the role of csr on financial performance of...

TRANSCRIPT

34

The Role of CSR on Financial Performance of Companies

Listed at the Nairobi Securities Exchange (NSE)

1John Karori Nyamiobo

2 Willy Mwangi Muturi

3Walter Bichanga Okibo

4Tobias Olweny

1 PhD Candidate, Jomo Kenyatta University of Agriculture and Technology (JKUAT),

Nairobi, Kenya, Email: [email protected] 2-4

Jomo Kenyatta University of Agriculture and Technology (JKUAT), Nairobi, Kenya

ABSTRACT

The relationship between corporate social responsibility (CSR) and firm performance has been a

subject for many extensive studies in the last decade. This study examined the effect of Corporate

Social Responsibility on Performance of listed firms at the Nairobi Securities Exchange (NSE). The

research was designed to use quantitative research method utilizing data collected from companies

listed at the NSE. The study employed simple linear regression analysis to observe the relationship

between the dependent variable (financial performance) of firms listed at NSE and the independent

variable (Corporate Social Responsibility). Questionnaires were used to collect primary data from the

targeted population NSE. The data collected was analysed by use of descriptive and inferential

statistics. The study carried out the analysis of the data with the help of statistical packages including

SPSS and MS-Excel. A correlation and regression analysis was carried out to determine the

relationship between financial performance of companies listed at the NSE and Corporate Social

Responsibility. The findings revealed that, R2 was .452 meaning that CSR contributed 45.2% to the

total variability in the dependent variable (Financial Performance). This demonstrated that Corporate

Social Responsibility had a significant influence on the dependent variable (financial performance).

From the findings the study concluded that, there was a significant positive effect of corporate social

responsibility on performance of listed firms in Nairobi Securities Exchange.

Keywords: Corporate Social Responsibility, Performance, Listed Companies

INTRODUCTION

The role of security exchanges are critical and play an important role in the economic development of

economies. They facilitate corporations and government units to raise capital; allocate capital toward

productive uses; provide opportunity for people to increase saving and investment; reveal investors’

perception about potential earnings capacity of firms. Thus giving guidance to firm managements and

most importantly, securities help to generate employment and increase income (Siljanen, 2012). On

the global scene, the largest Securities are located in the developed economies of the West, mainly in

United States and Europe. In the Eastern African region, the Nairobi Securities Exchange of Kenya

which was established in 1954, is the sub-Saharan Africa’s fourth largest and the largest in Eastern

and Central Africa. It is the most developed in East and Central African Countries (Kamau,

Namusonge & Bichanga, 2016). NSE plays an important role in economic development through

various channels: mobilization of domestic savings shifting critical resources from dormant agents to

active agents; major medium on incoming international capital; and facilitation of government

privatisation programme (Capital Markets Authority, 2012).

According to Carroll (1991) CSR is categorized into four types: economic, legal, ethical and

discretionary, and these are organized into a pyramid where economic responsibility is the most

important and fundamental responsibility. Further, Hasseldine, Salama and Toms (2005) and Toms

(2002) expressed that it is difficult for companies investing in CSR activities to maximize their

reputation without disclosing information of such activities. This scenario is utilitarian and strategic as

the disclosure of related information contribution to financial performance is of importance to firms

(Barnett, 2007; Mackey et al., 2007). Moreover, Patten (1992) suggested that social information in

International Journal of Business & Law Research 5(3):34-45, July-Sept., 2017

© SEAHI PUBLICATIONS, 2017 www.seahipaj.org ISSN: 2360-8986

35

annual reports can influence public policies directly by addressing public or legislative concerns or

indirectly by projecting an image of the company’s social awareness.

Statement of the Problem

The idea of business organisations engaging beyond legal requirements is ethically desirable even

though it appears to take away current resources from the firm’s immediate needs (Jooh, et al.,

2010).The relationship between corporate social responsibility and firm performance has been a

subject for many extensive studies in the last decade (Buiten, 2012). Past studies on the relationship

between CSR and financial performance of companies have not been conclusive. Griffin & Mahon

(1997) mapped several companies in their research in the 1970s, 1980s and 1990s and concluded that

the relationship between CSR and financial performance of firms could be positive, neutral or even

negative. Nkaiwatei (2011) in his study for instance, concluded that financial performance was one of

the important factors that determined CSR. Wanjala (2011) also arrived at similar conclusions for the

banking sector. Although CSR research has been the subject of discussion for firms listed at securities

exchange study for the past few decades, the empirical studies focused more on the developed

Western economies (Tsang & Kwan, 1999). Thus, this paper sought to find out the role of CSR on

financial performance of companies listed at the Nairobi Securities Exchange (NSE).

THEORETICAL AND EMPIRICAL LITERATURE

The study was directed by the following theories: Legitimacy Theory, Capital Structure Theory, and

Agency Theory.

Financial Performance

Financial performance is often measured based on accounting key performance indicators. These

include Return on Assets (ROA), Operating Profit Margin, Earnings before Interest and Income Tax,

Return on Capital Employed, Return of Equity (Itter & Larker, 1997; Fraquelli & Vannoni, 2000;

Crabtree & DeBusk, 2008). The advantage of using these measurements is that they are readily

available. All profit oriented businesses are required to produce annual financial statements where

these measurements can be obtained from (Chenhall & Euske, 2007; Langfield – Smith, 2007). ROA

percentage shows how profitable a company’s assets are in generating income. It is given by the ratio

between net income and total assets. This ratio informs us what the company can do with what it has

got. Thus, how many shillings of earnings the firm can derive from each shilling of assets it controls.

The number will vary widely across industries. Return on assets gives an indication of the capital

intensity of a company, which will depend on the industrial sector. Companies that require large initial

investment will generally have lower returns on assets.

Return on Equity ratio is extensively used in economic literature (Parker & Eilbirt, 1975; Waddock &

Graves, 1997). ROE is the percentage expression of a company’s net income as it is returned as value

to shareholders. It offer investors and analysts an alternative measure of the firm’s profitability and

calculates the efficiency with which the firm generates profit using the funds that shareholders have

invested. In equation form. In calculation of RE; Return on Equity = Net Income shareholders’ equity.

ROE is equal to a fiscal year’s net income (after preferred stock dividends but before common stock

dividends) divided by total equity (excluding preferred shares), expressed as a percentage. It measures

the rate of return on ownership interest (shareholders’ equity) of common stock owners. It measures a

firm’s efficiency at generating profits from every shilling of net assets (assets minus liabilities), and

shows how well a company uses investment shillings to generate earnings growth.

Corporate Social Responsibility

Bowen (1953) defines Corporate Social Responsibility as the obligation of businessmen to pursue

those policies, to make those decisions or to follow those lines of action which are desirable to society.

Thus, CSR can be interpreted to give a concept that firm will voluntarily integrate social and

environmental concerns into their business operations and interactions with stakeholders (Djalil,

2003). The broader understanding of this concept is that social responsibility becomes an integral part

of strategic investment, core business strategy and a management instrument. This concept implies

that CSR is not a cost but an investment for the firm (Kusumadilaga, 2010). Empirical research on the

link between CSR and financial performance has given varied results. Of particular interest is the

great variety in the sign of the relation studied. The relationship between corporate social performance

(CSP) and Corporate Financial Performance (CFP) has received considerable research from scholars

close to a century. There have been divergent opinions on CSR as to whether acting in an ethical and

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok

36

socially responsible manner adds any economic value to a firm. According to Friedman (1982), the

primary objective of the firm management should be to maximize shareholder wealth. Other opinions

are to the contrary opinion arguing that companies should try to be socially responsible, and gain

support for their activities from stakeholders. Thus, managers should maximize the well-being of

stakeholders in general. Some argue that in order to maximize profits, CSR may be a path to it

(Donaldson & Preston, 1995; Freeman, 1984; and Mitchell, Agle & Wood, 1997).

Profit making is the necessary reason for an enterprise to extend and grow while social responsibility

is the basic duty of the "state" to focus upon the setting of its stakeholders with social justice. Lai et al.

(2010) study indicate the effect of corporate social responsibility and firm’s profit on its brand equity

in business-to-business markets from the employee’s viewpoints on a sample of industrial purchasers

in Taiwan’s. The results supported their hypotheses that corporate social responsibility and corporate

reputation have positive effects on industrial brand equity and brand performance. The majority of the

companies believe that they should pay attention to corporate social responsibility however, their main

barrier to adopt corporate social responsibility is cost and lack of human resources; a moderate

positive relationship between CSR and performance exist. Mwangi (2013) stated that the relationship

between corporate social responsibility (CSR) practice and firm performance with some studies

showing a positive relationship. It is with this background that this study indicates that the relationship

between corporate social responsibility practice and determinants of financial performance of firms is

inadequate and these form the basis of this study.

On the negative relation, Waddock and Graves (1997) assumed that companies with responsible

behaviour may have a competitive disadvantage, since they incur unnecessary costs. These costs fall

directly on the bottom line and would necessarily reduce shareholder profits and wealth (Preston &

O’Bannon, 1997). CSP and CFP postulates that the fulfilment of CSR will bring competitive

disadvantage to the firm (Aupperle et al., 1985) methods or need to bear costs. According to this view,

when carrying out CSR activities, increased costs will result in little gain if measured in economic

interest. Neglecting some stakeholders like employees or the environment will lead to a lower CSP for

the firm. Hence, Waddock and Graves (1997) indicated that this theory was based on the assumption

of negative correlation between CSP and CFP. Joshi et al. (2007) found that there is a positive

relationship between profit making and social responsibility.

RESEARCH METHODOLOGY

This paper adopted a correlational survey design on all firms listed at NSE. The target population was

the employees of the 65 listed firms in Nairobi Securities Exchange. A stratified sampling was

employed in such a way that the target population was divided into, Top Level Management, Middle

Level Management and Lower Level Management. A representative sample size of 237 respondents

was derived from the target population. The study used primary data that was collected using

questionnaires. To achieve the aims of this study, the researcher employed multiple linear regression

analysis to observe the relationship between the dependent variable (financial performance) of firms

listed at NSE and Corporate Social Responsibility. The data collected was analysed by use of

descriptive and inferential statistics. The study carried out the analysis of the data with the help of

statistical packages including SPSS and MS-Excel. A correlation and regression analysis was carried

out to determine the relationship between Corporate Social Responsibility and financial performance

of companies listed at the NSE.

DATA ANALYSIS AND DISCUSSION OF THE FINDINGS

This paper sought to find out the role of CSR on financial performance of companies listed at the

Nairobi Securities Exchange (NSE). A sample of 237 respondents was used for the study and a

response rate of 72.6% was obtained.

Reliability Check on the Variables

Cho and Kim (2015) observed that Cronbach's alpha is the most common measure of internal

consistency (Reliability). The authors add that Cronbach's alpha is most commonly used when you

have multiple Likert questions in a survey/questionnaire that form a scale and you wish to determine if

the scale is reliable. The researcher carried out a reliability test taking into account a value of 0.7 or

higher as being sufficient (Bonett & Wright, 2015). From the results presented in Table 1, both the

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok

37

CSR and the dependent variable (financial performance) were found to be reliable at Cronbach’s

Alphas of .919 and .881 which were higher than the threshold of 0.7.

Table 1: Reliability Analysis of the Variables

Reliability Statistics

Variable Cronbach's Alpha N of Items

CSR Information .919 10

Firm Performance .881 8

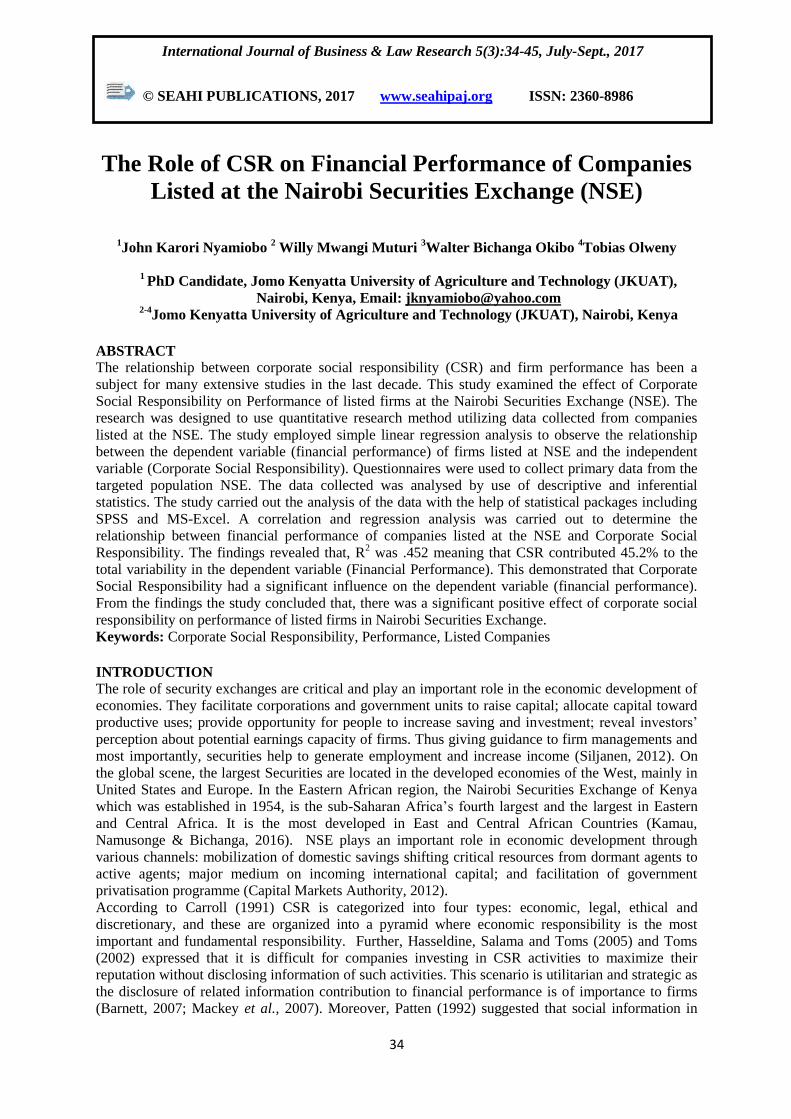

Factor Analysis According to Leech, Barrett and Morgan (2014), variable items should be retained if they are

consistent with the theoretical labels and have factor loadings greater than or equal to 0.4. A factor

analysis on Corporate Social Responsibility was carried out and the findings summarized in Table 2

revealed that none of the factors scored below the threshold of .4 and therefore none was dropped

from the analysis. A similar finding was observed in the dependent variable (Financial Performance)

which showed that all the factors loaded highly as all of them had scores above the threshold of 0.4

(Table 3).

Table 2: Factor Analysis of Corporate Social Responsibility

Component Matrixa

Component

1

The organization donates time, in-kind or financial contributions

to the local community e.g. education and training, cultural and

infrastructure development.

.820

The organization has documented procedures to enable decisions

to be made regarding issues covered by the Global Compact

principles

.820

The organization can demonstrate the impacts of its contribution

and how these are aligned to the organization's core and strategic

issues.

.802

The organization takes action to realise local and/or national

development goals following consultations with the local

community.

.795

The organization's policy includes a commitment to meeting local

legal requirements and international standards. .791

The organization take action in support of broader UN goals and

issues, such as the UN Millennium Development Goals (MDGs)

on combatting HIV, promoting education and women's rights.

.776

The organization has defined and communicated roles and

responsibilities with regard to issues covered by the Global

Compact principles.

.746

The organization has a written policy covering respect for human

rights, occupational health and safety, labour rights,

environmental and anti-corruption issues.

.720

The organization has appointed a senior person(s) responsible for

policies and plans related to issues covered by the Global

Compact principles.

.689

The organization seeks to contribute to community development

by entering partnerships with a range of stakeholders, including

UN agencies, governments, civil society, labour, and other non-

business interests.

.644

Extraction Method: Principal Component Analysis.

a. 1 components extracted.

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok

38

Table 3: Factor Analysis on Firm’s Financial Performance

Component Matrixa

Component

1

Net Profit .823

Operating margin .805

Return on Equity .803

Average revenue .798

Asset Base .736

Return on capital employed .705

Gross Profit Margin .689

Return on Assets .564

Extraction Method: Principal Component Analysis.

a. 1 components extracted.

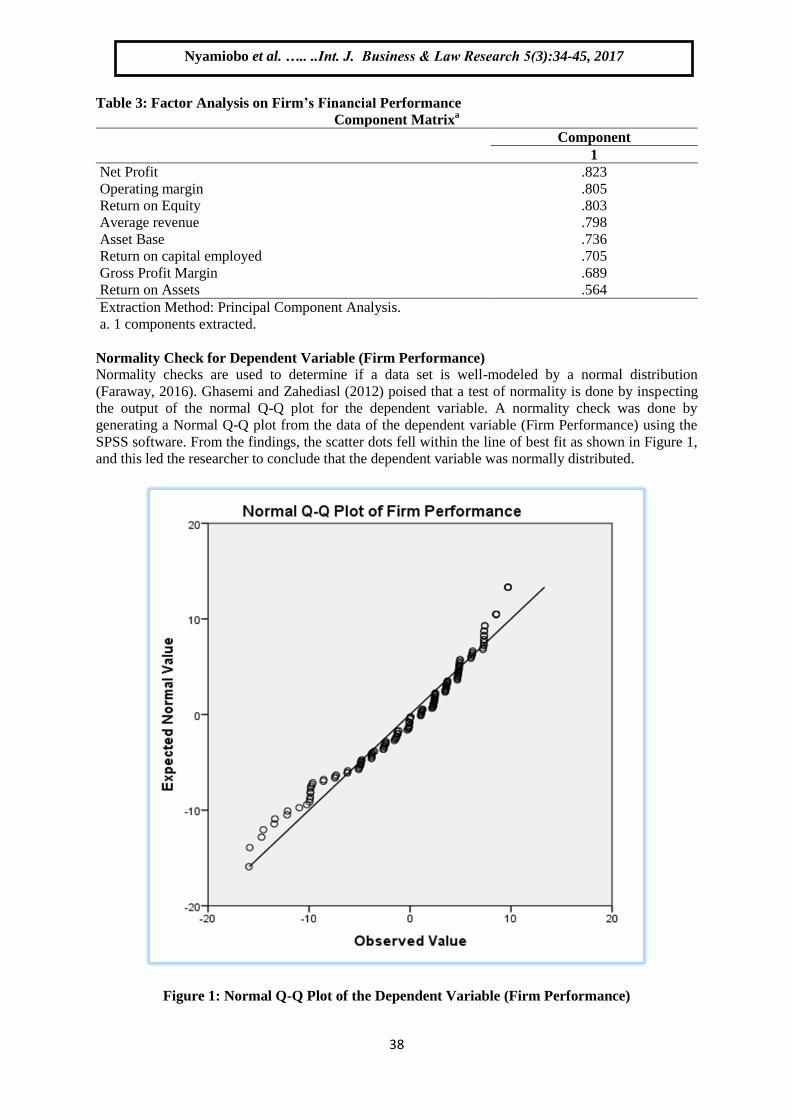

Normality Check for Dependent Variable (Firm Performance)

Normality checks are used to determine if a data set is well-modeled by a normal distribution

(Faraway, 2016). Ghasemi and Zahediasl (2012) poised that a test of normality is done by inspecting

the output of the normal Q-Q plot for the dependent variable. A normality check was done by

generating a Normal Q-Q plot from the data of the dependent variable (Firm Performance) using the

SPSS software. From the findings, the scatter dots fell within the line of best fit as shown in Figure 1,

and this led the researcher to conclude that the dependent variable was normally distributed.

Figure 1: Normal Q-Q Plot of the Dependent Variable (Firm Performance)

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok

39

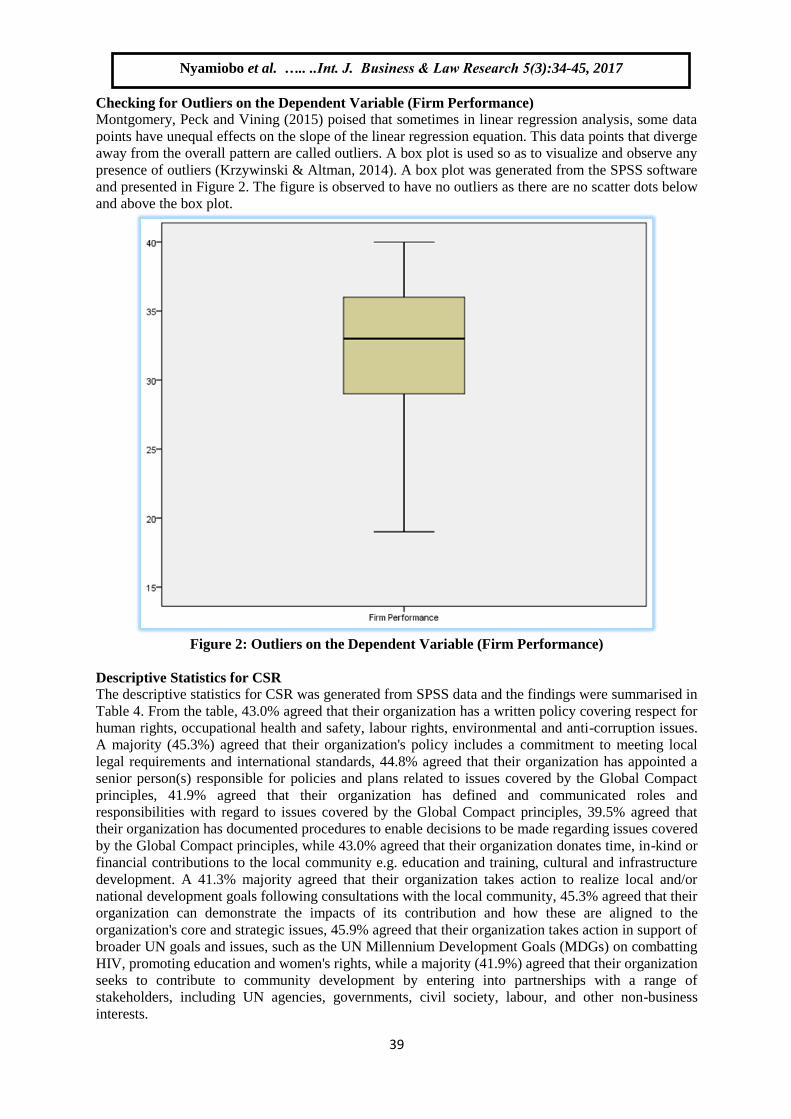

Checking for Outliers on the Dependent Variable (Firm Performance)

Montgomery, Peck and Vining (2015) poised that sometimes in linear regression analysis, some data

points have unequal effects on the slope of the linear regression equation. This data points that diverge

away from the overall pattern are called outliers. A box plot is used so as to visualize and observe any

presence of outliers (Krzywinski & Altman, 2014). A box plot was generated from the SPSS software

and presented in Figure 2. The figure is observed to have no outliers as there are no scatter dots below

and above the box plot.

Figure 2: Outliers on the Dependent Variable (Firm Performance)

Descriptive Statistics for CSR

The descriptive statistics for CSR was generated from SPSS data and the findings were summarised in

Table 4. From the table, 43.0% agreed that their organization has a written policy covering respect for

human rights, occupational health and safety, labour rights, environmental and anti-corruption issues.

A majority (45.3%) agreed that their organization's policy includes a commitment to meeting local

legal requirements and international standards, 44.8% agreed that their organization has appointed a

senior person(s) responsible for policies and plans related to issues covered by the Global Compact

principles, 41.9% agreed that their organization has defined and communicated roles and

responsibilities with regard to issues covered by the Global Compact principles, 39.5% agreed that

their organization has documented procedures to enable decisions to be made regarding issues covered

by the Global Compact principles, while 43.0% agreed that their organization donates time, in-kind or

financial contributions to the local community e.g. education and training, cultural and infrastructure

development. A 41.3% majority agreed that their organization takes action to realize local and/or

national development goals following consultations with the local community, 45.3% agreed that their

organization can demonstrate the impacts of its contribution and how these are aligned to the

organization's core and strategic issues, 45.9% agreed that their organization takes action in support of

broader UN goals and issues, such as the UN Millennium Development Goals (MDGs) on combatting

HIV, promoting education and women's rights, while a majority (41.9%) agreed that their organization

seeks to contribute to community development by entering into partnerships with a range of

stakeholders, including UN agencies, governments, civil society, labour, and other non-business

interests.

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok

40

Table 4. Descriptive Statistic for CSR

Strongly

Disagree Disagree Neutral Agree

Strongly

Agree

The organization has a written policy covering

respect for human rights, occupational health and

safety, labour rights, environmental and anti-

corruption issues.

1.2% 7.0% 25.6% 43.0% 23.3%

The organization's policy includes a commitment to

meeting local legal requirements and international

standards.

0.0% 7.6% 26.7% 45.3% 20.3%

The organization has appointed a senior person(s)

responsible for policies and plans related to issues

covered by the Global Compact principles.

1.7% 5.2% 22.1% 44.8% 26.2%

The organization has defined and communicated

roles and responsibilities with regard to issues

covered by the Global Compact principles.

3.5% 15.7% 20.9% 41.9% 18.0%

The organization has documented procedures to

enable decisions to be made regarding issues covered

by the Global Compact principles

2.9% 7.6% 24.4% 39.5% 25.6%

The organization donates time, in-kind or financial

contributions to the local community e.g. education

and training, cultural and infrastructure development.

1.7% 8.7% 22.1% 43.0% 24.4%

The organization takes action to realise local and/or

national development goals following consultations

with the local community.

2.3% 7.6% 19.8% 41.3% 29.1%

The organization can demonstrate the impacts of its

contribution and how these are aligned to the

organization's core and strategic issues.

2.3% 6.4% 19.2% 45.3% 26.7%

The organization take action in support of broader

UN goals and issues, such as the UN Millennium

Development Goals (MDGs) on combatting HIV,

promoting education and women's rights.

2.3% 7.6% 25.0% 45.9% 19.2%

The organization seeks to contribute to community

development by entering partnerships with a range of

stakeholders, including UN agencies, governments,

civil society, labour, and other non-business

interests.

1.7% 8.1% 22.1% 41.9% 26.2%

This findings are in line with Toms (2002) suggestions that firm’s implementation, monitoring and

disclosure of environmental policies in the annual reports make a significant contribution in the

formation of good environmental reputation in the company. In a similar study, Hasseldine, Salama

and Toms (2005) tested the effect of both qualitative and quantitative disclosure on the company’s

reputation, their study revealed that quality of environmental disclosures have a stronger influence on

the creation of good environmental reputation more than merely quantitative disclosure. Another study

by Rettab, Brik and Mellahi (2009) examined the relationship between corporate social responsibility

and reputation of the company; they found a positive relationship between the two variables.

Descriptive statistics for Firm’s Financial Performance

The researcher sought to find the descriptive statistics of Firm’s Financial Performance. The findings

were summarized in Table 5. From the table, 48.8% said their Asset Base was good, 48.3% rated their

Gross Profit Margin as good, 44.8% said their Return on Assets was good, 48.3% rated their average

revenue as good, 48.8% rated their company’s operating margin as good, 49.4% rated their company’s

Return on Equity as good, 38.4% rated return on capital employed in their company as good, while a

44.8% majority said Net Profit was good.

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok

41

Table 5: Descriptive statistics for Financial Performance

Poor Fair Average Good Very Good

Asset Base 0.6% 1.2% 19.2% 48.8% 30.2%

Gross Profit Margin 0.6% 4.1% 14.0% 48.3% 33.1%

Return on Assets 1.7% 7.6% 34.3% 44.8% 11.6%

Average revenue 0.0% 4.7% 20.9% 48.3% 26.2%

Operating margin 0.0% 5.2% 16.9% 48.8% 29.1%

Return on Equity 0.0% 2.3% 18.6% 49.4% 29.7%

Return on capital employed 0.6% 4.7% 14.0% 38.4% 42.4%

Net Profit 0.0% 5.2% 14.5% 44.8% 35.5%

Linearity between Firm Performance and Corporate Social Responsibility

Whilst there are a number of ways to check whether a linear relationship exists between the two

variables, Mertler and Reinhart (2016) suggested creating a scatterplot where the dependent variable is

plotted against the independent variable and then the scatterplot is visually inspected to check for

linearity. The researcher sought to find the linearity between Firm Performance and Corporate Social

Responsibility. The findings summarised in Figure 3 show that a strong positive linear relationship

existed between Firm Performance and Corporate Social Responsibility.

Figure 3: The linearity between Firm Performance and Liqudity

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok

42

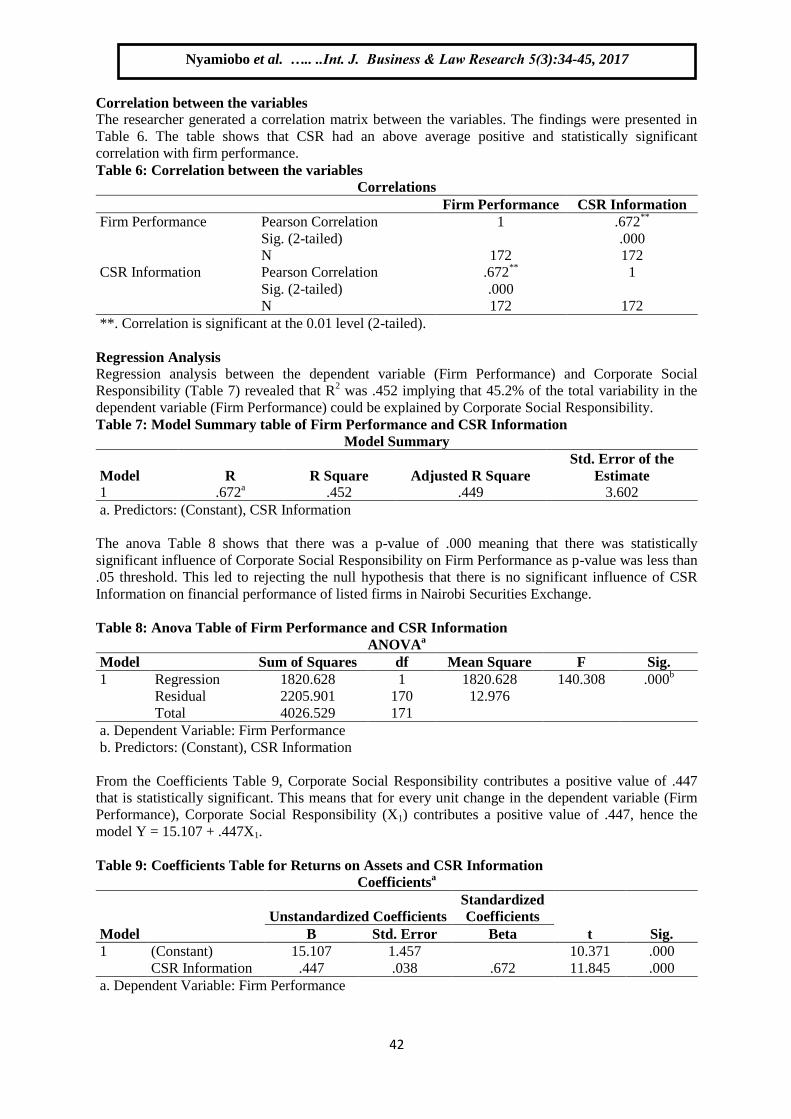

Correlation between the variables

The researcher generated a correlation matrix between the variables. The findings were presented in

Table 6. The table shows that CSR had an above average positive and statistically significant

correlation with firm performance.

Table 6: Correlation between the variables

Correlations

Firm Performance CSR Information

Firm Performance Pearson Correlation 1 .672**

Sig. (2-tailed) .000

N 172 172

CSR Information Pearson Correlation .672**

1

Sig. (2-tailed) .000

N 172 172

**. Correlation is significant at the 0.01 level (2-tailed).

Regression Analysis Regression analysis between the dependent variable (Firm Performance) and Corporate Social

Responsibility (Table 7) revealed that R2 was .452 implying that 45.2% of the total variability in the

dependent variable (Firm Performance) could be explained by Corporate Social Responsibility.

Table 7: Model Summary table of Firm Performance and CSR Information

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .672a .452 .449 3.602

a. Predictors: (Constant), CSR Information

The anova Table 8 shows that there was a p-value of .000 meaning that there was statistically

significant influence of Corporate Social Responsibility on Firm Performance as p-value was less than

.05 threshold. This led to rejecting the null hypothesis that there is no significant influence of CSR

Information on financial performance of listed firms in Nairobi Securities Exchange.

Table 8: Anova Table of Firm Performance and CSR Information

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1 Regression 1820.628 1 1820.628 140.308 .000b

Residual 2205.901 170 12.976

Total 4026.529 171

a. Dependent Variable: Firm Performance

b. Predictors: (Constant), CSR Information

From the Coefficients Table 9, Corporate Social Responsibility contributes a positive value of .447

that is statistically significant. This means that for every unit change in the dependent variable (Firm

Performance), Corporate Social Responsibility (X1) contributes a positive value of .447, hence the

model Y = 15.107 + .447X1.

Table 9: Coefficients Table for Returns on Assets and CSR Information

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) 15.107 1.457 10.371 .000

CSR Information .447 .038 .672 11.845 .000

a. Dependent Variable: Firm Performance

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok

43

SUMMARY OF FINDINGS AND CONCLUSION

From the findings, 43.0% agreed that their organization has a written policy covering respect for

human rights, occupational health and safety, labour rights, environmental and anti-corruption issues.

A majority (45.3%) agreed that their organization's policy includes a commitment to meeting local

legal requirements and international standards, 44.8% agreed that their organization has appointed a

senior person(s) responsible for policies and plans related to issues covered by the Global Compact

principles, 41.9% agreed that their organization has defined and communicated roles and

responsibilities with regard to issues covered by the Global Compact principles, 39.5% agreed that

their organization has documented procedures to enable decisions to be made regarding issues covered

by the Global Compact principles, while 43.0% agreed that their organization donates time, in-kind or

financial contributions to the local community e.g. education and training, cultural and infrastructure

development. A 41.3% majority agreed that their organization takes action to realize local and/or

national development goals following consultations with the local community, 45.3% agreed that their

organization can demonstrate the impacts of its contribution and how these are aligned to the

organization's core and strategic issues, 45.9% agreed that their organization takes action in support of

broader UN goals and issues, such as the UN Millennium Development Goals (MDGs) on combatting

HIV, promoting education and women's rights, while a majority (41.9%) agreed that their organization

seeks to contribute to community development by entering into partnerships with a range of

stakeholders, including UN agencies, governments, civil society, labour, and other non-business

interests. Correlation analysis showed that CSR had an above average positive and statistically

significant correlation with firm performance at .672. Regression analysis between the dependent

variable (Firm Performance) and Corporate Social Responsibility revealed that R2 was .452 implying

that 45.2% of the total variability in the dependent variable (Firm Performance) could be explained by

Corporate Social Responsibility.

From the findings therefore, the study concluded that corporate social responsibility has a positive

effect on financial performance of listed firms in Nairobi Securities Exchange. In a similar study,

Waddock and Graves (1997) also found a significant positive relation between CSP index and

performance. Further, Joshi et al. (2007) concluded that there is a positive relationship between profit

making and social responsibility. Based on these findings, the study recommends that policy makers

and other stakeholders in the institutions under study identify ways to engage in and promote

meaningful CSR programs and activities for the long terms value of the company, its shareholders and

the community.

REFERENCES

Aupperle, K.E., Carroll, A.B. & Hatfield, J.D. (1985). An empirical examination of the relationship

between corporate social responsibility and profitability. Academy of Management Journal

28(2), pp.446-463.

Barnett, M.L., (2007). Stakeholder Influence Capacity And The Variability of Financial Returns To

Corporate Social Responsibility, Academy Of Management Review, 32(3), pp.794-816.

Belkanoui, A. & Karpik, P.G. (1989). Determinants of Corporate Decision or Disclosure Social

Information, Accounting, auditing and accountability Journal, 2 (1): 36-51.

Bonett, D. G., & Wright, T. A. (2015). Cronbach's alpha reliability: Interval estimation, hypothesis

testing, and sample size planning. Journal of Organizational Behavior, 36(1), 3-15.

Bowen, H.R. (1953). Social Responsibilities of Businessman, Harper & Brothers, New York. NY.

Buiten, M. (2012).The Role of Enforcement Mechanisms for Corporate Governance in India.

Gandhi Institute of Development Research, Mumbai, India.

Capital Markets Authority. (2012). How Does the Stock Market Work? Retrieved from

http://www.cma.or.ke/index.php?option=com_content&task=view&id=10&Itemid=36.

Carroll, A. B. (1991). The Pyramid of Corporate Social Responsibility: Toward the Moral

Management of Organizational Stakeholders, Business Horizon, 34(4), pp.39-48.

Chenhall, R.H. & Euske, K.J. (2007). The Role of Management Control Systems in Planned

Organizational Change: An Analysis of Two Organizations. Accounting, Organizations and

Society, 32, pp. 601-637. Performance measures. European Management Journal, 25(4), pp.

266-282.

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok

44

Cho, E., & Kim, S. (2015). Cronbach’s coefficient alpha: Well known but poorly

understood. Organizational Research Methods, 18(2), 207-230.

Cornell, B. & Shapiro, A.J. (1987). Corporate stakeholders and corporate finance. Financial

management, pp. 5-14.

Crabtree, A.D. &DeBusk, G.K. (2008). The effects of adopting the balanced scorecard on shareholder

returns. Advances in Accounting, 24(1), pp. 8 – 15.

Djalil (2003). Good Corporate Governance: Kelemahan Fundamental Makiroekonomi. Indonesia

www.BusinessDictionary.com

Donaldson, T., & Preston, L.E. (1995). The stakeholder theory of the modern corporation: concepts,

evidence and implications. Academy of Management Review, 20, pp. 65-91.

Faraway, J. J. (2016). Extending the linear model with R: generalized linear, mixed effects and

nonparametric regression models (Vol. 124). CRC press.

Fraquelli, G. & Vannoni D. (2000). Multidimensional performance in telecommunications regulation

and competition: Analysing the European major players. Information Economics and policy.

12(1), 27-46.

Freeman, R.E. (1984). Strategic management: A stakeholder perspective. Englewood Cliffs: Prentice

Hall USA.

Friedman, M. (1982). Monetary policy: Theories and practice, The Journal of Money, Credit and

Banking, Vol. 14(1), 98-118.

Ghasemi, A., & Zahediasl, S. (2012). Normality tests for statistical analysis: a guide for non-

statisticians. International journal of endocrinology and metabolism, 10(2), 486-489.

Griffin, J.J., & Mahon, J.T. (1997). The Corporate Social Performance and Corporate Financial

Performance Debate, Business and Society, 36, 5-32. Grossman, S., and Hart, O. (1983).An

Analysis of Principal-Agent Problem. Econometrica 51: pp. 7-45.

Hasseldine, J., Salama, A. I. &Toms J. S. (2005). Quantity versus Quality: The Impact of

Environmental Disclosures On The Reputations Of UK PLCS‟, The British Accounting

Review, 37(2), pp. 231-248.

Itter, C.D., Larker, D.F. & Rajan, M.V. (1997). The choice of performance measure in annual bonus

contracts. The Accounting Review, (April 1997). pp. 231-255.

Jooh, L., Niranjan, P., Roh, J.J. (2010). Relationship between Corporate Sustainability Performance

and Tangible Business Performance: Evidence From Oil and Gas Industry. ISBIT, 3, sp. Iss. 3

January 2011.

Josh, M., Joshi, N., and Joshi, V. (2007). Business War: Competitive Innovation Velocity. Ewing

Marion Kauffman Foundation.

Kamau, C. G., Namusonge, G. S., & Bichanga, W. O. (2016). Creative Accounting among

Corporations Listed in NSE: Sector Analysis. The International Journal of Business &

Management, 4(1), 161.

Krzywinski, M., & Altman, N. (2014). Points of significance: visualizing samples with box

plots. Nature methods, 11(2), 119-120.

Kusumadilaga, R. (2010). Pengaruh Corporate Social Responsibility. Journal FE UNS. Semarang.

Lai, C.S.; Chiu, C.J.; Yang, C.F.; Da. C. (2010). The Effects of Corporate Social Responsibility on

Brand Performance: The Mediating Effect Of Industrial Brand Equity and Corporate

Reputation. Journal of Business Ethics, 95:pp.457-469.

Langfield – Smith, K. (2007). A Review of Quantitative Research in Management Control Systems

and Strategy. In: Chapman, C.S., Hopwood, A.G. Shields, M.D. (Eds.). Handbook of

Management Accounting Research, Vol. 1 Elsevier, Oxford, U.K. pp. 753-784.

Leech, N. L., Barrett, K. C., & Morgan, G. A. (2014). IBM SPSS for intermediate statistics: Use and

interpretation. Routledge.

Mackey, A., Mackey T. B., &Barney J. B. (2007). Corporate Social Responsibility and

Firm Performance: Investor Preference and Corporate Strategies, Academy of Management

Journal, 32(3), pp.817-835.

Mertler, C. A., & Reinhart, R. V. (2016). Advanced and multivariate statistical methods: Practical

application and interpretation. Routledge.

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok

45

Mitchell, R.K., Agle, B.R., & Wood, D.K. (1997). Toward a Theory of Stakeholder Identification and

Salience: Defining the Principle of Who and What Really Counts. Academy of

Management Review, 22: 853-886.

Montgomery, D. C., Peck, E. A., & Vining, G. G. (2015). Introduction to linear regression analysis.

John Wiley & Sons.

Mwangi C. I. (2013). The Relationship between Corporate Social Responsibility Practices and

Financial Performance of Firms In The Manufacturing, Construction and Allied Sector Of The

Nairobi Securities Exchange. International Journal Of Business, Humanities And Technology.

Nkaiwatei, A.O. (2011). Relationship between Social Accounting Practices and Profitability: The

Case of Oil Industry in Kenya, Unpublished Thesis, University of Nairobi.

Ocloo, C. E., Akaba, S., & Worwui-Brown, D. K. (2014). Globalization and competitiveness:

Challenges of small and medium enterprises (SMEs) in Accra, Ghana. International Journal

of Business and Social Science, 5(4).

Parker, I.R. & Eilbirt, H. (1975). Social Responsibility: The Underlying Factors, Business Horizon,

18, 4 pp.5-10

Preston, L. E., & O'bannon, D. P. (1997). The corporate social-financial performance relationship: A

typology and analysis. Business & Society, 36(4), 419-429.

Rettab, B., Brik, A. B., & Mellahi, K. (2009). A study of management perceptions of the impact of

corporate social responsibility on organisational performance in emerging economies: the case

of Dubai. Journal of Business Ethics, 89(3), 371-390.

Schmukler, S. L. (2004). Financial globalization: gain and pain for developing countries. Economic

Review-Federal Reserve Bank of Atlanta, 89(2), 39.

Siljanen, M. (2012). The Evolution of Securities Lending and Risk Mitigation: A Finnish Market Case

Study.

Toms, J.S. (2002). Company Resources, Quality Signals and The Determinants of Corporate

Environmental Reputation: Some UK Evidence‟, The British Accounting Review, 34(3),

257-282.

Tsang, E.W.K. and Kwan, K. (1999). Replication and Theory Development in Organizational Science:

A Critical Realistic Perspective. Academy Of Management Review 24(4), 759-780.

Waddock, S.A., Graves, S.B., (1997). The Corporate Social Performance – Financial Performance

Link. Strategic Management Journal, 18(4):303-319.

Wanjala, D.N. (2011). Factors Influencing the Practice of Corporate Social Responsibility by

Commercial Banks in Kenya, Unpublished Thesis, University of Nairobi.

Nyamiobo et al. ….. ..Int. J. Business & Law Research 5(3):34-45, 2017

Ok