time for action on apra changes - taylor fry … 2012 3 time for action on apra changes the road so...

TRANSCRIPT

Taylor Fry Newsletter on the APRA Capital Update February 20123

Time for action on APRA changesThe APRA capital standards review is now at a stage where you, as general insurers, can get a fair idea of the potential implications of the changes to your business ahead of implementation in 2013.

Many issues have been clarified since Taylor Fry’s updates in February and August 2011. APRA has undertaken a second Quantitative Impact Study (QIS2), called for insurer feedback and in December 2011 issued their response. Key draft prudential standards have also been released for comment.

APRA believes that the proposed capital standards will result in an overall reduction to industry solvency coverage and anticipates that insurers are already in the process of reviewing their business and capital management strategies in order to mitigate the impact of these proposed changes.

This newsletter is a timely summary for Board and senior management of insurers regarding the upcoming requirements of the ICAAP, the composition of capital base and the ICRC. We also discuss the implications of these changes and what insurers should be looking out for. Insurers must start to act now in order to be prepared for the changes that come into play on 1 January 2013. In our view, these are the most significant aspects of the revised proposals and, of course, you should also review the response for other potential impacts on your business.

APRAupdate

This newsletter at a glanceWe’ve analysed the current state of the APRA Capital Standards Review according to the following breakdown. Click on the headings below to read our analysis of what is coming and what you can do to prepare.

Time for action on APRA changes

The road so far 3

What came out of APRA’s review? 3

Critical milestones for insurers 4

ICAAP (Internal Capital Adequacy Assessment Process) 5

What’s coming up? 5ICAAP 5Supervisory adjustment 6

What needs to be done? 7

Composition of Capital Base 8

What’s coming up? 8

What needs to be done? 8

ICRC (Insurance Concentration Risk Charge) 9

What’s coming up? 9

What needs to be done? 11

SO, IN SHORT… 12

Any questions or feedback? Contact us 12

February 2012 12

February 2012 3

Time for action on APRA changes

The road so far

In December 2011 APRA released a response paper discussing the main issues from the last round of submissions on the March 2011 response paper and the results of QIS2. At the same time, they also released some key draft prudential standards. APRA has been carrying out industry-wide consultation since the first discussion paper was released in May 2010 and is currently seeking industry feedback on this most recent response paper and the draft prudential standards by 24 February 2012.

What came out of APRA’s review?

APRA’s second quantitative impact statement (QIS2) attracted a strong industry response, with contributions from 79 general insurers comprising 94% of the industry capital base. The response rate for Level 2 insurance groups was also high with 13 insurance groups participating, representing 95% of the capital base of this group.

APRA estimates that the new standards will affect the capital position of individual insurers to varying degrees, and that at an industry level there will be an overall reduction in solvency coverage. However, the reduction is less than predicted by the first QIS, due to subsequent refinements to the standards. Further refinements in the current APRA response paper are expected to only marginally improve industry solvency coverage compared to the QIS2 results.

Similar to the conclusion of the first QIS, the overall reduction in solvency coverage is mainly caused by an increase in the asset concentration risk charge and the introduction of the operational risk charge, but to a lesser extent than was indicated by the first QIS. There have also been some small increases resulting from asset risk charge and insurance concentration risk charge that are partially offset by the aggregation benefit.

Critical milestones for insurers

We believe the proposed changes are more or less in place and we do not anticipate any further major changes by APRA. The diagram below shows the critical milestones in the lead up to implementation of the new capital standards on 1 January 2013.

February 2012 14

Time for action on APRA changes

Insurers requesting transitional arrangements will be considered on a case-by-case basis. Any requests for transitional arrangements must be made to APRA before 30 September 2012, along with an appropriate rationale and details of the arrangements sought (such as the period over which transition will occur). In addition, you will need to provide details of the projected capital position as at 1 January from 2013 up to at least 2016.

Submissions due on response paper and draft prudential standards

Release of draft standards on measurement of capital (GPS112)

Submissions due on draft reporting standards released in June 2012

Release of draft reporting standards (including draft reporting forms and calculation workbook)

Release of remaining final prudential standards and draft Prudential Practice Guides (PPGs)

Release of final reporting standards

First reporting period for Level 1 general insurers

First reporting period for Level 2 general insurers

New standards effective

Submissions due on draft reporting standards released for consultation in March 2012 and May 2012

Release of final versions of key prudential standards and draft versions of other prudential standards with consequential changes

24 FEB 2012

24 FEB 2012 MAR 2012

MAR 2012AUG 2012

MAY 2012

MAY 2012

JUN 2012

JUN 2012

SEP 2012

OCT 2012

1 JAN 2013

JUL 2012

JUL 2012 AUG 2012 SEP 2012 OCT 2012 1 JAN 2013 1 JAN 2013 - 31 MAR 2013

1 JAN 2013 - 31 MAR 2013

1 JAN 2013 - 31 MAR 2013

1 JAN 2013 - 30 JUN 2013

ICAAP (Internal Capital Adequacy Assessment Process)

Insurers asked APRA for more information on the Internal Capital Adequacy Assessment Process (ICAAP) and on the process APRA will follow to determine the need for and amount of their supervisory adjustment (either within the calculation of the prescribed capital amount or outside the prescribed capital amount). APRA’s response can be found in Section 3 of their response document and in the draft version of GPS 110 (Capital Adequacy), the contents of which are discussed below.

What’s coming up?

ICAAPThe ICAAP is designed to capture insurers’ processes for assessing and managing target and actual capital levels, and to provide a more comprehensive picture of the insurer’s risks and their capital adequacy framework in light of these risks.

Existing capital management plans will be subsumed into the ICAAP, but APRA will still require a separate business plan to be completed. Appointed Actuaries (AA) will continue their responsibility for the Financial Condition Report (FCR) and the Insurance Liability Valuation Report (ILVR) whereas the ICAAP will be the responsibility of the Board of the insurer (although the AA will clearly be in a position to assist in putting it together).

ICAAP includes:

An articulation of the risk appetite/risk profile of the insurer

A description of the risk and capital management framework of the insurer, including the setting of target capital levels in light of the Board’s risk appetite

The ongoing Board and management oversight, risk assessment, monitoring and reporting of actual capital against the target capital policy

Details of the stress and scenario testing and capital projections used to develop the target capital levels and the ongoing capital management policy

Trigger points and associated actions (i.e. strategies for managing deviations from target capital levels, whether by raising additional capital, reducing dividend payments, or changing the risk profile and thereby reducing the capital requirements. The communication protocol with APRA should also be included), and

A process for undertaking an independent review of ICAAP, at a minimum of every three years. Note that the form of ‘target capital’ is not specified by APRA. While this could be a single target level of capital, a target capital range is also acceptable, and this may give the insurer greater flexibility in managing actual capital levels with respect to the target.

February 2012 5

Time for action on APRA changes

••

•

•

•

•

There are three distinct aspects to ICAAP:

The overall process and documentation thereof;

An annual ICAAP report that is submitted to APRA, detailing aspects such as forward three year capital projections and target levels, the application of ICAAP over the previous year and any changes in ICAAP or reviews of ICAAP since the previous annual ICAAP report; and

An ICAAP summary statement.

The ICAAP summary statement, which may form part of the ICAAP annual report, is intended to be a high level “road map” to the insurer’s ICAAP that informs the Board and APRA about the process itself as well as the process for the independent review of ICAAP.

Additional guidance on ICAAP will be issued by APRA through a Prudential Practice Guide (PPG) expected later this year.

Supervisory adjustmentUnder the new regime, there will be two kinds of supervisory adjustments that APRA may apply to an insurer:

A Pillar 1 adjustment applied within the calculation of the prescribed capital amount should APRA consider an adjustment warranted

A Pillar 2 adjustment applied separately from the prescribed capital amount, in the form of an increase to the Prudential Capital Requirement (PCR) and/or a strengthening of the composition of an insurer’s capital base.

In the March 2011 response paper, only a Pillar 2 adjustment was considered, and APRA was clear that “the supervisory adjustment, by its nature, cannot be negative” (it being designed to “address risks not covered in the prescribed capital amount”). In the December 2011 response paper, APRA recognised that the Pillar 1 adjustment “could result in an increase or decrease in the prescribed capital amount depending on the circumstances and nature of the adjustment”. While not explicitly stated, the Pillar 2 adjustment is presumably non-negative.

APRA will inform an insurer of any supervisory adjustment in writing including the reasons for the adjustment. However, an insurer is not permitted to disclose the supervisory adjustment.

APRA will issue a PPG to offer additional guidance on the process for determining supervisory adjustments, the nature of the adjustments that may be applied and the circumstances when an adjustment may be considered.

Generally, APRA can be expected to apply an adjustment if they consider there to be any unusual assets or liabilities that are not appropriately dealt with by the standards, or if they believe that the insurer has an incorrect or inappropriate interpretation of the standards.

The adjustments will be determined through a number of processes including but not limited to the full range of APRA’s supervision activities. These will generally be driven by circumstances as assessed by APRA that indicate weak governance, an ill-defined ICAAP, non-compliance of prudential standards, inappropriate allowance of risks or poor risk management to name a few.

February 2012 16

Time for action on APRA changes

1

2

3

•

•

APRAupdate

What needs to be done? Now that more details on the ICAAP have been released, we strongly advise that Board and senior management get started on the form and content of their ICAAP. As a starting point, it is imperative the Board can clearly articulate its risk appetite and the risk profile of the company. The current Risk Management Strategy (RMS) and Reinsurance Management Strategy (REMS) will no doubt provide a good starting point.

For companies with a 31 December balance date, the first ICAAP report is due on 30 April 2013. We suggest you commence resource planning as soon as possible in order to develop and complete the ICAAP with sufficient time for internal stakeholder review and feedback. Note that this is one month after the FCR is due (noting that delivery of the FCR has been brought forward by one month), which might present issues for the AA if there are aspects of the ICAAP that they would like to incorporate into the FCR which have not yet been finalised.

In planning for resources, the Board will need to consider who will be given responsibility for preparing and reviewing the ICAAP. The Chief Risk Officer will be a likely candidate, and the AA will also be well placed to add value in considering the types of stress and scenario testing required in assessing the appropriate level of target capital.

In terms of the implications of the supervisory adjustments, forewarned is forearmed. You should seek to assess your prescribed capital amount and review your capital base under the proposed requirements sooner rather than later. In this way, any unusual assets or liabilities that may potentially attract a supervisory adjustment will be recognised and mitigation actions, if necessary, can be planned ahead.

The Board should bear in mind that a comprehensive ICAAP, the ability to pre-empt problem areas and the preparedness of an insurer to address them, will most certainly lessen the likelihood and impact of a supervisory adjustment.

February 2012 17

Time for action on APRA changes

Composition of Capital Base

APRA issued a discussion paper for authorised deposit-taking institutions (ADIs) in September 2011 outlining its proposed implementation of the Basel III capital reforms for ADIs in Australia. The alignment of the composition of capital base for ADIs and general insurers had been foreshadowed in an APRA discussion paper (May 2010) and response paper (March 2011).

What’s coming up?

APRA formally proposed to align the composition of insurers’ capital base with the Basel III requirements for ADIs in its December 2011 response paper.

Under the Basel III definition of capital, total regulatory capital (i.e. capital base), net of regulatory adjustments, is defined as the sum of Tier 1 Capital comprising of Common Equity Tier 1 capital (CET1) and Additional Tier 1, and Tier 2 Capital.

Full details of the proposed requirements relating to the determination of capital base and detailed eligibility criteria of capital instruments is expected to be released in the draft GPS 112 in March 2012.

The proposed minimum capital base requirement that an insurer has to maintain at all times is:

CET1 must exceed 70% of the PCR;

Tier 1 capital must exceed 80% of the PCR; and

Capital base must exceed the PCR.

The limits are expressed as percentages relative to the PCR instead of the capital base. Effectively, this ensures insurers who have lower capital levels will have to hold a higher proportion of their capital bases in the highest quality forms of capital.

What needs to be done?

In order to meet the proposed requirements, you should immediately review your current capital base to determine the extent of compliance with the proposed minimum requirements. If there is any non-compliance, you can take action to address the imbalance before 1 January 2013. A good starting point is to become familiar with the proposed details of the criteria for assessing the components of the capital base for the proposed regulatory capital purposes as set out in Appendices 5 to 8 in the December 2011 response paper.

With the minimum regulatory capital requirements now defined, the Board and senior management can take these into consideration in developing the ICAAP. These requirements together with a comprehensive understanding of the risk profile and risk appetite of your business will enable you to set boundaries in determining the target level of capital base and trigger points. Your AA can suggest a range of stress and scenario testing that would be appropriate to examine these factors.

February 2012 18

Time for action on APRA changes

•••

ICRC (Insurance Concentration Risk Charge)

Compared to the current requirement for a Maximum Event Retention, the ICRC represents a significant increase in both the complexity of the calculation and the need to communicate with APRA in advance. This is not going to be straightforward, and your AA’s input will be required. In many cases, specific consultation and approval will be required from APRA before credit can be taken for the individual circumstances of each insurer.

As part of QIS2, APRA has comprehensively reviewed the appropriateness of the ICRC and concluded that no changes are required to its overall approach. Instead they have provided further clarification on some aspects of the calculation, and this additional guidance has only increased the complexity of the calculation. The main calculation issues are explored below.

Whilst the new capital regime won’t apply until after 1 January 2013, any reinsurance renewed during 2012 will determine the ICRC for 2013. Insurers need to immediately get to grips with the impact of the ICRC before placing their reinsurance for 2012/13.

What’s coming up?

Broadly, the ICRC represents the net financial cost of the maximum of one very large individual loss (1 in 200 year) event from a natural peril (Vertical Requirement), or the cost of a sequence of more frequent (1 in 10 year and 1 in 6 year) natural peril loss events (Horizontal Requirement). This includes allowance for recoveries, reinstatements and amounts already included in the premium liability risk charge. The diagram below provides an overview of the calculation.

You can find full details of the ICRC in Draft GPS 116, including a host of new acronyms to become familiar with. APRA may also add further guidance in a PPG.

February 2012 19

Time for action on APRA changes

APRAupdate

February 2012 10

Time for action on APRA changes

The ICRC is calculated as the maximum of the following four components:

Natural Perils Horizontal Requirement• Must be updated quarterly

• Gross of tax adjustment

• Higher of value on current and next RI program

Aggregate stop loss and catastrophe recoveries agreed with APRA

Risk charge on portion of premium liability provision relating to catastrophe costs

• Catastrophe events must occur less frequently than once every three months.

• Determined by Appointed Actuary and included in ILVR

Maximum of H3 and H4 amount

less Aggregate offset

less PL offset

Net cost of 3 times H3 loss or 4 times H4 loss• Including allowance for RI recoveries, reinstatement

premiums, and reinstatement costs

• Loss determined on whole of portfolio 10% (1 inten year - H3) or 16.7% (1 in six year - H4) probability of occurrence over one year

• Include non-modelled Risks

• Allow for portfolio growth

• Recoveries exclude aggregate stop loss andcatastrophe covers (see aggregate offset)

• Allow for any reinstatement premiums receivableon contractually binding netting arrangements with cedants

• Reinstatement cost of two losses (H3), three losses(H4). If no contractually agreed rates, estimate withno allowance for time expired and must at least be the full original cost.

• On a whole of portfolio 0.5% (1 in 200 year) probability of occurrence over one year

• Include non-modelled Risks

• Allow for portfolio growth

• Excluding aggregate stop loss and catastrophecovers (see Other Adjustments)

• Must have contractually binding netting arrangements with cedant

• Must have contractually agreed rates for one full reinstatement at start of year. Thereafter, estimate cost with no allowance for time expired, and must at least be the full original cost.

• Aggregate stop loss and catastrophe recoveriesagreed with APRA

Natural Perils Vertical Requirement• Must be updated quarterly

• Gross of tax adjustment

• Higher of value on current and next RI program

COMPONENT CALCULATION NOTES

Probable Maximum Loss

less RI Recoveries

less Reinstatement Premiums Receivable

plus Reinstatement Cost

less Other Adjustments

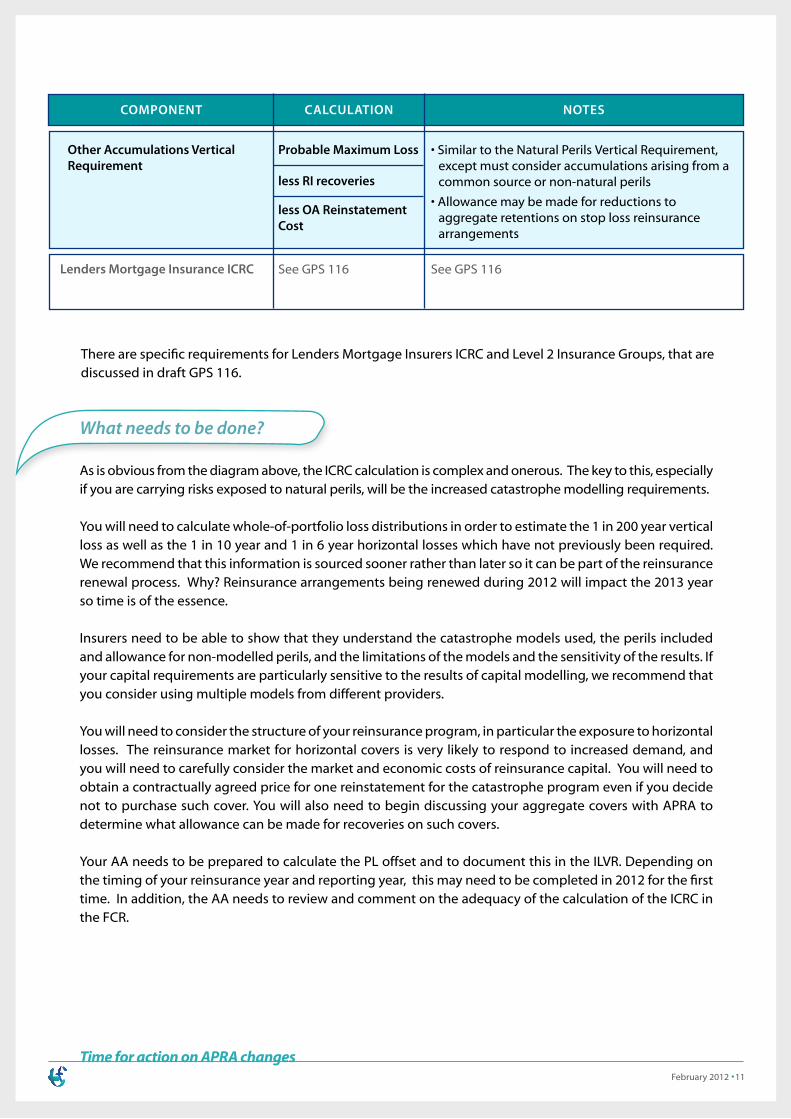

What needs to be done?

As is obvious from the diagram above, the ICRC calculation is complex and onerous. The key to this, especially if you are carrying risks exposed to natural perils, will be the increased catastrophe modelling requirements.

You will need to calculate whole-of-portfolio loss distributions in order to estimate the 1 in 200 year vertical loss as well as the 1 in 10 year and 1 in 6 year horizontal losses which have not previously been required. We recommend that this information is sourced sooner rather than later so it can be part of the reinsurance renewal process. Why? Reinsurance arrangements being renewed during 2012 will impact the 2013 year so time is of the essence.

Insurers need to be able to show that they understand the catastrophe models used, the perils included and allowance for non-modelled perils, and the limitations of the models and the sensitivity of the results. If your capital requirements are particularly sensitive to the results of capital modelling, we recommend that you consider using multiple models from different providers.

You will need to consider the structure of your reinsurance program, in particular the exposure to horizontal losses. The reinsurance market for horizontal covers is very likely to respond to increased demand, and you will need to carefully consider the market and economic costs of reinsurance capital. You will need to obtain a contractually agreed price for one reinstatement for the catastrophe program even if you decide not to purchase such cover. You will also need to begin discussing your aggregate covers with APRA to determine what allowance can be made for recoveries on such covers.

Your AA needs to be prepared to calculate the PL offset and to document this in the ILVR. Depending on the timing of your reinsurance year and reporting year, this may need to be completed in 2012 for the first time. In addition, the AA needs to review and comment on the adequacy of the calculation of the ICRC in the FCR.

February 2012 11

Time for action on APRA changes

There are specific requirements for Lenders Mortgage Insurers ICRC and Level 2 Insurance Groups, that are discussed in draft GPS 116.

• Similar to the Natural Perils Vertical Requirement, except must consider accumulations arising from a common source or non-natural perils

• Allowance may be made for reductions toaggregate retentions on stop loss reinsurance arrangements

Other Accumulations Vertical Requirement

Lenders Mortgage Insurance ICRC

Probable Maximum Loss

less RI recoveries

less OA Reinstatement Cost

See GPS 116 See GPS 116

COMPONENT CALCULATION NOTES

Any questions or feedback? Contact us

Consult ing Ac tuar ies &Analyt ics Profess ionals

Disclaimer

This newsletter is general in nature and provided for information purposes only. It does not constitute actuarial or investment

advice. In certain cases the discussion is based on incomplete information from APRA that is subject to change. We recommend

that you refer to APRA (www.apra.gov.au) for updated information regarding the proposed changes, and discuss your specific

circumstances with your Appointed Actuary, or the Taylor Fry contacts above.

Paul Driessenph: + 61 2 9249 2922e: [email protected]

Evelyn Chowph: + 61 2 9249 2919e: [email protected]

Samantha Fullerph: + 61 2 9249 2925e: [email protected]

Sharanjit Paddamph: + 61 2 9249 2914e: [email protected]

Sydney officeLevel 1155 Clarence StreetSydney NSW 2000ph: + 61 2 9429 2900fax: + 61 2 9249 2999e: [email protected]

Melbourne officeLevel 652 Collins StreetMelbourne VIC 3000ph: +61 3 9658 2333fax: + 61 3 9658 2344e: [email protected]

www.taylorfry.com.au

Now that APRA has released additional detail on the proposed capital standards, insurers should be preparing themselves for the changes as soon as possible, if they have not already done so. There is still time to consider the impacts of the changes and determine the best strategies to mitigate these impacts before implementation on 1 January 2013.

Here at Taylor Fry, we will continue to keep you posted on any further news and updates from APRA. If you would like to discuss any aspect of the capital standards review and its implications on your business, please contact your regular Taylor Fry Actuary, or one of the team listed below.

Until next time,

SO, IN SHORT...