title here (times new roman 42pt) - global … · loan-loss provisioning dr james cummings lecturer...

TRANSCRIPT

Loan-loss provisioning

Dr James Cummings

Lecturer

Faculty of Business and Economics

Macquarie University

June 2015

2 | © 2012 Global Association of Risk Professionals. All rights reserved.

Objectives

Forward-looking provisioning model

Evaluate the expected loss approach advocated by BCBS under Basel III

Examine the responsiveness of these provisions to credit risk

Role of regulatory provisioning in supporting capital requirements

Relationship with risk-based capital under the Basel rules

Explore the extent to which banks use provisioning for risk management

Basel II: Different rules for IRB banks

Direct linkage between provisioning and expected losses derived from a bank’s CRM

Test whether increased the incentives to use provisions for risk management

3 | © 2012 Global Association of Risk Professionals. All rights reserved.

Bank Discretionary Behaviour

Role of provisions in absorbing expected future credit losses

Provisioning varies with the business cycle (Bikker and Metzemakers, 2005)

Test the extent regulatory provisions reflect both problem loans and overall asset quality

Bank managers take account of capital adequacy and earnings

Capital management (Kim and Kross, 1998; Ahmed et al, 1999)

Income smoothing (Shrieves and Dahl, 2003; Hess et al, 2007)

Counter-cyclical explanation

Credit risk sown in a boom and materialises in a downturn (Bouvatier and Lepetit, 2008)

Test whether surplus regulatory capital and earnings used to cover future credit losses

4 | © 2012 Global Association of Risk Professionals. All rights reserved.

APRA’s Provisioning Model

Specific provisions

Credit losses expected in the short term (within 12-18 months)

Relevant factors clearly defined in the credit quality standard (APS 220)

General reserve for credit losses (GRCL)

Credit losses expected but not certain to arise over the full life of all the bank’s loans

Factors less clearly defined; requires subjective judgements

5 | © 2012 Global Association of Risk Professionals. All rights reserved.

Treatment of Provisions

Basel I banks and Basel II standardised banks

Impact on:

Tier 1 capital ratio

Numerator

Denominator

Net impact

Total capital ratio

Numerator

Denominator

Net impact

Basel II IRB banks

Impact on:

Tier 1 capital ratio

Numerator

Denominator

Net impact

Total capital ratio

Numerator

Denominator

Net impact

No impact on RWA

None (when in shortfall)

Shortfall

No impact on RWA

Total capital ratio

Retained earnings

Shortfall

No impact on RWA

Total capital ratio

Retained earnings

Shortfall (50%)

No impact on RWA

Tier 1 capital ratio

Retained earnings

Shortfall

Surplus (max 0.6% RWAC)

No impact on RWA

None

Shortfall (50%)

No impact on RWA

Step 2: EP non-defaulted

Impact of a one dollar increase in: Impact of a one dollar increase in:

Step 1: EL defaulted Step 2: EP defaulted

Tier 1 capital ratio

Retained earnings

Tier 1 capital ratio

Shortfall

Step 1: EL non-defaulted

No impact on RWA

Tier 1 capital ratio

Retained earnings

Shortfall (50%)

No impact on RWA

Tier 1 capital ratio

Shortfall (50%)

Impact of a one dollar increase in: Impact of a one dollar increase in:

RWA

Total capital ratio

No impact on RWA

None

Specific provisions GRCL

Retained earnings

No impact on RWA

Tier 1 capital ratio

Retained earnings

GRCL (max 1.25% RWA)

Retained earnings

RWA

6 | © 2012 Global Association of Risk Professionals. All rights reserved.

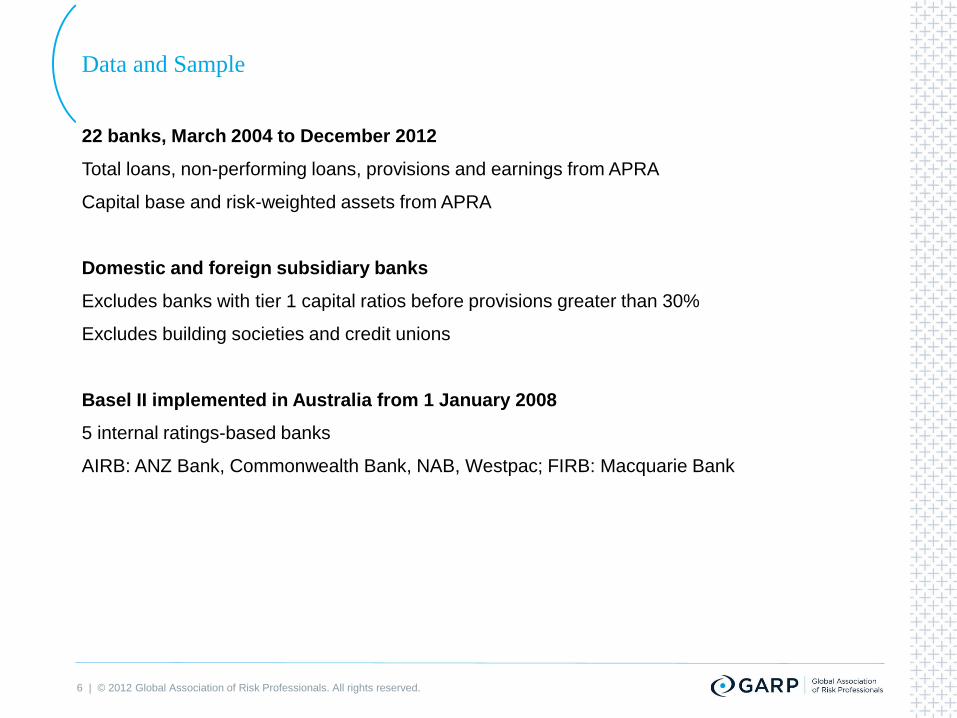

Data and Sample

22 banks, March 2004 to December 2012

Total loans, non-performing loans, provisions and earnings from APRA

Capital base and risk-weighted assets from APRA

Domestic and foreign subsidiary banks

Excludes banks with tier 1 capital ratios before provisions greater than 30%

Excludes building societies and credit unions

Basel II implemented in Australia from 1 January 2008

5 internal ratings-based banks

AIRB: ANZ Bank, Commonwealth Bank, NAB, Westpac; FIRB: Macquarie Bank

7 | © 2012 Global Association of Risk Professionals. All rights reserved.

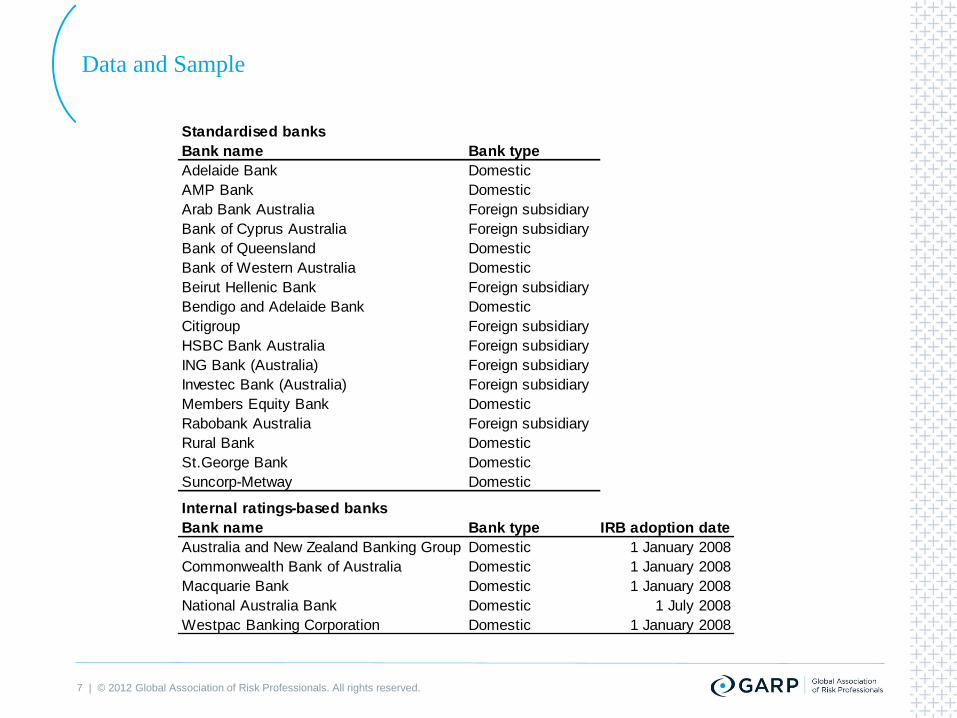

Data and Sample

Standardised banks

Bank name Bank type

Adelaide Bank Domestic

AMP Bank Domestic

Arab Bank Australia Foreign subsidiary

Bank of Cyprus Australia Foreign subsidiary

Bank of Queensland Domestic

Bank of Western Australia Domestic

Beirut Hellenic Bank Foreign subsidiary

Bendigo and Adelaide Bank Domestic

Citigroup Foreign subsidiary

HSBC Bank Australia Foreign subsidiary

ING Bank (Australia) Foreign subsidiary

Investec Bank (Australia) Foreign subsidiary

Members Equity Bank Domestic

Rabobank Australia Foreign subsidiary

Rural Bank Domestic

St.George Bank Domestic

Suncorp-Metway Domestic

Internal ratings-based banks

Bank name Bank type IRB adoption date

Australia and New Zealand Banking Group Domestic 1 January 2008

Commonwealth Bank of Australia Domestic 1 January 2008

Macquarie Bank Domestic 1 January 2008

National Australia Bank Domestic 1 July 2008

Westpac Banking Corporation Domestic 1 January 2008

8 | © 2012 Global Association of Risk Professionals. All rights reserved.

Descriptive Statistics

All banks, N=744

Data item Mean

Standard

deviation

Lower

quartile Median

Upper

quartile

Total loans $mil 62,327 102,602 3,375 12,953 48,581

Loans to households % 57.6 29.2 43.3 63.0 76.9

Loans to corporates % 42.0 29.1 21.7 36.7 55.3

Loans to other % 0.4 0.8 0.0 0.0 0.5

Non-performing loans % 2.00 2.64 0.61 1.06 2.10

RWA for credit risk % 95.3 46.7 70.4 86.7 103.2

Deposits % 19.8 14.7 8.8 18.9 28.7

Specific provisions % 0.38 0.53 0.06 0.17 0.47

GRCL % 0.57 0.35 0.33 0.52 0.78

Total provisions % 0.95 0.75 0.47 0.76 1.18

Tier 1 capital ratio 11.0 4.0 8.3 9.9 12.3

Total capital ratio 13.4 3.6 11.2 12.3 14.5

EBPT % pq 0.34 0.45 0.18 0.30 0.42

9 | © 2012 Global Association of Risk Professionals. All rights reserved.

Descriptive Statistics

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Pro

vis

ion

s (

% o

f to

tal lo

an

s)

Year

All banks: Regulatory loan-loss provisions by type

GRCL Specific provisions

Basel I Basel II

10 | © 2012 Global Association of Risk Professionals. All rights reserved.

Provisioning: All Banks

Effects of credit risk, capital adequacy and earnings

Panel regression:

PROVi,t = ratio of provisions (specific provisions, GRCL or total provisions) to total loans

NPLi,t = non-performing loans / total loans

RWACi,t = ratio of credit RWA before provisions to total loans - 1

GDPGRt = growth of real GDP over the past year

BCONFt = NAB business confidence index

RT1CAPi,t = tier 1 capital ratio before provisions (actual - required)

EBPTi,t = earnings before provisions and taxes / average assets

LOGSIZEi,t = logarithm of total loans in billions of Australian dollars

DEPi,t = total deposits / total loans

tititititi

tttitiiti

DEPLOGSIZEEBPTRT1CAP

BCONFGDPGRRWACNPLPROV

,,3,2,1,

43,2,1,

11 | © 2012 Global Association of Risk Professionals. All rights reserved.

Provisioning: All Banks

Independent variables

NPL (β1) 0.1578 ** (13.38) 0.0191 ** (4.70) 0.1769 ** (15.86)

RWAC (β2) 0.0004 (0.57) 0.0028 ** (4.83) 0.0031 ** (4.36)

GDPGR (β3) -0.0038 (-0.34) -0.0448 ** (-4.48) -0.0486 ** (-3.09)

BCONF (β4) -0.0008 (-0.51) -0.0001 (-0.11) -0.0009 (-0.47)

RT1CAP (ϕ1) 0.0165 ** (4.72) 0.0143 ** (4.35) 0.0308 ** (5.38)

EBPT (γ1) -0.0039 (-0.11) 0.0307 ** (2.15) 0.0268 (0.79)

Log size (γ2) 0.0006 ** (2.24) 0.0004 (0.98) 0.0010 (2.01)

Deposits (γ3) -0.0039 ** (-4.10) -0.0025 ** (-2.30) -0.0064 ** (-3.53)

Bank intercepts Yes Yes Yes

Adj. R 2 0.78 0.70 0.78

Banks 22 22 22

Observations 744 744 744

Numbers in parentheses are t -statistics. ** indicates significance at the 5% level.

SPROV LLPGRCL

Dependent variables

12 | © 2012 Global Association of Risk Professionals. All rights reserved.

Further Analysis for IRB Banks

Descriptive statistics, N=98

Data item

Eligible provisions

Mean %

Median %

Standard deviation %

Expected losses

Mean %

Median %

Standard deviation % 1.68

1.28

1.13 2.010.88

1.30

0.53

0.45

0.72

Defaulted

exposures

Non-defaulted

exposures Total

0.83 0.53 1.37

0.46 0.47 0.90

0.80 0.23 0.98

13 | © 2012 Global Association of Risk Professionals. All rights reserved.

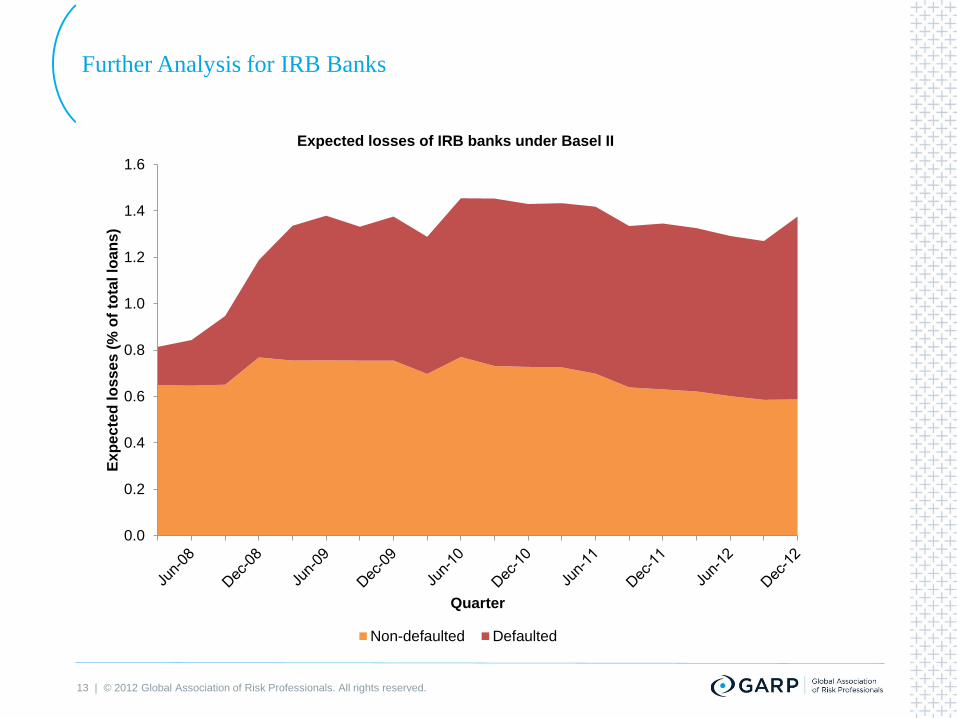

Further Analysis for IRB Banks

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Exp

ecte

d lo

sses (

% o

f to

tal lo

an

s)

Quarter

Expected losses of IRB banks under Basel II

Non-defaulted Defaulted

14 | © 2012 Global Association of Risk Professionals. All rights reserved.

Further Analysis for IRB Banks

0

5

10

15

20

25

30

0

10

20

30

40

50

60

70

80

90

100

Cap

ital (%

of

RW

A)

Eli

gib

le p

rovis

ion

s (

% o

f E

L)

Quarter

Eligible provisions and bank capital ratios before provisions

Tier 1 capital Tier 2 capital Total EP

15 | © 2012 Global Association of Risk Professionals. All rights reserved.

Further Analysis for IRB Banks

Independent variables

NPL 0.4325 ** (12.39) 0.0189 (0.84) 0.4514 ** (12.46)

T1CAPTA 0.1832 ** (3.02) 0.1388 ** (5.91) 0.3220 ** (5.90)

EBPT 0.1184 (0.66) -0.2075 (-1.75) -0.0891 (-0.52)

Bank intercepts Yes Yes Yes

Adj. R 2 0.96 0.84 0.97

Banks 5 5 5

Observations 98 98 98

Numbers in parentheses are t -statistics. ** indicates significance at the 5% level.

Dependent variables

ELtot / TLELdef / TL ELnon-def / TL

16 | © 2012 Global Association of Risk Professionals. All rights reserved.

Further Analysis for IRB Banks

Independent variables

RT1CAP 0.9895 (0.53) 5.2613 ** (4.10) 3.7937 ** (3.72)

EBPT -2.5055 (-0.28) -0.4804 (-0.11) -4.2600 (-0.79)

Bank intercepts Yes Yes Yes

Adj. R 2 0.43 0.54 0.55

Banks 5 5 5

Observations 98 98 98

Numbers in parentheses are t -statistics. ** indicates significance at the 5% level.

Dependent variables

EPdef / ELdef EPnon-def / ELnon- EPtot / ELtot

17 | © 2012 Global Association of Risk Professionals. All rights reserved.

Conclusion

Banks use the regulatory provisioning model for risk management

Provisions reflect problem loans, inherent asset quality and macroeconomic conditions

Part of surplus capital and above-average earnings allocated to fund future credit losses

Internal ratings-based banks

Use freshly raised capital for replenishing provisions after IRB adoption

Loss expectations may be influenced by capital adequacy

Allocate more provisions against EL when tier 1 capital ratios are stronger

Creating a culture of

risk awarenessTM

Global Association of

Risk Professionals

111 Town Square Place

Suite 1215

Jersey City, New Jersey 07310

USA

+ 1 201.719.7210

2nd Floor

Bengal Wing

9A Devonshire Square

London, EC2M 4YN

UK

+ 44 (0) 20 7397 9630

www.garp.org

About GARP | The Global Association of Risk Professionals (GARP) is a not-for-profit global membership organization dedicated to preparing professionals and organizations to make

better informed risk decisions. Membership represents over 150,000 risk management practitioners and researchers from banks, investment management firms, government agencies,

academic institutions, and corporations from more than 195 countries and territories. GARP administers the Financial Risk Manager (FRM®) and the Energy Risk Professional (ERP®)

exams; certifications recognized by risk professionals worldwide. GARP also helps advance the role of risk management via comprehensive professional education and training for

professionals of all levels. www.garp.org.

© 2012 Global Association of Risk Professionals. All rights reserved.