to fasb or to iasb. that is the question · to fasb or to iasb. that is the question ... accounting...

TRANSCRIPT

International Center for Captive Insurance Education

To FASB or to IASB. That is the Question

Joel Chansky, Principal and Consulting Actuary, Milliman, Inc.Magali Welch, Partner, Johnson Lambert & Co.

Tuesday, March 15th- 3:45pm – 5:00pm

Agenda

• Learning Objectives

• Background and Overview of Proposed Insurance Standards

• Risk Adjustment: IASB Version

• Case Study

• Additional Disclosures

• Update on Insurance Standards

2

Learning Objectives

3

Learning Objectives: Impact on Captive Accounting

• Potential Changes in Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS)

– Likely to Increase Loss Reserves

– Likely to Lower Surplus

– Will Create More Work for Auditor and Actuary

4

Background and Overview of Proposed Standards

5

Key Players

• IASB. International Accounting Standards Board which issues:

– IFRS – International Financial Reporting Standards

• IFRIC. International Financial Reporting Interpretations Committee, which issues:

– IFRICs – Interpretations of the IFRS

• FASB. Financial Accounting Standards Board

6

7

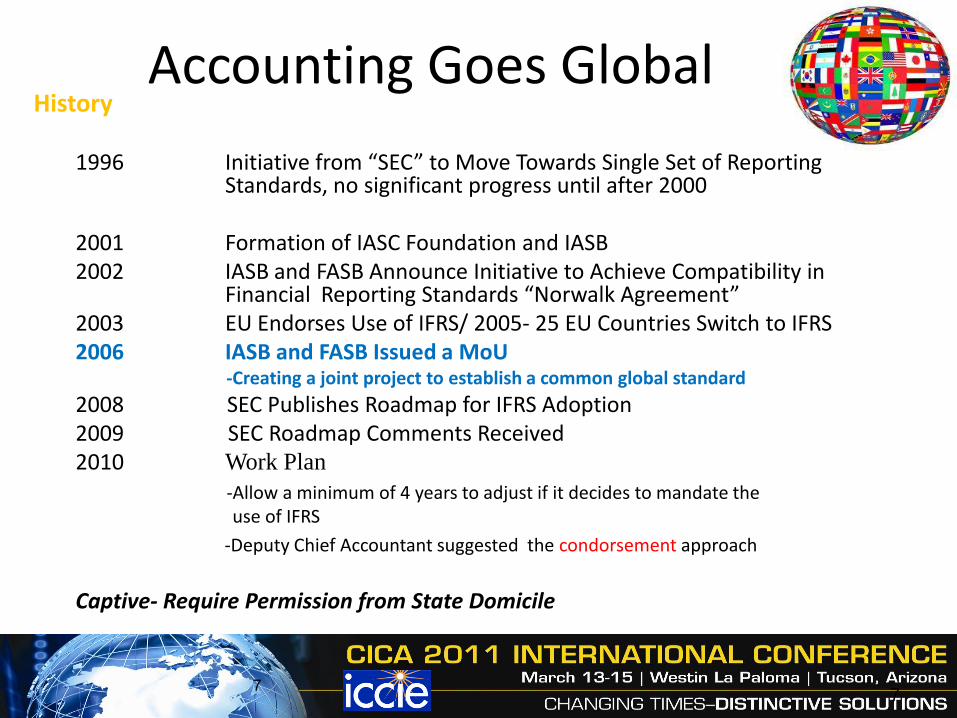

Accounting Goes GlobalHistory

1996 Initiative from “SEC” to Move Towards Single Set of Reporting Standards, no significant progress until after 2000

2001 Formation of IASC Foundation and IASB2002 IASB and FASB Announce Initiative to Achieve Compatibility in

Financial Reporting Standards “Norwalk Agreement”2003 EU Endorses Use of IFRS/ 2005- 25 EU Countries Switch to IFRS2006 IASB and FASB Issued a MoU

-Creating a joint project to establish a common global standard

2008 SEC Publishes Roadmap for IFRS Adoption2009 SEC Roadmap Comments Received2010 Work Plan

-Allow a minimum of 4 years to adjust if it decides to mandate the use of IFRS

-Deputy Chief Accountant suggested the condorsement approach

Captive- Require Permission from State Domicile

7

More than 100 Countries Require, Permit or Are Converting to the Use of IFRS

Country As of April 2010

Argentina IFRS

Australia IFRS

Brazil IFRS Banks & Issuers

Canada IFRS/ permitted for private sector

China IFRS

France IFRS

Germany IFRS

India Converting to IFRS

Indonesia Converting to IFRS

Italy IFRS

Japan Permitted

Mexico IFRS 2012

Republic of Korea IFRS

Russia

Required for banking & issuers

Permitted for others

South Africa IFRS

Turkey IFRS for Issuers

United Kingdom IFRS

United States Allowed for foreign issuers 8

IASB/FASB Joint Project“Insurance Contracts”

• In October 2008, the IASB and FASB began process of developing a single standard on “Insurance Contract”

• Objective:

– Develop common, high-quality guidance that will address recognition, measurement, presentation, and disclosure requirements for insurance contracts (including reinsurance contracts).

9

IASB/FASB Joint Project

• IASB Exposure Draft issued July 2010 (comment period ended November 2010)

• FASB Discussion Paper issued September 2010 (comment period ended December 2010)

10

Insurance Contract

• “A contract under which one party (the insurer) accepts significant insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event (the insured event) adversely affects the policyholder.”

– Current GAAP→ A contract in which an insurance entity unconditionally undertakes a legal obligation to provide specified benefits to specific individuals in return for a fixed consideration or premium.

11

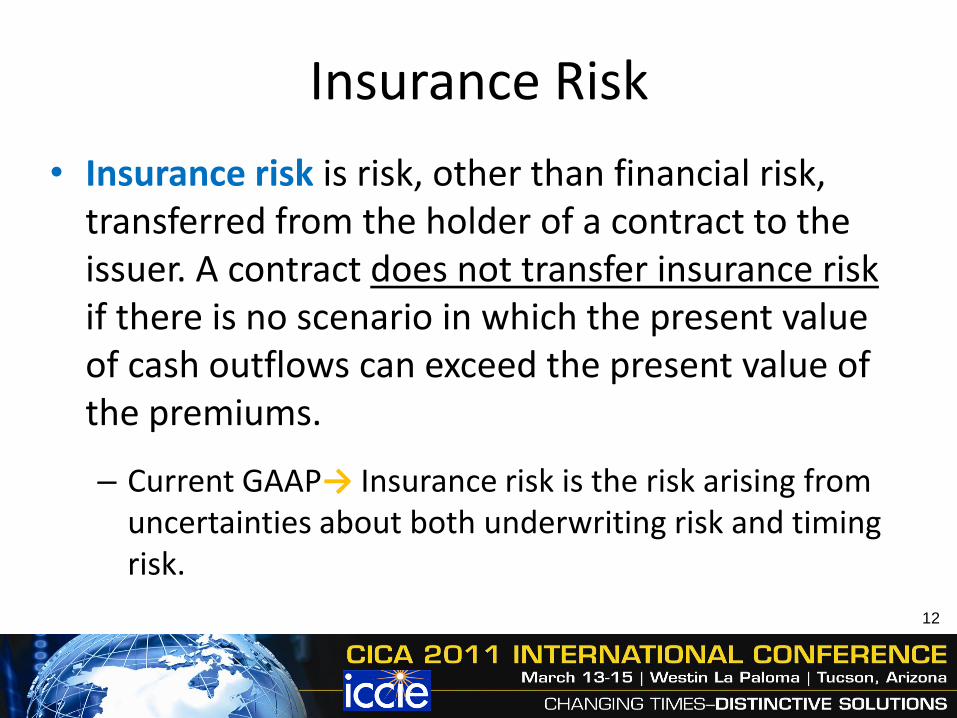

Insurance Risk

• Insurance risk is risk, other than financial risk, transferred from the holder of a contract to the issuer. A contract does not transfer insurance risk if there is no scenario in which the present value of cash outflows can exceed the present value of the premiums.

– Current GAAP→ Insurance risk is the risk arising from uncertainties about both underwriting risk and timing risk.

12

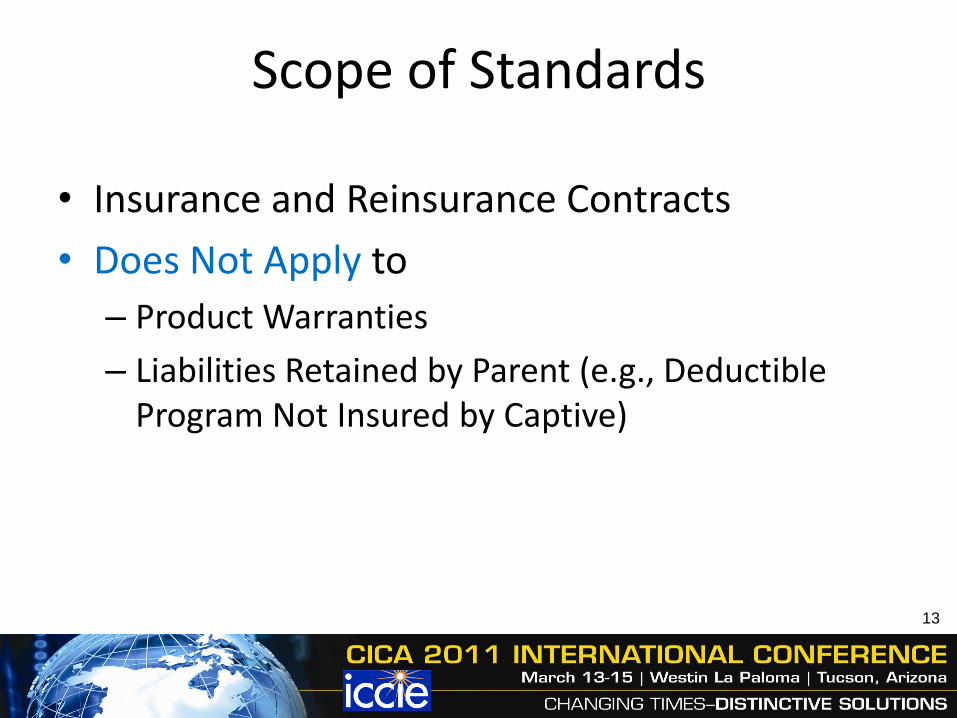

Scope of Standards

• Insurance and Reinsurance Contracts

• Does Not Apply to

– Product Warranties

– Liabilities Retained by Parent (e.g., Deductible Program Not Insured by Captive)

13

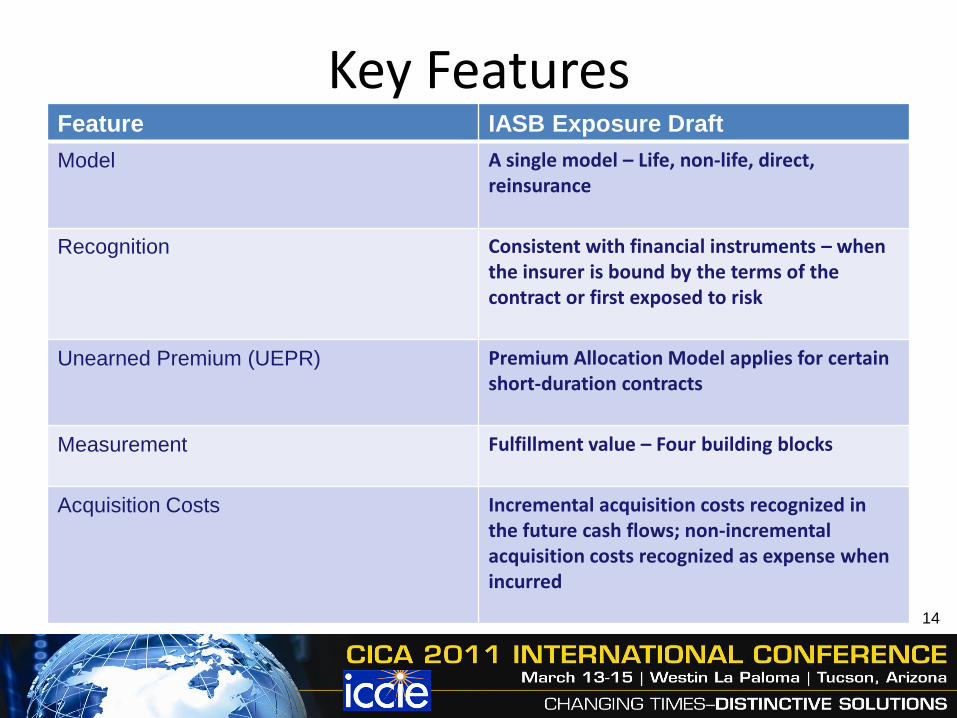

Key FeaturesFeature IASB Exposure Draft

Model A single model – Life, non-life, direct, reinsurance

Recognition Consistent with financial instruments – when the insurer is bound by the terms of the contract or first exposed to risk

Unearned Premium (UEPR) Premium Allocation Model applies for certain short-duration contracts

Measurement Fulfillment value – Four building blocks

Acquisition Costs Incremental acquisition costs recognized in the future cash flows; non-incremental acquisition costs recognized as expense when incurred

14

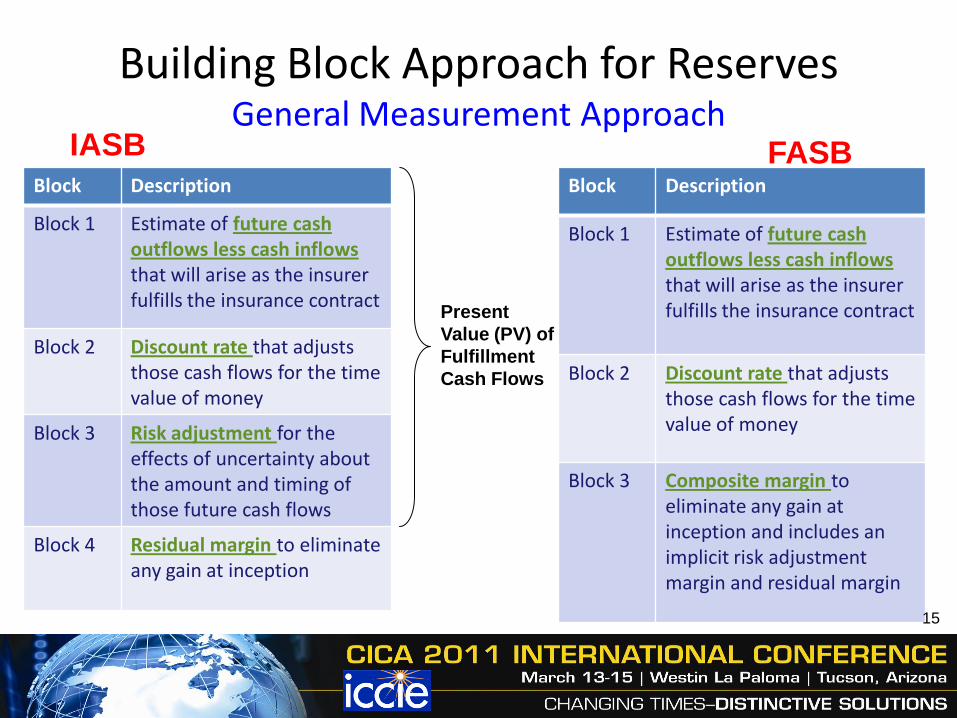

Building Block Approach for ReservesGeneral Measurement Approach

Block Description

Block 1 Estimate of future cash outflows less cash inflows that will arise as the insurer fulfills the insurance contract

Block 2 Discount rate that adjusts those cash flows for the time value of money

Block 3 Risk adjustment for the effects of uncertainty about the amount and timing of those future cash flows

Block 4 Residual margin to eliminate any gain at inception

Block Description

Block 1 Estimate of future cash outflows less cash inflows that will arise as the insurer fulfills the insurance contract

Block 2 Discount rate that adjusts those cash flows for the time value of money

Block 3 Composite margin to eliminate any gain at inception and includes an implicit risk adjustment margin and residual margin

IASB FASB

Present

Value (PV) of

Fulfillment

Cash Flows

15

Building Block Approach for Captives

• Captives Generally Write Short Duration Contracts (Policy Period of 12 Months or Less)

• Under IFRS, Modified Approach Applies to Short Duration Contracts

– Discounted

– With Risk Adjustment

– Without Residual Margin

16

Calculation of Loss ReservesOld Way New Way

Estimated

Undiscounted

Reserves

Sum of

Projected Paid

Loss Cash

Flows

Estimated

Discounted

Reserves

Estimated

Discounted

Reserves

Plus Risk

AdjustmentLess Amount of

Discount

17

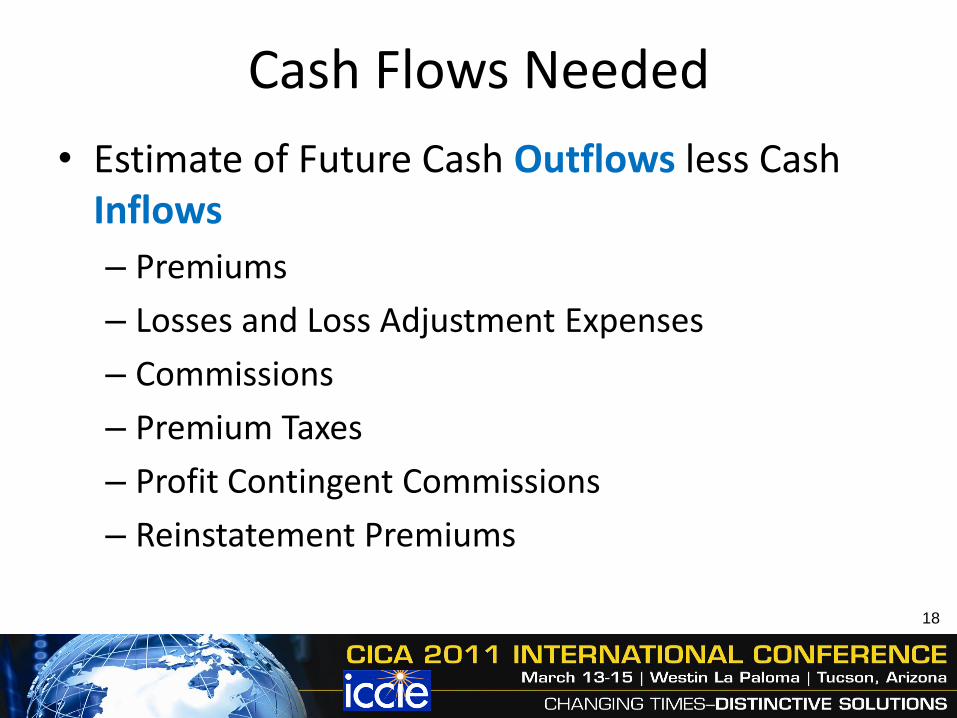

Cash Flows Needed

• Estimate of Future Cash Outflows less Cash Inflows

– Premiums

– Losses and Loss Adjustment Expenses

– Commissions

– Premium Taxes

– Profit Contingent Commissions

– Reinstatement Premiums

18

Reserving Assumptions

• Portfolios of Insurance Contracts

• “Mean” Reserve Estimate

• Discount Rate

• Payment Pattern

• Risk Adjustment

19

Portfolio of Insurance Contracts

Insurance Contracts that are Subject to Broadly Similar Risks and Managed Together as a Single Pool

By similar date of initial recognition of the contract and coverage periods

20

Mean Reserve Estimate

• Estimate Cash Outflows

– Explicit, Unbiased and Probability-Weighted Estimates of Future Paid Losses• Range of scenarios that reflect full range of possible outcomes

• Not to include all scenarios but must incorporate all relevant information

• Not reasonably possible scenarios not expected to be considered

The Mean

21

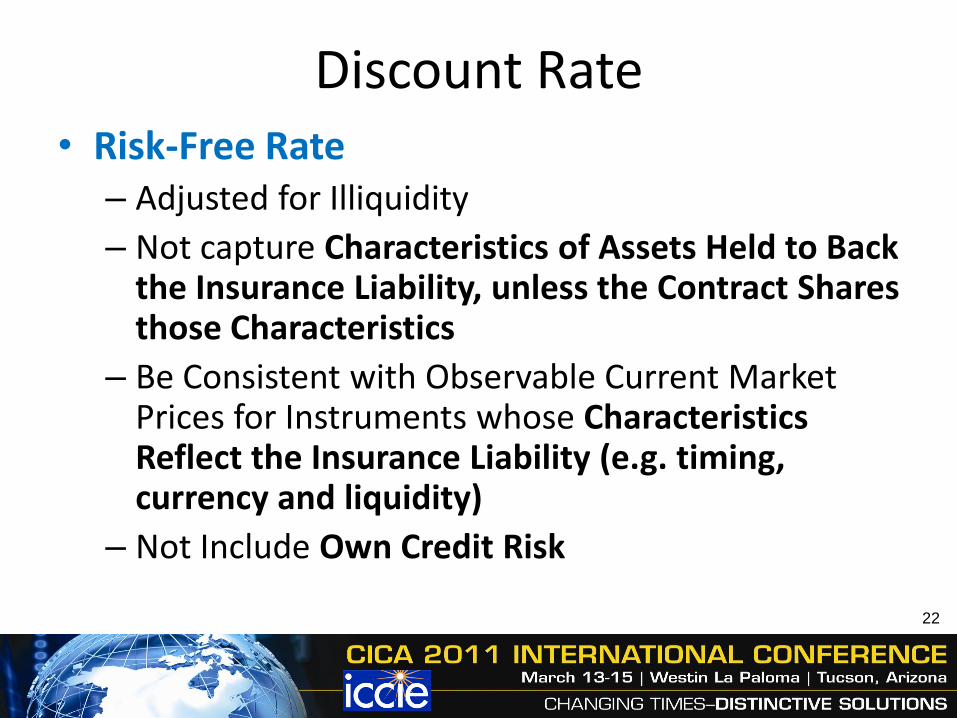

Discount Rate• Risk-Free Rate

– Adjusted for Illiquidity

– Not capture Characteristics of Assets Held to Back the Insurance Liability, unless the Contract Shares those Characteristics

– Be Consistent with Observable Current Market Prices for Instruments whose Characteristics Reflect the Insurance Liability (e.g. timing, currency and liquidity)

– Not Include Own Credit Risk

22

Payment Pattern

• Used to Project Paid Losses (Block 1)

• Discount Paid Losses (Block 2)

• Needed to Compare Actual vs. Expected Paid Losses

23

Risk AdjustmentIASB Version

24

Risk Adjustment

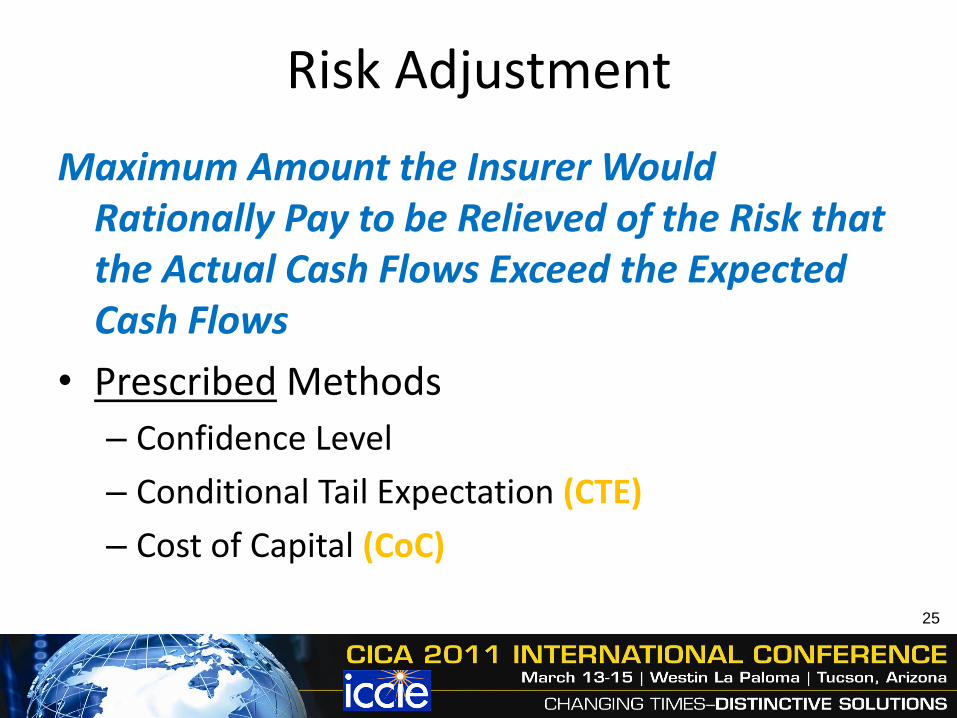

Maximum Amount the Insurer Would Rationally Pay to be Relieved of the Risk that the Actual Cash Flows Exceed the Expected Cash Flows

• Prescribed Methods

– Confidence Level

– Conditional Tail Expectation (CTE)

– Cost of Capital (CoC)

25

Risk Adjustment Example

• Workers Compensation

• $100 Million Annual Expected Losses

– 10-Year Payment Pattern

– Year 1 Expected Paid Losses = $15 Million

– Expected Reserves end of Year 1 = $85 Million

26

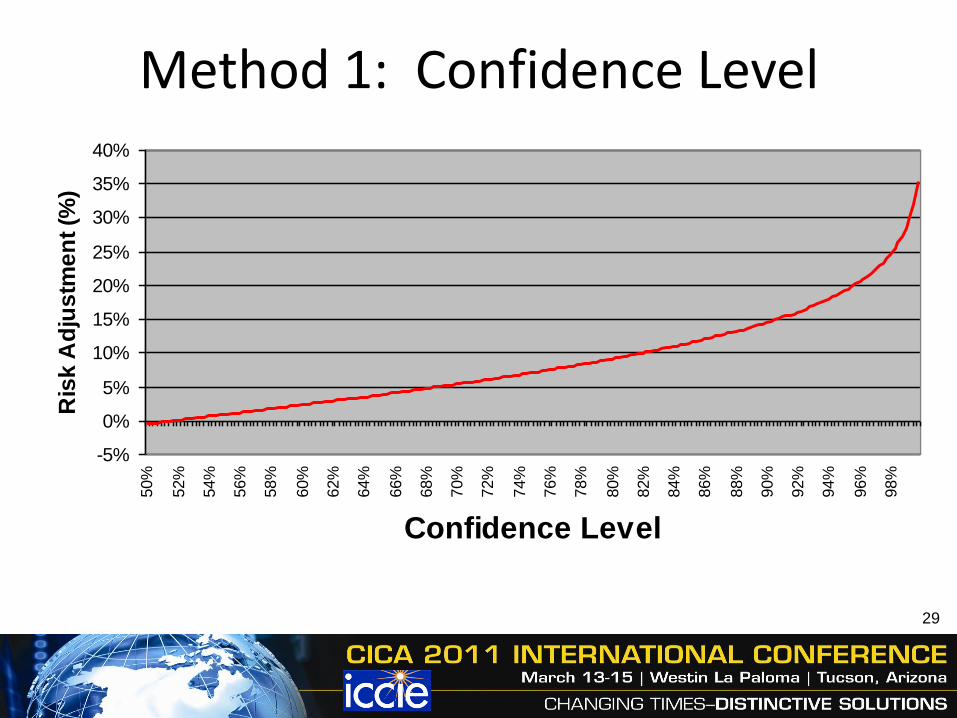

Method 1: Confidence Level

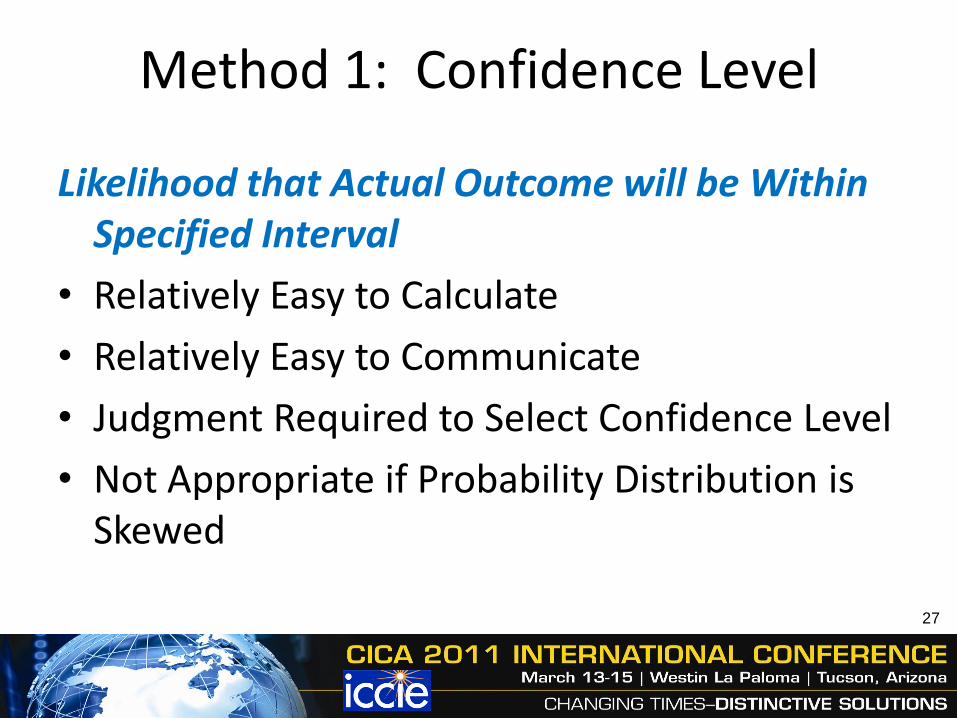

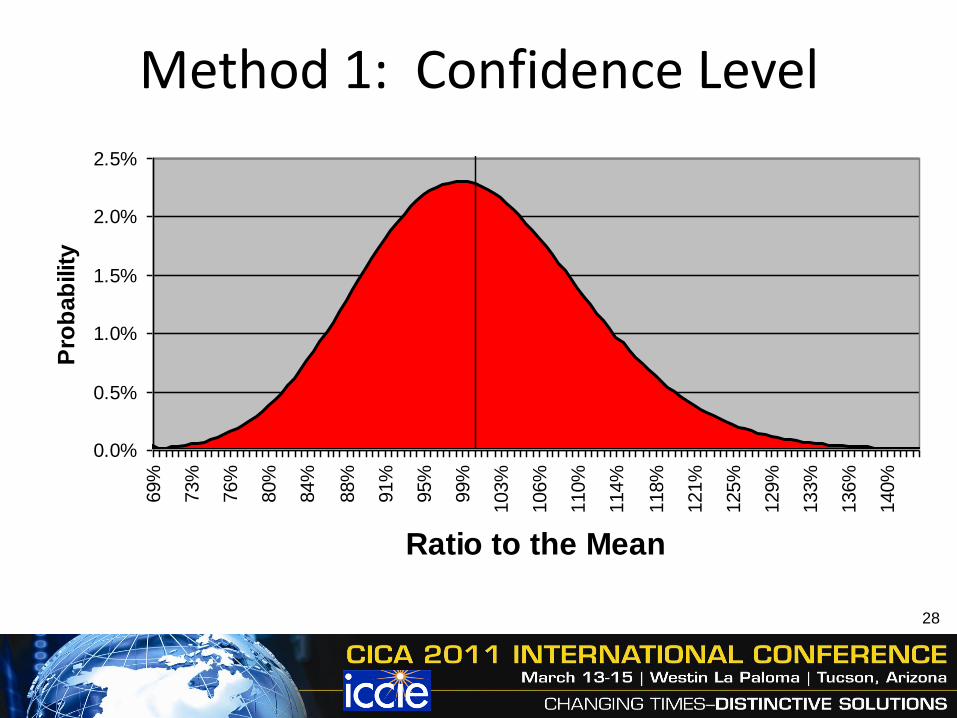

Likelihood that Actual Outcome will be Within Specified Interval

• Relatively Easy to Calculate

• Relatively Easy to Communicate

• Judgment Required to Select Confidence Level

• Not Appropriate if Probability Distribution is Skewed

27

Method 1: Confidence Level

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%69%

73%

76%

80%

84%

88%

91%

95%

99%

103%

106%

110%

114%

118%

121%

125%

129%

133%

136%

140%

Ratio to the Mean

Pro

ba

bilit

y

28

Method 1: Confidence Level

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%50%

52%

54%

56%

58%

60%

62%

64%

66%

68%

70%

72%

74%

76%

78%

80%

82%

84%

86%

88%

90%

92%

94%

96%

98%

Confidence Level

Ris

k A

dju

stm

en

t (%

)

29

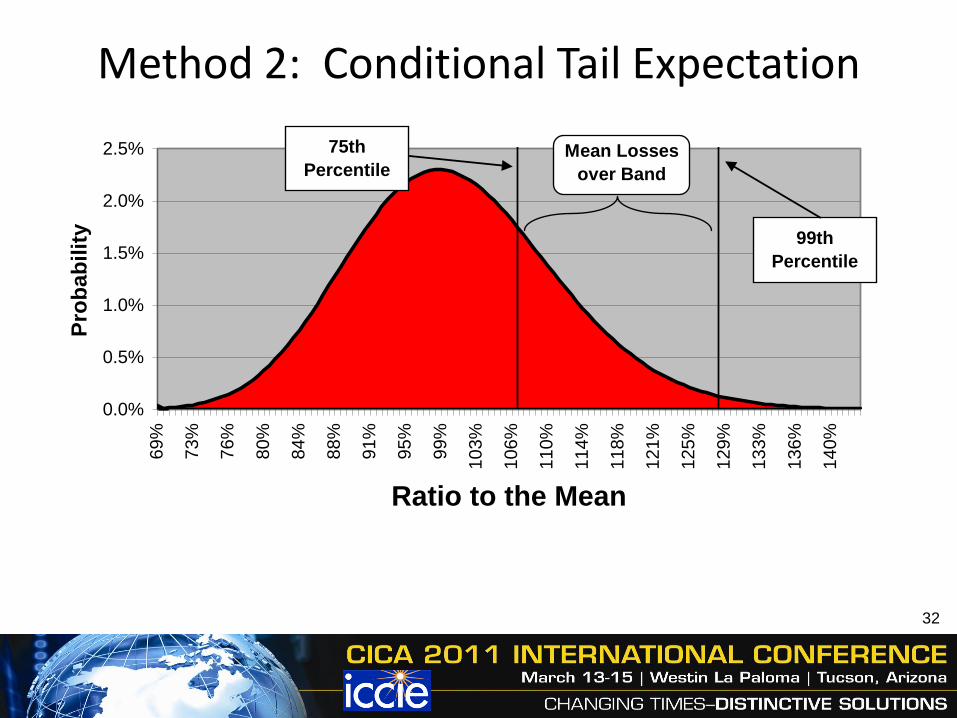

Method 2: Conditional Tail Expectation

Expected Value of Extreme Losses

• Relatively Easy to Calculate

• Little Harder to Communicate

• Appropriate if Probability Distribution is Skewed

• Judgment Required to Select CTE Band

• Difficult to Reliably Estimate Tail of Reserve Distribution

30

Method 2: Conditional Tail Expectation

(1) Select Confidence Level Band

Low End = 75th Percentile 106.9% of Expected Losses

High End = 99th Percentile 128.1% of Expected Losses

(2) Calculate Mean Losses within Band * 113.6% of Expected Losses

* probability-weighted average across CTE band

(3) Risk Adjustment 13.6% of Expected Losses

31

Method 2: Conditional Tail Expectation

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%69%

73%

76%

80%

84%

88%

91%

95%

99%

103%

106%

110%

114%

118%

121%

125%

129%

133%

136%

140%

Ratio to the Mean

Pro

ba

bilit

y

Mean Losses

over Band

75th

Percentile

99th

Percentile

32

Method 3: Cost of Capital

Present Value of Cost of Holding Capital Required to Provide for Targeted Confidence Level of Reserves

• Target Confidence Level Should be High

• Capital Rate Reflects Only Risks Relevant to Insurance Liability

• Appropriate if Probability Distribution is Skewed

33

Method 3: Cost of Capital(1) (2) (3) (4) (5) (6) (7) (8)

Risk (2)x(3) (4)x(5)

Adjustment Discounted Percent

Ending at 99.5th Capital Capital Cost of Cost of of Year 1

Year Reserves Percentile Needed Rate Capital Capital Reserves

1 85 31.9% 27.09 15% 4.06 4.06

2 65 31.9% 20.71 15% 3.11 2.70

3 45 31.9% 14.34 15% 2.15 1.63

4 30 31.9% 9.56 15% 1.43 0.94

5 20 31.9% 6.37 15% 0.96 0.55

6 15 31.9% 4.78 15% 0.72 0.36

7 10 31.9% 3.19 15% 0.48 0.21

8 5 31.9% 1.59 15% 0.24 0.09

9 2 31.9% 0.64 15% 0.10 0.03

10 0 31.9% 0.00 15% 0.00 0.00

Total 13.24 10.57 12.4%

34

Comparison of Methods

0%

5%

10%

15%

20%

25%

30%

35%

40%60%

63%

65%

68%

71%

74%

76%

79%

82%

85%

87%

90%

93%

96%

98%

Confidence Level

Ris

k A

dju

stm

en

t (%

)

CTE Band to 99th

CTE Band to 95th

Confidence Level

Cost of Capital at 15%

35

10% Risk Adjustment Equivalents

0%

5%

10%

15%

20%

25%

30%

35%

40%60%

63%

65%

68%

71%

74%

76%

79%

82%

85%

87%

90%

93%

96%

98%

Confidence Level

Ris

k A

dju

stm

en

t (%

)

CTE Band to 99th

CTE Band to 95th

Confidence Level

Cost of Capital at 15%

36

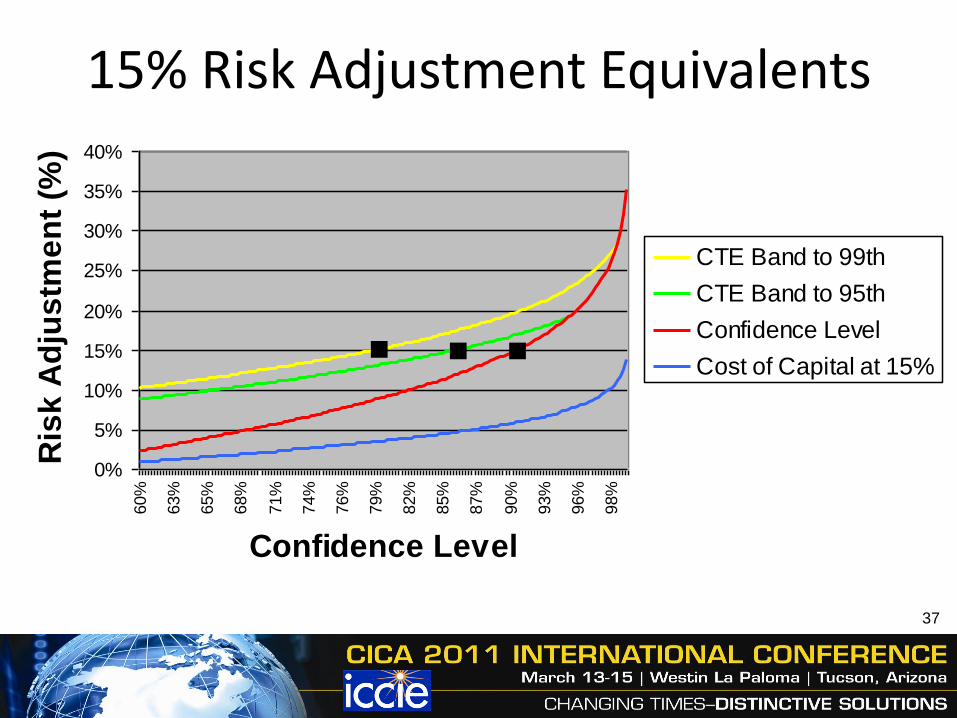

15% Risk Adjustment Equivalents

0%

5%

10%

15%

20%

25%

30%

35%

40%60%

63%

65%

68%

71%

74%

76%

79%

82%

85%

87%

90%

93%

96%

98%

Confidence Level

Ris

k A

dju

stm

en

t (%

)

CTE Band to 99th

CTE Band to 95th

Confidence Level

Cost of Capital at 15%

37

Factors that Increase “Risk Adjustment”

• Low Frequency and High Severity

• Long-Tail Lines of Business

• Wide Probability Distribution

• Uncertainty of Current Estimate and Trend

• Maturity of Policy Year

38

Risk Adjustment Across Portfolios

• IFRS Exposure Draft States Risk Adjustment Shall Not Reflect Diversification Between Portfolios

– Frequent Subject of Comment Letters

39

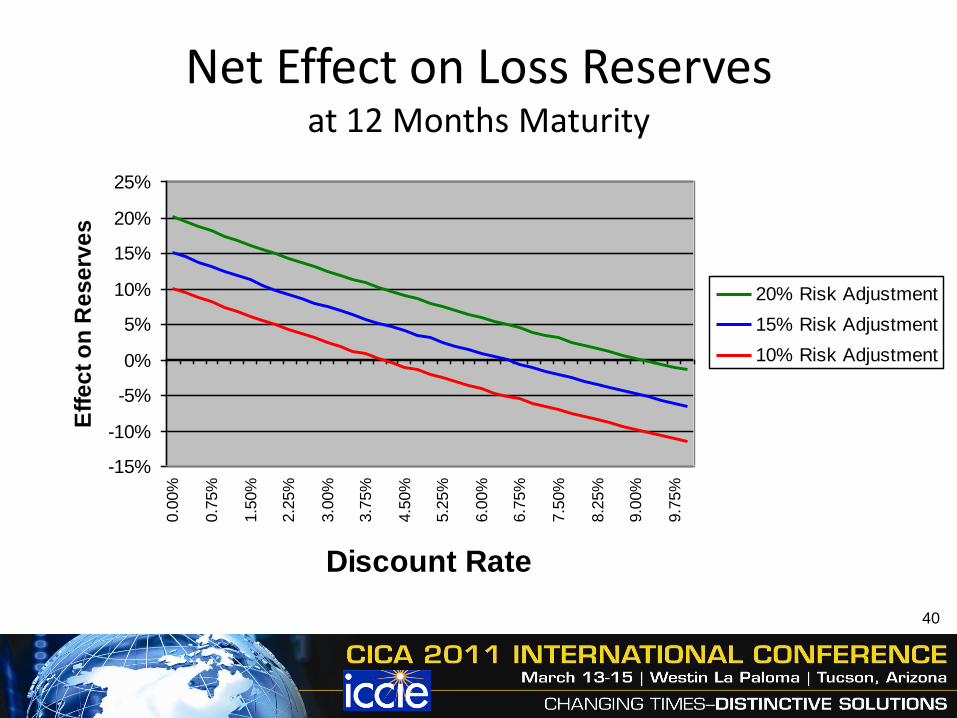

Net Effect on Loss Reservesat 12 Months Maturity

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%0.0

0%

0.7

5%

1.5

0%

2.2

5%

3.0

0%

3.7

5%

4.5

0%

5.2

5%

6.0

0%

6.7

5%

7.5

0%

8.2

5%

9.0

0%

9.7

5%

Discount Rate

Eff

ec

t o

n R

es

erv

es

20% Risk Adjustment

15% Risk Adjustment

10% Risk Adjustment

40

Case Study

41

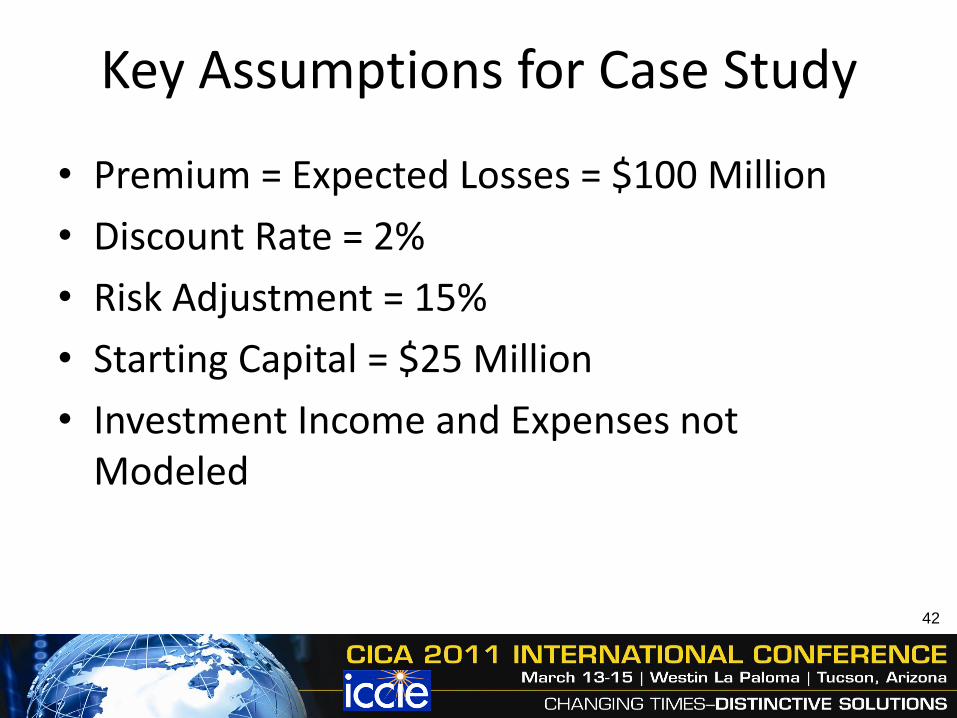

Key Assumptions for Case Study

• Premium = Expected Losses = $100 Million

• Discount Rate = 2%

• Risk Adjustment = 15%

• Starting Capital = $25 Million

• Investment Income and Expenses not Modeled

42

Calculation of Loss ReservesOld Way New Way

Estimated

Undiscounted

Reserves

Sum of

Projected Paid

Loss Cash

Flows

Estimated

Discounted

Reserves

Estimated

Discounted

Reserves

Plus Risk

AdjustmentLess Amount of

Discount

43

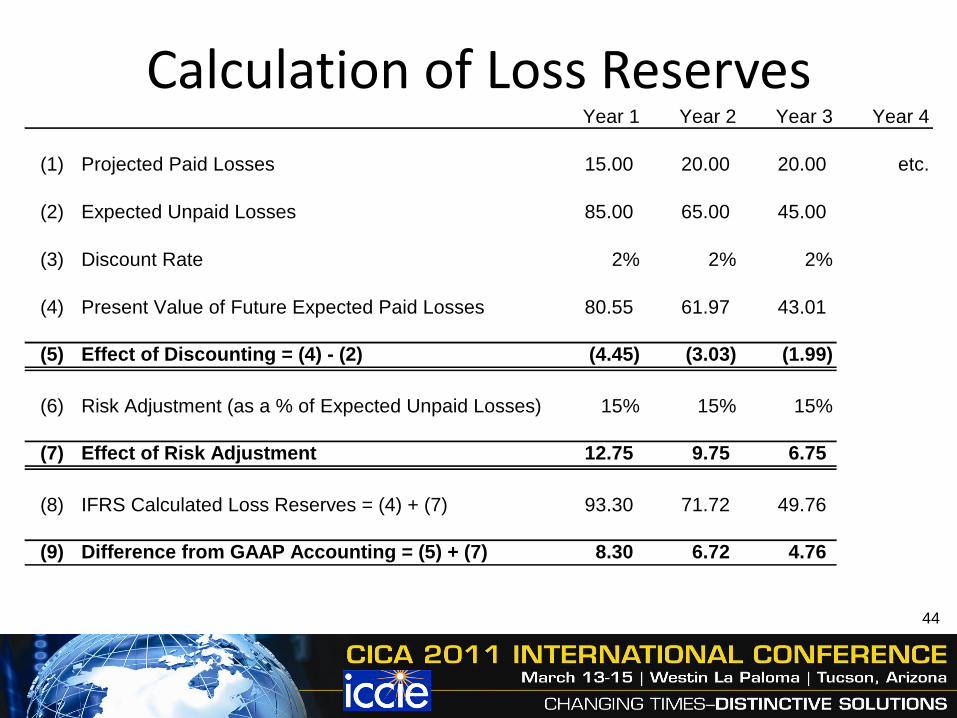

Calculation of Loss ReservesYear 1 Year 2 Year 3 Year 4

(1) Projected Paid Losses 15.00 20.00 20.00 etc.

(2) Expected Unpaid Losses 85.00 65.00 45.00

(3) Discount Rate 2% 2% 2%

(4) Present Value of Future Expected Paid Losses 80.55 61.97 43.01

(5) Effect of Discounting = (4) - (2) (4.45) (3.03) (1.99)

(6) Risk Adjustment (as a % of Expected Unpaid Losses) 15% 15% 15%

(7) Effect of Risk Adjustment 12.75 9.75 6.75

(8) IFRS Calculated Loss Reserves = (4) + (7) 93.30 71.72 49.76

(9) Difference from GAAP Accounting = (5) + (7) 8.30 6.72 4.76

44

Effect on Financial Statements

• Does Not Affect Cash Items

– Paid Losses and Expenses

– Investment Income

• Affects Earned Income

– Loss Reserves

– Underwriting Income

– Net Income

– Surplus

45

Effect on Financial Statements

• All Else Equal

– Provision for Adverse Loss Development Carried as Loss Reserve (not Surplus)

– Affects Solvency Ratios

– May Affect Dividend Potential

46

Financial StatementsSingle Policy Year

GAAP Basis Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10

(1) Earned Premium 100 0 0 0 0 0 0 0 0 0

(2) Paid Losses 15 20 20 15 10 5 5 5 3 2

(3) Loss Reserves 85 65 45 30 20 15 10 5 2 0

(4) Incurred Losses 100 0 0 0 0 0 0 0 0 0

(5) Net Income 0 0 0 0 0 0 0 0 0 0

(6) Ending Surplus 25 25 25 25 25 25 25 25 25 25

IFRS Basis Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10

(1) Earned Premium 100 0 0 0 0 0 0 0 0 0

(2) Paid Losses 15 20 20 15 10 5 5 5 3 2

(3a) Undisc Reserves 85 65 45 30 20 15 10 5 2 0

(3b) Discount Adjustment (4.45) (3.03) (1.99) (1.28) (0.81) (0.47) (0.23) (0.09) (0.02) 0.00

(3c) Risk Adjustment 12.75 9.75 6.75 4.50 3.00 2.25 1.50 0.75 0.30 0.00

(3) Loss Reserves 93.30 71.72 49.76 33.22 22.19 16.78 11.27 5.66 2.28 0.00

(4) Incurred Losses 108.30 (1.59) (1.96) (1.54) (1.03) (0.42) (0.51) (0.60) (0.38) (0.28)

(5) Net Income (8.30) 1.59 1.96 1.54 1.03 0.42 0.51 0.60 0.38 0.28

(6) Ending Surplus 16.70 18.28 20.24 21.78 22.81 23.22 23.73 24.34 24.72 25.00

47

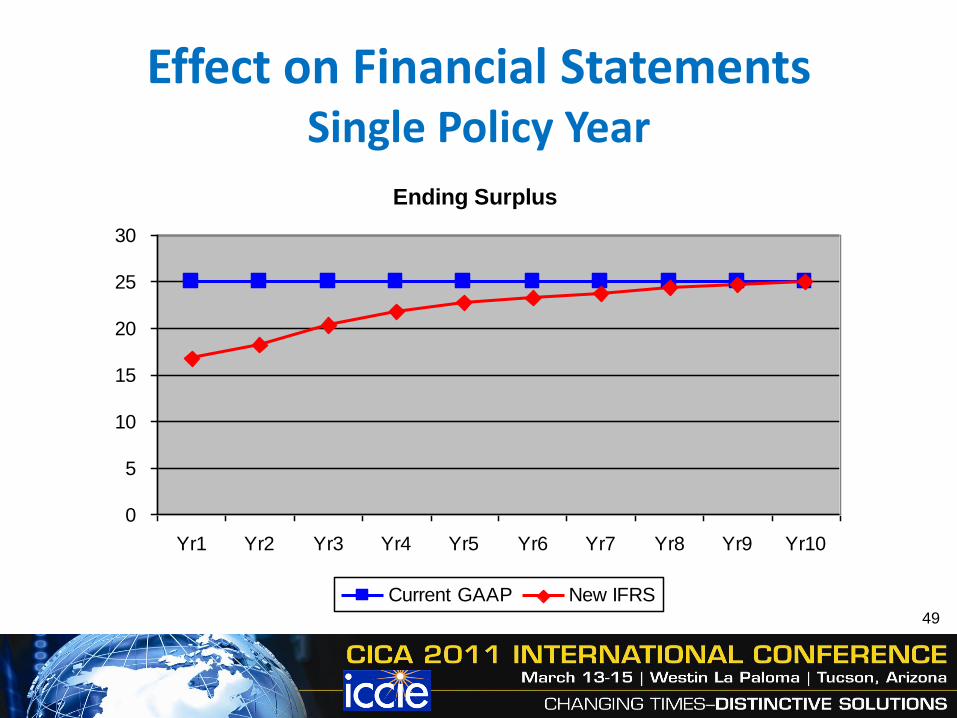

Effect on Financial StatementsSingle Policy Year

Calendar Year Incurred Losses

Change in Change in

Year GAAP Discount Risk Adj IFRS

1 100.00 (4.45) 12.75 108.30

2 0.00 1.41 (3.00) (1.59)

3 0.00 1.04 (3.00) (1.96)

4 0.00 0.71 (2.25) (1.54)

5 0.00 0.47 (1.50) (1.03)

6 0.00 0.33 (0.75) (0.42)

7 0.00 0.24 (0.75) (0.51)

8 0.00 0.15 (0.75) (0.60)

9 0.00 0.07 (0.45) (0.38)

10 0.00 0.02 (0.30) (0.28)

Total 100.00 0.00 0.00 100.00

Loss of $8.30

48

Effect on Financial StatementsSingle Policy Year

Ending Surplus

0

5

10

15

20

25

30

Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10

Current GAAP New IFRS49

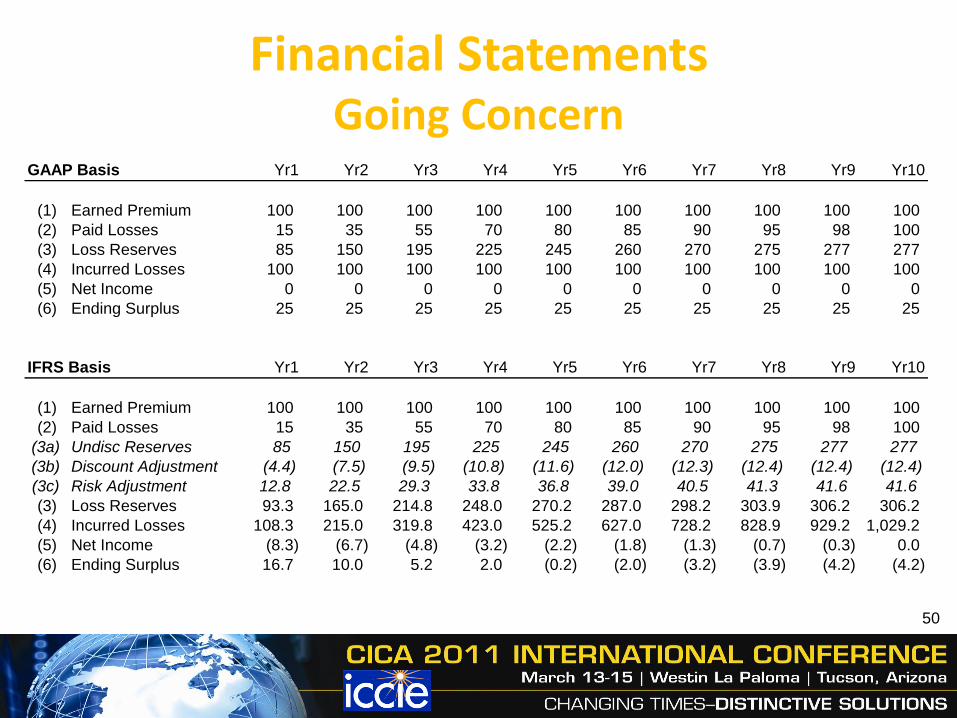

Financial StatementsGoing Concern

GAAP Basis Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10

(1) Earned Premium 100 100 100 100 100 100 100 100 100 100

(2) Paid Losses 15 35 55 70 80 85 90 95 98 100

(3) Loss Reserves 85 150 195 225 245 260 270 275 277 277

(4) Incurred Losses 100 100 100 100 100 100 100 100 100 100

(5) Net Income 0 0 0 0 0 0 0 0 0 0

(6) Ending Surplus 25 25 25 25 25 25 25 25 25 25

IFRS Basis Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10

(1) Earned Premium 100 100 100 100 100 100 100 100 100 100

(2) Paid Losses 15 35 55 70 80 85 90 95 98 100

(3a) Undisc Reserves 85 150 195 225 245 260 270 275 277 277

(3b) Discount Adjustment (4.4) (7.5) (9.5) (10.8) (11.6) (12.0) (12.3) (12.4) (12.4) (12.4)

(3c) Risk Adjustment 12.8 22.5 29.3 33.8 36.8 39.0 40.5 41.3 41.6 41.6

(3) Loss Reserves 93.3 165.0 214.8 248.0 270.2 287.0 298.2 303.9 306.2 306.2

(4) Incurred Losses 108.3 215.0 319.8 423.0 525.2 627.0 728.2 828.9 929.2 1,029.2

(5) Net Income (8.3) (6.7) (4.8) (3.2) (2.2) (1.8) (1.3) (0.7) (0.3) 0.0

(6) Ending Surplus 16.7 10.0 5.2 2.0 (0.2) (2.0) (3.2) (3.9) (4.2) (4.2)

50

Effect on Financial StatementsGoing Concern

Calendar Year Incurred Losses

Change in Change in

Year GAAP Discount Risk Adj IFRS

1 100.00 (4.45) 12.75 108.30

2 100.00 (3.03) 9.75 106.72

3 100.00 (1.99) 6.75 104.76

4 100.00 (1.28) 4.50 103.22

5 100.00 (0.81) 3.00 102.19

6 100.00 (0.47) 2.25 101.78

7 100.00 (0.23) 1.50 101.27

8 100.00 (0.09) 0.75 100.66

9 100.00 (0.02) 0.30 100.28

10 100.00 0.00 0.00 100.00

Total 1,000.00 (12.38) 41.55 1,029.1751

Effect on Financial StatementsGoing Concern

Ending Surplus

(10)

(5)

0

5

10

15

20

25

30

Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10

Current GAAP New IFRS

52

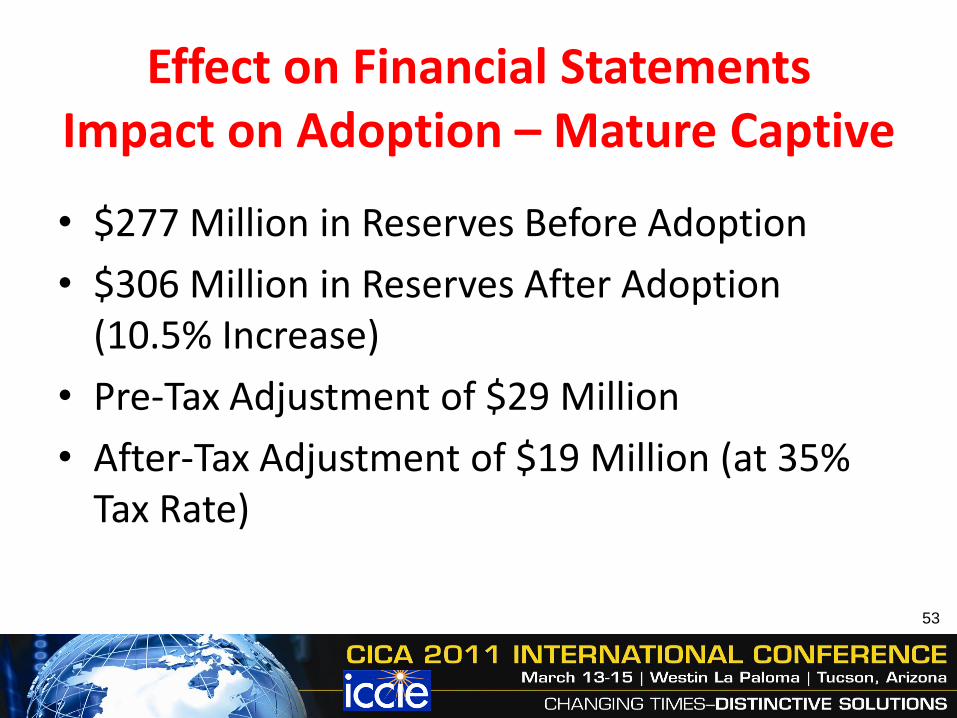

Effect on Financial StatementsImpact on Adoption – Mature Captive

• $277 Million in Reserves Before Adoption

• $306 Million in Reserves After Adoption (10.5% Increase)

• Pre-Tax Adjustment of $29 Million

• After-Tax Adjustment of $19 Million (at 35% Tax Rate)

53

Effect of Discount Rate Changes

• Changes in Discount Rate will Cause Fluctuations in Earned Income

Calendar Year Incurred Losses

90

95

100

105

110

115

Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10

IFRS at Constant 3.5% Rate IFRS at Actual 2001 to 2010 Rates

54

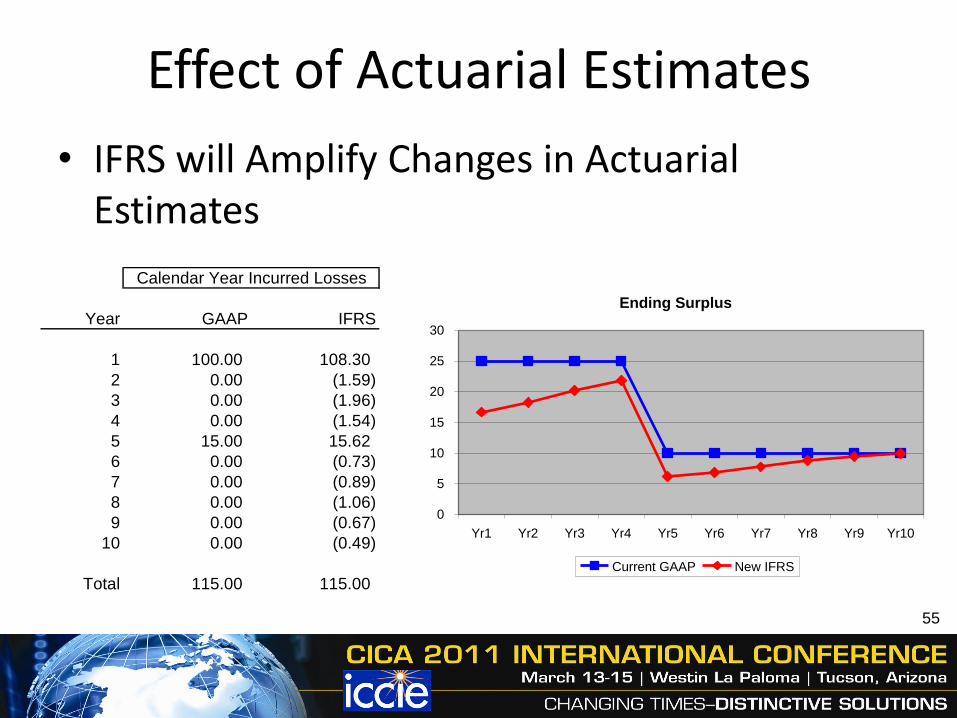

Effect of Actuarial Estimates

• IFRS will Amplify Changes in Actuarial Estimates

Calendar Year Incurred Losses

Year GAAP IFRS

1 100.00 108.30

2 0.00 (1.59)

3 0.00 (1.96)

4 0.00 (1.54)

5 15.00 15.62

6 0.00 (0.73)

7 0.00 (0.89)

8 0.00 (1.06)

9 0.00 (0.67)

10 0.00 (0.49)

Total 115.00 115.00

Ending Surplus

0

5

10

15

20

25

30

Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10

Current GAAP New IFRS

55

Additional Disclosures

56

Additional Disclosures

• “An Insurer shall Disclose Information About the Nature and Extent of Risks Arising from Insurance Contracts in Sufficient Detail to Help Users of Financial Statements Evaluate the Amount, Timing, and Uncertainty of Future Cash Flows Arising from Insurance Contracts.”

57

Additional Disclosures

• Exposures to Risk and How They Arise

• Objectives and Policies for Managing Risk

• Effect (if any) of Regulatory Framework

• Sensitivity to Insurance Risk in Relation to Effect on Profit/Loss/Equity

• Concentrations of Insurance Risk

• Actual Claims vs. Previous Estimates

58

Additional Disclosures

• Methods Used to Estimate Risk Adjustment

• Process for Estimating Inputs to Methods

• Confidence Level Assumptions

• Discount Rates

• Effect of Changes in Inputs (if Material)

59

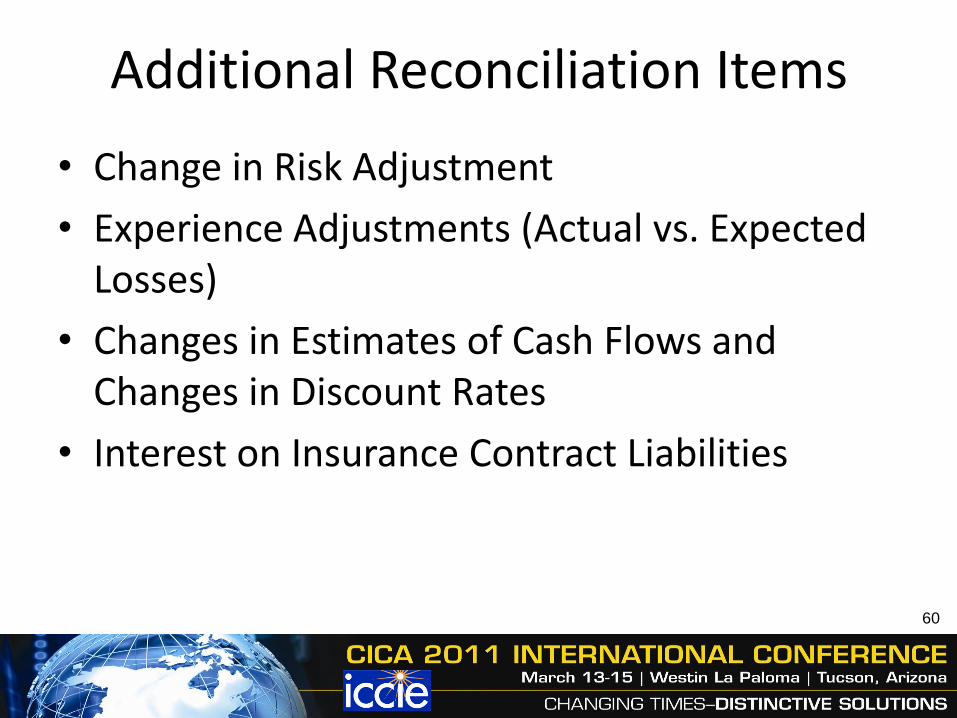

Additional Reconciliation Items

• Change in Risk Adjustment

• Experience Adjustments (Actual vs. Expected Losses)

• Changes in Estimates of Cash Flows and Changes in Discount Rates

• Interest on Insurance Contract Liabilities

60

Update on Proposed Standards

61

Recent FASB/IASB Activity• 2011 Boards’ Discussions

– Received Many Comment Letters of Very High Quality (249 IASB/ 49 FASB)

– Comments Similar in Nature

62

62

Recent FASB/IASB ActivityJanuary 2011 Update

– Widespread Agreement that an International Standard was Needed

• Develop a Convergence Standard/Continue Desirable Goal of a Common Accounting Standard

• Time to Come to a Conclusion

• Appropriate Testing of Models

63

63

Recent FASB/IASB ActivityJanuary 2011 Update

• Model

– Generally Supported the Basics of the Building Block Approach

» Supported fulfillment value

» Strong views on discounting and the composite margin versus the risk and residual margins

• Loss of Valuable Information– Ex: premium volume (LT contracts)

64

64

Recent FASB/IASB ActivityJanuary 2011 Update

• Short-Term Contracts– Concerned about the cut-off and issues with reinsurance

contracts

– Difficult calculation for onerous contracts

• Concerns about Profit/Loss Volatility– Locking discount rate for certain contracts at inception

65

Recent FASB/IASB ActivityFebruary/March 2011 Update

• Acquisition Costs– IASB- Portfolio Level

– FASB -Individual Contract Level (successful vs. unsuccessful)

– Direct or Directly Attributable To?

• Discount Rate– Not Required if Effect is Immaterial

– Use of Current Rate (remeasured each reporting period) • Top-down approach

• Bottom-down approach66

Recent FASB/IASB ActivityFebruary-March 2011 Update

• Critical ratios and Benchmarking

• Report of Field Testing

• Timeline

67

Expected Impact on Captives

• More Input Required from Management

• More Work for Auditors and Actuaries

• More Disclosures in Financial Statements

• Delayed Recognition of Income

• Increased Variability of Financial Results

68

Question and Answer

69