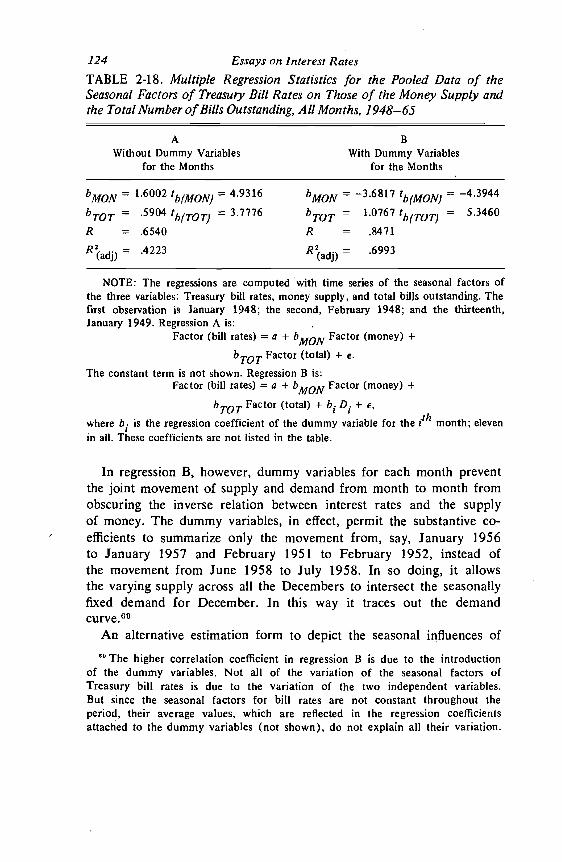

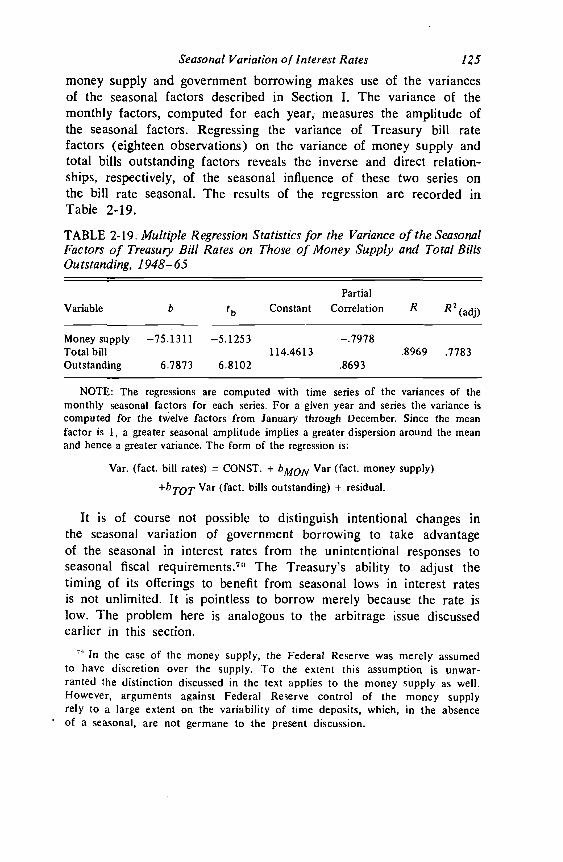

the seasonal variation of interest rates - national bureau of

TRANSCRIPT

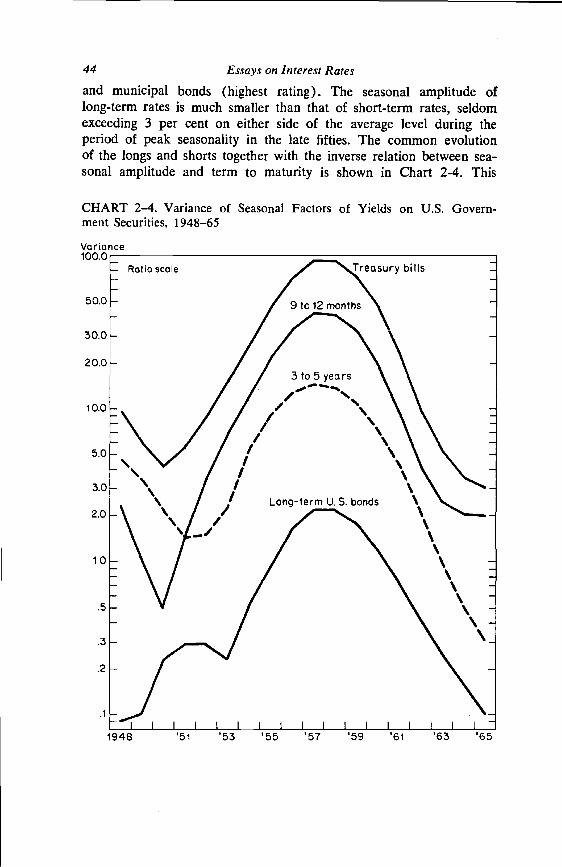

52 Essays on Interest Rates

Stable Seasonal Factors

Estimated stable seasonal factors are defined as the mean value ofthe SI ratios for each month. They are called stable or constantbecause they are computed once for the entire sample period. Anydeviation of the SI ratios computed for a given month from thefactor computed for that month is attributed to the irregular com-ponent. In other words, the SI ratios consist of a systematic and arandom component called, respectively, the seasonal and the irregularcomponents. Since the irregular component, expressed as a fractionof the seasonal component, is defined to vary with equal likelihoodabove and below the seasonal component, its ratio to the seasonalcomponent is on average equal to 1. (In the additive case the meanof the irregular component is zero.) Therefore, the mean SI ratio,say for January, is equal to the seasonal component, assumed to bea constant, multiplied by 1. In the absence of seasonality the meanSI ratios would not differ significantly from each other or from 1.

A simple test for the presence of stable seasonality is thereforeto determine the statistical significance of the differences among thecomputed mean SI ratios for each month. The test is a one-wayanalysis of variance of the monthly SI ratios, twelve columns of themfor the twelve months, and the number of rows equalling the numberof annual observations.18 The F-statistic, computed for N full years,is equal to

N times variance of monthly meanstotal variance minus N times variance of monthly means

Except for the graphic method of fitting smooth curves to SIratios of a given month over the years most of the earlier methodsand many of those used currently result in estimates of stable seasonalfactors. For example, the widely used dummy variable technique,whereby the monthly series X is regressed on twelve dummy variables,eleven of which assume the value 1 when the series is measured ina particular month and zero otherwise, the twelfth dummy variablewith the boundaries selected." (Burns and Mitchell, op. cit., p. 49 fn.) Incommenting thus, Burns and Mitchell were concerned with a particular methodof adjustment, the Kuznets amplitude-ratio method (described later); althoughthe principal is apropos of any method.

The X-l I performs the analysis of variance test on the SI ratios after theyhave been modified to reduce the effect of extreme observations. See X-1 1manual, op. cit., p. 5.

Seasonal Variation of Interest Rates 53always assumes the value zero, estimates stable seasonal factors.19 Thecomputation of stable seasonals is justified when there are goodreasons for believing that the parameters are stable in the hypotheticalpopulation from which the observed series is drawn. This belief is notanalogous to the assumed constancy of the parameters in the structuralrelation of, say, consumption and income. A change in the seasonalparameters (as distinct from the estimated factors) of interest ratesdoes not require that the structural relation between, say, interest ratesand money supply change but only that the seasonal pattern of moneysupply change. In fact, by assuming the structural relation fixed, onecan, in principle, estimate it by relating the changes in the seasonalpattern of one series to those in the other.2° Therefore, the assumptionof fixed seasonal parameters for a given series implies the assump-tion of fixed structural relations between this series and others, aswell as of fixed seasonal patterns in these related series.

Moving Seasonal Factors

Typically there are changes not so much in the original cause of theseasonal movement but in the economy's adaptation to it. The in-creased demand for funds in the fall months will result in a seasonalhigh in interest rates only in the absence of a corresponding increasein the supply of funds. The willingness or ability of the bankingsystem to supply the funds will determine whether the increased de-mand will result in higher rates. Seasonal increases in the demand,as well as in the supply, of funds have varied in the postwar period,and the seasonal increase in interest rates has varied along with it.

Changes in seasonal patterns are difficult to distinguish from ir-regular movements—the more difficult, the greater is the varianceof the irregular component relative to that of the total series. Oneidentifies with greater confidence very small changes in the seasonalvariation of money supply, a series with an almost negligible irregular

Michael C. Lovell, "Seasonal Adjustment of Economic Time Series andMultiple Regression Analysis," American Statistical Association Journal, Decem-ber 1963, p. 993.

20 The distinction here is between a structural relation between two economicvariables, on the one hand, and between an economic variable and time, onthe other. Economic models assume constancy in the first case but not thesecond. The fact that a timing relationship has changed does not imply achange in structural relationship since it may reflect merely the timing changeof the variables with which it is structurally related.

54 Essays on Interest Ratescomponent,2' than changes in the seasonal variation of the highlyirregular Treasury bill rate series. The problem of identifying thesechanges is analogous to one of identifying the components themselves:The method already described for that is predicated on the assumedsmoothness of each of the components within its particular frequency;a method for dealing with changes in the components is to assumethese changes themselves evolve along a smooth path. This methodinvolves either fitting by eye a smooth curve to the SI ratios for allthe Januaries, another for the Februaries, and so on, instead of astraight line at the means of the ratios for each month as in thestable factors, or computing a moving average, one month at a time,of the SI ratios adjusted for extreme values. If a simple three-termmoving average were used, for example, the seasonal factor forJanuary 1953 would equal the average of the SI ratios for January1952, 1953, and 1954. In practice, such a simple moving averagewould be used only for series whose irregular component, being small,is in little danger of distorting the evolution of the seasonal factors.A weighted five-term moving average was used to compute the mov-ing seasonal factors of the interest rate series. When the assump-tion of gradually evolving seasonal factors is not apposite, the use ofthis method will impose a spurious similarity on the estimated factorsfor adjacent years of a given month. However, by observing graphsof the SI ratios themselves one may judge the appropriateness of themethod.

There are several alternative methods of caiculating moving seasonalfactors. The simplest one merely divides the whole sample periodinto subperiods and computes stable seasonal factors for each of thesubperiods. This method is particularly useful for separating thesubperiods with clear evidence of seasonality from those without it.There is some evidence, for example, that yields on long-termTreasury securities manifested seasonality during the late fifties butnot before or since. A method based on evolving factors would spreadthe estimated period of seasonality past its true period, at the sametime that it dilutes what seasonality there is. The method is alsouseful when there is an abrupt change in some institutional factoraffecting the seasonal pattern, as, for example, when the Treasury-Federal Reserve accord in 1951 removed the peg on U.S. governmentbonds. Another method is to compute a set of stable factors for thewhole period and, on the assumption that the true factors for any

The variation of the rate of change of the money supply has, of course,a much larger irregular component.

Seasonal Variation of Interest Rates 55

given year remain in fixed relation, compute factors for each yearproportional to the stable factors (that is, with an identical patternbut different amplitude). The proportion used for a given year is theregression coefficient obtained by regressing the SI ratios for that yearon the stable factors, one regression for each year.22 The applicationof this method to the Treasury bill rates would result in an adjustmentnot very different, and perhaps a little better, than that obtained withthe moving average method. This point is considered in the nextsection. Finally, some writers recommend tying the moving seasonalfactors of one series to the variation of related variables. This methodis, of course, limited by the researcher's ability to specify the ap-propriate relations •23

Sometimes the term moving seasonal is applied to a differentphenomenon than the one described above, where the term referredto changes in the true seasonal component requiring an estimationprocedure capable of detecting these changes. If the seasonal com-ponent is a function of the trend cycle component of the same series,then an estimation procedure that assumes the components are in-dependent will yield biased estimates of the moving seasonal factors.The seasonal decline in unemployment, for example, is said to bemilder when the level of unemployment is low than otherwise becausefirms are reluctant to temporarily discharge workers at a time whenthe labor force is fully employed. The appropriate seasonal factorwill therefore vary between periods of high and low unemployment.Unlike the other reason for moving seasonals, this one does notinvolve a change in the relation among the components of the series(sometimes called the structure of the series) but simply a morecomplicated relation among them.

During the four decades preceding the Federal Reserve Act of1913, a problem analogous to that alleged for unemployment pre-vailed on interest rates and the components of the money stock,although with consequences much more severe than the computationof biased estimates of seasonal factors. In his study written for theNational Monetary Commission organized in response to the panicof 1907,24 Kemmerer concluded that the greater incidence of banking

22 See Simon Kuznets, Seasonal Variations in Industry and Trade, New York,NBER, 1933, p. 324.

23 Mendershausen, op. cit., pp. 254—262.24 See also Milton Friedman and Anna Jacobson Schwartz, A Monetary

History of the United States, 1867—1960, Princeton for NBER, 1963, pp.171—172.

56 Essays on Interest Rates

panics in the fall than at other times of the year was due not tothe normal seasonal tightness in the fall money market but to thattightness coming at the same time as a cyclical crisis. The seasonalmovement, in effect, played the role of the proverbial

Even if the seasonal component, expressed as a ratio to the movingaverage, were systematically related to the level of the moving average(or trend-cycle component) the estimated seasonal factors would notreveal this relation. Since the factors are computed from averages ofthe SI ratios across years, the variation of the SI ratios due to thecyclical variation is canceled out in the averaging process. In the caseof an extreme cyclical movement, a related seasonal movement wouldlikely result in an SI ratio that would be regarded as an extreme ob-servation and be eliminated from the computation of the seasonalestimates. However, any relation that exists between the seasonal andcyclical components would present itself in a time series of the SI ratios.Section III considers this point.

Even in the absence of a true relation between the seasonal andcyclical components the inappropriate use of either an additive or multi-plicative adjustment, that is, the use of one when the other is required,will result in an apparent relation between the seasonal and cyclicalcomponents.

When the level of rates is low the basis point equivalent of a multi-plicative adjustment factor is smaller than when the level of rates ishigh. If the true seasonality were additive, and a multiplicative adjust-ment method were used, there would result an inverse relation betweenthe SI ratios and the level of rates. Assume, for example, the true sea-sonal difference for a particular month to be 50 basis points. If inestimating the seasonal variation a multiplicative method were used, theSI ratio computed for this month would be high when the level of rateswere, say, 100 basis points (i.e., 150/100) and low when the levelwere, say, 400 basis points (i.e., 450/400). Application of this test tothe computed SI ratios for the Treasury bill rates does not reveal asystematic inverse relation between these ratios and the level of rates.

28 The evidence on this point is mixed. Kemmerer found that "of the eightpanics which have occurred since 1873 [as of 1910], four occurred in the fallor early winter (i.e., those of 1873, 1890, 1899, and 1907); three broke outin May (i.e., those of 1884, 1893, and 1901); and one (i.e., that of 1903)extended from March until well along in November." After discussing the"minor panics or 'panicky periods,'" he concludes that "The evidence accord-ingly points to a tendency for the panics to occur during the seasons normallycharacterized by a stringent money market." (Op. cit., p. .232.)

Seasonal Variation of Interest Rates 57

However, the opposite procedure designed to test the efficacy of a multi-plicative adjustment, assuming the true seasonal were multiplicativeand the estimates additive, fails to confirm the appropriateness of amultiplicative adjustment. The question is therefore open and invitesdeference to convention—which is to use a multiplicative adjustmentunless an additive one is clearly indicated.26

There is a method that combines elements of both the additive andmultiplicative adjustment. Seasonal-irregular ratios are computed foreach month and the set for each month regressed on the trend-cyclecomponent for that month; twelve regressions in all. The constant termof each regression is an estimate of the additive component of thatmonth's seasonal factor and the regression coefficient of the multipli-cative component. This method, however, assumes stable seasonality inthe sense used earlier in this report.27

Seasonal Adjustment on Computers

The X-1 1 program, used in this study, embodies a series of refine-ments in the original ratio-to-moving-average technique that Macaulaydeveloped in the 1930's. By reducing the cost and virtually eliminatingthe tedium of the vast number of elementary calculations this methodof adjustment requires, the program makes feasible the use of complexweighting schemes in computing moving averages that are both elastic(i.e., remain faithful to the original series) and smooth (i.e., avoidthe irregular wiggles). It allows, moreover, the extensive use of itera-tion to mitigate the obscuring influence of the irregular component onthe separation of the seasonal from the trend-cycle components. Itsmost important advantage is the reduction in the time-cost and skillsrequired in manual adjustments.

26 See Julius Shiskin and Harry Eisenpress, Seasonal Adjustment by ElectronicComputer Methods, Technical Paper 12, New York, NBER, 1958, p. 434.

27 There is clearly room here for variations on a theme. One can adapt theregression method to allow for a moving seasonal by applying the regressionmethod as stated and applying the X-l 1 method to the residuals of theregressions. In that case one could obtain: an additive component, a componentrelated to the trend cycle, and a moving seasonal component. Since this studyuncovered no evidence of a relation between the seasonal and trend-cyclecomponents of the interest rate series there was no reason to experiment withthis method. In his exhaustive article, Mendershausen (op. cii.) describes manyexotic techniques for circumventing this or that problem of conventionalmethods; virtually all of them are in desuetude either because they introducedother problems or they were too unwieldy.

58 Essays on Interest Rates

The program's advantages are particularly obvious through the stagein which the modified seasonal-irregular ratios or differences are com-puted as, of course, are their mean values, or the stable seasonal factors,when relevant. An experienced draftsman, however, can graphically fitmoving seasonals to. the SI ratios as well as the program does, andprobably better than the program does when the series has a prominentirregular component. Moreover, judgment is often required in deter-mining whether an adjustment for any subperiod should be undertakenat all. Since the analysis of variance is a test of the means of the SIratios for the whole sample period, there is some danger that the pres-ence of a relatively strong seasonal component in one subperiod willaffect the means for the whole period sufficiently to lend an apparentsignificance to the computed differences among them. (This effect wouldhave to be large enough to overcome the increased within-group vari-ance as a result of the greater heterogeneity of the SI ratios of a givenmonth that a moving seasonal implies.) The program adjusts the wholeseries regardless of the results of the analysis of variance. The usercannot rely on the F-test alone to decide whether to accept the adjust-ment in its entirety.

The absence of objective criteria for selecting the period of adjust-ment, the extent of the adjustment, or the quality of the results28 pre-cludes an elaborate tabulation of this study's findings replete with stan-dard errors. Nevertheless, from the descriptive statistics, the diagrams,and the verbal entourage, patterns emerge that are worth noting. SectionIII presents this material for seventeen interest rate series.

III. THE EVIDENCE OF SEASONALITYIN INTEREST RATES

This section evaluates the evidence of seasonality in postwar interestrates and suggests suitable adjustments where appropriate. The evalua-tion consists of graphically identifying biases in the SI ratios over orunder the 100.0 level. While the one-way analysis of variance test forseasonality is a useful method for identifying systematic deviations ofthe SI ratios from 100.0, its reference to the entire period makes itineffective as a means of distinguishing the s.ubperiods with evidence of

26 "A statistician who has struggled with seasonal adjustments of numeroustime series is not likely to underestimate the part played by 'hunch' and'judgment' in his operations." (Burns and Mitchell, op. cit., p. 44.)

Seasonal Variation of Interest Rates 59

seasonality from those without it.2° The consistent deviation of a givenmonth's SI ratio in the same direction from the 100.0 line is strongevidence of seasonality regardless of the variation in the magnitude ofthese deviations, that is, in the seasonal amplitude. The evidence ofseasonality is weak when there are constant reversals of direction orwhen the relationship among the patterns of SI ratios is generally un-stable from year to year. The summary statistics that most computerprograms for seasonal adjustment supply (such as the average month-to-month change in the seasonal component by itself or relative to thatof the other components) do not help evaluate the evidence of season-ality since, aside from the analysis of variance test, they only sum-marize what the program has done. They do not provide independentmeasures of either the evidence of seasonality or the quality of the ad-justment. Once the existence of a seasonal pattern is confirmed and theadjustment decided, then the summary statistics provide a useful sum-mary of the results.

In seasonal analysis, as in regression analysis, one places greaterconfidence in tests for the existence of a relation than in its actualmeasurement. In addition to the problem of sampling error commonto both analyses, the moving seasonal amplitude implies changingparameters and requires the adjustment method, in effect, to shoot ata moving target. Except for a few experiments this study does notoriginate any methods of adjustment, nor does it even compare theadjustments obtainable with existing methods.3° Instead, charts of theseasonal factors obtained with the X-1 1 are superimposed on chartsof the corresponding SI ratios to determine the method's success incapturing what appears to be the systematic movement of the SI ratios.There is no question but that one could fit by eye a curve that is morefaithful than is the curve of factors to variation of the SI ratios; in theextreme, one could perfectly fit a curve to the SI ratios by simplyconnecting the points—that is, by simply treating them as the factors.The art of the adjustment is in identifying the systematic movementof the SI ratios. When the pattern of SI ratios is stable from year toyear there is no problem; nor is there any when the seasonal amplitudechanges gradually or the pattern evolves with an apparent method. Butduring transition periods, in which the series has strong irregular move-

20 One can apply the analysis of variance to separate subperiods, but theproblem of choosing the limits of the subperiods remains.

The potential gain from these experiments is not, in this study's view,commensurate with the effort required.

60 Essays on interest Rates

ments, such as 1954, the SI ratios and estimated factors appear to bevirtually unrelated. This study recommends ignoring the adjustmentwhen the gap between the two is pervasive.

Short-Term Securities

Summary Statisfics

Table 2-1 lists some of the summary statistics that are useful in de-scribing the extent and significance of seasonal influence.31 Columns1—3 divide the total variance of the series into the parts due to eachof the three components: the trend-cycle, seasonal, and irregular. Thesefigures are analogous to readings from the spectral density function,which decomposes the variance of a time series according to the fre-quency of the recurring variation.82 Column 4 lists the average month-to-month percentage changes (without regard to sign) of the seasonalcomponent, and column 5 the ratio of column 4 to the correspondingstatistics of the cyclical component. These figures, columns 1 through 5,strike averages for the whole study period, averages not of the trueseasonal but of the estimated one, including a spill-over into periodswithout significant seasonality. Columns 7—10 give the dates and am-plitudes of the highest and lowest seasonal factors observed during thestudy period.

But these figures may be only statistical artifacts; hence, the needexists to ascertain their statistical significance. To partially satisfy thisneed, column 6 records the F statistics.

The F statistic may be low for any of several reasons, the enumera-lion of which will help in evaluating the charts that follow. The most

The statistics are copied directly from the X-1 I printout and are describedmore fully in the X-11 Manual, op. cit.

32 Some recent studies have applied spectral analysis to the problem ofidentifying seasonal variation. While the principle is the same as that in themoving average method—to simultaneously or sequentially filter, or separate,different frequencies of variation—spectral analysis is a more sophisticatedand more rigorous method of doing so. Some of the mathematical advantageis lost, however, in its application to a limited number of observations. Thismethod, moreover, provides no direct adjustment for the seasonal and resembles,in this respect, analysis of variance instead of regression analysis. In Chapter 7of this book, Tom Sargent has applied spectral analysis to interest rates, amongother financial variables, and has reached conclusions virtually identical to thosein the present study with respect to the extent and evolution of the seasonalin interest rates.

TAB

LE 2

-1. M

easu

res o

f the

Rel

ativ

e Im

porta

nce

of th

e Se

ason

al C

ompo

nent

s of t

he F

our S

erie

s of S

hort-

Term

Secu

ritie

s, 19

48—

65

Ave

rage

Rat

io o

fM

onth

-to-M

onth

Col

umn

4D

ate

and

Fact

or o

f Sea

sona

l Hig

h

.

Ser

ies

Perc

enta

ge o

fTo

tal V

aria

nce

ofSe

ries D

ue to

Each

Com

pone

nt

IC

S(1

)(2

)(3

)

Perc

enta

geC

hang

esW

ithou

t Reg

ard

to S

ign

ofSe

ason

alC

ompo

nent

3 (4)

to C

orre

-sp

ondi

ngFi

gure

sfo

r the

Cyc

lical

Com

pone

ntS/

C(5

)

F Te

st fo

rSt

able

Seas

onal

itya

(6)

and

Low

for W

hole

Per

iodb

Hig

hLo

w

Fact

or(p

erce

nt-

Dat

eag

e)D

ate

(7)

(8)

(9)

Fac

tor

(per

cent

-ag

e)(1

0)

Yie

lds o

n:91

-day

bill

s37

.72

42.5

219

.76

2.54

0.68

9.66

2D

ec. 1

957

113.

9Ju

ly 1

957

87.4

9—12

mon

thse

curit

ies

35.9

149

.77

14.3

21.

850.

544.

557

Dec

. 195

610

9.0

June

195

790

.7C

omm

erci

alpa

perc

35.3

842

.98

21.6

41.

81.7

14.

034

Dec

. 195

810

7.5

May

195

992

.8B

anke

rs'

acce

pt-

ance

s24

.57

49.3

926

.04

2.07

.72

11.2

93D

ec. 1

957

111.

4Ju

ly 1

956

89.3

aAll

ratio

s are

stat

istic

ally

sign

ifica

nt a

t the

5 p

er c

ent l

evel

.bA

mov

ing

seas

onal

com

pone

nt w

as e

stim

ated

for b

oth

serie

s. C

olum

ns 7

and

9 li

st th

e da

tes w

hen

the

ampl

itude

s of t

he se

ason

alva

riatio

ns w

ere

grea

test

and

col

umns

8 a

nd 1

0 th

e va

lues

of t

he e

stim

ated

seas

onal

fact

ors f

or th

ese

date

s.C

The

sam

ple

perio

d fo

r com

mer

cial

pap

er ra

tes e

nds i

n Ju

ne 1

965.

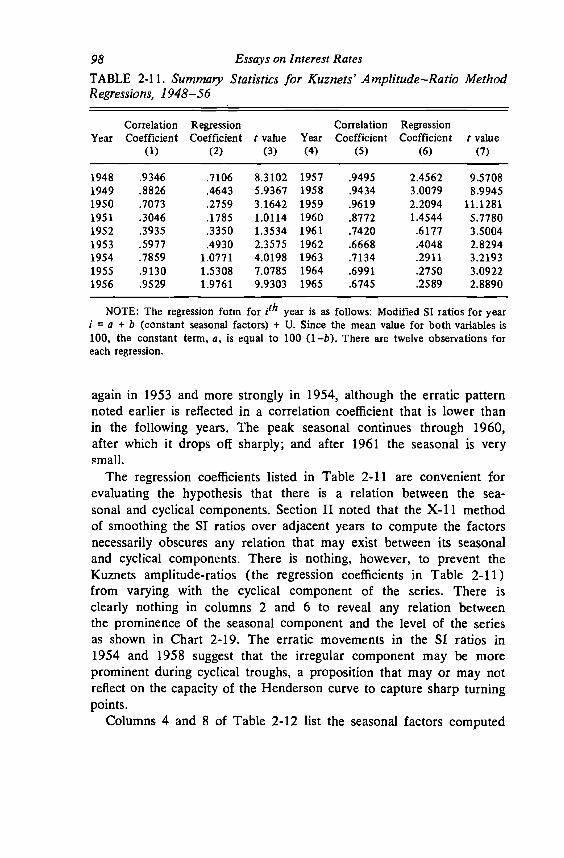

62 Essays on interest Ratesimportant reason, of course, is the absence of any bias in the monthlySI ratios away from the mean value of 100.0; in other words, no sea-sonality. But a low F statistic does not imply the absence of seasonalityover the whole sample period. The smaller the subperiod of true sea-sonality the greater the burden on this period's SI ratios to influence themeans for the whole sample period and thereby enlarge the betweenmeans variance, the numerator of the F ratio. The burden is aggravatedby the fact that a moving seasonal component combines with the ir-regular component to enlarge the within-group variance, the denomina-tor of the F ratio. When, for example, the F statistic is computed forlong-term Treasury securities over the entire period, its value (1.787)signifies the absence of seasonality; whereas, when computed overthe period. 1955 through 1962 the result (4.726) confirms the pres-ence of seasonality. Similarly, the F statistic in Table 2-1 for nine-to twelve-month Treasury securities is low because the seasonal pat-tern before 1955 was at best highly irregular. When the seasonalpattern changes over the sample period, even when in each subperiodthe pattern is unambiguous, the F statistic suffers as the differencesamong the mean monthly SI ratios are reduced. Combine this prob-lem with the fact that seasonal patterns do not change instantaneouslybut rather evolve through periods of transition during which a coherentpattern is virtually nonexistent. In the eighteen-year sample periodthe seasonal pattern of commercial paper rates underwent severalchanges, and the low F statistic shown in Table 2-1 in part reflectsthis fact.33 Finally, the F statistic may be low not because there isno seasonality but because of a strong irregular component; the meansof the SI ratios are different from 100.0, but the standard errors ofthe means are high. This condition applies to all the interest rateseries and in particular to commercial paper rates and yields onmunicipal bonds. Here again the diagrams are essential for deter-mining whether the seasonal pattern has sufficient stability to war-rant adjustment.

At its highest the seasonal component pushes the Treasury bill rate14 per cent (rounded to nearest integer) above its trend-cycle value;at its lowest, 13 per cent below. For a bill rate in the neighborhoodof 4 per cent (i.e., 400 basis points) these seasonal factors correspondto about 50 basis points.34 At 11 per cent on either side of the trend-

These changes are described later in the section.These figures are actually underestimates since they embody the dampening

effects of the lower peak levels of adjacent years. Later in this section anexperiment is described that exemplifies this point.

Seasonal Variation of Interest Rates 63

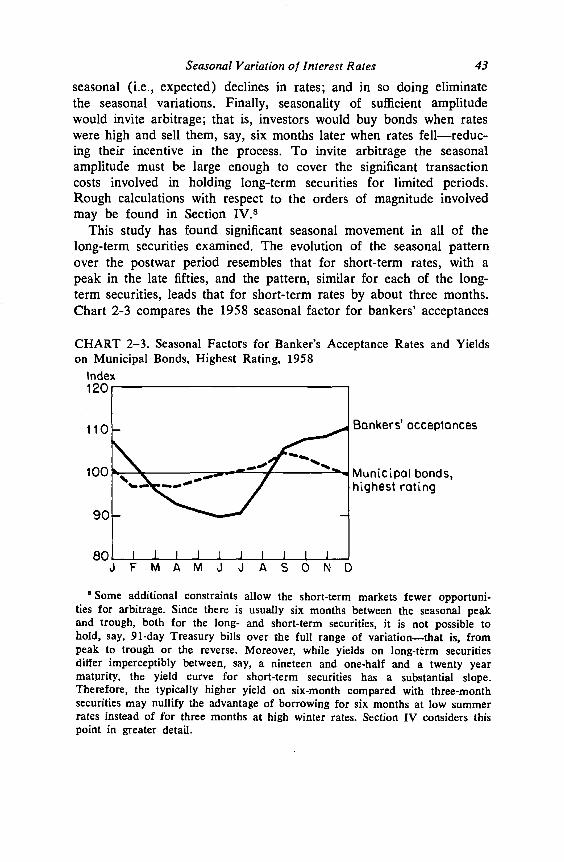

cycle values, the peak seasonal amplitude for yields on bankers' ac-ceptances is somewhat less. Relative to the total variation of theseries, however, the seasonal component of the yields on bankers' ac-ceptances is the most important of the four series, and its F statisticis highest. The diagrams, to be. discussed presently, support the con-clusion that this series evinces the strongest seasonal component. Theseries for which the summary statistics are least reliable is the serieson commercial paper rates, for which, in addition, the F statistic islowest. The diagrams will justify this conclusion as well.

Treasury Bill Rates

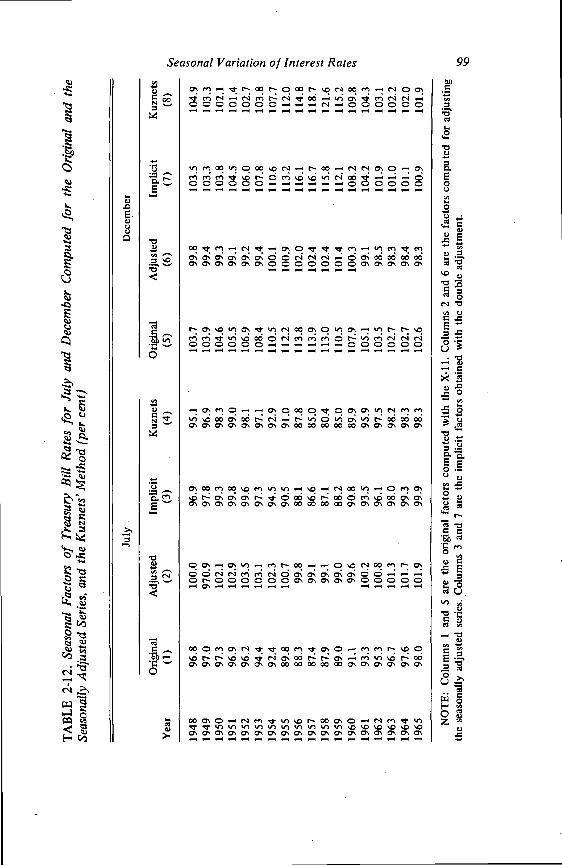

Chart 2-7 plots the seasonal factors for Treasury bill rates super-imposed on the corresponding SI ratios. From a relative high inJanuary the Treasury bill rate seasonal pattern typically declines pastseasonally neutral February, downward through the spring monthsto its trough in June or July and then turns sharply upward throughseasonally neutral August to September, from which it rises graduallyto its peak in December.35 Surprisingly, this pattern is quite apparent,although the amplitude is small, in 1948, when the Federal Reservepegged the prices of Treasury bills within narrow limits. This curveis shown in the first panel of Chart 2-7 together with the unmodifiedSI ratios. In subsequent panels of Chart 2-7, the pattern is shown todissolve until about 1953 and then gradually to emerge again, butwith greater amplitude, in the middle fifties, keeping this shape intothe sixties as its amplitude virtually disappeared. By 1965 there waslittle left but a 2 per cent trough in June—July and a 2 per cent peakin December—January.

The factor curves, the broken lines of Chart 2-7, are for the mostpart dampened versions of the corresponding SI ratios, although attimes the factor curve for one year betrays the influence of itspredecessor more than that of its contemporary SI ratios. In thisregard the factor curves ignore certain abrupt movements of the SIratios, as in April 1955, the program being designed to sidesteppoints it regards as extreme.3°

Before 1957, the movement between September and December was notmonotonic.

Briefly, an extreme point is one that falls outside the range of 1.5 standarddeviations, the latter computed for the entire set of data several times toeliminate the effect on it of the extreme points. The extremes are weighted

64 Essays on Interest RatesC}IART 2—7. SI Ratios and Seasonal Factors for Treasury Bill Rates,1948—65

FMAMJ JASON FMAMJ J A

SI ratiosSeasonal factors

Index Index Index

Seasonal Variation of interest Rates 65

The relative stability of the seasonal pattern is in part a measureof the adjustment's effectiveness since the program does not attemptto directly fit the solid lines in Chart 2-7. Instead it smooths the SIratios month by month as shown in Chart 2-8. As a given month'sCHART 2—8. Variation of Monthly Factor Curves and SI Ratios ofTreasury Bill Rates, 1948—65

SI rQtiosSeasonal factors

factors evolve through the years, any persistent change in their rela-tion to another month's factors, that is, any change in the orderinglinearly from 1 to 0 as they fall between 1.5 and 2.5 standard deviations. Anextreme SI ratio different from 100 by two standard deviations is weighted 0.5.See X-11 Manual, op. cii., pp. 4—5.

66 Essays on Interesr Rates

of the twelve factors, will change the seasonal patterns given inChart 2-7. Barring the extremes, the factor curves in Chart 2-8 fit theSI ratios quite closely although severely dampening their movement.One may wish to quarrel with the fit at a few places, but it will soonbe shown that any reasonable alterations would have little quantitativeimportance. The two or three years preceding 1954 and following1960 appear overly dependent on the years in between; and cor-respondingly, the peak period is excessively dampened. Aside fromthe transitional months, February and August, the monthly factorcurves trace out the bell-shaped curves noted earlier, inverted in thelow months, of course, and most of them remain above 100 or below100 throughout the period. While most of the curves as of 1965roughly coincide with the 100.0 line, the curves for July and Decem-ber are still about 2 per cent under and over the line, denoting thepersistence of a small seasonal variation in Treasury bill rates.However, the pattern for the last four years differs somewhat fromthat in earlier years: the trough appears in June instead of July; theJanuary factors become at least as prominent as the ones for Decem-ber; and, in the last two years, the November factors dip below the100.0 line. Similar changes will be shown to have occurred in yieldson bankers' acceptances as well.37

Other Short-Term Rates

The seasonal patterns of the other short-term rates considered, ex-cept for commercial paper rates prior to 1956, are very similar tothe one for Treasury bill rates. The similarity is greatest in the peakperiod, when the patterns for all the series have their greatest stability.Table 2-2 lists the simple correlation coefficients between the twelveseasonal factors for Treasury bill rates and those for the other seriesover selected years. In 1957 the correlations were all in excess of .95,indicating virtual identity among the four patterns; by 1965, however,the correlations were much less, and could be in part the spuriousaftermath of the earlier similarity.

Closest in pattern and evolution to that of Treasury bill rates isthe seasonal movement of yields on bankers' acceptances. As in thecase of bills, the seasonal pattern for yields on bankers' acceptances

The appendix to this section uses alternate adjustment procedures toevaluate the X-I 1 adjustment of Treasury bill rates.

'1

Seasonal Variation of Interest Rates 67TABLE 2-2. Simple Correlation Coefficients Between the Seasonal Factorsfor Treasury Bill Rates and Those for Other Short-Term Rates for SelectedYears

1953(1)

1957(2)

1963(3)

1965(4)

Bankers' acceptances .6430 .9742 .7926 .5283Commercial paper .1380 .9724 .8917 NA9—12 month Treasury securities .8447 .9510 .7700 .6492

NOTE: The numbers are all simple correlation coefficients between the seasonalfactors of Treasury bill rates and the factors in the corresponding years for the otherthree series.

NA = not available.

is fairly stable from 1948 through 1950, but, again like bills, the fitis less adequate from 1951 through 1954. In Chart 2-9 the estimatedfactors are shown to grossly exaggerate the trough in July. Sea-sonality exists in the period (July, for example, is always below the100.0 line and December above), but its pattern is less stable thanand differs from the patterns of other years. During the peak periodits pattern is the familiar high in January, declining past neutral Febru-ary through the spring lows to a trough in July, then climbing steeplyupward to September and, more gradually, to a December peak. Al-though its peak amplitude, at 12 per cent on either side of the corre-sponding trend-cycle values, is somewhat less than the peak in thebill rate seasonal pattern, the seasonal amplitude on yields on bankers'acceptances is more prominent in the total variation of the series(columns 3 and 5 of Table 2-1), and the estimated factors are morefaithful to the SI ratios (Chart 2-9). Beginning in 1959. the patternbegins to change somewhat, the trough shifts from July to June andthe peak from December to January. These changes, as well as thedip in November, are virtually identical to those that occurred some-what later in Treasury bill rates. Chart 2-9 reveals the low and de-clining seasonal amplitude in yields on bankers' acceptances in thesixties. Although the last year of the adjustment period, is alwaystricky, the factors for 1965 appear to signal the end of the seasonalcomponent.

Because its pattern is less stable than the patterns of the two short-term series described above, the seasonal variation of commercialpaper rates is more difficult to isolate. Chart 2-10 plots the SI ratiosand corresponding factors for commercial paper rates. From 1948

68 Essays on Interest RatesCHART 2—9. SI Ratios and Seasonal Factors for Bankers' AcceptanceRates, 1948—65

Index110

SI rotLosSeasonal factors

Index Index

90 -1949

-

110

100

- -

II,...,

90

1950

90 - - 110

110

100

1951

.',._

- -

100

901952

——

90

110

100

90

110

100

- - 110

90

110

100

90

-

1954

-

1956

90 -

I I I II I I I I I

F MAM J .J A SO ND

Index

110

Seasonal Variation of Interest Rates 69CHART 2—10. SI Ratios and Seasonal Factors for Commercial PaperRates, 1948—65

J FM AM J JASON 0

Index

90

110

100

90

110

100

90

110

100

90

Index

SI rattosSeasonal factors

Index Index130

10

100

70 Essays on Interest Rates

through 1950 the seasonal pattern, except for a high in October, isvirtually the mirror image of the pattern in the late fifties—the firsthalf year in the earlier period being above the 100.0 line, the secondhalf below. The pattern evolves through a transition period in 1951to a pattern that extends through 1955 and is quite similar to the onefor long-term rates. Beginning with a low in January the factors dropto a trough in March, turn up through May or June to a peak inOctober and then sharply down. The pattern in 1955 already blendsinto the new pattern that is characteristic of the other short-termseries: From a high in January the factors turn down through neutralFebruary and the springtime lows to a trough in July then go upthrough neutral August to a peak in December. This pattern persiststhroughout the period of peak seasonality in the late fifties, duringwhich, however, the seasonal amplitude never exceeds 8 per cent ofthe corresponding average values of the series. Beginning in 1962 thepattern appears to drift back towards the earlier one that resembledthe pattern of long-term series. Nevertheless, the seasonal amplitudepersists through the end of the period.

As in the case of the other short-term series, there is a repetitiveripple in the yields on nine- to twelve-month Treasury securities from1948 through 1950, but, as Chart 2-11 shows, the factors do not fitthe SI ratios as well as in the case of the other short-term series.Several years of erratic movement follow before the final patternemerges in 1955. Choppy at first, it evolves rapidly into full shapein 1957 and slowly down again but persisting through the end of theperiod. Indeed, in 1965 the amplitude is greater and the pattern morediscernible than in the case of bill rates.

The pattern during the late fifties is very similar to that of the othershort-term series except that the trough comes a month earlier (inJune) and a fall plateau replaces the December peak. This change inpattern is in the direction of the long-term series.

Summary of Short-Term Series

While the seasonal patterns of short-term rates are not entirely uni-form throughout the postwar period, for the most part they have incommon springtime lows and a midyear trough, as well as fall highsand a December peak continuing with some diminution through Jan-uary. This pattern describes all four series in the period of greatestseasonality, 1956 through 1960. Treasury bill rates and yields on

Seasonal Variation of Interest Rates 71

CHART 2—11. SI Ratios and Seasonal Factors for Yields on Nine. toTwelve-Month U .S. Government Securities, 1948—65

SI rutLosSeasonal factors

Index Index Index Index1 130

72 Essays on Interest Ratesbankers' acceptances sustain this pattern throughout the 1948—65period, although not with as much stability and amplitude as duringthe 1956—60 period. The patterns for commercial paper rates prior to1956 are quite different from those of the other short-term rates and,in fact, resemble those of the long-term rates that are described be-low. There are actually two distinct patterns for commercial paperrates during 1948—55, a fact making the adjustment for this periodof questionable value. While the pattern for to twelve-monthTreasury securities prior to 1955 is quite similar to the one for Trea-sury bills (column 1 of Table 2-2), the factors are not sufficiently faith-ful to the SI ratios, in this study's view, to warrant an adjustment. Inthe later period, however, the seasonal influence is unambiguous;Chart 2-12 plots the time series of seasonal factors of the four short-term series considered in this study.

After 1960 the seasonal amplitudes of all the short-term seriesrapidly decline. While some seasonality persists after 1963, an adjust-ment will unavoidably introduce some additional error into the series.Whether the elimination of the true seasonal is worth the increaseddanger of introducing error as a result of adjusting for a spuriousseasonal factor is an isssue the user must decide. Table 2-3 lists theperiods during which, in this study's view, the seasonal is worth ad-justing for.

TABLE 2-3. Suggested Periods for Adjusting Short-Tenn Series

Security Adjustment Period

Treasury bill rates 1948—65Bankers' acceptance rates 1948—63Commercial paper rates 1956—659—12 month Treasury security rates 1955—65

Long-Term SecuritiesSummary Statistics

The seasonal amplitudes of yields on long-term bonds are not high.In only two of the thirteen cases listed in Table 2-4 does the highestestimated factor for a given bond exceed 4 per cent and in only fourcases 3 per cent (column 8). Notwithstanding the low amplitudes,the computed F statistics signify stable seasonality in all but twocases and in most cases by a wide margin (column 6). Finally,

CH

AR

T 2—

12. S

easo

nal F

acto

rs fo

r Sho

rt-Te

rm In

tere

st S

erie

s, 19

48—

65In

dex

Inde

xI

II

II

II

II

II

II

II

I

—B

anke

rs a

ccep

tanc

e ra

tes

110-

Co

alat

—

110

100 90

-U

. S. G

ovt.

secu

ritie

s, 9

—12

mon

ths

120

— -C

90 120 10

—T

reas

ury

bill

rate

s

II

II

—1

1948

'51

'53

'55

'57

'59

'61

'63

'65

90

II

II

II

II

I80

TAB

LE 2

-4. M

easu

res o

f the

Rel

ativ

e Im

porta

nce

of th

e Se

ason

al C

ompo

nent

s in

the

Var

iatio

n of

Yie

lds o

n Lo

ng-T

erm

Bon

ds, 1

948

—65

Ave

rage

Rat

io o

fM

onth

-to-M

onth

Col

umn

4D

ate

and

Fact

or o

f Sea

sona

l Hig

h

Perc

enta

ge o

fTo

tal V

aria

nce

ofSe

ries D

ue to

Each

Com

pone

nt

Perc

enta

geC

hang

esW

ithou

t Reg

ard

to S

ign

ofSe

ason

al

to C

one-

spon

ding

Figu

res

for t

heC

yclic

alF

Test

for

and

Low

for W

hole

Per

ioda

Hig

hLo

w

Fact

orFa

ctor

IC

SC

ompo

nent

SC

ompo

nent

S/C

Stab

leSe

ason

ality

(per

cent

-(p

erce

nt-

Dat

eag

e)D

ate

age)

Serie

s(1

)(2

)(3

)(4

)(5

)(6

)(7

)(8

)(9

)(1

0)

Mun

icip

alsb

Hig

hest

ratin

g44

.23

34.7

821

.00

1.18

0.78

Sept

. 195

810

4.7

Feb.

195

896

.6Lo

wes

tra

ting

45.9

736

.30

17.7

20.

860.

701.

515

Sept

. 195

810

2.3

Apr

. 196

097

.7H

igh

grad

e(S

& P

)55

.38

26.7

417

.88

1.05

0.82

Sept

. 195

810

3.5

Feb.

195

507

.1

Rai

lroad

sH

ighe

stra

ting

34.6

545

.46

19.8

90.

440.

667•

230C

Sept

. 195

710

1.8

Mar

. 195

798

.3Lo

wes

tra

ting

36.9

238

.36

24.7

10.

590.

81'L

lllc

Dec

. 195

610

1.6

Mar

. 195

497

.9

(con

tinue

d)

TAB

LE 2

-4 (c

ontin

ued)

0 0 0 0

Ave

rage

Rat

io o

fM

onth

-to-M

onth

Col

umn

4D

ate

and

Fact

or o

f Sea

sona

l Hig

h

Perc

enta

ge o

fTo

tal V

aria

nce

ofSe

ries D

ue to

Each

Com

pone

nt

Perc

enta

geC

hang

esW

ithou

t Reg

ard

to S

ign

ofSe

ason

al

to C

orre

-sp

ondi

ngFi

gure

sfo

r the

Cyc

lical

F Te

st fo

r

and

Low

for W

hole

Pen

oda

Hig

hLo

w

Fact

orFa

ctor

IC

SC

ompo

nent

SC

ompo

nent

S/C

Stab

leSe

ason

ality

(per

cent

-(p

erce

nt-

Dat

eag

e)D

ate

age)

Ser

ies

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Cor

pora

tes

Hig

hest

ratin

g37

.74

38.6

323

.62

.54

.78

5•80

6CSe

pt. 1

957

102.

2M

ar. 1

957

97_s

Low

est

ratin

g31

.34

45.7

222

.94

.43

.72

7•85

1CO

ct.

1957

101.

7M

ar. 1

955

98.5

Publ

ic u

tiliti

es.

Hig

hest

ratin

g34

.60

38.9

226

.48

0.61

0.82

Oct

. 195

810

3.2

Mar

. 195

897

.2Lo

wes

tra

ting

38.2

641

.22

20.5

20.

440.

70O

ct. 1

957

101.

7M

ar. 1

955

98.5

Indu

stria

lsH

ighe

stra

ting

46.4

229

.75

23.8

30.

660.

894j

30C

Sept

. 195

710

2.3

Mar

. 195

897

.6

(con

tinue

d)

TAB

LE 2

-4(c

oncl

uded

)

Ave

rage

Rat

io o

fM

onth

-to-M

onth

Col

umn

4D

ate

and

Fact

or o

f Sea

sona

l Hig

h

Perc

enta

ge o

fTo

tal V

aria

nce

ofSe

ries D

ue to

Each

Com

pone

nt

Perc

enta

geC

hang

esW

ithou

t Reg

ard

to S

ign

ofSe

ason

al

to C

one-

spon

ding

Figu

res

for t

heC

yclic

alF

Test

for

and

Low

for W

hole

Per

ioda

Hig

hLo

w

Fact

orFa

ctor

IC

SC

ompo

nent

SC

ompo

nent

S/C

Stab

leSe

ason

ality

(per

cent

-(p

erce

nt-

Dat

eag

e)D

ate

age)

Ser

ies

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Indu

stria

lsLo

wes

tra

ting

29.1

253

.34

17.5

40.

360.

57O

ct.

1957

101.

4M

ar. 1

958

98.6

U.S

. Tre

asur

yLo

ng te

rm7.

5140

.42

2.08

0.50

0.55

1.78

7Se

pt. 1

957b

102.

8A

pr. 1

957

98.0

3—5

year

s3.

7337

.76

8.51

1.45

0.71

Sept

. 195

710

5.8

Apr

. 195

995

.2

aA m

ovin

g se

ason

al c

ompo

nent

was

est

imat

ed fo

r the

four

serie

s. C

olum

ns 7

and

9 li

st th

e da

tes w

hen

the

ampl

itude

s of t

hese

ason

al c

ompo

nent

wer

e gr

eate

st a

nd c

olum

ns 8

and

10

the

valu

es o

f the

est

imat

ed se

ason

al fa

ctor

s for

thes

e da

tes.

bThe

est

imat

ed se

ason

al fa

ctor

for S

epte

mbe

r 195

8 w

as a

lso

102.

8.cs

igni

fican

t at t

he 1

per

cen

t lev

el.

I

Seasonal Variation of Interest Rates 77

again notwithstanding the low peak amplitudes, as well as the sea-sonal components' relatively low average month-to-month percentagechanges without regard to sign (column 4), the estimated percent-ages of total variation of the series due to the seasonal components(column 3) are roughly comparable and a little higher than thecorresponding figure for Treasury bill rates.

These summary statistics are likely to be more reliable than thecorresponding statistics for short-term securities because in the long-term bond rates, exclusive of the two Treasury series, the seasonalitypersisted throughout most of the study period, although with somechanges in both pattern and amplitude. The summary statistics forthree- to five-year and long-term Treasury securities, however, largelyreflect the seasonal flourish in the. late fifties. Both its small amplitudeand its shifting pattern likely contribute to the persistence of sea-sonality in long-term bonds (as of 1965 the seasonal influence inmost of the series was minute but discernible) since these character-istics in effect obscure the seasonal variation and thereby lessen thelikelihood of investors trading them away.38

Although there is a general bell-shaped pattern to the seasonalamplitudes of the long-term securities during the postwar period, therelative rise in the late fifties is not as pronounced as in the case ofthe short-term securities nor is it as pronounced in the private long-term rates as in the Treasury rates. Table 2-5 lists the variances ofthe seasonal factors of a given year for selected years for all thesecurities considered in this study. The variance of the twelve monthlyfactors is a convenient measure of the over-all seasonal amplitudefor a given year. The bell-shaped pattern refers to the increase inthe securities from 1953 to 1957 and their decrease to 1963. (Thebell is actually quite symmetrical, a fact that is hidden by the differ-ent spans of the two periods.) Except for the railroad (lowest quality)securities, the table supports the generalization stated above.

There is a curious consistency in the relations among the seasonalfactors of the several long-term series, a consistency for which thereis no mechanical explanation. In Table 2-5, for example, the seasonal

88 A small amplitude does not by itself impugn the significance of theseasonal component. The seasonal amplitude for the series on the stock ofmoney, for example, is never more than 3 per cent; although the value ofthe F statistic in the postwar period is a robust 281. A comparison betweencolumn 5 in Tables 2-1 and 2-4 shows that relative to the variation of thecyclical component the seasonal amplitude of long-term bond rates is typicallygreater than that of short-term rates.

78 Essays on interest RatesTABLE 2-5. Variance of Seasonal Factors for Selected Years for AllSecurities Considered

Security 1953 1957 1963 1965

Long-term bondsMunicipals

Highest rating 2.789 6.386 1.395 1.279Lowest rating 1.182 2.085 0.734 0.605High grade (S & P) 2.9 14 3.6 14 1.624 1.445

CorporatesHighest rating 0.516 2.208 0.224 0.145Lowest rating 0.664 1.132 0.071 0.053

IndustrialsHighest rating 0.557 2.286 0.398 0.302Lowest rating 0.588 1.014 0.112 0.075

RailroadsHighest rating 0.386 1.350 0.115 0.062Lowest rating 1.300 0.846 0.211 0.223

Public utilitiesHighest rating 0.762 3.580 0.260 0.144Lowest rating 0.381 2.490 0.094 0.075

U.S. TreasuryLong term 0.231 2.161 0.253 0.096

3—5 years 2.756 14.455 0.992 0.308

Short-term securitiesU.S. Treasury bills 15.453 92.9 10 5.080 2.996Commercial paper 5.684 25.341 4.252 NABankers' acceptances 12.816 67.158 1.603 0.734U.S. Treasury 9—12 months 6.843 42.367 2.425 1.977

NOTE: Each number signifies the variance of the twelve seasonal factors com-puted separately for each of the years and securities shown.

NA = not available.

amplitude in 1957 for yields on lowest rated security groups is inevery case less than the amplitude for the corresponding highest ratedgroup; except for railroad bonds, this relationship holds in 1963 and1965 as well.39 Table 2-6 lists the correlation coefficients for thetwelve monthly factors in 1957 of each of the long-term groups ofsecurities with those of each of the other groups. In almost all cases

Column 3 of Table 2-4 shows that the seasonal accounts for a smallerpart of the total variation of low quality than of high quality bonds and thecyclical component accounts for a higher proportion (except for rails). Thisstudy is unable to explain the phenomenon.

TAB

LE 2

-6. C

oeff

icie

nts A

mon

g th

e Se

ason

al F

acto

rs in

195

7 fo

r All

the

Long

-Ter

m S

ecur

ities

Con

side

red

C.., 0 0 0 0 -t 0 0 0

Mur

sici

pals

Cor

pora

tes

Hig

hest

Low

est

Indu

stria

ls

Hig

hest

Low

est

U.S

.Tr

easu

ry

Long

3—5

Rai

lroad

s

Hig

hest

Low

est

Publ

icU

tiliti

es

Hig

hest

Hig

h G

rade

Hig

hest

Low

est

Serie

s(S

&P)

Rat

ing

Rat

ing

Rat

ing

Rat

ing

Rat

ing

Rat

ing

Term

Yea

rsR

atin

gR

atin

gR

atin

g

Mun

icip

als

Hig

hest

ratin

g.9

627

Low

est r

atin

g.9

385

.959

6C

orpo

rate

sH

ighe

st ra

ting

.964

4.9

349

.913

4Lo

wes

t rat

ing

.722

6.7

040

.756

8.8

263

Indu

stria

lsH

ighe

st ra

ting

.974

9.9

307

.906

7.9

660

.722

3Lo

wes

t rat

ing

.732

0.7

178

.752

9.8

196

.976

5.7

237

U.S

. Tre

asur

yLo

ng te

rm.9

222

.915

3.8

942

.879

3.7

708

.843

8.8

062

3—5

year

s.6

553

.851

4.8

163

.903

6.7

914

.844

0.8

251

.940

0R

ailro

ads

Hig

hest

ratin

g.9

370

.894

3.9

036

.956

8.8

654

.892

3.8

559

.9 1

63.9

346

Low

est r

atin

g.7

920

.698

6.7

568

.875

2.9

126

.808

4.9

168

.756

7.8

334

.899

3P

ublic

util

ities

Hig

hest

ratin

g.9

156

.919

4.8

980

.974

1.8

905

.905

7.8

749

.886

0.9

015

.946

9.8

597

Low

est r

atin

g.6

860

.725

2.7

452

.796

7.9

650

.696

2.9

5 12

.743

5.7

369

.801

5.8

152

.877

4

NO

TE: E

ach

coef

ficie

nt, b

ased

on

twel

ve o

bser

vatio

ns, i

s com

pute

d by

cro

ss c

orre

latin

g th

e tw

elve

fact

ors o

f the

ver

tical

and

horiz

onta

l ser

ies.

Dia

gona

l ele

men

ts a

re o

mitt

ed.

80 Essays on interest Rates

the coefficients exceed .7; in most they exceed .8; and in many theyexceed .9. The high correlations denote the substantial uniformity inthe seasonal patterns of the long-term yields during the period ofpeak seasonality. Moreover, in virtually every case the correlation be-tween any group of securities, say corporates and industrials, isgreater for comparisons among security groups of the same qualityrating. Along the last row, for example, the correlation between thefactors for the lowest rated version of the public utility group andthose for, say, industrials-lowest rating, is greater than the correlationbetween the former and industrials-highest rating. In the row above,the correlations between the factors for the highest rated public utilitygroup are greater in cases where the highest rated version of thepaired group is considered in place of the lowest rated version of thesame group. The correlations, of course, are not as high in years out-side the period of peak seasonality; nor is the characteristic just de-scribed as conspicuous. These figures are shown in Tables 2-7 and 2-8.

By far the lowest correlations are with the long-term Treasurysecurities in 1965. These low coefficients help substantiate the con-clusion that there is no seasonality in the series at the end of thestudy period. Evidence of uniformity is never more than suggestive.However, the more uniformity, the greater are the similarities amongindependently calculated results and the less likely are explanationsof any given result that depend on alleged accidents or quirks in thecomputation. In this sense the similarity of the seasonal patterns andthe curious relations among security groups of homogeneous ratingconstitute prima facie cases for the existence of a seasonal pattern,indictments, so to speak, on which it now behooves this study to ob-tain a conviction.

Before 1955 the typical seasonal pattern for yields on long-termsecurities describes low points in the first four months of the year andhighs for the remainder, excepting a slight dip below 100.0 in Novem-ber. The trough usually appeared in February or March, while thepeak varied between July a.nd December. The pattern changed in the1954—56 period to one with a slight high in January, a rapid fall to atrough usually in March, continued lows through July, then a steepincline to a peak in September, and finally a gradual decline to De-cember, still above the line. Table 2-9 lists the average seasonalfactors for yields on long-term securities for selected years, computedby arithmetically averaging the monthly factors for a given year, oneat a time, of the thirteen long-term series. The recorded Januaryfactor, for example, is the average of all the January factors for the

TAB

LE 2

-7.

Coe

ffici

ents

Am

ong

the

Seas

onal

Fac

tors

in 1

953

for A

ll th

e Lo

ng-T

enn

Secu

ritie

s Con

side

red

Mun

icip

als

Cor

pora

tes

Indu

stria

ls

Hig

hest

Low

est

U.S

.Tr

easu

ry

Long

3—5

Rai

lroad

s

Hig

hest

Low

est

Publ

icU

tiliti

es

Hig

hest

Hig

h G

rade

Hig

hest

Low

est

Hig

hest

Low

est

Serie

s(S

&P)

Rat

ing

Rat

ing

Rat

ing

Rat

ing

Rat

ing

Rat

ing

Term

Yea

rsR

atin

gR

atin

gR

atin

g

Mun

icip

als

Hig

hest

ratin

g.9

609

Low

est r

atin

g.7

981

.808

7C

orpo

rate

sH

ighe

st ra

ting

.867

9.7

863

.745

4Lo

wes

t rat

ing

Indu

stria

ls.7

224

.594

3.5

041

.811

4

Hig

hest

ratin

g.8

880

.826

8.8

020

.918

5.5

921

'

Low

est r

atin

gU

.S. T

reas

ury

.638

4.5

045

.457

7.7

622

.966

9.5

380

Long

term

3—5

year

s.7

881

.347

2.7

092

.187

9.8

303

.305

2.7

772

.609

7.6

281

.585

4.7

944

.426

9.5

338

.590

6.5

879

Rai

lroad

sH

ighe

st ra

ting

.705

6.5

705

.428

9.8

722

.902

1.7

061

.837

3.5

518

.550

5Lo

wes

t rat

ing

.731

6.6

001

.512

7.8

660

.977

4.6

681

.940

7.6

040

.579

2.9

6 19

Publ

ic u

tiliti

esH

ighe

st ra

ting

.846

8.7

739

.747

0.9

737

.816

5.8

522

.790

7.7

718

.673

9.8

037

.838

2Lo

wes

t rat

ing

.558

0.4

714

.426

6.6

534

.917

1.3

765

.933

1.4

897

.608

8.7

142

.854

8.7

272

NO

TE: S

ame

as T

able

2-6

.

TAB

LE 2

-8. C

oeff

icie

nts A

mon

g th

e Se

ason

al F

acto

rs in

196

5 fo

r All

the

Long

-Ter

m S

ecur

ities

Con

side

red

U.S

.Pu

blic

Mun

icip

als

Cor

pora

tes

indu

stria

lsTr

easu

ryR

ailro

ads

Util

lties

Hig

h G

rade

Hig

hest

Low

est

Hig

hest

Low

est

Hig

hest

Low

est

Long

3—5

Hig

hest

Low

est

Hig

hest

Serie

s(S

&P)

Rat

ing

Rat

ing

Rat

ing

Rat

ing

Rat

ing

Rat

ing

Term

Yea

rsR

atin

gR

atin

gR

atin

g

Mun

icip

als

Hig

hest

ratin

g.8

655

Low

est r

atin

g.8

308

.706

3C

orpo

rate

sH

ighe

st ra

ting

.683

7.7

054

.821

8Lo

wes

t rat

ing

.776

2.7

062

.817

4.9

384

Indu

stria

lsH

ighe

st ra

ting

.576

9.5

751

.673

2.9

535

.895

8Lo

wes

t rat

ing

.501

2.5

032

.376

0.6

152

.624

8.6

149

U.S

. Tre

asur

yLo

ngterm

—.0939

—.3798

—.0377

—.1206

.0191

.0169

—.4666

3—5 years

.2306

.0658

.5929

.591

1.55 10

.6210

.1167

.5138

Railroads

Highest rating

.3308

.1636

.6548

.6029

.5654

.5585

.1542

.2523

.8091

Lowest rating

.730

3.6

211

.841

8.8

538

.918

9.7

912

.343

5.1191

.5646

.6900

Public

utili

ties

Hig

hest

ratin

g.7

939

.750

4.8

317

.921

6.8

983

.883

3.6

508

—.1

121

.493

9.3

914

.760

7Lo

wes

t rat

ing

.543

3.3

077

.421

9.6

064

.720

5.7

434

.497

2.4

636

.553

0.4

100

.585

7.6

382

NO

TE: S

ame

as T

able

2-6

.

Seasonal Variation of Interest Rates 83TABLE 2-9. Average Seasonal Factors for Yields on Long-Term Securitiesfor Selected Years

1953 1957 1963 1965

January 99.3 100.4 100.1 99.8February 98.7 98.4 99.6 99.5March 98.8 97.9 99.3 99.6April 99.3 98.3 99.3 99.5May 100.4 98.6 99.3 99.4June 101.1 99.2 100.0 100.0July 100.7 99.4 100.4 100.4August 100.5 103.1 100.3 100.2September 101.1 102.5 100.7 100.6October 100.5 101.9 1,00.5 100.4November 99.8 101.2 100.3 100.1December 100.4 101.0 100.4 100.3

NOTE: The figures for each month are computed by arithmetically averaging theseasonal factors for that month of the thirteen long-term securities considered in thisstudy.

given year. In addition to the change in the seasonal pattern, thedifferences in the seasonal amplitude between the peak period in thelate fifties and that before and after the period are revealed as well.

While Table 2-9 adequately describes the general seasonal pattern,its evolution, and the order of magnitude involved, it necessarily ob-scures important differences in the several series. The high correlationsin Table 2-6 reveal a similarity in the patterns of most series during thelate fifties; although the considerable differences in amplitude revealedin Table 2-5 are not, of course, accounted for. The somewhat lowercorrelations in 1953 and the considerably lower ones in 1965 lessenthe usefulness of the computed average pattern outside the 1955—60period. In addition to the variety of patterns and amplitudes in thelong-term series, there are also differences in the quality of the esti-mates of the seasonal factors. To decide on the extent of appropriateadjustment for each series it is therefore necessary to examine thefamiliar charts of factors and SI ratios, which we do now.

Graphic Analysis of Seasonal Variation

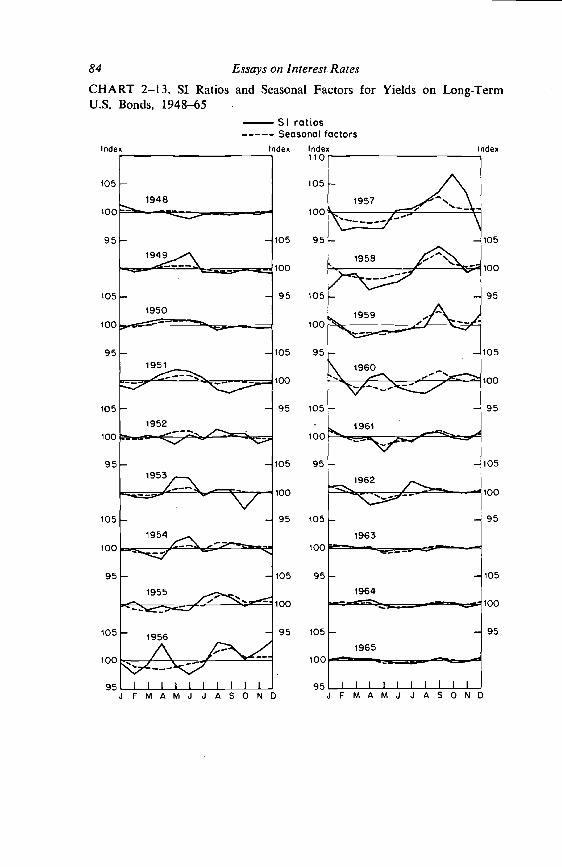

U.S. TREASURY SECURITIES. Chart 2-13 plots the seasonal factors andSI ratios for long-term U.S. Treasury securities (the scale is twicethat used for short-term securities). The pattern prior to 1953 is very

- - 95

1950 -- - 105

1951

100

- - 95

1952

- -105

100

95

- 1956 —

84 Essays on interest. RatesCHART 2—13. SI Ratios and Seasonal Factors for Yields on Long-TermU.S. Bonds, 1948—65

SI ratiosSeasonal factors

Index Index110

105

1948—

Index

105

100

Index

105

100

95

105

100

95

105

100

95

105

100

95

105

100

95

105

100

95

I 11111 liiiJFMAMJJASOND FM AMJ J AS

Seasonal Variation of Interest Rates 85

similar to the early pattern of commercial paper rates, the peak com-ing in midyear and the trough in the fall. Although the amplitude issmall, the pattern is quite real. The reason for the asserted realityresides not only in the similarity between the curves connecting theSI ratios and the ones connecting the factors but also in the positionof the factors, falling as they do between the SI ratios and the 100.0level. The latter result is most conspicuous for 1951 and has theeffect of both dampening the adjusted series and minimizing the possi-bility of the adjustment contributing to the random fluctation of theseries. As in the case of the Treasury bill rates during the late fifties,the assurance that all that is removed is seasonal comes at the expenseof understating what seasonal influence there is. The data for 1952provide a good example of the dilemma involved in adjusting a serieswith a rapidly shifting pattern: the two curves are virtually unrelated.Use of the estimated factors may then introduce random errors intothe series. In 1953 the pattern assumes the shape of the average pat-tern of Table 2-9 and, hence, the high correlations in Table 2-7 be-tween the long-term Treasuries and the other securities. In the follow-ing years the pattern rapidly bends into the one typical of all therates in the late fifties. Even in this period the fit is not very good,although the pattern is clearly there; and the amplitude is among thehighest of the long-term security groups. One notices, even in the latefifties, how the low part of the pattern is gradually extended throughthe summer, as with the short-term securities. By 1965 the pattern isvery different from the average pattern and, in fact, inversely corre-lated with those of most of the long-term series (Table 2-8). It isclear, then, that the low F statistic noted earlier for this series is dueboth to a constantly shifting pattern resulting in a mediocre fit and anunstable pattern even within the periods it describes. That a seasonalpattern existed in the late fifties and even that a systematic ripplepersisted to the end of the study period is, in this study's view, es-tablished. Whether there is reasonable cause to adjust the series Out-side the 1955—59 period is somewhat dubious; and whether it wouldbe meaningful to adjust a series for such a short period is equallydubious. This series is perhaps one that may be profitably left alone.

Chart 2-14 plots the seasonal factors and SI ratios for U.S. Treasurysecurities with three- to five-year maturities. There is a fairly clearpattern for the years 1948—60 followed by several years of erraticmovement—the pattern for 1953 is typical. In 1955 the patternassumes the shape it maintains for the remainder of the decade. In

SI rQtios— Seasonal factors

Index Index Index110 1

86 Essays on interest RatesCHART 2—14. SI Ratios and Seasonal Factors for Yields on U.S. Goyern-ment Three- to Five-Year Securities, 1948—65

48

901949—

Index

110

110-S. — — •_ —

-

RJU

90

ICC1950

90

110-

- 1951110

- 90

100

-11090-

110-

100

- 90

90- —110

100

110- -90

I I I I I I I I I I

J EMAM J J ASO NDthis period the seasonal amplitude of this series is somewhere betweenthe typical amplitude of short- and long-term securities. From 1960on, however, the seasonal pattern is too unstable to justify an adjust-ment.

120 Essays on Interest Rates

(such as income and expected changes in the price level) that de-termine demand are fixed, the demand curve is itself fixed, and theobserved changes in interest rates and money supply may be read aspoints along a given demand curve. The method breaks down, how-ever, when the same variables influence both the demand and the supplycurves (such as, the preponderance of the common cyclical com-ponent in the variables affecting both curves).60

The study of seasonal behavior in the money market partly alleviatesthis problem for two reasons: (1) The use of the ratios-to-movingaverage of the relevant variables, or the smoothed seasonal factors,abstracts from the common cyclical component. This method is, ofcourse, not peculiar to seasonal analysis. More importantly, (2) sea-sonal fluctuations in the demand for money are probably fairly stableover time; so that the seasonal shift in demand relative to the cyclicalcomponent of the shift from, say, November to December is relativelystable from year to year.°7 These seasonal shifts are determined byeconomic forces outside the control of the monetary authorities. Shiftscretion in the matter of seasonality and would bias the estimated elasticity ofdemand for credit, since a simultaneous solution would be required. I am in-debted to Walter Fisher for this point.

Using averages for cyclical stages Cagan is able to show an inverse rela-tionship between interest rates and changes in the money supply. (See hisChanges in the Cyclical Behavior of Interest Rates, Occasional Paper 100, NewYork, NBER, 1966; reprinted as Chapter 1 of this volume.) Note he relateschanges in money supply to levels of interest rates; whereas this study dealswith seasonal changes in both series.

Since demand per se is not observable, this proposition must be hypothe-sized rather than demonstrated. Some evidence in support of the propositionlies in the absence of any systematic variation in the seasonal amplitude ofGNP within the study period. The implicit seasonal factors for the fourthquarter, the period of peak seasonality in the GNP, are given below. The rawdata, of adjusted and nonajjusted series, are given in The National Income andProduct Accounts of the United Slates, 1929—1965, pp. 11 30.

Implicit Factors f,nplicit FactorsYear Fourth Quarter Year Fourth Quarter

1948 107.2 1957 106.01949 106.7 1958 105.91950 ]0$.7 1959 105.9

1951 1960 105,8

1952 105.6 1961 105.8

1953 1962 105.9

1954 105.6 1963 105.8

1955 105.3 1964 105.6

1956 105.9 1965 106.6

Seasonal Variation of Interest Rates 119supply of short-term credit in November results in a given interestrate, RN. In December there is an increase in the demand, depictedby the outward shift in the demand curve. If the Federal Reserve didnot increase the supply at all—that is, in the present context, if therewere no seasonal movement in the money supply—the rate of interestwould rise to At the other extreme, if the Federal Reserve hadfully anticipated the rise in demand and increased the supply of moneycorrespondingly (to S0), the rate of interest would remain at RN. Again,in the present context that would imply a relatively greater seasonalamplitude in the supply of money. Finally, if the Federal Reserveanticipated part but not all of the increase in demand, the rate wouldmove to some intermediate position—say, The necessary seasonalamplitude in the supply of money to effect any given interest, rateclearly would depend on the elasticity of demand for short-term credit:The more elastic the demand for short-term credit is with respect tothe interest rate, the greater must be the seasonal amplitude in monetsupply necessary to prevent the seasonal increases in demand fromimparting a seasonal variation to interest rates.