“the philippine experience in developing a vision/strategy for financial services to the poor and...

TRANSCRIPT

“The Philippine Experience in Developing A Vision/Strategy for

Financial Services to the Poor and Adjusting the Regulatory Framework”

Ricardo P. LirioManaging Director

Bangko Sentral ng Pilipinas

•High overhead costs•High incidence on non-payment of

loans

Social Intermediation vs. Financial Intermediation

•Distorted the financial market

•Suppressed the development of private financing institutions

BanksShy away from granting loans

•High risk

•High operational cost

Informal Financing

Institutions

Weak institutional capacity

of the 75 million Filipinos are living below the poverty lineSource:World Development Poverty Indicators, 2001 (Survey Year 1997)

36.8%

are engaged in entrepreneurial activities but only one-fourth had access to loans.Source:Annual Poverty Indicators Survey, 1999

3 out of 5 Filipino families

Philippine population grows by 2.36% or by 1.7 million persons a year.

Philippine Commission to Fight Poverty

1. Promote and sustain economic growth to create employment and livelihood opportunities.

2. Sustain growth based on people-friendly strategies.

3. Expand social services to provide minimum basic needs.

4. Foster sustainable income-generating community projects

5. Build capabilities of the poor to help themselves

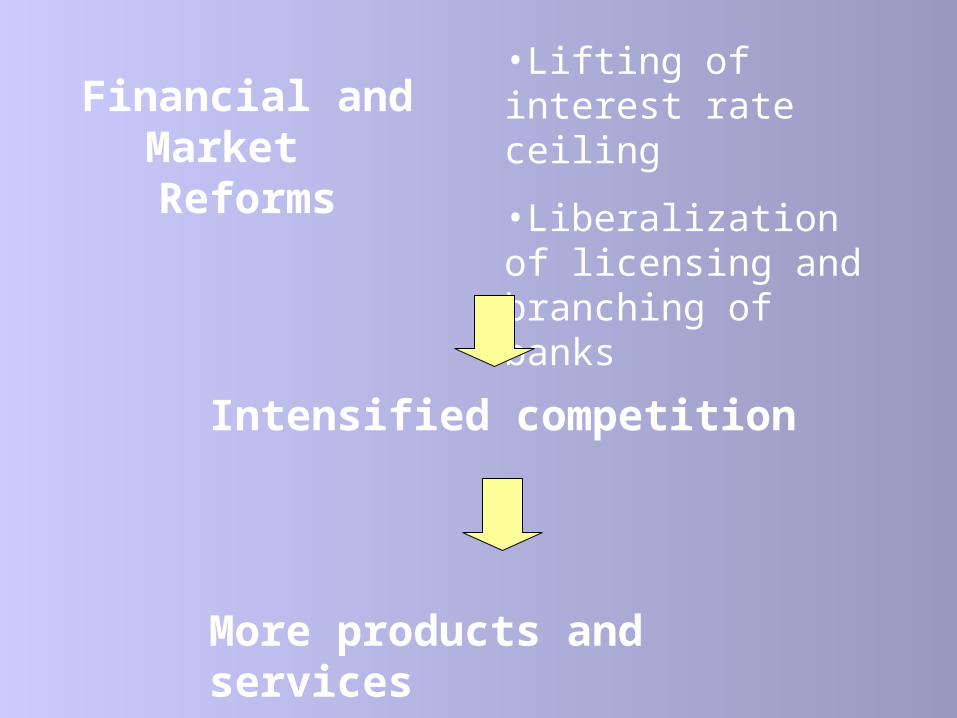

Financial and Market Reforms

•Lifting of interest rate ceiling

•Liberalization of licensing and branching of banks

Intensified competition

More products and services

Mandated Credit Allocation of Loanable Funds

• PD 71725% for agri-agra loans(10% for agrarian and 15% for agricultural loans)

• R.A. 6977 as amended by R.A. 82296% for small enterprises

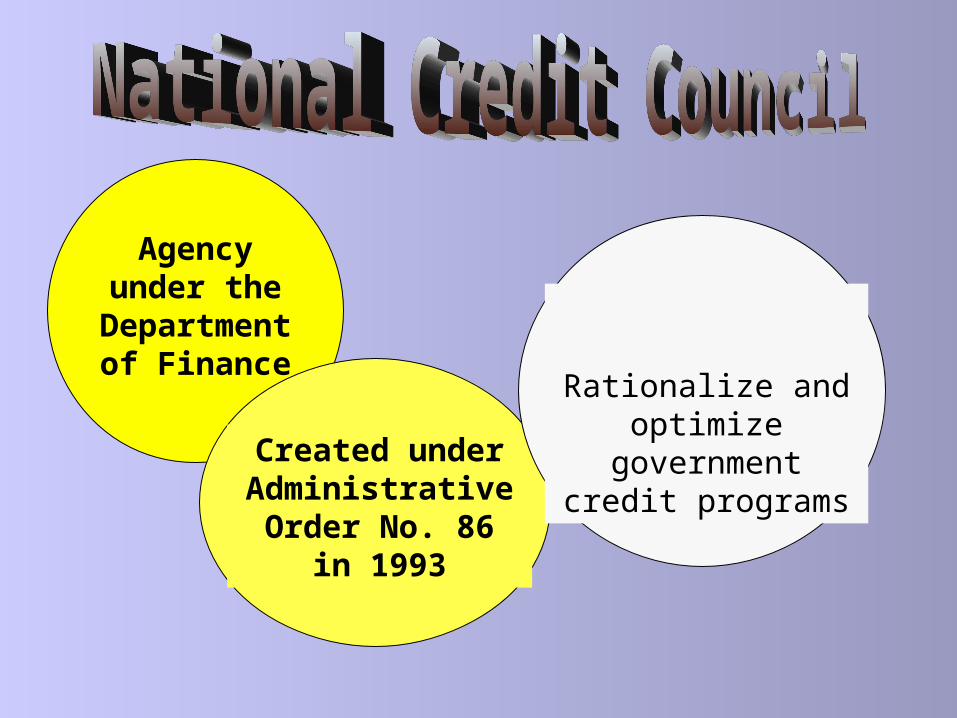

Agency under the

Department of

Finance

Created under Administrative Order No. 86 in

1993

Rationalize and

optimize government credit

programs

“To have a viable and sustainable private micro (Financial) market, with the government providing a supportive and appropriate policy environment and institutional framework to that market.”

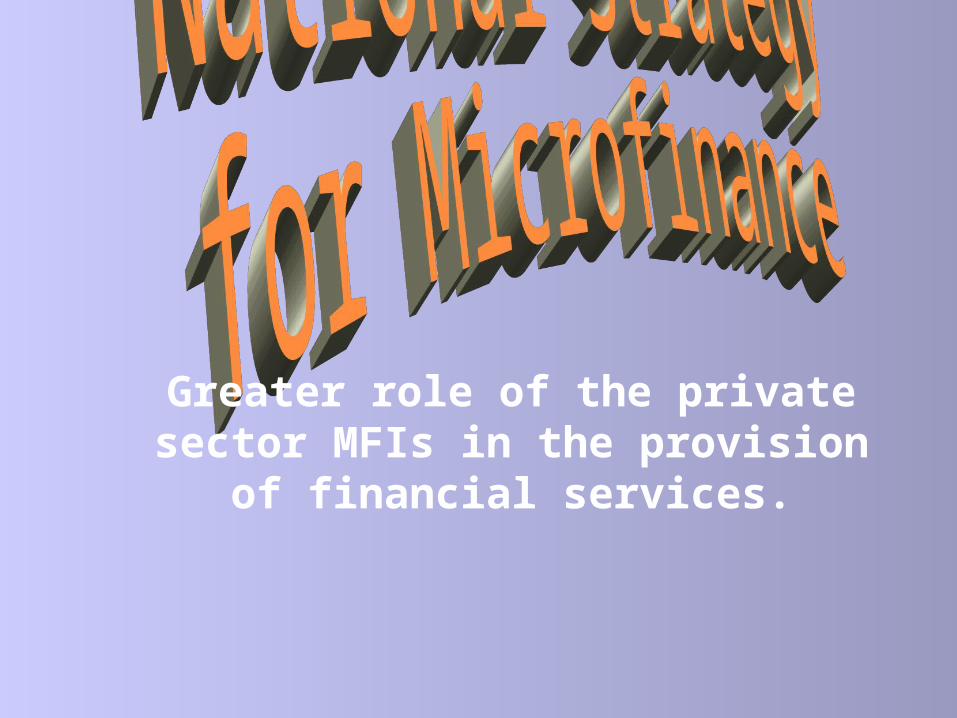

Vision of National Strategy for Microfinance

Greater role of the private sector MFIs in the provision of

financial services.

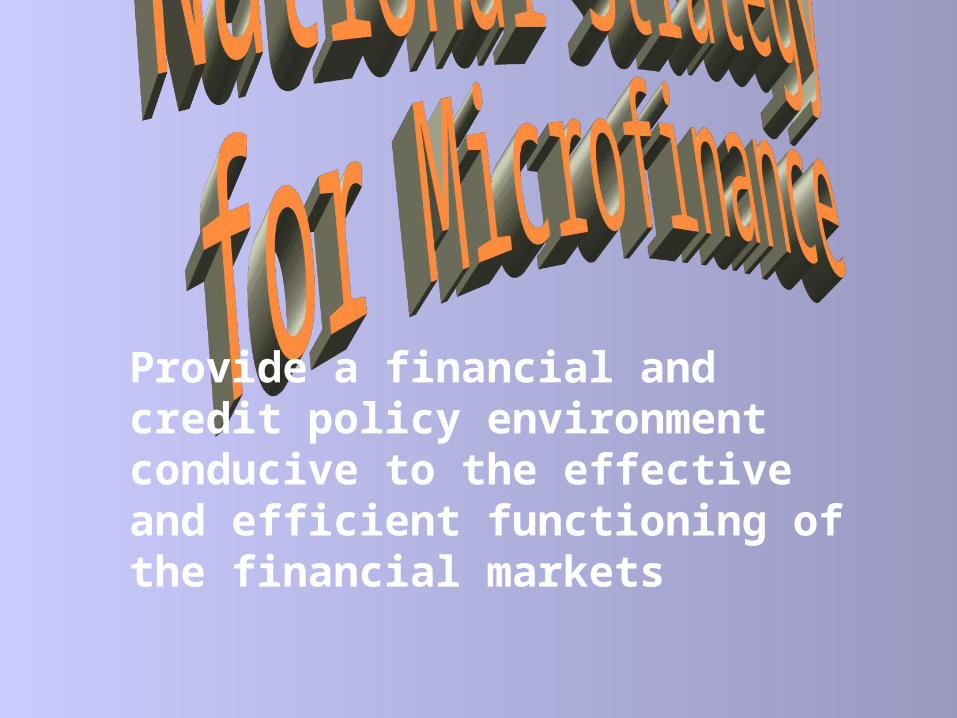

Provide a financial and credit policy environment conducive to the effective and efficient functioning of the financial markets

Establish market-oriented financial and credit policy environment, which is conducive for the broadening and deepening of microfinancial services. Broadening and deepening mean the development of new product lines and services, the design and implementation of new microfinance technologies and practices which will result to increased microfinance intermediation between the target clientele and MFIs.

Implement capacity building program for MFIs

Social Reform and Poverty

Alleviation Act (1997)

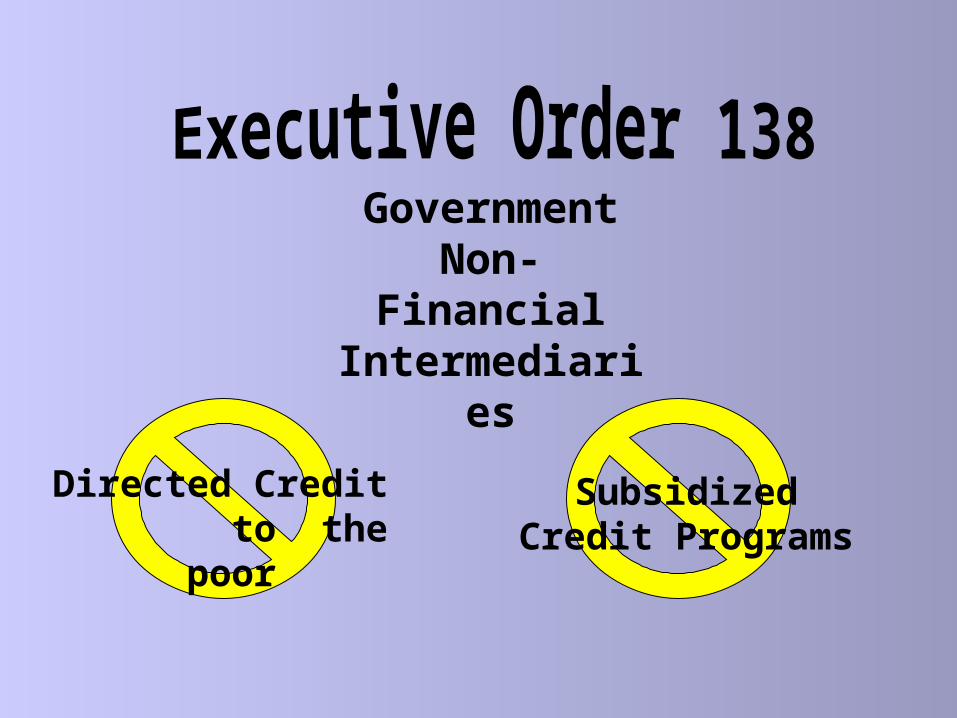

Executive Order 138

(1999)

Agriculture and Fisheries Modernizatio

n Act (RA 8435)

•Role of the state in institutionalizing and enhancing a Social Reform Agenda that would pursue programs for the disadvantaged sectors

•Creation of People’s development Trust Fund

Government Non-

Financial Intermediari

es

Directed Credit to the poor

Subsidized Credit Programs

Complements Executive Order

138

Phase-out of agriculture

directed credit

programs

Action Plan

“Provide an appropriate supervisory and regulatory framework for

Microfinance Institutions which will enable them to engage in the

development of new and innovative product lines and services

appropriate for the demand for financial services/products by poor households and microenterprises”

Requirements for Granting Unsecured Loans

At least one co-maker

Proof of financial capacity

(documents)

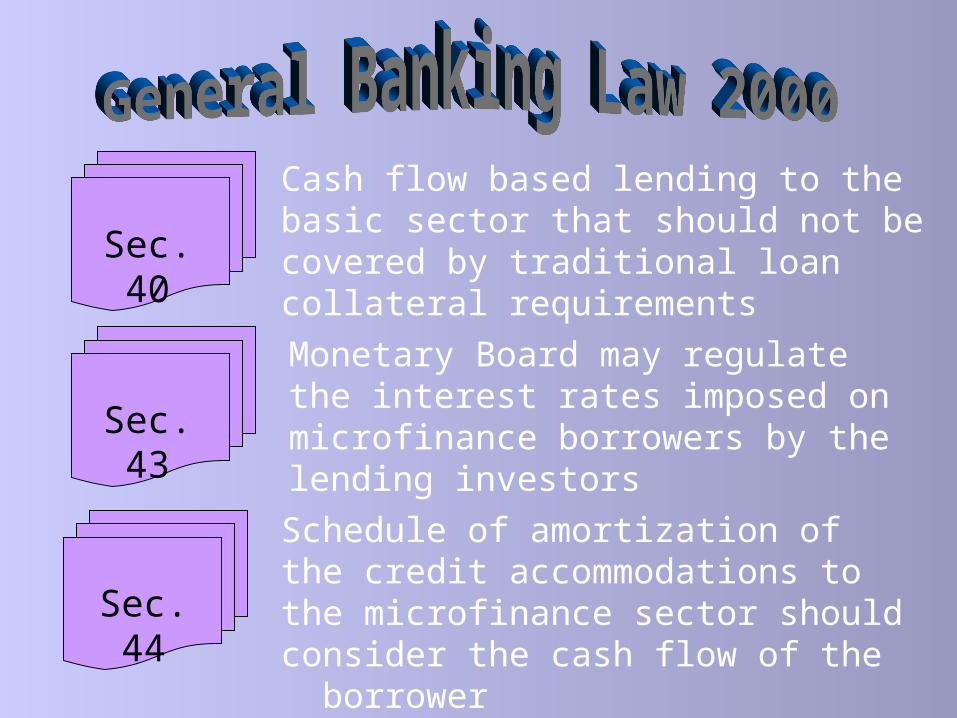

Sec. 40

Sec. 43

Sec. 43

Sec. 44

Cash flow based lending to the basic sector that should not be covered by traditional loan collateral requirements

Monetary Board may regulate the interest rates imposed on microfinance borrowers by the lending investors

Schedule of amortization of the credit accommodations to the microfinance sector should consider the cash flow of the borrower

Bangko Sentral ng Pilipinas

272

273

282

Guidelines for implementing the provisions in the General Banking Law 2000

Licensing of Microfinance Oriented Banks

Rediscounting facilities for Microfinance Loans

Bangko Sentral ng PilipinasMinimum Capital

Requirement Type of Bank

Pesos(Millions)

US $(Millions)

Thrift Bank(within Metro

Manila)325 6.373

Thrift Bank(outside Metro

Manila)52 1.020

Rural Bank(1st,2nd,3rd class) 6.5 .127

Rural Bank(other areas) 5 .098

Bangko Sentral ng PilipinasReserve Requirement

•Maintain % of deposits as cash, deposits in BSP and government securities

Type of BankDemand Deposit

Savings Deposit

Thrift Bank 8% + 2%* 6% + 2%*

Rural Bank 7% 2%

*Liquidity reserve =2%

Bangko Sentral ng PilipinasReserve Requirement

•Serves as liquidity buffer in case of sudden inadequacy of operational funds

•Prompts bank to adopt an effective fund allocation system

Bangko Sentral ng PilipinasLoan Classification and Valuation Requirement

ClassificationValuation

RequirementEspecially Mentioned

5%

SubstandardUnsecured

Secured25%10%

Doubtful 50%

Loss 100%

Bangko Sentral ng Pilipinas

Risk – Based Supervision Approach

•Considers other types of risk (liquidity, interest rate, market, compliance, operations)

•Overall assessment of the system

•Mitigates examiners’ biases against unsecured loans

Bangko Sentral ng PilipinasOpportunity Microfinance Bank

(started its operations on August 17, 2001)

Figures as ofDecember 31,

2001

Total Number of Clients Served

8,874

Total Loans Provided

P60.262 million US$1.182 million

Deposits Generated

P12.429 millionUS$.244 million

Dutch

International Micro Investment (Germany)

20%

Microenterprise Bank(started its operations on November 21, 2001)

International Finance Corporation

(10%)

Netherlands Development Finance

Company (10%)

Bangko Sentral ng PilipinasCARD Rural Bank

•Pioneer of microfinance lending in the Philippines

•Started as a non-stock non-profit organization offering savings deposit and lending services under the Landless People’s Fund

•Authorized to operate as a bank in 1997

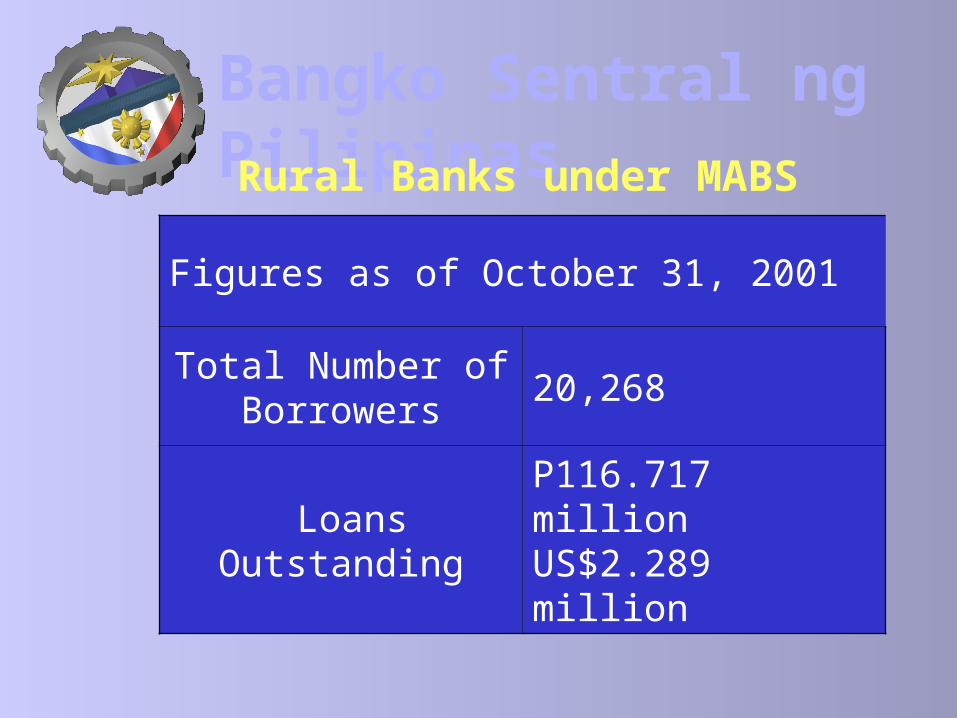

Bangko Sentral ng PilipinasRural Banks under MABS

Figures as of October 31, 2001

Total Number of Borrowers

20,268

Loans Outstanding

P116.717 million US$2.289 million

Bangko Sentral ng Pilipinas

Microenterprise Access to Banking Services

•USAID-financed effort operated by the Rural Bankers Association of the Philippines

•Aims to accelerate national economic transformation by encouraging rural banks to significantly expand microenterprise access to innovative microfinance services

•Under the mandate of the Cooperative Development Authority

•Allowed to mobilize deposits from their members

•Resources come from the capital contribution of members and their surplus from credit, marketing and economic activities

•Not under any regulatory body

•Developed and adopted their own standards

•Microfinance Council of the Philippines, Inc. and other microfinance networks provide self-regulatory measures to their members

Government Non-Governmental Organizations

Other Civic

Groups

Philippine Coalition

for Microfinanc

e Standards

To develop and promote standards for NGO microfinance operations that seek to provide the poor with greater access to financial services on a viable and sustainable basis

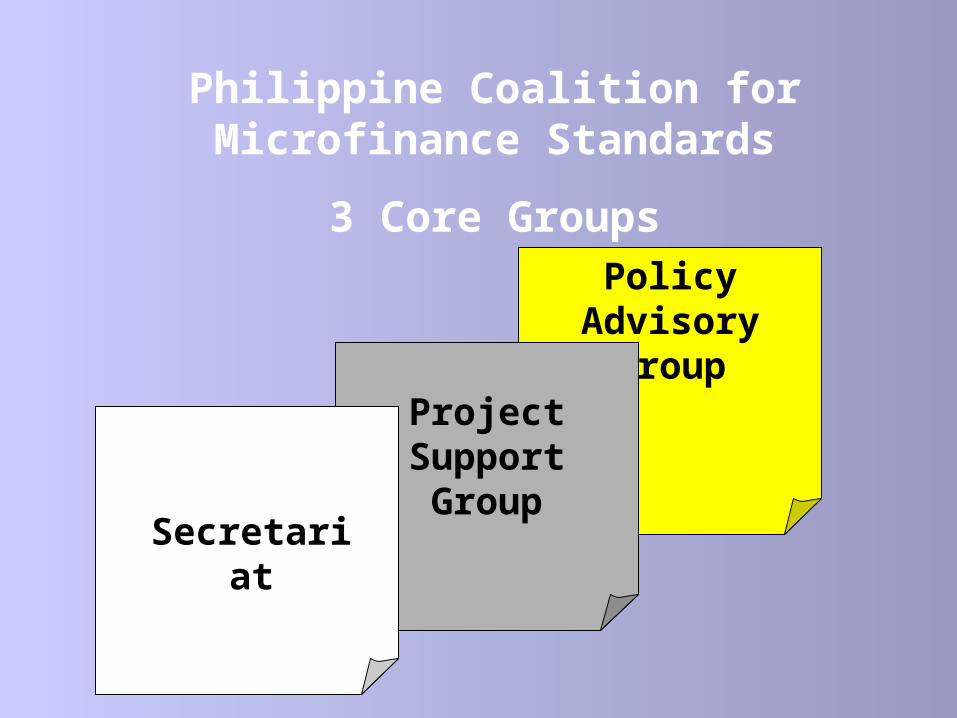

Philippine Coalition for Microfinance Standards

3 Core GroupsPolicy

Advisory Group

Project Support Group

Secretariat

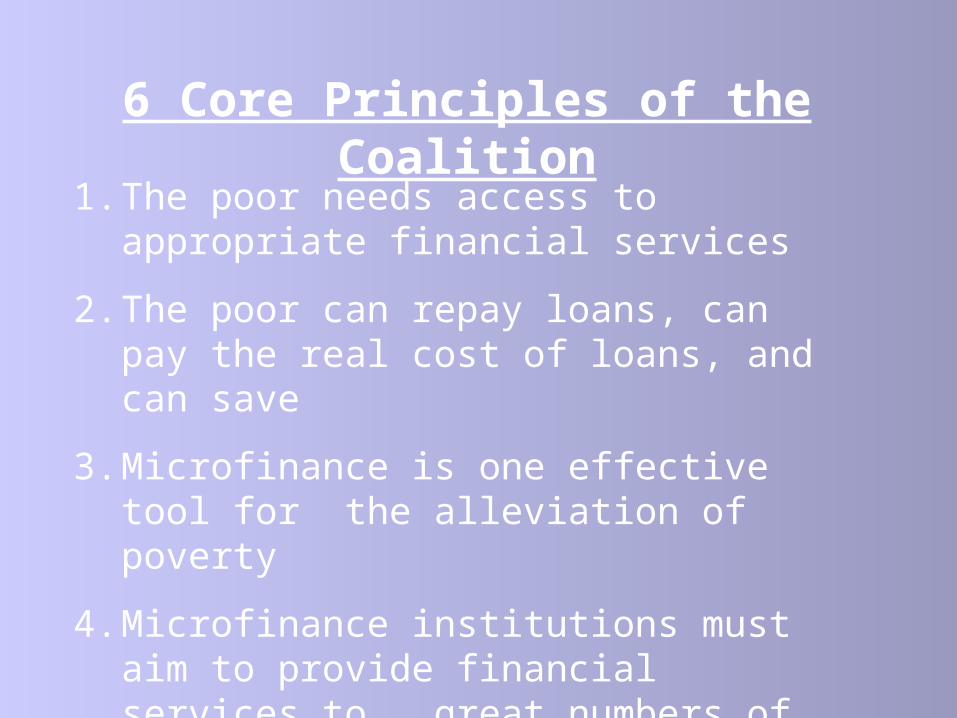

6 Core Principles of the Coalition

1. The poor needs access to appropriate financial services

2. The poor can repay loans, can pay the real cost of loans, and can save

3. Microfinance is one effective tool for the alleviation of poverty

4. Microfinance institutions must aim to provide financial services to great numbers of poor people

6 Core Principles of the Coalition

5. Microfinance can and should be undertaken on a viable and sustainable basis

6. Microfinance non-governmental organizations must develop performance standards that will help define and govern the microfinance industry toward greater reach and sustainability

Microfinance is the cornerstone of the current administration’s fight against poverty.

Lead Agency to Promote Microfinance

•Spearheads the standardization of the chart of accounts and the creation of performance standards for credit cooperatives

•Created a Technical Working Group (TWG) that will develop a uniform set of standards applicable to all types of microfinance institutions

•National Credit Council

•National Anti-Poverty Commission

•Bangko Sentral Ng Pilipinas

•People’s Credit and Finance Corporation

•Cooperative Development Authority

•Agricultural Credit Policy Council

•National Council for Filipino Women

•Bureau of Rural Workers

•Rural Bankers Association of the Philippines

•Microfinance Council of the Philippines

•Landbank of the Philippines

•Philippine Deposit Insurance Corporation

Differentiate Social from financial Intermediation ProgramsInitiate reforms that will create a financial system conducive to operations of financing conduits

Enact laws upholding the fight against poverty through microfinance.

Take on strategies promoting microfinance as a primary tool to fight poverty

Synergize anti-poverty efforts with non-governmental organizations and other stakeholders