the pathfinder report

DESCRIPTION

June 2014TRANSCRIPT

THE PATHFINDER REPORT: JUNE 2014 1

THANKS FOR WRITING IN

CHARTING THE COURSE A Behind-the-Scenes Look at the Burgeoning Single-Family Home Rental Business

FINDING YOUR PATHToo Many Cranes in the Air?

BREAKING NEW GROUND: GUEST FEATURECommentary on the Multifamily Market

ZEITGEIST: NEWS HIGHLIGHTS

TRAILBLAZING Homewood Suites, La Quinta, CA

NOTABLES AND QUOTABLESOn Appreciation

2

2

6

8

10

11

12

IN THIS ISSUE

THE PATHFINDER

REPORTJune 2014

THE PATHFINDER REPORT: JUNE 2014 2

THANKS FOR WRITING INThanks for writing in. Please keep those cards and letters coming.

If you have expertise in an area that could be of interest to our readers, please email us at [email protected] with information about your proposed subject matter. We will be happy to consider it for a future edition.

Congratulations to Pathfinder’s Mitch Siegler, Matt Quinn and Amanda Snyder (along with their friends Ember and Brittany) for successfully completing the Camp Pendleton 10K (6.2 mile) Mud Run earlier this month! Here are before and after snapshots of the Pathfinder gang.

CHARTING THE COURSEA Behind-the-Scenes Look at the Burgeoning Single-Family Home Rental BusinessBy Mitch Siegler, Senior Managing Director

Cognitive dissonance is the stress and discomfort created by a person who holds two contradictory beliefs. We’re suffering from it as we digest the goings-on in the burgeoning single-family home rental business – in which we’re a tiny participant (the proverbial fly on the elephant’s behind).

A few years ago, most of us hadn’t heard of investors acquiring and renting out homes. Then, the business was all the rage as mega-private equity firms like Blackstone Group and Colony Capital swarmed high foreclosure markets and scooped up homes left and right. Then, when home prices there skyrocketed, these groups moved on as fast as they came on the scene. Now, some firms have gone public while others have sold bonds via Wall Street securitizations. What gives?

The Emergence of a New Asset Class – Single-Family Home Rentals

A handful of private equity firms and institutional investors – led by Blackstone, Colony American Homes, Silver Bay Realty Trust Co., Starwood Waypoint Residential Trust and American Homes 4 Rent – have

invested over $20 billion to buy and fix up an estimated 150,000 homes during the past several years and rent them out. That’s just the tip of the iceberg – these groups represent around 1% of the estimated 14 million investor-owned single-family rental homes in the U.S., according to John Burns Real Estate Consulting. Lest you think investors haven’t been a critical driver of the overall housing market (and the general economy), note that single-family rentals comprise 25% of rentals (including apartments) and 11% of the total housing stock, also per Burns.

This highly fragmented mom and pop business is just beginning to undergo consolidation. Bulls believe it could emerge as an asset class similar to apartments, where publicly-traded apartment-rental companies own 600,000 units and have an aggregate market capitalization of $88 billion, according to The Wall Street Journal.

The latest buying opportunity was created following the real estate collapse in 2008-2009 but the big boys really got into the game during the past three years and their portfolios were essentially created from whole cloth since 2012. They’ve been helped along by capital raised from the public markets and through low-cost securitizations (bond-like financing structures where investors’ collateral is pooled into loans backed by rental income from the homes).

In May, American Homes 4 Rent, a publicly-traded REIT which owns 25,000 homes demonstrated the power of scale and access to Wall Street capital when it raised nearly $500 million in a securitization backed by the rental income from 3,850 homes at LIBOR+154 (a jaw-droppingly low rate of just 1.79%). This is the second time around for American Homes 4 Rent’s CEO,

THE PATHFINDER REPORT: JUNE 2014 3

Wayne Hughes, a sharecropper’s son who founded Public Storage and who sees a similar consolidation opportunity in the single-family home rental space. From 2009-2012, buying and renovating single-family homes and aggregating them in a rental pool was a bit like shooting fish in a barrel. It didn’t so much matter where you went or even which homes you acquired – prices had been pummeled in many cities to such a degree that investors could realize astonishing cash-on-cash returns from renting these homes – plus, they could hold out decent hope that prices may one day return to pre-crash levels, doubly rewarding them with an attractive current yield and juicy future price appreciation. Today, the space is tougher because of the meteoric rise in home prices the past two years. In housing markets hardest hit by the bust (think Phoenix, California’s Sacramento and Inland Empire regions, Florida and Las Vegas) prices have risen 30% to 50% off their post-crash lows. Across the country, prices are up 11% in the past two years, according to Zillow Inc.

Pathfinder’s Single-Family Rental Experiences

By way of perspective, when Pathfinder and a partner began acquiring homes in San Diego County in 2010, cap rates (a measure of the first year net operating income divided by the home’s total cost, including renovation expenses) of 7-8% were attainable. That’s a pretty attractive yield in any market but all the more so in San Diego, historically a high-flying housing market with strong rental demand

(95% occupancies) and home prices in some areas which had fallen 30-40% below peak levels. We built a little rental portfolio, buying, renovating and renting 125 homes before the buying window closed last

year. Today, there’s very little supply of homes for sale in San Diego, investor and owner-occupied demand is through the roof and appreciation of 30% in the past couple of years caused cap rates to plummet – cap rates of 4% are what you’d likely receive today on rental homes in good neighborhoods in America’s Finest City.

Yet, we really liked the business and didn’t want to stop buying single-family homes altogether just because the opportunity in our backyard had passed. So, we dug into other hard-hit markets that might provide a second act. Surely, places like southern California’s Inland Empire and Phoenix might have some opportunity. No such luck. We even looked at Las Vegas, the epicenter of the housing bust. No dice even in Sin City. In 2012, investors could buy in Sunbelt markets for gross yields approaching 15%; that’s now below 10%, according to real estate advisory firm Green Street Advisors. So, after stepping in, buying hundreds, even thousands of homes and setting a floor and sparking a housing recovery in many hard-hit markets, big investors are now rethinking the next chapter in the home-rental business story.

What’s Changed?

The first thing is there’s less demand for entry-level homes today than a few years ago. During the downturn, millions of Americans lost their homes through foreclosure, leading to a substantial decline in the homeownership rate (from about 69% to 64%). Those whose credit remains damaged won’t be buying another home anytime soon. For others, the pain that their neighbors and friends experienced means the bloom is off their homeownership rose – maybe for years. And, younger people are waiting longer to get married, one of the primary drivers of home purchases. The youngest, Millennials, want to live near major transportation corridors, employment centers and entertainment and dining options. That means they tend to gravitate to urban cores in major markets – not to suburban areas or – gasp – tertiary markets.

Meanwhile, from a supply perspective, there’s a lot less distress than even a couple of years ago. In 2012, the high-water mark for distress, 31.4% of homeowners with a mortgage were “underwater” – meaning they owed more on their mortgages than their homes were worth. That fell to 18.8% in May (9.7 million households), according to Zillow Inc. This is a huge improvement but we still have nearly 10 million households with negative equity (plus millions more with insufficient equity to sell and pay their brokerage commissions and closing costs). Those underwater and those in a zombie state combine to create a huge drag on these homeowner’s confidence and consumer spending, which adds to the pressure on the overall housing market and the general economy.

THE PATHFINDER REPORT: JUNE 2014 4

What are the Implications?

Pathfinder’s experience in San Diego was far from unique. Rising home prices forced many investors to accept lower returns than they originally had projected, or to buy homes in cities where price appreciation has been less rapid. The public filings of Blackstone and the other big boys tell the tale. As home prices rose in many parts of the country, the institutions’ pace of buying slowed dramatically. Blackstone, the industry leader, scooped up more than 43,000 homes in 14 cities since April 2012. However, the firm’s acquisition pace has declined 70% from its July 2013 peak, when the private equity firm was spending about $140 million a week on homes; now it’s spending $30 million to $40 million. Blackstone’s recent acquisitions are now primarily focused in a handful of markets, including Atlanta, Tampa, Orlando, Miami and Seattle (we’re scratching our heads as to where they’re finding outstanding home buying opportunities in the Emerald City, whose economy, housing market and job prospects are on fire). Colony American, which owns 16,000 homes, also appears to have slowed its acquisition pace, based on their public filings. The common theme seems to be a 20-40% slowdown in the pace of acquisitions, a greater focus on executing operational strategies with their existing portfolios and a shift to new markets.

The large acquirers seem to be migrating from their historic markets (California’s Inland Empire, Phoenix, Las Vegas and other cities with high rates of foreclosures and plummeting home prices) to smaller markets which still have a bit of distress (Jacksonville, Indianapolis and Nashville are examples). These markets are characterized by lower-priced homes and less long-term home price appreciation – it’s more about going-in cap rates and current yield and it’s harder to put capital to work. Capital initially flowed to the coasts, then to major inland markets (like Atlanta) and is now flowing to the Midwest.

What’s Next?

Of course, when you’re an 800-lb. gorilla and you have more money than God, there’s more than one way to rule the jungle. The big boys have been finding new and innovative ways to profit, by securitizing the rental income from their existing properties, by using their market position and economies of scale to wring cost savings from portfolios they scoop up from moms and pops (the classic second phase in a consolidation or

“roll-up” strategy) and lately, by leveraging their market position and using their low-cost debt to lend to moms and pops (borrowing at 2% and lending at 5-7% isn’t too shabby). Plus, it places Blackstone and Colony in a pretty good position when their borrowers ultimately decide it’s time to sell since they have imbedded relationships and know the market and portfolio well.

The Land Grab is Over, the Low-Hanging Fruit is Gone and Solid Execution and Niche Acquisition Approaches are the New Strategies

We spoke last month at a single-family rental aggregation conference in south Florida. About 1,000 attendees discussed the ebbs and flows this new market has seen in just the past couple of years. We heard everything from “there are 20 other guys buying at auctions all-cash” to “I’m the only guy still at the auctions since the large funds left.” One of the more interesting discussions centered on a proliferation of niche (guerilla) strategies, now that the low-hanging fruit has been picked and not everyone wants to travel to Jacksonville or Indianapolis to monitor a portfolio. A few of the more interesting ideas:

• Good old-fashioned “shoe leather” approaches, like knocking on doors and conducting direct mail campaigns.

• Seeking out “trigger” events (death notices, homes that have had fires where the owner collected an insurance settlement and wants to sell rather than rebuild).

• You know those obnoxious “We Buy Houses” signs on the side of the road? They must be effective – because if it didn’t work, you wouldn’t keep seeing the signs. (Various groups are having success with this approach in cities coast to coast.)

• We heard a fair bit of chatter about companies that are building homes with an eye to renting rather than selling them. Now, that doesn’t really work in California or other markets with high fees, long entitlement lead times and other barriers to entry. But, in places like Georgia and Texas, where land is inexpensive and the entitlement process is quick and easy, folks are doing this.

THE PATHFINDER REPORT: JUNE 2014 5

• Niche geographical strategies abound. One Michigan-based company is extolling the virtues of buying inexpensive homes in one of the country’s more economically depressed regions.

How to Achieve Attractive Returns in the Current Environment?

In 2010-2012, returns were driven by “known” factors (buying for a price that represents a substantial discount to peak value and replacement cost and at a level that generates a 6-7% “cap” rate). Today, as prices have skyrocketed, cap rates have fallen to 4-5% in many markets and rents have remained essentially flat, total returns are driven largely by “unknown” factors (future home price appreciation or “HPA”– which is anybody’s guess).

That’s the natural evolution or life cycle of the business. The vintage of the portfolio (Were the homes acquired earlier or later in the cycle?) provides clues about the location of the homes while both factors determine the current yield and likely future HPA. As noted above, we’ve seen a migration in terms of geography (from primary to secondary, even tertiary markets) as well as in age/quality (from newer homes to older and lower-quality properties. Seems like homes acquired a couple of years ago are money in the bank while homes acquired now and in the future – especially in some of these new markets – are a bit more speculative.

What Could Go Wrong?

People need a place to live, rental homes are here to stay and there’s an opportunity to institutionalize and consolidate this sector. That said, we’re never completely comfortable when big institutions rush to raise billions by selling securities on Wall Street. Since much of the initial capital to build these portfolios was raised in 2010-2012 and many funds have predetermined lives (basically a contractual requirement that they will sell their assets by a set date), there could be a rush for the exits (read “selling pressure”) in five or so years. So, in the merry game of musical chairs, don’t be caught standing if the music stops in 2016-2018.

Mitch Siegler is Senior Managing Director of Pathfinder Partners, LLC. Prior to co-founding Pathfinder in 2006, Mitch founded and served as CEO of several companies and was a partner with an investment banking and venture capital firm. He can be reached at [email protected].

THE PATHFINDER REPORT: JUNE 2014 6

If you take a tour these days through downtown Denver, Austin or Seattle, you would not be far off the mark if you conclude that Colorado, Texas and Washington share a common state bird; the construction crane. It’s hard to believe, but there are about 20 cranes in the air in the downtown areas of each of these three cities.

The numbers are quite staggering. According to the annual Hendricks Berkadia forecast report, Denver currently has over 7,400 multifamily units under construction. Another 6,500 units are in the planning/entitlement stage. The numbers are similar in Austin and Seattle. The Texas state capital has 9,440 units under construction and another 7,930 units in planning/entitlement, while the Emerald City has 8,800 units under construction and another 8,250 units in planning/entitlement.

Things are a little slower back home in the Golden State, but we’ve also seen a pretty big ramp up in construction. In fact, San Francisco currently has 3,900 multifamily units under construction, Los Angeles is at 2,500, while San Diego lags behind at a mere 2,100 units.

Moods change quickly these days. Seems like only yesterday when the financial world was falling apart (okay, it was about six years ago) and the prospects for anything new coming out of the ground were as distant as a San Diego Padres World Series win. Since we predicted the downfall of the residential real estate market in 2006, we tend to get a little nervous around the Pathfinder cappuccino maker when we see things getting too frothy. Jeez, are we back there already? Is the real estate market getting overheated again? Should we all sell everything we own? I don’t think so, and here are five reasons why.

Lack of Construction

If you look at multifamily construction from a historical perspective, we still haven’t caught up from the five years of little to no activity that occurred from 2008 to 2012. Looking at a rolling 30-year average (that will take you through a few cycles), there was an average of 271,483 multifamily units constructed nationally. During 2008-2012, that number fell to 171,000 (a 37% decrease), a massive reduction. Yet, at the same time, populations in the nation’s largest cities continued to grow. Did everyone double bunk, move back in with their parents or get a new roommate? Sure, some did. But vacancy numbers trended down to historic lows in many cities across the west and now that the economy is heating up again, we expect that we will continue to see an uptick in demand as the Millennials, the largest group of renters, complete college, move back out of their parents’ homes, and start exploring independent living arrangements.

Assuming static demand (and we believe demand is increasing, not staying static), at the current pace of construction and development, it will take almost five years in the three referenced cities to make up for the lack of construction which occurred during the preceding five years. Now that doesn’t mean that a flood of new units won’t have a near-term effect on vacancy and rents. We think they will. In fact, we’re predicting relatively minor rent growth and increased vacancy in most of the markets we are investing in over the next few years. But that’s not a bad thing. A 2.8% vacancy in the market (Portland, by way of example), isn’t healthy from our perspective. It encourages landlords to impose significant rent increases, and causes a general imbalance in supply/demand. We’ve been underwriting to a five percent vacancy factor going forward and believe that is both reflective of the new incoming supply but also a healthy supply/demand balance.

Lending Standards

Boy, did these ever get lax in the early 2000s. Major banks decided that just clipping a seven or eight percent yield was insufficient, and started working their way down the capital stack to increase yield. Even large money center banks started doing it, spinning off mezzanine loan

FINDING YOUR PATHToo Many Cranes in the Air?By Lorne Polger, Senior Managing Director

THE PATHFINDER REPORT: JUNE 2014 7

divisions under different names (gee, Bank of America, did you think that if you called your mezzanine loan group “Trisail”, Wall Street would never figure out it’s part of BofA?).

I’ve told the story many times over the years, but the big light bulb went off on my head in 2005 when I was involved as a lawyer in a $72,000,000 transaction that was structured with $71,750,000 of debt and $250,000 of equity. The good news is that while banks are lending again, it does not appear that they are making crazy loans, certainly nothing even close to that marquis level of leverage. Memories of the Great Recession and the significant crackdown imposed by the FDIC remain vivid. We’ve been borrowing on assets in major markets throughout the western U.S. and while we are pleased to report that the number of lenders willing to work with us has increased significantly, we have not seen any meaningful relaxation in underwriting standards, or significant variations in leverage. Equity Return Requirements

There is a significant disconnect in equity return requirements for new development vs. existing income properties. That’s a good thing. The financial markets are pretty efficient these days. Continuation of disciplined underwriting is a self-regulating mechanism for new development. Is “dumb money” out there today? Perhaps. But we haven’t seen it very often across the markets that we invest in. Bottom line is that so long as the return requirements for new development significantly exceed the return requirements for existing investments, there will be a hard stop to the flow of equity into new deals.

Population Demographics

Cities are continuing to grow. Good cities are growing more. A growing population means an increased need for new housing (both rental and for sale). And the good cities are REALLY growing these days. Austin’s

metropolitan area population is expected to grow by 759,889 people over the next ten years. For Seattle, that number in the King County metro area (Seattle, Bellevue, and Tacoma) is 411,636. For the Denver metro area, it’s 702,524. Similar stories throughout California and

Texas, and in Portland and Phoenix. Not seeing a lot of cranes in Des Moines, Detroit or Cleveland? If you do, the party is probably over again. A little biased on the left side of the coast here, but I’m reminded of the words from the 1967 Doors song, The End: “The west is the best. Get here and we’ll do the rest.”

Adaptive Reuse and Redevelopment are Healthy Phenomena

Don’t mean to brag, but we’re pretty proud around here about a significant redevelopment project we just embarked upon in downtown Longmont, Colorado. In May, we closed on the purchase of the shuttered Butterball Turkey processing plant. The plant and some outlying properties comprise a 28-acre site. The plant was closed in 2011 after a Chinese company purchased Butterball from its parent company, ConAgra, and moved processing operations to China.

Now, what makes us excited about the project? We believe that projects like the Butterball redevelopment will spur on new vintage creative office and retail growth in areas that have been previously dormant. We also believe that a significant number of office buildings in major urban areas have now become functionally obsolete. And turning them into residential housing or other modern uses is now occurring now throughout southern California. We think that the new and readaptive housing will spur the office and retail markets in those environments, creating vibrant, walkable communities. Taking old and making new. That’s a positive and sustainable trend.

Times have changed. There’s still some distress around and we expect to continue to make opportunistic buys. But there are some very interesting development opportunities throughout the western U.S. and we believe that the dramatic lack of new construction that occurred over a six-year period leaves room for development ahead without cause for too much worry.

Lorne Polger is Senior Managing Director of Pathfinder Partners, LLC. Prior to co-founding Pathfinder in 2006, Lorne was a partner with a leading San Diego law firm, where he headed the Real Estate, Land Use and Environmental Law group. He can be reached at [email protected].

THE PATHFINDER REPORT: JUNE 2014 8

In many of the markets where Pathfinder is active, including southern California, Seattle, Portland, Denver and Phoenix, it’s a similar story on the economic and residential fronts. Economic drivers are firing on all cylinders, employment is at or above pre-recession levels and housing prices have seen a couple of years of double-

digit gains. The impact to the multifamily market has been a compression of capitalization rates to historic lows, occupancy rates nearing all-time highs and opportunities to push rents which have never been better.

As a result of the strengthening fundamentals, development is back in a big way in these metro areas – which were some of the first to recover and which are now kicking into high gear. Cranes are in the air. Land is trading again. Dirt is moving. Lenders have loosened the purse strings on construction lending.

But, with development comes a caution flag. Are we heading for a period of over-supply? Will the demand drivers continue to move in the right directions? I hear and read a lot on both sides of the issue. Below are some pros, cons and musings on what it all means.

Pros: Arguments for a Healthy Market

• The national multifamily vacancy rate is 4.9%, which is 40 basis points below the historic norm of 5.3%. We still have some room for additional supply to get back to a balanced market.

• Annualized 2014 rent growth of 3.2% is above its long-term average and above the rate of inflation as measured by the Consumer Price Index.

• Over the past four quarters, net multifamily absorption was 250,451 units, while supply increased by 231,150

units – that suggests that supply is not yet meeting demand.

• We’re coming off a period where there has been very limited product built. National multifamily completions were fairly steady from 1989-2008 at 253,000 per year. We are just starting to get to those levels after a period of significant under-supply from 2009-2013.

• As housing prices continue to increase, the affordability index for home ownership will continue to decline, and more people will be priced out of the housing market, creating additional “renters by necessity”. Additionally, many believe that the trend of “renters by choice” is here to stay as well.

Cons: Arguments for an Unhealthy Market

• We’re entering a period where, in some markets, supply is exceeding demand. You can look at Seattle on this point. In the next year, 9,403 units will be delivered, compared to forecasted annual demand of 7,963 units (see Chart “A” below). San Diego is another example where 5,014 units are projected to be added to the supply, with annual demand of 3,674 units (see Chart “B” below). If building continues at this pace, the undersupply of the previous years will be quickly wiped out.

• Banks are just now opening the spigot to construction lending. We’re seeing some construction loans in the 3% interest rate range. We all know that developers haven’t historically been the greatest at refusing money, especially when it costs next to nothing to borrow.

• The home ownership rate, now at 64.8%, continues to fall from its high of more than 69% in 2005. If the trend reverses, which some predict, it would have an adverse effect on the rental market.

• While we’ve had a jobs recovery, it has been marked by high income jobs being replaced by lower income jobs; wage growth, in general, has not been strong. An ever larger proportion of renter’s salaries are going toward housing costs, a trend that can’t continue forever.

Predictions

• Much of the development is at the luxury end of the spectrum. There is a lack of affordable housing, and it’s a problem that will likely worsen. Buying well located,

BREAKING NEWGROUNDCommentary on the Multifamily MarketBy Scot Eisendrath, Managing Director

- GUEST FEATURE

THE PATHFINDER REPORT: JUNE 2014 9

“bread and butter” affordable apartments that provide the opportunity to implement renovations and increase rents has and is likely to remain a winning strategy.

• A large portion of the high end, luxury, for rent multifamily units being built in core urban markets will ultimately be converted to condominiums. Those developers who don’t sell upon completion and those investors that buy the finished buildings as rental properties better hope I’m right because it’s probably the only way they’ll make money acquiring at today’s nosebleed prices.

• The majority of the broken condominium deals that are left over from the last cycle will continue to languish. Most of those that remain are apartment grade projects that were converted to condos, unsuccessfully, because they never should have been for sale condominiums in the first place. There may be a way to make money with these, although we haven’t quite figured out what it is yet.

• There are a number of purpose-built condominium and townhome projects that were completed in 2007-2009 where no units have been sold and the buildings are now being operated as rentals. As the current cycle evolves, these will make excellent condominium conversion candidates – someone could make a lot of money.

Chart A – Spotlight on the Seattle Multifamily Market

• 5.2% unemployment rate, down from a high of 8.8% in June 2009• Forecasted annual supply of 9,403 units vs. forecasted annual demand of 7,963 units• 96.4% current occupancy rate• 6.2% annual rent growth for 12 months ending March 31, 2014• 11.6% housing price increase in last 12 months

Chart B – Spotlight on the San Diego Multifamily Market

• 6.0% unemployment rate, down from a high of 10.9% in January 2010• Forecasted annual supply of 5,014 units vs. forecasted annual demand of 3,674 units• 97.2% current occupancy rate• 4.7% annual rent growth for 12 months ending March 31, 2014• 18.9% housing price increase in last 12 months

Sources: RealPage MPF Research, CBRE, Kidder Mathews, S&P/Case-Shiller, SDCAA

Scot Eisendrath is Managing Director of Pathfinder Partners, LLC. He is actively involved with the firm’s financial analysis and underwriting and has spent 20 years in the commercial real estate industry. He can be reached at [email protected].

THE PATHFINDER REPORT: JUNE 2014 10

Tide Slowly Receding on Underwater Homeowners

In early 2012, at the peak of the housing decline, about one-third of U.S. homeowners were underwater on their homes (their homes were worth less than their mortgages). At the end of March 2014, that had fallen to 18% – a decrease of 38%. While this is good news for housing, there are still 10 million homeowners who remain stuck in their homes. And, another 10 million households have such little equity in their homes that they would be unable to cover the brokerage fees, closing costs required to sell their homes and scrape together a down payment to purchase new homes. This condition hits first-time home buyers particularly hard because most of the underwater and treading water homes are lower-priced homes, creating a lack of for-sale affordable home inventory. Many of these homeowners aren’t budging anytime soon – rather than facilitate a short-sale or walk away from their homes, they are planning to stay put and wait for a better day.

Top 10 U.S. Apartment “Boomtowns”

SpareFoot, an Austin, TX based online marketplace for self-storage solutions, recently published a list of their top apartment boomtowns in the U.S. They looked at several factors including apartment affordability and availability, job and population growth and local economic activity. Some of the cities come as no surprise – others are less predictable.

1. San Jose, CA2. Austin, TX3. Houston, TX4. Grand Rapids, MI5. Nashville, TN6. Dayton, OH7. Portland, OR8. San Francisco, CA9. Dallas-Fort Worth, TX10. Oklahoma City, OK

It’s no shocker that Texas cities are three of the top ten metros to build or own apartments – economic growth coupled with friendly government make the Lone Star State a regular on most “Top Ten” lists. Grand Rapids and Dayton make the list largely due to the number of their residents willing to spend more of their salaries on apartments – 43% of residents in both cities are currently spending more than 35% of their income on rent. As for San Jose and San Francisco, when residents are willing to spend $2.50 per square foot for an older apartment without parking you know it’s a good place to be a landlord.

ZEITGEIST -SIGN OF THE TIMES

THE PATHFINDER REPORT: JUNE 2014 11

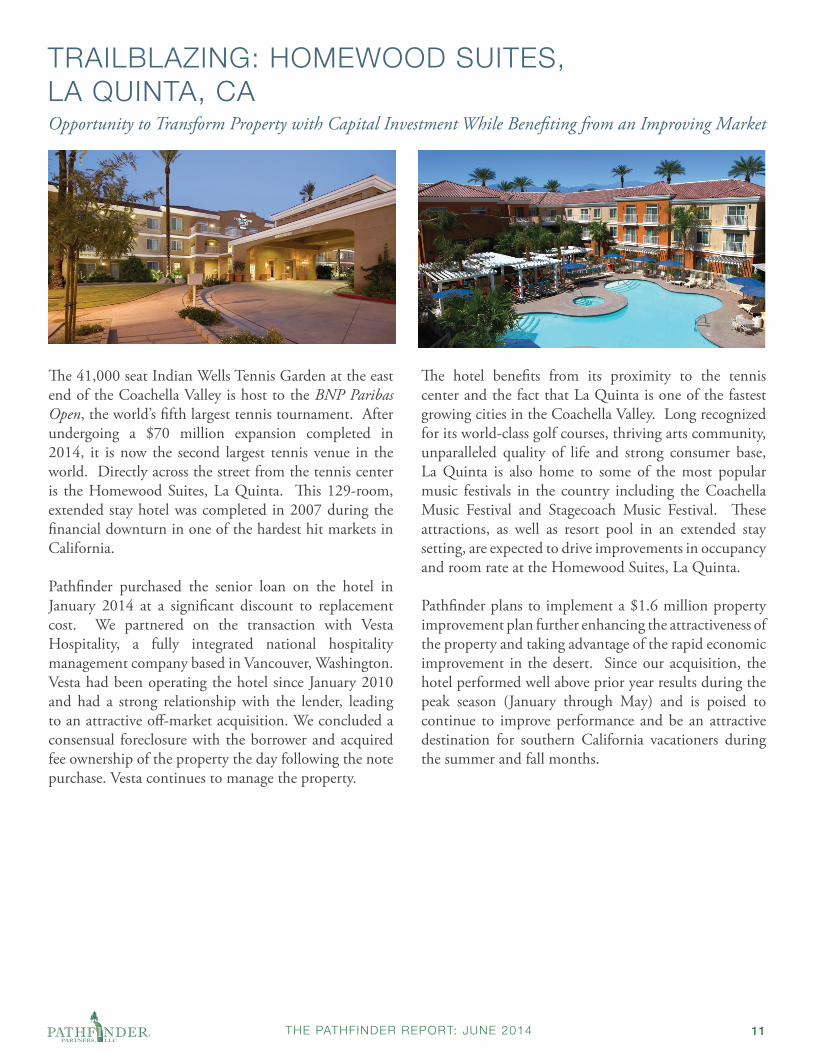

TRAILBLAZING: HOMEWOOD SUITES, LA QUINTA, CAOpportunity to Transform Property with Capital Investment While Benefiting from an Improving Market

The 41,000 seat Indian Wells Tennis Garden at the east end of the Coachella Valley is host to the BNP Paribas Open, the world’s fifth largest tennis tournament. After undergoing a $70 million expansion completed in 2014, it is now the second largest tennis venue in the world. Directly across the street from the tennis center is the Homewood Suites, La Quinta. This 129-room, extended stay hotel was completed in 2007 during the financial downturn in one of the hardest hit markets in California.

Pathfinder purchased the senior loan on the hotel in January 2014 at a significant discount to replacement cost. We partnered on the transaction with Vesta Hospitality, a fully integrated national hospitality management company based in Vancouver, Washington. Vesta had been operating the hotel since January 2010 and had a strong relationship with the lender, leading to an attractive off-market acquisition. We concluded a consensual foreclosure with the borrower and acquired fee ownership of the property the day following the note purchase. Vesta continues to manage the property.

The hotel benefits from its proximity to the tennis center and the fact that La Quinta is one of the fastest growing cities in the Coachella Valley. Long recognized for its world-class golf courses, thriving arts community, unparalleled quality of life and strong consumer base, La Quinta is also home to some of the most popular music festivals in the country including the Coachella Music Festival and Stagecoach Music Festival. These attractions, as well as resort pool in an extended stay setting, are expected to drive improvements in occupancy and room rate at the Homewood Suites, La Quinta.

Pathfinder plans to implement a $1.6 million property improvement plan further enhancing the attractiveness of the property and taking advantage of the rapid economic improvement in the desert. Since our acquisition, the hotel performed well above prior year results during the peak season (January through May) and is poised to continue to improve performance and be an attractive destination for southern California vacationers during the summer and fall months.

THE PATHFINDER REPORT: JUNE 2014 12

“

“Appreciation is a wonderful thing, it makes what is excellent in others belong to us as well.”

- Voltaire

“There is no value in life except what you choose to place upon it and no happiness in any place except what you bring to it yourself.”

- Henry David Thoreau

“That which we obtain too easily, we esteem too lightly.”

- Thomas Paine

“The roots of all goodness lie in the soil of appreciation for goodness.”

- Dalai Lama

“Next to excellence is the appreciation of it.”

- William Thackeray, 19th century English novelist

“NOTABLES AND QUOTABLES

On Appreciation

And on the other kind of “Appreciation”...

“As a bull market continues, almost anything you buy goes up. It makes you feel that investing in stocks is a very easy and safe and that you’re a financial genius.”

- Mitch Albom, American Author

“A stockbroker urged me to buy a stock that would triple its value every year. I told him, ‘At my age, I don’t even buy green bananas.”

- Claude Pepper, American Politician

THE PATHFINDER REPORT: JUNE 2014 13

IMPORTANT DISCLOSURES

Copyright 2014, Pathfinder Partners, LLC (“Pathfinder”). All rights reserved. This report is prepared for the use of Pathfinder’s clients and business partners and subscribers to this report and may not be redistributed, retransmitted or disclosed, in whole or in part, or in any form or manner, without our written consent.

The information contained within this newsletter is not a solicitation or offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction. Pathfinder Partners LLC does not render or offer to render personal investment advice through our newsletter. Information contained herein is opinion-based reflecting the judgments and observations of Pathfinder personnel and guest authors. Our opinions should be taken in context and not considered the sole or primary source of information.

Materials prepared by Pathfinder research personnel are based on public information. The information herein was obtained from various sources. Pathfinder does not guarantee the accuracy of the information.

All opinions, projections and estimates constitute the judgment of the authors as of the date of the report and are subject to change without notice.

This newsletter is not intended and should not be construed as personalized investment advice. Neither Pathfinder nor any of its directors, officers, employees or consultants accepts any liability whatsoever for any direct, indirect or consequential damages or losses arising from any use of this report or its contents.

Do not assume that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended or undertaken by Pathfinder Partners LLC) made reference to directly or indirectly by Pathfinder Partners LLC in this newsletter, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal past performance level(s).

Investing involves risk of loss and you should be prepared to bear investment loss, including loss of original investment. Real estate investments are subject to the risks generally inherent to the ownership of real property and loans, including: uncertainty of cash flow to meet fixed and other obligations; uncertainty in capital markets as it relates to both procurements of equity and debt; adverse changes in local market conditions, population trends, neighborhood values, community conditions, general economic conditions, local employment conditions, interest rates, and real estate tax rates; changes in fiscal policies; changes in applicable laws and regulations (including tax laws); uninsured losses; delays in foreclosure; borrower bankruptcy and related legal expenses; and other risks that are beyond the control of the General Partner. There can be no assurance of profitable operations because the cost of owning the properties may exceed the income produced, particularly since certain expenses related to real estate and its ownership, such as property taxes, utility costs, maintenance costs and insurance, tend to increase over time and are largely beyond the control of the owner. Moreover, although insurance is expected to be obtained to cover most casualty losses and general liability arising from the properties, no insurance will be available to cover cash deficits from ongoing operations.

Please add [email protected] to your address book to ensure you keep receiving our notifications.