the quantity theory and the keynesian theory of money

Post on 21-Dec-2015

240 views

TRANSCRIPT

The Quantity Theory and the The Quantity Theory and the Keynesian Theory of MoneyKeynesian Theory of Money

Classical analysis of prices and inflationClassical analysis of prices and inflation

This model gives an introduction to equilibrium in the money market

It further highlights important theoretical controversies between different schools of thought in economics Keynesians Monetarists

This model gives an introduction to equilibrium in the money market

It further highlights important theoretical controversies between different schools of thought in economics Keynesians Monetarists

Milton FriedmanMilton Friedman

The Quantity TheoryThe Quantity Theory

The quantity theory is by definition correct

MV = PY M = money supply V = velocity of circulation P = price level Y = national income

The quantity theory is by definition correct

MV = PY M = money supply V = velocity of circulation P = price level Y = national income

Money and the price levelMoney and the price level

Since MV = PY, it must be that P = MV/Y

Y is given like Yf (flexible prices), V is constant. Therefore, Change in M = change in P ”Inflation is anywhere and everywhere a

monetary phenomenon”

Since MV = PY, it must be that P = MV/Y

Y is given like Yf (flexible prices), V is constant. Therefore, Change in M = change in P ”Inflation is anywhere and everywhere a

monetary phenomenon”

AD2

AD1

O

AS

P1

Pric

e le

vel

National output

P2

Q1

The effect of printing extra money: the classical analysisThe effect of printing extra money: the classical analysis

Money and prices in Norway 1900-2000Money and prices in Norway 1900-2000

-20

-10

0

10

20

30

40

50

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990

MoneyCPI

-20

-10

0

10

20

30

40

50

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990

MoneyCPI

Money and Interest RatesMoney and Interest Rates

The Demand for MoneyThe Demand for Money

Keynesian money demandKeynesian money demand

Why do we need money: Transaction purposes Precautionary purposes Safety purposes

Money demand is above all dependent on: income (+) interest rates (-)

Why do we need money: Transaction purposes Precautionary purposes Safety purposes

Money demand is above all dependent on: income (+) interest rates (-)

THE DEMAND FOR MONEYTHE DEMAND FOR MONEY

The motives for holding money: liquidity preference

transactions and precautionary demand for money: L1

The motives for holding money: liquidity preference

transactions and precautionary demand for money: L1

The transactions-plus-precautionary demand for money: L1The transactions-plus-precautionary demand for money: L1

O

Ra

te o

f in

tere

st

L1

Active balances

THE DEMAND FOR MONEYTHE DEMAND FOR MONEY

The motives for holding money: liquidity preference

transactions and precautionary demand for money: L1

speculative demand for money: L2

The motives for holding money: liquidity preference

transactions and precautionary demand for money: L1

speculative demand for money: L2

The speculative demand for money: L2The speculative demand for money: L2

O

Ra

te o

f in

tere

st

L2

Idle balances

THE DEMAND FOR MONEYTHE DEMAND FOR MONEY

The motives for holding money: liquidity preference

transactions and precautionary demand for money: L1

speculative demand for money: L2

the total demand for money: L1 + L2

The motives for holding money: liquidity preference

transactions and precautionary demand for money: L1

speculative demand for money: L2

the total demand for money: L1 + L2

The total demand-for-money curve: L (= L1 + L2)The total demand-for-money curve: L (= L1 + L2)

O

Ra

te o

f in

tere

st

Total money balances

L ( = L1 + L2)

L2

L1

Money and Interest RatesMoney and Interest Rates

Equilibrium in the Money Market

Equilibrium in the Money Market

The supply of money curve: (a) exogenous money supplyThe supply of money curve: (a) exogenous money supply

O

Ra

te o

f in

tere

st

Quantity of money

MS

Equilibrium in the money marketEquilibrium in the money market

O

Ra

te o

f in

tere

st

L

Money

MS

re

Me

O

Ra

te o

f in

tere

st

L

Money

MS

re

Me

Equilibrium in the money marketEquilibrium in the money market

Relationship between theRelationship between theMoney and Goods MarketsMoney and Goods Markets

Relationship between the Money and Goods Markets

Relationship between the Money and Goods Markets

Effects of Monetary Changes on National

Income

Effects of Monetary Changes on National

Income

I

O O

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

MS

L

r1

Money InvestmentI1

r1

Effect of a rise in money supply:the traditional Keynesian transmission mechanism

Effect of a rise in money supply:the traditional Keynesian transmission mechanism

I2O O

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

MS

L

r1 r1

I

Money InvestmentI1

MS'

r2 r2

(b) Stage 2: r I (b) Stage 2: r I (a) Stage 1: MSr (a) Stage 1: MSr

Effect of a rise in money supply:the traditional Keynesian transmission mechanism

Effect of a rise in money supply:the traditional Keynesian transmission mechanism

O O

(a) Keynesian(a) Keynesian (b) New classical / Monetarist(b) New classical / Monetarist

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

r1

Investment Investment

I

I

I1 I1

r1

Different views on the demand for investmentDifferent views on the demand for investment

O O

(a) Keynesian(a) Keynesian (b) New classical / Monetarist(b) New classical / Monetarist

r1

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

r1

Investment Investment

I

I

I1 I1

r2

I2

Different views on the demand for investmentDifferent views on the demand for investment

O O

(a) Keynesian(a) Keynesian (b) New classical / Monetarist(b) New classical / Monetarist

r1

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

r1

Investment Investment

I

I

I1 I1

r2 r2

I2 I2

Different views on the demand for investmentDifferent views on the demand for investment

Relationship between the Money and Goods Markets

Relationship between the Money and Goods Markets

ISLM AnalysisISLM Analysis

Sir John Hicks (1904 – 1989)Sir John Hicks (1904 – 1989)

Inje

ctio

ns,

With

dra

wa

ls

OI1

S1R

ate

of i

nte

rest

O

r1

Assume that an interestrate of r1 gives investment

of I1 and saving of S1

Goods market equilibrium: deriving the IS curveGoods market equilibrium: deriving the IS curve

Inje

ctio

ns,

With

dra

wa

ls

OI1

S1

Assume that an interestrate of r1 gives investment

of I1 and saving of S1

Y1

Ra

te o

f in

tere

st

O

r1

Goods market equilibrium: deriving the IS curveGoods market equilibrium: deriving the IS curve

Inje

ctio

ns,

With

dra

wa

lsR

ate

of i

nte

rest

O

O

r1

I1

S1

Assume that an interestrate of r1 gives investment

of I1 and saving of S1

Y1

Y1

Goods market equilibrium: deriving the IS curveGoods market equilibrium: deriving the IS curve

Inje

ctio

ns,

With

dra

wa

lsR

ate

of i

nte

rest

O

O

r1

I1

S1

Assume that an interestrate of r1 gives investment

of I1 and saving of S1

Y1

Y1

a

Goods market equilibrium: deriving the IS curveGoods market equilibrium: deriving the IS curve

Inje

ctio

ns,

With

dra

wa

lsR

ate

of i

nte

rest

O

O

r1

I1

S1

Now assume that the interestrate falls to r2, giving

investment of I2 and saving of S2

Y1

Y1

I2

S2

Y2

r2

a

Goods market equilibrium: deriving the IS curveGoods market equilibrium: deriving the IS curve

Inje

ctio

ns,

With

dra

wa

lsR

ate

of i

nte

rest

O

O

r1

I1

S1

Now assume that the interestrate falls to r2, giving

investment of I2 and saving of S2

Y1

Y1

I2

S2

Y2

r2

a

Goods market equilibrium: deriving the IS curveGoods market equilibrium: deriving the IS curve

Inje

ctio

ns,

With

dra

wa

lsR

ate

of i

nte

rest

O

O

r1

I1

S1

Y1

Y1

I2

S2

Y2

r2

a

b

Now assume that the interestrate falls to r2, giving

investment of I2 and saving of S2

Goods market equilibrium: deriving the IS curveGoods market equilibrium: deriving the IS curve

Inje

ctio

ns,

With

dra

wa

lsR

ate

of i

nte

rest

O

O

r1

I1

S1

Now assume that the interestrate falls to r2, giving

investment of I2 and saving of S2

Y1

Y1

I2

S2

Y2

r2

IS

b

a

Goods market equilibrium: deriving the IS curveGoods market equilibrium: deriving the IS curve

The IS curveThe IS curve

Inje

ctio

ns,

With

dra

wa

lsR

ate

of i

nte

rest

O

O

r1

I1

S1

Y1

Y1

I2

S2

Y2

r2

IS

b

a

O O

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

Money National income

Y1

L'

Assume that at a level ofnational income, Y1,

the demand for money is L'

Money market equilibrium: deriving the LM curveMoney market equilibrium: deriving the LM curve

O O

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

Money National income

Y1

MS

L'

Assume that at a level ofnational income, Y1,

the demand for money is L'

Money market equilibrium: deriving the LM curveMoney market equilibrium: deriving the LM curve

O O

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

Money National income

Y1

MS

r1 r1

L'

Assume that at a level ofnational income, Y1,

the demand for money is L'

Money market equilibrium: deriving the LM curveMoney market equilibrium: deriving the LM curve

O O

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

Money National income

Y1

MS

r1 r1

L'

c

Assume that at a level ofnational income, Y1,

the demand for money is L'

Money market equilibrium: deriving the LM curveMoney market equilibrium: deriving the LM curve

O O

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

Money National income

Y1

MS

r1 r1

Y2

L"L'

c

Now assume that at the higher level of national income, Y2,

the demand for money rises to L"

Money market equilibrium: deriving the LM curveMoney market equilibrium: deriving the LM curve

O O

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

Money National income

Y1

MS

r1 r1

r2 r2

Y2

L"L'

c

Now assume that at the higher level of national income, Y2,

the demand for money rises to L"

Money market equilibrium: deriving the LM curveMoney market equilibrium: deriving the LM curve

O O

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

Money National income

Y1

MS

r1 r1

r2 r2

Y2

L"L'

c

d

Now assume that at the higher level of national income, Y2,

the demand for money rises to L"

Money market equilibrium: deriving the LM curveMoney market equilibrium: deriving the LM curve

O O

Ra

te o

f in

tere

st

Ra

te o

f in

tere

st

Money National income

Y1

LMMS

r1 r1

r2 r2

Y2

L"L'

c

d

Now assume that at the higher level of national income, Y2,

the demand for money rises to L"

Money market equilibrium: deriving the LM curveMoney market equilibrium: deriving the LM curve

O

Ra

te o

f in

tere

st

National income

LM

IS

Equilibrium in both the goods and money marketsEquilibrium in both the goods and money markets

O

Ra

te o

f in

tere

st

National income

IS

Y1

a

Assume that national incomeis currently at a level of Y1

LM

Equilibrium in both the goods and money marketsEquilibrium in both the goods and money markets

O

Ra

te o

f in

tere

st

National income

IS

r1

Y1

a

This gives a rate ofinterest of r1 (point a)

LM

Equilibrium in both the goods and money marketsEquilibrium in both the goods and money markets

O

Ra

te o

f in

tere

st

National income

IS

r1

Y1 Y2

a

But at r1, national incomeis below the goods market

equilibrium level (Y2)

b

LM

Equilibrium in both the goods and money marketsEquilibrium in both the goods and money markets

But as income rises, so therewill be a movement up theLM curve. The interest ratewill rise, thereby reducingnational income below Y2.

O

Ra

te o

f in

tere

st

National income

IS

r1

Y1 Y2

a b

LM

Equilibrium in both the goods and money marketsEquilibrium in both the goods and money markets

O

Ra

te o

f in

tere

st

National income

IS

re

Ye

LM

Equilibrium in both the goods and money marketsEquilibrium in both the goods and money markets

O

Ra

te o

f in

tere

st

National income

LM

IS

r1

Y1

ISLM analysis of changes in the goods and money markets

ISLM analysis of changes in the goods and money markets

O

Ra

te o

f in

tere

st

National income

IS1

r1

Y1

IS2

r2

Y2

A rise ininjections

LM

ISLM analysis of changes in the goods and money markets

ISLM analysis of changes in the goods and money markets

O

Ra

te o

f in

tere

st

National income

LM1

IS

r1

Y1

LM2

r3

Y3

A rise in themoney supply

ISLM analysis of changes in the goods and money markets

ISLM analysis of changes in the goods and money markets

LM2LM1

O

Ra

te o

f in

tere

st

National income

IS1

r1

Y1

IS2

Y4

A rise in bothinjections andmoney supply

ISLM analysis of changes in the goods and money markets

ISLM analysis of changes in the goods and money markets

R

Y

LM

ISIS`

Liquidity trapLiquidity trap

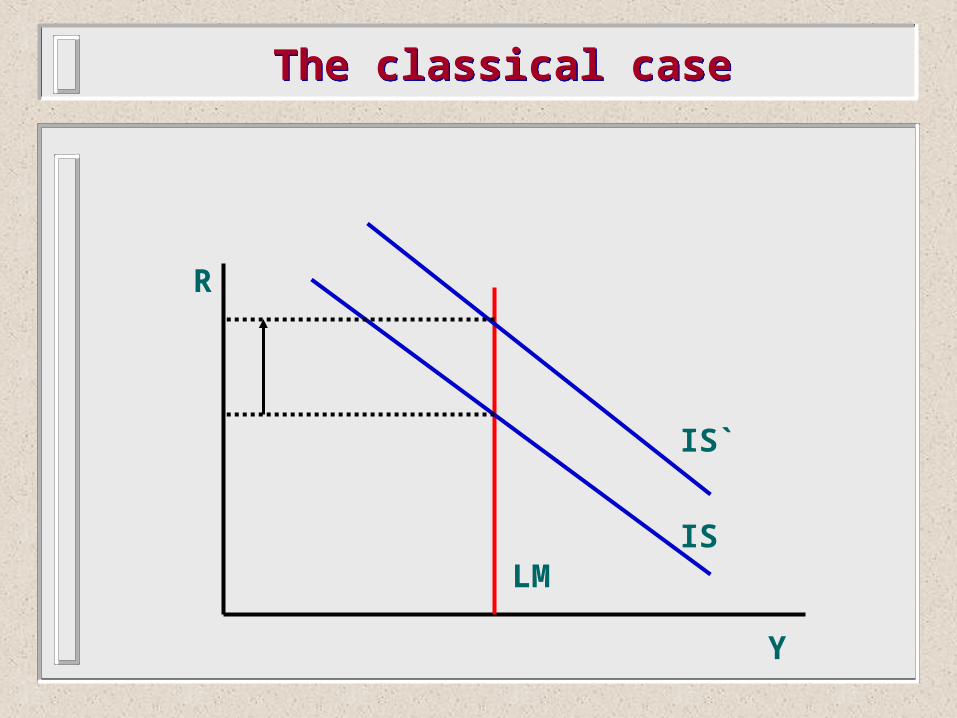

The classical caseThe classical case

R

Y

LMIS

IS`