the state of food and agriculture, 1986 · the state of food and agriculture in 1986 gives rise to...

TRANSCRIPT

Worm oan regional reviews, , ,

*nancing agricultural development

r I

I " I 1

' 1

r, r

1

r

o 9 1 FlOODIAINIJDI AGR*ULTURE ÒIZGANIZIATIÓN ÓF THE UNITED NATIOIN'.<., i

1

1 r 1

1 /-1 r e t'..`1.r

rr

r

r

r

r

rr

r

i

Special Chapters

In addition to the usual review of the recent world food and agriculturesituation, each issue of this report from 1957 has included one or more specialstudies of problems of longer-term interest. Special chapters in earlier issueshave covered the following subjects:

1957Factors influencing the trend of food consump-tionPostwar changes in some institut onal factorsaffecting agriculture

1958Food and agricultural developments in Africasouth of the SaharaThe growth of forest industries and their impacton the world's forests

1959Agricultural incomes and levels of living in

countries at different stages of economic devel-opmentSome general problems of agricultural develop-ment in less-developed countries in the light ofpostwar experience

1960Progra ming for agricultural development

1961Land reform and institutional changeAgricultural extension, education and researchin Africa, Asia and Latin America

1962The role of forest industries in the attack oneconomic underdevelopmentThe livestock industry in less developed coun-tries

1963Basic factors affecting the growth of produc-tivity in agricultureFertilizer use: spearhead of agricultural develop-ment

1964Protein nutrition: needs and prospectsSynthetics and their effects on agricultural trade

1966Agriculture and industrializationRice in the world food economy

1967Incentives and disincentives for farmers indeveloping countriesThe management of fishery resources

1968Raising agricultural productivity in developingcountries through technological improvementImproved storage and its contribution to worldfood supplies

1969Agricultural marketing improvement program-mes: some lessons from recent experienceModernizing of institutions to promote forestrydevelopment

1970Agriculture at the threshold of the SecondDevelopment Decade

1971

Water pollution and its effects on living aquaticresources and fisheries

1972Education and tra ning for developmentAccelerating agricultural research in thedeveloping countries

1973Agricultural employment in developing coun-tries

1974Population, "food supply and agricultural devel-opment

1975The Second United Nations DevelopmentDecade: mid-term review and appraisal

1976Energy and agriculture

1977The state of natural resources and the humanenvironment for food and agriculture

1978Problems and strategies in developing regions

1979Forestry and rural development

1980Marine fisheries in the new era of nationaljurisdiction

1981

Rural poverty in developing countries andmeans of poverty alleviation

1982Livestock production: a world perspective

1983Women in developing agriculture

1984Urbanization, agriculture and food systems

1985Energy use in agricultural productionEnvironmental trends in food and agricultureAgricultural marketing and development

THE STATE OF FOOD AND AGRICULTURE 1986

FAO Agriculture Series No. 20

-

FOOD AND AGRICULTURE ORGANIZATION OF THE UNITED NATIONSRome, 1987

The statistical material in this publication hasbeen prepared from the information available toFAO up to March 1987.

The designations employed and thepresentation of the material in this publicationdo not imply the expression of any opinionwhatsoever on the part of the Food andAgriculture Organization of the United Nationsconcerning the legal status of any country,territory, city or area, or of its authorities, orconcerning the delimitation of its frontiers orboundaries. In some tables, the designations"developed" and "developing" economies areintended for statistical convenience and do notnecessarily express a judgement about thestage reached by a particular country or areain the development process.

Chapter III, Financing Agricultural Development,was prepared by the Policy Analysis Division incollaboration with the Agricultural ServicesDivision, FAO, and was based on the work of DaleW. Adams, D. Diakosavvas, R. Roberts, J. Sharpleyand M. Spinedi, consultants.

David Lubin Memorial Library Cataloguing inPublication Data

FAO, Rome (Italy)The state of food and agriculture 1986.(FAO Agriculture Series, no. 20)

1. Agriculture. 2. Food production. 3. Trade.

I. Title II. Series

FAO code: 70 AGRIS: E16 E70 1987ISBN 92-5-102595-9ISSN 0081-4539

ISBN 92-5-102595-9ISSN 0081-4539© FAO 1987

Printed in Italy

Foreword

In hindsight, 1986 could be regarded as agenerally favourable year for agriculturalproduction, but also as a year tarnished byuncertainties in the overall economicenvironment and increasing problems in thearea of food and agricultural trade.

It was a year of solid agriculturalachievement in many developing countries,where a single good or bad crop year canmake the difference between starvation orsurvival for millions of human beings. This wasnotably the case in Africa, where the recoveryfrom the recent drought was widely sustainedand contributed to the alleviation of the foodsupply situation in many countries. Even moresignificant in a global perspective, given thelarge populations involved, several Asiancountries further improved their record ofrecent performances in food supply.

Welcome as these achievements were, theyshould not conceal the fragility of the currentworld economic and agricultural situation.Despite overall slow but steady long-termprogress in global nutritional status, hunger andmalnutrition still affect hundreds of millions ofpeople. The long-term guarantee of adequateaccess to food is contingent upon sustainedeconomic growth and a more equitabledistribution of its benefits.

The continuing lethargy of the worldeconomy and its pervasive negative effects onglobal demand, and policies toward trade andinternational cooperation, remained a matter ofprofound concern in 1986. For reasons largelybeyond their control, many developingcountries saw their chances recede fromreturning to strong economic growth. The fall in

their export earnings was further aggravated bya resurgence of protectionism in the industrialcountries. Yet, in order to honour their debtobligations, many of these developing countrieswere pressed to generate trade surpluses at anycost. The trade situation offered them littleoption but to reduce imports, investment, andeven subsistence consumption levels, thusprotracting a situation of economic and socialregression. The circumstances of severa! LatinAmerican and Caribbean countries, which wereforced into recessive adjustments, should berecalled. The gravity of the economic andfinancial problems in many Latin American andCaribbean countries prompted the request thatFAO undertake a major study on the obstaclesto agricultural and rural development andfeasible actions to enhance development,reduce poverty and improve nutritional status.The study will offer a Plan of Action to helpsolve the major food and agricultural problems

of the region. It will be presented at the nextFAO Regional Conference for Latin America andthe Caribbean in October 1988.

For many countries, current economicdifficulties are both a cause and an effect ofagricultural difficulties. The year 1986 witnessedthe continuation of an often decriedphenomenon the paradoxical coexistence offood shortages in some developing countriesand surpluses in other countries, especially thedeveloped countries. Despite the need toreduce budgetary imbalances and restoreequilibrium in world markets, most industrialcountries largely failed in their attempts toreconcile measures to control surpluses andpreserve farm incomes.

Despite a slowdown in the growth ofagricultural output in 1986, worldstocks particularly cereals soared, agriculturalprices plummeted to their lowest levels in halfa century, and competition in world agriculturalmarkets led to mounting conflicts amongtrading areas and a growing disregard for thefundamental principle of comparativeadvantage.

Developing country economies saw thepurchasing power of their agricultural exportssuffer sharp losses in 1985 and 1986, largelycancelling the gains of the two previous years.In some of these countries, good harvestsgenerated unmarketable surpluses, createdserious storage and financial problems and,ultimately, proved almost as harmful to farmerincomes as bad harvests.

The problem of abnormal food shortagespersisting in several other countries could notbe ignored. Nor could we underrate thedangers posed to Africa by the recurrence ofgrasshopper and locust infestations. Althoughthe response of the international community in1986 to FAO's warnings and appeals forassistance can be regarded as successful, largeareas in sub-Saharan Africa remain underthreat, requiring continuing vigilance andpreparedness.

This brief review of some of the highlights ofthe state of food and agriculture in 1986 givesrise to a number of reflections. In particular, I

must point to the need to improve theagricultural terms of trade of developingcountries, assure them stable prices for theirexports, free access to international markets,and the means to diversify and increase theprocessing of their products. We, at FAO, sharethe frustration of those countries that havedevoted much effort and resources toimproving their agricultural production andproductivity, only to discover that the fruits of

vi

such labour were unmarketable, costly to storeand, ultimately, unwanted.

FAO has taken decisive action to helpchannel cereal surpluses toward deficit areasthus avoiding driving down prices. To thiseffect, I urged donorsactual and potentialtoprovide maximum help in financing suchtriangular transactions and barter agreements.

The recent improvement in the food supplysituation in Africa should not allow us to relaxour vigilance on the immediate food problemsof the region. There is now a general consensusthat sustained economic and social progress inAfrica can only be through an integratedapproach to its agricultural and food problems.In the FAO study, African Agriculture: The Next25 Years, I made a number of concreteproposals for policy action, and FAO remainsready to assist African countries in theimmense amount of work required to translatethese proposals into programmes, andprogram mes into effective, practical action.

In the area of trade negotiations, I amlooking forward to the forthcoming negotiationsby GATT contracting parties to take a positivestep toward instituting a sounder basis foragricultural trade. I have earlier referred toanother basic ingredientfinancial resources foragricultural developmentwhich is the subjectof. the special chapter in this year's The Stateof Food and Agriculture.

It is important that countries mobilizeresources both domestic and external forinvestment. External commitments to agriculturehave stagnated since the early 1980s, and thosegranted on favourable terms have tended evento decline. Short-term prospects are also poor,as official development assistance is expected toincrease by barely 2% a year, in real terms, forthe rest of the decade.

I must once again underline the need formore external aid to the agricultural sector.Given the scarcity of aid, ways also have to befound for its more efficient allocation, bearingin mind the actual needs of farmers. I haveemphasized, more particularly in the context ofAfrica, the case for considerably expandinginput aid to developing countries. Inputs suchas agricultural equipment, tools, means oftransport, spare parts, and fertilizers could easilyand abundantly be made available by industrialcountries.

In making proposals for policy action, I amdeeply aware of the magnitude of the problemsand challenges facing us. There are recentexamples from developing countries, includingsome from the most populous ones, whichhave undertaken sound policy reforms and

measures to deal with the problems ofwidespread hunger and malnutrition. The firststep toward the adoption of sound policyaction is an adequate knowledge andunderstanding of the facts and issuessurrounding the current state of food andagriculture.. It is my hope that this documentwill contribute to this objective.

Edouard SaoumaDIRECTOR-GENERAL

Contents

GlossaryExplanatory noteIntroduction

PART ONEWORLD REVIEW

ECONOMIC, FINANCIAL ANDTRADE ENVIRONMENT

Overview

Output Growth and Patterns

Trade Growth and Patterns

Domestic Prices and Interest Rates

WORLD FOOD ANDAGRICULTURAL SITUATION ANDPROSPECTS

Food and Agricultural Production 12

The Outlook for Cereals

Prices and Consumption ofFertilizers

FISHERIES

Fish Production

International Trade in Fish andFishery Products

Prospects for 1986

Major Issues

xiiixiv FORESTRY 21

1

Forestry Production and Trade in1985 21

Price Developments of ForestProducts during 1970-85 23

7 The Tropical Forestry Action Plan 24

AGRICULTURAL TRADE

16Overview

17 Terms of Trade

18 EXTERNAL ASSISTANCE

18 Resource Flows to Agriculture

Food Aid18

ANNEX 1.1. Recent Economic,20 Financial and Institutional Events

Related to Agriculture21

vii

29

29

34

37

37

39

40

7SOME TRENDS IN THE EARLY 1980s

7 IN FOOD AND AGRICULTURE 25

9 Food Availability 25

10 Land and Labour Productivity 27

Changes in Input Use During the1970s and Early 1980s 28

12 Agricultural Exports and Incomes 28

Causes of Retarded AgriculturalGrowth

Recent Policy Reforms

Food and Agricultural Situation in1986 and the Early 1980s

LATIN AMERICA

Recent Food and AgriculturalPerformance

Characteristics of AgriculturalPolicies

Adjustment Policies and theAgricultural Sector in the 1980s 56

48 CENTRALLY PLANNED ECONOMIES 72

49 Eastern Europe and the USSR 72

Overall economic performance in52 1985 72

54 Recent developments in agriculture 72

Some characteristics of agricultural54 policy in Hungary 75

ANNEX 2.1. List of Countries Used56 in the Regional Review Tables 78

DEVELOPED MARKET ECONOMIES 67

The United States 67

The European EconomicCommunity (EEC) 69

Canada, Oceania and Japan 69

FAR EAST 59

Recent Food and AgriculturalPerformance 59

Emerging Issues and Problems 59

NEAR EAST 63

Recent Economic and AgriculturalPerformance 63

Emerging Issues and Problems 66

PART TWOREGIONAL REVIEW

AFRICA 45

Political Commitment to Food andAgricultural Growth 45

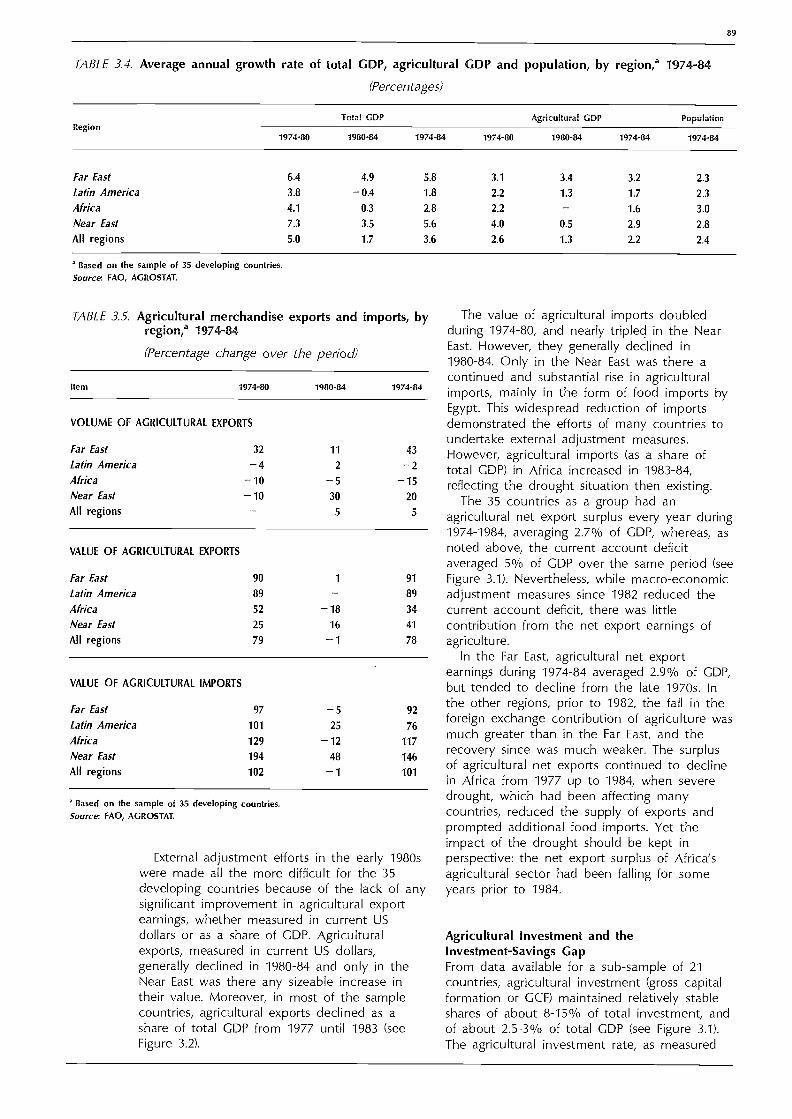

AGRICULTURAL PERFORMANCE 88

Growth of Agricultural ValueAdded

Agriculture and the CurrentAccount Deficit 88

Agricultural Investment and theInvestment-Savings Gap 89

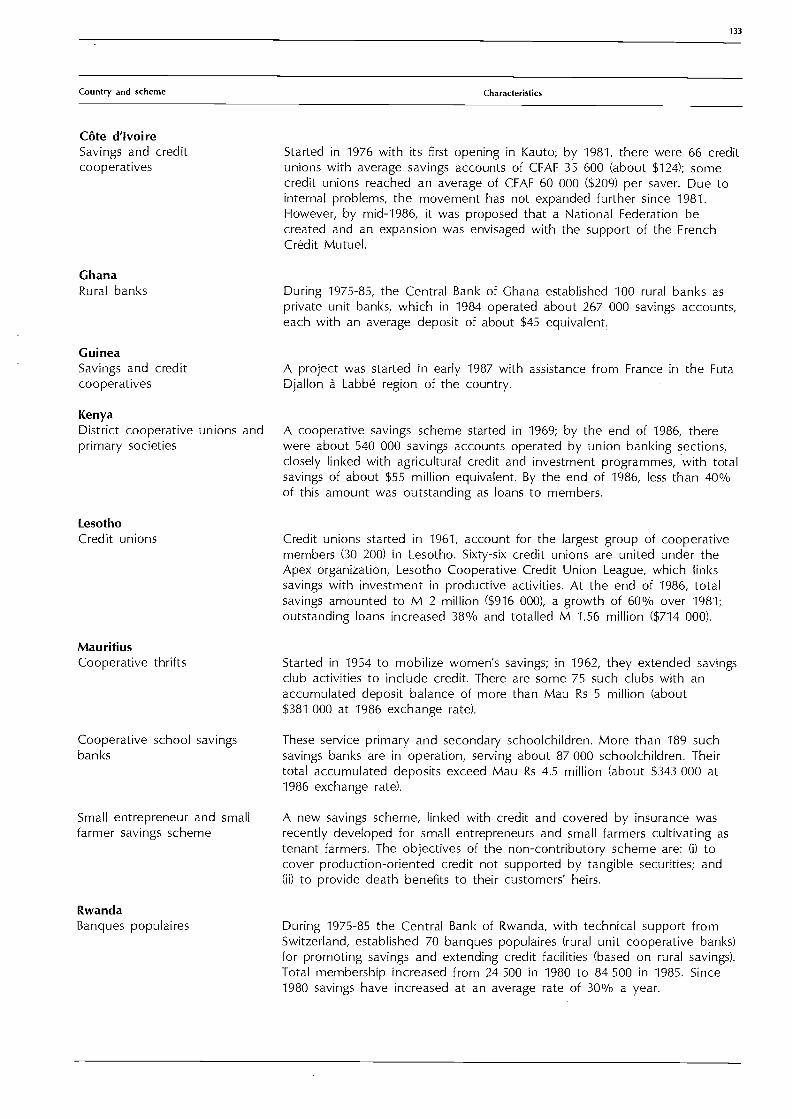

ANNEX 3.1. Features of SelectedSavings Schemes in Rural Areas of

88 Developing Countries, 1985

AGENDA FOR FUTURE RESEARCH 129

131

ix

PART THREE THE PRIVATE SECTOR 115FINANCING AGRICULTURALDEVELOPMENT Overview 115

INTRODUCTION 81 Rural Financial Markets (RFMs) 118

Foreign Direct Investment (FDI) inMACRO-ECONOMIC OVERVIEW 82 Developing Countries 126

External Adjustment 82 Transnational Corporations:Evolution and Characteristics 128

Domestic Adjustment 86

THE FISCAL BUDGET 92

Introduction 92

Overview of the Fiscal Budget 92

Agricultural Expenditure by thePublic Sector 93

Vulnerability of AgriculturalExpenditure 95

External Sources of Finance toAgriculture 97

Government Revenue andAgricultural Taxation 107

Some Conclusions and PolicyIssues 112

TABLES

WORLD REVIEW

1.1 Annual Changes in SelectedEconomic and Financial Indicators,1980-86

1.2 UN World Export Price Indices, ByQuarter, 1984-86

1.3 Food and Non-Food Production,1984-86

1.4 Agricultural Production, byCommodity, 1985-86

1.5 Percentage Rate of Change in PerCaput Food Production, 1985-86

1.6 Fertilizer Consumption, by MajorNutrients, 1982-85

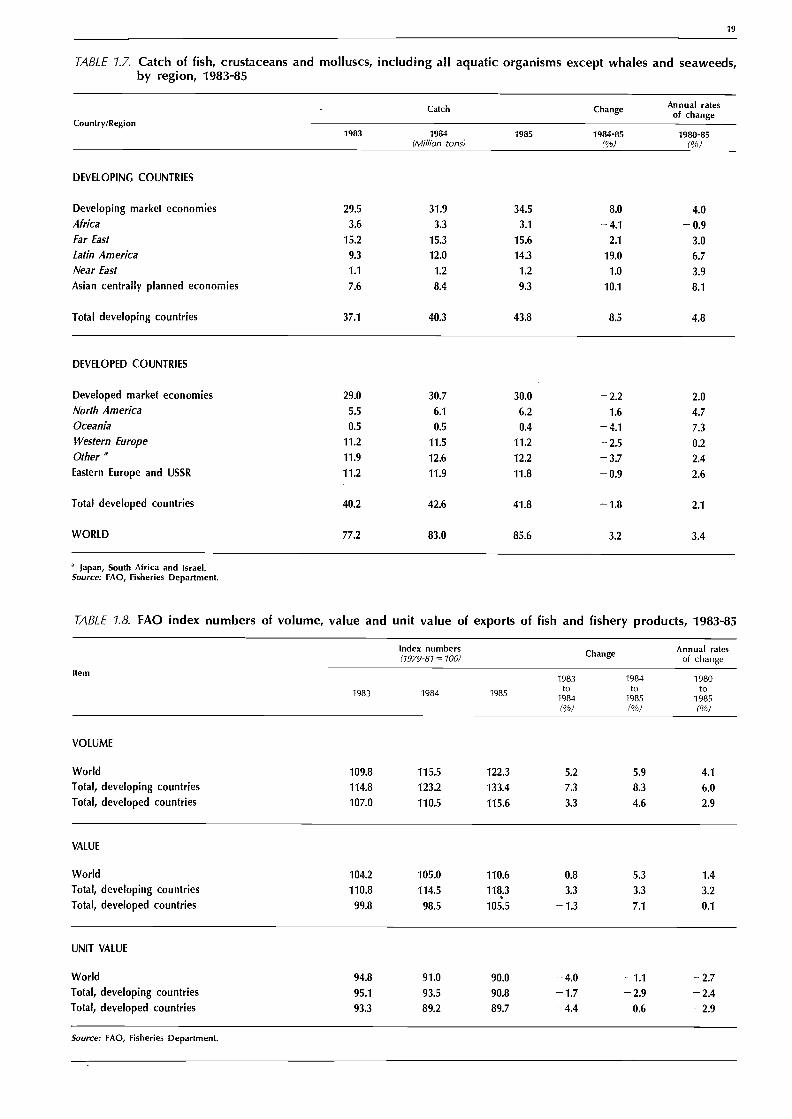

1.7 Catch of Fish, Crustaceans andMolluscs, Including all AquaticOrganisms except Whales andSeaweeds, by Region, 1983-85

1.8 FAO Index Numbers of Volume,Value and Unit Value of Exports ofFish and Fishery Products, 1983-85

1.9 Output of Main Forest Products,Total Developing and DevelopedCountries and World, 1983-85

1.10 Volume of Exports of Main ForestProducts, Total Developing andDeveloped Countries, 1983-85

1.12 Annual Rates of Change in Land andLabour Productivity, by Region,1971-80 and 1980-84

1.13 Annual Rates of Change in SelectedAgricultural Inputs, by Region,1971-80 and 1980-83

1.14 Value of World Exports ofAgricultural (Crops and Livestock),Fishery and Forest Products, atCurrent Prices, 1983-85

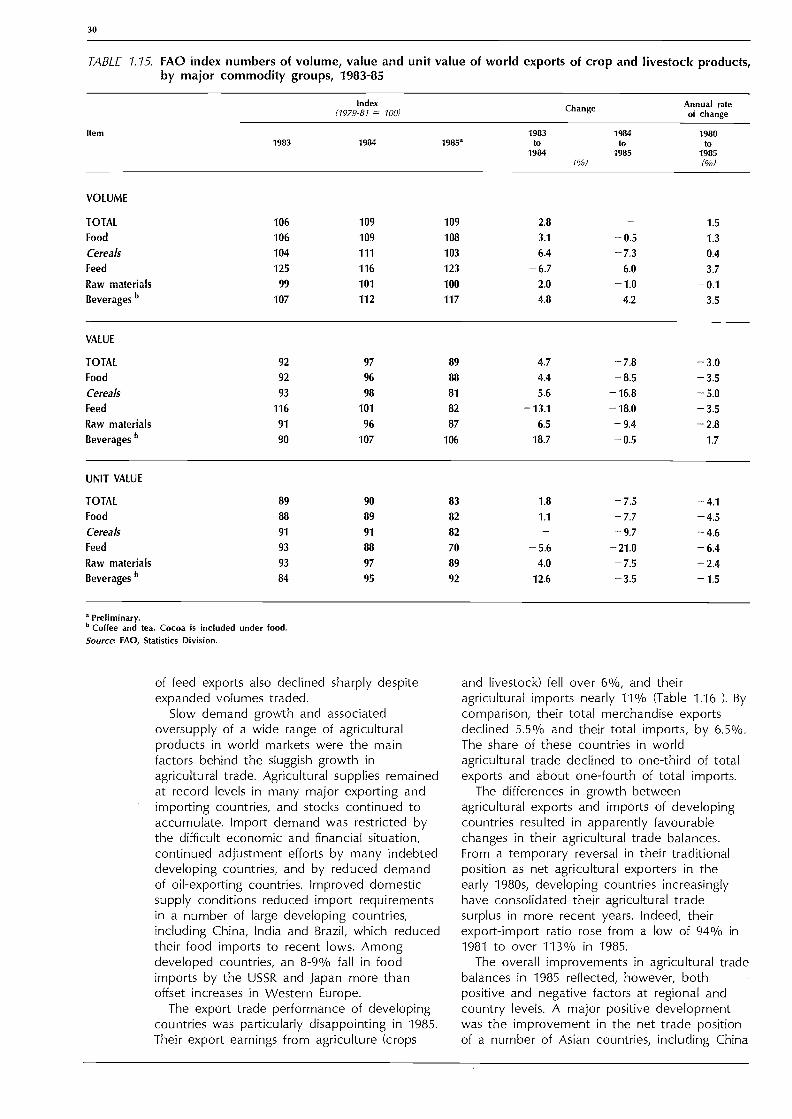

1.15 FAO Index Numbers of Volume,Value and Unit Value of WorldExports of Crop and LivestockProducts, by Major CommodityGroups, 1983-85

13

1.16 Value of World Agricultural Trade(Crops and Livestock), at CurrentPrices, by Region, 1983-85

REGIONAL REVIEW

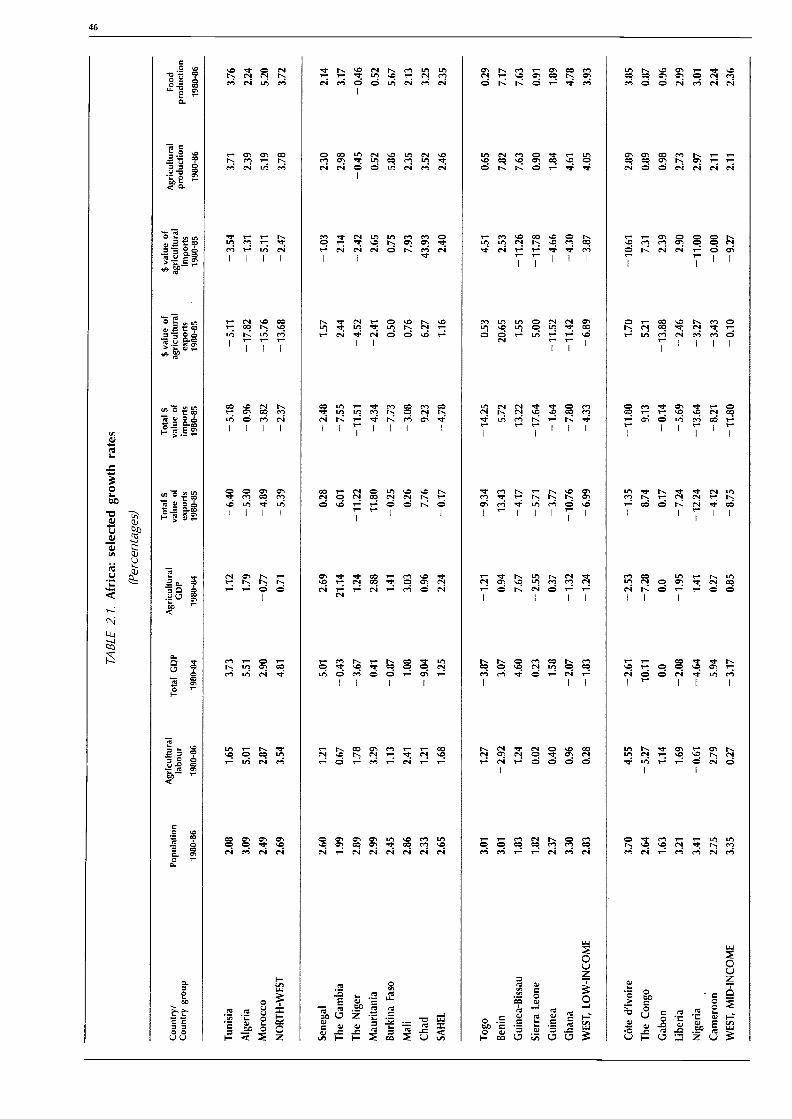

14 2.1 Africa: Selected Growth Rates

2.2 Latin America: Selected Growth Rates15

2.3 Far East: Selected Growth Rates

16 2.4 Near East: Selected Growth Rates

2.5 Developed Market Economies:Annual Rates of Change inProduction of Agricultural and Food

19 Products, 1984-86 and 1980-86

2.6 Eastern Europe and USSR: AnnualChanges in Selected EconomicIndicators, 1981-85

2.7 Eastern Europe and USSR: AnnualChanges in Food and AgriculturalOutput, 1983-86

23 FINANCING AGRICULTURAL DEVELOPMENT

3.2 Debt-Service Payments as aPercentage of Total Exports of Goodsand Services, by Region, 1975,

27 1980-84

3.3 Foreign Exchange Reserves as aPercentage of Total Imports of

28 Goods and Services, by Region, 1975,1980-84

3.4 Average Annual Growth Rate of TotalGDP, Agricultural GDP and

29 Population, by Region, 1974-84

3.5 Agricultural Merchandise Exports andImports, by Region, 1974-84

3.6 Annual Average Central Government30 Agricultural Expenditure, by Region,

1974-83

31

46

55

60

64

68

73

74

86

86

89

89

94

1.11 Changes in Per Caput Dietary Energy 3.1 Total External Merchandise Trade, bySupplies (DES) and Related Factors, Region, 1974-84 85

102 Developing Countries, 1980-84 26

1.17 Net Barter and Income Terms ofTrade of Agricultural Exports forManufactured Goods and Crude

8 Petroleum, 1981-85 32

1.18 Commitments of External Assistance

9to Agriculture (Broad Definition),1983-85 38

19

22

3.7 Growth in Real AgriculturalExpenditure and Agricultural LabourForce, by Region, 1974-83

3.8 Instability of Real AgriculturalExpenditure, by Region, 1974-83

3.9 Overall Trends in OfficialCommitments to Agriculture (OCA),(Including Technical AssistanceGrants), 1974-84

3.10 Percentage Distribution of OCA, byPurpose, Developing Countries,Mid-1970s and Early 1980s

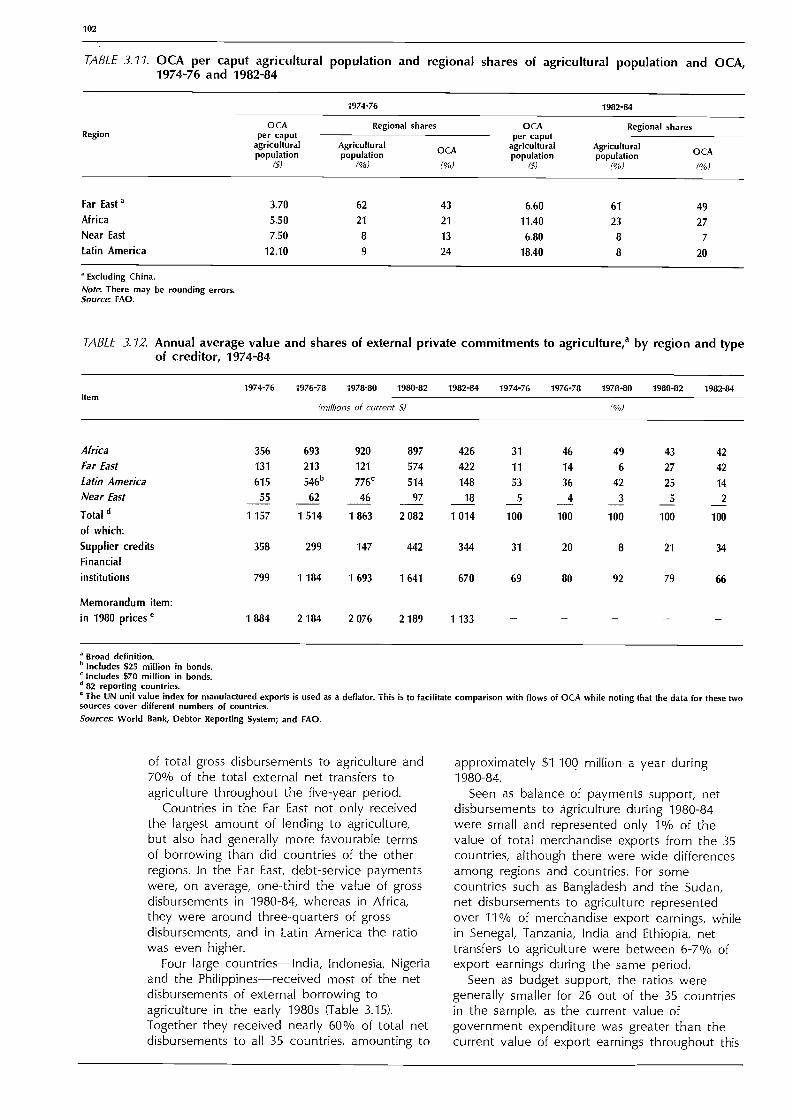

3.11 OCA Per Caput AgriculturalPopulation and Regional Shares ofAgricultural Population, and OCA1974-76 and 1982-84

3.12 Annual Average Value and Shares ofExternal Private Commitments toAgriculture, by Region and Type ofCreditor, 1974-84

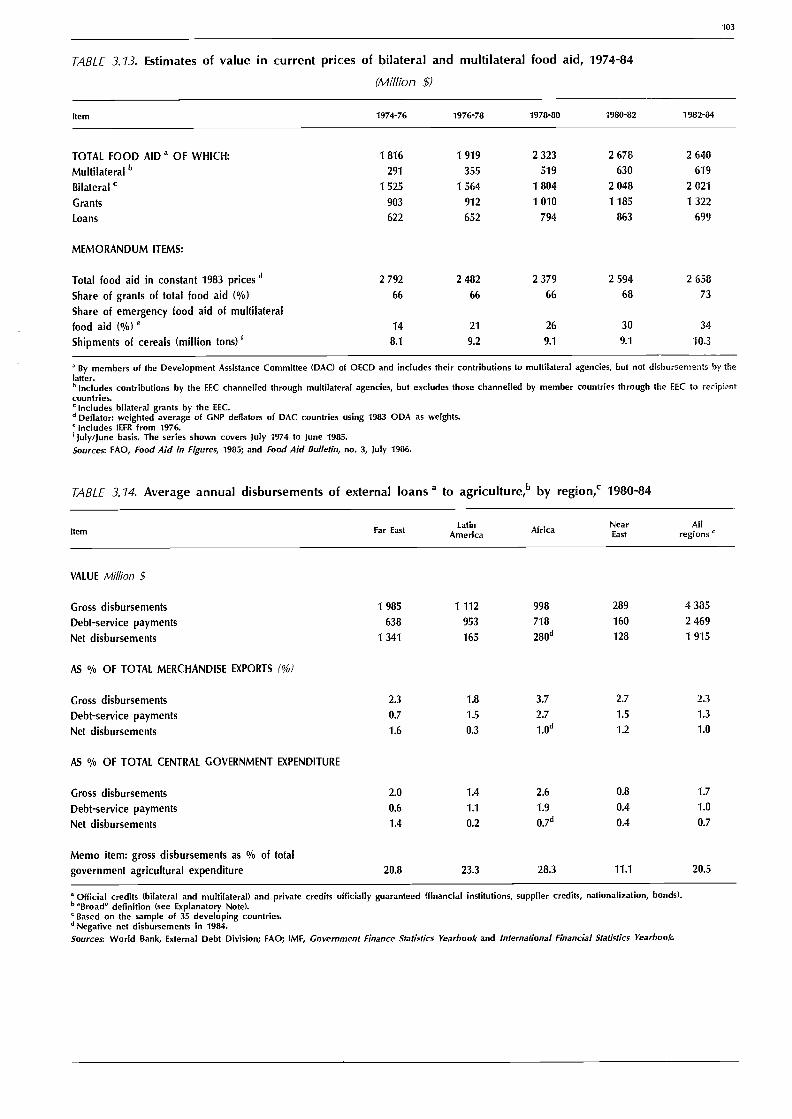

3.13 Estimates of Value in Current Pricesof Bilateral and Multilateral FoodAid, 1974-84

3.14 Average Annual Disbursements ofExternal Loans to Agriculture, byRegion, 1980-84

3.15 Major Recipients of Disbursements toAgriculture, Selected Countries,1980-84

3.16 Annual Average ExternalDisbursements to All Sectors, byRegion, 1980-84

3.17 Cereal Food Aid, by Region, 1980-84Average

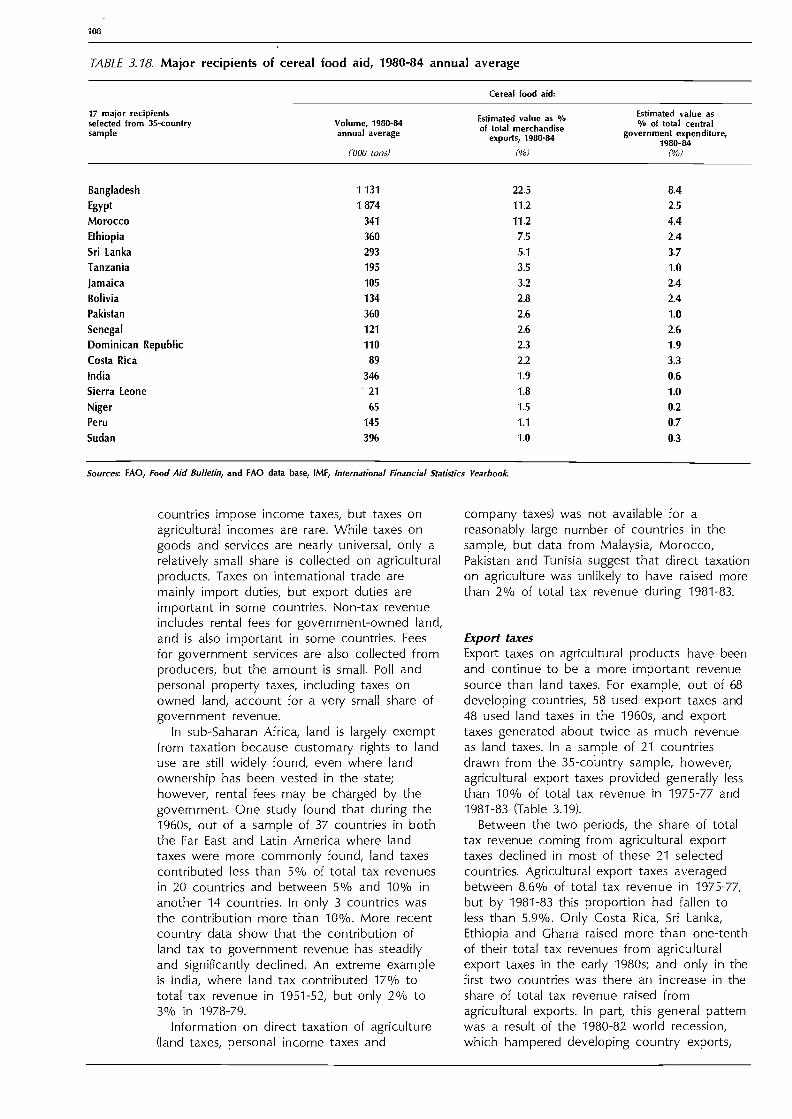

3.18 Major Recipients of Cereal Food Aid,1980-84 Annual Average

3.19 Agricultural Export Taxation andExpenditure, Selected Countries,1975-77 and 1981-83

3.20 Financing of the Fiscal Deficit inSelected Countries, 1983

3.21 Percentage of Overdue AgriculturalLoans to Farmers in Asian Countriesin Recent Years

3.22 Borrowing Transaction Costs at theFarm Level in Selected Countries, byLoan Size

3.23 Difference Between Rate of Intereston Deposits and Rate of Inflation,

94 Selected Developing Countries,1976-84 125

97 3.24 Foreign Direct Investment (FDI) inDeveloping Countries, 1974-84 126

FIGURES100

104 BOXES

xi

1.1 Export Prices of Fertilizers, 1980-1986 17

101 1.2 International Prices of SelectedAgricultural Commodities, 1981-86 34

1.3 Shipments of Food Aid, Cereals,1974/75-1986/87 37

1023.1 External and Domestic Adjustment,

by Region, 1974-84 84

3.2 Agricultural GDP, Exports and102 Imports as a Share of Total GDP, by

Region, 1974-84 90

3.3 Central Government Expenditure and103 Revenue as a Share of Total GDP,

All Regions, 1974-83 93

3.4 Monetary Survey: Domestic Credit to103 Private Sector and Government, by

Region, 1974-84 116

/./ The Chernobyl Nuclear Accident 11

1051.2 The International Tropical Timber

Agreement 33

1051.3 Agriculture in the GATT: The

Uruguay Round 35

1082.1 FAO's In-Depth Study on Food and

Agricultural Problems in Africa 51

109 2.2 Locust and Grasshopper Attacks inAfrica and the Near East 53

117 2.3 FAO's In-Depth Study on Agriculturein Latin America and the Caribbean 58

2.4 Growth, Equity and Poverty in the

123 Far East 62

2.5 Labour Mobility in the Near East 65

124 2.6 US/EEC Agricultural Trade Relations:Some Success, ContinuingDifferences and Third-Party Reactions 70

ANNEX TABLES

A.4 Volume of Exports of MajorAgricultural, Fishery and ForestProducts

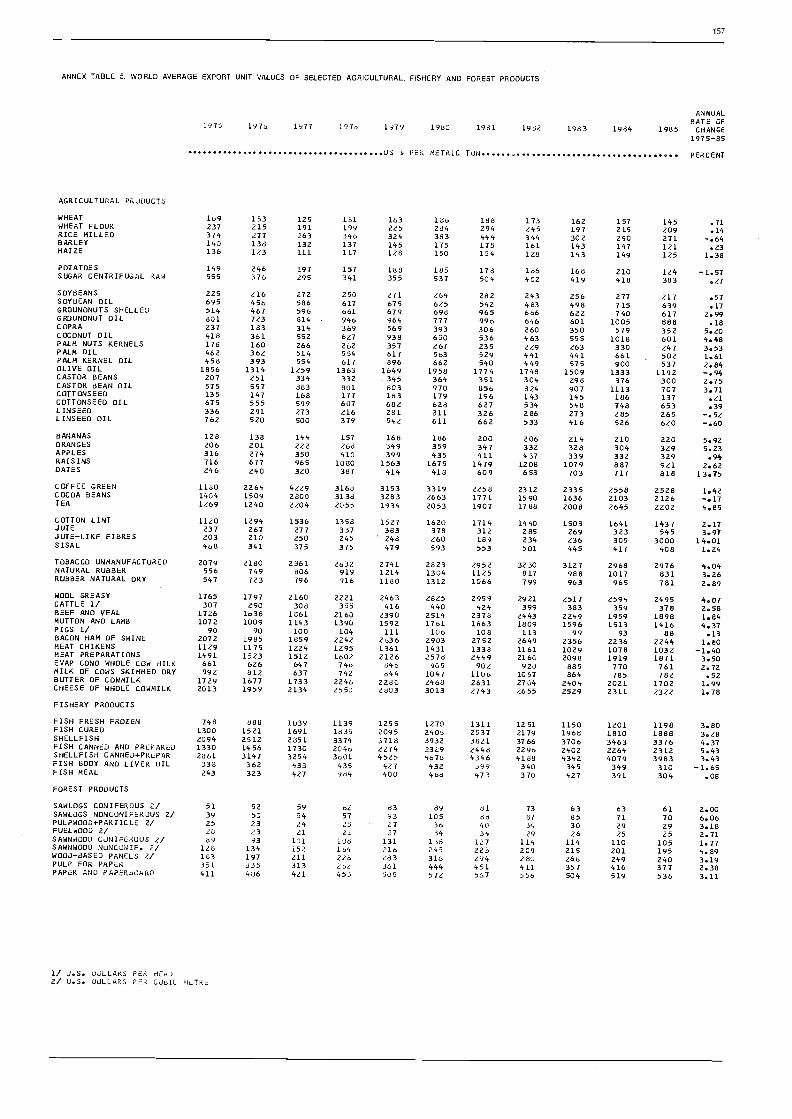

A.5 World Average Export Unit Values ofSelected Agricultural, Fishery andForest Products

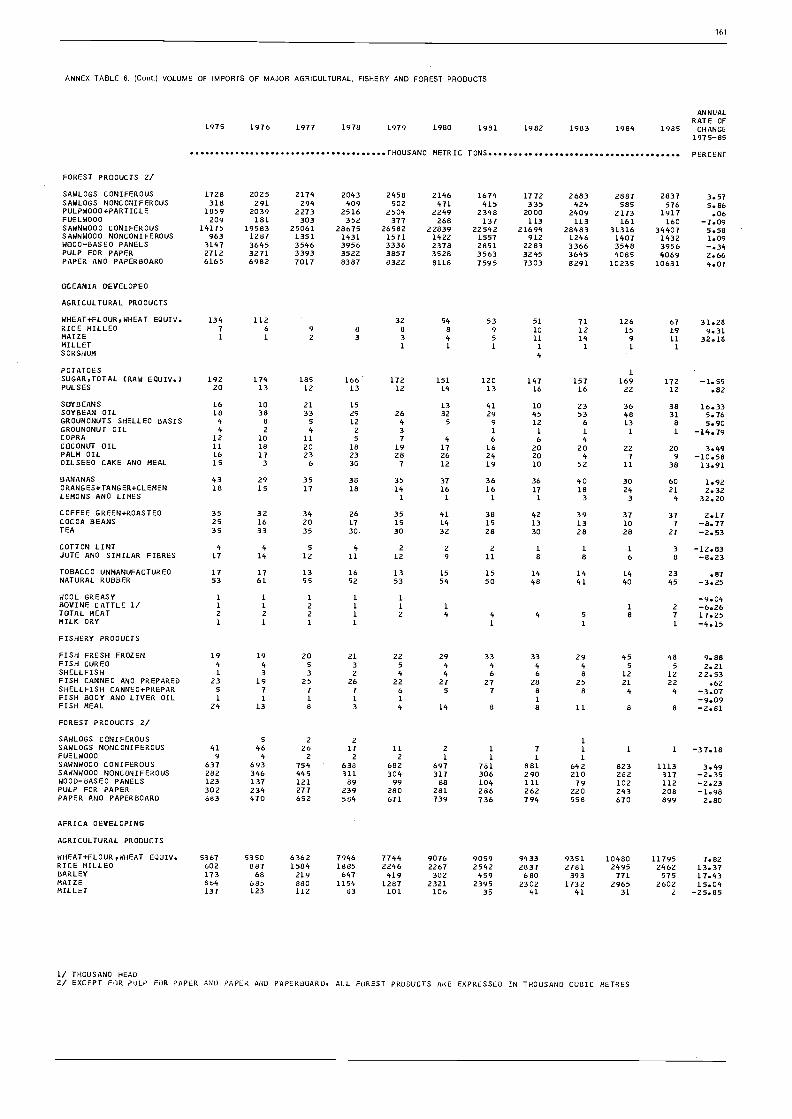

A.6 Volume of Imports of MajorAgricultural, Fishery and ForestProducts

A.7 Indices of Value of Exports ofAgricultural, Fishery and ForestProducts

A.8 Indices of Volume of Exports ofAgricultural, Fishery and ForestProducts

A.9 Indices of Value of Imports ofAgricultural, Fishery and ForestProducts

A.10 Indices of Volume of Imports ofAgricultural, Fishery and ForestProducts

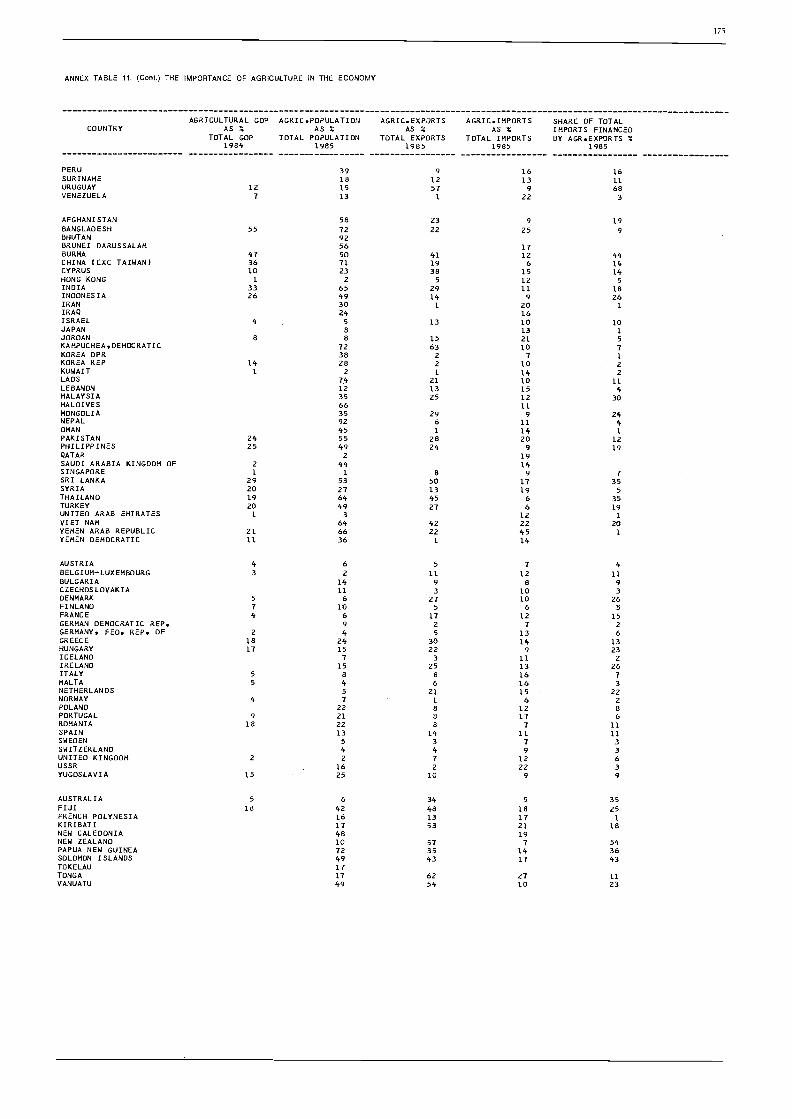

A.11 The Importance of Agriculture inthe Economy

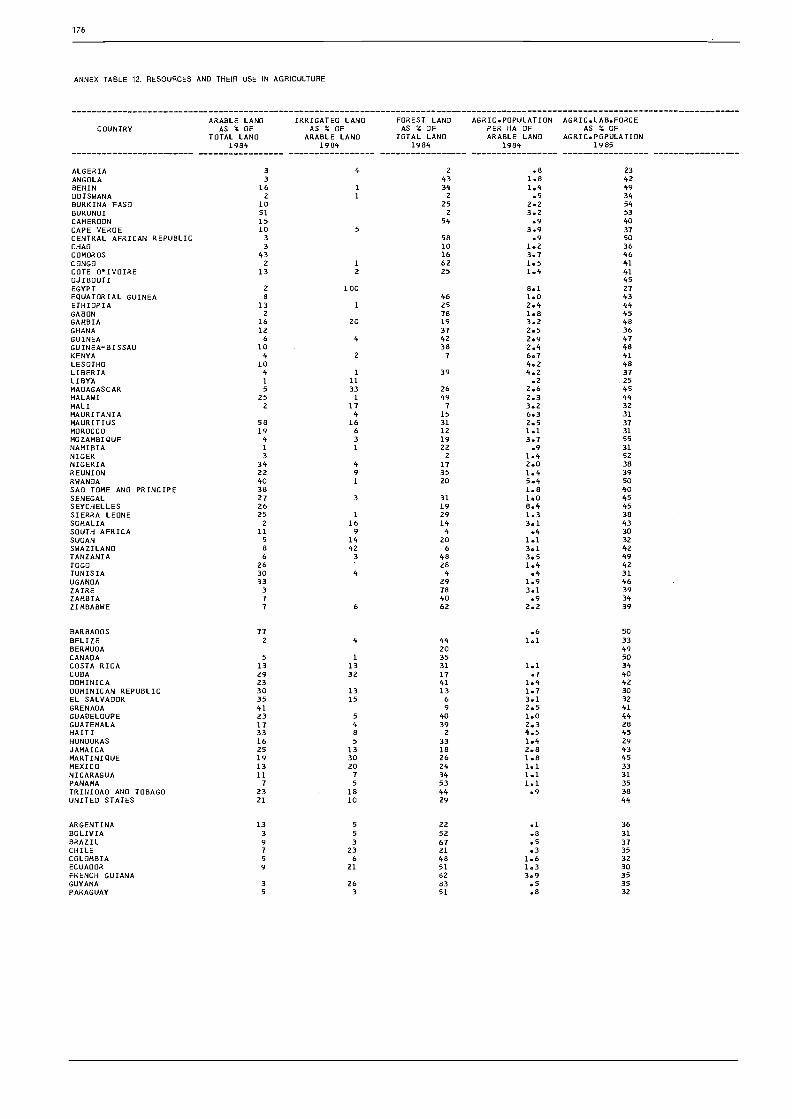

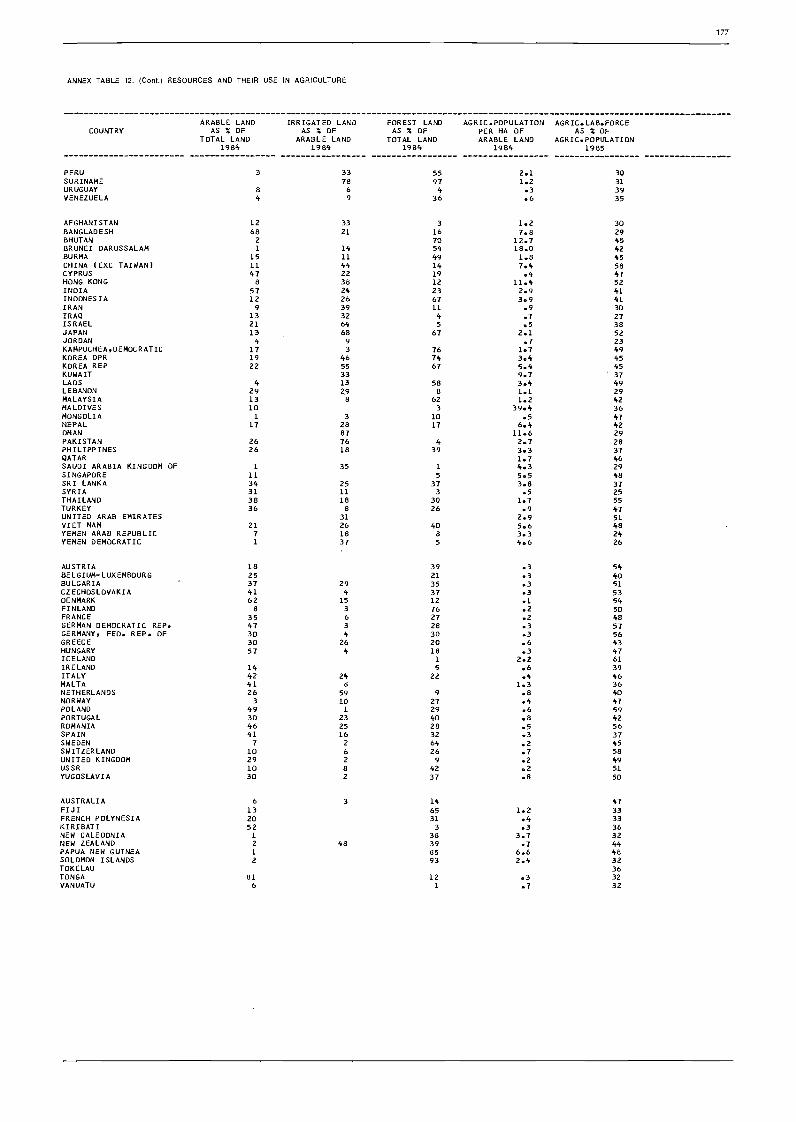

A.12a Resources and Their Use inAgriculture

76 A.12b Resources and Their Use inAgriculture

83

A.13 Measures of Output and Productivity87 in Agriculture

98 A.14 Carry-Over Stocks of SelectedAgricultural Products

110A.15 Annual Changes in Consumer Prices:

111 All Items and Food

114 A.16 Per Caput Dietary Energy Supplies inSelected Developed and DevelopingCountries

119

A.17 Annual Agricultural Shares of TotalOfficial Commitments to all Sectors

120 (Broad Definition), by Multilateraland Bilateral Sources, 1978-85 187

166

168

170

172

174

176

A.18 Percentage Distribution of OfficialCommitments to Agriculture (BroadDefinition), by Multilateral andBilateral Sources, 1978-85

A.19 DAC Countries: Bilateral ODACommitments from Individual

145 Countries and Proportion toAgriculture (Broad Definition)

A.20 Percentage Distribution of OfficialCommitments to Agriculture,(Excluding Technical Assistance

149 Grants), by Purpose, 1978-85

A.21 Distribution of Official Commitmentsto Agriculture, Excluding Technical

157 Assistance Grants (Broad Definition),from all Sources, by Region andEconomic Groups, 1978-85

158

178

180

182

183

185

188

189

190

191

A.1 Volume of Production of MajorAgricultural, Fishery and ForestProducts 137

A.2 Indices of Food Production

A.3 Indices of Agricultural Production 147

xii

2.7 Agriculture in Poland in the 1980s

3.1 The 35-Country Sample

3.2 Agriculture's Share of Investment

3.3 The Recurrent Cost Problem

3.4 External Assistance to Fisheries

3.5 Financing Forestry Development

3.6 Agricultural Export Taxes

3.7 Mobilizing Rural Savings: Indonesiaand the Dominican Republic

3.8 Innovative Financial Intermediaries inZimbabwe

Glossary

ACPE Asian centrally plannedeconomies

AFPLAN Regional Food Plan forAfrica (FAO)

APK Agro-Industrial Complex,USSR

APPER Africa's Priority Programmefor Economic Recovery

CFDT Committee on ForestDevelopment in theTropics (FAO)

CGIAR Consultative Group onInternational AgriculturalResearch(FAO/UNDP/World Bank)

CMEA Council for MutualEconomic Assistance

CRP Conservation ReserveProgramme

DES Dietary energy suppliesECU European Currency UnitEEC European Economic

CommunityFDI Foreign direct investmentGA I I General Agreement on

Tariffs and TradeGCF Gross capital formationGEA Government expenditure

on agricultureGDP Gross domestic productGDR German Democratic

RepublicGIEWS Global Information and

Early Warning System forFood and Agriculture (FAO)

IBRD International Bank forReconstruction andDevelopment

ICOR Incremental capital outputratios

IDA International DevelopmentAssociation

IEFR International EmergencyFood Reserve (WFP)

IFAD International Fund forAgricultural Development

IFC International FinanceCorporation

IMF International MonetaryFund

ITTO International TropicalTimber Organization

LDCs Least-developed countriesLIFDC Low-income food-deficit

countriesMIGA Multilateral Investment

Guarantee Agency (WorldBank)

MTN Multilateral TradeNegotiations

NAMBOARD National AgriculturalMarketing Board, Zambia

OAU Organization of AfricanUnity

OCA Official Commitments toAgriculture

ODA Official DevelopmentAssistance (DAC)

OECD Organisation for EconomicCooperation andDevelopment

OPEC Organization of PetroleumExporting Countries

RFMs Rural financial marketsSDR Special drawing rightsTFAP Tropical Forestry Action

PlanTF/TCP Trust Funds/Technical

Cooperation Programme(FAO)

TNCs Transnational corporationsUNCTAD United Nations Conference

on Trade and DevelopmentUNDP United Nations

Development ProgrammeUSAID United States Agency for

International DevelopmentUSDA United States Department

of AgricultureWCARRD World Conference on

Agrarian Reform and RuralDevelopment

xiv

Explanatory note

The following symbols are used in thestatistical tables:

= none or negligible.= not available.

"1985/86" signifies a crop, marketingor fiscal year running from one calendaryear to the next; "1984-86" signifies theaverage for three calendar years.

Figures in statistical tables may notadd up because of rounding. Annualchanges and rates of change have beencalculated from unrounded figures.Unless otherwise indicated, the metricsystem is used throughout. The dollarsign ($) refers to US dollars.

Production Index NumbersThe FAO index numbers have 1979-81as the base period. The production datarefer to primary commodities (e.g.,sugarcane and sugarbeet instead ofsugar) and national average producerprices are used as weights. The indicesfor food products exclude tobacco,coffee, tea, inedible oilseeds, animal andvegetable fibres and rubber. They arebased on production data presented ona calendar-year basis.'

Trade Index NumbersThe indices of trade in agriculturalproducts also are based on 1979-81.They include all the commodities andcountries shown in the F110 TradeYearbook 1985. Indices of total foodproducts include those edible productsgenerally classified as "food."

All indices represent changes incurrent values of exports (f.o.b.) andimports (c.i.f.), all expressed in USdollars. If some countries report importsvalued at f.o.b. (free on board), theseare adjusted to approximate c.i.f. (cost,insurance, freight) values. This methodof estimation shows a discrepancy

whenever the trend of insurance andfreight diverges from that of thecommodity unit values.

Volume and unit value indicesrepresent the changes in theprice-weighted sum of quantities and ofthe quantity-weighted unit values ofproducts traded between countries. Theweights are respectively the price andquantity averages of 1979-81, which isthe base reference period used for allthe index number series currentlycomputed by FAO. The Laspeyresformula is used in the construction ofthe index numbers.2

Definitions of "Narrow" and "Broad"The OECD definitions of agriculture aregenerally used in reporting on externalassistance to agriculture. The narrowdefinition of agriculture, now referred toas "directly to the sector" includes thefollowing items:

Appraisal of natural resourcesDevelopment and management ofnatural resourcesResearchSupply of production inputsFertilizersAgricultural servicesTraining and extensionCrop productionLivestock developmentFisheriesAgriculture (subsector unallocated)

The broad definition includes, inaddition to the above items, activitiesthat are defined as "indirectly to thesector." These activities are:

ForestryManufacturing of inputsAgro-industriesRural infrastructureRural developmentRegional developmentRiver development

For full details, see FAO Production Yearbook 1985, Rome, 2 For full details, see FAO Trade Yearbook 1985, Rome,1986. 1985.

Regional Coverage"Developing countries" include: (i)Developing market economies (Africa,Latin America, Near East 3, Far East andOther) and (ii) Asian centrally plannedeconomies or ACPE (China, DemocraticKampuchea, Democratic People'sRepublic of Korea, Mongolia and VietNam).

"Developed countries" include 4: (i)

Developed market economies (NorthAmerica, Western Europe, includingYugoslavia, Oceania, Israel, Japan andSouth Africa) and (ii) Centrally plannedeconomies of Eastern Europe and theUSSR (Bulgaria, Czechoslovakia, GermanDemocratic Republic, Hungary, Poland,Romania and USSR).5

3 The Near East includes: Egypt, Libyan Arab Jamahiriya, the

Sudan, Afghanistan, Bahrain, Cyprus, Islamic Republic ofIran, Iraq, Jordan, Kuwait, Lebanon, Oman, Qatar, Kingdom

of Saudi Arabia, Syrian Arab Republic, Turkey, United Arab

Emirates, Yemen Arab Republic and Democratic Yemen.

Note that "industrial countries", as defined by the Interna-

tional Monetary Fund (IMF) (see Table 1.11, include: Aus-

tralia, Austria, Belgium, Canada, Denmark, Finland, France,

Germany (Fed. Rep. of), Iceland, Ireland, Italy, Japan, Luxem-

bourg, the Netherlands, New Zealand, Norway, Spain,Sweden, Switzerland, United Kingdom and United States.(They do not include Yugoslavia, Greece, Israel, South

Africa, the centrally planned economies and some smallerother countries).

5 Albania is omitted in this report for lack of sufficient data.

XV

Introduction

While showing a wide variety of regional andcountry experiences, the world food andagricultural situation in 1986 was broadlyframed by two opposing features. On the onehand, there was a marked improvement insome important aspects of food security: moredeveloping countries achieved gains in percaput food output than in the preceding fiveyears, several heavily populated countriesconsolidated their food supply situations, andfood supply conditions also eased in somecritical areas, notably in Africa. On the otherhand, for some industrial countries, expandedavailability of food and agricultural productswas a mixed blessing in the context of anoversupply of many agricultural commodities,mounting stocks, depressed prices, deterioratingfarm incomes, despite rising costs of agriculturalprogrammes, and increasing protectionism inagricultural trade.

In this present period of transition betweeneconomic recession and full recovery, the reliefbrought about by the improvement inagricultural output has constituted, for manypoor countries, a badly needed stimulus for aneconomic revival. The first chapter of thisreport shows that domestic efforts of thesecountries to overcome the crisis have not metwith a favourable overall economicenvironment. Many of the problems currentlyfacing agriculture are closely related to theinconsistencies and weaknesses of the presenteconomic climate: (i) failure by the industrialcountries to significantly resume and transmitthe momentum of economic growth, despitelower inflation and interest rates and generallymore realistic patterns of exchange rates; (ii)disappointing trade performances, with exportvolumes failing to respond to low internationalcommodity prices; and (iii) a worsening debtsituation for many developing countries, despitereduced capital inflows, lower interest rates andadjustment efforts, which have been costly interms of human welfare.

As regards agriculture, the current situationof ample food supplies, while theoreticallywelcome in the context of global food security,also presents perverse aspects. Despite aslowdown in the growth of food production in1986, sluggish global demand continued to lagbehind output. As a consequence, the problemof global oversupply of many agriculturalproducts did not subside, unmarketable stocks,especially of cereals, dairy products and beef,continued to accumulate in several industrial

countries and some developing onesandinternational prices plummeted. Agriculturalmarkets became distorted by fierce competition,export subsidies and by other marketincentives, which vitiated comparativeadvantage relationships and undermined theefficiency of markets.

However, some progress was made in 1986in controlling the oversupply of agriculturalproducts in industrial countries. While amajority of these countries increased their foodoutput in per caput terms (some substantially)during 1980-85, only a minority of themcontinued to do so in 1986. Conversely, agreater number of developing countries werecredited with encouraging results in foodproduction in 1986. Moreover, some of themost significant gains occurred where they wereneeded most: in heavily populated countriesand in Africa where severe food shortages hadpersisted in prior years.

While such opposing trends in food outputwere, on balance, favourable,regional and country experiences differedwidely. The generally high rate of growth infood and agricultural output exacerbated thedifficulties in some agricultural commoditymarkets, as some countries became moreself-sufficient in food and others becamepotential exporters and faced problems ofsurplus disposal.

Africa achieved a cumulative growth of over8% in food production in 1985 and 1986. Thisremarkable recovery should not conceal,however, the persistence of abnormal foodshortages in five African countries. Also, thesudden emergence of localized surpluses andthe difficulty in marketing them, underlined theprecariously poised equilibrium of Africa's foodchain. This report shows the unfortunate,incongruous situation of such countrieseconomically dependent on agriculture, whichsucceeded in improving their outputperformances, yet were deprived of marketopportunities that would have permitted themto benefit from their successes.

The threat of major food losses in Africa,from grasshopper and locust infestations, whicharose in late 1985 and into 1986, receded,although the persisting danger of new upsurgesin some areas still required continuing controlefforts. Nevertheless, one year after FAO's firstwarning of a grasshopper and locust upsurge,

2

the massive efforts mobilized have alreadyyielded encouraging results.

In Latin America, the moderate recoveryachieved in 1984 and 1985 failed to consolidatein 1986. Despite slower inflationary pressures,economic activity slowed down and thesituation in the external sector deterioratedmarkedly. The difficulties in surmounting thegrave economic crisis were compounded by aseries of setbacks in the agricultural sector:food and agricultural output stagnated andexport earnings were affected by a dramaticdeterioration in the terms of trade. A sharpworsening in the debt-servicing situationbrought again the problem of indebtedness tothe forefront of the region's economicconcerns.

A generally more favourable turn of eventsoccurred in the Far East. For many Asiancountries, 1986 was a good agricultural yearand several of the most populous of themcontinued to achieve sustained growth.Paradoxically, the success in boosting agriculturecreated, in some countries, increased difficultiesin marketing and in adjusting supply todemand.

Many of the main problems and issuessurrounding agriculture in the Near East in 1986were linked to the fall in export earnings fromoil, and the consequent reduction of economicactivity and employment opportunities. Foodand agriculture in both oil-exporting and non-oilcountries were affected by cutbacks ininvestment, production and consumer subsidies,and by massive movements of migratoryworkers.

It is in the area of trade that the agriculturalsituation appeared the least encouraging. Thesituation of oversupply of many agriculturalproducts, together with depressed importdemand from industrial, oil-exporting anddebt-burdened countries, contributed to astagnation in the volume of agricultural exportsand a fall in their value. The collapse in theprices of agricultural products and a strongdeterioration in agricultural terms of traderesulted in a heavy setback for the exportearnings of many developing countries. Whileagricultural trade balances tended to improve indeveloping countries, for many of them thiswas only the consequence of a depressedcapacity to pay and, hence, an inability to takeadvantage of low international prices to importfood.

Although complete data on fishery andforestry performances in 1986 are not yetavailable, both sectors recorded substantialgains in output in 1985. Fish output expandedfor the eighth consecutive year, mainly owingto larger catches in South American waters.Being largely confined to fishmeal manufacture,such catches were, however, less significant fordirect food consumption than their largevolumes might suggest. The stagnation in fishoutput in Africa, despite the rich marineresources off West Africa especially, continuedto be a cause for concern. The volume ofworld fish trade expanded in 1985, twice as fastas output. Indeed, in 1985, fisheries appeared asthe only bright spot in a generally depressedfood and agricultural trade environment.

Forestry production also continued to expandin 1985 for the third consecutive year andexceeded previous peaks in all product areas.While trade in forest products had expandedconsiderably over the past 15 years, itstagnated in 1985, however, and actually fell indeveloping countries. Recent institutionaldevelopments of considerable potentialimportance for forestry were: the establishmentin mid-1986 of the International Tropical TimberAgreement, the support for FAO's ForestryAction Plan by the Ninth World ForestryCongress, and the International Conference onForests and Trees, along with its approval bythe FAO Committee on Forestry.

This report also reviews trends in selectedareas related to food and agriculture in theearly 1980s. This period of serious economicstress was reflected in declining nutritionallevels in nearly a half of the 100 or socountries reviewed, while a third showed onlymodest gains in per caput calorie intake. Mostregrettably, countries whose populations alreadyhad the lowest average nutritional levelssuffered the most pronounced losses in percaput calorie intake. The greatest losses werefound in Africa and Latin America, whilecountries in the Near East achieved some gainsin calorie consumption only through increasedfood imports. On the other hand, improvementin food availability in some Asian countries,which account for a major share of the totalpopulation of developing countries, can beregarded as a major accomplishment.

The crisis of the early 1980s had varyingeffects on agricultural productivity and inputusage in the different regions. This report showsthat both land and labour productivity declined

significantly in Africa and Latin America, butimproved in Asia and the Near East. Fertilizerconsumption, tractor usage and irrigationavailability were, in many cases, severelyconstrained by the economic recession. It wasalso observed that the early 1980s heightenedthe divergence in the source of agriculturalincomes of the different countries: thoserelatively more export-dependent becameincreasingly so, while for others, the domesticmarket assumed increasing importance.

The second chapter of this report focuses onthe agricultural performances of the differentregions, including the developed countries,against the background of the economic crisisof the 1980s.

Apart from greatly improved weatherconditions in 1985 and 1986, a shift in policystance was noted in Africa, conferring greaterpriority to the agricultural sector to lead to theresumption of economic growth. In LatinAmerica, agriculture was a leading sector inimplementing adjustment policies necessitatedby the economic crisis, particularly in the driveto prdmote exports and reduce imports.

Agricultural incomes are still low in Asiaand, while some countries in the region,including China and India, experiencedimpressive agricultural performances in recentyears, they face problems of adjusting outputto market demand. The potential size of China,both as an agricultural market and as a majorexporter of agricultural products, hasimplications not only for the trading countriesof Asia, but for the world as a whole.

Agriculture played a widely varying role inthe economies of the Near East region. In bothoil-exporting and oil-importing countries,however, the sector had to adjust to theconsequences of declining oil revenues. Largeagricultural subsidies for producers andconsumers were cut as part of austeritymeasures in some countries, and decliningremittances affected others, which alsowitnessed a return of migratory labourers.

Questions of agricultural adjustment werevery much to the fore in the developed marketeconomies, although the concerns were mainlyabout the need to restore farm incomes andthe size of farm supports, programmes andbudgets. The small, exporting countries of thisgroup found it difficult to maintain their marketshares in the face of fierce competition, and

their agricultural sectors suffered as aconsequence.

The agricultural sectors of Eastern Europe andthe USSR had some success in adapting to theharsh economic climate of the 1980s. In somecountries, the higher costs of energy andinputs, the declining willingness of states toapply large subsidies, and reduced levels ofimported inputs and supplies, had to beabsorbed. By and large, this was achieved andoutput growth accelerated.

This year's special chapter in The State ofFood and Agriculture reviews agriculturalfinancing in developing countries, identifying itsmain sources and uses, and examining anumber of issues it raises. Recent experiencesshared by many developingcountriesadjustment of their economies dueto balance of payment difficulties, theworsening external debt situation and excessivefiscal deficitshave led to a reappraisal of therole of agriculture during this period ofadjustment. The sector's contribution toexternal and domestic adjustments areexamined from the perspective of agriculture asa recipient and a generator of financialresources. This discussion also provides thebackground for a review of public and privatesources of funds for agricultural development,among other development objectives and theiruses.

In many developing countries, agriculturalfinancing is seriously constrained by budgetarydifficulties, the levelling off in the growth inflows of external assistance, a reluctance toincur further debts from additional externalborrowings if these are available and theunwillingness to raise domestic budgetarycommitments. As a consequence, only twofeasible broad lines of policy action remainopen to increase resource flows for agriculturaldevelopment.

The first approach is to promote foreigndirect investment (FDI) in the sector. Yetthis is particularly difficult for poorercountries whose structure of agriculture isunlikely to attract much foreign investment.Furthermore, such flows to agriculture havebeen relatively small in the past, except for alimited number of countries, and although FDI,strictly speaking, is not regarded as debt beingequity investment, it has costs andcommitments for the recipient country thatmust be considered.

3

4

The second approach is the adoption ofpolicies to strengthen rural financial markets, toenable them to stimulate and mobilize domesticsavings and intermediate more effectivelybetween savers and borrowers. Althoughlow-income rural people may not be able tosave much, there is evidence to show that theirpropensity to save is surprisingly high. Givenadequate financial incentives, rural savings couldattain large volumes mainly by the numbers ofrural people in most developing countries.Previous policies, based on parastatal financialinstitutions and subsidized credit programmes,have inhibited the development of ruralfinancial markets. Nevertheless, policy reformsmay not be uniformly easy to introduce, ifinterest rates are allowed to become seriouslydistorted. The path of adjustment may be adifficult one.

This brief review of sources and uses ofagricultural finance, during a period of profoundmacro-economic adjustment, shows the needfor further work and research. Concepts oftenare inconsistent and reliable data are lacking.The need for further improving availability andanalysis of data on public expenditure, as wellas on rural private savings and investment,cannot be overemphasized. The dearth ofinformation is particularly acute for componentsof public expenditure on agriculture, not onlythrough the government budget, but throughagricultural parastatals and quasi-governmentagencies. The potential for rural savings, theamounts saved, and in what form, need to bethoroughly assessed. The amount and nature ofprivate investment in agriculture need to bemore accurately quantified. Explicit taxation ofthe agricultural sector needs further study andanalysis.

PART ONEWORLD REVIEW

ECONOMIC, FINANCIAL ANDTRADE ENVIEGNMENT

OverviewEconomic and trade performances in 1985 andthe first half of 1986 present a mixed picture ofaccomplishments and uncertainties. Severalfactors, which would generally supporteconomic growth and trade expansion, tendedto consolidate: inflation receded in mostcountries, largely as a result of sharply fallingprices of oil and other commodities; nominalinterest rates fell to their lowest levels since theearly 1980s; and the US dollar depreciatedsteeply, though in a relatively orderly way.Despite such stimulus to economic activity,estimates for 1985 and the first half of 1986indicated a slowdown in growth in industrialcountries more pronounced than had beenexpected, particularly in the United States. Atthe same time, world trade stagnated,protectionist pressures intensified and manydeveloping countries, already severely burdenedby their external debt and related austeritymeasures, faced a continuing fall in the pricesof their commodity exports.

Capital-importing countries significantlyconstrained imports and improved their tradebalances from a deficit of $67 200 million in1981 to a surplus of $10 000 million in 1985,although a deficit of $6 600 million was againexpected in 1986. Despite this improvementand a restructuring of their debt, external debtremained a major obstacle to a resumption ofgrowth in many developing countries. Thedebt-service ratio of capital-importing countriesworsened in 1985 to 24%, a little higher thanthe previous peak of 1982, and was expectedto worsen further to 25.5% in 1986 (Table 1.1).

Prospects for the medium term were for aresumption of momentum in economic activityand a generally more balanced pattern ofgrowth. These expectations are uncertainhowever, as economic prospects are contingentupon such unpredictable factors as movementsin exchange and interest rates, future trends inprices of oil and other commodities, and theability by developing countries to benefit fromthe momentum of growth in industrialcountries. It is also uncertain whether privateand official creditors will adequately increasetheir lending to heavily indebted countries, soas to enable them to reabsorb their debt andresume growth, and whether governments ofmajor importing countries will succeed incontaining protectionist pressures.

The beneficial effects for agriculture of a

continued economic recovery should not beunderestimated. As shown by the experience ofrecent years, the overall economic environmentcan exert an influence on food and agriculturalproduction, trade and consumption comparableto that of policies and factors specificallyrelated to agriculture.

Progress in international economiccooperation has been uneven. Some broadareas of disagreement remain among industrialcountries on such issues as exchange andinterest rates, and the ways to tackle thecurrent account imbalances in differentcountries. In the area of international trade, amajor event was the decision to launnpch 3t5h)e.eighth round of multilateral trade negotiations(the Uruguay Round) (see Box 1.3

Output Growth and PatternsAccording to International Monetary Fund (IMF)estimates, world output of goods and servicesrose 3.1% in 1985, considerably below theexpansion of 4.4% recorded in 1984. Theslowdown was particularly pronounced inindustrial countries (3% in 1985, down from4.8% the previous year). This resulted largelyfrom a tapering off in the economic expansionof the United States, although growth was alsosmaller in Japan and Europe.

In the first half of 1986, the pace ofeconomic activity in industrial countries sloweddown substantially reflecting, among othercountry-specific factors, reduced stockbuildingand lower net exports by the United States,and the negative impact of currencyre-evaluations in Japan and the Federal Republicof Germany. Although there were signs of astrengthening in domestic demand andeconomic activity later in the year, the overallgrowth in real GDP in 1986 in industrialcountries was not expected to have reachedthe previous year's level.

Prospects for 1987 were for a modeststrengthening of economic activity in industrialcountries fostered by successful efforts ofbudgetary consolidation, declining inflation andinterest rates and improved terms of trade.These factors should more than offsetgovernment spending restraint and weak exportopportunities in developing-country markets.

Developing countries as a whole experienceda decline in output growth from slightly over4% in 1984 to 3.2% in 1985. Latin Americawas the only developing region whereeconomic growth in real terms acceleratedsignificantly in the latter year. Although some ofthe largest developing countries, namely India

7

TABLE 1.1. Annual changes in selected economic and financial indicators, 1980-86

(Percentages)

Preliminary.b Payments (interests, amortization or both) as percentage of exports of goods and services.Source: IMF, World Economic Outlook, October 1986.

Item 1980 1981 1982 1983 1984 1985 1986'

OUTPUT

Industrial countries 1.2 1.4 -0.4 2.6 4.8 3.0 2.7

Developing countries 3.5 2.2 1.6 1.4 4.1 3.2 2.7

Africa 3.7 1.8 0.8 -1.7 1.7 2.0 1.4

Asia 5.4 5.5 5.0 7.6 7.9 6.0 4.6

Near East -2.2 -1.8 -0.1 0.1 0.9 -1.2 -Latin America 5.3 0.9 - 1.0 -3.1 3.2 3.7 2.7

CONSUMER PRICES

Industrial countries 11.8 9.9 7.3 4.9 4.7 4.0 2.2

Developing countries 27.1 26.1 24.4 33.0 37.9 39.6 28.4

Africa 16.4 22.0 11.4 19.3 20.0 13.1 12.6

Asia 13.1 10.6 6.3 6.6 7.2 7.4 5.8

Near East 16.8 15.2 12.7 12.3 14.7 11.7 11.2

Latin America 54.2 59.0 66.4 102.7 123.4 145.7 86.5

EXPORT VOLUMES

Industrial countries 4.0 3.6 -2.1 2.7 9.6 4.3 3.0

Developing countries -4.1 -5.9 -8.2 3.1 6.7 0.7 5.8

Africa -0.6 -15.8 -7.5 3.1 4.8 3.7 5.0

Asia 9.0 8.2 0.8 10.8 13.8 3.8 6.9

Near East -15.2 -17.6 -19.7 -9.2 -5.4 -5.4 12.8

Latin America 1.2 6.1 -2.5 8.5 8.6 -1.7 -0.1

IMPORT VOLUMES

Industrial countries -1.7 -2.2 0.6 4.6 12.5 4.8 7.5

Developing countries 8.5 6.7 -4.1 -2.7 1.7 -1.1 -3.7Africa 8.7 10.9 -8.3 -10.3 0.2 -7.0 -9.8Asia 10.2 3.4 -0.3 8.1 5.5 5.6 1.7

Near East 9.4 16.0 5.9 -2.9 -7.0 -14.0 -18.7Latin America 9.8 2.5 -17.7 -22.3 3.0 -0.6 -

TERMS OF TRADE

Industrial countries -7.2 -2.0 1.9 1.5 0.5 0.9 8.0

Developing countries 16.8 3.0 -0.9 -3.8 1.4 -2.2 -16.3Africa 15.5 2.4 -3.2 -2.7 2.8 -1.2 -24.2Asia -1.7 -4.4 -0.7 -0.5 1.3 -1.8 -3.9Near East 41.3 13.3 2.2 -8.8 0.1 -3.6 -44.0Latin America 7.1 -4.3 -5.4 -3.0 3.5 -2.6 -12.4

DEBT-SERVICE RATIO"

Capital-importing countries 17.3 20.7 24.7 22.3 23.9 24.0 25.5Africa 13.8 15.4 20.6 23.0 25.8 28.4 33.5

Asia 8.2 9.6 11.3 10.9 11.9 12.7 13.1

Non-oil Near East 17.3 21.1 26.4 26.5 28.9 31.7 34.6

Latin America 33.7 41.2 50.6 41.9 41.1 40.3 46.0

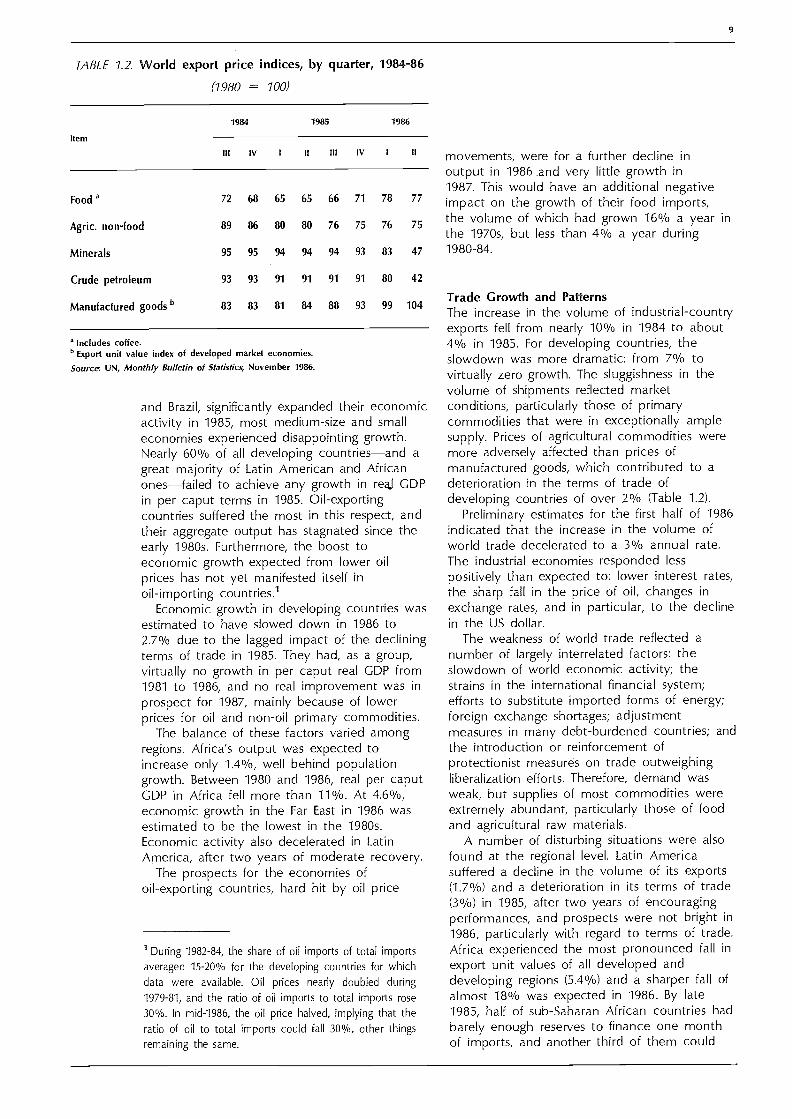

TABLE 1.2. World export price indices, by quarter, 1984-86

includes coffee.Export unit value index of developed market economies.

Source: UN, Monthly Bulletin of Statistics, November 1986.

and Brazil, significantly expanded their economicactivity in 1985, most medium-size and smalleconomies experienced disappointing growth.Nearly 60% of all developing countriesand agreat majority of Latin American and Africanonesfailed to achieve any growth in rea.1 GDPin per caput terms in 1985. Oil-exportingcountries suffered the most in this respect, andtheir aggregate output has stagnated since theearly 1980s. Furthermore, the boost toeconomic growth expected from lower oilprices has not yet manifested itself inoil-importing countries.'

Economic growth in developing countries wasestimated to have slowed down in 1986 to2.7% due to the lagged impact of the decliningterms of trade in 1985. They had, as a group,virtually no growth in per caput real GDP from1981 to 1986, and no real improvement was inprospect for 1987, mainly because of lowerprices for oil and non-oil primary commodities.

The balance of these factors varied amongregions. Africa's output was expected toincrease only 1.4%, well behind populationgrowth. Between 1980 and 1986, real per caputGDP in Africa fell more than 11%. At 4.6%,economic growth in the Far East in 1986 wasestimated to be the lowest in the 1980s.Economic activity also decelerated in LatinAmerica, after two years of moderate recovery.

The prospects for the economies ofoil-exporting countries, hard hit by oil price

1 During 1982-84, the share of oil imports of total importsaveraged 15-20% for the developing countries for whichdata were available. Oil prices nearly doubled during1979-81, and the ratio of oil imports to total imports rose30%. In mid-1986, the oil price halved, implying that theratio of oil to total imports could fall 30%, other thingsremaining the same.

movements, were for a further decline inoutput in 1986 and very little growth in1987. This would have an additional negativeimpact on the growth of their food imports,the volume of which had grown 16% a year inthe 1970s, but less than 4% a year during1980-84.

Trade Growth and PatternsThe increase in the volume of industrial-countryexports fell from nearly 10% in 1984 to about4% in 1985. For developing countries, theslowdown was more dramatic: from 7% tovirtually zero growth. The sluggishness in thevolume of shipments reflected marketconditions, particularly those of primarycommodities that were in exceptionally amplesupply. Prices of agricultural commodities weremore adversely affected than prices ofmanufactured goods, which contributed to adeterioration in the terms of trade ofdeveloping countries of over 2% (Table 1.2).

Preliminary estimates for the first half of 1986indicated that the increase in the volume ofworld trade decelerated to a 3% annual rate.The industrial economies responded lesspositively than expected to: lower interest rates,the sharp fall in the price of oil, changes inexchange rates, and in particular, to the declinein the US dollar.

The weakness of world trade reflected anumber of largely interrelated factors: theslowdown of world economic activity; thestrains in the international financial system;efforts to substitute imported forms of energy;foreign exchange shortages; adjustmentmeasures in many debt-burdened countries; andthe introduction or reinforcement ofprotectionist measures on trade outweighingliberalization efforts. Therefore, demand wasweak, but supplies of most commodities wereextremely abundant, particularly those of foodand agricultural raw materials.

A number of disturbing situations were alsofound at the regional level. Latin Americasuffered a decline in the volume of its exports(1.7%) and a deterioration in its terms of trade(3%) in 1985, after two years of encouragingperformances, and prospects were not bright in1986, particularly with regard to terms of trade.Africa experienced the most pronounced fall inexport unit values of all developed anddeveloping regions (5.4%) and a sharper fall ofalmost 18% was expected in 1986. By late1985, half of sub-Saharan African countries hadbarely enough reserves to finance one monthof imports, and another third of them could

9

(1980 = 100)

item

1984 1985 1986

III IV II III IV

Food a 72 68 65 65 66 71 78 77

Agric. non-food 89 86 80 80 76 75 76 75

Minerals 95 95 94 94 94 93 83 47

Crude petroleum 93 93 91 91 91 91 80 42

Manufactured goods b 83 83 81 84 88 93 99 104

10

only finance two months of imports. Asia alsowas affected by sluggish growth in trade, withexport volumes increasing only 3.8% in 1985,well below the average of the 1980s. Its termsof trade also deteriorated and were expected toworsen further in 1986, but export volumesshould improve.

The combination of low export earnings andhigh debt-service costs imposed severecontraints on imports. Imports declinedconsiderably in volume in all developing regionsexcept Asia, and adversely affected sectorsproducing tradable goods, particularly thosedependent on imported inputs.

Estimates for 1986 provided littleencouragement for most developing countries.According to the IMF, the continuing fall in

commodity prices was expected to cause a16% deterioration in their terms of trade, morethan offsetting a 6% expansion in exportvolumes. The resulting fall in export earningswill inevitably depress the import- anddebt-payment capacity of many developingcountries and retard their resumption ofeconomic growth. On the other hand,oil-importing countries will benefit from loweroil prices, particularly as regards their tradebalances, but also on the side of theirproduction costs. Indeed, the group of netoil-importing developing countries was expectedto reduce its deficit of current accounts, froman aggregated $21 400 million in 1985 to $12900 million in 1986.

Domestic Prices and Interest RatesA number of developments combined in 1985and 1986 to ease inflation in and narrowinflation rate differentials among industrialcountries. These developments were: the lowercost of imported oil, food and raw materials; agenerally cautious attitude of governments andcentral banks in implementing their monetaryand fiscal policies; a restrained "cost push" fromwages reflecting the persistence of highunemployment; and exchange rate factors,including the depreciation of the US dollarsince the second quarter of 1985, whichcontributed to hold down costs and pricesoutside the United States.

The result was a further decline in averageinflation rates of developed countries, from4.2% in 1984 to 3.8% in 1985. IMF forecastsyearly increases of barely over 3% in consumerprices in industrial countries for the whole of1986 and 1987, figures last seen in the 1960s.But inflationary fears remain as may bewitnessed by the rise in the price of gold and

sudden declines in stock markets that occurredin the third quarter of 1986.

For developing countries, price inflation was amajor problem during the past decade.Abatement in inflationary pressures, however,appears to have taken place in a majority ofthem since 1985. Furthermore, radicaladjustment measures taken in recent monthsby several of the countries most severelyaffected by inflation already have resulted indramatic falls in month-to-month increases indomestic prices.

For developing countries as a whole,consumer prices in 1986 were expected toincrease by about 28%, a low figure in thecontext of the 1980s. This was due mainly to asharp reduction in the inflation rate in LatinAmerica, from 146% in 1985 to 86% in 1986.

One consequence of the overall decline ininflation rates in developed countries has beena decline in nominal interest rates, althoughthey remain high by historic standards. ByNovember 1986, the average short-term interestrate in seven major industrial countries wasabout 6%, down from 8.5% in 1985, and anaverage long-term rate. of 7% compared with9.8% in 1985.

The balance among the various regions andgroupings of countries of the various factorscontributing to economic growth lead todifferent conclusions depending on theperspective taken. Low commodity prices,particularly for oil, will promote globaleconomic growth and, combined with lowerinflationary expectations, should cause nominalinterest rates to fall. Yet these same low priceswill reduce export earnings in some indebtedcountries and worsen their debt situation,despite lower interest rates.

There are two main areas of disagreementamong various observers of economic trends,which can be summarized as follows. The firstrelates to the ability of industrial countries toact as an engine of growth and pull along theeconomies of developing countries at anadequate pace. It is argued that concerns forbudgetary restraint in the industrial countrieswill not allow for sufficiently high rates ofeconomic growth, despite recent welcomemoves on their part to coordinate economicpolicies so as to remove distortions in exchangeand interest rates. Furthermore, despite movestoward negotiations aimed at achieving greatertrade liberalization, protectionist pressures seemlikely to remain a powerful force hampering theresumption of former growth rates in worldtrade. In addition, structural changes have takenplace in the demand of industrial countries for

BOX 1.1

The Chernobyl nuclearaccident

primary commodities, which further hamperexport prospects of developing countries.

Even assuming a favourable turn of events ininternational economic and trade relationships,the ability of developing countries to positivelyreact to external stimuli to growth would alsodepend on their own efforts to establish stablemonetary and fiscal policies, reduce pricedistortions and introduce more flexibility intolabour markets.

The second area of disagreement concernsthe adequacy of resource flows to restoresocially acceptable rates of economic growth indeveloping countries. Between 1981 and 1984,the capital-importing countries improved theirtrade balances mostly by reducing theirimports. Their net capital flows (net external

borrowing plus non-debt creating flows plusasset transactions) fell from $128 000 million to$49 000 million during 1981-85. Their netinvestment income turned more negative at thesame time ( $42 000 million to $60 000million). Hence, net resource transfers fellsharply from $86 000 million in 1981 to

$11 000 in 1985. Therefore, although thesecountries had a trade surplus and were stillmajor importers of capital, they suffered a netoutflow of resources in 1985. The argument isfor an increase in resource flows tocapital-importing countries to enable them toresume growth.

A number of recent initiatives andsuggestions centre on this argument. InSeptember 1985, an initiative was announced

This accident, which took place on26 April 1986 and releasedsignificant quantities of radioactiveisotopes into the atmosphere,underlined the susceptibility ofagriculture to disasters of this kind.

Although the reactor damagedby the accident is located in theUkraine, which accounts for about20% of the USSR's output ofcereals, the area of worstcontamination was limited to aradius of approximately 30 kmaround the reactor. The impact oncereal production may, therefore,be relatively limited. Nevertheless,winds spread the radioactivitywidely throughout Eastern andWestern Europe and into parts ofAsia. The resulting contaminationof fruit, vegetable and livestockproducts caused serious disruptionsto domestic and internationaltrade. A ban was imposed by theEEC until the end of May 1986 onimports of these products fromareas within a radius of 1 000 kmof Chernobyl.

The long-term environmentalimpact of this accident cannot yetbe assessed. However, it hasshown a clear need forinternational action that will leadto acceptable limits forradionuclide contamination offoods, since such limits did notexist at the time of the accident.

Activities leading torecommended international limitswould involve the CodexAlimentarius and the jointFAO/International Atomic EnergyAgency (IAEA) Division.' As a firststep, FAO convened an expertconsultation, held 1-5 December1986, that recommendedinternational limits for radionuclidecontamination in all foods. Theselimits will be widely publicized andwill be submitted also to theCodex Alimentarius Commission forconsideration. Uniform adoptionand application of these limits byregulatory authorities will preventtrade disruptions such as occurredafter the Chernobyl accident.

1 Of Isotope and Radiation Applications of

Atomic Energy for Food and Agricultural

Development (AGE).

11

12

(the Baker Plan) to form a partnership amongdebtor countries, multilateral agencies andcommercial banks to lend $29 000 million tothe 15 most heavily indebted countries-overthree years, subject to some policy changes inthe indebted countries. Other recentsuggestions, which encompass both the needfor new lending and some form of debt releasefor debtor countries, hinge on the activeparticipation of commercial banks. A suggestionof particular interest made in July was for thecreation of special financing facilities fromrecycled Japanese and northern Europeancurrent-account surpluses in favour of thedebtor countries.

The case for Africa, specifically for agricultureand for sectors directly supporting agriculture,was presented to the UN General AssemblySpecial Session on Africa's Economic and SocialCrisis, in May 1986 (see Regional Reviewchapter on Africa).

The difficulties that some of these recentinitiatives encountered to overcome the debtproblems were clearly linked to thedeterioration in the debt-export earnings ratioand the severity of adjustment programmesinvolved. The July 1986 agreement betweenMexico and the IMF provided, however, anexample of how flexibility could be introducedinto adjustment measures that take account ofspecific needs and circumstances of a debtorcountry.

WORLD FOOD ANDAGRICULTURAL SITUATION ANDPROSPECTS

Food and Agricultural Production 2World agricultural production increased 1.3% in1986 as a net result of 2% growth in food and7.3% decline in non-food production (Table 1.3).The latter was the most significant decline since1970.

These results showed a fall back in overallagricultural performances if compared with 1985or indeed the average for 1980-86. Theyconcealed, however, substantial variationsamong regions and country groups.

Food output growth in developing countriesin 1986 was at a similar rate as that of 1980-86(3.7% and 3.5% a year respectively). Growth inAfrica (3.1%) was substantially lower than in1985, when a 7% increase was achieved; itwas, however, above the average growth ratefor 1980-86. Food output in the Far Eastmarginally increased and the growth was belowthe average for the 1980s. Also, in LatinAmerica the rise was limited in 1986 to 0.4%,thus much less than the 2.2% a year for1980-86, which was just below the populationgrowth rate of around 2.3% a year. Theincrease in food output in the Near East was5.8%, following the 5.1% increase in 1985. Thepace of food output growth in the Asiancentrally planned economies (AGPE)mainlyChina which slowed in 1985, accelerated againin 1986, to 6.6%.

In the developed countries, 1986 food outputbarely changed as a net result of a 1.6% fall inthe countries with market economies and a4.3% increase in East European countries andthe USSR. Output of the 12-member countriesof the European Economic Community (EEC) didnot change as a group.

In developing countries, growth in output ofnon-food products, which are major sources ofincome and foreign exchange, fell in 1986 by7.6%. Output of the main non-foodcommodities such as cotton, tobacco, coffeeand tea declined (Table 1.4).

As regards changes in food production at theindividual country level, 1986 was on the whole

fdvoui able yea'. Out of 97 developingcountries, 40, mostly in Asia and Africa,increased their food output in per caput terms.

This general review is complemented by a more detaileddiscussion in the Regional Review.

Item

TABLE 1.3. Food and non-food production, 1984-86

Index Annuale

(1979-81=100)Chang

ratesof change

1984 1985 1986 1984-85 1985-86 1980-86(%) (8ó)

Source: FAO, Statistics Division.

13

FOOD PRODUCTION

Developing market economies 111 115 118 3.6 2.4 2.7

Africa 104 112 115 6.9 3.1 2.1

Far East 116 119 122 2.4 2.7 3.5

Latin America 109 113 114 3.4 0.4 2.2

Near East 106 111 118 5.1 5.8 2.1

Asian centrally planned economies 125 126 135 0.8 6.6 5.4

Total developing countries 115 119 123 2.7 3.7 3.5

Developed market economies 106 107 105 1.1 -1.6 1.1

North America 103 108 104 5.6 -3.5 1.0

Oceania 105 107 105 1.0 -1.5 2.0

Western Europe 110 107 107 -3.4 0.2 1.1

Eastern Europe and the USSR 110 110 115 -0.1 4.3 2.6

Total developed countries 107 108 108 0.8 0.1 1.5

WORLD 111 113 115 1.8 2.0 2.5

NON-FOOD PRODUCTION

Developing market economies 105 115 105 9.6 -9.1 1.9

Africa 110 123 125 12.1 2.0 3.9

Far East 109 120 110 10.1 -8.0 2.7

Latin America 99 110 92 10.8 -16.9 0.3

Near East 107 108 106 0.9 -1.8 1.4

Asian centrally planned economies 178 153 148 -14.1 -3.6 7.6

Total developing countries 121 124 114 1.8 -7.6 3.3

Developed market economies 100 105 92 4.6 -11.5 -0.1

North America 95 96 75 0.6 -22.0 -2.6

Oceanía 106 119 118 12.8 -0.9 2.8

Western Europe 116 124 121 6.7 -2.0 4.0

Eastern Europe and USSR 98 103 104 5.0 0.9 0.2

Total developed countries 99 104 97 4.8 -6.8

WORLD 114 117 108 2.7 -7.3 2.2

Pre

limin

ary.

Incl

udin

g ric

e as

pad

dy.

'Tot

al h

arve

sted

pro

duct

ion.

Sou

rce.

FA

O, S

tatis

tics

Div

isio

n.

TA

BLE

1.4

. Agr

icui

tUra

l pro

duct

ion,

by

com

mod

ity, 1

985-

86

Item

1985

(Mill

ion

tons

)

1986

'

Cha

nge

1985 to 1986

(%)

1985

1986

'

(Mill

ion

tons

)

Cha

nge

1985 to

1986

(96)

1985

1986

'

(Mill

ion

tons

)

Cha

nge

1985 to

1986

(%)

Tot

al c

erea

ls b

918.

690

7.1

-1.3

925.

095

3.0

3.0

1 84

3.6

1 86

0.0

0.9

Whe

at30

1.8

308.

22.

120

3.6

216.

36.

250

5.4

524.

53.

8

Ric

e26

.325

.9-1

.544

6.4

454.

21.

847

2.7

480.

21.

6

Coa

rse

grai

ns59

0.5

572.

9-3

.027

5.0

282.

42.

786

5.5

855.

4-

1.2

Roo

t cro

ps21

5.8

212.

4-1

.636

9.3

373.

51.

158

5.1

585.

901

Pul

ses

17.1

18.5

8.2

34.3

35.9

4.5

51.4

54.4

5.8

Oil-

bear

ing

crop

s

Oil

cont

ent

24.1

23.4

-3.0

40.6

42.6

4.8

64.7

66.0

1.9

01/c

ake

cont

ent

67.5

65.2

-3.3

67.7

65.7

-2.8

135.

113

1.0

-3.1

Sug

ar, c

entr

ifuga

l (ra

w)

41.9

41.0

-2.1

79.6

81.5

2.3

121.

512

2.5

0.8

Coc

oa b

eans

--

-2.

02.

02.

02.

0

Cof

fee

--

-6.

05.

2-1

3.8

6.0

5.2

-13.

8T

ea0.

30.

3-4

.02.

12.

0-1

.72.

32.

3-1

.1

Cot

ton

lint

6.2

5.4

-12.

511

.010

.2-7

.317

.215

.7-9

.2T

obac

co2.

12.

0-6

.84.

44.

3-2

.66.

66.

3-4

.0

Tot

al m

eat

95.3

97.0

1.8

54.8

57.9

5.7

150.

115

4.9

3.2

Tot

al m

ilk38

6.2

391.

21.

312

5.1

128.

12.

451

1.3

519.

31.

6

Hen

egg

s18

.819

.11.

411

.812

.34.

730

.631

.42.

7

Dev

elop

ed c

ount

ries

Dev

elop

ing

coun

trie

sW

orld

Percentagerate of change

5.01 to 10.00

3.01 to 5.00

1.01 to 3.00

2.01 to 1.00

0.01 to 1.00

1.00 to 3.00

3.01 to 5.00

5.01 to 10.00

Source: FAO, Policy Analysis Division.

TABLE 1.5. Percentage rate of change in per caput food production, 1985-86

Developing countries

Chile, Syrian Arab Republic, Yemen Arab Republic,

Mauritania, Mali, Guinea-Bissau, Mauritius, Malaysia,

Lebanon, China

The Sudan, Swaziland, Burundi, Ghana, Chad

Turkey, Burkina Faso, Pakistan, Burma, Jordan, India,

Indonesia, Haiti

Colombia, Egypt, Republic of Korea, Argentina, Rwanda,

Ethiopia, Gabon, Jamaica, Cameroon, Philippines, Trinidad

and Tobago, Uruguay, Bhutan

Kuwait, Oman, United Arab Emirates, Kenya,

Mozambique, Nepal, Brunei, Islamic Republic of Iran,

Singapore, Guatemala, United Republic of Tanzania,

Somalia, Congo, Cyprus, Zaire

Sierra Leone, Bangladesh, Panama, Namibia, Madagascar,

Venezuela, Botswana, Papua New Guinea, Costa Rica,

Zambia, Zimbabwe, Mexico, Malawi, Honduras, Nigeria,

Brazil, Central African Republic, Angola, DominicanRepublic, Benin, Nicaragua

Developed countries

Yugoslavia, Canada, Bulgaria

USSR, Poland, Federal Republic of Germany

German Democratic Republic, Spain

The Netherlands, Denmark

United Kingdom, Romania, Japan,

Switzerland, Norway

Italy, Finland, Australia, Belgium,

Luxembourg, France, Iceland, Ireland

Peru, Guinea, Ecuador, Niger, Democratic Yemen, Cuba, Greece, Austria, Czechoslovakia, HungarySri Lanka

El Salvador, Thailand, Togo, Côte d'Ivoire, Algeria, United States, South Africa, New Zealand,Paraguay, Afghanistan, Bolivia, Guyana, Lesotho, Liberia Sweden

Below 10.00 Tunisia, the Gambia, Senegal, Libyan Arab Jamahiriya Israel

This group, which includes such heavilypopulated countries as China, India, Pakistan,Indonesia and Egypt, accounts for a majorshare of the total population of developingcountries (Table 1.5). By comparison, only 33countries achieved gains in per caput foodproduction on an average annual basis during1980-85.

An opposite trend was found in industrialcountries: during 1980-85, per caput foodoutput expanded in all but four of them,namely South Africa, Iceland, Greece andYugoslavia. Several of the major food producingand exporting countries experienced substantialincreases, in the average range of 1.50/0 to4.8% a year, during this period. These included

Denmark, Australia, Japan, Federal Republic ofGermany, the United Kingdom, and most EastEuropean countries. In 1986, however, theirfood production growth slowed. In onlyone-third of all developed countries did outputgrowth still exceed population increase.

Such opposing broad trends in developedand developing countries were, paradoxically,equally welcome. In developing countries,higher food production growth in 1986contributed to alleviate food shortages andoverall economic conditions in many criticalareas, particularly in Africa. On the other hand,the slowdown in food output growth was apositive development for many industrialcountries, in the context of the complex

15

More than 10.00 Uganda, Kingdom of Saudi Arabia, Iraq, Morocco

16

Item

Source: FAO, Land and Water Development Division.

TABLE 1.6. Fertilizer consumption, by major nutrients, 1982-85

1982/83

Consumption

1983/84

(Million tons)

problem of their growing food surpluses. Asreviewed in the Regional Review chapter of thisdocument, however, the problem of foodsurpluses also emerged, or became more acute,in some developing countries facing the viciouscircle of limited domestic absorption capacity inmarket conditions, insufficient storage andmarketing facilities, and difficult access tointernational markets.

The Outlook for CerealsThe world cereal situation in 1986/87 was notexpected to change substantially from recentyears: supply surpluses had led to new recordlevels of stocks, and imports and pricesremained depressed.

World cereal harvests increased slightly in1986, mainly because of reduced harvests ofrice and coarse grains in developed countries(down 1.5% and 3% respectively) and a rise inall cereals in developing countries, whereproduction of wheat expanded by more than6%.

1984/851982/83

to1983/84

Change

(%)

1983/84to

1984/85

Annual rateof change

1980/81to

1984/85(%)