the u.s. economy and lodging demand the supply … october 23, 2015 ... • the u.s. economy and...

TRANSCRIPT

ECONOMETRIC ADVISORS

STATE OF THE U.S. LODGING INDUSTRY October 23, 2015

Robert Mandelbaum – Director of Research Information Services

2 ECONOMETRIC ADVISORS

• The U.S. Economy and Lodging Demand • The Supply Story • Tracking the Business Cycles of U.S. Hotels • U.S. Lodging Market Forecast • Profit Trends • Questions and Answers

PRESENTATION OUTLINE

3 ECONOMETRIC ADVISORS

HOTEL HORIZONS® FORECAST REPORTS Prepared For:

• 59 major cities • 6 national chain-scales • 6 location types

Five Year Forecasts Of:

• Supply • Demand • Occupancy • ADR • RevPAR

4 ECONOMETRIC ADVISORS

STR, Inc. • Historical rooms occupied, room available,

rooms revenue

• Pipeline of future hotel construction

Moody’s Analytics • Economic forecasts

HOTEL HORIZONS® FORECAST REPORTS Sources of Variables

ECONOMETRIC ADVISORS

THE U.S. ECONOMY AND LODGING DEMAND

6 ECONOMETRIC ADVISORS

THE ECONOMICS OF HOTEL DEMAND

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020Pe

rcen

t Cha

nge

(4 Q

tr. M

ovin

g Av

g.)

Demand Income Employment

Forecast

Source: Moody‘s Analytics; PKF-HR, a CBRE Company; STR, Inc.

7 ECONOMETRIC ADVISORS

THE OUTLOOK FOR THE DRIVERS THAT ARE MOST IMPORTANT TO HOTELS REMAINS FAVORABLE

-2.7%

2.0%

-1.9%

-8.2% -5.4%

-0.5%

1.3%

3.9% 1.7%

3.9%

2.7% 2.5%

-1.5%

2.9%

0.8%

4.6%

2.7% 1.9%

0.5% 0.1%

1.9% 1.1%

3.0% 3.8%

-0.9%

4.6% 4.3%

2.1% 0.6% 3.7%

2.6% 3.8% 3.7% 3.4% 3.4% 3.0%

-10

-8

-6

-4

-2

0

2

4

6

8

10

I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV

2008 2009 2010 2011 2012 2013 2014 2015 2016

(GOVERNMENT) Government consumption expendituresand gross investmentTRADE (Net exports of goods and services)

BUSINESS (Gross private domestic investment)

CONSUMERS (Personal consumption expenditures)These matter the most.

4.6%

GDP Component Forecast

Source: BEA, Moody’s Analytics, PKF Hospitality Research, a CBRE Company Hotel Horizons: September – November 2015, STR, Inc.

8 ECONOMETRIC ADVISORS

1. Average weekly hours, manufacturing 2. Average weekly initial claims for unemployment insurance 3. Manufacturers’ new orders, consumer goods and materials 4. ISM® Index of New Orders 5. Manufacturers' new orders, nondefense capital goods excluding aircraft

orders 6. Building permits, new private housing units 7. Stock prices, 500 common stocks 8. Leading Credit Index™ 9. Interest rate spread, 10-year Treasury bonds less federal funds 10. Average consumer expectations for business conditions.

THE CONFERENCE BOARD L.E.I. The ten components of The Conference Board Leading Economic Index® for the U.S. include:

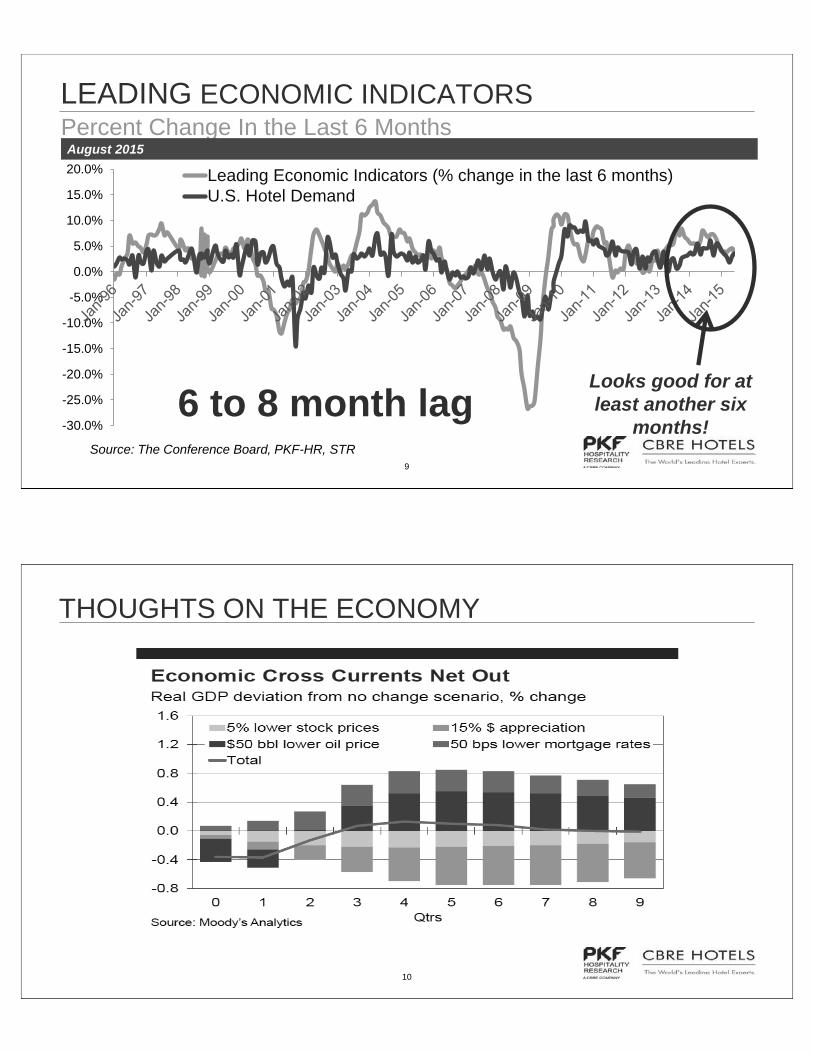

9 ECONOMETRIC ADVISORS

Percent Change In the Last 6 Months LEADING ECONOMIC INDICATORS

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0% Leading Economic Indicators (% change in the last 6 months)U.S. Hotel Demand

Source: The Conference Board, PKF-HR, STR

6 to 8 month lag Looks good for at least another six

months!

August 2015

10 ECONOMETRIC ADVISORS

THOUGHTS ON THE ECONOMY

11 ECONOMETRIC ADVISORS

THOUGHTS ON THE ECONOMY

ECONOMETRIC ADVISORS

THE SUPPLY STORY

13 ECONOMETRIC ADVISORS

When did we hit our last peak number of new hotels entering the market?

U.S. SUPPLY CHANGE

Long Run Average = 1.9%

4.0%

3.0%

-0.2%

0.8%

1.8%

2.8%

3.8%

4.8%

5.8%Forecast

Source: PKF Hospitality Research, STR, Inc.

Q2 1999 Q1 2009

14 ECONOMETRIC ADVISORS

U.S. Pipeline, Number of Rooms by Phase, August 2015 and March 2008

TODAY VS. THE PREVIOUS PEAK OF CONSTRUCTION ACTIVITY

Phase 2015 Q1/2008 % Difference Change

In Construction 132,401 207,468 -36.1%

Final Planning 175,090 113,419 54.4%

Planning 132,353 344,363 -61.6%

Active Pipeline 439,844 665,250 -33.9%

Source: STR, Inc.

2.5%

0.7%

3.5%

2.1%

Change from July 2015

15 ECONOMETRIC ADVISORS

1. Financing remains a challenge. 2. Elevated uncertainty that characterized this past cycle

has not yet been forgotten. 3. Construction costs are rising faster than property values

in many markets, undermining the feasibility of new development.

4. Scarcity of brands that lenders are willing to finance.

WHY SO LITTLE NEW CONSTRUCTION?

15

rands that lenders are willing to finance.citpty of b

A NEW DISRUPTOR?

17 ECONOMETRIC ADVISORS

Roughly 215,000 Units available in the U.S. (July 2015) AIRBNB – U.S.

Source: Insideairbnb.com (July 2015); PKF Hospitality Research, a CBRE Company

18 ECONOMETRIC ADVISORS

We Estimate 68% of Airbnb Units are competitive with U.S. Hotels HOW MANY ARE COMPETITIVE WITH HOTELS?

Source: Insideairbnb.com (July 2015); PKF Hospitality Research, a CBRE Company

65%

35%

Entire home/apt Private room95,169 Units = 182,495 Rooms

1.9 Rooms per Unit 50,651 Units

233,146 Competitive Rooms in the U.S.

05,000

10,00015,00020,00025,000

New

York,

NY

Los A

ngele

s/Lon

gBe

ach,

CASa

n Fran

cisco

/San

Mateo

, CA

Color

ado A

rea

Austi

n, TX

New

York

State

Rivers

ide/S

anBe

rnardi

no, C

A

Miam

i/Hial

eah,

FL

San D

iego,

CA

Wash

ington

, DC-M

D-VA Bo

ston,

MA

Califo

rnia N

orth

Chica

go, IL

Orlan

do, F

L

Seatt

le, W

A

Califo

rnia C

entra

lCo

ast

New

Orlea

ns, L

A

Massa

chus

etts A

rea

Sacra

mento

, CA

Portla

nd, O

R

Top 20 Markets

19 ECONOMETRIC ADVISORS

INDUCED SUPPLY?

Source: Insideairbnb.com (July 2015); PKF Hospitality Research, a CBRE Company, STR, Inc.

20 ECONOMETRIC ADVISORS

0%

5.0%

10.0%

15.0%

20.0%

25.0%

Austi

n, TX

New

York,

NY

Long

Islan

dSa

n Fran

cisco

/San

Mate

o, CA

Oakla

nd, C

ALo

s Ang

eles/L

ong B

each

, CA

Sacra

mento

, CA

Portla

nd, O

RMi

ami/H

ialea

h, FL

Seatt

le, W

ABo

ston,

MASa

n Dieg

o, CA

New

Orlea

ns, L

ASa

n Jos

e/Sa

nta Cr

uz, C

AOa

hu Is

land,

HINa

shvil

le, TN

Phila

delph

ia, PA

-NJ

Fort

Laud

erdale

, FL

Charl

eston

, SC

Phoe

nix, A

ZDe

nver,

COWa

shing

ton, D

C-MD

-VA

West

Palm

Bea

ch/B

oca…

Omah

a, NE

Salt L

ake C

ity/O

gden

, UT

Tucso

n, AZ

Anah

eim/S

anta

Ana,

CACh

icago

, IL

Louis

ville,

KY-IN

Alban

y/Sch

enect

ady,

NYOr

lando

, FL

Sava

nnah

, GA

Baltim

ore, M

DJa

ckson

ville,

FLTa

mpa/

St Pe

tersb

urg, F

LRa

leigh

/Durh

am/C

hape

l…Pit

tsburg

h, PA

Minn

eapo

lis/S

t Pau

l, MN-

WIAlb

uque

rque,

NMRic

hmon

d/Pe

tersb

urg, V

ANe

wark,

NJ

Cleve

land,

OHCin

cinna

ti, OH

-KY-

INAtl

anta,

GAInd

ianap

olis,

INHa

rtford,

CTHo

uston

, TX

San A

ntonio

, TX

Charl

otte,

NC-S

CMe

mphis

, TN-

AR-M

SCo

lumbu

s, OH

St Lo

uis, M

O-IL

Dalla

s, TX

Norfo

lk/Vir

ginia

Beac

h, VA

Detro

it, MI

Fort

Worth

/Arlin

gton,

TXKa

nsas

City,

MO-

KSCo

lumbia

, SC

Dayto

n/Sp

ringfi

eld, O

H

Competitive Airbnb Rooms as a Percent of Hotel Rooms INCREASING THREAT FROM AIRBNB

19 Markets above 5%

Source: Insideairbnb.com (July 2015); PKF Hospitality Research, a CBRE Company, STR, Inc.

21 ECONOMETRIC ADVISORS

INCREASING THREAT FROM AIRBNB

Data suggests that increases in Airbnb supply negatively impacts ADR growth.

Source: PKF Hospitality Research, STR, Airbnb.com

ECONOMETRIC ADVISORS

TRACKING THE BUSINESS CYLCES OF U.S. HOTELS

23 ECONOMETRIC ADVISORS

Rapid Development

Occupancy Declines, ADR Follows

Development at Minimum Levels

Lodging Decline, Leads Other

Sectors

Occupancy Recovers

ADR and Margins Recover

Development Picks Up

Development Slows

Lodging Recovers, Lags Other Sectors (Not this

Time!)

Long Run Occupancy

Accelerated Development ?

Equilibrium ADR

U.S. is Here 2015

p2017/8

THE LODGING INDUSTRY BUSINESS CYCLE

24 ECONOMETRIC ADVISORS

A Look at Past Cycles – 1991 Recession REAL ADR PERFORMANCE – U.S.

Real Average Daily Rate Level (2014 $’s)

Duration: 7 Years

The Path and Duration of Occupancy and Real ADR Recovery

Source: PKF Hospitality Research, STR, Inc.

54%

56%

58%

60%

62%

64%

66%

68%

$95 $100 $105 $110 $115 $120 $125 $130 $135

End: 1997 Q1

Start: 1990 Q2

Occupancy Level

25 ECONOMETRIC ADVISORS

A Look at Past Cycles – 2001 Recession REAL ADR PERFORMANCE – U.S.

Real Average Daily Rate Level (2014 $’s)

Duration: 6 Years – 1 Quarter

The Path and Duration of Occupancy and Real ADR Recovery

54%

56%

58%

60%

62%

64%

66%

68%

$95 $100 $105 $110 $115 $120 $125 $130 $135

End: 2007 Q1

Start: 2001 Q1

Source: PKF Hospitality Research, STR, Inc.

Occupancy Level

26 ECONOMETRIC ADVISORS

Current Cycle REAL ADR PERFORMANCE – U.S.

Real Average Daily Rate Level (2014 $’s)

The Path and Duration of Occupancy and Real ADR Recovery

54%

56%

58%

60%

62%

64%

66%

68%

$95 $100 $105 $110 $115 $120 $125 $130 $135

Present

Start: 2008 Q1

Source: PKF Hospitality Research, STR, Inc.

Occupancy Level

27 ECONOMETRIC ADVISORS

54%

56%

58%

60%

62%

64%

66%

68%

$95 $100 $105 $110 $115 $120 $125 $130 $135

2015 Q2

Start: 2008 Q1

Forecast End: 2015 Q4

Current Cycle – cont’d REAL ADR PERFORMANCE – U.S.

Real Average Daily Rate Level (2014 $’s)

The Path and Duration of Occupancy and Real ADR Recovery

Current Cycle – Sept 2015

Forecast Duration: 8.5 Years

Source: PKF Hospitality Research, STR, Inc.

Occupancy Level

28 ECONOMETRIC ADVISORS

54%

56%

58%

60%

62%

64%

66%

68%

$95 $105 $115 $125 $135

2015 Q2

Start: 2008 Q1

Forecast End: 2015 Q4

Current Cycle – cont’d REAL ADR PERFORMANCE – U.S.

Occupancy

Level

Real Average Daily Rate Level (2014 $’s)

The Path and Duration of Occupancy and Real ADR Recovery

Forecast Duration: 8.5 Years

Source: PKF Hospitality Research, STR, Inc.

CycleCycle Start

Cycle Peak

At Real ADR

Recovery Delta1990 64.4% 64.8% 64.3% -0.1%2001 63.1% 63.5% 62.9% -0.2%2008 62.3% 65.8% 65.4% 3.1%

Occupancy Level

ECONOMETRIC ADVISORS

U.S. LODGING MARKET FORECAST

30 ECONOMETRIC ADVISORS

2014-2016 NATIONAL FORECAST – ALL U.S. HOTELS

Long Run Average 2012 2013 2014 2015F 2016F

Supply 1.9% 0.4% 0.7% 0.8% 1.1% 1.8%

Demand 2.0% 2.8% 2.0% 4.4% 3.3% 2.2%

Occupancy 62.0% 61.4% 62.2% 64.4% 65.8% 66.1%

ADR 3.0% 4.2% 3.9% 4.5% 5.0% 5.9%

RevPAR 3.2% 6.6% 5.2% 8.2% 7.2% 6.3%

RevPAR driven by ADR Growth

Source: PKF Hospitality Research - Hotel Horizons® September-November, 2015, STR, Inc.

31 ECONOMETRIC ADVISORS

Lower-Priced Categories Moving Up The Recovery Curve REVPAR FORECAST BY CHAIN-SCALE

Chain-Scale 2014 2015F 2016F

Luxury 6.3% 6.4% 7.0%

Upper-Upscale 7.1% 6.1% 6.0%

Upscale 8.5% 6.4% 6.5%

Upper-Midscale 8.3% 6.8% 7.1%

Midscale 8.3% 7.7% 6.0%

Economy 8.7% 7.3% 7.1%

All Hotels 8.2% 7.2% 6.3% Source: PKF Hospitality Research - Hotel Horizons® September-November, 2015, STR, Inc.

32 ECONOMETRIC ADVISORS

U.S. HOTEL MARKETS GREATEST AND LEAST CHANGE IN REVPAR

-7.6% 0.3% 0.3% 0.3% 0.6%

6.3% 7.9%

8.3% 9.6%

10.4% 11.6%

-10% -5% 0% 5% 10% 15%

HoustonPittsburgh

MiamiNew York

OmahaNational Average

SeattleAtlanta

NashvilleSan Jose-Santa Cruz

Oakland

Source: PKF Hospitality Research - Hotel Horizons® September-November, 2015, STR, Inc.

Forecast Change 2015 to 2016

ECONOMETRIC ADVISORS

PROFIT TRENDS

34 ECONOMETRIC ADVISORS

PKF HOSPITALITY RESEARCH, A CBRE COMPANY Trends® in the Hotel Industry – Financial Benchmarking • Annual voluntary survey of thousands

of U.S. hotel financial statements • First survey conducted in 1937

– Occ: 64.4% – ADR: $3.04

• Data converted to USALI to ensure comparability

• 2015 Survey Sample • 7,135 hotels across the U.S. • Occupancy: 74.3% • ADR: $158.62

35 ECONOMETRIC ADVISORS

Percent of Hotels** Posting an Increase in Total Revenue or Profits From Prior Year MORE HOTELS ENJOYING GROWTH IN PROFITS* (*) - Before deductions for capital reserves, rent, interest, income taxes, depreciation, and amortization. (**) - Trends® in the Hotel Industry sample.

70.2%

47.9%

4.5%

67.4%

80.8% 77.1% 79.3% 86.2%

61.6%

44.4%

8.6%

58.9%

72.3% 70.4% 70.4% 78.2%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011 2012 2013 2014

Total Hotel Revenue Profits*Source: PKF Hospitality Research, a CBRE Company, 2015 Trends® in the Hotel Industry

36 ECONOMETRIC ADVISORS

Change – 2013 to 2014 2014 U.S. HOTEL REVENUES

Source: PKF Hospitality Research, a CBRE Company, 2015 Trends® in the Hotel Industry

1.2%

3.1%

3.1%

4.1%

3.8%

4.3%

6.2%

6.2%

7.3%

6.9%

0% 3% 6% 9%

Rentals and Other Income

Other Operated Departments

Food and Beverage

Rooms

Total Hotel Revenue

$ Per Available Room $ Per Occupied Room

37 ECONOMETRIC ADVISORS

Annual Real Change REVENUE VS EXPENSE* GROWTH

(*) - Before deductions for capital reserves, rent, interest, income taxes, depreciation, and amortization.

Source: PKF Hospitality Research, a CBRE Company, Trends® in the Hotel Industry

4.9% 5.4% 5.0% 2.6%

-5.1%

-18.2%

3.2% 3.1% 2.9% 3.9% 5.3% 3.7% 3.1% 3.0% 1.9%

-4.1%

-11.5%

1.7% 1.0% 1.2% 2.3%

3.2%

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Rev Exp CPI

38 ECONOMETRIC ADVISORS

Percent of Total Operating Expenses* WHERE DID THE DOLLARS GO?

Salaries, Wages, and Benefits

44.2%

Cost of Goods Sold 8.6%

Management Fees 4.9%

Property Taxes and Insurance

6.2% Operating Expenses

36.1%

Note: * Before deductions for capital reserves, rent, interest, income taxes, depreciation, and amortization Source: PKF Hospitality Research, a CBRE Company, 2015

39 ECONOMETRIC ADVISORS

CHANGE IN HOSPITALITY EMPLOYMENT COMPENSATION

Source: PKF Hospitality Research, A CBRE Company, Bureau of Labor Statistics, 2015

3%

4%

5%

6%

7%

8%

9%

10%

-1%

0%

1%

2%

3%

4%

5%

6%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Change in Average Hourly Compensation for Hospitality Employees U.S. Unemployment Rate

Change In Hourly Compensation U.S. Unemployment Rate

40 ECONOMETRIC ADVISORS

CHANGE IN HOURS WORKED VS. CHANGE IN ROOMS OCCUPIED

Source: PKF Hospitality Research, A CBRE Company, Bureau of Labor Statistics, 2015

-15%

-10%

-5%

0%

5%

10%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Change in Total Hours Worked Change in Occupied Rooms

Annual Change

41 ECONOMETRIC ADVISORS

Annual Change in ExPAR: 2013 to 2014 SELECT COMPONENTS OF OPERATING COSTS

Source: PKF Hospitality Research, a CBRE Company, Trends® in the Hotel Industry

3.7%

6.5% 5.3% 4.8%

0%

2%

4%

6%

8%

Labor Costs C.C. Commissions +Franchise and

Management Fees

Cost of Goods Sold Utilities

42 ECONOMETRIC ADVISORS

Annual Nominal Change REVENUE VS EXPENSE* GROWTH

5.5%

-1.3%

-18.5%

4.8% 6.2% 5.0% 5.4% 6.9% 6.9% 6.1% 4.8%

-0.3%

-12.1%

3.4% 4.3% 3.3% 3.7% 4.9%

3.7% 3.5%

-24%

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

2007 2008 2009 2010 2011 2012 2013 2014 2015F 2016F

Total RevPAR ExPAR* C.P.I.

Note: * Before deductions for capital reserves, rent, interest, income taxes, depreciation, and amortization Source: PKF Hospitality Research, a CBRE Company, Moody’s Analytics 2015

43 ECONOMETRIC ADVISORS

Six Years of Double Digit Growth NOMINAL DOLLAR OPERATING PROFITS*

$17,

042

$16,

394

$10,

591

$11,

629

$13,

105

$14,

442

$15,

894

$17,

849

$20,

490

$22,

928

$0

$5,000

$10,000

$15,000

$20,000

$25,00020

07

2008

2009

2010

2011

2012

2013

2014

2015

F

2016

F

Compound Annual Growth 2010 – 2016F: 12.0%

Nominal Dollars Per Available Room

Growth 2010 – 2016F: 12.0%

Note: * Before deductions for capital reserves, rent, interest, income taxes, depreciation, and amortization Source: PKF Hospitality Research, a CBRE Company, 2015

44 ECONOMETRIC ADVISORS

HISTORICAL BUDGET ACCURACY

-8.0% -10.9%

0.1% 1.3% 1.6%

-0.5%

-8.0%

-14.6%

3.5%

-0.1% -1.3% -0.04%

0.4%

-22.3%

-29.1%

-1.9%

3.5%

-4.2%

3.8%

-14.0%

-28.2%

9.2%

0.8% 0.1% 0.07%

0.4%

-35%-28%-21%-14%-7%0%7%

14%

2001 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Total Revenue Profit**

Note: * - Sample of properties that reported budget data. ** - Before deducting capital reserves, rent, interest, income taxes, depreciation, and amortization. Source: PKF Hospitality Research, a CBRE Company, 2015

Percent Difference Actual Compared To Budgeted Dollars*

45 ECONOMETRIC ADVISORS

THANK YOU FOR YOUR TIME

PKF HOSPITALITY RESEARCH | CBRE HOTELS

www.pkfc.com

Robert Mandelbaum