the university of chicago law school 66th annual … university of chicago law school 66th annual...

TRANSCRIPT

The University of Chicago Law School

66th Annual Federal Tax Conference

Corporate Inversions

Chicago, Illinois

November 8, 2013

Page 2

Panel

► Session Chair: Hal Hicks, Skadden, Arps, Slate, Meagher

& Flom LLP

► Presenting this Topic: Steven M. Surdell, Ernst & Young

LLP

► Commenting on this Presentation: Lewis R. Steinberg,

Credit Suisse (USA) LLC, John J. Merrick, Special

Counsel to the Associate Chief Counsel (International),

Internal Revenue Service

Page 3

Premise

► Inversion (or Expatriation) Transactions are not going away.

The competition to acquire productive business assets around the world will

continue. This competition will likely be waged primarily by large multinational

corporations that are subject to various taxing jurisdictions and thus a myriad of

international tax rules. Regardless of one’s broader view of the merits of different

international tax regimes (e.g., whether you support “capital export neutrality” or

“capital import neutrality”) the application of different international tax regimes to a

single set of productive assets will affect the value of those assets in the hands of

various bidders. This will force bidders to examine (particularly where the subject

assets constitute an important pre-tax strategic opportunity) whether it makes

economic sense to consider reincorporating in a jurisdiction whose international tax

rules allow it to more efficiently hold (and thus bid on) the productive assets.

Although this panel will not comment on the broader issues of the US international

tax system cross border merger and acquisition transactions present an excellent

prism through which to illustrate those issues.

The observation above is supported by decisions taken in at least some of the

recent cross border combination transactions.

Page 4

The phenomenon of locally incorporated entities reincorporating in jurisdictions

deemed more advantageous to a multinational corporation is not unique to the US.

Consider the recent experience of the UK with its multinationals inverting and how

the UK responded to those actions.

Significantly, although the conventional wisdom is that new waves of inversions

occurred because creative tax planning identified ways to circumvent earlier

limitations, in reality the analysis is far more complex. In many circumstances

outside economic and legal considerations (which were external to US international

tax rules) helped to drive the new wave of inversions.

Premise

Page 5

A Brief History of Inversion Transactions

► Illustrative Transactions

► Response

► Tax Policy Implicated by Each Response

Page 6

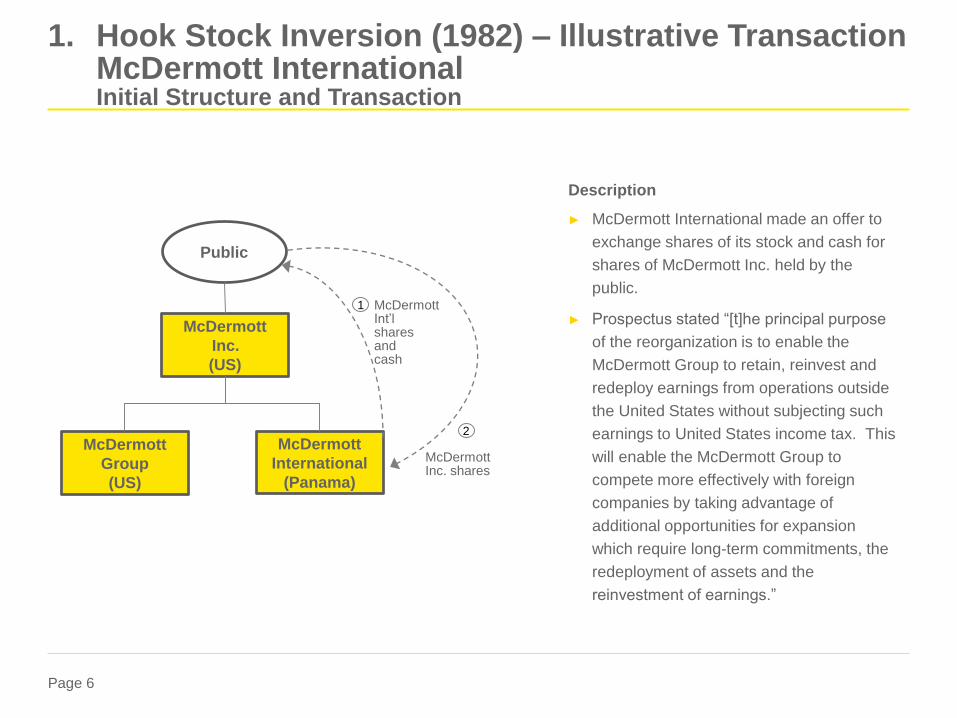

1. Hook Stock Inversion (1982) – Illustrative Transaction McDermott InternationalInitial Structure and Transaction

Description

► McDermott International made an offer to

exchange shares of its stock and cash for

shares of McDermott Inc. held by the

public.

► Prospectus stated “[t]he principal purpose

of the reorganization is to enable the

McDermott Group to retain, reinvest and

redeploy earnings from operations outside

the United States without subjecting such

earnings to United States income tax. This

will enable the McDermott Group to

compete more effectively with foreign

companies by taking advantage of

additional opportunities for expansion

which require long-term commitments, the

redeployment of assets and the

reinvestment of earnings.”

McDermott

Inc.

(US)

McDermott

International

(Panama)

Public

McDermott

Group

(US)

1

2

McDermottInt’lsharesandcash

McDermottInc. shares

Page 7

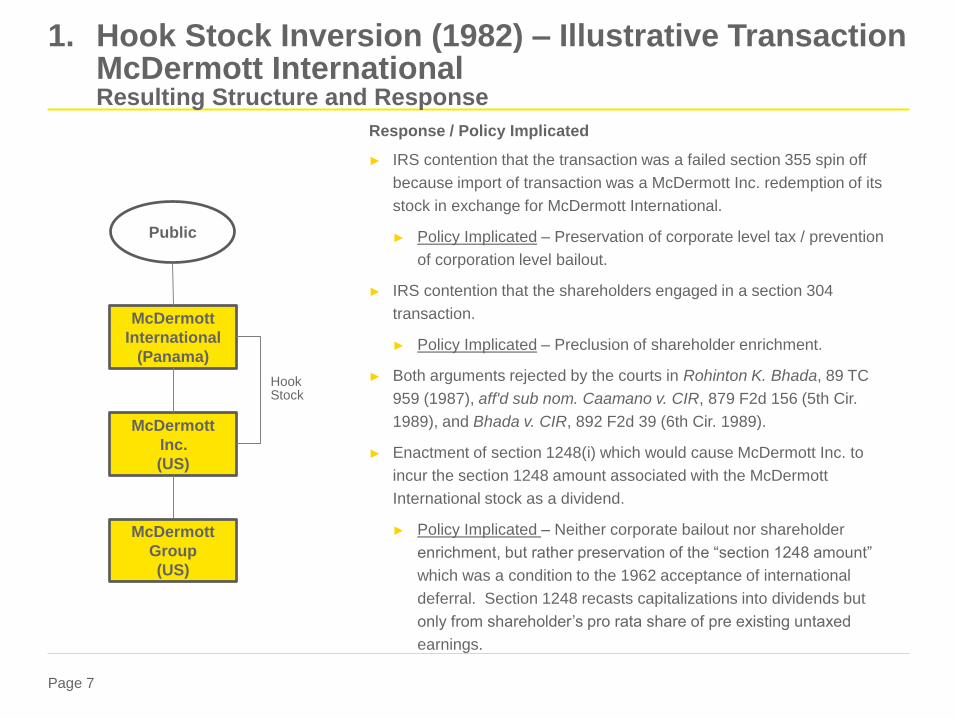

1. Hook Stock Inversion (1982) – Illustrative Transaction McDermott InternationalResulting Structure and Response

Response / Policy Implicated

► IRS contention that the transaction was a failed section 355 spin off

because import of transaction was a McDermott Inc. redemption of its

stock in exchange for McDermott International.

► Policy Implicated – Preservation of corporate level tax / prevention

of corporation level bailout.

► IRS contention that the shareholders engaged in a section 304

transaction.

► Policy Implicated – Preclusion of shareholder enrichment.

► Both arguments rejected by the courts in Rohinton K. Bhada, 89 TC

959 (1987), aff'd sub nom. Caamano v. CIR, 879 F2d 156 (5th Cir.

1989), and Bhada v. CIR, 892 F2d 39 (6th Cir. 1989).

► Enactment of section 1248(i) which would cause McDermott Inc. to

incur the section 1248 amount associated with the McDermott

International stock as a dividend.

► Policy Implicated – Neither corporate bailout nor shareholder

enrichment, but rather preservation of the “section 1248 amount”

which was a condition to the 1962 acceptance of international

deferral. Section 1248 recasts capitalizations into dividends but

only from shareholder’s pro rata share of pre existing untaxed

earnings.

McDermott

Inc.

(US)

McDermott

International

(Panama)

Public

McDermott

Group

(US)

HookStock

Page 8

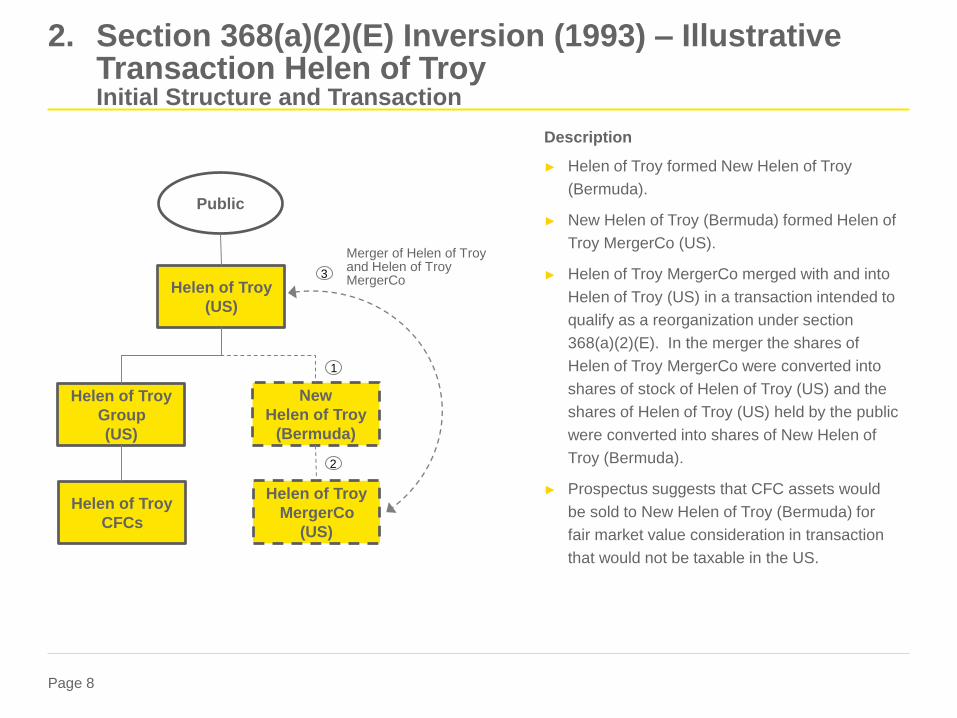

2. Section 368(a)(2)(E) Inversion (1993) – Illustrative Transaction Helen of TroyInitial Structure and Transaction

Description

► Helen of Troy formed New Helen of Troy

(Bermuda).

► New Helen of Troy (Bermuda) formed Helen of

Troy MergerCo (US).

► Helen of Troy MergerCo merged with and into

Helen of Troy (US) in a transaction intended to

qualify as a reorganization under section

368(a)(2)(E). In the merger the shares of

Helen of Troy MergerCo were converted into

shares of stock of Helen of Troy (US) and the

shares of Helen of Troy (US) held by the public

were converted into shares of New Helen of

Troy (Bermuda).

► Prospectus suggests that CFC assets would

be sold to New Helen of Troy (Bermuda) for

fair market value consideration in transaction

that would not be taxable in the US.

Helen of Troy

(US)

New

Helen of Troy

(Bermuda)

Public

Helen of Troy

Group

(US)

1

2

Helen of Troy

MergerCo

(US)

Helen of Troy

CFCs

3

Merger of Helen of Troy and Helen of Troy MergerCo

Page 9

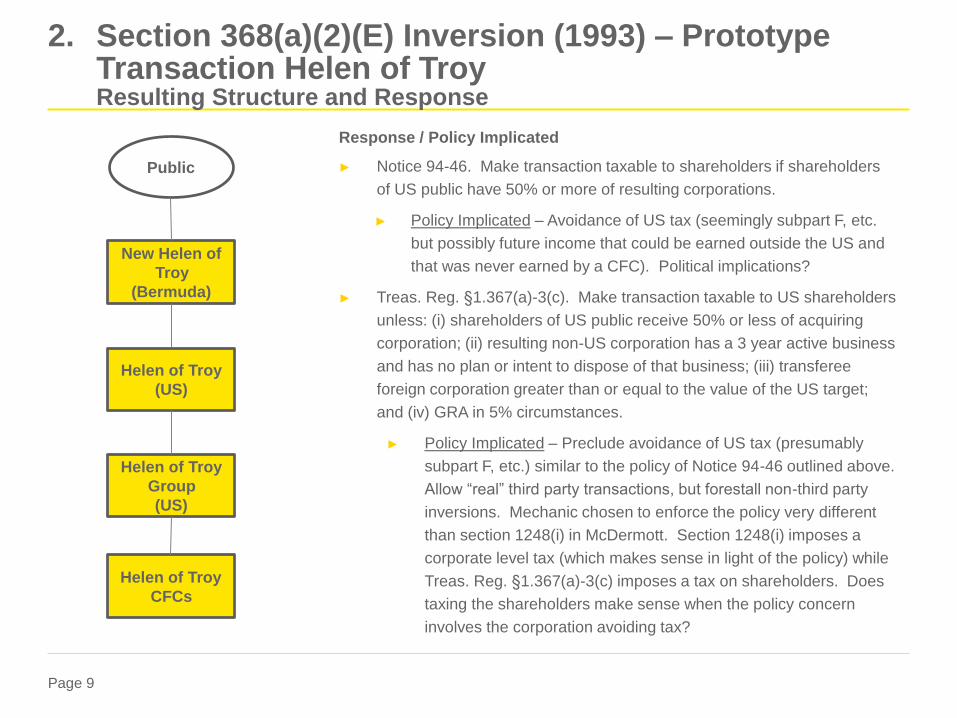

2. Section 368(a)(2)(E) Inversion (1993) – Prototype Transaction Helen of Troy Resulting Structure and Response

Response / Policy Implicated

► Notice 94-46. Make transaction taxable to shareholders if shareholders

of US public have 50% or more of resulting corporations.

► Policy Implicated – Avoidance of US tax (seemingly subpart F, etc.

but possibly future income that could be earned outside the US and

that was never earned by a CFC). Political implications?

► Treas. Reg. §1.367(a)-3(c). Make transaction taxable to US shareholders

unless: (i) shareholders of US public receive 50% or less of acquiring

corporation; (ii) resulting non-US corporation has a 3 year active business

and has no plan or intent to dispose of that business; (iii) transferee

foreign corporation greater than or equal to the value of the US target;

and (iv) GRA in 5% circumstances.

► Policy Implicated – Preclude avoidance of US tax (presumably

subpart F, etc.) similar to the policy of Notice 94-46 outlined above.

Allow “real” third party transactions, but forestall non-third party

inversions. Mechanic chosen to enforce the policy very different

than section 1248(i) in McDermott. Section 1248(i) imposes a

corporate level tax (which makes sense in light of the policy) while

Treas. Reg. §1.367(a)-3(c) imposes a tax on shareholders. Does

taxing the shareholders make sense when the policy concern

involves the corporation avoiding tax?

Helen of Troy

(US)

New Helen of

Troy

(Bermuda)

Public

Helen of Troy

Group

(US)

Helen of Troy

CFCs

Page 10

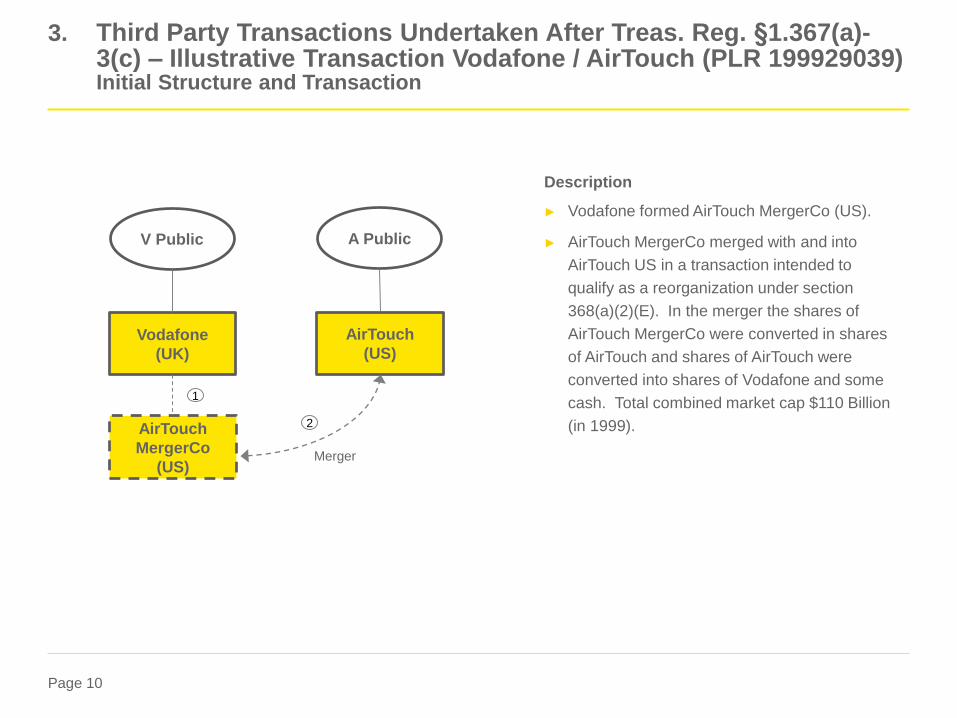

3. Third Party Transactions Undertaken After Treas. Reg. §1.367(a)-3(c) – Illustrative Transaction Vodafone / AirTouch (PLR 199929039)Initial Structure and Transaction

Vodafone

(UK)

V Public

AirTouch

(US)

A Public

AirTouch

MergerCo

(US)

1

2

Merger

Description

► Vodafone formed AirTouch MergerCo (US).

► AirTouch MergerCo merged with and into

AirTouch US in a transaction intended to

qualify as a reorganization under section

368(a)(2)(E). In the merger the shares of

AirTouch MergerCo were converted in shares

of AirTouch and shares of AirTouch were

converted into shares of Vodafone and some

cash. Total combined market cap $110 Billion

(in 1999).

Page 11

3. Third Party Transactions Undertaken After Treas. Reg. §1.367(a)-3(c) – Illustrative Transaction Vodafone / AirTouch (PLR 199929039)

Vodafone

(UK)

Legacy

V Public

Legacy

A Public

AirTouch

(US)

Response / Policy Implicated

► PLR 199929039. Vodafone had traded at a higher market

capitalization than AirTouch for all but 3 days of the six

month period before announcement. However because

Vodafone had agreed to pay a premium for AirTouch (in

part because of bid competition) the market capitalization

of AirTouch at the time of the merger closing date would in

all likelihood exceed that of Vodafone.

► IRS exercised its discretion under Treas. Reg. §1.367(a)-

3(c)(9) to issue a PLR that the transaction was in

substantial compliance with the active trade or business

test.

► Policy Implicated – Allow third party transactions to

occur even if in a “merger of equals” (or a merger

where the US corporation was actually larger) the

parties chose a foreign jurisdiction as the resulting

corporation.

Page 12

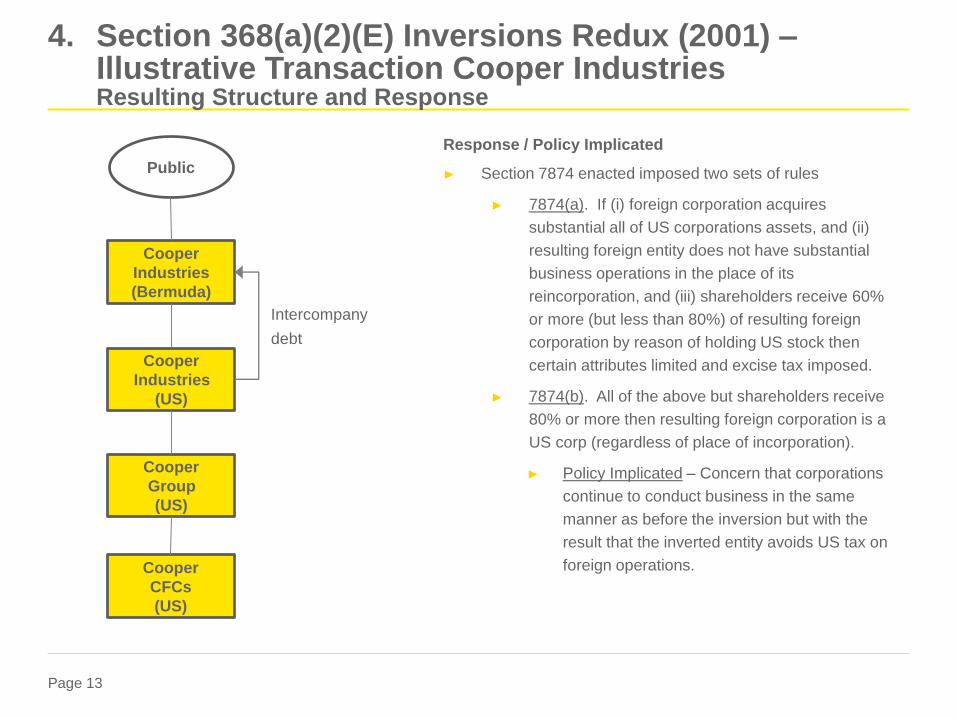

4. Section 368(a)(2)(E) Inversions Redux (2001) –Illustrative Transaction Cooper IndustriesInitial Structure and Transaction

Description

► Cooper formed Cooper (Bermuda).

► Cooper (Bermuda) formed Cooper MergerCo.

► Cooper MergerCo merged with and into Cooper

(US) in a transaction intended to qualify as a

reorganization under section 368(a)(2)(E). In the

merger the shares of Cooper MergerCo were

converted into shares of stock of Cooper (US) and

the shares of Cooper (US) held by the public were

converted into shares of Cooper (Bermuda).

Intercompany leverage inserted as part of the

transaction.

► Section 367(a) and Treas. Reg. §1.367(a)-3(c)

“worked” to impose a shareholder level tax. Belief

however was that due to large number of

institutional shareholders the shareholder level tax

did not act as a sufficient impediment to the

transaction occurring. In other words external

economic factors rendered the Treas. Reg.

§1.367(a)-3(c) toll change ineffective in certain

cases.

Cooper

Industries

(US)

New

Cooper

(Bermuda)

Public

Cooper

Group

(US)

1

2

Cooper

MergerCo

(US)

Cooper

CFCs

3

Merger of CooperIndustries andCooper MergerCo

Page 13

4. Section 368(a)(2)(E) Inversions Redux (2001) –Illustrative Transaction Cooper IndustriesResulting Structure and Response

Response / Policy Implicated

► Section 7874 enacted imposed two sets of rules

► 7874(a). If (i) foreign corporation acquires

substantial all of US corporations assets, and (ii)

resulting foreign entity does not have substantial

business operations in the place of its

reincorporation, and (iii) shareholders receive 60%

or more (but less than 80%) of resulting foreign

corporation by reason of holding US stock then

certain attributes limited and excise tax imposed.

► 7874(b). All of the above but shareholders receive

80% or more then resulting foreign corporation is a

US corp (regardless of place of incorporation).

► Policy Implicated – Concern that corporations

continue to conduct business in the same

manner as before the inversion but with the

result that the inverted entity avoids US tax on

foreign operations.

Cooper

Industries

(US)

Cooper

Industries

(Bermuda)

Public

Cooper

Group

(US)

Cooper

CFCs

(US)

Intercompany

debt

Page 14

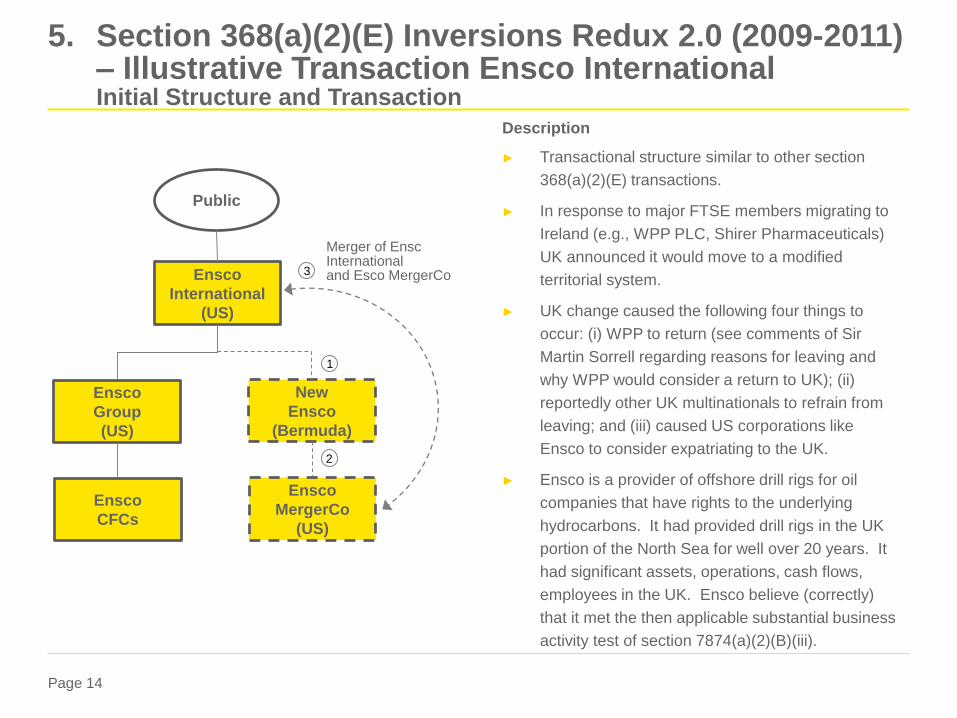

5. Section 368(a)(2)(E) Inversions Redux 2.0 (2009-2011) – Illustrative Transaction Ensco InternationalInitial Structure and Transaction

Description

► Transactional structure similar to other section

368(a)(2)(E) transactions.

► In response to major FTSE members migrating to

Ireland (e.g., WPP PLC, Shirer Pharmaceuticals)

UK announced it would move to a modified

territorial system.

► UK change caused the following four things to

occur: (i) WPP to return (see comments of Sir

Martin Sorrell regarding reasons for leaving and

why WPP would consider a return to UK); (ii)

reportedly other UK multinationals to refrain from

leaving; and (iii) caused US corporations like

Ensco to consider expatriating to the UK.

► Ensco is a provider of offshore drill rigs for oil

companies that have rights to the underlying

hydrocarbons. It had provided drill rigs in the UK

portion of the North Sea for well over 20 years. It

had significant assets, operations, cash flows,

employees in the UK. Ensco believe (correctly)

that it met the then applicable substantial business

activity test of section 7874(a)(2)(B)(iii).

Ensco

International

(US)

New

Ensco

(Bermuda)

Public

Ensco

Group

(US)

1

2

Ensco

MergerCo

(US)

Ensco

CFCs

3

Merger of EnscInternationaland Esco MergerCo

Page 15

► Speaking at the CEO Summit, organized by The Times, [Chancellor of the Exchequer

George] Osborne singled out WPP as an example of a UK business that had moved the

location of its headquarters from London to Dublin due to stringent tax laws, which mean UK

companies are charged corporate taxes for all overseas interests.

► Almost 90% of WPP Group revenue is earned outside the UK.

► Osborne said: "I want to reform the corporate tax system so that international

companies locate in Britain rather than leave Britain.“

► In April, Sir Martin Sorrell stated that he would be open to returning WPP's interests to the

UK if a new government changed the overseas tax law.

► And following the Chancellor's comments, Sorrell said he was, "delighted to hear the

Chancellor’s comment" and to hear the Chancellor and the prime minister "stress that Britain

must be open for business.“

► The move reduced the network's effective tax rate from 31.2% in 2008 to 23.5% in 2009.

► [Sir Martin Sorrell] "We made the move because it makes the tax planning process much

easier. You don't have to deal with the British Treasury trying to tax any of your foreign

profits."

5. Section 368(a)(2)(E) Inversions Redux 2.0 (2009-2011) – Illustrative Transaction Ensco InternationalInitial Structure and Transaction

Page 16

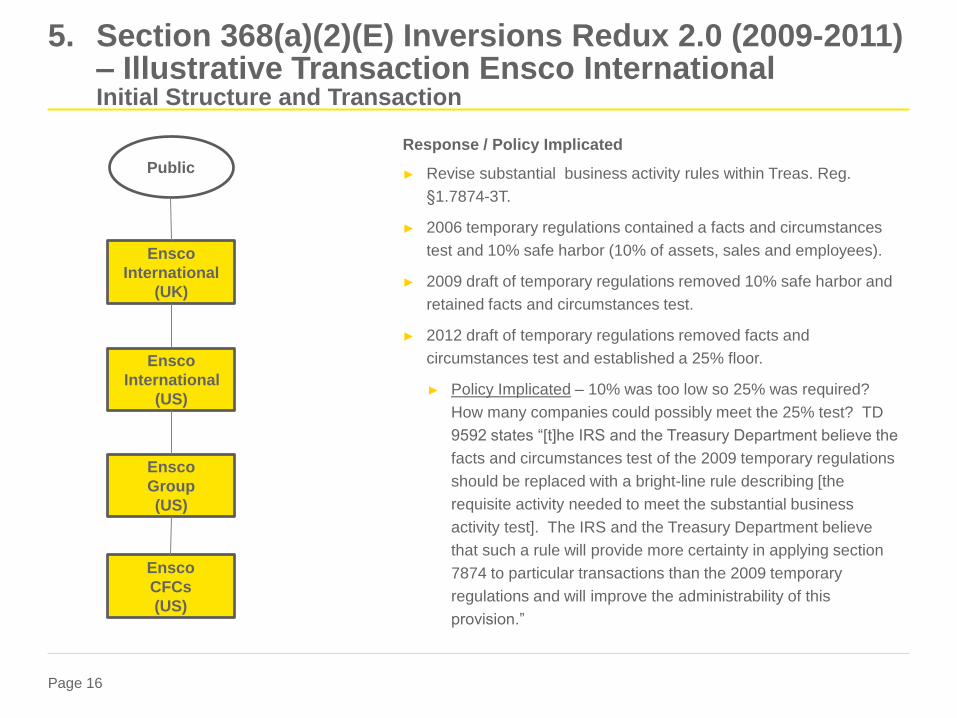

5. Section 368(a)(2)(E) Inversions Redux 2.0 (2009-2011) – Illustrative Transaction Ensco InternationalInitial Structure and Transaction

Response / Policy Implicated

► Revise substantial business activity rules within Treas. Reg.

§1.7874-3T.

► 2006 temporary regulations contained a facts and circumstances

test and 10% safe harbor (10% of assets, sales and employees).

► 2009 draft of temporary regulations removed 10% safe harbor and

retained facts and circumstances test.

► 2012 draft of temporary regulations removed facts and

circumstances test and established a 25% floor.

► Policy Implicated – 10% was too low so 25% was required?

How many companies could possibly meet the 25% test? TD

9592 states “[t]he IRS and the Treasury Department believe the

facts and circumstances test of the 2009 temporary regulations

should be replaced with a bright-line rule describing [the

requisite activity needed to meet the substantial business

activity test]. The IRS and the Treasury Department believe

that such a rule will provide more certainty in applying section

7874 to particular transactions than the 2009 temporary

regulations and will improve the administrability of this

provision.”

Ensco

International

(US)

Ensco

International

(UK)

Public

Ensco

Group

(US)

Ensco

CFCs

(US)

Page 17

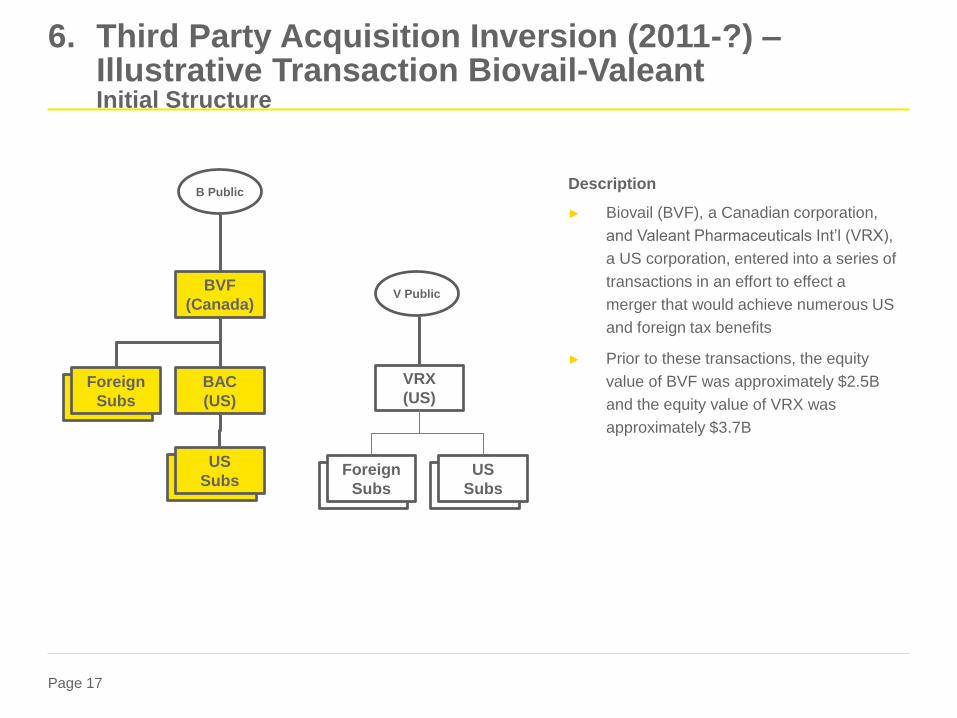

6. Third Party Acquisition Inversion (2011-?) –Illustrative Transaction Biovail-ValeantInitial Structure

Description

► Biovail (BVF), a Canadian corporation,

and Valeant Pharmaceuticals Int’l (VRX),

a US corporation, entered into a series of

transactions in an effort to effect a

merger that would achieve numerous US

and foreign tax benefits

► Prior to these transactions, the equity

value of BVF was approximately $2.5B

and the equity value of VRX was

approximately $3.7B

BVF

(Canada)

BAC

(US)

VRX

(US)

V Public

B Public

Foreign

Subs

US

SubsForeign

Subs

US

Subs

Page 18

Transaction Steps

► VRX obtains a $3B loan from Lenders

(the “VRX Debt”).

► VRX distributes $1.3B cash to VRX

shareholders. This shrinks the value of

VRX from $3.7B to $2.4B (thus making

its market cap less than that of BVF).

► Newly formed Merger Sub merges into

VRX with VRX surviving the merger.

Each VRX share is converted into 1.78

shares of BVF stock.

► BVF guarantees the VRX Debt.

BVF

(Canada)

BAC

(US)

Merger

Sub

VRX

(US)

Lenders

(4) Guarantee

(3b) BVF Stock

(3a) Merger

(1) $3B Loan

(2) $1.3B

Distribution

VRX

S/hs

6. Third Party Acquisition Inversion (2011-?) –Illustrative Transaction Biovail-ValeantTransaction Overview

Page 19

Intended US Tax Treatment

► Pre- distribution intended to be treated

as a Section 301 distribution, not Section

356 “boot” (See Reg. §1.368-1(e)(7), ex.

9).

► Merger intended to qualify as a B

Reorganization (Rev. Rul. 74-565).

► VRX shareholders avoid Treas. Reg.

§1.368(a)-3(c) shareholder level tax.

► Retention and utilization of BVF’s

existing corporate tax structure, which is

highly advantageous.

► Insertion of debt in the US.

BVF

(Canada)

BAC

(US)

VRX

(US)Lenders$3B Loan

VRX

S/hs

BVF

historic

ops

BVF

S/hs

~50.5% ~49.5%

Sources of Deal Consideration (Per Share)

Value %

Cash $16.77 53.5%

Shares $14.60 46.5%

Total $31.37 100%

6. Third Party Acquisition Inversion (2011-?) –Illustrative Transaction Biovail-ValeantResulting Structure

Page 20

Biovail-Valeant InversionSelect Key US Tax Issues

► Independence of the special distribution from the share-for-share exchange

► Qualification of the transaction as a B Reorganization

► Relevant to the Section 301 versus Section 356 treatment of the cash received

by VRX’s shareholders via the pre-merger distribution?

► Should the BVF guarantee affect the analysis? If so, how?

► Establishing the value of VRX on the closing date

► For the share exchange to remain tax-free, Section 367 requires that the FMV

of BVF’s equity equal or exceed the FMV of VRX’s equity at closing

► How do you establish value in the case of a pure share-for-share exchange –

fixed exchange ratio?

► Treatment of prior acquisitions by BVF in the 36-month pre-closing period?

Comparison of anti-inversion rules

Section 7874 Reg. §1.367(a)-3(c)

Consequence

if applicable

BVF will be taxed as a US corporation if 80% owned by

former VRX shareholders. Alternatively, if former VRX

shareholders own between 60% and 80% of BVF,

certain limitations apply to the use of VRX’s attributes to

offset “inversion gain”.

Gain or loss recognized by US shareholders of VRX. All

shareholders of VRX are presumed to be US persons

(subject to rebuttal).

Rule applies if: (i) BVF acquires substantially all the assets of VRX (the

“Acquisition Test”);

(ii) More than 60% (or 80%) of the BVF stock (by vote

OR value) is held by the former shareholders of VRX

(not just US shareholders) (the “Ownership Test”);

AND

(iii) BVF does not have substantial business activities in

its country of incorporation compared to the activities of

the “expanded affiliated group” (EAG) (the “Substantial

Business Activities Test”)

(i) More than 50% (by vote or value) of the stock of BVF is

received in the transfer by US transferors (presumed to be

all VRX shareholders);

(ii) More than 50% (by vote and value) of the stock of the

BVF is owned immediately after the transfer by US persons

that are either officers or directors of VRX or that are 5%

VRX shareholders;

OR

(iii) BVF fails the active trade or business test.

(Also a GRA requirement for 5% shareholders of VRX).

Internal group

restructurings

Reg. §1.7874-1(c) provides an “internal group

restructuring” exception to the ownership test in which

stock held by members of the EAG is included in the

denominator for purposes of the Ownership Test

Effectively permits certain internal restructurings to

avoid application of §7874.

Section 367(a) applies to internal restructuring transactions

without any special exceptions for internal transactions.

Internal transactions remain subject to all of the rules of

§367(a) and must satisfy the usual exceptions to

qualify for nonrecognition treatment.

Page 21

Comparison of anti-inversion rules

Section 7874 Reg. §1.367(a)-3(c)

Business test Based on facts and circumstances, including: (1)

conduct of continued business activities in Canada by

the EAG; (2) amount of (i) EAG property located in

Canada , (ii) services performed by employees of the

EAG in Canada and (iii) sales by EAG members to

customers in Canada ; (3) performance of substantial

managerial activities by EAG members, officers and

employees based in Canada ; (4) substantial degree of

ownership of the EAG by investors resident in Canada ;

(5) existence of business activities in Canada that are

material to the achievement of the EAG’s overall

business objectives.

• Business must be performed in BVF’s country of

incorporation

(1) BVF or its “qualified subsidiaries” (80%-owned

subsidiaries not affiliated with VRX before the transaction

and not acquired with the principal purpose of satisfying

the active trade or business test) must engage in the

active conduct of a trade or business outside the US for

the entire 36-month period immediately before the

transaction; (2) at the time of the transaction, there can be

no intention to substantially dispose of or discontinue such

trade or business; and (3) the entire value of BVF

(including BVF) must be at least equal to the entire value

of VRX.

• Active business may be performed outside BVF’s

country of incorporation

Effect of

acquisition of

BVF

-- Might be able to take into account business activities

of BVF and its subs to satisfy the Substantial Business

Activities Test, if necessary (but only if BVF and subs

are organized in same jurisdiction as BVF).

-- Activities of BVF may be relied on to satisfy the active

business test.

-- Cannot rely on business of its CFCs in this case.

Page 22

Comparison of anti-inversion rules

Section 7874 Reg. §1.367(a)-3(c)

Application of

rule

Taxpayers must “fail” one (but not all) of the

requirements (the Acquisition Test, the Ownership Test

or the Substantial Business Activities Test) to avoid the

application of §7874.

Taxpayers must meet all of the enumerated requirements

in order to qualify for nonrecognition treatment.

Page 23

Page 24

Policy Issues

► How do the recent inversion transactions (involving cross border combinations) differ

from historic inversion transactions?

► What underlying international tax policies were furthered by the responses to the

various historic inversion transactions?

► When reviewed collectively did the responses to the various historic inversion

transactions constitute a cohesive set of policies?

► Given the differences between the various historic inversion transactions and the recent

cross border combination transactions what international tax policy implications (if any)

are raised by the latter transactions?

► Given that many of the cross border acquisition provisions were enacted or

promulgated in response to transactions that occurred in arguably very different

economic circumstances is it time to rethink the applicability of all of those provisions?

► If we are rethinking these issues should broader macroeconomic issues inform the

international tax policy analysis of cross border transactions in general?

Should we encourage/discourage US multinationals to be the acquirers in these transactions?

Should we encourage/discourage non-US multinationals from being the acquirers in these

transactions?

Should this examination include the consideration of other international tax policy/economic

issues such as locations of headquarters, encouragement of employment in particular

jurisdictions, etc.