the ott-video services market

TRANSCRIPT

THE OTT-VIDEO SERVICES MARKETTODAY’S TRENDS AND WHAT IS NEXT FOR 4K, HDR, HFR & VR

By Tim Siglin, Contributing Editor, Streaming Media magazine, and Co-founder & Principal Analyst, Transitions, Inc.

Produced by Streaming Media magazine and Unisphere Research, a Division of Information Today, Inc. May 2016

Sponsored by

2

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

TABLE OF CONTENTS

INTRODUCTION �������������������������������������������������������������������������������������������������������������������������������3

IS OTT A VIABLE REVENUE OPPORTUNITY? �����������������������������������������������������������������������������������5

WHY OFFER OTT SERVICES? �����������������������������������������������������������������������������������������������������������7

WHAT CHALLENGES DO OTT PROVIDERS FACE? ���������������������������������������������������������������������������8

MONETIZING, SCALING, AND SECURING CONTENT ���������������������������������������������������������������������9

WHAT DOES THE FUTURE HOLD, I WONDER �������������������������������������������������������������������������������11

SUMMARY �������������������������������������������������������������������������������������������������������������������������������������14

ABOUT LEVEL 3 ������������������������������������������������������������������������������������������������������������������������������14

3

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

INTRODUCTION

“CDN services are hot,” a CDN vendor recently told me, “but OTT Video Services are even hotter.”

How hot is the OTT Video Services market? Hulu recently announced an annualized growth rate of more than 30% year-over-year, and is now nearing 12 million paid subscribers; Netflix has in excess of 75 million subscribers, and is available in almost 200 countries worldwide; and Amazon has almost 50 million Prime members, all of which have access to original and licensed video on-demand (VOD) OTT content as part of their memberships.

Even beyond this Big 3 of OTT, though, there are hundreds of OTT providers, catering to various niches. Whether building a base of OTT subscribers around user-generated content (UGC), linear channel OTT as part of the “TV Everywhere” initiatives, or even live event OTT pay-per-view or event models, OTT providers serve the needs of viewers across the content spectrum.

To properly assess the potential of OTT, one needs to understand that OTT comes in a variety of device types and services.

In the past, due to both device and delivery limitations, most OTT was a way to deliver on-demand content—those file-based assets that cover everything from cat videos to premium movie and television episodes.

OTT customers watched on-demand content and catch-up services on their laptops, which gave way to streaming set-top boxes (STBs) and internet streaming “sticks,” which in turn gave way to higher numbers of consumption minutes for smartphones and tablets.

In addition, content in 4K (UltraHD, or the newer high-dynamic-range UltraHD Premium) is becoming mainstream, as is high-frame-rate 1080p content. Even emerging content formats such as VR-video show promise, as borne out in responses to this year’s survey, sponsored by Level 3 Communications and Streaming Media magazine.

During the course of survey response analysis for last year’s OTT report—“Over-The-Top Video Delivery: Challenges And Opportunities For Global OTT Service Providers,” sponsored by Level 3—we noticed a number of emerging trends that seemed to

indicate interest in both new services that can’t be delivered by a traditional over-the-air broadcast infrastructure as well as a desire in the OTT community to increase quality.

Building on that insight, we expanded this year’s Level 3-sponsored survey to explore several of these emerging trends, testing which of them appear to have longevity and which appear to be flash but no fire.

We asked respondents to examine OTT from a variety of angles, ranging from business and technology challenges to the competitive challenges and revenue viability of offering OTT services.

Along the way, survey takers—both the key number of respondents working in OTT today, as well as the larger group who are exploring OTT opportunities—provided insights into trends and opportunities.

After eliminating a number of partial answers, Transitions analyzed 628 survey responses. We were able to then further sort the responses into two groups: those who currently offer OTT services, and those who do not.

Almost 45% of respondents, or 280 of our 628 survey takers, indicated their companies offer OTT services today. It’s interesting to note that only 35% of last year’s survey respondents offered OTT services, which potentially indicates a growing adoption trend since Streaming Media surveys attract a high number of respondents from within the streaming media and OTT industry.

The 45% response rate for those offering OTT services gave us a solid footing on which to explore the differences between those thinking of adding OTT services and those that already have done so.

In keeping with last year’s survey respondents, in which 13% of respondents said their companies were part of a larger media group, this year’s numbers are slightly higher, with 15% of respondents working for a company that’s part of a larger media group and not part of an independent media firm, enterprise, or educational institution.

4

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

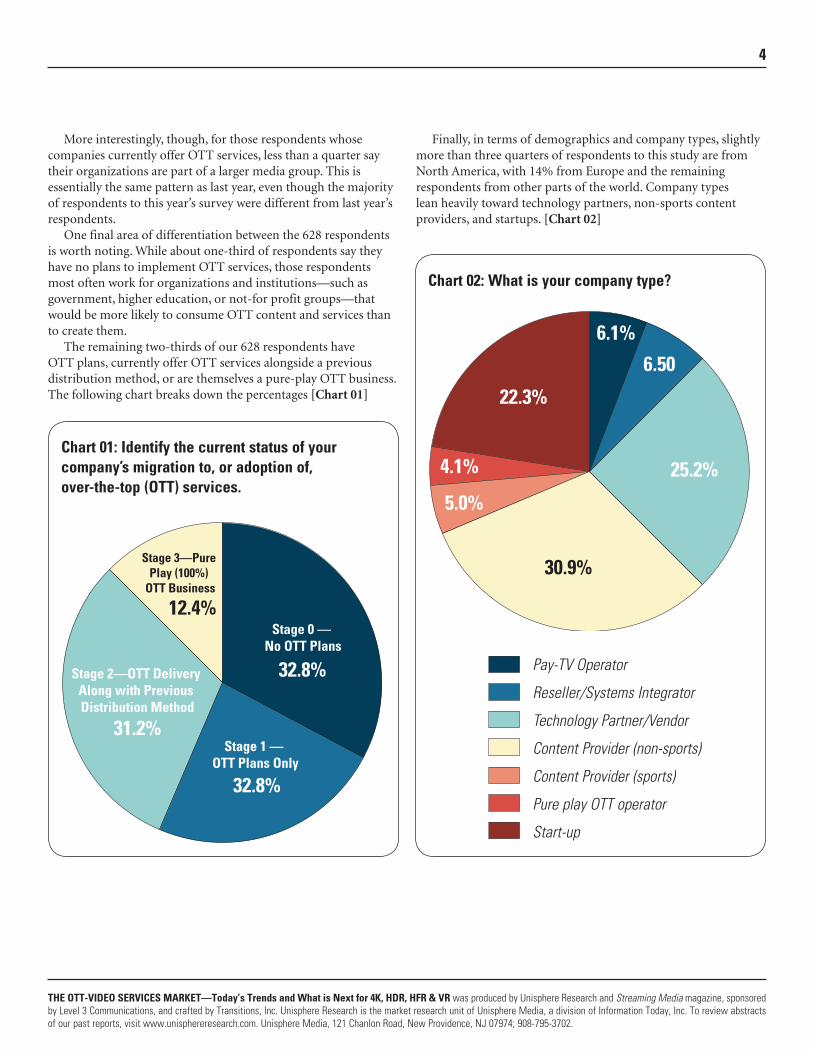

More interestingly, though, for those respondents whose companies currently offer OTT services, less than a quarter say their organizations are part of a larger media group. This is essentially the same pattern as last year, even though the majority of respondents to this year’s survey were different from last year’s respondents.

One final area of differentiation between the 628 respondents is worth noting. While about one-third of respondents say they have no plans to implement OTT services, those respondents most often work for organizations and institutions—such as government, higher education, or not-for profit groups—that would be more likely to consume OTT content and services than to create them.

The remaining two-thirds of our 628 respondents have OTT plans, currently offer OTT services alongside a previous distribution method, or are themselves a pure-play OTT business. The following chart breaks down the percentages [Chart 01]

Finally, in terms of demographics and company types, slightly more than three quarters of respondents to this study are from North America, with 14% from Europe and the remaining respondents from other parts of the world. Company types lean heavily toward technology partners, non-sports content providers, and startups. [Chart 02]

Chart 02: What is your company type?

22.3%

4.1%

5.0%

30.9%

25.2%

6.50

6.1%

Pay-TV Operator

Reseller/Systems Integrator

Technology Partner/Vendor

Content Provider (non-sports)

Content Provider (sports)

Pure play OTT operator

Start-up

Chart 01: Identify the current status of your company’s migration to, or adoption of, over-the-top (OTT) services.

Stage 3—Pure Play (100%)

OTT Business

Stage 2—OTT Delivery Along with Previous Distribution Method

Stage 1 — OTT Plans Only

Stage 0 — No OTT Plans

31.2%

12.4%

32.8%

32.8%

22.3%

4.1%

5.0%

30.9%

25.2%

6.50

6.1%

5

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

IS OTT A VIABLE REVENUE OPPORTUNITY?

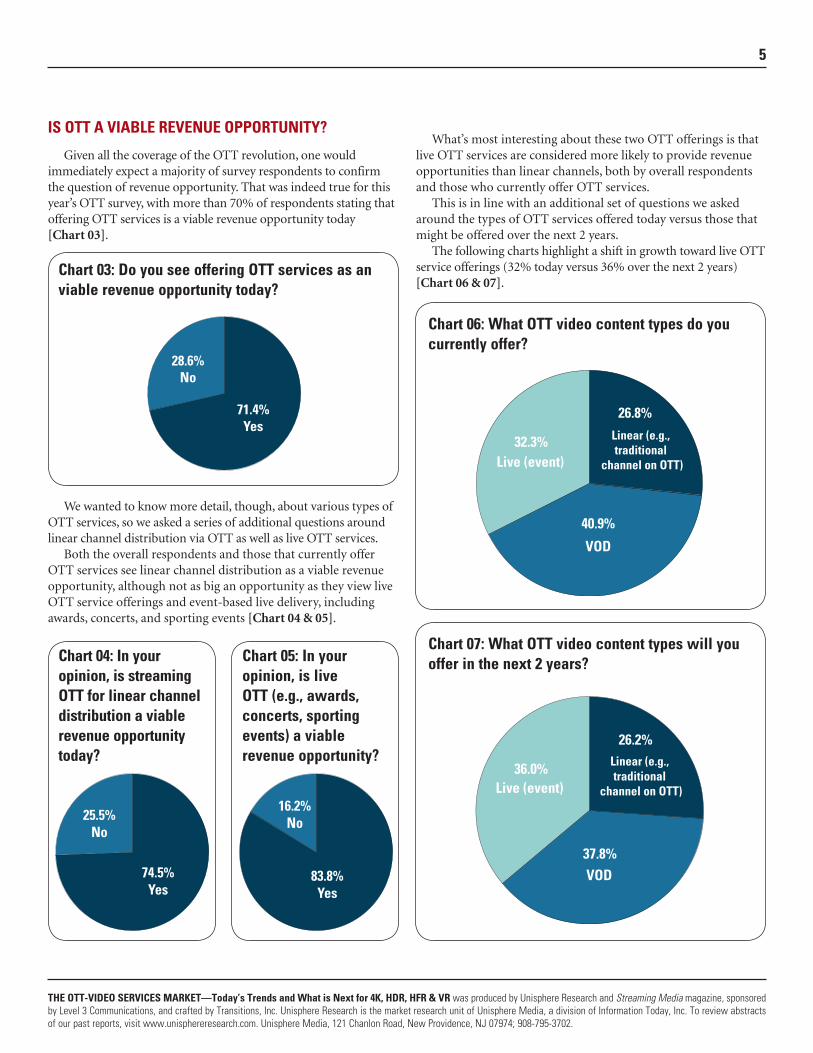

Given all the coverage of the OTT revolution, one would immediately expect a majority of survey respondents to confirm the question of revenue opportunity. That was indeed true for this year’s OTT survey, with more than 70% of respondents stating that offering OTT services is a viable revenue opportunity today [Chart 03].

We wanted to know more detail, though, about various types of OTT services, so we asked a series of additional questions around linear channel distribution via OTT as well as live OTT services.

Both the overall respondents and those that currently offer OTT services see linear channel distribution as a viable revenue opportunity, although not as big an opportunity as they view live OTT service offerings and event-based live delivery, including awards, concerts, and sporting events [Chart 04 & 05].

What’s most interesting about these two OTT offerings is that live OTT services are considered more likely to provide revenue opportunities than linear channels, both by overall respondents and those who currently offer OTT services.

This is in line with an additional set of questions we asked around the types of OTT services offered today versus those that might be offered over the next 2 years.

The following charts highlight a shift in growth toward live OTT service offerings (32% today versus 36% over the next 2 years) [Chart 06 & 07].

Chart 03: Do you see offering OTT services as an viable revenue opportunity today?

Chart 05: In your opinion, is live OTT (e.g., awards, concerts, sporting events) a viable revenue opportunity?

Chart 06: What OTT video content types do you currently offer?

Chart 04: In your opinion, is streaming OTT for linear channel distribution a viable revenue opportunity today?

Chart 07: What OTT video content types will you offer in the next 2 years?

28.6%No

71.4%Yes

25.5%No

74.5%Yes

28.6%No

16.2%No

83.8%Yes

28.6%No

Live (event)

VOD

Linear (e.g., traditional

channel on OTT)

12.4%26.8%

32.3%

40.9%

Live (event)

VOD

Linear (e.g., traditional

channel on OTT)

12.4%26.2%

36.0%

37.8%

6

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

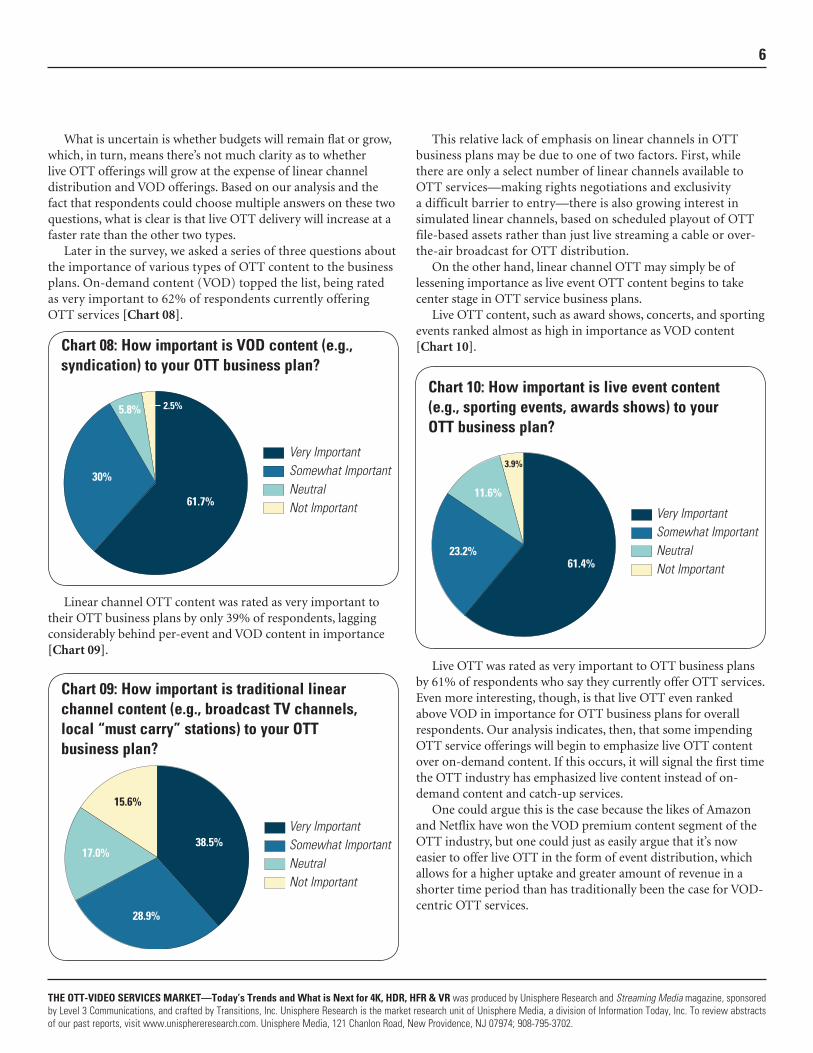

What is uncertain is whether budgets will remain flat or grow, which, in turn, means there’s not much clarity as to whether live OTT offerings will grow at the expense of linear channel distribution and VOD offerings. Based on our analysis and the fact that respondents could choose multiple answers on these two questions, what is clear is that live OTT delivery will increase at a faster rate than the other two types.

Later in the survey, we asked a series of three questions about the importance of various types of OTT content to the business plans. On-demand content (VOD) topped the list, being rated as very important to 62% of respondents currently offering OTT services [Chart 08].

Linear channel OTT content was rated as very important to their OTT business plans by only 39% of respondents, lagging considerably behind per-event and VOD content in importance [Chart 09].

This relative lack of emphasis on linear channels in OTT business plans may be due to one of two factors. First, while there are only a select number of linear channels available to OTT services—making rights negotiations and exclusivity a difficult barrier to entry—there is also growing interest in simulated linear channels, based on scheduled playout of OTT file-based assets rather than just live streaming a cable or over-the-air broadcast for OTT distribution.

On the other hand, linear channel OTT may simply be of lessening importance as live event OTT content begins to take center stage in OTT service business plans.

Live OTT content, such as award shows, concerts, and sporting events ranked almost as high in importance as VOD content [Chart 10].

Live OTT was rated as very important to OTT business plans by 61% of respondents who say they currently offer OTT services. Even more interesting, though, is that live OTT even ranked above VOD in importance for OTT business plans for overall respondents. Our analysis indicates, then, that some impending OTT service offerings will begin to emphasize live OTT content over on-demand content. If this occurs, it will signal the first time the OTT industry has emphasized live content instead of on-demand content and catch-up services.

One could argue this is the case because the likes of Amazon and Netflix have won the VOD premium content segment of the OTT industry, but one could just as easily argue that it’s now easier to offer live OTT in the form of event distribution, which allows for a higher uptake and greater amount of revenue in a shorter time period than has traditionally been the case for VOD-centric OTT services.

Chart 08: How important is VOD content (e.g., syndication) to your OTT business plan?

Chart 10: How important is live event content (e.g., sporting events, awards shows) to your OTT business plan?

Very ImportantSomewhat ImportantNeutralNot Important

2.5%5.8%

30%

61.7%Very ImportantSomewhat ImportantNeutralNot Important

3.9%

11.6%

23.2%61.4%

61.7%

Very ImportantSomewhat ImportantNeutralNot Important

15.6%

17.0%

28.9%

38.5%

61.7%

Chart 09: How important is traditional linear channel content (e.g., broadcast TV channels, local “must carry” stations) to your OTT business plan?

7

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

WHY OFFER OTT SERVICES?

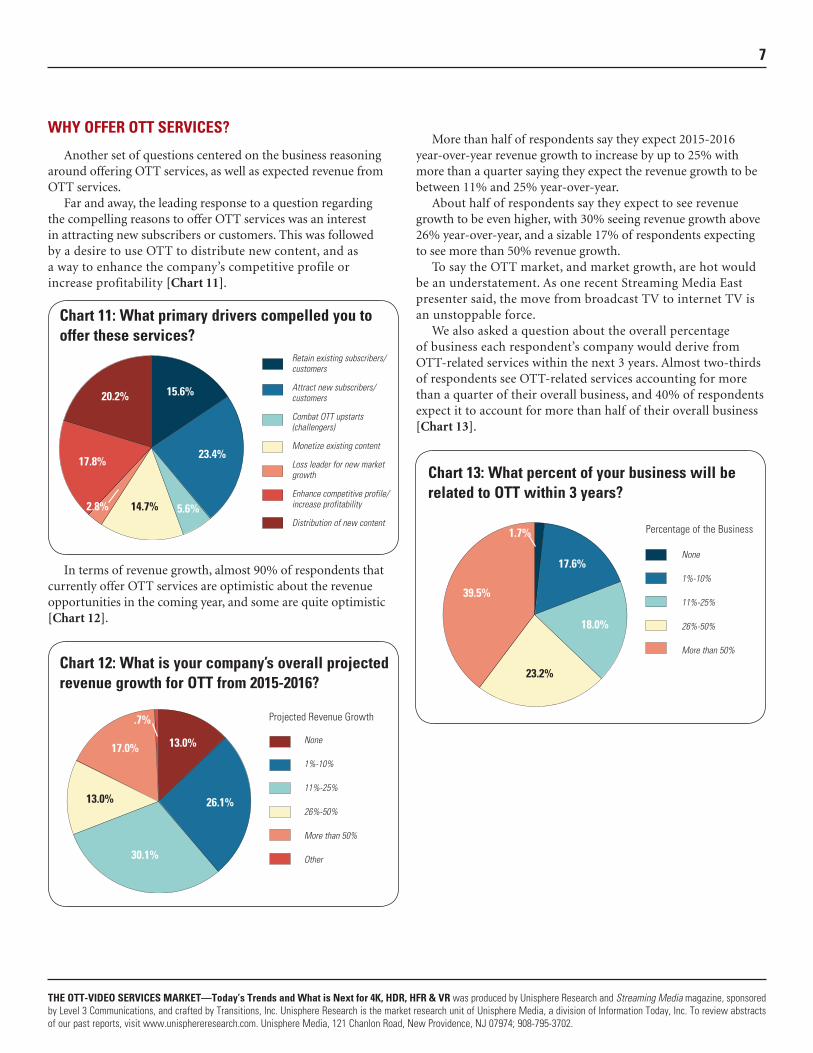

Another set of questions centered on the business reasoning around offering OTT services, as well as expected revenue from OTT services.

Far and away, the leading response to a question regarding the compelling reasons to offer OTT services was an interest in attracting new subscribers or customers. This was followed by a desire to use OTT to distribute new content, and as a way to enhance the company’s competitive profile or increase profitability [Chart 11].

In terms of revenue growth, almost 90% of respondents that currently offer OTT services are optimistic about the revenue opportunities in the coming year, and some are quite optimistic [Chart 12].

More than half of respondents say they expect 2015-2016 year-over-year revenue growth to increase by up to 25% with more than a quarter saying they expect the revenue growth to be between 11% and 25% year-over-year.

About half of respondents say they expect to see revenue growth to be even higher, with 30% seeing revenue growth above 26% year-over-year, and a sizable 17% of respondents expecting to see more than 50% revenue growth.

To say the OTT market, and market growth, are hot would be an understatement. As one recent Streaming Media East presenter said, the move from broadcast TV to internet TV is an unstoppable force.

We also asked a question about the overall percentage of business each respondent’s company would derive from OTT-related services within the next 3 years. Almost two-thirds of respondents see OTT-related services accounting for more than a quarter of their overall business, and 40% of respondents expect it to account for more than half of their overall business [Chart 13].

Chart 11: What primary drivers compelled you to offer these services?

Chart 12: What is your company’s overall projected revenue growth for OTT from 2015-2016?

Retain existing subscribers/customers

Attract new subscribers/customers

Combat OTT upstarts (challengers)

Monetize existing content

Loss leader for new market growth

Enhance competitive profile/increase profitability

Distribution of new content

20.2%

17.8%

2.8% 14.7% 5.6%

23.4%

15.6%

6.1%

Chart 13: What percent of your business will be related to OTT within 3 years?

None

1%-10%

11%-25%

26%-50%

More than 50%

Other

.7%

17.0%

13.0%

30.1%

26.1%

13.0%

6.1%Projected Revenue Growth

None

1%-10%

11%-25%

26%-50%

More than 50%

39.5%

23.2%

18.0%

17.6%

1.7% 6.1%Percentage of the Business

8

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

WHAT CHALLENGES DO OTT PROVIDERS FACE?

For all the rosy pictures around revenue growth, however, the OTT provider still faces several primary business and technical challenges.

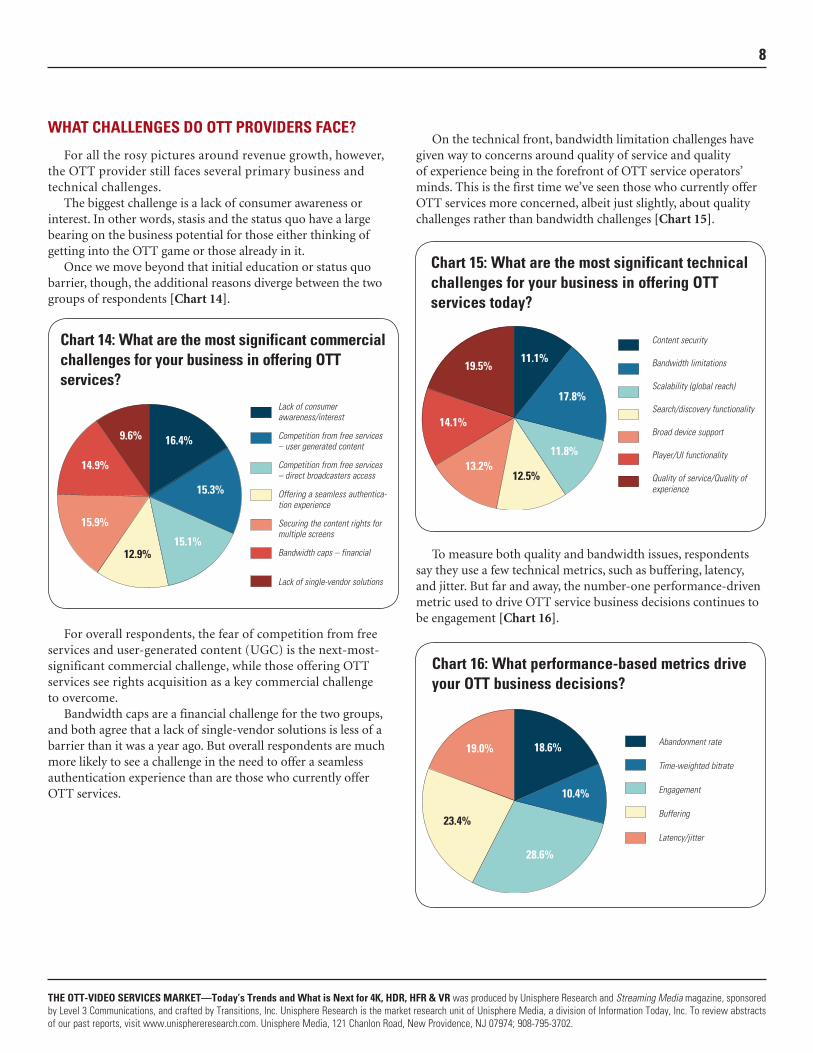

The biggest challenge is a lack of consumer awareness or interest. In other words, stasis and the status quo have a large bearing on the business potential for those either thinking of getting into the OTT game or those already in it.

Once we move beyond that initial education or status quo barrier, though, the additional reasons diverge between the two groups of respondents [Chart 14].

For overall respondents, the fear of competition from free services and user-generated content (UGC) is the next-most-significant commercial challenge, while those offering OTT services see rights acquisition as a key commercial challenge to overcome.

Bandwidth caps are a financial challenge for the two groups, and both agree that a lack of single-vendor solutions is less of a barrier than it was a year ago. But overall respondents are much more likely to see a challenge in the need to offer a seamless authentication experience than are those who currently offer OTT services.

On the technical front, bandwidth limitation challenges have given way to concerns around quality of service and quality of experience being in the forefront of OTT service operators’ minds. This is the first time we’ve seen those who currently offer OTT services more concerned, albeit just slightly, about quality challenges rather than bandwidth challenges [Chart 15].

To measure both quality and bandwidth issues, respondents say they use a few technical metrics, such as buffering, latency, and jitter. But far and away, the number-one performance-driven metric used to drive OTT service business decisions continues to be engagement [Chart 16].

Abandonment rate

Time-weighted bitrate

Engagement

Buffering

Latency/jitter

19.0%

23.4%

28.6%

10.4%

18.6%

6.1%

Chart 14: What are the most significant commercial challenges for your business in offering OTT services?

Chart 15: What are the most significant technical challenges for your business in offering OTT services today?

Chart 16: What performance-based metrics drive your OTT business decisions?

Lack of consumer awareness/interest

Competition from free services – user generated content

Competition from free services – direct broadcasters access

Offering a seamless authentica-tion experience

Securing the content rights for multiple screens

Bandwidth caps – financial

Lack of single-vendor solutions

9.6%

14.9%

15.9%

12.9%15.1%

15.3%

16.4%

6.1%

9.6%

14.9%

15.9%

12.9%15.1%

15.3%

16.4%

6.1%

Content security

Bandwidth limitations

Scalability (global reach)

Search/discovery functionality

Broad device support

Player/UI functionality

Quality of service/Quality of experience

19.5%

14.1%

13.2%12.5%

11.8%

17.8%

11.1%

6.1%

19.5%

14.1%

13.2%12.5%

11.8%

17.8%

11.1%

6.1%

9

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

MONETIZING, SCALING, AND SECURING CONTENT

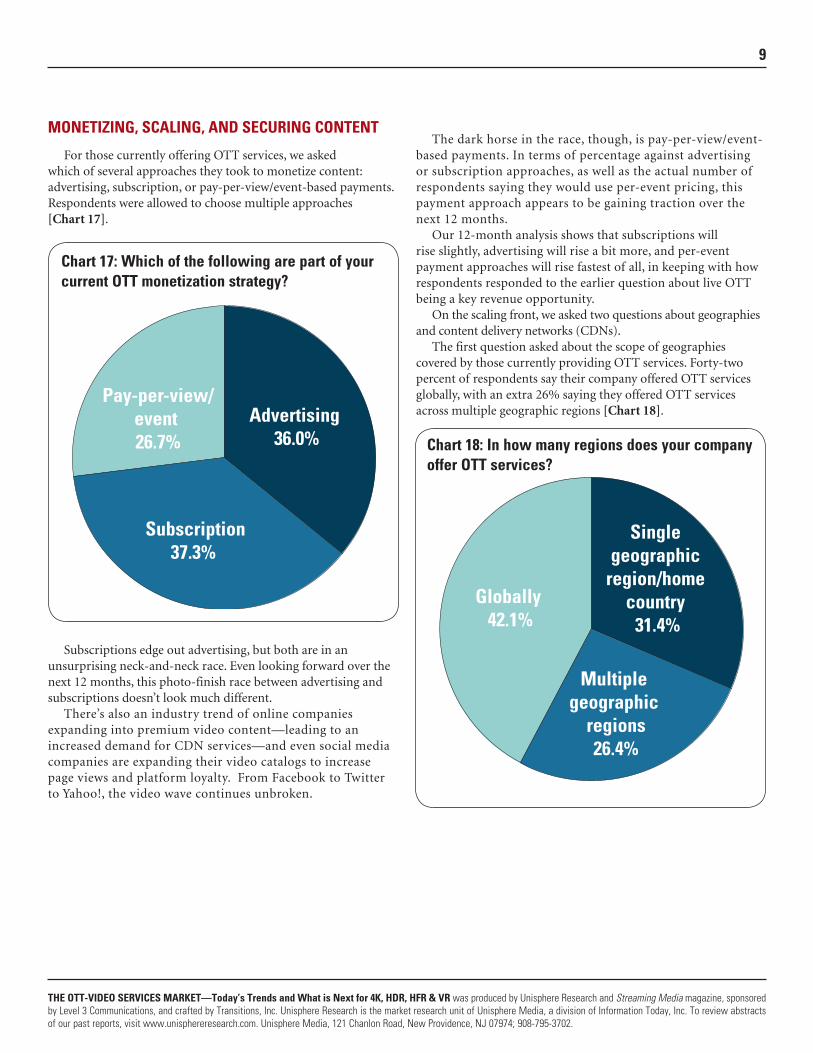

For those currently offering OTT services, we asked which of several approaches they took to monetize content: advertising, subscription, or pay-per-view/event-based payments. Respondents were allowed to choose multiple approaches [Chart 17].

Subscriptions edge out advertising, but both are in an unsurprising neck-and-neck race. Even looking forward over the next 12 months, this photo-finish race between advertising and subscriptions doesn’t look much different.

There’s also an industry trend of online companies expanding into premium video content—leading to an increased demand for CDN services—and even social media companies are expanding their video catalogs to increase page views and platform loyalty. From Facebook to Twitter to Yahoo!, the video wave continues unbroken.

The dark horse in the race, though, is pay-per-view/event-based payments. In terms of percentage against advertising or subscription approaches, as well as the actual number of respondents saying they would use per-event pricing, this payment approach appears to be gaining traction over the next 12 months.

Our 12-month analysis shows that subscriptions will rise slightly, advertising will rise a bit more, and per-event payment approaches will rise fastest of all, in keeping with how respondents responded to the earlier question about live OTT being a key revenue opportunity.

On the scaling front, we asked two questions about geographies and content delivery networks (CDNs).

The first question asked about the scope of geographies covered by those currently providing OTT services. Forty-two percent of respondents say their company offered OTT services globally, with an extra 26% saying they offered OTT services across multiple geographic regions [Chart 18].

Pay-per-view/event 26.7%

Subscription37.3%

Advertising 36.0%

12.4%

Globally 42.1%

Multiple geographic

regions26.4%

Single geographic

region/home country

31.4%

12.4%

Chart 17: Which of the following are part of your current OTT monetization strategy?

Chart 18: In how many regions does your company offer OTT services?

10

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

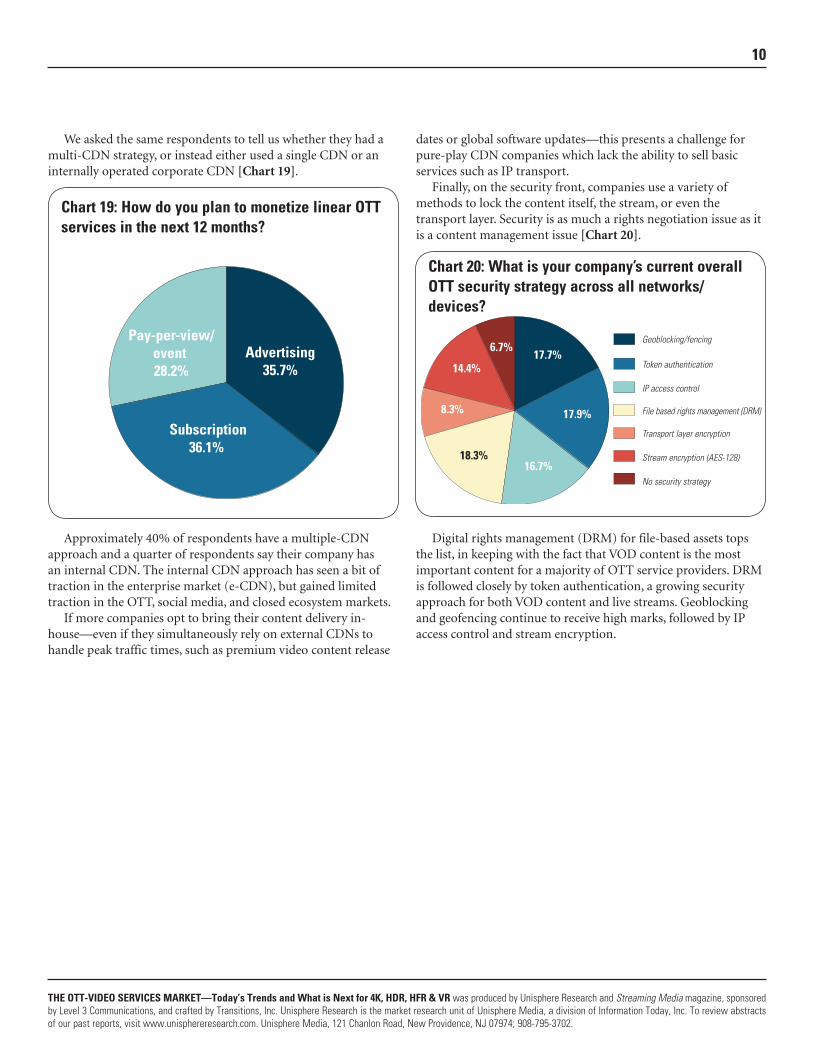

We asked the same respondents to tell us whether they had a multi-CDN strategy, or instead either used a single CDN or an internally operated corporate CDN [Chart 19].

Approximately 40% of respondents have a multiple-CDN approach and a quarter of respondents say their company has an internal CDN. The internal CDN approach has seen a bit of traction in the enterprise market (e-CDN), but gained limited traction in the OTT, social media, and closed ecosystem markets.

If more companies opt to bring their content delivery in-house—even if they simultaneously rely on external CDNs to handle peak traffic times, such as premium video content release

dates or global software updates—this presents a challenge for pure-play CDN companies which lack the ability to sell basic services such as IP transport.

Finally, on the security front, companies use a variety of methods to lock the content itself, the stream, or even the transport layer. Security is as much a rights negotiation issue as it is a content management issue [Chart 20].

Digital rights management (DRM) for file-based assets tops the list, in keeping with the fact that VOD content is the most important content for a majority of OTT service providers. DRM is followed closely by token authentication, a growing security approach for both VOD content and live streams. Geoblocking and geofencing continue to receive high marks, followed by IP access control and stream encryption.

Pay-per-view/event 28.2%

Subscription36.1%

Advertising35.7%

12.4%

Chart 19: How do you plan to monetize linear OTT services in the next 12 months?

Chart 20: What is your company’s current overall OTT security strategy across all networks/devices?

Geoblocking/fencing

Token authentication

IP access control

File based rights management (DRM)

Transport layer encryption

Stream encryption (AES-128)

No security strategy

6.7%

14.4%

8.3%

18.3%16.7%

17.9%

17.7%

6.1%

6.7%

14.4%

8.3%

18.3%16.7%

17.9%

17.7%

6.1%

11

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

WHAT DOES THE FUTURE HOLD, I WONDER…

OTT providers are in an enviable position of being able to rapidly deploy and test new video technologies and formats, especially compared to their cable and satellite counterparts. This capability can provide for differentiation, viral publicity, credibility, and also help attract new subscribers.

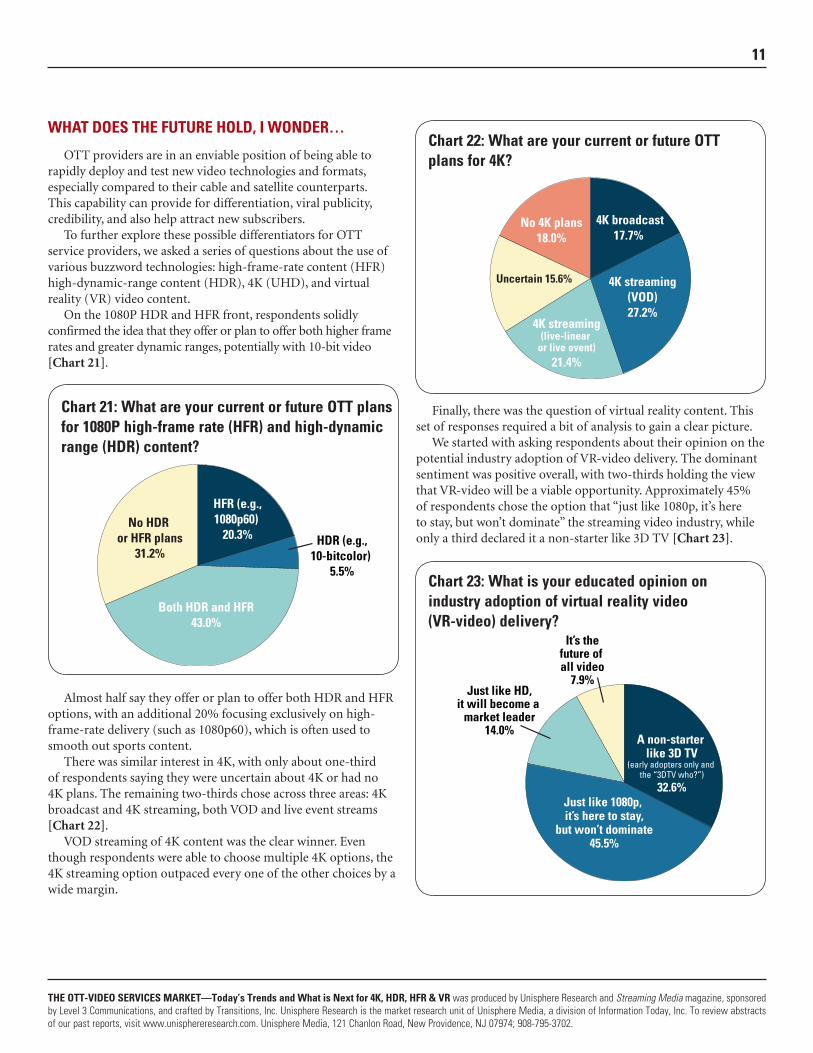

To further explore these possible differentiators for OTT service providers, we asked a series of questions about the use of various buzzword technologies: high-frame-rate content (HFR) high-dynamic-range content (HDR), 4K (UHD), and virtual reality (VR) video content.

On the 1080P HDR and HFR front, respondents solidly confirmed the idea that they offer or plan to offer both higher frame rates and greater dynamic ranges, potentially with 10-bit video [Chart 21].

Almost half say they offer or plan to offer both HDR and HFR options, with an additional 20% focusing exclusively on high-frame-rate delivery (such as 1080p60), which is often used to smooth out sports content.

There was similar interest in 4K, with only about one-third of respondents saying they were uncertain about 4K or had no 4K plans. The remaining two-thirds chose across three areas: 4K broadcast and 4K streaming, both VOD and live event streams [Chart 22].

VOD streaming of 4K content was the clear winner. Even though respondents were able to choose multiple 4K options, the 4K streaming option outpaced every one of the other choices by a wide margin.

Finally, there was the question of virtual reality content. This set of responses required a bit of analysis to gain a clear picture.

We started with asking respondents about their opinion on the potential industry adoption of VR-video delivery. The dominant sentiment was positive overall, with two-thirds holding the view that VR-video will be a viable opportunity. Approximately 45% of respondents chose the option that “just like 1080p, it’s here to stay, but won’t dominate” the streaming video industry, while only a third declared it a non-starter like 3D TV [Chart 23].

No HDR or HFR plans

31.2%

Both HDR and HFR43.0%

HDR (e.g.,10-bitcolor)

5.5%

HFR (e.g.,1080p60)

20.3%12.4%

No 4K plans18.0%

Uncertain 15.6%

4K streaming(live-linear

or live event)21.4%

4K streaming(VOD)27.2%

4K broadcast17.7%12.4%

It’s thefuture of all video

7.9%Just like HD,

it will become a market leader

14.0%

Just like 1080p, it’s here to stay,

but won’t dominate45.5%

A non-starter like 3D TV

(early adopters only and the “3DTV who?”)

32.6%

12.4%

HDR (e.g.,10-bitcolor)

only 5.5%

Chart 21: What are your current or future OTT plans for 1080P high-frame rate (HFR) and high-dynamic range (HDR) content?

Chart 22: What are your current or future OTT plans for 4K?

Chart 23: What is your educated opinion on industry adoption of virtual reality video (VR-video) delivery?

12

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

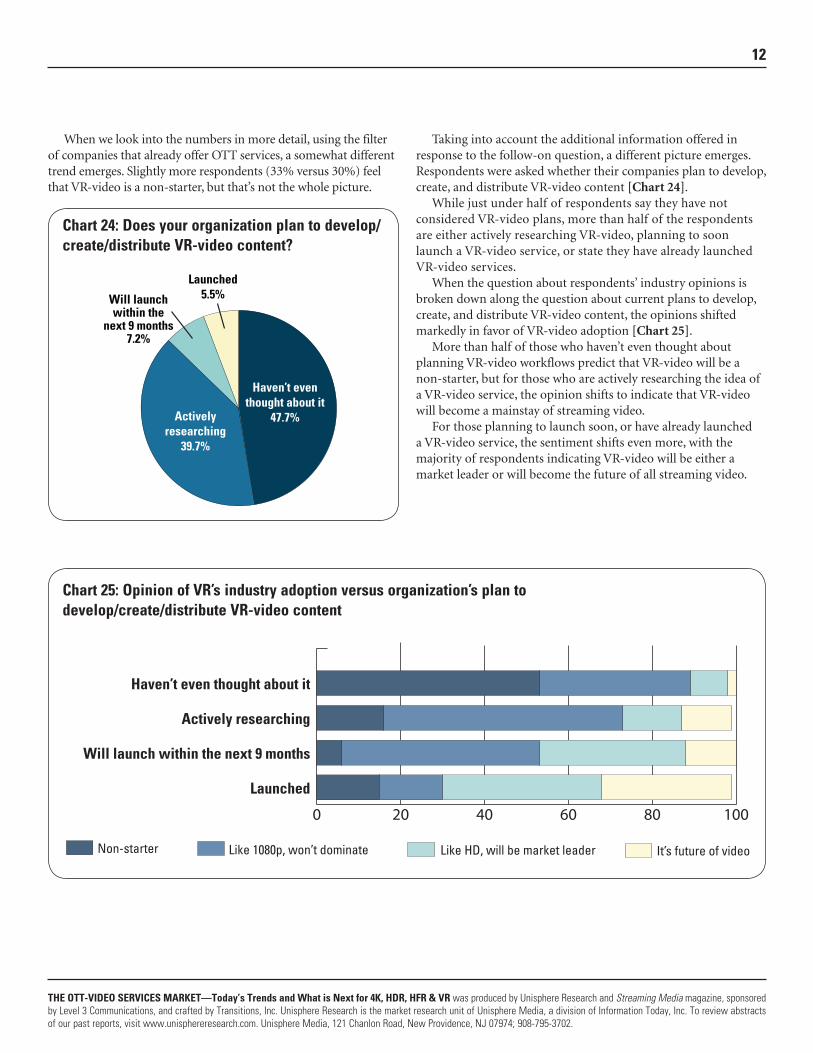

When we look into the numbers in more detail, using the filter of companies that already offer OTT services, a somewhat different trend emerges. Slightly more respondents (33% versus 30%) feel that VR-video is a non-starter, but that’s not the whole picture.

Taking into account the additional information offered in response to the follow-on question, a different picture emerges. Respondents were asked whether their companies plan to develop, create, and distribute VR-video content [Chart 24].

While just under half of respondents say they have not considered VR-video plans, more than half of the respondents are either actively researching VR-video, planning to soon launch a VR-video service, or state they have already launched VR-video services.

When the question about respondents’ industry opinions is broken down along the question about current plans to develop, create, and distribute VR-video content, the opinions shifted markedly in favor of VR-video adoption [Chart 25].

More than half of those who haven’t even thought about planning VR-video workflows predict that VR-video will be a non-starter, but for those who are actively researching the idea of a VR-video service, the opinion shifts to indicate that VR-video will become a mainstay of streaming video.

For those planning to launch soon, or have already launched a VR-video service, the sentiment shifts even more, with the majority of respondents indicating VR-video will be either a market leader or will become the future of all streaming video.

Chart 25: Opinion of VR’s industry adoption versus organization’s plan to develop/create/distribute VR-video content

6.1%

0 20 40 60 80 100

Launched

Will launch within the next 9 months

Actively researching

Haven’t even thought about it

Non-starter Like 1080p, won’t dominate Like HD, will be market leader It’s future of video

Chart 24: Does your organization plan to develop/create/distribute VR-video content?

Launched5.5%Will launch

within thenext 9 months

7.2%

Activelyresearching

39.7%

Haven’t eventhought about it

47.7%

12.4%

HDR (e.g.,10-bitcolor)

only 5.5%

13

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

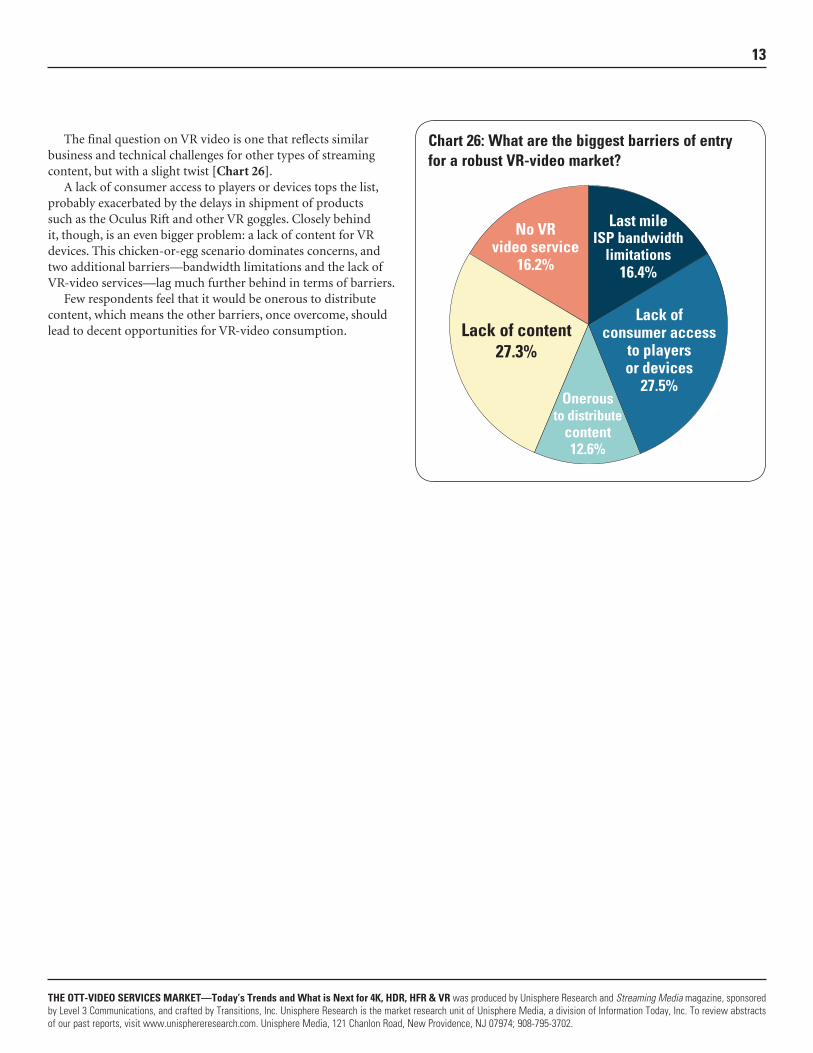

The final question on VR video is one that reflects similar business and technical challenges for other types of streaming content, but with a slight twist [Chart 26].

A lack of consumer access to players or devices tops the list, probably exacerbated by the delays in shipment of products such as the Oculus Rift and other VR goggles. Closely behind it, though, is an even bigger problem: a lack of content for VR devices. This chicken-or-egg scenario dominates concerns, and two additional barriers—bandwidth limitations and the lack of VR-video services—lag much further behind in terms of barriers.

Few respondents feel that it would be onerous to distribute content, which means the other barriers, once overcome, should lead to decent opportunities for VR-video consumption.

Chart 26: What are the biggest barriers of entry for a robust VR-video market?

No VRvideo service

16.2%

Lack of content27.3%

Onerousto distribute

content12.6%

Lack ofconsumer access

to playersor devices

27.5%

Last mileISP bandwidth

limitations16.4%12.4%

HDR (e.g.,10-bitcolor)

only 5.5%

14

THE OTT-VIDEO SERVICES MARKET—Today’s Trends and What is Next for 4K, HDR, HFR & VR was produced by Unisphere Research and Streaming Media magazine, sponsored by Level 3 Communications, and crafted by Transitions, Inc. Unisphere Research is the market research unit of Unisphere Media, a division of Information Today, Inc. To review abstracts of our past reports, visit www.unisphereresearch.com. Unisphere Media, 121 Chanlon Road, New Providence, NJ 07974; 908-795-3702.

SUMMARY

Responses to this year’s survey emphasized two seemingly disparate facts, if each is taken in isolation.

For those offering OTT services today, the trend toward offering 1080p content is fast becoming table stakes. Even beyond 1080p24 or 1080p30, though, there’s a move afoot by online video providers to offer 1080p with HDR and HFR as a counterbalance to the longer-term trend of moving to 4K delivery. In keeping with this, the growth in OTT subscribers viewing 1080p content (instead of the industry standard 720p content) continues to accelerate.

On the other hand, interest in 4K (UHD) and VR-video is also gaining ground, with each seeing more rapid acceptance in the OTT space than they are in traditional broadcast delivery. Both are in their infancy, but have already attracted interest from major content providers.

Taken together, these two facts mean that OTT service providers, while just reaching the point where they are consistently delivering 1080p content, must now pivot and begin to invest in 4K and VR video delivery.

On top of that, live OTT is also gaining ground, with event- and venue-based live streaming moving to center stage from both a business planning and revenue opportunity for OTT service providers.

When it comes to the bottom line of the move from traditional television to internet television, one fact is clear: Not only are OTT providers able to rapidly implement next-generation video formats and content, in stark contrast to the slow uptake of new technologies from their cable and direct-to-home (DTH) ancestors, but OTT providers are actually leveraging this adoption of new technologies as a new way to monetize content.

As they seek to differentiate and grow their subscriber base, it is critical that OTT providers realize they aren’t just battling status-quo methods of media delivery, but are also competing with each other, both in the present transformative and exciting state of video consumption, as well as in the near future.

The agility of OTT providers to simultaneously look backward to gather best practices while also looking toward the future of an OTT-only delivery landscape is what will enable their accelerated market growth.

ABOUT LEVEL 3

This report’s key sponsor, Level 3, has more than a quarter-century’s experience in live content acquisition, including connectivity to over 155 professional and college sports venues, broadcast video distribution, and encoding for linear streaming channels combined with a global content delivery network covering major metro markets across six continents. For those hesitant to move into the OTT video space due to security concerns, Level 3 also offers integrated security products.