the renminbi: 2014 and beyond - deutsche bank · the renminbi: 2014 and beyond 4 switching to the...

TRANSCRIPT

The Renminbi: 2014 and beyondTranslating developments into tangible business opportunities

Deutsche BankGlobal Transaction Banking

Deutsche BankThe Renminbi: 2014 and beyond

3

The purpose of this whitepaper

As internationalisation of the Renminbi continues at a rapid pace, actively driven by China’s economic strategy, corporates must ensure they’re positioned to translate the currency’s development into tangible business opportunities.

This applies to any corporate that has (or is likely to have) any form of exposure to the currency, whether via trade connections with China, an onshore branch or subsidiary, or where Renminbi payments constitute a large part of treasury risk. Certainly, corporate treasurers in particular have much to gain from adopting the Renminbi – no longer idly cited as the currency of the future, but quantifiably and undeniably the currency of today.

Of course, making the switch is undoubtedly a complex undertaking. With this in mind, this Deutsche Bank whitepaper, coming in addition to regular Renminbi updates, outlines the benefits of utilising the Renminbi as a treasury management currency, alongside its investment possibilities, and addresses the challenges companies will face in this respect.

The Renminbi has been cited quantifiably and undeniably the currency of today

Deutsche BankThe Renminbi: 2014 and beyond

4

Switching to the Renminbi

In order to convert Renminbi-related regulatory and market developments into real business benefits, corporates must first gain a clear understanding of the currency’s continued (and policy-driven) upward trajectory, and the opportunities this creates.

As a trade settlement currency, the Renminbi is already employed in the same way as the US dollar and euro, in that it can be used as the underlying currency for Letters of Credit. Its use in this respect has grown exponentially since the 2009 launch of a cross-border settlement pilot programme. Just four years later, the Renminbi moved ahead of the Hong Kong dollar and Singapore dollar to become the eighth most-traded world currency, and overtook the euro to become the second most-utilised currency in trade finance. The speed of progress has been phenomenal. In the last month of 2013, the value of Renminbi used globally rose by 15%, compared to a 7% increase for other currencies.

The growing importance of the currency can be seen not just in these rising figures but also in the Renminbi’s increasingly international reach. As of October 2013, the top three markets (outside of China and Hong Kong) using the currency for trade settlement were Singapore, Germany and Australia. While the Asia/Australia bias is hardly surprising due to geographic proximity, its growing use as a trade settlement currency in Europe is notable. And it’s not just Germany that is embracing the currency; France is also realising the competitive advantages to be gained from Renminbi-denominated trade, with nearly 10%1 of Sino-French trade now settled in Renminbi. In fact, Renminbi settlement in EU-China bilateral trade is likely to triple to 5-6%2 of China’s global trade within the next three years.

Looking further afield, use of the Renminbi as a trade settlement currency is also expected to pick up in emerging markets. Africa is a prime example, with swift progress expected thanks to the region’s burgeoning bilateral trade flows with China, its largest trading partner3.

In one month alone (between November and December 2013) the value of Renminbi used globally rose by

15%

1http://www.euromoney.com/Article/3201243/European-capitals-scramble-to-arrange-currency-trade-deals-with-China.html 2June CNH Market Monitor3http://www.fxweek.com/fx-week/feature/2254234/renminbi-hedging-and-africa-the-final-frontier

Deutsche BankThe Renminbi: 2014 and beyond

5

Two key factors lie behind the currency’s continued advance. First is China’s economic strategy. A determination to internationalise the Renminbi as a means to economic growth has sparked a series of policy changes designed to improve the currency’s accessibility. For example, documentary requirements have been significantly eased for corporates boasting good track records, and Renminbi trade transactions are now available electronically. This not only immediately enhances ease-of-use, but also ties in with corporates’ growing demand for the automation of processes and resulting efficiencies.

Second, and adding real momentum to the growth kick-started by such policy-driven developments, are the commercial benefits to be gained from settling obligations of Chinese enterprises in Renminbi. Certainly, for foreign corporates with commercial flows with China, there are practical and quantifiable benefits to pricing and accepting payment in Renminbi. By being able to forgo the often costly surcharges associated with acquiring a foreign exchange quota and hedging currency exposure using onshore rates, Chinese corporates could reduce their transaction costs with foreign companies and pass along savings of around 3-5%, and even up to 7%. For companies in lower-margin businesses, for example importing consumer goods or electronics from China, a saving of this magnitude could have a significant impact on their bottom line.

In addition, for foreign companies with a growing presence in the country, adopting the Renminbi will enable them to self-fund investments and/or expand their market share with greater flexibility than if they had to raise Renminbi from the market. This is because onshore access to foreign currencies isn’t always straightforward, potentially limiting a company’s Chinese customer base. With the Renminbi, such limitations disappear; a clear motivation for making the switch.

Ultimately, for corporates with any form of commercial exposure to China or its internationalising currency, the ability to use the Renminbi is both an immediate competitive advantage and vital to future strategy.

Deutsche BankThe Renminbi: 2014 and beyond

6

Of course, adopting the Renminbi is easier said than done. It’s a task that requires the engagement and cooperation of major stakeholders and counterparties throughout each stage of the process. Furthermore, as China’s administration continues to implement a stream of reforms, corporates will need to overcome a number of multifaceted regulatory and operational obstacles that form the primary source of complexity.

For example, while the Renminbi is a single currency, FX controls and regulations mean companies need to separate Renminbi funds into two distinct onshore and offshore pools. In practical terms, this means treating Renminbi as two currencies: CNY (Renminbi held onshore) and CNH (Renminbi held offshore).

This may be further complicated, however, by the fact that CNH is only a “convenience term”. CNY is the only official ISO code for the Renminbi and does not in itself allow systems to differentiate and make payments across the onshore and offshore pools. As the onshore rate is regulated and the offshore rate is determined by the market, interest rates and exchange rates between the two pools differ. Therefore, it is vital that corporates’ operating systems can distinguish between the two.

For corporates looking to switch to the Renminbi, the scale of the challenge should not be underestimated. Indeed, it is vital corporates gain a clear overview of what is ultimately a tri-partite journey. This applies equally to those corporates that have yet to commit to moving to the Renminbi. In this respect, market dynamics may soon dictate their behaviour.

Pinpointing the challenges

Deutsche BankThe Renminbi: 2014 and beyond

7

Stage one is the need to secure buy-in from internal stakeholders and counterparties. Ensuring that in-house operations and thinking are aligned across departments is a vital consideration, and corporates should look to their banks to provide education and consultative support.

Stage two is the need to overcome high-level hurdles with regards to evolving rules and regulations. This, in reality, is a matter of communication and understanding. Indeed, understanding is perhaps the most important element throughout Renminbi adoption. Companies need to make every effort to stay abreast of regulatory developments, again looking to their banks to help them in this regard.

Finally, there is the more practical question of technology. Corporates will need to upgrade their infrastructure, beginning with treasury and accounting systems. This can be a complex undertaking, not least because there can be no “one-size-fits-all” approach to making systems and procedures Renminbi-ready. In fact, the process will largely depend on individual companies’ existing set-ups. Deutsche Bank’s checklist (see next page) of the issues that must be considered at a granular level can provide some guidance here.

For corporates looking to switch to the Renminbi, the scale of the challenge should not be under-estimated

Deutsche BankThe Renminbi: 2014 and beyond

8

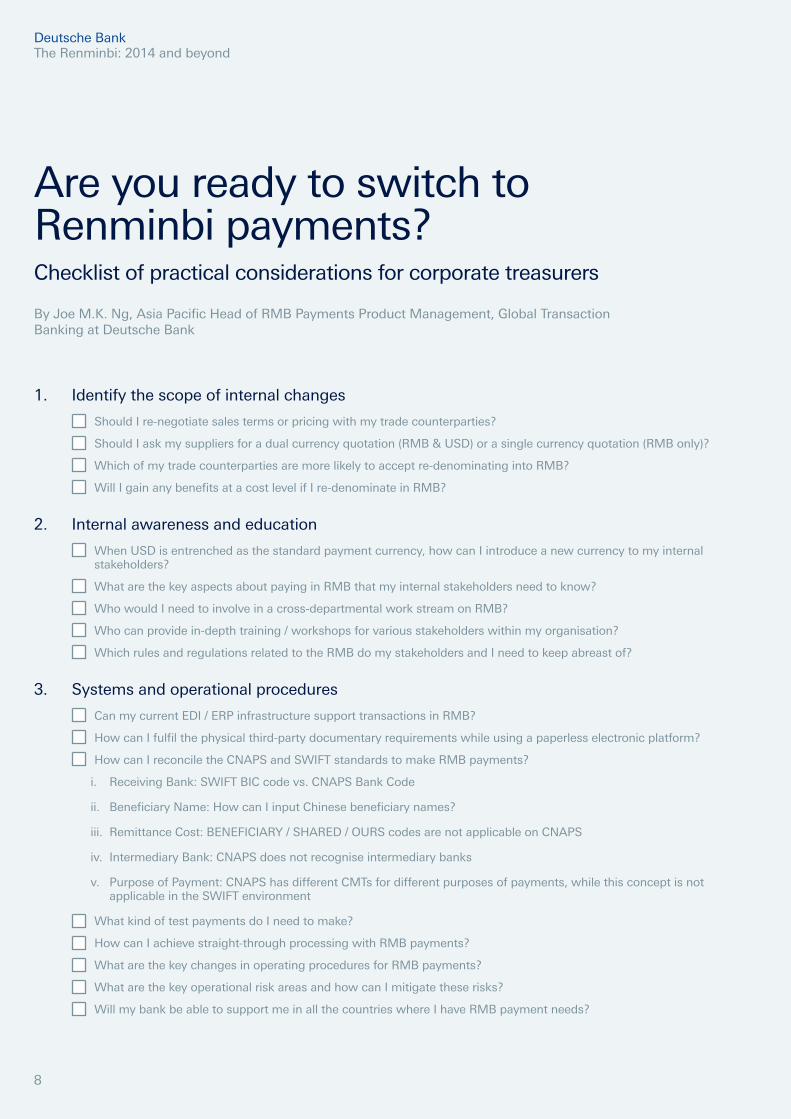

Are you ready to switch to Renminbi payments?Checklist of practical considerations for corporate treasurers

By Joe M.K. Ng, Asia Pacific Head of RMB Payments Product Management, Global Transaction Banking at Deutsche Bank

1. Identify the scope of internal changes

Should I re-negotiate sales terms or pricing with my trade counterparties?

Should I ask my suppliers for a dual currency quotation (RMB & USD) or a single currency quotation (RMB only)?

Which of my trade counterparties are more likely to accept re-denominating into RMB?

Will I gain any benefits at a cost level if I re-denominate in RMB?

2. Internal awareness and education

When USD is entrenched as the standard payment currency, how can I introduce a new currency to my internal stakeholders?

What are the key aspects about paying in RMB that my internal stakeholders need to know?

Who would I need to involve in a cross-departmental work stream on RMB?

Who can provide in-depth training / workshops for various stakeholders within my organisation?

Which rules and regulations related to the RMB do my stakeholders and I need to keep abreast of?

3. Systems and operational procedures

Can my current EDI / ERP infrastructure support transactions in RMB?

How can I fulfil the physical third-party documentary requirements while using a paperless electronic platform?

How can I reconcile the CNAPS and SWIFT standards to make RMB payments?

i. Receiving Bank: SWIFT BIC code vs. CNAPS Bank Code

ii. Beneficiary Name: How can I input Chinese beneficiary names?

iii. Remittance Cost: BENEFICIARY / SHARED / OURS codes are not applicable on CNAPS

iv. Intermediary Bank: CNAPS does not recognise intermediary banks

v. Purpose of Payment: CNAPS has different CMTs for different purposes of payments, while this concept is not applicable in the SWIFT environment

What kind of test payments do I need to make?

How can I achieve straight-through processing with RMB payments?

What are the key changes in operating procedures for RMB payments?

What are the key operational risk areas and how can I mitigate these risks?

Will my bank be able to support me in all the countries where I have RMB payment needs?

Deutsche BankThe Renminbi: 2014 and beyond

9

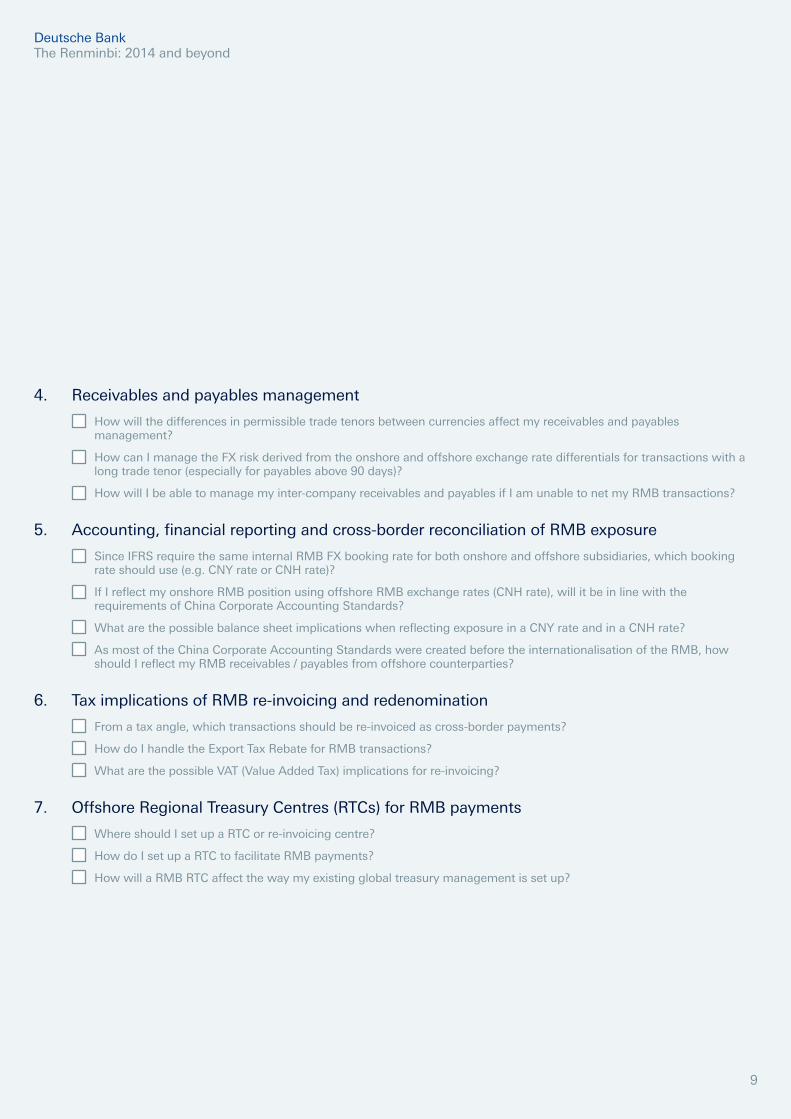

4. Receivables and payables management

How will the differences in permissible trade tenors between currencies affect my receivables and payables management?

How can I manage the FX risk derived from the onshore and offshore exchange rate differentials for transactions with a long trade tenor (especially for payables above 90 days)?

How will I be able to manage my inter-company receivables and payables if I am unable to net my RMB transactions?

5. Accounting, financial reporting and cross-border reconciliation of RMB exposure

Since IFRS require the same internal RMB FX booking rate for both onshore and offshore subsidiaries, which booking rate should use (e.g. CNY rate or CNH rate)?

If I reflect my onshore RMB position using offshore RMB exchange rates (CNH rate), will it be in line with the requirements of China Corporate Accounting Standards?

What are the possible balance sheet implications when reflecting exposure in a CNY rate and in a CNH rate?

As most of the China Corporate Accounting Standards were created before the internationalisation of the RMB, how should I reflect my RMB receivables / payables from offshore counterparties?

6. Tax implications of RMB re-invoicing and redenomination

From a tax angle, which transactions should be re-invoiced as cross-border payments?

How do I handle the Export Tax Rebate for RMB transactions?

What are the possible VAT (Value Added Tax) implications for re-invoicing?

7. Offshore Regional Treasury Centres (RTCs) for RMB payments

Where should I set up a RTC or re-invoicing centre?

How do I set up a RTC to facilitate RMB payments?

How will a RMB RTC affect the way my existing global treasury management is set up?

Deutsche BankThe Renminbi: 2014 and beyond

10

The onshore and offshore perspectives

Although bank support may still be required, successful development of these key elements (internal buy-in, understanding and technology) should help companies manage the challenges and risks associated with Renminbi.

For those onshore, convincing foreign suppliers to accept Renminbi could still prove challenging despite the commercial advantages to be gained. This is for three key reasons.

First, many chief financial officers (CFOs) have yet to determine precisely how the Renminbi may be leveraged to the benefit of their companies, and are still assessing the scope and cost of the adoption challenge. Managing the move will largely depend on the CFO’s experience. For example, those that were involved in the implementation of the euro will have a working knowledge of what Renminbi adoption will involve, although the need to manage the challenges posed by onshore and offshore Renminbi pools adds to the complexity.

Second, the move to the Renminbi requires involvement at all levels within the company. Payables and receivables management presents particular challenges, in that the use of a new currency (for both invoicing and pricing) is not something that can be implemented overnight. While many cross-border trade deals are now settled in Renminbi, they remain largely priced and invoiced in US dollars. If the Renminbi is to become an international currency, its adoption must gain critical mass across the various ways companies utilise international currencies.

Finally, non-Chinese companies may be deterred by FX risks. The complexities associated with convertibility issues, and limitations with respect to the deployment and reinvestment of the Renminbi they receive, must also be addressed. Indeed, corporate treasurers can no longer view the Renminbi as a “sure bet”. In March 2014, the People’s Bank of China (PBOC) announced that the USD/CNY Spot FX intraday trading band would widen from 1% to 2% (or 4% in aggregate). And in February 2014, the currency experienced its biggest three-day fall since 2011, dropping as much as 1.3% against the US dollar. With the introduction of greater two-way volatility, companies must fully understand the implications of paying, receiving and holding Renminbi on their balance sheets.

Corporate treasurers can no longer view the Renminbi as a “sure bet”

Deutsche BankThe Renminbi: 2014 and beyond

11

Anticipating developments

Of course, anticipating such developments and their implications is easier said than done. Corporates will need to consider not just the short and long-term effects of two-way volatility (and how best to manage the resulting FX risk) but also the Chinese central bank’s broader aims and likelihood of intervention. That said, two key trends are clear.

First, widening the trading band has emerged as a preferred means for gradually liberalising the exchange rate. The band was widened from +/-0.3% to +/-0.5% in May 2007, then to +/-1% in April 2012, and most recently to +/-2% in March 2014, so further developments should be expected and we predict the band could potentially be widened to +/-3% in the next two years. The implications of this policy move include near-term upside risk on USD/RMB in the onshore and offshore spot and forwards markets, as well as upside risk on Renminbi FX volatility. As market forces play an ever-greater role in determining the Renminbi exchange rate, there are likely to be fewer occurrences of intervention from the central bank, unless there is a significant surge of speculative inflows or outflows.

The second trend is the rapid development of the offshore Renminbi cross-currency swap (CCS) market, as corporates take positions on FX spots, forwards and structured products to hedge FX risk in their cash flows. Daily turnover has jumped from US$1.5-2 billion in January 2013 to US$4.5-5 billion today, and there is growing demand for corporate funding and liability hedging (in accordance with greater offshore Renminbi, or CNH, bond issuance). Furthermore, more real money and hedge fund investors are trading on the offshore CCS curve for hedging or trading purposes. In fact, the curve has now evolved into the most important offshore Renminbi benchmark interest rate curve, with substantial growth potential.

+/-3%

The trading band may become as wide as

Deutsche BankThe Renminbi: 2014 and beyond

12

Understanding all these changes is undoubtedly a challenging task, and the ability to successfully manage Renminbi funds requires further effort, from assessing how the disproportionate flow of Renminbi funds will be managed, to how the Renminbi funds received are best deployed. While FX swaps are available, they may not be cost-effective. And other possibilities, such as using Renminbi funds to invest in China, are not without their complications.

These are weighty issues, but foreign corporates that have yet to make the switch should look beyond these factors. With the rise of the Renminbi and importance of Chinese companies to global supply chains set to continue, such foreign entities may run the risk of losing business as the ability to settle in Renminbi becomes not only a competitive advantage but a minimum requirement.

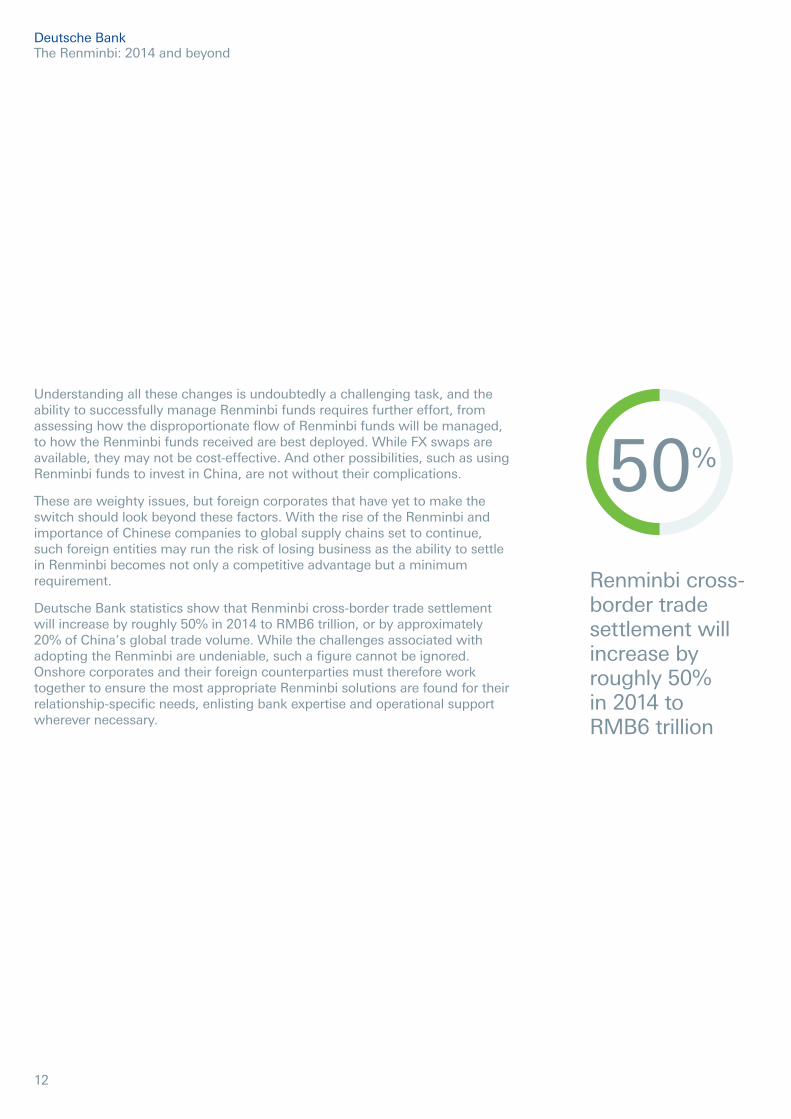

Deutsche Bank statistics show that Renminbi cross-border trade settlement will increase by roughly 50% in 2014 to RMB6 trillion, or by approximately 20% of China’s global trade volume. While the challenges associated with adopting the Renminbi are undeniable, such a figure cannot be ignored. Onshore corporates and their foreign counterparties must therefore work together to ensure the most appropriate Renminbi solutions are found for their relationship-specific needs, enlisting bank expertise and operational support wherever necessary.

50%

Renminbi cross-border trade settlement will increase by roughly 50% in 2014 to RMB6 trillion

Deutsche BankThe Renminbi: 2014 and beyond

13

Optimising Renminbi funds

While the Renminbi’s evolution from a trade settlement currency to a treasury management currency is encouraging, it will not be a true global currency until it is fully convertible. Indeed, the currency’s capital controls have posed certain limitations on cross-border Renminbi trading.

However, there is every indication that this relatively tight grip is loosening. And as convertibility risk has been a concern for corporates, investors and fund managers alike, positive developments in this respect can only be for the greater good. In fact, further improvements are likely to act as a catalyst for market participants to use the Renminbi not just for trade settlement but also for investment, asset allocation and diversification. In time, usage of the currency could even extend to include central bank reserve management.

Regulatory reform and formal statements of intent are the market’s best way of gauging China’s intentions with regard to moving towards full convertibility. The country’s twelfth five-year plan (for 2011-2015) is perhaps the most significant indicator, and makes it clear that efforts to improve convertibility and reform exchange rate restrictions are set to continue.

The market has already seen notable progress in this respect. For example, in July 2013, the PBOC simplified the documentary review of underlying trade transactions and announced new measures to further promote offshore activity, including the extension of the cross-border intercompany loan pilot scheme. For MNCs looking to free up liquidity trapped in China, deregulation can be a boon for working capital management, enabling them to utilise their Renminbi in China with and across subsidiaries.

Convertibility risk has been a concern for corporates, investors and fund managers

Deutsche BankThe Renminbi: 2014 and beyond

14

Foreign Exchange

Such developments come against a broader backdrop of growing market confidence and a deepening FX market. In March 2014, London and Frankfurt were added to the list of locations outside mainland China where Renminbi transactions can be settled directly, following on from the appointment of clearing banks in Taiwan, Singapore and Malaysia.

The establishment of offshore clearing banks has not only facilitated Renminbi cross-border trade settlement, but has also provided a channel for potential Renminbi liquidity supply in the offshore market, and possibly a window for cross-border flows to be channelled back onshore.

Deposit growth in these locations has also exceeded many expectations. Data from Taiwan’s central bank shows that Renminbi deposits soared to RMB268 billion in April 20144, from RMB17.4 billion in August 2012. In Singapore, the value of Renminbi deposits reached approximately RMB200 billion5 at the end of 2013, having stood at RMB60 billion6 just a year earlier. And Renminbi deposits in London reached RMB14 billion7 at the end of 2013. By the end of 2014, the total offshore Renminbi deposit base (including certificates of deposit) is likely to hit RMB2.5 trillion8.

Basic convertibility will likely see significant expansion for FX conversion quotas as well as the Renminbi Qualified Foreign Institutional Investor (RQFII) and Qualified Domestic Individual Investor (QDII) programmes. These combined initiatives should further drive the two-way flow of Renminbi funds and encourage greater market participation. That said, there is still some work to be done, so 2020 may be a more realistic timeframe for the currency’s maturation to full convertibility. Indeed, this date would correlate with China’s plans to develop Shanghai into an international finance centre.

4http://www.wantchinatimes.com/news-subclass-cnt.aspx?id=20140417000095&cid=1203 5http://www.shanghaidaily.com/article/article_xinhua.aspx?id=206527 6http://www.icbc.com.cn/icbc/%E6%B5%B7%E5%A4%96%E5%88%86%E8%A1%8C/%E5%B7%A5%E9%93%B6%E6%AC%A7%E6%B4%B2%E7%BD%91%E7%AB%99/en/aboutus/news/ICBCs%20Inauguration%20of%20RMB%20Clearing%20Bank%20Services%20in%20Singapore.htm

7Deutsche Bank Markets Research, CNH Market Monitor, 27th June 2014, page 48Deutsche Bank Markets Research, CNH Market Monitor, 27th June 2014, page 1

In April 2014, Renminbi deposits soared to RMB268 billion, from RMB17.4 billion in August 2012

Deutsche BankThe Renminbi: 2014 and beyond

15

In the short-term, however, the impact of reforms will most likely remain incremental in scope and significance. In practical terms, this means the variances between the onshore and offshore markets are likely to remain for some time to come. But once understood, these differences need not pose too great a challenge.

In fact, when considered alongside the opening-up of channels for cross-border Renminbi flows, which will facilitate corporate access to both markets, onshore/offshore differences could potentially present opportunities with respect to pricing and hedging that could work in a corporate’s favour. Certainly, the existence of two Renminbi capital markets means there are respective pricing gaps for FX, interest rates and derivatives.

That said, the difference between the two markets creates basis risk on spots, forwards and interest rates, as well as cash bond financing. Although 2013 exhibited greater basis stability than was observed in 2010-2012, this risk will remain until the liberalisation of the capital account leads the onshore and offshore Renminbi to converge. In the meantime, managing the differences between the onshore and offshore Renminbi depends on a detailed understanding of the FX markets and the factors that drive them.

In fact, the FX market for Renminbi consists of three tiers: onshore CNY, offshore CNH and non-deliverable forwards (NDF). An NDF is an outright forward contract, through which counterparties settle the differences between the contracted NDF price/rate and the prevailing spot price/rate on an agreed notional amount. As the underlying currency is the same, these three markets trade with strong correlation but track different spot levels, including the London Interbank Offered Rate (LIBOR), the Hong Kong Interbank Offered Rate (HIBOR) and the Shanghai Interbank Offered Rate (SHIBOR), which are in turn affected by different funding activities. If companies fail to fully appreciate the various factors that can drive basis risk, they will not only potentially miss market opportunities but could also suffer as a result of incorrect hedging.

The three-tier FX market

Onshore CNY

Offshore CNH

Non-deliverable forwards (NDF)

Deutsche BankThe Renminbi: 2014 and beyond

16

Investment potential

Market participants should also look out for interest rate deregulation and the further development of the bond market. At present, interest rates in China are regulated, which means there is a ceiling for deposits. While this creates a gap in which banks can make their margins, the spread will disappear as markets deregulate and have the scope to move more freely.

The market has already seen some progress with respect to interest rate deregulation. In July 2013, China eliminated the lower limit on lending rates, thereby removing a floor set at 30% below the 6% benchmark; an important step towards the liberalisation of deposit rates. If the deposit ceiling were to be raised, it would boost financial institutions’ pricing capabilities and reduce funding costs for corporates. Steps in this direction are already being taken, with June 2014 seeing the removal of the foreign-currency deposit rate ceiling for small accounts within the China (Shanghai) Pilot Free Trade Zone, in an early-stage experiment that has since been extended to the entirety of Shanghai9. While there is no official guidance from China on the timing of a broader abolition of the deposit rate ceiling and benchmark rates, market expectation is that it will take place within the next two or three years.

Eventually, deposit rates are likely to be abolished entirely, with the establishment of a prime rate as a market rate for lending. Looking at the evolution of other markets such as Hong Kong and Singapore, the introduction of prime rates marked a turning point in their development as financial centres. For China, the establishment of a prime rate for lending would allow banks to more accurately price risk, which would in turn provide flexibility, attract capital and drive competition.

For corporates looking to raise funds in Renminbi, the dim sum bond market is also important, and has come a long way since its inception. Initially it was mainly perceived as a tool for investors looking to capture Renminbi appreciation, but it is now priced according to risk rather than FX. Funds are more expensive than they used to be, but this has not dampened the market’s relevance. Indeed, in January of this year, Bank of China sold a record RMB2.5 billion bond to investors (the biggest offshore Renminbi bond to date in London), providing evidence that foreign investor appetite for Renminbi funds continues to grow.

9http://www.bloomberg.com/news/2014-06-26/china-removes-cap-on-fx-deposit-rates-in-shanghai.html

China eliminated the lower limit on lending rates, removing a floor set at 30%

Deutsche BankThe Renminbi: 2014 and beyond

17

In fact, 2014 may see the dim sum market matched by the panda bond market (the market for domestic bonds for foreign entities), which will be a major milestone in the evolution of China’s capital market. Substantial growth in the panda bond market (as predicted in the next 12 months) would create a fully-functioning onshore debt capital market that would include international issuers, and would encourage some of the world’s major corporations to tap the market. Daimler, the German automotive company, has led the charge in this respect, selling an RMB500 million10 panda bond in March 2014. Other MNCs may follow as their China-focused strategies demand more Renminbi-denominated capital, increasing the importance of building a local investor community.

For domestic banks and institutional investors, the development of the panda bond market could help them with portfolio diversification; a goal currently hampered by capital account quotas. Panda bonds could allow them to diversify by enabling them to gain exposure to international borrowers via the onshore market, although quality names will be important for the market from a credit risk perspective.

Further developments can be seen in the use of the Renminbi for Foreign Direct Investment (FDI). Prior to 2011, capital inflows were hindered by procedural difficulties, such as the need to obtain approvals from China’s Ministry of Commerce and the PBOC. But new rules announced in October 2011 introduced greater levels of clarity and certainty, opening the door for the use of Renminbi for capital infusion into China. China’s Ministry of Commerce further simplified the rules in December 2013, removing the need for additional ministry approvals for Renminbi-denominated FDI deals.

Of course, other limitations remain in place. For example, foreign entities cannot currently use Renminbi funds to trade domestic securities or financial derivatives, or make entrusted loans. However the December 2013 relaxation will undoubtedly make it easier for foreign firms to use offshore-raised Renminbi to invest in mainland China, a common use of dim sum bond proceeds.

Alongside greater liquidity, other key indicators of progress to look out for include higher volumes of third-party transactions (i.e. Renminbi-denominated transactions not involving a Chinese party) and greater circulation between the onshore and offshore pools. While these factors are a work in progress, there can be no doubting the overarching trend. Indeed, Renminbi trading more than tripled between 2010 and 2013, to reach $120 billion a day. This momentum will only increase as China takes steps to liberalise the capital account and to encourage the flow of two-way Renminbi traffic.

10http://www.ft.com/cms/s/0/9261b22c-ab65-11e3-8cae-00144feab7de.html#axzz35pgdIROp

Deutsche BankThe Renminbi: 2014 and beyond

18

Breaking down the barriers

In this respect, there are clear signs of progress, with Shanghai providing a case in point. China plans to develop Shanghai into an international finance centre by 2020, and the journey has already begun with the establishment of the China (Shanghai) Pilot Free Trade Zone (FTZ). This is the first of its kind in China, and is likely to be followed by further FTZs in Tianjin, Chongqing, Xiamen, Zhoushan and Zhuhai11.

The Shanghai FTZ brings a number of benefits for corporates and non-bank financial institutions alike, enabling them to more freely move cash on and offshore. Recent developments within the FTZ extend the ways in which the Renminbi can be used as a treasury management currency. For example, foreign firms registered in the zone can now make use of Renminbi-denominated cross-border borrowing and settlement (for investment items in the FTZ) and “payments- and collections-on-behalf-of” (POBO/COBO) structures. Furthermore, the administration has given the green light to two-way cross-border sweeping in the zone, making it easier to conduct treasury tasks such as channelling liquidity into mainland operations, or sweeping funds out of China to a regional treasury centre, for example.

The Shanghai FTZ will continue to serve as a testing ground for new economic reforms as well as for many of the Renminbi’s next steps, from further interest rate deregulation and capital account convertibility to free Renminbi convertibility. Indeed, such FTZs are likely to give rise to new pools of offshore Renminbi liquidity and new Renminbi instruments. This will undoubtedly affect both the onshore and offshore markets, though it is impossible to predict precisely how at present.

11Deutsche Bank Markets Research, Tracking China’s Reforms, 13th June 2014, page 5

Deutsche BankThe Renminbi: 2014 and beyond

19

Making the right move

The currency’s potential (and the corresponding scope for commercial opportunity) is clear. China is the world’s largest goods trader, and history dictates that the currencies of major players in global trade become vital to the health of the global economy. Furthermore, ongoing changes brought about by China’s economic policy, which has actively driven the Renminbi’s liberalisation from the outset, will cement the currency’s position on the international stage.

With respect to trade finance and trade settlement, the Renminbi for all intents and purposes has already staked its claim as a global currency. The continued deconstruction of onshore/offshore barriers (via the Shanghai FTZ) heightens the Renmimbi’s use and importance as a treasury management currency. And ongoing financial reform and capital markets expansion (to cater to the needs of both domestic and foreign borrowers and investors) mean the Renminbi’s progress as an investment currency is picking up pace.

With regard to switching to the Renminbi, the question then is not “if” or even “when”, but from a corporate’s perspective, “how”. In this respect education is key, not only to keep up-to-date and fully understand the significance of developments but also to subsequently convert these changes into commercial opportunities.

Of course, commercial expansion into new markets, new product lines or new currencies always carries an element of risk, but the complexity and relative lack of clarity surrounding the Renminbi’s future means the risks may be perceived to be higher. This means corporates must not lose sight of the importance of migration management, and access to banks’ intellectual support (in the form of consultation and guidance) may prove just as important as operational support. In fact, at least during the early stages of the Renminbi adoption process, intellectual support may be the most critical element.

The Renminbi has already staked its claim as a global currency

Deutsche BankThe Renminbi: 2014 and beyond

20

Ultimately, corporates looking to capitalise on the advantages of the Renminbi must be aware that there can be no “one-size-fits-all” solution. The most appropriate path to Renminbi adoption will depend on corporates’ individual commercial strategies and optimal timelines for implementation. With this in mind, there can be no substitute for banks’ analysis of client requirements on an individual basis, and the subsequent design and implementation of bespoke structures. Indeed, it is only through looking at the Renminbi’s development from the perspective of trade entities worldwide, as well as that of regulating bodies, that banks can not only help corporations convert the Renminbi’s challenge into an opportunity, but also ensure they are best-placed to seize this opportunity and realise its full potential.

DISCLAIMERThe information contained in this brochure is designed to serve as a general overview of the services and does not purport to contain all the information you may require. Deutsche Bank AG is not acting or purporting to act in any way as your advisor. It is recommended that you seek your own independent advice in relation to any issues (whether legal, tax, accounting, regulatory or otherwise) relating to the merits or otherwise of the services discussed. The information and the general description of the services contained herein are in their nature only illustrative and do therefore not contain or cannot result in any contractual or non-contractual obligation of Deutsche Bank AG or any of its respective branches or affiliates. Deutsche Bank does not assume any liability or guarantee for other websites that may be accessed through hyperlinks. Deutsche Bank AG assumes no responsibility for the contents of websites that can be accessed through such links. Copyright ©September 2014 Deutsche Bank AG. All rights reserved.