the role of accounting in business chapter 1. types of businesses service business merchandising...

TRANSCRIPT

The Role of Accounting in Business

Chapter 1Chapter 1

Types of Businesses

Service BusinessService Business Merchandising BusinessMerchandising BusinessManufacturing BusinessManufacturing Business

Differences in Forms of Business Organization

Form EaseLegal Liability Taxation

Limited Life

Capital Access

Proprietorship Simple No limit Nontaxable Yes Limited

Partnership Simple No limit Nontaxable Yes Average

Corporation Complex Limited Taxable No Extensive

Limited Liability Co. Moderate Limited Nontaxable Yes Average

By providing goods and services to customers so that they can make a profit. To maximize their profits, companies may use one of the following two strategies:

PremiumPremiumPricePrice

StrategyStrategy

LowLowCostCost

StrategyStrategy

How Do Businesses Make Money? How Do Businesses Make Money?

Common Business Activities

Investments by Owners Loans from Creditors

Cash (Capital) Retained earnings

Buy land, buildings,

equipment, patentsPurchase materials

Pay

employees

Pay other operating

expenses

Produce and market goods and services

Monetary resources (revenues) from sale

of goods and services

Pay dividendsPay back loans/

interestPay taxes

Continue business

activity (market goods,

buy materials, etc.)

contribute

results in

used to

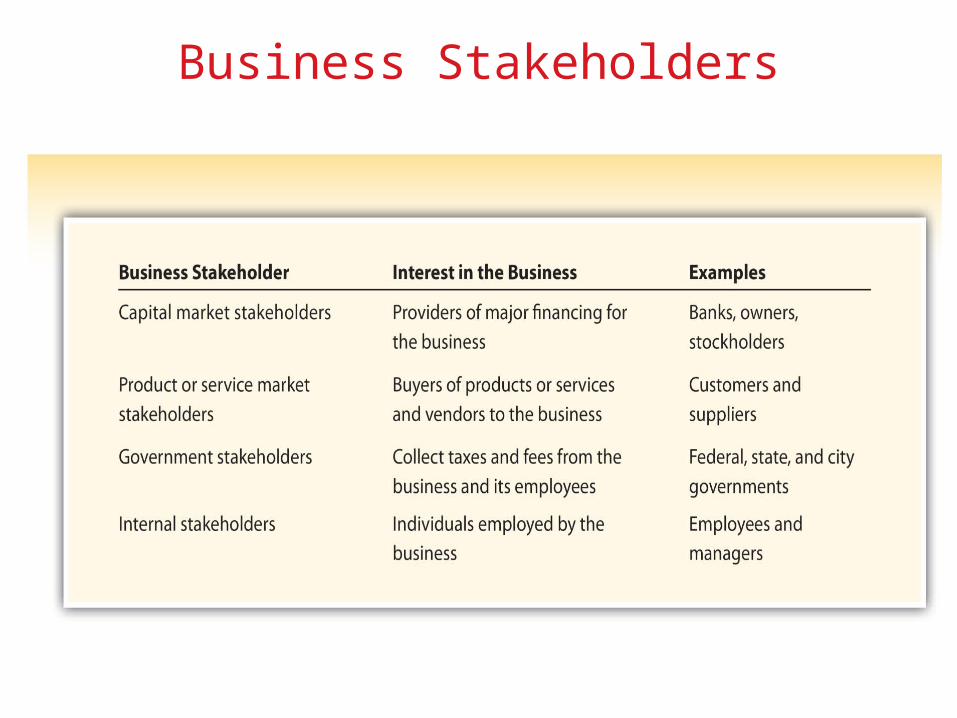

Business Stakeholders

The Role of Accounting in Business

• Financial Accounting measures and communicates results of business activities to external stakeholders)

• External stakeholders want to know:External stakeholders want to know: The financial condition of a business at a point The financial condition of a business at a point

in timein time

Changes in the financial condition of a business Changes in the financial condition of a business over a period of timeover a period of time

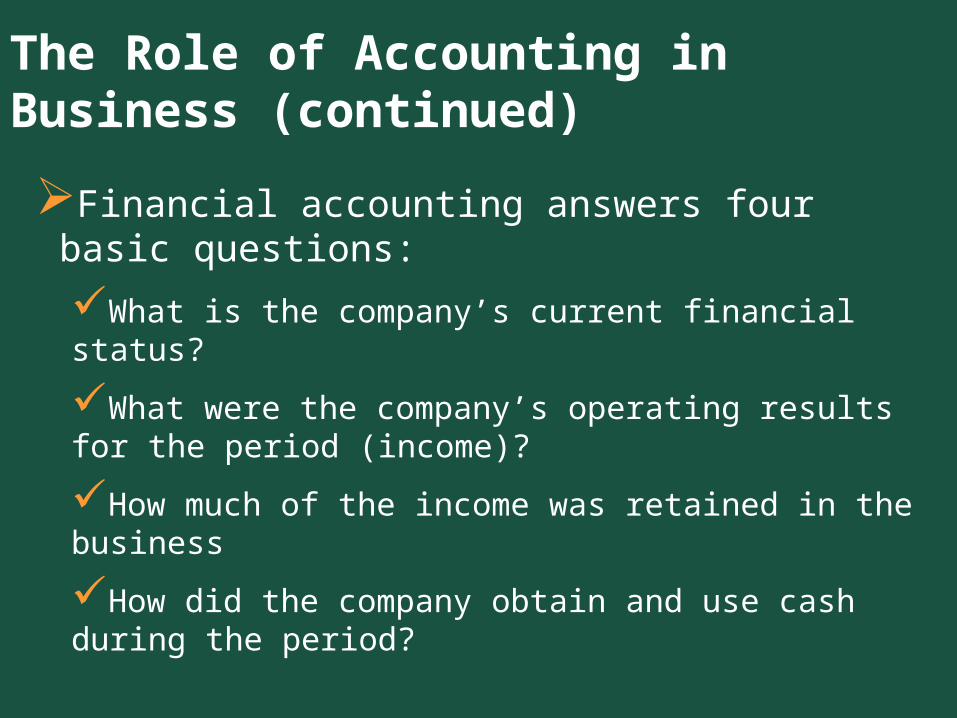

The Role of Accounting in Business (continued)

Financial accounting answers four basic questions:

What is the company’s current financial status?

What were the company’s operating results for the period (income)?

How much of the income was retained in the business

How did the company obtain and use cash during the period?

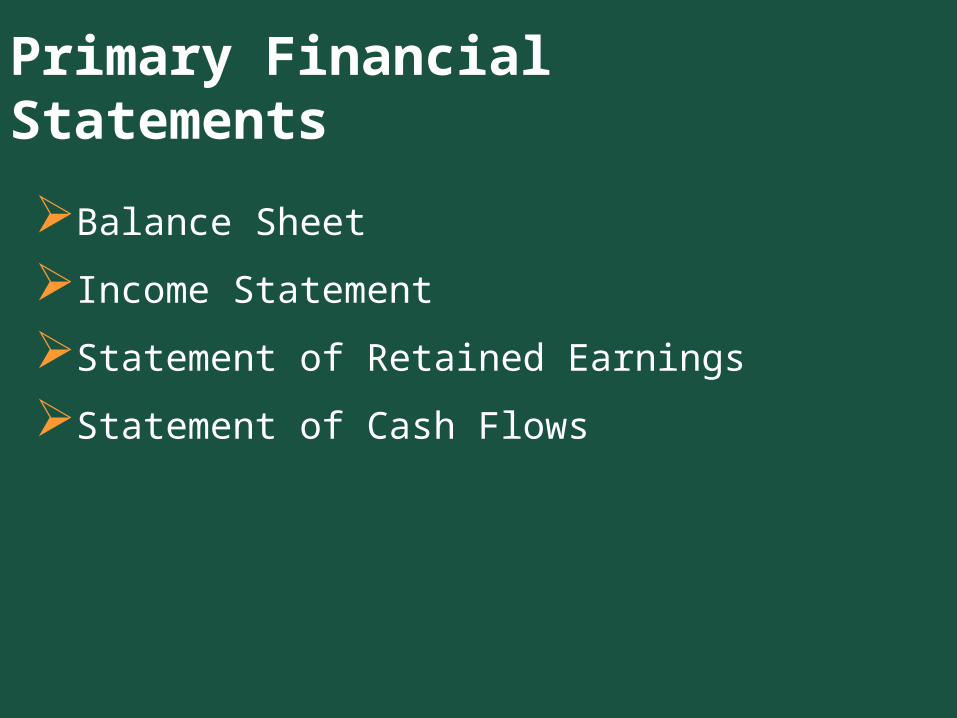

Primary Financial Statements

Balance Sheet

Income Statement

Statement of Retained Earnings

Statement of Cash Flows

Sometimes referred to as a

Statement of Financial Position

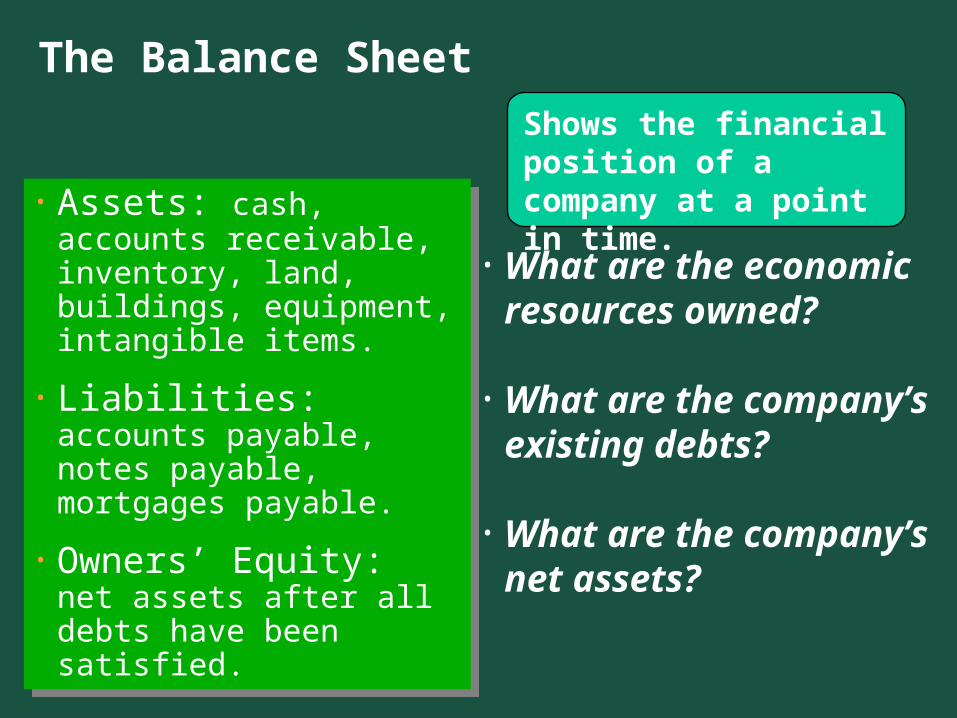

• What are the economic resources owned?

• What are the company’s existing debts?

• What are the company’s net assets?

Shows the financial position of a company at a point in time.

The Balance Sheet

• Assets: cash, accounts receivable, inventory, land, buildings, equipment, intangible items.

• Liabilities: accounts payable, notes payable, mortgages payable.

• Owners’ Equity: net assets after all debts have been satisfied.

• Assets: cash, accounts receivable, inventory, land, buildings, equipment, intangible items.

• Liabilities: accounts payable, notes payable, mortgages payable.

• Owners’ Equity: net assets after all debts have been satisfied.

Sometimes referred to

as a Statement of

Earnings

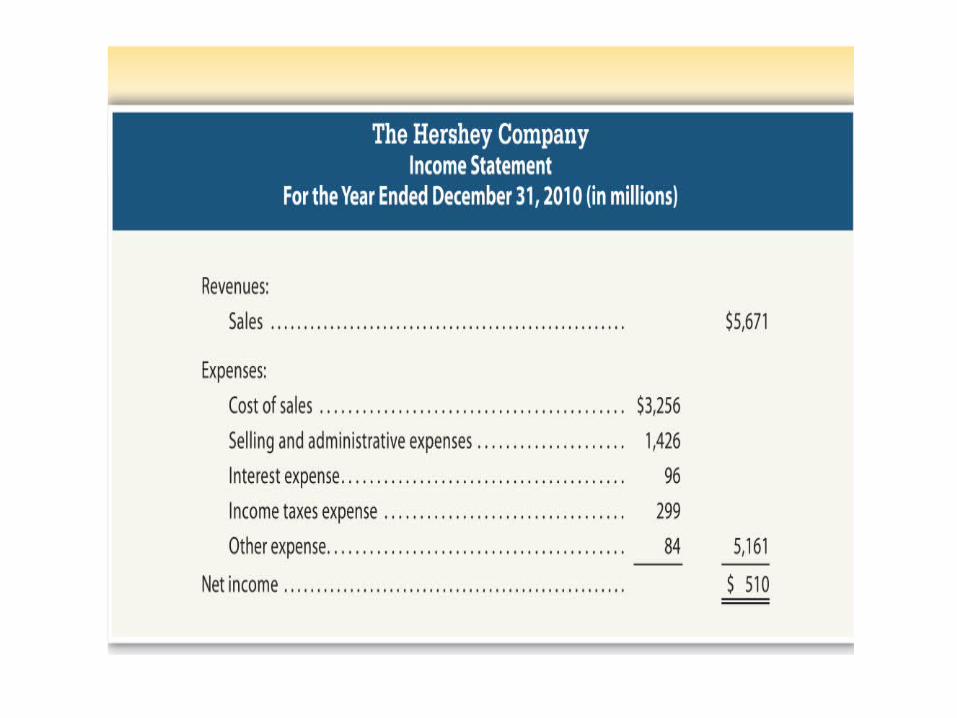

• What goods were sold or services performed that provided revenue?

• What costs were incurred to generate these revenues?

• What are the earnings or company profit?

Shows the results of a company’s operations over a period of time.

The Income Statement

RevenuesAssets (cash or AR) created through business operations

ExpensesAssets (cash or AP) consumed through business operations

Net Income or (Net Loss)

Revenues - Expenses

An additional financial statement that identifies changes in retained earnings from one accounting period to the next.

Statement of Retained Earnings

Beginning retained earnings

+ Net income

– Dividends paid

= Ending retained earnings

Beginning retained earnings

+ Net income

– Dividends paid

= Ending retained earnings

Net income results in:Increase in net assetsIncrease in retained earningsIncrease in owners’ equity

Dividends result in:Decrease in net assetsDecrease in retained earningsDecrease in owners’ equity

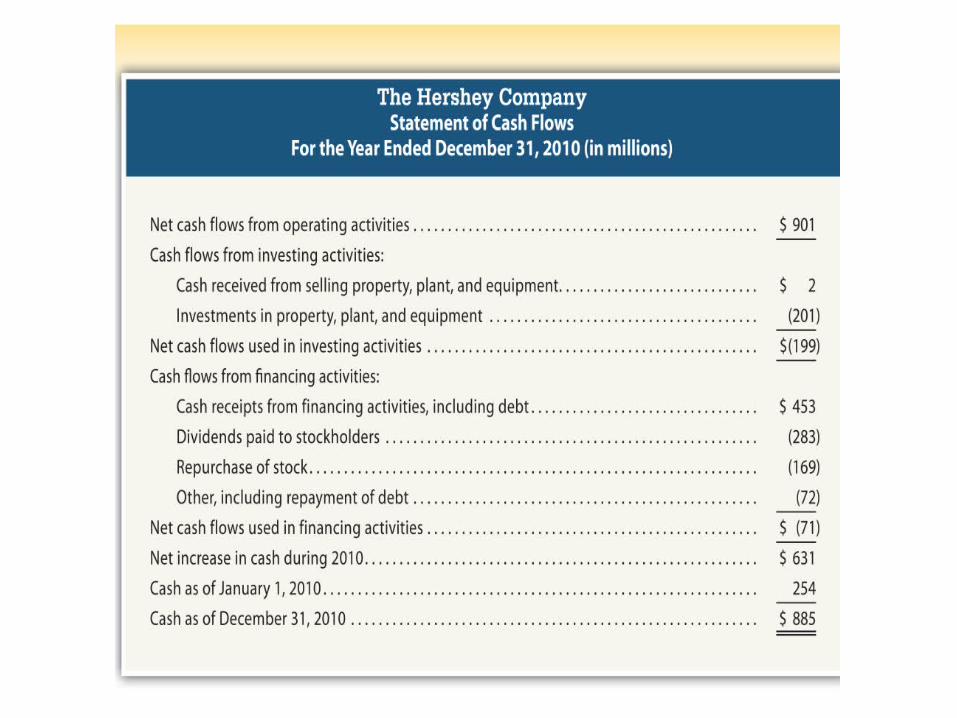

Operating activities: Investing activities: Financing activities:

*Selling goods *Selling buildings *Borrowing money*Providing services *Selling land

Operating activities: Investing activities: Financing activities:*Paying wages *Purchasing buildings *Repaying loans*Paying utilities *Purchasing land *Distributions to owners*Paying taxes

Cash

Outflows of Cash(Payments)

*Receiving investments from owners

Cash Flows

Inflows of Cash(Receipts)

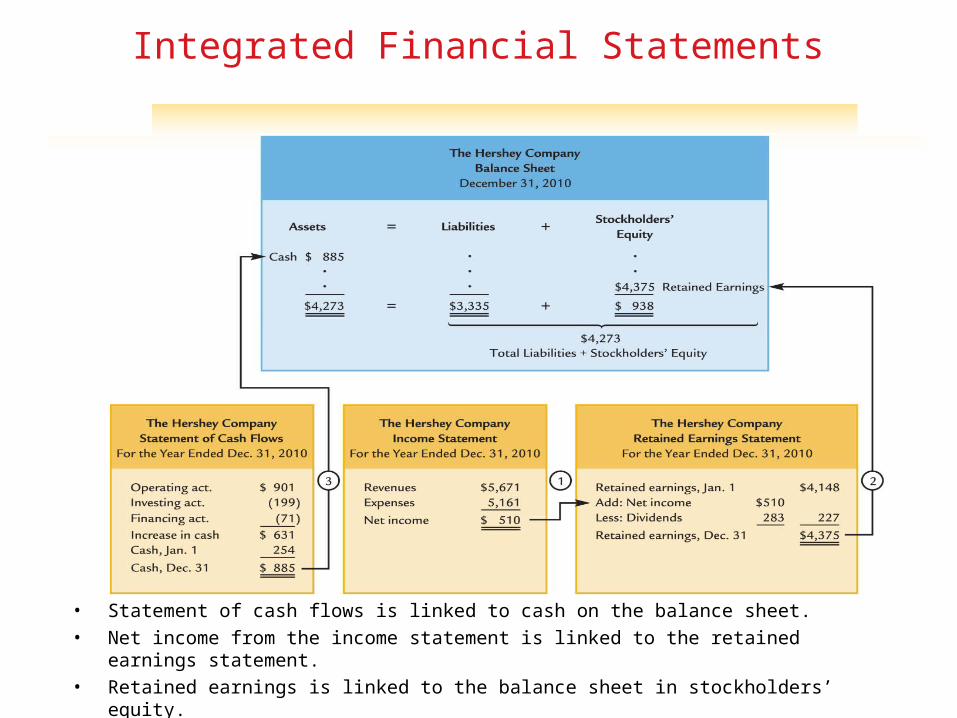

• Statement of cash flows is linked to cash on the balance sheet.

• Net income from the income statement is linked to the retained earnings statement.

• Retained earnings is linked to the balance sheet in stockholders’ equity.

Integrated Financial Statements

Paul’s Valet ParkingPaul’s Valet ParkingPaul’s Valet ParkingPaul’s Valet Parking

Given list of Account titles: (Note: the business started March 1Given list of Account titles: (Note: the business started March 1stst.).)

CashCash $2,000$2,000 Note PayableNote Payable $1,200$1,200

Fees EarnedFees Earned $3,600$3,600 Retained EarningsRetained Earnings $1,600$1,600

Rent ExpenseRent Expense $500$500 Wage ExpenseWage Expense $800$800

LandLand $1,500$1,500 Capital StockCapital Stock $1,300$1,300

DividendsDividends $700$700 SuppliesSupplies $600$600

Complete the following Statements:Complete the following Statements:

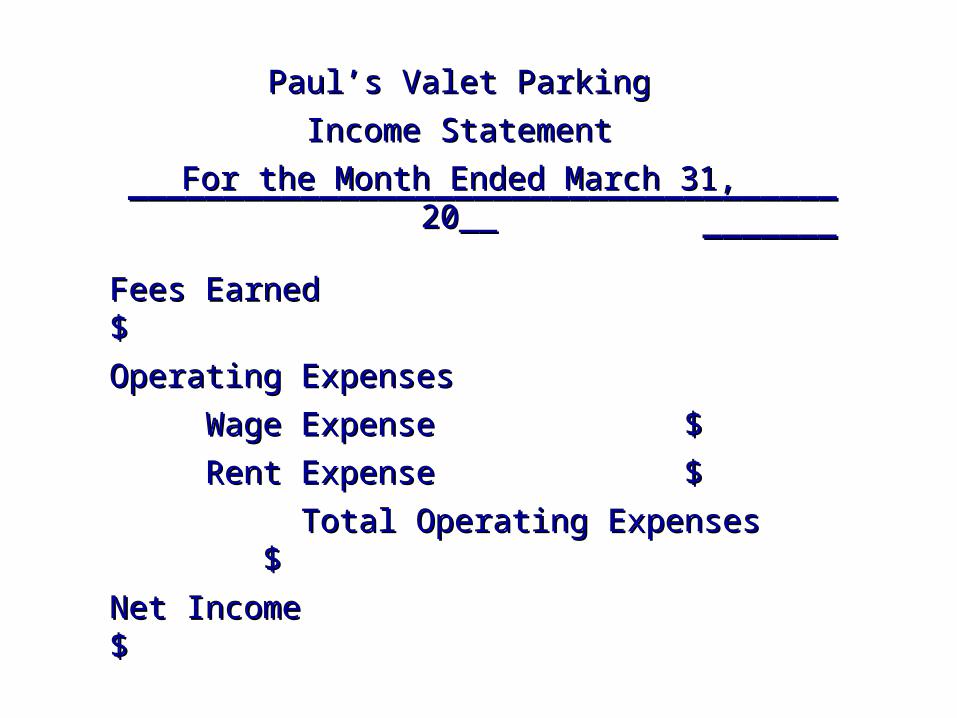

Paul’s Valet ParkingPaul’s Valet Parking

Income StatementIncome Statement

For the Month Ended March 31, 20__For the Month Ended March 31, 20__________________________________________________________________________________________

Fees EarnedFees Earned $ $

Operating ExpensesOperating Expenses

Wage ExpenseWage Expense $$

Rent ExpenseRent Expense $$

Total Operating ExpensesTotal Operating Expenses $ $

Net Income Net Income $ $

Paul’s Valet ParkingPaul’s Valet Parking

Retained Earnings StatementRetained Earnings Statement

For the Month Ended March 31, 20__For the Month Ended March 31, 20__________________________________________________________________________________________

Retained Earnings, March 1Retained Earnings, March 1 $ -0-$ -0-

Net Income for MarchNet Income for March $$

Less DividendsLess Dividends $$

Retained Earnings, March 31Retained Earnings, March 31 $$

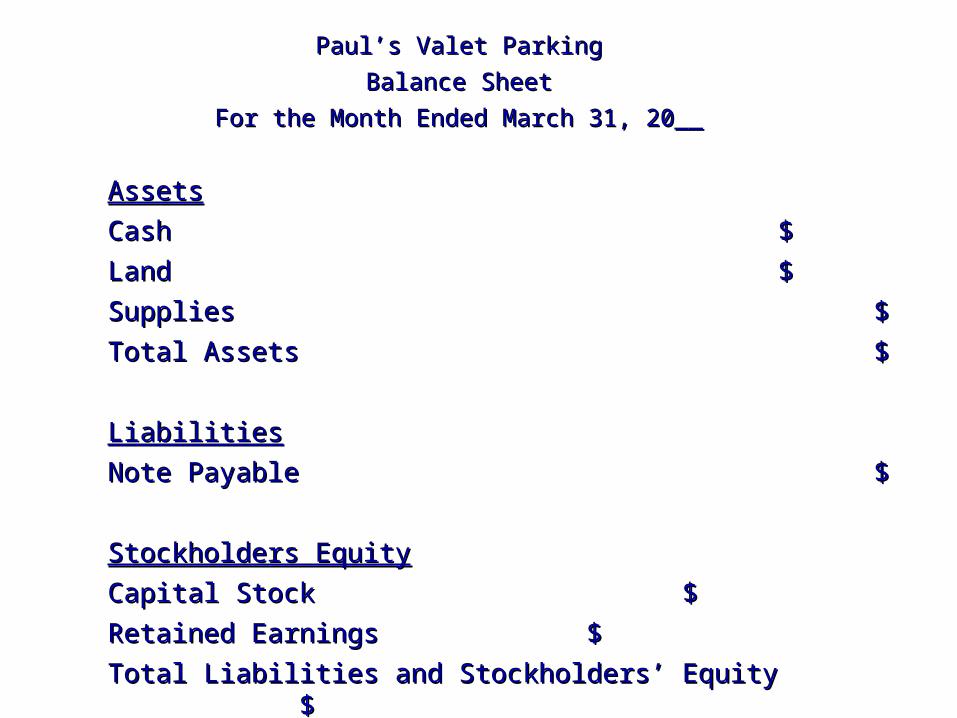

Paul’s Valet ParkingPaul’s Valet Parking

Balance SheetBalance Sheet

For the Month Ended March 31, 20__For the Month Ended March 31, 20__

AssetsAssets

CashCash $$

LandLand $$

SuppliesSupplies $$

Total AssetsTotal Assets $$

LiabilitiesLiabilities

Note PayableNote Payable $$

Stockholders EquityStockholders Equity

Capital StockCapital Stock $$

Retained EarningsRetained Earnings $$

Total Liabilities and Stockholders’ EquityTotal Liabilities and Stockholders’ Equity $$

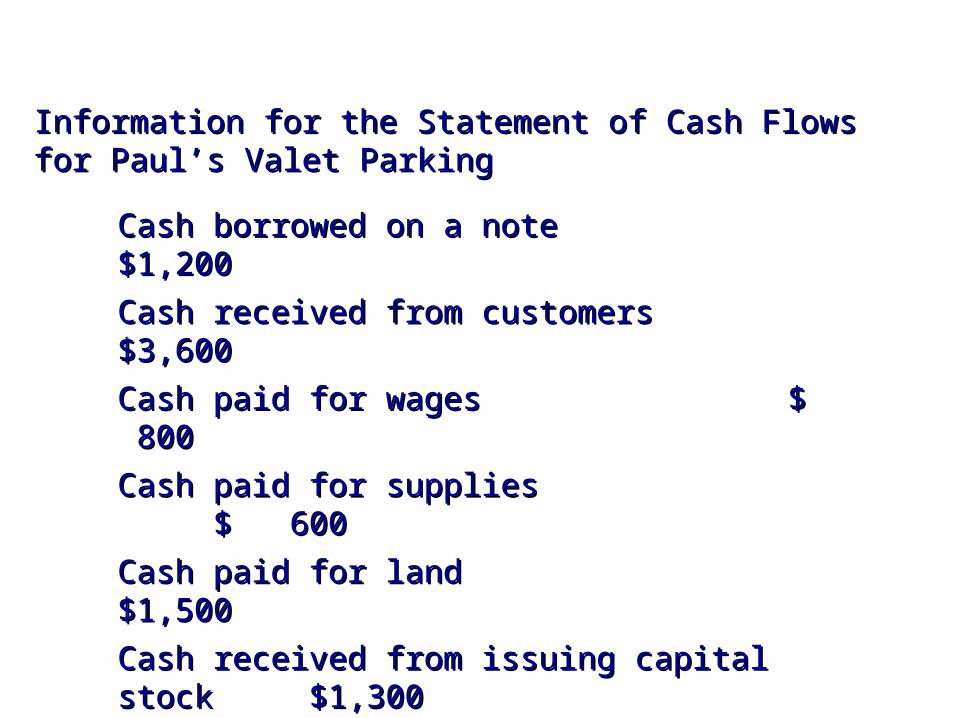

Information for the Statement of Cash Flows for Paul’s Valet Information for the Statement of Cash Flows for Paul’s Valet ParkingParking

Cash borrowed on a noteCash borrowed on a note $1,200$1,200

Cash received from customersCash received from customers $3,600$3,600

Cash paid for wagesCash paid for wages $ 800$ 800

Cash paid for suppliesCash paid for supplies $ 600$ 600

Cash paid for land Cash paid for land $1,500$1,500

Cash received from issuing capital stockCash received from issuing capital stock $1,300$1,300

Cash paid for rentCash paid for rent $ 500$ 500

Cash paid in dividendsCash paid in dividends $ 700$ 700

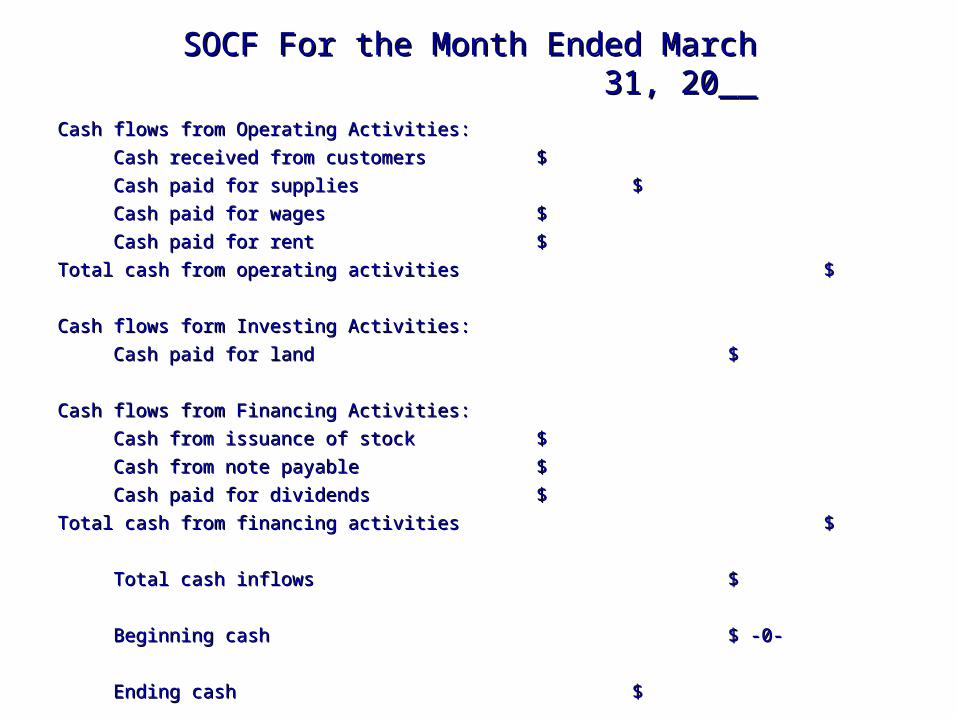

SOCF For the Month Ended March 31, 20__SOCF For the Month Ended March 31, 20__

Cash flows from Operating Activities:Cash flows from Operating Activities:

Cash received from customersCash received from customers $$

Cash paid for suppliesCash paid for supplies $$

Cash paid for wagesCash paid for wages $$

Cash paid for rentCash paid for rent $$

Total cash from operating activitiesTotal cash from operating activities $$

Cash flows form Investing Activities:Cash flows form Investing Activities:

Cash paid for landCash paid for land $$

Cash flows from Financing Activities:Cash flows from Financing Activities:

Cash from issuance of stockCash from issuance of stock $$

Cash from note payableCash from note payable $$

Cash paid for dividendsCash paid for dividends $$

Total cash from financing activitiesTotal cash from financing activities $$

Total cash inflowsTotal cash inflows $$

Beginning cashBeginning cash $ -0-$ -0-

Ending cashEnding cash $$

The Accounting “Rules”

Accounting Environment

Accountants follow generally accepted accounting principles (GAAP), which are authoritative guidelines that define accounting practice at a particular time

WHY?•Financial statements must be comparable and reliable. •External users need to understand the rules and assumptions used by companies when constructing financial statements.

Eight Concepts

ADEQUATE ADEQUATE DISCLOSUREDISCLOSUREADEQUATE ADEQUATE

DISCLOSUREDISCLOSURE

ACCOUNTING ACCOUNTING PERIODPERIOD

ACCOUNTING ACCOUNTING PERIODPERIOD

BUSINESS BUSINESS ENTITYENTITY

BUSINESS BUSINESS ENTITYENTITY

UNIT OF UNIT OF MEASUREMEASUREUNIT OF UNIT OF

MEASUREMEASURE OBJECTIVITY OBJECTIVITY CONCEPTCONCEPT

OBJECTIVITY OBJECTIVITY CONCEPTCONCEPT

COST COST CONCEPTCONCEPT

COST COST CONCEPTCONCEPT

MATCHING MATCHING CONCEPTCONCEPTMATCHING MATCHING CONCEPTCONCEPT

GOING GOING CONCERNCONCERN

GOING GOING CONCERNCONCERN

1. Sally Vertrees purchased a personal computer for use 1. Sally Vertrees purchased a personal computer for use at home. Sally owns a dental practice. She occasionally at home. Sally owns a dental practice. She occasionally uses the computer for a task related to her dental uses the computer for a task related to her dental practice; however, the computer is used primarily by practice; however, the computer is used primarily by Sally’s children. Could the computer be recorded as an Sally’s children. Could the computer be recorded as an asset in the accounting records of Sally’s dental office? asset in the accounting records of Sally’s dental office? Why or why not?Why or why not?

Accounting PrinciplesAccounting PrinciplesAccounting PrinciplesAccounting Principles

2. Jason Thompson purchased an office building 10 2. Jason Thompson purchased an office building 10 years ago for $780,000. The building was just appraised years ago for $780,000. The building was just appraised at $1.25 million. What value should be used for the at $1.25 million. What value should be used for the building in Jason’s accounting records? Support your building in Jason’s accounting records? Support your answer.answer.

Accounting Principles (Continued)Accounting Principles (Continued)Accounting Principles (Continued)Accounting Principles (Continued)