the state of pay in online travel - cybersource · the state of pay in online travel. ......

TRANSCRIPT

MARKET RESEARCH • INDUSTRY INTELLIGENCE

PhoCusWright

PhoCusWright White Paper

Written and researched by

Mike Gerra, Maggie Rauch,

Deepak Jain, Chetan Kapoor,

Bing Liu and Douglas Quinby

Sponsored by

The State of Pay in Online Travel

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved.Page 2

This PhoCusWright White Paper is made possible by CyberSource®

CyberSource, a Visa company

CyberSource simplifies payment and fraud management for the travel industry. As a world leader in payment management, CyberSource extends multi-channel pay-ment management services to over 400,000 merchants across the globe, ranging from leading travel suppliers to small businesses. Approximately 1 out of every 7 dollars spent online worldwide are managed by CyberSource. Services include: fraud management, secure global payment acceptance services across mobile, web, call center, and kiosk sales channels and professional services.

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved. Page 3

About PhoCusWrightPhoCusWright is the travel industry research authority on how travelers, suppliers and intermediaries connect. Independent, rigorous and unbiased, PhoCusWright fosters smart strategic planning, tactical decision-making and organizational effectiveness.

PhoCusWright delivers qualitative and quantitative research on the evolving dynamics that influence travel, tourism and hospitality distribution. Our marketplace intelligence is the industry standard for segmentation, sizing, forecasting, trends, analysis and consumer travel planning behavior. Every day around the world, senior executives, marketers, strategists and research professionals from all segments of the industry value chain use PhoCusWright research for competitive advantage.

To complement its primary research in North and Latin America, Europe and Asia, PhoCusWright produces several high-profile conferences in the United States and Germany, and partners with conferences in China and Singapore. Industry leaders and company analysts bring this intelligence to life by debating issues, sharing ideas and defining the ever-evolving reality of travel commerce.

The company is headquartered in the United States with Asia Pacific opera-tions based in India and local analysts on five continents.

PhoCusWright is a wholly owned subsidiary of Northstar Travel Media, LLC.

PhoCusWright Inc.116 West 32nd Street, 14th FloorNew York, NY 10001

PO Box 760 Sherman, CT 06784

+1 860 350-4084+1 860 354-3112 fax

www.phocuswright.com

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved.Page 4

JANUARY 2013

Table of ContentsIntroduction 5

Background and Methodology 6

The State of Pay 7

Current Conventional Payment Acceptance 7

Future Alternative Forms of Payment Acceptance 7

Credit Card is King 8

Alternative Forms of Payment 9

Mobile Payments 10

Payment Priorities: Travel’s Key Challenges 11

Credit Card Fraud 11

Money vs. Mobile 13

Summary and Recommendations 14

Table of ChartsFigure 1 6 Respondents by Region

Figure 2 7 Distribution of Respondents by Functional Area

Figure 3 8 Supported Payment Methods and Future Plans

Figure 4 9 Payment Methods Use in Website Bookings by Region

Figure 5 9 Global Average (Mean) of Alternative Online Forms of Payment as a Percentage of all Website Gross Bookings

Figure 6 10 Online Leisure/Unmanaged Business Travel Penetration of the Total Travel Market by Region, 2012

Figure 7 12 Payment-Related Challenges for OTAs, Airlines and Lodging Suppliers

Figure 8 12 Average Fraud Rate as a Percentage of Bookings on their own Websites in 2012, by Industry Sector

Figure 9 13 Typical Payment Methods Used for Mobile Bookings, Suppliers and Retailers

Contents

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved. Page 5

The State of Pay in Online Travel

Written and researched by Mike Gerra, Maggie Rauch,Deepak Jain, Chetan Kapoor, Bing Liu and Douglas Quinby

IntroductionThe travel service marketplace has seen tremendous change and upheaval over the last decade. Some change has been evolutionary, such as the continued consoli-dation of major and national airlines, and the mainstream emergence of low-cost, low-frills carriers. Other change has been more revolutionary, fueling new industry markets, new travel suppliers and distribution partners and an array of new pro-cesses, disruptive business models, cool products and sticky customer services. A few examples here include Google Maps, GPS navigation services, TripAdvisor and traveler reviews, and alternative accommodation marketplaces such as HomeAway and Airbnb.

We see three key underlying factors driving this significant change: first, the rap-id rise of global markets and the increasing pace of globalization; second, the increased market penetration and in some regions dominance of e-commerce; third, the swift adoption of mobile tools and services covering all links of the travel distribution chain.

The most significant change is occurring in the dynamic online travel marketplace, where companies can test, launch, expand or sunset ideas, models, products and technologies much more rapidly than ever before. We have already seen significant change in such areas as distribution, merchandising, and pricing. Suppliers are dis-tributing products in new ways; intermediaries are packaging and selling products via new business models; and consumers are shopping, purchasing and paying for services through new tools, such as smartphones. And the market is not standing still. With competition as fierce as ever, suppliers and retailers continue to investi-gate and pursue any viable strategy through which they can claim a market advan-tage, an improved margin, or both.

One such area is payments processing. Once a sleepy back-office process, pay-ments is gaining prominence in the increasingly competitive battle among sup-pliers, retailers and other intermediaries. New and emerging alternative forms of

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved.Page 6

payment offer the promise of lower costs and improved customer experience. But the rapid expansion of online travel globally also brings new payment challenges, such as the need to support more payment methods and processes, as well as the increased risk of fraud.

This white paper examines the travel payment processing area in the context of globalization, e-commerce and mobile services. It identifies the key challenges and concerns for travel suppliers and retailers, especially in the area of payment fraud. This paper also reviews the state of mobile payments and the concerns and oppor-tunities this still-nascent technology presents.

Background and MethodologyThis analysis focuses on online payments across airlines, lodging and travel interme-diaries based upon research conducted for PhoCusWright’s Payment Unsettled: Cost, Opportunity and Disruption in Travel’s Complex Payment Landscape. A central compo-nent of this study was a quantitative travel industry survey fielded through the following organizations: African Business Travel Association (ABTA), Association of Corporate Travel Executives (ACTE), Hotel Electronic Distribution Network Association (HEDNA), International Air Transport Association (IATA), Tnooz, Travel Trade Gazette (TTG) and Web in Travel (WIT).

The survey yielded over 1,500 qualified industry responses covering airlines, lodging suppliers and intermediaries, between November 2012 and January 2013 (see Figure 1). Of the total respondents there were 323 travel suppliers and 733 travel retailers,

including 174 airlines, 102 lodging suppliers and 111 online travel agencies (OTAs). All major global regions are represented with suf-ficient sample for segmentation. This included 22% from Western Europe, 13% from North America and 10% based in Asia.

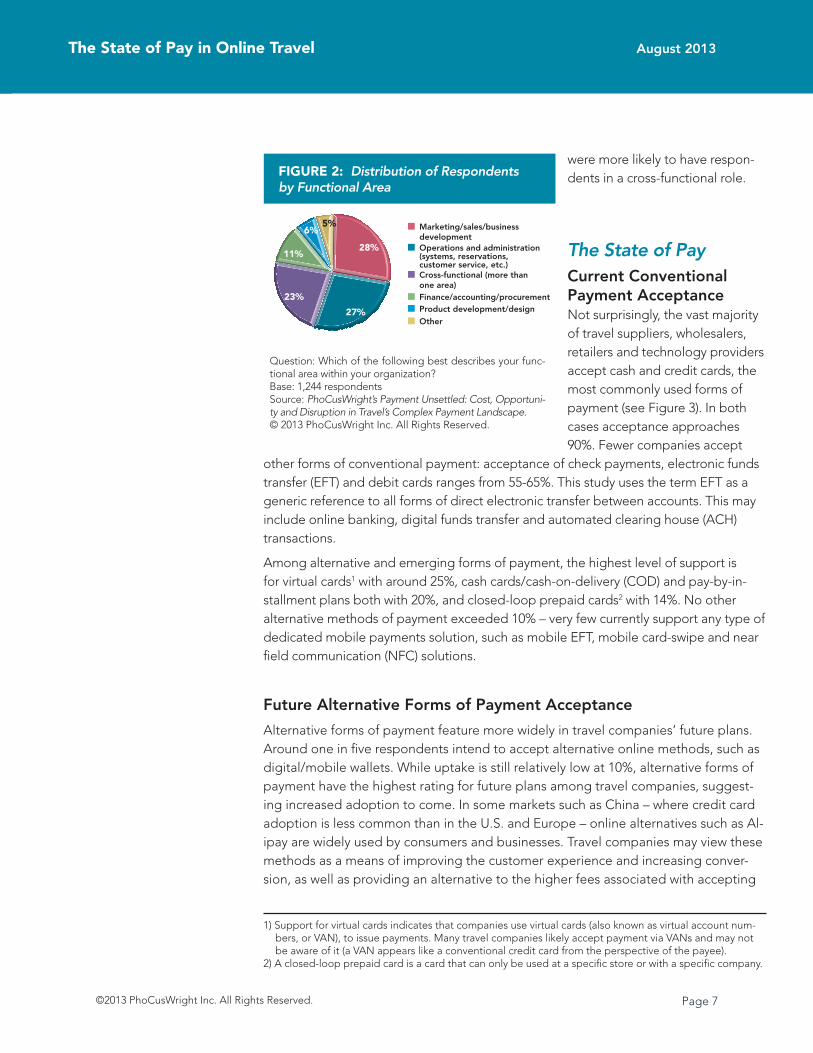

Survey respondents reflect a range of functional areas within their organizations (see Figure 2). More than one in four was in a marketing and sales role or in an operational or administration function, and 23% in a cross-func-tional position (covering more than one business area). Travel retailers and smaller companies

FIGURE 1: Respondents by Region

Question: Which of the following best describes your company? Base: 1,434 respondentsNote: *Global – operational in three or more regions and in-cludes some overlap, so the pie exceeds 100%.Source: PhoCusWright’s Payment Unsettled: Cost, Opportunity and Disruption in Travel’s Complex Payment Landscape.© 2013 PhoCusWright Inc. All Rights Reserved.

Western EuropeNorth AmericaEastern EuropeMiddle EastAsiaCentral &South AmericaAfricaAustralia/New ZealandCaribbeanGlobal*

22%

13%

11%

11%10%

10%

1%

9%

5%

13%

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved. Page 7

were more likely to have respon-dents in a cross-functional role.

The State of PayCurrent Conventional Payment AcceptanceNot surprisingly, the vast majority of travel suppliers, wholesalers, retailers and technology providers accept cash and credit cards, the most commonly used forms of payment (see Figure 3). In both cases acceptance approaches 90%. Fewer companies accept

other forms of conventional payment: acceptance of check payments, electronic funds transfer (EFT) and debit cards ranges from 55-65%. This study uses the term EFT as a generic reference to all forms of direct electronic transfer between accounts. This may include online banking, digital funds transfer and automated clearing house (ACH) transactions.

Among alternative and emerging forms of payment, the highest level of support is for virtual cards1 with around 25%, cash cards/cash-on-delivery (COD) and pay-by-in-stallment plans both with 20%, and closed-loop prepaid cards2 with 14%. No other alternative methods of payment exceeded 10% – very few currently support any type of dedicated mobile payments solution, such as mobile EFT, mobile card-swipe and near field communication (NFC) solutions.

Future Alternative Forms of Payment Acceptance

Alternative forms of payment feature more widely in travel companies’ future plans. Around one in five respondents intend to accept alternative online methods, such as digital/mobile wallets. While uptake is still relatively low at 10%, alternative forms of payment have the highest rating for future plans among travel companies, suggest-ing increased adoption to come. In some markets such as China – where credit card adoption is less common than in the U.S. and Europe – online alternatives such as Al-ipay are widely used by consumers and businesses. Travel companies may view these methods as a means of improving the customer experience and increasing conver-sion, as well as providing an alternative to the higher fees associated with accepting

FIGURE 2: Distribution of Respondents by Functional Area

Question: Which of the following best describes your func-tional area within your organization? Base: 1,244 respondentsSource: PhoCusWright’s Payment Unsettled: Cost, Opportuni-ty and Disruption in Travel’s Complex Payment Landscape.© 2013 PhoCusWright Inc. All Rights Reserved.

Marketing/sales/business developmentOperations and administration(systems, reservations, customer service, etc.)Cross-functional (more than one area)Finance/accounting/procurementProduct development/designOther

28%

27%

23%

11%

6%5%

1) Support for virtual cards indicates that companies use virtual cards (also known as virtual account num-bers, or VAN), to issue payments. Many travel companies likely accept payment via VANs and may not be aware of it (a VAN appears like a conventional credit card from the perspective of the payee).

2) A closed-loop prepaid card is a card that can only be used at a specific store or with a specific company.

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved.Page 8

credit cards online. However, it remains unclear to what extent this intent will trans-late into more payment transactions, especially in markets where customers’ payment behavior is entrenched and incented, such as for rewards-driven credit cards in the U.S. For years, airlines in the U.S. have offered several alternative forms of payment, such as PayPal, Bill Me Later, Western Union and EFT, but with little uptake.

Approximately 10% of respondents plan to support virtual cards, cash cards, pay-by-installment and prepaid cards. A similar number have future plans to accept payment via mobile payment methods, including EFT, mobile card-swipe and mobile NFC. A substantial majority of respondents either have no future plans to support any of the listed alternative forms of payment, or they are not aware of their compa-nies’ future plans.

Credit Card is King

Support of payment methods as presented in Figure 3 only indicates whether or not a company has the capability to accept and/or issue payments by that method; it does not show many significant differences on a regional or even an industry seg-ment basis. On a transaction volume basis for travel websites, however, the mix of payment methods used varies widely by region. Although generally the more widely accepted forms of payment – cards, cash and EFT – are most commonly used, there are some notable regional variations.

Question: Please indicate whether your organization currently supports or plans to support the following payment methods for travel bookings?Base: 1,244 respondentsSource: PhoCusWright’s Payment Unsettled: Cost, Opportunity and Disruption in Travel’s Complex Payment Landscape.© 2013 PhoCusWright Inc. All Rights Reserved.

FIGURE 3: Supported Payment Methods and Future Plans

Already supported Not yet but planning to Not yet; no plans to Do not know/not aware of

Cash

Credit cards

Debit cards

Virtual cards

Closed prepaid cards

Alternative online methods

Mobile payment EFT services

Dedicated terminal payments

Mobile card-swipe services

NFC-based mobile payment solutions

Pay-by-installment plans

Cash cards/cash-on-delivery (COD)

Check

Electronic funds transfer

Con

vent

iona

lEm

ergi

ng/A

ltern

ativ

e

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved. Page 9

Globally, credit cards are the dominant form of payment across all regions. Cards as a percentage of total website bookings range from a high of 82% in North America to a low of 34% in the Middle East and Africa (MEA). Regions with high levels of credit card payments, such as North America and Australia/New Zealand, have a much low-er share of website bookings using EFT and alternative forms of payment. Converse-ly, Asia and Latin America have a higher percentage of transactions from alternative forms of payment (see Figure 4).

Middle East/Africa, Eastern Europe and Latin America have the highest rates of payment via check and cash, with MEA leading the pack with a 30% share of website gross travel bookings. Western Europe leads with 15% share of bookings via debit card. Eastern Europe leads with a 30% share of transactions with EFT, followed by MEA at 24%.

Alternative Forms of Payment

From a global perspective, alter-native forms of payment rep-resent a small share of average gross website bookings. Online travel agencies (OTAs) lead the way with a 6% rate, followed by lodging suppliers at 2.7% (see Figure 5).

FIGURE 5: Global Average (Mean) of Alternative Online Forms of Payment as a Percentage of All Website Gross Bookings

Base: 174 airlines, 102 lodging suppliers and 111 OTAsSource: PhoCusWright’s Payment Unsettled: Cost, Opportunity and Disruption in Travel’s Complex Payment Landscape.© 2013 PhoCusWright Inc. All Rights Reserved.

Airlines OTAsLoadingSuppliers

1.9% 2.7% 6%

Question: Please estimate the percentage of your website gross travel bookings that are paid for via the following payment methods. Base: 198 travel suppliers, 348 retailers and 93 wholesalersSource: PhoCusWright’s Payment Unsettled: Cost, Opportunity and Disruption in Travel’s Complex Payment Landscape.© 2013 PhoCusWright Inc. All Rights Reserved.

FIGURE 4: Payment Methods Used in Website Bookings by Region

Credit cards Cash or check Debit card EFT Alternativeonline method

0%

10%

20%

30%

40%

50%

60%

70%

80%

90% North America ANZ Asia LATAM Western Europe Eastern Europe MEA

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved.Page 10

Alternative forms of payment have a generally low level of penetration in all sectors of the industry and across all regions. However, those companies with the most on-line sales show the highest future intent to implement alternative payment methods. But travel companies face some key challenges, such as lack of customer demand and technical implementation issues. On the airline side, 37% that report having no plan to implement alternative forms of online payment cite a lack of customer de-mand. Lodging suppliers, meanwhile, are more concerned about the technical issues of implementing alternative forms of payment into their e-commerce properties, and the challenges around integrating these into their existing accounting and financial reporting processes.

Online Travel Payments

Most travel companies worldwide support conventional payment methods, but the actual volume of travel bookings transacted through these methods can vary significantly by region. This regional variation is broadly in line with the general maturity of online markets, as well as overall consumer adoption of credit cards and other forms of electron-ic and cashless payment. In fact, credit card adoption is often cited as a precondition to a robust e-commerce environment.

North America has a higher level of credit card adoption, and is also home to the most mature e-commerce and online travel landscapes. Conversely, card use is significantly lower among consumers in MEA, Latin America and Eastern Europe, and the online travel markets in those regions remain at significantly earlier stages in their development.

Western Europe has a generally higher rate of debit card transac-tions; consumers have taken to debit cards as a logical extension of checks and cash, more so than in other regions. These regional differences are magnified online, where the penetration of Inter-net-based e-commerce is much more prevalent in North America and Europe. Online travel in North America has a 42% share of the total travel market; Europe is not far behind with an online share of 41% (see Figure 6).

Mobile Payments

As more and more transactions occur via a mobile device, the ability to pay easily and efficiently via a smartphone has become a major topic of interest across a range of in-

FIGURE 6: Online Leisure/Unmanaged Business Travel Penetration of the Total Travel Market by Region, 2012

Source: PhoCusWright Inc.© 2013 PhoCusWright Inc. All Rights Reserved.

U.S.

42% 41%

24% 21% 19%

Europe APAC LatinAmerica

EasternEurope

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved. Page 11

dustries, including travel. In this study, PhoCusWright examined travel industry support and attitudes around those methods that could only be implemented on a mobile plat-form, such as a smartphone or tablet. This includes mobile account-to-account or EFT solutions (e.g. M-Pesa), mobile card-swipe systems (e.g., GoPayment, Square) and any close-proximity contactless payment solutions such as systems using near-field commu-nications (NFC), like Visa payWave.

While these services are gaining attention, mobile payments are still very much in their infancy across the travel industry. The incidence of survey respondents indicating current support for any of these forms of payment is negligible, with 3% or less of re-spondents saying they support any of those methods (see Figure 3). There is, however, some measurable uptake in Africa (where M-Pesa is based) and Asia, but even here the percentage supporting mobile payments remains in the low single digits.

Payment Priorities: Travel’s Key ChallengesAmid the rapid changes in travel distribution and new developments in payment methods and technologies, travel companies harbor a range of concerns around han-dling payment. The foremost travel industry concerns around payments are credit card fraud, credit card fees and chargebacks. With the predominant use of credit cards and broad industry efforts to reduce payment processing costs and foster consumer use of alternative forms of online payment, one might expect to see credit card merchant fees as the most common concern among travel companies. However, businesses did not rank this highest. It is credit card fraud that emerged as the most widely held con-cern; 37% of all travel companies cited credit card fraud as a key payments concern. Not surprisingly, finance and accounting staff are more concerned about credit card fraud than other groups within the same organization.

There are, however, significant differences across key industry sectors. Card fraud is of greatest concern for companies with the strongest online presence – OTAs, airlines and larger firms ($100 million or more in gross travel bookings). Nearly half of OTAs and two in five airlines cited concern over credit card fees (see Figure 7). Generally, lodging suppliers are more concerned than OTAs and airlines over a broader range of issues, including: supporting new mobile methods of payment, currency manage-ment, invoice reconciliation, managing multiple payment service providers (PSP), supporting new card payment standards and PCI (payment card industry) compliance.

Credit Card Fraud

Credit card fraud is the most widely held payment concern among travel companies, and it’s not hard to see why. E-commerce as an industry averaged a 0.9% rate of fraud on online revenue, amounting to $3.5 billion in lost revenue in North America in 2012.3

3) CyberSource: 2013 Online Fraud Report, 14th Edition

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved.Page 12

The online revenue fraud rate for travel companies globally is slightly lower at 0.8%. However, this includes a long tail of traditional travel agencies and travel management companies (TMCs), many of which do little or no online selling.

Travel firms that sell more online generally have a broader fraud exposure. OTAs have the highest rate of fraud at 1.2%, followed by airlines and lodging suppliers, each with a fraud rate of 1.1% of website bookings. Tra-ditional travel agencies and TMCs have a smaller online footprint and thus fraud rates of 0.5%, well below the global average (see Figure 8). Travel companies in emerging market regions where credit card markets are less mature and consumer adoption lower, are all more likely to cite credit card fraud as a problem. Respondents from Latin America, Eastern Europe and MEA were significantly more likely to report fraud as a key concern.

Question: Which of the following would you consider to be major challenges with regard to managing payments for your organization? Select all that apply. Base: 111 OTAs, 174 airlines and 102 lodging suppliersSource: PhoCusWright’s Payment Unsettled: Cost, Opportunity and Disruption in Travel’s Complex Payment Landscape.© 2013 PhoCusWright Inc. All Rights Reserved.

FIGURE 7: Payment-Related Challenges for OTAs, Airlines and Lodging Suppliers

OTAsAirlinesLodging

Credit card fraud

Credit card fees for card not present

Chargebacks

Supporting new mobile payment methods

Currency conversion and management

Processing manual payments

Reconciling payments with invoices

Credit card fees for card present

Length of time between payment and invoicing

Managing multiple PSPs

Takes too long for payments to be settled

Tracking taxes and fees

Supporting new card payment standards

PCI compliance

FIGURE 8: Average Fraud Rate as a Percentage of Bookings on Their Own Websites in 2012, by Industry Sector

Question: What percentage of your company’s website bookings were fraudulent in 2012? (Please consider only chargebacks or cancelled payments as a result of fraud, and not all chargebacks.)Base: 651 respondentsSource: PhoCusWright’s Payment Unsettled: Cost, Opportu-nity and Disruption in Travel’s Complex Payment Landscape© 2013 PhoCusWright Inc. All Rights Reserved.

Total Airlines Lodging OtherTravelerSupplies

OTAs TMCsTravelAgencies

0.8%

0.5% 0.5%

1.1% 1.1% 1.1%1.2%

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved.Page 13

Money vs. Mobile

Mobile is one of the most widely cited payment concerns for travel companies after card fraud. Significantly, more lodging suppliers are concerned about supporting new mobile methods of payment than any other payment-related concern, and this may be because of hotels’ much higher exposure to in-person retail purchases than airlines or online travel agencies. While most airline tickets and travel purchases via OTAs are purchased in advance and online, hotels play home and host to their guests and offer a range of retail and on-property purchasing opportunities for their guests. As travel-ers become more accustomed to paying for common retail purchases via their mobile devices, hotels may be signaling their concern about being able to meet this future customer expectation.

Airlines and OTAs also report mobile payment as a key concern. But this is despite the fact that use and uptake of mobile payment methods are currently non-existent. Travel companies see the writing on the wall – consumers are flocking to mobile devices, and e-commerce via mobile devices is gaining traction. As a result, compa-nies have a widespread concern and high level of interest in learning about mobile payment methods.

Mobile is quickly become an enormous transactional platform in travel. Mobile travel bookings will reach $22 billion by 2014, accounting for 16% of the overall U.S. online trav-

el market.4 However, the current payment methods used for mobile bookings are generally a transplant of existing, traditional online pay-ment solutions. In most cases, mo-bile payments are transacted using a method ported from a website to the mobile platform, such as a stored credit card via an existing account. Thus, travel suppliers and retailers show credit cards as the top mobile payment method by far, at 89% and 88%, respectively. The next most frequently report-ed methods are debit cards, and cash or check. Alternative payment methods for mobile platforms show little penetration, with travel retailers reporting 14% and travel suppliers 8% of mobile bookings (see Figure 9).

FIGURE 9: Typical Payment Methods Used for Mobile Bookings, Suppliers and Retailers

Question: Which of the following payment methods do you offer through mobile devices? Select all that apply. Base: 130 travel retailers and 123 suppliersSource: PhoCusWright’s Payment Unsettled: Cost, Opportu-nity and Disruption in Travel’s Complex Payment Landscape© 2013 PhoCusWright Inc. All Rights Reserved.

Credit card

Debit card

EFT

Cash orCheck

Alternativeonline

method

89%88%

Suppliers

33%33%

20%25%

16%

15%

8%

14% Retailers

4) PhoCusWright’s U.S. Mobile Travel Report: Market Sizing and Consumer Trends, February 2013

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved.Page 14

Summary and RecommendationsThe travel marketplace is continuing to undergo tremendous change brought about by accelerating globalization, increased adoption of online commerce and the emergence of mobile platforms. Over the last decade, companies across the entire travel industry have rolled out significant innovations in distribution, merchandising and pricing; much of this innovation has happened in the online arena. The pressure for travel companies to innovate continues, as businesses compete for higher market share and improved margins. One area where we see growing innovation and change is in payments processing.

While there is a burgeoning array of new and emerging alternative payment solu-tions, credit card payments remain dominant across all travel industry segments and geographic regions. The percentage of online gross travel bookings charged to cred-it cards ranges from a low of 34% in MEA to a high of 82% in North America. How-ever, there are some regional differences: cash and check payments are much more common in emerging market regions, debit cards have a firm following in Western Europe, and EFT payments remain important in Eastern Europe.

This high incidence of credit card use also means card fraud is a key payments concern for travel companies. Large online sellers in particular, including OTAs, airlines and hotels, report an online fraud rate above the North American average for all e-commerce. A small, but growing number of travel companies are looking at alternative forms of payment to reduce card expenses and potentially fraud as well. Both of these challenges feature highly as concerns of travel suppliers and retailers. This is particularly evident in larger companies with a significant online presence. The uptake of new payment methods remains low, however, notably due to poor custom-er demand and challenges with integrating such methods into existing online and back-office systems.

Although mobile platforms are rapidly becoming commonplace for travel transac-tions, it is not clear which, if any, of the current mobile payment solutions may prevail in the long term. Current implementation across the travel industry is virtually non-existent, customer uptake is still uncertain, but industry interest and expectations remain high. Travel companies must walk a fine but vigilant line between uncertain customer uptake and a mix of competing standards, as mobile payments inevitably gain acceptance. z

The State of Pay in Online Travel August 2013

©2013 PhoCusWright Inc. All Rights Reserved. Page 15

PhoCusWright thanks our partners and sponsors for PhoCusWright’s Payments Unsettled Special Project

Without their active support, this research would not have been possible.

PARTNERS

African Business Travel Association (ABTA)

Association of Corporate Travel Executives (ACTE)

Business Travel News (BTN Group)

Hotel Electronic Distribution Network Association (HEDNA)

International Air Transport Association (IATA)

Pacific Asia Travel Association (PATA)

Tnooz

TTG Digital

WebInTravel (WIT)

SPONSORS

CyberSource

Elavon

eNett International Pty Ltd.

GlobalCollect Services BV

Ixaris Systems Ltd.

Mastercard Worldwide

PayPal Inc.

UATP

U.S. Bank Corporate Payment Systems

PhoCusWright Inc.116 West 32nd Street, 14th Floor

New York, NY 10001 USA

PO Box 760Sherman, CT 06784 USA

+1 860 350-4084+1 860 354-3112 fax

www.phocuswright.com