the review of economic studies ltd. - postingsbutterscotchbeausake.com/pricediscrimination.pdf ·...

TRANSCRIPT

The Review of Economic Studies Ltd.

A Price Discrimination Analysis of Monetary PolicyAuthor(s): John Bryant and Neil WallaceSource: The Review of Economic Studies, Vol. 51, No. 2 (Apr., 1984), pp. 279-288Published by: The Review of Economic Studies Ltd.Stable URL: http://www.jstor.org/stable/2297692Accessed: 03/09/2009 14:21

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available athttp://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unlessyou have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and youmay use content in the JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained athttp://www.jstor.org/action/showPublisher?publisherCode=resl.

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printedpage of such transmission.

JSTOR is a not-for-profit organization founded in 1995 to build trusted digital archives for scholarship. We work with thescholarly community to preserve their work and the materials they rely upon, and to build a common research platform thatpromotes the discovery and use of these resources. For more information about JSTOR, please contact [email protected].

The Review of Economic Studies Ltd. is collaborating with JSTOR to digitize, preserve and extend access toThe Review of Economic Studies.

http://www.jstor.org

Review of Economic Studies (1984), LI, 279-288 0034-6527/84/00190279$00.50

? 1984 The Society for Economic Analysis Limited

A Price Discrimination Analysis of

Monetary Policy JOHN BRYANT

Rice University

and

NEIL WALLACE University of Minnesota

Monetary policy is analysed within a model that appeals to legal restrictions on private intermediation to explain the coexistence of currency and interest-bearing default-free bonds. The interaction between such legal restrictions and monetary policy is illustrated in a version of the overlapping generations model. The model shows that legal restrictions and the use of both currency and bonds permit the government to levy a nonlinear inflation tax and that such a tax may be better in terms of the Pareto criterion than a linear inflation tax.

This paper applies price discrimination analysis to the study of monetary policy in a setting in which revenue is raised using an inflation tax. Our approach is to treat the two liabilities of the government that we consider, currency and nominally default-free bonds, as perfect substitutes except insofar as legal restrictions on private intermediation create separate markets for them.1 More generally, our view is that legal restrictions on private intermediation turn otherwise innocuous differences among government liabilities-for example, denominational differences-into differences which the government exploits. The government uses differences among its liabilities and the quantities (or prices) of the different liabilities in much the same way as a sole supplier of electricity uses a nonlinear price schedule.

In a sense, our analysis is a naive public finance analysis. We take as given a time path of the real government deficit (net of interest payments) and consider the effects of various ways of financing that deficit. Our contribution is to show that there are circum- stances under which the imposition of legal restrictions on private intermediation and the issuance of large-denomination bonds permit the levying of a nonlinear inflation tax which can improve upon the linear inflation tax implied by currency issue only.

In the model we study, legal restrictions make the government the sole supplier of saving opportunities. The use of currency and large-denomination bonds allows the government to face savers with a nonlinear rate-of-return schedule on saving. In par- ticular, the use of such bonds permits the government to face savers with all-or-nothing choices. These choices can give rise to corner solutions in which intertemporal marginal rates of substitution exceed the (negative) real returns on the government's liabilities. This divergence of marginal rates of substitution from real returns is what permits outcomes better than those implied by a linear inflation tax.

Our main purpose in this paper is to suggest the potential fruitfulness of price discrimination analysis in the study of monetary policy. We want readers to consider the possibility that this type of analysis is a productive way to study the often observed concurrence of legal restrictions on private intermediation and the tailoring of debt issues to the needs of the market. With that purpose, we present the possibilities for price

279

280 REVIEW OF ECONOMIC STUDIES

discrimination in an extremely simple setting. In particular, in the simple setting presented, there is no diversity among people. The hope is that this simple setting isolates the essential price discrimination possibilities in monetary policy.

1. THE MODEL

We illustrate the potential for price discrimination using a simple overlapping generations model. We describe equilibrium conditions for our model under costlessly enforced portfolio restrictions that rule out private borrowing. Although this is an extreme form of legal restriction, in our setting it is equivalent to giving the government a monopoly on the creation of small-denomination assets.2

1.1. Endowments, preferences, and technology

The model is of a stationary, pure exchange, discrete-time economy. We let t, an integer, denote the date and let t = 1 be the current or initial date. At each date t, a new generation of N identical persons, generation t, appears, and it is present in the economy at t and t +1. Generations are identical, and there is a single consumption good at each date t.

Each member of generation t is endowed with some of the time t good, wi > 0, and with some of the time t + 1 good, w2> 0. As for preferences, each member of generation 0 (those who at t = 1 are in the second and last period of their lives) maximizes consumption of the time 1 good, while each member of generation t, t> 0, has preferences that are represented by a twice differentiable, increasing, and strictly concave utility function, u[c,(t), ct(t+ 1)], where ct(t+ i) is consumption of the time t+ i good by a member of generation t.3

1.2. Government

We assume that the government attempts to consume G ? 0 units of the time t good at all dates to 1 and that its only method of financing this expenditure is by running a deficit. It can issue fiat currency, and it can issue one-period default-free discount bonds. Each bond issued at t is a title to a known amount of currency at t +1. Thus, the cash flow constraint of the government is

G = p(t)[M(t) -AM(t- 1)]+ p(t)Pb(t)B(t) -p(t)B(t- 1) (1)

where p(t) is the time t price of a unit of currency in terms of the time t good (the inverse of the price level), M(t- 1) is the stock of currency held by the public from t -1 to t, B(t- 1) is the total face value in units of time t currency of the government bonds issued at t -1, and Pb(t) is the price at t in terms of currency of an amount of bonds that pays one unit of currency at t +1. [1/Pb(t) is unity plus the nominal interest rate on bonds issued at t.]4

Note that M(0) and B(0) are initial conditions at t = 1. We assume that M(O) + B(O) is the initial nominal wealth of the members of generation 0, the old at t = 1. We also assume that the government specifies a minimum real purchase price of F per bond. It is this minimum size restriction that distinguishes bonds from currency.

1.3. The choice problem and equilibrium conditions

Being subject to a legal prohibition against borrowing, each member h of generation t,

BRYANT & WALLACE MONETARY POLICY 281

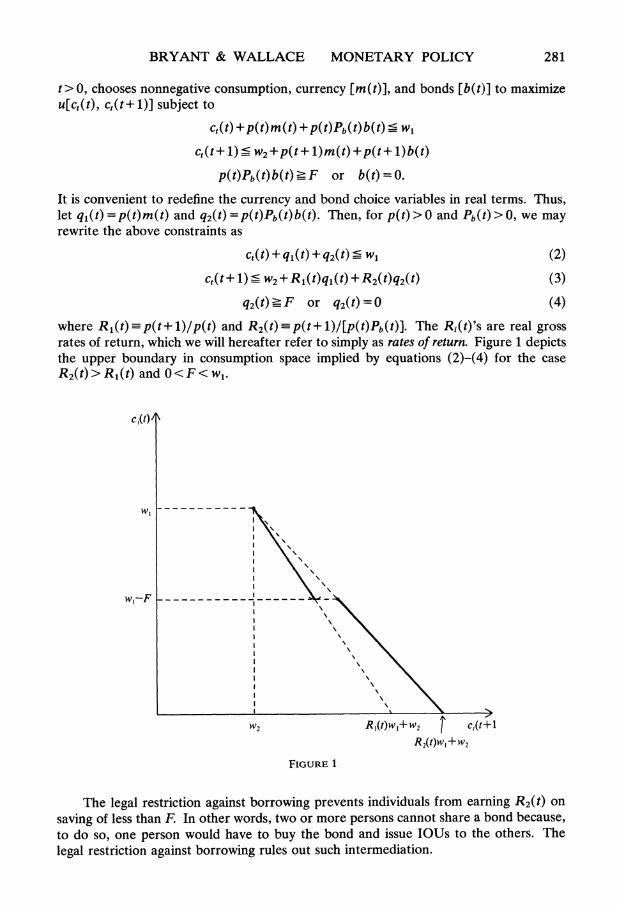

t> 0, chooses nonnegative consumption, currency [m(t)], and bonds [b(t)] to maximize u[ct(t), c,(t+ 1)] subject to

Ct(t) + p(t) m(t) + p(t)Pb(t) b(t) '5 w,

ct(t + 1) cw2+ p(t ) m (t) + p(t + l) b(t)

p(t)Pb(t)b(t) > F or b(t) = O.

It is convenient to redefine the currency and bond choice variables in real terms. Thus, let q1(t) = p(t)m(t) and q2(t)= p(t)Pb(t)b(t). Then, for p(t)>0 and Pb(t)>O, we may rewrite the above constraints as

ct(t) + q1(t) + q2(t) c wI (2)

ct (t+ 1) cW2 +R1(t)q1(t) +R2(t)q2(t) (3)

q2(t) '-F or q2(t) = 0 (4)

where R1(t)-p(t+1)/p(t) and R2(t)=p(t+1)/[p(t)Pb(t)]. The Ri(t)'s are real gross rates of return, which we will hereafter refer to simply as rates of return. Figure 1 depicts the upper boundary in consumption space implied by equations (2)-(4) for the case R2(t)>R1(t) and 0<F< w.

c(t)l

WI \.

w -F ___ __-_- __------ _

W2 R l(t)WI+ W2 C,(t+ I

R2(t)w, + W2

FIGURE 1

The legal restriction against borrowing prevents individuals from earning R2(t) on saving of less than F. In other words, two or more persons cannot share a bond because, to do so, one person would have to buy the bond and issue IOUs to the others. The legal restriction against borrowing rules out such intermediation.

282 REVIEW OF ECONOMIC STUDIES

The solution to the above maximization problem consists in part of demand correspon- dences q,(t) = di[R1(t), R2(t), F] for i = 1, 2. We define an equilibrium im terms of aggregate correspondences, DJ[RI(t), R2(t), F] Ndi[R1(t), R2(t), F] for i = 1, 2.

Given G, F, and M(O) + B(O)> 0, a monetary equilibrium consists of positive {p(t)} and {Pb(t)} and nonnegative {M(t)} and {B(t)} such that, for all t-' 1,

DI[RI(t), R2(t), F]= p(t)M(t) (5)

D2[R1(t), R2(t), F] = p(t)Pb(t)B(t) (6)

and such that equation (1) holds, it being understood that the Ri(t) are defined, as above, in terms of currency and bond prices.

2. STATIONARY EQUILIBRIA

We find it convenient to describe-stationary equilibria in the following way. If Ri denotes a constant value of Ri(t), it follows from (1) for t ?-2 and (5) and (6) that an equilibrium (R1, R2) must satisfy G = (1 -R1)Di(R1, R2, F) +(1 -R2)D2(R1, R2, F), where (1 -R1) should be interpreted as the tax rate on currency holdings and (1 - R2) as the tax rate on bond holdings. Moreover, to be a monetary equilibrium, the equilibrium (Rl, R2) must also satisfy R2 _ R, > 0 and DA(R1, R2, F) > 0 for at least one value of i. In order to have a symbol to represent the set of (Rl, R2)'s that satisfies these conditions and its dependence on G and F, we let

S(G, F) = {(R1, R2): (1 - R1)D1(R1, R2, F) +(1 -R2)D2(R1, R2, F) = G,

R2 ' RI > 0, and DL(R1, R2, F) > 0 for at least one value of i}. (7)

To go from a given G and F and a pair, (RI, R2), in S(G, F) to equilibrium price sequences for currency and bonds, we need an associated initial price of currency, p(l). Using equations (5) and (6) for t = 1 and an initial condition for M(0) + B(0), we find an associated p(l) from equation (1) for t = 1; namely,

G = D1(R1, R2, F) + D2(R1, R2, F) -p(l)[M(0) + B(0)]. (8)

Thus, given G, F, and M(0) +B(0), a monetary equilibrium is any (R1, R2) in S(G, F), an associated solution for p(l) from (8), and the associated paths of nominal supplies of currency and bonds given by (5) and (6), respectively. Thus, we can first study the set S(G, F) and then find the nominal asset supplies that support various elements of S(G, F) as stationary monetary equilibria. Notice that, since 1/Pb(t), the gross nominal yield on bonds, is R2(t)/R1(t), it follows from (5) and (6) that the currency and bond sequences imply a constant ratio of currency to bonds.5

Before we turn to a proposition about the set S(G, F), we present a proposition that relates initial price levels, p(l)'s, to features of the S(G, F) set. We are interested in p(l) because it determines the effects of alternative policies on the current old; p(1) determines the value of the given initial nominal wealth of the current old, M(0) + B(0). The following proposition says that, if an interest-bearing bond solution has as low an inflation rate as a noninterest-bearing bond (or money-only) solution, then it has a lower initial price level.

Proposition 1. Forgiven GandM(O) +B(O)>O, if(R*, R*) E S(G, F*), (Ri, R') E

S(G, F'), D2(R1, R2, F')> 0, and Rf > R1-? R*, then p'(1) > p*(1), where p'(1) is the p(l) solution to (8) for (R, R', F') and p*(1) is that for (R *, R*, F*).

BRYANT & WALLACE MONETARY POLICY 283

Proof. In view of (8), we need only show that D* + D* <D' + D', where D- Di(R*, R*, F*) and D' Di(R', R, F'). Since (R*, R*)ES(G, F*) and (R', R') e S(G,F'), we have (1-R*)(D* +D*) =(1-R )D1 +(1-RI)DI <(1-R )(D1 +D'), where the inequality follows from R' > R'. But then R_ h R* implies D* + D*< D1+D2. I1

Note that the prime (') solution is a solution in which bonds bear interest, while the star (*) solution is one in which bonds, if they exist, sell at par.

We begin our discussion of the set S(G, F) by recalling that all individuals in equilibrium face a budget set like that shown in Figure 1. Since all individuals are alike, if currency and interest-bearing bonds are held, some people (money holders) end up situated at a point like A in Figure 2, while the rest (bondholders) end up situated at a point like B. Before stating conditions under which such equilibria exist, some additional notation is needed.

C,(t)\

indifference curve

14'j

C,(t+1)

FIGURE 2

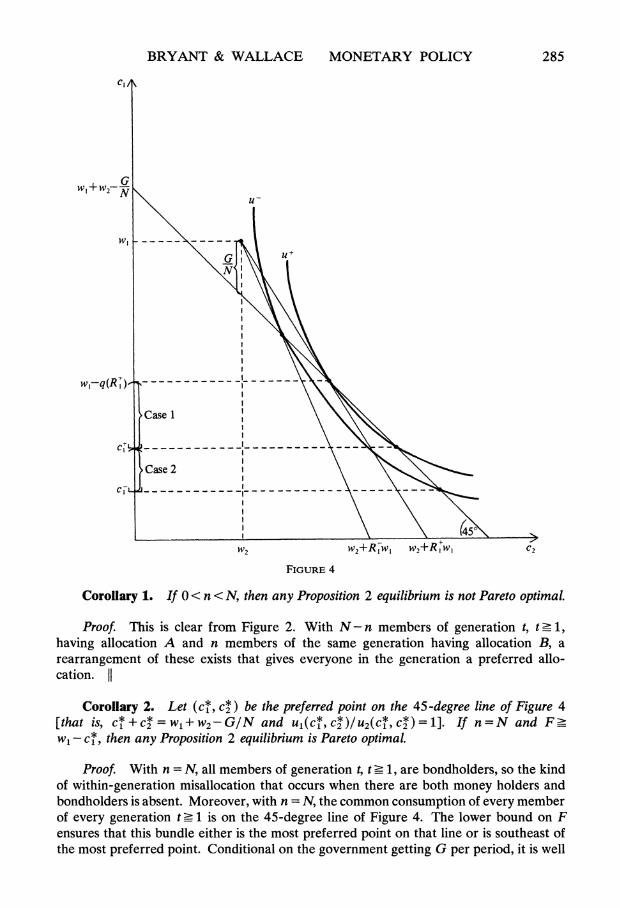

Let q(R)-= d(R, R, 0) + d2(R, R, 0) [where di(R1, R2, F) is the demand correspon- dence defined above], let S(G, 0) ={R: N(l -R)q(R) = G}, and let R- =min S(G, 0) and RI -max S(G, 0). Moreover, let (cj, Cl) be the unique solution to the following three conditions: cj + c2 = w1 + w2- GIN, u(cl, c2) = u[w1-q(R7), w2+R7q(R )], and cl w1-q(Rj). And, finally, let (ct, c') be the unique solution to these con- ditions: c1 + c2 = w1 + w2- GIN, u(c7, cj) = u[w1 -q(R8), w2+Rq(Rfl)], and c+ < w1-q(Rl ).

Note that q(R) is per capita saving when all assets bear the rate of return R. Equivalently, it is per capita desired real currency holding when currency bears the rate of return R and there are no other- assets. In Figure 3, we depict the function (1 -R)q(R), which is the real per capita revenue obtained by the government when R is the return

284 REVIEW OF ECONOMIC STUDIES

X~~~~~( 1-R)q(R)

R RI RI 1.0

FIGURE 3

on currency and holding currency is the only option. For any G, S(G, 0) is the set of values of R that satisfies N(l -R)q(R) = G. Elements ot the set S(G, 0) can be inter- preted as alternative currency-only equilibria or as currency and bond equilibria when the minimum size restriction on bonds is not binding. Of course, if S(G, 0) is not empty, then there are in general at least two elements in it.

Figure 4 depicts the allocations corresponding to the minimal and maximal elements of S(G, 0) and the corresponding indifference curves, labeled u- and u+, respectively. The 45-degree line represents consumption bundles that, if common to everyone in every generation t, t ' 1, are consistent with the government consuming G in every period. Moreover, for consumption profiles that are identical across all generations t, t ' 1, and are consistent with the government consuming G, if bondholders end up outside the 45-degree line, then money holders end up inside it, and vice versa. Finally, Cases 1 and 2 in Figure 4 are relevant under different magnitudes for F.

We can now state our main proposition.

Proposition 2. If S( G, O) is not empty and F E (q(R ), w1 - c), then for any number of bonds n E {1, 2,... , N} there exists a stationary equilibrium with positive nominal interest on bonds and N-n money holders and n bondholders. Moreover, if Fe (q(R w, w1- cfl (Case 1), then R2 < 1 and every member of generation t, t '-1, is on an indifference curve at least as high as u+; if FE (w1 - c', w1-c7 ) (Case 2), then every member of generation t, t 1, is on an indifference curve lower than u+.

A proof of Proposition 2 is given in the Appendix.6 We now discuss some conse- quences of Proposition 2 and of well-known optimality results for overlapping generations models.

BRYANT & WALLACE MONETARY POLICY 285

C'A

WI+WI - u-

WI-

N'

Case I

Case 2

w2+Rw,w w2+Rw,C

FIGURE 4

Corollary 1. If 0< n <N, then any Proposition 2 equilibrium is not Pareto optimal.

Proof. This is clear from Figure 2. With N - n members of generation t, t: 1, having allocation A and n members of the same generation having allocation B, a rearrangement of these exists that gives everyone in the generation a preferred allo- cation. 11

Corollary 2. Let (c0 c*) be the preferred point on the 45-degree line of Figure 4 [that is, c*+c*=w1+w2-G/N and u1(c*,c*)/u2(c1,c*)=1]. If n=N and F?- WI - c*, then any Proposition 2 equilibrium is Pareto optimal

Proof. With n = N, all members of generation t, t ' 1, are bondholders, so the kind of within-generation misallocation that occurs when there are both money holders and bondholders is absent. Moreover, with n = N, the common consumption of every member of every generation t ?1 is on the 45-degree line of Figure 4. The lower bound on F ensures that this bundle either is the most preferred point on that line or is southeast of the most preferred point. Conditional on the government getting G per period, it is well

286 REVIEW OF ECONOMIC STUDIES

known that all such allocations are Pareto optimal. [If the bundle is southeast of the most preferred bundle, then it is easily shown that no allocation improves the well-being of any member of generation t for any t ? 1 without hurting the current old. See, for example, the proof of Proposition 5 in the Appendix in Wallace (1980).] 11

Corollary 3. If G> 0, then Case 1 is not empty and any Proposition 2 Case 1 equilibrium is Pareto superior to any currency-only stationary equilibrium.

Proof. Under the hypotheses of Proposition 2, nonemptiness of Case 1 is obvious if G>0. Under the current setup, Pareto superiority of any Proposition 2 Case 1 equilibrium follows if we can establish that any such equilibrium satisfies the hypotheses of Proposition 1.

The currency-only stationary equilibrium that puts all members of generation t, t : 1, on the u+ indifference curve is Pareto superior to any other currency-only stationary equilibrium (see Figure 4). But Proposition 2 says that a Case 1 equilibrium exists which puts all the members of generation t, t ? 1, on an indifference curve at least that high and which has rates of return on money and bonds, (R1, R2), that satisfy R2> R1 ' R . These satisfy the conditions of Proposition 1 and imply, therefore, that the initial price level is lower in the Case 1 equilibrium than in the best currency-only equilibrium. Note, by the way, that R2 < 1 in any Case 1 equilibrium; although bonds bear a positive nominal interest rate, they bear a negative real interest rate in any Case 1 equilibrium. 11

Corollary 3 describes how the prohibition on private borrowing and the use of bonds helps in an unambiguous way. The general idea is familiar from public finance or second- best theory. With G > 0, it is well known that laissez-faire gives rise to a nonoptimal equilibrium. [See, for example, Proposition 7 of Wallace (1980).] It gives rise to an equilibrium with a linear, distorting excise tax on second-period consumption. Our legal restriction allows for the imposition of nonlinear taxes through the use of bonds. It is no surprise, then, that better allocations are possible under this broader set of possible tax schemes. In particular, the all-or-nothing choice presented by bonds allows for corner solutions in which the marginal rate of substitution, u1/ u2, exceeds the rate of return on bonds.

As this discussion suggests, it should not be possible to produce Pareto superior allocations with bonds if G = 0. This is so. With G = 0, it is evident that Case 1 is empty; u+ is tangent to the 45-degree line of Figure 4. Thus, if G = 0, only Case 2 exists, and the members of generation t, t ' 1, are worse off in any Case 2 equilibrium than under the best currency-only equilibrium.

Finally, we should note that the prohibition on borrowing and the use of bonds can make possible the financing of larger deficits than would be possible using currency issue only. In particular, letting (c*, c*) satisfy UI(C*l, C*)/U2(C*, C*) = 1 and u(c*, c*)= u(w1, w2) and letting G*=N(wi +w2-c*-c2*), we can easily show that, if c*> w2, then any G ? G* can be financed using bonds only and that G* exceeds the maximum of (1- R)q(R) -that is, S(G*, 0) is empty-so that G* cannot be financed using currency issue only.

3. CONCLUDING REMARKS

If we take for granted that lump-sum taxes are not feasible, then the model presented above shows that legal restrictions that inhibit arbitrage between different government liabilities can in some circumstances make sense. Of course, such infeasibility of lump-sum

BRYANT & WALLACE MONETARY POLICY 287

taxes would be more credible in a model with diversity and private information about, for example, individual endowments. Such settings, in turn, give rise to more possibilities for price discrimination.

Consider, for example, a version in which people differ only in endowments and in which the government is assumed to know the distribution of endowments. If the prohibition on private borrowing is maintained so that the government is the sole supplier of net saving to each person, then the model is in all relevant respects formally identical to ones studied in the price discrimination literature. [See, for example, Guesnerie and Seade (1982)]. In such settings, it would not be appropriate to limit the government a priori to two liabilities. The results of the price discrimination literature suggest that it would be desirable to have as many types of bonds as there are types of people.

Although the results of the price discrimination literature can be applied directly in such settings, the extreme nature of the assumption that the government is the sole supplier of each individual's saving ought to be emphasized. In any price discrimination analysis, there are potential profits to be earned by breaking down the market segmenta- tion. However, in the usual applications-say, to electricity pricing or income taxes-there seem to be natural barriers to breaking down the market segmentation. In the case of rate-of-return discrimination, the only major barriers would seem to be legal restrictions on private intermediation.

APPENDIX

Proof of Proposition 2

Let um(R)= u[w1-q(R), w2+Rq(R)] and let Ub(R)= u(w1-F, w2+RF), where u r is to be interpreted as money-holder utility and ub as bondholder utility. For each R1 E

[Rl, 1] there exists a unique R2= f(R1) such that um(R1) = ub(R2). The function f is continuous and strictly increasing.

Let R' satisfy (1 -R')F = GIN. [Note that R' is such that (w1-F, w2+R'F) is on the 45-degree line of Figure 4.] By the assumption that FE (q(R), w1 - c), we know that ub(R' > u-. We consider separately two cases which correspond to Cases 1 and 2 in Figure 4.

Case 1. ub(R)' u+. Since Ub(R) is increasing in R, Um(Rt) = Ubf(RI )] u+_ ub(R') implies f(R?)cR'. By definition, R'<1. Since (1-R )q(Rt)=(1-R')F= GIN, we then have (N-n)(1 -R )q(R8 ) + n[1-f(R )]F' (N-n)G/N+ n(1 -R')F= G> n[1 -f(1)]F Since (N-n)(1 -R)q(R)+ n[1 -f(R)] is continuous in R, we conclude by the intermediate value theorem that there exist R E [R 1) and R* = f(R*) such that (N-n)(1 -R*)q(R) + n[1 -f(R*)]F = G.

Case 2. ub(R')<u+. Here um(R)= u-< ub(R)< u+= um(RD) so that f(Rj)<Rl <f(R8). Since (1-Rf)q(R )=(1-R-)q(R-)=(1-R')F= GIN, we then have (N-n)(1 -R-)q(R- )+n[l-f(R-)]F> (N-n)G/N+n(l-R')F= G> (N-n)(1-R+ )q(R) )+n[1-f(R )]F Once again by the intermediate value theorem, we conclude that there exist R * E (R -, R i) and R* = f(R *) such that (N -n)(1-R* )q(R* ) +n[1- f(R* )]F=-G.

In both cases, we have shown that there exist an R and an R * such that um(R*)= ub(R*) and (N-n)(1-R *)q(R *) + n(1-R *)F = G. To complete the argument, we must show that F> q(RI), for otherwise money holders could simply replace their currency holdings by bond holdings and increase utility. We know R* f(R )> R because f(RI*) = RI* implies F = q(R) _ q (Rt), which has been ruled out by assumption,

288 REVIEW OF ECONOMIC STUDIES

and f(R )<R* violates the assumption that q(R) solves the maximization problem. Suppose F-' q(R*). Then (1-R* )q(R* ) ' G/N> (1-R*)F In words, money holders are on or inside the 45-degree line of Figure 4 and bondholders are on or outside it. This fact, um(R*) - ub(R *), and F _ q(R* ) imply F < q(R ), a violation of our assump- tion on F.

First version received November 1982, final version accepted July 1983 (Eds). This research was supported by the Federal Reserve Bank of Minneapolis. However, the views expressed

herein are those of the authors and not necessarily those of the Federal Reserve Bank of Minneapolis or the Federal Reserve System. An earlier and longer version appeared as a Bank Staff Report, Bryant and Wallace (1983).

NOTES 1. See Wallace (1983) for a defence of the proposition that legal restrictions are necessary for monetary

policy to be other than completely innocuous. 2. See Wallace (1981) and Sargent and Wallace (1982) for the analysis of other forms of legal restrictions. 3. If government consumption of the time t good, G, affects individual welfare, it is assumed to do so in

a separable way. That is, if V[c(t), c(t+ 1), G] is the utility function of a member of generation t, then V(*) = U{u[c(t), c(t+ 1)], v(G)}, where U is increasing in its first argument.

4. Note that equation (1) implies that explicit taxes are not levied and, in particular, are not levied to cover interest on debt. One interpretation of this is that the government has exhausted the possible use of explicit taxes and that G represents government consumption in excess of that financed by explicit taxes.

5. That stationary solutions for real variables are supported by constant ratios of currency to bonds is not surprising. Basically, it follows from a well-known neutrality result: neutrality holds for once-for-all proportional changes in both bonds and currency. [See, for example, Patinkin (1961).]

6. That proof, suggested by Martin Hellwig, is simpler than our original proof, and we are grateful.

REFERENCES BRYANT, J. and WALLACE, N. (1983), "A Price Discrimination Analysis of Monetary Policy" (Research

Department Staff Report 51, Federal Reserve Bank of Minneapolis). GUESNERIE, R. and SEADE, J. (1982), "Nonlinear Pricing in a Finite Economy", Journal of Public Economics,

17, 157-179. PATINKIN, D. (1961), "Financial Intermediaries and the Logical Structure of Monetary Theory: A Review

Article", American Economic Review, 51, 95-116. SARGENT, T. S and WALLACE, N. (1982). "The Real-Bills Doctrine Versus the Quantity Theory: A

Reconsideration", Journal of Political Economy, 90, 1212-1236. WALLACE, N. (1980), "The Overlapping-generations Model of Fiat Money", in J. Kaveken and N. Wallace

(eds.) Models of Monetary Economies (Federal Reserve Bank of Minneapolis) 49-82. WALLACE, N. (1981), "A Modigliani-Miller Theorem for Open-Market Operations", American Economic

Review, 71, 267-274. WALLACE, N. (1983), "A Legal Restrictions Theory of the Demand for 'Money' and the Role of Monetary

Policy", Federal Reserve Bank of Minneapolis Quarterly Review, 7, 1-7.