the uk retail market - bordbia.ie · tankers, like coke and cadbury acquiring speedboats (innocent...

TRANSCRIPT

Achieving breakthrough and increasing your sales and distribution

The UK Retail Market

The good news is, it is usually easier to innovate and change direction if you are a smaller progressive company – innovation and differentiation will always be the key to success.

Big manufacturers and retailers recognise the benefits of this type of business and we have seen tankers, like Coke and Cadbury acquiring speedboats (Innocent and Green & Blacks) as part of their innovation and growth strategies.

We are a small company with big ideas for growth in the UK – how can we be successful?

The big manufacturers and retailers are like tankers – it is difficult for them to change direction.

Smaller businesses are like speedboats – they can change direction quickly.

Naturalness Better ingredients Modern technology

The UK retailers are looking to add value to developed categories – these innovative brands have driven incremental growth by building on common trends...

Delivering better taste

Stronger personality and brand experience

Their success was due to their clear point of difference – in Packaging (stands out), Product (quality), and Price (which in these cases is higher)

The most compelling reason for a retailer to list you, is if you have something different and innovative but before you commit to the UK market, you need to understand it and how it works………

Understanding the dynamics/rules of engagement of the UK market

• Is your business fully committed to supplying the UK?

• Do you have the expertise/people/systems?

• Is the factory capable of supplying the customer? Do you have enough capacity?

• Is the supply chain set up to meet the demands -

warehouse/logistics/system/forecasting/technology/production

planning/technical recall.

• Is there an understanding of the service levels required?

• How will customer service levels be monitored?

• How will any issues be communicated to the customer?

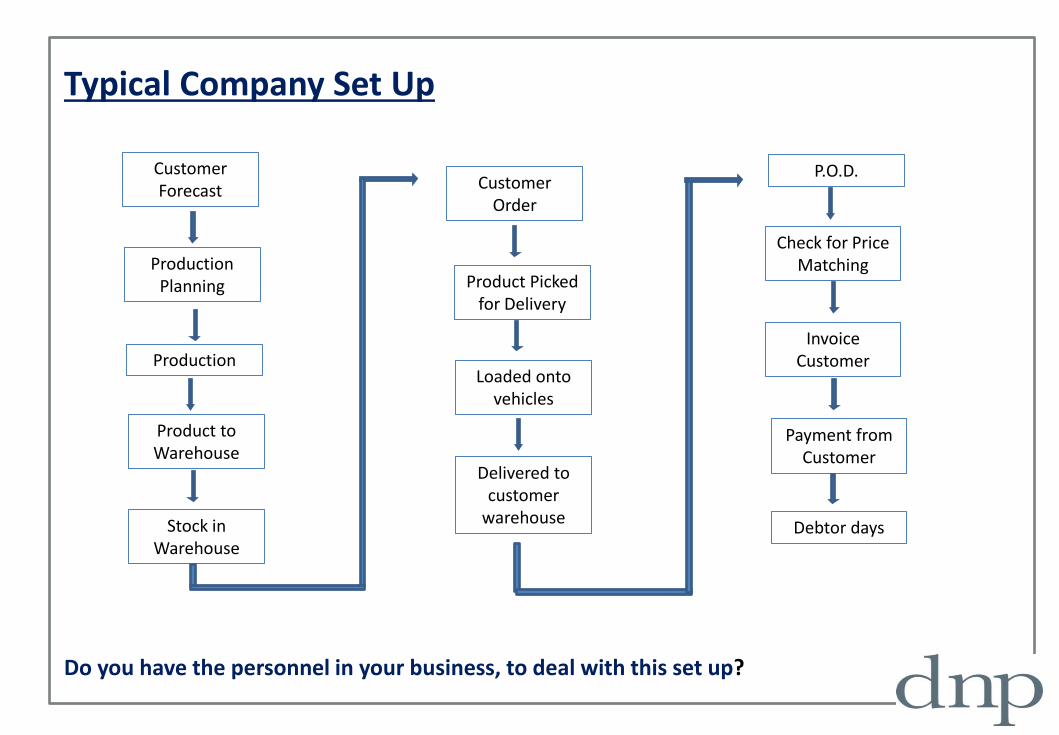

The next slide shows how a typical food and drink business should function…..

Typical Company Set Up

Customer Forecast

Production Planning

Production

Product to Warehouse

Stock in Warehouse

Customer Order

Product Picked for Delivery

Loaded onto vehicles

Delivered to customer

warehouse

P.O.D.

Check for Price Matching

Invoice Customer

Payment from Customer

Debtor days

Do you have the personnel in your business, to deal with this set up?

Understanding the Category/Market that you are entering

Pitching the product at the right cost price and retail price – Is it a brand or retailer label?

Marketing Support – Do you appreciate/understand what is going on around you, within the category?

Advertising – What is affordable/what works best for your product/category

Promotional Activities - When is the best time to promote? Christmas/Easter/Summer? - What are the promotional implications for you, the supplier?

- Increased costs/volumes/factory capacities and capabilities/forecasting/warehousing/logistics/packaging

- Underlying costs of the activities? What are they? - Effect on your margins? - Ask the question of your business – do you fully understand the costs involved within the

category?

Don’t forget, the overall objective is to make profit!

Still up for the challenge?

• All your homework is done. You’ve answered yes to all the questions, now which retailer should you approach. Which retailer is best suited to you and your products.

• Please give this careful consideration. Your business maybe more suited to convenience and independents. It is not always about the BIG 4.

The next slide gives you an overview of the UK market….

Share of

Total Grocers Penetration £ Spend per Visit

2012 2013 %

Value

Change

2012 2013 %

Change 2012 2013 %

Change

Pre- Family

New Family

Maturing Family

Established Family

Post Family

Older Couples

Older Singles

Mega Convenience Small Large Super

52 we data

to 20.07.13

Store Numbers

as of 20.07.13

Store Numbers

SOT based on Total FMCG, Benchmark Total Grocers

% Change Penetration = % Change in actual buyers

Value Index

(52 we 20.07.13) Total

Store Portfolio

Lifestage

Share of Trade

28.4% 28.2% 3.4% 86.2 85.5 0.2% 26.72 27.58 3.2%

16.4% 16.4% 4.2% 67.3 68.2 2.3% 26.49 26.77 1.1%

15.5% 15.4% 3.0% 70.4 72.6 4.2% 28.89 28.38 -1.8%

12.1% 11.9% 2.3% 62.4 62.6 1.3% 23.89 24.33 1.8%

5.5% 5.4% 2.3% 54.6 53.8 -0.4% 9.61 9.59 -0.2%

4.8% 5.1% 10.2% 25.6 26.8 6.1% 22.85 23.98 4.9%

3.4% 4.4% 34.2% 39.9 44.6 12.8% 15.97 18.07 13.1%

4.3% 3.9% -4.5% 49.9 49.1 -0.6% 15.77 14.57 -7.6%

3.3% 3.4% 8.4% 41.9 45.5 9.5% 14.54 14.12 -2.9%

2.5% 2.5% 5.9% 42.0 43.2 3.8% 12.81 13.02 1.6%

2455 1572 30 314 178 361

1120 546 47 177 152 198

521 0 114 73 94 240

510 13 28 192 229 48

3912 2717 928 267 0 0

295 7 49 196 36 7

733 274 285 162 10 2

762 82 680 0 0 0

127 110 124 108 93 91 86

119 95 95 88 107 99 103

91 127 133 135 104 83 67

80 99 76 96 100 115 102

67 81 67 79 103 104 156

102 110 74 85 105 113 97

67 100 96 102 94 115 90

60 37 45 57 101 135 148

58 87 79 86 86 128 106

82 106 128 142 107 74 93

Before you decide who you want to work with…..

This is where the retail market is expected to be over the next few years

43.6%

20.5% 21.0%

5.6% 3.9% 5.4%

38.9%

18.2%22.4%

9.0% 7.1%4.4%

Superstores and Hypermarkets

Small supermarkets

Convenience Discount Online Other

2013 2018

Convenience, online and discount to grow fastest

Store

remodelling will be key to reviving sales with a focus

on fresh, foodservice and creating a more

welcoming experience

Targeting the

mini-main mission, alongside showing

relevance, convenience and value are key to

lifting performance

Tailored format

rollouts and mission-specific

ranging will drive growth

New store development and a wider and more engaged

shopper base will sustain

growth at both food and high

street discounters

Flexible fulfilment

solutions, new market

entrants and a better

understanding of the online shopper will

be key

Poorly

differentiated retailers will struggle to

compete, but niche

specialists could prosper

Channel value change £bn

2013-2018: +6.0 +2.5 +10.6 +9.1 +8.1 -0.2

These three channels will be the clear out-performers over the next five years, being closely aligned with shoppers’ increasing desire for convenience and value. Together they will account for over £3 in every £4 of the cash growth in the market to 2018.

Shopper behaviour

The next slide shows what shoppers are doing

- How they are behaving

- What they are looking out for.

You need to bear this in mind, as you prepare your plan for the UK.

How will these shopper behaviours affect your UK strategy?

Shoppers remain defensive In spite of more positive media coverage, shoppers remain very defensive, with reference to grocery shopping

This suggests that volumes in UK grocery will remain under pressure for some time to come

Do you think you will do less or more of the following, next 6 months (top 15 answers)?

Source: ShopperVista, IGD Research, September 2013 (fieldwork: June 2013, Top 10 items only)

Base: 1,000 main shoppers, balanced sample IGD ShopperVista

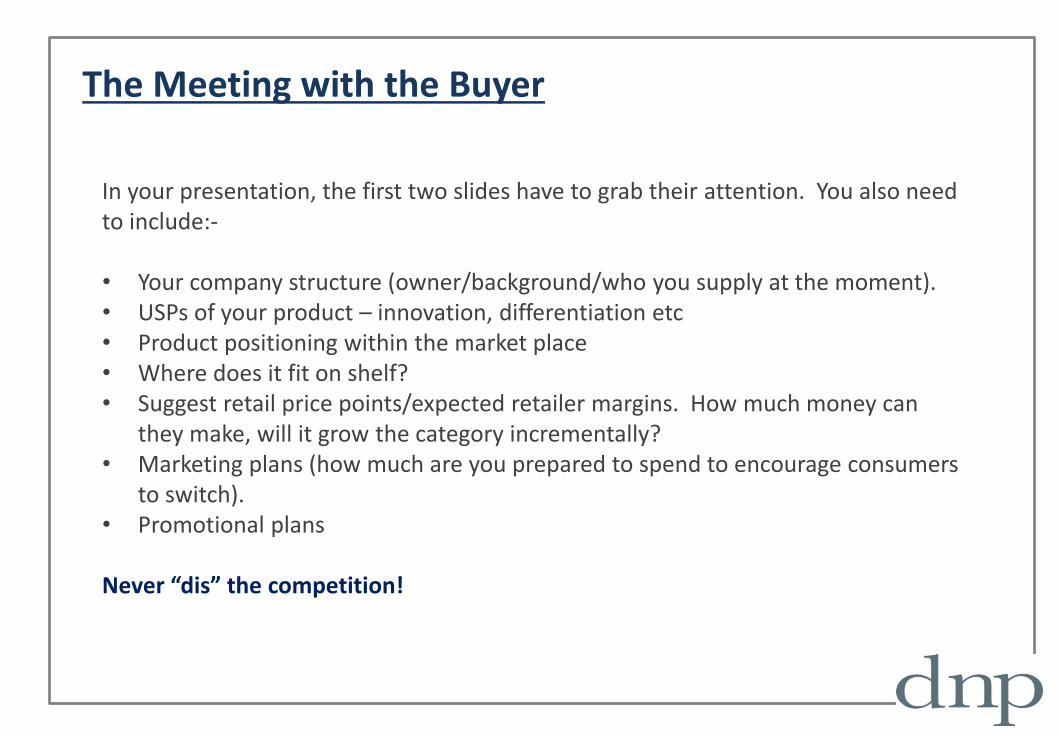

The Meeting with the Buyer

A typical buyer could be buying a 1000 different lines (sometimes across several categories). They expect you to be the expert. You have to know your particular category, better than they do. In the meeting, they need to know what’s in it for them quickly - engage them immediately. Keep your presentation simple but impactful. Buyers are time poor. Important points: • Your personality and that of the brand has to be very evident • Your passion for your product is pivotal • Professionalism is a given • Confidence is a must • Knowledge is king • Make them feel that they will lose out, if decide not to list you

The first meeting with the buyers has to be the best!

In your presentation, the first two slides have to grab their attention. You also need to include:- • Your company structure (owner/background/who you supply at the moment). • USPs of your product – innovation, differentiation etc • Product positioning within the market place • Where does it fit on shelf? • Suggest retail price points/expected retailer margins. How much money can

they make, will it grow the category incrementally? • Marketing plans (how much are you prepared to spend to encourage consumers

to switch). • Promotional plans Never “dis” the competition!

The Meeting with the Buyer

You have a listing!!!!!

Take a moment to celebrate, then down to business – how to maintain the listing and importantly, grow the business (above and below the line marketing activity and support).

6 weeks later, you have a listing!

What to do next?

Firstly, find out • How many stores you will be in? • What is the retail price “likely” to be? • Exact listing date? • Exact first delivery date? • Will there be an allocation of product to stores and how much?

You then need to ensure that you keep your listing and growth. How are we going to do this?

Above the line activity/typical communication opportunities

In-store Sampling

Retailer magazine

6 Sheet poster campaign and foyer

/ in store media

Retailer In-store Radio

Retailer website advertising

Merchandise for in store colleagues

Below the line activity (promotions)

Period P1 P2 P3 P4 P5 P6 P7 P8 P9 P10 P11 P12 P13 P14 P15 P16 P17

Weeks 3 3 3 3 5 3 3 3 3 3 3 3 3 3 2 3 3

Promo start in storeTue. 27-Dec 17-Jan 07-Feb 28-Feb 20-Mar 24-Apr 15-May 05-Jun 26-Jun 17-Jul 07-Aug 28-Aug 18-Sep 09-Oct 30-Oct 13-Nov 04-Dec

Promo end in store Mon. 16-Jan 06-Feb 27-Feb 19-Mar 23-Apr 14-May 04-Jun 25-Jun 16-Jul 06-Aug 27-Aug 17-Sep 08-Oct 29-Oct 12-Nov 03-Dec 24-Dec

Nom Creamy

Singles

Better

than 1/2

price 30p

Nom Creamy 6

Pack

Rollback

to £2

Nom Favourites

ROLLBACK £0.40 ROLLBACK £0.40

Rollback to £2 EDLP £2.50 EDLP £2.50

EDLP £1.38

EDLP 50p EDLP 50p

SUPERMARKET DISTRIBUTION ONLY PLAN TO GET INTO MAIN ESTATE

4 for £2 4 for £2

£2.50 any 2 for £4 Rollback to £2£2.50 any 2 for £4

£1.38 any 2 for £2 Rollback to £1 EDLP £1.38

• A bespoke plan that you can deliver and is likely to be pre-agreed upon listing with the buyer – the

deeper the promotion the higher the volume, can you cope with the volume demand?

• Promotions will have to be in line with retailer themes – also to gain discretional space (i.e: Gondola

end) this will cost you!

• Promotions work differently with different product groups.

More than 50% of all food sales today are achieved through price promotions – this will be and should be your biggest investment – you need to get this right!

Managing and growing your business

• In the UK, communication is so important with the buyer.

• Monitor the sales as often as possible – each day/week.

• If your plan isn’t working, change it.

• Be working on new ideas.

• Be ahead of your competitors.

• Get into a place where you are the best supplier.

In Summary – To be successful

PEOPLE Knowledge - Expertise - Commitment - Have the right people in your business

PRODUCTS Continue to innovate as innovation is key - Packaging, products, improve taking cost out where you can but not on quality

COMMUNICATION/

PROMOTIONS Must be effective - Have a plan - Be creative with promotions - Ensure that you are getting a return on your investments - Bringing in new consumers - Switching consumers to your product

PRICES Competitive within its competitive set – not cheap! - Don’t forget your margins – ensure that you build enough into your cost prices, to be able to pay for any support.

Finally,

Be committed Don’t do this tentatively – it won’t work. And as I said in the first slide, continuous innovation and differentiation will always be the key to a successful, sustainable business. `