there are three important securities in the capital market. bonds / debentures preference shares...

TRANSCRIPT

There are three Important securities in the capital market.

Bonds / DebenturesPreference sharesEquity shares

Securities and their valuation

What is a security ? A legal representation of the right to receive prospective future benefits under stated conditions – Investments ; W.F Sharpe, G.J Alexander, J.V Bailey

What is a capital market ?

Bond / Debenture valuation

Face value

Coupon rate

Maturity dateRedemption valueMarket value

Bond with maturity period

Bond holder receives two types of cash flows

Periodic interest income

Maturity Value

Following formula helps to determine the value of the bond

INT1 INT2 INTn +Bn

Pm = + +-------+

(1+kd) (1+kd) (1+kd)n

Pm = n

t=1

Ci

(1+ i)t

Pp

(1+ i)n+

Pm = The current market price of the bond/debenture

Ci = The annual coupon payment for bond i

i = The prevailing yield to maturity for this bond issue

Pp = The par value of the bond

n = The number of years to maturity

Suppose an investor is considering to purchase a five-year, Rs.1000 par value bond ,Bearing a nominal rate of interest of 7%. The prevailing yield to maturity for this bond (required rate of return) is 8%. What should he be willing to pay now to purchase the bond if it matures at par?

B0 = 70/(1.08)1+70/(1.08)2+70/(1.08)3+70/(1.08)4+70/(1.08)5

= 64.81 + 60.01 + 55.568 + 51.45 + 47.64

Bo = 960.51

The government is proposing to sell a 5-years bond of Rs1000 at 8% rate of interest per annum. The bond amount will be amortized equally over it’s life. If an investor has a minimum required rate of return 7% what would be the bond’s present value for him?

Amortizing value per year = 1000 / 5 = 200 per each.

The amount of interest + Amortizing value

1st year 1000 x 8% = RS. 80.00 + 200 = 280

2nd year (1000-200) x8% = RS.64.00 + 200 =264

3rd year (800-200) x8% = RS.48.00 + 200 =248

4th year (600-200) x8% =RS.32.00 + 200 =232

5th year (400-200) x8% =RS.16.00 +200 =216

Bo =RS. 1025.66

Semi-annual interest payment

In practice, it is quite common to pay interest on bonds / debentures semiannually

Pm = 2n

t=1

Ci /2

(1+i /2)t

Pp

(1+i /2)2n+

A Ten-year bond of RS.1000 has an annual rate of interest of 12% the interest is paid half-yearly. If the required rate of return is 16%, what is the value of the bond?

210 (120)/2 1000

Bo = +

T=1 (1+0.16/2) t (1+0.16/2) 210

Bo =609.818 +10000.215

Bo =589.08 + 215 = RS.804.08

Perpetual Bonds

Bonds, which will never mature, are known as perpetual bonds.

Assume that a bond will pay RS.80 interest annually in to perpetuity what would be its Value

If the current yield is 7%?

If the current yield is 8%?

If the current yield is 12%?

INT 80

Bo = = = RS.1142.85

Kd 0.07

Assume a bond pays 10% interest for 20 years and has a par or maturity value of Rs. 1000. The interest rate in the market place is assumed to be 12%.

Bo = 747 + 104

Bo =RS. 851

If the price of Bond less than 851 better to purchase Otherwise better to reject.

Marvin Ranaweera is a knowledge investor who is always looking for a sound company to include in his portfolio of stocks and bonds. Being somewhat risk-averse, his main objective is to buy stock in firms that are mature and well-established in their respective industries. Wal-Mart (International company) is one of the stocks Marvin is currently considering for inclusion in his portfolio. Wal-Mart has four major areas of business: traditional Wal-Mart discount stores, Super-centers, Sam's Clubs, and international operations. Although Wal-Mart was established over 50 years ago, it continues to achieve growth through expansion.

The Super-center concept, which combines groceries and general merchandise, is extreme success as 75 new Super-centers were opened last year alone. Another 95 will be opening over the next two years.

Sam's clubs have also seen success as 99 Pace stores (Pace is one of Sam's former Competitors) were converted to Sam's stores in 1995. In addition to taking over competitor stores, Sam's also opened 22 new stores of its own.

Internationally, the picture is equally as rosy. In Canada, 122 former Woolco stores were converted to Wal-Mart discount stores. Expansion has reached Mexico and Hong Kong as well, as 24 Clubs and Super-centers and 3 "Value Clubs" were established, respectively.

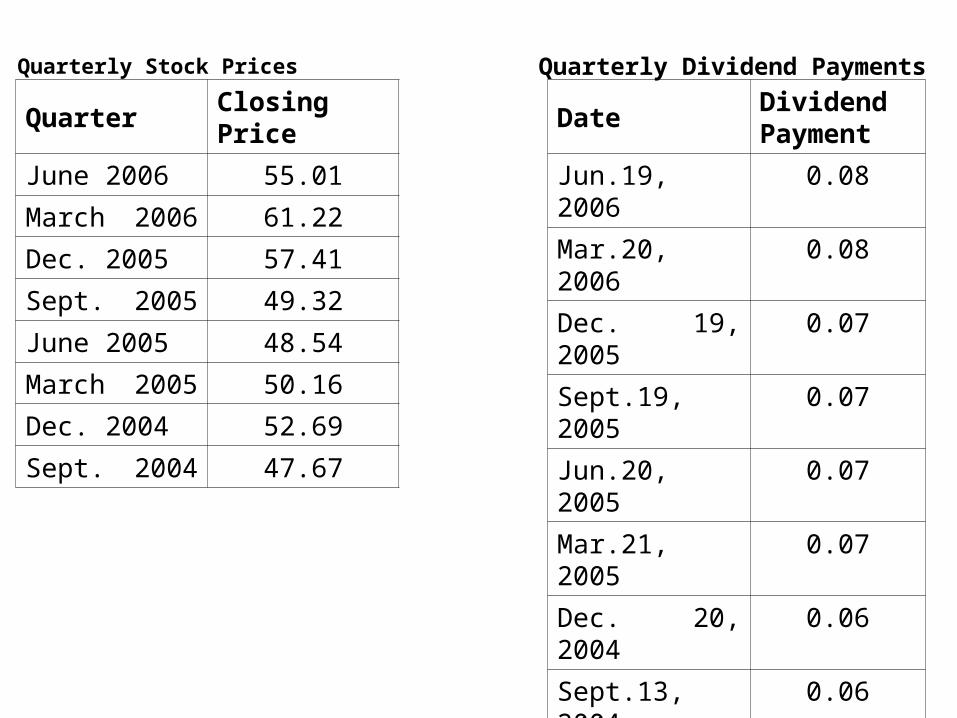

Wal-Mart plans to continue its reign as the world's largest retailer through expansion by developing the previously discussed 95 Wal-Mart discount stores, 12 new Super-centers and 9 new Sam's Clubs. Internationally, 20 to 25 new stores will be built in Hong Kong, China, Argentina, Brazil and Canada. In order to determine if Wal-Mart is a "good buy," Marvin has to perform several analyses. First, he must calculate the returns on Wal-Mart's common stock over the past eight quarters as an indicator of how the stock might perform over the next year. He must then calculate the standard deviation of the stock as a proxy for its risk. To aid in his calculation, Marvin has gathered the following stock price and dividend data.

Quarterly Stock Prices

Quarter Closing Price

June 2006 55.01

March 2006 61.22

Dec. 2005 57.41

Sept. 2005 49.32

June 2005 48.54

March 2005 50.16

Dec. 2004 52.69

Sept. 2004 47.67

Quarterly Dividend Payments

Date Dividend Payment

Jun.19, 2006 0.08

Mar.20, 2006 0.08

Dec. 19, 2005

0.07

Sept.19, 2005

0.07

Jun.20, 2005 0.07

Mar.21, 2005 0.07

Dec. 20, 2004

0.06

Sept.13, 2004

0.06

Calculate the returns for each of the seven quarters.

Calculate the standard deviation of the returns from question 1.

Marvin has decided to reduce his risk through diversification. In

which way he can diversify away his risk? What is the ideal

number of securities he should maintain in his portfolio? Justify

your answer with valid reasons.

Bond maturity and interest rate risk

The value of a bond depends upon the interest rate. As interest rate changes, the value of a bond also varies. There is an inverse relationship between the value of a bond and the interest rate. The value will decline when the interest rate rises and vice-versa. The intensity of interest rate risk would be higher on bonds with long maturities than those in short periods. Using the following three types of bonds can identify this situation.

Bond 5Y.B 10Y.B Perp.B

Interest Rate 7% 7% 7%

Maturity Value 1000 1000 Perpetuity

Int.Rate Value 5Y.B Value 10 Y.B Perp.B

4 1134 1244 1750

5 1087 1155 1400

6 1042 1073 1167

7 1000 1000 1000

8 961 933 875

9 922 871 778

10 886 816 700

Preference share valuation

P0 = Dp / Kd

Assume that a preference share pays Rs.12 dividend annually. What is the value of share if the current required rate of return is 10%.

P0 = 12 / 0.1

=120

Equity share valuation

One of the most widely used equity valuation model is the Dividend Discounting model (DDM).The DDM defines the intrinsic value of a share as the present value of future dividend. There are several valuation of the DDM because of different assumptions about the growth rate of dividend and its relationship to the discount rate used to calculate present value.

Zero growth model

Constant growth model / Normal growth model

Super normal growth model

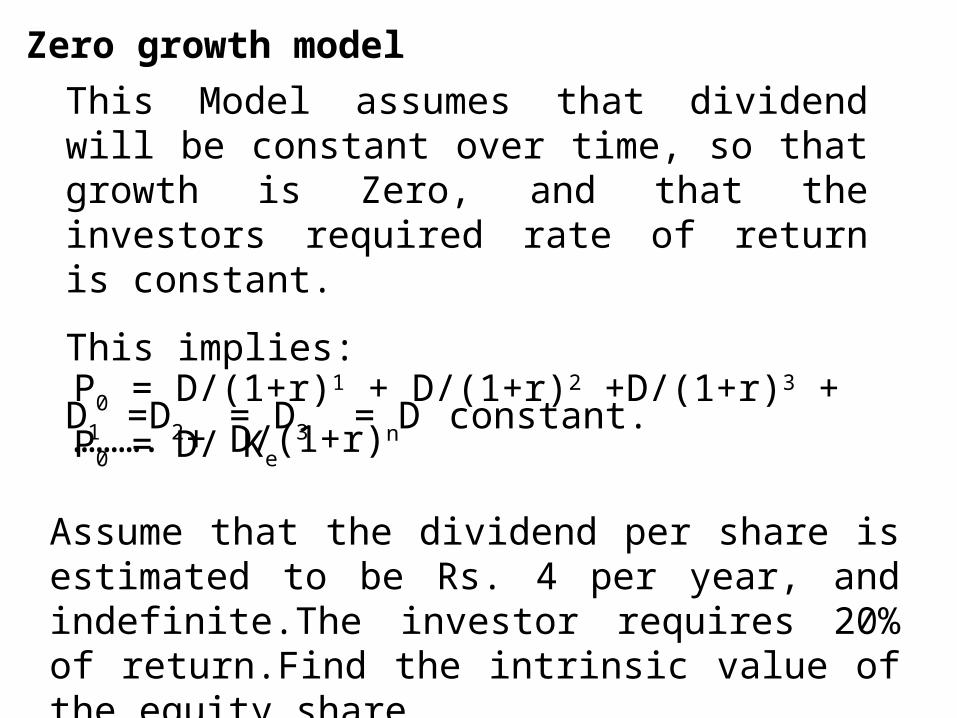

Zero growth model

This Model assumes that dividend will be constant over time, so that growth is Zero, and that the investors required rate of return is constant.

This implies:

D1 =D2 = D3 = D constant.

P0 = D/(1+r)1 + D/(1+r)2 +D/(1+r)3 + ………. + D/(1+r)n

P0 = D/ Ke

Assume that the dividend per share is estimated to be Rs. 4 per year, and indefinite.The investor requires 20% of return.Find the intrinsic value of the equity share.

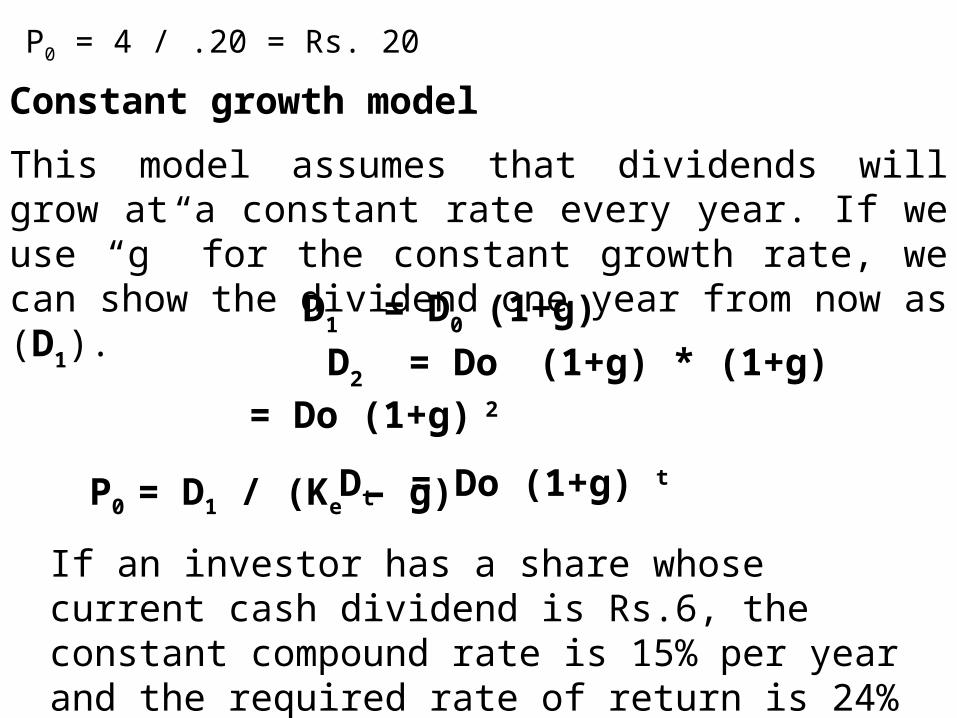

P0 = 4 / .20 = Rs. 20

Constant growth model

This model assumes that dividends will grow at a constant rate every year. If we use “g” for the constant growth rate, we can show the dividend one year from now as (D1).

D1 = D0 (1+g)

D2 = Do (1+g) * (1+g) = Do (1+g) 2

Dt = Do (1+g) t

P0 = D1 / (Ke – g)

If an investor has a share whose current cash dividend is Rs.6, the constant compound rate is 15% per year and the required rate of return is 24% find the Value of the equity share.

P0=D1/(Ke–g) =6(1+0.15)/(0.24–0.15) =6.9/0.09=76.67Current dividend is Rs.2.30, required rate of return is 13%, constant growth rate is 5%. Find the Value. Rs. 30.19

The dividends of HPT over the last five years have been as follows. Year Dividend (Rs.)

1998 150,000 1999 192,000 2000 206,000 2001 245,000 2002 262,550

The company entirely financed by 100,000equity shares. Expected rate of return on equity share is 24%.You are required to calculate, The growth rate over the last four years The value of equity share?

D0 = 150,000, D4 =262,550

D0 (1+g)4 = D4

150,000 (1+g)4 = 262,550

(1+g)4 = 262,550/150,000 ; (1+g)4 = (1.75033)1/4

g = (1.75033)1/4-1 = g = 1.1502 -1 =g = 0.15 = 15%

P0 = D5 = 2.6255(1+0.15) = 3.019325 = Rs.33.55

ke – g 0.24 - 0.15 0.09

The model is based as following assumptions

The required rate of return (K) must be greater than the growth rate

Ke g

The initial dividend must be greater than zero

Do O

The relationship between K and g is assumed to be constant and perpetual.

Super normal growth

Suppose that a company’s expected dividend is Rs. 2. It is expected to grow at 15% for next 3 years and then at a rate of 8% indefinitely. The required rate of return is 12%. What is the price of the share today?

Step 1Calculation of present value of the first three years dividends. Year Dividends Discount factor PV of the

At 12% dividends 1 2(1+.15)1 = 2.30 0.893 2.05 2 2(1+.15)2 = 2.65 0.797 2.11 3 2(1+.15)3 =3.04 0.712 2.16

-----------PV of the share during super growth period 6.32

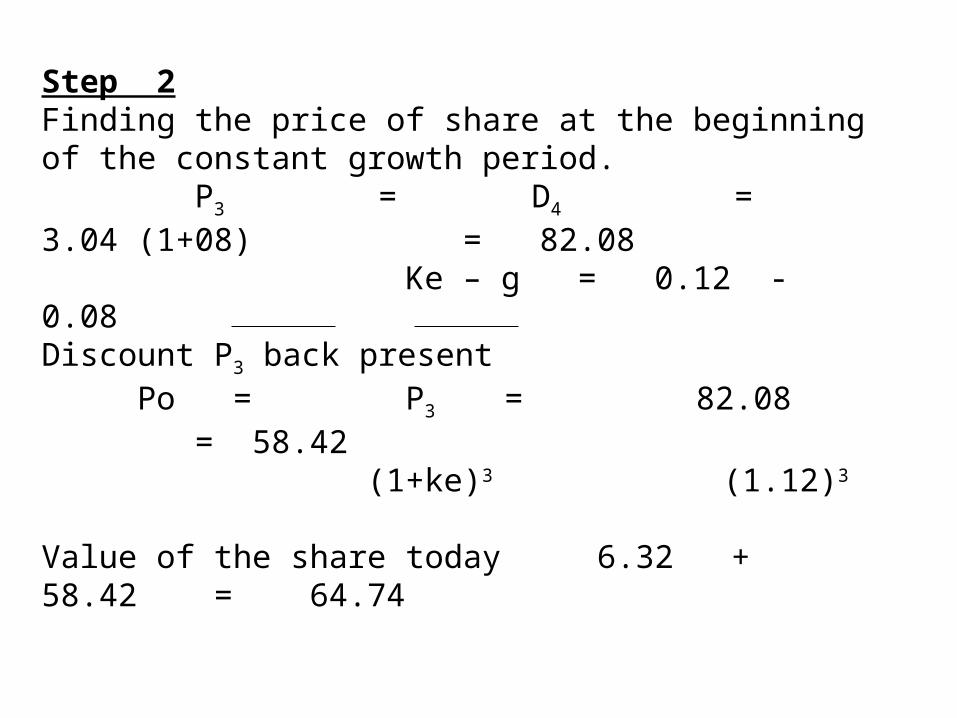

Step 2Finding the price of share at the beginning of the constant growth period. P3 = D4 = 3.04 (1+08) = 82.08 Ke – g = 0.12 - 0.08Discount P3 back present

Po = P3 = 82.08 = 58.42 (1+ke)3 (1.12)3

Value of the share today 6.32 + 58.42 = 64.74

Lanka pharmaceuticals is currently paying a dividend of Rs.2.00 per

share, which is not expected to change. Investors require a rate of

return of 20% to invest in a stock with the riskiness of Lanka

pharmaceuticals. Calculate the intrinsic value of the stock.

D0/k = 2.00/0.20 = Rs.10.00

Richter construction company is currently paying a dividend of Rs.2.00

per share, which is expected to grow at a constant rate of 7% per year.

Investors require a rate of return of 16% to invest in stocks with this

degree of riskiness. Calculate the implied price of Richter.

D1 = D0(1+g) = 2.14

P0 = D1/(ke-g) = Rs.23.78

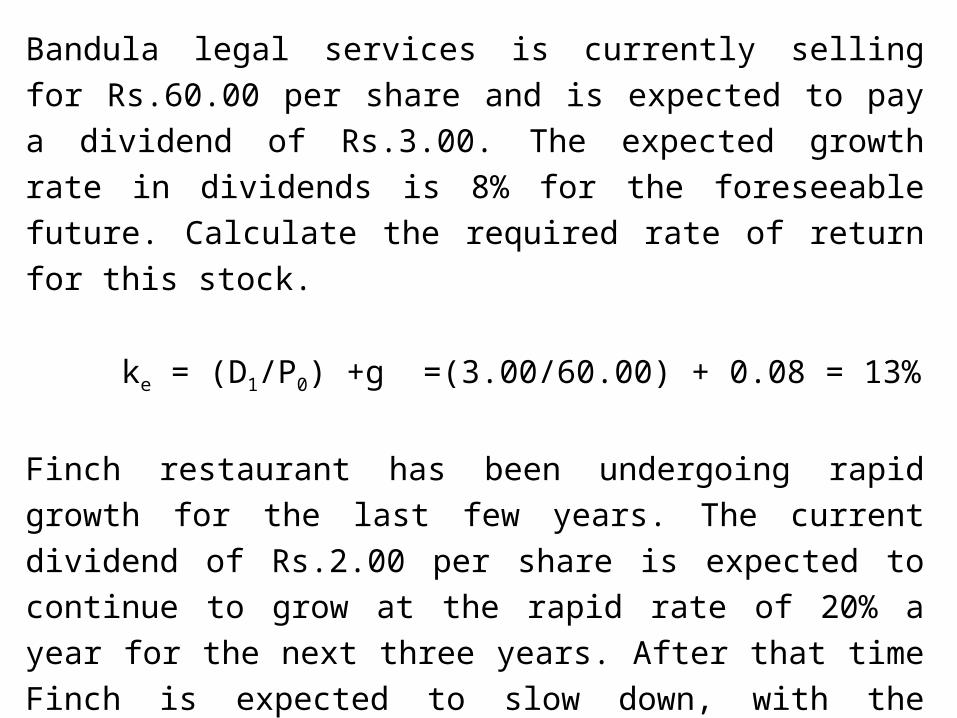

Bandula legal services is currently selling for Rs.60.00 per share and

is expected to pay a dividend of Rs.3.00. The expected growth rate in

dividends is 8% for the foreseeable future. Calculate the required rate

of return for this stock.

ke = (D1/P0) +g =(3.00/60.00) + 0.08 = 13%

Finch restaurant has been undergoing rapid growth for the last few

years. The current dividend of Rs.2.00 per share is expected to

continue to grow at the rapid rate of 20% a year for the next three

years. After that time Finch is expected to slow down, with the

dividend growing at a more normal rate of 7% a year for the

indefinite future. Because of the risk involved in such rapid growth,

the required rate of return on this stock is 22%. Calculate the implied

price for Finch.

D1 = 2.00(1+0.20) = 2.40 0.820 1.97D2 = 2.00(1+0.20)2 = 2.88 0.672 1.94D3 = 2.00(1+0.20)3 = 3.46 0.551 1.91

5.82

P3 = [3.46(1.07)] / 0.22 – 0.07)

PV at the end of year 3 = 24.68

PV at time period zero = 24.68(0.551) = 13.60

V0 = 5.82 + 13.60 = 19.42

The next dividend for the Golden growth company will be Rs. 4.00 per

share. Investors require a 16% return on companies such as Golden.

Golden’s dividend increases by 6% every year. Based on the dividend

growth model, what is the value of Golden’s stock today? What is the

value in four years?

P0 = D1/ (Ke – g)

= 4/ (.16 - .06)

= Rs.40.00

Dividend in four years

= D1 * (1+g)3 = Rs.4.764

Price in four years;

P4 = [D4(1+g)]/(Ke-g) = [4.764*1.06]/(.16-.06)

= Rs.50.50

P4 = P0*(1+g)4

P4 = 50.50 = 40.00*(1.06)4 = P0*(1+g)4

P4 =

D5/(Ke-g)

D5 =

D1*(1+g)4

P4 = D1*(1+g)4/(Ke-g)

= [D1/(Ke-g)]*(1+g)4

= P0*(1+g)4

The last dividend was Rs.2.00. The dividend is expected to grow steadily at 8%. The required return is 16%. Calculate the current price and price in five years.

P0 = D1/(Ke-g)

= 2(1.08)/(.16-.08) = Rs.27.00

D5 = D0(1+g)5

= 2(1.08)5 = 2.9387

P5 = D5(1+g)/(Ke-g)

= Rs.39.67

P5 = P0(1+g)5

= Rs.39.67

What is growth rate?

Earnings next year = Ear. this year + Ret. Ear. This year * R.on

Ret.Ear.

g = Retention ratio * Return on retained earnings

Julian enterprises just reported earnings of Rs.2 million. It plans to

retain 40% of its earnings The historical ROE has been 0.16, a figure

that is expected to continue into the future. How much will earnings

grow over the coming year?

Firm will retain = 2 million * 40% = 800000

The anticipated increase in earnings = 800000 * 0.16 = 128000

The percentage growth in earnings =Change in earnings / Total earnings = 128000/2Mi. = 0.064

So earnings in one year will be 2Million * 1.064 = 2128000

g = retention ratio * Return on retained earnings

0.4 * 0.16 = 0.064

Consider the above example, has 1000000 shares of outstanding. The stock is selling at Rs.10.00. What is the required return on share?

Pay-out ratio =1-0.40 = 0.60

Earnings a year from now = 2000000 *1.064 = 2128000

Dividend = 2128000 * 0.60 = 1276800

DPS =1276800/1000000 = 1.28

r = (Div / P0) + g

(1.28/10) + 0.064 = 0.192

Growth opportunities

The company pays all of its earnings to share holders as dividends

EPS = DPSA company of this type called a cash cow

Value of a share when firm acts as a cash cow

EPS/r = DPS/r

Growth opportunities means, the opportunities to invest in profitable projects.Suppose a company retains the entire dividend at date 1 in order to invest in a project. The NPV (per share) of the project as of date 0 (NPVGO)

What is the price of a share at date 0 if the firm decides to take on the

project at date 1?

The share price must now be

EPS/r +NPVGO

Saroja company expects to earn Rs.1 million per year in perpetuity if

it undertakes no new investment opportunities. There are 100000

shares outstanding. The firm will have an opportunity at date 1 to

spend Rs.1000000 in new marketing campaign. The new campaign

will increase earnings in every subsequent period by Rs.210000. This

is a 21% return per year on the project. The firms discount rate is 10%.

What is the value per share before and after deciding to accept the

marketing campaign?

Value of share when acts as a cash cowEPS/r = 10/0.1 = Rs.100

The value of marketing campaign as of date 1-1000000 + 210000/0.1 = 1100000

Value of marketing campaign at date 01100000/1.1 = 100000

The NPVGO per share is =1000000/100000 = Rs.10

Price per shareEPS/r + NPVGO = Rs.110

Straight NPV basis

Dividend in all subsequent periods are 1000000 + 210000 = 1210000

DPS =1210000/100000 = 12.10

Price per share at date 1 =12.10/0.1 = 121

Price per share at date 0 =121/1.1 = 110