the only way is up - c.ymcdn.comc.ymcdn.com/sites/batterycouncil.org/resource/resmgr/2017... ·...

TRANSCRIPT

Neil Hawkes (CRU)

BCI Convention, Hyatt Regency, Jacksonville, Florida, USA

(2nd May 2017)

Global trends and issues in the lead market

The Only Way Is Up ?

1,000

1,500

2,000

2,500

3,000

Jan-0

9

Ma

r-0

9

Ma

y-0

9

Jul-0

9

Sep-0

9

No

v-0

9

Jan-1

0

Ma

r-1

0

Ma

y-1

0

Jul-1

0

Sep-1

0

No

v-1

0

Jan-1

1

Ma

r-1

1

Ma

y-1

1

Jul-1

1

Sep-1

1

No

v-1

1

Jan-1

2

Ma

r-1

2

Ma

y-1

2

Jul-1

2

Sep-1

2

No

v-1

2

Jan-1

3

Ma

r-1

3

Ma

y-1

3

Jul-1

3

Sep-1

3

No

v-1

3

Jan-1

4

Ma

r-1

4

Ma

y-1

4

Jul-1

4

Sep-1

4

No

v-1

4

Jan-1

5

Ma

r-1

5

Ma

y-1

5

Jul-1

5

Sep-1

5

No

v-1

5

Jan-1

6

Ma

r-1

6

Ma

y-1

6

Jul-1

6

Sep-1

6

No

v-1

6

Jan-1

7

Ma

r-1

7

$2,500/t

$2,000/t

Data: LME

LME 3-month lead price, daily ($/tonne)

Lead price rallies in 2H2016 to touch highs last seen in 2011

$1,700/t

80

100

120

140

160

180

200

Ja

n…

Fe

…

Ma

…

Apr…

Ma

…

Ju

n…

Ju

l-…

Au…

Se…

Oct…

No

…

De

…

Ja

n…

Fe

…

Ma

…

Apr…

Ma

…

Ju

n…

Ju

l-…

Au…

Se…

Oct…

No

…

De

…

Ja

n…

Fe

…

Ma

…

Apr…

Nickel

LME 3-months prices, index to 4th January 2016 = 100

Copper

Zinc

All LME metal prices lifting through 2016-2017, but zinc running

ahead of the chasing pack

AluminiumLead

Tin

Data: LME

• Combination of broader metal price drivers and lead-specific price drivers turning more positive over last

year or so

• Broader drivers - stronger US dollar trend starting to stall, Chinese slowdown levelling out, tightening

supply picture across metals

• Lead-specific drivers - steady (if not spectacular) demand growth, tighter global primary (mine)

availability, firmer inside China, tightening outlook outside China, smaller stock ‘iceberg’ already shrinking

What has been driving lead price renaissance ?

What’s the lead demand picture ?

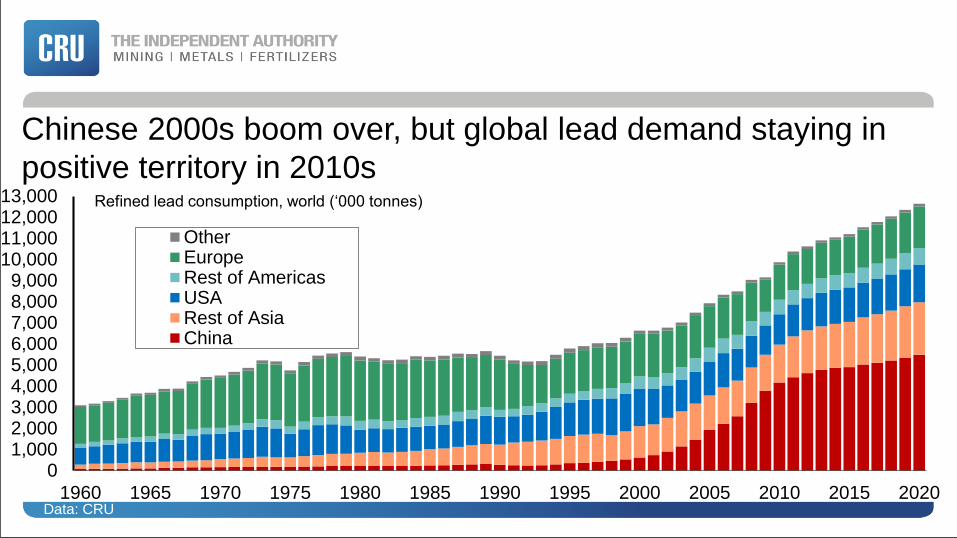

01,0002,0003,0004,0005,0006,0007,0008,0009,000

10,00011,00012,00013,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

OtherEuropeRest of AmericasUSARest of AsiaChina

Refined lead consumption, world (‘000 tonnes)

Chinese 2000s boom over, but global lead demand staying in

positive territory in 2010s

Data: CRU

01,0002,0003,0004,0005,0006,0007,0008,0009,000

10,00011,00012,00013,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Non-battery uses

Batteries - automotive & industrial

Refined lead consumption, world (‘000 tonnes)

Long-run rise in global lead demand intimately linked to growing

dominance of use in lead-acid batteries

Data: CRU

0

50

100

150

200

250

2013 2014 2015 2016 2017 2018 2019 2020

Non-ICE**

ICE*

Light vehicle production by powertrain, world (million units)

*ICE = Internal Combustion Engine vehicle, includes ‘stop-start’ vehicles

**Non-ICE = HEVs, EVs and Fuel Cell ‘new technology ‘vehicles.

Majority of new vehicles are ‘conventional’ (ICE) rather than ‘new

technology’ (non-ICE), though latter’s share is rising

2.3% 2.7% 2.8%3.7% 6.2% 7.6% 8.8%% shown are ‘Non-ICE’ as % of total

4.7%

Data: LMC Automotive

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014 2015 2016 2017 2018 2019 2020

Excluding stop-start

Including stop-start

32%

18%22% 26%

36% 39% 42%

‘Stop-start’ vehicles as % of ICE* vehicle production, global

‘Stop-start’ vehicles rising to account for over 40% of all new

vehicles produced globally in 2020

29%

Data: LMC Automotive Note: *ICE = Internal Combustion-Engine vehicle

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Steadier ‘normal’ global lead demand growth in 2010s compared

to earlier Chinese-boom fuelled yearsRefined lead consumption, world (‘000 tonnes) % year-on-year change

2.4% per year (1960-2016)

Data: CRU

What’s happening in lead production ?

• Before the recent lift in metal prices, lower earlier values prompted lead-producing polymetallic mine cuts (led by

Glencore), alongside well-flagged ‘running out of ore’ mine cuts (e.g. Century)

• 2016 marked another drop in global mine output (led by Australia), alongside higher primary smelter demand (led

by Korea Zinc) resulting in a marked tightening in global lead concentrate availability

• So long-standing scramble for scrap has been joined by harder fight for lead concentrate

• Now waiting for response of polymetallic mines to higher metal prices and lower TCs, including reversal of price-

related mine cuts

• Having drained excess feed, primary smelter production path to more closely follow ‘fresh’ mine production this

year and beyond

• Unlike in other metals, impact of primary production path will be diluted by the importance of secondary supplies

that will continue to grow

Slower primary supplies diluted in lead by importance of rising

secondary supplies

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Lead Copper Zinc

Primary

Secondary

10%17%

Secondary and primary production as % of total, world - 2016

Secondary production far more important in lead than in copper

or zinc

Data: CRU

60%

• Further steady growth in lead demand to ensure further steady growth in scrap supplies

• Alongside high recycling rates and sufficient smelter capacity, secondary lead production to remain the main driver

of global supply growth

• Main issue in secondary lead industry remains one of the ongoing fight for scrap share

• US lead recycling dominated by main lead-acid battery makers, through own smelters or tolling

• New entrant Aqua ramping up new technology Reno facility - need to show can recycle at lower costs and

emissions than existing conventional secondary smelters

• Resolution to entrenched problem of excess lead recycling capacity in Europe remains elusive. EC scrap fines for 3

lead recyclers - Eco-Bat, Campine and Recylex

• Environmental clampdown and more organised scrap collection in China re-directing more scrap away from informal

small-scale operators towards more modern, cleaner and larger-size lead recyclers

• Still too many smelters chasing the scrap pool available around the world inevitably leads to higher scrap prices and

higher scrap flows, both within regions and between regions

Secondary lead industry trends and issues

-300

-200

-100

0

100

200

300

400

500

600

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1990 1995 2000 2005 2010 2015 2020

Year-on-year change - secondary (RHS)

Year-on-year change - primary (RHS)

Total - primary (LHS)

Total - secondary (LHS)

Global secondary production typically bigger growth in contrast to

more erratic global primary pictureRefined lead production, world (‘000 tonnes) year-on-year change (‘000t lead)

Data: CRU

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Steadier ‘normal’ global lead output growth in 2010s compared to

earlier Chinese-boom fuelled yearsRefined lead production, world (‘000 tonnes) % year-on-year change

2.3% per year (1960-2016)

Data: CRU

What’s the supply/demand balance picture ?

-250

-200

-150

-100

-50

0

50

100

150

200

250

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Balance (RHS)

Production

Consumption

Refined lead balance, world (‘000t)

Pulling demand and supply together, lead surplus shrinks

before moving into deficit

Refined lead consumption/production, world (‘000t)

Data: CRU

-250

-200

-150

-100

-50

0

50

100

150

200

250

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Balance outside China

Balance inside China

World outside China joining already tighter lead market inside

China this year, most of early 2010s surplus ‘ex-China’

Refined lead – market balance (‘000 tonnes)

Data: CRU

-200

-150

-100

-50

0

50

100

150

200

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 1Q2017

Reported

Implied unreported*

Refined lead stocks, world year-on-year change (‘000 tonnes, year-end)

Smaller stock ‘iceberg’ already ‘melting’?

* Derived from difference between change in reported stocks and market balance

Data: CRU, ILZSG, LME, SHFE

What path lies ahead for lead prices ?

0

500

1,000

1,500

2,000

2,500

3,000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Tick up in lead prices, but longer-term trend still down from 2007

peak

LME 3-months price - $ of the day (nominal terms)

LME 3-months price - 2016$ (real terms)

$2,000/t

$500/t - old 1900s ‘long-term floor’

LME 3-month price , nominal/real terms, annual average ($/tonne lead)

$1,800/t

Data: LME, CRU

• Still room for reasonably robust lead demand growth, helped by LAB usage in ‘stop-start’ vehicles

• Worst over for adjustment in China - orderly transition to slower growth path

• Tighter raw material feed (concentrates joining scrap) restraining smelter production - future primary growth path

less certain than secondary growth path. Mine project pipeline zinc-rich and lead-poor

• Switch into deficit - scope for error could see bigger shortfalls drawing down from smaller stockpiles

• Not just size of lead stock ‘iceberg’ - composition (‘use-ability’) and rate of ‘drip feed’ to the market will be key in

determining lead price path ahead

• More favourable ‘external’ drivers - more bullish outlook for other metals, notably zinc; US dollar rally running out

of steam. Lead swept higher by wider rally in zinc and other metal prices

• LME lead price already taken a step up into low $2,000s from high $1,000s - greater volatility as market tries to

work out ‘real v fake’ improvements in underlying lead market dynamics

• November 2016 high in $2,500s provides first upside target - next is 2011 high of around $2,850/t - 2007 record of

nearly $4,000/t still seems out of reach

The only way is up...

• More political and geopolitical events could blow metals off course – 2017 European elections, ‘Brexit’ process,

less conventional Trump administration, more assertive Russia, Middle East war/tensions, maverick North

Korea, more ‘surprises’ (unknown unknowns)...

• US and Chinese spending sprees disappoint - slower world economic growth and slower metals demand growth

• Underestimating rising threat to LAB dominance from alternative battery chemistries, notably LIBs on vehicle

electrification path. Chinese government moves faster down this path

• Higher metal prices (lower TCs) triggers swifter/greater polymetallic mine response than expected

• January 2017 removal of Chinese 10% export tax had been successful tool in slowing Chinese lead exports to a

trickle - could they lift again ?

• Less tight lead market (weaker demand/better supplies) and renewed investor caution could see LME lead price

struggle to sustain further steps higher

• Even struggle to hold recent gains back up into low $2,000s - instead falls back into previous high $1,000s

trading - next downside targets late 2015 lows in $1,500s then late 2008/early 2009 lows (dip below $1,000/t)

...or is it ?

Time for reflection and any questions...

Neil Hawkes

Lead market analyst (CRU)

T +44 20 7903 2101

W www.crugroup.com

BCI Convention, Hyatt Regency, Jacksonville, Florida, USA (2nd May 2017)