timber mart-south & southern trends€¦ · timbermart-south. 1. southern timber trends. 9...

TRANSCRIPT

TimberMart-South 1

Southern Timber Trends9 March 2012

Four State Forestry on The GrowIdabel, Oklahoma

Thomas G. Harris, Jr., Jacek Siry. Sara Baldwin, Jonathan Smith & Robert Simmons

TimberMart-South 2

TimberMart-SouthCenter for Forest Business

D.B. Warnell School of Forest ResourcesThe University of Georgia

Thomas G. Harris, Jr. , Jacek Siry, Sara Baldwin, Jonathan Smith & Robert Simmons

TimberMart-South 3

Outline of Presentation

• Major Forest Industry Changes– Acreage Changes/ Forest Industry Changes– Production declines– Prices changes– Global Market Conditions– What does in mean for investors– Finish on time.

TimberMart-South 4

Forested Regions of the World

TimberMart-South 5

World Markets

Major News

• Recession• Forest Products Company dis-

integrate and sell Timberland• TIMOs & REITS new landowners.• Changing paper demand.• Sawtimber dominates Southern

Markets• Bio energy

TimberMart-South 6

TimberMart-South 7

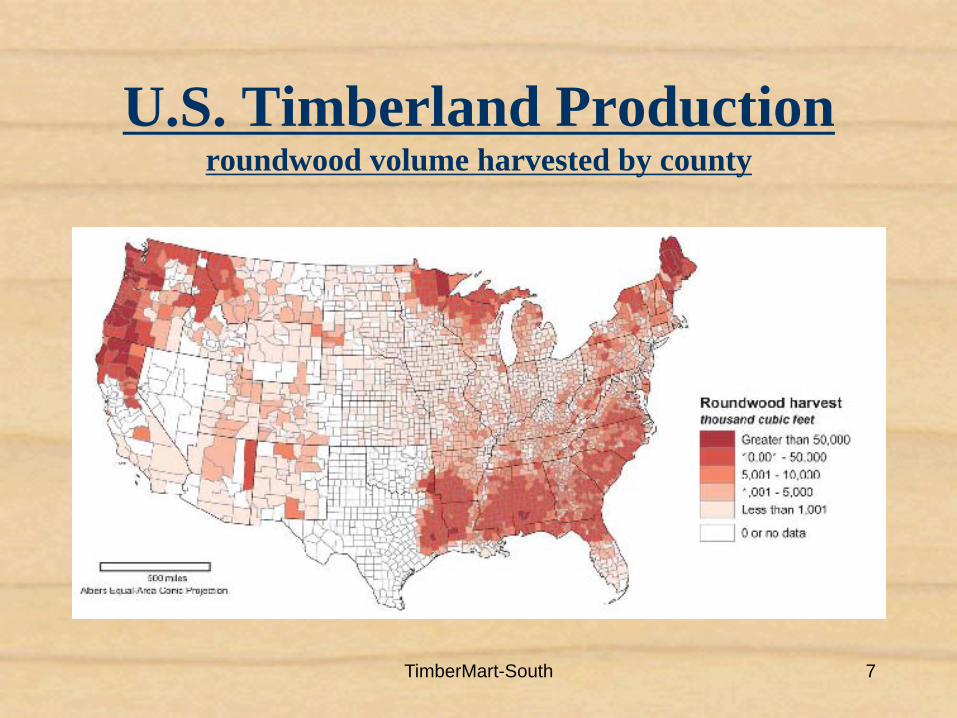

U.S. Timberland Production roundwood volume harvested by county

TimberMart-South 8

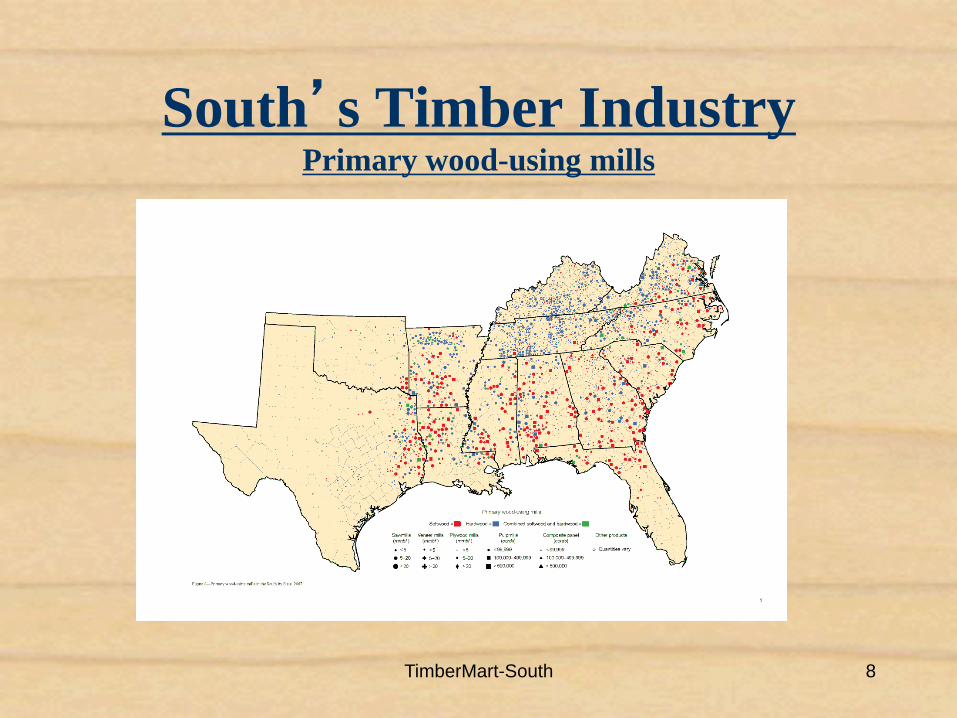

South’s Timber IndustryPrimary wood-using mills

TimberMart-South 9

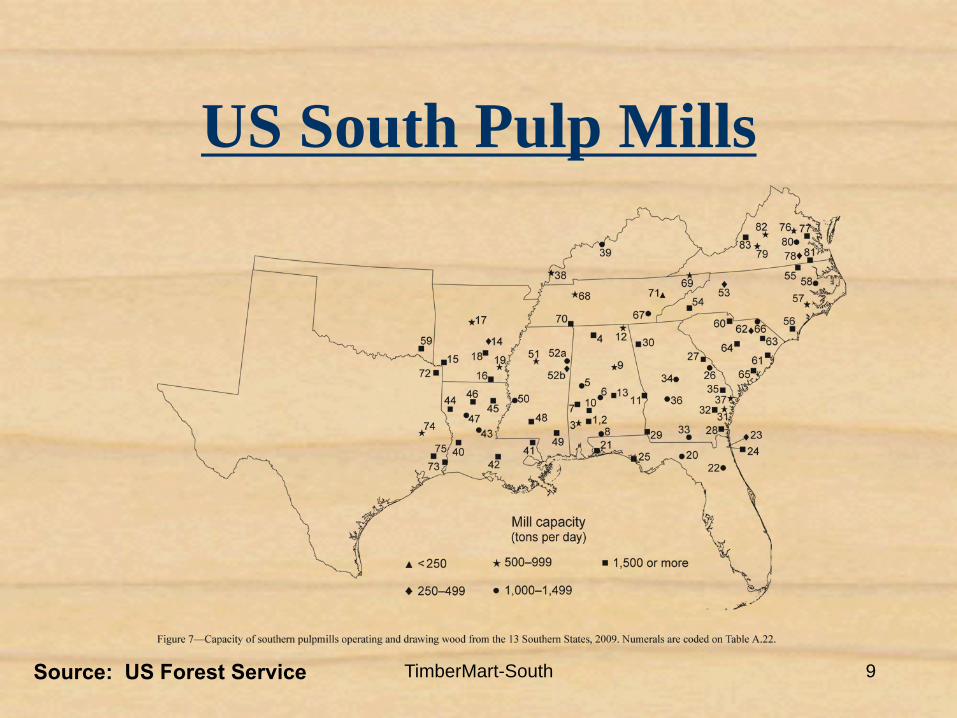

US South Pulp Mills

Source: US Forest Service

TimberMart-South 10

North American Softwood Sawmills

TimberMart-South 11

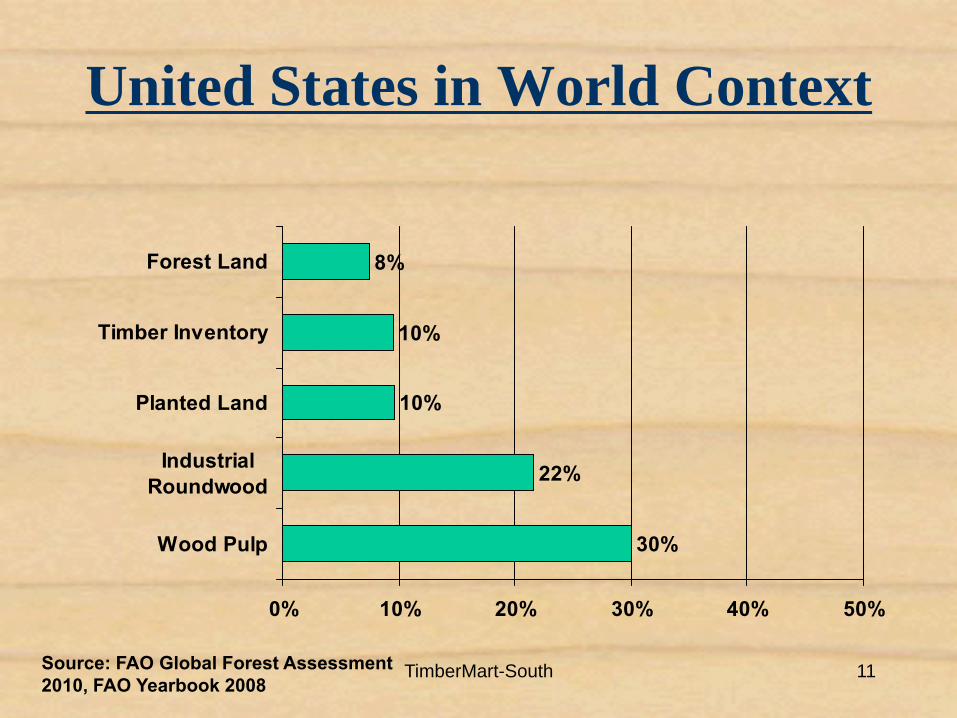

United States in World Context

8%

10%

10%

22%

30%

0% 10% 20% 30% 40% 50%

Forest Land

Timber Inventory

Planted Land

IndustrialRoundwood

Wood Pulp

Source: FAO Global Forest Assessment 2010, FAO Yearbook 2008

TimberMart-South 12

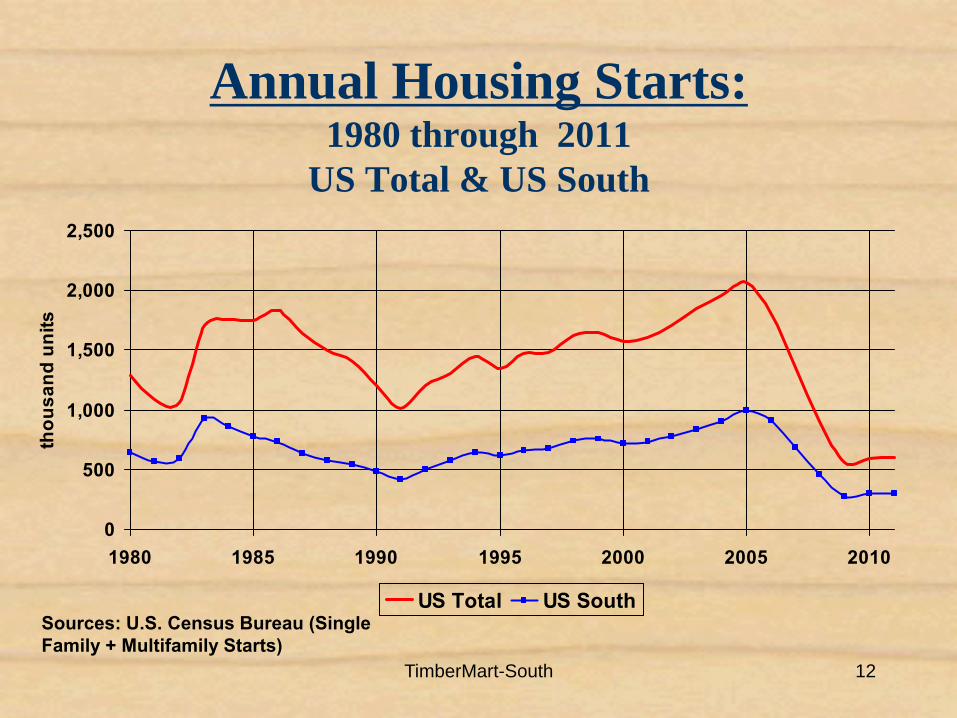

Annual Housing Starts:1980 through 2011

US Total & US South

0

500

1,000

1,500

2,000

2,500

1980 1985 1990 1995 2000 2005 2010

thou

sand

uni

ts

US Total US SouthSources: U.S. Census Bureau (Single Family + Multifamily Starts)

TimberMart-South 13

U. S. South Pine Sawtimber Stumpage Prices – Long History2011 average was $23.97 up from a low of $0.02 per ton in 1880

to a high of $40.46 per ton in 1998

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

1880 1900 1920 1940 1960 1980 2000

US$

per

ton

Source: U.S. Forest Service & Timber Mart-South

TimberMart-South 14

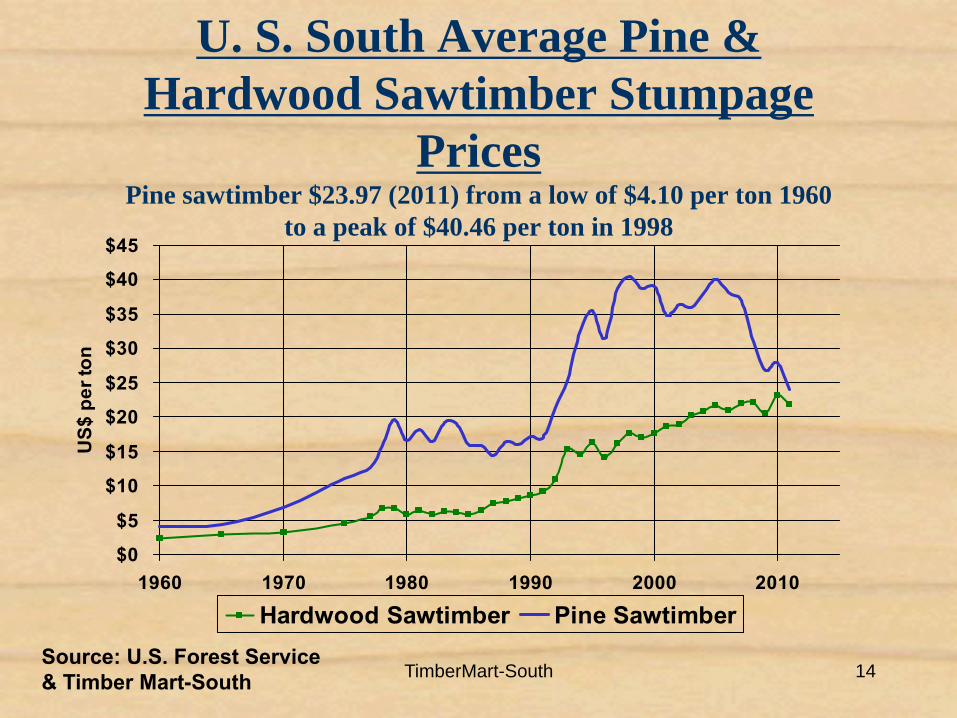

U. S. South Average Pine & Hardwood Sawtimber Stumpage

PricesPine sawtimber $23.97 (2011) from a low of $4.10 per ton 1960

to a peak of $40.46 per ton in 1998

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

1960 1970 1980 1990 2000 2010

US$

per

ton

Hardwood Sawtimber Pine SawtimberSource: U.S. Forest Service & Timber Mart-South

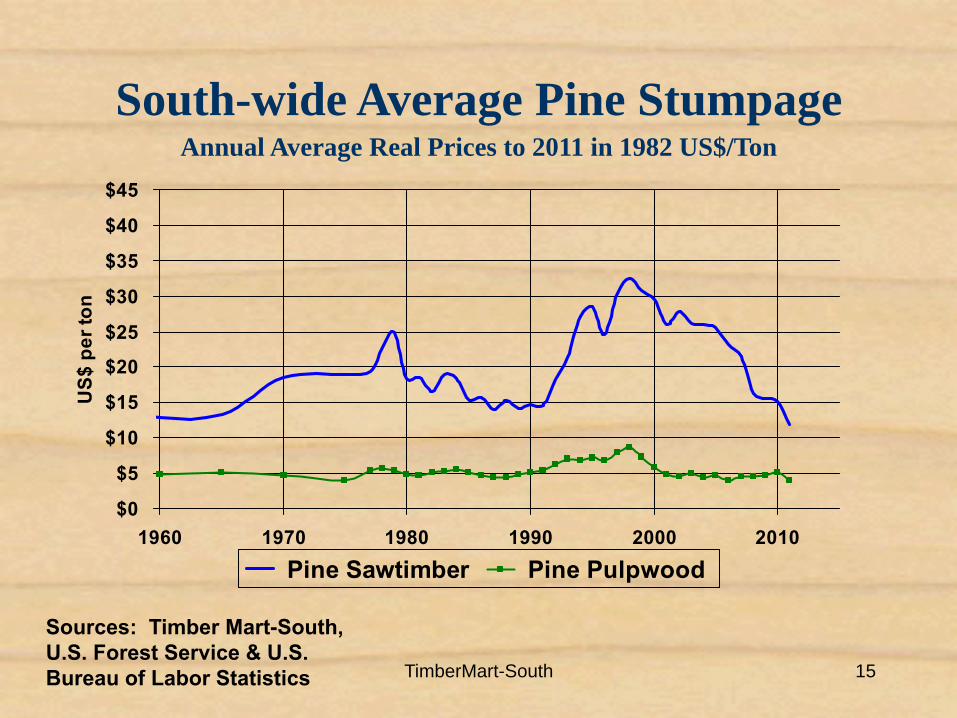

TimberMart-South 15

Sources: Timber Mart-South, U.S. Forest Service & U.S. Bureau of Labor Statistics

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

1960 1970 1980 1990 2000 2010

US$

per

ton

Pine Sawtimber Pine Pulpwood

South-wide Average Pine StumpageAnnual Average Real Prices to 2011 in 1982 US$/Ton

TimberMart-South 16

U. S. South Average Pulpwood Stumpage Prices

Annual Average 1960 to 2011

$0

$2

$4

$6

$8

$10

$12

1960 1970 1980 1990 2000 2010

US$

per

ton

Hardwood Pulpwood Pine PulpwoodSource: U.S. Forest Service & Timber Mart-South

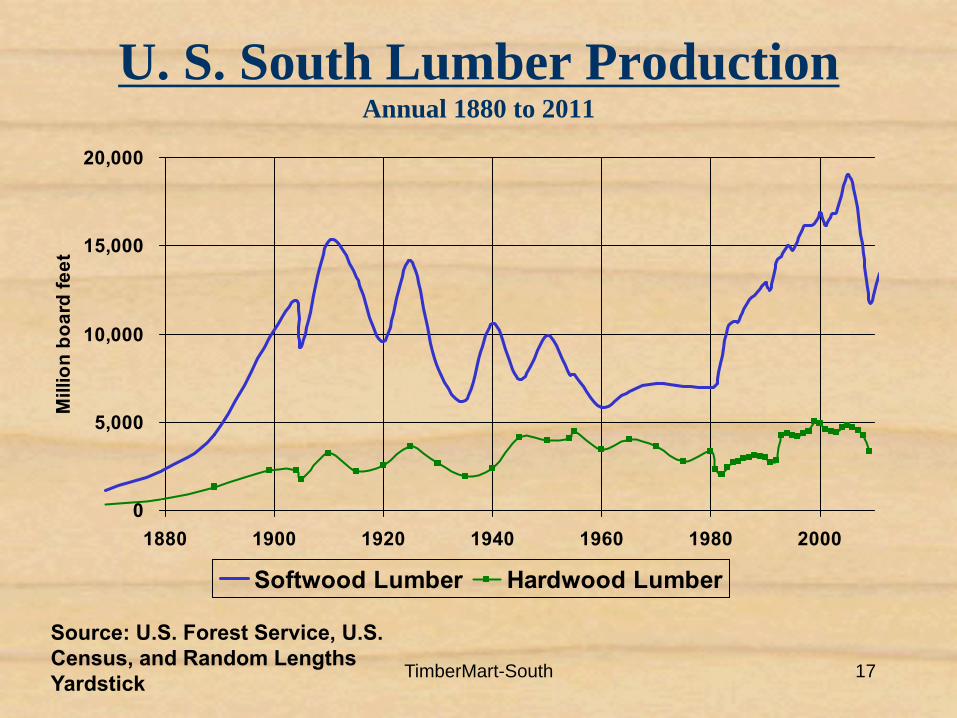

TimberMart-South 17

U. S. South Lumber ProductionAnnual 1880 to 2011

0

5,000

10,000

15,000

20,000

1880 1900 1920 1940 1960 1980 2000

Mill

ion

boar

d fe

et

Softwood Lumber Hardwood Lumber

Source: U.S. Forest Service, U.S. Census, and Random Lengths Yardstick

TimberMart-South 18TimberMart-South 18

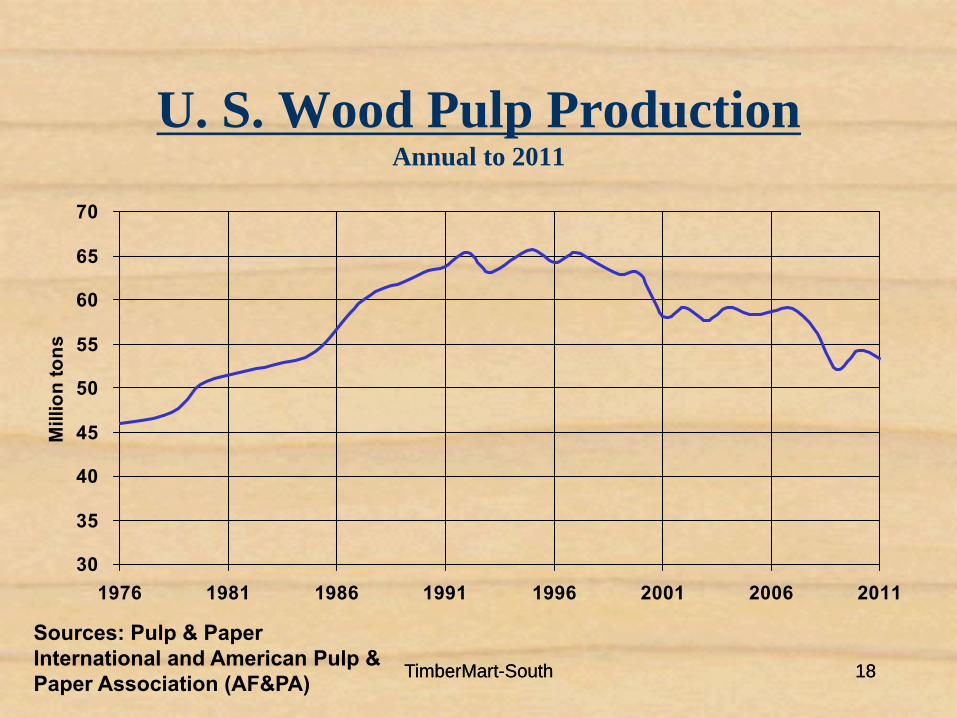

U. S. Wood Pulp Production Annual to 2011

30

35

40

45

50

55

60

65

70

1976 1981 1986 1991 1996 2001 2006 2011

Mill

ion

tons

Sources: Pulp & Paper International and American Pulp & Paper Association (AF&PA)

TimberMart-South 19

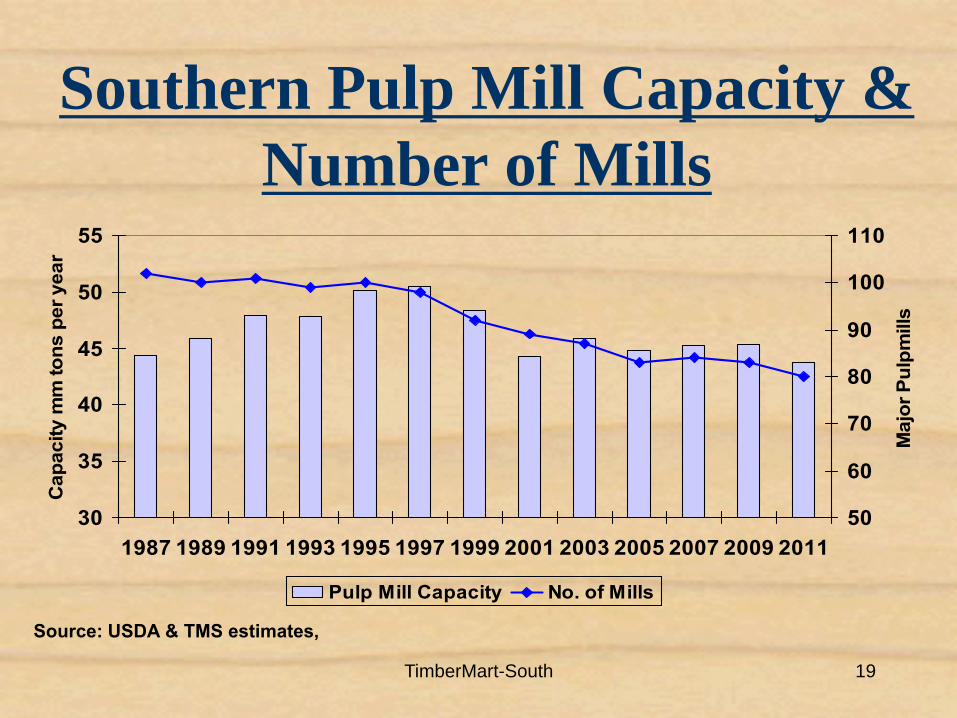

Southern Pulp Mill Capacity & Number of Mills

Source: USDA & TMS estimates,

30

35

40

45

50

55

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

Cap

acity

mm

tons

per

yea

r

50

60

70

80

90

100

110

Maj

or P

ulpm

ills

Pulp Mill Capacity No. of Mills

TimberMart-South 20

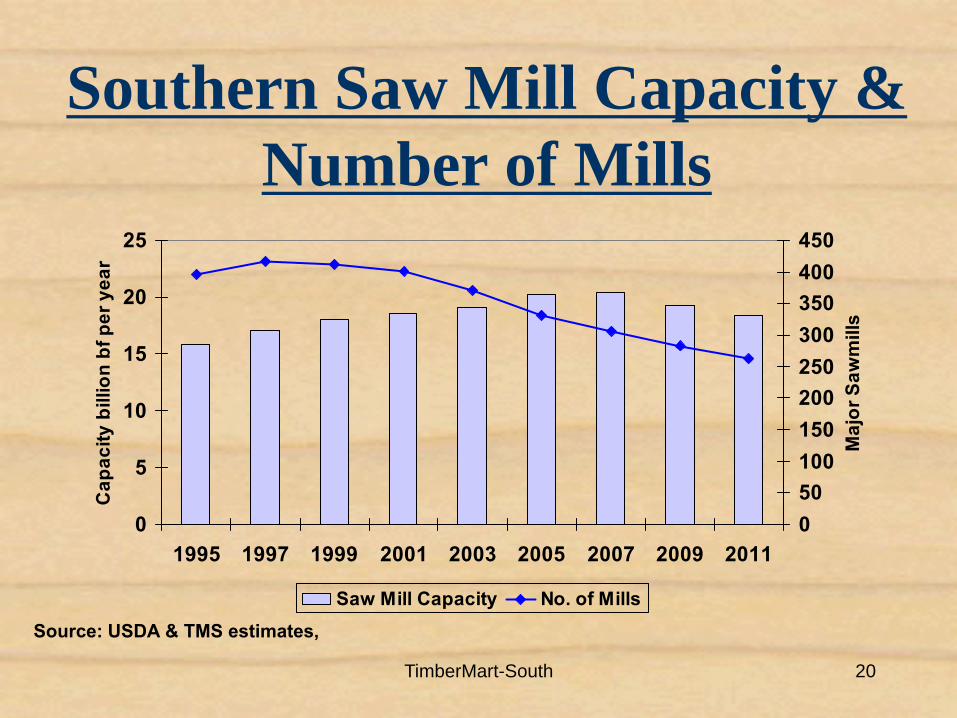

Southern Saw Mill Capacity & Number of Mills

Source: USDA & TMS estimates,

0

5

10

15

20

25

1995 1997 1999 2001 2003 2005 2007 2009 2011

Cap

acity

bill

ion

bf p

er y

ear

050100150200250300350400450

Maj

or S

awm

ills

Saw Mill Capacity No. of Mills

TimberMart-South 212121

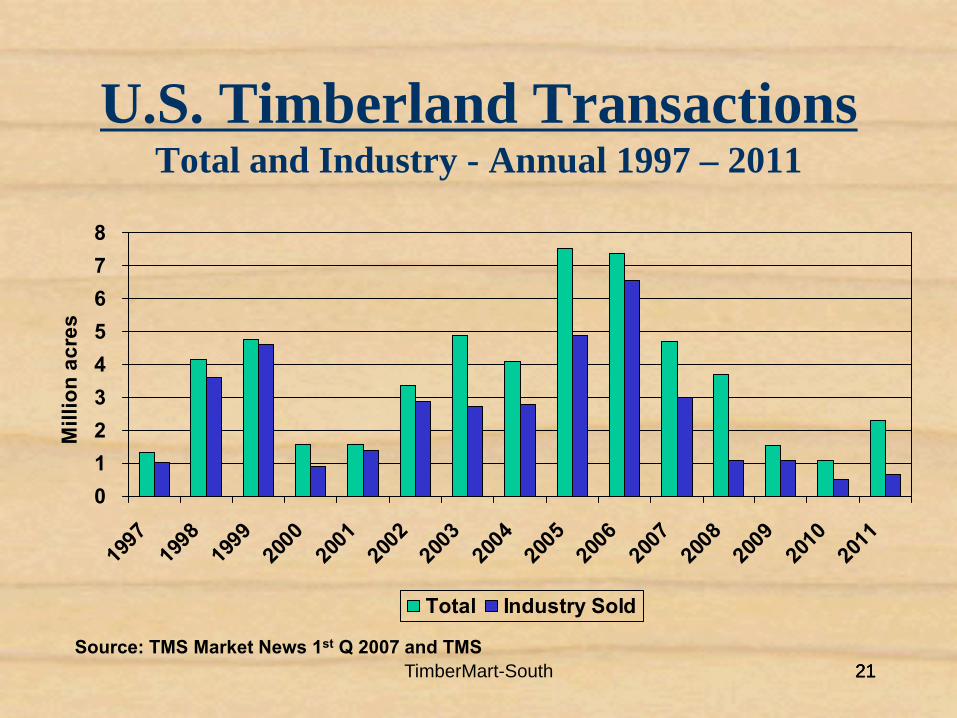

U.S. Timberland TransactionsTotal and Industry - Annual 1997 – 2011

012345678

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Mill

ion

acre

s

Total Industry Sold

Source: TMS Market News 1st Q 2007 and TMS

TimberMart-South 2222TimberMart-South 22

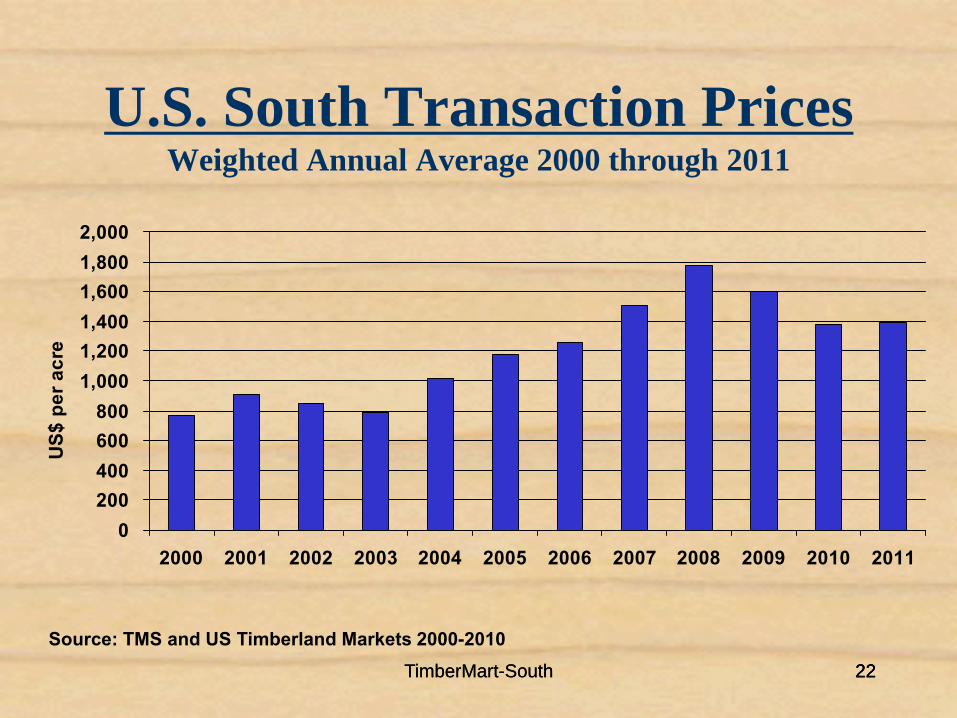

U.S. South Transaction PricesWeighted Annual Average 2000 through 2011

0200400600800

1,0001,2001,4001,6001,8002,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

US$

per

acr

e

Source: TMS and US Timberland Markets 2000-2010

TimberMart-South 23

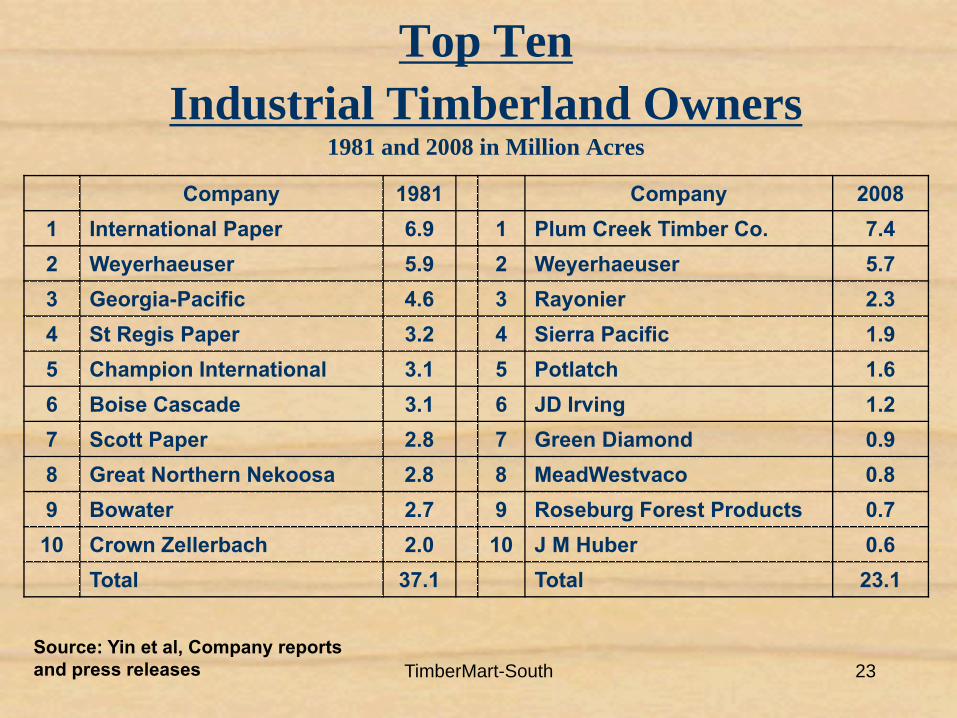

Top Ten Industrial Timberland Owners

1981 and 2008 in Million Acres

Source: Yin et al, Company reports and press releases

Company 1981 Company 20081 International Paper 6.9 1 Plum Creek Timber Co. 7.42 Weyerhaeuser 5.9 2 Weyerhaeuser 5.73 Georgia-Pacific 4.6 3 Rayonier 2.34 St Regis Paper 3.2 4 Sierra Pacific 1.95 Champion International 3.1 5 Potlatch 1.66 Boise Cascade 3.1 6 JD Irving 1.27 Scott Paper 2.8 7 Green Diamond 0.98 Great Northern Nekoosa 2.8 8 MeadWestvaco 0.89 Bowater 2.7 9 Roseburg Forest Products 0.710 Crown Zellerbach 2.0 10 J M Huber 0.6

Total 37.1 Total 23.1

TimberMart-South 24

Top Ten Industrial Timberland Owners 2011

Rank CompanyAcres

Millions1 Plum Creek Timber Co. (REIT)* 6.62 Weyerhaeuser (REIT)* 5.43 Rayonier (REIT)* 2.34 Sierra Pacific 1.85 Potlatch (REIT)* 1.46 JD Irving 1.37 Green Diamond 0.88 MeadWestvaco* 0.79 J.M. Huber 0.710 Roseburg Forest Products 0.6

Total 21.7* Publicly traded entities.

TimberMart-South 25

Top Ten Timberland Investment Managers 2011

Rank CompanyAcres

Millions1 The Forestland Group 3.12 The Campbell Group 3.03 Hancock Timber Resource Group 3.04 Resource Management Service 2.65 Forest Investment Associates 2.06 Forest Capital Partners 1.9

7 Regions Morgan Keegan Timberland Group 1.7

8 Wagner Forest Management 1.39 Seven Islands/Orion 1.2

10 GMO Renewable Resources 1.0Total 20.8

TimberMart-South 26

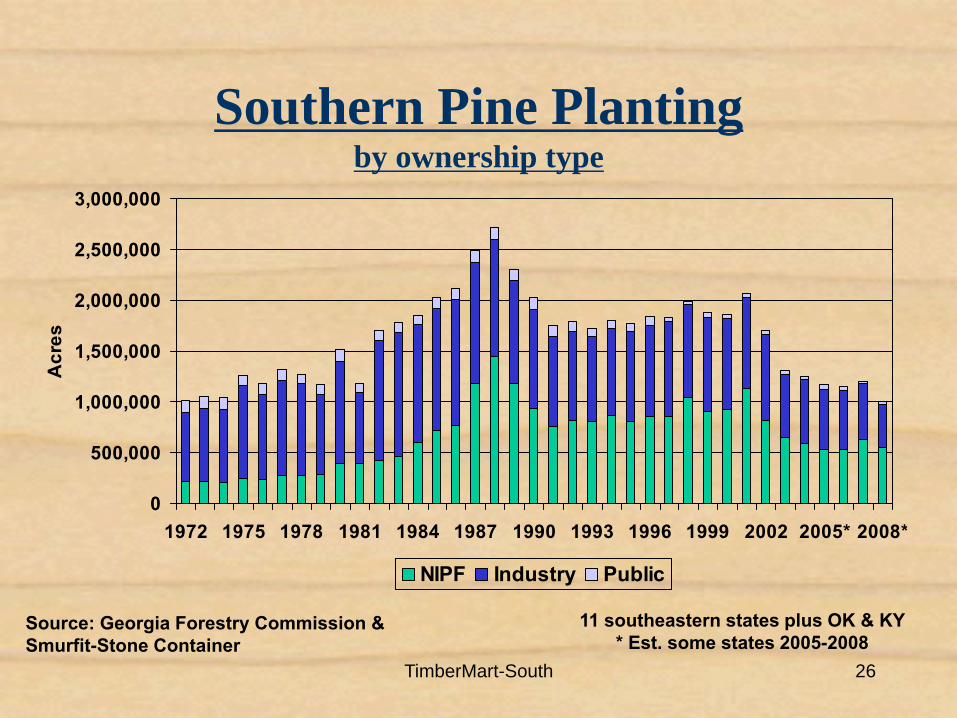

Southern Pine Plantingby ownership type

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005* 2008*

Acr

es

NIPF Industry Public

Source: Georgia Forestry Commission & Smurfit-Stone Container

11 southeastern states plus OK & KY* Est. some states 2005-2008

TimberMart-South 27

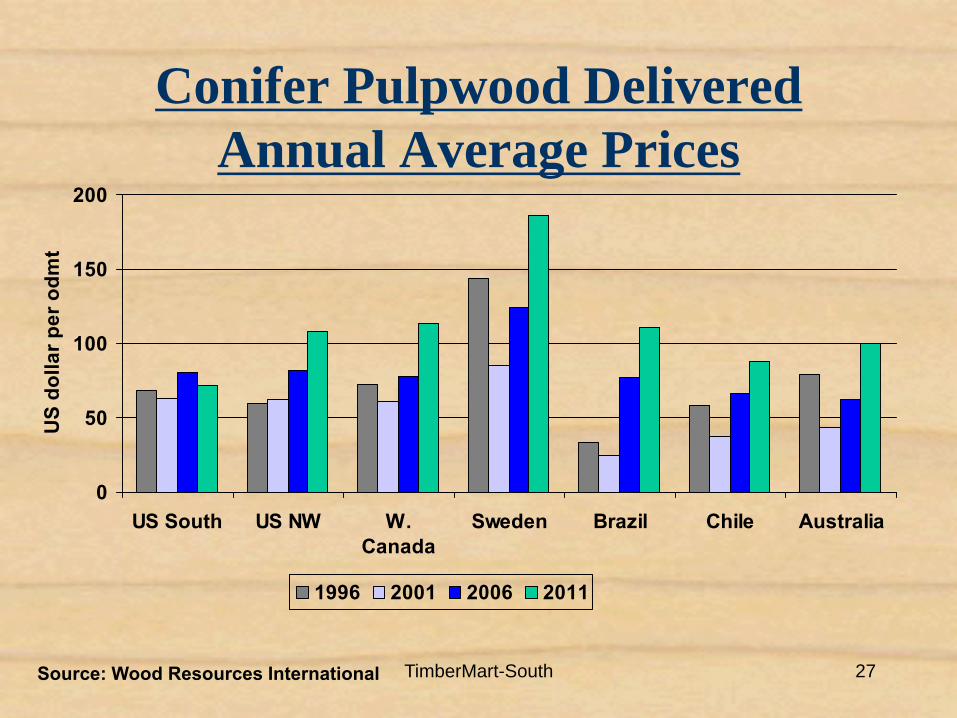

Conifer Pulpwood Delivered Annual Average Prices

0

50

100

150

200

US South US NW W.Canada

Sweden Brazil Chile Australia

US

dolla

r per

odm

t

1996 2001 2006 2011

Source: Wood Resources International

TimberMart-South 2828

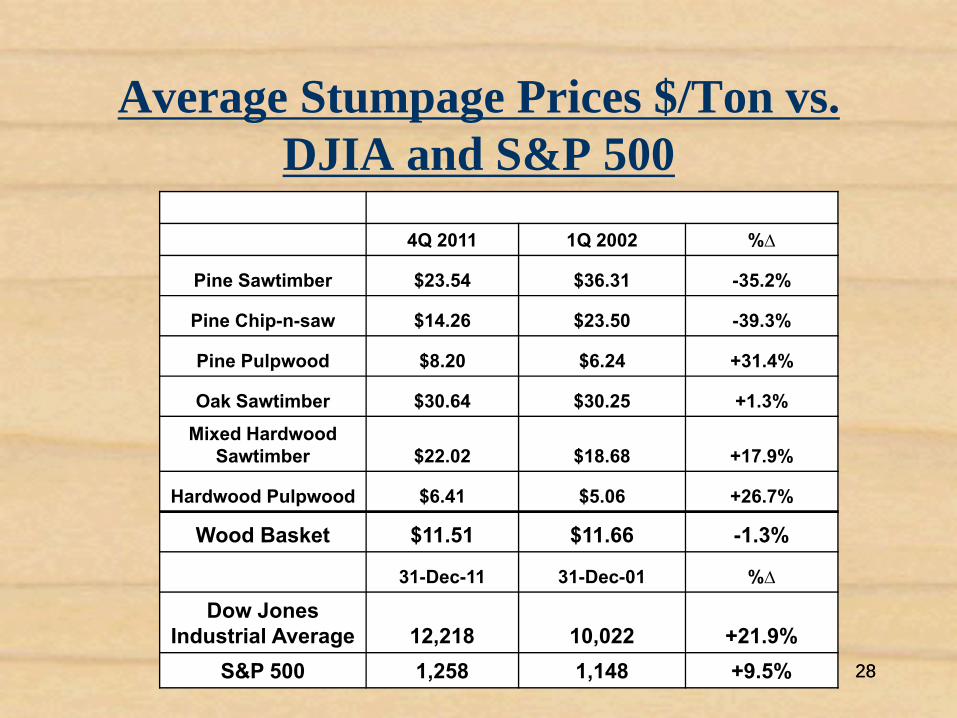

Average Stumpage Prices $/Ton vs. DJIA and S&P 500

4Q 2011 1Q 2002 %∆

Pine Sawtimber $23.54 $36.31 -35.2%

Pine Chip-n-saw $14.26 $23.50 -39.3%

Pine Pulpwood $8.20 $6.24 +31.4%

Oak Sawtimber $30.64 $30.25 +1.3%

Mixed Hardwood Sawtimber $22.02 $18.68 +17.9%

Hardwood Pulpwood $6.41 $5.06 +26.7%

Wood Basket $11.51 $11.66 -1.3%

31-Dec-11 31-Dec-01 %∆

Dow Jones Industrial Average 12,218 10,022 +21.9%

S&P 500 1,258 1,148 +9.5%

TimberMart-South 2929

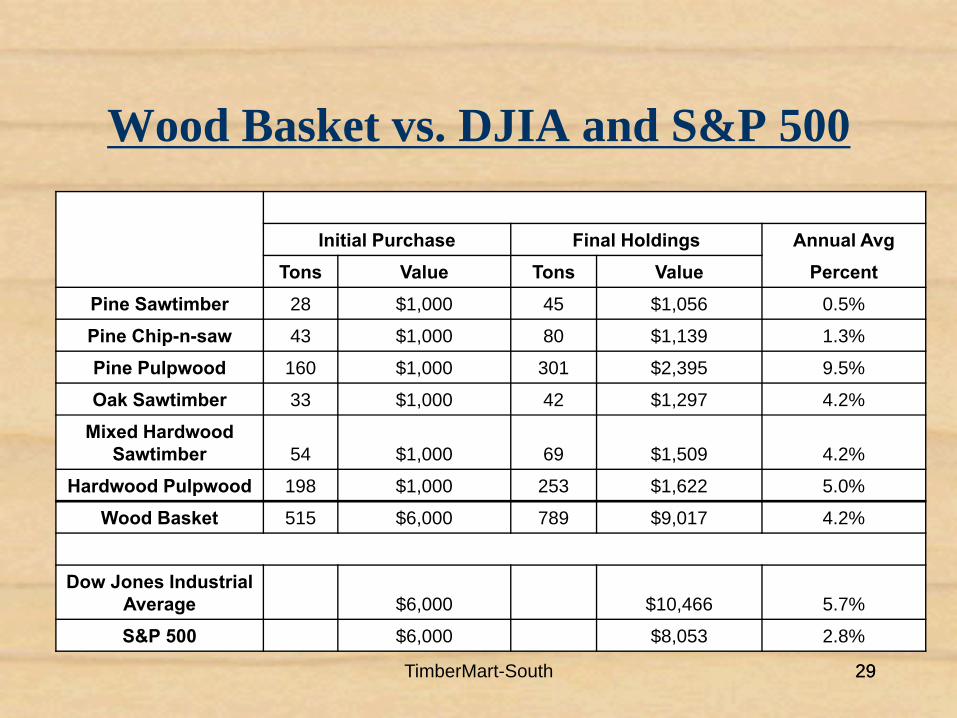

Wood Basket vs. DJIA and S&P 500

Initial Purchase Final Holdings Annual AvgTons Value Tons Value Percent

Pine Sawtimber 28 $1,000 45 $1,056 0.5%

Pine Chip-n-saw 43 $1,000 80 $1,139 1.3%

Pine Pulpwood 160 $1,000 301 $2,395 9.5%

Oak Sawtimber 33 $1,000 42 $1,297 4.2%

Mixed Hardwood Sawtimber 54 $1,000 69 $1,509 4.2%

Hardwood Pulpwood 198 $1,000 253 $1,622 5.0%

Wood Basket 515 $6,000 789 $9,017 4.2%

Dow Jones Industrial Average $6,000 $10,466 5.7%

S&P 500 $6,000 $8,053 2.8%

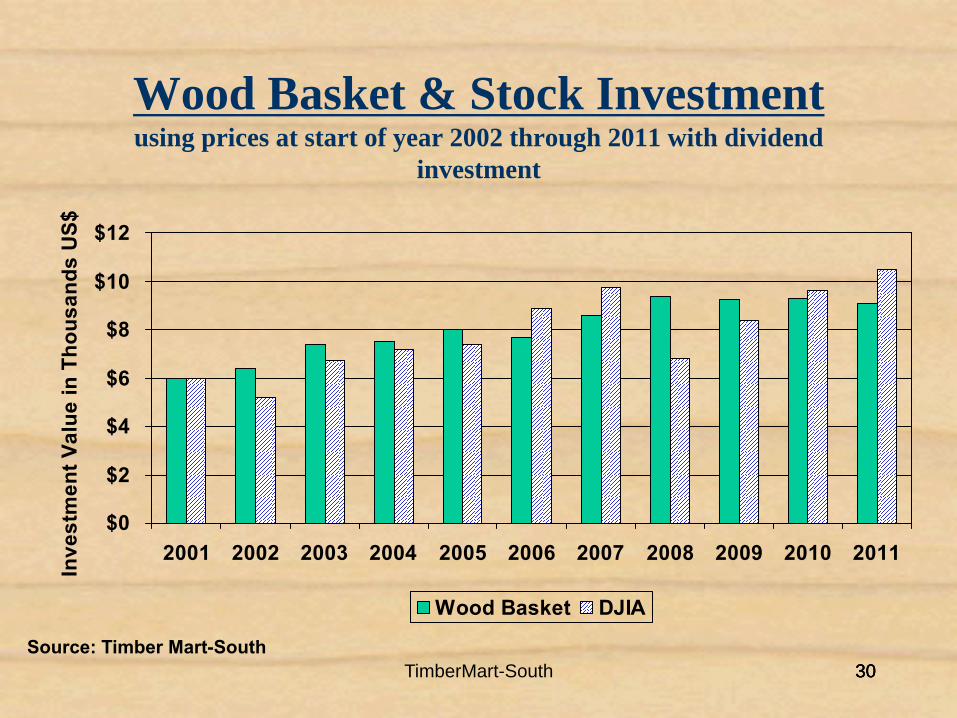

TimberMart-South 303030

Wood Basket & Stock Investmentusing prices at start of year 2002 through 2011 with dividend

investment

$0

$2

$4

$6

$8

$10

$12

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Inve

stm

ent V

alue

in T

hous

ands

US$

Wood Basket DJIA

Source: Timber Mart-South

TimberMart-South 31

The South’s Competitive Advantage

Favorable combination of:Location/Market Access

TerrainClimateSpecies

Wood QualityInfrastructureManagementGovernment

Private ownershipInvestment opportunities

TimberMart-South 32

Competitive Challenges:The U. S. South

• Changing Paper Demand• High Labor Costs• High Tax Rates• High Environmental Costs• Regulatory environment• Declining research base• Rising Neo-Druidism

TimberMart-South 33

Looking AheadSome Reponses:

• Research Re-direction toward Demand Side• Reject Neo-Druidism• Global Marketing Efforts

– Wood is Good– Southern Wood Promotions– Check Offs

• New Products?• New Manufacturing Capacity • Level Playing field

– Timber Access– Labor Practices

TimberMart-South 3434

Wood is Good

• Renewable• Available• Sustainable• Energy efficient• Versatile• Essential

TimberMart-South 35

Southern Timber TrendsForest Investment Outlook

Questions ?