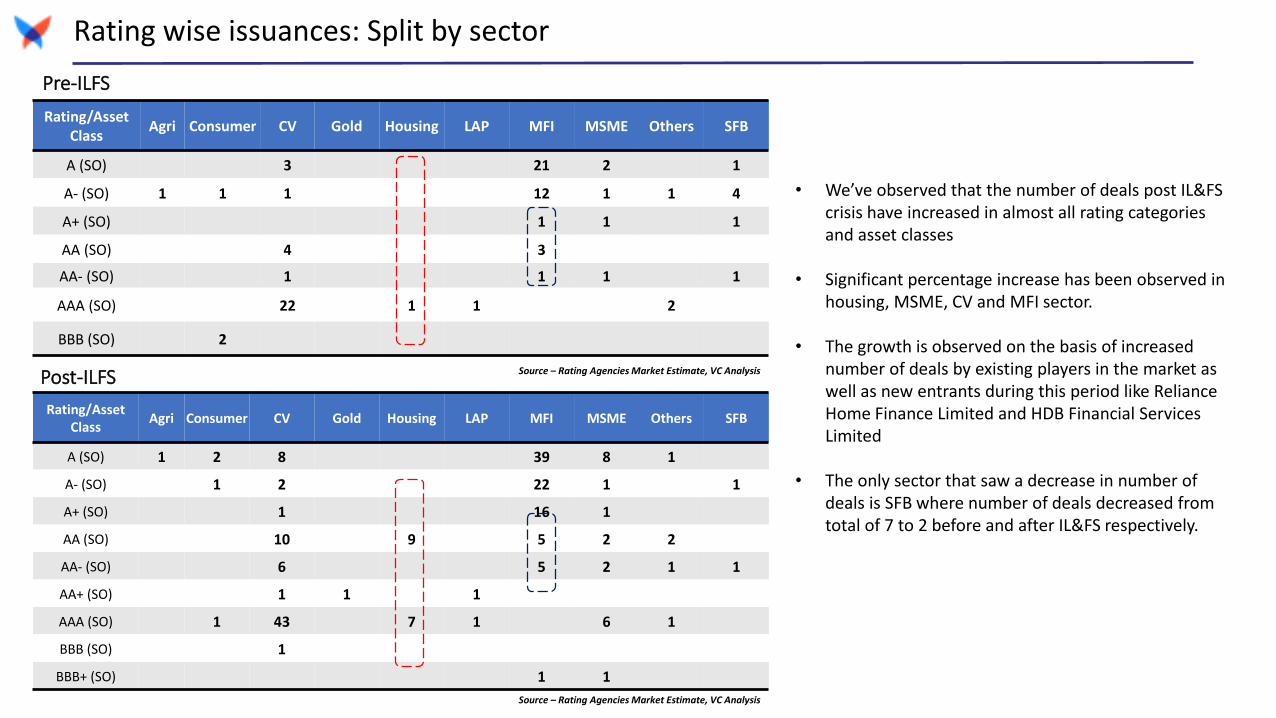

Rating wise issuances: Split by sector

Rating/Asset Class

Agri Consumer CV Gold Housing LAP MFI MSME Others SFB

A (SO) 3 21 2 1

A- (SO) 1 1 1 12 1 1 4

A+ (SO) 1 1 1

AA (SO) 4 3

AA- (SO) 1 1 1 1

AAA (SO) 22 1 1 2

BBB (SO) 2

Rating/Asset Class

Agri Consumer CV Gold Housing LAP MFI MSME Others SFB

A (SO) 1 2 8 39 8 1

A- (SO) 1 2 22 1 1

A+ (SO) 1 16 1

AA (SO) 10 9 5 2 2

AA- (SO) 6 5 2 1 1

AA+ (SO) 1 1 1

AAA (SO) 1 43 7 1 6 1

BBB (SO) 1

BBB+ (SO) 1 1

Pre-ILFS

Post-ILFS

• We’ve observed that the number of deals post IL&FS crisis have increased in almost all rating categories and asset classes

• Significant percentage increase has been observed in housing, MSME, CV and MFI sector.

• The growth is observed on the basis of increased number of deals by existing players in the market as well as new entrants during this period like Reliance Home Finance Limited and HDB Financial Services Limited

• The only sector that saw a decrease in number of deals is SFB where number of deals decreased from total of 7 to 2 before and after IL&FS respectively.

Source – Rating Agencies Market Estimate, VC Analysis

Source – Rating Agencies Market Estimate, VC Analysis

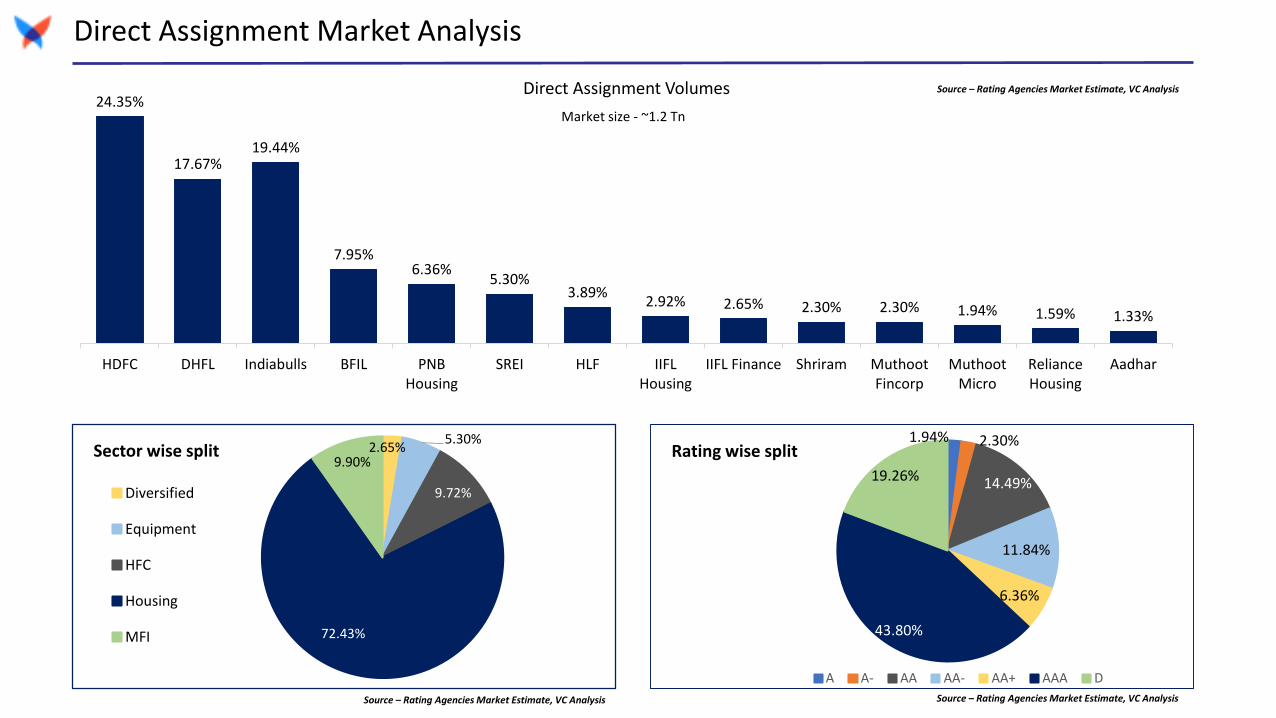

Direct Assignment Market Analysis

1.94% 2.30%

14.49%

11.84%

6.36%

43.80%

19.26%

Rating wise split

A A- AA AA- AA+ AAA D

2.65%5.30%

9.72%

72.43%

9.90%Sector wise split

Diversified

Equipment

HFC

Housing

MFI

Source – Rating Agencies Market Estimate, VC Analysis Source – Rating Agencies Market Estimate, VC Analysis

Source – Rating Agencies Market Estimate, VC Analysis

24.35%

17.67%19.44%

7.95%6.36%

5.30%3.89%

2.92% 2.65% 2.30% 2.30% 1.94% 1.59% 1.33%

HDFC DHFL Indiabulls BFIL PNBHousing

SREI HLF IIFLHousing

IIFL Finance Shriram MuthootFincorp

MuthootMicro

RelianceHousing

Aadhar

Direct Assignment Volumes

Market size - ~1.2 Tn

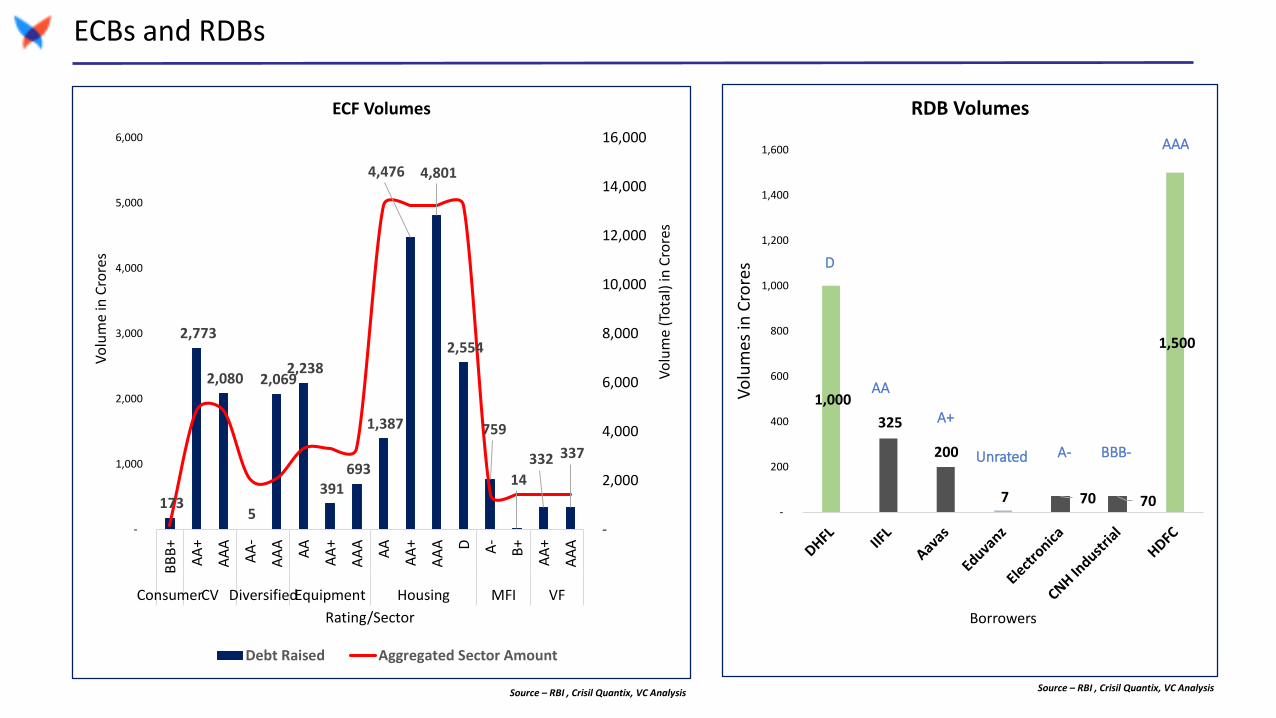

ECBs and RDBs

173

2,773

2,080

5

2,069 2,238

391 693

1,387

4,476 4,801

2,554

759

14

332 337

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

-

1,000

2,000

3,000

4,000

5,000

6,000

BB

B+

AA

+

AA

A

AA

-

AA

A

AA

AA

+

AA

A

AA

AA

+

AA

A D A-

B+

AA

+

AA

A

ConsumerCV DiversifiedEquipment Housing MFI VF

Vo

lum

e (T

ota

l) in

Cro

res

Vo

lum

e in

Cro

res

Rating/Sector

ECF Volumes

Debt Raised Aggregated Sector Amount

1,000

325

200

7 70 70

1,500

-

200

400

600

800

1,000

1,200

1,400

1,600

Vo

lum

es in

Cro

res

Borrowers

RDB Volumes

D

AA

A+

A-Unrated BBB-

AAA

Source – RBI , Crisil Quantix, VC AnalysisSource – RBI , Crisil Quantix, VC Analysis

Cost of funds

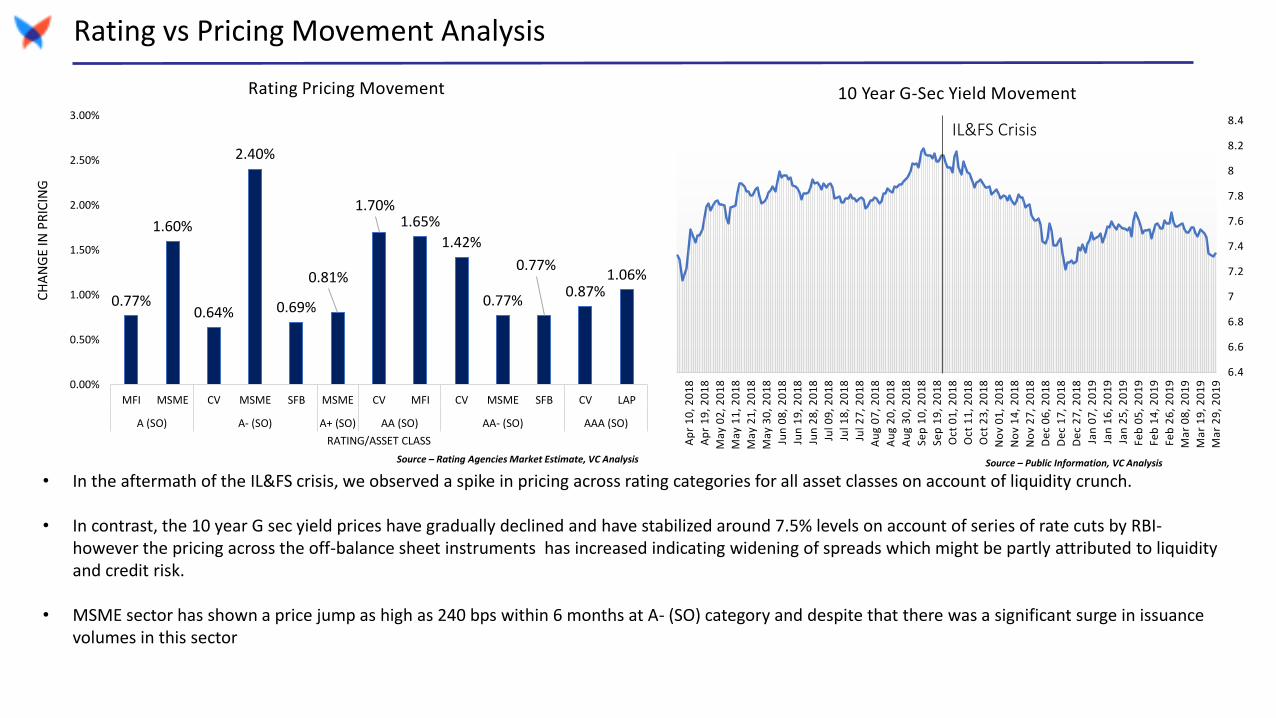

Rating vs Pricing Movement Analysis

0.77%

1.60%

0.64%

2.40%

0.69%

0.81%

1.70%1.65%

1.42%

0.77%

0.77%

0.87%1.06%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

MFI MSME CV MSME SFB MSME CV MFI CV MSME SFB CV LAP

A (SO) A- (SO) A+ (SO) AA (SO) AA- (SO) AAA (SO)

CH

AN

GE

IN P

RIC

ING

RATING/ASSET CLASS

Rating Pricing Movement

6.4

6.6

6.8

7

7.2

7.4

7.6

7.8

8

8.2

8.4

Ma

r 2

9,

20

19

Ma

r 1

9,

20

19

Ma

r 0

8,

20

19

Feb

26

, 2

01

9

Feb

14

, 2

01

9

Feb

05

, 2

01

9

Jan

25

, 2

01

9

Jan

16

, 2

01

9

Jan

07

, 2

01

9

De

c 2

7,

20

18

De

c 1

7,

20

18

De

c 0

6,

20

18

No

v 2

7,

20

18

No

v 1

4,

20

18

No

v 0

1,

20

18

Oct

23

, 2

01

8

Oct

11

, 2

01

8

Oct

01

, 2

01

8

Sep

19

, 2

01

8

Sep

10

, 2

01

8

Au

g 3

0,

20

18

Au

g 2

0,

20

18

Au

g 0

7,

20

18

Jul 2

7,

20

18

Jul 1

8,

20

18

Jul 0

9,

20

18

Jun

28

, 2

01

8

Jun

19

, 2

01

8

Jun

08

, 2

01

8

Ma

y 3

0,

20

18

Ma

y 2

1,

20

18

Ma

y 1

1,

20

18

Ma

y 0

2,

20

18

Ap

r 1

9,

20

18

Ap

r 1

0,

20

18

10 Year G-Sec Yield Movement

IL&FS Crisis

• In the aftermath of the IL&FS crisis, we observed a spike in pricing across rating categories for all asset classes on account of liquidity crunch.

• In contrast, the 10 year G sec yield prices have gradually declined and have stabilized around 7.5% levels on account of series of rate cuts by RBI-however the pricing across the off-balance sheet instruments has increased indicating widening of spreads which might be partly attributed to liquidity and credit risk.

• MSME sector has shown a price jump as high as 240 bps within 6 months at A- (SO) category and despite that there was a significant surge in issuance volumes in this sector

Source – Rating Agencies Market Estimate, VC Analysis Source – Public Information, VC Analysis

Factors impacting liquidity

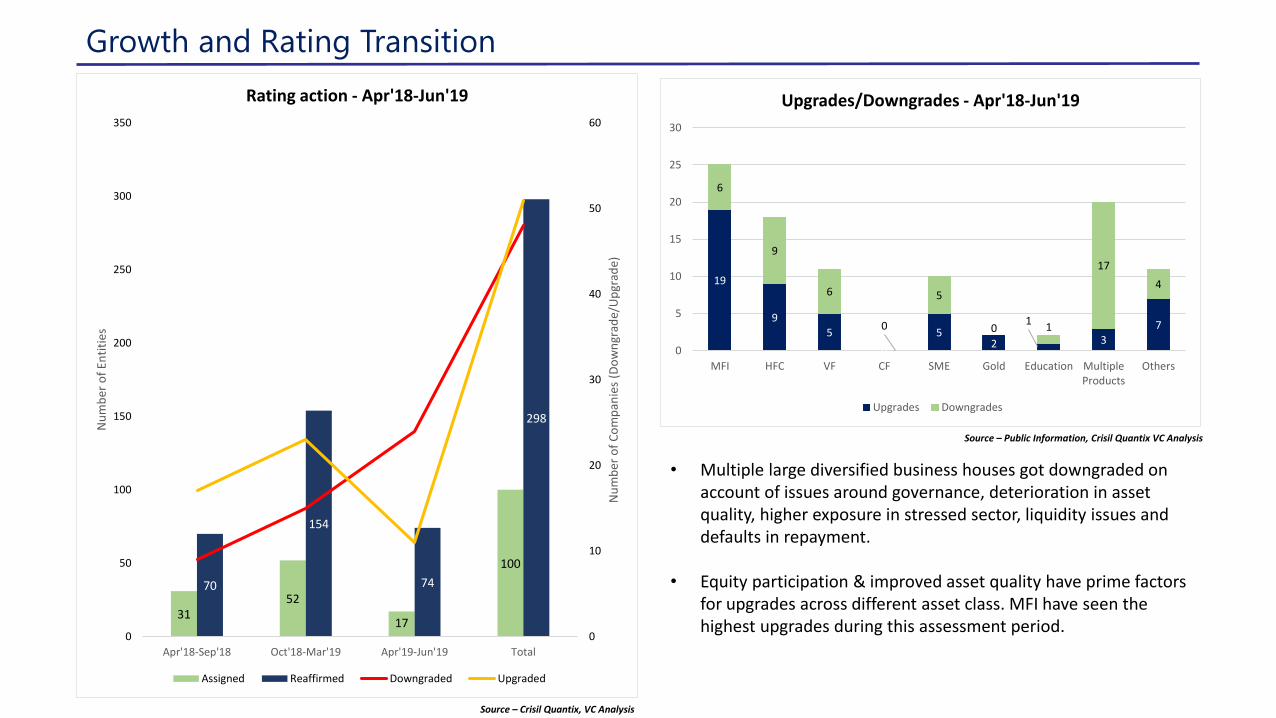

Growth and Rating Transition

3152

17

100

70

154

74

298

0

10

20

30

40

50

60

0

50

100

150

200

250

300

350

Apr'18-Sep'18 Oct'18-Mar'19 Apr'19-Jun'19 Total

Nu

mb

er o

f C

om

pan

ies

(Do

wn

grad

e/U

pgr

ade)

Nu

mb

er o

f En

titi

esRating action - Apr'18-Jun'19

Assigned Reaffirmed Downgraded Upgraded

19

95

0

52

1

37

6

9

6

0

5

0 1

17

4

0

5

10

15

20

25

30

MFI HFC VF CF SME Gold Education MultipleProducts

Others

Upgrades/Downgrades - Apr'18-Jun'19

Upgrades Downgrades

• Multiple large diversified business houses got downgraded on account of issues around governance, deterioration in asset quality, higher exposure in stressed sector, liquidity issues and defaults in repayment.

• Equity participation & improved asset quality have prime factors for upgrades across different asset class. MFI have seen the highest upgrades during this assessment period.

Source – Crisil Quantix, VC Analysis

Source – Public Information, Crisil Quantix VC Analysis

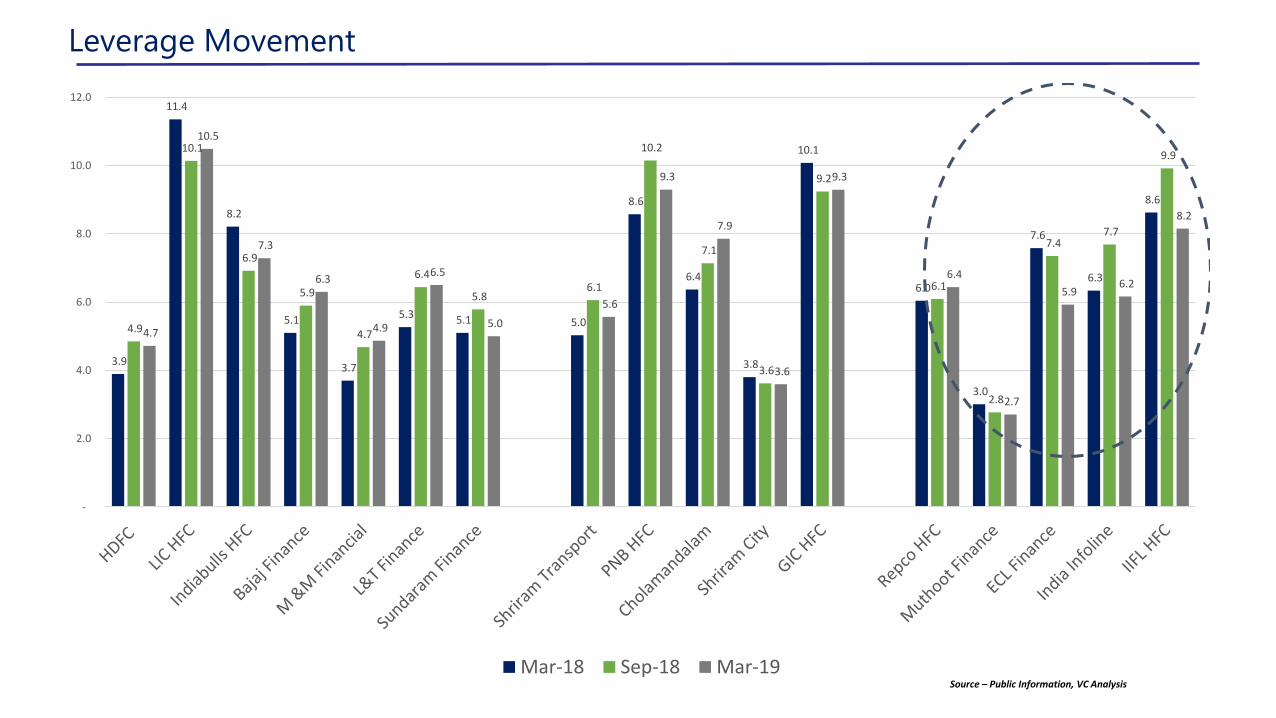

Leverage Movement

3.9

11.4

8.2

5.1

3.7

5.3 5.1 5.0

8.6

6.4

3.8

10.1

6.0

3.0

7.6

6.3

8.6

4.9

10.1

6.9

5.9

4.7

6.4

5.8 6.1

10.2

7.1

3.6

9.2

6.1

2.8

7.4 7.7

9.9

4.7

10.5

7.3

6.3

4.9

6.5

5.0

5.6

9.3

7.9

3.6

9.3

6.4

2.7

5.9 6.2

8.2

-

2.0

4.0

6.0

8.0

10.0

12.0

Mar-18 Sep-18 Mar-19Source – Public Information, VC Analysis

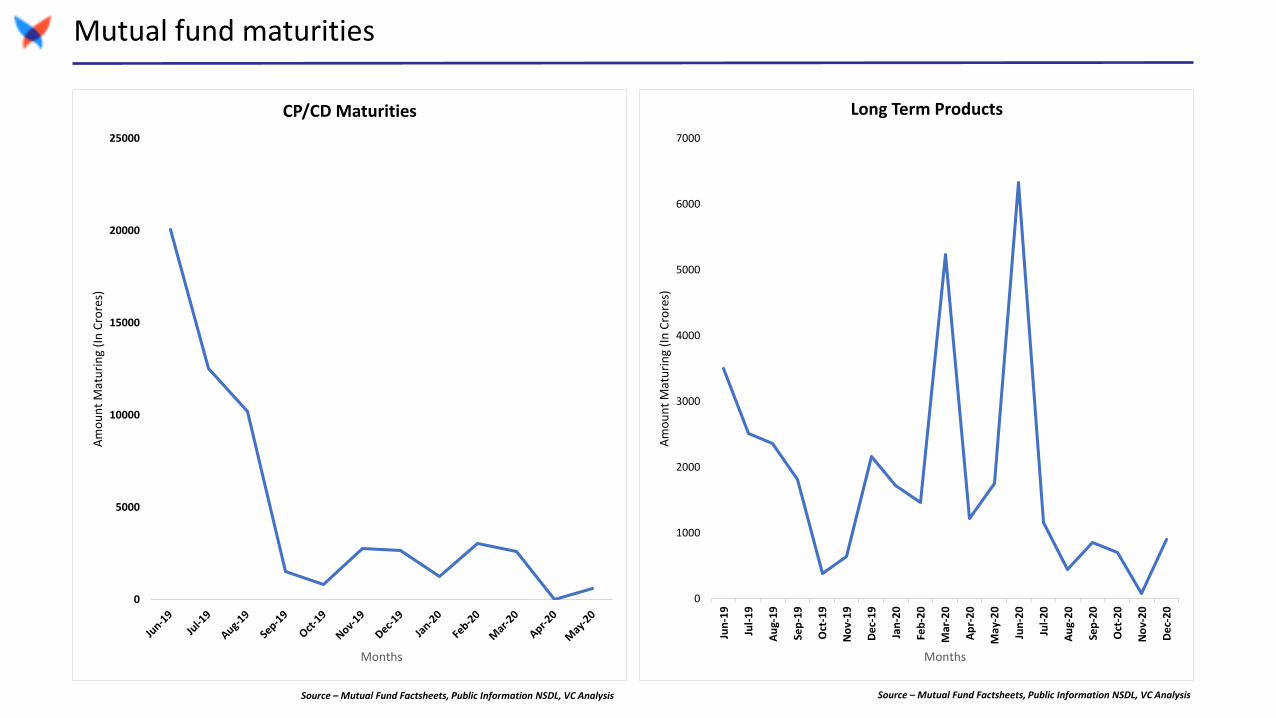

Mutual fund maturities

0

5000

10000

15000

20000

25000

Am

ou

nt

Mat

uri

ng

(In

Cro

res)

Months

CP/CD Maturities

0

1000

2000

3000

4000

5000

6000

7000

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

De

c-1

9

Jan

-20

Feb

-20

Mar

-20

Ap

r-2

0

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

De

c-2

0

Am

ou

nt

Mat

uri

ng

(In

Cro

res)

Months

Long Term Products

Source – Mutual Fund Factsheets, Public Information NSDL, VC Analysis Source – Mutual Fund Factsheets, Public Information NSDL, VC Analysis

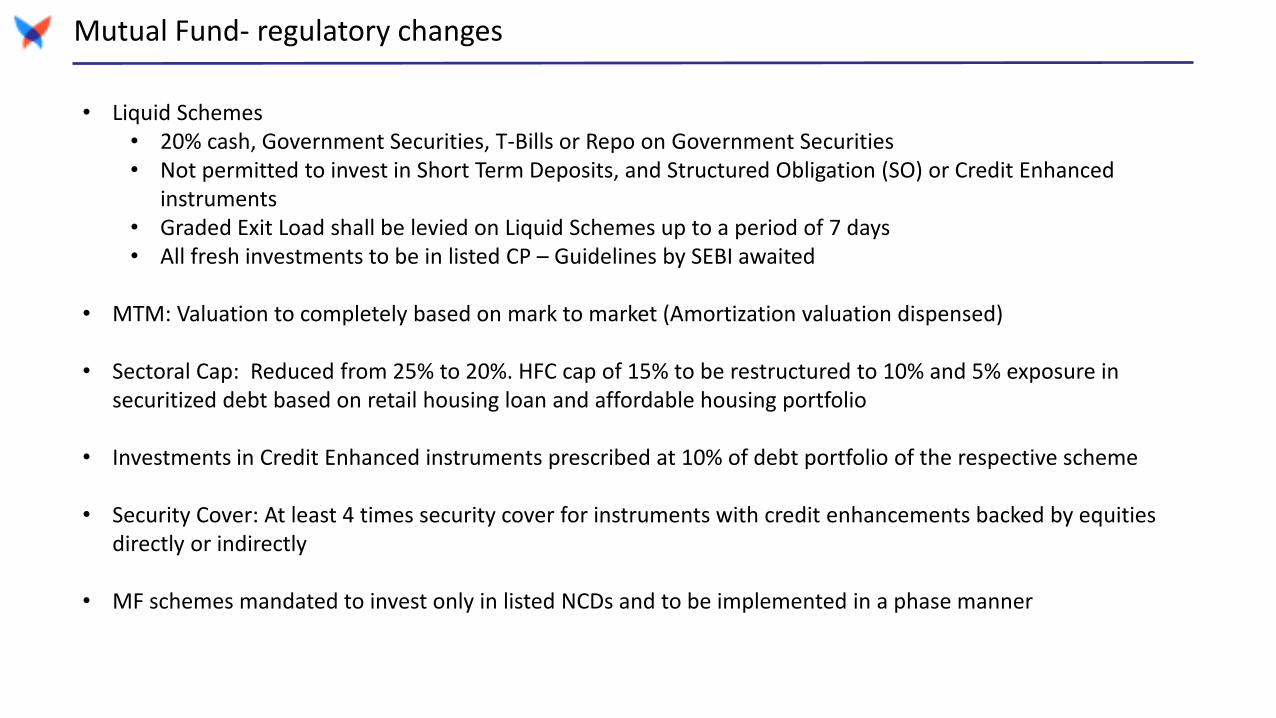

Mutual Fund- regulatory changes

• Liquid Schemes• 20% cash, Government Securities, T-Bills or Repo on Government Securities• Not permitted to invest in Short Term Deposits, and Structured Obligation (SO) or Credit Enhanced

instruments• Graded Exit Load shall be levied on Liquid Schemes up to a period of 7 days• All fresh investments to be in listed CP – Guidelines by SEBI awaited

• MTM: Valuation to completely based on mark to market (Amortization valuation dispensed)

• Sectoral Cap: Reduced from 25% to 20%. HFC cap of 15% to be restructured to 10% and 5% exposure in securitized debt based on retail housing loan and affordable housing portfolio

• Investments in Credit Enhanced instruments prescribed at 10% of debt portfolio of the respective scheme

• Security Cover: At least 4 times security cover for instruments with credit enhancements backed by equities directly or indirectly

• MF schemes mandated to invest only in listed NCDs and to be implemented in a phase manner

Vivriti Capital client base

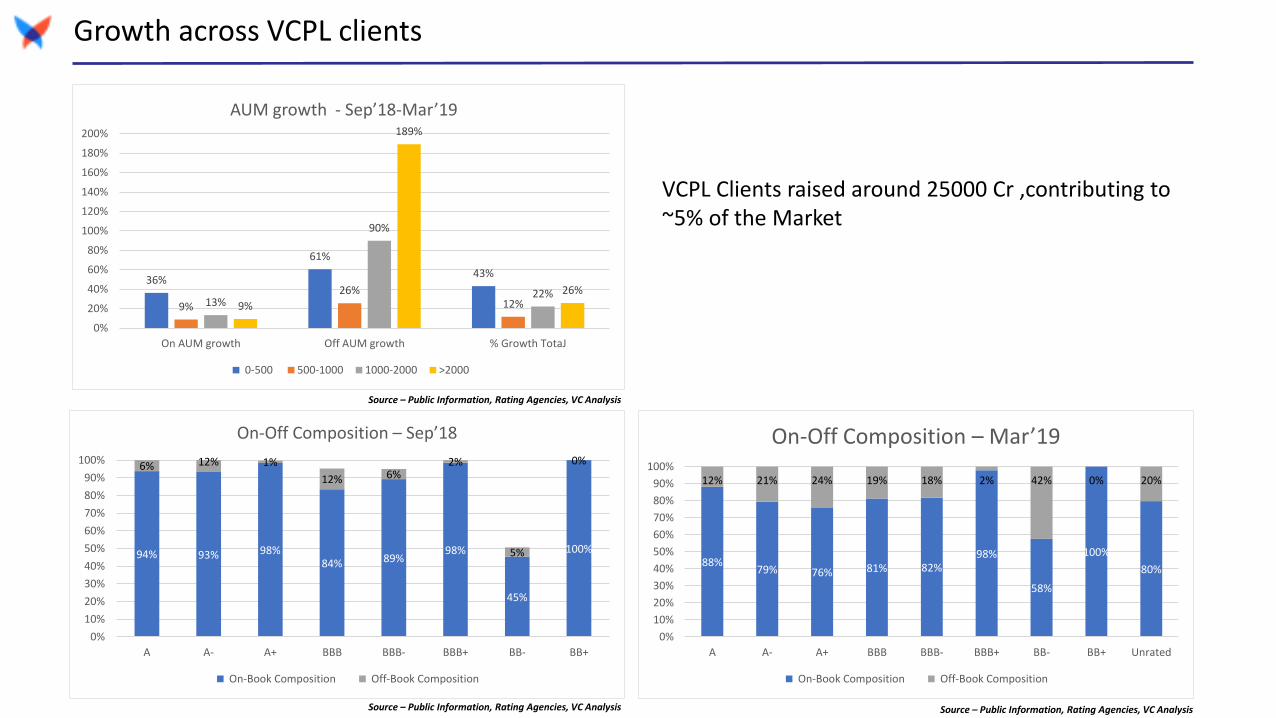

Growth across VCPL clients

36%

61%

43%

9%

26%12%13%

90%

22%9%

189%

26%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

On AUM growth Off AUM growth % Growth TotaJ

AUM growth - Sep’18-Mar’19

0-500 500-1000 1000-2000 >2000

94% 93% 98%84% 89%

98%

45%

100%

6% 12% 1%

12% 6%2%

5%

0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

A A- A+ BBB BBB- BBB+ BB- BB+

On-Off Composition – Sep’18

On-Book Composition Off-Book Composition

88%79% 76% 81% 82%

98%

58%

100%

80%

12% 21% 24% 19% 18% 2% 42% 0% 20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

A A- A+ BBB BBB- BBB+ BB- BB+ Unrated

On-Off Composition – Mar’19

On-Book Composition Off-Book Composition

VCPL Clients raised around 25000 Cr ,contributing to ~5% of the Market

Source – Public Information, Rating Agencies, VC Analysis

Source – Public Information, Rating Agencies, VC Analysis Source – Public Information, Rating Agencies, VC Analysis

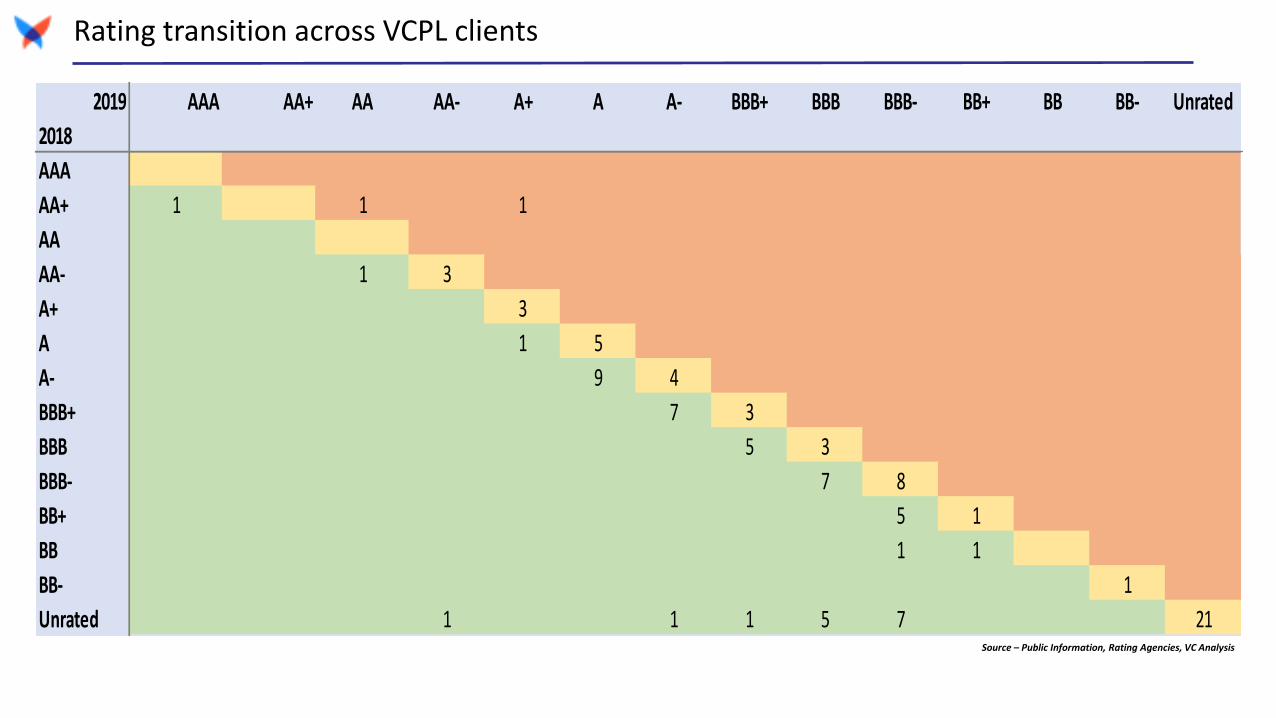

Rating transition across VCPL clients

2019 AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB+ BB BB- Unrated

2018

AAA

AA+ 1 1 1

AA

AA- 1 3

A+ 3

A 1 5

A- 9 4

BBB+ 7 3

BBB 5 3

BBB- 7 8

BB+ 5 1

BB 1 1

BB- 1

Unrated 1 1 1 5 7 21Source – Public Information, Rating Agencies, VC Analysis

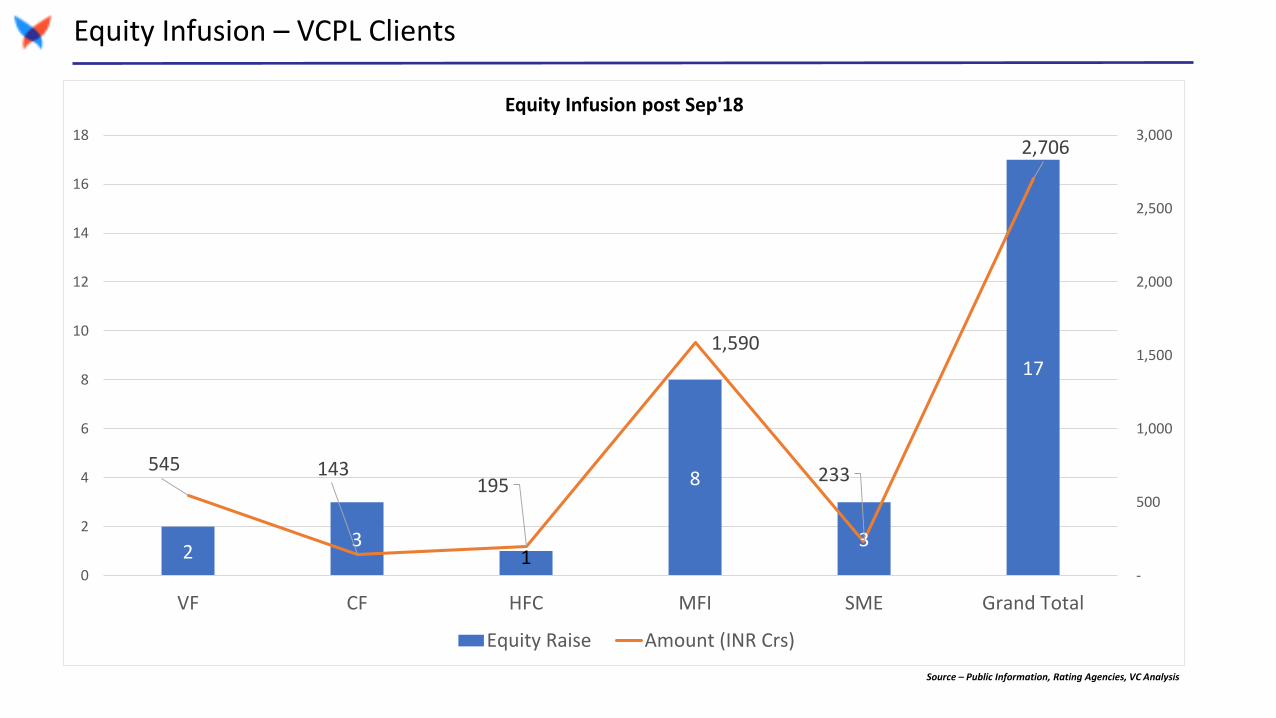

Equity Infusion – VCPL Clients

23

1

8

3

17

545 143 195

1,590

233

2,706

-

500

1,000

1,500

2,000

2,500

3,000

0

2

4

6

8

10

12

14

16

18

VF CF HFC MFI SME Grand Total

Equity Infusion post Sep'18

Equity Raise Amount (INR Crs)

Source – Public Information, Rating Agencies, VC Analysis

Outlook

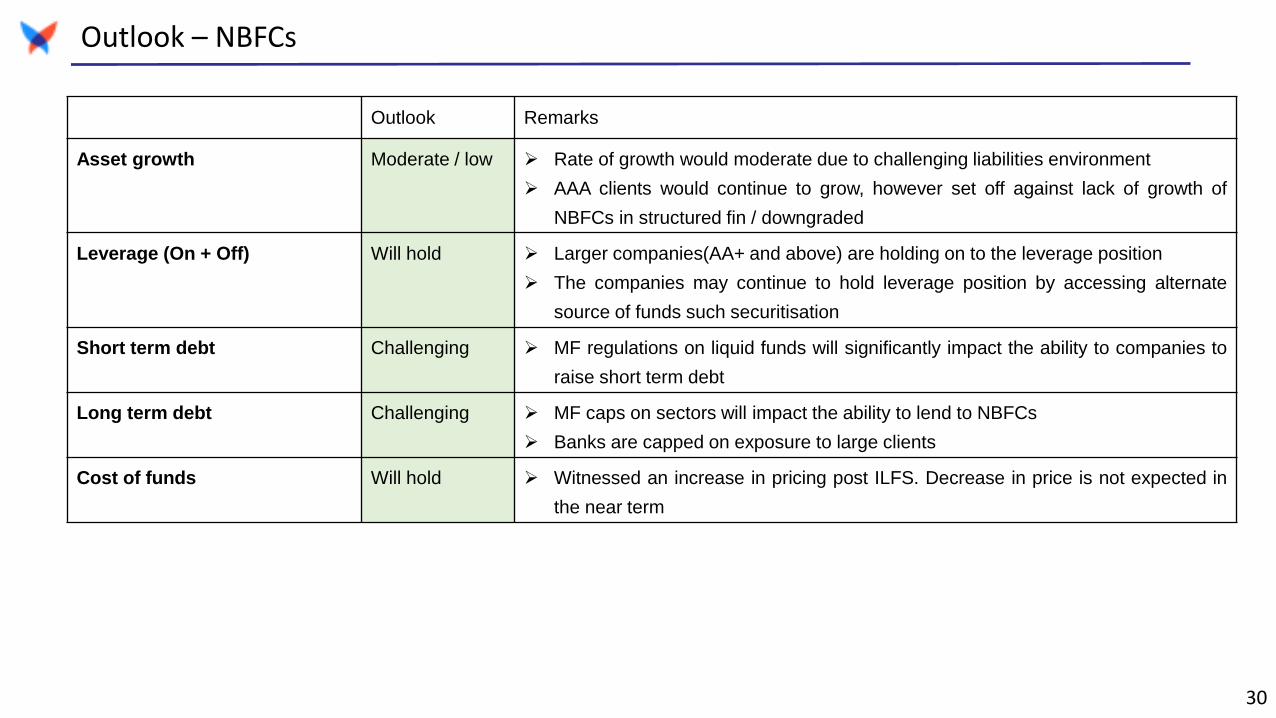

Outlook – NBFCs

30

Outlook Remarks

Asset growth Moderate / low ➢ Rate of growth would moderate due to challenging liabilities environment

➢ AAA clients would continue to grow, however set off against lack of growth of

NBFCs in structured fin / downgraded

Leverage (On + Off) Will hold ➢ Larger companies(AA+ and above) are holding on to the leverage position

➢ The companies may continue to hold leverage position by accessing alternate

source of funds such securitisation

Short term debt Challenging ➢ MF regulations on liquid funds will significantly impact the ability to companies to

raise short term debt

Long term debt Challenging ➢ MF caps on sectors will impact the ability to lend to NBFCs

➢ Banks are capped on exposure to large clients

Cost of funds Will hold ➢ Witnessed an increase in pricing post ILFS. Decrease in price is not expected in

the near term

Outlook – VCPL clients

31

Outlook Remarks

Asset growth Increase ➢ Asset growth fuelled by to equity infusion

Leverage Decrease ➢ Decrease due to equity infusion witnessed across sectors and increase in off

balance sheet transactions

➢ However, increasing % off balance sheet transactions may cap the ability to

securitize for few clients

Short term debt No access ➢ Never had access to short term debt

Long term debt Moderate ➢ Increase in rating due to equity infusion

➢ PSL tag increasing saleability of assets

Cost of funds Will hold ➢ Witnessed an increase in pricing post ILFS. Decrease in price is not expected in

the near term

Thank you