tic outlook 2018 - barclayscorporate.com · the next year will see multinational tic players expand...

TRANSCRIPT

TIC outlook 2018Trends and prospects in the Testing, Inspection and Certification sector

Contents3 Executivesummary

4 2017:TICindustryresilience

6 2018outlook:trendstowatch

7 DigitalTIC

8 M&A:adividedfield

10 Keytakeaways

11 Abouttheauthors

2of11

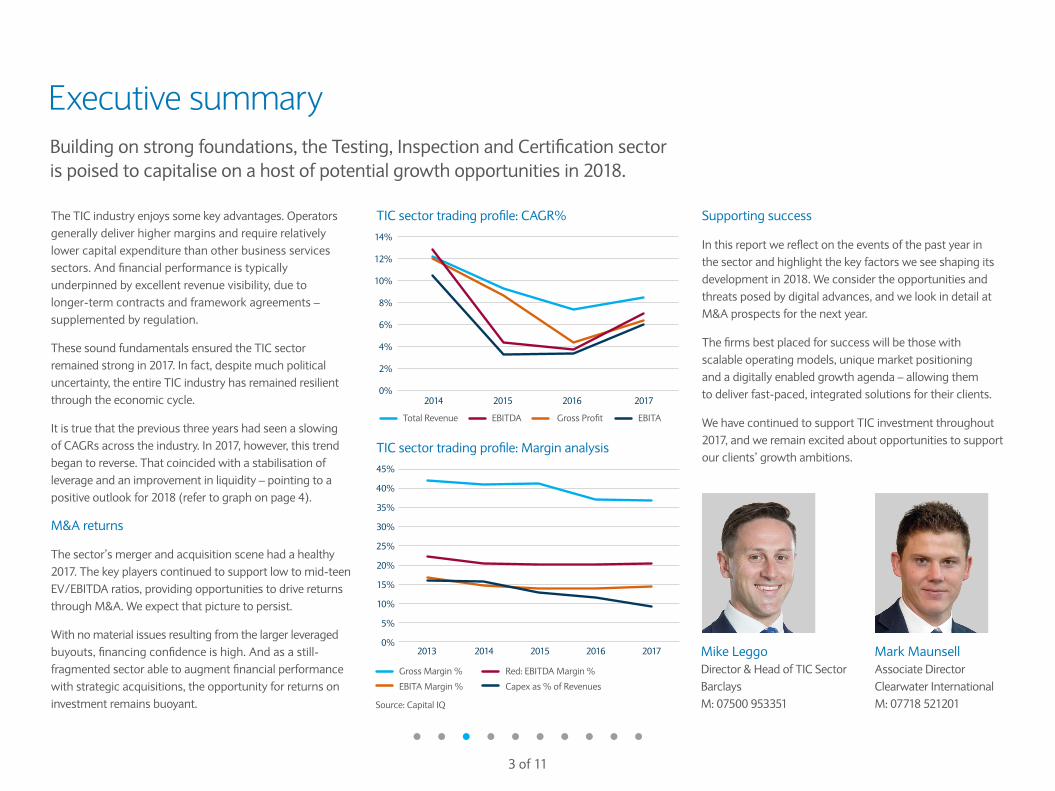

Executive summaryBuildingonstrongfoundations,theTesting,InspectionandCertificationsectorispoisedtocapitaliseonahostofpotentialgrowthopportunitiesin2018.

TheTICindustryenjoyssomekeyadvantages.Operatorsgenerallydeliverhighermarginsandrequirerelativelylowercapitalexpenditurethanotherbusinessservicessectors.Andfinancialperformanceistypicallyunderpinnedbyexcellentrevenuevisibility,duetolonger-termcontractsandframeworkagreements–supplementedbyregulation.

ThesesoundfundamentalsensuredtheTICsectorremainedstrongin2017.Infact,despitemuchpoliticaluncertainty,theentireTICindustryhasremainedresilientthroughtheeconomiccycle.

ItistruethatthepreviousthreeyearshadseenaslowingofCAGRsacrosstheindustry.In2017,however,thistrendbegantoreverse.Thatcoincidedwithastabilisationofleverageandanimprovementinliquidity–pointingtoapositiveoutlookfor2018(refertographonpage4).

M&Areturns

Thesector’smergerandacquisitionscenehadahealthy2017.Thekeyplayerscontinuedtosupportlowtomid-teenEV/EBITDAratios,providingopportunitiestodrivereturnsthroughM&A.Weexpectthatpicturetopersist.

Withnomaterialissuesresultingfromthelargerleveragedbuyouts,financingconfidenceishigh.Andasastill-fragmentedsectorabletoaugmentfinancialperformancewithstrategicacquisitions,theopportunityforreturnsoninvestmentremainsbuoyant.

Supportingsuccess

Inthisreportwereflectontheeventsofthepastyearinthesectorandhighlightthekeyfactorsweseeshapingitsdevelopmentin2018.Weconsidertheopportunitiesandthreatsposedbydigitaladvances,andwelookindetailatM&Aprospectsforthenextyear.

Thefirmsbestplacedforsuccesswillbethosewithscalableoperatingmodels,uniquemarketpositioningandadigitallyenabledgrowthagenda–allowingthemtodeliverfast-paced,integratedsolutionsfortheirclients.

WehavecontinuedtosupportTICinvestmentthroughout2017,andweremainexcitedaboutopportunitiestosupportourclients’growthambitions.

Source:CapitalIQ

TICsectortradingprofile:Marginanalysis

TICsectortradingprofile:CAGR%14%

12%

10%

8%

6%

4%

2%

0% 2014 2015 2016 2017

45%

40%

35%

30%

25%

20%

15%

10%

5%

0% 2013 2014 2015 2016 2017

GrossMargin% Red:EBITDAMargin%

EBITAMargin% Capexas%ofRevenues

TotalRevenue EBITDA GrossProfit EBITA

3of11

MikeLeggoDirector&HeadofTICSectorBarclaysM:07500953351

MarkMaunsellAssociateDirectorClearwaterInternationalM:07718521201

2017: TIC industry resilienceTheTICsectorstayedoncoursethroughayearofpoliticalturmoilandsomechallengingeconomicconditions.

Thestateofthemarket

TheglobalTICmarketisvaluedataround€200bn.ItisexpectedtogrowataCAGRof5%between2017and2023,withvariationsbysector.1Inlightofthechallengesfacingthewidereconomy,thisrepresentsaverypositiveoutlook.

Themarketishighlyfragmented.Thelargestthreeplayers–SGS,BureauVeritasandIntertek–holdacombinedmarketshareoflessthan25%.Thetop10playersaccountforlessthan40%ofthemarket.

Inthelastdecade,thethreetopoperatorsmentionedabovehaveexpandedswiftlyintonewgeographiesandsectors,

becomingdiversifiedglobalmajors.Second-tiercompaniessuchasDekra,ALSandULhavealsogatheredscaleandinternationalpresencewhileremainingmoresector-focused.Thereisalongtailofregionalcompaniesoperatinginnichedisciplines.

Achallengingstart

2017startedwithfurtherdowngradesofoilandgasrelatedearningsandarelativelychallengingoutlook.Weakdemandandlowpricescontinuedtoaffecttheindustry.However,livingwithloweroilpricesandaweakermineralssectorwascertainlynothingnew,andtheindustryhaslargelyrecalibrateditself.

1Source:BureauVeritas2016AnnualReport.

Creditmetrics

3.0x

2.5x

2.0x

1.5x

1.0x

0.5x

0.0x 2013 2014 2015 2016 2017

Currentratio Totaldebt/EBITDA Netdebt/EBITDA

The top 10playersaccountforlessthan

40%ofthemarket

SGS, Bureau Veritas and Intertekholdacombinedmarketshareoflessthan

25%4of11

9%

6%

6%

15%

15%9%

36%

3%

Commodities

Consumer

Compliance

Environmental

In Asset Inspection and Certificate

Industry and Infrastructure

Life Science and Pharma

Marine

TheTICsectorwasinfluencedbyacomplexpoliticallandscape.TheTrumpelectionvictorysuggestedashifttowardsprotectionismintheUSandthegrowthofanti-regulationsentiment.Andonaglobalscale,therateofchangeandtheimpactofgovernmentpolicywasuncertain,withanydilutioninstandardsnaturallyhavinganimpactongrowthprospects.Despitealloftheseheadwinds,though,thesectorcontinuedtothriveandtheprospectsin2018andbeyondremaingood.

ThefogofBrexit

IntheUK,uncertaintyovertheEuropeansinglemarketandtheSingleStandardmodelcontinuedafterArticle50wastriggered.TheconsensuswasthatEuropeanandUKregulationwouldcontinuetoleadtheworld,buttheUK’srolehasthepotentialtovarysignificantlyacrosssectorverticals.

ThosefirmsdependentontheUKbeingthedefaultcentreforEuropeanoperationshadtotakeahardlookattheroadahead.Meanwhile,theunderlyinguncertaintyaboutpublicinfrastructurespendandcurrencyvolatilitywasalsohighontheagendasofTICboards.

Lookingthroughawiderlens,theBrexitvotehasundoubtedlycausedamoderateslowingoftheUKeconomy.Apatternofsubduedconsumptionandinvestmentactivityhasemergedamidhigherinflation.However,sterlingdepreciation,healthynetexportsandimprovedglobaltrademomentumhaveoffsettheimpact.Brexitscenarioswillofcoursehavedifferenteconomicconsequences.

TheslowprogressintheEU–UKnegotiationswillmeanfurtheruncertaintyin2018.Again,thisissomethingthesectorhasweatheredpreviously,andweseenoreasonwhyTICbusinesseswillnotcontinuetoperformwellintheshortandmediumterm.

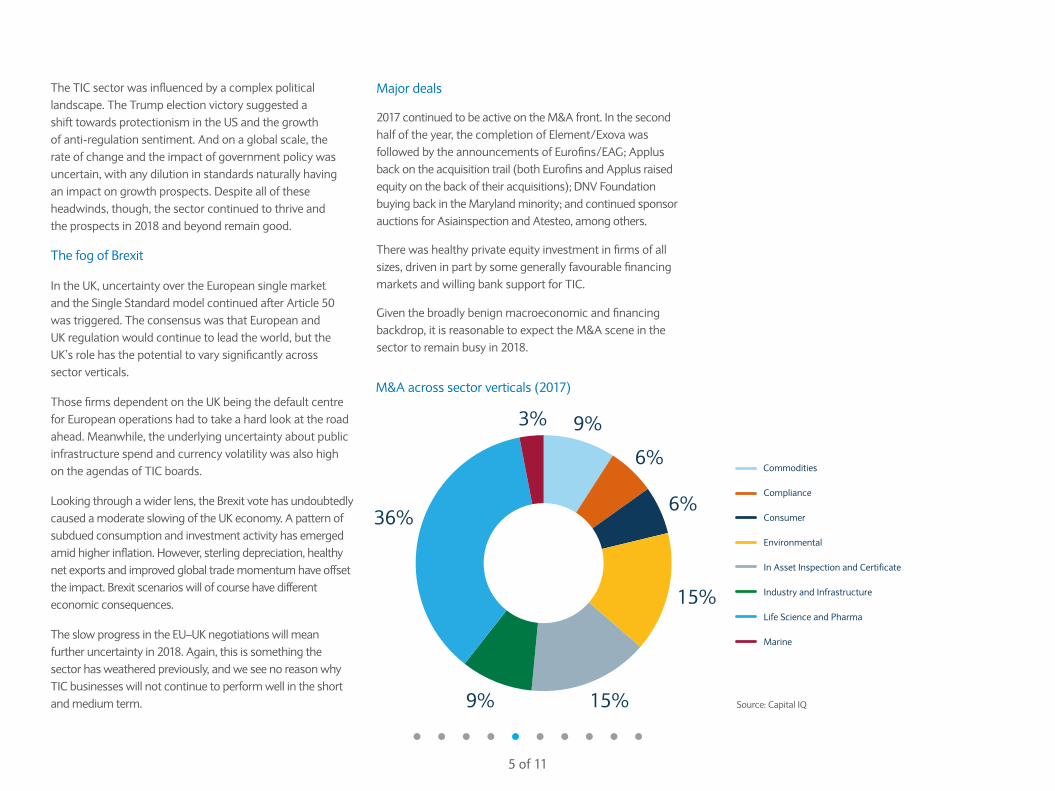

Majordeals

2017continuedtobeactiveontheM&Afront.Inthesecondhalfoftheyear,thecompletionofElement/ExovawasfollowedbytheannouncementsofEurofins/EAG;Applusbackontheacquisitiontrail(bothEurofinsandApplusraisedequityonthebackoftheiracquisitions);DNVFoundationbuyingbackintheMarylandminority;andcontinuedsponsorauctionsforAsiainspectionandAtesteo,amongothers.

Therewashealthyprivateequityinvestmentinfirmsofallsizes,driveninpartbysomegenerallyfavourablefinancingmarketsandwillingbanksupportforTIC.

Giventhebroadlybenignmacroeconomicandfinancingbackdrop,itisreasonabletoexpecttheM&Asceneinthesectortoremainbusyin2018.

Source:CapitalIQ

M&Aacrosssectorverticals(2017)

5of11

PE Seller

PE Buyer

PE to PE

Trade

Commodities

Consumer

Compliance

Environmental

In Asset Inspection and Certificate

Industry and Infrastructure

Life Science and Pharma

Marine

9%

82%

3%

6%

PE Seller

PE Buyer

PE to PE

Trade

9%

6%

6%

9%

82%

3%

6%

15%

15%9%

36%

3%

2018 outlook: trends to watchAriseinoutsourcingofTICfunctionsandever-tighteningregulationareamongthekeytrendsthatwillshapethesectorthisyear.

Outsourcing

Anestimated40%ofthemarketiscurrentlyoutsourced,withtheremainderofTICservicescarriedoutin-house.Theseservicesareoftennon-corebusinessforthecompany.Thepushtowardsoutsourcing–andinspecificinstances,theprivatisationofstate-ownedlaboratories–willcontinuetobeastrongdriverofgrowth.It’snotallone-waytrafficthough,andtheoutsourcedmodelcannotrelysolelyonitsthird-partyaccreditationcapabilityasjustificationforcontinuedgrowth.ThereareinstancesofTICservicesattributabletosomegovernmentagenciesmovingbackin-house,reflectingthepressureonpublicspending.

Regulation

Increasinglevelsofregulationhavetriggeredatransitionfromavoluntary-basedriskmanagementapproachtomandatorytestingservices–forexample,aftertherecenthigh-profilevehicleemissionsscandal.Additionally,thetragicGrenfellTowerfirehighlightedthecriticalneedforstandardsandcertificationintheconstructionandmaintenanceofpublicinfrastructure.AnevolvingregulatorylandscapeisanintrinsicpartoftheTICindustryandwillcontinuetogeneratenewopportunitiesforfirms–matchingtheirclients’needs.

Emergingmarketgrowth

ThenextyearwillseemultinationalTICplayersexpandfurtherintonewmarketsanddevelopingeconomies,chieflythroughacquisition,anddealwithnewcultural,taxandlegislativeregimes.Chinawillcontinuetobeaprimegrowthterritoryforthesector.

Globalisation

TICfirmscontinuetobecalledontoscrutiniseinternationalsupplychainsasaresultoftrendstowardslowersourcingandprocurementcosts.Thesourcingofrawmaterialsfromjurisdictionswithdifferentqualitycontrolprocedures,forinstance,willrequiremoreTICinput.Additionally–giventheproliferationoffirmsdeployingproductsonaglobalscale,oftensimultaneously,andinvolvingcomplexmanufacturingandsupplierarrangements–globalisationisamajorgrowthelementoftheTICindustry.

Brandprotection

Theriseinconsciousconsumerismwillcontinueonamajorscale,pilingpressureonbrandstoprotecttheirreputations.ThisismovingtheneedlefromTICservicesbeingseenasobligatory,tobeingabletoproviderealcompetitiveadvantage.Consumersexpectmorechoice,lowerpricesandbetterquality–hence,thetrustprovidedbycertificationisincreasinglyimportant.TheproliferationofsocialmedianetworksandthespeedofinformationsharingwilldrivefurthergrowthintheTICsector.Generalincreasesinglobalwealthwillhavethesameeffect,throughraisedexpectationsofsafetyandquality.

Protectionism

Therecentriseofprotectionistpolicyandtradebarriershasbeenoneofthe‘handbrakes’onthesoaringgrowthtrajectoriespreviouslyseeninTIC.Iffollowedthrough,thistrendhasthepotentialtolimitglobaltradegrowth,withanaturaldampeningeffectonthesector.However,weremainconfidentthattheresilienceandstrengthinherentintheindustrywillcompensateforthechallengesfaced.

Costsavings

Boardswillbelookingtoachievefurtherefficienciesinstaffing,procurementandgeneraloperatingmodels,tosaveoncostsandgrowmargins.TIChasanincreasinglyimportantroleinhelpingallindustriesachievethesecosttargets.

40%

60%

An estimated

of the market is currently outsourced.

of TIC services are carried

out in house.

6of11

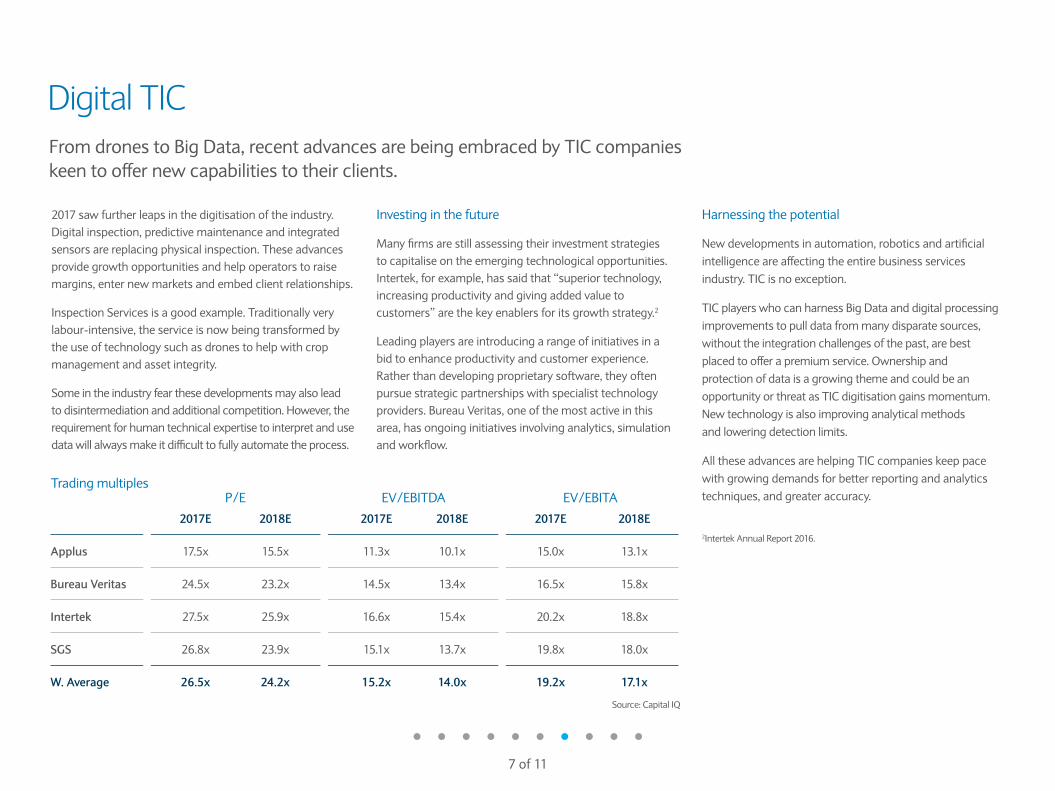

P/E EV/EBITDA EV/EBITA

2017E 2018E 2017E 2018E 2017E 2018E

Applus 17.5x 15.5x 11.3x 10.1x 15.0x 13.1x

Bureau Veritas 24.5x 23.2x 14.5x 13.4x 16.5x 15.8x

Intertek 27.5x 25.9x 16.6x 15.4x 20.2x 18.8x

SGS 26.8x 23.9x 15.1x 13.7x 19.8x 18.0x

W. Average 26.5x 24.2x 15.2x 14.0x 19.2x 17.1x

Digital TICFromdronestoBigData,recentadvancesarebeingembracedbyTICcompanieskeentooffernewcapabilitiestotheirclients.

2017sawfurtherleapsinthedigitisationoftheindustry.Digitalinspection,predictivemaintenanceandintegratedsensorsarereplacingphysicalinspection.Theseadvancesprovidegrowthopportunitiesandhelpoperatorstoraisemargins,enternewmarketsandembedclientrelationships.

InspectionServicesisagoodexample.Traditionallyverylabour-intensive,theserviceisnowbeingtransformedbytheuseoftechnologysuchasdronestohelpwithcropmanagementandassetintegrity.

Someintheindustryfearthesedevelopmentsmayalsoleadtodisintermediationandadditionalcompetition.However,therequirementforhumantechnicalexpertisetointerpretandusedatawillalwaysmakeitdifficulttofullyautomatetheprocess.

Investinginthefuture

Manyfirmsarestillassessingtheirinvestmentstrategiestocapitaliseontheemergingtechnologicalopportunities.Intertek,forexample,hassaidthat“superiortechnology,increasingproductivityandgivingaddedvaluetocustomers”arethekeyenablersforitsgrowthstrategy.2

Leadingplayersareintroducingarangeofinitiativesinabidtoenhanceproductivityandcustomerexperience.Ratherthandevelopingproprietarysoftware,theyoftenpursuestrategicpartnershipswithspecialisttechnologyproviders.BureauVeritas,oneofthemostactiveinthisarea,hasongoinginitiativesinvolvinganalytics,simulationandworkflow.

Source:CapitalIQ

Harnessingthepotential

Newdevelopmentsinautomation,roboticsandartificialintelligenceareaffectingtheentirebusinessservicesindustry.TICisnoexception.

TICplayerswhocanharnessBigDataanddigitalprocessingimprovementstopulldatafrommanydisparatesources,withouttheintegrationchallengesofthepast,arebestplacedtoofferapremiumservice.OwnershipandprotectionofdataisagrowingthemeandcouldbeanopportunityorthreatasTICdigitisationgainsmomentum.Newtechnologyisalsoimprovinganalyticalmethodsandloweringdetectionlimits.

AlltheseadvancesarehelpingTICcompanieskeeppacewithgrowingdemandsforbetterreportingandanalyticstechniques,andgreateraccuracy.

Tradingmultiples

2IntertekAnnualReport2016.

7of11

M&A: a divided fieldWhilethebiggestplayersarescalingbacktheiracquisitions,thehealthyappetiteofsecond-tierfirmsisdrivinganactiveM&Ascene.

KeyplayershaveallpledgedsignificantfundingforM&Aandannouncedambitiousshort-termtargets.Forexample,SGScompleted12transactionsin2017,movingitclosertoitsstrategicplanofacquiringrevenuesofCHF1bn(c.€867m)by2020.AndRINAislookingtospendaround€200maheadofanIPOinthenextthreeyears.

M&Ahas,however,becomemorechallenging.Thelargestlistedcompaniesaremainlyfocusingonsmalltuck-indeals.Thispartlyreflectsthelackofsizeabletargetsinafragmentedsector,butalsothepremiumpriceoflarge-scaletransactions,whichofferlessscopeforvaluecreation.Inaddition,somehigh-profileacquisitions–suchasBureauVeritas’spurchaseofMaxximatthetopoftheoilandgasmarket(10.7xEV/EBITDA)–haveunderperformed.

Meanwhile,however,second-tierandprivateequity-backedbusinessesarestillhighlyacquisitive.Thesecompaniesareoftenbetterplacedtojustifythepriceoflargerdeals,throughexpansionoftheirgeographicalandsectorreach.AgoodexampleisNetherlands-basedACTAHoldingBV’spurchaseofHelsinki-headquarteredInspectaGroupOyfor€200m(14.0xEV/EBITDA).

ThepowerofPE

Privateequitygroupsareresponsibleformanynotabletransactions.Inthelasttwoyears,high-profiledealshaveincludedPSPandPartnersGroup’sinvestmentinCerba(12.0xEV/EBITDA),Apax’sbuyoutoftheremainingstakeinUnilabs(11.8xEV/EBITDA)andBPAE’spublictoprivatepurchaseofSAIGlobal(9.4xEV/EBITDA).

Privateequitygroupsareincreasinglyopentolookingatsmallerplatforms,providedtheyhelpbuildsectorleadershipwithastrategicgeographicfootprint.Inflexion’srecentinvestmentinCawoodScientific,aspecialistinthefood,environmentalandveterinarysegments,isanexampleofinvestors’appetitetoacquirenicheoperators.

Akeyattractionofthesectoristhepotentialformultipleexitoptions.Inthemainthiscomesintheformofasaletoalargerprivateequityfundorawell-capitalisedtradepurchaser.Thiswasthecasewith3i’sdisposalofESGtoSOCOTEC,andUS-basedInclineEquityPartners’recentdisinvestmentofAmSpecHoldingCorp,apetroleumspecialist,toOlympusPartners(12.0xEV/EBITDA).

Insomesituations,anIPOisacrediblealternative.However,thepost-floatperformanceofExova(IPO’d12.0xEV/EBITDA,takenprivateat9.4x)andApplusraisesquestionsovertheoperationalgearingwhileacompanyislistedonthepublicmarkets.

Privateequity-backedtradeplatformswillcontinuetobeakeysourceofdealsinthenexttwoyears.Theinvestmentby3iandCITICCapitalinGermany-basedFormalD,aspecialistTICprovidertotheautomotivesector,isaprimeexample.ThebusinesswilllooktobuildpresenceintheUSandAsiaandtoreduceitsrelianceonEurope,whichstillrepresents75%ofrevenues.Other2017examplesincludeLLCP’splatformFlexXray,andSpectrumEquity’spurchaseofIreland-basedTheDigitalMarketingInstitute.

Privateequitygroupsareincreasinglyopentolookingatsmallerplatforms,providedtheyhelpbuildsectorleadershipwithastrategicgeographicfootprint.

8of11

Towardsconvergence

Thelastfewyearshaveseenincreasingconvergenceasinstrumentationandcontrolsmanufacturershavelookedtoaugmentproductsandaccessfaster-growing,higher-marginactivitiesbybuyingservicesbusinesses.

OneofthebestexamplesisSpectrisplc,whichbuiltonitsacquisitionofMillbrookGroup(12.0–13.0xEV/EBITDA)in2016throughthepurchaseofConceptLifeSciencesinJanuary2018for£163m(c.€185m).ThedealisseenashighlycomplementarytotheactivitiesofMalvernPanalytical,whichformspartofSpectris’stestandmeasurementdivision.OtherexamplesincludeHoriba–whichpurchasedMiraLtd(14.0xEV/EBITDA)–aswellasDanaherandITWInc.

Globalgrowthpaths

Emergingmarkets,especiallyChina,presentsignificantopportunitiesforM&A.Theseterritorieshavebecomeattractivethroughthedevelopmentofindigenousindustriesandsubsequentaccelerationinexports,theintroductionofstringentstandardsandrapidurbanisation.

Inaddition,theriseofthemiddleclasshasledtoanincreaseinprivateconsumptionandademandforbothsafetyandproductquality.Thisinturnoffersgrowthopportunitiesinareassuchasfoodandconsumergoodstesting.AprimeexampleistheacquisitionofTÜVRheinland’sfoodanalysislaboratoriesinChinaandTaiwanbyGermany-basedTentamusGroup.

OverlappingM&Astrategiesamongseveraloftheglobalconsolidatorsarelikelytoinfluencepricinginthecomingyear.VirtuallyalloftheEuropeheadquarteredTICplayersarestillsubscaleintheUSrelativetoglobalfootprint,andarealsokeentobuildpresenceinthefast-growingChinesemarket.Food,consumer,agricultureandautomotivemarketswillbeparticularlyattractive.

9of11

Key takeaways

10of11

• TheTICsectoriswellplacedtodisplaycontinuedresilienceandgrowthinthefaceofpoliticalandeconomicuncertaintyin2018

• CapitalexpenditureissettoincreasefurtherasTICplayerstakeadvantageofthepotentialofnewtechnologiestotransformthesector,oftenbyforgingpartnershipswithspecialistproviders

• Otherfactorstriggeringgrowthin2018includefurtheroutsourcingofTICfunctionsbyindustry,tighteningregulationinmanyfieldsandagrowingneedtoensurebrandprotection

• MultinationalTICoperatorsaresettoexpandfurtherintodevelopingeconomies,chieflythroughnewacquisitions,withChinaaprimetarget

• Second-tierplayersarelikelytobemoreacquisitivethanthebiggestbusinesses,whicharenowfindingitmorechallengingtocreatevaluefromnewtransactions

• Privateequity-backedplatformswillcontinuetobeaprimesourceofnewdealsoverthenexttwoyears

• Withconstructionoutputearmarkedtobebroadlyflatin2018andinthewakeoftheCarillionliquidation,TICvolumeswillbeimpacted.

About the authorsMikeLeggoDirector&HeadofTICSectorBarclays

MikeLeggoisHeadofTICatBarclaysCorporate,wherehesupportsthegrowthstrategiesofclientsinthesectorviastructuredfinancingsolutionsandglobaltreasurysupport.Hehas10yearsofexperiencecoveringtheBusinessServicessectorandhascompletedanumberofkeysectortransactionsinvolvingbothpublicandprivatecompanies.InMike’sroleasakeyClientCoverageBankeratBarclaysheworkswithmanagementteamslookingtoraisecapitalviaBankandCapitalMarkets.HeiscommittedtotheTICsectorandutilisesindustryexpertiseandafocusonlong-termrelationshipstodriveresults.

M:07500953351*[email protected]

MarkMaunsellAssociateDirectorBusinessServicesMarketIntelligenceClearwaterInternational

MarkisanAssociateDirectoratClearwaterInternational,amarketleadingindependentcorporatefinancehousespecialisinginmergersandacquisitions,managementbuyoutsandfundraisingtransactions.HehasworkedinM&Aforovereightyearsandhasbeeninvolvedinanumberofdealsinvolvingprivateequity,owner-managedbusinessesandcorporates.

M:07718521201*[email protected]

barclayscorporate.com

clearwaterinternational.com

*Pleasenote:thesearemobilephonenumbersandcallswillbechargedinaccordancewithyourmobiletariff.

Theviewsexpressedinthisreportaretheviewsofthirdparties,anddonotnecessarilyreflecttheviewsofBarclaysBankPLCnorshouldtheybetakenasstatementsofpolicyorintentofBarclaysBankPLC.BarclaysBankPLCtakesnoresponsibilityfortheveracityofinformationcontainedinthird-partynarrativeandnowarrantiesorundertakingsofanykind,whetherexpressedorimplied,regardingtheaccuracyorcompletenessoftheinformationgiven.BarclaysBankPLCtakesnoliabilityfortheimpactofanydecisionsmadebasedoninformationcontainedandviewsexpressedinanythird-partyguidesorarticles.

BarclaysBankPLCisregisteredinEngland(CompanyNo.1026167)withitsregisteredofficeat1ChurchillPlace,LondonE145HP.BarclaysBankPLCisauthorisedbythePrudentialRegulationAuthority,andregulatedbytheFinancialConductAuthority(FinancialServicesRegisterNo.122702)andthePrudentialRegulationAuthority.BarclaysisatradingnameandtrademarkofBarclaysPLCanditssubsidiaries.

March2018.BD06975-01.

11of11