the shape of things to come - oliverwyman.com shape of things to come this report examines the...

TRANSCRIPT

Oliver Wyman is a global leader in management consulting that combines deep industry knowledge with specialized expertise in strategy, operations, risk management, and organization transformation.

For more information please contact the marketing department by email at [email protected] or by phone at one of the following locations:

AmericAS

+1 212 541 8100

emeA

+44 20 7333 8333

ASiA PAciFic

+65 6510 9700

copyright © 2013 Oliver Wyman

All rights reserved. This report may not be reproduced or redistributed, in whole or in part, without the written permission of Oliver Wyman and Oliver Wyman accepts no liability whatsoever for the actions of third parties in this respect.

The information and opinions in this report were prepared by Oliver Wyman. This report is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accountants, tax, legal or financial advisors. Oliver Wyman has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied. Oliver Wyman disclaims any responsibility to update the information or conclusions in this report. Oliver Wyman accepts no liability for any loss arising from any action taken or refrained from as a result of information contained in this report or any reports or sources of information referred to herein, or for any consequential, special or similar damages even if advised of the possibility of such damages. The report is not an offer to buy or sell securities or a solicitation of an offer to buy or sell securities. This report may not be sold without the written consent of Oliver Wyman.

www.oliverwyman.com

The ShAPe OF ThingS TO cOmeWhAT recenT hiSTOry TellS uS AbOuT The FuTure OF eurOPeAn bAnking

THE SHAPE OF THINGS TO COME 2

INTRODUCTION 4

1. INDUSTRY CONTEXT: THE GREAT SURVIVAL 71.1. SURPRISING RESILIENCE 7

1.2. GROUNDS FOR CONCERN 14

2. RETURNS, LEADERS AND LAGGARDS 182.1. THE COLLAPSE IN ROE 18

2.2. A CAUTIOUS OUTLOOK 20

2.3. SOVEREIGN INFLUENCE – THERE’S NO PLACE LIKE HOME 23

2.4. DELEVERAGING AND DECOUPLING 27

3. THE CHALLENGES FOR BANKS 303.1. A BOND OR EQUITY STRATEGY 30

3.2. GETTING DELEVERAGING AND DECOUPLING RIGHT 32

3.3. CHANNELLING INVESTMENT 34

CONTENTS

THE SHAPE OF THINGS TO COMEThis report examines the recent history of the European banking industry and attempts to outline some of the salient dynamics underway. These include the changes to the competitive landscape, the role of shadow banking, the relationship between banks and governments, the returns delivered to shareholders, and the agenda for senior industry executives. Anchored in a hard analytical and shareholder value lens, we try to extrapolate what we do and do not know about the shape of the industry emerging. Our key projections:

1. New competitive structures slow to emerge … but setting down long term roots … and capital formation in danger of drifting out of the core banking sector

Unexpectedly, change to the competitive environment has been slow. The crisis and subsequent response have actually reinforced barriers to entry. However, new competitors, small today, are beginning to accumulate and incumbents would be wise not to discount the medium term threat. More dramatically, significant equity value is being created at the periphery of the industry by non-banks delivering infrastructure and information based services. Banks need to wake up quickly to this trend to avoid significant transfer of value outside the traditional banking ambit.

2. Increasing role of non-banks in financing … and opportunities for some banks in making it happen

The risk to banks of large scale disintermediation has been exaggerated. If anything, banks now need to push for more disintermediation to overcome their own balance sheet constraints, by accelerating the deepening of bond markets and bringing more investors into loan markets. Banks that can learn to partner effectively with non-bank lenders will generate disproportionate

value from the growth of the ‘direct’ credit markets.

3. Deleveraging likely to accelerate … but remain more limited than many think

Asset disposals to date have been very low, principally due to public funding support, a bank-heavy credit intermediation market structure, the need for net interest margin to cover operating costs and a lack of appetite to take capital write-downs associated with asset sales. We anticipate these factors will continue to drag on restructuring. Nevertheless, balance sheet restructuring will accelerate, driven by a potentially very significant inflection point created by the Asset Quality Review (AQR), the focus by regulators on Capital Requirements Directive (CRD) IV leverage ratios and by investors increasingly pricing leverage into valuations. We also predict substantial technical optimisation of banks’ balance sheets to take place in the coming twelve months.

4. Smooth withdrawal of public capital and funding … decoupling to gather pace

European Central Bank (ECB) funding has peaked and governments are beginning to plan for share sales. As banks’ solvency is improved by the introduction of capital buffers and leverage ratios, the decoupling of sovereign and bank risk should accelerate, somewhat offsetting the slow progress of a Europe-wide resolution authority and the lack of clarity around resolution and ‘ring-fencing’. We do not underestimate the risk of discontinuities in funding markets, enhanced by recent loading of government debt on banks’ balance sheets. However, the balance of information points to a base case of orderly, if very gradual, decoupling. Banks will face strategic choices about how aggressively to use the decoupling levers at their disposal.

5. Improving returns and valuation … but

only for some

Returns are at historic lows, with further

downward pressure from regulatory change

to come. These returns are highly correlated

with country, driven by factors such as funding

costs, GDP growth and non-performing loan

(NPL) ratios. Valuation has taken a similar

path, overwhelmingly driven by country and

sovereign. However, as NPLs begin to normalise

and the decoupling of sovereign and bank risk

progresses, there will be more opportunity for

idiosyncratic bank strategies to affect returns and

valuations. Capitalisation and cost management

will be key. Well-capitalised banks will be able

to make targeted strategic choices to optimise

their portfolios, while effective cost reduction

will deliver higher returns in the low-growth

environment. As a result we expect to see greater

divergence of performance and reward as bank

strategies reassert their significance. The logic

of technology-led consolidation will become

powerful, but concerns over creating larger

banks will deter M&A. A European stability

mechanism and single supervisor may change

this and put medium-sized deals in developed

Europe back on the agenda further down the line.

6. ‘Utility’ banking increasingly attractive … though there will be rewards for the few

who can grow earnings power

We take a different view to much of the negative

commentary about regulators forcing banks to

become utilities. If delivering stable earnings

with a predictable risk profile, drawing out core

market operating profits and returning excess

capital through a high dividend policy is a

utility, then for many banks this will become an

attractive vision to embrace, and will be rewarded

by investors looking for bond-like returns.

That said, we anticipate a handful of banks

will push for more equity-like earnings growth

and, if successful, will be rewarded with higher

valuations. We see grounds for caution for the

many banks implicitly following a hybrid strategy,

such as a convertible bond strategy or a bond

strategy juiced with some yield enhancement.

7. Sharper operating models will emerge …

partnerships and outsourcing key

The battleground for much of the industry will

be cost effectiveness. Costs have risen across

the big incumbents by an average of €3.5BN

each since 2006, despite waves of attempted

cost reduction. More radical thinking has to take

root, built on bigger spend, channelling more

technology-focused capex and accelerating

branch consolidation to generate substantial

and sustainable returns. In particular, we expect

supply chains to emerge where much more of

the cost base of the industry is sourced from

utilities or third party specialists. New entrants

and emerging markets players could appear as

the early winners here.

8. Better customer service … at least for those

willing to pay

Most European banks have been forced to

concentrate on their home markets. As the

need to squeeze out gains from market share

increases and conduct regulation stamps out the

scope to exploit price elasticity, the focus on the

customer experience has become paramount.

We see senior banking executives obsessing, as

never before, about how to make the customer

experience more satisfying and hassle-free.

The flipside is in more sophisticated use of

segmentation, giving higher levels of service

only to those able and willing to pay for it.

INTRODUCTIONThe financial crisis of 2008 has been followed by

a long economic downturn and a sovereign debt

crisis in the Eurozone. You might expect European

banking to have undergone tumultuous change:

declining revenues, swathes of bank failures,

consolidation and a significant shift of market

share to non-Europeans, new entrants and

non-bank competitors.

Such expectations have been thoroughly

confounded. Industry revenues have rebounded

and stabilised well above their 2008 low. Although

RoEs have declined sharply, only a handful of

small European banks have been wound up.

Bank balance sheets have remained the same

size they were pre-crisis and the competitive

landscape has not materially changed.

Neither non-Europeans nor new entrants have

significantly dented market share. And, while

there has been some shift of lending towards

capital markets, disintermediation and the growth

of so-called shadow banking has been muted.

Of course, there are grounds for concern – the

most obvious being the role of government

intervention in creating this remarkable

stability. Otherwise-insolvent banks have been

recapitalised and the monetary policies of the

ECB and national central banks have allowed

banks to fund themselves at low cost. However,

while the risk of ‘zombie banks’ is real and credit

extension is still sluggish, in the larger non-

peripheral European economies dependence on

governmental support is declining. Especially for

the larger banks, private funding is now easier

to find. Banks are rebalancing their government

bond portfolios and governments are increasingly

thinking about withdrawing their capital.

Nevertheless, banks’ fortunes remain tightly

bound to their home countries in two ways.

First, the RoEs of banks from the same country

have converged as country-specific factors

such as GDP growth, funding costs and NPL

rates have driven returns. Only a handful of

banks have bucked this trend and delivered

noticeably better returns through strategic

portfolio selection, better footprint or strong

execution. Second, idiosyncratic differences

of strategy and execution are making little

difference to market valuations. Investors need

very strong evidence to materially distinguish

valuations for banks in the same country.

This will not go on forever. As regulatory reform

settles and NPLs start to normalise, decoupling

is likely to gather pace, putting more emphasis

on bank-specific factors in driving returns.

We already see evidence of investors starting

to take more notice of certain factors, such

as leverage and dividend policy, in valuation.

Sooner or later individual performance will

reassert itself in returns and this will be reflected

in market valuations.

European banks will have to contend with three

main challenges in 2014. The first challenge

is strategy selection, where banks have two

broad options. One is a bond-like strategy,

where maximum dividend capital is returned

to shareholders and the business model is

designed to deliver revenue that grows at

roughly the same rate as GDP within a ‘safe zone’

of core markets. The other option is an equity-

like strategy, positioning for more growth and

earnings upside by investing in new industry

sub-sectors, client segments or markets, or in

emerging markets simply targeting the white

space for growth. We raise concerns about the

wisdom of various ‘hybrid’ strategies we see in

the market today.

The second challenge is getting deleveraging and

decoupling right. Whilst limited deleveraging

has been seen to date, and there will continue to

be drags on balance sheet restructuring, we do

anticipate some modest acceleration as new CRD

IV leverage targets and the AQR start to impact

banks. The withdrawal of liquidity support and

the introduction of regional stability mechanisms,

resolution authorities and insurance schemes

will also naturally encourage decoupling of banks

from their sovereigns. Getting the capital plan

right, managing regulatory balkanisation, timing

the disposal of assets to free up capital for growth

and determining how far to pursue measures

such as issuing bail-in capital and restructuring

legal entities will be a difficult balancing act for

most CFOs. Some banks will be able to exploit the

opportunity to pick up assets at knock-down prices.

The third challenge is effectively channelling

enough investment into new technology

and operating models to deliver radical cost

reductions while improving the way customers

are served. As of today, we still see too many

banks planning against short payback horizons,

making incremental changes to cost structures

and continuing to play by yesterday’s rules

on customer propositions, when more radical

action is required.

We discuss these challenges in Section 3 of this

report. In Section 1 we describe the current

condition of the European banking industry

and in Section 2 we look at what is determining

the fortunes of leaders and laggards. As our

analysis shows, the idea that European banking

is in terminal decline is wrong. The sector has

proved surprisingly resilient. But the focus

needs to shift beyond ensuring its salvation

to discerning its future direction. Senior

executives, whose attention has been directed

toward regulatory compliance, must return to

the question of strategy.

“You might expect European banking to have undergone

tumultuous change: declining revenues,

swathes of bank failures, consolidation and a significant shift

of market share to non-Europeans, new

entrants and non-bank competitors. Such expectations

have been thoroughly confounded.”

THE SHAPE OF THINGS TO COME

6 Copyright © 2013 Oliver Wyman

NOTES:Europe: Throughout the report, unless explicitly stated

otherwise, ‘Europe’ includes countries in the EU28

(excluding Cyprus and Malta), Switzerland, Norway,

Russia and Turkey.

Corporate and Institutional Banking (CIB): Includes

products and services offered to mid-cap (annual

turnover ≥€25MM) and large corporate clients across

capital markets, investment banking, lending and

transaction banking.

Retail and Business Banking (RBB): Includes all

products and services related to retail customers (with

a net worth <€1MM excluding primary residence)

and small and mid-sized corporates (annual turnover

<€25MM), excluding bancassurance and distribution

fees for asset management.

Wealth and Asset Management (WAM): Includes private

banking services offered to high net worth segment

(defined as individuals with a net worth ≥€1MM

excluding primary residence) and asset management

for institutions.

Insurance: Includes both life and non-life insurance

products (inclusive of bancassurance) offered to

households and institutions. For insurance companies,

revenues have been estimated as follows to allow for

like-for-like comparison with banking revenue: Life

insurance revenues = Profit before tax + administration

and acquisition cost, Non-life insurance revenues =

Gross written premiums (net of reinsurance) – claims +

investment income.

Sample: The sample of banks used within this report

consisted of 100 European banks selected based on

total revenue size and to provide a sufficient number of

banks within each assessed region. For each separate

analysis the greatest number of banks possible has

been used, based on the availability of data. Sample is

available on request.

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 7

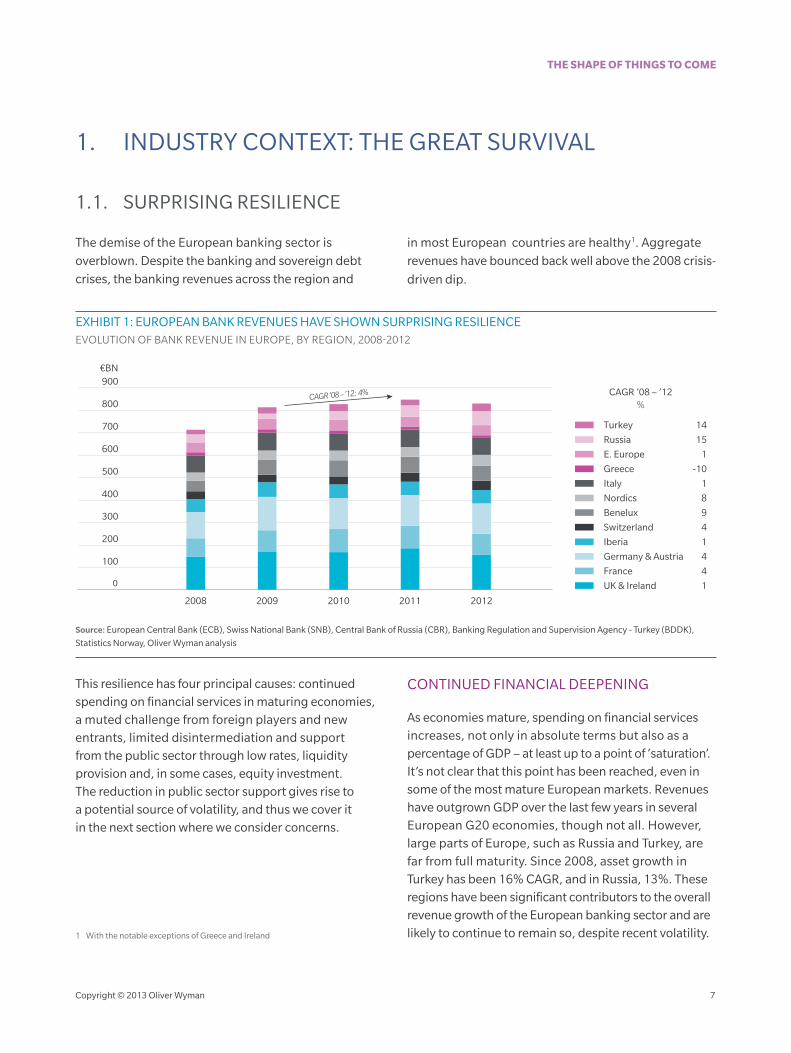

1. INDUSTRY CONTEXT: THE GREAT SURVIVAL

1.1. SURPRISING RESILIENCE

The demise of the European banking sector is

overblown. Despite the banking and sovereign debt

crises, the banking revenues across the region and

in most European countries are healthy1. Aggregate

revenues have bounced back well above the 2008 crisis-

driven dip.

EXHIBIT 1: EUROPEAN BANK REVENUES HAVE SHOWN SURPRISING RESILIENCEEVOLUTION OF BANK REVENUE IN EUROPE, BY REGION, 2008-2012

CAGR ’08 – ’12: 4%

€BN

500

600

300

400

200

100

700

800

2008 2009 2010 2011 2012

900

0 UK & Ireland 1

France 4

Germany & Austria 4

Iberia 1

Switzerland 4

Benelux 9

Nordics 8

Italy 1

Greece -10

E. Europe 1

Russia 15

CAGR ’08 – ’12%

Turkey 14

Source: European Central Bank (ECB), Swiss National Bank (SNB), Central Bank of Russia (CBR), Banking Regulation and Supervision Agency - Turkey (BDDK),

Statistics Norway, Oliver Wyman analysis

This resilience has four principal causes: continued spending on financial services in maturing economies, a muted challenge from foreign players and new entrants, limited disintermediation and support from the public sector through low rates, liquidity provision and, in some cases, equity investment. The reduction in public sector support gives rise to a potential source of volatility, and thus we cover it in the next section where we consider concerns.

CONTINUED FINANCIAL DEEPENING

As economies mature, spending on financial services increases, not only in absolute terms but also as a percentage of GDP – at least up to a point of ‘saturation’. It’s not clear that this point has been reached, even in some of the most mature European markets. Revenues have outgrown GDP over the last few years in several European G20 economies, though not all. However, large parts of Europe, such as Russia and Turkey, are far from full maturity. Since 2008, asset growth in Turkey has been 16% CAGR, and in Russia, 13%. These regions have been significant contributors to the overall revenue growth of the European banking sector and are likely to continue to remain so, despite recent volatility.1 With the notable exceptions of Greece and Ireland

THE SHAPE OF THINGS TO COME

8 Copyright © 2013 Oliver Wyman

EXHIBIT 2: REVENUE GROWTH POTENTIAL EXISTS, PARTICULARLY IN MATURING MARKETSBANK REVENUE BY SEGMENT AND REGION, 2012

60

80

40

120

100

140

160

20

0

€BN

Corporate & Institutional Banking

Retail & Business Banking

Wealth & Asset Management

Insurance

At average per capita*

Fran

ce

UK

& Ir

elan

d

Ben

elu

x

Ger

man

y &

Au

stri

a

Ital

y

Ru

ssia

Nor

dic

s

Swit

zerl

and

Gre

ece

Iber

ia

E. E

uro

pe

Turk

ey

2,300 1,500 1,400 1,300 2,300 400 1,9001,000 400 5,200 400 800Per capita€

7.5 4.6 4.7 5.0 6.4 3.9 4.04.9 4.4 8.4 5.5 4.7% of GDP

Source: International Monetary Fund (IMF), Eurostat, Central Intelligence Agency (CIA) fact book, Oliver Wyman analysis

* “At average per capita” is calculated by estimating additional revenue that could be expected if region achieved average European per capita revenues

MUTED CHALLENGE FROM FOREIGN PLAYERS AND NEW ENTRANTS

Competition from new entrants has been muted by the high cost of entry and expansion, especially given recent regulations. Retail entry requires scale, both for distribution purposes and to reduce the unit cost of brand-creation. Servicing large corporates has traditionally relied upon a relationship model, with weak lending economics offset by better returns elsewhere. However, specialist segments (e.g. financial sponsors) have attracted entrants. Traded markets in Europe continue to face a raft of shifting regulation, such as the financial transaction tax and bonus caps, which makes investment payback uncertain and wards off significant investment by new or foreign players.

‘Euro convergence’ prior to 2006 encouraged an expansion of cross-border banking across Europe. The

national location of lending or investment seemed increasingly irrelevant. The crisis put a stop to this. Non-domestic banks have withdrawn from the worst-hit countries, such as Greece, and private savings have flowed from those nations into safer countries, such as Germany. The anticipated tapering of the Federal Reserve bond-buying programme is also seeing investors retreat from riskier assets, adding recent impetus to this trend, particularly in emerging markets.

Similarly, the threat from non-traditional competitors has not proved as great as might have been expected. Many corporates and investor groups remain reluctant to launch or become banks, put off by the associated risks and regulation. Those that have entered banking

have largely pursued niches, such as payments, or

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 9

entered via partnerships with banks and insurers.

These players have remained small. For example, Tesco

Bank’s loans to customers total approximately £5.5BN,

less than 0.5% of the UK Personal Lending Market.

After a brief flurry of digital-only entrants, such as

ING Direct, Digital is now just another channel that

customers expect all suppliers to offer. Current trends

favour multi-channel offerings, which banks are better-

positioned to provide.

Whilst there are several players that have successfully

entered the market, these remain small in relation

to the banking sector and it seems unlikely that this

would change substantially in the near term. However,

these smaller players have demonstrated particular

strengths in gaining approval in a tough regulatory

environment. Starting with clean balance sheets and

with the potential to scale, we expect these challengers

could make an impact on the market and enhance

competition over time, though more on a seven to ten

year horizon.

As a result, not only have total banking revenues within

Europe remained resilient, so too has European banks’

share of this market (see Exhibit 4). Banks capture ~75%

of financial services revenues in Europe and European

banks capture ~88% of that total banking revenue: that

is, European banks capture 70% of the total financial

services revenue available, a figure which has not

shifted materially in five years.

EXHIBIT 3: POTENTIAL BANK DISRUPTERS – NEW ENTRANTS

COMPETITION TYPE EXAMPLES COMMENTS

Retailers Sainsbury’s Bank, Tesco Bank, Carrefour Banque, Financiera El Corte Inglés, ICA Banken

•Financial services targeted at existing consumer base to support principal retail offerings; another element of becoming a ‘one-stop-shop’ for customer needs

•Vanilla product offerings (little appetite to take on extra risk / capital requirements)

Brand-led offerings/new entrants/carve-outs

Virgin Money, Ikanobank (Ikea), Metrobank, TSB •More appetite to grow beyond existing customer base

•Key challenge is getting to scale

Car manufacturers Volkswagen, Audi, Peugeot, Ford •Relatively stable and limited market presence to support sales; limited footprint (especially in city centres) from which to establish branch structure

•Significant expansion not expected

Online/digital-only ING Direct, AXA Banque •Digital-only players being squeezed as digital channel becomes accepted norm, expected of all players

Non-traditional service providers Paypal, Zopa, Kickstarter •Successful, although small, in single-product offering

•Expansion into other products likely to only ever be ancillary to main offering

Source: Oliver Wyman research

THE SHAPE OF THINGS TO COME

10 Copyright © 2013 Oliver Wyman

EXHIBIT 4: EUROPEAN BANKS CAPTURE THE VAST MAJORITY OF BANKING REVENUES IN EUROPE, AND A SIGNIFICANT PROPORTION OF THE TOTAL FS REVENUETOTAL EUROPEAN REVENUE, 2012

1,000

400

200

600

800

European FSrevenue

Europeanbanking

revenues

Europeanbanks'

Europeanrevenues

1,200

€BN

Retail & BusinessBanking

Corporate &InstitutionalBanking

Wealth & Asset Management

Insurance

0

Source: Oliver Wyman analysis

EXHIBIT 5: FINANCIAL INTERMEDIATION IN EUROPE IS DOMINATED BY BANKSBANK ASSETS AND FINANCIAL ASSETS AS A PROPORTION OF GDP, BY GEOGRAPHIC REGION, 2012

BANK ASSETS/GDP FINANCIAL ASSETS/GDP

2.5 7.50

3.5 10.00

2.0 6.25

1.5 5.00

3.0 8.75

1.0 3.75

0.5 1.25

Europe Australia Canada Japan United States

4.0 11.25

00

Bank assets/GDP

Financialassets/GDP

Source: IMF, World Bank, ECB, Economist Intelligence Unit (EIU), Federal Reserve, Federal Deposit Insurance Corporation (FDIC), Oliver Wyman analysis

Note: US bank assets have been increased by a constant factor of 55%, based on estimates from the FDIC, to compensate for differences between GAAP and IFRS accounting rules

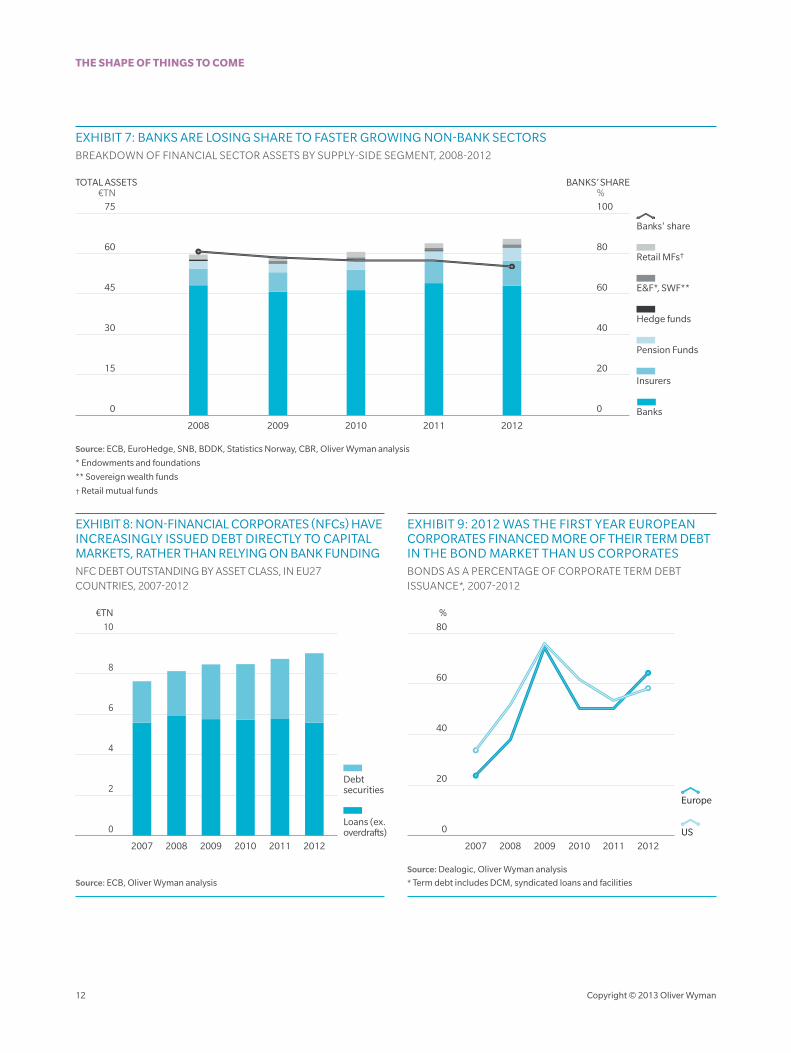

LIMITED THREAT FROM DISINTERMEDIATION

The assets of European banks have traditionally represented a much larger proportion of GDP than the banking sectors of other mature economies. This is not because more financial activity occurs in Europe but because financial intermediation has been dominated by bank balance sheets. This remains true today - the proportion of transfers from savers to borrowers intermediated by banks has been shrinking very slowly.

The assets of the European banking sector have not changed materially in absolute terms since the crisis. However, while banks’ assets have remained flat, they are losing share to faster-growing non-banks, such as insurers and pension funds (see Exhibit 7).

We expect further growth – for example savers will continue to switch to asset managers in search of yield, and non-banks look likely to provide additional funding in specialist sub-sectors such as Commercial Real Estate Finance and Leveraged Buyouts, as evidenced by recent Collateralised Loan Obligation activity. Nevertheless, these competitors continue to have a small share of the market in traditional banking products and services, and do not currently pose a significant threat to the banking sector.

Moreover, banks are still the principal arrangers and underwriters of such non-bank financing, facilitating the flow of money from investors to borrowers. Thus the banking sector remains an important element of the value chain for this growing part of the market.

Some of the trend is cyclical. Large European and multi-national corporates have traditionally relied on bank funding rather than issuing bonds directly into the capital markets. Since the crisis, however, banks’ funding has come under pressure and they have become more reluctant to use their balance sheets. Simultaneously, corporates have been offered cheap credit in capital markets – often cheaper than for equivalently rated banks. They have thus increasingly issued bonds to yield-hungry investors struggling in a low interest rate environment – though this has typically been distributed by banks. 2012 was the first year that European corporates financed a greater proportion of their term debt in the bond market than US corporates did.

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 11

EXHIBIT 6: ABSOLUTE LEVEL OF EUROPEAN BANK ASSETS HAS REMAINED REMARKABLY STABLEEVOLUTION OF EUROPEAN BANK ASSETS, 2008-2012

30

40

20

10

0

50€TN

2008

2012

Ger

man

y &

Au

stri

a-6

Ben

elu

x

-5

Fran

ce

-1

Gre

ece

-3

E. E

uro

pe

1

Ital

y

1

Iber

ia

16

Turk

ey

2

Swit

zerl

and

4

Ru

ssia

13

Nor

dic

s

6

UK

& Ir

elan

d

3

Tota

l net

chan

ge

0CAGR ’08 – ‘12%

Source: ECB, CBR, BDDK, SNB, Statistics Norway, Oliver Wyman analysis

Note: ECB defines European bank assets as the total consolidated assets of domestic banking groups and stand alone banks, foreign (EU and non-EU) controlled subsidiaries and foreign (EU and non-EU) controlled branches of European countries, therefore assets of European branches or subsidiaries of European banking groups based outside their home country will be double counted

“The threat of the shadow banking sector to earnings

and intermediation has proven overblown. As leverage

constraints kick in, the banks have every incentive to

find ways to finance their issuer clients without

consuming balance sheet.”

THE SHAPE OF THINGS TO COME

12 Copyright © 2013 Oliver Wyman

EXHIBIT 7: BANKS ARE LOSING SHARE TO FASTER GROWING NON-BANK SECTORSBREAKDOWN OF FINANCIAL SECTOR ASSETS BY SUPPLY-SIDE SEGMENT, 2008-2012

30 40

15 20

45 60

60 80

2008 2009 2010 2011 2012

00

75 100

TOTAL ASSETS €TN

BANKS’ SHARE%

Banks

Insurers

Pension Funds

Hedge funds

E&F*, SWF**

Retail MFs†

Banks' share

Source: ECB, EuroHedge, SNB, BDDK, Statistics Norway, CBR, Oliver Wyman analysis

* Endowments and foundations

** Sovereign wealth funds

† Retail mutual funds

EXHIBIT 8: NON-FINANCIAL CORPORATES (NFCs) HAVE INCREASINGLY ISSUED DEBT DIRECTLY TO CAPITAL MARKETS, RATHER THAN RELYING ON BANK FUNDINGNFC DEBT OUTSTANDING BY ASSET CLASS, IN EU27 COUNTRIES, 2007-2012

4

2

6

8

2007 2009 2010 20112008 2012

10

€TN

0Loans (ex.overdrafts)

Debtsecurities

Source: ECB, Oliver Wyman analysis

EXHIBIT 9: 2012 WAS THE FIRST YEAR EUROPEAN CORPORATES FINANCED MORE OF THEIR TERM DEBT IN THE BOND MARKET THAN US CORPORATESBONDS AS A PERCENTAGE OF CORPORATE TERM DEBT ISSUANCE*, 2007-2012

20

0

80

60

40

2007 2008 2009 2010 2011 2012

%

US

Europe

Source: Dealogic, Oliver Wyman analysis

* Term debt includes DCM, syndicated loans and facilities

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 13

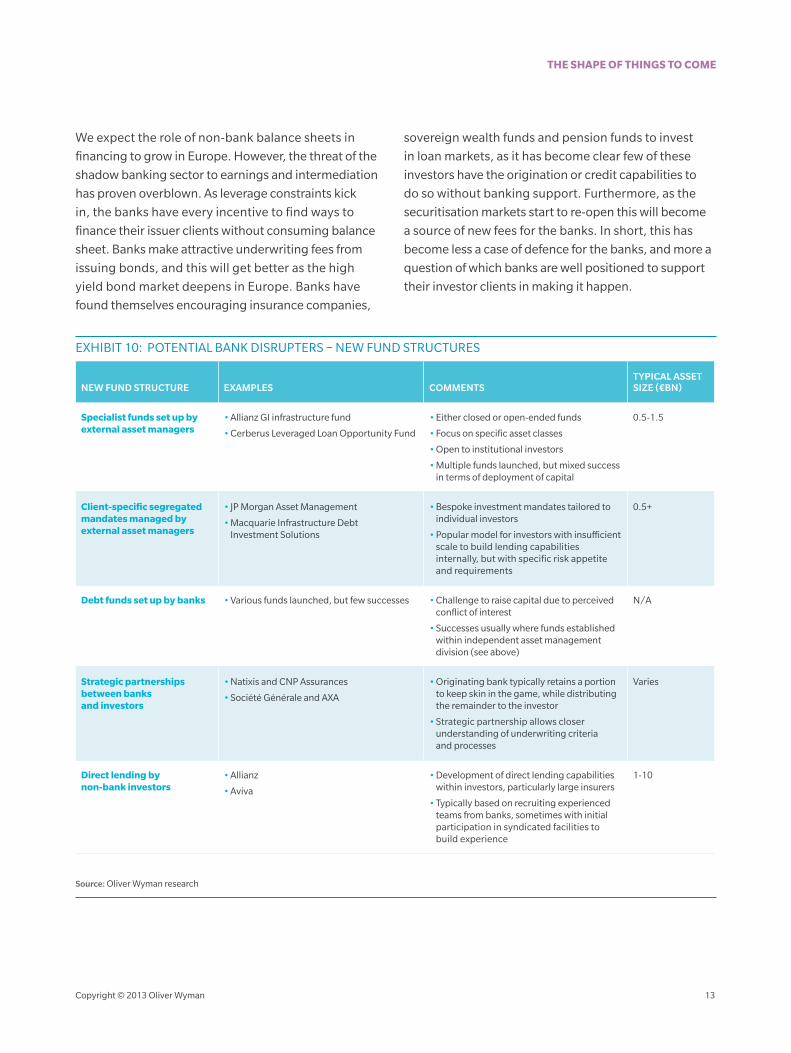

We expect the role of non-bank balance sheets in

financing to grow in Europe. However, the threat of the

shadow banking sector to earnings and intermediation

has proven overblown. As leverage constraints kick

in, the banks have every incentive to find ways to

finance their issuer clients without consuming balance

sheet. Banks make attractive underwriting fees from

issuing bonds, and this will get better as the high

yield bond market deepens in Europe. Banks have

found themselves encouraging insurance companies,

sovereign wealth funds and pension funds to invest

in loan markets, as it has become clear few of these

investors have the origination or credit capabilities to

do so without banking support. Furthermore, as the

securitisation markets start to re-open this will become

a source of new fees for the banks. In short, this has

become less a case of defence for the banks, and more a

question of which banks are well positioned to support

their investor clients in making it happen.

EXHIBIT 10: POTENTIAL BANK DISRUPTERS – NEW FUND STRUCTURES

NEW FUND STRUCTURE EXAMPLES COMMENTSTYPICAL ASSET SIZE (€BN)

Specialist funds set up by external asset managers

•Allianz GI infrastructure fund

•Cerberus Leveraged Loan Opportunity Fund

•Either closed or open-ended funds

•Focus on specific asset classes

•Open to institutional investors

•Multiple funds launched, but mixed success in terms of deployment of capital

0.5-1.5

Client-specific segregated mandates managed by external asset managers

• JP Morgan Asset Management

•Macquarie Infrastructure Debt Investment Solutions

•Bespoke investment mandates tailored to individual investors

•Popular model for investors with insufficient scale to build lending capabilities internally, but with specific risk appetite and requirements

0.5+

Debt funds set up by banks •Various funds launched, but few successes •Challenge to raise capital due to perceived conflict of interest

•Successes usually where funds established within independent asset management division (see above)

N/A

Strategic partnerships between banks and investors

•Natixis and CNP Assurances

•Société Générale and AXA

•Originating bank typically retains a portion to keep skin in the game, while distributing the remainder to the investor

•Strategic partnership allows closer understanding of underwriting criteria and processes

Varies

Direct lending by non-bank investors

•Allianz

•Aviva

•Development of direct lending capabilities within investors, particularly large insurers

•Typically based on recruiting experienced teams from banks, sometimes with initial participation in syndicated facilities to build experience

1-10

Source: Oliver Wyman research

THE SHAPE OF THINGS TO COME

14 Copyright © 2013 Oliver Wyman

1.2. GROUNDS FOR CONCERN

Although banking revenues have been remarkably

resilient since 2008, there are causes for concern. Chief

amongst these are dependence on the state, reduced

access to attractive markets and a shift in value to areas

not traditionally within the ambit of banks.

DEPENDENCE ON THE STATE

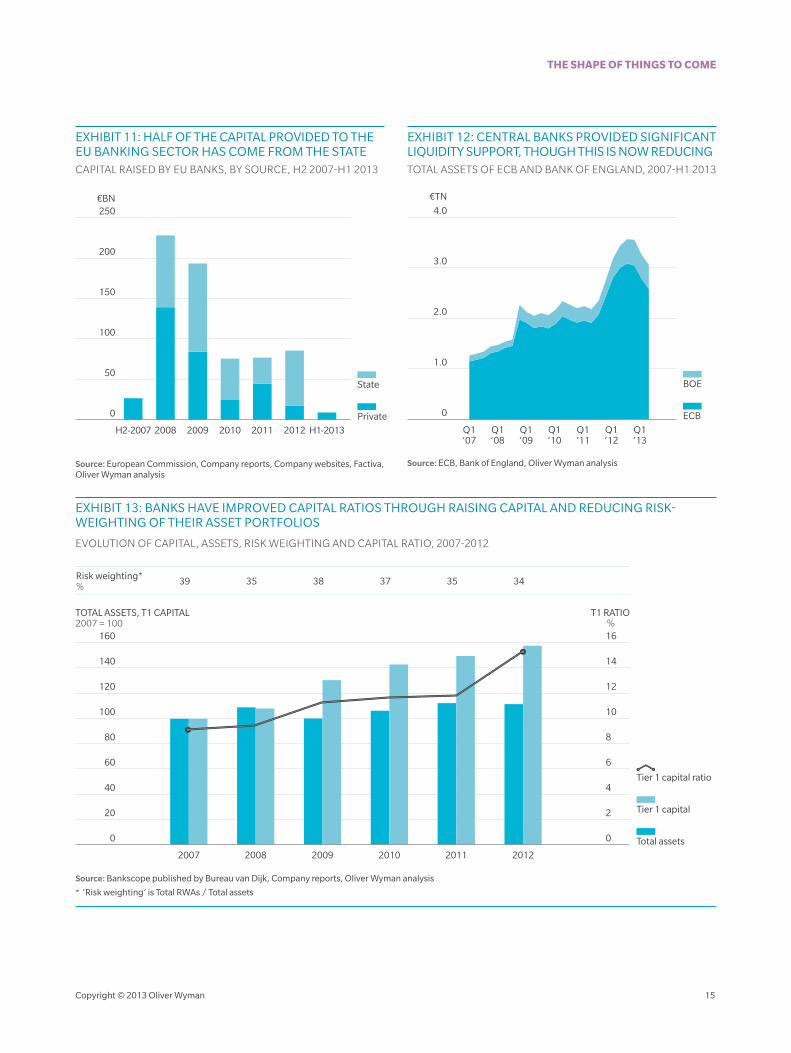

State injections of tax-funded capital, intended to

avert economic calamity by ensuring that banks could

continue to play their role intermediating credit flows,

have provided vital support to banks in recent years. We

calculate that since 2007 European banks have raised

€700BN of capital, of which €350BN has come from

the public sector. While maintaining critical solvency,

this has also prompted some banks to hold assets they

would otherwise have been forced to sell.

Banks have also taken steps to reduce the risk-weighting

of their asset portfolios. As a result, the assets of our

sample of banks actually increased over the period. For

many banks, this would have been impossible without

the state support they received.

In fact, total state support approved for the EU financial

sector since the Lehman default totals more than €5TN,

equivalent to 40% of GDP. Of this, €1.5TN had been used

by the end of 2011, with guarantees forming the largest

part of this aid. While these guarantees revitalised bond

markets, enabling banks to issue bonds and raise funds,

they also led to sovereign stress (especially in Ireland)

and helped create a sovereign-bank feedback loop,

which still plagues the market, and which we examine

further in the next section.

Most European governments have no desire to be long-

term investors in the sector. However, they have so far

been unable to exit because most banks are in no position

to repay their state investors and RoEs are generally

below the level at which governments could regain their

investment. Thus, only about 10% of the original capital

injected has been repaid, meaning that total public sector

ownership of European banks now stands at 17% of total

equity2 . While there is some fresh activity in this space,

such as the recent announcements regarding Lloyds

Banking Group, there remains a long way to go.

By comparison, the US Federal government injected

$250BN3 of capital into its banks through the

Troubled Asset Relief Program (TARP), which at its

height amounted to 17% of total equity, an equivalent

proportion to Europe today. Almost all of this has

been repaid, however, so that the outstanding TARP

capital now amounts to 1% of total US bank equity. The

relative health of the US banking system, with early and

aggressive write-downs, is an interesting counterpoint

to the European system and one that policy makers

should constantly challenge themselves against.

Beyond capital support, there has been extensive

monetary and funding support. Central bank balance

sheets exploded over the last four years as asset

purchase schemes, Quantitative Easing (QE) and

collateral windows were used to restore confidence and

keep interbank markets functioning. Although these

balance sheets have now begun to shrink, central banks

remain committed to providing liquidity to the debt

markets. The support provided by central banks has

contributed to favourable funding conditions for banks;

the withdrawal process will be difficult to manage and

will likely take significant time. Nevertheless, the process

has started and we remain hopeful it can continue

without severe discontinuities.

2 It should be noted that not all of the principal injected is expected to be repaid due to insolvencies

3 Source: SIGTARP Quarterly Report to Congress, July 24th 2013

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 15

EXHIBIT 11: HALF OF THE CAPITAL PROVIDED TO THE EU BANKING SECTOR HAS COME FROM THE STATECAPITAL RAISED BY EU BANKS, BY SOURCE, H2 2007-H1 2013

100

50

150

200

H2-2007 2008 2009 2010 2011 2012 H1-2013

0

250€BN

Private

State

Source: European Commission, Company reports, Company websites, Factiva, Oliver Wyman analysis

EXHIBIT 12: CENTRAL BANKS PROVIDED SIGNIFICANT LIQUIDITY SUPPORT, THOUGH THIS IS NOW REDUCINGTOTAL ASSETS OF ECB AND BANK OF ENGLAND, 2007-H1 2013

0 ECB

BOE

2.0

1.0

3.0

4.0

€TN

Q1‘07

Q1‘08

Q1‘09

Q1’11

Q1‘10

Q1‘12

Q1‘13

Source: ECB, Bank of England, Oliver Wyman analysis

EXHIBIT 13: BANKS HAVE IMPROVED CAPITAL RATIOS THROUGH RAISING CAPITAL AND REDUCING RISK-WEIGHTING OF THEIR ASSET PORTFOLIOS

EVOLUTION OF CAPITAL, ASSETS, RISK WEIGHTING AND CAPITAL RATIO, 2007-2012

80 8

120 12

100 10

60 6

40 4

20 2

140 14

2007 2008 2009 2010 20122011

00

160 16

TOTAL ASSETS, T1 CAPITAL2007 = 100

T1 RATIO%

Total assets

Tier 1 capital

Tier 1 capital ratio

39 35 38 37 35 34Risk weighting*%

Source: Bankscope published by Bureau van Dijk, Company reports, Oliver Wyman analysis

* ‘Risk weighting’ is Total RWAs / Total assets

THE SHAPE OF THINGS TO COME

16 Copyright © 2013 Oliver Wyman

BALKANISATION IS PUTTING PRESSURE ON BANKS TO PULL OUT OF POTENTIALLY ATTRACTIVE MARKETS AND BUSINESS LINES

Rising fixed costs and trapped capital and funding are encouraging many banks to exit markets in which they are subscale. While opportunities abroad may be attractive, many large banks are concluding that they will be unable to achieve the requisite scale to succeed in an appropriate timeframe and are thus choosing to exit. In other cases, such as AIB and KBC, foreign disposals are a condition of state aid.

Within Europe, the pre-crisis expansion of cross-border banking is thus now in reverse. Banks are cutting their foreign exposure and decamping for home. Over €1TN of assets have been repatriated since 2007.

European banks have also retreated from non-European foreign markets. For example, their US assets have declined by 20%, driven in part by reduced onshore presence of subscale investment bank divisions. This withdrawal has been prompted by the increased regulatory burden driving up unit costs and a shortage of US dollar funding for some. They are also beginning to repatriate lending from emerging markets as interest rate and foreign exchange risks increase globally.

This is all part of the same theme - banks are shedding non-core international businesses in an attempt to focus

resources and boost group-wide returns. For example, Nordea has agreed the sale of its Polish banking, financing and life insurance operations to PKO, and Erste has sold its Ukrainian subsidiary to FIDOBank.

Only banks that achieved scale prior to the crisis have been able to maintain growth strategies abroad. This includes European investment banks with long-established global scope (such as Barclays and Deutsche Bank) and banks from countries with historic links to emerging markets, such as Spanish banks in Latin America.

On one hand the discipline here can be applauded - it’s hard to argue with banks focusing on their core markets and what they do best. However, balkanisation carries a cost in less efficient trapped capital and funding. In some cases this is resulting in stronger banks exiting attractive markets, where their capital should be able to make good returns, support local growth, assist in channelling needed foreign capital into markets and drive the cost of capital down through greater competition with domestic banks.

This also raises a real concern for emerging economies

starved of bank capital, which are now facing their own

crises as investor capital heads for home.

EXHIBIT 14: OVER €1TN OF LOAN ASSETS HAVE BEEN REPATRIATED SINCE 2007EXTERNAL LOANS HELD BY BANKS, BY COUNTRY OF DOMICILE OF BANK, 2007-2012

€TN

6

8

2

4

10

2007 2008 2009 2010 2011 2012

12

0

% CHANGE ’07 – ‘12

UK & Ireland -8

Germany & Austria -20

France -3

Benelux -14

Iberia -10

Switzerland -52

Nordics 36

Italy -9

Greece -8

Turkey -27% change ’07 – ’12: -13%

Source: Bank of International Settlements (BIS), Oliver Wyman analysis

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 17

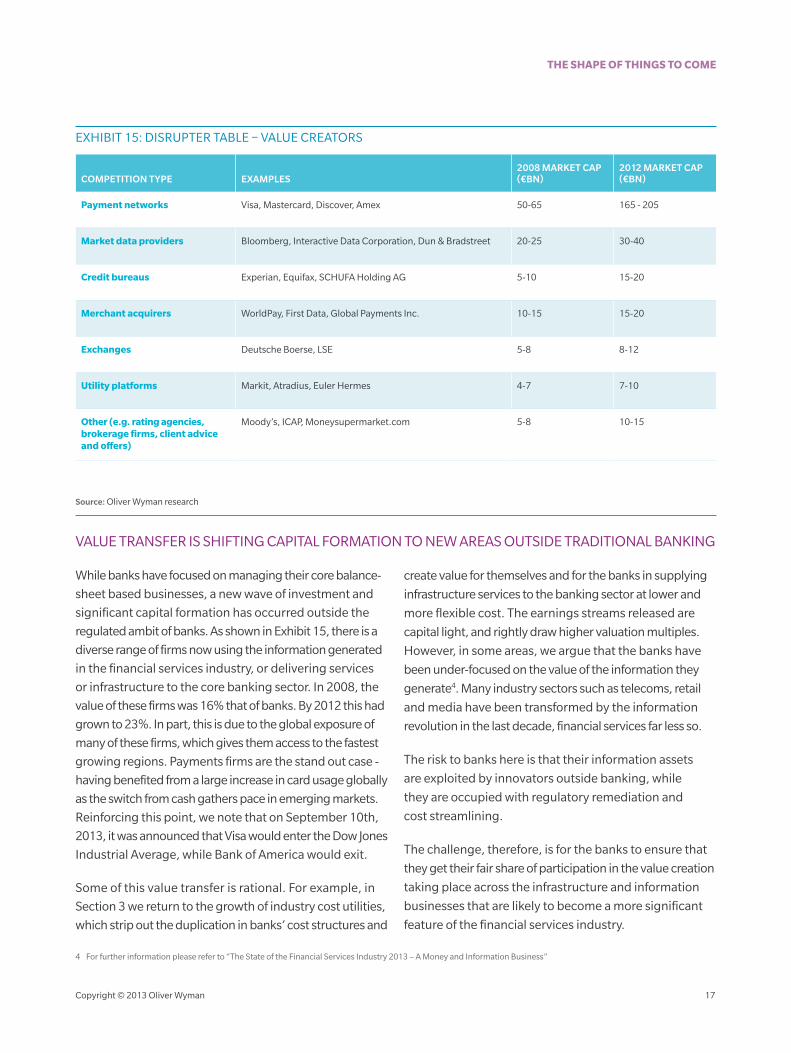

EXHIBIT 15: DISRUPTER TABLE – VALUE CREATORS

COMPETITION TYPE EXAMPLES2008 MARKET CAP (€BN)

2012 MARKET CAP (€BN)

Payment networks Visa, Mastercard, Discover, Amex 50-65 165 - 205

Market data providers Bloomberg, Interactive Data Corporation, Dun & Bradstreet 20-25 30-40

Credit bureaus Experian, Equifax, SCHUFA Holding AG 5-10 15-20

Merchant acquirers WorldPay, First Data, Global Payments Inc. 10-15 15-20

Exchanges Deutsche Boerse, LSE 5-8 8-12

Utility platforms Markit, Atradius, Euler Hermes 4-7 7-10

Other (e.g. rating agencies, brokerage firms, client advice and offers)

Moody’s, ICAP, Moneysupermarket.com 5-8 10-15

Source: Oliver Wyman research

VALUE TRANSFER IS SHIFTING CAPITAL FORMATION TO NEW AREAS OUTSIDE TRADITIONAL BANKING

While banks have focused on managing their core balance-

sheet based businesses, a new wave of investment and

significant capital formation has occurred outside the

regulated ambit of banks. As shown in Exhibit 15, there is a

diverse range of firms now using the information generated

in the financial services industry, or delivering services

or infrastructure to the core banking sector. In 2008, the

value of these firms was 16% that of banks. By 2012 this had

grown to 23%. In part, this is due to the global exposure of

many of these firms, which gives them access to the fastest

growing regions. Payments firms are the stand out case -

having benefited from a large increase in card usage globally

as the switch from cash gathers pace in emerging markets.

Reinforcing this point, we note that on September 10th,

2013, it was announced that Visa would enter the Dow Jones

Industrial Average, while Bank of America would exit.

Some of this value transfer is rational. For example, in

Section 3 we return to the growth of industry cost utilities,

which strip out the duplication in banks’ cost structures and

create value for themselves and for the banks in supplying

infrastructure services to the banking sector at lower and

more flexible cost. The earnings streams released are

capital light, and rightly draw higher valuation multiples.

However, in some areas, we argue that the banks have

been under-focused on the value of the information they

generate4. Many industry sectors such as telecoms, retail

and media have been transformed by the information

revolution in the last decade, financial services far less so.

The risk to banks here is that their information assets

are exploited by innovators outside banking, while

they are occupied with regulatory remediation and

cost streamlining.

The challenge, therefore, is for the banks to ensure that

they get their fair share of participation in the value creation

taking place across the infrastructure and information

businesses that are likely to become a more significant

feature of the financial services industry.

4 For further information please refer to “The State of the Financial Services Industry 2013 – A Money and Information Business”

THE SHAPE OF THINGS TO COME

18 Copyright © 2013 Oliver Wyman

2. RETURNS, LEADERS AND LAGGARDS

2.1. THE COLLAPSE IN ROE

Returns for European banks have collapsed, from highs

of ~20% in 2006 to ~4% in 2012. This is a result of large

provisions for NPLs, a flood of other extraordinary

charges (primarily for restructuring and conduct-related

fines), significantly increased equity-to-asset ratios and

insufficient reduction of operating costs.

The small growth of aggregate industry operating profits has been contributed almost exclusively by banks with positive exposure to high growth emerging markets or who are domestic players in emerging markets, in particular Russia and Turkey.

The cost base of the larger industry players has risen 30% in absolute terms since 2006, equivalent to a CAGR of 4% over the period. For the top 20 European banks the average increase in cost base was €3.5BN or 28%; for the top 50 banks the average increase was almost €2BN or 30%.

This is not because banks have been ignoring costs. On the contrary, most banks are on their second or third round of cost cutting. But the results have disappointed. This is partly because the rise in regulatory and compliance costs has swamped reductions and partly because many of the programmes have targeted tactical headcount reduction (which is quick and cheap) rather than longer term platform overhaul, which is costly and often takes more than three years to repay. Alas, tactical cost reductions are rarely sustainable and the rise in compliance spend is here to stay. As a result, operating costs have remained stubbornly high.

While operating margins have been stable, provisions have been anything but. Provisions for NPLs have significantly reduced earnings, almost quadrupling since 2006. The largest 20 banks in Europe posted provisions of just over €1BN each in 2006 and close to €4.5BN each

in 2012. At the same time, other so called one-off costs have proved enduring, with restructuring costs and industry fines contributing significantly over the period. The combination of provisions for NPLs and these other extraordinary cost items has increased 17x since 2006.

Finally, the increased capital required to satisfy

regulatory demands has further depressed returns.

Common equity in the sector has increased by 75%

in the last six years, on more or less static revenue.

“Returns for European banks have collapsed,

from highs of ~20% in 2006 to ~4% in

2012. This is a result of large provisions

for NPLs, a flood of other extraordinary

charges, significantly increased equity-

to-asset ratios and insufficient reduction of

operating costs.”

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 19

EXHIBIT 16: ROE* HAS DECLINED DRAMATICALLY, FROM 20% IN 2006 TO 4% IN 2012RELATIVE IMPACT OF DRIVERS OF ROE DECLINE, 2006-2012

15

10

5

20

0

25

%

2006 RoE

Operatingmargin

growth**

Rise inloan

losses

Increasein other

extraord.cost items

Taxreduction

Rise inequity

2012RoE

Source: Bankscope published by Bureau van Dijk, Company reports, Oliver Wyman analysis

* RoE is calculated as Net income /Average common equity

** Growth in operating margin almost exclusively contributed by banks with positive exposure to high growth emerging markets or who are domestic players in emerging markets

EXHIBIT 17: INCREASED CAPITAL TO MEET REGULATORY DEMANDS HAS FURTHER DEPRESSED RETURNSROE* DECLINE AND EQUITY EVOLUTION, 2006-2012

10

5

15

20

-5

0

25

RoE

ROE%

80

40

120

160

-40

0

200

COMMON EQUITY 2006 = 100

‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

Averagecommonequity

Source: Bankscope published by Bureau van Dijk, Company reports, Oliver Wyman analysis

* RoE is calculated as Net income / Average common equity

EXHIBIT 18: EUROPEAN BANKS’ OPERATING COSTS HAVE INCREASED 30% SINCE 2006 EVOLUTION OF EUROPEAN BANK OPERATING COSTS AND ASSETS, 2006-2012

2006 = 100

50

100

150

2006 2007 2008 2009 2010 2011 2012

0

Total % change ’06-’12

No change inoperating margin

Total assets 30

Total operatingexpenses

30

Other operatingexpenses

39

Personnelexpenses

22

Total assets

Personnelexpenses

Other operating expenses

Source: Bankscope published by Bureau van Dijk, Oliver Wyman analysis

THE SHAPE OF THINGS TO COME

20 Copyright © 2013 Oliver Wyman

2.2. A CAUTIOUS OUTLOOK

Looking ahead, we expect the continued implementation

of new regulation to drag further on returns. However,

we anticipate three positive tailwinds from normalisation

in NPLs, reduction in extraordinary items and improved

capital management. Effective cost management, which

has proved challenging to date, will be a drag for some,

but those that can make it work will see the benefits in

their returns.

The total cost of the regulatory programme is not yet

fully visible in current returns. With implementation

extending to 2018 (and beyond), this will lead to a

further drag on returns over the coming years. We

expect this drag from five principal sources: the final

implementation of increased capital requirements,

‘ring-fencing’ and resolution plans (which will increase

funding costs), the financial transaction tax in the

Eurozone, conduct policy implementation (which

will increase costs and reduce revenues) and the full

go-live on central counterparty clearing (which will

reduce revenues from market-making). There remain

uncertainties on most of these issues, but we estimate

that they will suppress returns by a further 2%-4% over

the coming period.

The outlook for NPLs and their impact on returns is more

positive, though improvement will be gradual.

Outside-in NPL estimation is hard – and no two crises

are the same. However, using prior crises as a ready

reckoner suggests it will be some time before NPL

levels normalise. Assuming Western European NPLs

have peaked, history suggests a further one to four

years before NPL levels normalise. However, NPL levels

at banks in Western Europe over the first half of 2013

suggest the time to recovery could be even longer. In

Eastern Europe, again assuming the peak has been

reached (given that GDP has returned to pre-crisis

levels), recovery may not come until after 2018. In the

periphery5 it does not appear that the peak has yet been

reached. Given the height NPLs have already reached in

these countries, a return to normality must be some way

off. The timing will depend on the successful resolution

of the European crisis, which will allow economic

stabilisation and a sustainable recovery.

A gradual improvement in NPLs feeds directly into bank

returns. We estimate that, for every 50bps reduction

in NPLs, RoE improves by 1%-1.5%, implying a full

normalisation of NPLs in Europe could translate into 4%-

6% sustainable improvement in returns.

Reductions in other extraordinary items also translate

directly into returns. They have cost the largest 20

banks in Europe €1BN per bank per year on average

over the last three years. We expect the existing issues,

such as derivatives and insurance mis-selling and index

manipulation, to continue to drag for at least one or

two years. But if the industry can reduce the frequency

of such events to pre-crisis levels (a big if), this would

translate into a 2%-3% benefit to returns.

“Looking ahead, we expect the continued

implementation of new regulation to drag

further on returns. However, we anticipate three positive tailwinds

from normalisation in NPLs, reduction

in extraordinary items and improved

capital management.”5 Periphery includes Greece, Ireland, Italy, Portugal and Spain

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 21

EXHIBIT 19: COMPARING NPL RATIO* EVOLUTION IN THE CURRENT CRISIS WITH THAT IN PREVIOUS CRISES SUGGESTS A RETURN TO NORMALITY IS STILL SOME WAY OFF

PREVIOUS CRISES %

18

T+2T-1 T T+1 T+3 T+4 T+5 T+6 T+7

16

14

12

10

2

4

6

8

0

2008

2009

2010

2011

2012

2013

E

2014

E

2016

E

2015

E

18

16

14

12

10

2

4

6

8

0

CURRENT CRISIS %

Not clear that peak in NPLs has yet beenreached in periphery

Argentina’00s

Spain’90s

Japan’00s

Germany’00s

US’90s

WesternEurope†

EasternEurope**

Periphery††

Belgium‘00s

Source: Bank of Spain, FRED, IMF, World Bank, OECD, ECB, Oliver Wyman analysis

* NPL ratio is total non-performing loans / total loans. Regional NPL ratio is a weighted average, using total commercial bank loan weights

** Eastern Europe includes Turkey and Russia. Czech Republic has been removed due to lack of data

† Switzerland has been removed due to lack of data

†† Periphery includes Greece, Ireland, Italy, Portugal and Spain

Note: “T” is 1993 for Spain, 1991 for the US, 2001 for Argentina, Belgium and Japan and 2002 for Germany. The speed of decline was calculated using the CAGR of previous

post-crisis NPL recoveries

As regulatory capital has become scarcer, banks have focused on making the best use of it. We expect this to partially offset the cost of increased capital minima and thus have a small positive impact on returns.

We believe that the aggregate impact of these items will get the industry to just above the cost of capital (circa 7%-9%). This leaves us with two big open questions.

The first is what happens to operating margins. We

believe that for the most part, revenues will rise with

GDP, which means margin improvement will be driven

by cost effectiveness. Banks have had several years to

contemplate cost reduction and yet they have been

unsuccessful in achieving sustainable reductions to

date. Many banks are undertaking significant cost

reduction and restructuring programmes, but these are

not planned to result in savings for some years to come.

Most programmes announced in the last year or so have

targets set for three to four years in the future (2015-

16), with many requiring significant investments to be

made in the meantime. In addition, many of these cost

programmes appear highly ambitious when compared

to past performance.

Across a sample of seven recently announced cost

programmes with target cost-income ratios, the

average targeted reduction in cost-income ratio is

10% over the next three years . This is greater than

any such reduction observed across the same sample

since 1998 (see Exhibit 20). The largest decline in

cost-income ratio over a three year period since 1998

was 7%, between 2002 and 2005. During this period,

revenue growth outstripped cost growth by a factor

of two (revenue CAGR was 11%). With revenues likely

constrained in the coming years, such a large reduction

in cost-income ratio will therefore require fundamental

shifts in operating model to support the targeted cost

reductions. However, it is unclear how these shifts will

be achieved given limited budget to invest in the types

of programmes likely required.

THE SHAPE OF THINGS TO COME

22 Copyright © 2013 Oliver Wyman

EXHIBIT 20: COST PROGRAMMES WITH ANNOUNCED COST-INCOME RATIO TARGETS APPEAR AMBITIOUS WHEN COMPARED WITH PAST PERFORMANCEEVOLUTION OF OPERATING COST, TOTAL REVENUE AND COST-INCOME RATIO,1998-2015E*

OPERATING COST, TOTAL REVENUE €BN

COST-INCOME RATIO %

200 65

150 60

100 55

50 50

250 70

0 45

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2009

2010

2011

2013

E

2014

E

2008

2012

2015

E

Total revenue

Operating cost

Cost-income

Source: Company reports, Company websites, Capital IQ, Oliver Wyman analysis

* Estimated cost-income ratio is based on a linear approximation of the stated 10% target reduction

Note: Based on 7 European banks with publically announced cost savings programmes with a target cost-income ratio

Whilst we do believe that some banks will be successful in reducing cost-income ratios by 10%, for the industry as a whole this is not achievable. A reduction of 3%-5% seems more credible. This would translate into a further 1%-2% improvement in RoE, leaving the aggregate industry RoE at 9%-11%.

The second question relates to the interest rate environment. Interest rates will rise, though the timing of this remains far from certain. The dynamics of rising rates are complex: most commercial and retail banks will benefit in the medium term, though there is a risk of rising NPL levels in some economies. Some of the wholesale banking divisions may suffer on trading book inventories in the short term. We anticipate a long term positive with some transitional pain for some. Either way, the longer term imperative to reduce costs will remain.

We also note that the most obvious means to improve system-wide returns would be significant consolidation and thereby reduced capacity, particularly in deals that are led by technology synergies. However, given the cost of capital associated with climbing the

global systemically important financial institutions (G-SIFI) size list, value creation becomes very hard at the large end of the M&A scale. Not to mention the minimal interest that regulators or governments have in allowing banks to become larger.

This is an industry-wide view. Footprint, strategy and management effectiveness will drive potentially high variations around these averages; we focus on some of these drivers over the remainder of the report.

“Whilst we do believe that some banks will be

successful in reducing cost-income ratios by 10%, for the industry

as a whole this is not achievable.”

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 23

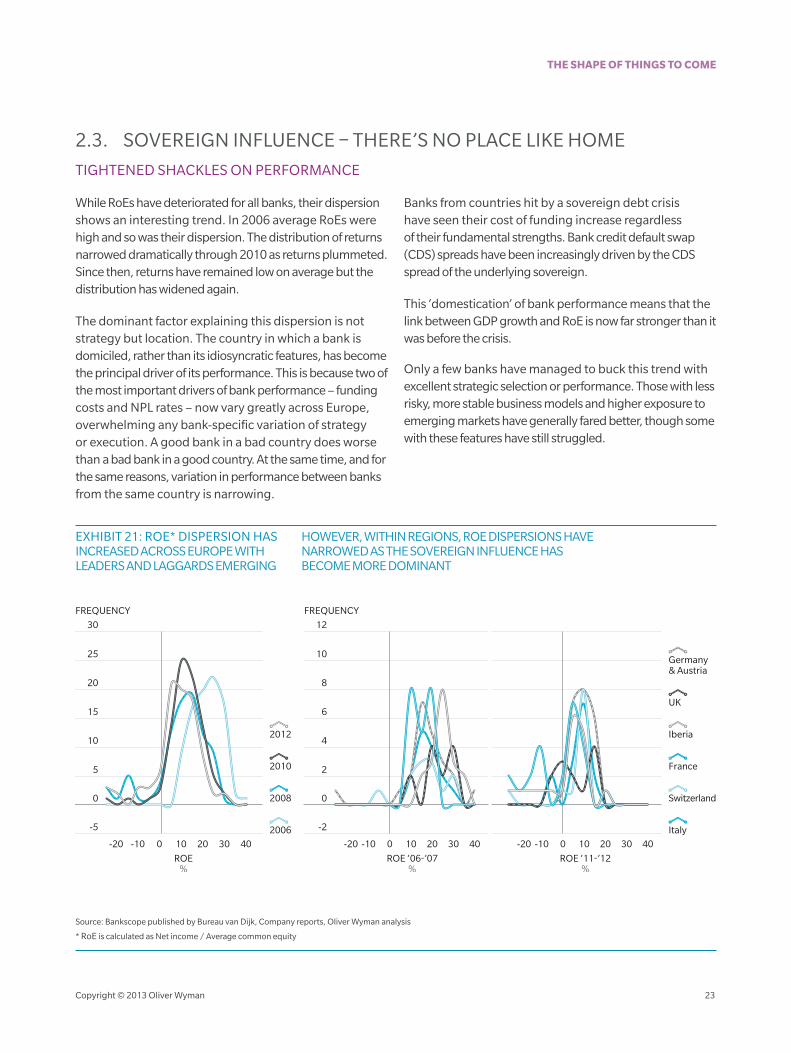

2.3. SOVEREIGN INFLUENCE – THERE’S NO PLACE LIKE HOME

TIGHTENED SHACKLES ON PERFORMANCE

While RoEs have deteriorated for all banks, their dispersion shows an interesting trend. In 2006 average RoEs were high and so was their dispersion. The distribution of returns narrowed dramatically through 2010 as returns plummeted. Since then, returns have remained low on average but the distribution has widened again.

The dominant factor explaining this dispersion is not strategy but location. The country in which a bank is domiciled, rather than its idiosyncratic features, has become the principal driver of its performance. This is because two of the most important drivers of bank performance – funding costs and NPL rates – now vary greatly across Europe, overwhelming any bank-specific variation of strategy or execution. A good bank in a bad country does worse than a bad bank in a good country. At the same time, and for the same reasons, variation in performance between banks from the same country is narrowing.

Banks from countries hit by a sovereign debt crisis have seen their cost of funding increase regardless of their fundamental strengths. Bank credit default swap (CDS) spreads have been increasingly driven by the CDS spread of the underlying sovereign.

This ‘domestication’ of bank performance means that the link between GDP growth and RoE is now far stronger than it was before the crisis.

Only a few banks have managed to buck this trend with excellent strategic selection or performance. Those with less risky, more stable business models and higher exposure to emerging markets have generally fared better, though some with these features have still struggled.

EXHIBIT 21: ROE* DISPERSION HAS

ROE%

20-10 0 10 30 40-20

-5

30

25

0

20

10

5

15

FREQUENCY

ROE ‘06-’07%

20-10 0 10 30 40-20

-2

12

10

0

8

4

2

6

FREQUENCY

ROE ‘11-’12%

20-10 0 10 30 40-20

Italy

Switzerland

France

Iberia

2006

2008

2010

2012

UK

Germany & Austria

Source: Bankscope published by Bureau van Dijk, Company reports, Oliver Wyman analysis

* RoE is calculated as Net income / Average common equity

HOWEVER, WITHIN REGIONS, ROE DISPERSIONS HAVE NARROWED AS THE SOVEREIGN INFLUENCE HAS BECOME MORE DOMINANT

INCREASED ACROSS EUROPE WITH LEADERS AND LAGGARDS EMERGING

THE SHAPE OF THINGS TO COME

24 Copyright © 2013 Oliver Wyman

EXHIBIT 22: THE RELATIONSHIP BETWEEN GDP GROWTH AND ROE HAS STRENGTHENED POST-CRISISAVERAGE GDP GROWTH VS. AVERAGE ROE, 2006-2007 AND 2010-2012

10

0

30

20

-10

-20

40

10

0

30

20

-20

40

-10

1050-5

AVERAGE GDP GROWTH ‘10-’12%

Correlation = 21%

1050-5

Correlation = 61%

AVERAGE GDP GROWTH ‘06-’07%

AVERAGE ROE ’06-’07 %

AVERAGE ROE ’10-’12 %

Source: Bankscope published by Bureau van Dijk, Company reports, IMF, Oliver Wyman analysis

Note: Chart shows relationship between bank RoE and real GDP growth in the bank’s home country. RoE is Net income / Average common equity

EXHIBIT 23: THE SOVEREIGN INFLUENCE ON BANK FUNDING COSTS HAS BECOME INCREASINGLY DOMINANTCHANGE IN SOVEREIGN CDS AS A % OF BANK CDS

40

80

120

160%

Germany

France

Spain

Portugal

Italy

Q2 '10 - Q2 '12

SOVEREIGNDEBT CRISIS

Q2 '12 - Q2 '13

POST-ECBSUPPORT

Q2 '07 - Q2 '09

CREDITCRISIS

0

Source: Thomson Reuters, Oliver Wyman analysis

Note: Change in sovereign CDS as a % of banks’ CDS is calculated as the change in sovereign CDS / the average change in the CDS of the country’s banks

EXHIBIT 24: EVOLUTION OF NPL RATIOS* HAS VARIED WIDELY BY REGION

NPL RATIO %

20

0

15

10

5

Nordics

France

UK & Ireland

E. Europe**

Italy

Turkey

Iberia

Russia

Greece

Benelux

Germany & Austria

‘06 ‘07 ‘08 ‘10 ‘11‘09 ‘12

Source: IMF Global Financial Stability report, World Bank, OECD, ECB, Oliver Wyman analysis

* NPL ratio is total non-performing loans / total loans. Regional NPL ratio is a weighted average, using total commercial bank loan weights

** E. Europe includes Turkey and Russia. Czech Republic has been removed due

to lack of data

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 25

EXHIBIT 25: THE NUMBER OF EUROPEAN BANKS TRADING AT A DISCOUNT TO BOOK VALUE HAS INCREASED DRAMATICALLY SINCE THE CRISIS PERCENTAGE OF BANKS TRADING AT DISCOUNT TO BOOK VALUE, 2006-2012

40

60

20

80%

2006 2007 2008 2009 2010 2011 2012

0

Source: Thomson Reuters, Capital IQ, Oliver Wyman analysis

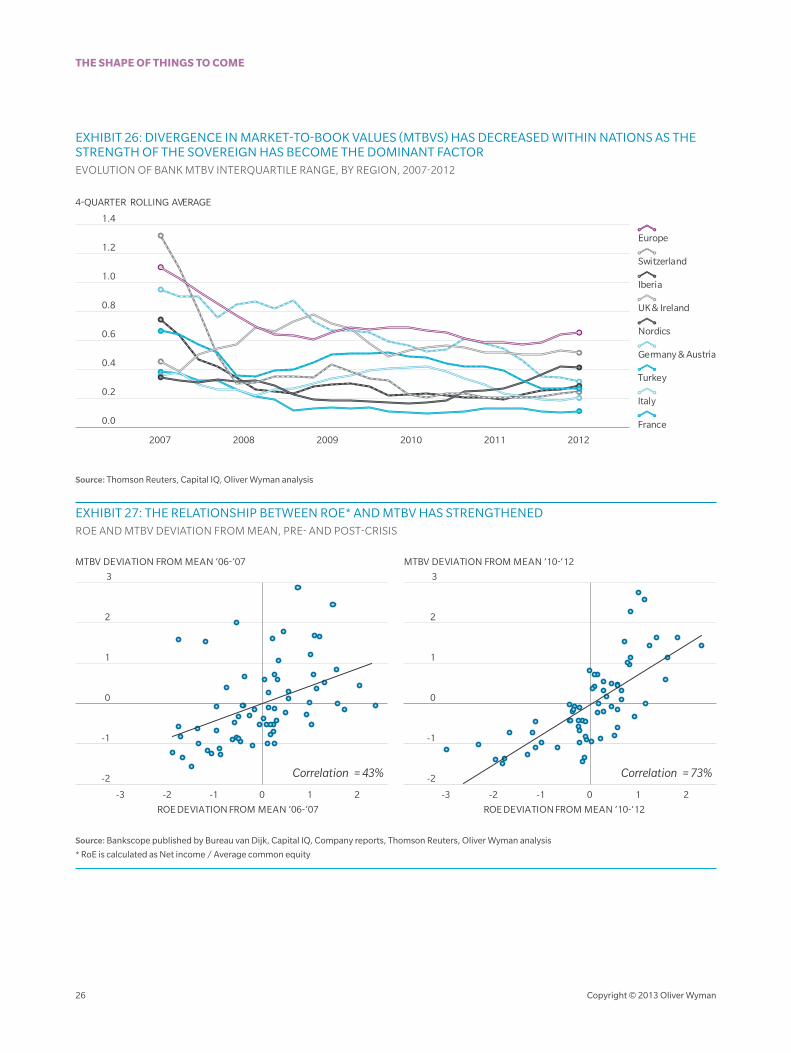

THE LINK BETWEEN VALUATION AND LOCATION

Market valuations, like RoEs, have declined dramatically since 2006 with most banks now trading at a discount to their book value.

As with RoE, the decline in bank value has been driven by country of domicile, largely reflecting the economic strength of the government. Average market-to-book values (MTBVs) have declined with sovereign credit ratings. And, as with RoEs, the dispersion of MTBVs for banks from the same country has narrowed.

Because this approach to valuation gives little weight to variations in banks’ long-term strategies, the relationship between current RoE and MTBV has become tighter.

However, there are signs that investors are beginning to pay greater attention to factors other than geography, such as leverage. In our sample, banks with better leverage ratios have received a modest MTBV premium given RoE. Examining the relationship between average RoE and MTBV over the period 2010-2012 we found that the average leverage ratio of banks receiving a MTBV premium was 6.1% compared with 4.9% for those below the trendline.

Strategic clarity also appears to have been rewarded in

recent months. For example, Deutsche Bank received

a positive boost to its share price on announcing

definitive action to raise capital and UBS’s restructuring

actions were positively received. However, we expect

strategic or other idiosyncratic factors to remain muted

influences on valuations until the sovereign decoupling

is further advanced.

“There are signs that investors are beginning to pay greater attention

to factors other than geography.”

THE SHAPE OF THINGS TO COME

26 Copyright © 2013 Oliver Wyman

EXHIBIT 26: DIVERGENCE IN MARKET-TO-BOOK VALUES (MTBVS) HAS DECREASED WITHIN NATIONS AS THE STRENGTH OF THE SOVEREIGN HAS BECOME THE DOMINANT FACTOR EVOLUTION OF BANK MTBV INTERQUARTILE RANGE, BY REGION, 2007-2012

2007 2008 2010 20112009 2012

0.6

0.4

0.2

0.0

1.4

1.2

1.0

0.8

4-QUARTER ROLLING AVERAGE

France

Germany & Austria

Iberia

Italy

Nordics

Switzerland

Turkey

UK & Ireland

Europe

Source: Thomson Reuters, Capital IQ, Oliver Wyman analysis

EXHIBIT 27: THE RELATIONSHIP BETWEEN ROE* AND MTBV HAS STRENGTHENEDROE AND MTBV DEVIATION FROM MEAN, PRE- AND POST-CRISIS

210-1-2-3

ROE DEVIATION FROM MEAN ’10-‘12

Correlation = 43%

210-1-2-3

Correlation = 73%

ROE DEVIATION FROM MEAN ’06-’07

MTBV DEVIATION FROM MEAN ’06-’07 MTBV DEVIATION FROM MEAN ’10-‘12

1

-1

0

2

-2

3

1

-1

0

2

-2

3

Source: Bankscope published by Bureau van Dijk, Capital IQ, Company reports, Thomson Reuters, Oliver Wyman analysis

* RoE is calculated as Net income / Average common equity

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 27

2.4. DELEVERAGING AND DECOUPLING

WHAT NEXT ON THE DELEVERAGE STAND-OFF?

We noted in Section 1 that the banking sector’s balance

sheet remained largely undiminished over the last five

years, and potential buyers of bank assets have been

serially disappointed by the lack of opportunities. A

stand-off has set in, where few sellers are willing to part

with assets at the prices on offer.

The most obvious explanation for this is the liquidity

provided by central banks, coupled with incentives

to buy domestic government bonds and to lend to

other domestic borrowers. Additionally, the European

credit intermediation market structure remains

widely dominated by banks, leaving limited room

for deleveraging levels comparable to US standards.

Yet banks have two further reasons to avoid asset

reduction. First, as fixed costs have proved difficult to

bring down, banks have been very reluctant to lose

assets that generate net interest margin to help cover

costs. Second, tightly capitalised banks have been

reluctant to incur accounting losses through asset

disposals, preferring to work them out over time. We

believe these conditions will continue to impact the

scale of asset reductions in the deleverage programme

in Europe. However, we anticipate that the stand-off

will relax and we are likely to see a significant increase

in balance sheet restructuring, driven by two factors.

The first factor is the new regulatory focus on CRD IV

leverage ratio. Many banks in Europe have become

highly leveraged. Using published figures for core tier 1

equity and total IFRS assets to calculate a proxy for the

CRD IV leverage ratio across our sample of banks, reveals

that a small but significant proportion of European

banks do not satisfy the proposed 3% minimum leverage

ratio, even on this basis.

The second factor is the impending Eurozone AQR, which

may also accelerate deleveraging, particularly in the most

challenged economies. Spain presents an interesting case

study in this regard. The transparency and confidence

introduced by a rigorous stress test carried out in 2012

has resulted in a wave of asset sales, restructuring and

consolidation that is rapidly putting the banking sector

on a more stable footing.

“The banking sector’s balance sheet has remained largely undiminished over the last five years. A stand-off has set in, where

few sellers are willing to part with assets at the prices on offer.”

THE SHAPE OF THINGS TO COME

28 Copyright © 2013 Oliver Wyman

THE DECOUPLING QUANDARY

The high degree of sovereign influence on returns

and valuations raises important questions around

decoupling. By decoupling we mean the scope for the

performance, risk profile and valuation of the banks to

separate from their sovereign, and indeed vice versa.

Banks and governments have a number of inherent

links. Banks have been large beneficiaries of the

significant government liquidity and equity injections.

Government balance sheets are now directly exposed

to the performance of the banking sector through these

injections. In addition, the broader economy is reliant on

a functioning banking system to support growth, which

in turn impacts government deficit positions. Both now

seek to decouple their fortunes. Much of this is in the

hands of the public sector. First, through central banks

managing an orderly withdrawal of public funding and

capital and tapering of QE, though these will be highly

challenging tasks. Second, through the establishment

of the much discussed European stability mechanisms,

resolution authorities and insurance schemes.

However, the banks have levers too, which we expect

to come more forcefully into play. The ramp up of bail-in

programmes, finalisation of Recovery & Resolution

plans and push to get ahead of the regulatory agenda

on legal entity structure are all tasks we see as having a

material impact on decoupling and therefore on each

bank’s ability to drive more idiosyncratic performance

and valuation.

Naturally the banks that have led on these initiatives

have been those for whom decoupling offers the

greatest immediate upside - typically those either in

economies with outsized banking sectors relative to

GDP (where regulators have been keen to encourage

decoupling), or where banking stability outstrips

sovereign stability, limiting the costs of the move. At

the other end of the spectrum, pressure to push the

decoupling agenda has been lower for struggling banks.

Currently the linkage is very much two-way. Many

banks own big government bond portfolios as part of

their liquid asset buffers and more generally on the

balance sheet. This connection further strengthens the

sovereign/bank credit feedback loop. The purchase of

these bonds by domestic banks has been crucial to the

sovereign’s ability to refinance itself.

Decoupling is likely to gather pace – as more banks

loosen the sovereign ties pressure will mount on the

slower movers. Laggards will start to bump up against

the timetable for finalisation of resolution plans and, in

some jurisdictions, the deadlines for ring-fencing.

The decoupling agenda is complex and will remain

opaque and political. Nevertheless, it is a key strategic

theme across the industry.

“The decoupling agenda is complex and will

remain opaque and political. Nevertheless, it

is a key strategic theme across the industry.”

THE SHAPE OF THINGS TO COME

Copyright © 2013 Oliver Wyman 29

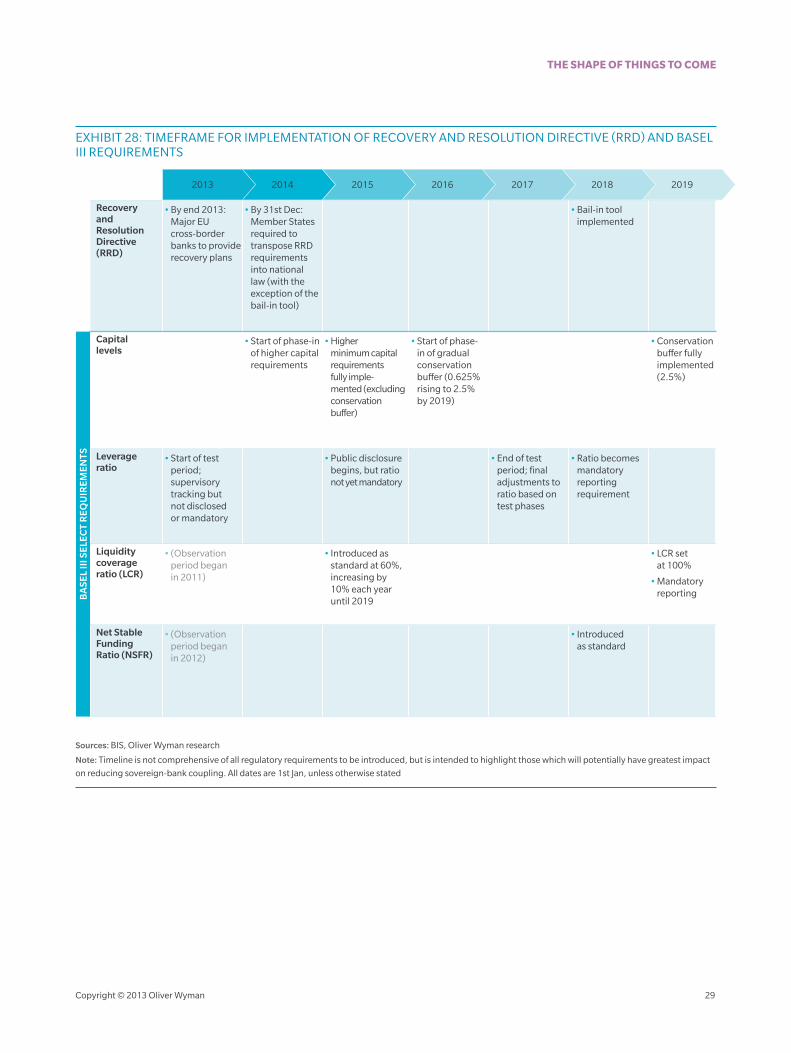

EXHIBIT 28: TIMEFRAME FOR IMPLEMENTATION OF RECOVERY AND RESOLUTION DIRECTIVE (RRD) AND BASEL III REQUIREMENTS

2013 2014 2015 2016 2017 2018 2019

Recovery and Resolution Directive (RRD)

•By end 2013: Major EU cross-border banks to provide recovery plans

•By 31st Dec: Member States required to transpose RRD requirements into national law (with the exception of the bail-in tool)

•Bail-in tool implemented

BA

SE

L II

I SE

LEC

T R

EQ

UIR

EM

EN

TS

Capital levels

•Start of phase-in of higher capital requirements

•Higher minimum capital requirements fully imple- mented (excluding conservation buffer)

•Start of phase-in of gradual conservation buffer (0.625% rising to 2.5% by 2019)

•Conservation buffer fully implemented (2.5%)

Leverage ratio

•Start of test period; supervisory tracking but not disclosed or mandatory

•Public disclosure begins, but ratio not yet mandatory

•End of test period; final adjustments to ratio based on test phases

•Ratio becomes mandatory reporting requirement

Liquidity coverage ratio (LCR)

• (Observation period began in 2011)

• Introduced as standard at 60%, increasing by 10% each year until 2019

•LCR set at 100%

•Mandatory reporting

Net Stable Funding Ratio (NSFR)

• (Observation period began in 2012)

• Introduced as standard

Sources: BIS, Oliver Wyman research

Note: Timeline is not comprehensive of all regulatory requirements to be introduced, but is intended to highlight those which will potentially have greatest impact

on reducing sovereign-bank coupling. All dates are 1st Jan, unless otherwise stated

THE SHAPE OF THINGS TO COME

30 Copyright © 2013 Oliver Wyman

3. THE CHALLENGES FOR BANKS

Banks face three key challenges moving forward:

1. Choosing between a bond-like or an equity-like strategy

2. Getting deleveraging and decoupling right

3. Channelling investment

3.1. A BOND OR EQUITY STRATEGY

The outlook across Europe is challenging for bank CEOs.

Although economic conditions are beginning to improve

and the drag from loan losses and other extraordinary

items should reduce, continued implementation of