the post-crisis cmbs market - bfjlaward.com · the post-crisis cmbs market: will regulations...

TRANSCRIPT

118 THE POST-CRISIS CMBS MARKET: WILL REGULATIONS PREVENT ANOTHER MARKET MELTDOWN? SPECIAL REAL ESTATE ISSUE 2015

The Post-Crisis CMBS Market: Will Regulations Prevent Another Market Meltdown?FRANK J. FABOZZI, JOE MCBRIDE, AND MANUS CLANCY

FRANK J. FABOZZI

is a professor of finance at EDHEC Business School in Nice, [email protected]

JOE MCBRIDE

is a research analyst at Trepp LLC in New York, [email protected]

MANUS CLANCY

is a senior managing director at Trepp LLC in New York, [email protected]

Structured financing techniques have boosted liquidity in the capital mar-kets and reduced borrowers’ reliance on banks. Asset-backed securities

issued through the securitization process are one example. Just prior to the onset of the global f inancial crisis, which can be traced back to the subprime mortgage crisis starting in the early summer of 2007—a crisis allegedly caused in part by securitization—major public off icials in the United States were commenting on the critical role of securitization in the f inancial markets. In congressional testimony on April 17, 2007, then Chair of the Federal Deposit Insurance Corporation Sheila Bair des-cribed the benef its of securitization as follows:

Securitization has had a positive impact on credit availability to the overall benefit of the nation’s hom-eowners. It is an essential process in the U.S. mortgage markets. By pack-aging loans into securities and diver-sifying risk by selling these securities to a broad array of investors, securiti-zation has increased credit availability to borrowers, reduced concentration of mortgage risk and improved the liquidity of the mortgage markets. (Blair [2007])

Several months after the beginning of the financial crisis, then U.S. Secretary of the Treasury Henry M. Paulson, Jr., described securitization in a speech as “a process that has been extremely valuable in extending the availability of credit to millions of home-owners nationwide and lowering their cost of financing” (Paulson [2007]). More recently, in January 2012, John Walsh, then acting Comptroller of the Currency, stated:

Securitization is sometimes maligned and frequently misunderstood, and its importance to our nation’s economy is often not fully appreciated… It is hard to imagine full recovery of the financial system without the liquidity and funding avenues provided by a well-functioning securitization market. (Walsh [2012])

The commercial mortgage-backed securities (CMBS) market did for commercial real estate (CRE) loans precisely what these commentators indicated. Before the turn of the century, banks and life insurers were the first and second suppliers, respectively, of capital to the CRE market. At the turn of the century, CMBS became the second major source replacing life insurers.

In this article, we review several issues that will play an important role in fostering

JPM-RE-FABOZZI.indd 118JPM-RE-FABOZZI.indd 118 9/18/15 4:13:27 PM9/18/15 4:13:27 PM

IT IS IL

LEGAL TO REPRODUCE THIS A

RTICLE IN

ANY FORMAT

Copyright © 2015

THE JOURNAL OF PORTFOLIO MANAGEMENT 119SPECIAL REAL ESTATE ISSUE 2015

recovery of the CMBS market or impeding the CMBS market or particular segments within that market. Although the most obvious is the threat of rising rates as a result of the end of quantitative easing, interest rate forecasts will not be discussed. Instead, we will look at three issues. The first is the risk-retention rule applicable to CRE loans and CMBS under the Dodd–Frank Wall Street Reform and Consumer Protection Act of 2010. The second is the U.S. federal banking regulators’ adop-tion of the U.S. Basel III rule. Finally, we discuss federal government participation in the reinsurance market for terrorist insurance. We begin with a brief review of the development of the market and its current state, popu-larly referred to as CMBS 2.0.

MARKET DEVELOPMENT

The CMBS market essentially emerged from the Resolution Trust Corporation (RTC) resolution pro-cess, which was the vehicle for securitizing and selling off defaulted bank loans. From this, the CMBS market was born in the mid-1990s. As with the residential MBS market, although the original use of securitization was to provide liquidity to loans originated by depository institutions and retained in their portfolio, securitiza-tion became an outlet for CRE loan originations by depository institutions and thereby an important funding source for the CRE loan market.

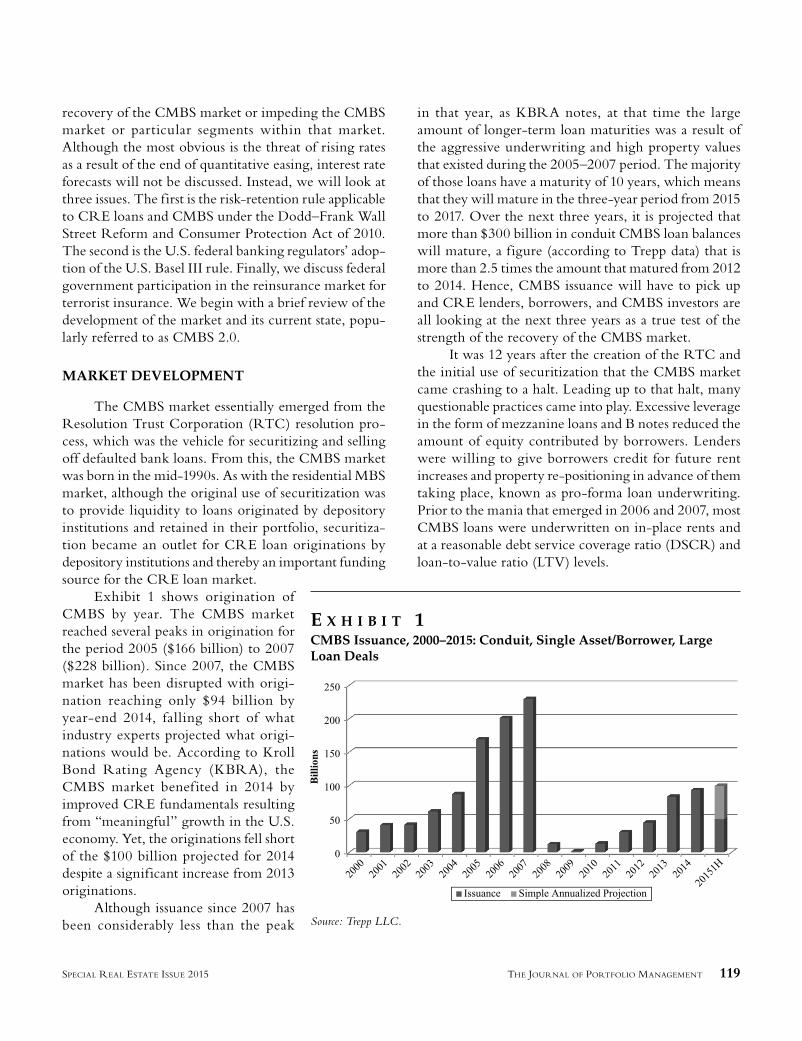

Exhibit 1 shows origination of CMBS by year. The CMBS market reached several peaks in origination for the period 2005 ($166 billion) to 2007 ($228 billion). Since 2007, the CMBS market has been disrupted with origi-nation reaching only $94 billion by year-end 2014, falling short of what industry experts projected what origi-nations would be. According to Kroll Bond Rating Agency (KBRA), the CMBS market benef ited in 2014 by improved CRE fundamentals resulting from “meaningful” growth in the U.S. economy. Yet, the originations fell short of the $100 billion projected for 2014 despite a significant increase from 2013 originations.

Although issuance since 2007 has been considerably less than the peak

in that year, as KBRA notes, at that time the large amount of longer-term loan maturities was a result of the aggressive underwriting and high property values that existed during the 2005–2007 period. The majority of those loans have a maturity of 10 years, which means that they will mature in the three-year period from 2015 to 2017. Over the next three years, it is projected that more than $300 billion in conduit CMBS loan balances will mature, a figure (according to Trepp data) that is more than 2.5 times the amount that matured from 2012 to 2014. Hence, CMBS issuance will have to pick up and CRE lenders, borrowers, and CMBS investors are all looking at the next three years as a true test of the strength of the recovery of the CMBS market.

It was 12 years after the creation of the RTC and the initial use of securitization that the CMBS market came crashing to a halt. Leading up to that halt, many questionable practices came into play. Excessive leverage in the form of mezzanine loans and B notes reduced the amount of equity contributed by borrowers. Lenders were willing to give borrowers credit for future rent increases and property re-positioning in advance of them taking place, known as pro-forma loan underwriting. Prior to the mania that emerged in 2006 and 2007, most CMBS loans were underwritten on in-place rents and at a reasonable debt service coverage ratio (DSCR) and loan-to-value ratio (LTV) levels.

E X H I B I T 1CMBS Issuance, 2000–2015: Conduit, Single Asset/Borrower, Large Loan Deals

Source: Trepp LLC.

JPM-RE-FABOZZI.indd 119JPM-RE-FABOZZI.indd 119 9/18/15 4:13:27 PM9/18/15 4:13:27 PM

120 THE POST-CRISIS CMBS MARKET: WILL REGULATIONS PREVENT ANOTHER MARKET MELTDOWN? SPECIAL REAL ESTATE ISSUE 2015

Beginning in 2010, the CMBS market began anew with a commitment to stick to its more conservative roots. In fact, the loans that emerged from the CMBS rebirth were done with lower leverage and without any pro-forma underwriting. We are now five years into the CMBS renewal and a certain leniency has begun to creep back into CMBS underwriting. However it is still too early to tell how far this second evolution will take us. The first cycle took a dozen years to play out, and we are not even half as far into the revival. Only time will fully tell if the market has learned its lessons from 2007 and 2008.

Exhibit 2 shows the LTV and DSCR for new-issue conduit deals from 2000 to 2015. Since about 2014, credit ratings agencies and some CMBS investors have expressed concerns about slipping underwriting standards. New-issue conduit deals are exhibiting increasing weighted average LTVs but fairly steady weighted average DSCR levels. Debt yields have steadily decreased since the 2010 issuance restart, reaching 11.01% in 2014 compared with 14.02% in 2010. On an LTV and DSCR basis, the cur-rent cycle has room to run before hitting pre-crisis levels pushing 70% leverage and 1.4× debt coverage.

So far in 2015, the weighted average LTV on new issue conduit loans is 66.68% and DSCR is a healthy

1.86×. Credit ratings agencies, B-piece buyers, and investment-grade investors have their eyes on the upward creep of leverage, interest-only (IO) loans, and pro-forma underwriting this time around. New issue bond spreads widen when there is enough negativity about a certain CMBS collateral pool. The question is how much will it take for investors to start discriminating between deals enough for issuers to take notice. There is already some tiering in the primary market based on who originates loans in a pool, property-type concen-tration, geographic distribution, and overall collateral financials. The question is when those price pressures will be strong enough to mark an underwriting line in the sand.

RISK-RETENTION RULE UNDER DODD-FRANK ACT

Six federal agencies are responsible for determining the risk-retention rule under the Dodd–Frank Act: the Board of Governors of the Federal Reserve, the Fed-eral Deposit Insurance Corporation, the Off ice of the Comptroller of the Currency, the Securities and Exchange Commission, Department of Housing and Urban Development, and the Federal Housing Adminis-

tration. The initial rule proposed by these regulators was revised based on industry comments that resulted in a re-proposal that relaxed or removed some of the more hotly debated aspects of the rule, such as the removal of the premium capture cash reserve account and the permission for issuers to sell the 5% retained interest to B-piece buyers. Although in the case of residential mortgages, the re-proposal loosened the standards for qualified resi-dential mortgages, the bar for qualified commercial real estate loans (QCRE) remained overly restrictive relative to his-torical delinquency and loss outcomes.

Risk retention is an attempt by lawmakers to improve the underwriting of collateral pools of securitized prod-ucts by forcing issuers to maintain some meaningful “skin in the game.” Under the current version of the rule, issuers of securitizations, B-piece buyers, or some combination thereof, will be required

E X H I B I T 2New Issue Conduit CMBS LTV and DSCR

Source: Trepp LLC.

JPM-RE-FABOZZI.indd 120JPM-RE-FABOZZI.indd 120 9/18/15 4:13:28 PM9/18/15 4:13:28 PM

THE JOURNAL OF PORTFOLIO MANAGEMENT 121SPECIAL REAL ESTATE ISSUE 2015

to hold 5% of the fair value of the transaction for five years. However, qualif ied mortgages under the rule would be exempt from risk retention. In other words, if a CMBS deal had $100 million in CRE loans as col-lateral and half of the balance met the qualified mortgage requirement, the issuer or B-piece buyer would only be required to retain 5% of the $50 million of unqualified collateral—or 2.5% of the whole issuance. It is easy to see how changing the parameters of a qualified mortgage could shift the scope of risk retention dramatically.

Under the re-proposal, a qualif ied commercial real estate loan must meet the criteria shown in the second column in Exhibit 3. Based on these parameters, looking at Trepp’s public conduit universe of CMBS deals, about 3.58% of loans (by balance) would be considered qualif ied (see Exhibit 4). That compares with a “vast majority” of loans in the residential MBS space that f it the Qualif ied Residential Mortgage criteria.

In their most recent comment letter, the CRE Financial Council (CREFC) suggested some minor changes to the qualified mortgage parameters that sig-nif icantly broadened the qualif ied pool without sac-rif icing its credit quality. The changes would allow 30-year amortization for all loan property types, elimi-nate the loan term minimum, and allow interest-only loans with LTVs of 50% or less. The CREFC’s pro-posed qualified commercial real estate loan parameters

are shown in the third column of Exhibit 3 with the changes shaded. Exhibit 4 compares the impact of the parameters as per the re-proposal and two recommenda-tions by the CREFC for QCRE, the CREFC proposals differing with respect to the DSCR.

These small changes open up the pool of qualified mortgages to include 15.6% of loan balance historically. Cumulative losses on the larger qualified pool is 0.74%, which is less than the loss on the regulator’s proposed qualified pool (0.83%, according to Exhibit 4). There is, as seen in Exhibit 4, slightly more delinquency in CREFC’s qualified pool; 5.22% of loans were ever 90+ days delinquent as opposed to 4.25% in the proposal by regulators. However, the improved loss severity and the significant increase in loan balance that would be exempt from risk retention seem to outweigh the slight increase in delinquency caused by the CREFC’s pro-posed changes. The industry could more easily meet the CREFC QCRE loan standards, but it would still be stringent enough to accomplish what the regulators are trying to accomplish.

CRE loan securitization is a vital tool that tranches and distributes real estate credit risk to bond investors willing to take it. B-piece buyers specialize in underwriting transactions, valuing the lowest classes in the CMBS deal, and determining exactly how much yield they require to take on that risk. Investment-grade investors rely on the credit enhancement pro-

vided by those lower tranches to protect them from loan losses. These quali-f ied institutional investors specialize in securitized products, due diligence, and cash f low modeling. Rules that promote transparency and effective loan data disclosures are important and welcome, especially when it comes to pro-forma loan underwriting that uses projected instead of in-place appraisals and income levels to write loans. Risk retention does little to satisfy that need, however, and instead increases the cost of borrowing for property investors in the CRE market. Many aspects of the rule are benef icial, but the qualif ied mortgage exemption should be more in line with historical collateral per-formance to decrease the ultimate cost of implementing the law.

E X H I B I T 3Risk Retention: Re-Proposal by Regulators and by CREFC

JPM-RE-FABOZZI.indd 121JPM-RE-FABOZZI.indd 121 9/18/15 4:13:29 PM9/18/15 4:13:29 PM

122 THE POST-CRISIS CMBS MARKET: WILL REGULATIONS PREVENT ANOTHER MARKET MELTDOWN? SPECIAL REAL ESTATE ISSUE 2015

EX

HI

BI

T 4

QC

RE

Loa

n A

nal

ysis

: Re-

Pro

pos

al v

s. C

RE

FC S

ugg

esti

ons

Not

es:

“Eve

r 90

+%”

mea

ns th

e pe

rcen

tage

of l

oans

in th

at g

roup

that

was

eve

r 90

+ da

ys d

elin

quen

t.

*For

Re-

Pro

posa

l par

amet

ers,

see

Exh

ibit

3.

**C

RE

FC

sug

gest

ion

1 pa

ram

eter

s: 3

0-ye

ar a

mor

tizat

ion;

no

mat

urity

term

; 1.

5 D

SCR

(1.2

5 fo

r mul

tifam

ily;

1.7

for h

ospi

talit

y);

65 L

TV

(IO

Loa

ns L

TV

≤ 5

0)

***C

RE

FC

sug

gest

ion

2 pa

ram

eter

s: 3

0-ye

ar a

mor

tizat

ion;

no

mat

urity

term

; 1.

35 D

SCR

(1.2

5 fo

r mul

tifam

ily;

1.5

for h

ospi

talit

y);

65 L

TV

(IO

Loa

ns L

TV

≤ 5

0)

Sour

ce:

Tre

pp P

ublic

Con

duit

Uni

vers

e.

JPM-RE-FABOZZI.indd 122JPM-RE-FABOZZI.indd 122 9/18/15 4:13:30 PM9/18/15 4:13:30 PM

THE JOURNAL OF PORTFOLIO MANAGEMENT 123SPECIAL REAL ESTATE ISSUE 2015

ADOPTION OF BASEL III

Approximately half of the outstanding CRE debt has been supplied by banks. Consequently, the banking sector is an important source of capital for CRE financing. Risk-based capital requirements affect both the decision by bank management as to the allocation of loans to not just CRE lending but also to specific property types within the CRE market. Risk-weighted capital requirements are in addition to the risk-retention rules described in the previous section.

In July 2013, U.S. federal banking regulators adopted a final rule that increased bank capital require-ments, narrowing the definition of assets that can be included in computing bank capital, and revising the method for computing risk-weighted assets so as to make capital requirements more sensitive to risk.

Prior to the new rules, a risk weight of 100% was assigned to loans classified as High Volatility Commer-cial Real Estate (HVCRE). Under the new rules that went into effect on January 1, 2015, the risk weight was increased to 150% for HVCRE loans. The rationale of regulators is that because these properties embody unique risks, the maximum weighting of 150% should be assigned to HVCRE loans. Such loans include credit facilities whose purpose, prior to conversion to perma-nent financing, is for acquisition, development, or con-struction (unless certain criteria are met).

However, there are special rules, depending on the loan characteristics, for multifamily properties under the new rules. The risk weighting is either 100% or 50% with the latter weighting applied to loans that meet certain criteria. For multifamily construction loans, the higher risk weighting of 100% applies. CRE loans that are not classified as HVCRE loans and that do not qualify as 50% risk-weighted multifamily loans have a risk weighting of 100%.

The result of the new rule has resulted in higher capital requirements for CRE lending. For this reason, there is decreased motivation for banks to originate CRE loans because of lower potential returns on invested cap-ital and, as a result, decreased profitability. Realloca-tion of capital from CRE lending due to higher capital requirements to other sectors of the market that have lower capital requirements, and thereby offer higher potential return on capital than CRE lending, may result in decreased liquidity for all CRE loans. Given the amount of refinancing expected in the 2015–2017 period

mentioned in the previous section and the demand for new loans for construction, this may limit bank partici-pation in the market, requiring other suppliers of the capital market to step up their participation. Yet, his-torically neither life insurers nor originators for CMBS transactions have been capable of providing the amount of new financing and refinancing needed.

In addition, in CMBS transactions, the new risk-based capital requirements have raised the cost for retained mortgage servicing rights when banks either securitize or sell CRE loans that they have originated.

Of course, bank management can pursue a policy of passing along the higher costs associated with CRE lending onto the borrower rather than reducing partici-pation in the market. Whether borrowers will have the ability to pass along these costs to tenants or recapture those costs in providing their offerings to their customers will depend on national and/or regional economic con-ditions. With the prevailing low interest rates, it may be easier for borrowers to pass along the higher financial costs. With the expected higher future interest rates, it may be more difficult for borrowers to do so, making borrowers more sensitive to higher borrowing costs.

The new rule may result in bank management reallocating exposure within the CRE market. Given the more favorable treatment of multifamily properties that would qualify for the lower weighting, this may increase origination of such loans reducing the capital that is allocated to other property types. Moreover, construction loans for multifamily properties may be adversely affected because such loans cannot qualify for the lower weighting.

FEDERAL TERRORISM BACKUP INSURANCE

Following the unprecedented losses resulting from the September 11, 2001, terrorist attacks, property and casualty (P&C) insurers reduced the availability of ter-rorism insurance coverage for commercial properties. Concerned with the impact of reduced availability of such coverage that would be sought by CRE lenders and CMBS investors in the post-9/11 era, Congress passed the Terrorism Risk Insurance Act (TRIA) in 2002 to provide for catastrophic federal reinsurance for terrorism risks.

Under TRIA, P&C insurers are required to offer terrorism coverage to their commercial policyholders with the federal government providing reinsurance to

JPM-RE-FABOZZI.indd 123JPM-RE-FABOZZI.indd 123 9/18/15 4:13:32 PM9/18/15 4:13:32 PM

124 THE POST-CRISIS CMBS MARKET: WILL REGULATIONS PREVENT ANOTHER MARKET MELTDOWN? SPECIAL REAL ESTATE ISSUE 2015

private insurers by reinsuring them for a portion of their terrorism-related losses resulting from terrorist attacks. The concern for lawmakers was the potential cost to tax-payers by the U.S. government becoming a reinsurer and the potential that federal involvement would impede the development of the private reinsurance market. Hubbard and Deal [2004] analyzed the need for TRIA because of the difficulty of the private sector’s ability to fully absorb terrorism risk. They also provided an analysis of the potential impact on the U.S. economy if the pro-gram is not extended beyond the December 2005 of the original act.

TRIA is now a vital component of the CMBS and CRE markets. As of December 31, 2014, TRIA had been reauthorized twice since its passage in 2002 (in 2005 and in 2007), each time shifting more of the risk from the public sector to the private sector. The 2007 reautho-rization was scheduled to terminate on December 31, 2014. Consequently, another issue impacting the CMBS market going into 2015 was the renewal of this federal reinsurance program, and if it was renewed, the concern was that there would be major changes, such as scaled-back coverage provisions.

The concern for renewal of TRIA was that CRE loan documents typically specify that terrorism insur-ance be in force over the loan’s life. CRE loan docu-ments vary as to what must be done if TRIA is not renewed. There are sunset provisions in some CRE loans that cancel all terrorism insurance coverage if TRIA is not renewed. In the absence of TRIA, the waiving of terrorism insurance can vary by property type and location of that property. For example, the requirement for terrorism insurance may be waived for property far away from metropolitan areas. There are some CRE loans whose documentation may impose a maximum premium on what the borrower must pay for terrorism insurance if a federal program is not available. Failure of a borrower to obtain terrorism insurance would require CMBS servicers to begin force-placed terrorism insur-ance coverage; the cost of that insurance is likely to be at a prohibitively high cost, and if that insurance cannot be obtained, the borrower would be in violation of the loan terms. An increase in premiums for terrorism insurance in the absence of TRIA or substantial revi-sions that reduce reinsurance protection could result in a decline in a property’s net operating income and raise investors’ required risk premium such that valuations will decline.

As a 2014 S&P report noted: “If history is any guide, commercial mortgage-backed securities (CMBS) credit and liquidity issues could develop if TRIPRA is not renewed or is cut back substantially.”1 In December 2014, just prior to the termination of the program, Fitch [2014] identified about 20 transactions that it rated that would be put on Rating Watch Negative if the pro-gram was not renewed. Although Fitch noted that the impact would vary from CMBS transaction to transac-tion, the ratings of office properties included in the pool of CMBS single-asset transactions would be negatively affected. Failure to renew the program could also nega-tively impact the ratings of multi-borrower transactions in cases where the number and size of the loans did not have sufficient coverage or the rest of the pool could not reduce the potential terrorism-related loss exposure.

On January 12, 2015, 12 days after the termina-tion of TRIA, Congress revised and extended the pro-gram through 2020. Under the revised and extended program—the Terrorism Risk Insurance Program Reau-thorization Act of 2015 (TRIPRA)—in the event of a terrorist attack, the share of the loss that insurers would be responsible for was increased significantly every year through 2020. Alternative mechanisms were considered by the GAO before passage of TRIPRA. The concern was the cost to taxpayers. As noted by several com-mentators, other than administrative costs, the program over the years that it was in effect (November 2002 to January 2015) did not impose any cost on taxpayers.2 The renewed structure for the program provides a good number of provisions for taxpayer protection by shifting more of the risk to the private sector. For example, there are triggering events that must be realized that are higher than under the 2007 reauthorization of TRIA.

A triggering threshold event means that payments under the program will be made by the federal govern-ment if a terrorist act occurs only if the total losses for the insurance industry exceed the threshold. Under TRIA, the triggering event threshold was set at $5 million, increased to $50 million in 2006, and then to $100 mil-lion in 2007, where it remained until December 2014. Under TRIPRA, the triggering event threshold begins at $100 million in 2015, increasing by $20 million a year until it reaches $200 million in 2020.

Another provision to shift the risk to the pri-vate sector is the increase in the amount of losses that the industry must cover through deductibles and co- payments (i.e., industry aggregate retention) before

JPM-RE-FABOZZI.indd 124JPM-RE-FABOZZI.indd 124 9/18/15 4:13:33 PM9/18/15 4:13:33 PM

THE JOURNAL OF PORTFOLIO MANAGEMENT 125SPECIAL REAL ESTATE ISSUE 2015

government payments are made. This amount was $10 billion in 2003, $12.5 billion in 2004, $15 billion in 2005, $25 billion in 2006, and $27.5 billion in 2007 where it stood until year-end 2014. TRIPRA increased the industry aggregate retention by $2 billion to $29.5 billion in 2015, increasing by an additional $2 billion a year to $37.5 billion in both 2019 and 2020.

Although there has been a resolution of federal ter-rorism insurance backup through December 31, 2020, market participants must monitor Congressional tem-perature for reauthorization of TRIPRA and the devel-opment of the private reinsurer market in the ongoing assessment of this risk and its impact on yield spreads.

CLOSING REMARKS

Clearly, the reboot of the CMBS market (CMBS 2.0) added much-needed discipline to the CMBS market. Lenders reverted to their roots of providing financing at more reasonable LTVs and DSCRs. Borrowers were no longer permitted to f inance their properties with microscopic equity levels and underwriters stopped giving borrowers credit for future lease increases. CMBS investors demanded quality collateral and new rating agencies emerged from the rubble, while existing ones became more challenging. The new discipline helped launch CMBS 2.0 on much firmer footing than existed in 2006 through early 2008. Now, an entirely new set of rules—driven not by market participants but by regulators—is emerging and will look to serve as addi-tional protection.

CMBS is now five years into its rebirth, and it is too early to tell if the additional market discipline will prevent another commercial real estate lending crisis. Similarly, the jury will remain out for some time as to whether the various new post-Dodd–Frank regulations will serve to effectively tap the brakes on bad lending habits or if they will lead to unintended consequences that will impede the further development and growth in the market.

ENDNOTES

1See Kay et al. [2014, p. 4].2See Hartwig [2013].

REFERENCES

Blair, S. “Possible Responses to Rising Mortgage Foreclo-sures.” Hearing before the Committee on Financial Services, U.S. House of Representatives, 110th Congress, April 17, 2007.

Hartwig, R. “Reauthorizing TRIA: The State of the Ter-rorism Risk Insurance Market.” Testimony before the United States Senate Committee on Banking, Housing and Urban Affairs, September 25, 2013.

Hubbard, R.G., and B. Deal. “The Economic Effects of Federal Participation in Terrorism Risk.” Report, Analysis Group, September 14, 2004.

Kay, L.D., T. Dolin, P.J. Eastham, and B.A. Hoeltz. “If TRIPRA Is Scaled Back, History Might Shed Light on the Impact to CMBS.” RatingsDirect, S&P, April 21, 2014.

Paulson, H.M., Jr. “Current Housing and Mortgage Market Developments.” Speech, Georgetown University Law Center, Washington, DC, October 16, 2007.

Walsh, J. Speech delivered at the American Securitization Forum Annual Conference, January 24, 2012. Available at http://www.occ.gov/news-issuances/speeches/2012/pub-speech-2012-11.pdf.

To order reprints of this article, please contact Dewey Palmieri at [email protected] or 212-224-3675.

JPM-RE-FABOZZI.indd 125JPM-RE-FABOZZI.indd 125 9/18/15 4:13:33 PM9/18/15 4:13:33 PM