the relation between equity incentives and earnings ... (2)_315695.docx · web viewthis shows the...

TRANSCRIPT

2010

[EQUITY INCENTIVES AND EARNINGS MANAGEMENTIN THE UNITED KINGDOM]

Equity incentives

and earnings management

in the United Kingdom

Erasmus University RotterdamErasmus School of EconomicsRotterdam, 2010

Author L.J.P. (John) de Vos (315695)Coach Dr. Y. WangCo-reader Drs. R. van der Wal RA

5

10

15

20

25

30

35

Equity incentives and earnings management in the U.K.

Preface

This thesis is written as the final assignment of my study Accounting, Auditing &

Control at the Erasmus University of Rotterdam. While writing this thesis earnings

management and the incentives for CEO’s to engage in earnings management were

of special interest to me. This period has come to an end with the conclusion of this

thesis. First of all I want to thank my family and friends for their support during my

master study. Secondly I would like to thank N. El-Haloush and R. van der Linden for

their support and comments on my thesis. Finally I would like to thank Dr. Y. Wang

for her support and critical review while writing this thesis.

John de Vos

Rotterdam, 2010

[]

5

10

Equity incentives and earnings management in the U.K.

Abstract

The past two decades have shown an enormous increase in stock-based

compensation. In the light of the credit crunch, the global financial crisis and the

following economic recession, variable compensation was a eyesore for a lot of

people. Some companies even asked their employees to hand in their bonuses. This

shows the importance of variable compensation in today’s world.

The use of stock-based compensation should make managers pay more attention to

share price and should provide better alignment between the stakeholders and the

managers of a company. However, recent studies (e.g. O’Connell and Brendan

2004) show that the incentives coming from variable compensation are not always

the right ones. A possible issue is their incentive to engage in earnings management.

This paper examines the relation between equity incentives and earnings

management in the United Kingdom (U.K.). Three types of compensation (i.e. fixed

salary, bonus and stock-based) are distinguished. Hypothesized is that fixed salary

has a negative relation and that bonus and stock-based compensation have a

positive relation with discretionary accruals as a tool for earnings management. To

test this, accrual and compensation data from FTSE listed firms is used. The accrual

approach will be used in measuring earnings management and the relative size of

the compensation types will be used to measure the compensation variables.

The results from this research show that fixed salary has a positive relationship with

discretionary accruals. For bonus compensation no linear relationship with

discretionary accruals is found and for stock-based compensation a negative

relationship with discretionary accruals is found. Moreover, this research has proven

that low equity incentive CEO’s have significant higher mean scores of discretionary

accruals than high equity incentive CEO’s. Therefore, the results seem to oppose the

results of studies from Bergstresser and Philippon (2006), Cheng and Warfield

(2005) and Gao and Shrieves (2002) who all found evidence that high equity

incentive CEO’s engage more in earnings management (through the use of

discretionary accruals) than low equity incentive CEO’s.

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

[]

Equity incentives and earnings management in the U.K.

Table of Contents

Preface........................................................................................................................3Abstract......................................................................................................................4

1 Introduction.........................................................................................................71.1 Problem statement..........................................................................................7

1.2 Research question..........................................................................................8

1.3 Contribution....................................................................................................9

1.4 Literature........................................................................................................9

1.5 Sample and methods....................................................................................10

1.6 Results..........................................................................................................11

2 Literature review...............................................................................................122.1 Earnings management..................................................................................13

2.1.1 What is earnings management?............................................................13

2.1.2 How are earnings managed?.................................................................14

2.1.3 Why do firms engage in earnings management?...................................16

2.1.4 How to detect earnings management?...................................................18

2.2 Compensation contracts...............................................................................23

2.2.1 Fixed salaries.........................................................................................24

2.2.2 Short-term incentives.............................................................................24

2.2.3 Long-term incentives..............................................................................25

2.2.4 Why do managers receive stock compensation?...................................25

2.3 Earnings management and equity compensation.........................................26

3 Hypotheses.......................................................................................................28

4 Research design...............................................................................................314.1 Data and sample...........................................................................................31

4.2 Dependant variable.......................................................................................32

4.3 Independent variable....................................................................................32

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

5 Data analysis and results.................................................................................325.1 Discretionary accruals and descriptive statistics...........................................32

5.2 Results..........................................................................................................32

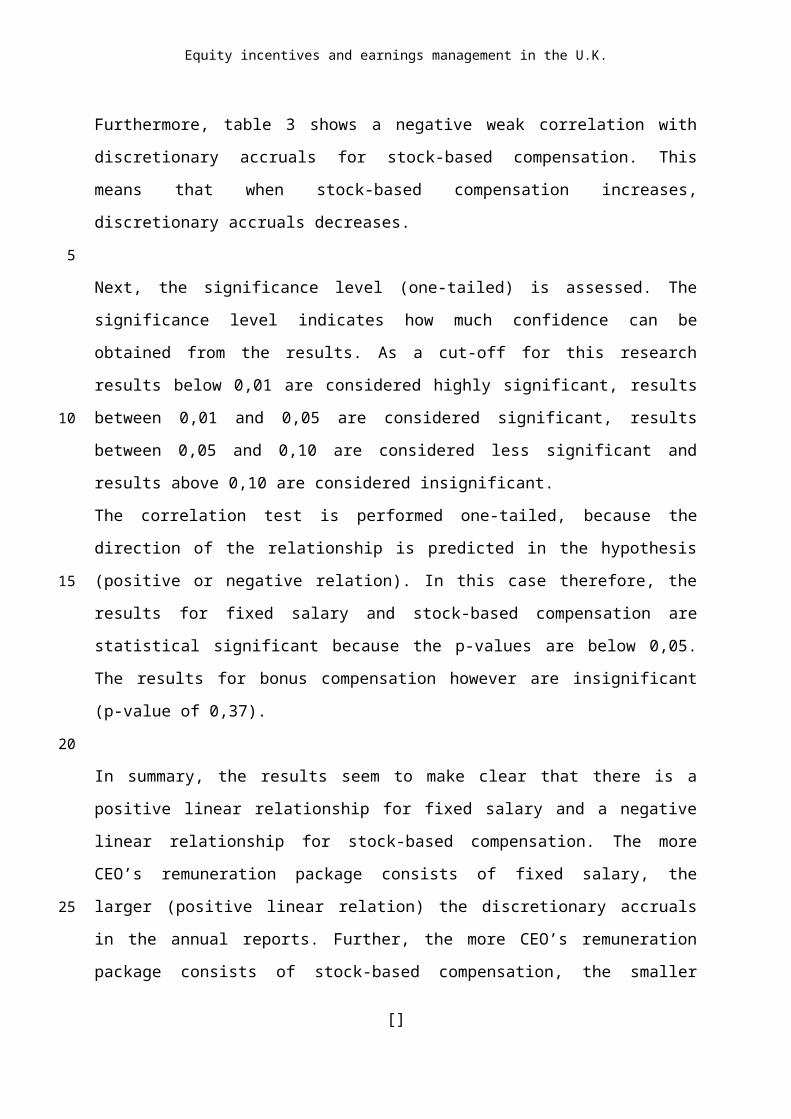

5.2.1 Correlation testing..................................................................................32

5.2.2 Independent-Samples T-Test.................................................................32

6 Conclusion, limitations and future research..................................................326.1 Research question........................................................................................32

6.2 Theoretical and empirical conclusions..........................................................32

6.3 Limitations and directions for future research...............................................32

References...............................................................................................................32

Appendix A...............................................................................................................32Appendix B...............................................................................................................32

[]

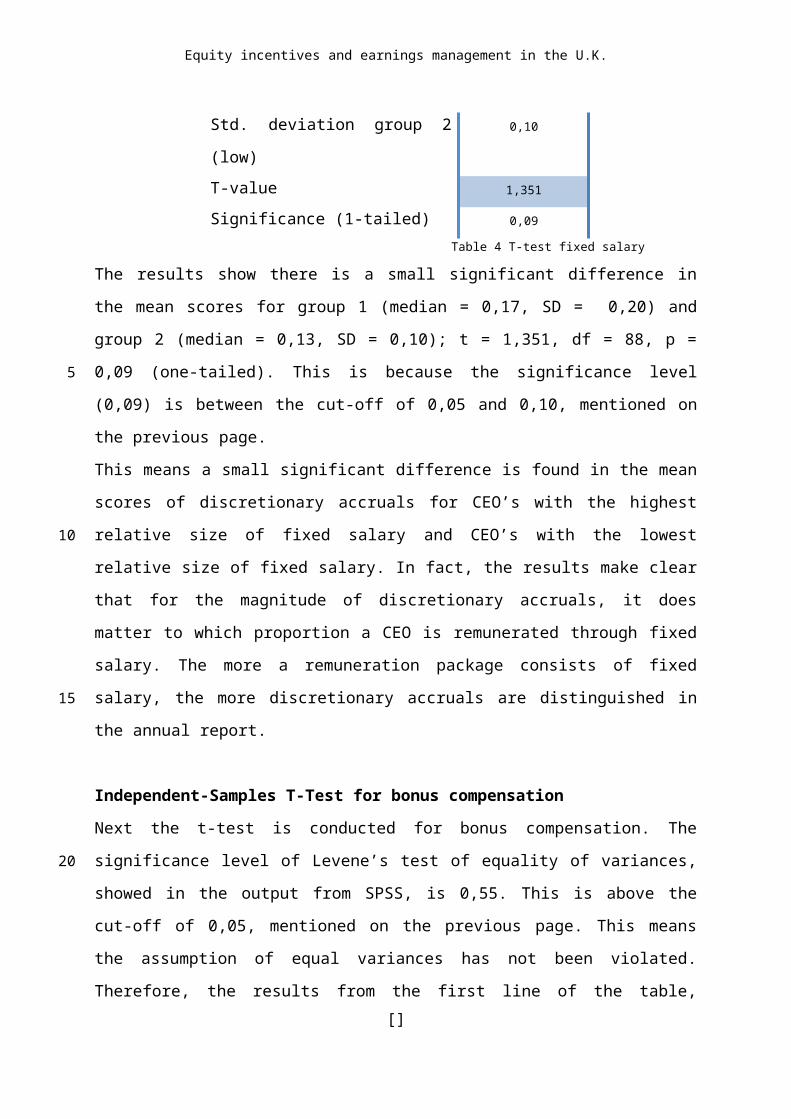

5

10

15

Equity incentives and earnings management in the U.K.

1 Introduction

1.1 Problem statement

Stock-based compensation, like stock options and shares for example, has been

frequently in the news the last couple of years. Despite the credit crunch, the global

financial crisis and the following economic recession, a lot of companies, also

financial institutions, gave their executives big bonuses. There were people who even

argued that executives should hand in their bonuses, because they thought

executives are responsible for the bad performances. Moreover here were

companies who asked their employees to hand in their bonuses, and in the United

States, the House passed legislation that significantly controls bonuses for

employees of financial institutions who received support from the government’s

financial rescue program1. For employees who earn more than $ 250,000, a 90%

surtax is granted on their bonuses. This example shows the importance of variable

compensation, and especially stock-based compensation, in today’s world.

The past two decades have shown an enormous increase in stock-based

compensation. The most important reason why managers nowadays have relatively

large stock-based compensation packages is that it should align managers’ aims with

the aims of stakeholders.

After two decades it seems however, that stock-based compensation has a short-

term perspective. Remuneration systems are working as they were designed to do.

Therefore they do not manage to align the interest of management with shareholders

(O’Connell and Brendan 2004). O’Connell and Brendan argue that, in a society

where CEO’s on average work four years for the same company, managers try to

appease the market through a variety of devices that ensure rising short-term stock

prices. With these devices they mean, among other thing, earnings management

practices to ensure steadily rising earnings that appease forecasts of the market.

On the other hand, Ronen and Yaari (2008) say it is difficult to make a profit in the

future when the market price is only rising. Therefore, Ronen and Yaari say long-term

1 http://online.wsj.com/article/SB123745823318182841.html[]

5

10

15

20

25

Equity incentives and earnings management in the U.K.

earnings management should aim at deflating earnings. Although the opinions differ,

it is, in regard to this study, assumed that equity-based compensation creates short-

term incentives for managers to manage earnings.

Literature divides compensation contracts for managers into three categories; fixed

salaries, bonuses and stock-based compensation (Merchant and Van der Stede

2007). Gao and Shrieves (2002) say that, in contrast to salary, the size of stock

options and bonuses is positively related to the use discretionary accruals as a tool

for earnings management. According to Murphy (1999) in the eighties and nineties of

the last century the main development in executive compensation was stock-based

compensation.

1.2 Research question

The purpose of this thesis is to provide more insight into the relation between equity

incentives (stock-based compensation) and earnings management. Besides the

relation of stock-based compensation and earnings management, also the relation of

fixed salary and (cash) bonus with earnings management will be investigated.

While prior research on the relation between equity incentives and earnings

management, which will be elaborated on more in chapter 2, mostly used United

States (U.S.) data, this research investigates the situation in the European Union

(E.U.). Within the E.U. this study focuses on companies based in the United Kingdom

(U.K.). European countries require companies to disclose detailed information on

executive compensation practices in the disclosures of the annual report. The U.K.

was the first country within the E.U. where these duties were introduced (Praag

2005). Therefore, most data is available for the U.K. This leads to the following

research question:

What is the relation between equity incentives and earnings management in the U.K.?

1.3 Contribution

During the past years, compensation for managers and earnings management have

been important topics in many debates. This research and its results are interesting

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

for two groups. First, for the Board of Directors of firms, because they provide the

compensation contracts to their top-managers. While stock-based compensation can

yield positive incentives effects, prior research has already shown that equity-

incentives have a negative effect on earnings management. Secondly, this study is

interesting for financial reporting regulators, because they criticize managers for their

focus on the short-term targets. It is expected that, with the results of this research,

financial reporting regulators can respond better to earnings management and its

incentives.

Moreover this thesis is a contribution to the knowledge on earnings management and

its relation with compensation for the academic world. It extends the growing

literature that examines the relation between equity incentives and earnings

management. Therefore this thesis may extent existing academic researches for

stock-based compensation outside the U.S.

1.4 Literature

This thesis is related to other papers on the subject of earnings management (e.g.

Daniel et al. 2008; Healy and Wahlen 1999; Stein 1989; Dechow et al. 1995). This

thesis is also related to studies on compensation contracts (e.g. Merchant and Van

der Stede 2007; Murphy 1999; Gao and Shrieves 2002). These studies have shown

what the different types of compensation are and how they are related to earnings

management.

Furthermore this thesis complements extant studies on the incentives for earnings

management (e.g. Cheng and Warfield 2005; Bergstresser and Philippon 2006;

Jensen and Murphy 1990; Bauman and Shaw 2006). These studies have shown that,

in general, the self-interest motivation of management is a great cause of earnings

management. Bergstresser and Philippon (2006) found evidence that earnings are

more manipulated through discretionary accruals when CEO’s total compensation is

more closely tied to the value of the shares. Cheng and Warfield (2005) examined

the relation between managers’ equity incentives and earnings management. They

found that high equity incentive managers are more likely to sell shares in the future.

This motivates these managers to engage in earnings management to increase the

value of the shares to be sold. Moreover, Gao and Shrieves (2002) examined how

the different types of compensation (i.e. fixed salary, bonuses, stock option, restricted

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

stock, and long-term incentive plans) influence earnings management behaviour.

This research extends and complements those researches by examining the relation

between equity incentives and earnings management.

1.5 Sample and methods

As mentioned earlier, most research done until now, focuses on companies in the

U.S. This research will focus on companies based in the U.K. because that was the

first country in the E.U. where companies were required to disclose detailed

information on executive compensation. Therefore most data is available for the U.K.

As the sample for this thesis the FTSE 100 index is used. This is a share index of the

100 most highly capitalised U.K. companies, listed on the London Stock Exchange.

This data provides a sample of about 176 entries and is spread out over two years,

i.e. 2005 and 2006. Financial data that is needed of the earnings management

component, and compensation data from the CEO’s that is needed for the

compensation component, will be gathered from the annual reports of the

companies.

Like other studies (Dechow et al. 1995; Bergstresser and Philippon 2006; Gao and

Shrieves 2002) the accrual approach will be used in measuring earnings

management. To measure earnings management the Modified Jones Model

(Dechow et al. 1995) is selected.

As explained earlier, this research distinguishes three components in compensation

contracts; fixed salary, bonuses and stock-based compensation (e.g. stock-options,

shares). It focuses on the relation between equity incentives and earnings

management, but it also tests the relation of the other two components (i.e. fixed

salary and bonus) with earnings management. Because relative figures are better

comparable with each other, the relative size of the compensation type will be used

to measure compensation.

1.6 Results

The results from this research show that fixed salary has a positive relationship with

discretionary accruals. For bonus compensation no linear relationship with

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

discretionary accruals is found and for stock-based compensation a negative

relationship with discretionary accruals is found.

Regarding the mean scores of discretionary accruals, no significant difference is

found for CEO’s with a relative high size and CEO’s with a relative low size of bonus

compensation. For fixed salary a small significant difference is found between the

mean scores of discretionary accruals for CEO’s with a relative high size and CEO’s

with a relative low size of fixed salary. Moreover, regarding stock-based

compensation, this research has proven that low equity incentive CEO’s have

significant higher mean scores of discretionary accruals than high equity incentive

CEO’s. Therefore, the results seem to oppose the results of studies from

Bergstresser and Philippon (2006), Cheng and Warfield (2005) and Gao and

Shrieves (2002) who all found evidence that high equity incentive CEO’s engage

more in earnings management (through the use of discretionary accruals) than low

equity incentive CEO’s.

Although the results in this thesis provide an indication on the relation between

earnings management and equity incentives additional research is needed to provide

a complete answer in the case of earnings management.

The thesis proceeds in five chapters. The next chapter provides background

information and the literature study. It describes the relevant academic literature on

earnings management, compensation contracts, and the link between these two

components. In chapter 3 the hypotheses are developed. The fourth chapter

discusses the research design. The research design describes the sample selection

and research method. In chapter 5 the results of the research are explained. In the

final chapter, chapter 6, the conclusions, limitations and directions for future research

are presented.

[]

5

10

15

20

25

Equity incentives and earnings management in the U.K.

2 Literature review

This section describes the background information and literature review on earnings

management and compensation contracts. Paragraph 2.1 elaborates on earnings

management. This paragraph will describe what earnings management is, how

earnings are managed, what activity manipulation is and why firms engage in

earnings management. The second paragraph will be about compensation contracts.

It describes fixed salaries, short-term incentives, and long-term incentives.

Furthermore it will elaborate on the fact why managers receive stock-based

compensation. In the last paragraph, paragraph 2.3, the link between earnings

management and equity compensation will be described.

Inefficient MarketThroughout this thesis, the asymmetric information gap between the principal and the

agent is discussed. This supports the notion that markets are not efficient in the

strong form2. According to the Efficient Market Theory (EMT) the strong form states

that all information (public and private) is included in the market price. This includes

that insider information (information known to management) is reflected in the share

price. If this is true, the reported information would not affect the stock price, because

the stock price already would reflect this information. In this scenario there would be

no incentive for management to manipulate earnings. If the market was efficient in

the strong form and managers reported manipulated earnings, the market would not

be fooled. Managers would therefore not be able to effect their compensation (Levy

and Post 2005).

2.1 Earnings management

In the light of past accounting scandals and the current world economics, the credit

crunch, the subject of earnings management has been receiving great attention. In

2 The three forms of the Efficient Market Theory (EMT) are: weak, semi-strong and strong. In the weak

form only historical data reflects the price of a share. In the semi-strong form all relevant public

information is reflected in the share price. The strong form states that all information (public and

private) is reflected in the stock prices.[]

5

10

15

20

25

Equity incentives and earnings management in the U.K.

2001 the investment world was shocked when the smartest guys in the room3 were

caught manipulating accounts. The Enron affair bought to daylight the significant

effects of earnings manipulation. Unfortunately, the Enron affair does not stand on its

own. Since 2002 there has been a number of accounting scandal were earnings

have been manipulated (Royal Ahold, Parmalat and more recently Satyam Computer

Services4).

It is not always clear if firms operate outside the boundaries set by regulators. As Van

der Bauwhede (2003) sais the one form of earnings manipulation is considered fraud,

the other is misleading and based on misjudgements by managers. The corrupt view

on the issue is revealed by managers that operate outside the boundaries set by

regulators. However, earnings management operates more than often within the

guidelines set by the reporting authorities. This thesis will concentrate on the later

form of earnings management.

2.1.1 What is earnings management?

Healy and Wahlen (1999) state earnings management as follows:

“Earnings management occurs when managers use judgment in financial

reporting and in structuring transactions to alter financial reports to either

mislead some stakeholders about the underlying economic performance of the

company or to influence contractual outcomes that depend on reported

accounting numbers.” (Healy and Wahlen 1999, 368)

In this definition Healy and Wahlen use a judgement criterion, as well as the goal of

earnings management.

The judgement criterion implies that earnings management is an activity that is

purposely undertaken by management. This judgement criterion is cited in a number

of articles as moving within the boundaries set by regulators (e.g. Daniel et al. 2008;

Benish 2001). This criterion implies that management does not intentionally

manipulate accounts. However, it implies the use of professional discernment used

by management. This discernment addresses the main challenge researches face 3 A documentary about the Enron corporation, its faulty and corrupt business practices (source:

www.imdb.com)4 (Source: http://en.wikipedia.org/wiki/Accounting_fraud)

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

(Beneish 2001). According to Bergstresser and Philoppon (2006) earnings

management occurs, when reported income includes cash flows and changes in firm

value. Cash flows are not difficult to establish, but changes in firm value requires a

greater deal of management discernment.

Healy and Wahlen also state the goal of earnings management. On the one hand

misleading stakeholders, and on the other hand influencing contractual outcomes. In

general earnings management is aimed at transferring wealth (Stolowy and Breton

2004).

2.1.2 How are earnings managed?

Financial reports convey earnings that have occurred throughout the past period.

These earnings are based on cash flow plus changes in firm value (Bergstresser and

Philippon 2006). Whilst cash flows are easily determined, changes in firm value are

more challenging. It is in determining this change in firm value that managers are

granted some freedom by regulators and standard setters. The accrual account,

designed by standard setters, is a common account used to manipulate earnings.

Benish (2001) states that it is like that earnings management takes place in the

accrual account. However the aim of standard setters was not to provide managers

with a possibility for earnings management. Accruals were designed to express

valuation changes that had not yet related in cash flows (Gao and Shrieves 2002).

This poses the problem that not all accruals are related to earnings management.

With regards to earnings management, only the discretionary component of accruals

is important (Benish 2001).

Based on their sales and value of assets, all firms are expected to have a certain

level of accruals (Van der Bauwhede 2003). However when these accruals exceed

non-discretionary levels, they could indicate to tend to manage earnings.

Over the years there have been a number of methods developed to detect earnings

management. Healy (1985) and DeAngelo (1986)5 developed methods that were

very dependent on years were no earnings management was suspected. This was

the biggest weakness for these models.

5 Cited from Van der Bauwheden (2003)[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

The Jones model (Jones 1991) and the modified Jones model (Dechow et al. 1995)

were created to try to eliminate the discretionary element of the accruals, by taking

into consideration changes in the economic environment (Benish 2001). However like

most models these models have various limitations (read for further details on the

models paragraph 2.1.4). Studies have shown that changes in inventory, and

accounts receivables can resemble earnings manipulation (Roychowdhury 2006;

Stowley and Berton 2004).

Rational minds would suggest that investors, being able to detect earnings

management, would punish firms that violate the freedom granted to them by

standard setters. Studies carried out by Teoh et al. (1998a, b) and Teoh and Wong

(2002) suggest that investors are “naïve” in detecting earnings manipulations, due to

the asymmetric information gap. Although there are models that can predict the

possibilities of earnings management, an accurate forecast remains difficult.

It should be said that most researches that are carried out assume that the market is

not aware of the tendency by managers to alter earnings. However according to a

study by Stein (1989) investors rationally expect managers to manage earnings. As a

result, in pricing stock analysts’ expect managers to manipulate earnings. The market

knows it cannot prevent earnings manipulation from happening so it anticipates that

earnings have been managed (Cheng and Warfield 2005). This would be consistent

with the efficient market hypothesis. The share price reflexes all information, i.e.

public and private. The share price therefore portrays a true view of the firm, where

managed earnings are processed in the market price.

Coles et al. (2006) suggest that investors are well informed and sophisticated in there

awareness of earnings manipulation. Nevertheless, the transparency into incentives

and account manipulation is limited. Even though models might be available, these

models face limitations and can only indicate the possible use of earnings

management.

Activity manipulationMost studies carried out focus on account manipulation, however Roychowdhury

(2006) suggest that the effects of direct account manipulation are relatively lower in

comparison to activity manipulation. Activity manipulation can be characterized as a

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

difference from normal operation with the objective to meet certain earnings targets

(Roychowdhury 2006). One might argue that activities that increase earnings are

only good for the firm. Roychowdhury mentions an increase in sales by means of

temporary discounts. This cannot harm the interest of a firm and investors might

even appreciate a certain degree of entrepreneurship to sell products that might have

not been sold without a discount. However earnings manipulation is known for its

short-term perspective. Therefore managers might mislead stakeholders (Stolowy

and Berton 2004). Activity manipulation doesn’t support this notion because it does

not mislead investors. Reported earnings by management are not incorrectly stated

and do not present an untrue view of the value of the company. Earnings

management through account manipulation does not always materialize and produce

cash flows, therefore not benefiting investors. Cash flows change the capacity of

firms to pay out dividend. DeAngelo and DeAngelo (2006) research suggests that

dividend payouts are important to investors. Further research has shown that

dividend cuts are punished at the stock market (Pettit 1972; Aharnoy and Swary

1980; Gullon et al. 2002). Therefore earnings that do not materialise into cash flow,

damage the cash position of the firm.

2.1.3 Why do firms engage in earnings management?

Although throughout the literature different forms of compensation are given for the

existence of earnings management, Stolowy and Berton (2004) state that the why

earnings management exist is to profit from the possibilities of wealth transfer.

Benish (2001) distinguished between four possible motives for earnings

management:

1. Debt contracts;

2. Compensation Agreements;

3. Equity Offerings;

4. Insider trading.

Firms’ performance are often regulated in debt covenants. Moreover dividend

restrictions are incorporated in them (Bradley and Roberts 2004). This is because the

position of the debt providers is weaken by dividends that exit the firm. Through

dividend payout, less cash remains in the firm to pay back the debt providers (Daniel

et al. 2008). Benish (2001) summarizes studies that reveal mixed results for the use

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

of earnings management to avoid defaults on loans. Influence debt covenants by

using earnings management to avoid defaults, might have the opposite effect that

firms eventually default. Some firms profit from a relatively cheap form of capital,

although they may not default on their loans (Stolowy and Breton 2004). Due to

higher earnings, companies could seem more profitable than in reality.

Compensation contracts seem to provide more evidence for the existence of

earnings management than debt contract. Extensive studies (e.g. Healy 1985;

Bergstresser and Philippon 2006; Bauman and Shaw 2006; Ronen et al. 2006; Gao

and Shrieves 2002) have shown that in general that the greatest cause of earnings

management is the self-interest motivation of management. This subject will be

addressed more in depth in the next paragraph.

Equity offerings also offer a great opportunity to manage earnings. Managers are

known to inflate earnings to receive a better price for new equity (Benish 2001). This

is possible due to the information asymmetry and is consistent with the notion that

management aspire to receive a relatively low cost of capital.

Insider trading has also been documented (Benish 1999; Ronen et al. 2006). Benish6

even argues that it is expected for managers to use their insider information about

earnings overstatements, to trade for their own benefit. Ronen et al. (2006) study

supports recommendation to ban insider trading.

2.1.4 How to detect earnings management?

The accrual approach will be used in measuring the dependant variable, earnings

management (Dechow et al. 1995; Bergstresser and Philippon 2006; Gao and

Shrieves 2002). Like Dechow et al. (1995), five models will be described that are

used in the extant earnings management literature. These five models are the Healy

Model, the DeAngelo Model, the Jones Model, the Modified Jones Model and the

Industry Model. In this paragraph the models will be described.

6 Benish, 2001, page 10. []

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

The models make use of accruals. Accruals are revenues and costs that make the

difference between the profit and the cash flow of a company. They depend on

accounting choices of managers, and it is therefore important to examine whether the

accruals are in line with expectations. Total accruals need to be decomposed into a

discretionary and a non-discretionary component. Discretionary accruals are those

which cannot be explained from normal activities. Managers can influence these

accruals. Non-discretionary accruals can be explained from normal activities of the

company and managers can not influence them.

The starting point of most models is the total accruals. The models then try to find the

non-discretionary element so they can divide the accruals in the non-discretionary

and the discretionary part.

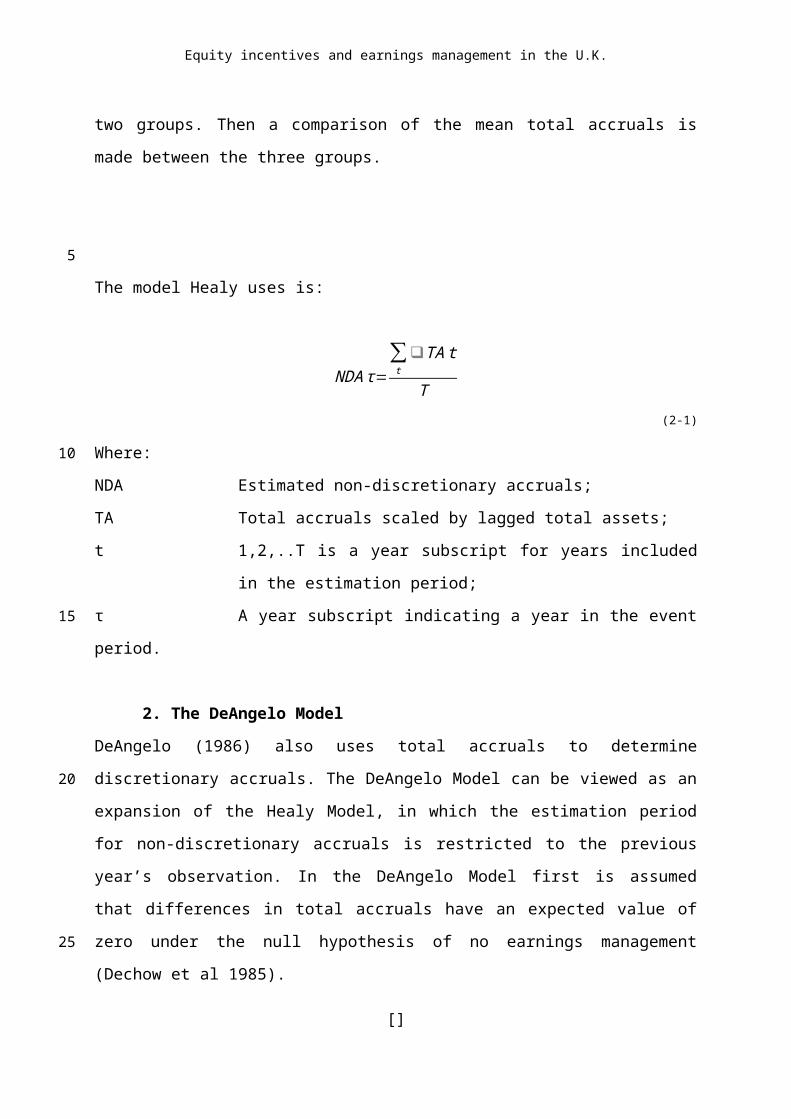

1. The Healy ModelHealy (1985) uses total accruals to determine discretionary accruals. The

discretionary accruals are equal to the difference of total accruals in two successive

years. The assumptions Healy (1985) makes, is that non-discretionary accruals are

constant. Further is assumed that systematic earnings management is occurring in

every period. In this last assumptions it is that Healy’s study differs from most other

earnings management studies.

The sample is divided into three groups, in one is predicted that earnings are

managed upwards, and downward in the other two groups. Then a comparison of the

mean total accruals is made between the three groups.

The model Healy uses is:

NDA τ=∑t

❑TA t

T (2-1)

Where:

NDA Estimated non-discretionary accruals;

TA Total accruals scaled by lagged total assets;[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

t 1,2,..T is a year subscript for years included in the estimation

period;

τ A year subscript indicating a year in the event period.

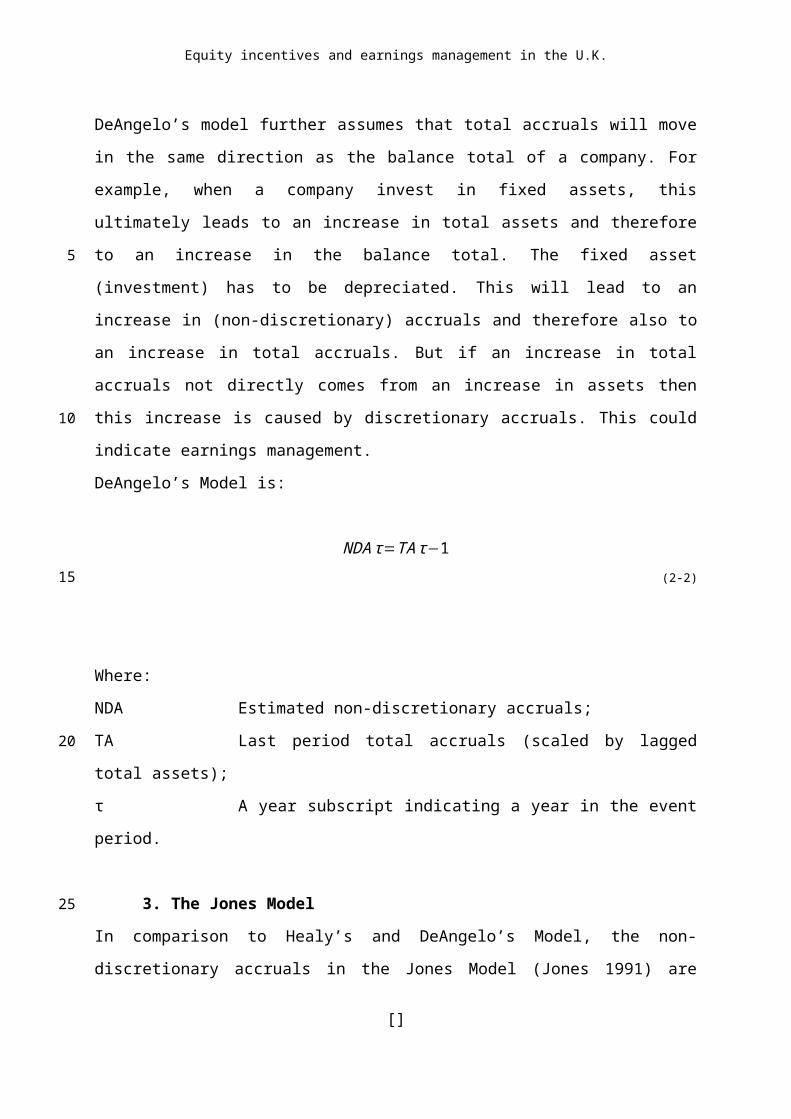

2. The DeAngelo ModelDeAngelo (1986) also uses total accruals to determine discretionary accruals. The

DeAngelo Model can be viewed as an expansion of the Healy Model, in which the

estimation period for non-discretionary accruals is restricted to the previous year’s

observation. In the DeAngelo Model first is assumed that differences in total accruals

have an expected value of zero under the null hypothesis of no earnings

management (Dechow et al 1985).

DeAngelo’s model further assumes that total accruals will move in the same direction

as the balance total of a company. For example, when a company invest in fixed

assets, this ultimately leads to an increase in total assets and therefore to an

increase in the balance total. The fixed asset (investment) has to be depreciated.

This will lead to an increase in (non-discretionary) accruals and therefore also to an

increase in total accruals. But if an increase in total accruals not directly comes from

an increase in assets then this increase is caused by discretionary accruals. This

could indicate earnings management.

DeAngelo’s Model is:

NDA τ=TA τ−1(2-2)

Where:

NDA Estimated non-discretionary accruals;

TA Last period total accruals (scaled by lagged total assets);

τ A year subscript indicating a year in the event period.

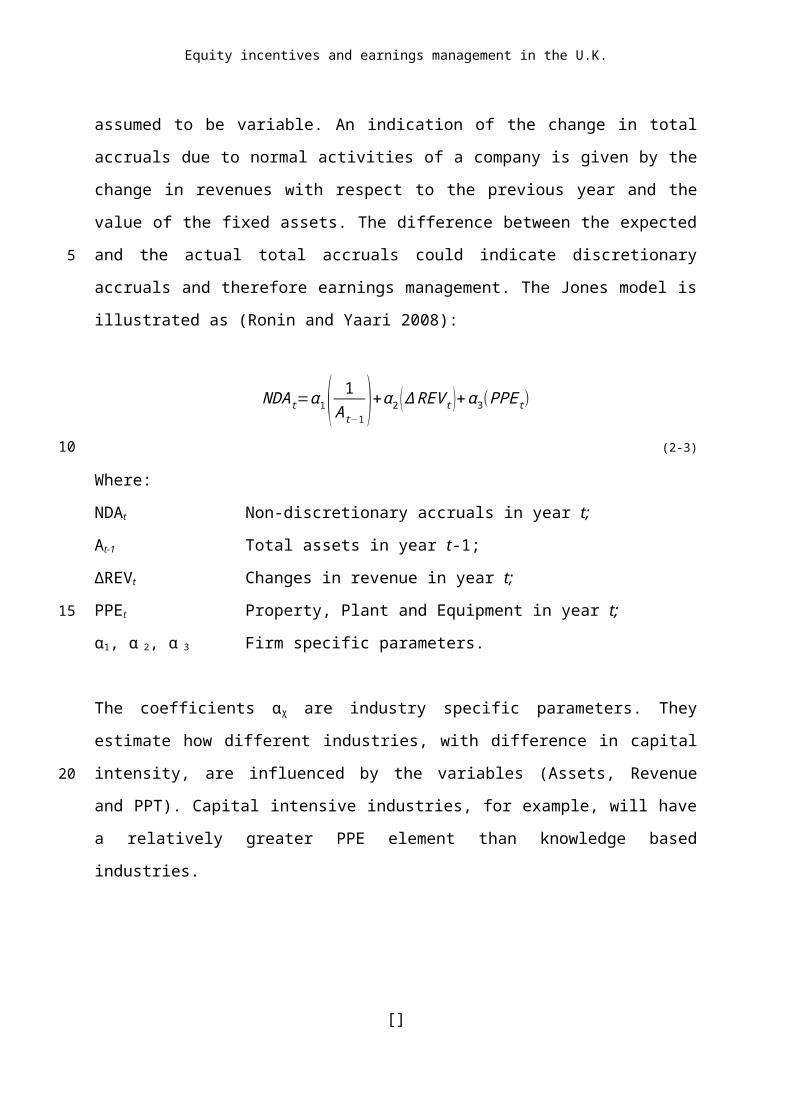

3. The Jones ModelIn comparison to Healy’s and DeAngelo’s Model, the non-discretionary accruals in

the Jones Model (Jones 1991) are assumed to be variable. An indication of the

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

change in total accruals due to normal activities of a company is given by the change

in revenues with respect to the previous year and the value of the fixed assets. The

difference between the expected and the actual total accruals could indicate

discretionary accruals and therefore earnings management. The Jones model is

illustrated as (Ronin and Yaari 2008):

NDA t=α1( 1At−1 )+α2 (∆ REV t )+α3(PPE t)

(2-3)

Where:

NDAt Non-discretionary accruals in year t;

At-1 Total assets in year t-1;

∆REVt Changes in revenue in year t;

PPEt Property, Plant and Equipment in year t;

α1, α 2, α 3 Firm specific parameters.

The coefficients αχ are industry specific parameters. They estimate how different

industries, with difference in capital intensity, are influenced by the variables (Assets,

Revenue and PPT). Capital intensive industries, for example, will have a relatively

greater PPE element than knowledge based industries.

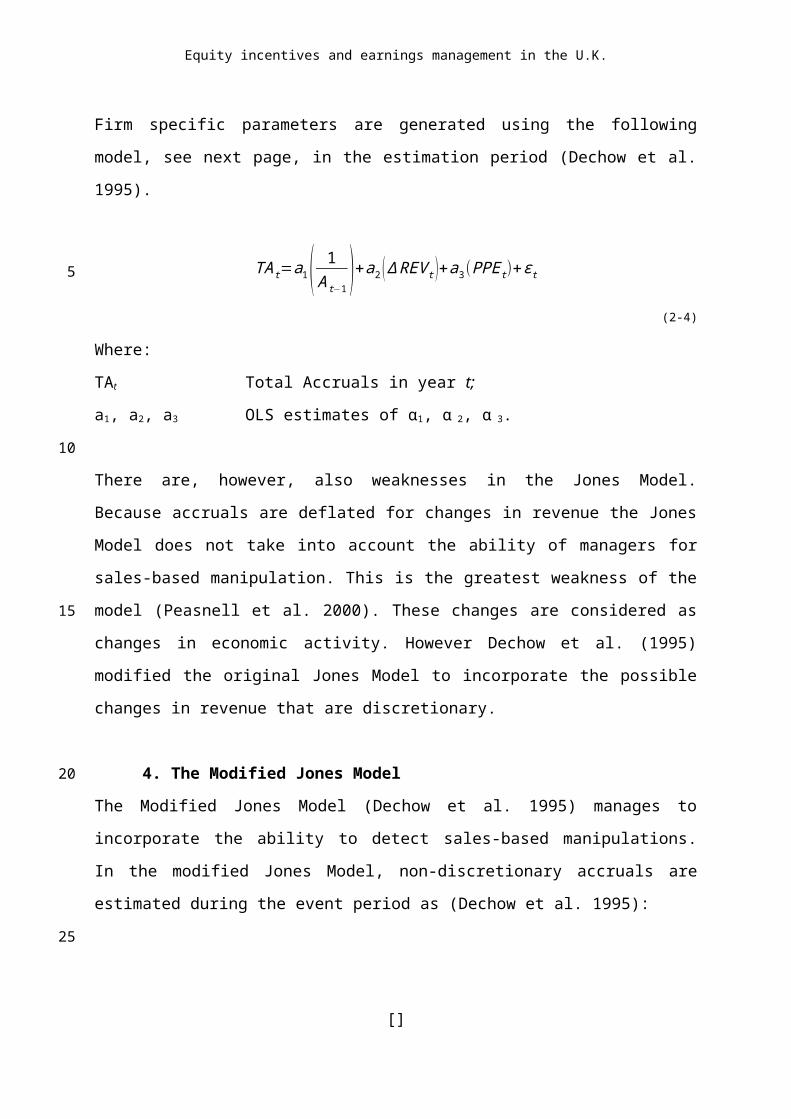

Firm specific parameters are generated using the following model, see next page, in

the estimation period (Dechow et al. 1995).

TAt=a1( 1A t−1 )+a2 (∆REV t )+a3(PPE t)+εt

(2-4)

Where:

TAt Total Accruals in year t;

a1, a2, a3 OLS estimates of α1, α 2, α 3.

There are, however, also weaknesses in the Jones Model. Because accruals are

deflated for changes in revenue the Jones Model does not take into account the

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

ability of managers for sales-based manipulation. This is the greatest weakness of

the model (Peasnell et al. 2000). These changes are considered as changes in

economic activity. However Dechow et al. (1995) modified the original Jones Model

to incorporate the possible changes in revenue that are discretionary.

4. The Modified Jones ModelThe Modified Jones Model (Dechow et al. 1995) manages to incorporate the ability to

detect sales-based manipulations. In the modified Jones Model, non-discretionary

accruals are estimated during the event period as (Dechow et al. 1995):

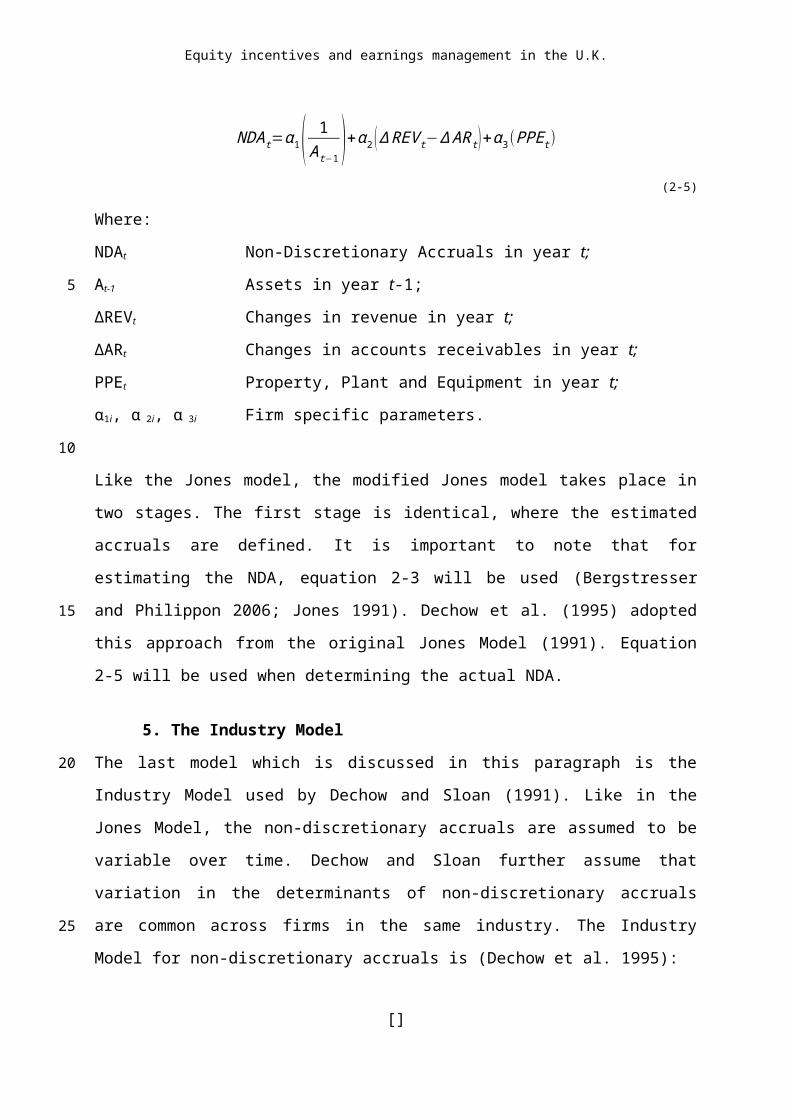

NDA t=α1( 1At−1 )+α2 (∆ REV t−∆ AR t )+α 3(PPE t)

(2-5)

Where:

NDAt Non-Discretionary Accruals in year t;

At-1 Assets in year t-1;

∆REVt Changes in revenue in year t;

∆ARt Changes in accounts receivables in year t;

PPEt Property, Plant and Equipment in year t;

α1i, α 2i, α 3i Firm specific parameters.

Like the Jones model, the modified Jones model takes place in two stages. The first

stage is identical, where the estimated accruals are defined. It is important to note

that for estimating the NDA, equation 2-3 will be used (Bergstresser and Philippon

2006; Jones 1991). Dechow et al. (1995) adopted this approach from the original

Jones Model (1991). Equation 2-5 will be used when determining the actual NDA.

5. The Industry ModelThe last model which is discussed in this paragraph is the Industry Model used by

Dechow and Sloan (1991). Like in the Jones Model, the non-discretionary accruals

are assumed to be variable over time. Dechow and Sloan further assume that

variation in the determinants of non-discretionary accruals are common across firms

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

in the same industry. The Industry Model for non-discretionary accruals is (Dechow

et al. 1995):

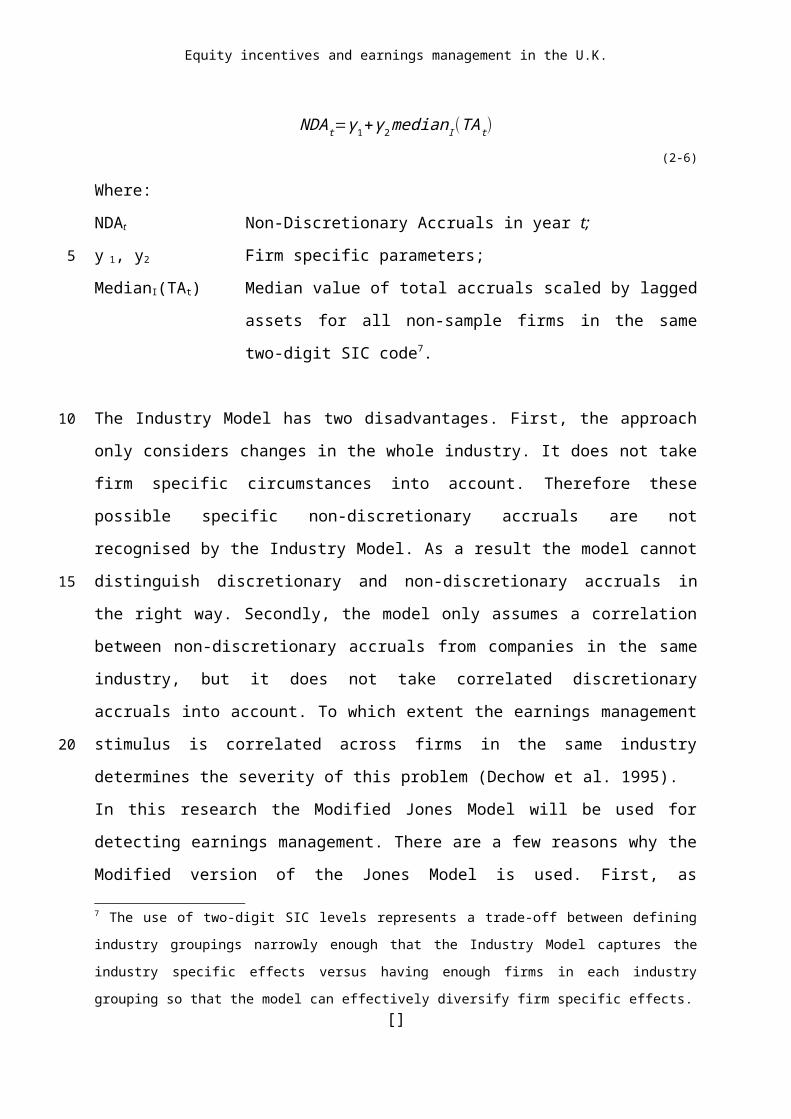

NDA t=γ1+γ2median I (TAt)

(2-6)

Where:

NDAt Non-Discretionary Accruals in year t;

y 1, y2 Firm specific parameters;

MedianI(TAt) Median value of total accruals scaled by lagged assets for all

non-sample firms in the same two-digit SIC code7.

The Industry Model has two disadvantages. First, the approach only considers

changes in the whole industry. It does not take firm specific circumstances into

account. Therefore these possible specific non-discretionary accruals are not

recognised by the Industry Model. As a result the model cannot distinguish

discretionary and non-discretionary accruals in the right way. Secondly, the model

only assumes a correlation between non-discretionary accruals from companies in

the same industry, but it does not take correlated discretionary accruals into account.

To which extent the earnings management stimulus is correlated across firms in the

same industry determines the severity of this problem (Dechow et al. 1995).

In this research the Modified Jones Model will be used for detecting earnings

management. There are a few reasons why the Modified version of the Jones Model

is used. First, as mentioned before, Dechow, Sloan, and Sweeny (1995) evaluated

the ability of the models described above to detect earnings management. Their most

important result was that the Modified version of the model developed by Jones

(1991) provides the best test to detect earnings management. It generated the fewest

type II errors, which represents cases in which earnings are managed, but are

identified as not. Guay et al. (1996) also evaluated the same five models. Their

findings suggest that the Jones Model and the Modified Jones Model are the most

effective models.

7 The use of two-digit SIC levels represents a trade-off between defining industry groupings narrowly

enough that the Industry Model captures the industry specific effects versus having enough firms in

each industry grouping so that the model can effectively diversify firm specific effects.[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

Second, the most popular and best accepted model in the academic literature seems

to be the Modified Jones Model. Therefore the results of this research will be better

comparable to other studies when the Modified Jones Model is used.

2.2 Compensation contracts

As mentioned in the previous paragraph, compensation contracts are one of the main

reasons for earnings management. The contracts are derived from the issues around

the agency theory. The agency theory is concerned with two problems. The first

problem is that the aims of the agent (financial reporters of the company) are not in

line with those of the principal (stakeholder). Secondly, it is impracticable for the

principal to assess the work of the agent efficiently (Eisenhardt, 1989).

Both agent and principal want to increase their wealth. The principal’s wealth

increases when that of the firms increases. The wealth of the agent increases when it

receives the maximum return for its input (i.e. labour). The problem occurs when the

incentives for the agent to increase the value of the firm are absent, and the agent is

primarily aimed at increasing its value. However, the principal can alter this problem

by adding incentives to the agent in their compensation contract. These incentives

can better align the ambitions of agent and principal.

Before 1986 is was unusual for managers to receive stock-based compensation

(Bergstresser and Philippon 2006). Between 1974-1986 shareholders wealth

increased with $ 1,000 for every $ 3 increase in wealth for the CEO’s (Jensen and

Murphy 1990). During these years therefore, CEO’s had no incentive to increase the

wealth of the firm.

Incentive contracts are designed to eliminate this problem and to align the personal

interests of financial reporters (managers) with those of the stakeholders (investors).

Investors try to increase their return on investment, by increasing earnings within

their investment. Therefore financial reporters should also try to increase true

company earnings.

According to Murphy (1999) compensation contract are designed to align executive

interest with those of the shareholder. Literature divides compensation contracts for

managers into three categories (Merchant and Van der Stede 2007):

1. Fixed salaries;

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

2. Short-term incentives; and

3. Long-term incentives

2.2.1 Fixed salaries

Although fixed salaries do not have much relation to management performance, most

incentives are based on fixed salary. Other elements within the compensation

contract increase when salary increases (Murphy 1999). Managers that are risk

obverse have a relatively larger part of fixed salary as part of their total remuneration

(Murphy 1999).

2.2.2 Short-term incentives

An example of a short-term incentive is the annual (cash) bonus. Although bonus

plan take many forms, most manager nowadays have a personal bonus plan that

contains a individual performance portion (Murphy 1999). These bonus then can be

achieved through predetermined targets and objectives, that can be both financial

and nonfinancial measurements. In a Towers Perrin survey, 65 of the 68 sample

companies using single performance measurement used accounting indicators as

performance measurement. 62% of companies using multiple performance

measurements used accounting indicators. Performance can be measured in a

number of ways from total earnings to growth rates.

2.2.3 Long-term incentives

Long term incentives are in particular stock options. These options are offered to

management as an incentive for long term earnings at the company. In most cases

these options can be exercised only over a period of time (Murphy 1999; Cheng and

Warfield 2005). More importantly executive options are non-tradable. Considering

these restrictions, managerial compensation contracts involve an increasingly higher

degree of stock compensation. Murphy (1999) even states that stock-based

compensation was most important development in executive compensation in the

1980s and 1990s.

Short-term and long-term compensation are the general compensation that is spoken

about when talking about earnings management. As proved in the Towers Perrin

survey, a large majority of companies (91% of the total sample of 177 companies)

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

use accounting information to measure performance. Apart from stock-based

compensation managers can obtain shares by purchasing them on the open market.

Core and Larcker (2002) say that some firms expect managers to own a unknown

number of shares of their own company (Core and Larcker 2002).

2.2.4 Why do managers receive stock compensation?

As explained before, there is an information asymmetry between investors and

managers. Managers know the truth about the (financial) performance and the

situation of the company. Investors must rely on the information that is granted to

them by the managers. To add value to the publicized information audit reports are

designed. However, Ronen et al. (2006) claim that audit technology seems to be

imperfect and managers can move within the boundaries set by regulators. Because

regulators leave managers some space in the accounting rules, this creates an

incentive for managers to engage in earnings management.

In an extensive study on equity incentives, Cheng and Warfield (2005) examine the

actions of managers that are compensated through stock options. Due to the

increasing stock-based compensation in the last decades, a managers compensation

largely consists of shares. This is consistent with the incentive alignment investors

want to create. If stock-based compensation increase, a greater portion of manager’s

wealth is invested in a relatively risky asset, i.e. company shares. Managers will

adapt their remuneration package to their to an acceptable risk level, selling shares

at short-term prices. Under the capital asset pricing assumptions, returns on stocks

are positive and stock prices rise under normal economic circumstances. This

causes short-term trading because managers need to constantly adapt their risk

profile (Sivakumar and Waymire 1994; Noe 1999).

As managers have relatively short-term personal incentives and investors often have

a long-term incentive, this could lead financial reporter to report short-term high

earnings. This short-term view could damage long-term interest for the firm and

investors. This phenomenon has been researched in numerous studies (e.g. Jensen

and Meckling 1976; Rajgopal and Shevlin 2002).

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

2.3 Earnings management and equity compensation

It is clear that extensive studies have been conducted on the subject earnings

management and compensation contracts. Compensation contract are often blamed

for their steer towards earnings management. However Gao and Shrieves (2002) say

that it is not the only incentive for managers to engage in earnings management. In

spite of the fact that there are more incentives, the incentive coming from

compensation contracts is the only form of earnings management that extracts

wealth from the company (Stolowy and Breton 2004).

Currently stock compensation is the biggest component in the executive

compensation package. The primary reason for the introduction of this form of

compensation was to eliminate the short-term orientation of executives. However in

eliminating this short-term awareness, does this form of compensation create a

greater incentive for managers to creatively report earnings? With managers

compensation coupled to firm performance – in a form of earnings –, and current

company earnings linked to stock prices, reporting managers have a seemingly

increased incentive to report colourful earnings.

Current earnings are based on past activities. Why are markets so possessed with

passed activities? Share prices are a reflection of the present value of future cash

flow. Therefore past earnings should have a very small impact on share prices.

Under normal economic situations share prices increase, because analysts’ expect

firms to increase their profit over the years. Put another way, if current earnings are

disappointing, future revenues will be lower than expected, effecting current share

prices. Therefore, current earnings give a good indication of future firm profits (Stein

1989).

Studies have shown that managers are more likely to report earnings greater than

the expectation of the market (investors and analyst’s), when they have a large

portion of stock-based compensation. (Bauman and Shaw 2006). Share prices

increase when firms beat the forecasts of analyst’s.This gives managers an incentive

to increase earnings. However this study does not imply earnings management as a

possible cause for these continuous surprises. Shaw nevertheless, does mention that

firms have even a greater incentive to beat analysts’ forecast by small amounts. This []

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

could indicate a certain level of income smoothing. These small surprises are also

documented by Cheng and Warfield (2006). Their research has shown that

managers with high equity incentives, are less prone to show large positive earnings

surprises.

Gao and Shrieves (2002) note that income smoothing is a matter of timing. Managers

that receive Long Term Incentive Plans (LTIP) have no profit in managing earnings.

Gao and Shrieves found no positive nor negative relation between LTIP and earning

management. This is because firms cannot manage earnings upwards continuously.

This would result in exorbitant accruals, and could bring the firm into discredit.

However, ensuring that higher earnings (greater than analysts’ expect) come at an

optimal time for the manager, is a timing choice. Gao and Shrieves find that it is very

dependent on the forms of compensation in the contract.

Even though markets expect earnings to be managed, managers caught in the act,

are punished by investors. Palmrose et al. (2004) say that firms lost 10% of the share

price at the announcement of restatements of their earnings. Moreover, monetary

fines and reputation losses are also important risk factors for firms who engage in

earnings management (Karpoff et al. 2008). Disciplinary actions taken by the market

towards managers is not possible, due to limited ability to withdraw past

compensation. However post-restatement compensation plans are significantly lower

(Cheng and Farber 2008).

[]

5

10

15

20

Equity incentives and earnings management in the U.K.

3 Hypotheses

As explained in paragraph 2.2, this research considers that compensation contracts

nowadays consist of three elements; fixed salary, bonus and stock-based

compensation (e.g. stock options). However, the main focus will be on the relation

between equity incentives and earnings management. The relation of earnings

management with the other two components of compensation contracts (i.e. fixed

salary and bonuses) will also be tested. By testing the relation of earnings

management with all three elements of compensation data, the results for the

different elements can be compared among each other. Therefore the relation of

equity incentives and earnings management can be understand better.

In the extant literature there is already a lot of research done on the subject earnings

management. Some of these researches investigated the relation of earnings

management with equity incentives. Gao and Shrieves (2002) say in their study that

equity incentives gives managers an incentive that may lead to earnings

management strategies for maximizing their compensation.

CEO salaries are usually set on an annual basis. In a static setting, salary’s

sensitivity to price movement is zero. Therefore, it seems unlikely that salaries are

positively related to earnings management. Moreover, earnings management seems

to be costly. As explained in the last paragraph of Chapter 2, firms lost 10% of the

share price at the announcement of restatements of their earnings (Palmrose et al.

2004), and earnings management also may result in monetary fines and reputation

loss. Moreover, Gao and Shrieves (2002) find in their study that salaries are

negatively related to earnings management. Therefore, both logic and empirical

evidence suggest that earnings management is a costly activity. It therefore seems

reasonable that a manager with a relatively large amount of fixed salary, compared to

the other two components (i.e. bonus and stock-based), would have an incentive to

reduce the extent of earnings management, and so reduce the costs. This leads to

the following hypothesis:

H1: Fixed salary is negatively related to the use of

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

discretionary accruals as a tool for earnings management.

Bonus compensation might also create incentives to engage in earnings

management, because some bonus plans might contain nonlinearities (Healy 1985;

Gaver 1995). Gao and Shrieves (2002) found in their study, that bonuses are

positively related to earnings management. On the other hand, bonus plans are

highly firm-specific, because of the structure and the pay-performance relation. This

makes it difficult to predict the magnitude of the relation between bonuses and

earnings management, but the expectation is a positive relation between bonus

compensation and discretionary accruals. This leads to the second hypothesis:

H2: Bonus compensation is positively related to the use of

discretionary accruals as a tool for earnings management.

Managerial compensation frequently contains stock-based compensation to align the

interest of managers and outside shareholders and reduce agency problems. The

results of Bergstresser and Philippon (2006) suggest that high equity incentive CEO’s

engage more in earnings management than low equity incentive CEO’s. They find

that CEO’s whose overall compensation is more sensitive to company share prices,

lead firms with higher levels of earnings management. Cheng and Warfield (2005)

examined the link between managers’ equity incentives, arising from stock-based

compensation, and earnings management. First they find high incentive managers

are more likely to sell shares a year after earnings announcements. Furthermore they

find that managers with high equity incentives are more likely to report earnings that

meet or just beat analysts’ forecasts. Their results indicate that equity incentives lead

to incentives for earnings management. Also, Gao and Shrieves (2002) find results

that indicate that the extent of stock-based compensation are positively related to

earnings management. Now that the incentives for managers are so closely tied to

the stock price of a firm it may have the perverse effect of stimulating managers to

manipulate their earnings (Bergstresser and Philippon 2006).

This thesis extends the previous cited studies by examining how stock-based

compensation relates to earnings management. The predicted linkage between

stock-based compensation and earnings management is as follows. Assume that a

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

manager receives a large component of his/her remuneration in the form of stock-

based compensation. He/she can increase the value of that component of stock-

based compensation by taking actions to reduce the exercise price. This prediction

suggests an incentive for managers to engage in earnings management. If, for

example, a manager expects to receive stock options, he/she can reduce current

earnings through discretionary accruals. The effect could be a reduction in the

exercise price of the stock options on the award date. By doing this, the manager

increases the chance that the options are ‘in the money’. Therefore, the third

hypothesis is:

H3: Stock-based compensation is positively related to the use of

discretionary accruals as a tool for earnings management.

In the next chapter the research design is described.

4 Research design

In this chapter the variables used for this research will be discussed. The approach

will be similar to that of Bergstresser and Philippon (2006) and Gao and Shrieves

(2002). In conformity with other papers that investigate earnings management, this

research will make use of a field study. For this study four main variables will be

used. The expectation is that the relative size of stock-based compensation will

determine the extent of earnings management. Furthermore the relative size of

salary and bonus will be used to see whether these variables can also determine the

extent of earnings management. Therefore earnings management will be the

dependant variable, and stock-based compensation, salary, and bonus will be the

independent variables.

First the data and sample will be outlined in paragraph 4.1. In the second paragraph

the dependant variable will be described. Finally the independent variables will be

discussed in paragraph 4.3.

[]

5

10

15

20

25

Equity incentives and earnings management in the U.K.

4.1 Data and sample

As mentioned earlier in this thesis, most research done until now, focuses on

companies in the U.S. This research investigates the European situation. The U.K.

was one of the first countries in Europe where companies were required to report on

the remunerations of their directors. Therefore this research will focus on companies

based in the U.K.

Listed companies on the FTSE 100 index from the period 2005 - 2006 will be used as

the sample for this research. The FTSE 100 index from April 13 th 2009 is used as the

start of the sample selection. From the 100 listed firms on that date, 8 firms are

excluded because they did not exist in 2005 and/or 2006, or because they were not

listed in 2005 and/or 2006 on the FTSE 100 index. Furthermore 4 firms are excluded

because there is not enough information regarding the compensation data available

in the annual reports. Therefore the actual sample consists of 88 firms and 176

entries. Appendix B contains a list of all the listed firms on the FTSE that are taken

into account in this study.

This research focuses on 2005 and 2006 and not on more recent years because of

two main reasons. First of all because the global financial crisis started in 2007. So

the figures from 2007 until now are less comparable with those of 2005 and 2006.

Second, there is more data available for 2005 and 2006. When the writing process

regarding this thesis started, the annual reports for 2008 for most companies were

not available yet.

Because of these complications in more recent years, the data sample is from 2005

to 2006. All the financial data that is needed for the earnings management

component, and compensation data from the CEO’s that is needed for the

compensation component, will be gathered from the annual reports of the

companies.

4.2 Dependant variable

The dependant variable in this study is earnings management. An accruals model

(the Modified Jones Model) will be used as a measure of earnings management. The

Modified Jones Model takes place in two stages. The first stage of the Modified

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

Jones Model is identical to the original Jones Model, therefore they both are

described in this paragraph.

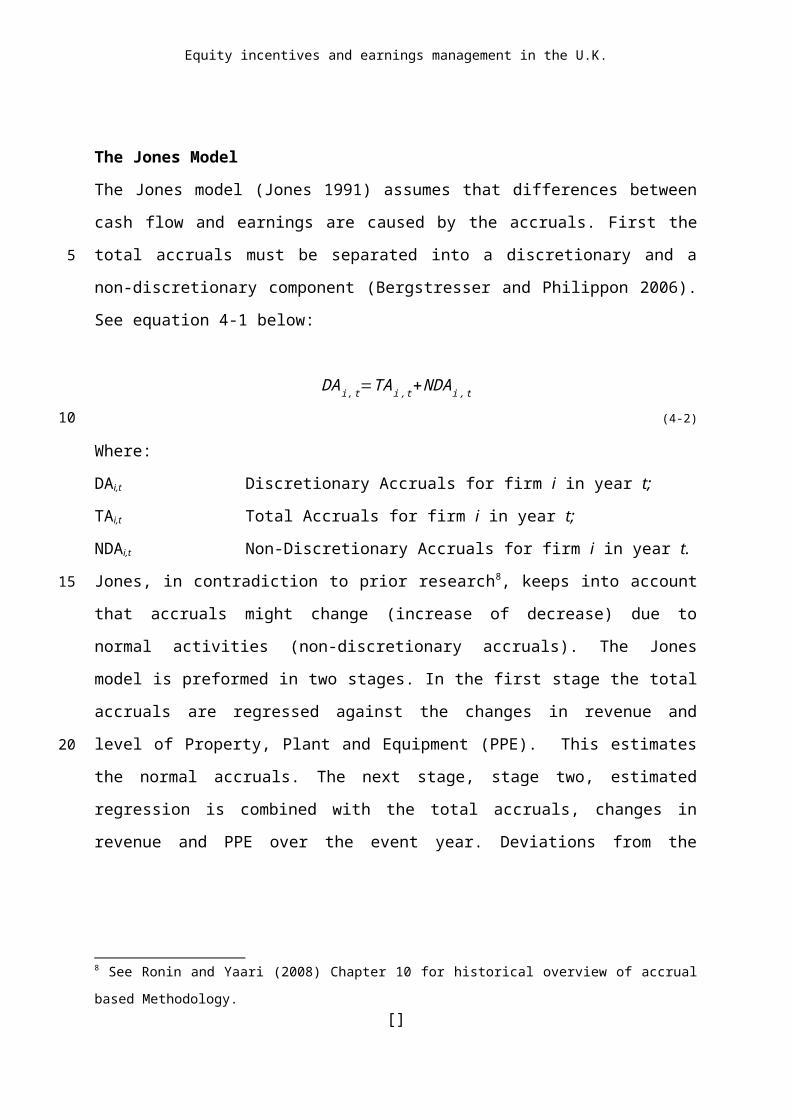

The Jones ModelThe Jones model (Jones 1991) assumes that differences between cash flow and

earnings are caused by the accruals. First the total accruals must be separated into a

discretionary and a non-discretionary component (Bergstresser and Philippon 2006).

See equation 4-1 below:

DAi ,t=TA i ,t+NDA i ,t

(4-2)

Where:

DAi,t Discretionary Accruals for firm i in year t;

TAi,t Total Accruals for firm i in year t;

NDAi,t Non-Discretionary Accruals for firm i in year t.

Jones, in contradiction to prior research8, keeps into account that accruals might

change (increase of decrease) due to normal activities (non-discretionary accruals).

The Jones model is preformed in two stages. In the first stage the total accruals are

regressed against the changes in revenue and level of Property, Plant and

Equipment (PPE). This estimates the normal accruals. The next stage, stage two,

estimated regression is combined with the total accruals, changes in revenue and

PPE over the event year. Deviations from the estimated regression depict the non-

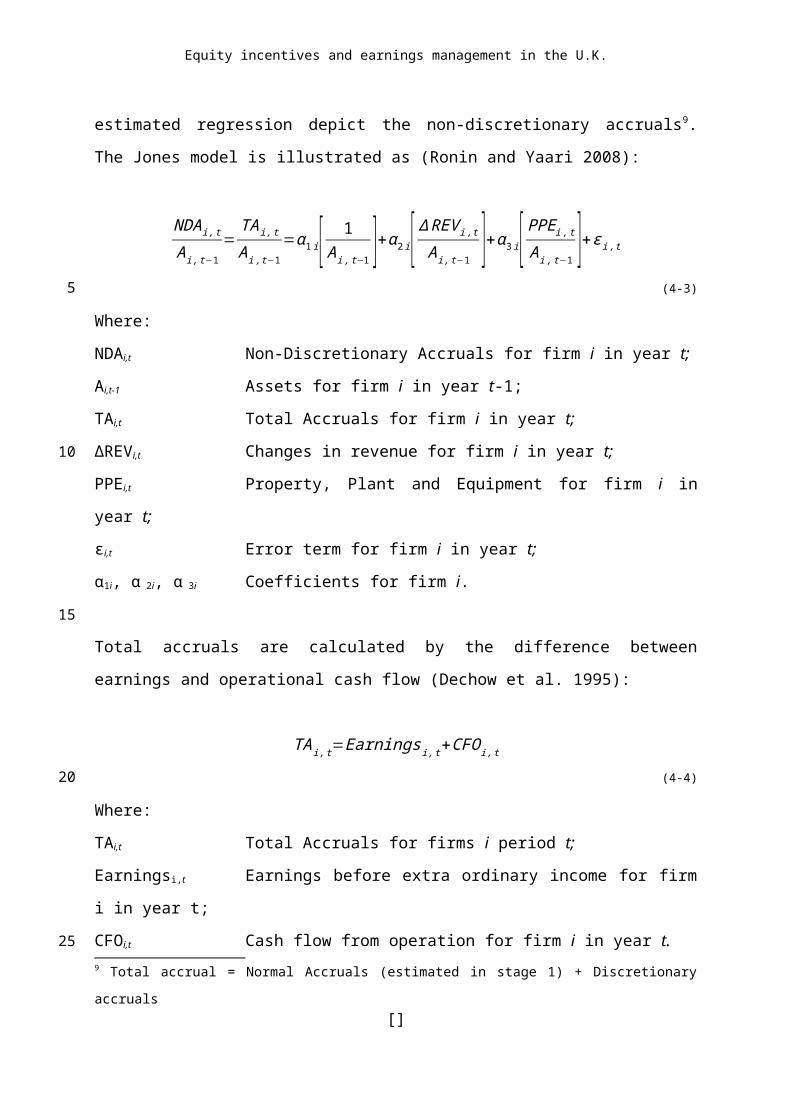

discretionary accruals9. The Jones model is illustrated as (Ronin and Yaari 2008):

NDA i , t

Ai ,t−1=

TAi , t

A i ,t−1=α1 i[ 1

Ai , t−1 ]+α 2i[ ∆ REV i , t

A i ,t−1 ]+α 3 i[ PPE i ,t

A i ,t−1 ]+εi ,t(4-3)

Where:

NDAi,t Non-Discretionary Accruals for firm i in year t;

Ai,t-1 Assets for firm i in year t-1;

TAi,t Total Accruals for firm i in year t;

8 See Ronin and Yaari (2008) Chapter 10 for historical overview of accrual based Methodology. 9 Total accrual = Normal Accruals (estimated in stage 1) + Discretionary accruals

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

∆REVi,t Changes in revenue for firm i in year t;

PPEi,t Property, Plant and Equipment for firm i in year t;

εi,t Error term for firm i in year t;

α1i, α 2i, α 3i Coefficients for firm i.

Total accruals are calculated by the difference between earnings and operational

cash flow (Dechow et al. 1995):

TAi , t=Earningsi , t+CFOi , t

(4-4)

Where:

TAi,t Total Accruals for firms i period t;

Earningsi,t Earnings before extra ordinary income for firm i in year t;

CFOi,t Cash flow from operation for firm i in year t.

When measuring earnings management, | TA it | will be used. The Jones model

deflates all variables (ΔREV and PPT) with total assets from t-1 (beginning-of-the-

year). This overcomes hetroskedasticity10 (Ronin and Yaari 2008).

The coefficients αχ are industry specific parameters. They estimate how different

industries, with difference in capital intensity, are influenced by the variables (Assets,

Revenue and PPT). Capital intensive industries will have a relatively greater PPE

element than knowledge based industries.

Using only the standard Jones model would be short-sighted. The greatest weakness

lies in the fact that the Jones model does not take into account the ability of

managers for sales-based manipulation (Peasnell et al. 2000), because accruals are

deflated for changes in revenue. Jones considers these changes, as changes in

economic activity. Therefore Dechow et al. (1995) modified the original Jones model

to incorporate the possible changes in revenue that are discretionary.

The Modified Jones Model

10 “... when residuals at each end of the [dependant] variable(s) have unequal variances.” Therefore

the spread in the data is different. Source: Fields (2002)[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

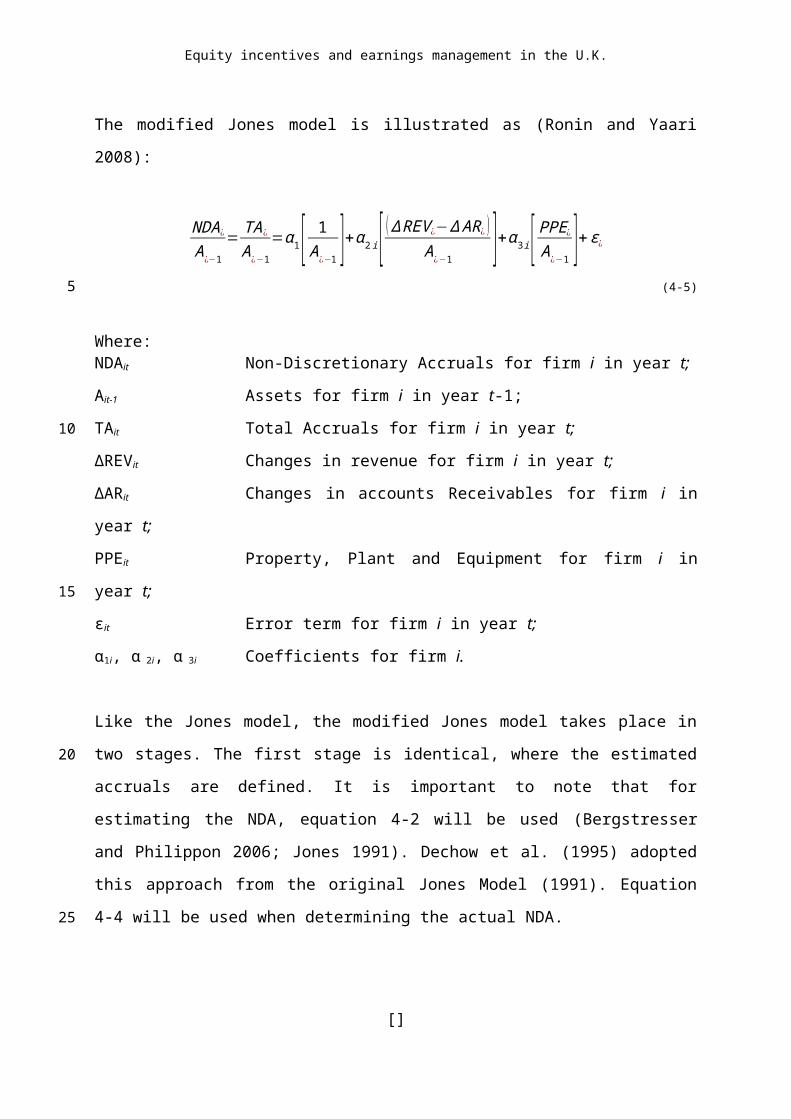

The model that will be used to determine the non-discretionary accruals is the

modified Jones model (Dechow et al. 1995). The model finds its origin in the

standard Jones Model. However, Dechow et al. (1995) have managed to incorporate

the ability to detect sales-based manipulations.

The modified Jones model is illustrated as (Ronin and Yaari 2008):

NDA¿

A¿−1=

TA¿

A¿−1=α1[ 1

A ¿−1 ]+α 2 i[ (∆ REV ¿−∆ AR¿ )A ¿−1 ]+α3 i[ PPE¿

A ¿−1 ]+ε¿

(4-5)

Where:NDAit Non-Discretionary Accruals for firm i in year t;

Ait-1 Assets for firm i in year t-1;

TAit Total Accruals for firm i in year t;

∆REVit Changes in revenue for firm i in year t;

∆ARit Changes in accounts Receivables for firm i in year t;

PPEit Property, Plant and Equipment for firm i in year t;

εit Error term for firm i in year t;

α1i, α 2i, α 3i Coefficients for firm i.

Like the Jones model, the modified Jones model takes place in two stages. The first

stage is identical, where the estimated accruals are defined. It is important to note

that for estimating the NDA, equation 4-2 will be used (Bergstresser and Philippon

2006; Jones 1991). Dechow et al. (1995) adopted this approach from the original

Jones Model (1991). Equation 4-4 will be used when determining the actual NDA.

4.3 Independent variable

The independent variables will be the type of compensation, for the different

hypotheses. For this research, the relative size of the compensation type will be used

to measure compensation. Relative figures are better comparable with each other. It

is generally accepted that absolute compensation differences between managers are

caused by firm characteristics.

To measure the relative power of the different compensation types (i.e. stock-based,

fixed salary, and bonus) an approach used by Bergstresser and Philippon (2006) will []

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

be adopted.

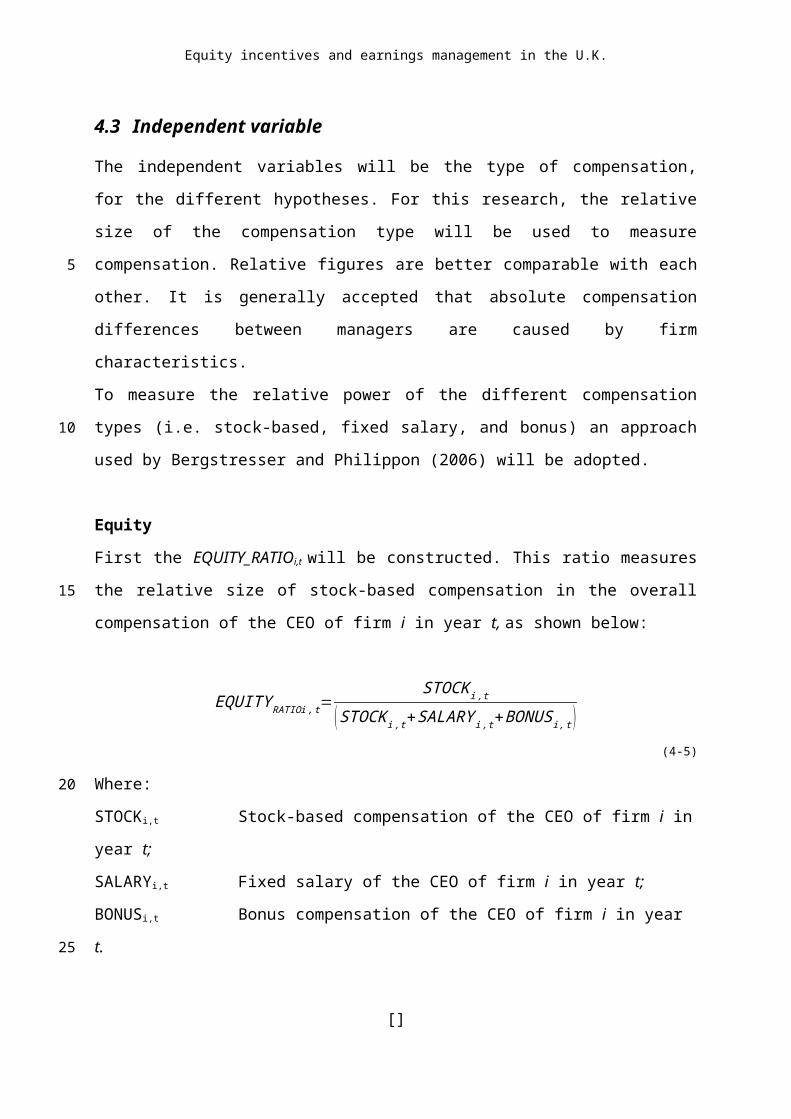

EquityFirst the EQUITY_RATIOi,t will be constructed. This ratio measures the relative size

of stock-based compensation in the overall compensation of the CEO of firm i in year

t, as shown below:

EQUITY RATIOi ,t=STOCK i ,t

(STOCK i ,t+SALARY i ,t+BONUSi , t )(4-5)

Where:

STOCKi,t Stock-based compensation of the CEO of firm i in year t;

SALARYi,t Fixed salary of the CEO of firm i in year t;

BONUSi,t Bonus compensation of the CEO of firm i in year t.

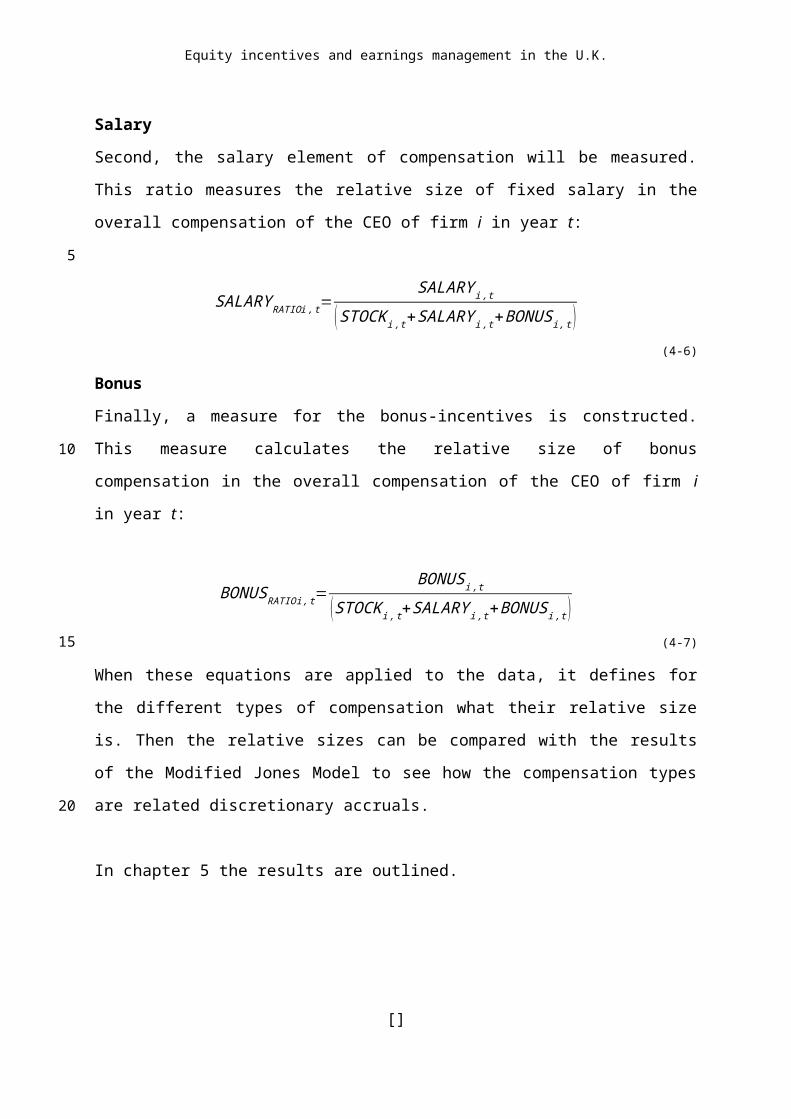

SalarySecond, the salary element of compensation will be measured. This ratio measures

the relative size of fixed salary in the overall compensation of the CEO of firm i in

year t:

SALARY RATIOi ,t=SALARY i ,t

(STOCK i , t+SALARY i, t+BONUSi ,t ) (4-6)

BonusFinally, a measure for the bonus-incentives is constructed. This measure calculates

the relative size of bonus compensation in the overall compensation of the CEO of

firm i in year t:

BONUSRATIOi ,t=BONUSi ,t

(STOCK i , t+SALARY i ,t+BONUSi ,t ) (4-7)

When these equations are applied to the data, it defines for the different types of

compensation what their relative size is. Then the relative sizes can be compared

[]

5

10

15

20

25

30

Equity incentives and earnings management in the U.K.

with the results of the Modified Jones Model to see how the compensation types are

related discretionary accruals.

In chapter 5 the results are outlined.

[]

5

Equity incentives and earnings management in the U.K.

5 Data analysis and results

The previous chapter explained the selection procedures in constructing a sample to

test the hypotheses. The total collected sample consists of 88 FTSE 100 index listed

firms and contains data over 2005 and 2006.

In this chapter the results from the research will be described. Paragraph 5.1 will

elaborate on the descriptive statistics and how the discretionary accruals by means

of the Modified Jones Model are computed. Next the hypotheses will be tested using

correlation testing and the independent-samples t-test. The results of these tests will

be outlined in paragraph 5.2.

5.1 Discretionary accruals and descriptive statistics

This paragraph will elaborate on the discretionary accruals and descriptive statistics.

First the discretionary accruals are determined. In the Modified Jones Model, the

error term is the discretionary accrual for a firm. On page 34 the modified Jones

model is illustrated as:

NDA¿

A¿−1=

TA¿

A¿−1=α1[ 1

A ¿−1 ]+α 2 i[ (∆ REV ¿−∆ AR¿ )A ¿−1 ]+α3 i[ PPE¿

A ¿−1 ]+ε¿

(4-4)

Where:

NDAit Non-Discretionary Accruals for firm i in year t;

Ait-1 Assets for firm i in year t-1;

TAit Total Accruals for firm i in year t;

∆REVit Changes in revenue for firm i in year t;

∆ARit Changes in accounts Receivables for firm i in year t;

PPEit Property, Plant and Equipment for firm i in year t;

εit Error term for firm i in year t;

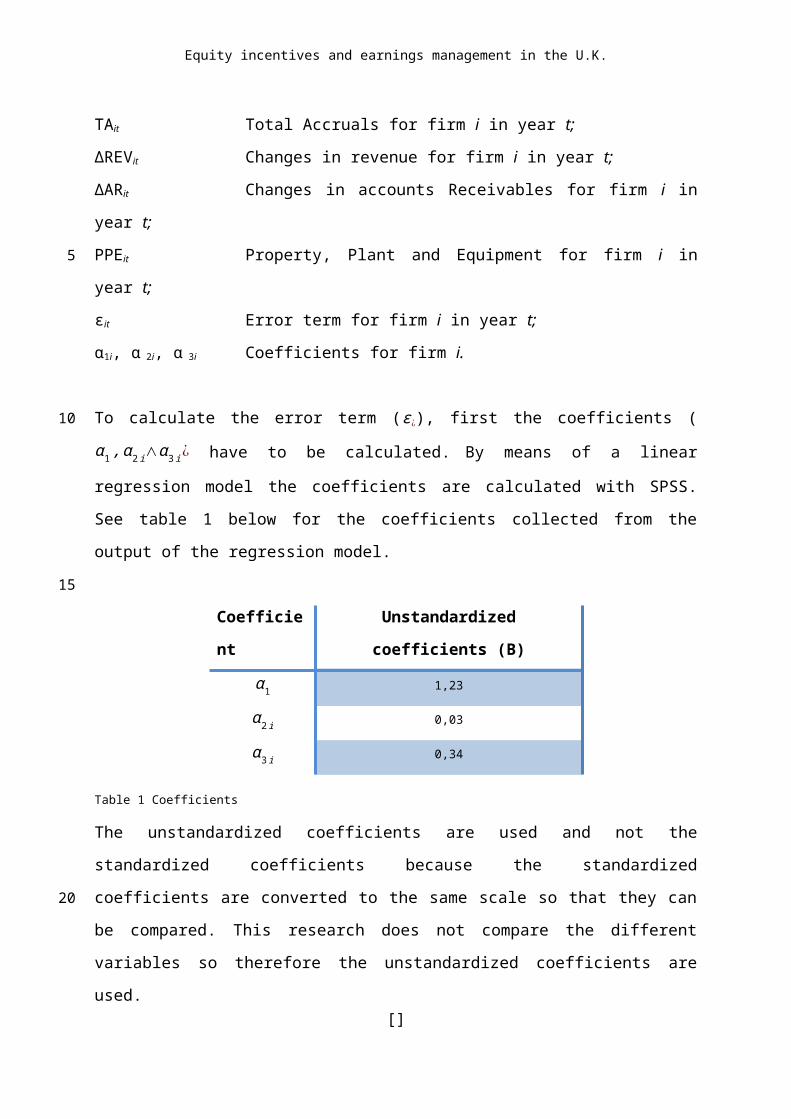

α1i, α 2i, α 3i Coefficients for firm i.

To calculate the error term (ε ¿), first the coefficients (α 1 , α 2 i∧α 3 i¿ have to be

calculated. By means of a linear regression model the coefficients are calculated with

[]

5

10

15

20

25

Equity incentives and earnings management in the U.K.

SPSS. See table 1 below for the coefficients collected from the output of the

regression model.

Coefficient Unstandardized coefficients (B)

α 1 1,23

α 2 i 0,03

α 3 i 0,34

Table 1 Coefficients

The unstandardized coefficients are used and not the standardized coefficients

because the standardized coefficients are converted to the same scale so that they

can be compared. This research does not compare the different variables so

therefore the unstandardized coefficients are used.

The output from SPSS further shows the adjusted R Square. The adjusted R Square

measures the proportion of the variation in the dependent variable (total accruals

scaled by assets) accounted for by the explanatory variables. For this model the

Adjusted R Square is 0,485 (48,5%), which is a reasonable percentage.

Now all variables are available, the error term (ε ¿) for each of the 176 companies is

determined. For the error terms (discretionary accruals) see appendix B on page 62.

The error terms in appendix B only concern absolute values. Even though earnings

management involves both positive and negative values of accruals, it does not

matter whether the value of the error term is positive or negative for this study. This is

because the magnitude of discretionary accruals is important, not whether the effect

is positive or negative. Now that the error terms (discretionary accruals) are

determined, the descriptive statistics over the data that is used in this research can

be computed.

From the 1st of January 2005 all listed European Union companies are required to

comply to the International Financial Reporting Standards (IFRS). Therefore the data

from 2005 and 2006, which is used in this research, is comparable. For this reason

the descriptive statistics for the data of 2005 and 2006 are calculated and presented

as one dataset.[]

5

10

15

20

25

Equity incentives and earnings management in the U.K.

For the descriptive statistics the mean, median, standard deviation, minimum and

maximum for the years 2005 and 2006 together are computed. The descriptive

statistics are computed for the error term (discretionary accruals), the accrual data

and for the compensation data. The compensation data consist of three different

types of compensation; fixed salary, stock-based compensation and bonus. For the

descriptive statistics, see table 2 on the next page.

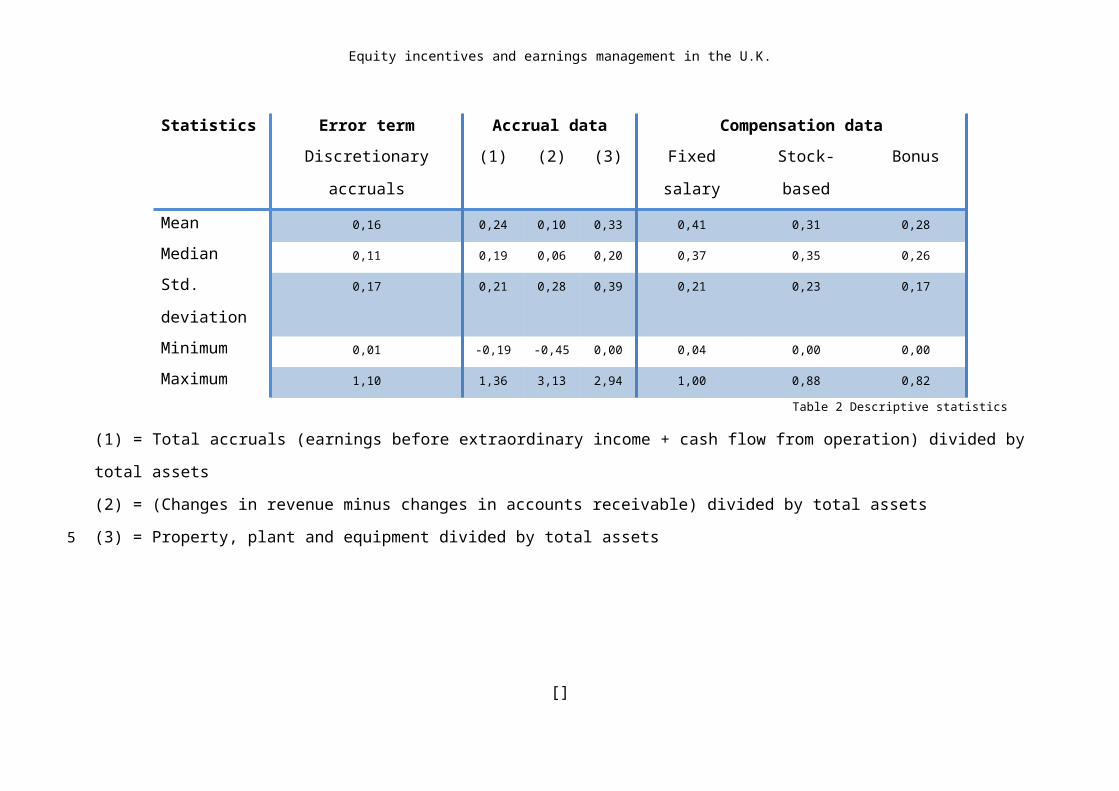

The statistics in table 2 show that, concerning the compensation data, fixed salary

has the highest mean (0,41) with respect to stock-based compensation (0,31) and

bonus compensation (0,28). Further stock-based compensation has the largest

standard deviation (0,23). See table 2 on the next page for detailed information about

the descriptive statistics.

5.2 Results

As described in Chapter 3, the hypotheses in this research is are:

1. Fixed salary is negatively related to the use of discretionary accruals as a tool for earnings management.

2. Bonus compensation is positively related to the use of discretionary accruals

as a tool for earnings management.

3. Stock-based compensation is positively related to the use of discretionary

accruals as a tool for earnings management.

To test the hypotheses, first a correlation test will be performed in paragraph 5.2.1 to

obtain understanding about the strength of the relationship between the different

types of compensation and discretionary accruals. Furthermore an independent-

samples t-test will be performed, see paragraph 5.2.2, to test whether there is a

significant difference in mean scores of discretionary accruals for each of the

compensation types.

[]

5

10

15

20

25

Equity incentives and earnings management in the U.K.

Statistics Error term Accrual data Compensation dataDiscretionary accruals (1) (2) (3) Fixed salary Stock-based Bonus

Mean 0,16 0,24 0,10 0,33 0,41 0,31 0,28

Median 0,11 0,19 0,06 0,20 0,37 0,35 0,26

Std. deviation 0,17 0,21 0,28 0,39 0,21 0,23 0,17

Minimum 0,01 -0,19 -0,45 0,00 0,04 0,00 0,00

Maximum 1,10 1,36 3,13 2,94 1,00 0,88 0,82