title industry panel discussion. agenda i.introduction monica wittrock, senior vice president, first...

TRANSCRIPT

Title Industry Panel Discussion

Agenda

I. IntroductionMonica Wittrock, Senior Vice President, First American Title Insurance Company

II. “Quoting” Title Insurance and Settlement FeesDawn Lewallen, Compliance Counsel/Senior Underwriter, Stewart Title Guaranty Company

III. “Delivery” of the Closing DisclosureDavid Patrick, Business Development, Capitol Abstract & Title Company

IV. “Collaborating” between the Title Company and the LenderMonica Wittrock, Senior Vice President, First American Title Insurance Company

V. The Title Company’s “Closing Statement”Vanessa Shadix, Agency Representative, Old Republic National Title Insurance Company

“QUOTING” TITLE INSURANCE AND SETTLEMENT FEES

Dawn Lewallen

Title Fee Estimates - 12 CFR §1026.37 (f)

• The amount imposed upon the consumer (or seller) for any settlement service must not exceed the amount actually received by the settlement service provider for that service – unless it is an Average Charge.

• Creditors may estimate disclosures using the best information reasonably available when the actual term or cost is not reasonably available to the creditor at the time the disclosure is made.

• Creditors must act in good faith and use due diligence in obtaining the information.

Title Insurance Fees and Charges• All title insurance charges and title fees

including title search fees, settlement agent fees, commitment binder fees, etc must be set out on both the Loan Estimate and Closing Disclosure and must proceeded by: “Title – [description of fee]”.

• All fees and charges must be separately

itemized. Fees and charges must be listed alphabetically.

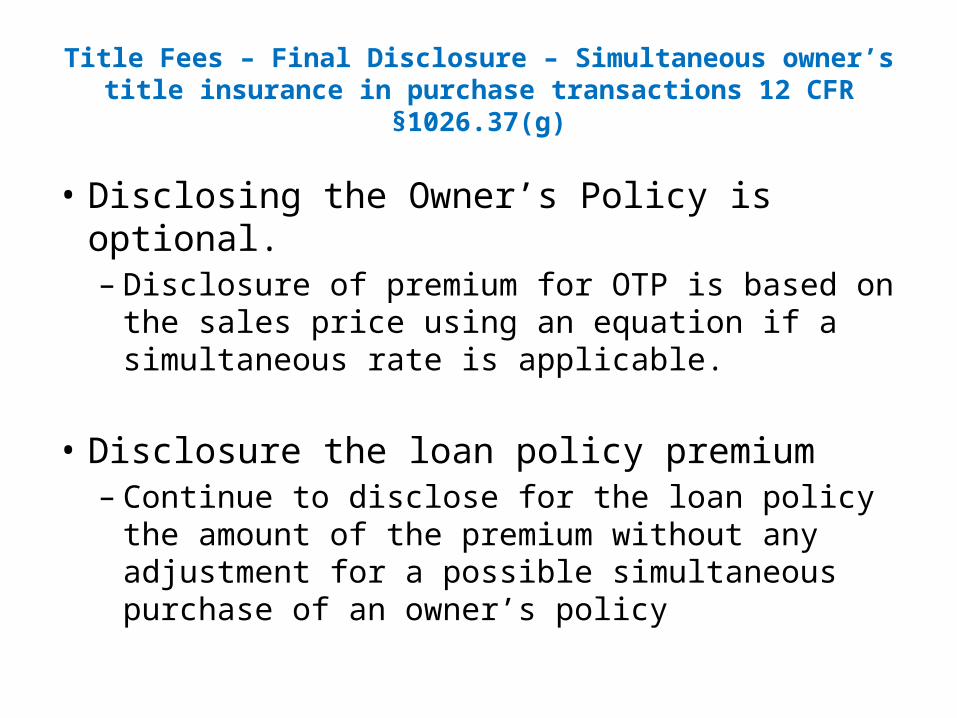

Title Fees – Final Disclosure – Simultaneous owner’s title insurance in purchase transactions 12 CFR §1026.37(g)

• Disclosing the Owner’s Policy is optional.– Disclosure of premium for OTP is based on the sales

price using an equation if a simultaneous rate is applicable.

• Disclosure the loan policy premium– Continue to disclose for the loan policy the amount

of the premium without any adjustment for a possible simultaneous purchase of an owner’s policy

7

8

The Problem - The TRID requires the lender or settlement agent to inaccurately disclose the title premiums on the Closing Disclosure.

Why is this a problem? – In roughly half the states, a consumer is entitled to discount on loan title insurance policy when an owner’s policy will be simultaneously issued.

How does the Rule handle:• Regardless of lower, actual simultaneous issue rate for Lender’s

Policy (LTP), pricing to be shown at full rate (even on CD)• If an Owner’s Policy (OTP) is also purchased, rate shown for OP

is in accordance with CFPB formula – again, not the actual rate charged

Title Insurance Concerns on the Loan Estimate and Closing Disclosure

Title Insurance Charges on the Loan Estimate and Closing Disclosure (cont.)

Buyer-Pay Location

Title Insurance Charges on the Loan Estimate and Closing Disclosure cont.

Seller-Pay Location

Title Insurance Charges on the Loan Estimate and Closing Disclosure cont.

Seller-Pay Location

Impact of rule of AfBAs

• Fees charged by affiliates of the creditor are in the “zero tolerance” or no variation bucket. 12 CFR §1024.7.

• If you are an affiliate of a lender, you may be included on the lender’s Settlement Service Provider List. Remember, your inclusion on this list is equal to a referral of business to you as the affiliate.

“DELIVERY” OF THE CLOSING DISCLOSUREDavid Patrick

DELIVERY OF THE CLOSING DISCLOSURE

New rules require that the lender deliver the Closing Disclosure at least 3 business days before consummation of the loan transaction.

Who is responsible for delivery of the Closing Disclosure?

Can the lender delegate that responsibility?

How can delivery be made?

Mail – Safe Harbor for Mail Delivery Hand Delivery Electronic Delivery Audit Trail – How do you document the delivery

for the auditors and examiners? Does each borrower receive a Closing

Disclosure?

Waiting Periods

• Delivery Period – Three Business Days for all Delivery other than hand delivery

• Waiting Period – Three Business Days after Delivery occurs. Begins after Delivery Period above.

• Rescission Period – Three Business Days after signing for most refinance transactions.

Restart the Waiting Period

Changes to the Closing Disclosure that would require the transaction to begin another three day waiting period.

Change in loan programChange in APR of over an eighth of a percentAddition of a prepayment penalty

“COLLABORATING” BETWEEN THE TITLE COMPANY AND THE LENDER

Monica Wittrock

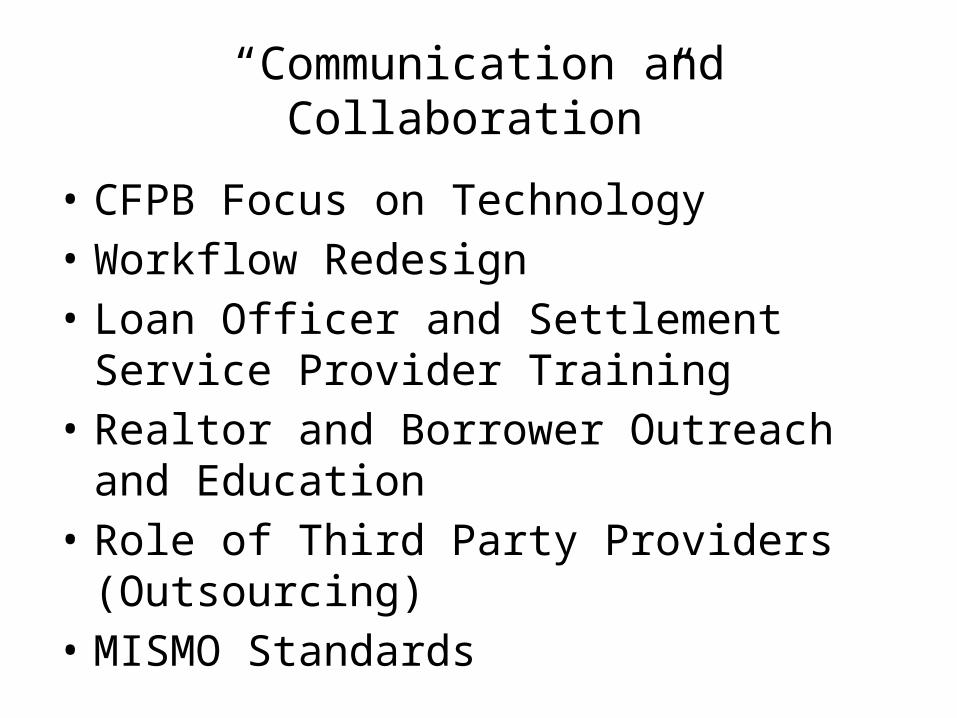

“Communication and Collaboration”

“Communication and Collaboration”

• CFPB Focus on Technology• Workflow Redesign• Loan Officer and Settlement Service Provider

Training• Realtor and Borrower Outreach and Education• Role of Third Party Providers (Outsourcing)• MISMO Standards

“Communication and Collaboration”

• Changes at the Closing Table – “Real Time” Coordination between Lenders and Settlement Providers

• Possible Gaps in the Process• Compliance:– Operational– Transactional– Vendor Management

“Communication and Collaboration”Collecting Information

• How will you be collecting information relating to the estimated title and escrow fees for your Loan Estimate?

• How do you envision managing "Variances" relating to any data/fee changes from the final Loan Estimate to the Closing Disclosure or Corrected Closing Disclosure within the closing package?

“Communication and Collaboration”Communication with Borrower

• Will you be issuing the CD to the Borrower?• How will you notice the Title Company that the

CD has been delivered and/or received?• If yes (Lender issued CD), will you have the Title

Company issue any corrected CDs at and/or after closing? Or will you issue the corrected CD's?

• If no (Title Company issued CD) , what proof will you require to show that the CD has been delivered and by what method?

“Communication and Collaboration”Communication with Borrower

• Will you be obtaining the Borrower's signature on the CD?

• What have you determined the date of consummation to be? What event will you use in timing the delivery of the Closing Disclosure? (i.e. date borrower signs, date the loan funds, date security instrument records, date loan funds are disbursed, etc.).

“Communication and Collaboration”Naming of Title Company Fees

• Are you familiar with MISMO standards for the naming of fees? Will you be using MISMO names?

“Communication and Collaboration”System Readiness

• What LOS do you use?• Are you working with your software vendor to

generate a new Loan Estimate?• Are you working with your software vendor to

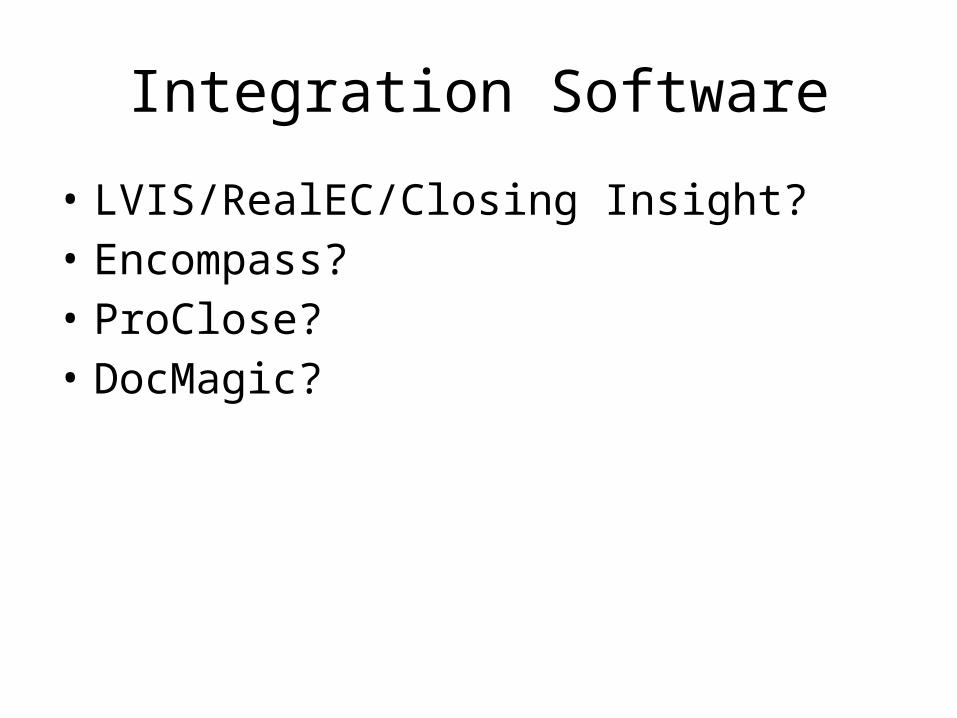

generate a new Closing Disclosure?• Do you anticipate using "integration" software

to collaborate / communicate with the Title Company? Is so, which software?

• Cost??

Integration Software

• LVIS/RealEC/Closing Insight?• Encompass?• ProClose?• DocMagic?

“Communication and Collaboration”

OR

THE TITLE COMPANY’S “CLOSING STATEMENT”

Vanessa Shadix