the sirius consulting group - tpa review - trade...

TRANSCRIPT

The Sirius Consulting Group Sharing The Brightest Ideas™

The Australian Automobile Dealers’ Association

‘Charter of Fairness’

Discussion Document

July 5 2002

Case Managers:Mark Wainwright MBIM. MBA. FIMI.

Frank Dennis LLB.

Level 10, 300 Flinders Street Tel: +61 (0) 418990919Melbourne Victoria 3001 Australia [email protected]

2

Contents

Executive Summary 3

1.0 Background discussion of ‘The Charter of Fairness’ 4

1.1 The Global Automotive Industry - Overview 4

1.2 The Consumer

1.3 Evidence of Regional Collaborative Behaviour

9

23

1.4 The Australian Automotive Industry – Overview 27

1.5 Competition in the Australian Automotive Industry 30

2.0 Legal Discussion of the Charter of Fairness

2.1 Background

2.2 Legal Issues

2.3 Applicable Law & Inadequacies in Law

2.4 Recommendations

50

50

51

51

63

3

Executive Summary

The Australian Automobile Dealers’ Association (AADA) has developed a ‘Charter of Fairness’as a considered response to the changing competitive dynamics of both the global and Australianautomotive industries. These changing dynamics are implicitly and explicitly increasing theconcentration of market power of the global automotive companies and have already beenobserved to be substantially lessening both inter and intra brand competition in the Australianmarkets for new and used vehicles.

There are now only six major global manufacturers all of whose profitability is being diminishedby global productive overcapacity. This is largely due to their new investment in regions wherethe cost factors of production can be minimised without sufficient closure of old capacity in aglobally static market. The automotive value chain has been radically restructured and now someof the global automotive companies are pursuing strategies of downstream continuousdiversification and forward integration including, in those jurisdictions that have not prohibited iton anti-competitive grounds, the disintermediation of their franchised networks.

This discussion paper utilises two recent, large-scale, independent European consumer surveysand other evidence to discern that the retail automotive industry is highly competitive at both interbrand and intra brand levels and that intra brand competitive issues are involved in eighty per centof consumers’ major concerns and over fifty per cent of their buying decision process. Thesurveys demonstrate that any significant diminution of intra brand competition would lead to asubstantial lessening of total competition in the markets for new and late model vehicles, service,parts and employment for skilled staff associated with that brand. The paper finds that Australianlegislators and regulators have neither fully understood the role of intra brand competition in theretail automotive market nor its importance to consumers.

Despite finding that inter brand competition is globally intensive the paper presents evidence oflarge scale regional pricing collaboration between the remaining big six vehicle manufacturers.

Utilising Professor Michael Porter’s ‘Five Forces Model’, the competitive dynamics of theAustralian retail automotive industry are analysed and the overwhelming dominance of the brandowning franchisors established. The paper demonstrates that inadequacies in relevant legislationand regulation have led to the franchisors exploiting this position of dominance via inequitablefranchise agreements and in some cases a total absence of good faith in dealing with theirfranchisees. It is in this environment that the Australian Automobile Dealers Association hasproduced its ‘Charter of Fairness’, a document setting out key industry issues that must beaddressed by legislators and regulators if intra-brand competition is to survive in the Australianmarket for new vehicles. The Charter does not seek protection for incompetent or genuinely underperforming businesses but a fair go for entrepreneurial Australian businesses often confrontedwith the prospect of untimely, ineffectual or prohibitively expensive means of resolving disputeswith global corporations.

This report seeks to explain the reasoning behind each of The Charter’s articles, identify thefederal and state laws and policies associated with each and advise the AADA as to ways toproceed in having them adopted as policy or law by the relevant authority, organisation orgovernment.

4

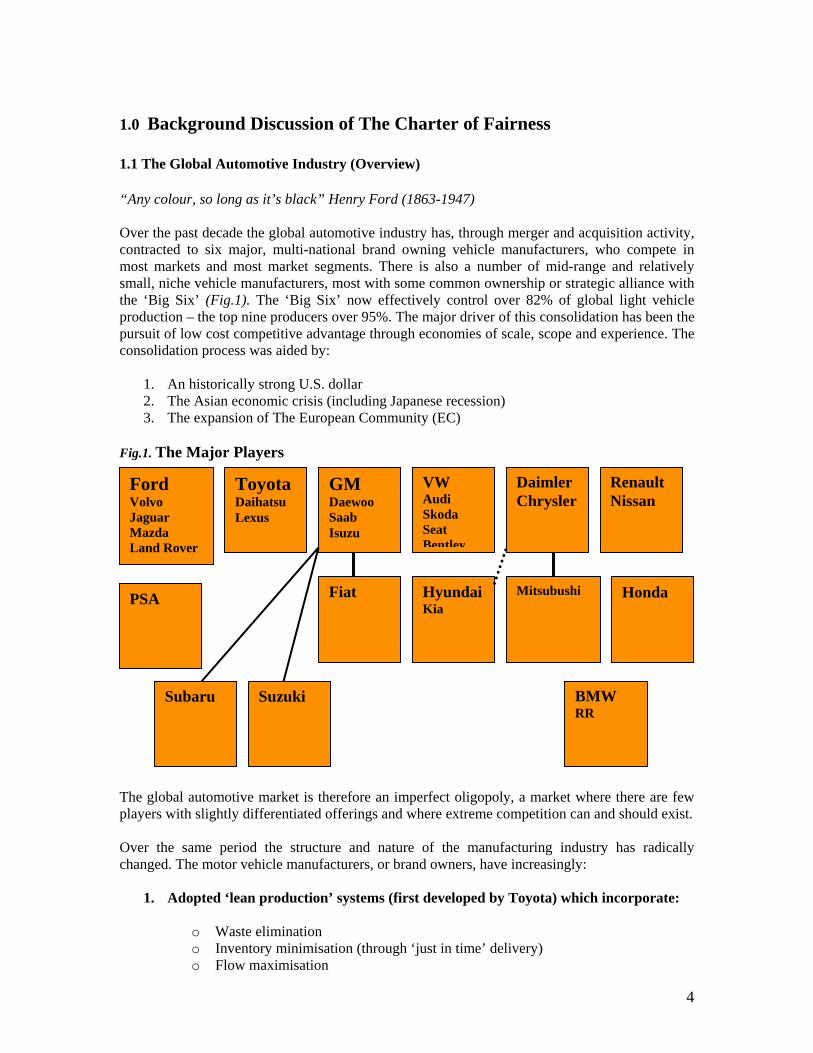

1.0 Background Discussion of The Charter of Fairness

1.1 The Global Automotive Industry (Overview)

“Any colour, so long as it’s black” Henry Ford (1863-1947)

Over the past decade the global automotive industry has, through merger and acquisition activity,contracted to six major, multi-national brand owning vehicle manufacturers, who compete inmost markets and most market segments. There is also a number of mid-range and relativelysmall, niche vehicle manufacturers, most with some common ownership or strategic alliance withthe ‘Big Six’ (Fig.1). The ‘Big Six’ now effectively control over 82% of global light vehicleproduction – the top nine producers over 95%. The major driver of this consolidation has been thepursuit of low cost competitive advantage through economies of scale, scope and experience. Theconsolidation process was aided by:

1. An historically strong U.S. dollar2. The Asian economic crisis (including Japanese recession)3. The expansion of The European Community (EC)

Fig.1. The Major Players

The global automotive market is therefore an imperfect oligopoly, a market where there are fewplayers with slightly differentiated offerings and where extreme competition can and should exist.

Over the same period the structure and nature of the manufacturing industry has radicallychanged. The motor vehicle manufacturers, or brand owners, have increasingly:

1. Adopted ‘lean production’ systems (first developed by Toyota) which incorporate:

o Waste eliminationo Inventory minimisation (through ‘just in time’ delivery)o Flow maximisation

FordVolvoJaguarMazdaLand Rover

ToyotaDaihatsuLexus

GMDaewooSaabIsuzu

VWAudiSkodaSeatBentley

DaimlerChrysler

RenaultNissan

MitsubushiFiatPSA HondaHyundaiKia

Subaru Suzuki BMWRR

5

o Demand driven productiono Meeting customer requirementso Doing it right the first timeo Worker empowermento Design for rapid changeovero Partner with supplierso Create a culture of continuous improvement

2. Improved supply chain efficiency through:

o Outsourcing design and production of components and, increasingly,component modules to specialist external ‘tier one’ suppliers. Thetier one suppliers have become strategic partners of the brand ownersand in turn partner with tier two (sub-componentry) and tier three(raw materials) elements of the supply chain. In the globalenvironment each of the tier one suppliers need to partner with thebrand owners wherever they produce vehicles. The capitalrequirements to roll out globally have led to unprecedented andongoing rationalisation of the supply chain. Industry experts predict a75% decline in the number of tier-one suppliers, and a 90% reductionof tier-two suppliers by 20101. Creating collaborative tradingnetworks that leverage industry-wide resources is an imperative.

o Adopting web based exchanges to manage procurement transactionse.g. in 2001 the Covisint joint venture between GM, Ford andDaimler Chrysler managed more than $129 billion in transactions--nearly 53% of the estimated $240 billion spent last year by itsfounders. GM has pushed $96 billion worth of procurement forcurrent and future auto models through the exchange, via ‘QuoteManager’, Covisint's online negotiating tool2.

3. Adopted platform rationalisation

The competitive imperative to lower design and manufacturing costs is driving platformrationalisation. It’s been predicted that by 2005 there will be at least 20 one-million-unitplatforms. Two of these platforms exist today, and each one serves as the building blockfor multiple brands and models. As a result, nearly 70-80% of content is shared acrosseach model (current world best practice is exhibited by the Volkswagen Group whichmarkets 54 model variants based upon just four platforms). As there is alreadyconvergence between brands, of quality, performance and complexity, the challenge forthe brand owners is to create a differentiated product with the remaining 20-30% ofcontent — which in turn requires suppliers to respond faster and more effectively in acollaborative environment in order to remain competitive.

1. ‘A2C: The Second Automotive Century’ Ferron, PWC 2000; 2. www.covisint.com

6

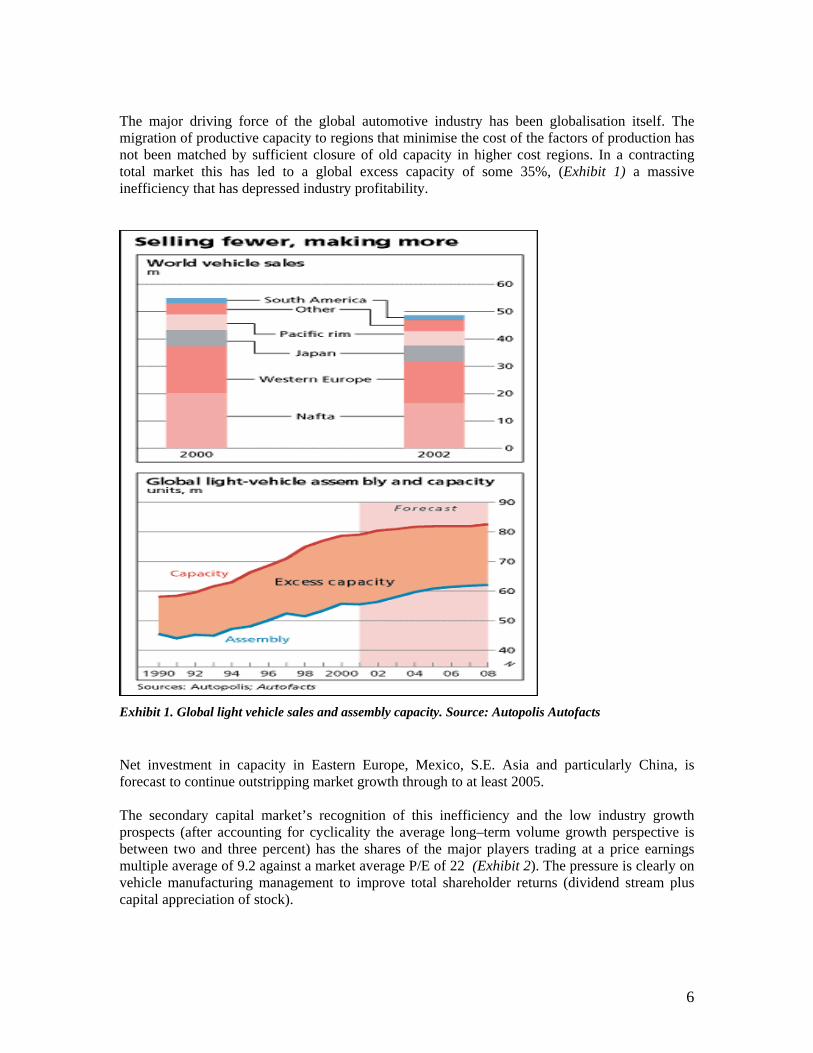

The major driving force of the global automotive industry has been globalisation itself. Themigration of productive capacity to regions that minimise the cost of the factors of production hasnot been matched by sufficient closure of old capacity in higher cost regions. In a contractingtotal market this has led to a global excess capacity of some 35%, (Exhibit 1) a massiveinefficiency that has depressed industry profitability.

Exhibit 1. Global light vehicle sales and assembly capacity. Source: Autopolis Autofacts

Net investment in capacity in Eastern Europe, Mexico, S.E. Asia and particularly China, isforecast to continue outstripping market growth through to at least 2005.

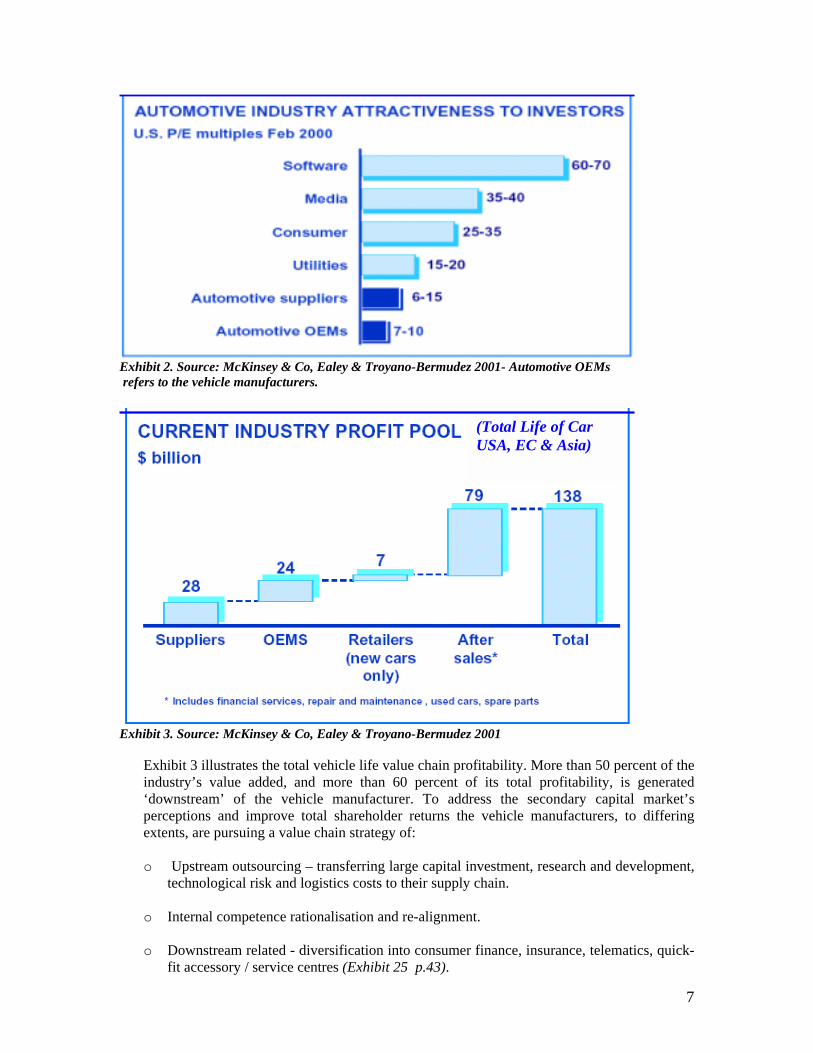

The secondary capital market’s recognition of this inefficiency and the low industry growthprospects (after accounting for cyclicality the average long–term volume growth perspective isbetween two and three percent) has the shares of the major players trading at a price earningsmultiple average of 9.2 against a market average P/E of 22 (Exhibit 2). The pressure is clearly onvehicle manufacturing management to improve total shareholder returns (dividend stream pluscapital appreciation of stock).

7

Exhibit 2. Source: McKinsey & Co, Ealey & Troyano-Bermudez 2001- Automotive OEMs refers to the vehicle manufacturers.

Exhibit 3. Source: McKinsey & Co, Ealey & Troyano-Bermudez 2001

Exhibit 3 illustrates the total vehicle life value chain profitability. More than 50 percent of theindustry’s value added, and more than 60 percent of its total profitability, is generated‘downstream’ of the vehicle manufacturer. To address the secondary capital market’sperceptions and improve total shareholder returns the vehicle manufacturers, to differingextents, are pursuing a value chain strategy of:

o Upstream outsourcing – transferring large capital investment, research and development,technological risk and logistics costs to their supply chain.

o Internal competence rationalisation and re-alignment.

o Downstream related - diversification into consumer finance, insurance, telematics, quick-fit accessory / service centres (Exhibit 25 p.43).

(Total Life of CarUSA, EC & Asia)

8

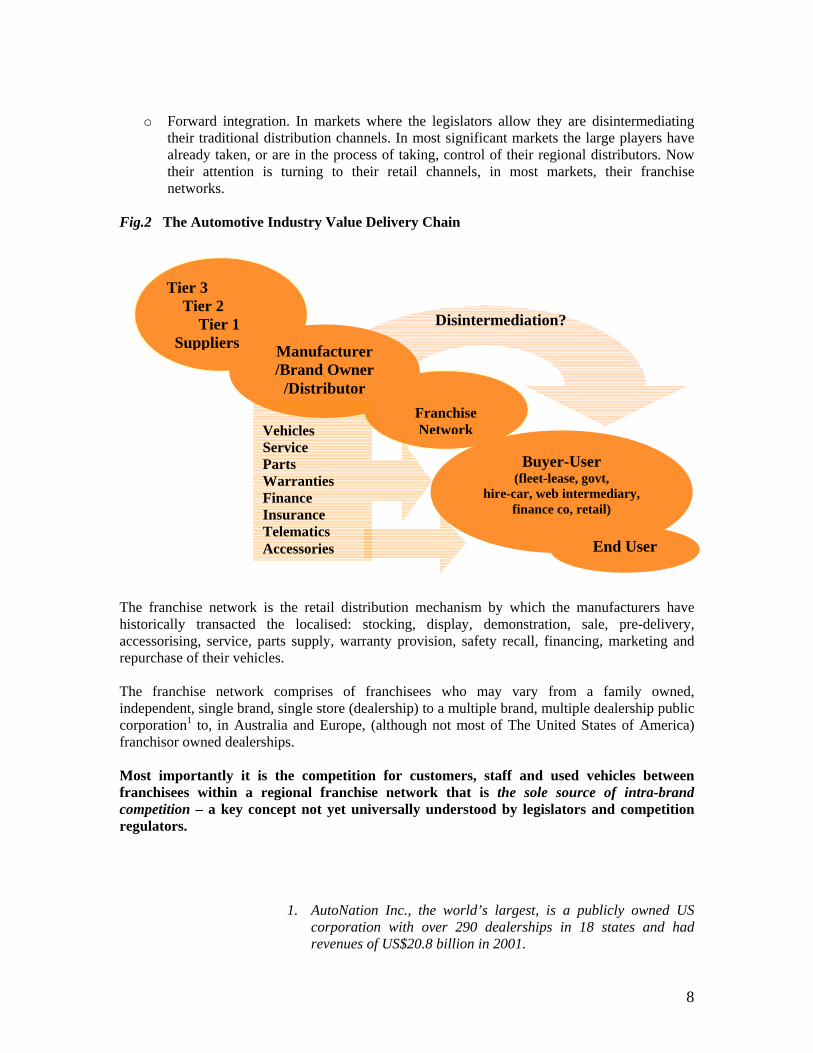

o Forward integration. In markets where the legislators allow they are disintermediatingtheir traditional distribution channels. In most significant markets the large players havealready taken, or are in the process of taking, control of their regional distributors. Nowtheir attention is turning to their retail channels, in most markets, their franchisenetworks.

Fig.2 The Automotive Industry Value Delivery Chain

The franchise network is the retail distribution mechanism by which the manufacturers havehistorically transacted the localised: stocking, display, demonstration, sale, pre-delivery,accessorising, service, parts supply, warranty provision, safety recall, financing, marketing andrepurchase of their vehicles.

The franchise network comprises of franchisees who may vary from a family owned,independent, single brand, single store (dealership) to a multiple brand, multiple dealership publiccorporation1 to, in Australia and Europe, (although not most of The United States of America)franchisor owned dealerships.

Most importantly it is the competition for customers, staff and used vehicles betweenfranchisees within a regional franchise network that is the sole source of intra-brandcompetition – a key concept not yet universally understood by legislators and competitionregulators.

1. AutoNation Inc., the world’s largest, is a publicly owned UScorporation with over 290 dealerships in 18 states and hadrevenues of US$20.8 billion in 2001.

FranchiseNetwork

Tier 3 Tier 2 Tier 1 Suppliers Manufacturer

/Brand Owner/Distributor

Buyer-User(fleet-lease, govt,

hire-car, web intermediary,finance co, retail)

VehiclesServicePartsWarrantiesFinanceInsuranceTelematicsAccessories End User

Disintermediation?

9

1.2 The Consumer

Competition is complex and multi-faceted - and so is its regulation. Any search of the literaturereveals well constructed arguments for and against the efficiencies of the current automotivedistribution system.

It should be looked at from the ultimate perspective, that of the consumer:

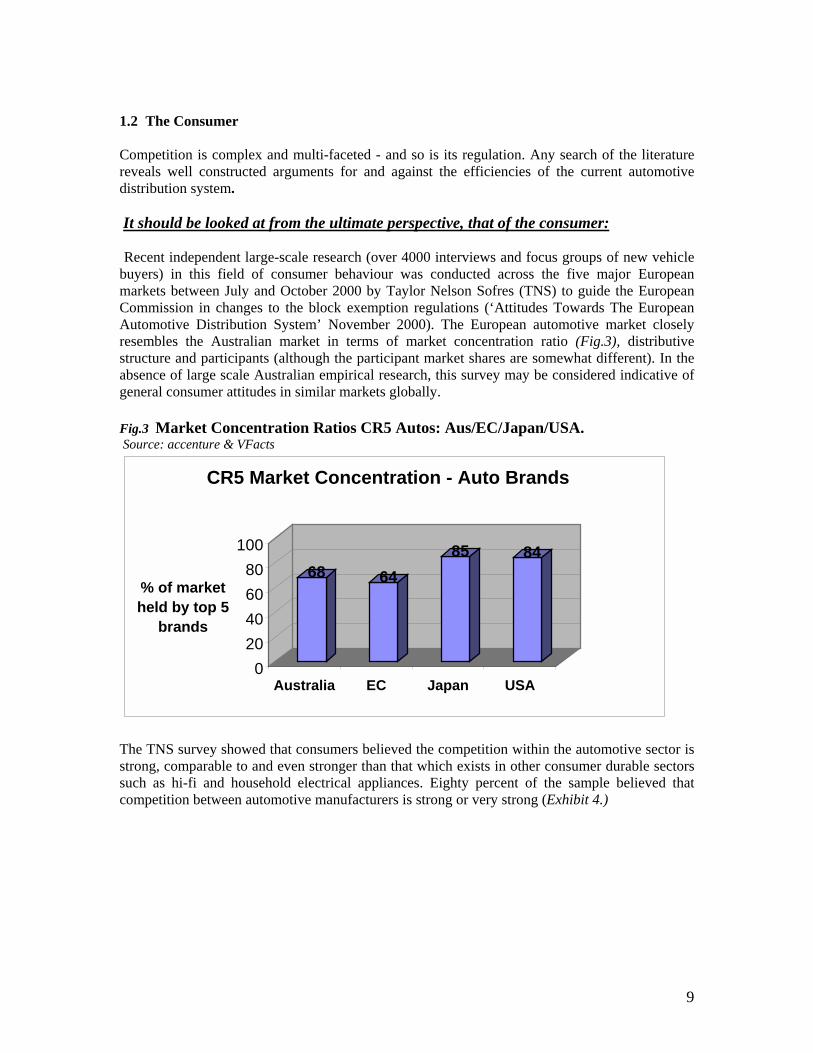

Recent independent large-scale research (over 4000 interviews and focus groups of new vehiclebuyers) in this field of consumer behaviour was conducted across the five major Europeanmarkets between July and October 2000 by Taylor Nelson Sofres (TNS) to guide the EuropeanCommission in changes to the block exemption regulations (‘Attitudes Towards The EuropeanAutomotive Distribution System’ November 2000). The European automotive market closelyresembles the Australian market in terms of market concentration ratio (Fig.3), distributivestructure and participants (although the participant market shares are somewhat different). In theabsence of large scale Australian empirical research, this survey may be considered indicative ofgeneral consumer attitudes in similar markets globally.

Fig.3 Market Concentration Ratios CR5 Autos: Aus/EC/Japan/USA. Source: accenture & VFacts

68 6485 84

020406080

100

% of market held by top 5

brands

Australia EC Japan USA

CR5 Market Concentration - Auto Brands

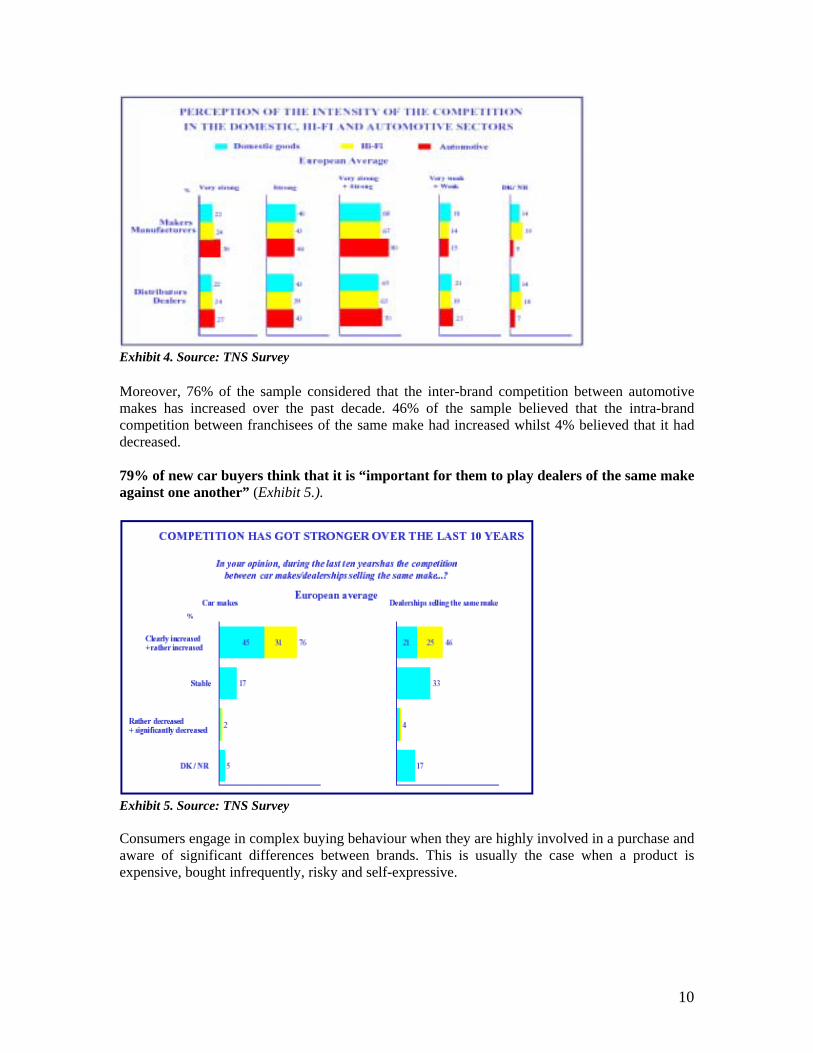

The TNS survey showed that consumers believed the competition within the automotive sector isstrong, comparable to and even stronger than that which exists in other consumer durable sectorssuch as hi-fi and household electrical appliances. Eighty percent of the sample believed thatcompetition between automotive manufacturers is strong or very strong (Exhibit 4.)

10

Exhibit 4. Source: TNS Survey

Moreover, 76% of the sample considered that the inter-brand competition between automotivemakes has increased over the past decade. 46% of the sample believed that the intra-brandcompetition between franchisees of the same make had increased whilst 4% believed that it haddecreased.

79% of new car buyers think that it is “important for them to play dealers of the same makeagainst one another” (Exhibit 5.).

Exhibit 5. Source: TNS Survey

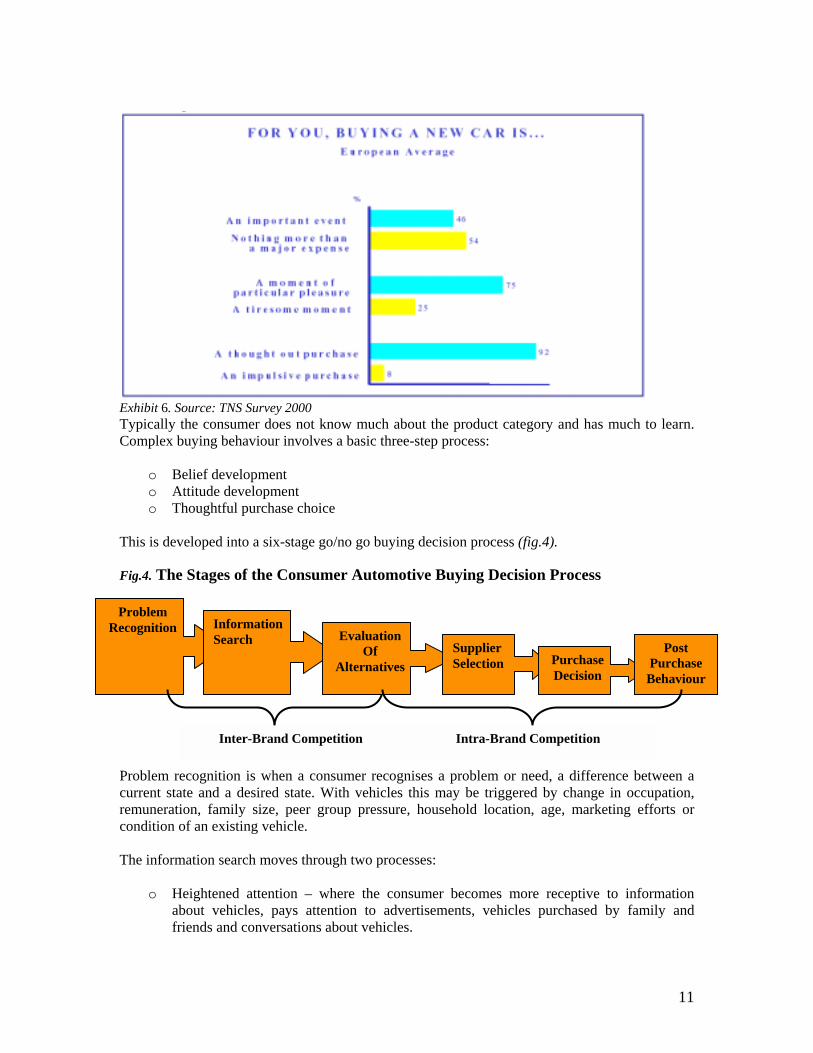

Consumers engage in complex buying behaviour when they are highly involved in a purchase andaware of significant differences between brands. This is usually the case when a product isexpensive, bought infrequently, risky and self-expressive.

11

Exhibit 6. Source: TNS Survey 2000Typically the consumer does not know much about the product category and has much to learn.Complex buying behaviour involves a basic three-step process:

o Belief developmento Attitude developmento Thoughtful purchase choice

This is developed into a six-stage go/no go buying decision process (fig.4).

Fig.4. The Stages of the Consumer Automotive Buying Decision Process

Problem recognition is when a consumer recognises a problem or need, a difference between acurrent state and a desired state. With vehicles this may be triggered by change in occupation,remuneration, family size, peer group pressure, household location, age, marketing efforts orcondition of an existing vehicle.

The information search moves through two processes:

o Heightened attention – where the consumer becomes more receptive to informationabout vehicles, pays attention to advertisements, vehicles purchased by family andfriends and conversations about vehicles.

ProblemRecognition Information

Search EvaluationOf

AlternativesSupplierSelection Purchase

Decision

PostPurchase

Behaviour

Inter-Brand Competition Intra-Brand Competition

12

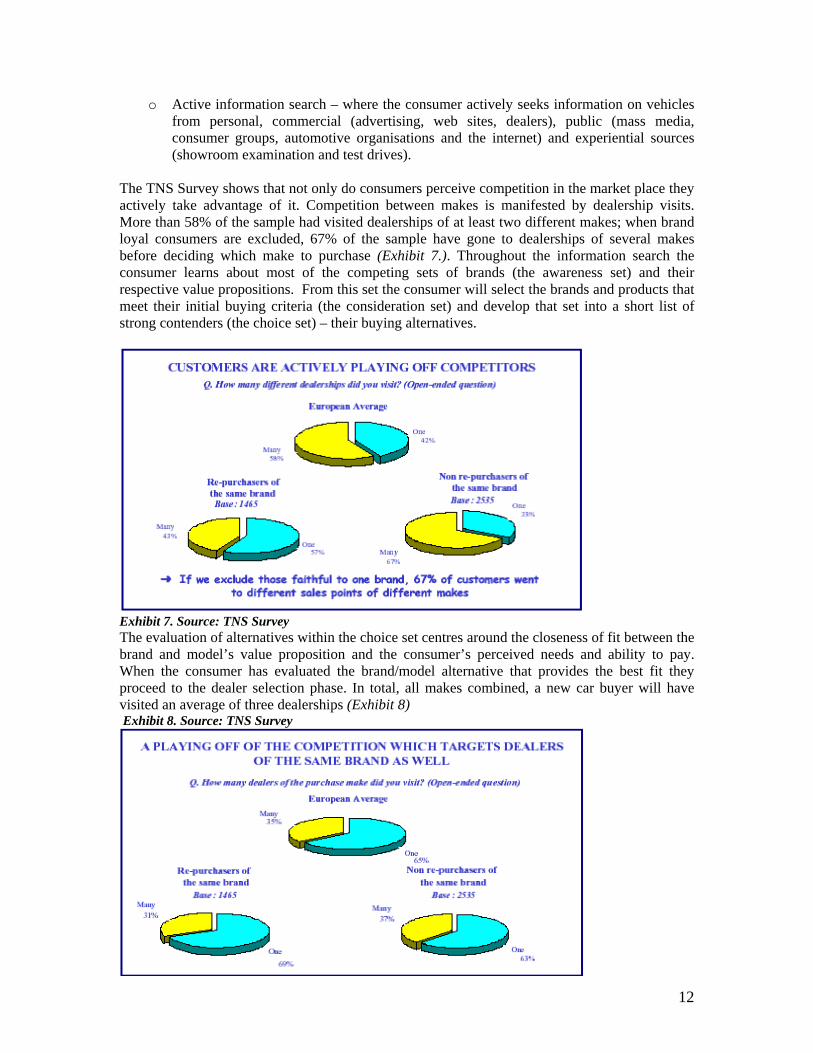

o Active information search – where the consumer actively seeks information on vehiclesfrom personal, commercial (advertising, web sites, dealers), public (mass media,consumer groups, automotive organisations and the internet) and experiential sources(showroom examination and test drives).

The TNS Survey shows that not only do consumers perceive competition in the market place theyactively take advantage of it. Competition between makes is manifested by dealership visits.More than 58% of the sample had visited dealerships of at least two different makes; when brandloyal consumers are excluded, 67% of the sample have gone to dealerships of several makesbefore deciding which make to purchase (Exhibit 7.). Throughout the information search theconsumer learns about most of the competing sets of brands (the awareness set) and theirrespective value propositions. From this set the consumer will select the brands and products thatmeet their initial buying criteria (the consideration set) and develop that set into a short list ofstrong contenders (the choice set) – their buying alternatives.

Exhibit 7. Source: TNS SurveyThe evaluation of alternatives within the choice set centres around the closeness of fit between thebrand and model’s value proposition and the consumer’s perceived needs and ability to pay.When the consumer has evaluated the brand/model alternative that provides the best fit theyproceed to the dealer selection phase. In total, all makes combined, a new car buyer will havevisited an average of three dealerships (Exhibit 8) Exhibit 8. Source: TNS Survey

13

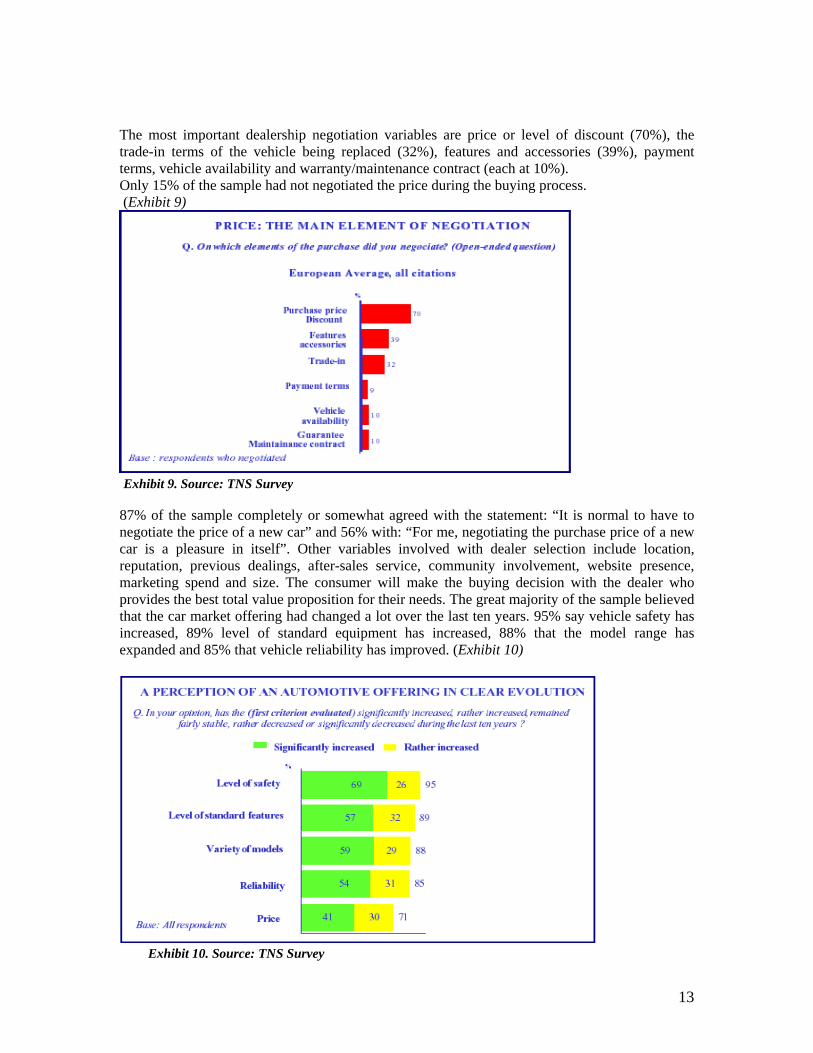

The most important dealership negotiation variables are price or level of discount (70%), thetrade-in terms of the vehicle being replaced (32%), features and accessories (39%), paymentterms, vehicle availability and warranty/maintenance contract (each at 10%).Only 15% of the sample had not negotiated the price during the buying process. (Exhibit 9)

Exhibit 9. Source: TNS Survey

87% of the sample completely or somewhat agreed with the statement: “It is normal to have tonegotiate the price of a new car” and 56% with: “For me, negotiating the purchase price of a newcar is a pleasure in itself”. Other variables involved with dealer selection include location,reputation, previous dealings, after-sales service, community involvement, website presence,marketing spend and size. The consumer will make the buying decision with the dealer whoprovides the best total value proposition for their needs. The great majority of the sample believedthat the car market offering had changed a lot over the last ten years. 95% say vehicle safety hasincreased, 89% level of standard equipment has increased, 88% that the model range hasexpanded and 85% that vehicle reliability has improved. (Exhibit 10)

Exhibit 10. Source: TNS Survey

14

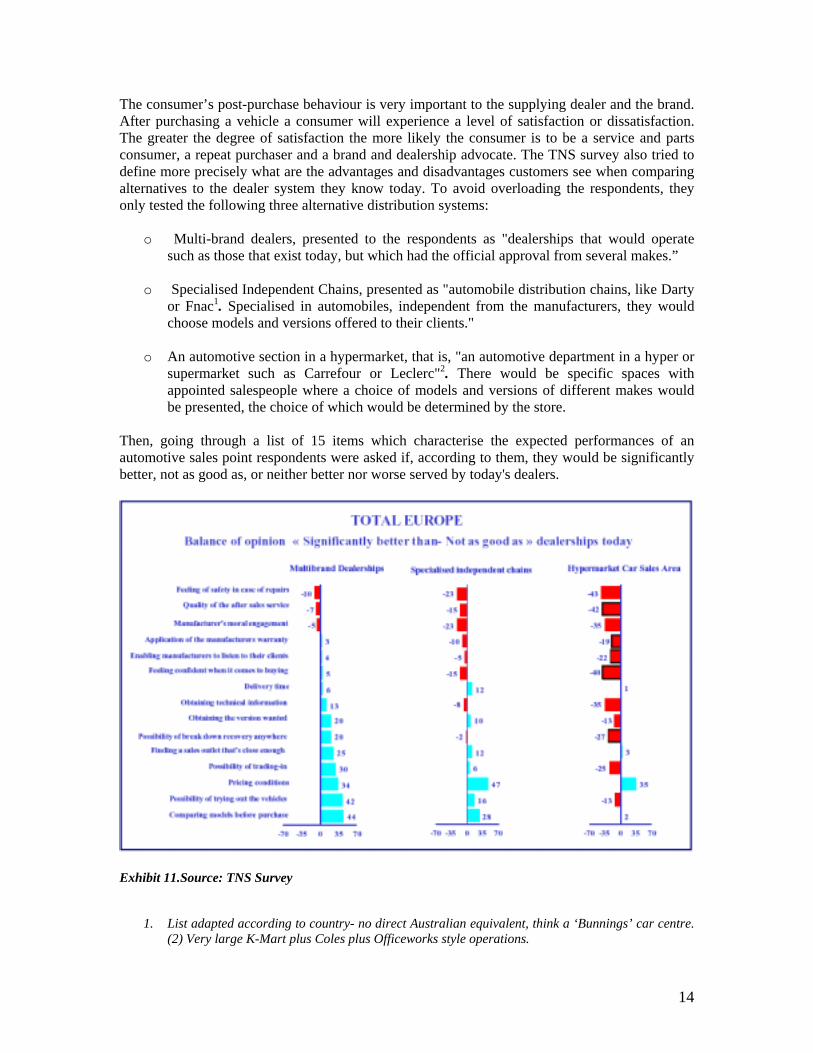

The consumer’s post-purchase behaviour is very important to the supplying dealer and the brand.After purchasing a vehicle a consumer will experience a level of satisfaction or dissatisfaction.The greater the degree of satisfaction the more likely the consumer is to be a service and partsconsumer, a repeat purchaser and a brand and dealership advocate. The TNS survey also tried todefine more precisely what are the advantages and disadvantages customers see when comparingalternatives to the dealer system they know today. To avoid overloading the respondents, theyonly tested the following three alternative distribution systems:

o Multi-brand dealers, presented to the respondents as "dealerships that would operatesuch as those that exist today, but which had the official approval from several makes.”

o Specialised Independent Chains, presented as "automobile distribution chains, like Dartyor Fnac1. Specialised in automobiles, independent from the manufacturers, they wouldchoose models and versions offered to their clients."

o An automotive section in a hypermarket, that is, "an automotive department in a hyper orsupermarket such as Carrefour or Leclerc"2. There would be specific spaces withappointed salespeople where a choice of models and versions of different makes wouldbe presented, the choice of which would be determined by the store.

Then, going through a list of 15 items which characterise the expected performances of anautomotive sales point respondents were asked if, according to them, they would be significantlybetter, not as good as, or neither better nor worse served by today's dealers.

Exhibit 11.Source: TNS Survey

1. List adapted according to country- no direct Australian equivalent, think a ‘Bunnings’ car centre.(2) Very large K-Mart plus Coles plus Officeworks style operations.

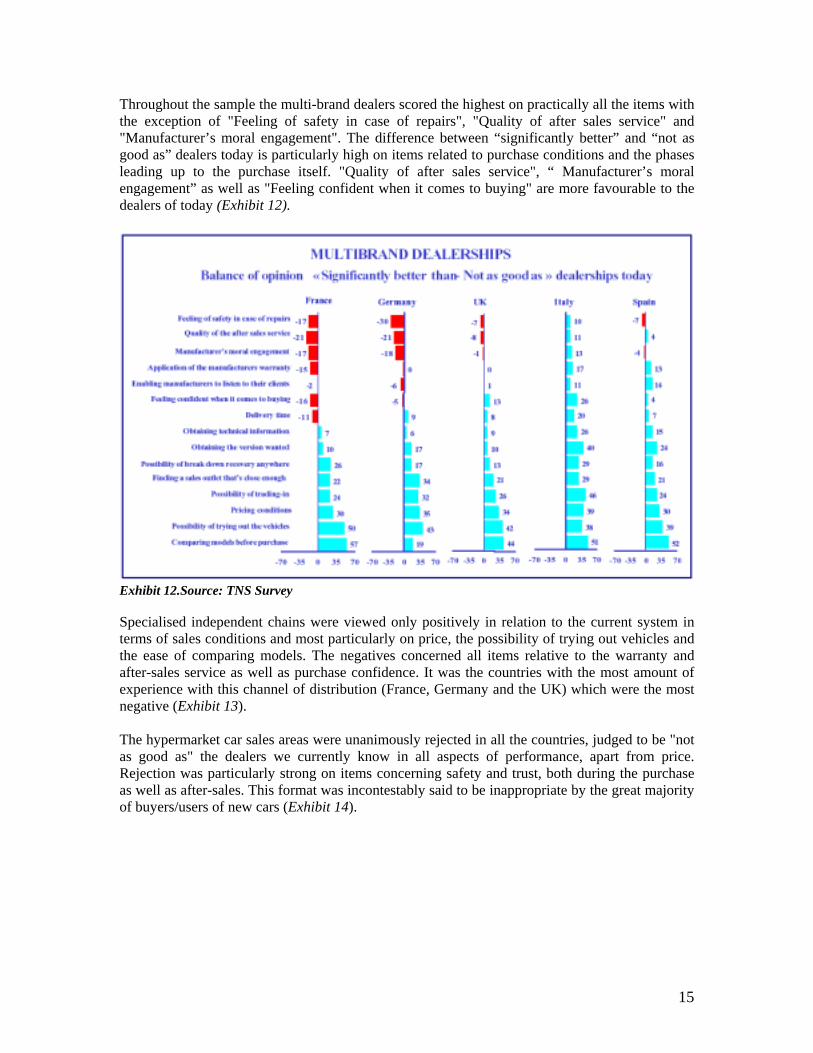

15

Throughout the sample the multi-brand dealers scored the highest on practically all the items withthe exception of "Feeling of safety in case of repairs", "Quality of after sales service" and"Manufacturer’s moral engagement". The difference between “significantly better” and “not asgood as” dealers today is particularly high on items related to purchase conditions and the phasesleading up to the purchase itself. "Quality of after sales service", “ Manufacturer’s moralengagement” as well as "Feeling confident when it comes to buying" are more favourable to thedealers of today (Exhibit 12).

Exhibit 12.Source: TNS Survey

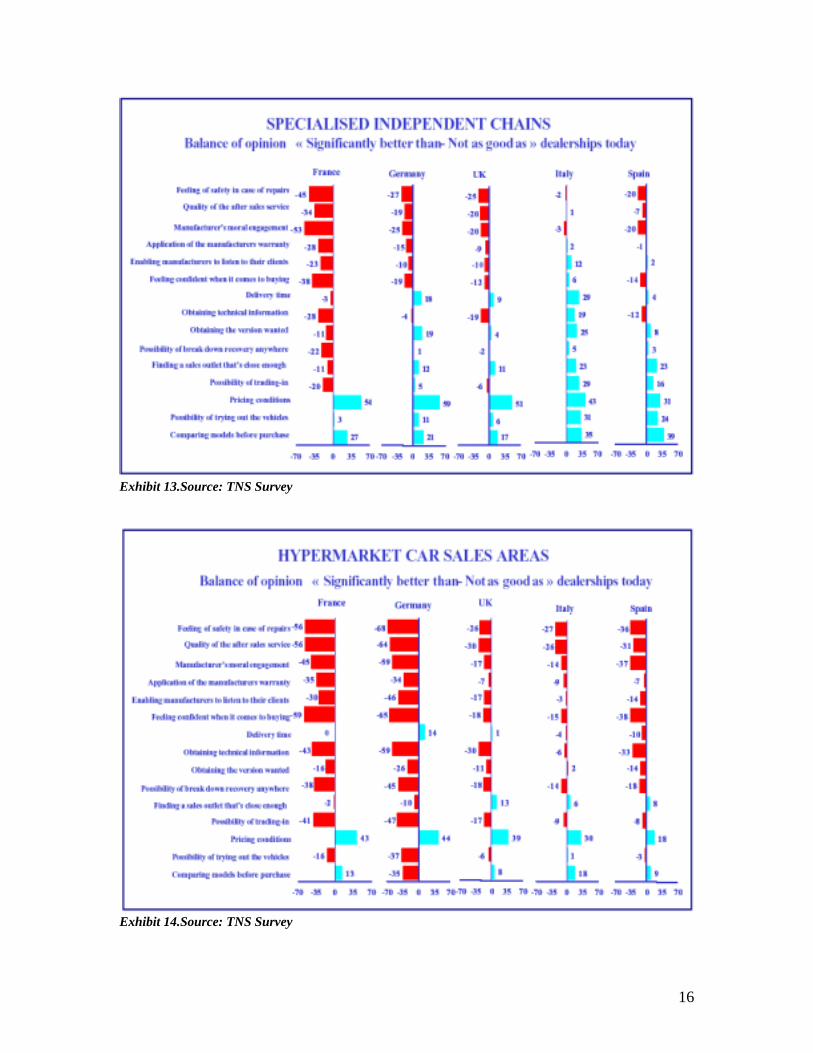

Specialised independent chains were viewed only positively in relation to the current system interms of sales conditions and most particularly on price, the possibility of trying out vehicles andthe ease of comparing models. The negatives concerned all items relative to the warranty andafter-sales service as well as purchase confidence. It was the countries with the most amount ofexperience with this channel of distribution (France, Germany and the UK) which were the mostnegative (Exhibit 13).

The hypermarket car sales areas were unanimously rejected in all the countries, judged to be "notas good as" the dealers we currently know in all aspects of performance, apart from price.Rejection was particularly strong on items concerning safety and trust, both during the purchaseas well as after-sales. This format was incontestably said to be inappropriate by the great majorityof buyers/users of new cars (Exhibit 14).

16

Exhibit 13.Source: TNS Survey

Exhibit 14.Source: TNS Survey

17

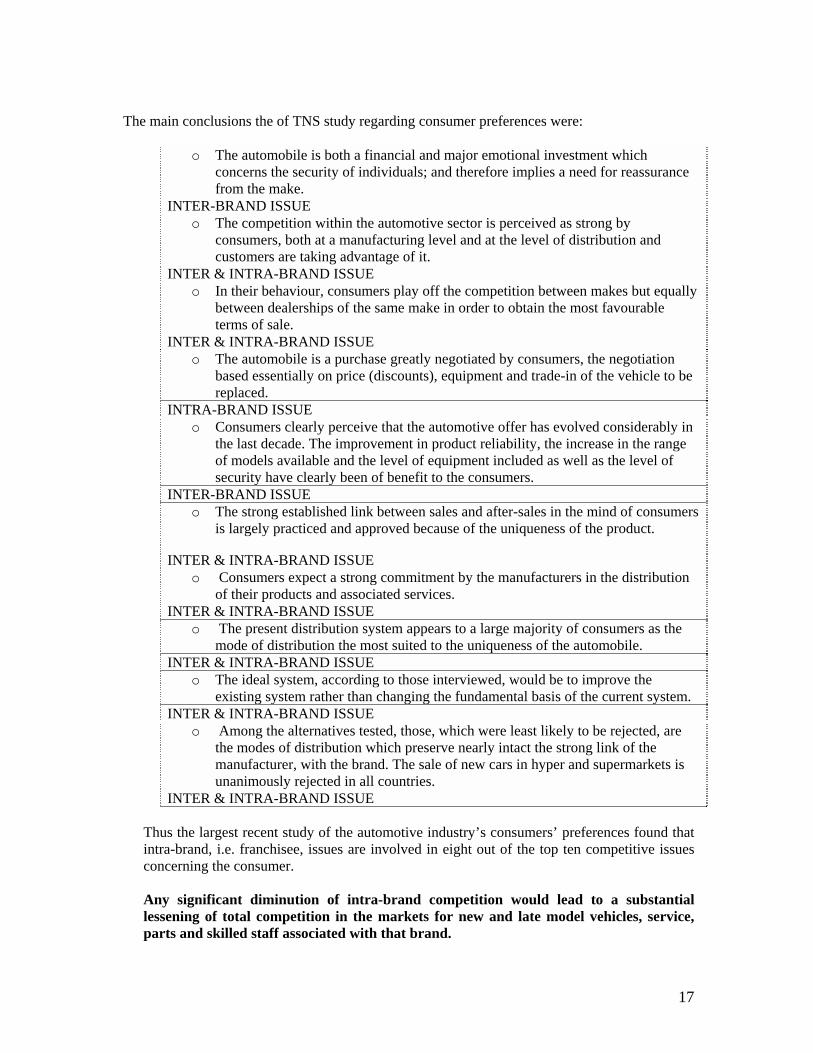

The main conclusions the of TNS study regarding consumer preferences were:

o The automobile is both a financial and major emotional investment whichconcerns the security of individuals; and therefore implies a need for reassurancefrom the make.

INTER-BRAND ISSUEo The competition within the automotive sector is perceived as strong by

consumers, both at a manufacturing level and at the level of distribution andcustomers are taking advantage of it.

INTER & INTRA-BRAND ISSUEo In their behaviour, consumers play off the competition between makes but equally

between dealerships of the same make in order to obtain the most favourableterms of sale.

INTER & INTRA-BRAND ISSUEo The automobile is a purchase greatly negotiated by consumers, the negotiation

based essentially on price (discounts), equipment and trade-in of the vehicle to bereplaced.

INTRA-BRAND ISSUEo Consumers clearly perceive that the automotive offer has evolved considerably in

the last decade. The improvement in product reliability, the increase in the rangeof models available and the level of equipment included as well as the level ofsecurity have clearly been of benefit to the consumers.

INTER-BRAND ISSUEo The strong established link between sales and after-sales in the mind of consumers

is largely practiced and approved because of the uniqueness of the product.

INTER & INTRA-BRAND ISSUEo Consumers expect a strong commitment by the manufacturers in the distribution

of their products and associated services.INTER & INTRA-BRAND ISSUE

o The present distribution system appears to a large majority of consumers as themode of distribution the most suited to the uniqueness of the automobile.

INTER & INTRA-BRAND ISSUEo The ideal system, according to those interviewed, would be to improve the

existing system rather than changing the fundamental basis of the current system.INTER & INTRA-BRAND ISSUE

o Among the alternatives tested, those, which were least likely to be rejected, arethe modes of distribution which preserve nearly intact the strong link of themanufacturer, with the brand. The sale of new cars in hyper and supermarkets isunanimously rejected in all countries.

INTER & INTRA-BRAND ISSUE

Thus the largest recent study of the automotive industry’s consumers’ preferences found thatintra-brand, i.e. franchisee, issues are involved in eight out of the top ten competitive issuesconcerning the consumer.

Any significant diminution of intra-brand competition would lead to a substantiallessening of total competition in the markets for new and late model vehicles, service,parts and skilled staff associated with that brand.

18

Dr. Lademann & Partner Gesellschaft fur Unternehmensund Kommunalberatung mbHEuropean Commission Report December 2001: Most of the TNS Survey findings wereconfirmed and re-enforced by Lademann et al in their “Customer Preferences for existing andpotential Sales and Servicing Alternatives in Automotive Distribution” report (Dec 2001)commissioned by the European Commission Competition Directorate-Generale. Lademann useddifferent methodology (Adaptive Conjoint Analysis) with a smaller sample (500) and a differentmix of five European countries (The Netherlands replaced Italy). The remarkable similarity inthe findings of the two reports is therefore mutually re-enforcing and more robust. Weincorporate certain relevant parts of it here:

Exhibit 15. Extracts from The Lademann Survey Source: “Customer Preferences for existing and potential Sales and Servicing Alternatives inAutomotive Distribution” Dr. Lademann & Partner Gesellschaft fur UnternehmensundKommunalberatung mbH. (Dec 2001).

Importance of the marketing and competitive instruments studied

The survey showed that the various features investigated were of similar importance to theconsumers in the five countries chosen. The type of after-sales servicing alternative proved to bethe most important feature, followed by advice from a salesperson and the type of salesalternative. Then came, in order of importance: the ability to test- drive the vehicle, the distanceto the workshop, the delivery time and the freedom to select equipment.The high value placed on after-sales servicing, as well as the importance of personal advice,shows that, when a new car is being purchased, the buying phase is already overshadowed by theexpectations placed on the utilisation phase. Therefore after-sales servicing is already of utmostimportance at the time of purchase.

It is also worth noting that price and personal contact with the dealer are seen to be of lesserimportance in comparison to the other features. This initially surprising statement becomesplausible, however, when looking at the research method: faced with the question of whether ahigh discount on the purchase of a new car is more important than, for example, doing withoutexpert advice, a test drive or an authorized workshop, the consumers always choose theseessential features of quality rather than going for the price reduction.

Price levels and personal contact with the dealer only gain in importance when the quality-oriented expectations of the buying process and the servicing are absolutely assured. Converselythis finding shows that the price (or discount given) or personal contact are hardly suitableinstruments for giving a supplier a competitive edge, unless he also offers the highly valuedquality features. The comparatively small competitive value of price is also due to the pricetransparency of the market. Because of the transparency of the market, the high mobility of theconsumers, and their limited brand and workshop loyalty, car dealers tend to offer the samediscounts as their competitors in order to bind customers to them. In this way attempts are madeto compete with other distributors and after-sales servicing providers.

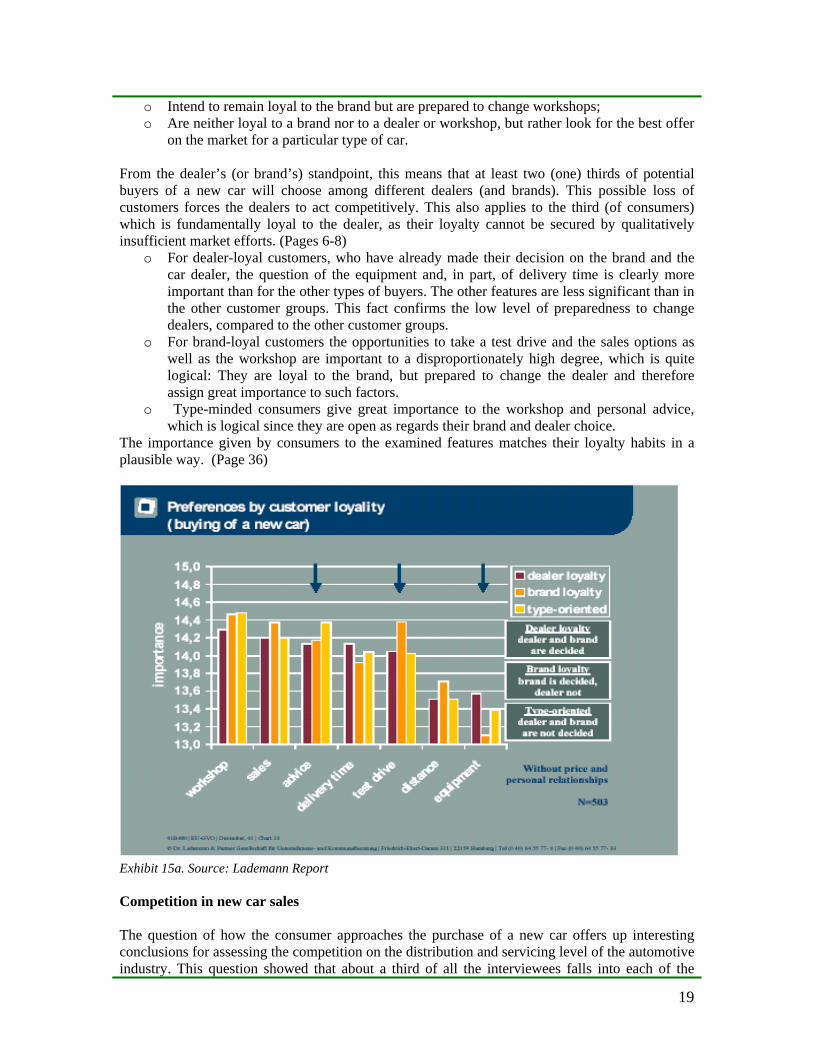

Brand and Dealer Loyalty

From the loyalty of consumers to a particular brand or dealer and his workshop, conclusions canbe drawn about the intensity of the competition within and between brands. The survey hasshown that approximately a third of the consumers buying a new car

o Intend to remain loyal to the dealer or the workshop and therefore also to the brand;

19

o Intend to remain loyal to the brand but are prepared to change workshops;o Are neither loyal to a brand nor to a dealer or workshop, but rather look for the best offer

on the market for a particular type of car.

From the dealer’s (or brand’s) standpoint, this means that at least two (one) thirds of potentialbuyers of a new car will choose among different dealers (and brands). This possible loss ofcustomers forces the dealers to act competitively. This also applies to the third (of consumers)which is fundamentally loyal to the dealer, as their loyalty cannot be secured by qualitativelyinsufficient market efforts. (Pages 6-8)

o For dealer-loyal customers, who have already made their decision on the brand and thecar dealer, the question of the equipment and, in part, of delivery time is clearly moreimportant than for the other types of buyers. The other features are less significant than inthe other customer groups. This fact confirms the low level of preparedness to changedealers, compared to the other customer groups.

o For brand-loyal customers the opportunities to take a test drive and the sales options aswell as the workshop are important to a disproportionately high degree, which is quitelogical: They are loyal to the brand, but prepared to change the dealer and thereforeassign great importance to such factors.

o Type-minded consumers give great importance to the workshop and personal advice,which is logical since they are open as regards their brand and dealer choice.

The importance given by consumers to the examined features matches their loyalty habits in aplausible way. (Page 36)

Exhibit 15a. Source: Lademann Report

Competition in new car sales

The question of how the consumer approaches the purchase of a new car offers up interestingconclusions for assessing the competition on the distribution and servicing level of the automotiveindustry. This question showed that about a third of all the interviewees falls into each of the

20

following categories:

o Loyal to the dealero Loyal to the brando Model-oriented

This result shows that inter-brand competition is mainly due to model-oriented consumers. Thisthird would, in our opinion, suffice to force the dealers to act competitively, as they wouldotherwise lose a third of their sales.

The survey shows that intra-brand competition is due to about a third of new car buyers, whoobviously seek out numerous car dealers selling one brand.35 It cannot be assumed that theremaining third, which is dealer-loyal (brand and dealer are decided on before the purchase of anew car) is insignificant for competition. For they will only remain loyal to their brand and dealeras long as the price and servicing of their car and dealer suit them.

Overall the findings regarding brand and dealer loyalty indicate intensive competition betweendealers and between manufacturers. For the brand-owners (industry) as well as the dealers sellingthese brands must, in their actions on the market, take into account that two-thirds of allconsumers are prepared to seek out other possibilities.36 This assessment is underlined by thebrand-loyalty in new car purchases in Germany, which is quoted at 57%.37 This also underlinesthe assessment regarding competition.

The findings regarding the accepted distances from servicing providers, which are clearlysurpassed by the distance travelled when buying a new car,38 show that the consumer currently hasa number of possibilities available, within one brand as well as among competing brands.

Functional competition is always present when the provider (here the automotive industry andtrade) must take the competitors into consideration in his actions on the market, and is forced totake these into consideration. One can assume this to be the case from the analysis of preferencesand in view of the mobility demonstrated by consumers, the limited brand and dealer loyalty aswell as the market transparency with respect to discounts.39

Market structure dynamics from the perspective of consumer preferences

The conjoint analysis of consumer preferences shows a tight, brand-exclusive connection betweensales and after-sales servicing. The consumer generally anticipates the later utilisation phase atthe time of buying a new car, or takes into account related experience. Already at the purchase ofa new car the subject of after-sales servicing has the highest preference. It is also noticeable thatthe benefit of a sales and servicing alternative is valued higher if it is brand-specific. Conversely,customer benefits decrease the more sales and servicing are manufacturer-dependent or notbrand-exclusive. In our opinion, this can be explained by the advantages of specialisation asopposed to all-brand suppliers and is incidentally a phenomenon that can be seen in otherconsumer goods areas apart from the automotive sector.40 New, stripped-down salesconcepts without their own after-sales servicing have practically no chance as long as carsrequire qualified maintenance and repairs (and the mobility of many people depends on thereliability, safety and durability).Based on this, the market simulations, from the perspective of preference analysis, can besummarised as follows:

o If sales alternatives that move away from the current pillars of sales brandexclusivity, an integrated workshop, personal advice and test drives - enter the

21

market, extensive market opportunities for direct sales by manufacturers wouldresult.

o The separation of sales (trade) and servicing (craft) would lead to dramatic structuralchanges in distribution. The market shares lost by franchise dealers would againbenefit the manufacturers direct sales systems.

o The market opportunities of pure sales channels would not rise above a nichefunction, as long as they operated in a system without servicing, personal advice andtest drives. This is especially true for the manufacturer-independent Internet dealerand car-sector-unrelated retailers.

o From a competitive view, these structure scenarios would not fit consumerpreferences better than the current situation. It could even lead to a lowering ofquality in sales and servicing provision, if certain services (workshop, advice, testdrives, even choice of equipment) are reduced or disappear due to a price wardeveloping in an even more fragmented and intensively competitive market.

A radical change in today’s sales and after-sales servicing structures due to the entry of salesalternatives without workshops, personal advice and test drive possibilities into the market wouldstrengthen the influence of manufacturers in new car trade on the retail level through an increaseon direct sales. Overall this would lead to market structures that fit consumer preferences lessthan today’s. 35 This result corresponds to the findings of the Taylor-Nelson-Sofres Study, according to which two-thirds of new carbuyers who are not brand-loyal seek out different brands and different dealers. Only 47% of brand-loyal consumers, onthe other hand, go to dealers selling the same brand; Cf. Taylor-Nelson-Sofres. Publ., Attitudes towards the EuropeanAutomotive Distribution System, Executive Summary Report, 2000, in the following TaylorNelson-Sofres/2000.36 In fact the purchasing process is a fairly complex process with many phases, which for most buyers, by the way,overlaps with the utilisation phase of the car owned before, and is shaped by this. Brand-loyalty (and probably alsodealer-loyalty) wavers throughout the planned utilisation and buying- decision that follows: see Diez/2000.37Cf. DAT/Veedol Report 1999, p. 4138 So on average 52 minutes by car are accepted here; Cf. Automobilverkauf/1999, 20.39 On the other hand, particular market results (e.g. size of discounts, amount of re-imports, etc.) are not decisive forthe competitive structure of a market. These do not allow conclusions on competition because they can be aconsequence of, for example, overcapacity (discounts) or of tax systems (amount of re-imports) or simply ofconsumer preferences (a lack of acceptance of re-import offers). From anti-trust legislation, only those restrictions thatcome from companies are relevant (e.g. hindering re-importers or consumers buying directly abroad), not the consumerdoing without other possibilities (e.g. regarding re-import providers). In addition, market results are not known inadvance, because they are the result of market processes. For this reason it cannot be said, which market results reflectcompetitive restrictions and which reflect essential competition. Therefore, also with Article 81, Section 81 (EU treaty)one can only ask whether the market results follow from a competitive market structure characterised by latentpossibilities; only then is competition taking place in new car sales . no matter what the market results are.40 For example, an ADAC comparison of customer service quality shows serious qualitative disadvantages to fast-fitrepair chains in comparison to authorised workshops, Cf. issue 11/2001; the quality of the advice given in specialitystores is as a rule higher than in department stores, but often even better in manufacturer-run outlets, see e.g. o.V.Outlet Malls in Consumer Reports 1998, p. 20ff. Particularly with technically sophisticated products requiringexplanation (e.g. in the areas of hifi, video, computers, software) it can be observed that retailers with a wide range ofgoods compensate for the lack of qualified advice with an aggressive price strategy. (Pages 61 – 63)

22

Intensity of competition

The findings regarding brand and dealership loyalty listed in this report have been taken as anindirect indication of intense competition in new car sales.

o Taylor-Nelson-Sofres (TNS)44 confirms this assessment in two ways. First, they askedconsumers directly about their perception of the intensity of competition betweendealerships. 80% assessed the competition as strong or very strong, 46% also noted arecent increase in the competitive intensity.45

o Secondly, TNS came to results similar to this study’s regarding the choice of dealer.According to TNS, barely 37% of all interviewees (4,000) remain loyal to their brand (re-purchasers)46 while our study found that about 63% intend to buy the same brand again.This is no contradiction, as TNS investigated the actual, and this study the intendedbrand-loyalty.

o Besides, other studies show that the intended brand loyalty is subject to considerablevariation during the utilisation and buying process; shortly after the purchase it is mostlyabout 90% and then it drops throughout the length of the utilisation period.47 Neverthelessour findings regarding intended brand loyalty are confirmed by other reports.48

The extent of brand loyalty may differ from study to study, but all the findings from theviewpoint of the private end consumer confirm a high intensity of intra-brand and inter-brand competition in new car sales.49

44 Cf. Taylor-Nelsen-Sofres Automotive, Attitudes towards the European Automotive Distribution System,Executive Summary Report, November 2000, Taylor-Nelsen-Sofres Automotive, Perception de laDistribution Automobile enEurope, Rapport Europe, Phase Quantitative, December 2000; cited in thefollowing text as TNS, Summary or Rapport.45 Cf. TNS Summary, p.4.46 Cf. TNS Summary, p.6.47 Cf. Diez/2000, 64f.48 According to the DAT-Veedol Report only 57% of new car buyers in Germany remain loyal to theirbrand, Cf. Diez/2000, p.64; Auto-Motor-Sport reports similar data regarding brand loyalty, Die besten Autos2001; among those consumers who have already made a decision, about 48% are potentially brand-loyal.49 However it is conceivable that the intensity of the competition could increase even more, e.g. throughnew sales alternatives or concentration of dealerships (Page 65)

Conclusions

Overall, the results of the consumer survey show that new distribution channels will in generalonly be accepted in connection with a minimum of quality-related services. New car retailerswho did not also provide brand-specific servicing facilities, test drives, a choice of equipment (atleast within limits), advice, and integrated customer service, would be likely to have only a verylimited success on the market. The preference structure shows that a lack of any or all of theseadvantages cannot be countered by price reductions.

In addition the survey made clear that brand-exclusive distribution and after-sales servicingconcepts are preferred. The skills possessed by dealers which sell and possibly maintain differentbrands are less valuable to most consumers than those possessed by dealers that specialise in onebrand, and have a close connection to, the manufacturer giving these brand-specialist dealers acompetitive advantage. In our opinion, this is connected to the present demand for qualified salesand servicing offers on the basis of which consumer expectations of safety, reliability and

23

durability can be better met by brand exclusivity.

Thus, the current market structures in new car sales and the brand-exclusive linking of sales andservicing are in line with the preferences of most consumers. Left to consumer preferences alone,the importance of re-importers will only increase slightly, and this in spite of the still inadequatedegree of price convergence within the European Union. The same applies to new car sales bymanufacturer-independent Internet suppliers. Younger buyers of new cars - contrary to what onemight expect, prefer the franchise dealers more than older consumers do, because for a majorityof them buying a new car involves taking a high risk and at the same time they have less buyingexperience. Only the multi-brand dealers, assuming they offer brand-specific after-sales servicing,appear to have some chances of success on the market. A growing number of possible new salesalternatives would however mainly improve the chances for manufacturers to increase their directsales. (Page 10)

End of extracts from Lademann’s Survey.

1.3 Evidence of Regional Collaborative Behaviour

1.31 Europe

Despite the apparent competitiveness of the automotive industry the major vehicle manufacturershave recently displayed regional anti-competitive behaviour. The major changes to Regulation1475/95 in the European Community, the ‘block exemption’ regulation, being enacted this year,were predicated by the major automobile companies failing to behave in the competitive mannerprescribed by the original regulation.

The EC Treaty lays down a basic rule (Article 81(1)) banning agreements which could have anti-competitive effects. However many common pro-competitive agreements, includingmanufacturer/dealer franchise agreements, contain clauses which limit the ability of one of itsparties to compete. Therefore Article 81(3) permits the EC to exempt such agreements from theban. The Commission often exempts a whole class of such agreements on condition they respectcertain competitive requirements and that they do not contain clauses proscribed by the Treaty.Such exemptions are called ‘Block Exemptions.’ The current automotive industry distributionblock exemption, Regulation 1475/95, expires in September this year and the new draft BlockExemption will be phased in over 24 months from then. The new regulation will have a ‘sunsetclause’ requiring its review in 2010.

In November 2000 an EC evaluation report evaluating the block exemption regulation(downloadable from: http://europa.eu.int/competition/car_sector/distribution…/report ) found thatthe terms of the 1995 block exemption had not delivered the degree of either inter or intra brandcompetition expected of it and, as a consequence:

o Consumers were unable to access their ‘Single Market’ right to buy their vehicleswherever in the EC the price was lowest.

o Dealers were still too dependent upon the manufacturers and

o Consumers were paying too much for service and parts.

24

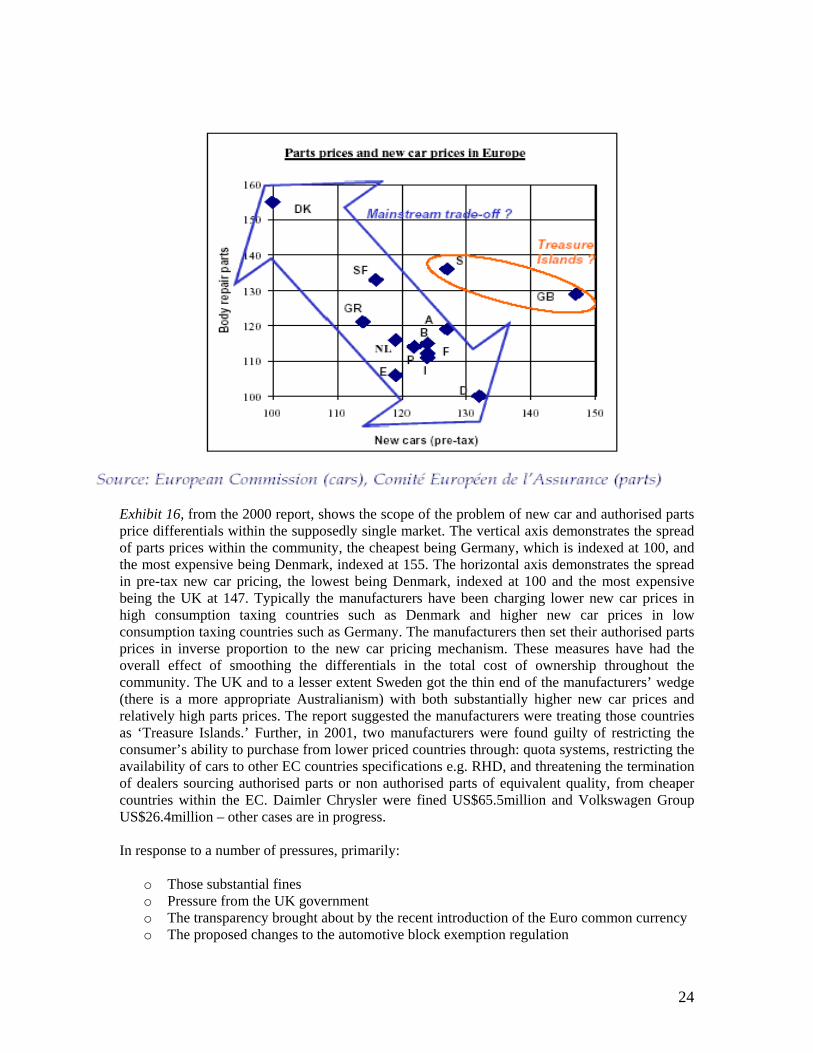

Exhibit 16, from the 2000 report, shows the scope of the problem of new car and authorised partsprice differentials within the supposedly single market. The vertical axis demonstrates the spreadof parts prices within the community, the cheapest being Germany, which is indexed at 100, andthe most expensive being Denmark, indexed at 155. The horizontal axis demonstrates the spreadin pre-tax new car pricing, the lowest being Denmark, indexed at 100 and the most expensivebeing the UK at 147. Typically the manufacturers have been charging lower new car prices inhigh consumption taxing countries such as Denmark and higher new car prices in lowconsumption taxing countries such as Germany. The manufacturers then set their authorised partsprices in inverse proportion to the new car pricing mechanism. These measures have had theoverall effect of smoothing the differentials in the total cost of ownership throughout thecommunity. The UK and to a lesser extent Sweden got the thin end of the manufacturers’ wedge(there is a more appropriate Australianism) with both substantially higher new car prices andrelatively high parts prices. The report suggested the manufacturers were treating those countriesas ‘Treasure Islands.’ Further, in 2001, two manufacturers were found guilty of restricting theconsumer’s ability to purchase from lower priced countries through: quota systems, restricting theavailability of cars to other EC countries specifications e.g. RHD, and threatening the terminationof dealers sourcing authorised parts or non authorised parts of equivalent quality, from cheapercountries within the EC. Daimler Chrysler were fined US$65.5million and Volkswagen GroupUS$26.4million – other cases are in progress.

In response to a number of pressures, primarily:

o Those substantial fineso Pressure from the UK governmento The transparency brought about by the recent introduction of the Euro common currency o The proposed changes to the automotive block exemption regulation

Exhibit 16.

25

there has been some movement towards pricing convergence within the EC over the last fifteenmonths. It has been this convergence rather than a buoyant economy that led to a record year fornew car sales in the UK in 2001 and year to date 2002. There is still some way to go to achieveCommunity pricing parity; as of yesterday it was possible for a UK consumer to source a newPeugeot to UK specifications from a Dutch dealer via Virgin Cars via the internet at 20% belowthe UK list price.

1.32 Echoes from North America

Other evidence of collaboratively charging what a market will bear, with scant regard to costcurves, exists much closer to Detroit:

Exhibit17. ‘The borderline price wheeze’Source: Institute of the Motor Industry Journal, Wyatt, (12/6/02)

The scene is familiar - wide discrepancies between new vehicle prices on either side of aninternational border. In one country, dealers grateful for the low prices they enjoy and theopportunity of selling across the border; on the other side, dealers either complaining bitterly ofunfair competition or else joining in the disputed traffic. And in the middle are indignantmanufacturers threatening legal action against what they perceive as infractions of their franchiseagreements.

The British reader might well have the sense of déjà vu, but this is not a European story, it’s apricing anomaly in the very cradle of commercial competition – North America. The past severaldecades have seen a steady fall in the value of the Canadian dollar against its American counterpart.At one time almost at parity, it now rates at only 58 U.S. cents. Manufacturers, however, have donelittle to adjust for this devaluation, thereby progressively causing a substantial gap as expressed inUS dollars.A good example is the Dodge 1500 Pick-up truck, listed at US$22,456 in the United States and atC$22,500 (US$17,540) in Canada, a difference of US$4,916. If one factors in various popular add-ons such as automatic transmission, leather seats and a cassette/CD player, that difference widens toUS$7,811 (leather seats are $889 in Canada, $1,380 in America). Studies taken two years agoshowed the average difference to be US$2,515, before accessories, since which time the gap hasfurther widened.

Unlike Europe, the controversy on this side of the Atlantic centres less on carmakers being accusedof gouging the retail customer by their lopsided pricing policies than on the damage done to thosevery manufacturers by wayward dealers taking advantage of the loophole. Dealers in NorthAmerica may well enjoy greater legal protection than in Europe, but in this instance it is thecarmakers that have resorted to the courts, not only to stop the traffic but to punish by financialsanctions those they regard as law-breakers. One can appreciate their concern; the traffic hasrocketed from 15,000 vehicles in 1996 to well over 200,000 in 2001 as the currency gap haswidened.

The litigation is aimed at Canadian dealers, on the grounds that export sales (whether direct orindirect) are expressly forbidden under the terms of their franchise agreement. Legal actions takevarious forms. Marlborough Ford of Calgary was penalised approximately $125,000, representingthe price difference on 23 vehicles (later reduced to $52,000 on ten vehicles), but the Alberta Courtof Queen’s Bench handed down an injunction, heading off Ford’s action. However, in legalcircles, nothing is final until ‘the fat lady sings’, the fat lady in this case being Canada’s SupremeCourt, where the case is likely to end up.

26

Already Ford has given notice of its intention to appeal, but it may face an uphill battle, judging bythe Alberta judge’s comments. Criticising Ford for its “lack of clearly-defined procedures toestablish an even playing field”, he characterised the manufacturer’s practices as a “nebulous andill-defined state of affairs that is constantly subject to its own unilateral and arbitrary review”. So, one may ask, what’s new?

Echoing a point made by the dealer’s attorney, the judge went on: “The charge is a clear penalty,not justified by way of any credible evidence of a figure commensurate with the loss suffered byFord of Canada or its network of dealers.” These last words have an ominous ring, perhaps castingdoubt on the legality of the manufacturer’s dealer agreement, not to mention questioning the logicof its Canadian pricing policies. After all, a not inconsiderable number of vehicles retailed inCanada are made in the US. Certainly the precise clause in the agreement that forbids export saleswill come under close scrutiny. When I spoke with Ted Babie, owner of Marlborough Ford, heconceded that these cross-border sales do contravene the terms of the agreement, but points out thatthe clause arose in an unusual way. Some years ago, as the price gap became significant, Fordissued a single-page addendum to the agreement outlawing such sales, asking for it to be “stapledbetween pages 15 and 16”. Over the years since, dealers have been instructed to interrogatepotential customers, culminating in a four-page questionnaire. Not exactly the way to encouragebuyers. Babie explains that brokers across the border go to great lengths to evade being detected,using relatives’ and neighbours’ names. He therefore challenges Ford’s action, not only in itsprecise financial form but as an unreasonable, even unenforceable, burden on the dealer, effectivelytrying to prevent the buyer getting the best price. In terminating the franchise of a dealership inQuebec, Poirier Valleyfield, Ford accuses the dealer of being “an egregious and long-time repeatoffender [in engaging in export sales]”. Ford pleads that it is merely enforcing its dealer sales andservice agreement. Poirier Valleyfield, for its part, contends that there has been no contravention ofits agreement, and consequently repudiates Ford’s decision. Both parties have accepted court-appointed arbitration, the hearing to take place late summer. Literally, the jury is still out.

Of course, Ford is not the only manufacturer aggrieved over this traffic. Faced with a growingproblem in 1999, Honda abruptly stopped honouring warranties on the ‘grey’ cars, and claims nowto have halted the traffic. Other manufacturers point to dealer support. In backing Chrysler/Dodge,Ken Zangara, owner of Zangara Dodge of Albuquerque, New Mexico, and chairman of theNational Dodge Dealer Council, reserves particular contempt for non-franchise middlemen(brokers) who hover around this trade like bees around a honeypot. One broker in Port Huron,Michigan, last year processed 10,000 cars and has set his sights on 15,000 in the current year. Forhis brokerage income, he merely deals with compliance and the paperwork, posting a bond andconverting the speedometer to miles from metric, before passing on to a car dealer.Chrysler/Dodge is also threatening to withhold warranty, complaining that “thousands of cars” arefinding their way across the border. Even so, one Canadian Dodge dealer, who denies any part inthe illegal traffic, doubts the carmaker’s resolve to do so, having itself for years bought off-leaseand fleet cars in Canada and resold them in the United States. Then again, one dealer in Montana,just 100 miles south of the border, shrugs off the warranty issue anyway. He says he would just buythe customer an aftermarket warranty.

No one could have resisted the pressure for change more fiercely than Europe’s motormanufacturers, but the result was inevitable – a trend to more consistent pricing, which it is hopedwill continue with the advent of the euro. Not only are the courts in North America traditionallypro-dealer, and these artificial pricing policies appear to be difficult to defend, but themanufacturers have chosen to air the conflict. They may well live to regret doing so.

27

1.4 The Australian Automotive Industry - Overview

1.41 Relative Economic Importance of the Australian Motor Industry

Exhibit 18

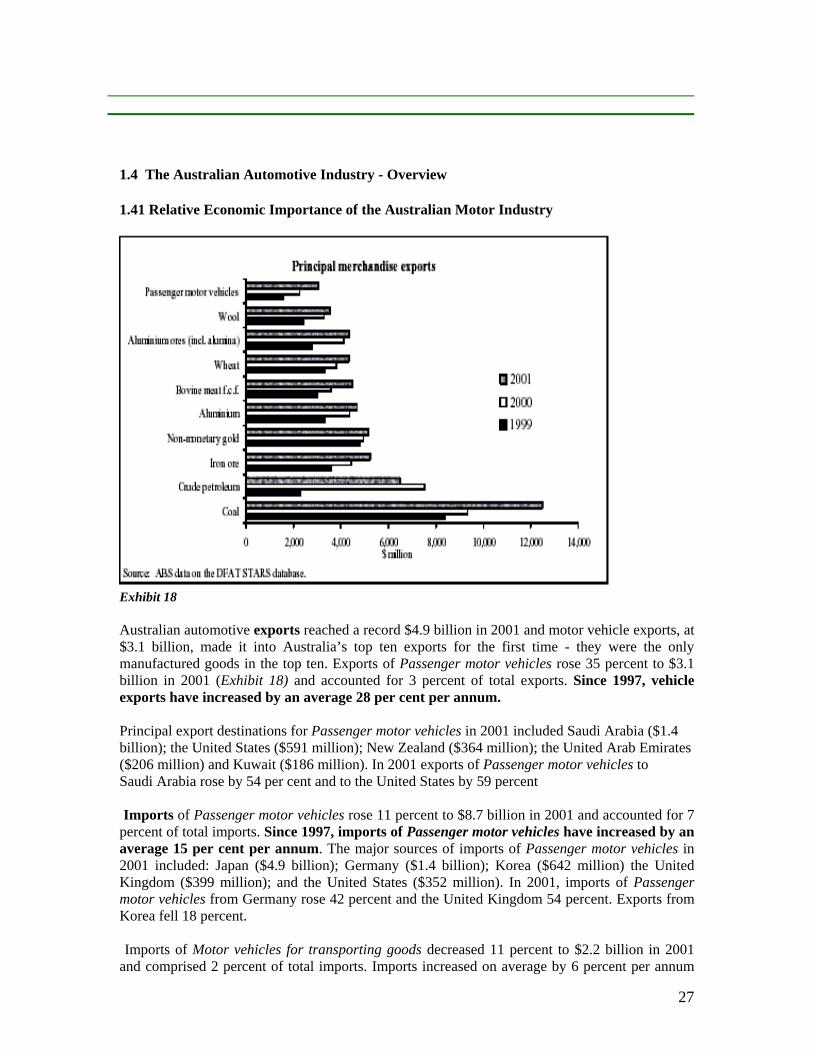

Australian automotive exports reached a record $4.9 billion in 2001 and motor vehicle exports, at$3.1 billion, made it into Australia’s top ten exports for the first time - they were the onlymanufactured goods in the top ten. Exports of Passenger motor vehicles rose 35 percent to $3.1billion in 2001 (Exhibit 18) and accounted for 3 percent of total exports. Since 1997, vehicleexports have increased by an average 28 per cent per annum.

Principal export destinations for Passenger motor vehicles in 2001 included Saudi Arabia ($1.4billion); the United States ($591 million); New Zealand ($364 million); the United Arab Emirates($206 million) and Kuwait ($186 million). In 2001 exports of Passenger motor vehicles toSaudi Arabia rose by 54 per cent and to the United States by 59 percent

Imports of Passenger motor vehicles rose 11 percent to $8.7 billion in 2001 and accounted for 7percent of total imports. Since 1997, imports of Passenger motor vehicles have increased by anaverage 15 per cent per annum. The major sources of imports of Passenger motor vehicles in2001 included: Japan ($4.9 billion); Germany ($1.4 billion); Korea ($642 million) the UnitedKingdom ($399 million); and the United States ($352 million). In 2001, imports of Passengermotor vehicles from Germany rose 42 percent and the United Kingdom 54 percent. Exports fromKorea fell 18 percent.

Imports of Motor vehicles for transporting goods decreased 11 percent to $2.2 billion in 2001and comprised 2 percent of total imports. Imports increased on average by 6 percent per annum

28

between 1997 and 2001. In 2001, imports of Motor vehicles for transporting goods weredominated by Japan ($1.1 billion) and Thailand ($475 million). Other major import sourcesincluded the United States ($287 million); and Germany ($92 million). In 2001, imports fromJapan of Motor vehicles for transporting goods fell by 19 percent, and imports from Thailand fellby 32 percent. Imports from the United States increased by 53 percent in 2001.

Imports of Motor vehicle parts decreased by 15 percent to $2.2 billion in 2001, and comprised 2percent of total imports. Between 1997 and 2001, imports increased by an average 9 per cent perannum. Major sources of imports of Motor vehicle parts in 2001 included: Japan ($867 million);the United States ($542 million); Germany ($202 million); Sweden ($83 million); and Taiwan($54 million). In 2001, imports of Motor vehicle parts from Japan fell by 30 percent and importsfrom the United States fell by 11 percent. (Source: ‘Composition of Trade Australia 2001’ MarketInformation & Analysis Section, Dept. of Foreign Affairs and Trade).

Thus Australia’s trade balance for all motor vehicles was negative $7.8 billion and for motorvehicle parts negative $0.4 billion, a total of negative $8.2 billion. This total vehicle trade netimbalance is roughly equivalent to all of Australia’s gross wheat and aluminium ores exportscombined. The recently announced Ford 4 wheel drive project, GM Holden’s sale of 18,000Monaros, re-badged as Pontiac GTOs, to the USA, the continuation and re-investment ofMitsubushi and the probable expansion of Toyota’s Altona plant are all likely to reduce thisdeficit in the near future. 1.42 Market Size & Characteristics

29

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01

Total Annual Vehicle Units - Market Australiaest.

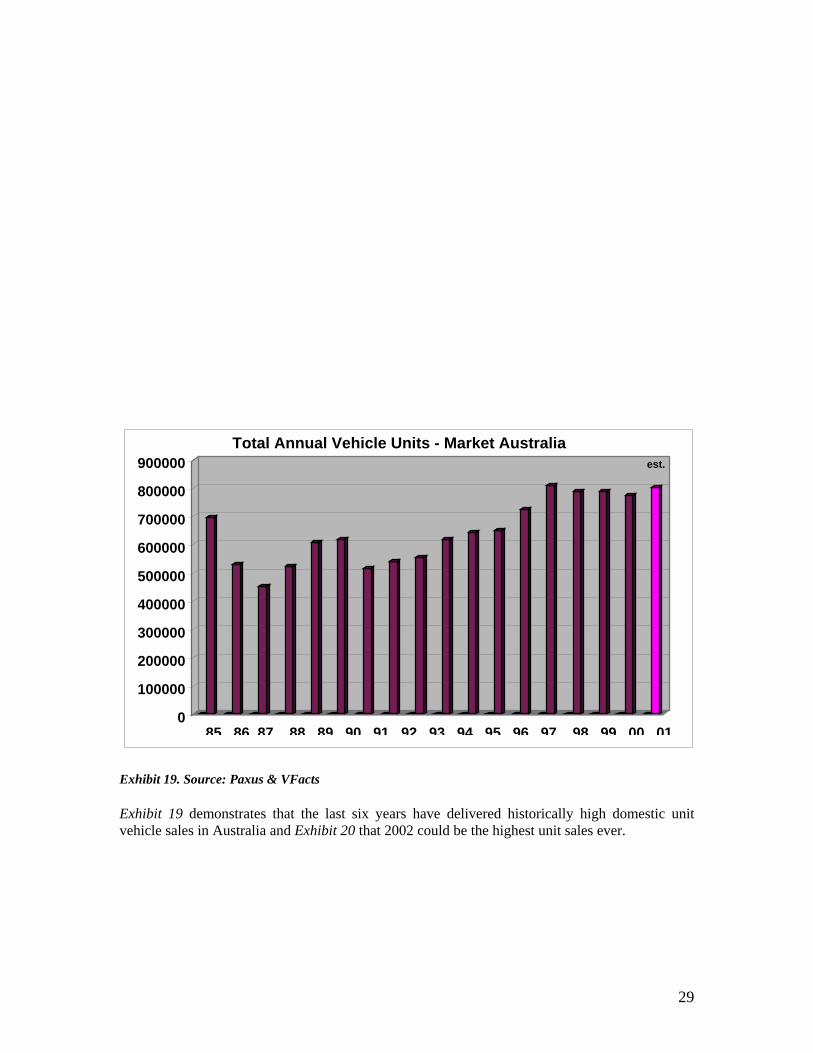

Exhibit 19. Source: Paxus & VFacts

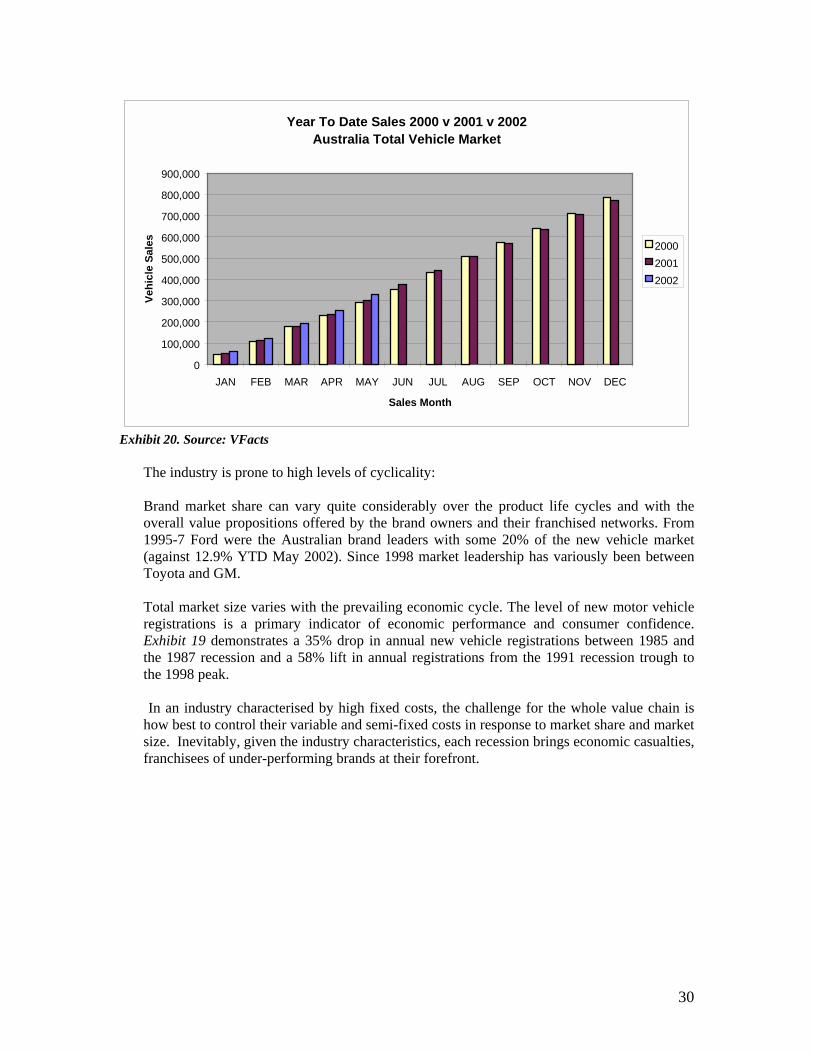

Exhibit 19 demonstrates that the last six years have delivered historically high domestic unitvehicle sales in Australia and Exhibit 20 that 2002 could be the highest unit sales ever.

30

Year To Date Sales 2000 v 2001 v 2002 Australia Total Vehicle Market

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Sales Month

Vehi

cle

Sale

s

200020012002

Exhibit 20. Source: VFacts

The industry is prone to high levels of cyclicality:

Brand market share can vary quite considerably over the product life cycles and with theoverall value propositions offered by the brand owners and their franchised networks. From1995-7 Ford were the Australian brand leaders with some 20% of the new vehicle market(against 12.9% YTD May 2002). Since 1998 market leadership has variously been betweenToyota and GM.

Total market size varies with the prevailing economic cycle. The level of new motor vehicleregistrations is a primary indicator of economic performance and consumer confidence.Exhibit 19 demonstrates a 35% drop in annual new vehicle registrations between 1985 andthe 1987 recession and a 58% lift in annual registrations from the 1991 recession trough tothe 1998 peak.

In an industry characterised by high fixed costs, the challenge for the whole value chain ishow best to control their variable and semi-fixed costs in response to market share and marketsize. Inevitably, given the industry characteristics, each recession brings economic casualties,franchisees of under-performing brands at their forefront.

31

1.5 Competition in the Australian Automotive Industry

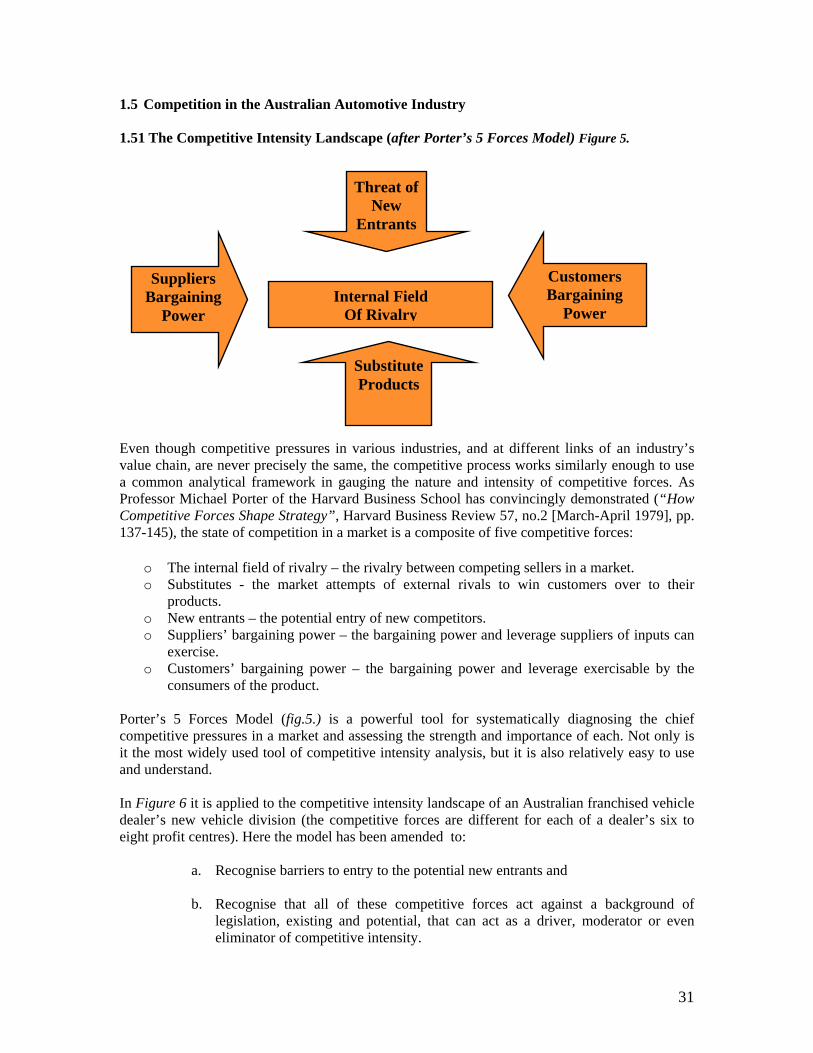

1.51 The Competitive Intensity Landscape (after Porter’s 5 Forces Model) Figure 5.

Even though competitive pressures in various industries, and at different links of an industry’svalue chain, are never precisely the same, the competitive process works similarly enough to usea common analytical framework in gauging the nature and intensity of competitive forces. AsProfessor Michael Porter of the Harvard Business School has convincingly demonstrated (“HowCompetitive Forces Shape Strategy”, Harvard Business Review 57, no.2 [March-April 1979], pp.137-145), the state of competition in a market is a composite of five competitive forces:

o The internal field of rivalry – the rivalry between competing sellers in a market.o Substitutes - the market attempts of external rivals to win customers over to their

products.o New entrants – the potential entry of new competitors.o Suppliers’ bargaining power – the bargaining power and leverage suppliers of inputs can

exercise.o Customers’ bargaining power – the bargaining power and leverage exercisable by the

consumers of the product.

Porter’s 5 Forces Model (fig.5.) is a powerful tool for systematically diagnosing the chiefcompetitive pressures in a market and assessing the strength and importance of each. Not only isit the most widely used tool of competitive intensity analysis, but it is also relatively easy to useand understand.

In Figure 6 it is applied to the competitive intensity landscape of an Australian franchised vehicledealer’s new vehicle division (the competitive forces are different for each of a dealer’s six toeight profit centres). Here the model has been amended to:

a. Recognise barriers to entry to the potential new entrants and

b. Recognise that all of these competitive forces act against a background oflegislation, existing and potential, that can act as a driver, moderator or eveneliminator of competitive intensity.

Internal FieldOf Rivalry

SuppliersBargaining

Power

CustomersBargaining

Power

Threat ofNew

Entrants

SubstituteProducts

32

Here the rivalry between competing sellers – the intra-brand competition, is between the regionalfranchise network (1.54) of the franchisor, which is itself the dominant supplier (1.56). Thesubstitutes are the offerings of the other manufacturers, other brands of this manufacturer and latemodel used examples of the desired vehicle (1.53). The potential new entrants are varied as isexamined later (1.55). The customer mix for non-prestige brands is some 60% fleet content(government, business, fleet-lease companies, hire-car companies etc.) and 40% retail (privateconsumers and micro businesses) (1.57). The legislative background is discussed in 2.0.

1.52 The Competitive Intensity Landscape of a Franchised Vehicle Dealer’s New VehicleDivision (after Porter’s 5 Forces Model) Figure 6.

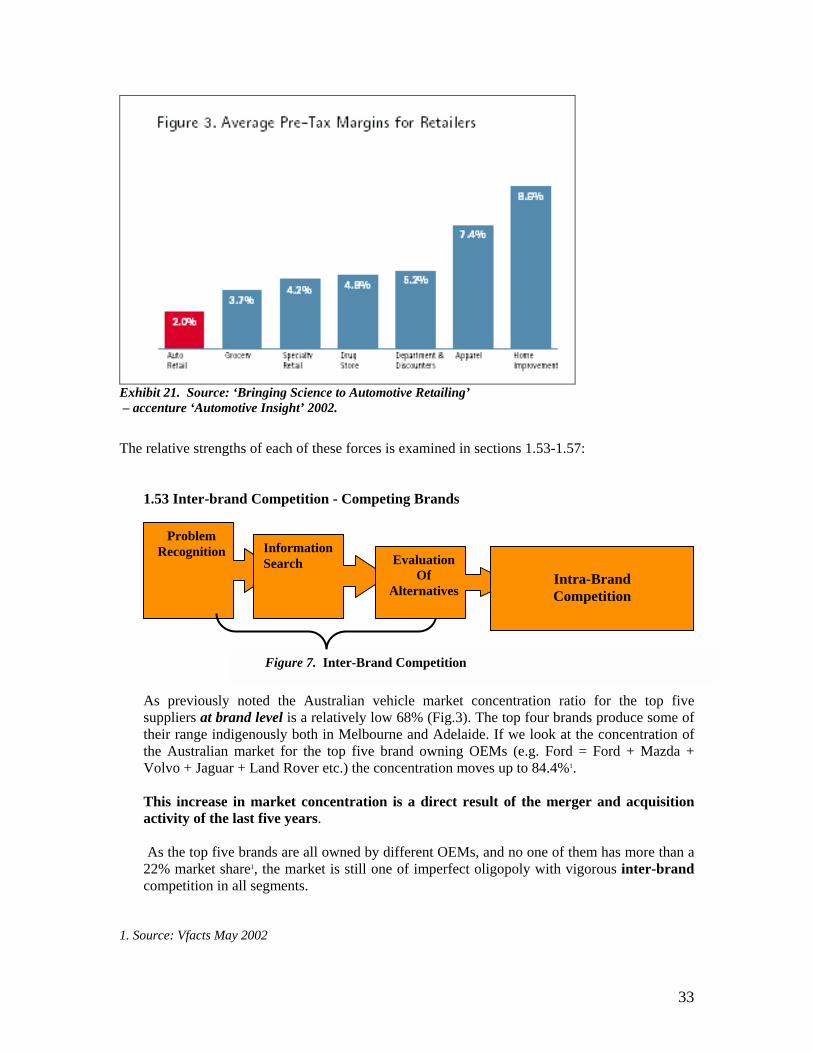

Each of these five forces in the Australian new vehicle market is formidable, as evidenced bythe average net profit before tax of 1.5% of revenue (Aon Martec ‘Dealer Performance andProfitability’ March 2002) and the U.S.A. figure of 2% (Exhibit 21). Exhibit 21 also demonstratesthat competition in the automotive retail industry, as delineated by margin to revenue, is moreintense than in the grocery, specialty retail, drug store, department store/discount chains, appareland home improvement retail markets. These studies are confirmed and made more robust bythe European consumer perceptions described in the TNS Survey (exhibit 4) andLademann’s Report (exhibit 15).

Legislation Legislation

Legislation Legislation

Barriers to entry

Regional Franchise Network1.54

OEM BrandOwner or

Distributor1.56

CustomersFleets 60%

Private 40%1.57

PotentialNew

Entrants1.55

Competing Brands1.53

33

Exhibit 21. Source: ‘Bringing Science to Automotive Retailing’ – accenture ‘Automotive Insight’ 2002.

The relative strengths of each of these forces is examined in sections 1.53-1.57:

1.53 Inter-brand Competition - Competing Brands

As previously noted the Australian vehicle market concentration ratio for the top fivesuppliers at brand level is a relatively low 68% (Fig.3). The top four brands produce some oftheir range indigenously both in Melbourne and Adelaide. If we look at the concentration ofthe Australian market for the top five brand owning OEMs (e.g. Ford = Ford + Mazda +Volvo + Jaguar + Land Rover etc.) the concentration moves up to 84.4%1.

This increase in market concentration is a direct result of the merger and acquisitionactivity of the last five years.

As the top five brands are all owned by different OEMs, and no one of them has more than a22% market share1, the market is still one of imperfect oligopoly with vigorous inter-brandcompetition in all segments.

1. Source: Vfacts May 2002

ProblemRecognition Information

Search EvaluationOf

Alternatives

Figure 7. Inter-Brand Competition

Intra-BrandCompetition

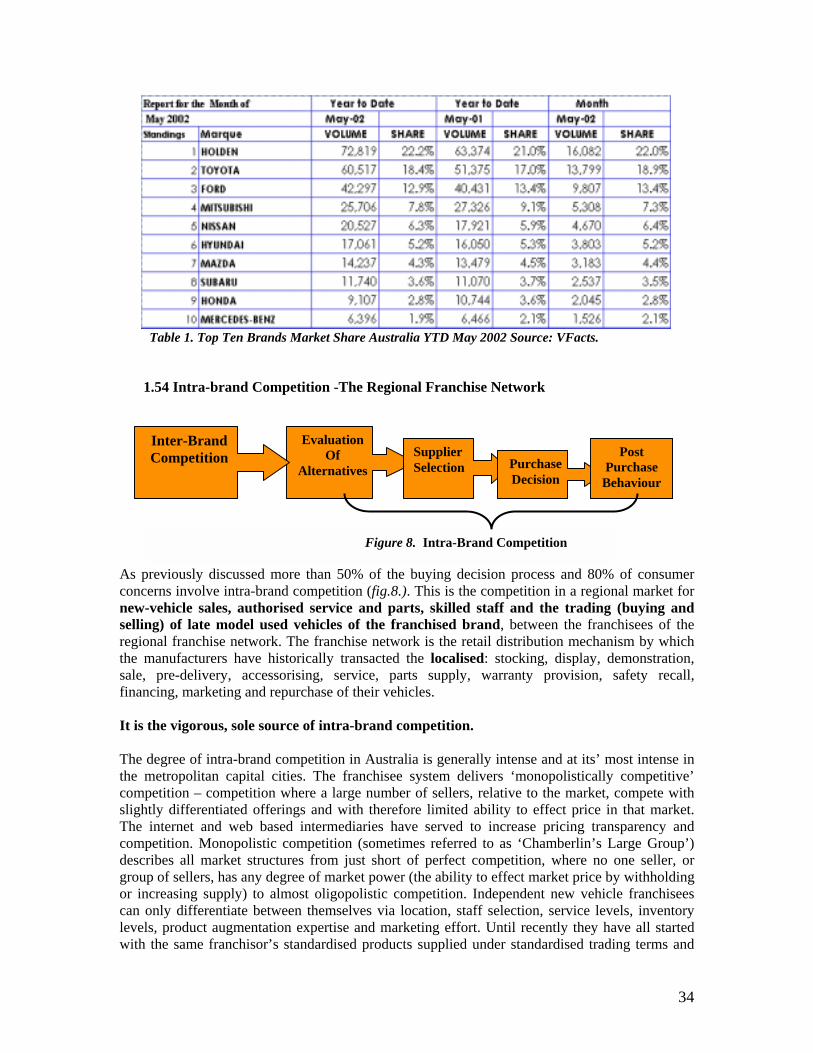

Table 1. Top Ten Brand

1.54 Intra-brand Com

As previously discussed more than 50%concerns involve intra-brand competition new-vehicle sales, authorised service aselling) of late model used vehicles of regional franchise network. The franchisethe manufacturers have historically transale, pre-delivery, accessorising, servicfinancing, marketing and repurchase of th It is the vigorous, sole source of intra-br

The degree of intra-brand competition in the metropolitan capital cities. The francompetition – competition where a large slightly differentiated offerings and withThe internet and web based intermediarcompetition. Monopolistic competition (sdescribes all market structures from justgroup of sellers, has any degree of marketor increasing supply) to almost oligopolcan only differentiate between themselvelevels, product augmentation expertise anwith the same franchisor’s standardised p

EvaluationOf

Alternatives

Inter-BrandCompetition

urce: VFacts.

ork

s Market Share Australia YTD May 2002 So

petition -The Regional Franchise Netw

34

of the buying decision process and 80% of consumer(fig.8.). This is the competition in a regional market fornd parts, skilled staff and the trading (buying andthe franchised brand, between the franchisees of the network is the retail distribution mechanism by which

sacted the localised: stocking, display, demonstration,e, parts supply, warranty provision, safety recall,

eir vehicles.

and competition.

Australia is generally intense and at its’ most intense inchisee system delivers ‘monopolistically competitive’number of sellers, relative to the market, compete with therefore limited ability to effect price in that market.ies have served to increase pricing transparency andometimes referred to as ‘Chamberlin’s Large Group’) short of perfect competition, where no one seller, or power (the ability to effect market price by withholdingistic competition. Independent new vehicle franchiseess via location, staff selection, service levels, inventoryd marketing effort. Until recently they have all startedroducts supplied under standardised trading terms and

SupplierSelection Purchase

Decision

PostPurchase

Behaviour

Figure 8. Intra-Brand Competition

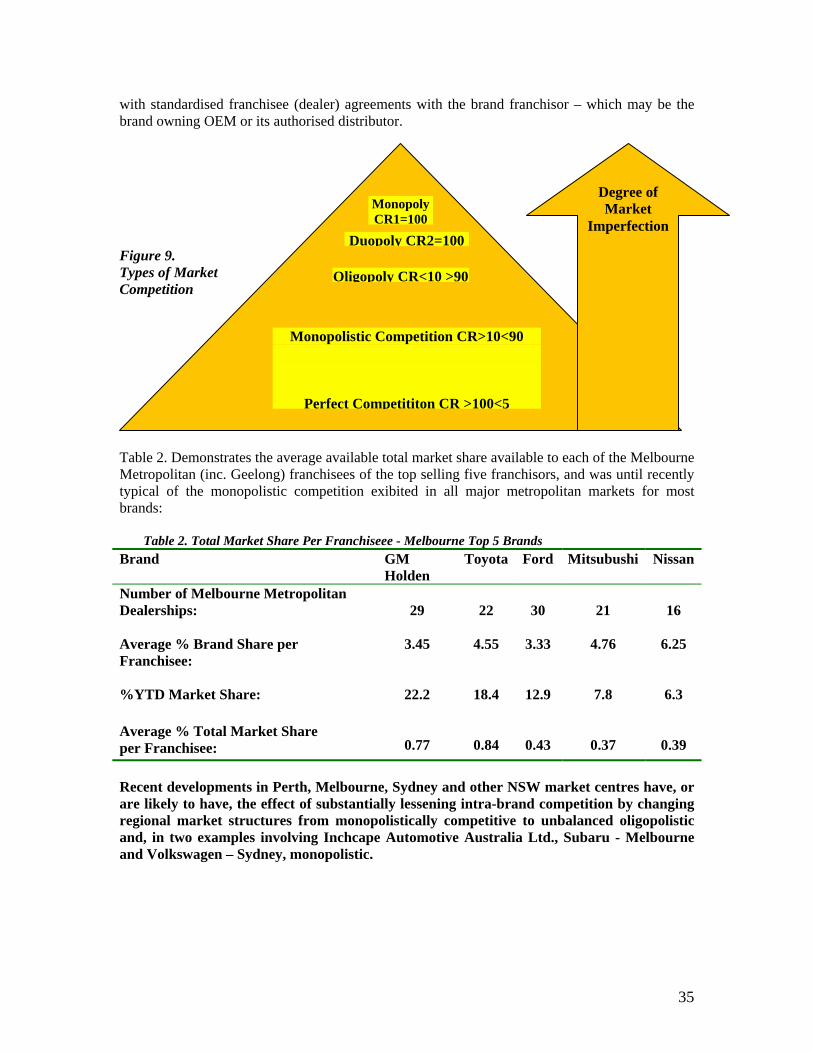

35

with standardised franchisee (dealer) agreements with the brand franchisor – which may be thebrand owning OEM or its authorised distributor.

Figure 9.Types of MarketCompetition

Table 2. Demonstrates the average available total market share available to each of the MelbourneMetropolitan (inc. Geelong) franchisees of the top selling five franchisors, and was until recentlytypical of the monopolistic competition exibited in all major metropolitan markets for mostbrands:

Table 2. Total Market Share Per Franchiseee - Melbourne Top 5 BrandsBrand GM

HoldenToyota Ford Mitsubushi Nissan

Number of Melbourne MetropolitanDealerships:

Average % Brand Share perFranchisee:

%YTD Market Share:

Average % Total Market Shareper Franchisee:

29

3.45

22.2

0.77

22

4.55

18.4

0.84

30

3.33

12.9

0.43

21

4.76

7.8

0.37

16

6.25

6.3

0.39

Recent developments in Perth, Melbourne, Sydney and other NSW market centres have, orare likely to have, the effect of substantially lessening intra-brand competition by changingregional market structures from monopolistically competitive to unbalanced oligopolisticand, in two examples involving Inchcape Automotive Australia Ltd., Subaru - Melbourneand Volkswagen – Sydney, monopolistic.

MonopolyCR1=100

Duopoly CR2=100

Monopolistic Competition CR>10<90

Perfect Competititon CR >100<5

Oligopoly CR<10 >90

Degree ofMarket

Imperfection

36

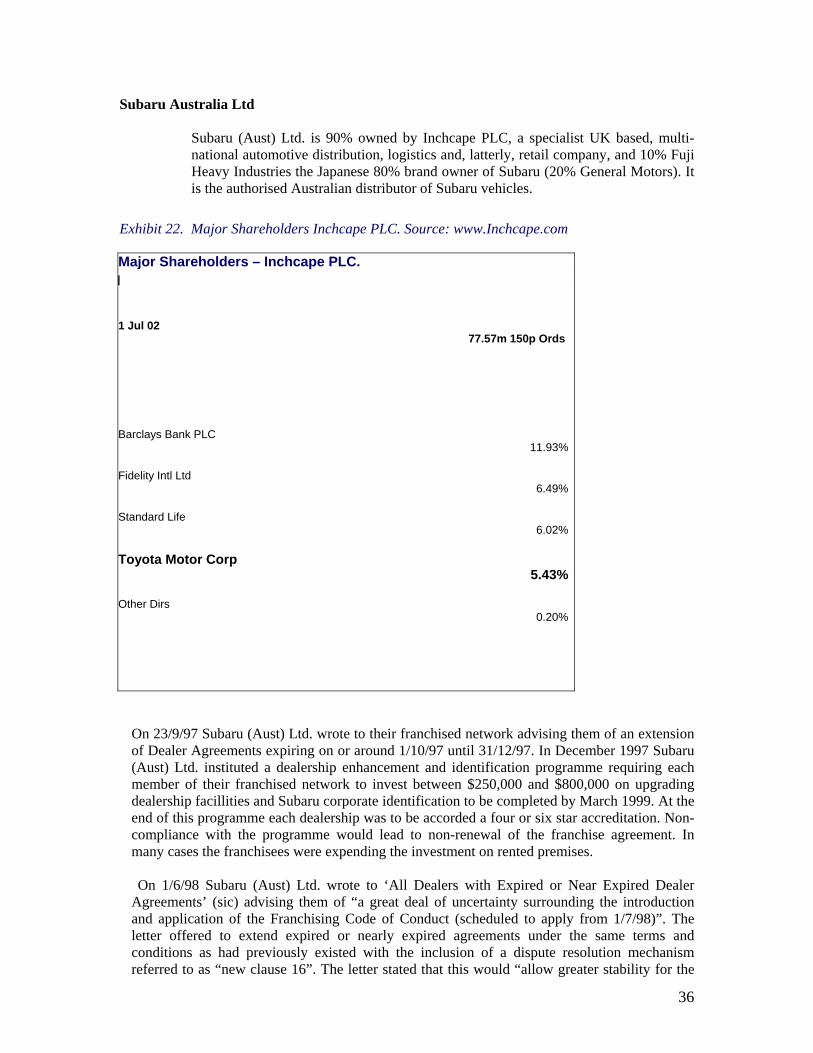

Subaru Australia Ltd

Subaru (Aust) Ltd. is 90% owned by Inchcape PLC, a specialist UK based, multi-national automotive distribution, logistics and, latterly, retail company, and 10% FujiHeavy Industries the Japanese 80% brand owner of Subaru (20% General Motors). Itis the authorised Australian distributor of Subaru vehicles.

Exhibit 22. Major Shareholders Inchcape PLC. Source: www.Inchcape.com

Major Shareholders – Inchcape PLC.

1 Jul 0277.57m 150p Ords

Barclays Bank PLC 11.93%

Fidelity Intl Ltd6.49%

Standard Life6.02%

Toyota Motor Corp5.43%

Other Dirs0.20%

On 23/9/97 Subaru (Aust) Ltd. wrote to their franchised network advising them of an extensionof Dealer Agreements expiring on or around 1/10/97 until 31/12/97. In December 1997 Subaru(Aust) Ltd. instituted a dealership enhancement and identification programme requiring eachmember of their franchised network to invest between $250,000 and $800,000 on upgradingdealership facillities and Subaru corporate identification to be completed by March 1999. At theend of this programme each dealership was to be accorded a four or six star accreditation. Non-compliance with the programme would lead to non-renewal of the franchise agreement. Inmany cases the franchisees were expending the investment on rented premises.

On 1/6/98 Subaru (Aust) Ltd. wrote to ‘All Dealers with Expired or Near Expired DealerAgreements’ (sic) advising them of “a great deal of uncertainty surrounding the introductionand application of the Franchising Code of Conduct (scheduled to apply from 1/7/98)”. Theletter offered to extend expired or nearly expired agreements under the same terms andconditions as had previously existed with the inclusion of a dispute resolution mechanismreferred to as “new clause 16”. The letter stated that this would “allow greater stability for the

37

introduction and management of the Subaru 6 Star Revitalisation Programme”. Franchiseeswere advised that the extension offer would lapse by 19/6/98 after which renegotiating a dealeragreement “may prove challenging”. The letter concluded with: “Should all reasonable attemptsto negotiate an immediate post-Code Dealer Agreement (sic) fail, we have been instructed byInchcape Motors Ltd to formalise the conclusion of our relationship.”

On 18/6/98 Subaru (Aust) P.L. wrote to all dealers with expired or near expired dealeragreements “clarifying” their letter of 1/6/98. They claimed that ‘due to the onerousrequirements’ of the franchising code that they, Subaru (Aust.) P.L. were still several monthsaway from the finalisation of their new dealer (franchise) agreements. They again reccomendedthe acceptance of the existing dealer agreement extension to 1/10/99 to “give Subaru Aust (sic)some breathing space to digest the requirements of the code and finalise the redesign of ourdealer agreement.” They further stated: “The renewal of the agreement will provide you withsome certainty that many of you have requested especially while undertaking improvementsto your facilities.” It is unlikely that other major franchisors or their franchisees lived with thisdegree of uncertainty.

On 26/6/98 Subaru (Aust) P.L. wrote to franchisees that had not formally agree to the non-negotiable, non-compliant with the Franchising Code of Conduct, proposed extension of theirDealer Agreements (to 1/10/99) extending the terms and conditions of the lapsed DealerAgreements until a new dealer agreement “is agreed”. This was the first of theircommunications to acknowledge copies to “Inchcape” and Minter Ellison, a firm of solicitors.In September 1999 Subaru Australia Ltd. submitted their new draft dealer agreement to theSubaru development board for approval / negotiation and on 24/3/2000 wrote to theirMelbourne franchisees with a new ‘final,’ take it or leave it, non-renewable franchiseagreement expiring on 1/1/2002 and informing them that Subaru Aust. (sic) would be takingover retail operations commencing mid 2001. Together with the new agreement was the offer ofa ‘consideration’ to offset business exit costs. This varied between $50,000 and $450,000 withthe most common offer being $150,000 and was conditional upon the franchisee granting arelease to all Subaru associated entities and their employees from any legal action. Theseamounts were, in some cases, subsequently negotiated upwards by $50,000 to an averagepayment of $165,000. Inchcape Automotive Australia P.L. had therefore taken monopolycontrol of the Melbourne market for Subaru sales, service and parts for a little over $1.1million.

In a ‘Dealer Bulletin to all Subaru Dealers & Staff’ of 27/3/2000 Subaru (Aust) P.L. advised thefranchise network of the terminations and their intention of “moving into the retail car marketin the Melbourne Metropolitan area”. The Bulletin went on to assuage ‘discomfort todealerships elsewhere’ as the initiative ‘relates only to the Melbourne metropolitan market.’ Itwas at about this time that the corporate entity known as Inchcape Automotive Australia P.L.was re-defined, which according to the Inchcape PLC annual report (2000) differs from Subaru(Aust) P.L. in two important respects:

o It is 100% owned by Inchcape PLCo It is concerned with retail operations as well as import and distribution

It is clear from Inchcape PLC.’s 1999 Annual report (Exhibits 23) that although the AustralianSubaru franchised network was vastly outperforming the market, Inchcape PLC. was intent onpursuing a global strategy of automotive concentration and forward integration into retail. Theyclearly prioritise regional clustering and regional market monopoly (their preferred andbelaboured euphenism is “exclusivity”). Their expenditure of 10.2million pounds sterling on

38

two Sydney retail groups delivered them (among other franchises) the monopoly retail positionfor Volkswagen products in Sydney.

Exhibit 23. Source Inchcape PLC Annual Report 1999

With the Subaru (Aust) P.L. inspired uncertainty over dealer agreement renewals fortheir franchisees it is probable that Inchcape saw a way of gaining another regionalmonopoly for a lot less than that of Volkswagen in Sydney. It is entirely possible this hadbeen their intention, even their strategic plan, for inspiring that uncertainty.

39

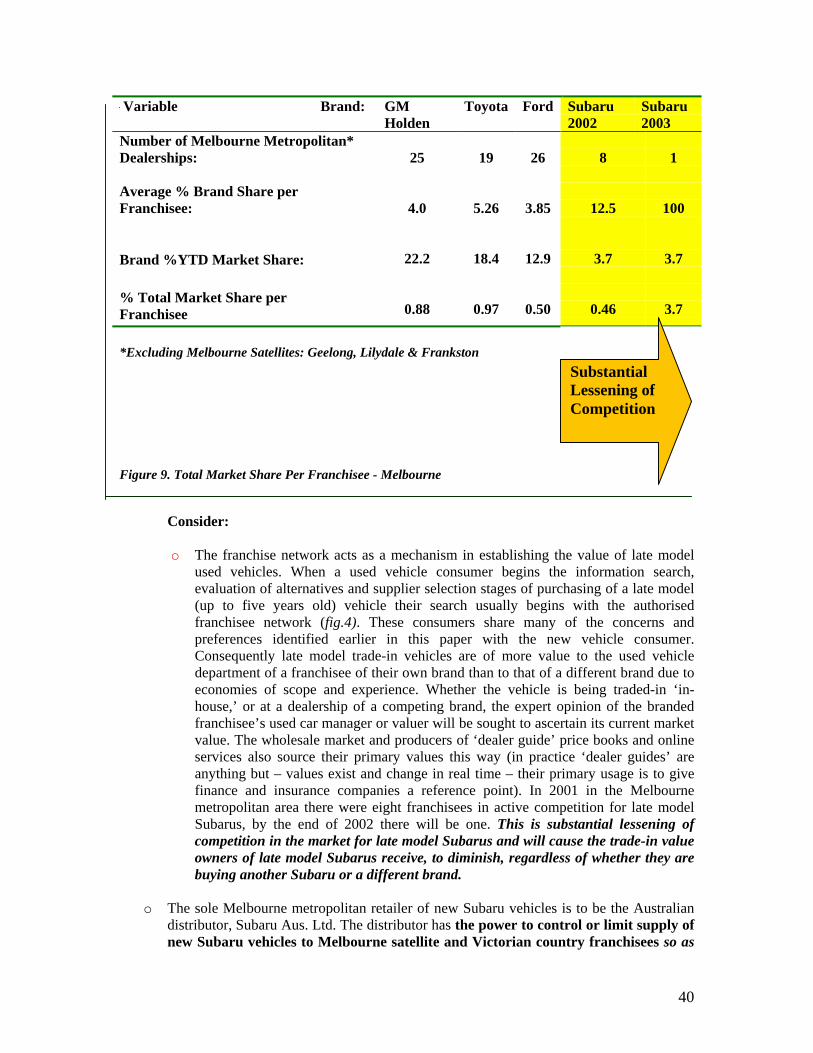

By 2003 Melbourne consumers will have had their Melbourne metropolitan choice of dealersreduced from eight vigorously competing independent businesses to one: Inchcape AutomotiveAustralia P.L. – 100% owned by Inchcape PLC. A distributor owned, regional monopolyconsisting of a centralised ‘experience’ centre, four sales and service satellite outlets and twosatellite service only outlets. In addition to concentrating the Melbourne market for new Subaruvehicles to a CR1 of 100% (ie monopoly) it delivers an average total market share perfranchisee of 3.7% - nearly four times that of the next highest (Toyota), seven times that ofFord and over four times that of the market leader (GM Holden) (Fig.9).

This market restructure alone would appear to be a prima facie breach of s45 & possibly s50 ofThe Trade Practices Act 1974 - but there are other real market effects, little understood outsideof the automotive industry (particularly by legislators and regulators), that have the potential,even likelihood, of breaching most sections of The Act.

40

Variable Brand: GMHolden

Toyota Ford Subaru2002

Subaru2003

Number of Melbourne Metropolitan*Dealerships:

Average % Brand Share perFranchisee:

Brand %YTD Market Share:

% Total Market Share perFranchisee

25

4.0

22.2

0.88

19

5.26

18.4

0.97

26

3.85

12.9

0.50

8

12.5

3.7

0.46

1

100

3.7

3.7

*Excluding Melbourne Satellites: Geelong, Lilydale & Frankston

Figure 9. Total Market Share Per Franchisee - Melbourne

Consider:

o The franchise network acts as a mechanism in establishing the value of late modelused vehicles. When a used vehicle consumer begins the information search,evaluation of alternatives and supplier selection stages of purchasing of a late model(up to five years old) vehicle their search usually begins with the authorisedfranchisee network (fig.4). These consumers share many of the concerns andpreferences identified earlier in this paper with the new vehicle consumer.Consequently late model trade-in vehicles are of more value to the used vehicledepartment of a franchisee of their own brand than to that of a different brand due toeconomies of scope and experience. Whether the vehicle is being traded-in ‘in-house,’ or at a dealership of a competing brand, the expert opinion of the brandedfranchisee’s used car manager or valuer will be sought to ascertain its current marketvalue. The wholesale market and producers of ‘dealer guide’ price books and onlineservices also source their primary values this way (in practice ‘dealer guides’ areanything but – values exist and change in real time – their primary usage is to givefinance and insurance companies a reference point). In 2001 in the Melbournemetropolitan area there were eight franchisees in active competition for late modelSubarus, by the end of 2002 there will be one. This is substantial lessening ofcompetition in the market for late model Subarus and will cause the trade-in valueowners of late model Subarus receive, to diminish, regardless of whether they arebuying another Subaru or a different brand.

o The sole Melbourne metropolitan retailer of new Subaru vehicles is to be the Australiandistributor, Subaru Aus. Ltd. The distributor has the power to control or limit supply ofnew Subaru vehicles to Melbourne satellite and Victorian country franchisees so as

SubstantialLessening ofCompetition

41