the perfect investment - nyupages.stern.nyu.edu/~iag/presentations/2006-2007/gcm.pdf · –open pit...

TRANSCRIPT

1

Presented by Krish Daftary

TSX: GCM, Pink Sheets: GEMCF

The Perfect Investment

Operational momentum

Long-term business sustainability, predictability, and visibility

Price that allows for a significant margin of safety

2

Understanding the Business

What does Gemcom do?

Provides software solutions that help its customers

manage the lifecycle of their mining operations

including:

• Drill-hole data entry in exploration phase

• Mining design & planning

• Mine operations & production management

3

How Does Mining Work?

• Two main types:– Open pit mining

– Underground Mining

• Extract tons of ore from the ground

• Extract tiny bits of precious/base metals– i.e. 1 g/ton

• Timing & efficiency matter!

Revenue Sources

• License fees: one-time in nature

• Professional Services

• Update Service & Technical Support (USTS): recurring in nature, renewed semi-annually or annually

BREAKDOWN TO COME

4

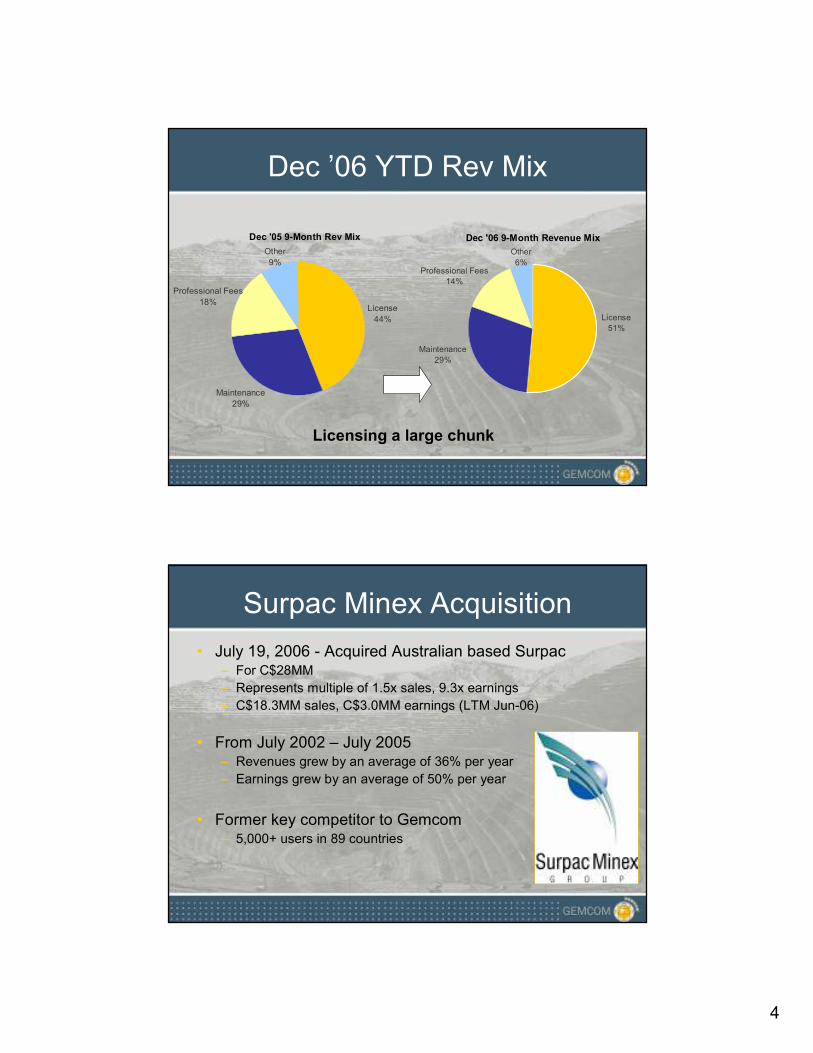

Dec ’06 YTD Rev Mix

Dec '06 9-Month Revenue Mix

Maintenance

29%

Professional Fees

14%

Other

6%

License

51%

Licensing a large chunk

Dec '05 9-Month Rev Mix

License

44%

Maintenance

29%

Professional Fees

18%

Other

9%

Surpac Minex Acquisition

• July 19, 2006 - Acquired Australian based Surpac– For C$28MM

– Represents multiple of 1.5x sales, 9.3x earnings

– C$18.3MM sales, C$3.0MM earnings (LTM Jun-06)

• From July 2002 – July 2005– Revenues grew by an average of 36% per year

– Earnings grew by an average of 50% per year

• Former key competitor to Gemcom– 5,000+ users in 89 countries

5

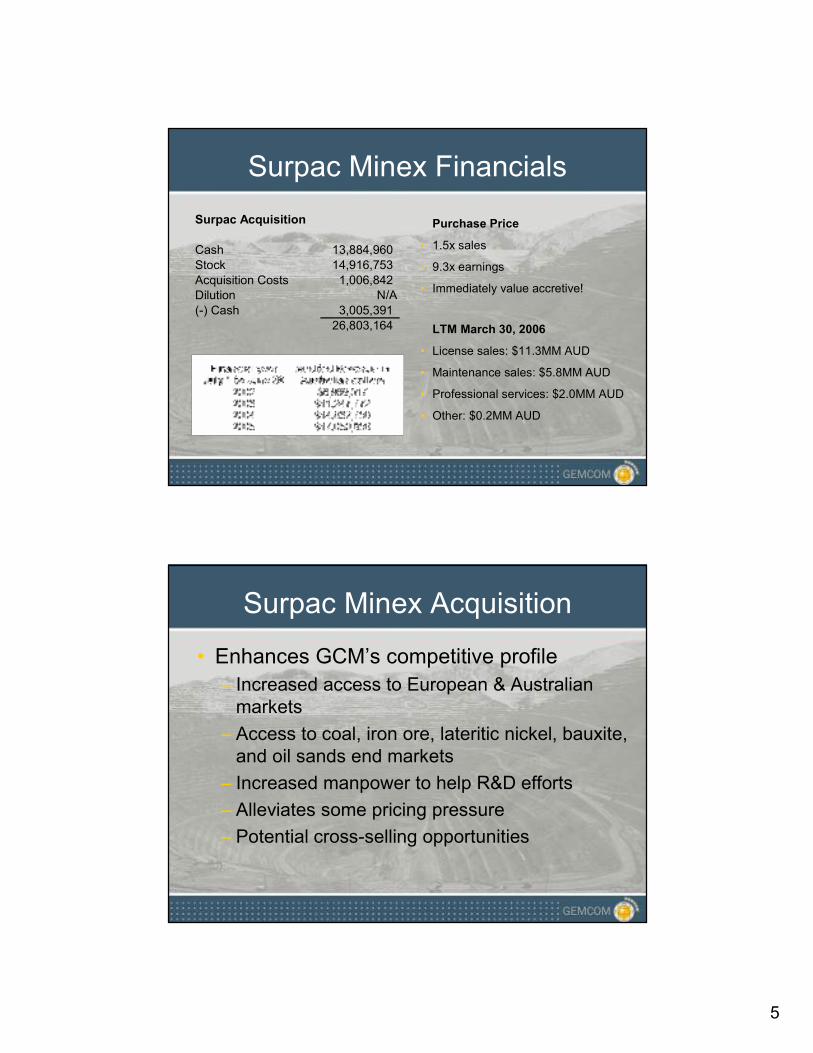

Surpac Minex Financials

LTM March 30, 2006

• License sales: $11.3MM AUD

• Maintenance sales: $5.8MM AUD

• Professional services: $2.0MM AUD

• Other: $0.2MM AUD

Surpac Acquisition

Cash 13,884,960

Stock 14,916,753

Acquisition Costs 1,006,842Dilution N/A

(-) Cash 3,005,391

26,803,164

Purchase Price

• 1.5x sales

• 9.3x earnings

• Immediately value accretive!

Surpac Minex Acquisition

• Enhances GCM’s competitive profile

– Increased access to European & Australian markets

– Access to coal, iron ore, lateritic nickel, bauxite, and oil sands end markets

– Increased manpower to help R&D efforts

– Alleviates some pricing pressure

– Potential cross-selling opportunities

6

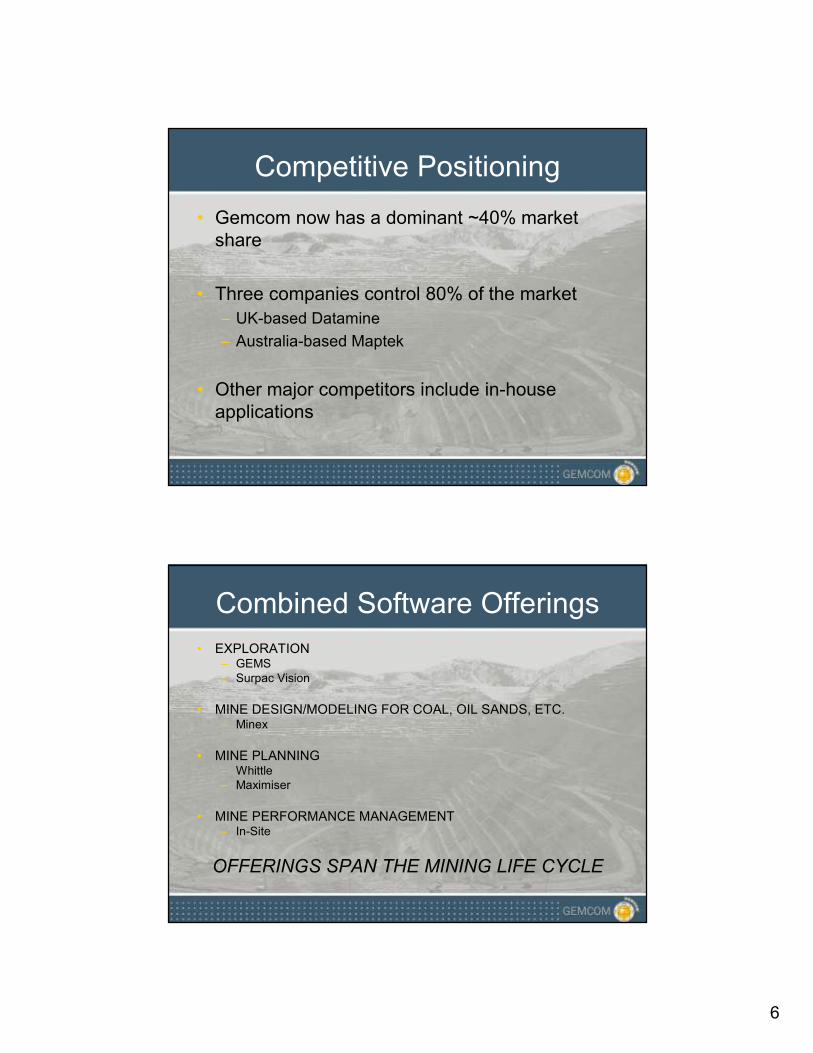

Competitive Positioning

• Gemcom now has a dominant ~40% market share

• Three companies control 80% of the market

– UK-based Datamine

– Australia-based Maptek

• Other major competitors include in-house applications

Combined Software Offerings

• EXPLORATION– GEMS– Surpac Vision

• MINE DESIGN/MODELING FOR COAL, OIL SANDS, ETC.– Minex

• MINE PLANNING– Whittle– Maximiser

• MINE PERFORMANCE MANAGEMENT– In-Site

OFFERINGS SPAN THE MINING LIFE CYCLE

7

Visuals

MineSched

Minex

Major Customers Covered

$15B

$20B$14B

$17B$25B

$139B

8

Mining Industry Overview

Gold Pricing

9

Silver Pricing

Copper Pricing

10

Zinc Pricing

Gold Reserves & Production

11

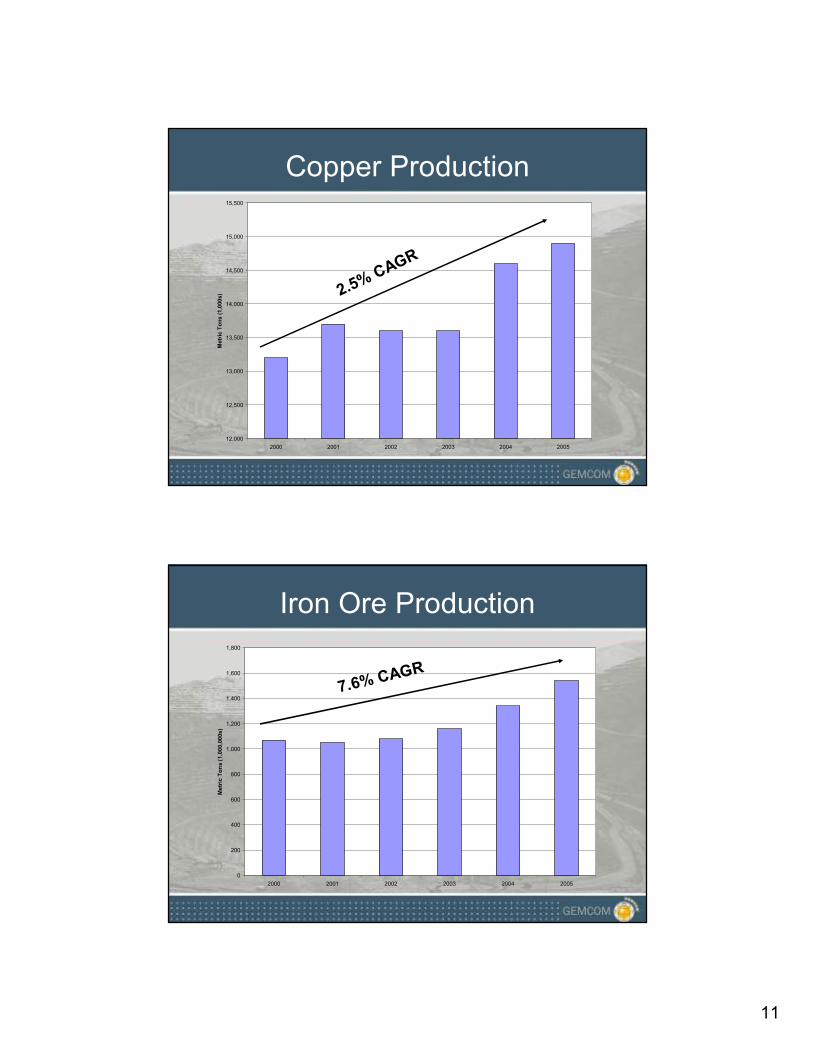

Copper Production

12,000

12,500

13,000

13,500

14,000

14,500

15,000

15,500

2000 2001 2002 2003 2004 2005

Metric Tons (1,000s) 2.5

% CA

GR

Iron Ore Production

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2000 2001 2002 2003 2004 2005

Metric Tons (1,000,000s)

7.6% CAG

R

12

Pricing/Production: GoldGold Price vs. Production 1970-2005

0

500

1,000

1,500

2,000

2,500

3,000

1970 1975 1980 1985 1990 1995 2000 2005

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

Production

Price ($/t)

Pricing/Production: CopperCopper Price vs. Production 1970-2005

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

1970 1975 1980 1985 1990 1995 2000 2005

0

500

1000

1500

2000

2500

3000

3500

4000

Production

Price ($/t)

13

Pricing/Production: Iron OreIron Ore Price vs. Production 1970-2005

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

1,800,000,000

1970 1975 1980 1985 1990 1995 2000 2005

0

5

10

15

20

25

30

35

40

45

50

Production

Price ($/t)

Financial Metrics

14

Price of GCM

Price/share 2.00Shares Outstanding 50,401,412

(+) Dilution 3,827,562Total Shares Outstanding 54,228,974

Market Capitalization 108,457,948

(-) Cash 10,224,370(+) Debt 260,234(+) Minority Interest 23,975

Enterprise Value 98,517,787

Last Q Gangbuster

• Acquisition accounted for 62% of growth

• Organic growth accounted for remaining 38% of increase in revenue

• Implies 56.2% organic

growth rate!

• Annualized, Surpac revenue totals C$16.9MM

3 Months

Dec-06 Dec-05

Revenue:

Products and services 11,055,990 4,575,348

Third-party products 360,596 30,108Total revenue 11,416,586 4,605,456

% Growth 147.9%

Cost of revenue 2,273,780 739,315Gross margin 9,142,806 3,866,141

% Margin 80.1% 83.9%

Research and development 2,491,167 1,007,355

Sales and marketing 3,873,253 1,821,495

General and administration 416,672 327,382EBITDA 2,549,758 860,052

% Margin 22.3% 18.7%

% Growth 196.5%

BreakdownLicense 6.2 2.1 % Growth 195.2%

Maintenance 3.1 1.3 % Growth 138.5%Professional Fees 1.6 0.7

% Growth 128.6%Other 0.5 0.5 % Growth 0

Total 16.0 4.6 % Growth 248.3%

15

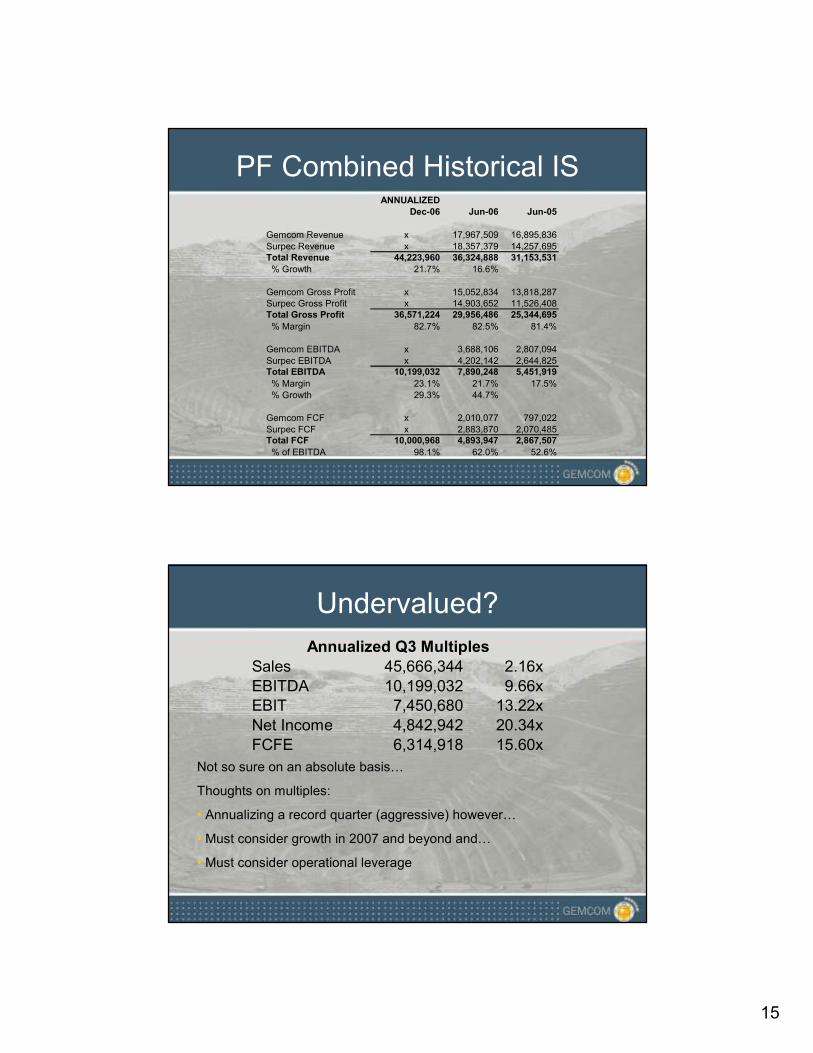

PF Combined Historical ISANNUALIZED

Dec-06 Jun-06 Jun-05

Gemcom Revenue x 17,967,509 16,895,836

Surpec Revenue x 18,357,379 14,257,695Total Revenue 44,223,960 36,324,888 31,153,531

% Growth 21.7% 16.6%

Gemcom Gross Profit x 15,052,834 13,818,287Surpec Gross Profit x 14,903,652 11,526,408Total Gross Profit 36,571,224 29,956,486 25,344,695

% Margin 82.7% 82.5% 81.4%

Gemcom EBITDA x 3,688,106 2,807,094

Surpec EBITDA x 4,202,142 2,644,825Total EBITDA 10,199,032 7,890,248 5,451,919

% Margin 23.1% 21.7% 17.5%

% Growth 29.3% 44.7%

Gemcom FCF x 2,010,077 797,022

Surpec FCF x 2,883,870 2,070,485Total FCF 10,000,968 4,893,947 2,867,507

% of EBITDA 98.1% 62.0% 52.6%

Undervalued?

Annualized Q3 Multiples

Sales 45,666,344 2.16x

EBITDA 10,199,032 9.66xEBIT 7,450,680 13.22x

Net Income 4,842,942 20.34x

FCFE 6,314,918 15.60x

Not so sure on an absolute basis…

Thoughts on multiples:

• Annualizing a record quarter (aggressive) however…

• Must consider growth in 2007 and beyond and…

• Must consider operational leverage

16

Relative: EV/S

Slightly undervalued

2006 2007E 2008E

EV EV/R EV/R EV/R

Autodesk Inc. (NasdaqNM:ADSK) 10,123 6.0x 4.9x 4.3xBusiness Objects SA (NasdaqNM:BOBJ) 3,658 2.2x 1.9x 1.7x

Cognos Inc. (NasdaqNM:COGN) 3,532 3.0x 2.7x 2.5x

Dassault Systemes SA (ENXTPA:DSY) 6,695 3.8x 3.2x 2.6xHyperion Solutions Corp. (NasdaqNM:HYSL) 2,977 3.1x 2.7x 2.4x

Matrikon Inc. (TSX:MTK) 83 1.1x 1.0x ???

Open Text Corp. (NasdaqNM:OTEX) 1,611 3.6x 2.5x 2.2x

Average 4,097 3.3x 2.7x 2.6x

Median 3,532 3.1x 2.7x 2.5x

Gemcom Software International Inc. (TSX:GCM) 99 3.4x 2.2x ???

Relative: EV/EBITDA

Slightly undervalued

2006 2007E 2008E

EV TEV/EBITDA TEV/EBITDA TEV/EBITDA

Autodesk Inc. (NasdaqNM:ADSK) 10,123 17.8x 14.9x 12.9x

Business Objects SA (NasdaqNM:BOBJ) 3,658 11.3x 8.6x 7.7x

Cognos Inc. (NasdaqNM:COGN) 3,532 15.7x 11.7x 10.1xDassault Systemes SA (ENXTPA:DSY) 6,695 12.3x 10.7x 9.6x

Hyperion Solutions Corp. (NasdaqNM:HYSL) 2,977 14.2x 11.2x 9.5xMatrikon Inc. (TSX:MTK) 83 8.5x 6.3x ???

Open Text Corp. (NasdaqNM:OTEX) 1,611 13.2x 8.0x 6.9x

Average 4,097 13.3x 10.2x 9.4x

Median 3,532 13.2x 10.7x 9.5x

Gemcom Software International Inc. (TSX:GCM) 99 15.7x 9.7x ???

17

Relative: P/E

In-line

2006 2007E 2008E

EV P/E P/E P/E

Autodesk Inc. (NasdaqNM:ADSK) 10,123 31.6x 25.7x 20.7xBusiness Objects SA (NasdaqNM:BOBJ) 3,658 21.2x 16.7x 13.8x

Cognos Inc. (NasdaqNM:COGN) 3,532 24.7x 18.8x 16.2x

Dassault Systemes SA (ENXTPA:DSY) 6,695 22.6x 20.2x 17.2xHyperion Solutions Corp. (NasdaqNM:HYSL) 2,977 30.3x 25.1x 21.1x

Matrikon Inc. (TSX:MTK) 83 19.0x 17.1x ???

Open Text Corp. (NasdaqNM:OTEX) 1,611 23.3x 17.6x 13.8x

Average 4,097 24.7x 20.2x 17.1x

Median 3,532 23.3x 18.8x 16.7x

Gemcom Software International Inc. (TSX:GCM) 99 36.0x 22.4x ???

Relative: Growth Rates

Grossly undervalued

EV 1-Yr Revenue G 1-Yr EBITDA G Est. LT G Rate

Autodesk Inc. (NasdaqNM:ADSK) 10,123 24.25 21.74 16.80

Business Objects SA (NasdaqNM:BOBJ) 3,658 16.40 23.14 16.15

Cognos Inc. (NasdaqNM:COGN) 3,532 7.63 (2.49) 13.73

Dassault Systemes SA (ENXTPA:DSY) 6,695 23.89 14.19 9.85

Hyperion Solutions Corp. (NasdaqNM:HYSL) 2,977 15.12 29.02 13.09

Matrikon Inc. (TSX:MTK) 83 1.49 (20.02) NA

Open Text Corp. (NasdaqNM:OTEX) 1,611 12.59 48.36 10.00

Average 4,097 14.48 16.28 13.27

Median 3,532 15.12 21.74 13.41

Gemcom Software International Inc. (TSX:GCM) 99 16.60 44.72 ???

18

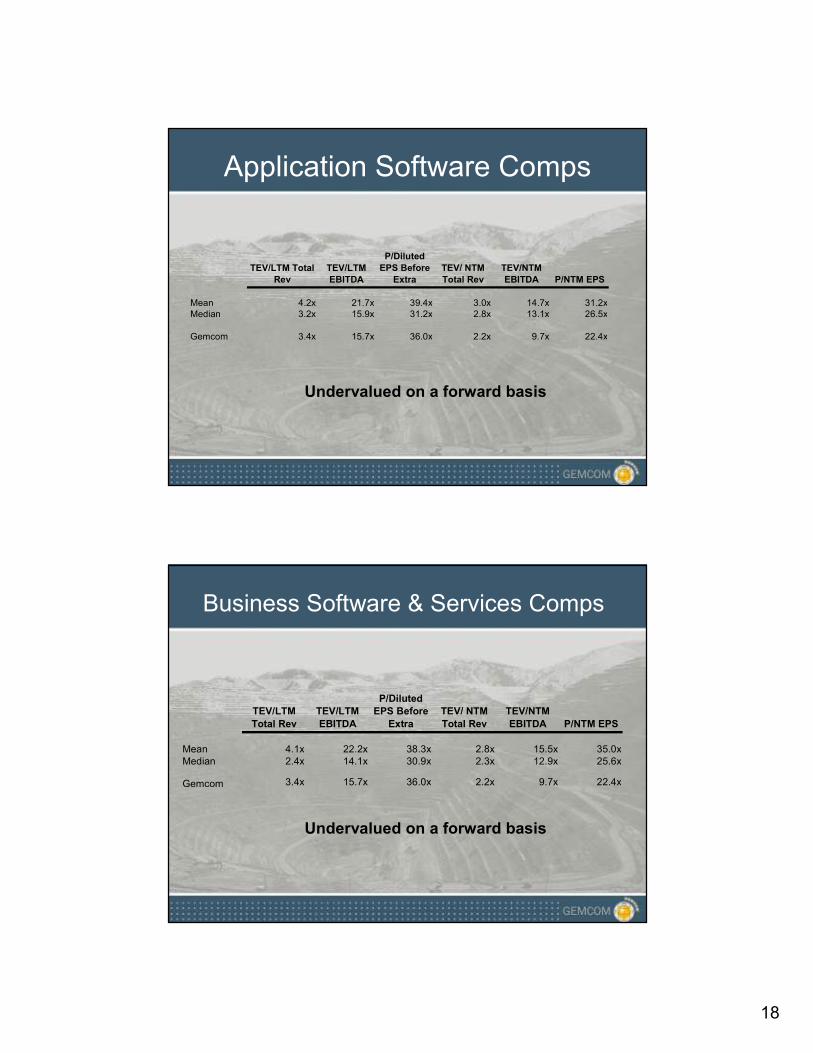

Application Software Comps

TEV/LTM Total

Rev

TEV/LTM

EBITDA

P/Diluted

EPS Before

Extra

TEV/ NTM

Total Rev

TEV/NTM

EBITDA P/NTM EPS

Mean 4.2x 21.7x 39.4x 3.0x 14.7x 31.2xMedian 3.2x 15.9x 31.2x 2.8x 13.1x 26.5x

Gemcom 3.4x 15.7x 36.0x 2.2x 9.7x 22.4x

Undervalued on a forward basis

Business Software & Services Comps

TEV/LTM

Total Rev

TEV/LTM

EBITDA

P/Diluted

EPS Before

Extra

TEV/ NTM

Total Rev

TEV/NTM

EBITDA P/NTM EPS

Mean 4.1x 22.2x 38.3x 2.8x 15.5x 35.0xMedian 2.4x 14.1x 30.9x 2.3x 12.9x 25.6x

Gemcom 3.4x 15.7x 36.0x 2.2x 9.7x 22.4x

Undervalued on a forward basis

19

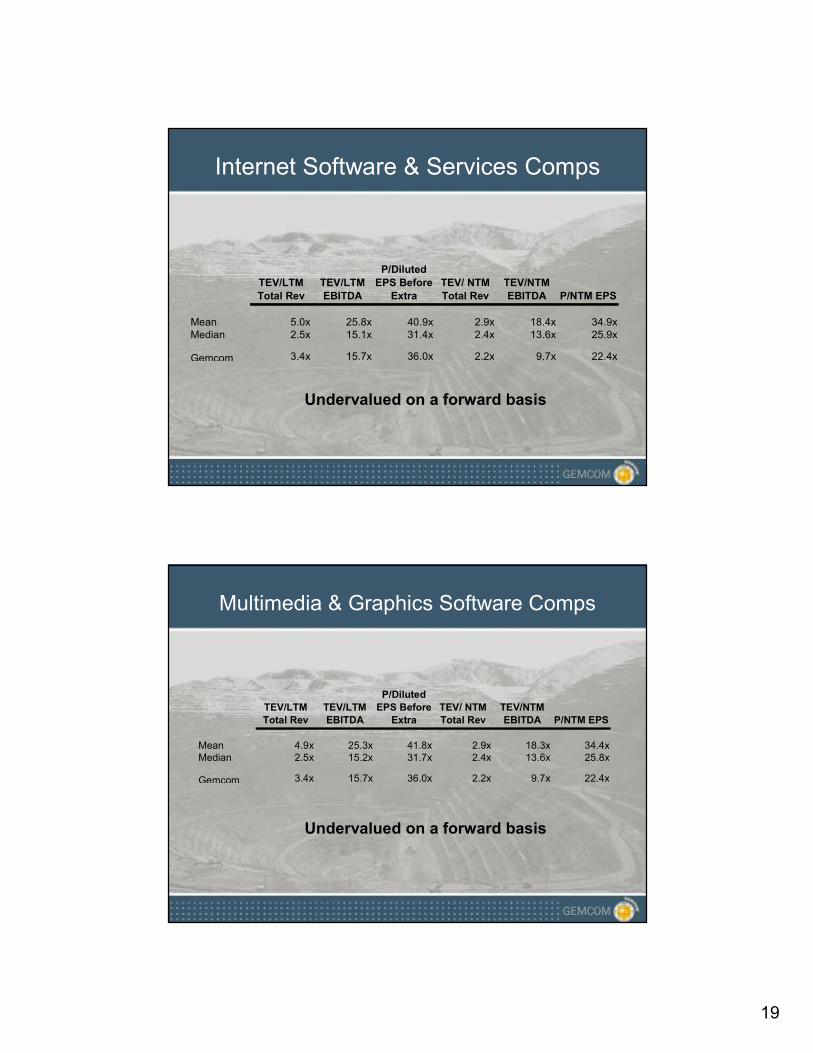

Internet Software & Services Comps

TEV/LTM

Total Rev

TEV/LTM

EBITDA

P/Diluted

EPS Before

Extra

TEV/ NTM

Total Rev

TEV/NTM

EBITDA P/NTM EPS

Mean 5.0x 25.8x 40.9x 2.9x 18.4x 34.9xMedian 2.5x 15.1x 31.4x 2.4x 13.6x 25.9x

Gemcom 3.4x 15.7x 36.0x 2.2x 9.7x 22.4x

Undervalued on a forward basis

Multimedia & Graphics Software Comps

TEV/LTM

Total Rev

TEV/LTM

EBITDA

P/Diluted

EPS Before

Extra

TEV/ NTM

Total Rev

TEV/NTM

EBITDA P/NTM EPS

Mean 4.9x 25.3x 41.8x 2.9x 18.3x 34.4xMedian 2.5x 15.2x 31.7x 2.4x 13.6x 25.8x

Gemcom 3.4x 15.7x 36.0x 2.2x 9.7x 22.4x

Undervalued on a forward basis

20

Security Software & Services Comps

TEV/LTM

Total Rev

TEV/LTM

EBITDA

P/Diluted

EPS Before

Extra

TEV/ NTM

Total Rev

TEV/NTM

EBITDA P/NTM EPS

Mean 5.0x 24.7x 41.0x 2.9x 18.1x 34.3xMedian 2.6x 15.2x 31.5x 2.4x 13.6x 25.8x

Gemcom 3.4x 15.7x 36.0x 2.2x 9.7x 22.4x

Undervalued on a forward basis

Technical & System Software Comps

TEV/LTM

Total Rev

TEV/LTM

EBITDA

P/Diluted

EPS Before

Extra

TEV/ NTM

Total Rev

TEV/NTM

EBITDA P/NTM EPS

Mean 4.9x 24.8x 43.0x 2.9x 17.8x 35.4xMedian 2.7x 15.3x 32.4x 2.4x 13.5x 25.7x

Gemcom 3.4x 15.7x 36.0x 2.2x 9.7x 22.4x

Undervalued on a forward basis

21

Reasons to Hate the Stock

Why I’m Hesitant

• Valuation may be rich

• Business ever changing, relies heavily on R&D

• Half of revenue stream dependent on bulky license sales

• Strengthening CAD

• Dilutive warrants, options could suppress stock in short-term

• Business difficult to understand

• No catalysts

• Integration risk

• Transaction comp

• 52-week highs

22

Missed the Boat?

…or more room to run?

GARP?