theory of storage and the dynamics of metals forward...

TRANSCRIPT

Theory of Storage and the Dynamics of Metals Forward Curves

Helyette GemanDirector, Commodity Finance Centre

University of London and ESCP EuropeScientific Advisor to the European Commission

To be presented at the Vale Conference on CommoditiesGetulio Vargas Foundation - Rio de Janeiro

August 16 & 17, 2012

Metals, Energy, Agriculturals : A Multi or Unique Asset Class?

→ Commodities have displayed over the last 30 years

. a period of low prices in the 1980s and 1990s, strictly declining if adjusted for inflation, and low volatility

. low correlations between metals, energy, agriculturals

→ Then much higher prices prevailed as of 2002 for crude oil, as of 2004 for copper, 2005 for agriculturals. In the case of iron ore, long-term contracts imposed by steelmakers broke down after the concerted action of Vale, Rio Tinto and BHP Billiton

High correlations appeared, created. by the massive arrival of financial actors buying at the same time several

commodities such as copper, gold, crude oil in the form of a commodity index

. by the effects of substitution between commodities and competition for the same rare resources, called electricity , water, land

CRB Commodity Index – 1988 to 2011

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Data from Yahoo Finance via Matlab Datafeed toolbox

Brazil Equity versus UK Equity

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

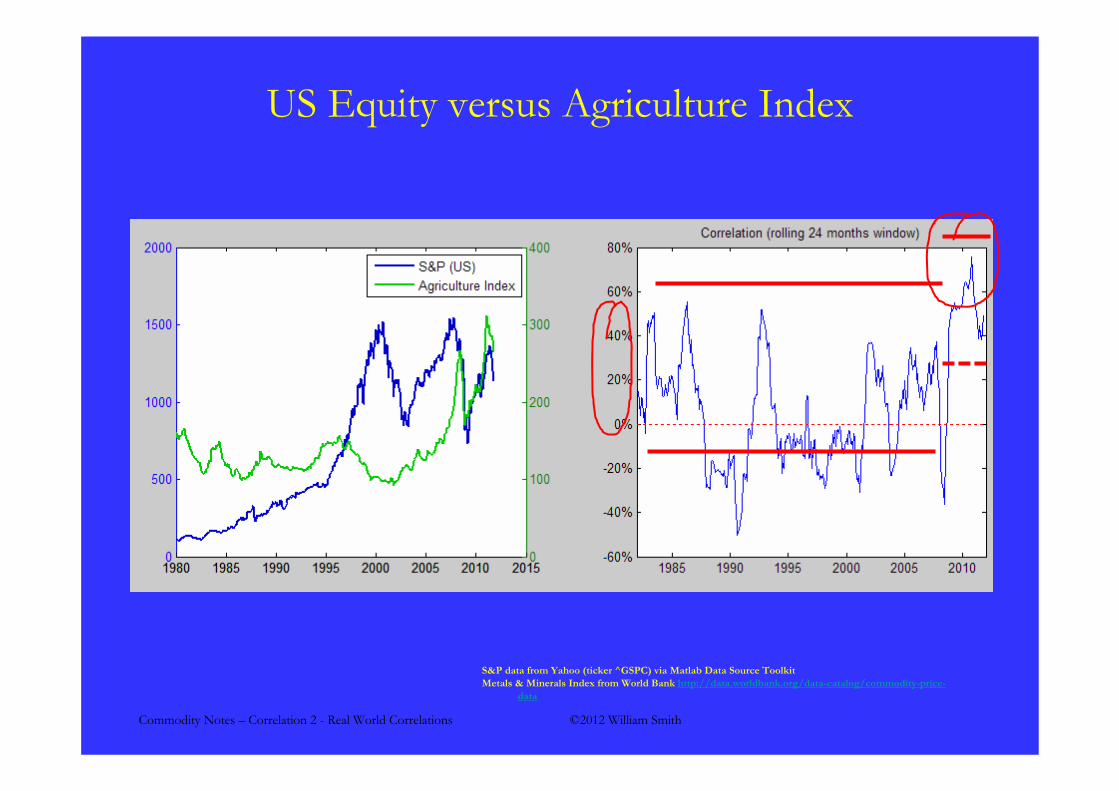

S&P data from Yahoo (ticker ^GSPC) via Matlab Data Source ToolkitAgriculture Index from World Bank http://data.worldbank.org/data-catalog/commodity-price-data

US Equity versus the Metals and Minerals Index:‘Risk on/ Risk off ‘ behaviour recently !

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

S&P data from Yahoo (ticker ^GSPC) via Matlab Data Source ToolkitMetals & Minerals Index from World Bank http://data.worldbank.org/data-catalog/commodity-price-

data

US Equity versus Agriculture Index

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

S&P data from Yahoo (ticker ^GSPC) via Matlab Data Source ToolkitEnergy Index from World Bank http://data.worldbank.org/data-catalog/commodity-price-data

US Equity versus Energy Index

Metal Reserves

New mining techniques, deeper drilling and mining in untapped places such as Greenland, Mongolia and the Arctic should lead to years in mineral reserves, at current production rates, estimated at 590 for iron ore, 136 for copper, 610 for potash; versus 18.9 for gold, 46.2 for crude oil and 82 for metallurgical coal

Hotelling in his (1931) paper on exhaustible commodities had established that the shadow price of the resource, which is an economic measure of its scarcity, should grow at least at the rate of interest

→ Young (1992) applies Hotelling model to Canadian copper mining firms and finds it poorly depicts the database he analyzes; but the period of analysis ended in 1990 and was the period of price mean- reversion ( G. 2005 : Is Mean Reversion in Commodity Prices Dead? )

→ It is useful to recognize that the possible decline in the quality of the

BDI, Copper and the world economy growth

Dislocation between BDI and Copper Prices

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Commodiity Monthly Prices from World Bank http://data.worldbank.org/data-catalog/commodity-price-data

Copper versus Crude Oil

Copper Volatility Smile - April 6, 2012

Merrill Lynch, “Modelling the Implied Volatility Surface”, http://finmath.stanford.edu/seminars/docs/ml2004win.pdf

Implied Volatility “Surface”(bottom axes are price and time to maturity)

Implied vol

Strike Price

Time to Maturity

0.15

0.17

0.19

0.21

0.23

0.25

0.27

0.29

0.8 0.85 0.9 0.95 1 1.05 1.1 1.15

Impl

ied

Vola

tility

K/S

Gold 1st Contract (22 Jun 2012)

Theory of StorageKeynes (1936), Kaldor (1939), Working (1949)

Three fundamentals results:

→ The holder of the physical commodity receives an implicit dividend called convenience yield

→ The volatility of the commodity spot price is high when inventory is low

→ Traditionally, forward curves used to be mostly declining with the maturity ( ‘normal backwardation’) and sometimes in contango. Today, we even get humps

→ The dynamics of the global forward curve matters, in hedging activities in particular, since one never hedges with the prompt- month

The Forward Curve

→ The set {FT (t) , T > t} is the forward curve prevailing at date t for a givencommodity in a given location

→ It is the fundamental tool when trading commodities, as spot prices may beunabservable and options not always liquid

→ It allows to identify the prices forecasted by the market at future dates since realtrades did take place at these prices

→ The shape of the forward curve is a crucial piece of financial information to becompared to all the other sources!

Crude Oil in Backwardation in September 2007

68

70

72

74

76

78

80

M1 M5 M9 M13 M17 M21 M25 M29 M33 M37 M41 M45 M49 M53 M57 M61

WTI Oil Prices Jan 2002 - Oct 2007

0

20

40

60

80

100

120

1/1/

2002

4/23

/200

2

8/13

/200

2

12/3

/200

2

3/25

/200

3

7/15

/200

3

11/4

/200

3

2/24

/200

4

6/15

/200

4

10/5

/200

4

1/25

/200

5

5/17

/200

5

9/6/

2005

12/2

7/20

05

4/18

/200

6

8/8/

2006

11/2

8/20

06

3/20

/200

7

7/10

/200

7

10/3

0/20

07

Spot-Forward Relationship for a Storable Commodity

Under no arbitrage

( ) ( ) ( ) ( ) ( )⎥⎥⎥

⎦

⎤

⎢⎢⎢

⎣

⎡−−−+−+=43421321321

dividendimplicitstorageoftcosfinancingoftcos

tTytTctTr1tStf 1T

If we define a convenience yield net of cost of storage

( ) ( ) ( )( )[ ]tTyr1tStf T −−+=

Or in continuous time, at a fixed date t (today), for a given maturity T

( ) ( ) ( )( )tTyrT etStf −−=

Copper Forward Curve - 27 May 2008 : Backwardation

345

350

355

360

365

370

375

380

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10 M11 M12 M13 M14 M15 M16 M17 M18 M19 M20 M21 M22 M23 M24

Copper COMEX

Crude Oil Future curve (17/11/2008)

50

55

60

65

70

75

80

85

M1 M4 M7 M10 M13 M16 M19 M22 M25 M28 M31 M34 M37 M40 M43 M46 M49 M52 M55 M58 M61

Forward Curve

62,37

63,37

64,37

65,37

66,37

67,37

68,37

mars-06

juil-0

6nov

-06mars-

07jui

l-07

nov-07

mars-08

juil-0

8nov

-08mars-

09jui

l-09

nov-09

mars-10

juil-1

0nov

-10mars-

11jui

l-11

nov-11

mars-12

juil-1

2nov

-12mars-

13jui

l-13

nov-13

mars-14

juil-1

4

Maturity

Forw

ard

Pric

e

WTI Forward Bid WTI Forward Offer

A hump in the Oil Forward Curve (bid/ ask) - March 2006

Copper Forward Curve, Oct 2009

3.1

3.15

3.2

3.25

3.3

3.35

3.4

3.45

1-Au

g-12

1-Oc

t-12

1-De

c-12

1-Fe

b-13

1-Ap

r-13

1-Ju

n-13

1-Au

g-13

1-Oc

t-13

1-De

c-13

1-Fe

b-14

1-Ap

r-14

1-Ju

n-14

1-Au

g-14

1-Oc

t-14

1-De

c-14

1-Fe

b-15

1-Ap

r-15

1-Ju

n-15

1-Au

g-15

1-Oc

t-15

1-De

c-15

1-Fe

b-16

1-Ap

r-16

1-Ju

n-16

1-Au

g-16

1-Oc

t-16

1-De

c-16

1-Fe

b-17

1-Ap

r-17

1-Ju

n-17

Copper 14 Aug 2012

Copper

0

10

20

30

40

50

60

70

80

90

Coal 14 Aug 2012

Coal

0

1

2

3

4

5

6

71-

Sep-

12

1-De

c-12

1-M

ar-1

3

1-Ju

n-13

1-Se

p-13

1-De

c-13

1-M

ar-1

4

1-Ju

n-14

1-Se

p-14

1-De

c-14

1-M

ar-1

5

1-Ju

n-15

1-Se

p-15

1-De

c-15

1-M

ar-1

6

1-Ju

n-16

1-Se

p-16

1-De

c-16

1-M

ar-1

7

1-Ju

n-17

1-Se

p-17

1-De

c-17

1-M

ar-1

8

1-Ju

n-18

1-Se

p-18

1-De

c-18

1-M

ar-1

9

1-Ju

n-19

1-Se

p-19

1-De

c-19

1-M

ar-2

0

1-Ju

n-20

1-Se

p-20

1-De

c-20

NG 14 Aug 2012

NG

From CME Group, http://www.cmegroup.com/trading/metals/ferrous/iron-ore-62pct-fe-cfr-china-tsi-swap-futures_quotes_settlements_futures.html

Iron Ore Futures Curve

China import Iron Ore Fines 62% FE spot (CFR Tianjin port), US Dollars per Metric Tonhttp://www.indexmundi.com/commodities/?commodity=iron-ore&months=60

Iron Ore – Evolution of Spot Price

Inventory, Volatility and Shape of the Forward Curve

→Working (1949) proposed to use the spread of the forward curve (long term forward – short term forward) as a proxy for inventory : when the spread is negative, inventory is low

→ Fama and French (1988) use LME Future prices over the period 1972 to1983 to test five base metals (copper, aluminium, copper, lead, tin and zinc) and find that the variance of spot prices declines with high inventories. In the case of gold, forward curve spreads provided little forecast for price volatility.

→Ng and Pirrong (1994) analyze four base metals over the period 1986 to 1992 and find persistence of the property that both spot and forward variance declines with inventory in the case of metals

→G - Nguyen ( 2005) reconstruct a world inventory of soybeans over several years and directly exhibit a quasi- perfect inverse relationship between inventory and spot price volatility

→G- Ohana (2009) . Examine at US crude oil and natural gas markets. Show that indeed the spread of the forward curve is a good proxy for

inventory. Exhibit that the correlation between the spread of the forward curve and low

inventory is particular significant during periods of scarcity

G – Smith (2012) . Reconstruct inventory for copper, lead, iron, tin from the addition of the LME and SHFE data. Validate the use of the spread of the forward curveas a measure of inventory. Display directly an affine relationship between inverse inventory and spot price volatility

Copper Inventory – 1985 to 2011

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Why Should Different Commodities Be Correlated?

Correlation (A,B) > 0

Economic Effects

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Why Should Different Commodities Be Correlated?

Correlation (A,B) > 0

Water for Agriculture or Mining or Oil & Gas “Fracking”

Shipping for Metal ore or Agriculturals

Land for Residential Land or Agriculture or Mining

Offshore Experts for Windfarms or Offshore Oil

Resource Competition

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Commodiity Montly Prices from World Bank http://data.worldbank.org/data-catalog/commodity-price-data

Agriculture Index versus Base Metals Index

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Why Should Different Commodities Be Correlated?

Aluminium Ore(Bauxite)

Aluminium

A is needed to produce B

Correlation (A,B) > 0

Lots of Electricity

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Why Should Different Commodities Be Correlated?

Substitution : A or B

Oil

Natural Gas

Electricity

Correlation (A,B) > 0

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Corn and Wheat Prices - 2000 to 2011

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

World Fertilizer Index – 2000 to 2011

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Why Should Different Commodities Be Correlated?

Correlation (B,C) > 0due to competition

Alternative Output : A can produce B or C

orSugar Cane

Sugar

Ethanol as Biofuel

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Commodiity Monthly Prices from World Bank http://data.worldbank.org/data-catalog/commodity-price-data

Sugar versus Crude Oil

?

Commodity Notes – Correlation 2 - Real World Correlations ©2012 William Smith

Why Should Different Commodities Be Correlated?

Correlation (A,B) > 0 since supplies of both occur at the same time.

Co-Production : A and B produced together

togetherwith

Zinc

Lead

COMEX Gold Prices - 2002 to 2010

Gold Prices since 1975

COMEX Gold 28/2/2007

600

650

700

750

800

850

mar

s-07

avr-

07

mai

-07

juin

-07

août

-07

oct-0

7

déc-

07

févr

-08

avr-

08

juin

-08

août

-08

oct-0

8

déc-

08

juin

-09

déc-

09

juin

-10

déc-

10

juin

-11

déc-

11

Contract months

Pric

e

COMEX Gold

Gold Forward Curve - 27 May 2008

800

850

900

950

1000

1050

1100

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10 M11 M12 M13 M14 M15 M16 M17 M18

Gold

Gold Forward Curve – Feb 2010

1550

1600

1650

1700

1750

1800

Apr-1

2

Jun-

12

Aug-

12

Oct-1

2

Dec-

12

Feb-

13

Apr-1

3

Jun-

13

Aug-

13

Oct-1

3

Dec-

13

Feb-

14

Apr-1

4

Jun-

14

Aug-

14

Oct-1

4

Dec-

14

Feb-

15

Apr-1

5

Jun-

15

Aug-

15

Oct-1

5

Dec-

15

Feb-

16

Apr-1

6

Jun-

16

Aug-

16

Oct-1

6

Dec-

16

Feb-

17

Apr-1

7

Jun-

17

Gold 4/ 9/ 2012

Gold

1540

1560

1580

1600

1620

1640

1660

1680

1700

1720

1740

Aug-

12

Oct-1

2

Dec-

12

Feb-

13

Apr-1

3

Jun-

13

Aug-

13

Oct-1

3

Dec-

13

Feb-

14

Apr-1

4

Jun-

14

Aug-

14

Oct-1

4

Dec-

14

Feb-

15

Apr-1

5

Jun-

15

Aug-

15

Oct-1

5

Dec-

15

Feb-

16

Apr-1

6

Jun-

16

Aug-

16

Oct-1

6

Dec-

16

Feb-

17

Apr-1

7

Jun-

17

Aug-

17

Oct-1

7

Dec-

17

Gold 14 Aug 2012

Gold

0.15

0.17

0.19

0.21

0.23

0.25

0.27

0.29

0.8 0.85 0.9 0.95 1 1.05 1.1 1.15

Impl

ied

Vola

tility

K/S

Gold 1st Contract (22 Jun 2012)

References

H. Geman and W. Smith (2012) “Inventories and Base Metals Forward Curves”, Resources PolicyH.Geman and S. Sarfo (2012) “Seasonality in Cocoa Spot and Forward Markets: Empirical Evidence”, Journal of Agricultural Expansion and Rural Development H.Geman ( 2011) “ Volatility in Commodity Spot Markets: Speculation or Scarcity?”, Swiss Derivatives ReviewH.Geman (2010) “Commodities and Numéraire”, Encyclopedia of Quantitative FinanceH. Geman and Yfong Shi (2009) “ The CEV model for Commodity Prices”, Journal of Alternative InvestmentsH. Geman and S. Kourouvakalis (2008) "A Lattice-Based Method for Pricing Electricity Derivatives under the Geman-Roncoroni Model", Applied Mathematical FinanceH. Geman and C. Kharoubi( 2008) “Diversification with Crude Oil Futures : the Time-to- Maturity Effect, Journal of Bankingand FinanceS. Borovkova and H. Geman (2006) "Seasonal and Stochastic Effects in Commodity Forward Curves", Review of Derivatives ResearchH. Geman and A. Roncoroni (2006) "Understanding the Fine Structure of Electricity Prices", Journal of BusinessH. Geman (2005) "Energy Commodity Prices: Is Mean Reversion Dead?", Journal of Alternative InvestmentsH. Geman and S. Ohana (2009) "Inventory, Reserves and Price volatility in Oil and Natural Gas Markets“,Energy EconomicsH. Geman (2005) "Commodities and Commodity Prices: Pricing and Modeling for Agriculturals, Metals and Energy", Wiley FinanceH. Geman and V. Nguyen (2005) "Soybean inventory and forward curves dynamics", Management ScienceH.Geman (2004) “Water as the Next Commodity”, Journal of Alternative InvestmentsH. Geman and M. Yor (1993) "An Exact Valuation for Asian Option", Mathematical FinanceA. Eydeland and H. Geman (1999) "Fundamentals of Electricity options" in Energy Price Modellng, Risk BooksH. Geman and O. Vasicek (2001) "Forwards and Futures on Non Storable Commodities", RISKH. Geman (2003) "DCF versus Real Option for Pricing Energy Physical Assets" Conference of the International Energy Agency - Paris