the special data dissemination standard plus - imf · the special data dissemination standard plus...

TRANSCRIPT

5293924v7

INTERNATIONAL MONETARY FUND

The Special Data

Dissemination Standard Plus

Guide for Adherents and Users

December 2015

ii

Contents

Preface iv

Acknowledgments v

Abbreviations vi

1. The Special Data Dissemination Standard Plus: Origin and Key Features ................ 1

2. Real Sector: Data Coverage, Periodicity, and Timeliness .......................................... 11

3. Fiscal Sector: Data Coverage, Periodicity, and Timeliness ....................................... 14

4. Financial Sector: Data Coverage, Periodicity, and Timeliness .................................. 21

5. External Sector: Data Coverage, Periodicity, and Timeliness ................................... 28

iii

Boxes

Tables

iv

Preface

SDDS Plus Guide

5293924v7

Acknowledgments

ii

Abbreviations

iii

5293924v7

Chapter 1

The Special Data Dissemination Standard

Plus: Origin and Key Features

Origin and Purpose

2

Box 1.1 Establishment of the SDDS Plus and the SDDS Plus Guide

The Special Data Dissemination Standard Plus (SDDS Plus) was approved by the IMF’s Executive Board during the

eighth review of the IMF’s Data Standards Initiatives in February 2012. Based on this review, a legal text describing the

requirements for SDDS Plus was prepared and approved by the Board in October 2012, and subsequently amended in

March 2014 to reflect: (i) the extension of the timeliness for three data categories (sectoral accounts, other financial

corporations survey, and debt securities) from one-quarter to 4 months; and (ii) updated methodologies under the Basel

Accords for the financial soundness indicators data category. (The revised legal text is available on the Internet at

http://www.imf.org/external/np/pp/eng/2014/031914a.pdf.)

This SDDS Plus Guide was first prepared by IMF staff, based on the understandings detailed in the SDDS Plus legal

text of October 2012, and is revised to reflect amendments approved by the Executive Board and elaboration of a few

aspects of the initiative to clarify requirements. Any future changes or enhancements to the SDDS Plus initiative,

including data coverage, periodicity, and timeliness, could only take place after discussion by the IMF’s Executive

Board and the approval of a revised legal text reflecting these changes. The legal text includes references to the

recommended methodologies based on the latest editions of manuals and guides for the nine SDDS Plus data

categories. The reference to a successor methodology is included to further encourage adherents to adopt the

successor methodology as it becomes available. It also allows countries that decide to adopt these successor

methodologies to report data, with comparable detail, using the new methodology.

The IMF’s Executive Board reviews the IMF’s Data Standards Initiatives periodically.

1 The SDDS requirements are detailed in the Special Data Dissemination Standard: Guide for Subscribers

and Users (SDDS Guide), available at http://dsbb.imf.org/Pages/SDDS/Home.aspx, which should be referred to

when using this guide.

3

4

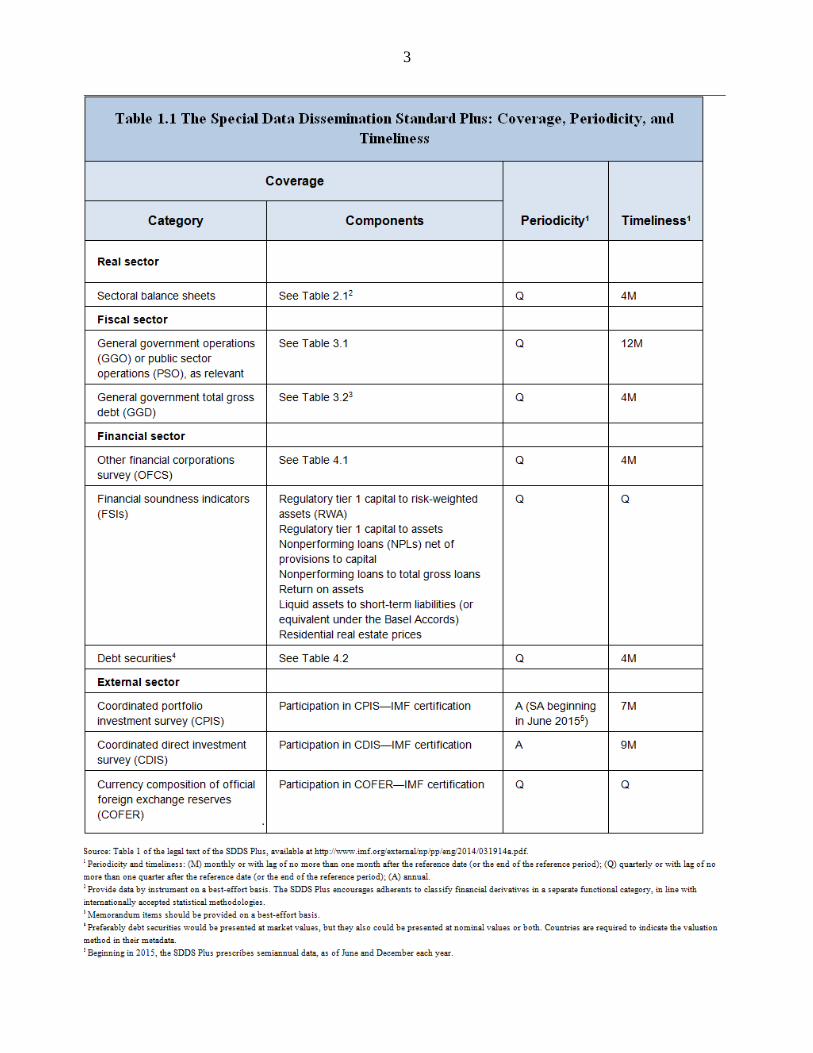

Key Aspects of Dissemination

2 For information on the prescribed SDDS data categories and the coverage, periodicity, and timeliness

requirements related to these data categories, see the SDDS Guide.

5

Box 1.2 The Dimensions and Monitorable Elements of the SDDS Plus

Data Coverage, Periodicity, and Timeliness: Comprehensive economic and financial data disseminated on a timely

basis are essential to the transparency of macroeconomic performance and policy analysis. Countries adhering to the

Special Data Dissemination Standard Plus (SDDS Plus) are obliged to disseminate the prescribed categories of data

with the specified coverage, periodicity, and timeliness.

Access by the Public: Dissemination of official statistics is an essential feature of statistics as a public good. The

SDDS Plus calls for providing the public, including market participants, ready and equal access to the data. Countries

adhering to the SDDS Plus are obliged to disseminate advance release calendars (ARCs) for the data except for

coordinated portfolio investment survey (CPIS), coordinated direct investment survey (CDIS), and currency composition

of official foreign exchange reserves (COFER) data; and release the data, except CPIS, CDIS, and COFER data, to all

interested parties simultaneously. There are no ARC dates associated with CPIS, CDIS, and COFER data. The SDDS

Plus only calls for reporting to the International Monetary Fund (IMF) within the specified timeliness for these three

categories, along with redissemination on the National Summary Data Page (NSDP) for only CPIS and CDIS (not

COFER). The time of dissemination could be at the same time as the reporting to the IMF or immediately after the CPIS

and CDIS data are disseminated by the IMF on the CPIS and CDIS websites maintained by the IMF. If adherents

decide to disseminate these data immediately after the data are disseminated by the IMF, they can either redisseminate

the data on the NSDP or provide a hyperlink on the NSDP to the CPIS and CDIS websites maintained by the IMF.

Integrity: To fulfill the purpose of providing the public with information, official statistics must have the confidence of

their users. In turn, confidence in the statistics ultimately becomes a matter of confidence in the objectivity and

professionalism of the agency producing the statistics. Transparency of practices and procedures is a key factor in

creating this confidence. Countries adhering to the SDDS Plus are obliged to (1) disseminate the terms and conditions

under which official statistics are produced, including those relating to the confidentiality of individually identifiable

information; (2) identify internal government access to data before release to the public; (3) identify ministerial

commentary on the occasion of statistical releases; and (4) provide information about revisions and advance notice of

major changes in methodology.

Quality: A set of standards that deals with the coverage, periodicity, and timeliness of data must also address the

quality of statistics. Although quality is difficult to judge, monitorable proxies, designed to focus on information the user

needs to judge quality, can be useful. Countries adhering to the SDDS Plus are obliged to (1) disseminate

documentation on methodology and sources used in preparing statistics, including the identification of methodological

deviations from internationally accepted statistical methodologies; (2) encouraging data modules of the Reports on the

Observance of Standards and Codes (Data ROSCs) or other quality assessments every 7–10 years; and (3)

disseminate component detail, reconciliations with related data, and statistical frameworks that support statistical cross-

checks and provide assurance of reasonableness.

6

3 Establishing a revision policy and publishing revisions in a transparent manner, as well as engaging in open

communication with data users, are recommended. The objective of revision policies is to disseminate to the

public data of better quality as it becomes available. For instance, quarterly data can be revised due to the

increase in the number of reporting entities or as a result of quality checks performed after the data have been

disseminated. A typical example of the latter is the benchmarking of quarterly data to annual data when the

annual data become available. Compilers are encouraged to develop integrated revision policies that explain

clearly how more frequent data can be revised as a result of the publication of less frequent data.

7

—

Adherence to the SDDS Plus

4 The communication should be addressed to the Director of the Statistics Department, International Monetary

Fund, 700 19th Street, N.W., Washington, DC 20431, USA; faxed to (202) 623-6165 or (202) 623-6460; or e-

mailed to [email protected].

8

The Dissemination Standards Bulletin Board

Commitment to Observance

5 The guidelines for establishing the NSDP for SDDS Plus adherents differ from the guidelines for SDDS

subscribers and include the dissemination of data in the formats of the Statistical Data and Metadata eXchange

(SDMX) standards. Reliance on SDMX standards is expected to reduce observance costs by SDDS Plus

adherents and monitoring costs for the IMF.

6 Adherents are required to observe guidelines set by the IMF, in consultation with adherents, for automating

the monitoring process. This includes, but is not limited to, observing formatting guidelines for NSDPs that

(continued)

9

Monitoring Observance

Removal from the DSBB

permit electronic scanning, using online procedures for reporting ARCs, and metadata updates and periodic

certification of the accuracy of those metadata. These guidelines and procedures may evolve as technology

changes.

7 An alternate coordinator may also be appointed. The appointment of an SDDS Plus coordinator is important

because for most adhering countries observance of the SDDS Plus and the provision of information to the IMF

involve at least three agencies: the central bank, the ministry of finance, and the national statistical office.

8 Monitoring is carried out by the staff of the IMF’s Statistics Department.

11

Chapter 2

Real Sector: Data Coverage, Periodicity,

and Timeliness

Sectoral Balance Sheets: Coverage

12

Periodicity and Timeliness

9 The Templates for Minimum and Encouraged Set of Internationally Comparable Sectoral Accounts and

Balance Sheets under the G-20/IMFC Data Gaps Initiative are available at

www.imf.org/external/np/sta/templates/sectacct/index.htm.

1

3

14

Chapter 3

Fiscal Sector: Data Coverage, Periodicity,

and Timeliness

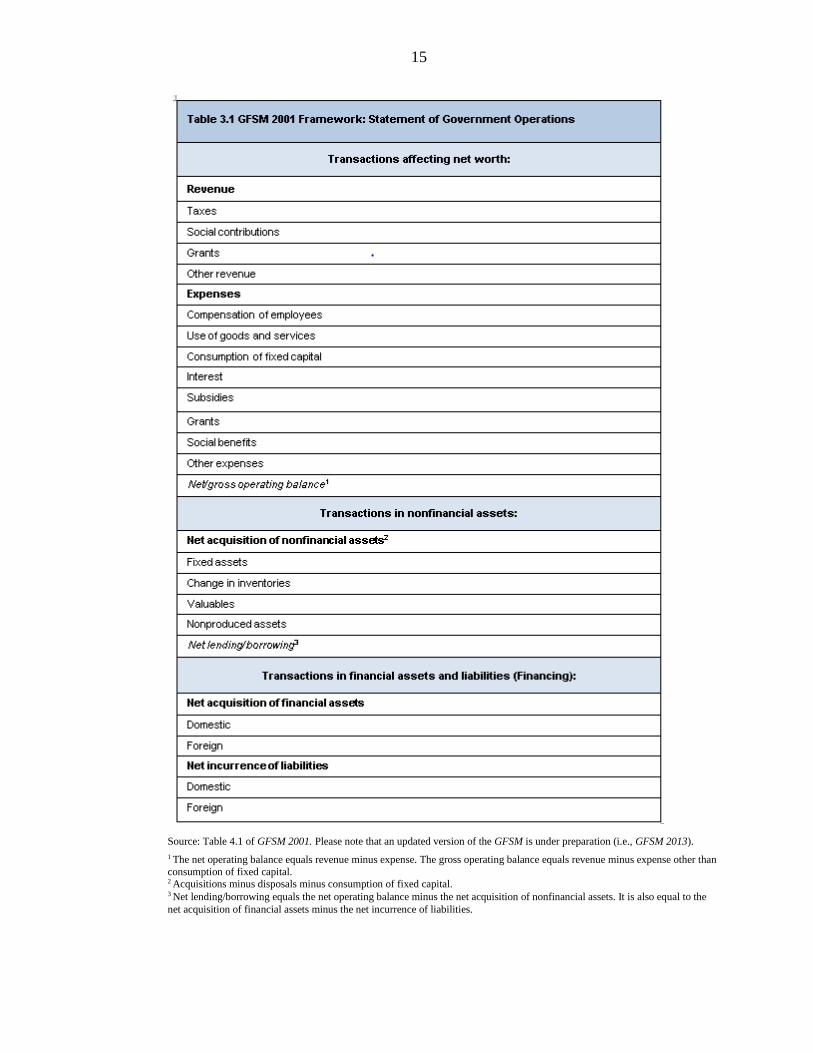

General Government Operations: Coverage

15

Source: Table 4.1 of GFSM 2001. Please note that an updated version of the GFSM is under preparation (i.e., GFSM 2013).

1 The net operating balance equals revenue minus expense. The gross operating balance equals revenue minus expense other than

consumption of fixed capital. 2 Acquisitions minus disposals minus consumption of fixed capital. 3 Net lending/borrowing equals the net operating balance minus the net acquisition of nonfinancial assets. It is also equal to the

net acquisition of financial assets minus the net incurrence of liabilities.

16

Periodicity and Timeliness

10 Any missing components can be estimated through various approaches to meet the minimum requirements

(see paragraph 3.4).

17

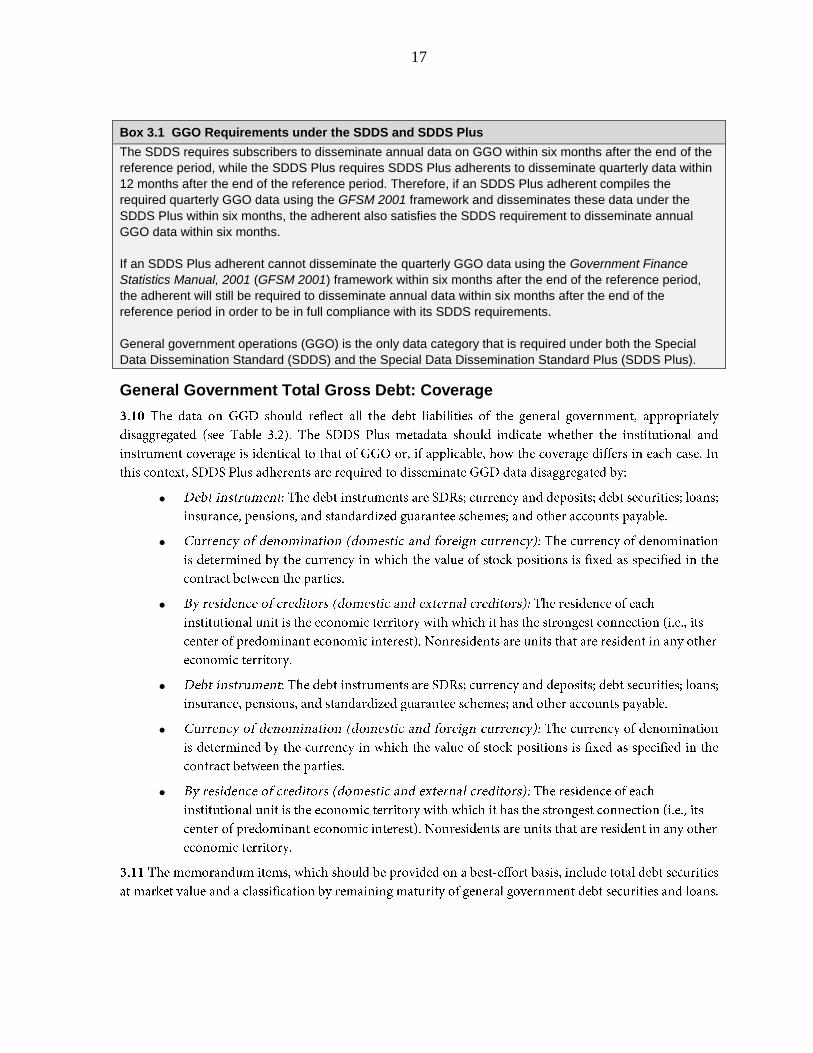

Box 3.1 GGO Requirements under the SDDS and SDDS Plus

The SDDS requires subscribers to disseminate annual data on GGO within six months after the end of the

reference period, while the SDDS Plus requires SDDS Plus adherents to disseminate quarterly data within

12 months after the end of the reference period. Therefore, if an SDDS Plus adherent compiles the

required quarterly GGO data using the GFSM 2001 framework and disseminates these data under the

SDDS Plus within six months, the adherent also satisfies the SDDS requirement to disseminate annual

GGO data within six months.

If an SDDS Plus adherent cannot disseminate the quarterly GGO data using the Government Finance

Statistics Manual, 2001 (GFSM 2001) framework within six months after the end of the reference period,

the adherent will still be required to disseminate annual data within six months after the end of the

reference period in order to be in full compliance with its SDDS requirements.

General government operations (GGO) is the only data category that is required under both the Special

Data Dissemination Standard (SDDS) and the Special Data Dissemination Standard Plus (SDDS Plus).

General Government Total Gross Debt: Coverage

18

Box 3.2 Treatment of Non-autonomous Unfunded Government Employee Pension Schemes in the General Government Total Gross Debt and Sectoral Balance Sheets Data Categories

SDDS Plus adherents are encouraged, but not required, to adopt the latest internationally accepted

methodologies in their compilation practices (paragraph 1.9). Under the encouraged international

guidelines for general government total gross debt (GGD) indicated in paragraph 3.12, pension

entitlements including non-autonomous unfunded government employee pension schemes (NUGEPS), are

an integral part of GGD to be reported (See the Public Sector Debt Statistics Guide paragraphs 4.133 and

Box 4.18). The 2008 SNA allows flexibility with regard to the inclusion of NUGEPS (in part or in total) in the

sectoral accounts data (see 2008 SNA, 17.193, and Table 17.10).

Against this background, SDDS Plus adherents are required to state in the metadata whether NUGEPS

(whether funded/underfunded or unfunded) exist and, if so, whether the liabilities for these schemes have

consistently been included under the data categories for GGD and the sectoral balance sheets. If not

included, SDDS Plus adherents are strongly encouraged to disclose these data on a best effort basis, for

instance, by providing supplementary information as recommended by the 2008 SNA. The encouraged

disclosure of information on NUGEPS with the required metadata should be sufficient to allow users to

understand and compare data categories for the adherent as well as to allow international comparisons

across adherents. The importance of disseminating comparable data across adherents through common

international standards as far as is feasible was a conclusion from the 2013 FSB/IMF Global Conference

on the G20 Data Gaps Initiative.

11 The TFFS includes representatives from the Bank for International Settlements (BIS), Commonwealth

Secretariat, European Central Bank (ECB), Eurostat, IMF (chair), Organization for Economic Cooperation and

Development (OECD), Paris Club, United Nations Conference on Trade and Development (UNCTAD), and

World Bank.

12 Available at http://databank.worldbank.org/ddp/home.do?Step=12&id=4&CNO=3009.

19

Table 3.2 General Government Total Gross Debt in Nominal Values

Total gross debt

By type of instrument

SDRs

Currency and deposits

Debt securities

Loans

Insurance, pensions, and standardized guarantee schemes1

Other accounts payable

By currency of denomination

Domestic currency

Foreign currency

By residence of the creditor

Domestic creditors

External creditors

Memorandum items:2

Debt securities at market value

Payable within one year or less (residual maturity)

Debt securities

Loans

Payable in more than one year (residual maturity)

Debt securities

Loans

20

Box 3.3 Treatment of Other Accounts Payable in General Government Total Gross Debt and Sectoral Balance Sheets Data

A driving principle underlying the SDDS Plus is the encouragement of the use of internationally accepted

methodologies for all data categories. For the fiscal sector, this primarily involves the Government Finance

Statistics Manual 2001 (GFSM 2001) and the Public Sector Debt Statistics Guide 2011 (PSDSG), GFSM

2001 and the PSDSG define general government total gross debt (GGD) by type of instrument (i.e.,

Special Drawing Rights, currency and deposits, debt securities, loans, insurance, pensions, and

standardized guarantee schemes, and other accounts payable).

If adherents present government debt excluding other accounts payable under the GGD data category,

they must (i) clearly indicate in the metadata that other accounts payable are excluded from GGD; (ii)

clearly indicate in the electronic data files (SDMX) that the total figure presented for general government

total gross debt does not include other accounts payable; and (iii) on the authorities’ webpage where GGD

data is to be disseminated, include a footnote stating that the total figure for GGD does not include other

accounts payable; and provide a hyperlink to the data on other accounts payable for the general

government sector in the sectoral balance sheets.

Periodicity and Timeliness

21

Chapter 4

Financial Sector: Data Coverage,

Periodicity, and Timeliness

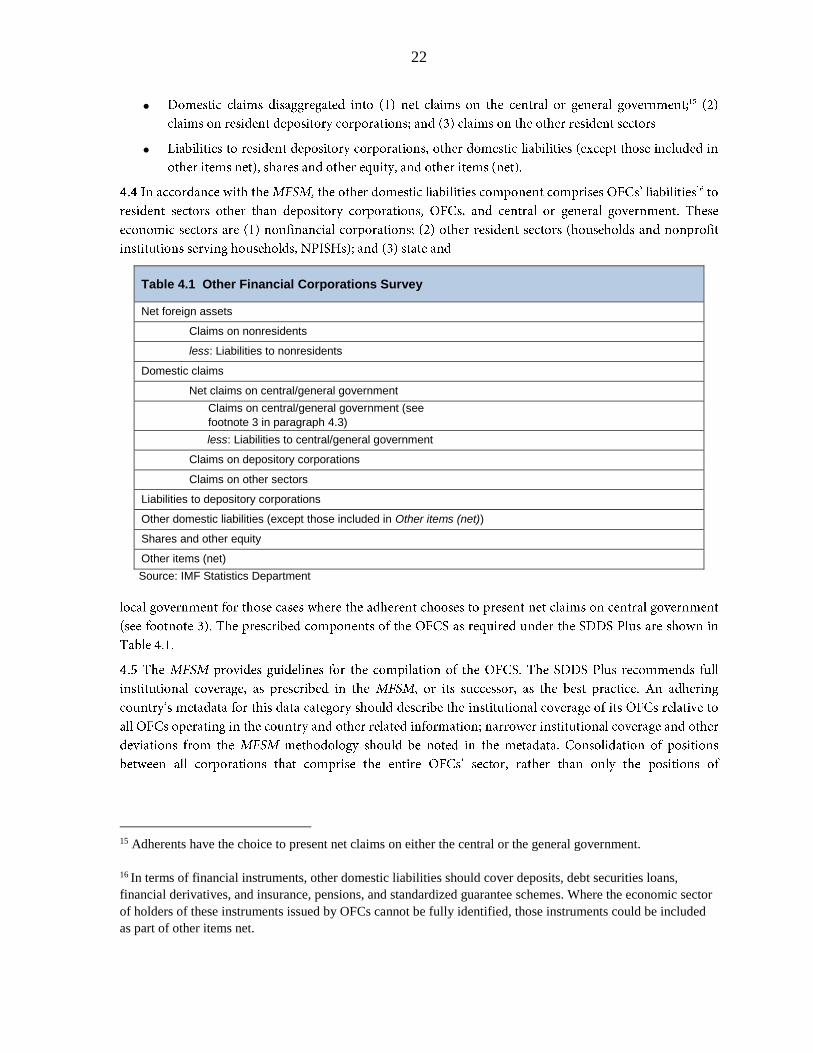

Other Financial Corporations Survey: Coverage

13 Liabilities to nonresidents exclude equity holdings of nonresidents, which are shown under “Shares and other

equity.”

14 The concept of residency distinguishes between foreign and domestic assets/liabilities. Where the residency

of holders of securities issued by OFCs cannot be fully identified in the computation of liabilities to

nonresidents, net foreign assets can be defined as “total claims on nonresidents minus total liabilities to

nonresidents for which a residency allocation is possible.”

22

Source: IMF Statistics Department

15 Adherents have the choice to present net claims on either the central or the general government.

16 In terms of financial instruments, other domestic liabilities should cover deposits, debt securities loans,

financial derivatives, and insurance, pensions, and standardized guarantee schemes. Where the economic sector

of holders of these instruments issued by OFCs cannot be fully identified, those instruments could be included

as part of other items net.

Table 4.1 Other Financial Corporations Survey

Net foreign assets

Claims on nonresidents

less: Liabilities to nonresidents

Domestic claims

Net claims on central/general government

Claims on central/general government (see

footnote 3 in paragraph 4.3)

less: Liabilities to central/general government

Claims on depository corporations

Claims on other sectors

Liabilities to depository corporations

Other domestic liabilities (except those included in Other items (net))

Shares and other equity

Other items (net)

23

Periodicity and Timeliness

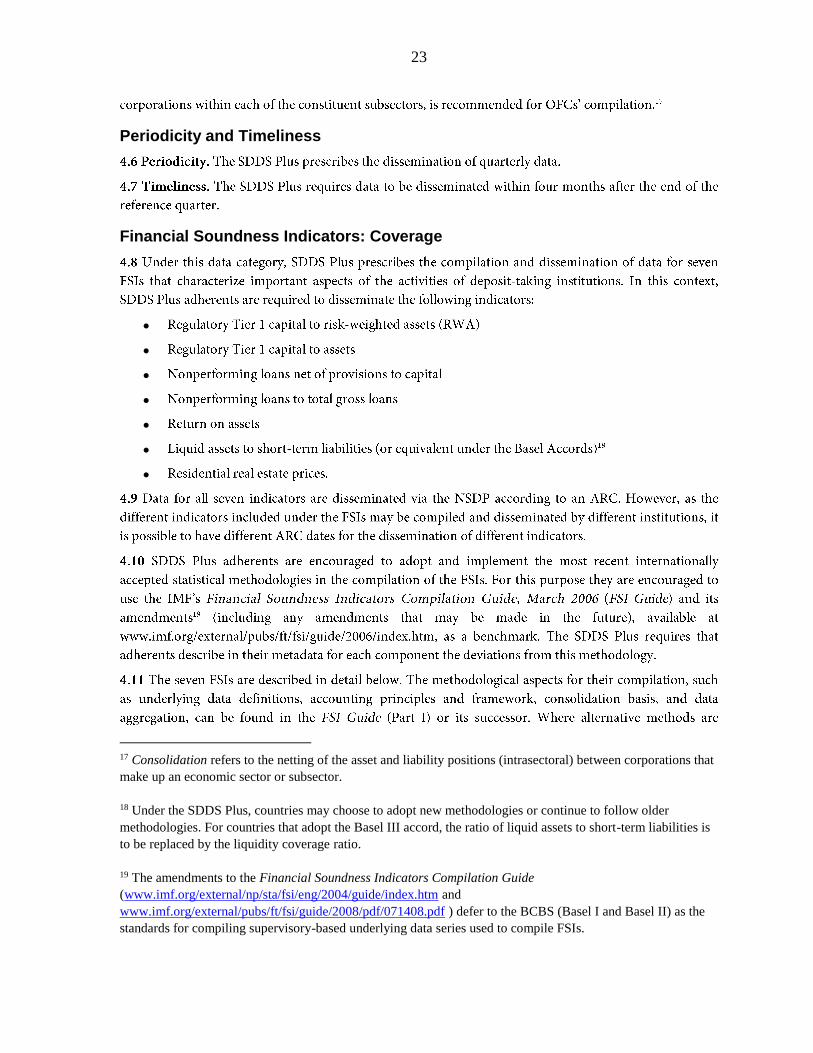

Financial Soundness Indicators: Coverage

17 Consolidation refers to the netting of the asset and liability positions (intrasectoral) between corporations that

make up an economic sector or subsector.

18 Under the SDDS Plus, countries may choose to adopt new methodologies or continue to follow older

methodologies. For countries that adopt the Basel III accord, the ratio of liquid assets to short-term liabilities is

to be replaced by the liquidity coverage ratio.

19 The amendments to the Financial Soundness Indicators Compilation Guide

(www.imf.org/external/np/sta/fsi/eng/2004/guide/index.htm and

www.imf.org/external/pubs/ft/fsi/guide/2008/pdf/071408.pdf ) defer to the BCBS (Basel I and Basel II) as the

standards for compiling supervisory-based underlying data series used to compile FSIs.

24

25

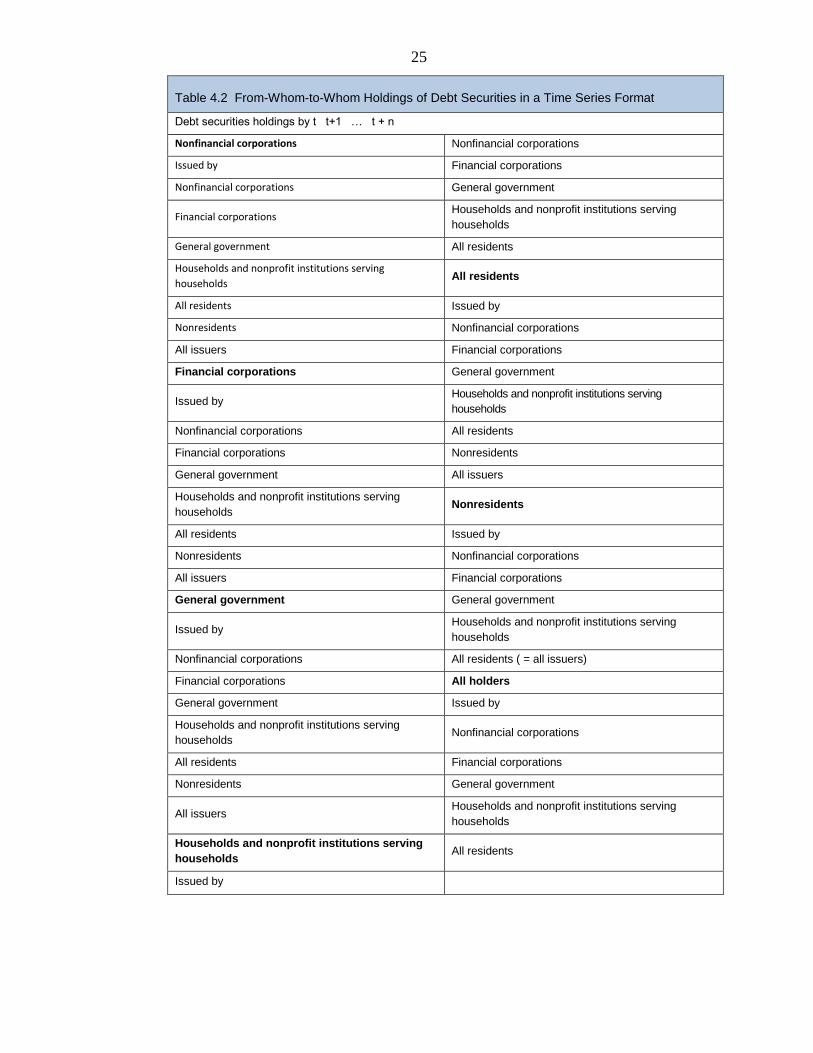

Table 4.2 From-Whom-to-Whom Holdings of Debt Securities in a Time Series Format

Debt securities holdings by t t+1 … t + n

Nonfinancial corporations Nonfinancial corporations

Issued by Financial corporations

Nonfinancial corporations General government

Financial corporations Households and nonprofit institutions serving

households

General government All residents

Households and nonprofit institutions serving

households All residents

All residents Issued by

Nonresidents Nonfinancial corporations

All issuers Financial corporations

Financial corporations General government

Issued by Households and nonprofit institutions serving

households

Nonfinancial corporations All residents

Financial corporations Nonresidents

General government All issuers

Households and nonprofit institutions serving

households Nonresidents

All residents Issued by

Nonresidents Nonfinancial corporations

All issuers Financial corporations

General government General government

Issued by Households and nonprofit institutions serving

households

Nonfinancial corporations All residents ( = all issuers)

Financial corporations All holders

General government Issued by

Households and nonprofit institutions serving

households Nonfinancial corporations

All residents Financial corporations

Nonresidents General government

All issuers Households and nonprofit institutions serving

households

Households and nonprofit institutions serving

households All residents

Issued by

26

Periodicity and Timeliness

Debt Securities: Coverage

20See footnote 19.

21 Please see

http://epp.eurostat.ec.europa.eu/portal/page/portal/hicp/methodology/owner_occupied_housing_hpi/rppi_handb

ook.

23Table 4.2 is based on the Handbook on Securities Statistics (the Handbook) Part 2, restated in terms of stocks.

23 The details of each institutional unit that constitutes these sectors are provided in Section 3 of the Handbook

Part 1 and Section 2 of the Handbook Part 2. The residence of an institutional unit is the economic territory with

which it has the strongest connection (i.e., its center of predominant economic interest).

27

Periodicity and Timeliness

24 Part 1: www.imf.org/external/np/sta/wgsd/pdf/051309.pdf; Part 2:

www.imf.org/external/np/sta/wgsd/pdf/090710.pdf.

25 See the Handbook Part 1, Section 4 for a detailed explanation of securitization.

28

Chapter 5

External Sector: Data Coverage,

Periodicity, and Timeliness

Coordinated Portfolio Investment Survey: Coverage

Periodicity and Timeliness

Source: IMF Statistics Department

29

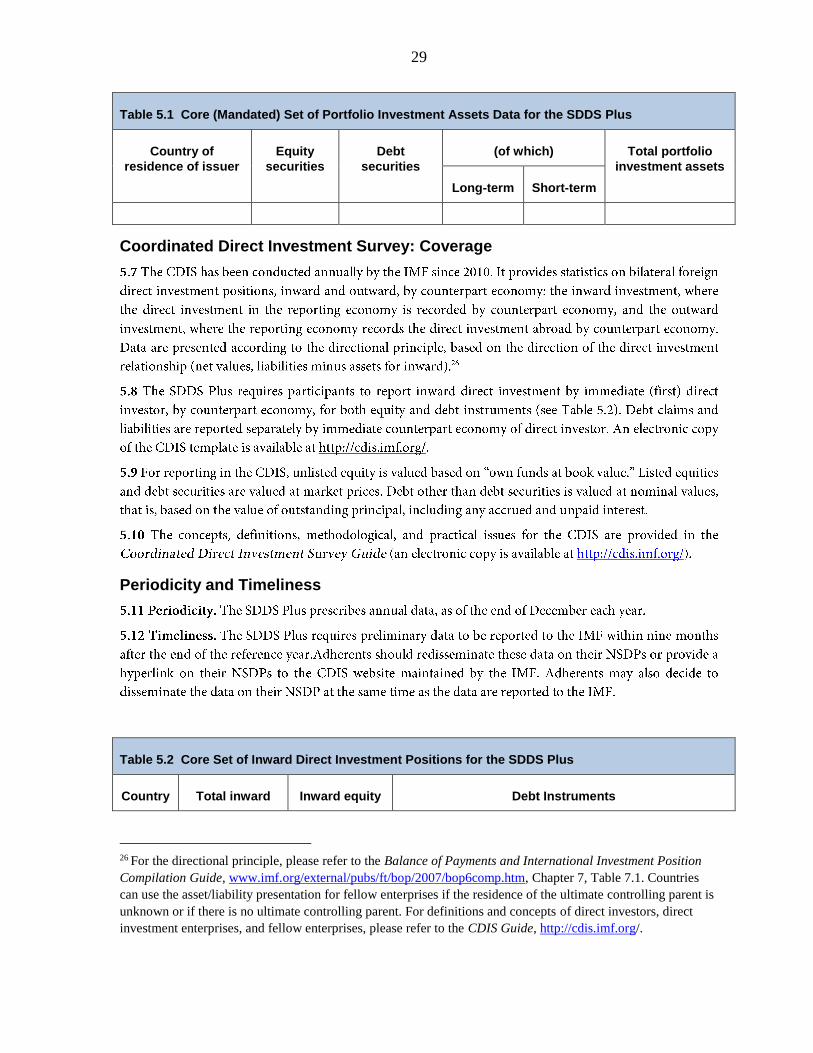

Coordinated Direct Investment Survey: Coverage

Periodicity and Timeliness

26 For the directional principle, please refer to the Balance of Payments and International Investment Position

Compilation Guide, www.imf.org/external/pubs/ft/bop/2007/bop6comp.htm, Chapter 7, Table 7.1. Countries

can use the asset/liability presentation for fellow enterprises if the residence of the ultimate controlling parent is

unknown or if there is no ultimate controlling parent. For definitions and concepts of direct investors, direct

investment enterprises, and fellow enterprises, please refer to the CDIS Guide, http://cdis.imf.org/.

Table 5.1 Core (Mandated) Set of Portfolio Investment Assets Data for the SDDS Plus

Country of

residence of issuer

Equity

securities

Debt

securities

(of which) Total portfolio

investment assets

Long-term Short-term

Table 5.2 Core Set of Inward Direct Investment Positions for the SDDS Plus

Country Total inward Inward equity Debt Instruments

30

Source: IMF Statistics Department.

Note: Gross debt liabilities and gross debt assets must be shown separately

Currency Composition of Official Foreign Exchange Reserves: Coverage

27 See BPM6, Chapter 6, Section F.

direct

investment

positions

positions (Net) Inward debt positions

(Net; liabilities minus

assets)

Gross debt positions

Debt

liabilities

Debt assets

31

Source: IMF Statistics Department

Periodicity and Timeliness

Table 5.3 Currency Composition of Official Foreign Exchange Reserves

Information to be provided by monetary authorities

Total foreign exchange reserves

Of which claims in U.S. dollar

Of which claims in euro

Of which claims in pound sterling

Of which claims in Japanese yen

Of which claims in Swiss franc

Of which claims in Australian dollar

Of which claims in Canadian dollar

Of which claims in other currencies