the thirty-seventh annual iowa high school mock …

TRANSCRIPT

1

THE THIRTY-SEVENTH ANNUAL IOWA HIGH SCHOOL

MOCK TRIAL TOURNAMENT 2019

KELLY CROWN

V.

BRYCE CUTTER d/b/a CHARITY OPERATIONS

NETWORK

A program of

The Iowa State Bar Association Center for Law & Civic Education

In cooperation with the Young Lawyer’s Division

Of The Iowa State Bar Association

With generous financial support from The Iowa State Bar Foundation

2

IOWA HIGH SCHOOL MOCK TRIAL TOURNAMENT

2019

KELLY CROWN

V.

BRYCE CUTTER d/b/a CHARITY OPERATIONS

NETWORK

Original Case Materials Developed for INDIANA MOCK TRIAL

© 2015

Case Adapted for Iowa High School Competition Use By: The Iowa State Bar Association

Center for Law & Civic Education 625 East Court Avenue

Des Moines, Iowa 50309

Many thanks to the Indiana Mock Trial Program & the Indiana Bar Foundation for permitting use and adaptation of the case material and especially to Susan Roberts, original author of the problem

3

CASE BACKGROUND

The wealthiest and most elite citizens of Iowa gathered together on a beautiful September evening in 2016 for one of the most publicized events of the year. The exclusive list of VIP guests arrived with much fanfare and media attention for the prestigious gala and fundraising event at the luxurious Hotel LeRoche Resort and Spa for the Thomas J. Levis Caring Hearts Children's Hospital Foundation. Plaintiff Kelly Crown, a recent multi-million dollar lottery winner, attended the charity art auction to purchase a collectible work of art as an investment while simultaneously supporting the Foundation's goal to provide funds for pediatric cardiology equipment and services for the children of Iowa.

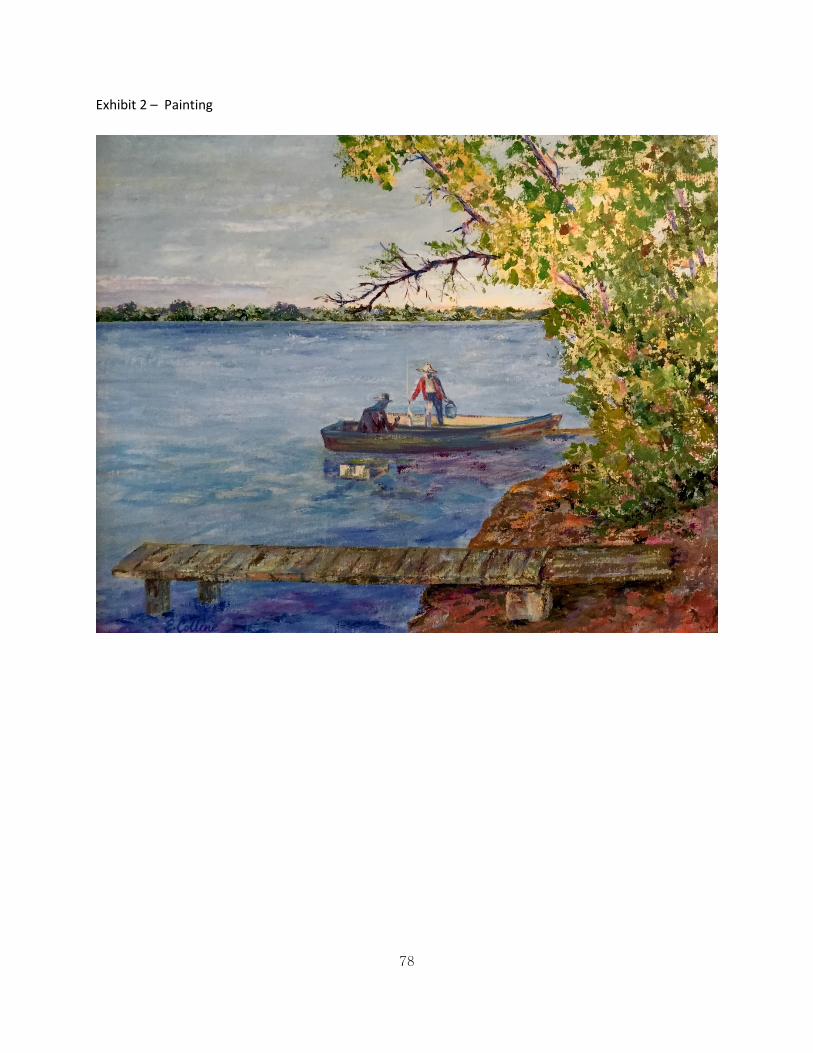

At the art auction, Crown was the successful bidder for a highly collectible E. Colline oil

painting. Bryce Cutter, d/b/a Charity Operations Network, the Defendant Auctioneer, purportedly represented that the painting was authentic and came with a Certificate of Authenticity. When the painting was in the process of some restoration work by Rene Beltracchi, Crown was notified that the painting was a fake.

Was the painting purchased by Crown at the art auction a fake? Was there a misrepresentation

of the painting's authenticity and provenance? Did the Defendant perform sufficient due diligence to determine the authenticity of the painting? Did the Plaintiff exercise due diligence before purchasing the painting? And, who can be trusted in this myriad of personalities and egos?

Plaintiff’s Witnesses: Kelly Crown - Plaintiff and Purchaser Rene Beltracchi – Art Restorer, Expert Witness, and Former Forger Taylor Hanratty – FBI Agent and Art Fraud and Forgery Investigator Defendant’s Witnesses: Bryce Cutter – Defendant, Auctioneer and Owner of Charity Operations Network Morgan Walden– Estate Representative of Painting’s Original Owner Evelyn Pears - Appraiser, Expert Witness, and Former Museum Curator Exhibits:

1. Charity Auction Catalogue 2. Painting 3. Sales Receipt 4. Certificate of Authenticity 5. Appraisal 6. Charity Operations Network Website Excerpts 7. Notes from Auction 8. Curriculum Vitae of Evelyn Pears

The Case Background is not to be used as evidence in the case, but rather is provided for background

purposes only. This case is a work of fiction. The names and events described herein are intended to be fictional. Any similarity or resemblance of any character to an actual person or entity should be regarded as only fictional for purposes of this mock trial exercise. However, the history of the American Impressionist Movement and the work of the Hoosier Group are real.

4

IN THE IOWA DISTRICT COURT OF POLK COUNTY KELLY CROWN ) ) CIVIL ACTION ) IAHSMT - 2019 Plaintiff, ) ) vs. ) PETITION AT LAW ) BRYCE CUTTER, d/b/a ) CHARITY OPERATIONS NETWORK )

) Defendant. )

COMPLAINT

Plaintiff, Kelly Crown, by counsel, files this Complaint against the Defendant, Bryce Cutter, and states:

General Allegations

1. Plaintiff Kelly Crown is a resident of St. Charles, Madison County, Iowa.

2. Defendant Bryce Cutter, d/b/a Charity Operations Network, is a resident of Gotham City, Gotham

County, Iowa and purports to be a professional charities art auctioneer.

3. On September 10, 2016, Plaintiff was at the Thomas J. Levis Caring Hearts Children’s Hospital

Foundation Gala & Charity Auction (Charity Auction) where Defendant offered for sale for the benefit of

the Foundation works of fine art represented to be collectibles and Masters.

4. Defendant organized and managed the Charity Auction from start to finish, including, but not

limited to, providing works of art for the auction, auctioning the works of art, collecting payment, and

delivering the works of art to the buyers.

5. Defendant prepared, published and distributed to Plaintiff a catalogue of all works of art

available for sale at the Charity Auction (“the Catalogue”).

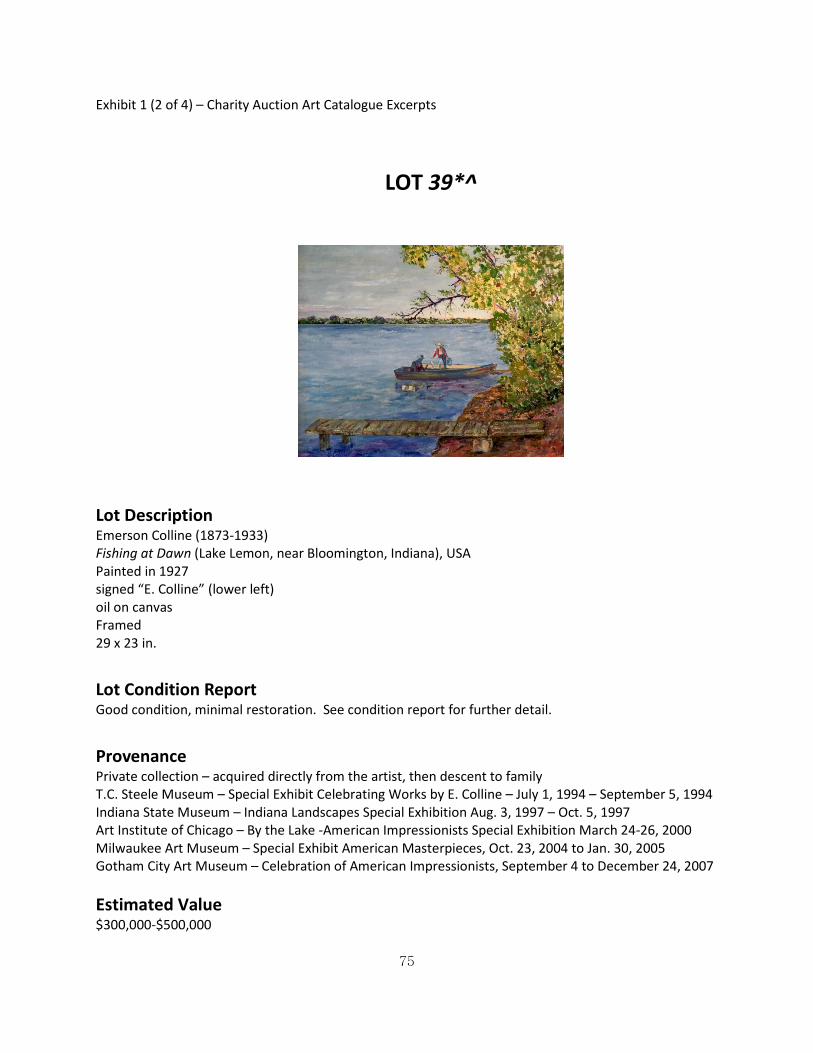

6. The Catalogue represented that Lot 39 was an original oil canvas painting by American

Impressionist Emerson Colline (“the Artist”), entitled Fishing at Dawn, painted in 1927 and signed by

artist Emerson Colline (“The Painting”).

7. The Catalogue further represented that the Painting was in “good condition” with minimal

restoration.

5

8. The Catalogue also represented that the owner obtained the Painting by descent from a

family member that received it directly from the Artist.

9. The Catalogue represented that the Estimated Value of the Painting was between $300,000-$500,000.

10. Paintings by the Artist in the American Impressionist style are highly collectible and valuable

11. At the beginning of the Charity Auction, Defendant represented that all works of art at the

Auction that contain a signature had been authenticated by a nationally recognized, indepe

ndent third party.

12. When the Painting came up for auction, Defendant represented that the Painting came

with a Certificate of Authenticity and that the Painting was authentic.

13. Defendant either knew or failed to perform sufficient due diligence to determine if the

representations made about the painting were false.

14. Plaintiff relied upon the representations made by Defendant in writing and verbally at the

Charity Auction.

15. Defendant failed to conduct adequate independent research into the authenticity of the

Painting.

16. Plaintiff was the highest bidder for the Painting in the amount of $455,000.

(“the Purchase”).

17. Plaintiff paid Defendant the purchase price of $455,000 by wire transfer on September 12,

2016.

18. Defendant delivered the Painting to Plaintiff at Plaintiff’s residence on October 12, 2016.

Count I Rescission Based on Mutual Mistake

19. Plaintiff incorporates the allegations in Paragraphs 1 through 18 as if fully set forth

herein.

20. Plaintiff bought the Painting believing it to be a genuine painting by Colline .

21. Defendant represented in the Sales Receipt issued to Plaintiff for said Purchase that the

Painting was the Artist’s work.

22. The Painting is a forgery.

23. Plaintiff had no knowledge that the Painting was a forgery.

24. Plaintiff relied upon the representations made by Defendant to his/her detriment.

6

25. To the extent Defendant was not aware of the forgery, Plaintiff and Defendant were

mutually mistaken in believing that the Painting was an authentic work by Emerson

Colline.

26. Plaintiff agreed to and did purchase the Painting without any knowledge of these

mistakes.

27. Plaintiff fully performed all of his/her obligations for the purchase.

28. Plaintiff has no adequate remedy at law and is therefore entitled to a rescission.

Count II Breach of Express Warranties

29. Plaintiff incorporates the allegations in Paragraphs 1 through 28 as if fully set forth herein.

30. Before and at the time of the sale, for the purposes of inducing Plaintiff to purchase the

Painting, Defendant represented to Plaintiff that the Artist who created the Painting was

Emerson Colline, that the Painting was authentic, that the Painting had a Certificate of

Authenticity, and that the Artist’s signature on the Painting had been independently

verified.

31. Plaintiff relied upon Defendant’s express warranties concerning the Painting's authenticity

and would not have purchased the work had he/she been aware that those warranties

were false.

32. Plaintiff fully performed any obligations under the purchase agreement.

33. Defendant breached its express warranty because the Painting is a forgery.

34. Plaintiff suffered damages, as a result of this breach.

Count III Fraud

35. Plaintiff incorporates the allegations in Paragraphs 1 through 34 as if fully set forth herein.

36. Defendant fraudulently induced Plaintiff to purchase the Painting by falsely stating the

Painting was authentic.

37. Defendant knew the Painting was a forgery, and that it had no value.

38. Defendant knowingly participated in the sale of a forgery.

39. Plaintiff had no reason to know that Defendant’s statements were false.

40. Plaintiff relied on each of the misrepresentations made by Defendant in purchasing the

Painting.

41 Plaintiff’s reliance on Defendant’s misrepresentations was reasonable.

7

42. In reliance on the misrepresentations and omissions of Defendant, Plaintiff was

damaged.

43 Because Defendant engaged in the fraudulent conduct, willfully and maliciously, and

with the intent to damage Plaintiff, Plaintiff is entitled to an award of punitive damages.

Count IV – Negligence

44. Plaintiff incorporates the allegations in Paragraphs 1 through 43 of the Complaint as if

fully set forth herein.

45. Defendant was negligent in failing to exercise due diligence in determining the

authenticity, provenance, condition and value of the Painting.

46. As a consequence of the negligence of Defendant, Plaintiff suffered damages.

47. The damages sustained by Plaintiff were proximately caused by the negligence of

Defendant.

WHEREFORE, Plaintiff, Kelly Crown, prays for damages against Defendant Cutter, and all other just

and proper relief.

________________ . Attorney for Plaintiff

JURY DEMAND Plaintiff respectfully requests trial by jury.

________________ .

Attorney for Plaintiff

8

IN THE IOWA DISTRICT COURT OF POLK COUNTY KELLY CROWN ) ) CIVIL ACTION ) IAHSMT - 2019 Plaintiff, ) ) vs. ) ANSWER ) BRYCE CUTTER, d/b/a ) CHARITY OPERATIONS NETWORK )

) Defendant. )

DEFENDANT’S ANSWER TO COMPLAINT

The Defendant, Bryce Cutter d/b/a Charity Operations Network, for his/her answer to the Complaint, states as follows:

1. Defendant is without knowledge or information sufficient to form a belief as to the truth of the allegations of paragraph 1 of the Complaint.

2. Defendant admits the allegations of paragraph 2 of the Complaint.

3. Defendant admits the allegations of paragraph 3 of the Complaint.

4. Defendant admits the allegations of paragraph 4 of the Complaint.

5. Defendant admits the allegations of paragraph 5 of the Complaint.

6. Defendant denies the allegations of paragraph 6 of the Complaint.

7. Defendant denies the allegations of paragraph 7 of the Complaint.

8. Defendant denies the allegations of paragraph 8 of the Complaint. 9. Defendant denies the allegations of paragraph 9 of the Complaint. 10. Defendant admits the allegations of paragraph 10 of the Complaint. 11. Defendant admits the allegations of paragraph 11 of the Complaint. 12. Defendant denies the allegations of paragraph 12 of the Complaint. 13. Defendant denies the allegations of paragraph 13 of the Complaint.

9

14. Defendant is without knowledge or information sufficient to form a belief as to the truth of the allegations

of paragraph 14 of the Complaint. 15. Defendant denies the allegations of paragraph 15 of the Complaint. 16. Defendant admits the allegations of paragraph 16 of the Complaint. 17. Defendant admits the allegations of paragraph 17 of the Complaint. 18. Defendant admits the allegations of paragraph 18 of the Complaint.

Count I

19. Defendant incorporates herein by reference its answers to the allegations of paragraphs 1 through 18 of the

Complaint.

20. Defendant is without knowledge or information sufficient to form a belief as to the truth of the allegations

of paragraph 20 of the Complaint.

21. Defendant denies the allegations of paragraph 21 of the Complaint.

22. Defendant is without knowledge or information sufficient to form a belief as to the truth of the allegations

of paragraph 22 of the Complaint.

23. Defendant is without knowledge or information sufficient to form a belief as to the truth of the allegations

of paragraph 23 of the Complaint.

24. Defendant is without knowledge or information sufficient to form a belief as to the truth of the allegations

of paragraph 24 of the Complaint.

25. Defendant denies the allegations of paragraph 25 of the Complaint.

26. Defendant is without knowledge or information sufficient to form a belief as to the truth of the allegations

of paragraph 26 of the Complaint.

27. Defendant admits the allegations of paragraph 27 of the Complaint.

28. Defendant denies the allegations of paragraph 28 of the Complaint.

Count II

29. Defendant incorporates herein by reference its answers to the allegations of paragraphs 1 through 28 of the

Complaint.

30. Defendant denies the allegations of paragraph 30 of the Complaint.

31. Defendant denies the allegations of paragraph 31 of the Complaint.

32. Defendant admits the allegations of paragraph 32 of the Complaint.

33. Defendant denies the allegations of paragraph 33 of the Complaint.

34. Defendant denies the allegations of paragraph 34 of the Complaint.

10

Count III

35. Defendant incorporates herein by reference its answers to the allegations of paragraphs 1 through 34 of the

Complaint.

36. Defendant denies the allegations of paragraph 36 of the Complaint.

37. Defendant denies the allegations of paragraph 37 of the Complaint.

38. Defendant denies the allegations of paragraph 38 of the Complaint.

39. Defendant denies the allegations of paragraph 39 of the Complaint.

40. Defendant denies the allegations of paragraph 40 of the Complaint.

41. Defendant denies the allegations of paragraph 41 of the Complaint.

42. Defendant denies the allegations of paragraph 42 of the Complaint.

43. Defendant denies the allegations of paragraph 43 of the Complaint.

Count IV

44. Defendant incorporates herein by reference its answers to the allegations of paragraphs 1 through 43 of the

Complaint.

45. Defendant denies the allegations of paragraph 45 of the Complaint.

46. Defendant denies the allegations of paragraph 46 of the Complaint.

47. Defendant denies the allegations of paragraph 47 of the Complaint.

WHEREFORE, Defendant prays for judgment in his/her favor, that Plaintiff take nothing by way of his/her complaint, for costs, and all other just and proper relief.

AFFIRMATIVE DEFENSES

First defense The sole proximate cause of the damages allegedly sustained by plaintiff was plaintiff's own negligence, and for that reason, plaintiff is not entitled to recover.

Second Defense The damages allegedly sustained by the plaintiff were caused in whole or in part, or were contributed to, by the negligence or fault of the plaintiff, and for that reason, the plaintiff is not entitled to recover, or, plaintiff's damages must be reduced accordingly.

Third Defense Plaintiff failed to exercise due diligence. WHEREFORE, the Defendant prays that Plaintiff take nothing by way of his/her complaint; that judgment be entered in favor of Defendant; and for such other and further relief as is just and proper.

_____________________ Attorney for Defendant

11

IN THE IOWA DISTRICT COURT OF POLK COUNTY

KELLY CROWN ) ) CIVIL ACTION ) IAHSMT - 2019 Plaintiff, ) ) vs. ) STIPULATIONS ) BRYCE CUTTER, d/b/a ) CHARITY OPERATIONS NETWORK )

) Defendant. )

1. All exhibits included in the case materials are authentic and accurate representations and the

proper chain of custody with regard to the exhibits has been maintained, teams must still use the

proper procedures for admitting exhibits into evidence.

2. The signatures and signature representations on the witness statements and all other documents are

authentic. No challenges based on the authenticity of witness signed documents will be

entertained.

3. The dates of witness statements are not relevant and therefore not included. No challenges based

on the dates of the witness statements will be entertained. All statements were taken after the

alleged incident but before trial.

4. The jurisdiction and venue for this mock trial case have been previously established and are

proper.

5. All of the witnesses can be portrayed by students of either gender. Any instances where a witness

is only referred to as only him or her or only he or she is inadvertent.

6. Whenever a rule of evidence requires that reasonable notice be given, it has been given.

7. All pretrial motions have been considered by the Court and do not affect the trial of this case.

8. The parties agree that Exhibits 1, 3 and 6 are created by a person with knowledge of the

information contained therein at or about the time of the events, that such records are kept in the

course of regularly conducted activity and that it is not necessary to enter the exhibits through the

custodian of the records.

9. The parties stipulate and agree that the Curriculum Vitae of Evelyn Pears (Exhibit 8) is

admissible, without objection.

12

10. As is the tradition in Civil mock trial problems, this trial is bifurcated. Damages will not be awarded in

this phase of the trial. While teams may choose to discuss elements of damages, it is neither necessary

nor expected in this trial.

11. All witnesses are familiar with their statements as provided with the case materials prior to trial. No

witness may feign either ignorance or inability to read or recall the substance of her/his statement

provided.

12. Exhibit 2 (listed as the “Painting” in the Exhibit List) is intended to be the actual painting currently in

possession of the Plaintiff, Kelly Crown.

13

APPLICABLE LAW

Burden of Proof in Negligence Cases

The plaintiff has the burden of proof by a preponderance of the evidence on the following propositions:

a. that the defendant was negligent ; b. that the plaintiff suffered damages; and c. that the negligence of the defendant was a proximate cause of the damages suffered by

the plaintiff. Negligence

Negligence is the failure to use reasonable care.

A person may be negligent by acting or by failing to act. A person is negligent if he or she does something a reasonably careful person would not do in the same situation or fails to do something a reasonably careful person would do in the same situation.

Reasonable or Ordinary Care

Reasonable or ordinary care is the care a reasonably careful and ordinarily prudent person would use under the same or similar circumstances. Reasonable care does not require a person to foresee and guard against that which is unusual and not likely to occur.

Proximate Cause

An act or omission is a proximate cause of the damages suffered if the damages are a natural and probable consequence of the act or omission. To establish that an act was the proximate cause of damages, a party must show:

(1) That damages would not have occurred but for another’s negligence; and (2) That damages were reasonably foreseeable as the natural and probable consequence of

the other’s negligence.

Fraud

Fraud exists when:

(a) there is a material misrepresentation of fact (b) made with knowledge of its falsity or recklessly made without knowledge of its truth (c) with the intention of being acted upon by another, which (d) is relied upon by another (a buyer) (e) to his/her damage.

14

STATUTES AND RELATED LAW:

2009 Iowa Code Title 13 - Commerce Subtitle 5 - Regulation of Commercial Enterprises CHAPTER 554 - UNIFORM COMMERCIAL CODE

554.2313 EXPRESS WARRANTIES BY AFFIRMATION, PROMISE, DESCRIPTION, SAMPLE. 1. Express warranties by the seller are created as follows: a. Any affirmation of fact or promise made by the seller to the buyer which relates to the goods and becomes part of the basis of the bargain creates an express warranty that the goods shall conform to the affirmation or promise. b. Any description of the goods which is made part of the basis of the bargain creates an express warranty that the goods shall conform to the description. c. Any sample or model which is made part of the basis of the bargain creates an express warranty that the whole of the goods shall conform to the sample or model. 2. It is not necessary to the creation of an express warranty that the seller use formal words such as "warrant" or "guarantee" or that the seller have a specific intention to make a warranty, but an affirmation merely of the value of the goods or a statement purporting to be merely the seller's opinion or commendation of the goods does not create a warranty. 554.2314 IMPLIED WARRANTY: MERCHANTABILITY – USAGE OF TRADE. 1. Unless excluded or modified (section 554.2316), a warranty that the goods shall be merchantable is implied in a contract for their sale if the seller is a merchant with respect to goods of that kind. Under this section the serving for value of food or drink to be consumed either on the premises or elsewhere is a sale. 2. Goods to be merchantable must be at least such as a. pass without objection in the trade under the contract description; and b. in the case of fungible goods, are of fair average quality within the description; and c. are fit for the ordinary purposes for which such goods are used; and d. run, within the variations permitted by the agreement, of even kind, quality and quantity within each unit and among all units involved; and e. are adequately contained, packaged, and labeled as the agreement may require; and f. conform to the promises or affirmations of fact made on the container or label if any. 3. Unless excluded or modified (section 554.2316) other implied warranties may arise from course of dealing or usage of trade. 554.2315 IMPLIED WARRANTY -- FITNESS FOR PARTICULAR PURPOSE. Where the seller at the time of contracting has reason to know any particular purpose for which the goods are required and that the buyer is relying on the seller's skill or judgment to select or furnish suitable goods, there is unless excluded or modified under section 554.2316 an implied warranty that the goods shall be fit for such purpose.

15

554.2316 EXCLUSION OR MODIFICATION OF WARRANTIES. 1. Words or conduct relevant to the creation of an express warranty and words or conduct tending to negate or limit warranty shall be construed wherever reasonable as consistent with each other; but subject to the provisions of this Article on parol or extrinsic evidence (section 554.2202) negation or limitation is inoperative to the extent that such construction is unreasonable. 2. Subject to subsection 3, to exclude or modify the implied warranty of merchantability or any part of it the language must mention merchantability and in case of a writing must be conspicuous, and to exclude or modify any implied warranty of fitness the exclusion must be by a writing and conspicuous. Language to exclude all implied warranties of fitness is sufficient if it states, for example, that "There are no warranties which extend beyond the description on the face hereof." 3. Notwithstanding subsection 2 a. unless the circumstances indicate otherwise, all implied warranties are excluded by expressions like "as is", "with all faults" or other language which in common understanding calls the buyer's attention to the exclusion of warranties and makes plain that there is no implied warranty; and b. when the buyer before entering into the contract has examined the goods or the sample or model as fully as the buyer desired or has refused to examine the goods there is no implied warranty with regard to defects which an examination ought in the circumstances to have revealed to the buyer; and c. an implied warranty can also be excluded or modified by course of dealing or course of performance or usage of trade. 4. Remedies for breach of warranty can be limited in accordance with the provisions of this Article on liquidation or limitation of damages and on contractual modification of remedy (sections 554.2718 and 554.2719). ADDITIONAL LAW:

Express warranties are not created from puffing or statements of personal opinion such as I think this is a beautiful painting or an affirmation of value such as this is one of the best values you can find today in art of this period.

One who sells a piece of art has a fiduciary responsibility to exercise due diligence in the authentication of a piece of artwork. Due diligence is the responsibility of one who sells, buys or donates personal property to establish that the item is not stolen and can change hands with good title and that it is real. Autocephalous Greek Orthodox Church v. Goldberg & Feldman Fine Arts, Inc. 917 F .2d 278 (7th Cir 1990)

“In a transaction like this, all the red flags are up and the red lights are on, all the sirens are blaring. In such cases, dealers can (and probably should) take steps such as a formal IFAR search, a documented authenticity check by disinterested experts, a full background check of the seller and his claim of title, insurance protection and contingency sales, contract, and the like.”

16

Rescission The abrogation of a contract, effective from its inception, thereby restoring the parties to the positions they would have occupied if no contract had ever been formed.

By Agreement Mutual rescission, or rescission by agreement, is a discharge of both parties from the obligations of a contract by a new agreement made after the execution of the original contract but prior to its performance. Rescission by mutual assent is separate from the right of one of the parties to rescind or cancel the contract for cause, or pursuant to a provision in the contract.

The parties to an executory or incomplete contract can rescind it at any time by mutual agreement, even if the contract itself contains a contrary provision. A rescission by mutual assent can properly include a promise by either or both parties to make restitution as part of the contract of rescission.

The right to rescind is limited to the parties to the contract or those legally authorized to act for them. As with other contracts, the parties to the rescission agreement must be mentally competent.

Form The rescission agreement can be either written or oral. An implied agreement is also effective, provided the assent of the parties can be shown by their acts and the surrounding circumstances. An express rescission of a contract as a whole is adequate and effective, without specifically designating each and every clause to be rescinded. Unless a statute provides otherwise, an oral rescission agreement is valid, even though the contract being rescinded contains a provision that it can be altered only in writing.

Assent All the parties to the contract must assent to its rescission because mutual rescission involves the formation of a new contract. A meeting of minds can be reached by an offer to rescind and an acceptance by the other party. One party to a contract cannot rescind it simply by giving notice to the other party that he or she intends to do so.

Although a breach of contract by one party is not an offer to rescind, the other party can treat the repudiation as an offer to rescind that he or she can accept, leading to rescission of the contract by mutual assent. Rescission must be clearly expressed, however, and the conduct of the parties must be inconsistent with the existence of the contract. The fact that some of the materials that form part of the subject matter of the contract have been returned is not conclusive as to whether rescission has occurred.

Consideration An agreement to rescind a prior contract must be based on a sufficient consideration, an inducement. When a contract remains executory on both sides, an agreement to rescind by one side is sufficient consideration for the agreement to cancel on the other, and vice versa. If the contract has been executed on one side, an agreement to rescind that is made without any new consideration is void, that is to say of no legal force or binding effect.

Operation and Effect The mutual rights of the parties are controlled by the terms of their rescission agreement. The parties are generally restored to their original rights in regard to the subject matter. They no longer have any rights or obligations under the rescinded contract, and no claim or action for subsequent breach can be maintained.

Whether rights or obligations already accrued are abandoned when the contract is rescinded in the course of performance depends on the intention of the parties, as deduced from all attending facts and circumstances, and on whether the parties have reserved such rights. Recovery can be allowed, however, for partial performance.

17

Wrong or Default of Adverse Party No arbitrary right exists to rescind a contract. An executory contract that is voidable can be rescinded on the grounds of fraud, mistake, or incapacity.

A contract, whether oral or written, can be rescinded on the ground of fraud. The right to rescind for fraud is not barred because the defrauded party has failed to perform. Generally, false statements of value, or the failure to perform a promise to do something in the future without fraudulent intent, will not provide a basis for rescission for fraud or misrepresentation. A party proves sufficient grounds for rescission by showing that he or she was induced to part with some legal right or to assume some legal liability that he or she otherwise would not have done but for the fraudulent representations.

On discovering the fraud, the victimized party can affirm the contract and sue for damages. He or she might instead repudiate the contract, tender back what he or she has received, and recover what he or she has parted with, or its value; the adoption of one remedy, however, excludes the other.

A contract obtained by duress can be rescinded, and in such a case, the same rules apply as in the case of fraud. A contract cannot be avoided because of duress or coercion, however, unless the duress was sufficient to overcome completely the will of the party who is seeking to avoid the contract.

A mutual mistake concerning a material fact entitles the party affected by the mistake to rescind the contract, unless the contract has already been completed and rescission would be an injustice to the other party. Rescission can also be allowed even for a unilateral, or one-sided, mistake in order to prevent an unjust enrichment of the other party. On rescission, the aggrieved party can recover the money he or she has paid or the property he or she has delivered under the contract.

A contract made by a person of unsound mind can be rescinded when the parties can be restored to the status quo. This rule applies even if the opposite party was unaware of the mental condition, and the contract was fair, reasonable, and made in good faith for adequate consideration. When one party knows of the other's incapacity, the contract can be rescinded on the ground of fraud. When both parties are sane and the contract is valid, subsequent insanity of one of the parties is not a ground for rescission, unless it affects the substance or purpose of the contract, as in the case of a personal services contract. As a general rule, a contract cannot be rescinded because one of the parties was intoxicated at the time it was made. If, however, unfair advantage was taken of a person's intoxicated condition, or if the intoxication was induced by the party seeking to take advantage of the contract, the contract can be set aside on the ground of fraud. Similarly, habitual drunkenness that impairs a party's mental abilities can constitute a ground for rescission.

Inadequate Consideration Mere inadequacy of consideration is not a sufficient reason to justify rescission. When the consideration is so inadequate that it shocks the conscience of the court or is so closely connected with suspicious circumstances or misrepresentations as to provide substantial evidence of fraud, it can furnish a basis for relief.

Nonperformance or Breach One party to a contract can rescind it because of substantial nonperformance or breach by the other party. The party who knowingly and willfully fails to perform cannot complain that the other party to the contract has injured him or her by terminating the contract. The right to rescind does not arise from every breach but is permitted only when the breach is so substantial and fundamental that it defeats the objective of the parties in making the agreement. The breach must pertain to the essence of the contract. The act must be an unqualified refusal by the other party to perform and should amount to a decision not to be bound by the contract in the future. A party to a contract who is in default cannot, however, rescind because of a breach by the other party.

18

When time is of the essence in a contract, failure to perform within the time stipulated is a ground for rescission. Otherwise a delay in the time of performance is not considered a material breach justifying rescission. When performance is intended within a reasonable time, one party cannot suddenly and without reasonable notice terminate the contract while the other party is attempting in good faith to perform it.

An unconditional notice by one party that he does not intend to perform a contract is a ground for rescission by the other party. In order to justify rescission, the refusal must be absolute and unconditional.

When one party to a contract abandons it and refuses further performance or her conduct shows that she is repudiating the contract, the other party is entitled to rescission. A disagreement over the terms of the contract and a subsequent refusal to perform in a particular manner by one of the parties do not constitute an abandonment of the contract justifying rescission.

Time A right to rescind must be exercised promptly or within a reasonable time after the discovery of the facts that authorize the right. A reasonable time is defined by the circumstances of the particular case. The rule that rescission must be prompt does not operate where an excuse or justification for a delay is shown.

19

GUIDANCE FROM THE FEDERAL TRADE COMMISSION

UNDERSTANDING WARRANTIES Generally, a warranty is your promise, as a warrantor, to stand behind your product. It is a statement about the integrity of your product and about your commitment to correct problems when your product fails.

The law recognizes two basic kinds of warranties—implied warranties and express warranties.

Implied Warranties Implied warranties are unspoken, unwritten promises, created by state law, that go from you, as a seller or merchant, to your customers. Implied warranties are based upon the common law principle of "fair value for money spent," There are two types of implied warranties that occur in consumer product transactions. They are the implied warranty of merchantability and the implied warranty of fitness for a particular purpose. The implied warranty of merchantability is a merchant's basic promise that the goods sold will do what they are supposed to do and that there is nothing significantly wrong with them. In other words, it is an implied promise that the goods are fit to be sold. The law says that merchants make this promise automatically every time they sell a product they are in business to sell. For example, if you, as an appliance retailer, sell an oven, you are promising that the oven is in proper condition for sale because it will do what ovens are supposed to do—bake food at controlled temperatures selected by the buyer. If the oven does not heat, or if it heats without proper temperature control, then the oven is not fit for sale as an oven, and your implied warranty of merchantability would be breached. In such a case, the law requires you to provide a remedy so that the buyer gets a working oven.

The implied warranty of fitness for a particular purpose is a promise that the law says you, as a seller, make when your customer relies on your advice that a product can be used for some specific purpose. For example, suppose you are an appliance retailer and a customer asks for a clothes washer that can handle 15 pounds of laundry at a time. If you recommend a particular model, and the customer buys that model on the strength of your recommendation, the law says that you have made a warranty of fitness for a particular purpose. If the model you recommended proves unable to handle 15-pound loads, even though it may effectively wash 10-pound loads, your warranty of fitness for a particular purpose is breached.

Implied warranties are promises about the condition of products at the time they are sold, but they do not assure that a product will last for any specific length of time. (The normal durability of a product is, of course, one aspect of a product's merchantability or its fitness for a particular purpose.) Nor does the law say that everything that can possibly go wrong with a product falls within the scope of implied warranties. For example, implied warranties do not cover problems such as those caused by abuse, misuse, ordinary wear, failure to follow directions, or improper maintenance.

Generally, there is no specified duration for implied warranties under state laws. However, the state statutes of limitations for breach of either an express or an implied warranty are generally four years from date of purchase. This means that buyers have four years in which to discover and seek a remedy for problems that were present in the product at the time it was sold. It does not mean that the product must last for four years. It means only that the product must be of normal durability, considering its nature and price.

A special note is in order regarding implied warranties on used merchandise. An implied warranty of merchantability on a used product is a promise that it can be used as expected, given its type and price range. As with new merchandise, implied warranties on used merchandise apply only when the seller is a merchant who deals in such goods, not when a sale is made by a private individual.

20

If you do not offer a written warranty, the law in most states allows you to disclaim implied warranties. However, selling without implied warranties may well indicate to potential customers that the product is risky—low quality, damaged, or discontinued—and therefore, should be available at a lower price.

In order to disclaim implied warranties, you must inform consumers in a conspicuous manner, and generally in writing, that you will not be responsible if the product malfunctions or is defective. It must be clear to consumers that the entire product risk falls on them. You must specifically indicate that you do not warrant "merchantability," or you must use a phrase such as "with all faults," or "as is."

You should be aware that even if you sell a product "as is" and it proves to be defective or dangerous and causes personal injury to someone, you still may be liable under the principles of product liability. Selling the product "as is" does not eliminate this liability.

Express Warranties Express warranties, unlike implied warranties, are not "read into" your sales contracts by state law; rather, you explicitly offer these warranties to your customers in the course of a sales transaction. They are promises and statements that you voluntarily make about your product or about your commitment to remedy the defects and malfunctions that some customers may experience. Express warranties can take a variety of forms, ranging from advertising claims to formal certificates. An express warranty can be made either orally or in writing.

21

Statement of Kelly Crown

My name is Kelly Crown. I live outside of St. Charles, Iowa, about 30 miles southwest of 1

downtown Des Moines on an acreage near the Imes Covered Bridge – one of the famed Bridges 2

of Madison County. I also have an estate in Key Largo, Florida. Even though I now live in 3

mansions in pretty swanky areas, I have humble beginnings. I grew up in the small town of 4

Dinkla, North Dakota, where life was pretty simple, and my family, neighbors, and friends felt 5

good about putting in an honest day's work. My parents instilled in me the core values of 6

fairness, honesty, integrity and truthfulness. I have held on to my core values from those 7

humble beginnings. The way I see it is that if a person has integrity, nothing else matters. If a 8

person does not have integrity, nothing else matters. Perhaps I have been naive in thinking that 9

once I ventured out into the world that others would abide by those same principles. 10

Unfortunately, the circumstances surrounding this lawsuit have shown me that is not the case. 11

If you're wondering how a simple 36-year-old from Dinkla, with just a high school 12

education, amassed such wealth to own two mansions and circulate among the rich and 13

famous, I guess you could say I won the lottery - literally. In August of 2015, I won one of the 14

largest Jackpots in the history of Powerball, with winnings of $750 million and some change. 15

Ordinarily, I didn't waste the little money I had on a game of chance. But I knew the jackpot 16

was going to be big the week I purchased my ticket and I thought that spending $20 for a few 17

chances at that size jackpot was at least worth the entertainment of looking at the winning 18

numbers the next day to see if they matched. Like they say, you can’t win if you don’t play. 19

After paying the IRS and Iowa their respective shares in taxes, I still was left with quite a 20

fortune. Becoming instantly wealthy gave me the opportunity to purchase a new home, 21

expensive cars, and some of the finer things in life, including artwork. 22

Prior to winning the lottery, I worked at the Lakeside Casino in Osceola, Iowa. During 23

my employment at Lakeside, I was assigned to the craps table. Craps is a dice game where 24

players make wagers on the roll, or a series of rolls, of a pair of dice. I rotated positions on the 25

craps table as either a Stickman (the person who announces the results of each roll and moves 26

the dice on the table with an elongated wooden stick) or a base dealer (the person who collects 27

22

and pays bets to the players). What I observed as an employee at Lakeside is that people would 28

lose hard-earned money with the roll of a dice. The “House” (the casino) always had the 29

advantage. There may be players who are really lucky for a period of time, but in the long run 30

those winning streaks end, and their money is lost. When I won the lottery, I didn’t want to risk 31

losing money in a “crapshoot.” I wanted to invest my winnings in something stable; something 32

that was “a sure bet.” 33

Many people came out of the woodwork when I won the lottery. There were relatives I 34

never knew and friends from even grade school that soon referred to me as their favorite 35

relative or best friend. Some wanted a loan, others had investment “opportunities.” I was even 36

solicited by a local soccer club, Scipio F.C., for a contribution. I remember my days as a kid 37

playing futbol, so I gave them money for new equipment and an update to their training 38

facilities. 39

There were many investment and financial advisors that contacted me with ways to 40

grow my money. Of course, I was a bit nervous about investing in the stock market when some 41

analysts were predicting that the market was headed for another crash, and I saw my 401K drop 42

to half of its value after the 2008 stock market crash. I’ve burned through a series of financial 43

advisors – one who was way too conservative, another who wanted to too freely spend my 44

cash, and another charged exorbitant fees for doing very little. I finally settled on Christina 45

Thompson Financial Advisors. She and her minions tried to steer me away from the art market, 46

but once they knew that I was serious about investing, they offered some sound advice. 47

You see a family friend, Jim Jessen, who had acquired some Salvador Dali signed prints, 48

told me that the value of the prints had quadrupled in value and suggested that I look into art 49

as an investment. I had always heard that art was a good investment. I admit I was, and still 50

am, new to the art scene and a novice buyer. However, I thought it would be a safe investment 51

for some of my money, if I purchased collectible art from a reputable dealer. 52

When I was invited as one of the exclusive, VIP guests to attend the Thomas J. Levis 53

Caring Hearts Children’s Hospital Foundation’s fundraising gala and art auction, I thought it 54

was the perfect opportunity to acquire a collectible art piece. At the same time, I thought I could 55

help a charitable cause, especially one that would provide for the health and well-being of 56

23

children. The Levis Foundation's goal was to provide funds for pediatric cardiology equipment 57

and services for the children of Iowa. So, on September 10, 2016, I attended the Foundation’s 58

Gala and Art Auction at the posh Hotel Le Roche Resort and Spa in West Des Moines. The 59

wealthiest and most elite citizens of Iowa were there. I even had a chance to meet the reclusive 60

billionaire, Van Everett. He mentioned that he had a few investment opportunities for me to 61

look over. I think he believes that the future is strong in alternative medicines. The Gala was 62

one of the most publicized events of the year in Iowa, and the fanfare surrounding the event 63

was over the top. The “buzz” of excitement at the gala set the mood to contribute and buy some 64

art to support the children of Caring Hearts. I shared the enthusiasm of other prospective 65

donors to give generously to the charity. 66

The art auction was conducted by Bryce Cutter of Charity Operations Network. A week 67

prior to the auction, I along with the other attendees received a glossy Catalogue of the art 68

pieces with photographs of the art that would be auctioned at the fundraiser. Anyone wishing 69

to view any of the art to be auctioned had the opportunity to schedule an appointment with 70

Cutter to have the art examined, or even appraised. I was busy negotiating the purchase of my 71

new estate in Key Largo and didn’t see any need to personally examine the paintings prior to 72

the auction. The catalogue noted that the paintings I was interested in came with a Certificate 73

of Authenticity, so I felt like I had a guarantee. I did not request any documentation of any 74

particular painting’s history, Certificate of Authenticity, or Lot Condition Report. It had not 75

occurred to me that a charitable auction company raising funds for a children’s hospital 76

couldn’t be trusted. Exhibit 1 is a true and accurate copy of excerpts of the Art Catalogue for 77

the Thomas J. Levis Caring Hearts Children’s Hospital Foundation Art Auction. 78

I was particularly drawn to the American Impressionist paintings because they depict a 79

lighter, carefree sense of life, which reminded me of my youth and growing up in Dinkla. The 80

Catalogue featured paintings by Daniel Garber, Theodore Robinson, and Emerson Colline 81

(pronounced EM-ur-son Cah-LEEN). I had no idea of the current market value for collectible 82

American Impressionist original paintings. Feeling like a fish out of water, I used ARTnet.com, 83

an internet data base, to determine the current market price for similar works of Garber, 84

Robinson and Colline. The recent sale prices on ARTnet.com for those artists were consistent 85

24

with the estimated prices listed in the Charity Operations Network Catalogue. In fact, the 86

recent sales prices that I located on the website sold higher than the estimated market value. 87

The line-up of artwork at the September 10th art auction was nothing less than 88

impressive. Charity Operations Network pulled out all of the stops. Early in the evening, it 89

was evident that bidding would be active, and the event would generate some serious cash and 90

the much-needed funds for the Children’s Hospital. Even to an art novice like me, I could tell 91

there were plenty of offerings that were drawing attention as highly desirable collector’s items. 92

The reactions of other guests and sophisticated potential buyers to many of the art lots 93

convinced me that this was my opportunity to purchase a collectible painting. As I browsed the 94

various lots displayed at the Gala, I referred to the Catalogue for each painting’s description, 95

provenance, condition, and estimated value. Then, I used a smartphone app that instantly 96

connects with auction house databases to check on comparable paintings by the artist. A few of 97

the guests told me that they had hired an appraiser to preview specific pieces at the Charity 98

Operations Network gallery prior to the auction, or to accompany and advise the buyer at the 99

auction. In retrospect, I wish I had done that. 100

I narrowed my selection to a painting by Daniel Garber, called Bayou, depicting two row 101

boats, and an Emerson Colline painting depicting a boat with two people ready to fish, entitled 102

Fishing at Dawn. I was drawn to both paintings because of the serenity of the water and the way 103

the light danced off the landscape. Both paintings were considered highly collectible and there 104

were crowds surrounding those displays. The Colline piece went up for auction first, so I 105

decided not to take any chances. I also thought the piece by Colline was a better investment 106

because the Catalogue noted that most of Colline’s American Impressionist paintings had been 107

destroyed in a fire, and that in later years she followed the movement into Modernism. In an 108

attempt to familiarize myself with some of the Lots in the Catalogue, I read a few blogs about 109

some of the American Impressionists. I learned through the blog that there were only a few 110

women American Impressionist painters, and Emerson Colline was quite prominent. I believe 111

the blog was authored by Rene Beltracchi, although I did not know him/her at the time. I recall 112

that the blogger said he/she would like to get his/her hands on a Colline painting and noted that 113

they were rare and in demand. I did not print the blog and I have since looked for it on the 114

25

Web but it has been taken down. I think it was by Rene Beltracchi, but I can’t recall with any 115

certainty. 116

Bryce Cutter, the owner of Charity Operations Network, was the auctioneer for the 117

Thomas J. Levis Caring Hearts Children’s Hospital Foundation Charity Auction. Of course, 118

auctioneers can talk really fast, but there were definitely some things that Cutter said that I 119

clearly understood and provided reassurance that I was purchasing something of great value 120

and a solid investment. At the opening of the auction, Cutter said Charity Operations Network 121

uses nationally known signature authenticators for all items. More specifically, when Cutter 122

described the Colline painting during the auction, he/she represented that the painting came 123

with a Certificate of Authenticity. Cutter said the painting had provenance and had been 124

verified as authentic. I also noted that the Catalogue indicated that a Certificate of Authenticity 125

was available for the Fishing at Dawn painting. 126

The bidding at the auction for Colline’s Fishing at Dawn was quite fierce. Ultimately, the 127

final bidders were some Chicago land developer, an investment firm, and me. The hammer 128

came down on my bid of $455,000. Of course, I was also required to pay the Buyer’s premium 129

fee of 20%, which I understand is fairly typical in the art auction world, and sometimes it is 130

even more. And I also paid the Iowa sales taxes. Exhibit 2 is the Painting I purchased at the 131

Auction and Exhibit 3 is a true and accurate copy of the Sales Receipt for the purchase of that 132

painting. I paid a premium price for the E. Colline painting, but I wouldn’t have been the 133

successful bidder if I had not bid the $455,000. In any event, I was happy to help out the 134

Children’s Hospital, and I was satisfied that because Fishing at Dawn was in such high demand, 135

it would be a great investment and would only increase in value over time. 136

When I purchased the Emerson Colline painting, it was the first “real” artwork I had 137

ever purchased and the first item I had ever purchased through an auction, charity or 138

otherwise. I purchased the painting, not because of its value, as there were lots of other works 139

of art at the auction that had greater value. Rather, I purchased it because I liked it. At the time, 140

I was not familiar with the artist, and had no idea that Fishing at Dawn was such a valuable, 141

coveted, piece. I subsequently gained more appreciation for the fact that Colline’s work is quite 142

an exception in the art world and that she was one of the few female American Impressionists 143

26

of that time, and certainly also in the Midwest. Colline had studied in Europe with many of the 144

Impressionists, such as Claude Monet and Pierre-Auguste Renoir. However, Colline was most 145

heavily influenced by the works of Alfred Sisley, a French Impressionist, who was the most 146

consistent of the Impressionists in his dedication to painting landscape en plein air (i.e., 147

outdoors). 148

I provided a wire transfer of the total sales price to Charity Operations Network the 149

Monday following the auction. When speaking with Cutter regarding the wire transfer, I also 150

asked about the Certificate of Authenticity. Cutter responded that everything would be 151

delivered in thirty days. On October 12th, the painting was delivered from Charity Operations 152

Network. When the painting was delivered, the Certificate of Authenticity was not presented to 153

me. I contacted Cutter again, and he/she said the paperwork had been misplaced. Cutter said 154

“Oh, I know we have it in a file somewhere.” I finally received the Certificate of Authenticity 155

one year later (after the painting was discovered to be a fake). Exhibit 4 is a true and accurate 156

copy of the Certificate of Authenticity. 157

When I first took receipt of the painting, of course I uncrated it. It was as I remembered 158

it from the auction – two people fishing from a rowboat. I can’t say that I noticed anything 159

different, but then so many factors change. The light in my house, for example, is much 160

different than the perfect auction gallery lighting. I admit that I did not get a real close look at 161

the painting prior to or at the auction. Truth be told, this is my first time ever handling such a 162

valuable work of art – or so I thought. 163

Hey, I did my research. I knew that this kind of painting from this kind of artist rarely 164

came up for auction. That meant the value was sure to rise over time. I considered it a great deal 165

with a much better rate of return than any traditional bank investment or simply stuffing cash 166

in my mattress. I’ve learned my lesson now. My only art purchases in the future will be from 167

the dude selling paintings on the college quad for $10. At least I know his paintings are real, 168

since he paints them right in front of you! 169

I did not press to receive the Certificate of Authenticity because it was just a piece of 170

paper; the artwork should speak for itself as to its authenticity. I needed to obtain an appraisal 171

anyway for valuation purposes to insure the painting and to determine any charitable 172

27

contribution I could take on my tax return. When I inquired at art galleries and dealers as to a 173

recommendation for a fine art appraiser, and particularly American Impressionist paintings, 174

Evelyn Pears kept coming up as the top recommendation for an appraiser. 175

I made arrangements for Pears to come to my home for purposes of appraising the 176

painting that I had purchased at the Caring Hearts Auction. Pears arrived at my home on 177

November 3, 2016. I was surprised by Pears’ demeanor. Even though his/her business thrives 178

on social and business connection, he/she was generally rude. Pears acted haughty. Perhaps 179

that know-it-all attitude, however, convinced me to blindly trust his/her opinions as to the 180

Colline painting. 181

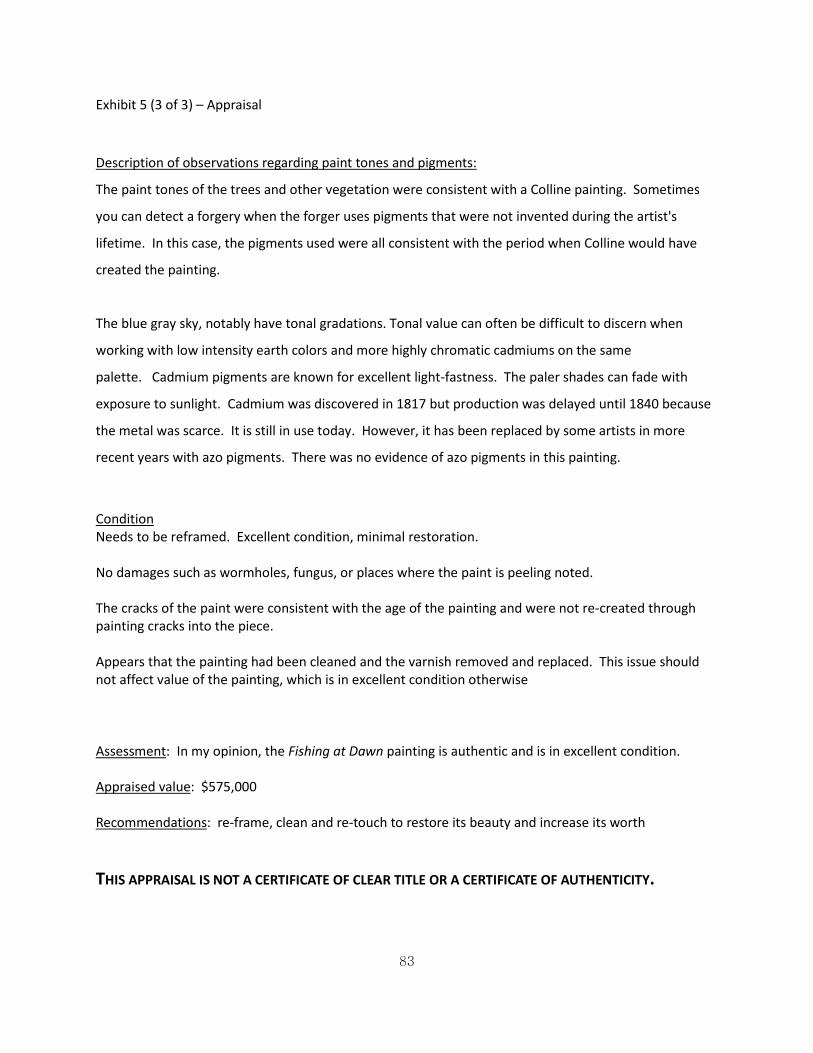

Pears attributed the painting to that of Emerson Colline. Pears was unequivocal that the 182

painting was authentic. Pears appraised the value of the painting at $575,000. Exhibit 5 is a true 183

and accurate copy of Pears’ appraisal. Pears did note some condition issues of the painting, 184

specifically some prior restoration work. However, Pears mentioned that these condition issues 185

were minor and did not affect the value of the painting. Pears recommended that I hire an art 186

conservator to perform restoration work to bring out the painting’s full beauty and to preserve 187

its value. Pears also suggested that I invest in re-framing it to highlight the painting’s flow of 188

lighting throughout the piece. Pears recommended Rene Beltracchi as the conservator and 189

restoration expert. Pears informed me that Beltracchi specialized in American Impressionist 190

paintings, and had a keen eye for Colline’s paintings, among others. After I found out the 191

painting was a fake, I filed suit against Pears. Unfortunately, Pears filed bankruptcy. The 192

lawsuit is probably why Pears is here in court testifying against me. In any event, any claim I 193

had against Pears has been discharged in the bankruptcy case. 194

Shortly thereafter, I followed up with Rene Beltracchi by phone to set up an 195

appointment to discuss the potential restoration work. On November 10, 2016, I met with 196

Beltracchi at his/her Des Moines East Village studio. My instant read on Beltracchi was that 197

he/she is a bit quirky, but very likeable. Beltracchi disclosed right from the beginning his/her 198

past and life of crime as a forger. Rene showed humility, yet strength of character. Beltracchi 199

shared with me his/her history of imprisonment for forgery and how it changed his/her life. I 200

learned that Rene now even works with the FBI. After Rene’s confession, I had no concerns of 201

28

his/her trustworthiness. As evidence that my trust was not misplaced, Rene is the one who 202

uncovered the forgery and it was Rene who notified the FBI and started an investigation on the 203

same day Rene notified me that my painting was a fraud. Beltracchi showed his/her stand-up 204

character and never even sent me a bill for any work he/she did on the painting. I guess he/she 205

felt bad that I was the victim of a forgery. 206

Beltracchi was passionate about his/her conservation work. Beltracchi discussed his/her 207

the meticulous attention to detail and care he/she takes to preserve the Masters. He/she did not 208

want to do anything that would decrease the value of a painting. In Beltracchi’s studio, he/she 209

showed me some of the work he/she had done for other collectors, museums, and galleries. 210

Beltracchi specialized in restoration work of American Impressionists. I knew that by hiring 211

Beltracchi, I was retaining a conservator who is very skillful and knowledgeable, and likely the 212

best in his/her field. Before Beltracchi would accept the restoration work, however, he/she said 213

it was necessary to view the painting in person. 214

The following Monday, on November 14th, Beltracchi came to my home and looked at 215

the Fishing at Dawn painting. Beltracchi’s reaction to seeing the painting for the first time was 216

priceless. It was like seeing a long-lost friend after years of separation. It was like Beltracchi 217

could not keep his/her eyes off the painting. Rene examined the painting closely and then told 218

me that he/she would be honored to be entrusted with the care of Fishing at Dawn and restoring 219

the painting to its original beauty. In addition, Beltracchi said that he/she had the perfect frame, 220

almost like it had been made just for it. 221

Rene talked to me about maintaining the quality of the painting once it had been 222

restored, including proper humidity levels, keeping it out of direct sunlight, proper methods to 223

hang the picture, and how to dust and clean it. Rene even suggested a place where he/she 224

thought the painting should be hung in my home. To enhance the painting, Beltracchi 225

suggested accent lighting and even recommended a contractor to do that work. Beltracchi also 226

recommended that I install added security measures given the significant value of the painting 227

and the lure of it for art thieves. Beltracchi made a recommendation for a security system 228

contractor, Jerry Schnurr, as well. Beltracchi won me over with all of his/her personal attention 229

and interest in making sure the painting would be preserved long-term. 230

29

Rene discussed his/her hourly fee for restoration work of $250.00 per hour plus the cost 231

of materials, including the frame, which would be $14,000.00. Rene noted that significant 232

restoration work was not necessary as the painting was in good condition. He/she estimated 233

30-40 hours of work and described in detail the work that would be performed to clean, make 234

repairs, and reframe it. 235

Rene could not start on the project immediately due to other pending projects and the 236

upcoming holidays. Beltracchi also explained he/she would need to work on it intermittently 237

between working on a significant project at a local school of restoring murals done through the 238

WPA. Beltracchi was also working on a mural at a local church. I was in no rush to get the 239

painting back. In fact, as I told Beltracchi, I had plans to leave right after Thanksgiving for a 240

four-month World Cruise. Satisfied with my arrangements with Beltracchi, I agreed to have 241

him/her do the restoration work and authorized him/her to pick-up the painting from my home 242

when he/she was ready to start the project. 243

Prior to departing for my World Cruise, I made arrangements for work to be done on 244

my house to upgrade the lighting and to upgrade my security system to safeguard the Colline 245

painting. The Schnurr Security Specialists began work on November 21st. I authorized the 246

contractors to release the painting to Beltracchi when he/she was ready to work on it. While I 247

was on my cruise, I received a text message confirming that Beltracchi had picked up the 248

painting on January 6, 2017. 249

I returned from my cruise on March 25th. I had no idea what news was in store for me. 250

Then on April 11, 2017, I received a call from Beltracchi. He/she said “Sit down. I have bad 251

news for you.” Beltracchi then told me that he/she had just begun the restoration work on the 252

painting and upon closer examination had discovered it was a forgery. Beltracchi told me that 253

he/she had notified FBI Special Agent Taylor Hanratty of the forgery and a federal investigation 254

had been started. Imagine my shock. Imagine my anger. Bryce Cutter and Charity Operations 255

Network had duped me. After I was informed by Special Agent Hanratty that the Justice 256

department would not be filing criminal charges in this matter, I consulted my own attorney 257

and we filed this lawsuit because one should be able to trust and rely upon the expertise of, and 258

statements made by, the auctioneer. 259

30

Statement of Rene Beltracchi

My name is Rene Beltracchi. I live at 309 East 5th Street in Des Moines, Iowa. For the past 1

eleven years, I have owned and operated The Art of Art, an art restoration business, also located 2

in Des Moines’ East Village. Specifically, I restore high-end master paintings. I also am a guest 3

art columnist for the Des Moines Tribune and blogger. 4

I primarily specialize and would consider myself a connoisseur of oil paintings by 5

Impressionists and American Impressionists. It is an art of immediacy and movement, of 6

candid poses and compositions, of the play of light expressed in a bright and varied use of 7

color. Impressionists were radicals. They violated the rules of traditional academic painting at 8

the time. Impressionists’ brush strokes are small, thin and short, but are visible. Their 9

paintings are characterized by the use of colors that are blended, but not smoothly, as was 10

customary, to achieve an effect of intense color vibration. They portray overall visual effects 11

instead of details. They used open composition with an emphasis on the accurate depiction of 12

light and its changing qualities. The subject matter of their paintings focused on realistic scenes 13

of modern life, with ordinary people, and used movement to illustrate the human perception and 14

experience. Impressionists often painted outdoors. Previously landscapes were usually painted 15

in a studio. 16

My restoration work includes preventing deterioration of paintings, repairing damages, 17

and re-framing the paintings. My business is successful, without advertising. Word of mouth 18

generates most of my business. I get referrals from numerous art galleries, art dealers, fine art 19

appraisers, collectors, and even museums. My ability to mirror the work of the masters in 20

order to preserve it is a critical component of my success as a restorer. I have a knack for 21

recreating the likeness of the artist’s original without disturbing the original painting and 22

decreasing its value. I have become well-respected in the inner sanctum of the art world 23

because when I restore a painting, I am meticulous about keeping the original art piece as true 24

as possible. I exercise great caution to not change the painting, or if I make changes to have 25

those changes documented and obvious. For example, I will use paints for the touch-up that are 26

chemically different than the original paint, so that they can be removed in the future without 27

damaging the original. 28

31

I am not a member of the Appraisers Association of America (AAA), nor am I a member 29

of the American Society of Appraisers (ASA). I also am not a member of the American Institute 30

for Conservation of Historical and Artistic Works (AIC). I do not need the labels to get referral 31

work. Not to say that I reject the purpose of establishing guidelines for this industry. As a 32

matter of fact, the manner in which I perform restoration work is consistent with AIC 33

guidelines. 34

I did not attend college, nor have any formal training in art restoration, appraisals, 35

forensics or art history. Instead, I have years of on the job training, so to speak. In my prior 36

life, I was an art forger. I forged several American Impressionists, and some have yet to be 37

discovered. A few of my forgeries are still hanging in museums. I never forged any works of 38

Emerson Colline, although I would have enjoyed the challenge of doing so. Her brushstrokes, 39

techniques, and visual acuity are quite unique. 40

I never forged for greed. Rather, I had been rejected by the art world for my original 41

works and so it was a sense of pride for me to pull off forged art to unsuspecting museum 42

curators, art galleries, and the like. To forge artwork also requires a cunning spirit. To be in on 43

the con, you have to project an image of expertise and sophistication that comes with years of 44

training. But the one thing that kept me from getting caught for many years was to follow the 45

cardinal rule of keeping lies to a minimum. I was turning around forgeries of major pieces in a 46

month to two months’ time. But it soon all caught up with me. My vanity got to me and I 47

started putting my initials hidden in the art work I forged. It was my little joke on the art 48

world. That’s how FBI finally caught me, and I landed in prison. My imprisonment for art 49

forgery hurt my family, and I vowed that when I got out I would lead an honest life. Shortly 50

after my release, I met with film producer and director Allyn Funt about a possible project to 51

bring light to the underworld of art forgery. As they say in the world of movies, the project is 52

still “in development.” 53

I ended my life of forgery, but I have used that knowledge, skill, and connoisseurship to 54

make an honest day’s wage. As you might expect, forgers make good conservators. My 55

experience as a forger has taught me the techniques and practices of individual artists, enabling 56

me to restore the work of an artist as if their hand was on my brush. I opened this little shop for 57

32

restoration work, and business has been great. I don’t hide the fact that I once was a con, 58

forging art work. I am completely upfront about it to all of my customers. In fact, my “bad” 59

reputation has been good for business. My ability to mimic almost identically an artist is a 60

much sought-after talent in art restoration. I have reaped personal rewards too. I now have 61

gained recognition and notoriety for my talents that I had to once hide as a forger. 62

As part of my transformation, and in a complete turnaround, I now work with the 63

Federal Bureau of Investigations to detect forgeries. I've turned a dark period of my life into 64

something good. People think a person can't change their stripes, but I am living proof that you 65

can. The FBI uses my expertise as a former forger to determine attribution and authenticity of a 66

painting. In addition to aiding the FBI in the detection of art forgeries, my experience with 67

known forgers has been helpful to the government to identify the forger. You see, I have the 68

unique experience, unlike most art experts, of recognizing a forger’s work, as well as the work 69

of particular artists. I am not a detective, nor am I trained as one. My training is in street 70

smarts, which candidly sometimes the stodgy FBI agents lack. I like to think of myself as an art 71

sleuth. I approach detecting forgeries by looking for clues. The more clues I have, the more I 72

learn about the forger, the more I am able to fit the clues together and wrap up a case. I’m 73

much like Sherlock Holmes. Each case is a study in collecting and analyzing clues, then 74

drawing logical conclusions from the clues. 75

The perception that an art piece was created by the artist is critical to its desirability and 76

salability. A buyer wants to believe that the art piece represents the artist's creative genius and 77

vision. Many artworks have value because of their attribution. A big name brings big bucks. 78

Unfortunately, art is an appealing target for a forger, and easier to get away with than forgers of 79

currency. A forger's mission is to create something that will be accepted as genuine and have 80

value, and it must go undetected by those who are practiced at examining a particular artist. 81

Through my blog, I try to help educate the public on acquiring art. Many people are 82

under the delusion that acquiring art is a solid investment. The best way to double your money 83

is to not buy art, but rather take your money out of your wallet, fold it in half and put it back in. 84

The perception that art is an investment is perpetuated by the myth that art always goes up in 85

value. While the myth may be true in certain circumstances, buyers should not accept this 86

33

wholesale. Buyers need to do their homework, know who they are dealing with, and refer 87

questions about a potential purchase to an art professional, such as an appraiser. 88

Buyers can be fooled by the "packaging" of a painting. If it looks old, it must be old, 89

right? For example, reproductions of seventeenth century paintings can be dummied up to look 90

authentic by using a top-grade color printer, gluing it on oak panels, then highlighting with oil 91

paint in places. You package up what appears to be an original in an elaborate gold frame, and 92

the painting appears to be more than it is. It is an easily affordable technique to masquerade as 93

an original antique oil painting. Also, it is common for a painting to be inherited and the later 94

generations believe they have a prize possession when, in fact, the artwork is merely decorative 95

art that looks like it could be something of value. 96

Nor should a buyer rely upon a Certificate of Authenticity (COA). Many COAs are 97

faked and forged, and simply are not reliable. Traveling charity auction companies and internet 98

sellers are notorious for offering a certificate of authenticity, such that there is now a cottage 99

industry willing to fabricate COAs. In many galleries, and particularly traveling charity auction 100

companies, the truth is replaced by a fictional narrative. 101

The Certificate of Authenticity is one of the most misunderstood and abused tools in the 102

art market. The only person who can authenticate a work of art is the person who created it. In 103

other words, the only certificate that matters is the one signed by the artist himself or herself. 104

All other certificates are merely opinions of authenticity and are only as valid and credible as 105

the reputation of whoever signed it and the extent of the research they performed to arrive at 106

their opinion. A certificate of authenticity does not become more valid if it is printed on special 107

paper with a fancy border and a gold seal. To be useful, a COA should contain the name, 108

nationality, and life dates of the artist, the title of the artwork, the medium, dimensions, location 109

and medium of the artist's signature, identification of the person signing the certificate and the 110

date, and most important, a guarantee of the truthfulness of the information. If a dealer or an 111

auctioneer is unwilling to provide a money back guarantee, there is reason to doubt the veracity 112

of the information provided by that dealer or auctioneer. Yet, I find it amazing how people are 113

so willing to accept a certificate that provides no guarantee. 114

People get the art they deserve. If you don’t enter the art market with a level of 115

34

sophistication you become fair game. Even those considered to be collectors and art aficionados 116

are in danger of buying a forgery attributed to a famous artist. They trust the dealer or auction 117

company and do little to nothing to obtain an independent opinion or scholarly review. The 118

best advice I can give any buyer of fine art, especially a novice buyer, is to rely upon an 119

independent expert, such as an appraiser. 120

A conservator is practiced in the art of looking at art as a physical object, paying less 121

attention to its content, like that of an art historian or connoisseur. The conservator is looking 122

closely at the painting to determine what needs to be restored. The initial visual inspection by 123

the conservator isn’t undertaken to determine authenticity. That’s not why you are hired. 124

Nevertheless, in some instances, just looking at the painting to do the conservation work reveals 125

something suspicious. 126

For me, the first thing about spotting a fake is something just seems a bit off. Something 127

seems not right. A forger almost always unintentionally incorporates something of his or her 128

own nuances to a painting. I have used my gut instincts to uncover other fakes because the 129

forger was not careful enough to do a thoroughly convincing job. If one develops an expertise 130

in a particular artist's works, that expert will trust their initial response to an art piece and 131

usually know at first contact that something is not right. As in many other professions, your 132

brain compares available data with prior experiences. Anomalies always raise red flags and 133

demand an explanation. The clues are always there. I find that 99% of the time, if I follow the 134