the use of strong structuration theory as a lens to … · web viewthe use of strong structuration...

TRANSCRIPT

The use of Strong Structuration Theory as a lens to evaluate

management accounting change.

Dr Angela Lorenz

Aston Business School

Draft paper

Abstract

Purpose – This paper aims to explore the use of strong structuration theory as a

lens for investigating management accounting change in organisations.

Design/methodology/approach – The paper is informed by structuration theory

drawing on alternative theories used to evaluate management accounting change to

develop a rationale for the use of Stones (2005) quadripartite model.

Findings – The use of Stones (2005) strong structuration theory has been

overlooked as a theory in management accounting research, in particular the

quadripartite model can overcome problems levelled at both institutional and

structuration theory in terms of their inability to get to the heart of the recursive

relationship between structure and agency, to provide a richer insight into barriers

and enablers of management accounting change from the perception of the

accountant.

Originality/value –There is a lack of empirical evidence of the use of strong

structuration theory and this paper provides a rationale for its use and provides

insights as to how it can be used productively to yield new insights into management

accounting change.

Keywords Management accounting change, institutional theory, structuration theory,

strong structuration theory

Paper type Conceptual paper

1. Introduction

Management accounting research has been described as diverse and eclectic

(Wanderley and Cullen, 2012b). It has evolved over time first following a rational

perspective utilising the neoclassical framework based on the assumption that

decision makers are profit maximisers (Hopper et al, 2001, Ryan et al, 2002) which

became linked to Chua’s 1986 definition of mainstream management accounting

research. The research subsequently developed to consider management

accounting in a wider socio-economic context, creating the paradigms of interpretive

and critical research in management accounting. Tomkins and Groves called in

1983 for accounting researchers to use different social science approaches to “get

closer to the practitioners everyday world” (1983:373).

Over time a number of different theoretical lenses have been applied to management

accounting research, Scapens (2006a), for example, summarises his personal

journey from the use of Economic and Contingency theory to Institutional theory and

Structuration.

The study of change in management accounting practices is a key area of research

which has been evaluated using these theoretical lenses.

Interest in management accounting change (or lack of change) was brought to

mainstream attention by Johnson and Kaplan (1987) who argued that management

accounting practices had failed to keep pace with changes in the organisational

environment. In response to this new techniques of management accounting have

been developed in organisations and it is these developments that have been

termed management accounting change (Wickramasinghe & Alawattage, 2007).

Early studies of management accounting change were based on the rational

perspective, viewed practices in an economic context and surmised that change

would only occur if there were financial benefit in the activity. Subsequently studies

from a rational perspective focused on the theory of the organisation which viewed

the relationship between management accounting change and contingencies

(Lapsley & Pettigrew, 1994, Ezzamel et al, 1996; Libby & Waterhouse, 1996;

Haldma and Laats, 2002; Baines & Langfield-Smith, 2003; Akbar, 2010). These

studies looked for linkages between organisational and environmental variables and

then evaluate how management accounting can be used in different situations

Institutional theory also rose as a lens with frameworks developed which linked this

theory to management accounting change (Granlund & Lukka, 1998; Burns and

Scapens, 2000; Lukka, 2007) and further work was undertaken which sought to look

at typologies and devise models of management accounting change (Sulaiman &

Mitchell, 2005, Ax & Bjornenak, 2007).

Whilst Burns and Scapens (2000) get close to interpreting rules and routines as

structure the use of structuration theory was slow to surface as a lens for evaluating

management accounting practice change.

Whilst each of these lenses has helped to shed new insights into management

accounting change no theory can address all of the issues associated with the

research in question and it becomes vital to test the validity and insights of new

theories and models when they materialise.

Lorenz (2015) during the course of collecting primary case study research data

relating to the use of contemporary management accounting tools in service

industries discovered that it was possible to evaluate the barriers and enablers of

change from the perspective of the accountant in the organisation and therefore the

use of structuration theory and particularly the quadripartite model of strong

structuration theory could be used as a sensitising lens with which to shed new

insights into how management accounting practices become embedded and

reproduced in organisations and how new tools and techniques may be introduced

over time.

Lorenz (2015) found little evidence of strong structuration being used and particularly

not in the context of management accounting change demonstrating a gap in the

literature for planning and evaluating how this theory could be used in future

research in this area.

This paper will review the development of the research relating to management

accounting change and the rise and use of structuration theory and strong

structuration theory in management accounting. The paper will then demonstrate

how the use of Stones (2005) strong structuration theory using the quadripartite

framework can be used as an alternative method to investigate and understand

management accounting change.

2. Review of the theories used to evaluate management accounting change

Since the early work of Johnson and Kaplan (1987) management accounting change

has become a topic of much debate. Akbar (2010) suggests that the profile and

importance of management accounting systems and practices in organisations has

increased resulting in a persistent call for change.

Over time academics have used a variety of theories and developed models and

frameworks in order to aid understanding of management accounting change in

organisations, these can be grouped into six categories which are shown in table 1

below.

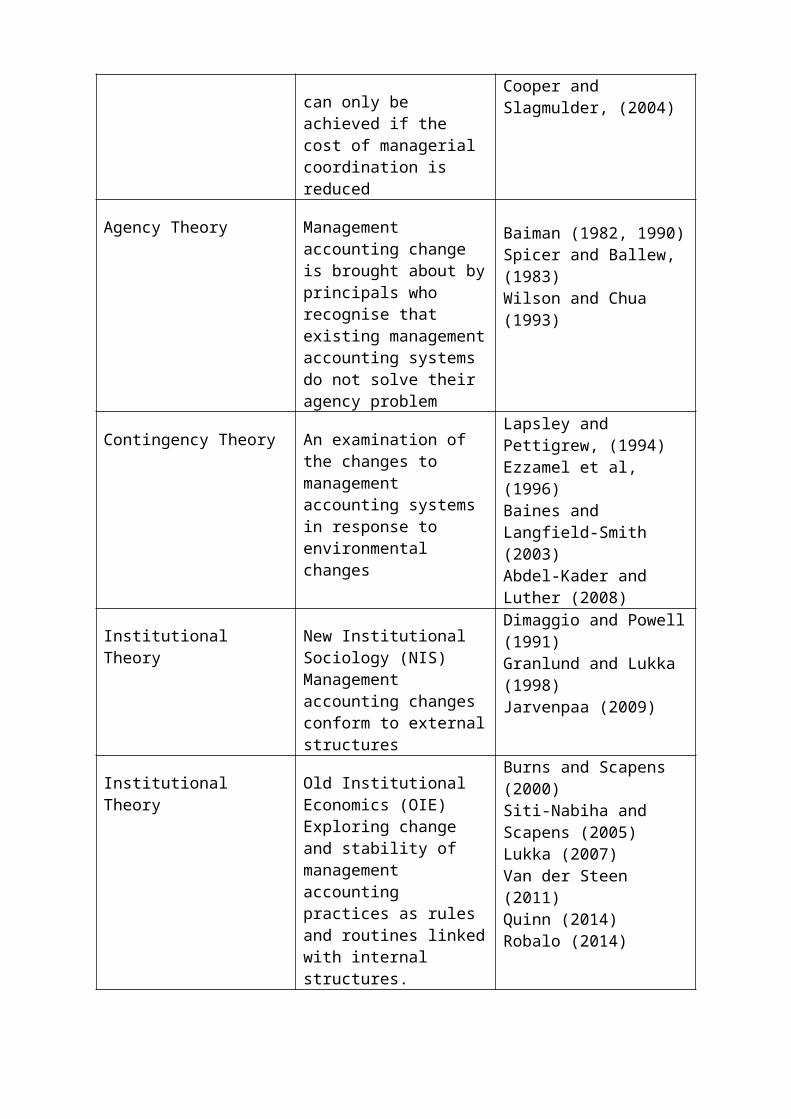

Table 1: Summary of the theoretical lenses used to evaluating management accounting change

Theory Key elements Key authors

Transaction Cost Theory Management accounting change can only be achieved if the cost of managerial coordination is reduced

Zimmerman, (1979)Banker et al (1996)Cooper and Slagmulder, (2004)

Agency Theory Management accounting change is brought about by principals who recognise that existing management accounting systems do not solve their agency problem

Baiman (1982, 1990)Spicer and Ballew, (1983)Wilson and Chua (1993)

Contingency Theory An examination of the changes to management accounting systems in response to environmental changes

Lapsley and Pettigrew, (1994)Ezzamel et al, (1996)Baines and Langfield-Smith (2003)Abdel-Kader and Luther (2008)

Institutional Theory New Institutional Sociology (NIS)

Dimaggio and Powell (1991)Granlund and Lukka

Management accounting changes conform to external structures

(1998)Jarvenpaa (2009)

Institutional Theory Old Institutional Economics (OIE) Exploring change and stability of management accounting practices as rules and routines linked with internal structures.

Burns and Scapens (2000)Siti-Nabiha and Scapens (2005)Lukka (2007)Van der Steen (2011)Quinn (2014)Robalo (2014)

The first three theoretical lenses can be described as following a rational perspective

(Wickramasinghe and Alawattage, 2007) using a neo-classical economic framework.

Hopper et al (2001) held the view that management accounting research was

dominated by economic theory up to the 1970’s and Scapens and Arnold (1986)

suggested that economic theory played a key role in the development of techniques

in all areas of management accounting and a review of the literature undertaken by

Sheilds in 1997 showed the majority of management accounting research was based

on economic theory.

Transaction cost economics has amongst its advocates Johnson and kaplan, (1987),

and rests on the assumption that organisational economy and efficiency are

increased through manageirial coordination and that the role of management

accounting is to reduce the cost of managerial coordination. Hence new techniques

of management accounting will be introduced if they can reduce this cost. David and

Han, (2004) recognise the high use of this theory in a variety of management

disciplines since the work of Williamson in 1975 but also reflect on the criticisms

levelled at this theory in terms of weak empirical evidence to support the theory

particularly as organisational forms have changed and boundaries have blurred

(Wickramasinghe and Alawattage, 2007). Baiman (1990) in his review suggests that

transaction cost economics whilst it has made a significant contribution to the

industrial organisation literature it has not been applied to specific managerial

accounting issues. Baiman (1990) goes on to criticise the imprecise nature of the

theory in defining transaction costs as being a particular impediment.

Agency Theory based on the contractual relationship between agent and principal

allows management accounting research to view the organisational relationships

which affect management accounting tool development and use. Baiman (1990:344)

suggested that agency theory has brought a…. “new appreciation for the role of

managerial accounting procedures and a more subtle understanding of the demand

for and effect of managerial accounting policies and procedures” Baiman (1990) also

goes on to reflect on the criticisms levelled at agency theory in respect to the

computational elements required, the simplicity of the models used and the lack of

consideration of trust, these are views mirrored by later academic criticism such as

Seal and Vincent-Jones (1997), Kunz and Pfaff (2002) and Lambert (2006). Kelly

and Pratt (1996:230) suggest that whilst it “provides convincing explanations for

some behaviour……… it is only selectively convincing and denies the possibility of

economically irrational or altruistic behaviour”.

The use of contingency theory in management accounting research can be traced

back some 40 years to academics such as Waterhouse and Tiessen (1978) and

Otley (1980) who were able to identify that there is not one overriding appropriate

management accounting system and that the design of management accounting

systems are shaped by environmental and organisational factors. Chenhall (2003)

identified that the popularity of using contingency theory had not waned and that

contemporary issues were continuing to be examined using this framework.

Research conducted Baines and Langfield-Smith (2003), for example, utilised a

contingency led approach to management accounting change linking changes in

management accounting systems and organisational variables to environmental

changes. Their conclusions suggest that successful organisations are changing their

strategies in line with environmental changes but could find no direct relationship

between them and advanced management accounting practices.

Additionally, Akbar (2010) suggests that internal and external organisational changes

such as information technology advancements, more competitive and customer

driven markets, changes in organisational structures and new management

practices, have had a direct impact on management accounting practices supporting

previous studies including Lapsley and Pettigrew, 1994 and Ezzamel et al, 1996,

Haldma and Laats, 2002 and Libby and Waterhouse, 1996.

Chenhall (2003) in his critique does however suggest that there are a number

criticisms of contingency theory including reliance on using the general

contingencies mentioned above rather than exploring new contingent factors.

Covaleski et al (1996:8) in their reflection of contingency theory suggest it has “been

criticised for presenting a deterministic, ahistorical view of organisations which

produces limited insight as to the mediating processes of organisations”.

Chenhall (2003) also concurs with earlier critics such as Otley (1980) and Hopper

and Powell, (1985) suggesting the contingent variables needed greater definition and

more importantly should recognise the social and institutional contexts of the

environment and the way these specifically exert pressure on management

accounting systems.

Zimmerman (2001) put forward a case for the superiority of the mainstream

functionalist approach to management accounting research based on economic

theory, suggesting at the time that other epistemological stances in management

accounting research lacked empirically tested theories. Zimmerman’s paper

received a number of criticisms at the time Luft and Shields, (2002) for example

suggested that management accounting research needed to be rich and diverse, a

view which supports Tomkins and Groves’ (1983) call for accounting researchers to

use different social science approaches and Burns and Scapens (2000) go on to

argue that economic approaches whilst they may suggest the techniques do not

assist in our understanding of how management accounting techniques come to be

used or not. Ryan et al, (2002) suggest that as a result research using the alternative

approaches (interpretive and critical management accounting research) have

expanded rapidly and have helped to reduce the theory practice gap by bringing

research closer to practice.

Institutional theory is one such alternative approach. A number of different strands of

institutional theory exist with the aim of gaining insights into organisational change

and these have been extended to consider management accounting change. They

include new institutional economics (NIE), new institutional sociology (NIS) and old

institutional economics (ONS).

NIE is concerned with the external institutions in the organisational environment

(economic social and political) and their effect on organisational practice (DiMaggio

and Powell, 1991). DiMaggio and Powell in their analysis suggested that

organisations conform to gain legitimacy and increase their probability of survival.

Scapens (2006b) suggests that NIE has drawn attention to the economic factors that

shape organisations structures, systems and management accounting practices.

NIS attempts to explain why organisations in a particular filed appear similar. It

distinguishes between technical (efficiency in operations) and institutional (rules,

social norms and expectations) environments. In terms of contemporary

management accounting tools such as ABC, Scapens (2006b) suggests it would be

useful to consider the technical concerns driving the adoption and also the desire to

conform to external expectations.

DiMaggio and Powell, (1991) considered different types of isomorphism (the extent

to which one organisation resembles another) and categorised them into three

groups: Coersive (legal/political); Mimetic (copying others); Normative (society and

professional bodies).

Using an NIE and NIS approach Granlund and Lukka (1998) produced a framework

of drivers of management accounting practice. They suggested that there was a

growing trend towards globalisation of management accounting practices and that

future management accounting research should focus on analysing the similarities.

Javenpaa (2009) considers the institutional pillars: normative; regulative and cultural-

cognitive in creating organisational legitimacy for management accounting practices

to add further insight into change and stability.

NIE clearly focuses on the economic and together with NIS focuses on external

social institutions however it does not give any insight into what is happening

internally in individual organisations with regard the influences over management

accounting practices, Scapens (2006b).

OIE is designed to look internally at institutions within the organisation to focus on

internal pressures which may shape management accounting practice. Whilst NIE

and NIS still have links to the classical economic theory that has shaped

management accounting research, OIE was built on questioning the classical

framework of rationality and recognises that actors’ behaviour can be shaped by the

organisational institutions, Scapens (2006b).

Burns and Scapens (2000) developed a framework based on OIE considering rules

and routines linking institution to action, to form a process for management

accounting change. They focus on the ways in which rules and routines exist in

organisations and how the nature of these combined with the behaviour and

relationships within groups in the organisation shape the process of change. They

suggest that “management accounting change which is consistent with the existing

routines and institutions will be easier to achieve than change which challenges

those routines and institutions” (Burns and Scapens, 2000:12). They suggest the

framework should be used in interpretive case studies for focusing on the

fundamental characteristics of change. It is interesting to note that whilst some refer

to the work of Burns and Scapens (2000) as institutional theory Englund et al (2011)

and Englund and Gurdin (2014) refer to this work as being in the field of structuration

theory due to the link that Burns and Scapens (2000)form to accounting rules and

routines as internal structures and the agents over time.

Lukka (2007) drew on the framework of Burns and Scapens (2000) considering both

the change and stability of management accounting systems over time and the

formal and informal domains of organisational life. Lukka (2007) goes someway to

extend Burns and Scapens (2000) work to consider informal routines which move

towards the use of structuration theory. Lukka (2007) concludes that it is possible to

have both change and stability in management accounting systems at a point in

time. Van der Steen (2011) sought to provide greater clarity as to the nature and

complexity of routines and found that the routines could be dynamic rather than

static. Robalo (2014) further extended the work by seeking to add the issues of trust

and power to Burns and Scapens (2000) original framework whilst Quinn (2014)

demonstrated that rules and routines can be considered separately.

Ribeiro and Scapens (2006) and Alsharai et al (2015) further extend the work of

Burns and Scapens by combining both their Old Institutional Economics (OIE)

approach to that of NIS and adding an extra dimension of circuits of power (Clegg,

1989) in the case of Ribeiro and Scapens and power and politics following Hardys

1996 work in the case of Alsharari et a (2015)l, their intention was to create more

inclusive contextual frameworks which could be used for research into management

accounting change.

Table 1 above shows how institutional theory has been dominant in the expansion of

research into management accounting change, however institutional theory suffers

from a variety of problems, such as the focus only on external or internal structures

which Ribeiro and Scapens (2006) and Alsharari et al (2015) have attempted to

overcome by combining NIS and OIE into new frameworks. Barley and Tolbert

(1997) and Dillard et al (2004) show how institutional theory does not show the

recursive relationship between institutions and actors and in that respect suggest

that structuration theory has an advantage over institutional theory.

3. Structuration theory and management accounting

Structuration theory is based on the work developed by Giddens (1984). The main

premise of the work relates to the duality of structure between the agency of

individuals (to make their own choices) and the social structures (rules and routines).

Therefore the structures are “both a product of and constraint on human action”

(Barley and Tolbert, 1997:97). Giddens suggests that structures exist because of

the routinised nature of human behaviour and hence existing rules can prevail for

long periods of time. Giddens is also clear “that structure is always both constraining

and enabling” (1984:25). Giddens model can be seen in Figure 1 below. Giddens

conception shows how the two realms of action and institution are related through

the modalities of structure. The institutional realm represents three key structures in

terms of signification (meaning), legitimation (morality) and domination (power). The

realm of action refers to actual arrangements of people, objects and events and

shows how they can be influenced by and influence the institutional realm in terms of

communication, power and where to sanction and reward behaviour through

modalities of interpretive schemes, resources and norms.

Figure 1: Giddens Model of Structuration

Source: Barley and Tolbert (1997:97)

Signification is the cognitive dimension; structures are semantic rules which are

interpreted as shared knowledge and accumulated skills drawn on to create meaning

and for actors to communicate with each other. In terms of management accounting

practice this will relate to the existing practices which are used and day to day

reports produced and communicated by actors based on the shared knowledge of

how the practice works (Macintosh and Scapens, 1991).

The domination dimension contains structures which constrain resources and but

also foster co-operation in order to achieve goals. Two types of resources are

controlled which are allocative resources (physical goods or even knowledge) also

known as artefacts and authoritative resources through the domination over other

actors (can be witnessed through chains of command) (Macintosh and Scapens,

1991). In terms of management accounting new tools may be slow to be introduced

as the subordinate actors do not have the power to change due to a lack of physical

resources and a lack of authority.

The legitimation dimension represents the moral underpinnings or collective

consciousness. Agents interact with this dimension through codes of conduct and

behaviour is rewarded or penalties imposed for compliance or non-compliance with

codes of conduct (Macintosh and Scapens, 1991). In terms of management

accounting this can be seen through systems which seek to attract responsibility and

accountability to agents and the way the agents react to those norms.

Using Giddens interpretation of routine and change, routine is welcomed by actors

and change does not occur easily however there are circumstances or “critical”

situations where conventional structures are abandoned and new ones emerge.

These may represent instances where changes in the external environment of an

organisation may force new accounting tools to be considered and implemented

through communication and power of individual actors (Macintosh and Scapens,

1991).

Work in management accounting using structuration theory has developed over time.

Scapens together with Roberts (1985) and Macintosh (1990) examined the

relationship between accounting practices and structure drawing on the duality of

structure. Macintosh and Scapens (1990) in particular suggest that “management

accounting systems represent the modalities of structuration in the three dimensions”

(1990:462), Busco (2009) adds that this alludes to the pivotal role of management

accounting in the relationship between agency and structure.

Other work such as Barrett et al (2005), Conrad (2005), Busco (2006) and Busco

and Scapens (2011) also explore Giddens theory of structuration and the role of

accounting information. Busco and Scapens (2011) conclude from their case study

research that management accounting change is mainly evolutionary but there are

periods of revolutionary change and by utilising the position practices and the three

dimensions of Giddens model a holistic explanation of the influence of management

accounting systems can be found. A further interesting finding from this research is

the ability of management accounting systems to pervade into common language

across a variety of actors in an organisation and as such improve communication

and breakdown cultural and operational boundaries.

Wanderley and Cullen (2012a) in their case study research of management

accounting change in a Brazilian electricity distribution company draw on both the

work of Dillard et al (2004) and Giddens structuration theory in framing their analysis

and were able to identify the extent of the relationship between structure and agents

and how therefore management accounting change was possible.

Gurd (2008) utilised structuration theory and Laughlins (1991) middle range thinking

framework. Gurd concluded that the use of structuration theory provided insights

into the role of accounting during a period of organisational change and the role of

individual agency.

Ogata and Spraakman (2013) also chose to use structuration theory in their archival

case study evaluation of management accounting change again demonstrating the

usefulness of the model in highlighting how management accounting tools persist

over time.

Busco et al (2007) also reflect on the use of structuration theory as being valuable to

overcome the dichotomy of “the complex interactions between management

accounting systems and organisational, institutional and contextual factors” (Busco

et al, 2007:130).

Englund and Gerdin (2014) and Englund et al (2011) reviewed the research that had

been conducted using structuration theory focusing not on the findings of the

research but on the way in which the researchers had used structuration theory, in

total they reviewed 65 papers mainly published in research journals, including those

mentioned above, up to 2010.

Englund et al (2011) suggest that structuration theory has made contributions to

accounting research in three key areas; by introducing the concept of duality and the

recursive nature of structure and agency; by conceptualising how accounting has

demonstrated insights into the three dimensions of structure (signification,

legitimation and domination); by providing a framework to allow theorising of

continuity and change in accounting practice.

They (Englund et al, 2011) comment that accounting researchers have tended to

focus on the key elements of structure and not on the agency, this view has also

been articulated by Conrad (2014) who draws on Cohen’s (1989) observation that

figure 1 above should not represent the dominance of structure over agency and the

diagram could be changed give greater emphasis on agency. Englund et al (2011)

conclude this part of their analysis by suggesting that future research should have a

focus on the role of the knowledgeable agent in structuration, this view is also

supported by Roberts (2014) who calls for the analysis of strategic conduct rather

than analysis that is a form of ‘institutional analysis’.

Busco (2009) draws on calls by earlier academics (Thrift 1985; Barley 1986) to

provide a clearer link between the two realms and purports that the social concept of

‘position practice’ can act as a link between them. Coad and Glyptis (2014) utilise

the concept of praxis and as such produce a study which “brings the agent more into

focus” (Conrad,2014:130).

Conrad (2014) stresses the importance of clear explanation of whether accounting

artefacts are to be considered as structures or as systems supporting Englund and

Gerdin’s (2014) view that this conceptual distinction is important in the interpretation

of Giddens theory.

Englund et al (2011) also illustrate that whilst structuration theory can aid insight into

change and continuity very little of the research conducted really reflects the

reciprocal relationship between structure and agency and does not focus on non-

events. Conrad (2014) supports this view and suggests that “little use has been

made to date of several of the concepts the theory proposes for the analysis of

change” (2014:133) and suggests that there is room for further exploration of the use

of structuration theory in this area particularly in large scale change.

Englund et al (2011) and Conrad (2014) suggest that research should be focused on

an intra-organisational perspective. Englund et al (2011) speculate that the use of

structuration theory can be used to view change across institutional fields. Some

attempt has been made to do this in prior research such as Lawrence et al (1997) by

considering ‘contradiction’ of structures in large scale change.

Englund et al (2011) whilst demonstrating the view that accounting research has not

been critical enough in their use of structuration theory do comment on exceptions to

this in the work of Coad and Herbert (2009) and Jack and Kohleif (2008). Both of

these pieces of research extend the use of Giddens original model by focusing on

the work of Stones (2005) and his development of strong structuration theory.

A number of critics of Giddens original work (Archer (1995); Cohen (1989)) suggest

that the flat local ontology that is advocated by Englund et al (2011) is not

sustainable as structure can be external to the human mind and also have different

levels. It is this problem that Stones (2005) work seeks to address by providing the

context for external structures which can also have hierarchical arrangements.

4. Strong structuration theory and management accounting

Coad et al (2015) whilst acknowledging the shortcomings highlighted by Englund et

al (2011) and Englund and Gerdin (2014) of structuration theory suggest that strong

structuration theory as advocated by Stones (2005) helps to reconcile some of the

problems and in particular can be used to aid understanding of how management

accounting practices become established and institutionalised. They [Coad et al,

2015] suggest Stones framework recognises that both the technical view of

mainstream accounting research steeped in classical economic theory that a

practice will be adopted if it is in the economic interest of the organisation, and the

social new institutional economic view that there is a strong mimetic link across

similar organisations are valid.

Coad et al (2015) further suggest that viewing organisational fields in relation to

position-practice relations can aid in the examining of the diffusion of management

accounting practices.

Stones (2005) work extends the original ontology to give a quadripartite framework

which considers four interconnected elements of external structures, internal

structures, active agency and outcomes. Figure 2 shows Stones framework. Stones

termed this work “strong” structuration theory as its intention was to add to the work

of Giddens to provide a current theory of use in empirical work (Jack and Kholeif,

2008) hence strengthening the original theory. A second underlying feature of

Stones work was the notion of position-practices and the understanding that we are

not necessarily addressing actors as individuals but perhaps as groups and even

considering the ghosts of past actors and their influence over practice (Jack and

Kholeif, 2008).

Stones framework reflects external structure (which we might equate with the macro

world relative to the organisation) and its ability to influence the actors. These would

relate well to the institutional macro framework of Granlund and Lukka (1998).

Internal structures are separated into two elements. Conjuncturally specific internal

structures which link the actor(s) to roles and position practices, in this context, that

would be the role of the accountant within the organisations and the rules and

routines specific to that role. General dispositions are elements that an agent draws

on without thinking such as cultural norms or communication skills.

The active agency reflects when and how the agent in focus acts whilst the fourth

component – outcome reflects the result of active agency in terms of whether the

internal or external structures have changed.

Figure 2: The Quadripartite Nature of Structuration

Source: Stones (2005:85)

Reviews of stones work such as Edwards (2006) and Parker (2006) suggest that it

moves structuration theory from a philosophical level to a specific level allowing for

greater utility in empirical research. Jack and Kholeif (2008) believed at the time that

Stones (2005) framework offered “significant potential for qualitative researchers”

(2008:210). Stones himself expressed the view that the framework considers the

relationship of ontological elements to practice and empirical work (Stones 2016).

Jack and Kholeif (2007) sought to use Stones framework to show how structuration

theory can be used in substantive empirical research and use two existing case

studies to demonstrate how the Stones (2005) framework could be used to enhance

research using a case study method. In their 2008 work Jack and Kholeif applied

the strong structuration perspective to a case organisation. The contribution of

strong structuration to the case meant it was possible to explore conflicting

dispositions and conjunctually specific understandings particularly the role of the

management accountant and perceptions of actors in relation to boundaries between

external and internal structures.

Coad and Glyptis (2014) reflect on the changing dynamics of structuration theory in

management accounting over time and comment that their view places greater

emphasis on the position-practice perspective and considering the role and relations

of actors across space and time. Coad and Glyptis go on to discuss the nature of

position-practice through its four main elements of praxis (the activity of the agents),

positioning (social positions with which the agent identifies), capabilities (how actors

make use of practices and resources now and consider the future of practices and

resources), and trust (confidence in the reliability of other actors or systems). This

work built upon the work of Coad and Herbert (2009) who also explored position

practices in a case study moving from agent to agent in the organisation and

concluded that this approach facilitates attention on the strategic conduct of agents

and the importance of power. Coad and Herbert (2009) also concluded that there

are still some deficiencies in Stones quadripartite framework in that whilst it allows

for the exploration of how external structures interact with the conduct of agents it

does not offer insight as to why the elements of the model interact. Their final

conclusion is that structuration theory should be used flexibly.

5. The use of the quadripartite framework to strengthen studies of management accounting change

Stones (2001) was keen to demonstrate that the criticisms laid at structuration theory

by Archer (1995) whose view suggested that there was a divide between the use of

realist social theory and structuration theory was unfounded. In his 2001 paper

Stones attempted to show that it was possible to combine these approaches to

produce more robust research. In particular he alluded to the combination of

ontology and methodology.

Ashraf and Uddin in their 2015 paper assert the shortcomings of structuration theory

and the richer analysis that can be undertaken by accounting researchers if following

a critical realist perspective. It is interesting that the key elements of critical realism

advocated are consistent with that purported by Stones strong structuration theory

including a greater understanding of the agent and the ability to examine the agent

separately from their structural position, a greater emphasis on the actions of the

agent termed by Stones (2005) as active agency. Ashraf and Uddin (2015) point to

a contradiction in that the moves made by Stones and Cohen to better debate the

interplay between structure and agency in terms of dualism moves away from the

central tenant of structuration theory : duality and that work drawing on Stones

(2005) strong structuration theory needs to maintain a link between duality and

dualism. Parker (2006) in his review of Stones 2005 book reflects on duality and

dualism. He first acknowledges the role of duality as cited by Giddens in that

structure is both the medium and outcome of agency but goes on to extend Archers

(1982) premise that accepting general duality demands adopting ‘analytical dualism’

which itself represents the understanding of how the relata are related to each other,

and this therefore diminishes the need to characterise duality. Parker concludes his

reflection by expressing that strong structuration theory could advance by embracing

insights from historical sociology and Morphogenetic social theory to widen it and

make it more explicit (2006).

In Stones 2012 working paper he shows how combining critical realism and strong

structuration theory could be used to enhance research relating to international

migration. It is proposed a similar approach could be followed by researchers in

management accounting to provide further explanation of the nature of structure and

agency in management accounting change.

Stones (2012) proposes a theorised contextual framework which would develop and

deepen the ontological level of structuration with epistemology and methodology.

The frame which works well with case studies can allow surface effects which could

be linked generally to management accounting practice with detailed observations

relating to specific agents. Messner (2015) considers the link between

organisational factors and industry suggesting that future research could consider

the industrial setting of management accounting practices in order to provide better

insights. This call sits well with the framework suggested above as it would identify

industrial settings as surface events when a number of cases are presented in the

same industry context.

Stones (2012) suggests the first stage should be to establish the research question

or event to be explained with the wider structural context. In this case the event of

interest is the reproduction of management accounting practices over time or the

emergence of new practices. Ashraf and Uddin (2015) in their critical realist view of

Mactintosh and Scapens (1990) paper also reflect on the need to look at the context

within which actions are taken.

Stones (2016) likened the process to a loop as there is a need to be reflexive as one

moves from the problem to how it may be explained with empirical evidence.

Reflexivity allows the researcher to see what they don’t yet know. Figure 3 shows

this loop.

Figure 3: the conceptual cycle

The ontology reflects the nature of entities and the relations that exist in the world

(Stones, 2015), it is necessary to conceptualise what these may be in the contextual

field where the problem sits. Ontological concepts we may use may be structure,

space, time, power, values, resistance, technology, culture, actors/agency for

example. Having considered the key objective factors they can be mapped to show

the contextual field. See figure 4 below where the black dot represents the agent in

focus and the white dots other individual or collective agents and their networked

links with each other.

Problem to be explained

Ontology (abstract)

Conceptual methodology (choosing key

features

Empirical evidence

Does this answer?

Do these match?

What has caused that?

Figure 4: A contextual field with position practice relations

Adapted from Stones (2015:36)

The establishment of the position-practice relationship can be refined at this stage

and the agent in focus identified. This enables a distinction between different

ontological levels of practice with the agent in focus. It becomes clearer which

elements are related to surface events (external structures) or detailed local relations

and the social level of the structures in terms of macro micro and meso and hence

dispensing with the flat local ontology present in Giddens (1985) model. In the case

of some studies it may be beneficial to consider the position practice relationships in

respect of one agent in focus such as the Chief Financial Office/Senior management

accountant this will allow comparisons to be made across cases to identify common

external structures and industry contexts which can shed light on the further

institutionalisation of practice which has been highlighted previously as a limitation of

structuration theory by Englund et al (2011). It is also possible to identify common

internal structures in an industry context. Lorenz (2015) identified common industry

specific internal and external structures present in 5 case studies of service sector

organisations where the 5 agents in focus who were all senior management

accountants considered the nature of the industry as a barrier to management

accounting change.

Position practice relations

Large historical and socio-structural forces

Alternatively the perception of different agents within one organisation can be viewed

in one case study in order to establish whether there are the same or differing views

as to why management accounting practices are reproduced over time, this was a

central tenant in Feeney and Pierce (2014) work which considered the position of

comparable actors in different divisions in one organisation and the way they used

accounting information in decision making.

Stones (2012) suggests the next necessary step is to link the ontological perspective

with the critical realist epistemological conception of retroduction. In relation to the

actor in focus this reflects their power or the power of other or collective actors or

structures to enact the events established at the start of the analysis. Stones

(2012:7) goes on to suggest that this identifies “the most salient forces at work” and

the most relevant actors, entities and relations in relation to answering the research

question. Other studies previously mentioned such as Ribeiro and Scapens (2006)

and Alsharai et al (2015) highlight the need to include power as a dimension of

research in management accounting change.

Having set the wider contextual frame it is then necessary to focus on the individual

agent through the conceptual methodology. The conceptual methodology provides a

bridge between the ontology and the empirical evidence and allows the relationships

to be seen between the concepts and the empirical evidence. There are three

elements to consider here:

1. The agents context (strategic context)

2. The agents conduct (strategic conduct)

3. Ontological sliding scale

Stones (2005) advocates beginning with the agents’ conduct which requires looking

inwards at how the agent deals with the situation and evaluating general dispositions

and conjecturally specific internal structures and then the agents context which ought

to reveal “perceived external structures, position-practice relationships, authorities

and material resources” (Coad et al, 2015:165). The ontological scale allows the

consideration of the problem from a variety of perspectives between the ontological

abstract and the empirical, in the work of Lorenz (2015), for example the degree of

knowledgeability of the agents, the choices available to the agent and the degree to

which external structures were long term barriers were considered.

Stones (2012) in reflecting on Morawska’s (2012:4) use of Emirbayer and Mische

(1998) three agentic orientations highlights how using these as a guide can help to

embellish the empirical research conducted with agents in focus. They are:

The iterational element – refers to the past and habitual behaviour. The actor will

repeat past patterns of thought and action.

The projective element – refers to the future. The actor will reconfigure thought and

action based on hopes fears and desires for the future.

The practical evaluative element – The actor will make practical and normative

judgements when presented with evolving situations. (Adapted from Emirbayer and

Mische, 1998:971).

Following Stones (2005:123) recurrent steps the information provided by the agent in

focus can be analysed using the quadripartite framework and whether the first two

elements of the framework result in possibilities or constraints in relation to the action

of the agent in focus and the final outcome.

An interview structure designed to be compatible with Stones (2005) quadripartite

framework will need to ensure data is collected which evaluates the agents conduct

and context and investigates the agents perception of internal and external

structures which affect their conduct in relation to the event under investigation.

Lorenz (2015) having conducted interviews in such a manner to answer the research

questions: “How do Management accounting tools become embedded in service

sector organisations and What are the reasons for change/lack of change in

management accounting tools used in service sector organisations” (2015:9) used a

thematic review of interviews with five agents in focus based on the four elements of

the quadripartite framework and highlighting for external and internal structures

whether these were perceived by the agent in focus as barriers or enablers to their

ability to change management accounting practices. The findings demonstrated a

wide range of external and internal structures influencing the embeddedness of tools

and the ability to diffuse and change practices over time. The evaluation of external

structures provided additional evidence of commonality of barriers and enablers

within service organisations and also provided further proof that in a service sector

context a theory practice gap was evident in terms of education.

In his 2012 working paper Stones additionally introduces the need to focus on the

empirical evidence “to help sharpen a sense of the value of the theoretical tools

presented for the critical appreciation of the status and quality of particular research

accounts” (2012:17), whilst this was in the context of migration issues there is no

reason that accounting researchers cannot also consider the hermeneutics of their

case studies in the same way. Stones (2012) created a framing mechanism which he

later refined and developed in 2015.

Stones (2015) suggests that the studies can be contextualising or floating and can

be based on Subjective analysis, objective analysis or a combination of both, see

figure 5 below. Stones (2012) differentiates between contextualising and floating in

relation to the detail, Stones likens floating to an air balloon ride where one surveys

the wider picture from afar but does not document the detailed interactions even if

they have that information, whereas a contextualising study focuses on the context in

detail of both the actors and structures that shape the future action. Subjective

analysis is based on the agents’ subjective perceptions and objective analysis on the

knowledge of the networks. Stones (2015) suggests that box 2a provides the best

combination as it provides research which provides detailed deep knowledge of the

relations but also shows how this interweaves with the agents own perceptions of

and orientation to the networks, this bringing together the content and the context of

the agent.

The use of this framing mechanism will allow accounting researchers to decide on

methodology and also make that methodological approach clear in regards to their

studies.

Figure 5: Types and degrees of knowledge regarding the contextual frame

Subjective Analysis Combined

Subjective and

Objective Analysis

Objective Analysis

High Levels of

Contextual

Detail

1a) Detailed

subjectivity

2a) Detailed

subjectivity situated

within dense

networks of

relations

3a) Detailed dense

networks of

relations

Low Levels of 1b) Thin, partial 2b) Thin, partial 3b) Thin, partial

Contextual

Detail

subjectivity subjectivity situated

within thin, partial

networks of

relations

networks of

relations

(Stones, 2015:108)

The research conducted by Lorenz (2015) using the quadripartite framework was

able to interweave both the objective analysis and subjective analysis which a high

level of contextual detail. By examining the external structures it was possible to

view those macro level structures which could have been identified with Institutional

theory but it was possible with strong structuration theory to add to those the

subjective views of the agents in terms of what they felt constrained them with

differing views of agents as to whether the nature of the industry was a barrier to

change or an enabler. A further interesting level was obtained by considering the

agent’s conduct and demonstrating how their relations with other agents and their

specific understanding regarding their jobs and roles shaped their actions and also

became either enablers or barriers to changing actions and therefore outcomes.

Without this combined approach to focusing on structure and people key insights

would have been missed.

The research conducted by Feeney and Pierce (2014) also used the same research

approach and was again able to establish the link between the subjective and

objective analysis to show the different way that accounting information is used in

two divisions of one company.

6. Conclusions

There has been a growing amount of management accounting research both in

terms of topics and theoretical basis. Much of the work conducted could be seen to

be based on economic theory (Coad et al, 2015) and can be seen from the

categorisation of mainstream management accounting research (Chua, 1986). There

has been a growing move to the use of social theory particularly the use of

institutional theory in management accounting resulting in the development of the

interpretive and critical management accounting research.

Over time that research has expanded to include studies linked to structuration

theory though review of the work provided by England et al, 2011 and Englund and

Gerdin, 2014) suggests that more use could have been made of structuration theory

in order to gain better insights into accounting practice. This is resonant with

Baldvinsdottir et al (2010) who reflect more generally that that there has still been a

lack of research related to what might benefit practice, and Scapens (2006b) also

reflected the need to make “theoretically informed management accounting research

more relevant to management accounting practitioners” (2006b:9).

Stones (2005) strong structuration theory which attempts to overcome problems

associated with structuration theory and also attempts to combine a framework for

ontology, epistemology and method provides accounting researchers with the tools

to provide deeper and more meaningful insights into practices and an understanding

of both agents and structures and their recursive relationship.

Studies are now coming to the fore which attempt to interpret Stones research

design and apply the methodology suggested (Lorenz, 2015, Feeney and Pierce,

2014). Coad et al (2015) highlight several unpublished theses which have made use

of the quadripartite framework and have revealed new insights in management

accounting.

This paper has reviewed management accounting research from the perspective of

management accounting change and has highlighted how the different theories have

added to our understanding of the reasons for lack of change or slow change in

management accounting tools used. The paper has also reviewed Stones work in

terms of providing a research design which could be followed by future researchers

in order to attempt to use theory flexibly and produce research using theory which is

of value to practice.

References

Abdel-Kader, M., & Luther, R. (2008). The impact of firm characteristics on management accounting practices: A UK-based empirical analysis. The British Accounting Review, 40(1), 2-27.

Akbar, S. (2010). Management accouting change: a comparative study of Indian and UK organsiations. Journal of Global Business Advancement, 3(1), 1-27.

Alsharari, N., Dixon, R., & Youssef, M. (2015). Management accounting change: critical review and a new contextual framework. Journal of Accounting & Organizational Change, 11(4),, 476-502.

Archer, M. (1982). Morphogenesis versus structuration: on combining structure and action. The British journal of sociology, 33(4), 455-483.

Archer, M. (1995). Realist Social Theory: The Morphogenetic Approach. Cambridge: Cambridge University Press.

Ashraf, J., & Uddin, S. (2015). Management Accounting Research and Structuration Theory: A Critical Realist Critique. Journal of critical realism, 14(5),, 485-507.

Baiman, S. (1982). Agency theory in managerial accounting: a survey. Jounrnal of Accountng Literature, 1(1), 154-213.

Baiman, S. (1990). Agency research in managerial accounting: A second look. Accounting, Organizations and Society, 15(4), 341-371.

Baines, A., & Langfield-Smith, K. (2003). Antecedents to management accounting change: a structural equation approach. Accounting, organizations and society, 28(7), 675-698.

Baldvinsdottir, G., Mitchell, F., & Nørreklit, H. (2010). Issues in the relationship between theory and practice in management accounting. Management Accounting Research, 21(2), 79-82.

Banker, R., Field, J., Schroeder, R., & Sintia, K. (1996). Impact of work teams on manufacturing performance: A longitudinal field study. Academy of Management Journal, 39(4), 867-890.

Barley, S. (1986). Technology as an occasion for structuring: Evidence from observations of CT scanners and the social order of radiology departments. Administrative science quarterly, 78-108.

Barley, S., & Tolbert, P. (1997). Institutionalization and structuration: Studying the links between action and institution. Organization studies, 18(1), 93-117.

Barrett, M., Cooper, D., & Jamal, K. (2006). Globalization and the coordinating of work in multinational audits. Accounting, Organizations and Society, 30(1),, 1-24.

Bjørnenak, T. (1997). Diffusion and accounting: the case of ABC in Norway. Management Accounting Research, 8(1), 3-17.

Burns, J., & Scapens, R. (2000). Conceptualizing management accounting change: an institutional framework. Management Accounting Research, 11, 3-25.

Burns, J., & Vaivio, J. (2001). Management accounting change. Management accounting research, 12(4), 389-402.

Burns, J., Ezzamel, M., & Scapens, R. (1999). Management accounting change in the UK. Management Accounting, 28-30.

Busco, C. (2006). Interpreting management accounting systems within processes of organisational change. Methodological Issues in Accounting: Theories and Methods, 2263-246.

Busco, C. (2009). Giddens’ structuration theory and its implications for management accounting research. Journal of Management & Governance, 13(3),, 249-206.

Busco, C., & Scapens, R. (2011). Management accounting systems and organisational culture: Interpreting their linkages and processes of change. Qualitative Research in Accounting & Management, 8(4),, 320-357.

Busco, C., Quattrone, P., & Riccaboni, A. (2007). Management accounting: issues in interpreting its nature and change. Management Accounting Research, 18(2), 125-149.

Chanegrih, T. (2008). Applying a typology of management accounting change: A research note. Management Accounting Research, 19(3), 278-285.

Chenhall, R. (2003). Management control systems design within its organizational context: findings from contingency-based research and directions for the future. Accounting, organizations and society, 28(2), 127-168.

Chua, W. (1986). Radical developments in accounting thought. Accounting review, 601-632.

Clegg, S. (1989). Frameworks of power. London: Sage.

Coad, A., & Glyptis, L. (2014). Structuration: A position–practice perspective and an illustrative study. Critical Perspectives on Accounting, 25(2), 142-161.

Coad, A., & Herbert, I. (2009). Back to the future: New potential for structuration theory in management accounting research? Management Accounting Research, 20(3), 177-192.

Coad, A., Jack, L., & Kholeif, A. (2015). Structuration theory: reflections on its further potential for management accounting research. Qualitative Research in Accounting & Management, 12(2), 153-171.

Cohen, I. (1989). Structuration theory: Anthony Giddens and the constitution of social life. London: Macmillan.

Conrad, L. (2005). A structuration analysis of accounting systems and systems of accountability in the privatised gas industry. Critical perspectives on accounting, 16(1), , 1-26.

Conrad, L. (2014). Reflections on the application of and potential for structuration theory in accounting research. Critical Perspectives on Accounting, 25(2), 128-134.

Cooper, R., & Slagmulder, R. (2004). Interorganizational cost management and relational context. Accounting, Organizations and Society, 29(1), , 1-26.

Covaleski, M., Dirsmith, M., & Samuel, S. (1996). Managerial accounting research: the contributions of organizational and sociological theories. Journal of

Management Accounting Research, 8, 1-36.

David, R., & Han, S. (2004). A systematic assessment of the empirical support for transaction cost economics. Strategic management journal, 25(1),, 39-58.

Dillard, J., Rigsby, J., & Goodman, C. (2004). The making and remaking of organization context: duality and the institutionalization process. Accounting, Auditing & Accountability Journal, 17(4),, 506-542.

DiMaggio, P., & Powell, W. (1991). Introduction. In P. DiMaggio, & W. Powell (Eds), The new institutionalism in organizational analysis (Vol. 17). Chicago, IL: University of Chicago Press.

Drury, C., Braund, S., Osbourne, P., & Tayles, M. (1993). A Survey of Management Accounting Practices in UK Manufacturing Companies. London: The Chartered Association of Certified Accountants.

Edwards, T. (2006). Book Review: Developments Toward the Operationalization of Structuration Theory. Organization, 13(6), , 911-913.

Emirbayer, M., & Mische, A. (1998). What is agency? American journal of sociology, 103(4),, 962-1023.

Englund, H., & Gerdin, J. (2011). Agency and structure in management accounting research: reflections and extensions of Kilfoyle and Richardson. . Critical Perspectives on Accounting, 22(6), 581-592.

Englund, H., & Gerdin, J. (2014). Structuration theory in accounting research: Applications and applicability. Critical Perspectives on Accounting, 25(2), 162-180.

Englund, H., Gerdin, J., & Burns, J. (2011). 25 Years of Giddens in accounting research: Achievements, limitations and the future. Accounting, Organizations and Society, 36(8), 494-513.

Ezzamel, M., Lilley, S., & Willmott, H. (1996). The View from the Top: Senior Executives' Perceptions of Changing Management Practices in UK Companies. British Journal of Management, 7(2), 155-168.

Feeney, O., & Pierce, B. (2016). Strong Structuration Theory and Accounting Information: An Empirical Study. Paper presented at SST workshop, Paris.

Giddens, A. (1984). The constitution of society: Outline of the theory of structuration. Cambridge: Polity Press.

Granlund, M., & Lukka, K. (1998). It's a small world of management accounting practices. Journal of Management Accounting Research, 10, 153-179.

Gurd, B. (2008). Structuration and middle-range theory—A case study of accounting during organizational change from different theoretical perspectives. Critical Perspectives on Accounting, 19(4),, 523-543.

Haldma, T., & Lääts, K. (2002). Contingencies influencing the management accounting practices of Estonian manufacturing companies. Management

Accounting Research, 13(4), 379-400.

Hardy, C. (1996). Understanding power: bringing about strategic change. British Journal of Management, 7(s1),, S3-S16.

Hopper, T., & Powell, A. (1985). Making sense of research into the organizational and social aspects of management accounting: A review of its underlying assumptions. Journal of management Studies, 22(5), 429-465.

Hopper, T., Otley, D., & Scapens, R. (2001). British Management Accounting Research: Whence and Whither: Opinions and Recollections. British Accounting Review, 33, 263-291.

Jack, L., & Kholeif, A. (2007). Introducing Strong Stucturation Theory for case studies in Organisation, Management and Accounting Research. Qualitative Research in Organizations and Management, 208-225.

Jack, L., & Kholeif, A. (2008). Enterprise resource planning and a contest to limit the role of management accountants: a strong structuration perspective. Accounting Forum Vol. 32, No. 1, 30-45.

Jarvenpaa, M. (1998). Management Accounting and strategy. Functional and Institutional perspectives; A case study. Proceedings, Asia Pacific Interdisciplinary Research in Accounting Conference, Osaka, Japan.

Johnson, H., & Kaplan, R. (1987). Relevance Lost: The Rise and Fall of Management Accounting. Boston: Harvard Business School Press.

Kelly, M., & Pratt, M. (1992). Purposes and paradigms of management accounting: beyond economic reduction. Accounting Education, 1(3), 225-246.

Kunz, A., & Pfaff, D. (2002). Agency theory, performance evaluation, and the hypothetical construct of intrinsic motivation. Accounting, organizations and society, 27(3), 275-295.

Lambert, R. (2006). Agency theory and management accounting. In C. Chapman, A. Hopwood, & M. Shields, Handbooks of management accounting research, 1, (pp. 247-268). London: Elsevier.

Lapsley, I., & Pettigrew, A. (1994). Meeting the challenge: accounting for change. Financial Accountability & Management, 10(2), 79-92.

Laughlin, R. (1995). Empirical research in accounting: alternative approaches and a case for 'middle-range thinking'. Accountng, Auditing and Accountability, 8(1), 63-87.

Lawrence, S., Alam, M., Northcott, D., & Lowe, T. (1997). Accounting systems and systems of accountability in the New Zealand health sector. Accounting, Auditing & Accountability Journal, 10(5), 665-683.

Libby, T., & Waterhouse, J. (1996). Predicting change in management accounting systems. Journal of management accounting research, 8, 137.

Lorenz, A. (2015). Contemporary management accounting in the UK service sector, unpublished thesis, University of Gloucestershire.

Luft, J., & Shields, M. (2002). Zimmerman's contentious conjectures: describing the present and prescribing the future of empirical management accounting research. European Accounting Review, 11(4), 795-803.

Lukka, K. (2007). Management accounting change and stability: loosely coupled rules and routines in action. Management Accounting Research, 18(1), 76-101.

Macintosh, N., & Scapens, R. (1990). Structuration theory in management accounting. Accounting, Organizations and Society, 15(5), 455-477.

Macintosh, N., & Scapens, R. (1991). Management accounting and control systems: a structuration theory analysis. Journal of Management Accounting Research, 3(3), 131-158.

Malmi, T. (1999). Activity-based costing diffusion across organizations: an exploratory empirical analysis of Finnish firms. Accounting, Organizations and Society, 24(8), 649-672.

Messner, M. (2015). Does industry matter? How industry context shapes management accounting practice. Management Accounting Research.

Mia, L., & Patiar, A. (2001). The use of management accounting systems in hotels: an exploratory study. International Journal of Hospitality Management, 20(2), 111-128.

Morawska, E. (2012). Studying International Migration in the Long (er) and Short (er) Durée: Contesting Some and Reconciling Other Disagreements Between the Structuration and Morphogenetic Approaches.

Ogata, K., & Spraakman, G. (2013). The persistence of delegitimated structures: Insights from changes to management accounting at the Hudson's Bay Company, 1670-2005. Journal of Accounting & Organizational Change, 9(3),, 280-303.

Otley, D. (1980). The contingency theory of management accounting: achievement and prognosis. Accounting, organizations and society, 5(4), 413-428.

Parker, J. (2006). Structuration's Future? From ‘All and Every’to ‘Who Did What, Where, When, How and Why? Journal of Critical Realism, 5(1), 122-138.

Quinn, M. (2014). Stability and change in management accounting over time—A century or so of evidence from Guinness. Management Accounting Research, 25(1), 76-92.

Ribeiro, J., & Scapens, R. (2006). Management accounting and power: a contested relationship. Faculdade de Economia, Universidade de Porto.

Robalo, R. (2014). Explanations for the gap between management accounting rules and routines: An institutional approach. Revista de Contabilidad, 17(1), 88-97.

Roberts, J. (2014). Testing the limits of structuration theory in accounting research. Critical Perspectives on Accounting, 25(2), 135-141.

Roberts, J., & Scapens, R. (1985). Accounting systems and systems of accountability—understanding accounting practices in their organisational contexts. Accounting, Organizations and Society, 10(4), 443-456.

Ryan, R., Scapens, R., & Theobald, M. (2002). Research Method and Methodology in Finance and Accounting 2nd Ed. Padstow: Thomson Learning.

Scapens, R. (2006a). Changing times: management accounting research and practice from a UK perspective. In A. Bhimani, Contemporary Issues in Management Accounting (pp. 329-354). Oxford: Oxford University Press.

Scapens, R. (2006b). Understanding Management Accounting Practices: A personal Journey. The British Accounting review, 38, 1-30.

Scapens, R. W., & Arnold, J. (1986). Economics and management accounting research. In M. Bromwich, & A. Hopwood, Research and Current Issues in Mangement Accounting. London: Pitman.

Scapens, R., & Arnold, J. (1986). Economics and management accounting research. In M. Bromwich, & A. Hopper, (Eds) Research and Current Issues in Management Accounting (pp. 78-102). London: Pitman.

Seal, W., & Vincent-Jones, P. (1997). Accounting and trust in the enabling of long-term relations. Accounting, auditing & accountability Journal, 10(3), 406-431.

Shields, M. (1997). Research in management accounting by North Americans in the 1990s. Journal of Management Accounting Research, 9, 3-61.

Siti-Nabiha, A., & Scapens, R. (2005). Stability and change: an institutionalist study of management accounting change. Accounting, Auditing & Accountability Journal, 18(1), 44-73.

Spicer, B. H., & Ballew, V. (1983). Management accounting systems and the economics of internal organization. Accounting, Organizations and Society, 8(1),, 73-96.

Stones, R. (2001). Refusing the Realism—Structuration Divide. European journal of social theory, 4(2), 177-197.

Stones, R. (2005). Structuration theory. Basingstoke: Palgrave Macmillan.

Stones, R. (2012). Causality, contextual frames and international migration: combining strong structuration theory, critical realism and textual analysis. Working papers, International Migration Institute,, November, 1-18.

Stones, R. (2015). Why Current Affairs Needs Social Theory. London: Bloomsbury.

Stones, R. (2016). Putting the Key features of Strong Structuration Theory to use. SST workshop. Paris.

Sulaiman, S., & Mitchell, F. (2005). Utilising a typology of management accounting change: An empirical analysis. Management Accounting Research, 16(4),

422-437.

Thrift, N. (1985). Bear and mouse or bear and tree? Anthony Giddens's reconstitution of social theory. Sociology 19(4), 609-623.

Tomkins, C., & Groves, R. (1983). The everyday accountant and researching his reality. Accounting, Orgasnization and Society, 8(4), 361-374.

van der Steen, M. (2011). The emergence and change of management accounting routines. Accounting, Auditing & Accountability Journal, 24(4),, 502-547.

Wanderley, C., & Cullen, J. (2012a). A Case of Management Accounting Change: the Political and Social Dynamics. Revista Contabilidade & Finanças-USP, 23(60)., 161-172.

Wanderley, C., & Cullen, J. (2012b). Management Accounting Research: Mainstream versus Alternative Approaches. Contabilidade Vista & Revista, 22(4), 15-44.

Waterhouse, J., & Tiessen, P. (1978). A contingency framework for management accounting systems research. Accounting, Organizations and Society, 3(1), 65-76.

Wickramasinghe, D., & Alawattage, C. (2007). Management accounting change: approaches and perspectives. Abingdon: Routledge.

Wijewardena, H., & De Zoysa, A. (1999). A comparative analysis of management accounting practices in Australia and Japan: an empirical investigation. The International Journal of Accounting, 34(1), 49-70.

Wilson, R., & Chua, W. (1983). Managerial accounting: method and meaning (Vol. 2). London: Chapman & Hall.

Zimmerman, J. (1979). The Costs and Benefits of Cost Allocations. Accounting Review, 54(3), 504-521.