three cas recognized for early achievement

TRANSCRIPT

R.I.P. shareholder capitalism?“Connected” corporation rulesPersonal problems lead to ethical dilemmas for one CA

In this issueMeet this year’s honourees for early achievement, along with our honourees for community service and volunteerism in the profession

On the Cover

June/Summer 2010

Three CAs Recognized for Early Achievement

June/Summer 2010 ica.bc.ca 3

contents

8

On the Cover

Early Achievement Award Winners Meet the three CAs who

were chosen

4 Notes from the President Wrapping up a productive

year

5 For the Profession Tools to help transition to new

standards

18 Tax Traps & Tips Why it pays to stay

“connected”

20 PD News Summer PD highlights

22 Plugged In News for and about members

& students Movers&shakersinthe

profession Congratstoour50and

60-yearmembers! Detailsontheupcoming

AGM

28 Ethical Dilemmas When personal and

professional lives collide

14Giving Back to the Community Five CAs are recognized for

outstanding volunteerism

17Making a Difference in the Profession Gord Cummings, CA, takes

home this year’s Ritchie W.

McCloy award

Want to get the word out?

Advertise in Beyond Numbers!

Here’s why:

90% of BC CAs surveyed read

BeyondNumbers

BeyondNumbersgoes out to

more than 9,000 members,

more than 1,800 students,

and over 200 external

stakeholders—including

other institutes, associations,

and professional organizations

BeyondNumbers has won

awards for both content

and design, including

Blue Wave Awards of Merit

from the International

Association of Business

Communications – BC Branch

To place an ad in

BeyondNumbers, contact our

representatives at:

Advertising in PrintTel: 604-681-1811

710 – 938 Howe St.Vancouver, BC V6Z 1N9

Fax: 604-681-0456

Email: [email protected]

10%

Cert no. SCS-COC-000648

4 ica.bc.ca June/Summer 2010

June/Summer 2010, No.488

Published eight times annually by the Institute of Chartered Accountants

of British Columbia.

EditorMichelle McRae

Design Blindfolio Design

604-761-9212

AdvertisingAdvertising In PrintPhone: 604-681-1811Fax: 604-681-0456

Senior Director of External AffairsLesley MacGregor

Institute CouncilKaren Keilty, FCA

President

Peter Norwood, FCA1st Vice-President

Lenard Boggio, FCA2nd Vice-President

Michael Macdonell, CATreasurer

Jack Arnold, CALinda Lee Brougham, CA

Kyman Chan, CAKaren Christiansen, CA

John Crawford, CAGordon Holloway, FCA

David HughesAnthony Mayer, CA

Al McNairSheila Nelson, CAJohn Sims, FCA

James Topham, CAKenneth Tung

Praveen Vohora, CA

Chief Executive OfficerRichard Rees, FCA

BeyondNumbers is printed in British Columbia and

mailed eight times annually to more than 9,000

chartered accountants and more than 1,800 CA students

in public practice, industry, education, and government

service throughout BC, Canada, and other countries.

BeyondNumbers’ editorial and business offices

are located at:

Suite 500, One Bentall Centre, 505 Burrard St., Box 22

Vancouver, BC V7X 1M4

Phone: 604-681-3264

Toll-free in BC: 1-800-663-2677

Fax: 604-681-1523

Internet: www.ica.bc.ca

Opinions expressed are not necessarily

endorsed by the Institute.

BeyondNumbers supports the CA profession in BC

by sharing news from the Institute and news about

members, by sharing viewpoints on issues of specific

interest to members, and by promoting member

involvement in Institute activities.

Publications Mail Agreement No: 40062742

Notes from the President

Closingwords

With my term as president drawing to a close this month, I want to take this opportunity to say a few words.I would like to start by thanking the volunteers of the BC Institute for helping

to make this past year such a rewarding and successful one. Thank you all for your hard work and support.I cannot stress enough the level of commitment I have seen from volunteers

this past year, and, in fact, throughout the length of my service on the BC Council. Volunteers contribute greatly to the running of the BC Institute, and are vital to the success of professional initiatives at the provincial and national levels. To those of you who have not yet volunteered with the Institute, I encourage you to get involved and experience this collaborative process firsthand. I would also like to take this opportunity to congratulate the members

featured in this month’s magazine. Our Early Achievement Award winners signal the strength of the profession going forward; our Community Service Award winners show just how committed CAs are when it comes to giving back; and our Ritchie W. McCloy Award winner demonstrates the kind of impact one member can have on the profession. Finally, I would like to wish Peter Norwood, FCA, well in his upcoming term as

ICABC president. Peter has been volunteering with the BC Institute for many years, and I have no doubt that he will make a fine president. Peter: I hope you find your presidential term as fulfilling and enjoyable as I have found mine to be.

–Karen Keilty, FCA

June/Summer 2010 ica.bc.ca 5

For the Profession

If you haven’t yet considered how you’re going to transition to the various new standards, there’s no better time than the

present to start planning. With that in mind, here’s an overview of some of the resources available to to help you in this process.

Learning more about new Canadian Auditing Standards “Opportunities to Improve Audit Quality in Transition to Canadian Auditing Standards”This webinar by the Canadian Public Account-ability Board (CPAB) and the Auditing and Assurance Standards Board (AASB) highlights examples of key changes in standards and the impact on auditors. The webcast covers group audits, auditing accounting estimates, and communications with audit committees.

CPAB CEO Brian Hunt, FCA, urges auditors to use the adoption of Canadian auditing standards (CAS) as an opportunity to reconsider their overall audit approach, allowing them to both improve audit quality and reduce audit risk. AASB Chair Bruce Winter, FCA, under-scores that while new standards are easier to understand and use, and have much in common with existing Canadian standards, there are some significant differences of which auditors need to become aware.

The webinar can be accessed at www.meetview.com/cas20100506/.

“The new Canadian Audit Standards: After Busy Season – What Firms Should Do Now” This CICA webinar discusses the key steps to success—both within your firm and for your clients. Key topics covered include: where to focus your efforts; how to leverage recent audit engagements; and which topics to discuss with clients regarding next year’s audit. The webinar can be accessed at www.snwebcastcenter.com/event/?event_id=833.

New resources to support your transition to IFRS“IFRS Ready… Or Not?”This CICA webinar focuses on transition issues faced by small and medium-sized companies. It can be accessed at www.snwebcastcenter.com/event/?event_id=785.

“IFRS Immersion 1” and “IFRS Immersion 2” These four-day courses include in-class technical lectures and small facilitated workshops. Both courses are aimed at senior accounting professionals. Immersion 1 is not being offered in BC this year (it was offered in Vancouver in 2009), but is being offered elsewhere in Canada. Immersion 2 will be offered in Vancouver on September 28 - October 1, 2010. For details and registration, go to: www.cica.ca/career-development/continuing-education/financial-reporting-and-governance/index.aspx.

Canadian MD&A disclosures on IFRSThis section of the IFRS Transition Resources webpage provides examples and commentary based primarily on a high-level review of over 400 annual MD&A filings by entities with a December 31, 2009 year-end. As an aid to preparers and users, recent examples of IFRS-related disclosures in the MD&A of Canadian issuers are organized by industry categories. Go to: www.cica.ca/ifrs/ifrs-transi-tion-resources/index.aspx#disclosures.

Financial reporting for not-for-profitsThe Accounting Standards Board (AcSB) and the Public Sector Accounting Standards Board (PSAB) have proposed changes to accounting standards for not-for-profit organizations.

As mentioned in the May issue of Beyond Numbers, exposure drafts issued by the AcSB and PSAB are open for comment until July 15, 2010. Go to www.acsbcanada.org/strategic-planning/not-for-profit-orgnizations/index.aspx and www.psab-ccsp.ca/documents-for-comment/item35463.pdf for more information.

PSAB’s webinar, “The future of financial reporting by government not-for-profit organizations,” provides an overview of the impact the proposals contained in its exposure draft. Transitional considerations and long-term objectives are also addressed. The webinar can be accessed at www.snwebcastcenter.com/event/?event_id=866.

Financial reporting for pension plansNew accounting standards for pension plans have been issued. These new standards will apply to pension plans and to benefit plans that have characteristics similar to pension plans, and will come into effect on January 1, 2011. The new set of standards is based on section 4100, “Pension Plans,” with some modifications. They comprise Part IV of the CICA Handbook – Accounting. More information at: www.knotia.ca/Login/Login.aspx?languageID=1.

Development of Canadian GAAP The unprecedented scope of changes in Canadian accounting standards is part of the ongoing development of Canadian GAAP. In a recent webinar entitled, “AcSB Update: Stay informed about developments in Canadian GAAP,” senior leadership of the Accounting Standards Board (AcSB) highlight current activities in each financial reporting framework in Canadian GAAP: IFRS, and accounting standards for private enterprises, not-for-profit organizations, and pension plans. The webinar features AcSB Chair Tricia O’Malley, FCA, AcSB Vice-Chair Gordon Fowler, FCA, and AcSB Director Peter Martin, CA. It can be accessed at www.snwebcastcenter.com/event/?event_id=825.

Transitioning to New StandardsBy Amy Lam, CASenior Director of Member Services

continuedonpage25

6 ica.bc.ca June/Summer 2010

Events over the last few years have led to much criticism of bankers, executives, business practices, and even capitalism

in general. One of the more popular attacks has been directed at the concept of shareholder capitalism—a concept that places the onus on corporations and their managers to maximize shareholder value. In fact, some news media have reported that even Jack Welch, the former CEO of General Electric (GE), whom many see as emblematic of shareholder capitalism, has apparently recanted on the idea—seeming to signal the end of an era.2

Confirming this trend, the Harvard Business Review has published a number of articles along these lines, including “The Myth of Shareholder Capitalism”3 and “The Age of Customer Capitalism.”4 The latter article, written by Roger Martin, dean of the Rotman School of Manage-ment at the University of Toronto, contains some provocative ideas that merit careful examination.

In his article, Professor Martin connects the rise of shareholder capitalism to the seminal 1976 article, “Theory of the firm: Managerial behavior, agency costs and ownership structure,” by Michael C. Jensen and William H. Meckling.5 Martin asserts that pursuing the goal of “maximiz-ing shareholders’ wealth... is a tragically flawed premise, and it is time we abandoned it and made a shift to... customer-driven capitalism.”6

To support this claim, Martin goes on to compare the performance of GE and Coca-Cola (as companies that focus on shareholder capitalism) with the performance of Johnson & Johnson (J&J) and Procter & Gamble (P&G) (as companies that maximize customer

satisfaction). Finding that the latter companies did as well or better than the former in terms of stock price performance, he concludes that more companies should focus on satisfying customers rather than shareholders.

It’s an appealing notion—after all, it’s what marketers have been trying to tell us for as long as marketing has existed. However, scratch below the surface and a number of cracks appear. To begin with, four case studies do not constitute systematic evidence, and selectively using hindsight to identify successful companies for comparative purposes is hardly objective. More importantly, however, there are fundamental flaws in the central argument.

First, customers are only one constituent—albeit an important one—among many constituents of an enterprise. So given finite resources, if a business maximizes customer satisfaction, what are the implications for employees, suppliers, the community, and, of course, shareholders? Martin argues that “companies should seek to maximize customer satisfaction while ensuring that shareholders earn an acceptable risk-adjusted return on their equity.”7 Practically speaking, this recommendation suggests that, if a company has met its hurdle rate, it should spend the excess resources on customers. But what is the effect of this additional spending, if not to increase future profits... and thereby create shareholder value? This then begs the question: Are there better ways to spend the excess resources?

Second, it only makes sense for professional managers to work in the interest of shareholders, rather than customers—no one in their right mind would advise owner-managers to make decisions that are not in their own interest. The corporate form is simply an extension of the owner-managed business, and professional managers should always have the owners’ interests in mind.

Third, of course, making and keeping customers happy often helps to maximize shareholder value, but this is the key: Customer satisfaction is not a goal but rather a means to the end goal of maximizing shareholder value. In his article, Martin inadvertently undermines his own argument for customer capitalism by measuring the success of J&J and P&G not by customer satisfaction, but by shareholder value. Ultimately, even according to Martin, shareholder value matters more.

Fourth, the relationship between customer satisfaction and business success is surely dependent on the type of the business. There is no doubt that a consumer product company such as J&J and P&G need to emphasize customer satisfaction, but how important is customer satisfaction for a producer of an undifferentiated product such as crude oil? Martin’s article does not address this consideration.

If there is any failure in shareholder capitalism, it is that there has been too little of it, rather than too much. Shareholders do not benefit when executives receive large pay packages despite poor performance. Shareholders do not benefit when managers misstate financial statements to inflate profits. Shareholders do not benefit when investment bankers receive large bonuses for inventing, buying, and selling financial instruments they do not fully understand because they don’t care about the consequences. These are all problems associated with inadequate corporate governance to oversee the actions of management and employees. And these are precisely the types of agency problems envisioned by Jensen and Meckling back in 1976.

Business failures and controversy are facts of life. We should not make knee-jerk reactions to the events of the day, nor hop on any popular bandwagon that passes by. Shareholder capitalism is still alive, though perhaps it’s not doing as well as it should be. The way forward is not to discard it, but to make sure it works better than before.

Kin Lo, CA, Ph.D., holds the CA Professorship in Accounting in the Sauder School of Business at UBC. The CA Professorship is funded by the CA Education Foundation of BC. Send your questions on accounting research to Kin at [email protected].

Research Corner

1 Quote from Mark Twain.2 See Financial Times, March 12, 2009. In a follow-up in Business Week (March 16, 2009), Welch

clarified that he did not mean that shareholder value is not important.3 Heracleous, Loizos and Luh Luh Lan. “The Myth of Shareholder Capitalism,” Harvard Business

Review, April 2010. 4 Martin, Roger, “The Age of Customer Capitalism,” Harvard Business Review, January-February 2010.5 Jensen, M. C. and W. H. Meckling, “Theory of the firm: Managerial behavior, agency costs and

ownership structure,” Journal of Financial Economics, University of Rochester: Rochester, New York,

October 1976. Volume 3, Issue 4, pgs 305-360. 6 Martin, p. 59.7 Martin, p. 62.

Shareholder Capitalism: “The Report of My Death Was an Exaggeration” 1

By Dr. Kin Lo, CA, Ph.D.

ZLC Financial Group offers a wide-range of customized and innovative solutions to help grow, protect, and perserve your wealth.

For more information, contact our associates on: Vancouver 1200 Park Place, 666 Burrard St | Vancouver BC | V6C 2X8

Tel 604 688 7208 | Fax 604 688 7268 | Toll Free 1.800.663.1499

Victoria 3711 Grange Road | Victoria BC | V8Z 4S9Tel: 250.727.3445 | Fax: 250.479.9716 | Toll Free 1.800.906.5666

www.zlc.net

Your team of experts in Insurance & Retirement | Employee Benefits

Private Investment Management | Structured Settlements

Peter G. Lambb.a., clu, tep,

epc, csa

Garry Zlotnikf.c.a., b.comm., cfp, clu, ch.f.c

Martin Zlotnikb.comm., ll.b

Mark A. Zlotnikc.a., clu

P.M (Pip) Steeleb.comm., cfp, clu,

ch.f.c.

Robert E. Olsonb.a.

H.G. (Howie) Young

cfp

Bruce K. Bergerb.a., cfp

W.A. (Bill) Finlayb.a., c.a.

Lynn NewsomeKen McNaughtoncfp, clu, ch.f.c.,

rhu, csa

Ross Gibsondipt.t

John V.R. Warkb.comm., c.a, cfp,

clu, ch.f.c

Amin E. Jamala.c.i.i., clu, tep

Michael A. Healeyb.a., cfp, rhu

John McKeachie

Carrie Lyleb.comm., mba,

cma, cim

Heidi U. Pullemcfp, cdfa

Matthew W.P. Anthonyb.a., cfp

Aeronn Zlotnikb.a.

Nancy Pereiragba.

Philip Levinsonc.a.

Daryl Kingb.sc., flmi

Peter Walmsleyepc

Trent Gurneycsa.

Jack Shaffercfp, clu, ch.f.c

Steven Koub.comm, b.sc., cga

ZLC Financial Group offers a wide-range of customized and innovative solutions to help grow, protect, and perserve your wealth.

For more information, contact our associates on: Vancouver 1200 Park Place, 666 Burrard St | Vancouver BC | V6C 2X8

Tel 604 688 7208 | Fax 604 688 7268 | Toll Free 1.800.663.1499

Victoria 3711 Grange Road | Victoria BC | V8Z 4S9Tel: 250.727.3445 | Fax: 250.479.9716 | Toll Free 1.800.906.5666

www.zlc.net

Your team of experts in Insurance & Retirement | Employee Benefits

Private Investment Management | Structured Settlements

Peter G. Lambb.a., clu, tep,

epc, csa

Garry Zlotnikf.c.a., b.comm., cfp, clu, ch.f.c

Martin Zlotnikb.comm., ll.b

Mark A. Zlotnikc.a., clu

P.M (Pip) Steeleb.comm., cfp, clu,

ch.f.c.

Robert E. Olsonb.a.

H.G. (Howie) Young

cfp

Bruce K. Bergerb.a., cfp

W.A. (Bill) Finlayb.a., c.a.

Lynn NewsomeKen McNaughtoncfp, clu, ch.f.c.,

rhu, csa

Ross Gibsondipt.t

John V.R. Warkb.comm., c.a, cfp,

clu, ch.f.c

Amin E. Jamala.c.i.i., clu, tep

Michael A. Healeyb.a., cfp, rhu

John McKeachie

Carrie Lyleb.comm., mba,

cma, cim

Heidi U. Pullemcfp, cdfa

Matthew W.P. Anthonyb.a., cfp

Aeronn Zlotnikb.a.

Nancy Pereiragba.

Philip Levinsonc.a.

Daryl Kingb.sc., flmi

Peter Walmsleyepc

Trent Gurneycsa.

Jack Shaffercfp, clu, ch.f.c

Steven Koub.comm, b.sc., cga

8 ica.bc.ca June/Summer 2010

On the Cover

Meet the Award Winners for Early Achievement By Ashley Hetherington and Michelle McRae, Editor

Every year the Institute grants awards for early achievement to CAs who have made significant professional accom-

plishments and community contributions within ten years of earning the CA designation. Three CAs have been chosen for this year’s awards: Rizwan Gehlen, CA; K. Scott Jeffery, CA; and Allan Wiekenkamp, CA.

Rizwan Gehlen, CAThough he grew up in a family of engineers, Rizwan Gehlen knew from an early age that he’d end up choosing a different career path. Drawn to business, he ultimately made the decision to become a CA after completing an accounting co-op term at Ellis Foster while attending Simon Fraser University.

“It was my first introduction to the accounting field,” he recounts, “and the interactions at the firm made me realize that accounting was the right choice for me.”

After graduating from SFU with a bachelor of business administration degree in 2000, Rizwan continued articling with Ellis Foster in Vancouver. The following year, he moved to the Vancouver office of Ernst & Young LLP (E&Y), where he completed his articles.

“I was fortunate to article at both firms,” he says. “It exposed me to a wide range of experiences, which helped me develop as a CA.”

After earning his designation in 2002, Rizwan worked in public practice for another two years, managing a group of real estate investment and development funds, including some of the largest real estate investment portfolios in Canada. The experience proved invaluable when he left E&Y in 2004 to serve as director of finance for Park Place Seniors Living, a small company that was looking to expand.

Under Rizwan’s oversight, the company has grown substantially over the past six years—from operating four long-term care homes to operating 15 properties with over 1,500 beds.

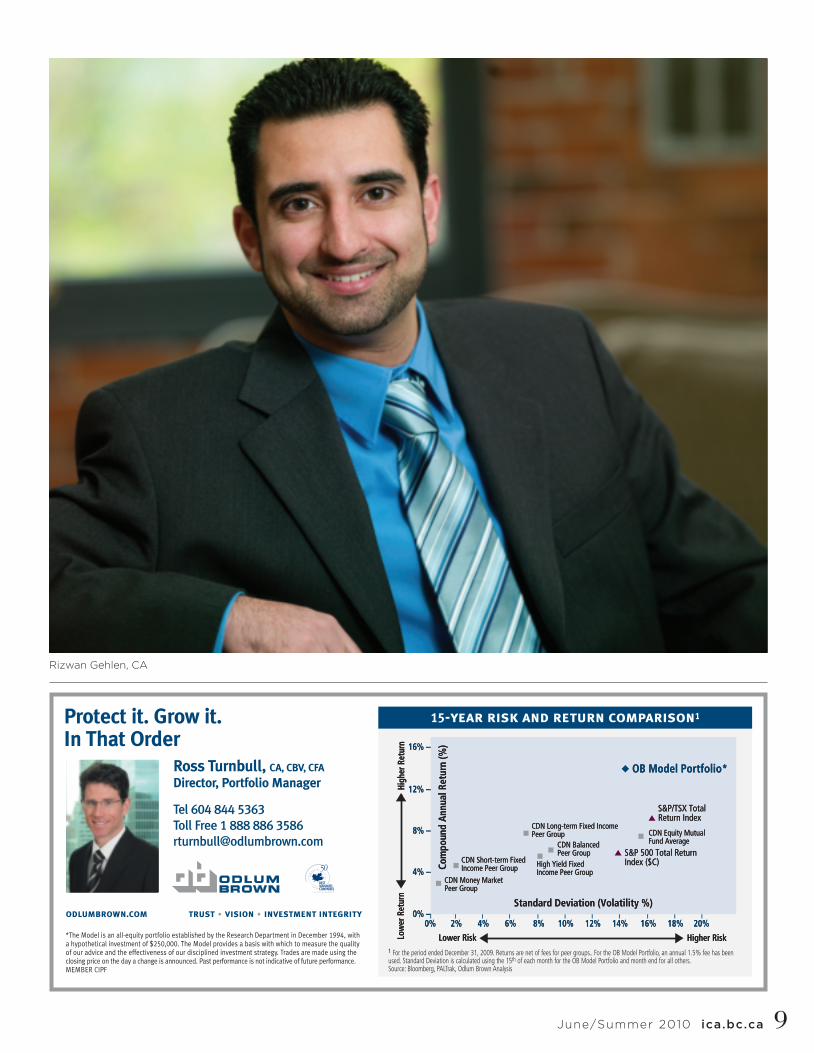

June/Summer 2010 ica.bc.ca 9

Rizwan Gehlen, CA

Standard Deviation (Volatility %)Standard Deviation (Volatility %)

16% –16% –

12% –12% –

8% –8% –

4% –4% –

0% –0% –

Com

poun

d An

nual

Ret

urn

(%)

Com

poun

d An

nual

Ret

urn

(%)

2%2%0%0% 4%4% 6%6% 8%8% 10%10% 12%12% 14%14% 16%16% 18%18% 20%20%

OB Model Portfolio*OB Model Portfolio*

S&P/TSX Total Return IndexS&P/TSX Total Return Index

S&P 500 Total Return Index ($C)S&P 500 Total Return Index ($C)

CDN Equity Mutual Fund AverageCDN Equity Mutual Fund Average

CDN Long-term Fixed Income Peer GroupCDN Long-term Fixed Income Peer Group

CDN Balanced Peer GroupCDN Balanced Peer Group

High Yield Fixed Income Peer GroupHigh Yield Fixed Income Peer Group

CDN Short-term Fixed Income Peer GroupCDN Short-term Fixed Income Peer Group

CDN Money Market Peer GroupCDN Money Market Peer Group

Lower RiskLower Risk Higher RiskHigher Risk

High

er R

etur

nHi

gher

Ret

urn

Low

er R

etur

nLo

wer

Ret

urn

Protect it. Grow it. In That Order

Ross Turnbull, CA, CBV, CFA

Director, Portfolio Manager

Tel 604 844 5363Toll Free 1 888 886 [email protected]

P L A T I N U M M E M B E R

*The Model is an all-equity portfolio established by the Research Department in December 1994, with a hypothetical investment of $250,000. The Model provides a basis with which to measure the quality of our advice and the effectiveness of our disciplined investment strategy. Trades are made using the closing price on the day a change is announced. Past performance is not indicative of future performance.MEMBER CIPF

odlumbrown.com trust • vision • investment integrity

15-year risk and return comparison1

1 For the period ended December 31, 2009. Returns are net of fees for peer groups.. For the OB Model Portfolio, an annual 1.5% fee has beenused. Standard Deviation is calculated using the 15th of each month for the OB Model Portfolio and month end for all others.Source: Bloomberg, PALTrak, Odlum Brown Analysis

10.OBRTurnbullAd1A 1/22/10 2:15 PM Page 1

10 ica.bc.ca June/Summer 2010

It’s now a multi-faceted company that operates seniors’ retirement residences, assisted-living facilities, and residential complex care homes in BC and Alberta.

“The growth has happened quickly,” says Rizwan, now the company’s VP of finance. “We have had to take steps along the way to make sure we expand carefully. This is healthcare—we’re dealing with people’s lives.”

As the company has grown, Rizwan has helped develop an information technology infrastructure and overseen initiatives to expand the role of IT in delivering care.

Committed as he is to ensuring that residents continue to receive the highest standards of care, Rizwan found it particularly gratifying when Park Place Seniors Living received an accredita-tion award in 2008 from the Canadian Council on Health Services Accreditation, the organization that oversees and sets national standards for residential care facilities and acute-care hospitals across Canada.

“We were thrilled not only to be accredited, but also to be nationally recognized as leaders in the healthcare field,” he remembers. “It was the check we needed to confirm that we were managing our growth well.”

Currently helping to provide input for a prov-

ince-wide funding model for the residential care sector in BC, Rizwan has advocated on behalf of the sector at the local and regional levels, provided information and recommendations to government, and developed and presented a funding model for long-term care facilities to the CEO of the Fraser Health Authority.

These efforts are part of an overarching com-mitment to giving back.

“Coming from a family that immigrated to Canada in the mid 1970s, I witnessed the sacrifices my parents made as they built a life for us,” he remembers. “They taught me the importance of hard work, and the importance of giving back to the community.”

In 2005, Rizwan helped the Pakistan-Canada Association raise $1.2 million in relief funds after an earthquake devastated Pakistan, and helped organize the transport of blankets and tents to damaged regions. Today, he serves on several boards and committees of the BC Muslim Association, most recently leading a team that is developing a new school here in BC.

Rizwan also serves on the board of the Vancouver Aquarium, and participated in the 2009 Ride to Conquer Cancer, a two-day, 260-kilometre bike ride from Vancouver to Seattle, to raise funds for cancer research.

But his proudest accomplishment, he says, is having helped to establish a youth centre for Muslim children in Surrey in 1999, while he was attending university. This centre continues to be a vital hub in the community.

“It’s the kind of resource that wasn’t around when I was a kid, because our community was very small back then,” Rizwan explains. “It’s great for kids to have a facility like this in their community.”

Today, his own two young children are part of this community, as he and his wife Imrana are raising their family in Surrey.

“I have an amazing support system,” Rizwan says of his loved ones. “I couldn’t do what I do without the support of my parents, my wife, and my family. They give me the energy to stay involved.”

He also gives credit to his mentors John Sims, FCA (Ellis Foster), Scott Palmer, FCA (E&Y), and Al Jina, LLB (Park Place), thanking them for the support and advice they’ve provided at various stages in his career.

“I’m honoured to receive the Early Achievement Award,” Rizwan says. “I’m always busy, so it’s nice to stop, pause, and accept the recognition.”

For more information contact the Institute of Chartered Accountants of Alberta at [email protected] or 1 800.232.9406

What Distinguishes our Programs?

The CFO Leadership and Corporate Controllership programs build on your current knowledge base, going beyond your technical accounting and financial expertise to give you the competencies you need to successfully lead your organization. In addition, a unique feature of our programs is the opportunity to work one-on-one with an Executive Coach.

The CFO Leadership and Corporate Controllership programs are designed specifically for CFOs and Controllers and aspiring CFOs and Controllers who are determined to move their careers and their organizations forward.

Executive Leadership Programs

November 27 – December 3, 2010Banff, AB

October 23 - 29, 2010 Banff, AB

www.controllership.ca www.cfoleadership.ca

June/Summer 2010 ica.bc.ca 11

K. Scott Jeffery, CA

K. Scott Jeffery, CAGrowing up, Scott Jeffery always knew that he wanted to be a CA.

“I knew that I wanted to be a professional, ” Scott says. “My dad [Don Jeffery] is a CA, so I saw the designation as a stepping stone to being successful in business. I didn’t know which industry I wanted to work in, but I knew I could figure that out later.”

Scott enrolled at the University of BC after high school, but rather than pursuing an under-graduate degree in commerce or accounting, as one might expect, he chose instead to earn a bachelor of arts degree, majoring in history.

“I wasn’t ready to jump on the CA path yet,” he says.

After graduating from UBC in 1998, Scott started taking the prerequisite courses for the CA program. To fast-track his career development, he took courses through the ICABC’s Graduate Admission Program (now known as DAP), the BC Institute of Technology and UBC simulta-neously, and finished all of his prerequisites in one year.

When it came time to find an articling position, Scott says he was fortunate to receive several offers. “The final choice was an easy one for me,” he says of his decision to article with KPMG LLP in Vancouver. “The firm was a good fit, and I connected with my interviewers during the recruiting process.”

These interviewers worked in KPMG’s resources group, which Scott joined in 1999.

“They were a dynamic group,” he says. “I could see that they enjoyed their work and had a lot of fun with each other. It had the ‘work hard, play hard’ environment I wanted to be a part of.”

During his articles, Scott was assigned to several clients in Vancouver’s mining sector, and had the opportunity to start developing expertise in this arena.

“The mining industry in Vancouver plays a huge role in the local business community and has so much to offer,” he says. “There are a lot of high-profile transactions, you’re exposed to international opportunities, and it is filled with some of the most interesting individuals you will ever meet—you encounter some real risk-takers and brilliant entrepreneurs. It’s a great sector to be a part of.”

On one of his earlier assignments, Scott had the chance to work with Ron Larter, CA, a partner in KPMG’s tax group and the firm’s lead resource tax partner in Vancouver. It proved to be a fortuitous opportunity, as it led to Scott’s recruitment into the tax group after he qualified as a CA in 2002.

Tax has turned out to be a great fit.“I enjoyed tax even before I started articling,” he says. “While I was completing my prerequisite

courses, I was drawn to the problem-solving nature of tax. Then when I started working in this area, I realized that every day is different—that every day brings a new challenge—and I love that aspect of my job.”

Having been promoted to the partnership in October 2009, Scott now has the best of both worlds, serving as the lead domestic tax partner for KPMG’s mining group in Vancouver.

He has quickly become a leader among accounting professionals in the mining industry. In 2006, he co-founded the Vancouver Exploration and Mining Industry Network (VEMIN), a networking organization for young professionals in the mining sector. The group facilitates networking events,

12 ica.bc.ca June/Summer 2010

brings in guest speakers, and organizes social functions. So far, VEMIN has over 100 mem-bers, and its events have drawn participation from the chief executives of some of Vancouver’s largest mining companies. Scott remains active with the organization.

“Today, Vancouver is one of the leading centers for mining and exploration companies in the world, and it is important that the next generation be engaged,” he explains. “Our goal with VEMIN is to help ensure that the mining sector in Vancouver remains strong, and that it continues to thrive.”

Scott’s people skills have not only helped contribute to VEMIN’s success—they have also benefited KPMG. In addition to helping with the firm’s campus recruiting efforts and with the training of new hires, he led the development of a comprehensive training program for summer students rotating through the tax practice in 2007, and served as a Level 1 course instructor for the CICA’s In-Depth Tax Course. Recogniz-ing these skills, KPMG appointed him “people leader” for the mining and industrial markets segments of its tax practice in 2007—a role that gave him oversight of staff and human resources.

Today, in addition to his roles at KPMG and VEMIN, Scott serves as assistant editor of the Canadian Resource Taxation book, and contri-butes to Resource Sector Taxation, a quarterly journal. In 2009 and 2010, he also served as a panellist at the Fundamentals of Canadian Mining Taxation Course in Vancouver.

“The most challenging aspect of my job,” he says, “is not having enough hours in a day to do all the things I want to do.”

Nevertheless, Scott still manages to find time to volunteer with the United Way and with Movember, a global campaign to raise funds for prostate cancer.

“I’m very humbled and extremely honoured,” he says of receiving the Early Achievement Award. “I have many people to thank for their support over the years—my family, especially my parents and grandparents; my fiancée, Laura Smith, CA; and my mentors at KPMG: Clark Hollands, FCA; Dale Peniuk, CA; Ron Larter, CA; and Walter Pela, CA.”

Allan Wiekenkamp, CA, TEP, CFPBy his third year of study as a science major at the University of Victoria, Allan Wiekenkamp knew that he would end up changing fields.

“I knew I didn’t want a career in science,” he remembers. “Being a doctor or working in a lab just wasn’t for me.”

It was a casual conversation with one of the patrons of a Sidney-area marina, where Allan worked during the summers throughout university, that first got him thinking about the CA profession.

“After work one day, a retired CA invited me to join him for a drink,” Allan recounts. “He asked me what I was going to do with my life, and when I didn’t have an answer, he suggested that I become a CA. He said it would be my ‘ticket to the game.’”

Allan took this advice. After graduating from UVic with a bachelor of science degree in 1995, he attended the University of British Columbia’s Graduate Admissions Program to complete the prerequisite courses for the CA program. He earned his CA designation in 1999 while articling with Bestwick & Partners Chartered Accountants in Nanaimo.

“If you had told me when I was a kid that I’d be an accountant when I grew up, I’d have laughed!” Allan admits. “But I found something that’s right for me: the foundation for entrepreneurship and a career in financial services.”

While attending a UFE preparation course during his articles, he met his future wife, Candice (also a CA), to whom he gives credit for his success on the UFE.

Allan Wiekenkamp, CA, TEP, CFP

June/Summer 2010 ica.bc.ca 13

“I wanted to study more,” he says, “because it gave me a reason to spend more time with her.”

Soon after qualifying as a CA, Allan moved to the Langley office of Deloitte & Touche LLP, where he worked in audit. Then in 2001, he ac-cepted a senior accounting position at the Bermuda branch of Ernst & Young LLP (E&Y), working in the private client accounting group, which specialized in trust and ultra high-net-worth accounting.

“Up until that point, I’d spent my CA career working in audit,” he says of the move. “I was ready for the next challenge.”

Allan was promoted to manager in July 2003, and earned his trust and estates practitioner (TEP) designation, with honours, in 2005. Shortly thereafter, he found himself at a bit of a crossroads.

“Early in 2005, the firm announced that it was going to exit all non-core services, which meant that my department was either going to be shut down or sold,” he recounts. “It took me about 30 seconds to go from shock to realizing that there was a business opportunity here.”

Convinced that the department should go out on its own, Allan launched FORS Limited (Family Office Reporting Solutions) in late November 2005. At 32 years old, he found himself managing director of a company with

five employees and a break-even budget at best. The gamble paid off. Under Allan’s leadership,

FORS experienced dramatic growth over the next three years. By 2008, the staff had increased to 11 employees, revenue had increased by a whopping 400% from the first-year budget, and the firm accounted for over $20 billion of client assets. Along the way, Allan earned a reputation as a leader in Bermuda’s trust accounting and investment reporting sector.

Still, he says his biggest source of pride came from creating a “people-first” work environment.

“I consider myself a people manager—a skill I learned from my days at E&Y,” he explains. “At FORS, we’ve tried to focus on work/life balance and building trust with our employees.”

Allan believes in balanced living, especially now that he and Candice have two young children. He sold FORS in 2009 to a group of investors looking to expand the brand and business internationally, and he and his family are moving back to Nanaimo, BC this month.

“On to the next step,” he says. That next step includes launching a new

consultancy firm, Sum Consulting Ltd., recon-necting with friends and former colleagues, and getting involved once again in the Nanaimo community, where he used to volunteer with Literacy Nanaimo and the United Way.

Life outside of work has always included volunteerism. In Bermuda, Allan volunteered as treasurer for a local charity, served on the executive committee of the local branch of the Society of Trust & Estate Practitioners (STEP), served as treasurer of the STEP board, spoke at STEP conferences, and wrote for STEP’s international journal. He also mentored young CAs who’d relocated to Bermuda.

“When I think back, I’m thankful to the many people who have influenced me,” he says of his life thus far. “I’m thankful for my wife’s support and understanding; for my parents having instilled in me the importance of family values and supporting me from the beginning— including when I lived at home during my articles; and for the advice of my partner and mentor at E&Y in Bermuda, Derek Stapley, CA.”

Allan also thanks that retired CA from the Sidney marina.

“That was a crucial juncture in my life that put my career on the right path,” he says. “I’m grateful that I went for that drink!”

Photos of Rizwan Gehlen and Scott Jeffery by Kent Kallberg of Kent Kallberg Studios Ltd. in Vancouver.

14 ica.bc.ca June/Summer 2010

Giving Back to the Community By Michelle McRae, Editor

Joanne Hausch, CAJoanne Hausch, an associate partner with Deloitte & Touche LLP in Vancouver, has made considerable contributions to the community over the years.

In 2000, Joanne co-founded the StreetMeals program of Canadian Memorial Church (CMUC) to prepare food for Vancouver’s homeless youth. Over the past decade, she has been a driving force for the program, enlisting the participation of members of her church, colleagues in the CA profession, friends, and family members. She even guided a student group at the University of BC to create their own street youth support group.

In a typical month, Joanne gathers donations of food, clothing, and hygiene supplies, and organizes and directs a group of people in the preparation of 700-800 sandwiches and gallons of chilli. She then personally delivers the food and other donations to Directions Youth Services for distribution.

Directions is a 24-hour multi-service centre operated by Family Services of Greater Vancouver to support Vancouver’s homeless and/or at-risk youth. The centre provides free counselling, basic services, and assistance in obtaining jobs, housing, and a positive future. It’s estimated that the centre helps more than 1,400 young people each year.

To date, Joanne has introduced over 50 people to Directions, increasing awareness and helping to raise funds. Her fundraising efforts include organizing two Deloitte “Impact” (firm-wide community service) days in support of Directions, which led to a significant donation.

“Our firm is very active in the community,” Joanne says, “and we support the personal efforts of partners and staff.”

It’s this kind of support that has enabled Joanne to take on new projects. In June 2008, for example, she established the CMUC Street-Meals Scholarship. This fund provides financial assistance to former street youth who are enrolled in college or university and want to pursue a career in child and youth services. Approximately $15,000 has gone towards sending young people to school so far. Joanne continues to organize donations and oversee the review of scholarship applications and the disbursement of bursaries.

“The current work I do with StreetMeals—particularly the creation of the scholarship program—has been incredibly rewarding,” she says. “I am so inspired by these youth who have turned their lives around and are counselling others to get off the streets.”

In 2009, Joanne took a more active role in developing the vision for Directions by joining the board of Family Services of Greater Vancouver. She also serves on several committees, and has played a key role in developing the agency’s strategic plan.

Another of Joanne’s notable contributions is her work as a founder of the BC chapter of the CATA Women in Technology (WIT) Forum. CATA WIT Forum is a national non-profit volunteer community network that helps women in high-technology sectors advance in their careers and start their own companies. Over the course of two years, Joanne spearheaded the creation of a local chapter, helping to set up an executive team, recruiting young women to serve on the committee, organizing meetings, and promoting the Forum’s mission. The chapter has thrived since its official launch in June 2009, and Joanne continues to provide leadership and mentorship as co-chair of the executive.

In all, it’s estimated that Joanne has put in literally thousands of hours of volunteer service in the past ten years. She has done this all while raising a family of her own and managing her professional responsibilities as a leader in Deloitte’s R&D practice.

The Institute’s Community Service Award recognizes CAs who’ve gone above and beyond in volunteering their skills for the betterment of the community. This year’s winners are: Joanne Hausch, CA; Steve Lake, CA; Erfan Kazemi, CA, Edward Robinson, CA; and John Webster, FCA.

APPLICATION DEADLINES

dap_beyondnumbers_jan26.eps 1/26/2010 10:56:59 AM

June/Summer 2010 ica.bc.ca 15

“There are many reasons why I make volunteer work a priority,” Joanne says. “I started doing things that I had a personal interest in, and then other opportunities started to come my way. Each one has brought new friends and new experiences.”

Steve Lake, CAIt was a life-changing experience as a newlywed that inspired Steve Lake to make volunteerism a key part of his life.

“My wife Pat and I toured Europe for a year, in our first year of

marriage,” Steve recounts. “This vacation was one of the best decisions of our lives, as we saw the world from different perspectives. It gave us a lot of time to reflect and consider how we fit into society.”

Within a month of returning home, Steve began volunteering with Big Brothers of Greater Vancouver. His pairing with a nine-year- old “little brother” ended up evolving into a 40+-year mentorship, and Steve’s mentee is now an established professional and friend.

Joining Big Brothers was his first foray into community service, but certainly not his last. His contributions are so numerous that what follows are just a few highlights.

Highly active in his local business community throughout his career, the semi-retired associate and former partner with MacKay LLP in Surrey is a long-time contributor to the Surrey Board of Trade. He currently serves on its board of directors, chairs the Finance and Police Officer of the Year Awards committees, and acts as treasurer. In the latter capacity, he helped turn around a deficit of $117,000 to a profit of $9,000 in 2007.

Steve is also a past board member and president of both the Fraser Valley Estate Planning Council, which he helped found in 1995, and the Scott Road Business Association. In 2001, the Scott Road Business Association recognized his efforts by naming him “Business Person of the Year.” An avid athlete, Steve has also applied his leader-ship skills to a number of sports organizations. In 1986, he became the director of administration for the 1987 BC Summer Games, and put in 1,200 volunteer hours over a two-year period. His efforts led to a legacy of $75,000 and over $1,000,000 being spent in the community, and garnered him a Certificate of Recognition from the 1988 Calgary Olympic Committee.

Steve has played and coached hockey at several

levels. He also led his Oldtimers’ Hockey team in sponsoring several North Delta Minor Hockey Association (NDMHA) teams, and coached minor hockey for the NDMHA while his children were playing in the league. He also served on the NDMHA board, and one of his many contributions was to systematize the accounting system. The Association later named him “Sportsman of the Year.”

Steve also volunteered for several years with the North Delta soccer league, the Air Canada Golf Championship, and the Delta Thistle Curling Club. More recently, he and his wife volunteered at the 2010 Winter Olympics.

Equally passionate about education, Steve helped to develop a diploma program for CA students, volunteered with Kwantlen’s Planned Giving Department, and lectured on the subject of handwriting analysis to business groups and Kwantlen students. Keenly interested in graphology, Steve served as treasurer and assistant editor of the International Grapho-Analysis Society (IGAS) for 15 years, and served as president of its Canada West Chapter from 2003 to 2007.

Eager to support others in his community, Steve has worked extensively to help local-area seniors and has provided mentorship to high school and post-secondary students. As the founder of Lake & Associates (now part of MacKay LLP), Steve spearheaded his firm’s involvement in scholarship programs for North Delta high schools and Kwantlen Polytechnic University. Under his leadership, Lake & Associates also became involved in career planning events at the Seaquam, North Delta, and Surrey high schools, and gave students a chance to gain valuable experience. In 2007, Steve began volunteering with Act II Children and Families, a non-profit organization that helps abused children and women.

“Having a great education, and developing the expertise that we have as CAs, makes you realize that you have something to offer to make a meaningful contribution in the world,” Steve says. “I have met a lot of interesting and positively motivated people through volunteering, and it makes me feel good that I can help make a difference.”

Erfan Kazemi, CA“Volunteering is something I’ve always felt strongly about,” says Erfan Kazemi, a manager with PricewaterhouseCoopers LLP in Vancouver.

The young CA (he qualified in 2007) has actually been volunteering in the community since he was an elementary school student.

“Volunteering was always supported and promoted by my teachers,” he recounts. “Additionally, the Baha’i faith, which I belong to, encourages members to provide service back to the community.”

Passionate about improving accessibility to learning, Erfan was inspired to start volunteering with the Vancouver Public Library (VPL) in 2006. The VPL is the third largest library system in Canada, with over 20 branches spread throughout the city. As vice-chair of the board of directors, Erfan helps set the strategic direction for the library, while taking into account the needs of the various communities it serves.

“I have always appreciated the unique role the library plays in our society,” Erfan says. “Its programs and services reflect and respond to the diversity of our many communities, including people who are socially excluded or vulnerable.

“Having emigrated to Canada,” he adds, “I also appreciate all of the services it provides to new immigrants.”

The VPL is focused on developing programs that foster an environment of learning, particularly for children and young people.

“Access to learning is an essential component of a child’s early educational development,” Erfan says. “Programs like ‘Ready to Read’ and ‘Homework Help’ encourage and facilitate readership among children. As well, the library offers programs that provide safe social spaces for youth in the Lower Mainland.”

Erfan, who also previously served as chair of the VPL’s Human Resources Committee, has worked tirelessly in support of the library’s mission over the last four years, consulting with stakeholders, building consensus, and representing the VPL at Vancouver City Council meetings and at community events.

“It can be a challenge committing to and finding the time to volunteer,” he acknowledges. “However, the experience is extremely satisfying, and I have always felt that I get more out of my volunteer work than I put in. Recently, some of my most rewarding experiences have been helping the library board to establish a presence in the downtown eastside, and to further develop programs that encourage people in under-serviced areas to participate. These are exciting initiatives for the community, and it’s very fulfilling to be part of them.”

16 ica.bc.ca June/Summer 2010

continuedonpage25

In addition to his commitment to the VPL, Erfan also acts as the treasurer of the board of directors of the Vancouver branch of the Canadian Institute of Mining.

“Michael Cinnamond, CA, PwC’s BC mining leader and a personal mentor, encouraged me to volunteer within the industry,” Erfan recounts. “Serving as treasurer of the local branch has been a great experience. Not only have I had the chance to learn even more about the industry, I’ve also met some great people along the way.”

He encourages other young CAs to get similarly involved in the community.

“Through my volunteer work, I’ve developed some strong friendships,” he says. “Volunteering has also given me the opportunity to meet great people and to feel more connected with my community. For younger CAs, it is a really great way to develop a different skill set.”

Edward (Ted) Robinson, CA·IFA/CBV“I’ve always maintained that I get far more out of volunteering than I ever put in,” says Ted Robinson, a partner with the Vancouver office of

LBC International Investigative Accounting Inc. “Volunteering has introduced me to a large number of like-minded people, many of whom have become long-time friends, and it has given me the satisfaction of knowing that I’ve contri-buted to the well being of my community. It has also made me appreciate the difference that dedicated people can make.”

Ted has been volunteering for more than 30 years, applying his unique set of skills, including his accounting and financial expertise, to a variety of charitable causes, with no job too big or too small. He first began volunteering in the mid-1970s, after Tom Cook, FCA, his boss at the time, encouraged him to get involved.

“Tom was on the board of the YMCA of Vancouver then, and he strongly believed in supporting community,” Ted recounts. “He used to say: ‘You have to pay your rent to the community, because it provides you with a career and a living.’”

Heeding this advice, Ted joined the board of directors of the YMCA. He has volunteered with the organization ever since.

“My involvement started as a career development tool, but I quickly realized that the YMCA is so much more than just “a gym and a swim,” he says. “Locally, it is the largest provider of childcare in the city and, in fact, across the

country. It provides programs and facilities for thousands of kids every year, and employment and career counselling to some of the city’s most disadvantaged people.”

Ted currently serves as a trustee of the Endowment Fund for the YMCA of Greater Vancouver. Over the years, he has also served as board chair for both the YMCA of Greater Vancouver and YMCA Canada. He is also a past member of the Executive and Finance committees of the World Alliance of YMCAs.

“Internationally, the YMCA provides assistance to some of the poorest communities around the world, providing infrastructure, training, health services, and more,” Ted says. “It has been a privilege to be part of an organization that operates in over 80 countries.”

In addition to his ongoing involvement with the YMCA, Ted volunteers with Kids Help Phone, Canada’s only source of free phone and online counselling, referral, and information services for children and youth in need.

“My involvement with Kid’s Help Phone started in 2005 after my wife got involved in a fundraising program to help troubled youth in Vancouver,” he says. “In today’s growingly impersonal times, I think Kid’s Help Phone provides a much needed service to a segment of our society that is too often ignored.”

Ted started as a signage coordinator for the organization’s “Homes for the Holidays” event, and developed the process and procedures for this role going forward. He has calculated accurate routes and maps to events held by the charity, and has taken a hands-on approach when it comes to the manual labour of installing and removing signage. He has also supported several committees with his computer expertise.

“Most of my volunteer work has gone towards organizations that are strongly youth oriented,” Ted says. “As a proud father of three children and now a grandfather of four, I’ve always enjoyed being involved with young people. And it keeps me young!

John Webster, FCADespite a demanding career as the BC region leader for Cleantech and Renewable Energy for PricewaterhouseCoopers LLP, John Webster volunteers extensively in the community to improve the quality of life for Lower Mainland residents.

Immediately after joining the board of directors of the United Way of the Lower Mainland in 2004, John became involved with the organization’s BC211 project, which aims to give Lower Mainlanders 24-hour access to the full range of non-emergency health and social services offered by community and government agencies.

“Not only does the service direct non-emergency traffic away from 911,” he explains, “it also allows the compilation of data to enable social service agencies to understand what and where the key issues are in the community.”

John has worked tirelessly over the past six years to bring the project to fruition, and when the United Way partnered with Information Services Vancouver to create the BC 211 Services Society in 2009, he assumed the role of co-chair—a position he continues to hold.

Thanks to funding from the United Way of the Lower Mainland, BC211 began providing free, confidential, and multilingual services by phone and online to communities in the Metro Vancouver, Fraser Valley, and Squamish-Lillooet Regional Districts in April 2010. The goal is to eventually take the service provincewide.

“211 is a service that represents a huge opportunity for us in BC,” John says. “It is already serving 65% of the US population, and it’s in place in Ontario and in several cities in Alberta and Quebec. Wherever the service has been introduced, it has been successful.”

John has contributed to the United Way of the Lower Mainland in a variety of other capacities as well. He served as vice-chair of the board of directors and chair of the Board Governance and Nominations Committee in 2006/2007, and chair of the board in 2007/2008. He is also a major donor to the organization, and currently serves as a liaison with its Campaign Cabinet.

When his children were growing up, John also volunteered in the community as a coach for several youth soccer teams and helped with the Jackrabbits program in cross-country skiing. His past volun-teerism also includes serving as a member of the Capilano Scouts’ executive; a director and treasurer for Presentation House Gallery; and co-chair of the Lions Gate Hospital Foundation’s Annual Giving Campaign (1989-90).

June/Summer 2010 ica.bc.ca 17

If giving back to the CA profession were an Olympic sport, Vancouver’s own Gord Cummings would most certainly have won

a gold medal this winter. Passionate about auditing and assurance standards, Gord has devoted himself to the betterment of the CA profession for over a decade. The accomplished CA and principal with Vancouver-based CA firm D&H Group LLP confesses that auditing standards are something he’s always been interested in. His peers would tell you that the profession is the better for it.

At D&H Group, Gord provides audit and assurance services to Canadian publicly listed and privately held businesses, and his clients include start-up and developing businesses in the technology and natural resource exploration sectors. But his day just starts there.

As a member of the CICA’s Auditing and Assurance Standards Board (AASB) since 2006 and the current chair of the AASB’s Review Engagement Task Force, Gord has already put in hundreds of hours to help ensure that Canada

Ritchie W. McCloy Award Goes to Gordon Cummings, CA By Lesli Boldt

The Ritchie W. McCloy Award for CA Volunteerism recognizes the value of a CA or non-CA’s contributions to the CA profession, whether through an individual project or a series of activities. In addition to their dedication to the profession, award recipients must embody values such as openness, honesty, and generosity. This year’s recipient is Gordon D. (Gord) Cummings, CA.

continues to have a high-quality suite of audit and other assurance and related standards that serve both the profession and the public well.

Stella Leung, CA, the ICABC’s professional standards advisor, can’t say enough about the value Gord has brought to the profession and to BC CAs on the national stage.

“Gord is one of my favourite people to work with,” she says with enthusiasm. “He wants to make sure practitioners in small and mid-sized firms in BC are represented at the national level. He appreciates the profession, is constantly growing as a professional, and—most importantly—always wants to give something back.”

“Giving back to the profession,” says Gord, “is one of the responsibilities you take on when you become a CA.”

He says the most rewarding thing about devoting so much time and energy to local, national, and international projects is getting the chance to meet a lot of interesting people along the way.

“I’ve learned a lot, met neat people, and made a lot of friends through the work I’ve done in the profession,” he says. “It’s also nice to know that I’m not the only crazy one who actually likes working on assurance standards!”

While his work with the AASB frequently requires him to attend meetings in Toronto, he hasn’t lessened his involvement with clients.

“The increased travel has meant investing in a BlackBerry and a good laptop, so that I can keep in touch with my clients and take some work with me while I’m on the road,” he says. “My clients come first, so I try to use my personal time for my volunteer activities whenever I can.”

These myriad volunteer activities include serving as a long-time member and past chair of the ICABC’s Exposure Draft Forum, and as a six-year member of the Institute’s Practice Review & Licensing Committee (2001-2006). In addition, Gord co-authored the Mid-Sized Firms Protocol and Practice Guide in 2004. Aimed at mid-sized CA firms, the Guide is designed to help with the implementation of new audit and review engagement quality control and independence standards, and has proven to be an invaluable resource for firms across the country.

When time permits, Gord also accepts speaking engagements at conferences and webinars to further share his knowledge on important issues in the profession, including the implementation of Canadian Auditing Standards, which come into effect in Canada at the end of 2010.

Gord admits that his volunteer work with the profession can be demanding and take up a lot of personal time, but he says putting in these extra hours is worth it. And before you assume that Gord has no life outside of work, rest assured that he still makes time for golf, family, and—albeit in rare instances—taking some time off. After this year’s busy tax season ended, for example, Gord and his wife took a vacation to Maui—the first holiday the couple had taken since their honeymoon in 2008. It was a well-deserved break for a CA who has given so much to his profession.

Lesli Boldt is a marketing communications consultant and owner of Boldt Communications in Vancouver. She was the editor of the Mid-Sized Firms Protocol and Practice Guide (2004), and has contributed several articles to ICABC publications.

The Ritchie W. McCloy Award provides a cash prize to the recipient’s charity of choice,

courtesy of the Vancouver Foundation. Gord has chosen the Canadian Cancer Society

Relay for Life.

18 ica.bc.ca June/Summer 2010

Tax Traps & Tips

Why It Pays to Stay “Connected”By Shane Onufrechuk, CA

The Income Tax Act (ITA) contains a myriad of terms that describe and define the nature of relationships between

taxpayers for income tax purposes. Taxpayers can be “connected,” “associated,” “affiliated,” “related,” and/or “not deal[ing] at arm’s-length.” For many accountants, it can be difficult to remember the distinctions between these terms. Unfortunately, failing to remember these dis-tinctions—particularly with regard to the definition of “connected corporations”—can prove costly. As this article will demonstrate, concluding that two corporations are connected when, in fact, they are not, can result in material adverse income tax consequences.

Defining what it means to be “connected”Before delving into the kinds of problems that may arise when two corporations are not connected, it is important to understand how the term is defined in the ITA. In general terms, subsection 186(4) states that one corporation will be connected with another corporation, at a particular time, when either of the following two tests are met: 1. One corporation is “controlled” by the

other corporation at that time (control is defined in the ITA as when more than 50% of the shares that have full voting rights belong to the other corporation, or to persons not dealing at arm’s length with the other corporation, or to a combination of the other corporation and persons not dealing at arm’s length with the other corporation); or

2. One corporation, at that time, owns shares in the other corporation that have more than 10% of full voting rights under all circumstances, and the shares owned represent more than 10% of the fair market value (FMV) of all of the corporation’s issued shares.

In situations where—either directly or indirectly—a person or related group controls both corporations, the corporations will generally be found to be connected for income tax purposes by virtue of test 1. Where both corporations are not controlled by a person or related group, test 2 will determine whether the two corporations are connected.

The trap most likely to trip up unsuspecting advisors is a common misconception that once a corporation has more than 10% of any class of another corporation’s shares, these corporations are connected for income tax purposes. In reality, test 2 requires one corporation to own shares that entitle it to 10% of the FMV of all of the other corporation’s shares and shares entitling it to more than 10% of the other corporation’s full voting rights. Where more than 10% of the votes and value are not held by the owning corporation, test 2 is not met and the corporations are not connected.

Here’s an example for illustrative purposes: Mr. A, a Canadian resident individual (or perhaps a family trust with Mr. A’s immediate family as beneficiaries of the trust), owns 100% of Aco, which in turn owns 50% of the non-voting, participating shares of Opco. Mr. B, a Canadian resident individual who deals at arm’s length with Mr. A, owns 100% of Bco, which, in turn, owns the other 50% of the non-voting, participating shares of Opco. Mr. A and Mr. B each own 50% of the voting, non-participating shares of Opco personally. Opco uses its assets to carry on an active business in Canada. This kind of structure—with Mr. A and Mr. B wanting direct voting control—is not uncommon.

When applying the connected corporation tests to this example, neither Aco nor Bco are considered connected to Opco for income tax purposes. Test 1 is not met, because neither Aco nor Bco “control” Opco; and test 2 is not met, because while Aco and Bco each hold shares that represent more than 10% of the FMV of all of Opco’s issued shares, neither corporation has more than 10% of the full voting rights of Opco (as the voting rights are held by Mr. A and Mr. B directly).

Costly repercussionsThis scenario illustrates just how easy it is for advisors to inadvertently find themselves dealing with a structure wherein two corporations are not connected for income tax purposes. Now let’s look at the potentially costly repercussions of this lack of connected status.

Part IV taxOne important consideration when two corporations are not connected arises when a dividend is paid. Part IV tax (of 1/3 of the dividend paid) will be payable by the recipient of the dividend. Using the previous example, if Opco paid a taxable dividend to Aco and Bco, 33 1/3% of the dividend amount would be payable by Aco and Bco as Part IV tax.

If the advisor to Aco and Bco does not realize that these companies are not connected to Opco, this tax could go unpaid, and arrears interest and penalties could accrue. Given that one of the primary purposes for the creation of Aco and Bco by Mr. A and Mr. B, respectively, may have been to allow for Opco to pay out inter-corporate dividends tax-free, it is unlikely that this result would be well received.

The only potentially mitigating factor about the Part IV tax is that where a private corporation receives the dividend from an unconnected corporation, the Part IV tax is refundable once the recipient corporation pays out sufficient dividends to its shareholders.

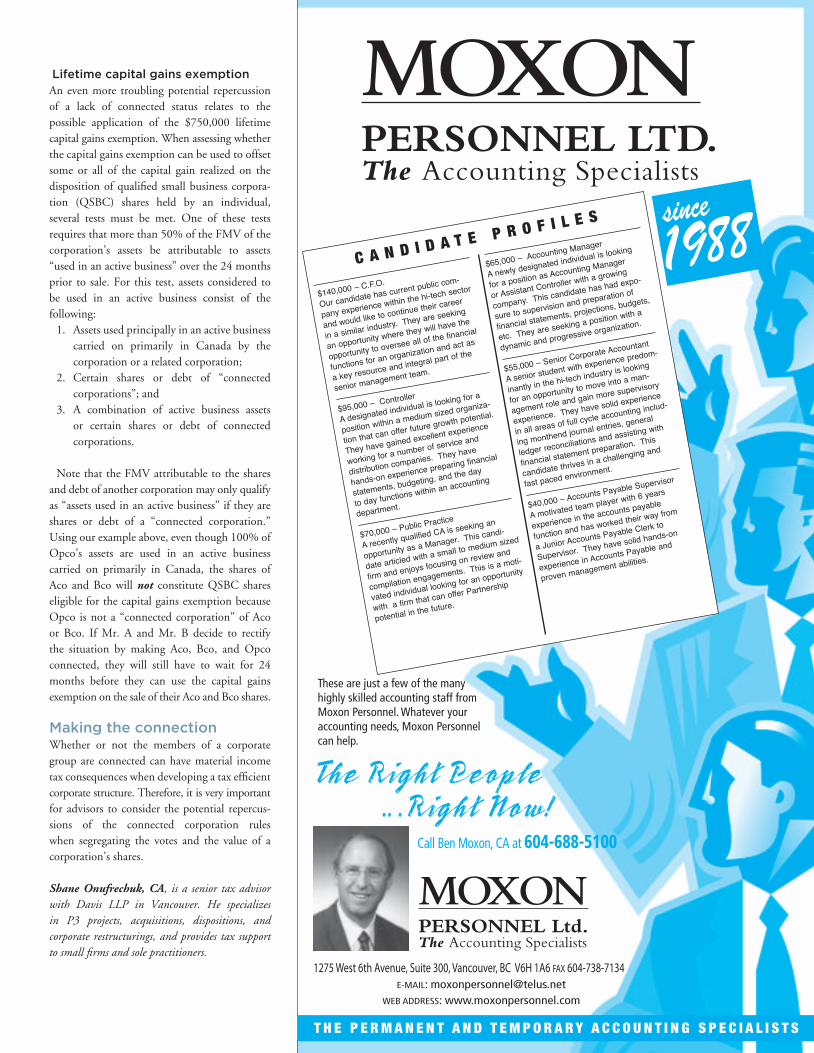

Lifetime capital gains exemptionAn even more troubling potential repercussion of a lack of connected status relates to the possible application of the $750,000 lifetime capital gains exemption. When assessing whether the capital gains exemption can be used to offset some or all of the capital gain realized on the disposition of qualified small business corpora-tion (QSBC) shares held by an individual, several tests must be met. One of these tests requires that more than 50% of the FMV of the corporation’s assets be attributable to assets “used in an active business” over the 24 months prior to sale. For this test, assets considered to be used in an active business consist of the following: 1. Assets used principally in an active business

carried on primarily in Canada by the corporation or a related corporation;

2. Certain shares or debt of “connected corporations”; and

3. A combination of active business assets or certain shares or debt of connected corporations.

Note that the FMV attributable to the shares and debt of another corporation may only qualify as “assets used in an active business” if they are shares or debt of a “connected corporation.” Using our example above, even though 100% of Opco’s assets are used in an active business carried on primarily in Canada, the shares of Aco and Bco will not constitute QSBC shares eligible for the capital gains exemption because Opco is not a “connected corporation” of Aco or Bco. If Mr. A and Mr. B decide to rectify the situation by making Aco, Bco, and Opco connected, they will still have to wait for 24 months before they can use the capital gains exemption on the sale of their Aco and Bco shares.

Making the connectionWhether or not the members of a corporate group are connected can have material income tax consequences when developing a tax efficient corporate structure. Therefore, it is very important for advisors to consider the potential repercus-sions of the connected corporation rules when segregating the votes and the value of a corporation’s shares.

Shane Onufrechuk, CA, is a senior tax advisor with Davis LLP in Vancouver. He specializes in P3 projects, acquisitions, dispositions, and corporate restructurings, and provides tax support to small firms and sole practitioners.

$140,000 – C.F.O.

Our candidate has current public com-

pany experience within the hi-tech sector

and would like to continue their career

in a similar industry. They are seeking

an opportunity where they will have the

opportunity to oversee all of the financial

functions for an organization and act as

a key resource and integral part of the

senior management team.

$95,000 – Controller

A designated individual is looking for a

position within a medium sized organiza-

tion that can offer future growth potential.

They have gained excellent experience

working for a number of service and

distribution companies. They have

hands-on experience preparing financial

statements, budgeting, and the day

to day functions within an accounting

department.

$70,000 – Public Practice

A recently qualified CA is seeking an

opportunity as a Manager. This candi-

date articled with a small to medium sized

firm and enjoys focusing on review and

compilation engagements. This is a moti-

vated individual looking for an opportunity

with a firm that can offer Partnership

potential in the future.

$65,000 – Accounting Manager

A newly designated individual is looking

for a position as Accounting Manager

or Assistant Controller with a growing

company. This candidate has had expo-

sure to supervision and preparation of

financial statements, projections, budgets,

etc. They are seeking a position with a

dynamic and progressive organization.

$55,000 – Senior Corporate Accountant

A senior student with experience predom-

inantly in the hi-tech industry is looking

for an opportunity to move into a man-

agement role and gain more supervisory

experience. They have solid experience

in all areas of full cycle accounting includ-

ing monthend journal entries, general

ledger reconciliations and assisting with

financial statement preparation. This

candidate thrives in a challenging and

fast paced environment.

$40,000 – Accounts Payable Supervisor

A motivated team player with 6 years

experience in the accounts payable

function and has worked their way from

a Junior Accounts Payable Clerk to

Supervisor. They have solid hands-on

experience in Accounts Payable and

proven management abilities.

20 ica.bc.ca June/Summer 2010

PD News

For detailed course descriptions or a complete schedule of upcoming PD seminars, consult your spring 2010 PD brochure or visit our website at www.icabc-pd.com. To register, call the PD department at 604-681-3264.

Audit & AccountingAuditing in the New CAS EnvironmentThe new Canadian auditing standards (CAS) will become effective for periods ending on or after December 14, 2010. Are you ready for the move? Is your firm? Do you know which steps you and your firm should start taking now to ensure a successful transition?

This course will provide participants with a solid foundation for the practical application of CAS in the new auditing environment. Through the use of case studies, participants will get the opportunity to enhance their understanding of the standards, and practice applying the standards to a set of client-specific facts. Jun 3&4, 9am-5pm, Sutton Place, Vancouver

Jun 28&29, 9am-5pm, Comfort Hotel, Victoria

Jul 12&13, 9am-5pm, Sutton Place, Vancouver

IFRS – Property, Plant, and EquipmentThe objective of this seminar is to prepare indi-viduals to: decide when a property should be recognized and what costs should be capitalized; apply the cost model and revaluation model with attention to the practical issues; determine how and when depreciation and losses in value should be recorded; record the appearance of property, plant, and equipment on the balance sheet; and determine which disclosures are appropriate.Jun 29, 9am-5pm, Sutton Place, Vancouver

A Practical Guide to Corporate FinanceThis seminar will provide participants with a working knowledge of the various ways to finance a business activity through the capital markets. It will also provide an understanding of the regulatory regime that governs different methods of raising capital, and the different players central to the field, such as underwriters.Jun 24, 9am-5pm Sutton Place, Vancouver

ManagementActivity-Based Costing and Management & Activity-Based Budgeting as a Strategic WeaponIn multi-product, multi-service, and multi- client companies, the accurate costing and performance-tracking of products and services is not only a matter of survival, it is also a strategic weapon for growth and profitability.

This workshop will introduce the key concepts and guidelines for implementing activity-based costing (ABC/M) and activity-based budgeting (ABB) to improve profitability. It will provide participants with a road map to initiate this framework and ensure its successful completion—thereby enabling them to deliver the necessary information to all decision-makers within their organizations.Jul 22, 9am-5pm, Sutton Place, Vancouver

An Introduction to Writing Business PlansWhat are the key ingredients to a successful business plan? What are the most common pitfalls you, your clients, and/or your organization need to avoid to ensure that your business plan hits the mark?

This one-day workshop will explore the essen-tial elements required to develop an effective business plan. It will introduce participants to the foundation of business planning , and walk them through templates and checklists to produce business plans that work. Jul 07, 9am-5pm, Sutton Place, Vancouver

Effective Financial Analysis for Business Decisions – Medium-Sized Privately Held BusinessesIn today’s fast-paced world, the effectiveness of business decisions and analyses made by owners and their advisors depends on their understanding of the financial impact of their decisions. More than ever, management is looking for well laid-out recommendations that go beyond a summary of financial information.

This seminar will introduce a decision-making format for the use of financial information and a road map for providing consistent, well-articu-lated analysis and recommendations.Jul 21, 9am-5pm, Sutton Place, Vancouver

Clinic on SupervisionGreat employees do not always make great supervisors—particularly if they are thrown into the job with little or no training. But if they can learn to bring out the best in their subordinates while still being effective producers themselves, they become doubly valuable to their organizations.

This clinic will help supervisors focus on specific, concrete techniques that will make them more effective in managing others.Jun 25, 9am-5pm, Sutton Place, Vancouver

Influence – Moving People to ActionThis seminar will teach business professionals how to use principled planning tools, strategies, and skills to influence others and accomplish their goals in an effective and positive manner.

At the end of this seminar, participants should be able to analyse various influencing principles; plan for an influencing interaction and then execute the plan; and assess the impact of their influencing efforts on others.Jun 18, 9am-5pm, Sutton Place, Vancouver

TaxationAdvanced Personal Cross-Border IssuesIn this intermediate-level, full-day seminar, a variety of Canadian and US personal income tax matters will be discussed. The seminar will provide an in-depth look at the Canadian depar-ture tax rules; returning former residents of Canada; social security and payroll tax issues; withholding taxes on payments to non-residents of Canada pursuant to Regulation 105; and US estate and gift tax issues. Canadian tax-planning ideas designed to reduce Canadian income taxes for new immigrants will also be discussed.Jun 22, 9am-5pm, Sutton Place, Vancouver

Future Income Taxes and Disclosure: Bringing Clarity to a Common, Complex IssueThis seminar will help practitioners identify and analyse some common, complex future income tax issues that are often overlooked in the transition to IFRS.

The course is designed for intermediate to advanced-level practitioners at companies and professional firms who are required to work with, and disclose the impact of, future income taxes.Jul 5, 9am-5pm, Sutton Place, Vancouver

The CICA IN-DEPTH TAX COURSE is the most comprehensive tax training available in Canada – the training ground of choice for qualified professionals in public practice, industry, government or legal environments, who are committed to working in the taxation area.

This course is for the serious professional – 2 Group Study Sessions plus 2 In-residence Sessions over 2 years! Integrating the knowledge you gain with work experience between classroom sessions will give you a competitive advantage in the marketplace, and a head start on your way to specializing in taxation.

For general information regarding the CICA In-depth Tax Courses, contact Cathy Williams at 416-204-3378, or email, [email protected] n To find out if these courses are right for you,

contact Steve Johnston, CA, at 416-204-3332, or email, [email protected]

An integral part of and logical follow-up to the CICA In-depth Tax Course – Parts 1 & 2, building on the concepts learned in Corporate Reorganizations and International Tax