the shifting narrative over the past 12 months

TRANSCRIPT

The shifting narrative over the past 12 months

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Sars?

A Chinese

problem

A global

problem

Lockdown

Spanish Flu 2?

Travel restrictions

Civil unrest

Social distancing

Empty CitiesEconomy

Building adaption

Vaccine

Working from home

Two different future time horizons – two different answers

Return to Normal

End 2021?

The Future of Cities

The Economy

Social Distancing

Health Concerns

Technology

Social Change

Resolution

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

% of total assetvalue accumulated

Years

The wood and the trees

>85% of YP perp

>5% of YP perp

This is what matters

Cities have always been the fireplaces of civilization, whence

light and heat radiated out into the dark.

Theodore Parker

US Reformer and Theologian

Why, Sir, you find no man, at all intellectual, who is willing to

leave London. No, Sir, when a man is tired of London, he is tired

of life; for there is in London all that life can afford.

Samuel Johnson

British Essayist and Poet

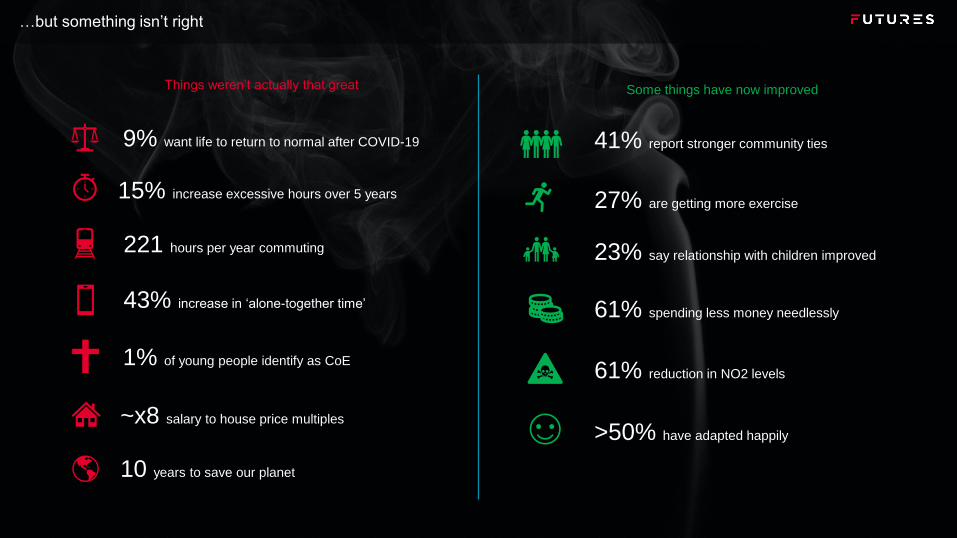

…but something isn’t right

9% want life to return to normal after COVID-19

15% increase excessive hours over 5 years

221 hours per year commuting

43% increase in ‘alone-together time’

~x8 salary to house price multiples

10 years to save our planet

1% of young people identify as CoE

41% report stronger community ties

27% are getting more exercise

23% say relationship with children improved

61% spending less money needlessly

>50% have adapted happily

61% reduction in NO2 levels

Things weren’t actually that great Some things have now improved

Caveman video

In the beginning…

Urban change is driven by technological and societal change

Stable settlements

Agriculture

?

Defence

Defined boundaries

Permanent Construction

Trade

Market place

Regional hub

Government

Public construction

Infrastructure

Economic shifts

Deserted settlements

Industrialisation

Massive urbanisation

Rapid mass transit

Suburbanisation

Why do cities exist?

Minimises average journey time

Existing infrastructure corridors aligned

Agglomeration benefits

Predictable interchange

Reduces pricing / exchange risk

Reduces investment risk

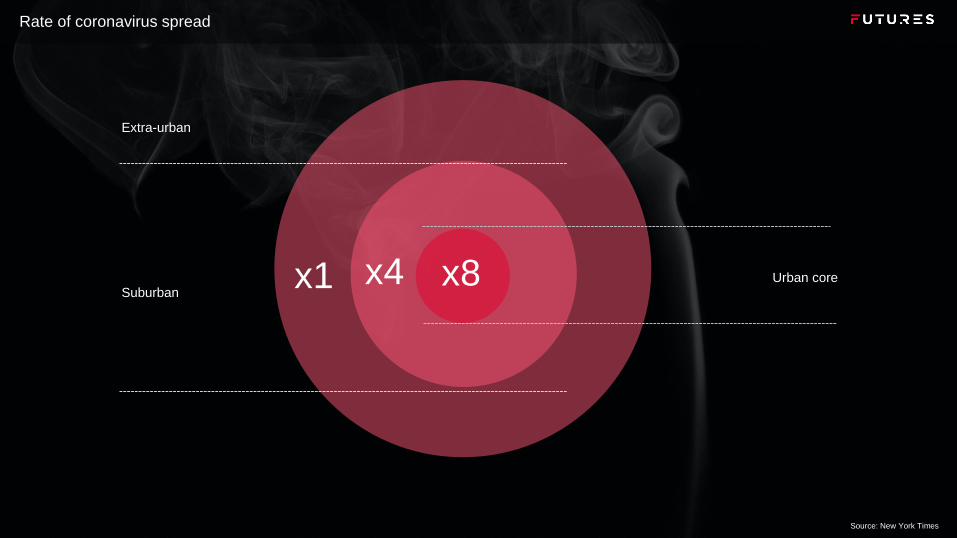

x1

Source: New York Times

Rate of coronavirus spread

x4 Urban coreSuburban

Extra-urban

x8

The failing proposition of our city centres

“The Urban Revival is Over “

Richard Florida

Cost of land > increased massing

Increased massing > wellness / safety

Worsening amenity ratios > worse quality of life

Land supply issues > public amenity suffers

Cost of rent > business penalties

Cost of housing > pushes out talent

Increasing city sizes > increase commute

Creaking infrastructure > penalties of distance

Central focus > lack of suburban amenity

Sources: ONS (2018), CityLabs, WSJ

Urban exodus

New York

Chicago

San Francisco

Washington

‘Most people in fact want

to live in detached

suburban homes’

Richard Florida

LondonAmsterdam

Paris-50000

-40000

-30000

-20000

-10000

0

10000

20000

30000

40000

0-9 10-19 20-29 30-39 40-49 50-59 60-69 70-79 80-+

Net migration to London by age group

Inner London

Outer London

London and Sectors in Focus

Source: Allianz Global Investors ‘The Sixth Kondratiev Wave’

Super-cycles and Kondratiev waves

Steam engine

Steel / Railways

Electrification

Petrochemicals

Computing

Digital / Biotech?

Rolli

ng

10

-ye

ar

yie

ld o

n S

&P

50

0

1800 1850 1900 20001950

The increasing impact of the internet

-

20

40

60

80

100

120

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Internet use (UK) Ecommerce (UK) IoT (m) Data Volume (Zb) Internet traffic

Source: Internet use (Statista), Ecommerce as % total sales (ONS), IoT devices (Ericcson), Data Volumes (Statista), Internet Traffic (Cisco)

% of global

population

using

internet in

past 3

months

Other series

indexed and

normalised

to 2020

Asymptotic to 100%

A shift from moving people and products to moving ideas

Home Office

Factory Shops

Source: Bain / Bank of England/ ONS

Some activities will be taken out of the real estate value chain

MOOCs Chat bots

Retail UniversitiesOffices

AnywhereOnline

consultations

GP

Surgeries Libraries

The internet

Sports

E-sportsE-commerce

Call

Centres

12

3 4

4 future scenarios

Output from C&W workshop

Hermit

Virtualisation

Urbanisation

Social Animals

The Matrix Hyper reality

REMOTE ECOSYSTEM

A new ecosystem of work-spaces

6

Core office

hub

Campus

On Demand

Event space’

Flexible touch down

and meeting spaces

Accessible &

memorable locations.

35

1Core office urban hub

Open to the public

Key meetings / Collaboration / Learning /

Mentoring / Innovation / Connection to

Culture

Third places in city

Lunch/Coffee

Informal meetings

4

Local Community

Hubs

Short commute

Atmosphere & services

3

Limited travel

Home work 2

CENTRAL ECOSYSTEM

Bid rent theory – the pricing of cities

M

F

F

$

$$

CBD

R

R

R

CBDCBD

CBD

R

David Ricardo ‘Bid Rent Theory’

New value drivers will take precedence

60% inverse correlation

Valu

e p

sf

Time to CBD

Lower density of amenity and

transport infrastructure in

outer zonesWinners will be areas of weak

transport infra and high

amenity

Zone of Defence

Zone of Disruption

The variable impact on different sectors

Impact of

COVID

measures

Ability to pivot to virtual delivery

High Street

HIGH

LOW /

POSITIVE

HIGHLOW

City Offices

Business

Parks

Retail

Warehouse

Retail

Showcase

Hotels

F&B

Resi

Health

Student

Industrial

Shopping

centre

Cinema

Data centres

The dislocation of assets

Sandwiches and pubs Business Parks Last mile logistics

A greater delineation between the central and outer zones of cities

INTERACTIVE ZONE FOCUS ZONE

Experience

Interaction

Innovation

Exhilaration

Wellness

Peace

Green

Community

Experience+

L+T Osnabrück

WeWorkAmazon Go

Deskdog

Second Home

Sidewalk Toronto

Facebook Menlo Park

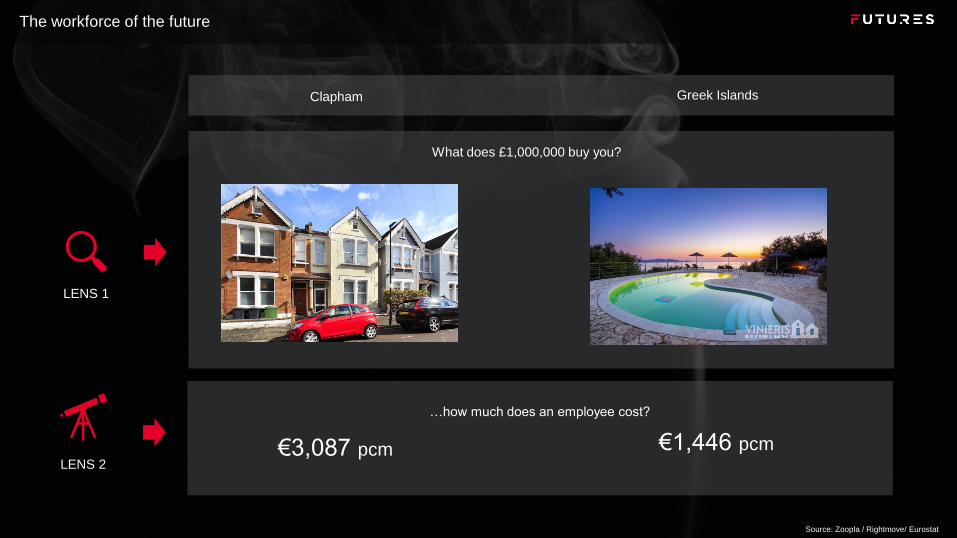

Source: Zoopla / Rightmove/ Eurostat

The workforce of the future

What does £1,000,000 buy you?

Clapham Greek Islands

…how much does an employee cost?

€1,446 pcm€3,087 pcm

LENS 1

LENS 2

A new world of digital experiences

Decentraland – a new world of real estate

1. Investment strategy – take risk off the table

0

2

4

6

8

10

12

14

16

18

Tota

l R

etu

rn (

%pa)

Long income outperforming

Double down on prime

Long income focus

Reverified covenants

Divest dynamic sectors

Longer structural tilts

Greater focus on stock selection

2. Product strategy – extend maturity phase / invest when you don’t need to.

INTRODUCTION GROWTH MATURITY DECLINE

Placemaking

Anchor letting

Leasing Stabilised income Vacancy

Obsolescence

EXTEND PHASE

High marketing spend

New commercialisation

Brand differentiation

‘INNOVATION WINDOW’

Planning consent

Capex

LIMIT OUTGOINGS

Dial off marketing

Reduce rents

Divest non-core income

Wind down

Source: Charles Handy ‘The Second Curve’

3. Business planning – shift from deterministic to stochastic approach

DETERMINISTIC

PROBABLISTIC

Assume:

(1) Tenant leaves = no

(2) Retail demand down 10%

NPV = £100

Assume:

(1) E(Tenant leaves) = 30%

(2) Retail demand: = -10% = 5%

£90< E(NPV) <£100 = 95% confidence

30%

70%

PREDICTIVE

Lead indicators

Machine learning

4. Design strategy - Don’t ‘build to last’ / eliminate waste in the design phase

Time

Value

100%

0%

50%Waste

Physical

deterioration

alone

Economic /

functional

obsolescence

Mass timber built with disassembly in mind

Source: Sidewalk Labs Toronto Tomorrow MIDP1

Technical

improvements

Industrial

change

5. Create real options – create value from ability to pivot

Real option

value levers

Period of which

option is valid

(+)

Present value

of fixed cost

(-)

Unpredictability of

expected cashflows

(+)

Present value of

expected cashflow

(+)

Yield of riskless

security

(+)

Source: McKinsey & Company, ‘The Real Power of Real Options’ / Corporate Finance Institute

Park 20|20, Amsterdam

Modular building components

Deconstructable / cradle to cradle by design

Overspecfication

Prefabrication

Externalised M&E

Value lost of

duration of option

(-)

6. Corporate sustainability strategy - Eliminate negative externalities to reduce value risk

P0

P1

Q0Q1

Cost / Price

Output

Private

Cost

Social

Cost

Negative

Externality

Regulation Pigovian taxes CSR

RISKS

Unsustainable

buildingsToxic tenants

Wellness

failings

Social

displacement

NEGATIVE EXTERNALITIES IN REAL ESTATE

Demand Supply

7. Vertical scope - Transfer risk to those better placed to manage it

Market cycle

Funding / Financing

Tenant Failure

RE operations

M&E Obsolescence

Economies of scale

Expertise

Learning / innovation

Risk Management

Analytics

SUPPLY CHAININVESTOR

Contracting

(Subscription rental)

UPSTREAM?

?

8. Corporate boundaries - position your business where you are most able to create value

Source: Harvard Business Review ‘Profit Pools: A new look at strategy’

25%

20%

15%

10%

5%

0%

100%

Share of industry revenue

Op

era

tin

g m

arg

in

Auto manufacturing

New car sales

Used car sales

Auto loans

Leasing

Warranty

Petrol Insurance

Service / repair

Aftermarket parts

Auto rental

If all else fails… a new generation of real estate professional

The Luddite Rebellion Mojo Vision + Hyper reality

Neuralink Epicenter

Summary – key takeaways

Cities have changed radically over the course of history. Change is the constant

The value proposition of cities rests on the agglomeration, centralised trade and serendipity

An internet enabled workforce threatens to break the concept of distance entirely.

Urban exodus is a reality not a threat.

In recent years, underinvestment combined with scale issues has created challenges that remain unaddressed.

We will work in new places. We will live in new places. This will break current value dynamics and leave some assets dislocated

We need to be willing to reinvent our system around how people want to live their lives, including amenity and free time

Find solutions through backing long term trends, being laser focused on product, creating real options, being clear on ESG,

and reconsidering your role in the industry value chain.

Find out more @ futures.cushmanwakefield.co.uk