the scope of application of management accounting methods in polish enterprises

TRANSCRIPT

Available online at http://www.idealibrary.com ondoi: 10.1006/mare.2002.0198Management Accounting Research, 2002, 13, 401–418

The scope of application of managementaccounting methods in Polish enterprises

Anna Szychta*

The transformation of Poland’s economic system in the 1990s as a result of transition froma centrally planned economy to a market-based system involves significant changes in theregulatory context and in accounting practice and education.

This paper presents the scope of application of management accounting concepts andmethods in 60 Polish enterprises covered by a questionnaire survey carried out by theauthor between November 1998 and December 1999 in enterprises located in central andsouthern Poland. The selected companies were interviewed by means of a postal survey,with inquiry forms delivered in person in some cases.

The detailed analyses carried out in this paper and the conclusions presented are alsobased on information obtained from documentary evidence kept by the enterprises andfrom direct interviews conducted in the course of work in teams engaged in analysis andassessment of cost accounting practices and in management accounting system design ina number of large and medium Polish enterprises.

The empirical research carried out is aimed at verification of a number of hypothesesincluding the following:

• modification of cost accounting systems and implementation of managementaccounting tools in Polish enterprises is brought about by many different factors,the most important being growth of competition and ownership changes in businessentities,

• Polish enterprises mostly implement the methods and techniques of operationalmanagement accounting,

• short-term budgeting for cost centres is the most widely used method of managementaccounting.

c© 2002 Elsevier Science Ltd. All rights reserved.

Key words: accounting practice in Poland; modification; implementation; cost accountingsystems; calculation; budgeting; future development trends.

*University of Łódz, Department of Accounting, Matejki Street, No. 22/26, 90-237 Łódz, Poland.E-mail: [email protected]

1044–5005/02/$ - see front matter c© 2002 Elsevier Science Ltd. All rights reserved.

402 A. Szychta

1. Introduction

It was only in the early 1990s that management accounting started to have practicalapplication in Polish enterprises, although it had been the subject of study in anumber of Polish higher education institutions for some time before.

By 1990 there was already a vast literature in the field of cost accounting andmanagement accounting. The most important books published in the period 1960–90 include Fedak (1962), Malc (1963), Binkowski (1964), Siwon (1972), Tenderaand Woznica (1974), Jaruga (1966, 1972, 1986), Jaruga et al. (1st edition, 1977, 2ndedition, 1983, 3rd edition 1990) and Jaruga and Skowronski (1st edition 1975, 2ndedition 1982, 3rd edition 1986). These works explained, among other things, therules and conditions for the application of direct costing, break-even point, standardcosting and cost budgeting in responsibility centres. Various methods of indirect costallocation and product costing, as well as principles of selling price and transfer pricedetermination, are presented and evaluated. Particularly interesting is an originalmodel of production factor costing, developed by Skowronski, which combines thefeatures of full costing and marginal costing and emphasizes the decision-usefulnessof cost accounting (Jaruga and Skowronski, 1986).

Many valuable publications and implementation projects have been contributed byacademic accountants: for example Siwon, Malc, Matuszewicz, Lewczynski, Sudoł,Ochman, Wierzbicki, Messner, Troszczynski, Sobanska and many others (Jaruga andSkowronski, 1994, p. 167). The publications stressed the need for the introductionand application in enterprises of cost accounting methods which would generateinformation useful in business management.

Until the late 1980s, cost accounting practice in Poland was determined by the fol-lowing factors: the system of central planning of the economy, dominance of fis-cal requirements and centralized mode of enterprise management. Cost account-ing, regulated by central government orders and guidelines (e.g. Wytyczne, 1968,Zarzadzenie, 1983), provided data for national statistics, calculation of taxes andsubsidies, and—just as the whole of accounting—was an instrument of control overstate-owned enterprises. Especially in the first decades after the Second World War,the chief function of accounting was the protection of property and execution of per-sonal accountability. The information function of accounting was of minor impor-tance (see Sobanska and Szychta, 1995, 1996).

The restoration of a market economy in Poland in the early 1990s and subsequentimplementation and improvement of its mechanisms has had great influence onchanges in accounting regulations, practice, research and education.

The new regulatory framework of accounting, in operation since 1 January 1991(Rozporzadzenie Ministra Finansów, 1991), was revised in 1994 so as to take moreaccount of market economy requirements (Ustawa z dn. 29.09.1991 o rachunkowosci)and this opened, for the first time in the post-war period, the possibility of developingcost accounting systems in enterprises in a way best suited to the specific characterof a given line of business and the particular conditions in which they operate.Business entities1 are now allowed to use individually developed charts of accounts

1Under the Accounting Act of 29 September 1994 (with later amendments) art. 83, certain types of businessentities may be (and are) required to adopt obligatory standard charts of accounts, e.g. banks, insurers,pension funds. The aim of this requirements is to achieve uniformity in grouping of business transactions

Management Accounting Methods in Polish Enterprises 403

appropriate to their particular needs, providing that they ensure that financialstatements are prepared in conformity with the principles and forms prescribed bythe regulations and make possible preparation of statistical statements. This meansthat enterprises can implement cost accounting systems and apply managementaccounting methods and instruments suitable for their size, line of business andmanagement information needs.

The year 1992 marked the beginning of increased interest in the design andimplementation of management accounting solutions in companies and growingrecognition by financial accounting personnel of the need to introduce changes,including development of new, internal reports for management purposes (Sobanskaand Szychta, 1996, p. 115).

The past decade has been a period of changes in accounting systems in a consider-able number of Polish enterprises. The main factors which determine the scope andintensity of these changes include:

— changes in accounting legislation, introduction of laws which effect structuralchanges in the energy sector, health service and social welfare system (establish-ment of independent public health care institutions),

— increased competition on the domestic market,— impact of changes in international economy as a result of globalization and

recession on eastern markets,— changes in the form of business ownership,— setting up of new business entities, also with foreign capital,— development of the money market (the Securities Exchange in Warsaw),— development and implementation of new information processing and transmis-

sion technologies,— acquisition of knowledge in the area of management accounting and controlling

by managers and employees of Polish enterprises, and entry into practice of anew generation educated in the ‘new times’.2

The effect of the factors listed above on accounting practice in Polish enterprisesand future development trends in this area are increasingly chosen as the subject ofacademic research. Some of the researchers are directly engaged in modification ordesign of new accounting systems, including management accounting systems forparticular enterprises, and many of them take part in the implementation of suchsystems.

The aim of this paper is to present the scope of application of the concepts andmethods of management accounting in 60 Polish enterprises covered by a question-naire survey. The paper specifically attempts to provide an empirical verification ofthe following hypotheses:

(1) modification of cost accounting systems and implementation of managementaccounting tools in Polish companies are caused by many different factors, ofwhich the most important are increased competition and ownership changes inbusiness entities;

and to save expenditure of labour on preparation of individual charts of accounts (see Jaruga and Szychta,1997).2For a more complete specification of factors which provide motivation for modification of cost accountingsystems and introduction of management accounting see Sobanska and Wnuk (1999, 2000a).

404 A. Szychta

(2) Polish enterprises mostly implement the methods and techniques of opera-tional management accounting;

(3) short-term budgeting for cost centres is the most widely used method ofmanagement accounting;

(4) in large enterprises operating as commercial companies (limited liability com-panies, joint-stock companies) the range of management accounting methodsis wider.

These hypotheses were formulated on the basis of direct observations andinformation obtained in the course of work in teams engaged in designing man-agement information systems for enterprises, as well as from interviews conductedwith practitioners—participants of postgraduate studies and training courses inmanagement accounting.

The results and findings of the survey presented in this paper do not apply to allcompanies operating in Poland, because the companies surveyed were not selectedas a random sample and their number was not large, and thus the sample is notsufficiently representative. However, this research is a starting point for furtherinvestigations and analysis.

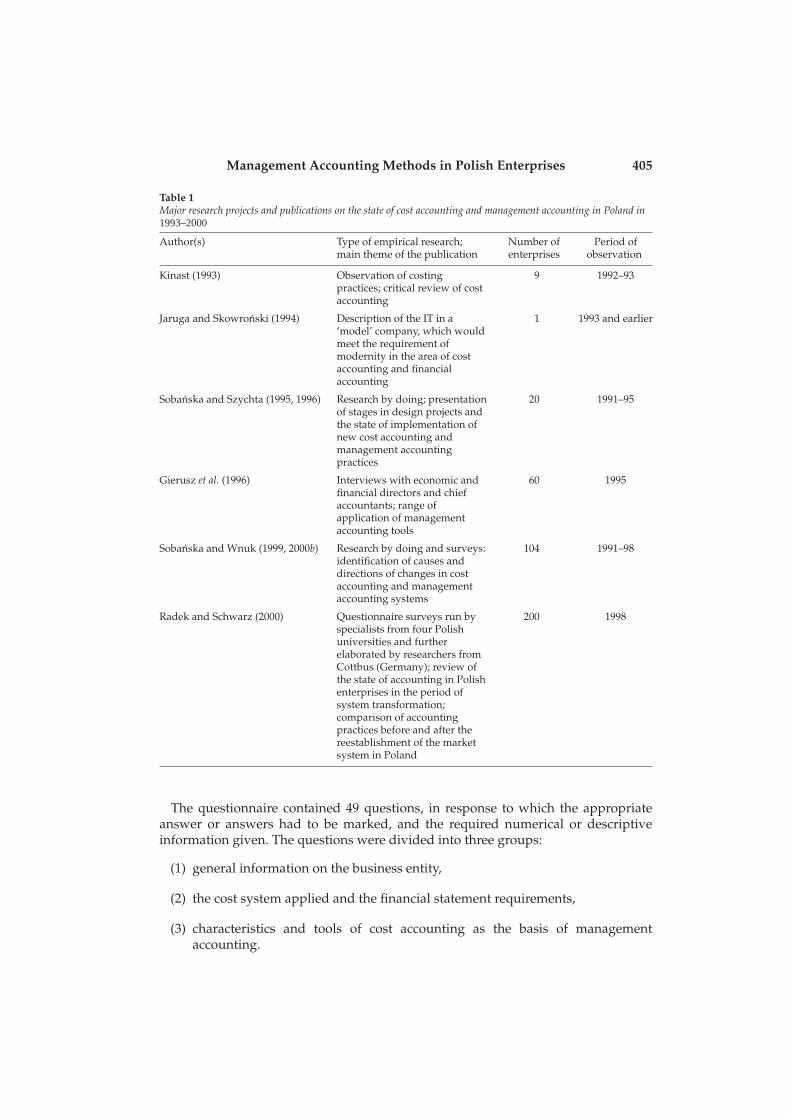

2. Earlier research in this area

In the 1990s and in 2000 there were several publications dealing with the state,causes and directions of changes in cost accounting and with the developmentof management accounting in Polish business practice. The type and scope of theempirical research was different in the case of each of the publications presented inTable 1.

3. Research methodology

The information presented in this paper was obtained by means of:

(1) questionnaires circulated by post or personally to 290 companies in the centraland southern part of the country,

(2) direct interviews carried out by the author with employees of nine largecompanies and documentation obtained in the course of work in teams whichcarried out analysis and assessment of cost accounting practices and designedmanagement accounting systems for these companies.

The survey was conducted from November 1998 to December 1999. Out of 290questionnaires delivered to the enterprises 62 were returned, but 2 were rejectedbecause of incomplete and—in the author’s opinion—unreliable answers. Eventually60 questionnaires (20.7%) were analysed. It turned out to be very difficult to get backcompleted inquiry forms and in the majority of successful cases repeated requests fortheir return were necessary.

Management Accounting Methods in Polish Enterprises 405

Table 1Major research projects and publications on the state of cost accounting and management accounting in Poland in1993–2000

Author(s) Type of empirical research;main theme of the publication

Number ofenterprises

Period ofobservation

Kinast (1993) Observation of costingpractices; critical review of costaccounting

9 1992–93

Jaruga and Skowronski (1994) Description of the IT in a‘model’ company, which wouldmeet the requirement ofmodernity in the area of costaccounting and financialaccounting

1 1993 and earlier

Sobanska and Szychta (1995, 1996) Research by doing; presentationof stages in design projects andthe state of implementation ofnew cost accounting andmanagement accountingpractices

20 1991–95

Gierusz et al. (1996) Interviews with economic andfinancial directors and chiefaccountants; range ofapplication of managementaccounting tools

60 1995

Sobanska and Wnuk (1999, 2000b) Research by doing and surveys:identification of causes anddirections of changes in costaccounting and managementaccounting systems

104 1991–98

Radek and Schwarz (2000) Questionnaire surveys run byspecialists from four Polishuniversities and furtherelaborated by researchers fromCottbus (Germany); review ofthe state of accounting in Polishenterprises in the period ofsystem transformation;comparison of accountingpractices before and after thereestablishment of the marketsystem in Poland

200 1998

The questionnaire contained 49 questions, in response to which the appropriateanswer or answers had to be marked, and the required numerical or descriptiveinformation given. The questions were divided into three groups:

(1) general information on the business entity,

(2) the cost system applied and the financial statement requirements,

(3) characteristics and tools of cost accounting as the basis of managementaccounting.

406 A. Szychta

Table 2Average annual level of employment

Number of Under 50 51–100 101–500 501–1000 1001–2000 Over 2000 Totalemployees

Number (per cent) 9 8 19 9 9 6 60of surveyed (15%) (13.3%) (31.7%) (15%) (15%) (10%) (100%)enterprises

17 43 60(28.3%) (71.7%) (100%)

This paper uses mainly the information obtained from the first and third part of thequestionnaire. The survey did not address the question of performance measurementby financial and non-financial measures because of its wide scope.

4. Presentation and analysis of research findings

4.1. Description of business entities covered by the surveyOn the basis of the information received the companies may be classed according tothe following criteria:

• company size measured by the number of employees, value of assets and salesrevenues,

• line of business and type of activity,• organizational and legal form of business,• source of equity.

The companies covered by the survey are dominated by entities which employ over100 persons (71.7%), that is large and medium companies (see Table 2). 15 companiesemployed over 1000 people (25%).

All the enterprises have been classified into small and large on the basis of thefollowing criteria, as set out in the Polish Accounting Act of 29 September 1994(art. 50) and according to the wording in force at the end of 2001 (that is, before itsamendment on 9 November 2000):

(1) average annual employment—50 persons,

(2) sum of the balance sheet assets at the end of the financial year—equivalent to1 million euros,

(3) net revenues from sale of goods and products and from financial operations—equivalent to 2 million euros.

If a company fulfils at least two of these three criteria, it is classified as large;if it does not fulfil two of these three criteria, it is included in the group of smallenterprises. 49 companies (81.7%) have been classed as large, and 11 (18.3%) makeup the group of small companies.

Large entities are manufacturing and service enterprises. The group of smallentities comprises mainly trade companies. Classification of companies by sector andline of business is presented in Table 3.

Management Accounting Methods in Polish Enterprises 407

Table 3Classification of companies by sector and line of business

Sector Line of business

Production 38 (63.4%) Electrical industry 12 (20%)Metal industry 5 (8.3%)Textiles and clothing 5 (8.3%)Chemicals and pharmaceuticals 4 (6.7%)Power stations 2 (3.3%)Various industrial branches 10 (16.7%)

Trade 11 (18.3%) Distribution and trade inelectrical energy and gas

3 (5%)

Sale of building materials,machines, equipment andclothing

8 (13.3%)

Services 11 (18.3%) Various services (installation,repairs, renting, IT)

11 (18.3%)

Total 60 (100%) Total 60 (100%)

Table 4Ownership forms of the surveyed companies

Organizational and legal form Number and per cent of companies

Joint-stock company 18 (30%)Limited liability company 18 (30%) Commercial

companies46 (76.6%)

Another form of commercialcompany

2 (3.3%)

One-person State Treasurycompany (joint-stock company)

8 (13.3%)

State or municipal enterprise 7 (11.7%)Ordinary partnership and soleproprietorship

7 (11.7%)

Total 60 (100%)

The majority of the surveyed enterprises, that is 46 (see Table 4), are commercialcompanies (76.7%), which include 8 (13.3%) one-person State Treasury companies.Among the enterprises surveyed are seven state-owned enterprises and seven in theform of ordinary partnership or sole proprietorship.

The equity capital in 47 of the surveyed companies is entirely from domesticsources, in seven companies it is from foreign sources, and in six companies it isboth domestic and foreign capital.

Nearly one-half of the enterprises (29) sell their products and goods on the homemarket; the remainder (31) sell both at home and abroad. For 12 companies inthe latter group export revenues account for 40 per cent or more of the total salesrevenues.

408 A. Szychta

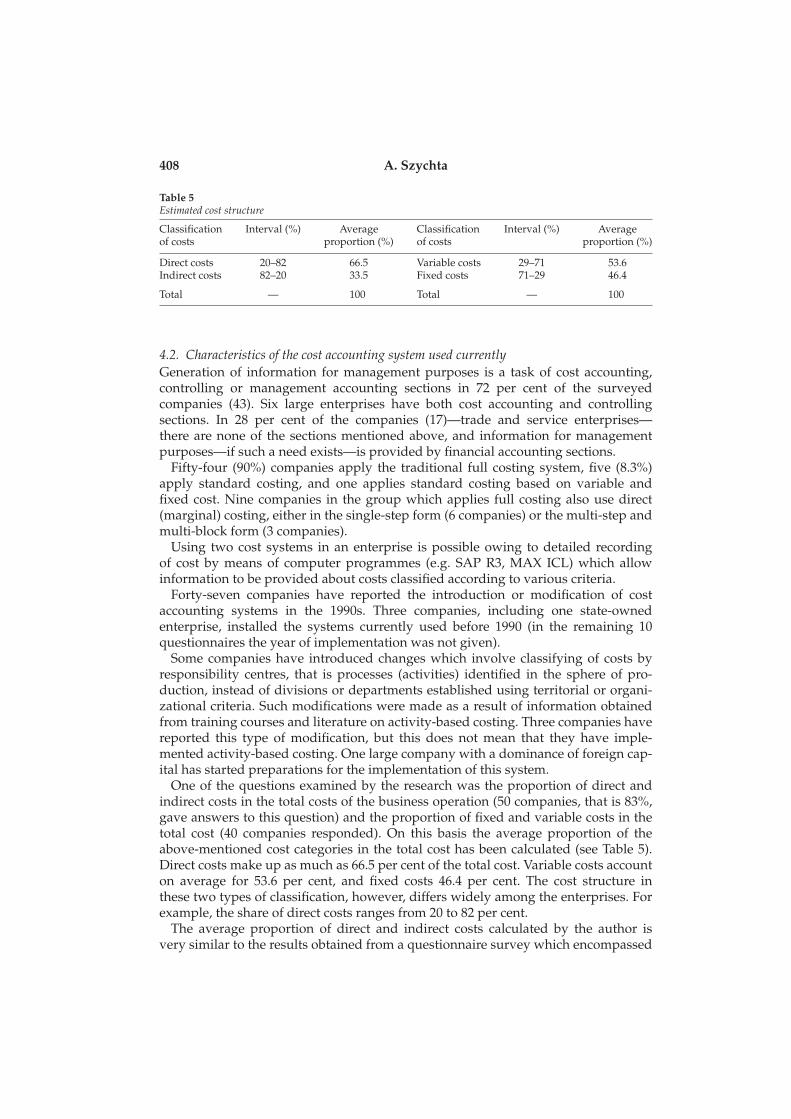

Table 5Estimated cost structure

Classification Interval (%) Average Classification Interval (%) Averageof costs proportion (%) of costs proportion (%)

Direct costs 20–82 66.5 Variable costs 29–71 53.6Indirect costs 82–20 33.5 Fixed costs 71–29 46.4

Total — 100 Total — 100

4.2. Characteristics of the cost accounting system used currentlyGeneration of information for management purposes is a task of cost accounting,controlling or management accounting sections in 72 per cent of the surveyedcompanies (43). Six large enterprises have both cost accounting and controllingsections. In 28 per cent of the companies (17)—trade and service enterprises—there are none of the sections mentioned above, and information for managementpurposes—if such a need exists—is provided by financial accounting sections.

Fifty-four (90%) companies apply the traditional full costing system, five (8.3%)apply standard costing, and one applies standard costing based on variable andfixed cost. Nine companies in the group which applies full costing also use direct(marginal) costing, either in the single-step form (6 companies) or the multi-step andmulti-block form (3 companies).

Using two cost systems in an enterprise is possible owing to detailed recordingof cost by means of computer programmes (e.g. SAP R3, MAX ICL) which allowinformation to be provided about costs classified according to various criteria.

Forty-seven companies have reported the introduction or modification of costaccounting systems in the 1990s. Three companies, including one state-ownedenterprise, installed the systems currently used before 1990 (in the remaining 10questionnaires the year of implementation was not given).

Some companies have introduced changes which involve classifying of costs byresponsibility centres, that is processes (activities) identified in the sphere of pro-duction, instead of divisions or departments established using territorial or organi-zational criteria. Such modifications were made as a result of information obtainedfrom training courses and literature on activity-based costing. Three companies havereported this type of modification, but this does not mean that they have imple-mented activity-based costing. One large company with a dominance of foreign cap-ital has started preparations for the implementation of this system.

One of the questions examined by the research was the proportion of direct andindirect costs in the total costs of the business operation (50 companies, that is 83%,gave answers to this question) and the proportion of fixed and variable costs in thetotal cost (40 companies responded). On this basis the average proportion of theabove-mentioned cost categories in the total cost has been calculated (see Table 5).Direct costs make up as much as 66.5 per cent of the total cost. Variable costs accounton average for 53.6 per cent, and fixed costs 46.4 per cent. The cost structure inthese two types of classification, however, differs widely among the enterprises. Forexample, the share of direct costs ranges from 20 to 82 per cent.

The average proportion of direct and indirect costs calculated by the author isvery similar to the results obtained from a questionnaire survey which encompassed

Management Accounting Methods in Polish Enterprises 409

200 enterprises in Poland (Radek and Schwarz, 2000, p. 69). According to thatstudy, the average proportion of direct costs is 64.3 per cent, and of indirect costs(manufacturing overhead costs, administrative and selling costs), 35.7 per cent.

The average figures for the variable costs (53.6%) and fixed costs (46.4%), however,differ considerably from those obtained by Radek and Schwarz—67.6 and 32.4 percent respectively.

The survey has shown that in more than one-half of the companies (34) the variableand fixed costs are estimated for the purposes of short-term decision-making. In32 cases the account analysis method is used; in one case the high–low method isused and in another case graphical trend estimation is used. None of the surveyedcompanies use statistical methods for determining the proportion of variable andfixed costs.

The break-even point is estimated in 28 companies (47%): in 18 cases for thecompany as a whole, and in 10 cases for individual divisions as well as the wholecompany.

Twenty-eight per cent of the 60 surveyed companies (17 cases) apply full recordingand repartition of costs; that is grouping of costs by nature, responsibility centreand object. 48.3 per cent of the companies (29) classify costs by nature and byresponsibility centre. Comprehensive cost records are therefore kept in about 66 percent of the enterprises. Simplified systems, where costs are classified only by nature,are applied in 20 per cent of the companies (12), and only by responsibility centre intwo companies. Simplified cost classification is adopted by small entities operatingin wholesale trades or services.

The profit and loss account with a classification of expenses by nature (comparativeformat) is prepared by two-thirds of the companies, while the other variant—calculation format (showing the cost of sales, distribution costs and administrationcosts)—is used by one-third.

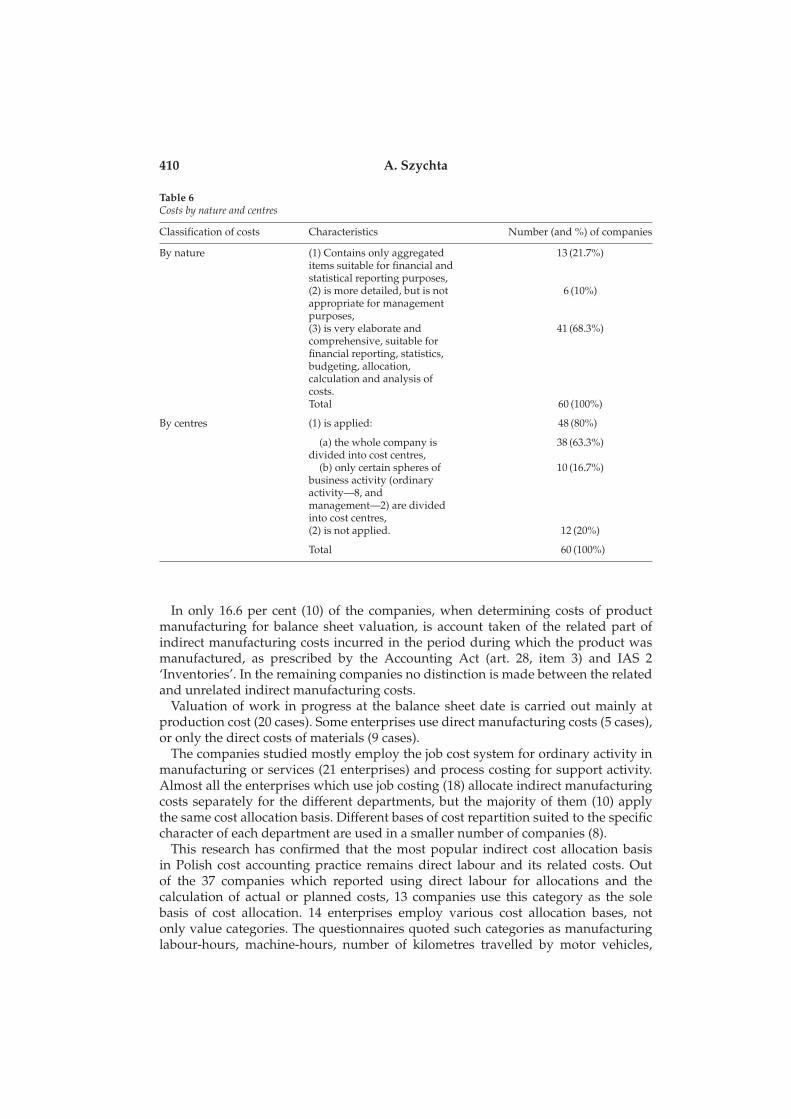

Detailed characteristics of cost classification by nature and by centre are presentedin Table 6. In 68 per cent of the companies the classification of costs by nature isvery detailed, suited to the specific character of the business entity, managementinformation needs and requirements concerning financial statements, as prescribedby the Accounting Act (comparative format of profit and loss account, and notes tothe financial statements). In the rest of the companies the structure of costs by typeis very synthetic or detailed, but it is not appropriate for management informationneeds.

In 80 per cent of the surveyed companies (48) costs are allocated to cost centres, butonly in about 63 per cent of cases are cost centres established for ordinary activity,auxiliary activity, administration and management. In the rest of the companies costcentres are mainly in the sphere of ordinary activity—manufacturing or services.

Costs are not classified by centre in small enterprises, operating in trade orservices (12).

4.3. Calculation of costs and pricesCalculation of costs of manufactured products is done in about 72 per cent of thesurveyed companies (43): in about 50 per cent of this group (31) at the end of eachmonth; in eight companies at the end of a quarter; in two, twice a year; and in two, atthe end of the financial year. The actual costs of product manufacturing are calculatedonce a month in large manufacturing enterprises.

410 A. Szychta

Table 6Costs by nature and centres

Classification of costs Characteristics Number (and %) of companies

By nature (1) Contains only aggregateditems suitable for financial andstatistical reporting purposes,

13 (21.7%)

(2) is more detailed, but is notappropriate for managementpurposes,

6 (10%)

(3) is very elaborate andcomprehensive, suitable forfinancial reporting, statistics,budgeting, allocation,calculation and analysis ofcosts.

41 (68.3%)

Total 60 (100%)

By centres (1) is applied: 48 (80%)

(a) the whole company isdivided into cost centres,

38 (63.3%)

(b) only certain spheres ofbusiness activity (ordinaryactivity—8, andmanagement—2) are dividedinto cost centres,

10 (16.7%)

(2) is not applied. 12 (20%)

Total 60 (100%)

In only 16.6 per cent (10) of the companies, when determining costs of productmanufacturing for balance sheet valuation, is account taken of the related part ofindirect manufacturing costs incurred in the period during which the product wasmanufactured, as prescribed by the Accounting Act (art. 28, item 3) and IAS 2‘Inventories’. In the remaining companies no distinction is made between the relatedand unrelated indirect manufacturing costs.

Valuation of work in progress at the balance sheet date is carried out mainly atproduction cost (20 cases). Some enterprises use direct manufacturing costs (5 cases),or only the direct costs of materials (9 cases).

The companies studied mostly employ the job cost system for ordinary activity inmanufacturing or services (21 enterprises) and process costing for support activity.Almost all the enterprises which use job costing (18) allocate indirect manufacturingcosts separately for the different departments, but the majority of them (10) applythe same cost allocation basis. Different bases of cost repartition suited to the specificcharacter of each department are used in a smaller number of companies (8).

This research has confirmed that the most popular indirect cost allocation basisin Polish cost accounting practice remains direct labour and its related costs. Outof the 37 companies which reported using direct labour for allocations and thecalculation of actual or planned costs, 13 companies use this category as the solebasis of cost allocation. 14 enterprises employ various cost allocation bases, notonly value categories. The questionnaires quoted such categories as manufacturinglabour-hours, machine-hours, number of kilometres travelled by motor vehicles,

Management Accounting Methods in Polish Enterprises 411

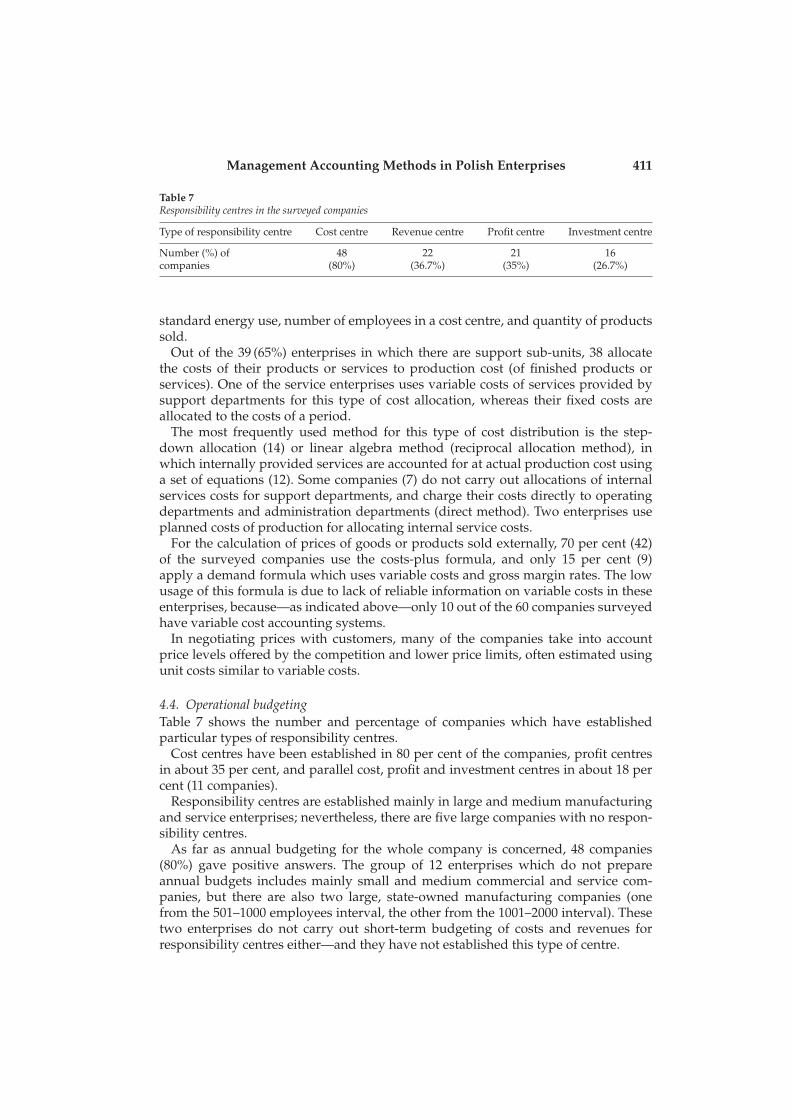

Table 7Responsibility centres in the surveyed companies

Type of responsibility centre Cost centre Revenue centre Profit centre Investment centre

Number (%) of 48 22 21 16companies (80%) (36.7%) (35%) (26.7%)

standard energy use, number of employees in a cost centre, and quantity of productssold.

Out of the 39 (65%) enterprises in which there are support sub-units, 38 allocatethe costs of their products or services to production cost (of finished products orservices). One of the service enterprises uses variable costs of services provided bysupport departments for this type of cost allocation, whereas their fixed costs areallocated to the costs of a period.

The most frequently used method for this type of cost distribution is the step-down allocation (14) or linear algebra method (reciprocal allocation method), inwhich internally provided services are accounted for at actual production cost usinga set of equations (12). Some companies (7) do not carry out allocations of internalservices costs for support departments, and charge their costs directly to operatingdepartments and administration departments (direct method). Two enterprises useplanned costs of production for allocating internal service costs.

For the calculation of prices of goods or products sold externally, 70 per cent (42)of the surveyed companies use the costs-plus formula, and only 15 per cent (9)apply a demand formula which uses variable costs and gross margin rates. The lowusage of this formula is due to lack of reliable information on variable costs in theseenterprises, because—as indicated above—only 10 out of the 60 companies surveyedhave variable cost accounting systems.

In negotiating prices with customers, many of the companies take into accountprice levels offered by the competition and lower price limits, often estimated usingunit costs similar to variable costs.

4.4. Operational budgetingTable 7 shows the number and percentage of companies which have establishedparticular types of responsibility centres.

Cost centres have been established in 80 per cent of the companies, profit centresin about 35 per cent, and parallel cost, profit and investment centres in about 18 percent (11 companies).

Responsibility centres are established mainly in large and medium manufacturingand service enterprises; nevertheless, there are five large companies with no respon-sibility centres.

As far as annual budgeting for the whole company is concerned, 48 companies(80%) gave positive answers. The group of 12 enterprises which do not prepareannual budgets includes mainly small and medium commercial and service com-panies, but there are also two large, state-owned manufacturing companies (onefrom the 501–1000 employees interval, the other from the 1001–2000 interval). Thesetwo enterprises do not carry out short-term budgeting of costs and revenues forresponsibility centres either—and they have not established this type of centre.

412 A. Szychta

The range of annual budgets which make up the master budget is different inparticular companies. About 17 per cent of the companies (10) prepare a full set ofoperating and financial budgets. The remaining companies which stated that theyemploy annual budgeting prepare at least two or three operating budgets, e.g. salesbudget, production budget, and pro-forma financial statements.

Cost budgeting for cost centres is done in 31 companies. Most of them preparebudgets for responsibility centres in the sphere of production, administration andmanagement. Several companies prepare budgets only for cost centres in productionor administration and management.

According to answers given in the questionnaires, 22 companies apply the incre-mental method of budgeting, and 17 use zero-based budgeting. In the rest of thequestionnaires the method of budgeting was not specified.

However, it seems unlikely that 17 companies in the group of 48 enterpriseswhich prepare budgets apply the zero-based budgeting method. On the basis ofmy direct cooperation with a dozen or so enterprises and numerous interviewswith participants of postgraduate studies and training courses I would estimate thisproportion to be much lower.

Twenty-one companies stated that they prepare flexible budgets, and 16, that theyuse fixed budgets.

Internal reports, which compare actual and planned figures and analyse variances,are prepared in 43 out of the 48 companies which budget their operations. Over 80per cent of these companies (39) prepare monthly reports on budget execution, whilethe rest do it at the end of a quarter. More than one-half of the surveyed companiesdistinguish controllable costs for the purpose of assessment and motivation of costcentre managers.

4.5. Long-term planning and appraisal of investment efficiencyThe situation with regard to long-term planning in the reviewed companies isworse than in the case of short-term budgeting, because long-term budgets spanning3–5 years are prepared by only 60 per cent of the companies. More specifically, 36companies (60%) have business plans, 34 companies (about 57%) prepare investmentexpenditures plans, and 13 companies (about 22%) have R&D plans.

These types of plans are mainly prepared by large manufacturing and servicecompanies. Only a few per cent of small companies have business plans.

The methods of investment appraisal for capital projects used in the analysedcompanies are shown in Table 8. Only 35–40 per cent apply simple measures, such asROI and the payback period. Discounted cash-flow methods of appraisal are used toan even lesser extent (see Table 8).

4.6. Present state and future development trends in the respondents’ opinionThe respondents mentioned various specific factors which have initiated the changescarried out in cost accounting systems and contributed to the introduction of newmanagement accounting techniques in their enterprises. These factors include:

— need to improve financial results,— seeking to recover lost markets,— need to reduce operating costs,— demands by a new owner to implement new methods of management and

Management Accounting Methods in Polish Enterprises 413

Table 8The use of methods of investment appraisal

Method Number and % of the survey companies

ROI 21 (35%)Payback period 24 (40%)Net present value (NPV) 18 (30%)Internal rate of return (IRR) 15 (25%)NPV sensitivity analysis 9 (15%)

accounting,— application of integrated computer programmes,— need to obtain information relevant to decision-making.

The appearance or intensification of these factors in Polish enterprises was doubt-less possible due to ownership changes taking place since the early 1990s, consistingof privatization of state-owned enterprises and setting up of new business entities inthe form of commercial companies. The process of systemic change involves growingcompetition on the domestic market. Ownership changes and increased competitionmay be regarded as primary causes of the recent modifications of cost accountingsystems and the implementation of management accounting methods in Polish enter-prises.

The questionnaire survey has not examined the importance attached by practition-ers to the role played by each of the factors listed above in stimulating accountingchange in their enterprises. However, research carried out by Sobanska and Wnuk(2000a, p. 76) indicates that ‘for 35 per cent of the respondents the main cause of intro-ducing changes in cost accounting and management accounting was implementationof sophisticated IT tools (MRP, MRP II, ERP). Next comes the growing competition(24%), and then ownership changes (17%), introduction of ISO 9000 standards (6%)and implementation of advanced information technologies’.

The findings of a questionnaire survey prepared by Radek and Schwarz (2000,p. 76) suggest that among factors which had a major impact on managementaccounting in Polish enterprises are customer demands and preferences and moderncomputer systems (3.5 points each against maximum 5 points). A surprisingly lowimportance was found to be attached to ownership changes and foreign investors(1.7 points).

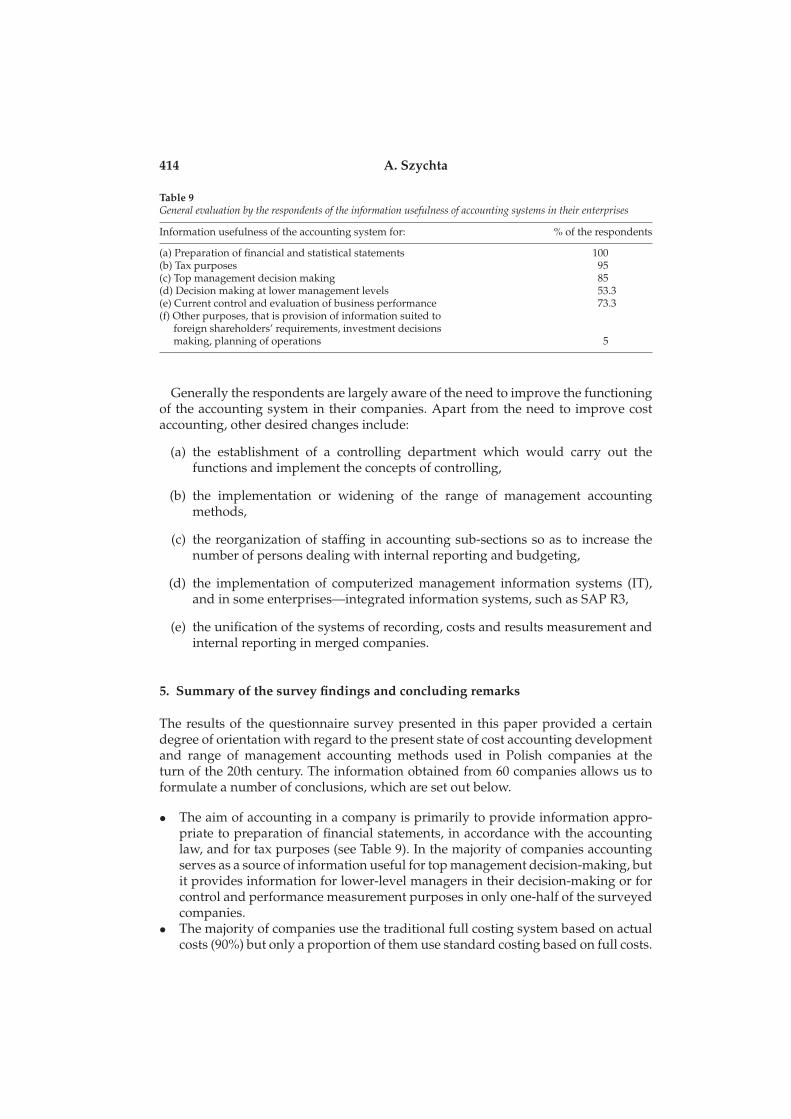

It is interesting to learn, after analysing the answers given in the returned question-naires, how respondents evaluate the overall usefulness of the accounting IT in theirenterprises. The results are presented in Table 9.

To the question whether any changes to the cost accounting system are plannedin the enterprise, 40 per cent of the respondents gave a positive answer. Theexisting system is to be replaced by variable costing in 10 cases (17%), activity-basedcosting in 8 (15%) and standard costing in four (8%). Several other companies areplanning to modify cost recording in the costing system presently in use and todevelop their analyses of variances between actual and planned costs. However, itis only the large manufacturing companies which intend to introduce changes ormodifications.

414 A. Szychta

Table 9General evaluation by the respondents of the information usefulness of accounting systems in their enterprises

Information usefulness of the accounting system for: % of the respondents

(a) Preparation of financial and statistical statements 100(b) Tax purposes 95(c) Top management decision making 85(d) Decision making at lower management levels 53.3(e) Current control and evaluation of business performance 73.3(f) Other purposes, that is provision of information suited to

foreign shareholders’ requirements, investment decisionsmaking, planning of operations 5

Generally the respondents are largely aware of the need to improve the functioningof the accounting system in their companies. Apart from the need to improve costaccounting, other desired changes include:

(a) the establishment of a controlling department which would carry out thefunctions and implement the concepts of controlling,

(b) the implementation or widening of the range of management accountingmethods,

(c) the reorganization of staffing in accounting sub-sections so as to increase thenumber of persons dealing with internal reporting and budgeting,

(d) the implementation of computerized management information systems (IT),and in some enterprises—integrated information systems, such as SAP R3,

(e) the unification of the systems of recording, costs and results measurement andinternal reporting in merged companies.

5. Summary of the survey findings and concluding remarks

The results of the questionnaire survey presented in this paper provided a certaindegree of orientation with regard to the present state of cost accounting developmentand range of management accounting methods used in Polish companies at theturn of the 20th century. The information obtained from 60 companies allows us toformulate a number of conclusions, which are set out below.

• The aim of accounting in a company is primarily to provide information appro-priate to preparation of financial statements, in accordance with the accountinglaw, and for tax purposes (see Table 9). In the majority of companies accountingserves as a source of information useful for top management decision-making, butit provides information for lower-level managers in their decision-making or forcontrol and performance measurement purposes in only one-half of the surveyedcompanies.

• The majority of companies use the traditional full costing system based on actualcosts (90%) but only a proportion of them use standard costing based on full costs.

Management Accounting Methods in Polish Enterprises 415

Modifications of these systems in the 1990s were mainly in the area of recordingcosts by nature and by cost centre.

• About 15 per cent of the companies generate information on variable and fixedcosts using direct costing. In some of them this system functions in parallel withfull (absorption) costing, or in a mixed form: that is, it uses the ideas of both fulland direct costing.

• Data on variable costs of products and fixed costs of enterprises for short-termdecisions are estimated using the account analysis method in more than one-half of the examined enterprises. Mathematical and statistical methods (high–lowmethod or regression analysis method) are used to a very small degree.

• Break-even points are calculated by simple methods for the whole companyin about 47 per cent of enterprises. The break-even points for divisions of theenterprise and the product range are determined only in rare cases.

• The most widely used method of calculating unit cost of products and services isjob costing, in which indirect manufacturing costs by production departments areallocated to product, chiefly on the basis of direct labour costs.

• Costs of services provided by support departments are accounted for on thebasis of actual manufacturing cost using the step-down allocation method or thereciprocal allocation method. There are also cases when reciprocal allocation ofinternal services of support departments are not taken into account.

• The most popular method used by Polish companies for product price determina-tion is the cost plus formula (70%). This is due to the nature of data available fromfull costing systems and the strong reliance of many practitioners on this method.

• Annual operating financial budgets for the whole enterprise are prepared by aconsiderable proportion of the companies studied, mainly large manufacturingand service enterprises (80% of the respondents). However, a complete or nearlycomplete master budget is prepared by a much smaller proportion of enterprises(17%). The remaining enterprises prepare varying numbers of componentbudgets, mainly sales, production and cost budgets. Budgeting is not applied insmall trade and service companies, nor in some large state enterprises. About50 per cent of the surveyed companies use cost centre budgets for managementpurposes.

• Long-term planning, mainly in the form of business plans and investmentexpenditure plans, is done in about 60 per cent of the surveyed companies. Butmany fewer companies apply the methods of investment appraisal proposed inaccounting literature, especially the discounted cash-flow methods (25–30%).

• The intensity and scope of cost accounting modification and the implementationof management accounting tools in Polish enterprises are far from satisfactory.This is confirmed by the survey findings as well as by the observations of authorsin the course of their field work (e.g. Sobanska and Wnuk, 1999, 2000b; Radek andSchwarz, 2000; Dyhdalewicz, 2001). The development of management accountingin business entities is still obstructed by numerous barriers: behavioural, financialand technological. Full discussion of these issues is provided by Sobanska andWnuk (2000b, pp. 218, 219).

• In order to speed up the development of management accounting systems inPolish enterprises, the following measures need to be taken:

— acquisition by managers and accounting department employees of knowledge

416 A. Szychta

about the principles and advantages of the new systems of cost accountingand methods of strategic management accounting;

— establishment in enterprises of departments, or the appointment of per-sons, responsible for the implementation and subsequent application ofmanagement accounting and controlling methods and techniques;

— implementation of modern integrated IT systems, which are useful formanagement accounting purposes;

— raising the status of management accountants in Poland.

Finally, the information provided by the questionnaire survey allows the author toverify, to varying degrees, the hypotheses formulated at the beginning of this paper.

Detailed analysis of the survey findings and its general conclusions make it possi-ble to confirm the three hypotheses, with a high degree of confidence. Specifically:

— since the early 1990s Polish companies have been implementing methods andtechniques of operational management accounting;

— short-term budgeting, in the form of master budgets and budgets for individualresponsibility centres, is the most widely used method of accounting for theeffects of economic resources management and for cost reduction;

— in large enterprises, which are commercial companies, management accountingmethods are used to a greater extent than in smaller companies.

However, the returned questionnaires made it difficult to verify the hypothesis thatincreased competition and ownership changes in Polish enterprises are the main fac-tors which cause changes in cost and management accounting in Polish companies.These changes are induced by many specific factors, as has been confirmed by theresults of questionnaire surveys carried out by other authors. However, most of thesefactors could come into play due to the ownership changes which are still in progressand the growing competition in Poland.

This issue will be further investigated in subsequent research, in which I intend tocover a much larger number of medium-sized and large enterprises in Poland and toexamine the relationship between financial and non-financial results of their businessactivity and the range and level of management accounting techniques which havebeen implemented in these companies.

References

Binkowski, B., 1964. Metody rozliczania kosztów posrednich produkcji (Methods of ManufacturingOverhead Costs Allocation), Warszawa, PWE.

Dyhdalewicz, A., 2001. Wykorzystanie rachunku kosztów w zarzadzaniu przedsiebiorst-wem—wyniki badan (Application of cost accounting in enterprise management—Resultsof research), Zarzadzanie kosztami w przedsiebiorstwach w aspekcie integracji Polski z UniaEuropejska, Prace Wydziału Zarzadzania Politechniki Czestochowskiej, Czestochowa, 33–38.

Fedak, Z., 1962. Rachunek kosztów produkcji przemysłowej, (Cost Accounting for IndustrialProduction), Warszawa, PWE.

Gierusz, J., Kujawski, A. and Kujawski, L., 1996. Stan obecny oraz kierunki ewolucji rachunkukosztów i rachunkowosci zarzadczej w przedsiebiorstwach Polski północnej, Current stateand development directions of cost accounting and management accounting in enterprisesof northern Poland, Zeszyty Teoretyczne Rady Naukowej, SKwP, Warszawa, 41–47.

Management Accounting Methods in Polish Enterprises 417

Jaruga, A., 1966. Koszty zarzadzania przedsiebiorstw przemysłowych, (Management Cost ofManufacturing Enterprises), Warszawa, PWE.

Jaruga, A., 1972. Koszty posrednie w przedsiebiorstwach przemysłowych (Indirect Costs inManufacturing Companies), Warszawa, PWE.

Jaruga, A., 1986. Rachunek kosztów w zarzadzaniu przedsiebiorstwem (Cost Accounting inEnterprise Management), Warszawa, PWE.

Jaruga, A., Malc, W. and Sawicki, K., 1990. Rachunek kosztów (Cost Accounting), 1st edition 1979,2nd edition 1982, 3rd edition, Warszawa, PWE.

Jaruga, A., Nowak, W. A. and Szychta, A., 1999. Rachunkowosc zarzadcza. Koncepcje izastosowania (Management Accounting. Concepts and Applications), Łódz, Absolwent, 861.

Jaruga, A. and Skowronski, J., Rachunek kosztów w systemie informacyjnym przedsiebio-rstwa (Cost Accounting in an Enterprise Information System), 1st edition 1975, 2nd edition 1982,3rd edition changed 1986, Warszawa, PWE.

Jaruga, A. and Skowronski, J., 1994. O wierny obraz rachunku kosztów, (Towards a fair viewof cost accounting), Rachunkowosc.

Jaruga, A., Sobanska, I. and Szychta, A., 1994. Rachunkowosc dla menedzerów (The Accounting forManagers), 1st edition 1992, 2nd edition, £ódz, RaFiB.

Jaruga, A. and Szychta, A., 1997. The origin and evolution of charts of accounts in Poland,European Accounting Review, 6, 509–526.

Kinast, A., 1993. Modernizacja rachunku kosztów, (Modernisation of cost accounting),Rachunkowosc, 299–302.

Malc, W., 1963. Rachunek kosztów postulowanych w przedsiebiorstwie przemysłowym (Pos-tulated Costing in a Manufacturing Enterprise), Warszawa, PWE.

Radek, M. and Schwarz, R., 2000. Zmiany w rachunkowosci zarzadczej w polskich przed-siebiorstwach w okresie transformacji systemu gospodarczego (na podstawie badanempirycznych), (Changes in management accounting in Polish enterprises during eco-nomic transition (on the basis of empirical research)), Zeszyty Teoretyczne Rachunkwosci, tom1(57), SKwP, Warszawa, 58–83

Siwon, B., 1972. Współczesne tendencje rozwoju rachunku kosztów i wyników (ContemporaryTrends in Cost Accounting Development), Warszawa, PWE.

Rozporzadzenie Ministra Finansów, 1991. z dn. 15 stycznia 1991r. w sprawie zasadprowadzenia rachunkowosci, (Decree of the Minister of Finance of 15 January 1991 on thePrinciples of Accounting), Dziennik Ustaw, 1991, No. 10 and 1992, No. 96.

Sobanska, I. and Szychta, A., 1995. Management Accounting in Polish Companies in thePeriod of Structural Transformations, paper at the 18th Annual Congress of EAA, Birm-ingham, 10–12 May.

Sobanska, I. and Szychta, A., 1996. Projektowanie systemów rachunkowosci zarzadczej.Uwarunkowania i mozliwosci, (Designing of management accounting systems. Condi-tions and opportunities), Rachunkowosc zarzadcza w teorii i praktyce, Akademia Ekonomicznaim, Katowice, Karola Adamieckiego, 111–122.

Sobanska, I. and Wnuk, T., 1999. The Development of Management Accounting in Enter-prises Operating in Poland in the 1990s, paper at the Conference Accounting and Audit:Problems of Development, Riga, Latvian University Press, January, 217–221.

Sobanska, I. and Wnuk, T., 2000a. Causes and Directions of Changes in Management Account-ing Practice in Poland, paper at the Conference on Economics & Management—2000: Actu-alities and Methodology, Kowno, May.

Sobanska, I. and Wnuk, T., 2000b. Zmiany w praktyce rachunkowosci na przełomie XXi XXI wieku (Changes in accounting practice at the turn of the 20th century), ZeszytyTeoretyczne Rady Naukowej, 215–221. SKwP, Warszawa.

Tendera, P. and Woznica, W., 1974. Rachunek kosztów normatywnych w przedsiebiorstwiewielowydziałowym (Standard Costing in Multidivisional Enterprise), Warszawa, PWE.

418 A. Szychta

Ustawa z dn. 29.09.1991 o rachunkowosci, (Act on Accounting, 29 September 1991), DziennikUstaw 1991, No. 121 and later amendments.

Wytyczne w sprawie zasad rachunku kosztów produkcji przemysłowej, przedsiebiorstwpanstwowych. Załacznik nr 1 Przewodniczacego Komisji Planowania przy Radzie Min-istrów i Ministerstwa Finansów z dn. 2.02.1968r, (Guidelines on the Principles of CostAccounting for State Manufacturing Enterprises of 2.02.1968).

Zarzadzenie Nr 83, Ministra Finansów z 7.11.1983r. w sprawie zasad ewidencji, kalkulacjii analizy kosztów produkcji przemysłowej, (Order No. 83 of the Minister of Finance of7 November 1983 on the Principles of Recording, Calculation and Analysis of IndustrialProduction Costs).