tn specific ethics 2 hours cpe hr tn specific ethics_haddock.pdf · 5. understand how complaints...

TRANSCRIPT

TN Specific Ethics2 Hours CPEDavid Haddock, EdD,CPA

2

Rules & Regulations

Tennessee Board of Accountancy

3

Today’s Objectives

1. Know how members of TN State Board of Accountancy are appointed

2. Know individual and firm rules for licensing

3. Understand CPE rules

4. Review AICPA Code of Professional Conduct

5. Understand how complaints are handled

4

Quiz Question

New Members of the Accountancy Board are selected by:

a. The Governor

b. The AICPA

c. Current members of the Board

d. A secret committee that meets in Nashville

e. A random drawing that includes all active Licensees

5

TN Board of Accountancy

• Chairman—C. Don Royston, (East TN)

• Vice-Chair—Casey Stuart, (East TN)

• Secretary—Stephen M. Eldridge (West TN)

Total of 11 members

• Nine must be CPAs

• One attorney

• One public member

6

TN Board of AccountancyPurpose

Legislatively charged to protect public by

>licensing CPAs/firms

>regulating conduct of CPAs

>prohibiting misleading titles/competencies

7

SBOA Appointments

• By governor for 3 year staggered terms

• Each Grand Division is equally represented

• Quarterly meetings-open to public (see website)

8

SBOA Oversight

CPA license

-individual

-firm

Investigate complaints

SBOA Attorney advises board not individual CPAs

http://tennessee.gov/

commerce/boards/tnsba/

9

Top 5 Problem Areas:

1. License renewal2. Firm permit renewal3. Continuing Professional Education4. Peer Review5. Professional Privilege Tax

9

10

TN Board of Accountancy

Executive DirectorWendy Garvin

500 James Robertson Parkway, Nashville, TN 37243-1141

615-741-2550 or 888-453-6150

11

Becoming a CPA in TN

Certificate of “certified public accountant” granted to:

• Persons of good moral character

• Persons meeting education, experience and examination requirements

12

Education

• At least 150 hours semester hours

• Holder of at least a baccalaureate degree from a college acceptable to TSBOA

• Educational program includes minimum 30 semester hours of accounting

13

Apply for License

• Pass the Exam!!

• Meet minimum 1 year experience

• Complete AICPA Ethics course

• Submit all forms/fees

14

Experience

Individuals seeking initial licensure must have one (1) year of experience

15

Reciprocity

TN recognizes the holder of a CPA license from any state which has been verified to be in substantial equivalence with the licensure requirements of the Tennessee Accountancy Act

Individual is granted all privileges of a TN CPA without need to obtain certificate or permit from TN

16

License Period and Fees

Period

• TN grants a 2 year license

• CPE is also reported for a 2year period

License Fees-Individuals

• Professional privilege tax is administered by the TN Department of Revenue

• Permit to practice fees due to TSBOA upon licensure renewal application

17

After Licensing

Renew Every 2 years

• 80 hours of appropriate CPE

• Pay license fee

• Notify SBOA of any changes (name, address, etc. w/in 30 days)

• Home, mailing, & business address

Make the Big Bucks!!

18

Address Changes Are Important

To communicate with you!

Business, home, mailing, & email

Must notify within 30 days of move—could cost you $$ if you don’t!!

19

Change in License Status

Inactive—removes you from CPE requirement, still have to register; cannot provide any public accounting services

May Smith, CPA (Inactive)

Retired—age 55+; not performing any public accounting services; still must register if using title

May Smith, CPA (Retired)

Age 70+; no renewal fee

20

TN CPE Rules

Basic Biennial Rules

1. At least 80 hours of CPE

2. Minimum of 20 hours in each year

3. At least 40 hours in accounting, accounting ethics, attest, taxation, or management advisory services

21

Qualifying Program

• Must contribute to professional competence

• Meet standards approved by AICPA and NASBA

22

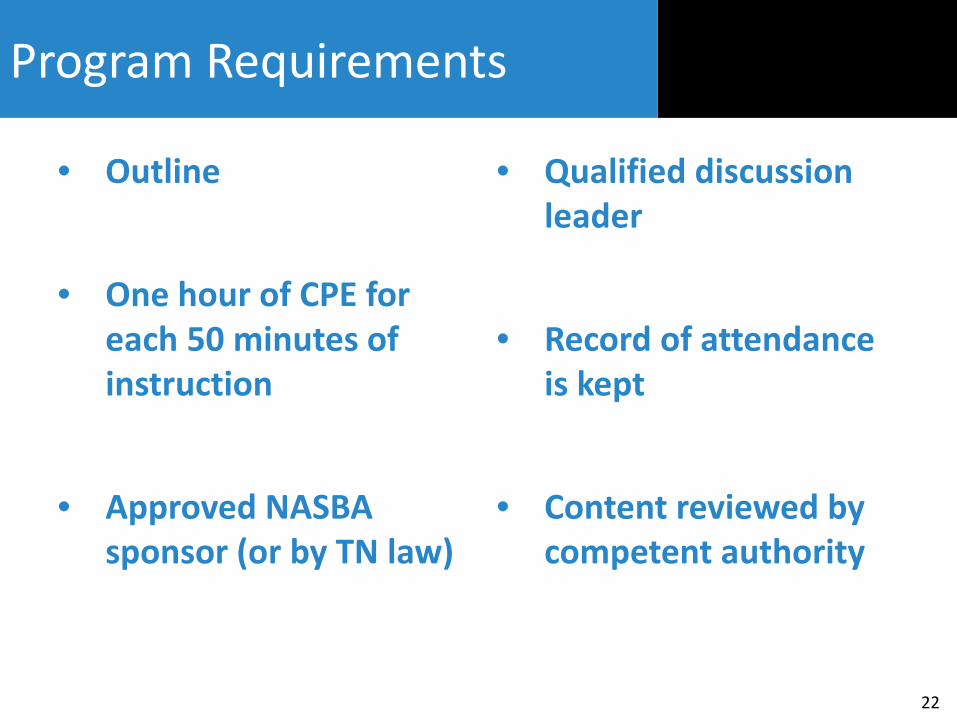

Program Requirements

• Outline

• One hour of CPE for each 50 minutes of instruction

• Approved NASBA sponsor (or by TN law)

• Qualified discussion leader

• Record of attendance is kept

• Content reviewed by competent authority

23

By Rule, Qualified Programs

• AICPA/TSCPA and chapters of TSCPA

• Technical sessions of meetings of AICPA, TSCPA, NASBA

• University or college courses

• Programs recognized by TN SBOA

• Organized in-firm or in-house programs offered without charge

24

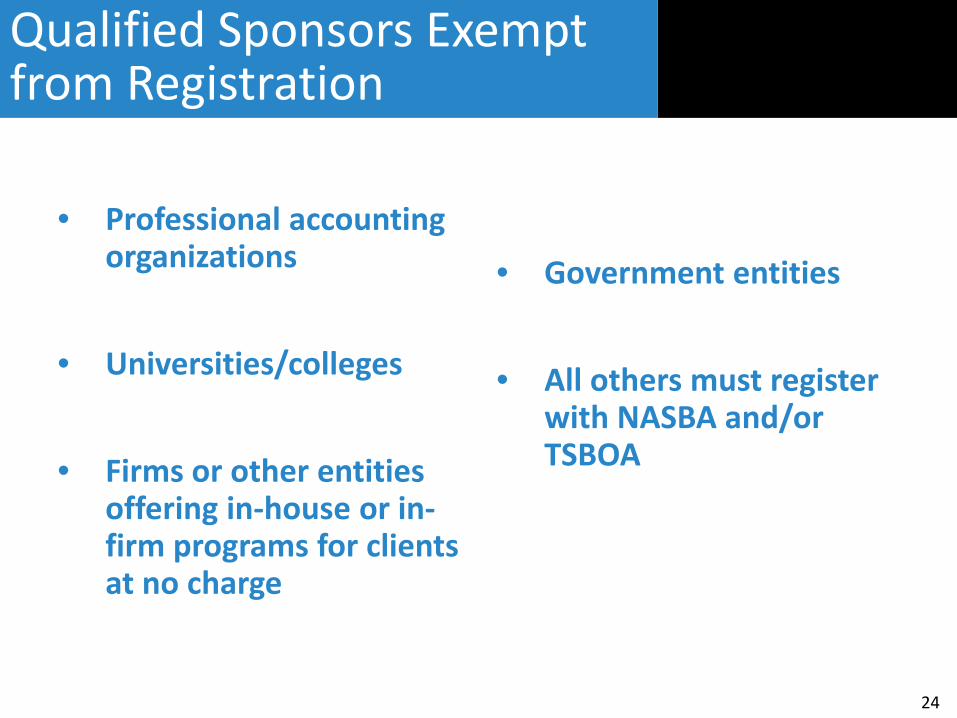

Qualified Sponsors Exempt from Registration

• Professional accounting organizations

• Universities/colleges

• Firms or other entities offering in-house or in-firm programs for clients at no charge

• Government entities

• All others must register with NASBA and/or TSBOA

25

Reporting of CPE

Affirmed biennially (every 2 years) w/renewal (“check the box”)

Even/odd reporting year requirement based on last digit of license number

Minimum of 80 hours each 2 year period (minimum 20 hours in one year)

26

CPE Audit

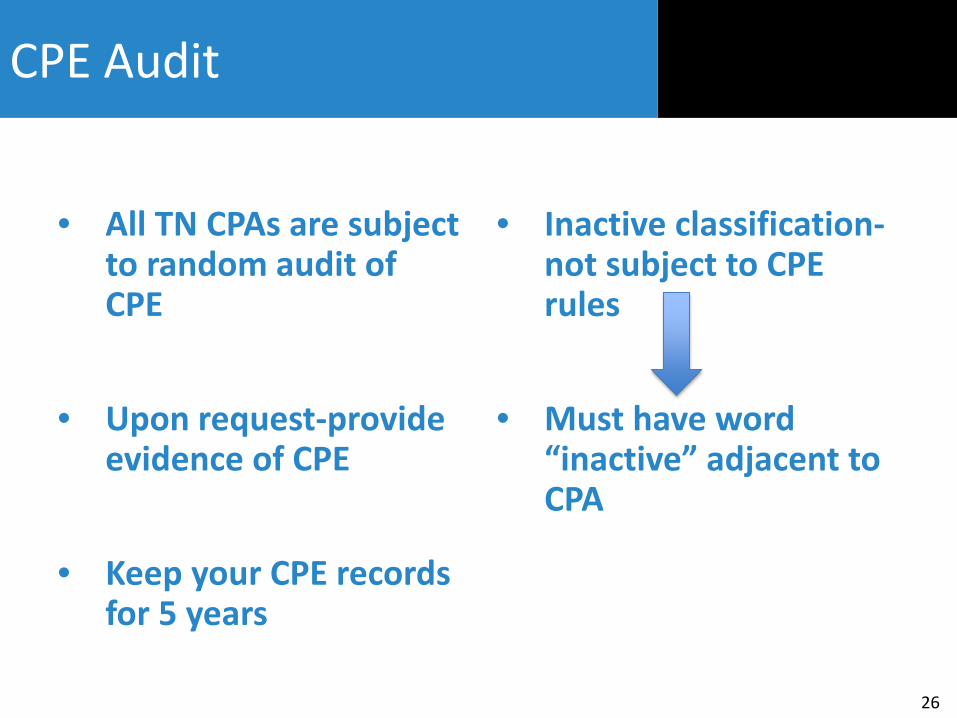

• All TN CPAs are subject to random audit of CPE

• Upon request-provide evidence of CPE

• Keep your CPE records for 5 years

• Inactive classification-not subject to CPE rules

• Must have word “inactive” adjacent to CPA

27

Failure to Meet Rules

• Penalty of additional CPE may be assessed (8 or more hours)

• Must be completed within 180 days of notice

• Extension may be granted to meet CPE

28

Additional CPE Requirements

• 2 hours of TN Specific Ethics

• If providing attest functions, at least 20 hours, biennially, in A&A

• Expert witness must have at least 20 hours in field of expertise

• Carry forward of 24 hours but not as specific content hours

29

Other Licensing Issues

Delinquent-failed to renew w/fee payment but still practicing

Expired-individual or firm that chooses not to renew and surrenders the license to SBOA

Reactivate-if “inactive”--needs 80 hrs of CPE during prior 24 month period

Reinstate-action requested following Board revocation of license

Lapse--80 hrs CPE in 6 mos/penalty hrs

30

Firm License

• Every firm providing services covered by the Tennessee Accountancy Act must register with the TSBOA

• Sole proprietorship is a firm

• Must pay annual registration/renewal fee

• Must maintain current address, partners, etc

• Firm must be majority owned by CPAs

31

Complaints Against Firms/CPAs

• Must be formal complaint citing failure of professional

• Firm/CPA is given opportunity to respond

• Board (with legal advice) will take appropriate action

Complaint made

Firm response

SBOA action

32

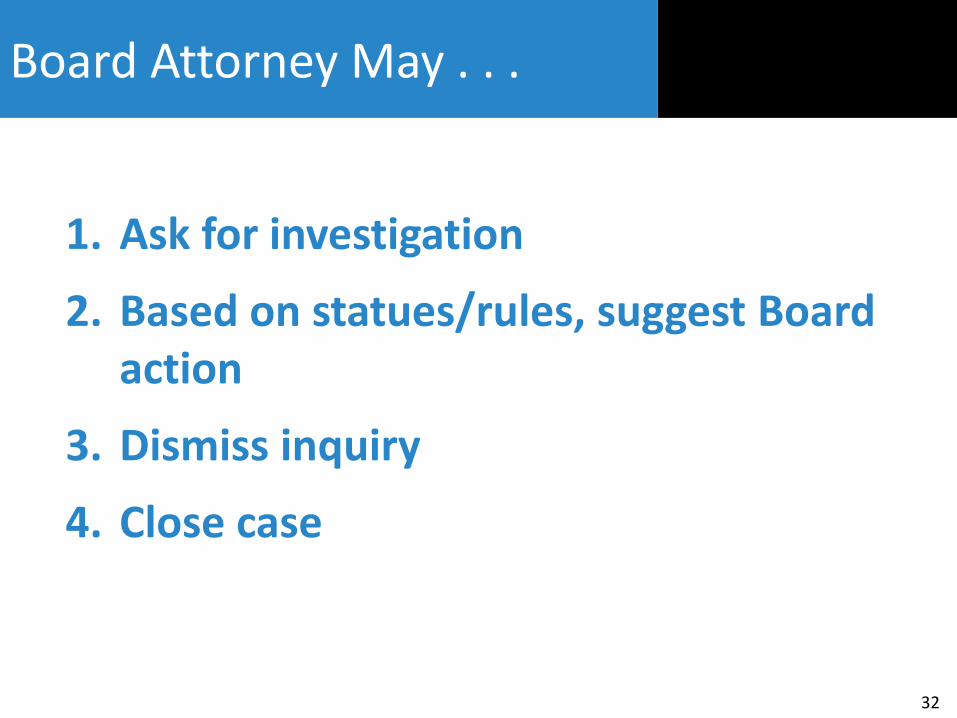

Board Attorney May . . .

1. Ask for investigation

2. Based on statues/rules, suggest Board action

3. Dismiss inquiry

4. Close case

33

Peer Review

Each firm in TN performing attest services will submit to a peer review at least once every three years

Review may be conducted by PCAOB, TSCPA, or AICPA

34

Results of Peer Review

• Results are communicated to firm

• If sub-standard, may require remediation

• Board may take further action if firm ignores or refuses to comply with review recommendation

35

What’s New?

• Reciprocity-49 states now honor individual CPA license

• Board may recognize substantially equivalent foreign designation

• Visit NASBA site for current info

• AICPA-is offering exam internationally

36

Setting Ethical Standards

• SEC—given federal statutory authority to define auditor independence

• PCAOB—given responsibility for ethics & independence rules for auditors of public companies

• AICPA—Code of Professional Conduct

37

Points to Ponder

1. It’s not about losing your license or going to jail—it’s about losing your integrity!!

38

1. It’s not about losing your license or going to jail—it’s about losing your integrity!!

2. Temptation is real, so how do you avoid temptation?

Points to Ponder

39

1. It’s not about losing your license or going to jail—it’s about losing your integrity!!

2. Temptation is real, so how do you avoid temptation?

3. Rationalization is a powerful temptation to be avoided at all costs.

Points to Ponder

40

END OF 1ST HOUR

Part 2Tennessee Specific Ethics 2016

41

AICPA Code of Professional Conduct

Revised January 28, 2014—generally effective 12/31/2014

Organized by topics

Conceptual framework for public and private CPAs

42

Preamble to COPC

• express the profession's recognition of its responsibilities to the public, to clients, and to colleagues

• guide members in the performance of their professional responsibilities

• express the basic tenets of ethical and professional conduct

43

Code of Professional Conduct

Calls for “. . . An unswerving commitment to honorable behavior, even at the sacrifice of personal advantage.”

ET 51.02

44

Threats/Safeguards

45

Basic Principles of Code of Professional Conduct

1. Responsibilities

2. Public interest

3. Integrity

4. Independence

5. Due care

6. Scope and nature of service

46

General Standards

A. Professional Competence

B. Due Professional Care

C. Planning and Supervision

D. Sufficient Relevant Data

47

General Standards

A. Professional Competence

1. Knowledge and skill

2. Reasonable care and diligence

3. Exercise sound judgment in application

48

Quiz Question

The AICPA’s Code of Professional Conduct requires that a CPA obtain an engagement letter from each client for all services provided.

a. True

b. False.

49

General Standards

B. Due Professional Care

1. Obtain new knowledge as needed

2. Observe what it means to be a “professional”

50

General Standards

C. Planning and Supervision

1. Responsible for staff

2. Training

51

General Standards

D. Sufficient Relevant Data

1. Professional standards dictate

2. Experience and expertise

--how do you get it?

52

53

Code of Professional Conduct

Pronouncements

• Intended to provide general guidance

• Applies to everyone

• Explains intent

Rulings & Interpretations

• Very specific situations

• Required to follow

• Interprets pronouncements

54

Rules

Rule 101, Independence Rule 102, Integrity and Objectivity Rule 201, General StandardsRule 202, Compliance With Standards Rule 203, Accounting PrinciplesRule 301, Confidential Client Information Rule 302, Contingent FeesRule 501, Acts Discreditable

55

Special Note

Independence

• In spirit

• In truth

• Cornerstone of CPAs reputation

Disclosures

• CPA must disclose to clients any potential conflicts of interest

• Contingency arrangements

• Commissions from sales

56

Rules 101-102

Independence, Integrity, and Objectivity

57

Independence

• Maintain an objective and impartial mental attitude

• Must appear independent to 3rd

party

• Not required for all services

58

Today’s Environment

No longer firm-based rules—looking more on engagement team and who influences the engagement team

Independence is an individual concern and a firm concern

59

“Covered Member”

Covered Member

• Individual, firm, or entity capable of influencing attest engagement

• All attest team members

• Partner/manager >10 hours on engagement

Impaired If

• Had or committed to acquire any direct or material indirect financial interest, loan, or joint business investment w/client

60

Other Independence Issues

• Multiple offices/partners not on engagement

• Past employment with client

• Future employment with client/offers/

• Close relatives

• If impaired—only one option

• --Issue a disclaimer of opinion

• --lost for that engagement year

61

Integrity & Objectivity

• Maintain objectivity

• Maintain integrity

• Free of conflicts of interest

• Not knowinglymisrepresent facts

• Must not subordinate our professional judgment

62

Confidentiality of Records

May not disclose any client info without consent (absent official legal or professional review)

63

TN Board of Accountancy

“The Rules of Professional Conduct adopted and enforced by the board cover a broad range of behaviors, but do not cover every possible unethical act. These rules include the issues of integrity, contingent fees, disclosures, competence, compliance with standards and confidential client information. When the rules are silent on any matter, the licensee should defer to the AICPA Code of Professional Conduct.” (Website TBOA)

64

Discreditable Acts

• Any act that reflects adversely on the profession

• Any licensee or candidate for licensure who solicits, discloses, and/or uses information obtained through violation of nondisclosure statement of the Uniform CPA Examination

65

Possible SBOA Actions

• Warning letter-put on notice• Civil penalties• Require additional CPE• Firm Peer Review-additional review

sooner than 3 year cycle• Probation• Suspension• Revocation of license!

66

Disciplinary Hearing

• May be formal or informal

• CPA must provide own Counsel

67

TN BOA FAQs

I think my CPA overcharged me for some work she did. Does the Board regulate fees charged by CPAs? Neither the Board nor any other state or federal agency has the authority to regulate fees.

68

How do I know if a complaint has been filed against me? Board staff will send written notification when a complaint is filed against you. Upon receiving a notice of complaint, you should respond in writing to the board within fourteen days.

TN BOA FAQs

69

I am not a CPA. I offer bookkeeping and tax preparation for my clients. Do I have to follow Tennessee's Accountancy law and rules? No. The Board's jurisdiction is limited to licensed CPAs, PAs and licensed accounting firms. However, unlicensed individuals are not allowed to call themselves CPAs, PAs or accountants. Unlicensed individuals and firms should not advertise any public accounting services in any media. Unlicensed individuals can not issue audits, reviews or compilation reports.

TN BOA FAQs

70

Disciplinary Actions and Penalties

• Specific and general disciplinary actions are in TAA

• Dishonesty, fraud or gross negligence

• Holding out as CPA when not licensed

• Conduct adversely affecting performance

• Civil penalties range from $0 - $1,000 per violation

• Revocation or suspension of license

71

July 2015 BOA Disciplinary Actions

Respondent: Melvin Travis, MemphisViolation: Failure to Pay Professional Privilege Tax Action: $500 Civil Penalty

Respondent: J. Andrew Lipscomb, Chattanooga Violation: Failure to Respond to CPE Audit Action: $250