thought line september 2010 - the banking & financial services e-newsletter from wipro...

TRANSCRIPT

SEPTEMBER 2010SEPTEMBER 2010

yldneirf oce

ethe Banking & Financial Services -newsletter from Wipro Technologies

Volume VIII Edition XXXIV

the Banking & Financial Services -newsletter from Wipro Technologies e

Feedback & Suggestions aremost welcome. Please email to

Editorial Team

Raghava PerrajuKiran DhanwadaApoorv Agrawal

Volume VIII Edition XXXIV

Index

yldneirf oce

2the Banking & Financial Services -newsletter from Wipro Technologiese

For Wipro internal circulation only

.......................................................................................................................3• Foreword

............................................................................................4• Know Your Domain Terms

• Demystification

• Innovation/ BTG Corner

Fun Corner•

• Bishnois: the first environmentalists........................................................................20

- Banking on the Environment.......................................................................................5

- Interview with Raghuraman Kalyanraman..................................................................9

- Green Data Centers....................................................................................................10

- Green Banking Products ...........................................................................................12

- IT: A pathway to Green Bank.....................................................................................14

- Banking for Environmental Sustainability – beyond Green IT ...................................16

- eBAM – A Go-Green initiative....................................................................................18

Foreword 3the Banking & Financial Services -newsletter from Wipro Technologiese

Greetings!!!

The earth's average temperature has increased 0.74 ± 0.18 °C due to continuous deforestation and fossil fuels usage in the 20th century. This has resulted in increase in ocean and air temperatures, melting snow and rising sea levels leading to floods, famines, hurricanes and other natural calamities. Thus it has become imperative for all, organizations and individuals, to reduce their carbon footprint and move towards greater environmental sustainability.

The significance of banks in reducing carbon footprint increases manifold as banks not only deal with organizational customers but also individuals in their day to day operations. The advent of information technology has assisted banks in achieving this objective by enabling paperless offices, e-statements and internet banking among a host of other green solutions. Banks and IT companies are looking for new initiatives, innovations and avenues to reduce carbon footprint. Wipro as an IT service provider has continuously dedicated itself to this cause of reducing carbon footprint and energy efficiency by undertaking various initiatives like sustainability measurement product, paper recycling units, extreme discretion in power and water consumption, and green consumer durables. No doubt the Greenpeace Guide to greener electronics has recently named Wipro as number one green electronics company in the world.

This month's theme on 'Green Banking in IT' discusses various topics on banks using information technology as a tool for energy efficiency along with multiple innovations that have hit the marketplace in this area. Sushankar Daspal's article on Banking on Environment discusses the Banking Environment Touch-point (BET) Model which establishes relationship between bank activities and its environmental touch-points. An interview with Raghuraman Kalyanraman throws light on challenges and trends faced by IT industry in space of green banking and Wipro's initiatives in this area. Kunal Chaudhary and Swati Sharma's article on Green Banking Products discusses various products contributing to cause of environment, while Nitin Sanan elaborates on the biggest initiative in Green across organizations - data centers. Neeraj Jain's article discusses a structured approach to address sustainability and alignment to organizational goals while Puja Didwaniya discusses about the eBAM initiative of SWIFT and its Green value. Last but not the least, we have Jayaprakash Kavala elucidates the concept of environmental sustainability beyond the ways and means of ensuring green operations within a bank.

We sincerely thank all the contributors and hope that you enjoy reading these articles.

Best Wishes from the Thoughtline Editorial Team Raghava PerrajuKiran DhanwadaApoorv Agrawal yldneirf oce

The views and opinions expressed in the articles/other contributions by individuals are strictly those of the authors and should not be viewed as professional advice with respect to your business.

Parts of the Images used in this Thought Line is from Reproductions of `Envionmental movement'

4the Banking & Financial Services -newsletter from Wipro Technologiese

Know Your Domain Terms

1. Carbon Footprint -

2. Kyoto Protocol –

3. Data Center -

4. Project finance -

The amount of greenhouse gases (GHG) emissions by a product, event or organization. Carbon footprint is expressed in terms of carbon dioxide, or its equivalent of other Green House Gases emitted. It is a measurement of all greenhouse gases that are individually produced and has units of tonnes (or kg) of carbon dioxide equivalent. The carbon footprint is made of sum of two parts – Primary footprint i.e. a measure of direct emissions of CO2 from the burning of fossil fuels; and Secondary footprint - a measure of the indirect CO2 emissions from the whole lifecycle of products used - those associated with their manufacture and eventual breakdown.

It is a set of rules meant for combating global warming. It was adopted on 11 December 1997 in Kyoto, Japan and entered into force on 16 February 2005. As of November 2009, 187 states have signed and ratified the protocol.

A data center is a place where computer systems and related components, such as telecommunications and storage systems are kept. It includes security devices, backup power supplies, redundant data communications connections and environmental controls (e.g. air conditioning, fire suppression).

Project finance is financing of large scale projects (infrastructure, industrial) based upon the projected cash flows of the project. This is a long term financing. Finance to such projects is provided by syndicate of banks and equity investors, known as sponsors.

5. Solar Powered ATMs –

6. Paperless office -

7. UNEP FI -

8. ISO 14000 -

An ATM which is run on solar power where solar power will charges the battery, and battery bank supports the ATM.

A paperless office is a work setting at which the use of paper is minimal and wisely used. The idealized office in which paper is absent because all information is stored and transferred electronically. The paperless office is a viewpoint of working with a negligible amount of paper; employ such processes and systems that eliminate the need for paper and to switch all documents in digital form.

The United Nations Environment Programme Finance Initiative (UNEP FI) is a global partnership between the United Nations Environment Programme (UNEP) and the global financial sector. UNEP FI works with 200 financial institutions who are also the signatories to the UNEP FI Statements, and a variety of partner organizations to develop association between sustainability and financial performance. UNEP FI undertakes missions to identify and promote the adoption of environmental and sustainability practices by providing peer-to-peer networks, research and training to financial institutions.

ISO 14000 is a series of international standards on environmental management. It provides a skeleton for the development of an environmental management system and the supporting audit program. The drive for its development came as a result of the Rio Summit on the Environment held in 1992. It outlines a

framework of control for an Environmental Management System on the basis of which an organization can be certified by third party.

5the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

Banking on the EnvironmentBET Model and customer behavioral influence

Sushankar Daspal Practice Head, BFSI

Introduction

Are these connected?

Why is this important?

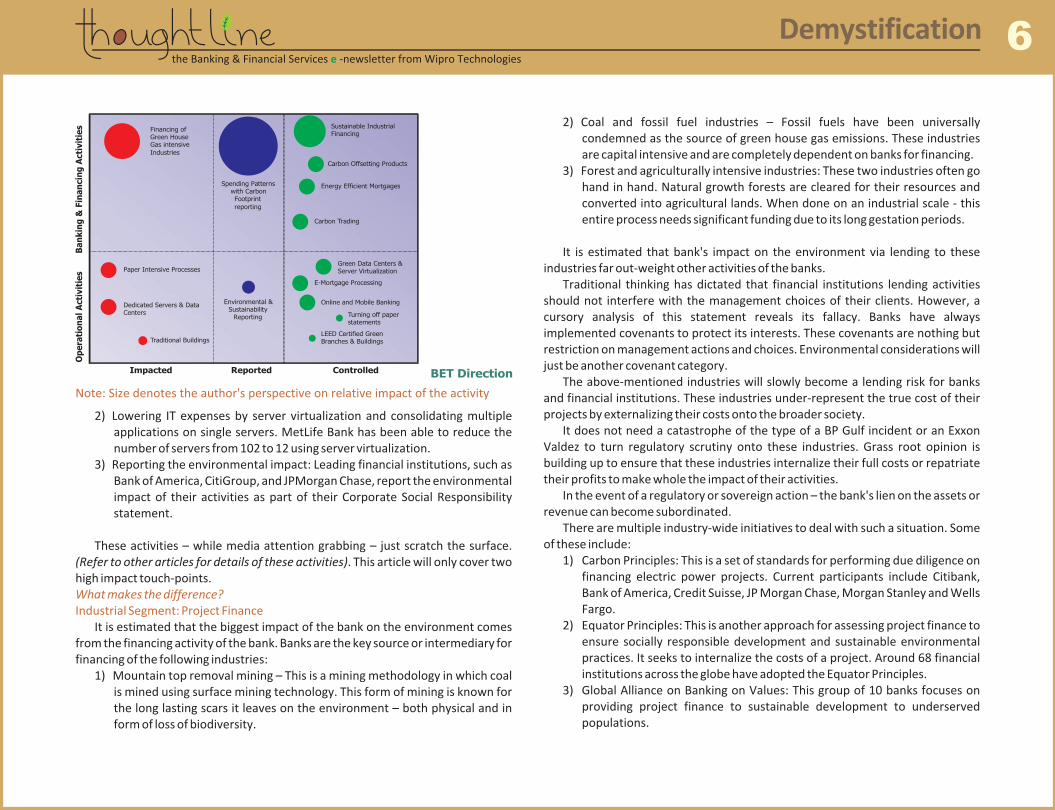

Banking Environmental Touch-point (BET) Model

Banking and the Environment?

Banking is all about finances. What has the environment got to do with it? Banking is all about maximizing shareholder value. Why should hard-nosed financial experts bother with the tree hugging radicals?

These were the first set of questions that crosses a typical banking professional when they hear “environment responsibility” and “Green Banking”. Do these concepts have a value beyond their marketing potential? This article will provide a perspective of the future where banks will literally bank on the environment.

Environmental concerns have slowly bubbled up into the public's conscience. There is a growing awareness that each generation is only a custodian of the environment for future generations.

Banks can no longer sit out on the sidelines in this debate. Many of the largest financial institutions are no longer private enterprises who focus only on profit maximization.

After the recent bailout of many financial institutions – tax-payers have become stakeholders in financial institutions – if not, shareholders. The day is not far off – where Jane and Joe Commoner will ask – “Are the banks doing the right thing to the environment?”

In order to understand the impact of banks and the environment – it is critical to have a conceptual model showing the interplay of bank activities and its environmental touch-points.

The Banking Environment Touch-point model provides this context in an easy-to-assimilate manner. This is subsequently referred as the BET Model.

Y Axis: The activities of banks can be classified into two broad headings:1) Operational activities: The bank's conduct of its day-to-day business2) Banking & Financing activities: The bank's core activities and usage of its

monies

X Axis: The result of bank's activity is classifiable under the categories of:1) Impacted: This is where the bank activity results in a negative

environmental impact2) Reported: The bank takes the first step towards impact resolution –

identification of the impact and reporting its results 3) Controlled: The bank has taken concrete action towards controlling its

impact on the environment

The diagram below has applied the BET model on currently known and conceptualized banking activities.This article shall provide an overview of some of the activities.

A lot has been said in the press about the activities of many banks in making their operations efficient and lowering its impact on the environment. Some of these include:

1) Assessing the impact of the banks utility costs and building practices and moving into more energy efficient data centers and LEED (Leadership in Energy and Environmental Design) certified buildings. Wells Fargo is acknowledged as a pioneer in this space among banks.

BET Model - Current state of the art

Impacted Reported Controlled

Op

era

tio

na

l A

ctiv

itie

s B

an

kin

g &

Fin

an

cin

g A

ctiv

itie

s

Banking Environmental Touch-point (BET) Model

6the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

2) Lowering IT expenses by server virtualization and consolidating multiple applications on single servers. MetLife Bank has been able to reduce the number of servers from 102 to 12 using server virtualization.

3) Reporting the environmental impact: Leading financial institutions, such as Bank of America, CitiGroup, and JPMorgan Chase, report the environmental impact of their activities as part of their Corporate Social Responsibility statement.

These activities – while media attention grabbing – just scratch the surface. (Refer to other articles for details of these activities). This article will only cover two high impact touch-points.

It is estimated that the biggest impact of the bank on the environment comes from the financing activity of the bank. Banks are the key source or intermediary for financing of the following industries:

1) Mountain top removal mining – This is a mining methodology in which coal is mined using surface mining technology. This form of mining is known for the long lasting scars it leaves on the environment – both physical and in form of loss of biodiversity.

What makes the difference?Industrial Segment: Project Finance

Note: Size denotes the author's perspective on relative impact of the activity

2) Coal and fossil fuel industries – Fossil fuels have been universally condemned as the source of green house gas emissions. These industries are capital intensive and are completely dependent on banks for financing.

3) Forest and agriculturally intensive industries: These two industries often go hand in hand. Natural growth forests are cleared for their resources and converted into agricultural lands. When done on an industrial scale - this entire process needs significant funding due to its long gestation periods.

It is estimated that bank's impact on the environment via lending to these industries far out-weight other activities of the banks.

Traditional thinking has dictated that financial institutions lending activities should not interfere with the management choices of their clients. However, a cursory analysis of this statement reveals its fallacy. Banks have always implemented covenants to protect its interests. These covenants are nothing but restriction on management actions and choices. Environmental considerations will just be another covenant category.

The above-mentioned industries will slowly become a lending risk for banks and financial institutions. These industries under-represent the true cost of their projects by externalizing their costs onto the broader society.

It does not need a catastrophe of the type of a BP Gulf incident or an Exxon Valdez to turn regulatory scrutiny onto these industries. Grass root opinion is building up to ensure that these industries internalize their full costs or repatriate their profits to make whole the impact of their activities.

In the event of a regulatory or sovereign action – the bank's lien on the assets or revenue can become subordinated.

There are multiple industry-wide initiatives to deal with such a situation. Some of these include:

1) Carbon Principles: This is a set of standards for performing due diligence on financing electric power projects. Current participants include Citibank, Bank of America, Credit Suisse, JP Morgan Chase, Morgan Stanley and Wells Fargo.

2) Equator Principles: This is another approach for assessing project finance to ensure socially responsible development and sustainable environmental practices. It seeks to internalize the costs of a project. Around 68 financial institutions across the globe have adopted the Equator Principles.

3) Global Alliance on Banking on Values: This group of 10 banks focuses on providing project finance to sustainable development to underserved populations.

Impacted Reported Controlled

Op

era

tio

na

l A

cti

vit

ies

Ba

nk

ing

& F

ina

ncin

g A

cti

vit

ies

Traditional Buildings

Paper Intensive Processes

Dedicated Servers & Data Centers

Financing of Green House Gas intensive Industries

Sustainable Industrial Financing

LEED Certified Green Branches & Buildings

Online and Mobile Banking

Turning off paper statements

Energy Efficient Mortgages Spending Patterns with Carbon Footprint

reporting

E-Mortgage Processing

Environmental & Sustainability

Reporting

Carbon Trading

BET Direction

Green Data Centers & Server Virtualization

Carbon Offsetting Products

7the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

4) NGO initiatives: Some NGOs focus on the performance of financial institutions from an environmental standpoint and publish their findings as a means of putting pressure on the institutions to change their behavior. For example, the Rainforest Action Network has published a report on the actions of Canadian banks in financing fossil fuel industries.

This is an emerging area of banking in which “green” products and services are targeted to retail customers. Some of these include:

1) Green checking and card accounts: These financial products eschew the usage of paper statements and processes and focus on online and mobile banking for all origination and servicing requirements. Customer behavior is influenced by having significant fees or charges for paper statements, branch visits or calls to the call center; and cash back for online behavior. These products are often marketed as “online only accounts” and the cards are created out of ecologically friendly non-PVC substances. Citizens Bank Green$ense is an example of this category.

2) Green rewards: In this, consumer rewards points are redeemable for green products like re-chargeable flashlights or solar / wind power certificates. These products offer consumers a tangible “green benefit” for their usage of financial products. Wells Fargo is one of the financial institutions providing such rewards.

3) Carbon offsets: Some financial institutions have made democratic the purchase of carbon offsets to retail consumers. These institutions offer basic calculators to enable consumers to estimate their carbon footprint and allow them to purchase carbon offsets. RBS allow personal and business customers to purchase Carbon Instruments.

4) Sustainable Banks / Ethical Banks: These banks accept deposits with a commitment to use the money only for sustainable development activities.

5) Energy Efficient Mortgages: Many financial institutions offer energy efficient mortgages. These mortgages allow the customer to qualify for a slightly higher mortgage amount if the property is energy efficient. The rationale is that the savings in utility expenses will enable the householder to take up additional mortgage payments. These loans are backed by FHA, Freddie Mac and Veteran Affairs. A related – but unproven and emerging concept – is Location Efficient Mortgage. In this, consumers purchasing properties near public transport points qualify for larger mortgages. The assumption is that usage of public transport will reduce transportation expenses and enable higher mortgage payment.

Consumer Segment: Green oriented products and services

Making a fundamental impact on customer behavior It is the author's view that all the above products and services are targeted for customers who are early adopters and green evangelists.

There is potential for banks to make a fundamental impact on the environment via consumer education. While 34% of consumers claim they want to reduce their impact on the environment by going paperless – only 26% of customers have gone only online.

In the non-banking world – while customer decry the impact on the environment – they continue to buy large cars, fuel guzzling SUVs and take multiple airline flights. All of these are known to have huge impact on the environment.

Like many industries - customers have not internalized the impact of their actions on the environment. The cause and effect relationship is not critically established in their minds.

What will happen if consumers are shown the environment impact of their purchases?

Once this is established – there will be dramatic changes in customer behavior. Organizational behavioral sciences has long established that tracking and reporting metrics results in behavioral influences on the individual.

As consumers use cards to make purchases – the bank could communicate to the customer their carbon footprint.

During purchase – the bank's mobile application can advise the customer – not just their financial position (“can I afford this purchase?”); but, “is this product carbon efficient?” and “do I have enough carbon allowances as per my target?”

When the customer accesses their credit or debit card statement on their bank site – the bank offers them another option on the personal finance management toolbox – “Know your carbon foot print”.

Based on the customer's purchase data – the bank estimates the carbon footprint of the customer and compares it to its peers.

Can this be done? Yes – with current technology and data – an approximation of the customer's carbon impact can be made. Online and mobile channels already support these types of interactions – and these features are logical extension of existing capabilities.

The bank has now become the trusted financial and environmental advisor to the customer. Are banks ready for this environmental advisor role? That – and not technology – is the current barrier.

8the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

Interview with Raghuraman Kalyanraman

Raghuraman is Managing partner for Green Services. He is with Wipro for more than 16 years and has worked on Innovation, Telecom, Value Added applications and Green Services. In this interview Raghuraman has highlighted about Wipro's initiatives and trends & challenges faced by IT industry.

Q. As an IT solution provider, Wipro might have provided solutions that have benefitted the client and society at large in the area of green initiative. Please provide some thoughts on this.

Q. How carbon footprint is being utilized by Wipro to keep its green initiatives upfront?

A. Wipro provides the Discover to Manage services and solutions in Green in the following broad areasi. Carbon tracking and reporting by assessing the regulatory risks due to

various Green laws coming into play ii. Sustainability performance management through capture, report, analyze

and manage of key set Sustainability KPIs iii. Leveraging IT to communicate green progress to share holders, suppliers,

partners and employees and build a green brand. iv. Assessing and setting up platforms and process to cut down energy, water,

fuel, paper use, packaging and logistics expenses through a portfolio of IT tools

v. Building low carbon products and services enabled by sustainable technology alternatives from product design to manufacture

vi. Creating KPIs to measure-validate-benchmark-optimize environmental data across all supply chain activities /processes and devise IT solutions for low Carbon supply chain

vii. Organizing a low carbon strategy for your data centre ranging from cloud, virtualization, low PUE strategy, new cooling techniques and implement /retrofit a green IT infrastructure

viii.Managed services for energy efficiency, O&M, and field optimization and lifecycle services for optimization, planning and managing energy, water and waste.

A. Carbon footprint is a very simple communication of the job ahead in sustainability. It reflects, all that a company does in implementing sustainability

across IT, facilities, energy infrastructure, supply chain, operations, products and services. Wipro has a 360 degree charter on sustainability that is structured around an internal brand called Ecoeye. Using Ecoeye, Wipro has built a credible foundation for its own low carbon future, and uses the learning and best practices to drive sustainability change of its customers. Wipro looks at this model as part of its Customer centricity.

A. “Best practices”, “Low carbon opportunities”, “Go Green” are part of the wish list that one associates with a sustainability strategy. In the last 3 years, many best practices on green have evolved, and pioneered by companies worldwide. Based on our experience in understanding and creating this best practices dictionary, we have arrived at sustainability suite comprising of both services and solutions that enterprises can adopt to formally embrace sustainability charter. The methodology is arrived at, based on the principle of triple –bottom-line, industry best practices and experiential business cases. We take customers towards their sustainability goals using a four step process. • Discover: Understand sustainability goals, capture and, analyze customer

environmental data, benchmark with industry and prioritize opportunities • Plan: Convert the sustainability opportunity into business requirements,

high level use cases and a program plan• Implement: Build & deploy Green applications & platforms across

sustainability domain areas • Manage: Manage energy efficiency, resource consumption, reporting, and

infrastructural support services on an ongoing basis

A. Green is about resource optimization. It is about doing more but using less resources. It is about looking a triple bottom line of people, planet and profits. If banks were taken as an example, some of the key green KPIs one could look at are

Q. We have heard of Wipro's own discovery services for Sustainability. Please throw some light on that and how organizations can utilize in implementation of that.

Q. What are the current “trends” when it comes to IT organizations and Banks in special in adopting green strategies or principles?

9the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

•• Paper used per employee or transaction• Data center energy productivity (DCeP)• Desktop energy use per employee• Risk in operations and portfolio assets due to climate change led physical

risk• Number of dematerialized or e or m-enabled transactions/customer• Carbon footprint per employee or transaction• Waste generated per employee

Using these KPIs, one could drive the sustainability agenda of a bank. The technologies, process and people changes can be driven as a result of driving these KPIs. Banks across the world have started to look at specific KPIs relevant to banking sector. Some of the KPIs discussed here are specific to banking industry.

A. The main challenges we see are in terms of identifying the top priority problem areas, assessing the As-Is state, and finding a solution that is a right fit, and arriving at a key set of best practices are some of the challenges in implementing sustainability. The other big challenge is people transformation. Considering that banks deal with people internally and the entire customer base is also people, transformation of this human capital to think sustainable and act sustainable is a bigger challenge of all. For example, transforming a customer to use a dematerialized transaction instead of a physical transaction is easier said than done. For banks to truly become sustainable, their customers have to become sustainable.

Energy used per employee or per transaction

Q. What are the biggest challenges that an IT organization see in implementing the Green Initiatives?

Delegates at Kyoto Protocol on Dec 4, 2007 at Bali

10the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

Green Data Centers Nitin Sanan, Senior Consultant, BFSI

As the role of IT within the banking sector widens its wings and tries to bring the whole gamut of banking under its fold, one must never forget that the heartbeat of IT infrastructure still remains the data centre. The move from paper to digital world has triggered the need for huge amount of data storage along with reliable and efficient information retrieval. The matter of fact being, there is no hidden thought that Data Centre are of prime importance during the planning and scheduling of any IT Roadmap of Financial Institutions globally.

Kyoto's Protocols of the United Nations Framework Convention on Climate Change is an international environmental agreement which targets greenhouse gas emissions. The protocol was adopted in 1997 and over the period of more than a decade some 187 states has signed the agreement to work towards the common goal of achieving "stabilization of greenhouse gas concentrations in the atmosphere at a level that would prevent dangerous anthropogenic interference with the climate system. "All of these states have been actively working towards this specified agenda and so have been the various FI's (Financial Institutions) across the world. Number of Green IT initiatives have been talked and written about in the media , but only a few rule over other , such as ''Carbon emission being released by the Data Centre''

It might being a shock to the readers but the truth remains the so called efficient Data Centre of today consumes roughly about 30 to 80 times more energy than a typical office building. This consumption translated into electricity cost is becoming a headache for the Bank IT teams, as they find it really difficult to justify the investments budgets.

As the world economy is back on roll after the global financial crisis, one can expect banks to make prudent investments in the various transformation projects. However, the known fact remains that the IT budgets will be squeezed, and there will be emphasize to Go Green, keeping in mind high availability and performance. Taking a futuristic approach, various solution vendors have come up with different set of offerings. Most of these offerings promise to make the data centers Eco friendly or Green by saving the energy and increasing efficiency thereby having minimum environmental impact. One of the major initiatives like 'The Green Grid' is solely dedicated to develop and promote energy efficiency for data centers, intend to facilitate both service providers and solution implementers.

Now taking a step forward from the Green Grid Initiative the business model transition some what looks like:

Situation today Green Data Center

• Tight IT budgets• Steep rise in global energy prices

• Efficient energy usage• Exploring alternative sources of energy

• Complex and spread physical layout• Aging data center technology• Uninhibited Exponential growth online data

• More computing performance per kilowatt• Highly flexible approach to use technology• Prohibited Exponential growth online data

• Need for corporate responsibilities• Short of public image• Employee commitment in the complete lifecycle is marginal

• Self driven , dedicated units in place• Improvised public image• Enhanced contribution by the employees towards the Green movement

Fin

anci

alO

per

atio

nal

Envi

ron

men

tal

There are various Techniques to support the GO GREEN Initiatives such as: -

Energy Utilization:Electricity has always been treated as an overhead expense which cannot be trimmed like the cost of space. But as the cost of power rises in recent times the issues regarding reliability and supply of electricity have become the concentration pointers.

Enlisted below are some of the initiatives followed by the industry circle to facilitate better utilization of electricity:

11the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

a) Exploration of renewal sources of energy b) Installation of new age UPS systems c) Ensconce motion activated lightning and selection of power economizer

mode to configure the power related software's d) Switching off the hardware when in idle or underutilized state usually for

testing and development servers. This can be achieved through integrated hardware scripts

A typical data center facility spends almost half of its energy consumption on the systems powering and cooling the infrastructure. Therefore, there arises a need to have powerful cooling mechanism in place to reduce this figure.

There are quite a few proven cooling techniques for the data center the primary one includes Computational Fluid Dynamics (CFD) and hot-aisle/cold-aisle management.

CFD enables the designer to optimize datacenter cool air flow by amending floor tiles based on the locations and also by regulating the percent of vents that are open at any given time. Maintenance of hot-aisle/cold-aisle configurations with suitable air conditioner locations in the floor layout of the data center will assist cool and warm air segregation thereby making cooling more effective. Another effective technique practices the principle of closely coupled cooling whereby the cooling air travels shorter distance to the hardware avoiding the mixing of warm air on the route.

It is a known fact that the software application can improvise the system performance many folds if it is designed and implemented in seamlessly. The right sizing of physical infrastructure also plays a critical role is system utilization both over sizing and under sizing is lethal. The nextGen technologies like Thin provisioning for disk storage system allows the desired space to be easily allocated to servers rides on just-enough and just-in-time principle avoiding issues related to over allocation. Another buzzing technology is the Cloud computing which if successfully implemented can eliminate over-provisioning of IT infrastructure and help draw the best out of the existing resources. It's upon the discretion of the application designers to have the best technology being implemented at the appropriate place to build a system which can drastically reduce the carbon emission.

Cooling techniques:

Apt Architecture:

Efficient Monitor and Control:

Conclusion:

In a case like this where we are finding ways to reduce the carbon emission being generated by the datacenters, the monitoring solution which will measure the end to end performance of these power houses becomes a pivotal force. An efficient monitoring system will allow the datacenter team of the bank to forecast future needs and at the same time find ways for the improvement in the current scope. OpenView from HP, Tivoli from IBM and Unicenter from Computer Associates are the leading solution providers in this space, trying rigorously to take it to the next level.

Green Data Centers will be the NextGen data Centers, where-in the organizations shall be obligated to implement green practices for financial benefits and environmental consideration. Many of us have a belief that such initiatives towards Green IT will be expensive and will require an additional effort but the hard truth is that, Going Green will actually save money and revolutionize the business for everybody's good.

Source:1. http://green.wikia.com2. http://www.thegreengrid.org/

12the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

Green Banking ProductsKunal Chaudhary and Swati Sharma, Consultants, Wipro Consulting Services

Green Banking or sustainable banking can be divided into 2 parts. The first is being environment friendly internally. This will include having things such as paperless transactions, using recycled paper, using lean to cut down wastage of power etc. The second part involves promoting green products. This impacts the banks business and also affects the people outside the bank. The idea is to motivate companies to go green. For this measure products such as green loans can be used.

Green Banking has advantages both for the environment and a Bank. Services such as online bill payment, online statements and direct debit facilities not only protect the environment but also reduce the amount of time, money and effort required to run banking processes. This directly translates into a healthier bottom-line. Adopting green banking practices portrays a bank as an environment friendly organization, which in turn attracts environmentally conscious customers.

In the following paragraphs, we discuss few ways by which banks could practice green banking:

Banks can economically incentivize its debtors to use the loaned money in environment friendly investments. This can be done by providing low interest rates, longer loan periods etc. Economically friendly investments could be anything from buying a solar power to constructing an economically friendly building. The demand for environmentally friendly investments, especially green buildings is on a steady rise. In India, the “green construction” segment of the infrastructure industry has been growing on an average of 45% per annum for the last 5 years1. The growth represents an opportunity for banks to attract this segment by providing them concession for investment in green buildings. This will also incentivize many builders to invest in buildings which are environmentally friendly.

A bank can encourage its customers to conduct their transaction in greener ways. For example, banks can remove the charges for online money transfer so that customers will be inclined to use the online services rather than traditional cheques. A bank can also accumulate the points that a customer has earned and use that for environmental cause. These points could be earned from rebates on

Green Credits

Green Rewards

using credit cards, use of online banking services etc. On the other hand a bank can also put economic penalties for customers who do not use environmentally friendly ways of conducting business. This would mean policies similar to charging customers for basic services such as query for bank balances in the bank's branches so that they are motivated to do that online. For example Coulee Bank rewards its customers 3.33% annual percentage yield on balances of $0 to $25,000 and 0.51% annual percentage yield for any balance over the $25,000 if the monthly online banking qualifications are met. In addition, customers can receive up to $20 in ATM fee refunds every month2.

They can be used to incentivize the cardholder to reduce their carbon footprint and involve them in renewable energy projects. One of the examples of this initiative is Bank of America's brighter planet visa card. A percentage of cardholder's spending goes to funding renewable energy initiatives. Also the users can calculate their carbon footprint, learn how to be more involved in green movement and the monitor the projects they are contributing towards. The cardholders are also given incentives to use electronic statements.

Credit Cards

Product Management

• Credit Cards

Sales

• Solar Powered ATM's

• Online Banking

Cash And Liquidity

Management

Savings and Investments

• Green Investment/ Green Funds

Securities, Funds and Derivatives

Financing

• Green Credits

TreasuryBank

Management

• Paperless Office

Green Banking Products Across the Value chain

13the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

Green Investment/Green Funds

Solar Powered ATM's

They are the funds which mainly invest in two kinds of companies. The first are the ones which are themselves environmentally sustainable and follow guidelines of emissions, wastes and other such issues. The second would be the companies which are working towards building environmental sustainability. These can be companies producing solar planes, green buildings or even the ones trying to find new sources of renewable energy. For example, SBI has installed 10 windmills in the states of Tamil Nadu, Maharashtra and Gujarat with which it plans to generate 15 MW for its own use.

Using solar powered ATM's will provide two distinct benefits for a bank. First, a solar powered ATM saves about 1980Kw of energy consumption per year and leads to a reduction of CO2 emission by 1942Kgs per annum. This also results in a saving of INR 60 per day as compared to an ATM deployed using power grid and a saving of INR 120 per day as compared to an ATM deployed using diesel generators3. Second, solar powered ATMs can be deployed in areas which have inadequate supply of electricity. In India, there are about .0033 ATMs per 100 people against .047 per 100 people standard set by OECD4. The low penetration is largely due to low number of ATMs in rural India. They would serve to be an efficient delivery channels for banks. Given the huge demand for it, using solar powered ATMs would make good business sense, both economically and environmentally.

A bank can redesign its entire organization to be pro-environment. The redesign can include a banks processes, systems and products/services. Given the increase in the number of corporations and individuals who are prefer an environmentally friendly organization, green banking makes good economical sense in the present market.

Source:1. http://www.ice.it/paesi/asia/india/upload/182/Green%20building%20buds%20in%20India.pdf2 http://www.couleebank.net/rewards_checking.php3 http://www.autonic.in/Solar-ATM-Solution.htm4 http://www.rbi.org.in/scripts/BS_SpeechesView.aspx?Id=519

14the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

IT: A pathway to Green BankNeeraj Jain, Senior Consultant, Productized Solutions Group

As part of our sustainability industry benchmarking initiative, Wipro has started to do a survey on sustainability performance of banking sector. As per our research, a Tier 1 multinational bank has around 6000 branches and offices, 4000 ATMs and has a 1:0.9 ratio of desktop infrastructure. So a Tier 1 bank will have an excess of hundred thousand desktops. Banks are paper intensive businesses. Approximate KPI analysis suggests a use of more than 50 KGs of paper per employee in a year. Banks are real estate intensive businesses with offices worldwide. The overall energy spends of a Tier 1 bank with an asset base of around $ 2 trillion is around 8 kWh per employee in a year.

Regulatory implication for banks from an environmental standpoint is minimal as of today, as only 2% of carbon emissions come from the service sector. From the global 500 commercial bank, 49 out of 60 have reported under Carbon Disclosure Project 2010. In terms of green products and services, there is a limited progress in the banking sector, since most banking products are paper based or dematerialized services. Out of 15 banks surveyed, 40% of banks have achieved carbon neutrality, 40% have set targets of at least 25% cut in the next 5 years, and the rest have reported their carbon. Out of 15 banks surveyed, 40% of multinational banks have become a part of Dow Jones sustainability index and NASDAQ 50 global sustainability index.

A report by investment bank Goldman Sachs found that companies that are considered leaders in environmental, social and governance (ESG) policies also lead the pack in stock performance - by an average of 25% (Goldman Sachs, 2007). Over a 5-year period Dow Jones Groups Sustainability Index (DJGSI) performed an average of 36.1% better than did the traditional Dow Jones Group Index (World Economic Forum, 2005). The DJSI 2008 report reaffirmed a “positive strategically significant correlation between corporate sustainability and financial performance”.

So, what is a sustainable bank? Is it a buzzword or is it the future? A sustainable bank can be measured using a set of simple KPIs – Energy used per

employee, paper usage per employee, area used per square feet per employee and green house gas emission per employee. Sustainable banks are important for four reasons:

1. Cost economics2. Sustainable future

3.Risk management4.Global growthA s t r u c t u r e d

approach is needed to c o m p r e h e n s i v e l y address sustainability strategy and to align to the business goals. A process map has to be created to monitor and manage the progress of the goals. The process involves developing c o m p e t e n c i e s i n following seven areas.

Banking industry is generally considered to be relatively environmental friendly industry (in terms of emissions and pollution). However, given their potential exposure to risk, they have been surprisingly slow to examine the environmental performance of their clients. A stated reason for this is still that such an examination would 'require interference' with a client's activities. This situation is now changing. There is growing awareness in the financial sector that environment brings risks (such as floods) and opportunities (such as environmental investment funds).There is an opportunity for bankers to lobby for more green labeled investment to receive subsidies. Few multinationals banks have already started chalking out the climate risk strategy.

Area 2: Reputation & brand – While banks may be internally working on the 'Green Campaigns' to improve their operational efficiency and decrease their overall cost, it is important for banks to build a credible foundation. The credible foundations start with building green credentials and expertise. There is a framework of transformation starting from assessment, reporting, certification, audits to be done for facilities, IT, products and supply chain. It is important for companies to map the best practices across business functions. For example, GRI framework for corporate, LEEDs , BREEAM for buildings, DC code of conduct for IT, ISO 14000 standards for product LCA and Green SCOR for supply chain are required to build a credible green brand.

Banking sector has one of the most complex and wide

Area 1: Compliance & Risk Management –

Area 3: Operations –

Focus areas of the Green Bank

Compliance

Reputation & Brand

Operations

Products

Supply Chain

PublicInfrastructure

ITInfrastructure

Reporting & Benchmarking

Risk ManagementSustainability Performance Management

Status reporting

Training & Learning Mgmt

Communication GRI certified reporting

Mobile enablement

Telepresence Branch building

management

Green Procurement

Logistics OptimizationVisibility & Dashboards

Dematerialization of banking products(Branchless banking, mobile payment)

Green Data center

Thin clientsPaperless Office –Hosted Document

Mgmt

Virtualization Services

Smart meter & Sensor management

Managed Print

services

Energy management solutions

E-waste management

15the Banking & Financial Services -newsletter from Wipro Technologiese

Demystification

processes with respect to regulators, government and customers. IT, paper and communication are the three most important resources for fulfilling these processes. Green operation for banks means that banks have to discover the low hanging fruits for carbon savings in terms of transforming IT, paper based processes and legacy communication channel. For example, forex operations are paper intensive, customer care is IT intensive and communication channels are paper intensive. By automating such processes banks can enhance carbon efficiency, improve business model efficiency. The e-enablement and paperless transactions can reduce the paper usage in banks by as much as 40%, and this will also reduce energy usage. Banks will have to discover ways to optimize their processes.

As more and more mobile penetration hits the market, banks can leverage this new medium to optimize the resource and energy utilization, by making use of this medium. Use of SMS instead of envelopes and printed material, mobile applications to replace branch based customer experience, and use of paperless transactions such as mobile money transfer, mobile payments, can not only enhance customer experience, but also reduce the overall lifecycle energy and carbon cost of the banking products. Banks can lead the way by assessing the lifecycle cost of banking products and services through use of innovative techniques such as applying Life Cycle Analysis (LCA) to service sector products. In addition product innovation can come from dematerialized services such as mobile money transfer, mobile payments, and mobile wallets which are both cutting edge technology as well as green.

In typical retail banking, banks bank hugely on supply chains for the customer- bank connect. Mailing, dispatch of documents, brochures, materials globally accounts for millions of tons of paper in banks. Banks can leverage the opportunity to be green by greening its supply chain through e-enablement, and also by using environmental data about assets from suppliers, and customers. The average paper usage in a bank per employee ranges from 50-80 kilograms per year. Banks need to identify a set of sustainability performance metrics such as waste generated per employee, paper usage per employee, CO2 emission per process to enable a green supply chain.

Banks can leverage the green building transformation happening worldwide by setting up a formal energy management and facility management strategy. The strategy spans assessment and audits, certifications, best practices in civil, electrical and cooling infrastructure. In addition to that banks have to invest in a comprehensive energy management strategy. This entails assessing As-Is energy source map, energy consumption map,

Area 4: Products -

Area 5: Supply Chain –

Area 6: Public and support Infrastructure -

energy asset map and treating energy as a corporate strategic resource and not as a utility resource. The next step is to setup an energy life cycle management system which can provide significant savings in energy through just in time cooling, heating, equipment efficiency improvement and better maintenance life cycle management. Technology innovations such as solar powered ATMs, sensor and smart metering networks, energy efficiency diagnostic tools can also enable banks to build a green infrastructure.

Banks can implement innovative solutions to decrease the energy use by implementing green data center. Almost 90% of the banking staff use computer desktops, and print infrastructure. Using software that can automatically switch off the desktops overnight can potentially save up-to 30% reduction in energy use by desktop IT. Desk PCs can be replaced with smaller devices, known as a 'thin clients', which typically use less than 10 per cent of the power of a standard PC. Using desktop virtualization banks can decrease their energy usage by more than 70%. Non critical application infrastructure consolidation is another area of energy reduction. Using tools to measure PUE, server utilization, and monitoring, banks can address the data center energy use and bring 8 – 10% savings in the least. Cloud infrastructure, and migration of applications to cloud can improve utilization percentages of IT infrastructure by at least 15 to 20%.

“Best practices”, “Low carbon opportunities”, “Go Green” are part of the wish list that one associates with a sustainability strategy. In the last three years, many best practices on green have evolved, and pioneered by companies worldwide. Based on Wipro's experience in understanding and creating this best practices dictionary, Wipro has arrived at sustainability suite comprising of both services and solutions that enterprises can adopt to formally embrace sustainability charter. The methodology is arrived at, based on the principle of triple –bottom-line, industry best practices and experiential business cases. Wipro take customers towards their sustainability goals using a four step process.

1. Discover: Understand sustainability goals, capture and, analyze customer environmental data, benchmark with industry and prioritize opportunities

2. Plan: Convert the sustainability opportunity into business requirements, high level use cases and a program plan

3. Implement: Build & deploy Green applications & platforms across sustainability domain areas

4. Manage: Manage energy efficiency, resource consumption, reporting, and infrastructural support services on an ongoing basis

Area 7: IT Infrastructure –

Conclusion

16the Banking & Financial Services -newsletter from Wipro Technologiese

Innovation/ BTG Corner

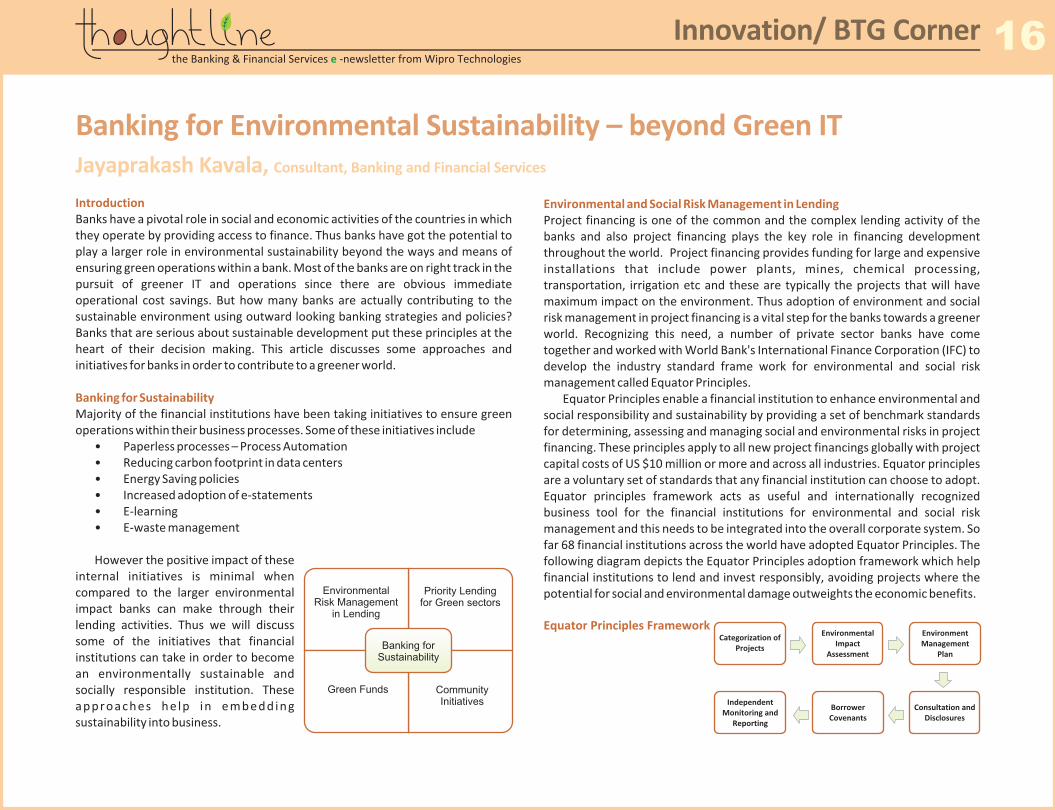

Banking for Environmental Sustainability – beyond Green ITJayaprakash Kavala, Consultant, Banking and Financial Services

Introduction

Banking for Sustainability

Banks have a pivotal role in social and economic activities of the countries in which they operate by providing access to finance. Thus banks have got the potential to play a larger role in environmental sustainability beyond the ways and means of ensuring green operations within a bank. Most of the banks are on right track in the pursuit of greener IT and operations since there are obvious immediate operational cost savings. But how many banks are actually contributing to the sustainable environment using outward looking banking strategies and policies? Banks that are serious about sustainable development put these principles at the heart of their decision making. This article discusses some approaches and initiatives for banks in order to contribute to a greener world.

Majority of the financial institutions have been taking initiatives to ensure green operations within their business processes. Some of these initiatives include

• Paperless processes – Process Automation• Reducing carbon footprint in data centers• Energy Saving policies• Increased adoption of e-statements• E-learning• E-waste management

However the positive impact of these internal initiatives is minimal when compared to the larger environmental impact banks can make through their lending activities. Thus we will discuss some of the initiatives that financial institutions can take in order to become an environmentally sustainable and socially responsible institution. These approaches he lp in embedding sustainability into business.

Environmental and Social Risk Management in Lending Project financing is one of the common and the complex lending activity of the banks and also project financing plays the key role in financing development throughout the world. Project financing provides funding for large and expensive installations that include power plants, mines, chemical processing, transportation, irrigation etc and these are typically the projects that will have maximum impact on the environment. Thus adoption of environment and social risk management in project financing is a vital step for the banks towards a greener world. Recognizing this need, a number of private sector banks have come together and worked with World Bank's International Finance Corporation (IFC) to develop the industry standard frame work for environmental and social risk management called Equator Principles.

Equator Principles enable a financial institution to enhance environmental and social responsibility and sustainability by providing a set of benchmark standards for determining, assessing and managing social and environmental risks in project financing. These principles apply to all new project financings globally with project capital costs of US $10 million or more and across all industries. Equator principles are a voluntary set of standards that any financial institution can choose to adopt. Equator principles framework acts as useful and internationally recognized business tool for the financial institutions for environmental and social risk management and this needs to be integrated into the overall corporate system. So far 68 financial institutions across the world have adopted Equator Principles. The following diagram depicts the Equator Principles adoption framework which help financial institutions to lend and invest responsibly, avoiding projects where the potential for social and environmental damage outweights the economic benefits.

Equator Principles Framework

Environmental Risk Management

in Lending

Priority Lending for Green sectors

Green Funds Community Initiatives

Banking for Sustainability

Categorization of Projects

Environmental Impact

Assessment

Environment Management

Plan

Independent Monitoring and

Reporting

Borrower Covenants

Consultation and Disclosures

17the Banking & Financial Services -newsletter from Wipro Technologiese

Innovation/ BTG Corner

All the projects to be funded by the financial institutions gets assessed for environmental imact based on the categorization of the projects. Examples of the impacts includes impacts on indigenous people, natural habitats, forestry, cultural property, involuntary settlement, child and forced labour, safety of dams, pest management, international waterways etc. The borrowers will have to come up with environmental management plan in order to mitigate the impacts. Borrowers also will have to comply with public disclosures norms regarding the impact and bind with the convenants they make for continous mitigations of environmental impacts. Finacial institutions also will have to ensure independent monitoring and reporting during the entire life cycle of the project for conitinuous environment risk management.

Similar to the project financing, other lending activities of the banks can be subjected to the environment and risk management policies. These lending activities include corporate and government loans, Official and export agency loans, acquisition finance, Debt securities placement, equity investment etc. Citibank is an example of this where they extended Environmental and Social Risk Management beyond project finance.

Prioritizing lending to environment friendly sectors as part of the principal lending activities of financial institutions will go a long way in achieving environmental sustainability. Examples of these sectors include the following:

• Renewable and alternate energy • Organic farming• Nature conservation• Environment friendly real estate projects• Recycling• Energy saving projects in micro, small and medium enterprise sector

Triodos Bank, headquartered in Netherlands and having offices in UK, Belgium and Spain, is an example of financial institutions which does majority of its lending to such environmental and socially conscious sectors. This bank invests customers' savings directly in sustainable companies and chooses not in invest in structured products, such as mortgage or other asset backed securities. This unique approach has actually kept them out the recent global credit crisis.

Green funds, also called as ethical funds, are the mutual funds or other investment

Priority lending to environment friendly sectors

Green Funds

vehicles which invest only in companies which are considered to be directly promoting environmental responsibility and are socially conscious in their business. Many financial institutions have started green funds with the intent of promoting environmental sustainability and also to tap the market segment of investors who opt to invest in environmental and socially conscious companies particularly in the sectors like alternative energy, green transport, waste management etc. Though this approach of investing may not match or beat the market returns, many investors appreciate these investments from a social consciousness perspective.

Financial institutions have got better reach and connect with the local communities in which they operate. Thus banks have the potential to play a great role in community initiatives such as clean and green drives, energy efficiency practices etc. They can also sensitize local corporate bodies, institutions and government bodies in planning on issues like biodiversity, wildlife habitats and environmental practices as part of the crusade against environmental degradation. Funding of the local self-help groups (SHG) and NGOs is also a social responsibility of the financial institutions.

To conclude, banks can take these initiatives beyond the green IT/operations towards environmental sustainability and some banks are pioneering these efforts recently. Banks need to embed environmental sustainability as part of their core business policies especially in lending and enable the larger society to contribute towards the same.

Community Initiatives

References1. About the Equator Principles, www.equator-principles.com2. Sustainable Green Banking : The Story of Triodos Bank, R.N. Dash, CAB calling October-December

2008 edition3. CitiBank Sustainability Information, www.citigroup.com

18the Banking & Financial Services -newsletter from Wipro Technologiese

Innovation/ BTG Corner

eBAM – A Go-Green initiativePuja Didwaniya, Business Analyst, BFSI

Setting the Context:

How does eBAM work?

Today, Competition demands an environment-friendly performance by most industries and banking industry is no exception. It has become imperative to engineer products and processes which are directly or indirectly benefitting the environment. One of the major environmental issues which banks are associated with is high level of paper consumption by banks and, in process by their customers. To counter this, over the years many initiatives have been taken by banks to automate their paper intensive processes e.g. introduction of online banking; and hence reducing their carbon footprint. But still there are improvement opportunities towards which continuous efforts are being taken. eBAM is one such green initiative.

eBAM stands for Electronic Bank account management and is an initiative pioneered by Society of Worldwide Interbank Financial Telecommunications (SWIFT). It aims to simplify and improve corporate bank account management processes including account opening, maintaining and closing. The inefficiencies in the current process which led to the need for a transformation are:

• Current methods are archaic and rely heavily on paper based processes that are time consuming

• Lack of common standards across geographies and regulatory jurisdictions• Cumbersome reporting and potential slack in regulatory compliance• Non Integrated Process flows• Impedes progress towards a fully integrated system capable of straight

through processing Following survey illustrates the massive slack in the current processes:

Time Taken by banks to open a new

account

40%

32%

26%

2% 0-2 Hours

2 Hrs - 2 Days

2 Days - 1Week

> 1 Week

Potential Cost Reduction Through

Automation

31%

31%

31%

7%> 40%

30-40%

20-30%

<20%

Source: Pega/Finextra 2009 Survey

eBAM proposes electronic flow of information between corporates and banks as against the current manual, paper driven processes. The current process requires corporates to send physical copy of the request letter and supporting documents to the bank for request processing. To automate this, standard electronic messages (ISO 20022 XML messages) which will substitute a physical request/information letter have been developed. Also, digital copy of ancillary documents can be attached to the message itself. To authenticate the documents Digital Signature will be used. Furthermore, eBAM provides acknowledgement, query and report messages which will be used by banks for their communication.

Currently, the turnaround time for the corporate bank account management process is sometimes so high that it takes months for fulfillment of a request. Introduction of eBAM is expected to bring down the turnaround time to days, making it an inevitable change for the industry. Other benefits of eBAM include: Standardization of process and improved service quality and customer satisfaction. Additionally, elimination of paper usage makes it an eco-friendly approach towards problem resolution.

The paperless process provides for additional benefits to both corporate and banks: It leads to reduced cost of operation through reduction in:

• Paper consumption• Storage space requirement• Mailing/Courier charges• Fax/printing cost• Man-power requirement

Also, Storage of information in digital form instead of files and folders assists integration into back-office applications and databases. This provides for centralized reporting, and auditing for all bank accounts; and better traceability.

Adopting eBAM provides banks a competitive edge, better customer satisfaction and retention. Last but not the least; The “Go-Green” approach helps both corporate and banks to strengthen their brand equity. The numerous benefits attached to the eBAM initiative make it justified effort for both corporate and banks. However, eBAM has a few more barriers to cross and the most significant barrier is the legal acceptance of electronic exchange of sensitive information. It remains to see if eBAM has the resilience to overcome these barriers and truly “Green” the corporate account management processes.

Conclusion

Fun CornerFun Cornerthe Banking & Financial Services -newsletter from Wipro Technologiese

For Wipro internal circulation only

19

Raghava Perraju and Apoorv Agrawal

Rush your answers to [email protected]

The winner of August 2010 Fun Corner is Dr. Anand Chopra

1. The _______________ are a voluntary set of standards for determining, assessing and managing social and environmental risk in project financing.

a. ISO 14000b. Equator Principlesc. Collevecchio Declarationd. IFC Sustainability – Environmental and Social Standards

2. The winner of 2010 FT Sustainable Banking Award for Sustainable Bank of the year is a. H.S.B.C, UKb. Financial Information Network and Operations (FINO), Indiac. Industrial Development Bank of Turkey (TSKB)d. Co-Operative Financial Services, U.K.

3. Each recycled laser cartridge conserves the equivalent of____ quart(s) of oil.a. 5b. 2c. 3d. 6

4. Which bank in India has recently started deploying the Solar powered ATM's on a large scale.

a. Citibankb. Central Bank of Indiac. State Bank of Indiad. ICICI Bank

5. Every Ton of recycled office paper saves____ gallons of oila. 250b. 420c. 380d. 170

6. Employing automatic power management features on your computer and shutting down computers and monitors after work hours can cut energy use by

a. 20%b. 40%c. 60%d. 80%

7. Every ton of paper that is recycled saves___ treesa. 20b. 15c. 13d. 17

8. The ISO _________ standards provide governments, businesses, regions and other organizations with an integrated set of tools for programs aimed at measuring, quantifying and reducing greenhouse gas emissions

a. 14064b. 14050c. 14001d. 14031

Here are the answers for Aug'2010 Thoughline edition fun corner -

100voices Barclays Bank

Open FORUM American Express

small business online community Bank of America

pickuradvisor ING

Little Black Book First Direct

Slingshot Capital One

Join2Grow Fortis

Money Manager Blog ANZ

Moving ForwardStandard Bank

The Next Great Innovator BlogRoyal Bank of Canada

My Vault Scotia Bank

Your Point of View HSBC

Flametree ABN Amro

Feedback &Suggestions aremost welcome.Please email to

[email protected] by: [email protected]

Bishnois: the first environmentalistsBy Channakeshava

Bishnois are known to be the first environmentalist in the world as they have known to be following environment & wildlife protection & conservation since 1485 when environmentalist saint Guru Jambheshwar made it religiously compulsory to 'Not cut green trees' and 'To be compassionate to all living beings.' Bishnois follow these two and another 27 rules(total 29 rules) despite facing hardship in Thar desert.

Amrita Devi protested against the Maharaja's men who were attempting to cut green trees as it was prohibited according to Bishnoi principles. The malevolent feudal party told her that if she wanted the trees to be spared, she would have to give them money as a bribe. She refused to acknowledge this demand and told them that she would consider it an act of insult to her religious faith and would rather give her life to save the green trees. At that point she spoke these words:

Sar santey rookh rahe to bhi sasto jaan(If a tree is saved even at the cost of one's head, it's worth it)

Having said these words she offered her head. The axes, which were brought to cut the trees, severed her head. The three young girls Asu, Ratni and Bhagu were not daunted, and offered their heads too.

Source: Wikipedia