three rivers community action, inc. and … · space costs and utilities 63,858 29,976 175,842...

TRANSCRIPT

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES

FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31, 2016 AND 2015

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES TABLE OF CONTENTS

YEARS ENDED DECEMBER 31, 2016 AND 2015

INDEPENDENT AUDITORS’ REPORT 1

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION 3

CONSOLIDATED STATEMENTS OF ACTIVITIES AND CHANGES IN NET ASSETS 4

CONSOLIDATED STATEMENTS OF CASH FLOWS 5

CONSOLIDATED STATEMENTS OF FUNCTIONAL EXPENSES 6

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 8

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS 26

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE FOR EACH MAJOR FEDERAL PROGRAM AND REPORT ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY THE UNIFORM GUIDANCE 28

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS 30

NOTES TO SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS 31

SCHEDULE OF FINDINGS AND QUESTIONED COSTS 32

CliftonLarsonAllen LLPCLAconnect.com

(1)

INDEPENDENT AUDITORS’ REPORT

Board of Directors Three Rivers Community Action, Inc. and Subsidiaries Zumbrota, Minnesota Report on the Financial Statements

We have audited the accompanying consolidated financial statements of Three Rivers Community Action, Inc. and Subsidiaries (a nonprofit organization), which comprise the consolidated statements of financial position as of December 31, 2016 and 2015, and the related consolidated statements of activities and changes in net assets, cash flows, and functional expenses for the years then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We did not audit the financial statements of Waseca Leased Housing Association, LP, which statements reflect total assets of $2,044,804 and $2,135,632 as of December 31, 2016 and 2015, and total revenues of $349,294 and $341,710 for the periods then ended, respectively. Those statements were audited by other auditors, whose report has been furnished to us, and our opinion, insofar as it relates to the amounts included for Waseca Leased Housing Association, LP, is based solely on the report of the other auditors. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Organization’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Organization’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

Board of Directors Three Rivers Community Action, Inc. and Subsidiaries

(2)

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion

In our opinion, based on our audit and the report of the other auditors, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of Three Rivers Community Action, Inc. and Subsidiaries as of December 31, 2016 and 2015, and the changes in their net assets, cash flows, and functional expenses for the years then ended in accordance with accounting principles generally accepted in the United States of America. Other Matters

Other Information – Schedule of Expenditures of Federal Awards

Our audit was conducted for the purpose of forming an opinion on the consolidated financial statements as a whole. The schedule of expenditures of federal awards, as required by Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, is presented for purposes of additional analysis and is not a required part of the consolidated financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the consolidated financial statements. The information has been subjected to the auditing procedures applied in the audit of the consolidated financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the consolidated financial statements or to the consolidated financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated, in all material respects, in relation to the consolidated financial statements as a whole. Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated June 19, 2017, on our consideration of Three Rivers Community Action, Inc. and Subsidiaries’ internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the result of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Three Rivers Community Action, Inc. and Subsidiaries’ internal control over financial reporting and compliance.

CliftonLarsonAllen LLP

Austin, Minnesota June 19, 2017

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

DECEMBER 31, 2016 AND 2015

See accompanying Notes to Consolidated Financial Statements. (3)

2016 2015

ASSETSCURRENT ASSETS

Cash and Cash Equivalents 3,458,368$ 3,716,437$ Cash Restricted 2,484,028 1,765,543 Investments 63,103 59,076 Grants Receivable 726,421 613,143 Accounts Receivable 377,350 281,486 Contracts Receivable 278,542 32,679 Prepaid Expenses 146,444 121,377

TOTAL CURRENT ASSETS 7,534,256 6,589,741

NONCURRENT ASSETSContracts Receivable 806,450 656,897 Other Assets 439,195 758,128 Affordable Housing Projects 34,821,250 33,418,257 Property and Equipment 1,764,286 1,646,968

TOTAL NONCURRENT ASSETS 37,831,181 36,480,250

TOTAL ASSETS 45,365,437$ 43,069,991$

LIABILITIES AND NET ASSETSCURRENT LIABILITIES

Current Portion of Long-Term Debt 256,090$ 452,079$ Accounts Payable and Accrued Expenses 2,329,748 1,708,759 Grant Advances and Other Deferred Revenue 97,022 271,405

TOTAL CURRENT LIABILITIES 2,682,860 2,432,243

NONCURRENT LIABILITIESAccrued Interest - Affordable Housing Projects 492,091 454,781 Deferred Loan Revenue 175,079 140,063 Long-Term Debt and Affordable Housing Projects 18,482,767 17,591,194

TOTAL NONCURRENT LIABILITIES 19,149,937 18,186,038

TOTAL LIABILITIES 21,832,797 20,618,281

NET ASSETSMinority Interest in Combined Subsidiaries 15,195,392 14,857,902 Unrestricted 8,337,248 7,593,808

TOTAL NET ASSETS 23,532,640 22,451,710

TOTAL LIABILITIES AND NET ASSETS 45,365,437$ 43,069,991$

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF ACTIVITIES AND CHANGES IN NET ASSETS

YEARS ENDED DECEMBER 31, 2016 AND 2015

See accompanying Notes to Consolidated Financial Statements. (4)

2016 2015

UNRESTRICTED REVENUE Federal Grant Revenue 4,033,050$ 4,283,048$ State Grant Revenue 4,042,921 2,658,538 Other Grant Revenue 81,268 116,621 Other Program Revenue 2,346,715 1,744,831 Rental Income 3,332,853 3,196,133 Investment Income 52,412 18,722

TOTAL UNRESTRICTED REVENUE 13,889,219 12,017,893

EXPENSESProgram Services

Housing 7,161,569 7,095,102 Transportation 3,759,113 3,127,133 Early Childhood 2,209,195 1,794,622 Senior Services 323,880 282,895 Other Program 230,320 446,982

Management and General 304,941 386,213

TOTAL EXPENSES 13,989,018 13,132,947

TOTAL CHANGE IN NET ASSETS BEFORE MINORITY INTEREST (99,799) (1,115,054)

CHANGE IN MINORITY INTEREST IN AFFORDABLE HOUSING PROJECTS 843,239 1,076,202

TOTAL CHANGE IN NET ASSETS 743,440 (38,852)

BEGINNING OF YEAR NET ASSETS 7,593,808 7,632,660

END OF YEAR NET ASSETS 8,337,248$ 7,593,808$

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF CASH FLOWS

YEARS ENDED DECEMBER 31, 2016 AND 2015

See accompanying Notes to Consolidated Financial Statements. (5)

2016 2015

CASH FLOWS FROM OPERATING ACTIVITIESChange in Net Assets 743,440 (38,852)$ Adjustment to Reconcile Increase in Net Assets

to Net Cash Provided by Operating Activities:Minority Interest in Change in Net Assets (843,239) (1,076,202) Depreciation and Amortization 1,813,115 1,765,526 Gain on Property and Equipment - (31,290) Net (Appreciation) Depreciation in Market Value of Investments (2,510) 1,552 Change in Assets and Liabilities

Cash Restricted (718,485) 44,915 Grants Receivable (113,278) 461,507 Accounts Receivable (95,864) 2,137 Contracts Receivable (395,416) (109,205) Prepaid Expenses (25,067) 11,904 Other Assets 503,640 (324,100) Accounts Payable and Accrued Expenses 299,867 (444,037) Grant Advances and Other Deferred Revenue (139,367) 145,993 Accrued Interest 37,310 37,186

NET CASH PROVIDED BY OPERATING ACTIVITIES 1,064,146 447,034

CASH FLOWS FROM INVESTING ACTIVITIESPurchase of Property and Equipment (492,228) (232,428) Purchase of Investments (1,517) (1,827) Payments Toward Affordable Housing Projects (1,889,780) (86,887)

NET CASH USED BY INVESTING ACTIVITIES (2,383,525) (321,142)

CASH FLOWS FROM FINANCING ACTIVITIESProceeds from Long-Term Debt 132,056 632,289 Partner Contributions 1,175,528 4,767,227 Principal Payments on Long-Term Debt (251,475) (5,213,994) Partner Distributions and Syndication Fees 5,201 (81,069)

NET CASH PROVIDED BY FINANCING ACTIVITIES 1,061,310 104,453

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS (258,069) 230,345

CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR 3,716,437 3,486,092

CASH AND CASH EQUIVALENTS, END OF YEAR 3,458,368$ 3,716,437$

SUPPLEMENTAL DATA - INTEREST PAIDCash Paid During the Year for Interest 517,182$ 467,475$

SUPPLEMENTAL DATA - NON CASH ACTIVITYTax Credit Exchange Program Loan Forgiveness -$ 70,032$ Assumption of Mortgage 909,331$ -$

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENT OF FUNCTIONAL EXPENSES

YEAR ENDED DECEMBER 31, 2016

See accompanying Notes to Consolidated Financial Statements. (6)

TotalEarly Senior Other Program Management

Housing Transportation Childhood Services Programs Services and General Total

Direct Services 1,312,933$ 88,241$ 210,699$ 132,837$ 46,109$ 1,790,819$ -$ 1,790,819$ Salaries and Wages 1,034,648 1,802,276 1,074,123 102,004 93,891 4,106,942 206,389 4,313,331 Fringe Benefits 399,969 640,202 487,972 50,539 36,957 1,615,639 3,197 1,618,836 Training and Travel 53,271 59,260 75,881 6,669 5,397 200,478 13,903 214,381 Telephone and Technology 95,213 102,571 85,212 6,880 2,709 292,585 14,348 306,933 Office Supplies 64,179 23,955 53,461 14,456 2,240 158,291 8,461 166,752 Space Costs and Utilities 63,858 29,976 175,842 5,704 2,671 278,051 6,437 284,488 Equipment and Maintenance 174,018 1,294 - - - 175,312 700 176,012 Vehicle Repairs and Maintenance - 474,849 - - - 474,849 - 474,849 Other Costs 295,352 189,584 46,005 4,791 15,856 551,588 47,991 599,579 Housing Partnerships 1,712,741 - - - - 1,712,741 - 1,712,741 Depreciation and Amortization 1,438,205 346,905 - - 24,490 1,809,600 3,515 1,813,115 Interest 517,182 - - - - 517,182 - 517,182

Total 7,161,569$ 3,759,113$ 2,209,195$ 323,880$ 230,320$ 13,684,077$ 304,941$ 13,989,018$

Program Services Supporting Services

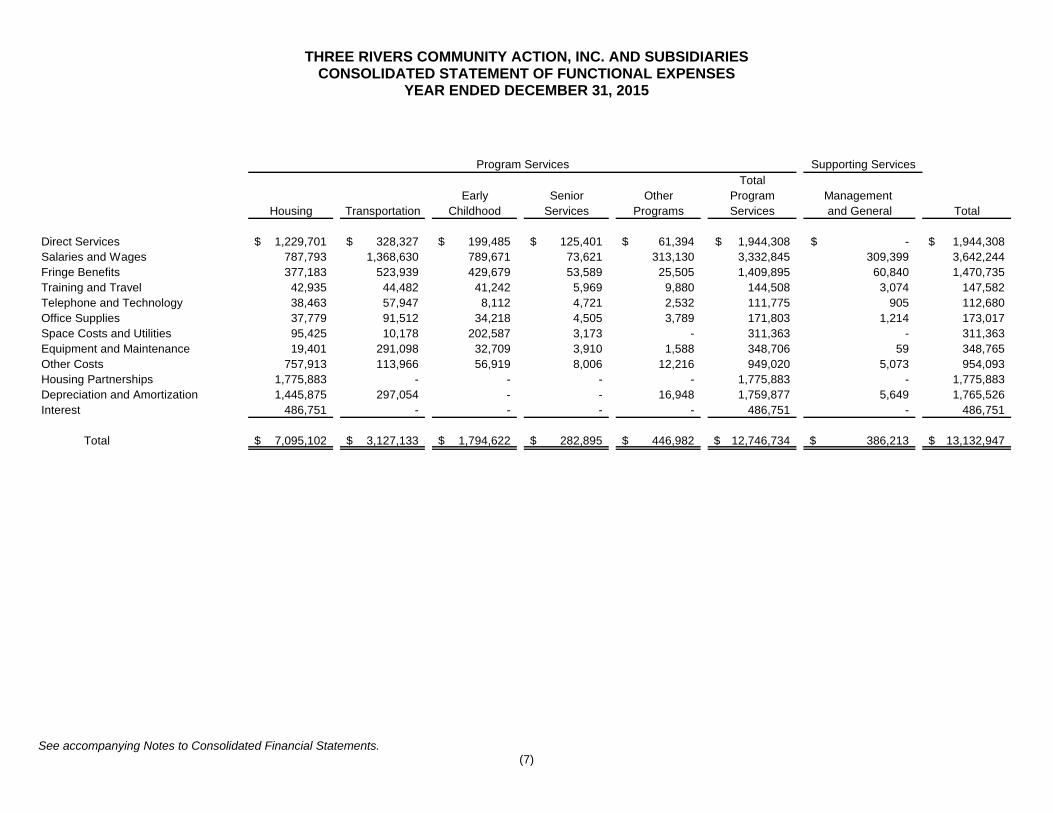

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENT OF FUNCTIONAL EXPENSES

YEAR ENDED DECEMBER 31, 2015

See accompanying Notes to Consolidated Financial Statements. (7)

TotalEarly Senior Other Program Management

Housing Transportation Childhood Services Programs Services and General Total

Direct Services 1,229,701$ 328,327$ 199,485$ 125,401$ 61,394$ 1,944,308$ -$ 1,944,308$ Salaries and Wages 787,793 1,368,630 789,671 73,621 313,130 3,332,845 309,399 3,642,244 Fringe Benefits 377,183 523,939 429,679 53,589 25,505 1,409,895 60,840 1,470,735 Training and Travel 42,935 44,482 41,242 5,969 9,880 144,508 3,074 147,582 Telephone and Technology 38,463 57,947 8,112 4,721 2,532 111,775 905 112,680 Office Supplies 37,779 91,512 34,218 4,505 3,789 171,803 1,214 173,017 Space Costs and Utilities 95,425 10,178 202,587 3,173 - 311,363 - 311,363 Equipment and Maintenance 19,401 291,098 32,709 3,910 1,588 348,706 59 348,765 Other Costs 757,913 113,966 56,919 8,006 12,216 949,020 5,073 954,093 Housing Partnerships 1,775,883 - - - - 1,775,883 - 1,775,883 Depreciation and Amortization 1,445,875 297,054 - - 16,948 1,759,877 5,649 1,765,526 Interest 486,751 - - - - 486,751 - 486,751

Total 7,095,102$ 3,127,133$ 1,794,622$ 282,895$ 446,982$ 12,746,734$ 386,213$ 13,132,947$

Program Services Supporting Services

(This page intentionally left blank)

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(8)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A. Nature of Activities Three Rivers Community Action, Inc. and Subsidiaries (Three Rivers) is a nonprofit corporation implementing the policies and procedures of the Office of Economic Opportunity by providing financial assistance to individuals and communities for the development, conduct, and administration of community action programs under Section 204 and 205 of Title II-A of the Economic Opportunity Act of 1964, as amended. Three Rivers’ major programs consist of Housing, Head Start, Transportation, Senior Services, and other community action programs.

B. Basis of Presentation The accompanying consolidated financial statements have been prepared on the accrual basis of accounting in accordance with accounting principles generally accepted in the United States of America. Revenues are recorded when earned and expenses are recorded when a liability is incurred. Contributions received are recorded as an increase in unrestricted, temporarily restricted, or permanently restricted support depending on the existence or nature of any donor restrictions. Accordingly, consolidated net assets of Three Rivers and changes therein are classified and reported as follows: Unrestricted Net Assets Unrestricted net assets are those resources over which Three Rivers has discretionary control. Designated amounts represent revenues that the Board of Directors has set aside for a particular purpose. Temporarily Restricted Net Assets Temporarily restricted net assets are those resources subject to donor imposed restrictions, which will be satisfied by actions of the Organization or passage of time. Permanently Restricted Net Assets Permanently restricted net assets are those resources subject to donor imposed restrictions that they be maintained permanently by Organization. There were no permanently restricted net assets. Contributions that are restricted by the donor are reported as increases in unrestricted net assets if the restrictions expire in the reporting period in which the revenue is recognized. All other donor-restricted contributions are reported as increases in temporarily restricted or permanently restricted net assets. When a restriction expires, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the consolidated statement of activities and changes in net assets as net assets released from restriction.

C. Use of Estimates The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect certain reported amounts and disclosures. Accordingly, actual results could differ from those estimates.

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(9)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

D. Cash and Cash Equivalents For purposes of the consolidated statement of cash flows, all highly liquid investments with a maturity of three months or less are considered to be cash equivalents.

E. Investments Three Rivers reports its investments in accordance with Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 820, Fair Value Measurements and Disclosures. ASC Topic 820 provides guidance for accounting for investments in certain equity securities and for all debt securities. The guidance prescribes that covered investments be reported in the statement of financial position at fair value with any realized or unrealized gains or losses reported in the consolidated statement of activities. Donated investments are recorded at fair value on the date of donation and thereafter carried in accordance with the above provisions.

F. Grants Receivable Grants receivable are due primarily from the federal government and other nonprofit organizations and arise primarily from Three Rivers grants and contracts with those agencies to administer various programs. As of December 31, 2016 and 2015 there were no uncollectible amounts. All accounts are reviewed annually for collectability.

G. Accounts Receivable Accounts receivable are stated at the amount management expects to collect from outstanding balances determined from contractual agreements. Management provides for probable uncollectible amounts through a provision for bad debt expense and an adjustment to a valuation allowance based on its assessment of the current status of individual receivables from grants, contracts and others. Balances that are still outstanding after management has used reasonable collection efforts are written off through a charge to the valuation allowance and a credit to the applicable accounts receivable. The allowance for doubtful accounts at December 31, 2016 and 2015 was estimated at $-0- and $-0-, respectively. Changes in the valuation allowance have not been material to the financial statements.

H. Contracts Receivable Contracts receivable arise from the sale of rehabilitated homes to low-income persons on a contract for deed basis. As part of the low-income housing rehabilitation program, contracts bear no interest and payment terms are based on the purchaser’s income. Contracts that are part of the MHFA Bridge Pilot Program bear market rate interest. Due to program restrictions, contracts for deed receivable are reported at outstanding principal. No allowance for estimated defaults is provided as each loan is secured by the property on a contract for deed allowing for immediate property repossession. Repossession only occurs if a contract falls into contractual default and a repayment plan cannot be agreed upon. Houses held for resale are repossessed homes from the low-income purchaser housing rehabilitation program. Houses held for resale are recorded at net realizable value.

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(10)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

I. Property and Equipment Furniture and equipment and building and improvements with an initial cost of $5,000 or more are reported on the consolidated statement of financial position and are stated at cost. Purchases of furniture and equipment of less than $5,000 are expensed immediately. Donated property and equipment are valued at fair value based on estimated value on date of donation. Depreciation is determined using the straight-line method over five to seven years for furniture and equipment and generally 25 years for the building. Upon retirement or other disposition, the cost and related accumulated depreciation of disposed assets are removed from the accounts and the resulting gain or loss is recognized in income. Repairs and maintenance are charged to expense as incurred. Renewals and improvements that extend the useful lives of assets are capitalized and depreciated over future periods.

J. Other Assets Other Assets are investments, valued at cost, in future affordable housing projects and various reserves for affordable housing projects as required by certain loan covenants and restricted by funding source agreements.

K. Affordable Housing Projects and Other Assets - Principles of Consolidation Three Rivers has consolidated all limited partnerships and limited liability companies in which Three Rivers controls as the general partner or managing member. These financial statements consolidate the statements of Wazuweeta Woods Limited Partnership, Waseca Leased Housing Associates Limited Partnership, Eagle Ridge Apartments Limited Partnership, Harvest Ridge Townhomes Limited Partnership, Trailside Apartments of Albert Lea Limited Partnership, Bridge Run Townhomes Limited Liability Company, Spring Creek Townhomes Limited Partnership, Prairiewood Townhomes Limited Partnership, and North and South Oak Apartments Limited Partnership (collectively, the Organization). Inter-organization balances and transactions have been eliminated in the combination. Hayfield Greens Partnership and Opportunity Homes Limited Liability Company continue to be accounted for using the equity method of accounting for investments. Affordable housing projects owned solely by Three Rivers, Northern Oaks Townhomes, Clover Patch Apartments, Southside Apartments, Deerwood Lane Townhomes, and Northbridge Apartments of Albert Lea are valued at cost. Affordable housing projects that are interests in partnerships where Three Rivers and all partners have substantive participating rights, Hayfield Greens Partnership and Opportunity Homes Limited Liability Company, continue to be accounted for using the equity method of accounting based on amounts reported on calendar year ended Schedule K-1 (Form 1065) partnership tax returns.

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(11)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

K. Affordable Housing Projects and Other Assets - Principles of Consolidation (Continued) NORTHERN OAKS: Three Rivers has completed construction on a larger family affordable rental housing project in Northfield, Minnesota (Northern Oaks). Northern Oaks resulted in the development of eight units (two triplexes and one duplex) of large family affordable housing. The units were completed for occupancy May 1998. Northern Oaks was designed to address a critical housing shortage in the City of Northfield for large families earning less than 50 percent of area median income based on household. Four units have three bedrooms, four units have four bedrooms, and one unit is modified to accommodate handicapped individuals. Northern Oaks is owned solely by Three Rivers and is valued at cost. HAYFIELD GREENS PARTNERSHIP: Three Rivers has entered into a general partnership agreement with James J. and Kristin K. Fiebiger (HAYFIELD GREENS) to construct, develop, acquire, hold for investment, lease, and sell a 24-unit residential apartment development located in Hayfield, Minnesota. Three Rivers owns 50 percent of HAYFIELD GREENS and it continues to be accounted for using the equity method of accounting due to the substantial participating rights of all partners. WAZUWEETA WOODS, LP: Three Rivers has entered into a limited partnership agreement with Douglas A. Amundson and Ron Carlsen (WAZUWEETA WOODS) to construct, develop, acquire, hold for investment, lease, and sell a 24-unit residential apartment development located in Pine Island, Minnesota. Three Rivers serves as the general partner with 1 percent ownership. This partnership is reported as a consolidated subsidiary of Three Rivers due to the control Three Rivers has over the partnership as the partnership’s general partner. WASECA LEASED HOUSING ASSOCIATES, LP: Three Rivers has entered into a limited partnership agreement with Waseca Woods, LLC, American Tax Credit Corporate Fund XIV Limited Partnership and Protech Development Corporation to own, develop, lease, and operate five (5) buildings totaling a 33-unit affordable housing apartment rental complex also known as Charter Oaks Apartments (WASECA) located in Waseca, Minnesota. Three Rivers serves as co-managing general partner with .005 percent ownership. This partnership is reported as a consolidated subsidiary of Three Rivers due to the control Three Rivers has over the partnership as the partnership’s co-managing general partner. OPPORTUNITY HOMES, LLC: Three Rivers has entered into a limited partnership agreement with Ron Carlsen (OPPORTUNITY HOMES) to construct, develop, acquire, hold for investment, lease, and sell five (5) residential homes located in Kasson, Rochester and Faribault, Minnesota. Three Rivers owns 50 percent of OPPORTUNITY HOMES and it continues to be accounted for using the equity method of accounting due to the substantial participating rights of all partners.

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(12)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

K. Affordable Housing Projects and Other Assets - Principles of Consolidation (Continued) EAGLE RIDGE APARTMENTS, LP: Three Rivers has entered into a limited partnership agreement with NDC Corporate Equity Fund VI, LP (EAGLE RIDGE) to construct, develop, acquire, hold for investment, lease, and sell a 48-unit residential apartment development located in Red Wing, Minnesota. Three Rivers serves as general partner with .01 percent ownership. This partnership is reported as a consolidated subsidiary of Three Rivers due to the control Three Rivers has over the partnership as the partnership’s general partner. HARVEST RIDGE TOWNHOMES, LP: Three Rivers has entered into a limited partnership agreement with NDC Corporate Equity Fund VI, LP (HARVEST RIDGE) to construct, develop, acquire, hold for investment, lease, and sell a 20-unit residential townhomes development located in Plainview, Minnesota. Three Rivers serves as general partner with .01 percent ownership. This partnership is reported as a consolidated subsidiary of Three Rivers due to the control Three Rivers has over the partnership as the partnership’s general partner. CLOVER PATCH: Three Rivers has completed acquisition and rehabilitation of a multi-family affordable rental housing project financed by Rural Development in St. Charles, Minnesota (Clover Patch). Clover Patch resulted in the development of 32 affordable units. Clover Patch is owned solely by Three Rivers and is valued at cost. TRAILSIDE APARTMENTS, LP: Three Rivers has entered into a limited partnership agreement with NDC Corporate Equity Fund VII, LP (TRAILSIDE) to construct, develop, acquire, hold for investment, lease, and sell a 110-unit residential rental housing development located in Albert Lea, Minnesota. Three Rivers serves as general partner with .01 percent ownership. This partnership is reported as a consolidated subsidiary of Three Rivers due to the control Three Rivers has over the partnership as the partnership’s general partner. SOUTHSIDE APARTMENTS: Three Rivers has completed acquisition and rehabilitation of a multi-family affordable housing project financed by Rural Development in Lonsdale, Minnesota (Southside). Southside resulted in the development of 12 affordable units. Southside is owned solely by Three Rivers and is valued at cost. BRIDGE RUN TOWNHOMES, LLC: Three Rivers organized a limited liability company (LLC) to acquire, rehabilitate, own, maintain, and operate an 18-unit rental housing project located in Cannon Falls, Minnesota. Three Rivers is the single member of the LLC. Initial rentals occurred in November 2010. DEERWOOD LANE TOWNHOMES: Three Rivers has completed acquisition of a multi-family market rate housing project in Faribault, Minnesota (Deerwood). Deerwood resulted in the development of four market rate units. Deerwood is owned solely by Three Rivers and is valued at cost.

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(13)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

K. Affordable Housing Projects and Other Assets - Principles of Consolidation (Continued) SPRING CREEK TOWNHOMES, LP: Three Rivers has entered into a limited partnership agreement with NDC Corporate Equity Fund X, LP (SPRING CREEK) to construct, develop, acquire, hold for investment, lease, and sell a 28-unit residential rental housing development located in Northfield, Minnesota. Three Rivers serves as general partner with .01 percent ownership. This partnership is reported as a consolidated subsidiary of Three Rivers due to the control Three Rivers has over the partnership as the partnership’s general partner. NORTHBRIDGE, LLC: Three Rivers organized a limited liability company (LLC) to acquire, rehabilitate, own, maintain, and operate a 48-unit rental housing project located in Albert Lea, Minnesota. Three Rivers is the single member of the LLC. PRAIRIEWOOD TOWNHOMES, LP: Three Rivers organized a limited liability company (LLC) Prairiewood Townhomes GP LLC and entered into a limited partnership agreement with MEF Multi-State LIHTC Fund 1 LLLP (PRAIRIEWOOD) to construct, develop, acquire, hold for investment, lease, and sell a 30-unit residential rental housing development located in Faribault, Minnesota. Prairiewood Townhomes GP LLC serves as general partner with .01 percent ownership. This partnership is reported as a consolidated subsidiary of Three Rivers due to the control Three Rivers has over the partnership as the partnership’s general partner. NORTH AND SOUTH OAK APARTMENTS, LP: Three Rivers organized a limited liability company (LLC) North and South Oak GP LLC and entered into a limited liability partnership agreement with Cinnaire fund for housing Limited Partnership 31 (NORTH AND SOUTH OAK) to acquire rehabilitate, own, maintain, and operate a 43-unit residential rental housing development located in Northfield, Minnesota. North and South Oak GP LLC serves as general partner with .01 percent ownership. This partnership is reported as a consolidated subsidiary of Three Rivers due to the control Three Rivers has over the partnership as the partnership’s general partner.

L. Income Taxes Three Rivers Community Action, Inc. and Subsidiaries is exempt from income taxes under Section 501(c)(3) of the Internal Revenue Code. Three Rivers adopted the provisions of ASC Topic 740, Income Taxes, relating to unrecognized tax benefits on April 1, 2009. The adoption of these provisions did not result in an increase of recognized tax liabilities as Three Rivers believes its filing positions would be sustained on audit and does not anticipate any adjustments that would result in a material adverse effect on Three Rivers financial condition, results of operations or cash flows. Three Rivers recognizes interest accrued related to unrecognized tax benefits, if any, in interest expense and penalties in operating expenses. During the years ended December 31, 2016 and 2015, Three Rivers did not recognize any interest or penalties.

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(14)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

M. Affordable Housing Project, Notes, and Mortgages Three Rivers does not discount noninterest or low interest loans for affordable housing projects due to legal restrictions prescribed by governmental agencies.

N. Amortization Fees paid to Minnesota Housing Finance Agency are amortized over a 15-year period using the straight-line method.

O. Functional Allocation of Expenses The costs of providing the Organization’s various programs have been summarized on a functional basis. Accordingly, certain costs have been allocated among the programs and supporting services benefited.

P. Concentration of Credit Risk Financial instruments that potentially subject Three Rivers to concentrations of credit risk consist principally of temporary cash investments. Three Rivers places its temporary cash investments with financial institutions and limits the credit exposure to any one financial institution by requiring specific collateral pledges of investment quality securities, (U.S. government or municipalities) for balances in excess of FDIC insurance limits. As of December 31, 2016 and 2015, Three Rivers had obtained collateral pledges of these securities in excess of bank balance, and thereby limited credit exposure.

Q. Subsequent Events Three Rivers evaluated subsequent events, in accordance with FASB ASC Topic 855, Subsequent Events, through June 19, 2017, the date the financial statements were available to be issued.

R. Change in Accounting Principle Three Rivers Community Action, Inc. has adopted the accounting guidance in FASB Accounting Standards Update (ASU) No. 2015-03, Interest – Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs. ASU 2015-03 requires organizations to present debt issuance costs as a direct deduction from the face amount of the related borrowings, amortize debt issuance costs using the effective interest method over the life of the debt, and record the amortization as a component of interest expense. The effect of adopting the new standard decreased the debt issuance costs asset to zero and decreased the long-term debt liability by $254,700 as of January 1, 2015. The adoption of the standard had no effect on previously reported net assets. The ASU is effective for fiscal years beginning after December 15, 2015, with early adoption permitted. The ASU is retrospectively applied. Three Rivers has elected to adopt this change in accounting principle as of January 1, 2015.

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(15)

NOTE 2 FAIR VALUE INVESTMENTS

Three Rivers has adopted ASC Topic 820, Fair Value Measurements and Disclosures. ASC Topic 820 applies to reported balances that are required or permitted to be measured at fair value under an existing accounting pronouncement. It emphasizes that fair value is a market-based measurement, not an entity-specific measurement. Therefore, a fair value measurement should be determined based on the assumptions that the market participants would use in pricing the asset or liability and establishes a fair value hierarchy. The fair value hierarchy consists of three levels of inputs that may be used to measure fair value, as follows:

Level 1 – Inputs that utilize quoted prices (unadjusted) in active markets for identical assets or liabilities that Three Rivers has the ability to access. Level 2 – Inputs that included quoted prices for similar assets and liabilities in active markets and inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument. Fair values for these instruments are estimated using pricing models, quoted prices of securities with similar characteristics, or discounted cash flows. Level 3 – Inputs that are unobservable inputs for the assets or liability, which are typically base on an entity’s own assumptions, as there is little, if any, related market activity.

In instances where the determination of fair value measurement is based on inputs from different levels of the fair value hierarchy, the level in the fair value hierarchy within which the entire fair value measurement falls into is based on the lowest level input that is significant to the fair value measurement in its entity. Three Rivers also has adopted ASC Topic 825, Financial Instruments. ASC Topic 825 allows entities the irrevocable option to elect fair value for the initial and subsequent measurement for certain financial assets and liabilities that are not otherwise required to be stated at fair value, on a contract-by-contract basis. Three Rivers has not elected to change the measurement of any existing financial instruments at fair value. However, Three Rivers may elect to measure newly acquired financial instruments at fair value in the future. Financial assets and liabilities recorded at fair value on a recurring basis are as follows at December 31:

2016 2015Assets, Investments Level 1 63,103$ 59,076$ Level 2 - - Level 3 - -

Total 63,103$ 59,076$

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(16)

NOTE 3 CASH RESTRICTED

Cash restricted consisted of the following at December 31:

2016 2015Operating Reserve 1,036,988$ 900,181$ Replacement Cost Reserve 694,519 396,862 Tenant Security Deposits 253,062 226,943 Residual Receipts Reserve 112,975 103,575 Development Cost Escrow 322,201 97,323 Real Estate Tax and Insurance Escrow 64,283 40,659

Total 2,484,028$ 1,765,543$

NOTE 4 CONTRACTS RECEIVABLE

Three Rivers purchased dilapidated houses, rehabilitated and later sold the houses to eligible families on contracts for deed at 0 percent interest. Three Rivers built a townhome and later sold to an eligible family on a contract for deed at 4.5 percent interest. Three Rivers has a pilot program where they are purchasing single family homes in Rochester, Minnesota, rehabbing them, and selling them on a three year contract for deed at a 7.25 percent interest. Contracts receivable are as follows:

2016 2015Contracts Receivable 1,084,992$ 689,576$ Less Current Portion (278,542) (32,679)

Total Noncurrent Portion 806,450$ 656,897$

Estimated future collections are as follows:

2017 278,542$ 2018 36,938 2019 437,482 2020 25,872 2021 25,872

2022 and Thereafter 280,286

Total 1,084,992$

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(17)

NOTE 5 PROPERTY AND EQUIPMENT

2016 2015Furniture and Equipment 2,762,487$ 2,629,237$ Building and Improvements 1,310,287 1,302,762 Land 41,032 41,032

4,113,806 3,973,031

Accumulated Depreciation 2,349,520 2,326,063

Total 1,764,286$ 1,646,968$

Property, equipment, and furniture acquired are owned by Three Rivers while used in the program for which it was purchased or in other future authorized programs. However, the funding sources have a reversionary interest in equipment purchased with grant funds and its disposition, as well as the ownership of any proceeds thereof, is subject to funding source regulations. Depreciation on parent property and equipment was $370,047 and $319,560 for the years ended December 31, 2016 and 2015, respectively.

NOTE 6 OTHER ASSETS

Other Assets consist of investments in future affordable housing projects and various reserves for affordable housing projects as required by certain loan covenants and restricted by funding source agreements as follows:

2016 2015Bridge Loan Program -$ 324,100$ Bridge Run 3,684 4,100 Eagle Ridge 6,029 7,792 Harvest Ridge 3,366 4,394 North and South Oak 19,391 - Northbridge 2,231 2,612 Prairiewood 36,299 39,325 Rochester Multi-Family Project 195,122 195,122 Scattered Single Family Housing Developments 126,000 126,000 Spring Creek 35,113 40,315 Trailside Apartments 11,960 14,368

Total 439,195$ 758,128$

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(18)

NOTE 7 AFFORDABLE HOUSING PROJECTS

Affordable Housing projects were comprised of the following at December 31:

2016 2015

Land 4,524,197$ 4,218,038$ Building and Improvements 39,675,709 37,166,425 Furniture and Equipment 2,694,881 2,687,342

46,894,787 44,071,805 Accumulated Depreciation (12,073,537) (10,653,548)

Total 34,821,250$ 33,418,257$

Depreciation on affordable housing projects was $1,419,994 and $1,403,982 for the years ended December 31, 2016 and 2015, respectively.

NOTE 8 LONG-TERM DEBT AND AFFORDABLE HOUSING PROJECTS

Affordable Housing Projects long-term debt consists of the following at December 31:

2016 2015Northern Oaks

MHFA, Home Targeted Program, deferred loan, proceeds used for Northern Oaks purchase. This loan is to be forgiven if all conditions are met, May 1, 2018. 320,000$ 320,000$

Northfield Community National Bank, mortgage payable, secured by Northern Oaks, payable in monthly installments of $1,065 including interest at 6.75%, final payment due December 3, 2022.

35,846 45,831

GMHF, mortgage payable, secured by Northern Oaks, payable on December 4, 2022, including 0% interest. 60,000 60,000

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(19)

NOTE 8 LONG-TERM DEBT AND AFFORDABLE HOUSING PROJECTS (CONTINUED)

2016 2015Wazuweeta Woods

MHFA, mortgage payable, secured by Wazuweeta Woods, personally guaranteed by two limited partners, payable in monthly installments of $5,480, including interest at 5.75%, final payment due August 2032.

695,566$ 720,549$

MHFA, Challenge Program, secured by Wazuweeta Woods, payable on July 1, 2032, including 0% interest. 567,701 567,701

GMHF, mortgage payable, secured by Wazuweeta Woods, payable on July 1, 2032, including 0% interest. 360,000 360,000

First Homes, mortgage payable, secured by Wazuweeta Woods, payable July 1, 2032, including 0% interest. 388,000 388,000

Waseca Housing

Glaser Financial Group, Inc., mortgage payable, secured by Charter Oaks, payable in monthly installments of $6,769 from December 1, 2003 to December 1, 2022 and monthly installments of $6,084.68 from January 1, 2023 until final payment due January 1, 2042, including interest at 8.05%.

819,958 834,535

GMHF, mortgage payable, secured by Charter Oaks, payable on January 1, 2042, including 0% interest. 280,000 280,000

Eagle Ridge

MHFA, mortgage payable, secured by Eagle Ridge, payable in monthly installments of $5,165, including interest at 5.75%, final payment due November 1, 2035. 715,428 735,633

MHFA, mortgage payable, secured by Eagle Ridge, payable on November 1, 2035, including interest at 1%. 456,670 456,670

GMHF, mortgage payable, secured by Eagle Ridge, payable on September 16, 2034, including interest at 1%. 665,000 665,000

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(20)

NOTE 8 LONG-TERM DEBT AND AFFORDABLE HOUSING PROJECTS (CONTINUED)

2016 2015

Harvest Ridge

GMHF, mortgage payable, secured by Harvest Ridge, payable on June 8, 2035, including interest at 1%. 400,000$ 400,000$

First Homes, mortgage payable, secured by Harvest Ridge, payable June 8, 2035, including interest at 1%. 300,000 300,000

MHFA, mortgage payable, secured by Harvest Ridge, payable March 1, 2036, including interest at 1%. 262,031 262,031

MHFA, mortgage payable, secured by Harvest Ridge, payable in monthly installments of $1,128, including interest at 6.05%, final payment due March 1, 2036. 155,185 159,206

Clover Patch

USDA, Rural Development, mortgage payable, secured by Clover Patch Apartments purchase, payable in monthly installments of $5,113.80 including interest at 6%, final payment due February 25, 2035.

882,260 890,422

MHFA, Preservation Affordable Rental Investment Fund Program mortgage payable, secured by Clover Patch Apartments, payable in full on February 25, 2035, including 0% interest. 350,000 350,000

Greater Minnesota Housing Fund, mortgage payable, secured by Clover Patch Apartments, payable in full on June 30, 2035, including 0% interest. 120,000 120,000

First Homes Properties, mortgage payable, secured by Clover Patch Apartments, payable in full on June 30, 2035, including 0% interest. 50,000 50,000

Trailside

Minnwest Bank, M.V., mortgage payable, secured by Trailside Apartments, payable in monthly installments of $12,850 including interest at 7.48%, final payment due December 10, 2024. 1,624,669 1,654,112

MHFA, HOME, mortgage payable, secured by Trailside Apartments, payable in full on December 19, 2036, including interest at 1%. 1,184,921 1,184,921

GMHF, mortgage payable, secured by Trailside Apartments, payable on December 19, 2036, including interest at 1%. 400,000 400,000

SWMHP, mortgage payable, secured by Trailside Apartments, payable on December 19, 2025, including interest at 1%. 50,000 50,000

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(21)

NOTE 8 LONG-TERM DEBT AND AFFORDABLE HOUSING PROJECTS (CONTINUED)

2016 2015

Southside Apartments

USDA, Rural Development, mortgage payable, secured by Southside Apartments purchase, payable in monthly installments of $821 including interest at 4%, final payment due March 1, 2049. 146,805$ 148,995$

MHFA, HOME, Preservation Affordable Rental Investment Fund Program Loan, secured by Southside Apartments, payable in full on December 9, 2048, including 0% interest. 175,000 175,000

GMHF, mortgage payable, secured by Southside Apartments, payable on December 9, 2048, including 0% interest. 175,000 175,000

SWMHP, mortgage payable, secured by Southside Apartments, payable on December 9, 2048, including 0% interest. 26,000 16,000

Bridge Run Townhomes, LLC

MHFA, mortgage payable, secured by Bridge Run Townhomes, LLC, payable on November 4, 2040, including 0% interest.

360,000 360,000

MHFA, exchange program loan, secured by Bridge Run Townhomes, LLC, payable on December 4, 2025, including 0% interest. 700,314 770,346

MHFA, mortgage payable, secured by Bridge Run Townhomes, LLC, payable on November 4, 2040, including 0% interest.

252,000 252,000

MHFA, mortgage payable, secured by Bridge Run Townhomes, payable in monthly installments of $2,784, including interest at 5.5%, final payment due October 1, 2041. 451,877 460,178

GMHF, mortgage payable, secured by Bridge Run Townhomes, LLC, payable on November 4, 2040, including 0% interest.

60,000 60,000

SWMHP, mortgage payable, secured by Bridge Run Townhomes, LLC, payable on November 4, 2040, including 0% interest. 18,000 18,000

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(22)

NOTE 8 LONG-TERM DEBT AND AFFORDABLE HOUSING PROJECTS (CONTINUED)

2016 2015

Northbridge Apartments

USDA, Rural Development, mortgage payable, secured by Northbridge Apartments, payable in monthly installments of $4,392 including interest at 3.125%, final payment due May 31, 2043. 1,290,486$ 1,302,659$

MHFA, PARIF mortgage payable, secured by Northbridge Apartments, payable on May 31, 2043, including 0% interest. 480,250 480,250

MHFA, HOME mortgage payable, secured by Northbridge Apartments, payable on May 31, 2043, including 0% interest. 1,000,000 1,000,000

GMHF, deferred loan, secured by Northbridge Apartments, payable on May 31, 2043, including 0% interest. 200,000 200,000

GMHF, mortgage payable, secured by Northbridge Apartments, payable in monthly installments of $759 including interest at 2%, final payment due May 31, 2033. 131,025 137,358

Spring Creek Townhomes, LP

Mortgage note, First National Bank of Northfield, payable in monthly installments of $2,892 including interest at 4.5% collateralized by all property and equipment, balance due January 2029. 494,611 506,272

Prairiewood Townhomes, LP

GMHF, mortgage payable, secured by Prairiewood Townhomes, payable in monthly installments of $1,678.74, including interest at 6%, final payment due May 2031. 272,482 275,889

North and South Oak, LP

USDA, Rural Development, mortgage payable, secured by North & South Oak Apartments payable in monthly installments of $2,867.41 including interest at 2.875%, final payment due October 3, 2046. 909,331 -

Bridge Pilot Program

GMHF, mortgage payable, secured by 1014 10th Avenue NW, Rochester, MN, payable in monthly installments of $232.93, including interest at 3%, final payment due December 3, 2018. 39,615 41,100

GMHF, note payable, secured by 815 11th Street NW, Rochester, MN, interest accrues on the principal balance at 3% per annum through August 7, 2016, when the principal balance and accrued interest are due. 40,914 42,000

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(23)

NOTE 8 LONG-TERM DEBT AND AFFORDABLE HOUSING PROJECTS (CONTINUED)

2016 2015

Bridge Pilot Program (Continued)GMHF, note payable, secured by 1412 15th Avenue NE, Rochester, MN, interest accrues on the principal balance at 3% per annum through November 13, 2016, when the principal balance and accrued interest are due. 47,578$ 48,300$

GMHF, note payable, secured by 1709 18th Ave NE, Rochester, MN, interest accrues on the principal balance at 3% per annum throgh November 13, 2019, when the pincipal balance and accrued interest are due. 55,000 -

First Alliance Credit Union, mortgage payable, secured by 1014 10th Avenue NW, Rochester, MN, payable in monthly installments of $494.97, including interest at 5%, final payment due December 3, 2018. 72,722 74,987

First Alliance Credit Union, mortgage payable, secured by 1014 10th Avenue NW, Rochester, MN, payable in monthly installments of $494.97, including interest at 5%, final payment due December 3, 2018. 73,282 75,000

First Alliance Credit Union, mortgage payable, secured by 1014 10th Avenue NW, Rochester, MN, payable in monthly installments of $494.97, including interest at 5%, final payment due December 3, 2018. 73,771 75,000

First Alliance Credit Union, mortgage payable, secured by 1709 18th Ave NW, Rochester, MN, payable in monthly installments of $494.64, including interest at 5%, final payment due April 15, 2021. 75,000 -

Rochester Multi Family

GMHF, mortgage payable, secured by 703 and 707 4th Street, Rochester, MN, payable September 1, 2016, including interest at 0%. - 195,122

Plainview Scattered SitesGMHF, mortgage payable, secured by seven single family lots in Plainview, MN, payable upon sale of lots, including interest at 0% 126,000 126,000

Other Long-Term Debt

Marco Technologies, capital copier lease 43,767 -

Total Long-Term Debt 18,934,065 18,270,067 Less: Unamortized Debt Issuance Costs (195,208) (226,794) g

Costs 18,738,857 18,043,273 Less Current Maturities (256,090) (452,079)

Long-Term Debt 18,482,767$ 17,591,194$

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(24)

NOTE 8 LONG-TERM DEBT AND AFFORDABLE HOUSING PROJECTS (CONTINUED)

Estimated future long-term debt maturities are as follows:

Year Ended December 31, Amount2017 256,090$ 2018 587,427 2019 278,498 2020 278,685 2021 586,812

2022 and Thereafter 16,946,553 Total 18,934,065$

Interest expense paid for the years ended December 31, 2016 and 2015 was $517,182 and $467,475, respectively, as follows:

2016 2015Three Rivers 66,439$ 54,432$ Bridge Run 825 25,640 Eagle Ridge 116,310 43,010 Harvest Ridge 28,754 9,906 North and South Oak 6,205 - Prairiewood 17,277 74,106 Spring Creek 23,819 23,428 Trailside 143,120 126,884 Waseca Housing 67,507 67,775 Wazuweeta 46,926 42,294

Total 517,182$ 467,475$

NOTE 9 OPERATING LEASES

Three Rivers is subject to operating leases covering primarily premises and office equipment with lease periods expiring between 2016 and 2021. Lease expense was $348,577 and $147,033 for the years ended December 31, 2016 and 2015, respectively. Minimum future lease obligations are as follows:

Year Ended December 31, Amount2017 262,104$ 2018 186,712 2019 22,510 2020 17,520 2021 17,520 Total 506,366$

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

(25)

NOTE 10 RETIREMENT PLANS

Three Rivers maintains a defined contribution retirement plan covering substantially all employees. Three Rivers’ contributions to the Plan are based on employee contributions and length of service. This Plan is intended to qualify under Internal Revenue Code Section 403(b). Three Rivers contributed $142,252 and $134,763 to the Plan for the years ended December 31, 2016 and 2015, respectively.

NOTE 11 DONATED SERVICES

Each program is responsible for keeping records to support the in kind contribution claimed. To calculate the value of services, space, or material donated, a rate at or below current market rate is used. A substantial number of unpaid volunteers have made significant contributions of their time. The value of this contributed time is at a fair value wage plus fringe and is reported as revenue and expense in the period in which the volunteer hours are provided. Volunteer hours are not recorded in the audited financial statements.

NOTE 12 CONTINGENCIES

Three Rivers provides a self-insured short-term disability program to certain qualifying employees, which may provide 67 percent of an employee’s weekly earnings up to a maximum of 12 weeks. Under this program the historical average annual payout has been $8,229. Three Rivers paid amounts $13,051 and $16,735 out in benefits under this program for the years ended December 31, 2016 and 2015, respectively.

NOTE 13 SUBSEQUENT EVENTS

Three Rivers has received $1.3 million in grant funds to construct an administrative facility to increase transit activity. The grant requires a twenty percent local match by Three Rivers.

CliftonLarsonAllen LLPCLAconnect.com

(26)

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER

FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN

ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS Board of Directors Three Rivers Community Action, Inc. and Subsidiaries Zumbrota, Minnesota We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of Three Rivers Community Action, Inc. and Subsidiaries, which comprise the consolidated statements of financial position as of December 31, 2016 and 2015, and the related consolidated statements of activities and changes in net assets, cash flows, and functional expenses for the years then ended, and the related notes to the consolidated financial statements, and have issued our report thereon dated June 19, 2017. Internal Control over Financial Reporting

In planning and performing our audit of the consolidated financial statements, we considered Three Rivers Community Action, Inc. and Subsidiaries’ internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the consolidated financial statements, but not for the purpose of expressing an opinion on the effectiveness of Three Rivers Community Action, Inc. and Subsidiaries’ internal control. Accordingly, we do not express an opinion on the effectiveness of Three Rivers Community Action, Inc. and Subsidiaries’ internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the Organization’s consolidated financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

Board of Directors Three Rivers Community Action, Inc. and Subsidiaries

(27)

Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be a material weakness. However, material weaknesses may exist that have not been identified. Compliance and Other Matters

As part of obtaining reasonable assurance about whether Three Rivers Community Action, Inc. and Subsidiaries’ financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the result of that testing, and not to provide an opinion on the effectiveness of the Organization’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Organization’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

CliftonLarsonAllen LLP Austin, Minnesota June 19, 2017

CliftonLarsonAllen LLPCLAconnect.com

(28)

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE FOR EACH MAJOR

FEDERAL PROGRAM AND REPORT ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY THE UNIFORM GUIDANCE

Board of Directors Three Rivers Community Action, Inc. and Subsidiaries Zumbrota, Minnesota Report on Compliance for Each Major Federal Program

We have audited Three Rivers Community Action, Inc. and Subsidiaries’ compliance with the types of compliance requirements described in the OMB Compliance Supplement that could have a direct and material effect on each of Three Rivers Community Action, Inc. and Subsidiaries’ major federal programs for the year ended December 31, 2016. Three Rivers Community Action, Inc. and Subsidiaries’ major federal programs are identified in the summary of auditors’ results section of the accompanying schedule of findings and questioned costs. Management’s Responsibility

Management is responsible for compliance with the requirements of laws, regulations, contracts, and grants applicable to its federal programs. Auditors’ Responsibility

Our responsibility is to express an opinion on compliance for each of Three Rivers Community Action, Inc. and Subsidiaries’ major federal programs based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and the audit requirements of Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance). Those standards and the Uniform Guidance require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about Three Rivers Community Action, Inc. and Subsidiaries’ compliance with those requirements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion on compliance for each major federal program. However, our audit does not provide a legal determination of Three Rivers Community Action, Inc. and Subsidiaries’ compliance.

Board of Directors Three Rivers Community Action, Inc. and Subsidiaries

(29)

Opinion on Each Major Federal Program

In our opinion, Three Rivers Community Action, Inc. and Subsidiaries complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs for the year ended December 31, 2016. Report on Internal Control Over Compliance

Management of Three Rivers Community Action, Inc. and Subsidiaries is responsible for establishing and maintaining effective internal control over compliance with the types of compliance requirements referred to above. In planning and performing our audit of compliance, we considered Three Rivers Community Action, Inc. and Subsidiaries’ internal control over compliance with the types of requirements that could have a direct and material effect on each major federal program to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for each major federal program and to test and report on internal control over compliance in accordance with the Uniform Guidance, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of Three Rivers Community Action, Inc. and Subsidiaries’ internal control over compliance. A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance. Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies and therefore, material weaknesses or significant deficiencies may exist that were not identified. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses. The purpose of this report on internal control over compliance is solely to describe the scope of our testing of internal control over compliance and the result of that testing based on the requirements of the Uniform Guidance. Accordingly, this report is not suitable for any other purpose.

CliftonLarsonAllen LLP Austin, Minnesota June 19, 2017

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

YEAR ENDED DECEMBER 31, 2016

(30)

Federal Agency or Passed Federal

Federal Pass-through CFDA Pass-through Through to Disbursements/Fund # Grantor Grantor Program Title Number Number Subrecipients Expenditures

600 USDA RD Clover Patch Rural Rental Housing Loan 10.415 002-001 486,691$ *600 Clover Patch Rural Rental Housing Loan 10.415 020-003 403,731 *601 Southside Rural Rental Housing Loan 10.415 039-003 148,995 *603 Northbridge Rural Rental Housing Loan 10.415 012-001 1,302,659 *

2,342,076

115 & 116 MDE CACFP 10.558 8-260-501 91,842

855& 856 MN DHS Food Support 10.561 102215 28,939 aTOTAL U.S. DEPARTMENT OF AGRICULTURE 2,462,857

306 HUD Northfield City Community Development Block Grant 14.218 Home Matters 2.0 13,646 b

695 MN DHS ESG-RH 14.231 63521 82,130

607 MHFA Home Investment Partnerships Program 14.239 Northern Oaks 320,000

634 Permanent Supportive Housing Prairiewood 14.267 MN0306L5K021300 8,068 635 Permanent Supportive Housing Prairiewood 14.267 MN0306L5K021401 36,241 636 Permanent Supportive Housing Prairiewood 14.267 MN0306L5K021501 35,310 646 Continuum of Care Planning Grant 14.267 MN0331L5K021400 25,404 656 Continuum of Care Coordinated Entry 14.267 MN0366L5K021500 23,470 675 SHP - RHASP 14.267 MN0065L5K021407 42,996$ 55,092 676 SHP - RHASP 14.267 MN0065L5K021508 52,735 86,719 685 SHP - THP 14.267 MN0056L5K021407 - 64,072

95,731 334,376 TOTAL U.S. HOUSING & URBAN DEVELOPMENT 95,731 750,152

776 DOT MN DOT TRANSIT BUSES 20.509 1001746 340,157 TOTAL U.S. DEPARTMENT OF TRANSPORTATION 340,157

515 DOE MN DOC DOE/WX 81.042 95418 116,883 516 DOE/WX 81.042 A2500 67,306

TOTAL U.S. DEPARTMENT OF ENERGY 184,189

726 HHS SEMAAA Assisted Transportation 93.044 310-16-003B-063 27,093 c

716 SEMAAA HDM 93.045 310-16-03C2-002 59,491 c

706 SEMAAA CAREGIVER 93.052 310-16-003E-005 46,000

716 SEMAAA HDM 93.053 310-16-03C2-002 15,878 c

895 MNSure MNSure 93.525 MNSure 28,676 64,543

526 HHS MN DOC EAP/WX Carryover 93.568 95418/A2105 22,487 545 EAP/WX Carryover 93.568 95418/A2106 83,516 546 EAP/WX Carryover 93.568 A2107 44,788 556 Energy Assistance Program 93.568 100535/7297 557,244 557 Energy Assistance Program 93.568 1583 289,485

997,520

024 MN DHS CSBG 93.569 65012 115,546 025 CSBG 93.569 45263 102,619 036 CSBG Discretionary Grant 93.569 42715 24,770

242,935

115 Head Start 93.600 05CH8380/02 535,792 116 Head Start 93.600 05CH8380/03 849,986 115 CCRR Child Care Partnership 93.600 2015 89,826

1,475,604

716 MN DHS Medical Assistance - HDM 93.778 462713000 28,615 d726 Medical Assistance - VT 93.778 462713000 92 d

28,707 TOTAL U.S. DEPARTMENT OF HEALTH & HUMAN SERVICES 28,676 2,957,771

Total Federal Expenditures 124,407$ 6,695,126$

* indicates programs audited as major programs

a - SNAP Cluster - Total Expenditures = $28,939.

b - CDBG Entitlement Grants Cluster - Total Expenditures = $13,646.

c - Aging Cluster - Total Expenditures = $102,462.

d - Medicaid Cluster - Total Expenditures - $28,707.

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES NOTES TO SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

YEAR ENDED DECEMBER 31, 2016

(31)

NOTE 1 BASIS OF PRESENTATION

The accompanying schedule of expenditures of federal awards (the Schedule) includes the federal award activity of Three Rivers Community Action, Inc. and Subsidiaries (Organization) under programs of the federal government for the year ended December 31, 2016. The information in this Schedule is presented in accordance with the requirements of 2 CFR Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance). Because the Schedule presents only a selected portion of the operations of the Organization, it is not intended to and does not present the consolidated financial position, activities and changes in net assets, cash flows, and functional expenses of the Organization.

NOTE 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Expenditures reported on the Schedule are reported on the accrual basis of accounting. Such expenditures are recognized following the cost principles contained in the Uniform Guidance, wherein certain types of expenditures are not allowable or are limited as to reimbursement. The Organization has elected not to use the 10-percent de minimis indirect cost rate allowed under the Uniform Guidance.

NOTE 3 FEDERAL LOAN PROGRAMS

The federal loan programs balances and transactions relating to these programs are included in Organization’s basic financial statements. Loans outstanding at the beginning of the year and loans made during the year are included in the federal expenditures presented in the Schedule. The balance of loans outstanding at December 31, 2016 consists of:

Federal CFDA Amount

Program Title Number OutstandingClover Patch Rural Rental Housing Loan 10.415 482,230$ Clover Patch Rural Rental Housing Loan 10.415 400,030 Southside Rural Rental Housing Loan 10.415 146,805 Northbridge Rural Rental Housing Loan 10.415 1,290,486 Home Investment Partnerships Program 14.239 320,000

The Organization is obligated on three Rental Assistance and Interest Credit loans. The Organization is also obligated on a Home Targeted deferred loan. These loans require significant continuing compliance, primarily eligibility, and allowability.

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES SCHEDULE OF FINDINGS AND QUESTIONED COSTS

YEAR ENDED DECEMBER 31, 2016

(32)

Part I: Summary of the Independent Auditors’ Results:

Financial Statements

1. Type of auditors’ report issued: Unmodified

2. Internal control over financial reporting:

Material weakness(es) identified? yes x no

Significant deficiency(ies) identified that are not considered to be material weakness(es)? yes x none reported

3. Noncompliance material to financial

statements noted? yes x no

Federal Awards

1. Internal control over major federal programs:

Material weakness(es) identified? yes x no

Significant deficiency(ies) identified that are not considered to be material weakness(es)? yes x none reported

2. Type of auditors’ report issued on

compliance for major federal programs: Unmodified

3. Any audit findings disclosed that are required to be reported in accordance with 2 CFR 200.516(a)? yes x no

Identification of Major Federal Programs U.S. Department of Agriculture: Rural Rental Housing Loans CFDA #10.415 Dollar threshold used to distinguish between Type A and Type B programs: $ 750,000 Auditee qualified as low-risk auditee pursuant to Uniform Guidance? _x yes _ no

THREE RIVERS COMMUNITY ACTION, INC. AND SUBSIDIARIES SCHEDULE OF FINDINGS AND QUESTIONED COSTS

YEAR ENDED DECEMBER 31, 2016

(33)

Part II: Findings Related to the Basic Financial Statements: None Part III: Findings and Questioned Costs for Federal Awards: None Part IV: Prior Year Findings: There were no findings in the prior year that were required to be reported.