to make the agriculture & rural sector economically prosperous · pdf fileto make the...

TRANSCRIPT

To make the Agriculture & Rural sector Economically Prosperous andFinancially Secure by providing a Safety Net in times of

Natural Calamities and large scale Variations in Crop Yields andFluctuations in Market Prices of their produce.

To utilise the most appropriate Modern Technology to Serve Farmers

• Efficiently • Quickly • Accurately

And

Make our Rural Clientele Safe & Secure by following transparent andhassle free methods.

Our Vision

1

Contents

S.No. Page No.

1. Corporate Information 3

2. Board of Directors 4

3. Performance Highlights 5

4. From the Chairman’s Desk 6

5. Directors’ Report 8

6. Management Discussion & Analysis 20

7. Attendance Log for the Board of Directors 23

8. CAG Report 24

9. Auditors’ Report 26

10. Management Comment on Auditors Observations 28

11. Revenue Account 31

11. Balance Sheet 32

12. Profit & Loss Account 33

13. Schedules to the Accounts 34

14. Summary of Financial Statement 47

15. Accounting Ratios 48

16. Cash Flow Statement 49

17. Balance Sheet Abstract 50

18. Management Report 51

32

Corporate Information as on 31.03.2005REGISTERED OFFICE: 13th Floor, Ambadeep Building, 14, K.G. Marg, Connaught Place, New Delhi-110001

DIRECTORS

1. Shri Suparas Bhandari Chairman-cum-Managing Director

2. Shri G.C. Chaturvedi, IAS Government NomineeJt. Secretary (B&I),Ministry of Finance, GOI

3. Shri Satish Chander Government NomineeJt. Secretary,Ministry of Agriculture, GOI

4. Shri S.S. Prasad Government NomineeJt. SecretaryMinistry of Agriculture, GOI

5. Shri Naved Masood Government NomineeJt. Secretary (Drought Management& International Co-operation)Ministry of Agriculture, GOI

6. Shri K.N. Bhandari Government Nominee7. Shri M. Raghavendra Nominee GIC of India8. Dr. K.G. Karmakar Nominee NABARD9. Shri A.V. Purushothaman Nominee New India Assurance Co. Ltd.10. Shri T.K. Das Nominee National Insurance Co. Ltd.11. Shri S.K. Chanana Nominee Oriental Insurance Co. Ltd.12. Shri T.K. Roy Nominee United India Insurance Co. Ltd.

KEY MANAGEMENT PERSONNEL

Assistant General Manager Mr. B. M. SharmaDeputy Manager (Accounts) Mr. Avinanda GhoshAssistant Company Secretary Mrs. Kanika Sharma

Appointed Actuary Mr. Nalin Kapadia

Bankers UTI Bank Ltd., HDFC Bank Ltd.

Statutory Auditors J.P. Kapur & Uberai, LGF, C-4/5, SafdurjungDevelopment Area, New Delhi 110016

REGIONAL OFFICES:

Ahmedabad Dehradun MumbaiBangalore Guwahati PatnaBhopal Hyderabad RaipurBhubaneshwar Jaipur RanchiChandigarh Kolkata ThiruvananthapuramChennai Lucknow

54

Performance HighlightsBoard of Directors

Shri Suparas BhandariChairman-Cum-ManagingDirector

Shri S.K. ChananaDirector

Shri T.K. RoyDirector

Shri S.S. PrasadDirector

Shri Satish ChanderDirector

Shri A.V.Purushothaman

Director

Shri T.K. DasDirector

Shri M. RaghavendraDirector

Shri G.C. ChaturvediDirector

Dr. K.G. KarmakarDirector

Shri K.N. BhandariDirector

Shri Naved MasoodDirector

Particulars Current Period Previous Period01.04-04-31.03.05 20.12.02-31.03.04

(Rs.’000) (Rs.’000)

Rs. US $ Rs. US $

Net Earned Premium 4553743 103990 1890950 43254

Net Claims incurred 2768451 63221 2825108 64622

Net Commission (1000) (23) NIL NIL

Operating Expenses and Other outgo less other Income 84520 1930 54089 1237

Investment Income Apportioned to Revenueless Expenses 471446 10766 58829 1346

Underwriting Profit 2173218 49628 (929417) (21260)

Interest, Dividends and Rents 74927 1711 107083 2449

Other Income less Other Outgo 457 10 128 3

Amortisation of Premium on Investments 2052 47 502 11

Other Expenses 4810 110 6532 149

Profit before Tax 2241741 51193 (829240) (18968)

Provision for tax including deferred tax 557142 12723 NIL NIL

Profit after Tax 1684599 38470 (829240) (18968)

Assets:

Investments 4066613 92866 968824 22161

Loans 2502 57 965 22

Fixed Assets 48445 1106 39612 906

Cash and Bank Balances 6380813 145714 8129365 185952

Advances and Other Assets 628437 14351 449617 10285

Misc Expenses 13580 310 848169 19401

Total Assets 11140390 254405 10436552 238727

Liabilities:

Share Capital 2000000 45673 2000000 45748

Reserve and Surplus 846150 19323 NIL NIL

Fair Value Change Account 7265 166 NIL NIL

Borrowings 206071 4706 NIL

Current Liabilities & Provisions 8080904 184538 8436552 192979

Total Liabilities 11140390 254405 10436552 238727

For the convenience of readers, Performance Highlights have been converted into United StatesDollar (US $ 1 = Rs. 43.79)

76

From the Chairman’s Desk

Dear shareholders,

It gives me immense pleasure to welcome you all to the 2nd ANNUAL GENERAL MEETING of yourCompany, where the 2nd ANNUAL ACCOUNTS are being presented.

The seed of AIC, which was planted only two years ago, has already sprouted into a fine sapling, withfirm roots and spreading branches. This year was one of consolidation of operations, and of spreadingout in new directions. Many milestones were achieved during the period under review. This year theCompany posted healthy financials from its operations. The premium income increased from Rs. 369crores to Rs. 550 crores. Further, after wiping off last year's loss of Rs. 82.92 crores, and making addi-tional provisions of Rs. 93.85 crores towards "Reserve for Unexpired Risks" and of Rs. 171.58 Crorestowards "Claims Incurred But Not Reported", the Company could still earn a "Profit after Tax" of Rs.84.62 crores. My dream is to see this sapling grow into a mighty tree, bringing shade and relief to asignificant portion of the rural populace.

India is a land of agricultural bounty. Globally, India holds a premier position in the field of agricul-ture. We are the second largest producer of rice, and the third largest producer of wheat. In pulses,fruits, and tea, India is number one in the world; in groundnut and vegetables, India is number two.The national poet, Bankim Chandra Chatterjee has saluted this eminence of Indian agriculture by coin-ing the immortal epithet "sujalaang-sufalaang".

Indian agriculture, however, is heavily dependent on monsoon; - every third year sees an abnormalrainfall incidence. An adverse monsoon or similar natural peril can spell disaster for an individualfarmer. The Indian farmer is forever carrying the cross of this weather uncertainty on his shoulders. Itis our endeavour to take this burden of uncertainty from the farmer on to ourselves.

To address the varied and diverse concerns of the rural community, we are devising innovative andtailor-made products. We have already implemented the "Varsha Bima", "Sookha Suraksha Kavach","Coffee Insurance", and are set to launch "Wheat Insurance", "Poppy Insurance", and "Mango Insur-ance" very soon. We are also exploring the applicability of Remote Sensing Technology in crop insur-ance.

AIC contributed its bit for victims of the devastating Tsunami by expeditiously paying the claims inthe affected districts in Pondicherry and Tamil Nadu.

Suparas BhandariChairman Cum-Managing Director

A Joint Group was constituted by the Ministry of Agriculture on the directions of the Hon'ble PrimeMinister, to evaluate the crop insurance schemes being implemented in the country. I was nominatedas a member of the Group on behalf of the Company. The Group has submitted its report to the Gov-ernment of India.

AIC engaged the Indian Institute of Management, Ahmedabad to help evolve its long-term businessplan and to suggest a suitable organisation structure to implement the same. Its report has been re-ceived, and is being studied by a Board Committee.

AIC has also commissioned a study on the crop insurance schemes, and how the intended beneficiariesperceived them, by the Institute of Development Studies, Jaipur, under the chairmanship of Prof. V. S.Vyas, an eminent agro-economist.

AIC has secured a prestigious technical assistance from the World Bank for its premium-rating project.The World Bank has engaged reputed international actuaries for the project. The study would be con-cluded during the current financial year.

This year, we have been able to extend crop insurance coverage to 1.8 crores farmers, up from 1.2crores last year. This has been possible through sustained publicity and awareness drives undertakenby us. We have publicised our activities and schemes through different media in all States and UTs.Apart from these regular publicity efforts, the Company has also taken up a country-wide awarenessproject for NAIS, titled "Krishi Bima Kissan Tak", wherein we plan to reach 1,00,000 villages in 3600tehsil/talukas across 400 districts of the country. Crop insurance has already touched 540 out of about600 districts in 23 States and 2 Union Territories. We aim to steadily expand the coverage-base, until wehave 6 crore farmers under our umbrella. The day we achieve this target, I shall have realised mydream.

To extend our service to the remotest corners of the country, we are in the process of building up anetwork of "Krishi Bima Sansthans", who will be our rural representatives at the doorstep of the farm-ers. We plan to have KBS's in the major districts in the country. This work-force will also generate ruralemployment, and thus we hope to contribute to the country's social needs in our small way.

In this hour of achievement, we must pause to register our gratitude to the Government of India andthe various State & UT Governments, for their unstinting support, both in terms of policy and in termsof finance. Our thanks also go out to the Directors of the Company, as well as all the employees, fortheir dedicated service to the Company. We must thank the various financial institutions for the ser-vices rendered. We have received logistic and moral support from many other organisations and indi-viduals, including the NSSO, NIA (Pune), various NGOs, Consultants, people's representatives at alllevels etc. We post our heartfelt thanks to them all.

To achieve such a daunting task, our own infrastructure also needs to be strengthened. The HeadOffice of the Company has been shifted to a central location in a modern building, and has been equippedwith state-of-the-art-technology. In addition to our 14 existing Regional Offices, 3 more have com-menced independent operations, - at Jaipur, Chandigarh, and Dehradun. We are also taking new pre-mises for 4 ROs, namely, Kolkata, Lucknow, Patna & Bhopal. The Company has also developed itsown dynamic website.

We have come a long way in a very short span of time, but much more remains to be done. As the poetRobert Frost had famously said, ……..

"The woods are lovely, dark and deep,

But I have promises to keep,

And miles to go before I sleep,

And miles to go before I sleep."

SUPARAS BHANDARIChairman cum Managing Director

98

The Directors have great pleasure in presenting the Second Annual Report on the workingand affairs of the Company and the audited statement of accounts for the year ending 31stMarch, 2005.

FINANCIAL RESULTS

The summarised financial results of the Company for the period under review are as under:

Rs. in Crores

Current Year Period endedEnded 31/03/05 31/03/04

REVENUE ACCOUNT

1. Net Premium 455.37 189.10

2. Net Incurred Claims 276.84 282.51

3. Operating Expenses and OtherOutgo less Other Income 8.35 5.41

4. Investment Income Apportioned toRevenue less Expenses 47.14 5.88

5. Revenue Profit/(Loss) (1+4-2-3) 217.32 (92.94)

Profit & Loss Account

6. Interest, Dividends and Rents (gross) 7.49 10.71

7. Other income less Other Outgo 0.05 0.01

8. Amortisation of Premium on Investments Written Off 0.21 NIL

9. Preliminary and other expenses 0.48 0.70

10. Profit before tax (5+6+7-8-9) 224.17 (82.92)

11. Provision for Taxes 55.71 NIL

12. Profit After Tax (10-11) 168.46 (82.92)

13. Profit Available for Appropriation 84.62 NIL

14. Transfer to General Reserve 83.84 NIL

15. Prior period losses & other adjustments NIL NIL

16. Balance of Profit C/F NIL (82.92)

DIVIDEND

During the period under review the Company earned a post tax profit of Rs.168.46 Croresfrom its operations after providing for the required provisions and reserves. After adjust-ment for prior period losses, balance of Rs. 84.62 Crores profit left has been transferred to theGeneral Reserve. Your directors do not recommend any dividend in order to conserve theresources of the Company to meet claims liability in the current year and to build up AIC'sfinancial strength for meeting its liabilities when crop insurance schemes being implementedby it are brought under the actuarial regime.

OPERATIONS

The period under review was a period of consolidation and enhancing the operations of theCompany. The Farmers brought under the insurance net increased from 12 million to 18 mil-

lion. AIC now insures the larg-est number of farmers in theworld. All past and pendingclaims of NAIS have beencleared by AIC. The NationalAgricultural InsuranceScheme is implemented in 23States and 2 Union Territorieswith Rajasthan, Jammu &Kashmir, Haryana andUttaranchal joining theScheme. The Company hopesto bring in Punjab into its in-surance fold soon. TheCompany's operations arenow run from the H.O at NewDelhi and 17 Regional Offices.

A Research and Development Department has been set up at the H.O to design more farmerfriendly and affordable insurance products. An actuarial cell has also been created at H.O toprovide actuarial evaluation of various crop insurance products.

Several new products viz Coffee Insurance, Varsha Bima2005 and Sukha Suraksha Kavach,which were either pilot projects or in different stages of development last year have beenlaunched during Khariff 2005. Basmati Rice Insurance and Poppy Insurance products areready and will be launched at the appropriate time. Development work is also on for insur-ance for perennial horticulture crops, plantation crops (tea, rubber, coconut, etc.), vegetablesand medicinal & aromatic plants.

During the year under review, the Company was able to wipe off last year's loss of Rs. 82.92crores and still show a post tax profit of Rs 168.46 crores after making additional provisionsfor Reserve for Unexpired Risks of Rs. 93.85 crores and Claims incurred But Nor Reported ofRs.338.52 Crores. The year 2004 - 05 started with a delayed and deficit monsoon adverselyaffecting the Khariff 2004 crop. The Rabi 2004 - 05 season was average. Agricultural produc-tion in the country grew at a meager 1.1% during the year. Despite such adverse conditionsAIC has shown encouraging results both in terms of profits and increase in business. This wasbrought about through sus-tained promotion activitiesand awareness campaignsundertaken by the Com-pany. The gross premiumincreased by 148.8% Morefarmers were brought intothe insurance net by offeringthem better products andservices and through thecrop insurance educationand awareness programsand sustained publicityreaching upto village level.

The Head Office of the Com-pany has been shifted to amodern building and has

Directors’ Report

1110

been equipped with state ofthe art technology and allmodern conveniences. Thiswill be a great help in mak-ing its operations more effi-cient. The Board of Directorshas approved the introduc-tion of better InformationTechnology to provideinterconnectivity upto all re-gional offices through theCompany's IT project.

The Company was repre-sented in the Joint Group setup by the Ministry of Agricul-ture at the behest of the PrimeMinister to study crop insur-ance programs being imple-mented in the country. AICprovided the group with sta-

tistical data and other technical inputs and helped the group in formulating its recommenda-tions. AIC undertook a project to obtain first hand information on the farmer's perception ofthe Crop Insurance Schemes being currently implemented and their insurance needs. Underthe project 15000 farmers, 3000 State Government Officials and 3000 Officials of other stakeholders like Commercial Banks, Regional Rural Banks, and Cooperative Societies were inter-viewed and their feedback analysed. AIC has engaged Prof. V.S. Vyas and his team at TheInstitute of Development Studies, Jaipur to carry out a comprehensive study of the workingof crop insurance schemes. Such a study is being conducted for the first time in 20 years. TheIndian Institute of Management, Ahmedabad has been engaged to recommend a businessstrategy and an efficient organisation structure and personnel policies for the Company.

AIC has secured a prestigious technical assistance from the World Bank for its premium rat-ing project. The World Bank would engage reputed international actuaries for the project.The study would be con-cluded during the currentfinancial year.

AIC contributed its bit forvictims of the devastatingTsunami by quickly pro-cessing the claims in the af-fected districts inPondichery and TamilNadu. As the whole districtwas not affected, the claimswere treated as 'localisedcalamity' and claims of in-dividual farmers werepassed as a special case fortotal loss on the sum in-sured.

NATIONALAGRICULTURALINSURANCE SCHEME(NAIS)

National Agriculture InsuranceScheme is the main scheme beingimplemented by AIC. The concertedefforts of the Company towards edu-cating the farmers and making themaware of crop insurance productsduring the period under review haveborne rich dividends.

During the period under review thenumber of farmers insured under

NAIS grew 26% to 156.42 lac farmers; the area covered grew 53% to 287.9 lac hectares andpremium received under NAIS grew 45%. The figures reflect the data received upto date ofmaking this report and the number of farmers covered under the Scheme is estimated to crossthe 18 million mark when all data is received.

As a result of the various studies conducted a number of improvements in NAIS have beensuggested. The Joint Group has also recommended extensive improvement and enhancedcoverage under the Scheme. The technical aspects of the recommendations made are beingstudied in detail and will be included in the Scheme where ever possible.

FARM INCOME INSURANCE SCHEME (FIIS)

FIIS is an extension of NAIS and protects the farmers income fluctuation arising out of eitherlow yield or low price or both. Government support was granted to the scheme. The schemewas launched on an experimental basis in 18 districts of 11 states during Rabi 2003-04. FIISwas continued on pilot basis in 4 states in 19 districts during Kharif 2004. The results of theproject were as under:

Season No. of Farmers Area Covered Premium Received Claims Paid Insured (Hectares) Rs. Rs.

Rabi 2003 - 04 1,89,206 1,91,027 14,07,32,493 1,43,65,059

Khariff 2004 2,34,839 2,10,808 14,85,39,148 10,17,00,000

The Government has withdrawn thisScheme with effect from Rabi 2004 - 05season.

CLAIMS INVESTIGATIONBesides post harvest investigation ofbank's records, land holding records andsupervision of crop cutting experiments,the Company also carried out concurrentinvestigations to assess the area sown,crop health and yield assessment whilethe crops were still standing in the fields.Use was also made on experimental ba-sis of remote sensing technology in someareas. These investigations have yieldedgood results and were of immense help

1312

in monitoring the risks being underwritten by AIC.

The creation of a panel of investigators to investigate and assess claims is under consider-ation of the Board of Directors and is expected to be operationalised during the current year.

NEW PRODUCTS LAUNCHED

The Company has, during the period, after carrying out extensive research and study devel-oped the under mentioned new products which will benefit the agricultural sector in times tocome.

A. VARSHA BIMA 2005

The Company's Rainfall Insurance product (Varsha Bima) was developed to combat effects ofadverse rainfall incidence. The product is aimed at mitigating some of the adverse financialeffects of rainfall variation on farm incomes. In this product, the percentage deviation in cropoutput due to adverse deviation in rainfall is estimated and the farmers compensated as perthe deviation from normal. The advantage of the scheme is that rainfall data is available fromthe rain gauge stations of the Meteorological Department and claims can be quickly pro-cessed.

Varsha Bima 2005 was launched by the Hon'ble Finance Minister, Mr.P.Chidambaram on 2ndJune 2005 and is being implemented in 125 (IMD) Rain Gauge Station areas across 10 statesduring Khariff 2005. During the current season of Khariff 2005, 1.25 lac farmers covering anarea of 97.105 hectares have been insured for a sum of Rs. 5537.11 lacs and a premium of Rs.314.6 lacs has been received.

B. SUKHA SURAKSHA KAVACH

AIC has launched a rainfall index based insurance product exclusively for the State of Rajasthan.It was implemented in 23 districts for the benefit of farmers in draught prone areas. Theproduct has been designed to cover popular and widely grown crops like Gaur, Bajra, Maize,

Jowar, Soyabean and Groundnut whichare grown in semi arid climate ofRajasthan.

C. COFFEE INSURANCE.

Coffee Rainfall Index & Area Yield In-surance has been introduced on a pilotbasis in the state of Karnataka, to pro-tect the insured against the likelihood ofdiminished coffee output yield resultingfrom either shortfall in actual rainfall in-dex within a specified geographical lo-cation and specified time period and/oryield losses due to other non preventablenatural factors, upto the maximum suminsured.

The product was launched by theHon'ble Minister of State (independentcharge), Statistics and Program Imple-mentation Mr. Oscar Fernandes on 22ndMarch 2005. 58 coffee plantations covering an area of 514.21 Hectares have been insured forRs. 169.43 Lacs so far.

USE OF REMOTE SENSING TECHNOLOGY (RST)

This satellite based technology was put to use on a pilot basis and will make available to AICindependent, timely, accurate and reliable data which can be utilised in underwriting, risksmonitoring and claims processing. The Company has already commenced the pilot project in3 districts i.e. one each in Andhra Pradesh, Gujarat, and Maharashtra for Khariff 2004 and 2districts each in Karnataka and and Maharashtra during Rabi 2004 - 05 season and will pro-vide AIC:

• Crop Health Reports;

• Acreage Sown ; and

• Yield Modeling

If the pilot is successful in givingthe requisite data, RST will be intro-duced in our operations on a muchlarger scale.

CAPITAL

The Company did not raise any fur-ther capital during the period underreview.

INVESTMENTS

The funds that became availablefrom the Crop Insurance operationswere invested by the Company asper the IRDA Guidelines and thedirections of its investment policy

1514

under the supervision of the Investment Committee of the Board. Income from investmentsduring the year was Rs.40.97 Crores. AIC;s equity investments showed a capital appreciationof Rs.72.65 lacs. During the period under review efforts were made to achieve the investmentpattern prescribed by the IRDA guidelines. With rising interest rates during the year marketyields of Government securities purchased earlier fell but coupon rates of fresh issues rose tocompensate the notional losses. As the Company investments in such securities is long termthe average interest income will not be effected. The Company participated in three auctionsof Government securities and also purchased Treasury Bills for investing its shorter termfunds. AIC also made limited investment of Rs.2.82 Crores in equity shares. Investmentswere made in Power, Banking and Infotech sectors mostly during IPOs. These investmentshave shown very good appreciation.

INSURANCE REGULATORY AND DEVELOPMENT AUTHORITY (IRDA)

The Company is engaged in the crop insurance business and is, thus, governed, among oth-ers, under the Insurance Act, 1938, IRDA Act, 2000 and the Rules and Regulations framedthereunder. The Company had obtained the necessary R-3 Licence in October, 2003 fromIRDA and the same has been renewed upto date. Its paid-up capital of Rs. 200 Crores con-forms to the minimum required under the Insurance Act, 1938 for General Insurance Compa-nies. The accounts of the Company for the period under review are drawn up in compliancewith the provisions of the IRDA (Preparation of Financial Statements and Auditors Report)Regulations, 2002. An appointed actuary has also been appointed as required under the IRDAGuidelines.

CLAIMS

Claims amounting to Rs.185.67 Crores were incurred during the year. Additional provisionfor un-expired risks amounting to Rs. 93.84 Crores has been made in the accounts for the year.A provision of Rs.338.52 Crores has been made towards claims incurred but not reportedbased on actuarial valuation.

AWARENESS & PUBLICITY PROGRAMMES

Besides making the farming community, rural banks and local administration aware of thebenefits of crop insurance, the Company interacted with 15000 farmers, 3000 state govern-ment officials and 3000 officials of Commercial banks, Regional Rural Banks and CooperativeSocieties during the year under review to determine their insurance needs and obtain theirfeedback on the crop insurance and rainfall insurance schemes being implemented by AIC.

The Company engaged in ex-tensive awareness and pub-licity activities during theyear. Use was made of bothprint and electronic media,posters, audio visual vansand TV. A number of aware-ness meetings were alsoorganised at state and districtlevels wherein farmers, bankofficials, district level govern-ment functionaries and otherinterested parties werebriefed about the services onoffer. A special effort wasmade to give wide publicityto the newly launched

schemes. It can be hoped that wide decimation of information on our schemes would attractmore and more non-loanee, small, large and medium farmers to opt for insurance cover.

A massive Crop Insurance awareness campaign amongst farmers called "Krishi Bima KisanTak" touching 25,000 villages in 3,200 Tehsils of 400 Districts is being undertaken. The cam-paign was launched in the State of Maharashtra by the Hon'ble Chief Minister Sh. VilasraoDeshmukh, in Andhra Pradesh by the Hon'ble Chief Minister Sh. Rajashekhar Reddy and inKerela by its Hon'ble Chief Minister Sh. Oommen Chandy. The object is to take the cropinsurance program down to the farmer's doorstep.

MICRO LEVEL MARKETING STRATEGYIn our quest to reach out to the farmer at his doorstep AIC has made plans to launch the'Krishi Bima Sansthan'. The plan conceptualises using the resources of rural organisationslike the panchayats, self help groups, cooperatives etc. and the rural entrepreneurs to marketcrop insurance schemes especially to non-loanee farmers who are left out of the net of ruralfinancial institutions. The KBSs are to be established at District levels and Agents placed atTehsil level on an outsourcing basis. This will help AIC to reach out to millions of farmers attheir village. This will also provide ample employment opportunity to rural youth.

The draft plan for establishing KBS is ready and will be put into operation after receivingBoard approval.

IT PROJECT

In its quest to improve efficiency in operations, AIC has computerised its H.O and all itsRegional Offices. The H.O and some of the major R.Os were equipped with the latest state ofthe art Hardware and Software during the period under review. All officers at the H.O andtwo officers at each R.O were allotted e-mail IDs. The Company's website was redesigned.This is a dynamic website and enables AIC to interact with both outsiders and own officesand officers. Software was also developed for salary accounting and processing of feedback

1716

received from the surveys carried out. All avail-able data is now computerised and can be readilyaccessed and analysed.

AIC is hiring a reputed consultant to further aug-ment its computerisation project. The object is toestablish all India interconnectivity. Effort willalso be made to establish interconnectivity withthe Nodal Banks and other intermediaries.

DIRECTORS

The Board of Directors of AIC has played a veryactive role in the progress of the Company. TheBoard of Directors met six times during the pe-riod under review. Several committees of theBoard were formed for different functions andto study various plans of the Company. Therewere 6 meetings of the committees includingAudit Committee during the year.

Mr. M. Raghavendra, Mr. K.N. Bhandari and Mr.G. C. Chaturvedi, rotational directors who haveheld office for the longest period, will retire byrotation at the ensuing AGM and being eligibleoffer themselves for re-appointment.

HUMAN RESOURCEDEVELOPMENT

Insurance, being a service industry, can run effi-ciently only on the commitment and dedication of its officers and employees. Besides officersand employees laterally transferred from GIC and absorbed in AIC, a need was felt to aug-ment the employee strength due to the increased operations and its complexities. AIC re-

cruited 16 officers at AAOs levelduring the year. In order to helpthem in achieving the Compa-nies ambitious plans along withachievement of their personalgoals, the Company places spe-cial emphasis on training. Dur-ing the year under review 14 em-ployees underwent inductiontraining program at NIA, Pune,one officer underwent training infinancial management in FORCESchool of Management, NewDelhi and one officer was trainedin actuarial subjects. A numberof officers were deputed to at-tend various seminars and work-shops in their relevant fields ofspecialisation. The Board of Di-rectors has also approved the in-

duction of a small specialised team of officers for product development. The recruitment pro-cess has been initiated and will be completed during the current year.

Employee relations remained cordial through out the period under review and the Companyand its management received unstinted cooperation during this challenging and trying year.

EXPENSES OF MANAGEMENT

The Company incurred Rs.8.45 Crores as expenses of management which is 1.45% of its grosspremium receipts.

STATUTORY AUDITORS

M/S J.P, Kapur & Umbrai, Chartered Accountants, New Delhi were appointed statutory au-ditors of the Company u/s 619 B of the Companies Act, 1956 by the Comptroller and AuditorGeneral of India. Various other firms of Chartered Accountants were appointed by CAG asbranch auditors for the different regional offices of AIC. The Board of Directors wishes toplace its appreciation of the guidance provided by them.

The management's comments on the auditor's observations are given by way of addendum tothis report.

ADDITIONAL INFORMATION REQUIRED U/S 217 OF THE COMPANIESACT, 1956

Additional information regarding conservation of energy is not applicable to the Companybeing a service organisation wherein only minimal domestic power is used in running offices.

No foreign technology was imported or absorbed by the Company. The inflow or outgo offoreign exchange during the year was as under:

Foreign Exchange Earned: NIL

1918

Expenditure in Foreign Exchange: NIL

No employee of the Company was in receipt of remuneration in excess of limits specified u/s 217(2A) of the Companies Act, 1956.

DIRECTOR’S RESPONSIBILITY STATEMENTPursuant to section 217(2AA) of the Companies Act, 1956 directors hereby confirm that:

i) in preparation of Annual Accounts for the year ended 31st March 2005, the applicableaccounting standards have been followed alongwith proper explanations relating tomaterial departures, if any;

ii) appropriate accounting policies have been selected and have been applied consistentlyand that the judgments and estimates made are reasonable and prudent so as to give atrue and fair view of the state of affairs of the Company as at the end of the financial yearand the profit of the Company for the period ended 31st March, 2005;

iii) proper and sufficient care has been taken for the maintenance of adequate accountingrecords in accordance with the provisions of the Companies Act, 1956, for safeguardingthe assets of the Company and for prevention and detection of fraud and other irregu-larities;

iv) the Annual Accounts have been prepared on a 'going concern' basis.

OFFICIAL LANGUAGE IMPLEMENTATIONDuring the period under review the Company made continuous efforts in the implementa-tion of the Official Language Policy of the Government of India. Replies to a large number ofRajya Sabha, Lok Sabha and Parliamentary Committee queries were prepared in Hindi. Mostpress releases of AIC are both in Hindi and English. All crop insurance schemes implementedby AIC and presentations prepared for them are prepared and published in Hindi and En-

glish. Calendars, posters and other publicity materials of the Company are also bilingual.Being a rural oriented company, AIC places a lot of emphasis on the use of the NationalLanguage. Hindi Pakhwadas are held annually at the H.O and R.Os.

ACKNOWLEDGEMENTSThe directors place on record their deep appreciation of the excellent work and enthusiasmshown by the managers, officers and other employees of the Company in very trying circum-stances for the running, enhancing and streamlining its operations.

They are also grateful to RIBs, Banks, local administration officials of State Governments andother intermediaries for their valuable contribution to the success of AIC's crop insuranceschemes.

The Directors also express their gratitude to the Ministry of Finance, GOI, Ministry of Agri-culture, GOI, IRDA and the concerned officials of CAG for their guidance and support.

For and on behalf of the Board of Directors,

Dated the 25th day of November, 2005 SUPARAS BHANDARI

Place: New Delhi Chairman-cum-Managing Director

2120

1. INTRODUCTION :

Indian economy is to a very large extent dependent on the agriculture sector. A majority ofIndians are still rural based. Growth in agriculture production directly influences the growthof Indian GDP. A good crop season puts purchasing power in the pockets of a large portionof the Indian population and therefore boosts the sales in the FMCG sector. This in turnincreases production and sales in the manufacturing sector and the services sector revenuesare also proportionately enhanced. The UPA Government has, therefore, laid a lot of stresson rural development. The Prime Minister and the Finance Minister have time and againreiterated their intent to focus on developing rural infrastructure and the budget for the yearearmarked a transfer of large resources for the purpose. Agriculture insurance plays a vitalpart in giving financial security to the farming community and encouraging the use of modernfarming techniques, tools, seeds, fertilizers and other inputs. The availability of rural creditfor farming operations is also encouraged by the various crop insurance schemes beingimplemented by AIC.

The year under review saw only a modest 1.1% growth in agricultural production. Themonsoons were delayed and deficient in some areas adversely affecting the Khariff 2004yields. The Rabi 2004 – 05 was also only average. The Government’s efforts in increasingrural credit and additional investments made in rural infrastructure did improve the situationto some extent. The number of farmers covered by crop insurance schemes saw a dramaticrise to 18 million and the sum insured also rose proportionately.

The upliftment of the rural economy is expected to be a top priority for the United ProgressiveAlliance Government. This has been made clear by the statements made by the Prime Minister,Dr. Manmohan Singh, the Finance Minister, Mr. P. Chidambram and leaders of the othercoalition parties. As the thrust will also be on reducing rural poverty, efforts will also bemade to increase agricultural production by making available rural credit. Crop and otherrural insurance products may be able to contribute in the government’s efforts at providingfinancial security and thereby help in reducing rural poverty and indebtedness.

2. INVESTMENTS & STOCK MARKET SCENARIO :

Although interest rates rose marginally during the year and there was also a mild but risinginflation rate the placement of funds in time deposits in banks was unattractive. Theseconditions are best suited to investments in manufacturing, construction and other basicindustries and products. Cheaper bank credits encourage capital purchases which result increation on long term values. Although there is a general mood of optimism in the Indianeconomy investments have been slow in coming. Good IPOs are still few and far between.This indicates the cautious approach adopted by industry leaders.

Although the stock markets are not considered good indicators of the state of the economy,its sharp rise during the period under review does indicate the optimism and confidence ineconomic development. During this period the indicative BSE sensex saw a sharp rise tocross the psychological 7000 mark. There have thereafter been some fluctuations reflectingthe caution due to rising crude prices and hiccups in the government’s liberalization policy.The sensex is now well on its way to stabilize at a fair level. Keeping in mind the soundfundamentals and the excellent results declared recently most market watchers believe thatit will touch 8000 level by the end of this fiscal year.

The Company took advantage of the Bull market conditions to start a modest portfolio ofequity investments. The Company made investments in the IPOs of Banking, Infrastructure

Management Discussion & Analysisfor the Financial Year ended on 31st March 2005

and Information Technology sectors. The investments have shown very good capitalappreciation and the same has been reflected in the ‘Fair Value Change Account’. Most ofAIC’s investments are still in government securities and other top rated debt instrumentsand have not been effected by the recent market fluctuations.

3. AIC’S OPERATIONS:

In the given situation, with the expected growth in agriculture, the Company is poised torecord a growth in business in all its existing and future schemes. It has a young, dynamicand enthusiastic work force as a major Strength. New and innovative ideas and thedetermination to relentlessly pursue its goals will see it grow in the service of the rural andagricultural sector.

The experience of its initial years of operations revealed certain organisational Weaknesses.A gap was felt in certain specialized skills in key disciplines and fields. The gap was bridgedtemporarily by outsourcing certain routine functions, recruiting a small number of personnelwith the required qualifications and experience and seeking assistance of experiencedprofessionals in the field. The Company has engaged the services of Indian Institute ofManagement – Ahmedabad as a consultant to conduct a study of its operations andrecommend the most appropriate organisation structure and to help the Company in devisinga long term business plan to achieve its ambitious goals. Once this report is ready, most ofthese gaps will be filled. Training of the officers and staff of AIC will be pursued vigorouslyto hone their existing skills and help them acquire new skills. The challenge is to sustain theirpresent level of enthusiasm with appropriate motivational inputs from time to time. A studywas also commissioned to study the current crop insurance schemes and to suggestimprovements and point out additional insurance needs of the farming community. The studywas carried out by a team of eminent agro-economists of the Institute of Development Studies,Jaipur. AIC has bagged a prestigious technical assistance from the World Bank to providepremium rating for the crop insurance products and give support in the ongoing researchand development activities. Being a newly incorporated company AIC has not yet achievedthe financial strength to be able to fully support its future programs. A few good years willhelp it achieve the required financial muscle.

Rural and Agriculture Insurance is a largely unexplored field and enormous Opportunitiesbeckon AIC. The existing crop insurance schemes of the Company are not even covering allthe loanee farmers, let alone the crores of non-loanee, medium and large farmers spreadacross the country. States are only notifying a limited number of districts and crops for coverageunder NAIS. The Company is making efforts to get the states to notify a larger number ofdistricts and obtain coverage of more crops. AIC is also making concerted efforts throughpublicity and awareness programmes to educate the farmers about the schemes being operatedby it and the benefits of having insurance cover for their crops. A portion of crop credit doesnot have insurance cover at present. This is a large untapped market which must be exploitedin the years to come.

The major Threat to the Company is not competition but a catastrophic loss in its initial fewformative years. A study of historic claims data reveals that claims ratios in crop insuranceare very high. Consequently the premium rates would also be prohibitively high when theactuarial regime is put in place. Government support to its schemes goes a long way inovercoming these problems. AIC is also making efforts to obtain reinsurance cover from theIndian Reinsurer and from the international market to mitigate the risk of catastrophic lossesfor its rainfall product. The only competition AIC faces are from small rural schemes being

2322

run by other general insurance companies.

Our aim in the near future is:

• To develop a variety of rural insurance products.

• To arrange tie-ups with financial institutions operating in rural areas for provision ofinsurance cover to agricultural activities financed by them.

• To bring corporate/contact farming under insurance cover.

• To link-up with different sponsoring agencies like sugar factories and food processingunits who have an interest in agro products.

• To bring under insurance cover High Tech Agricultural projects such as Horticultureand Floriculture.

• To develop a vast network of intermediaries operating in rural areas to keep AIC intouch with the insurance needs of the farming community and to develop our business.

The growing rural economy will usher in a bright future for AIC and help it to serve its ruralclientele better ensuring prosperity and financial security to all the participants in this nobleendeavour.

AG

RIC

UL

TU

RE

IN

SU

RA

NC

E C

OM

PA

NY

OF

IND

IA L

IMIT

ED

A

tten

dan

ce L

og f

or t

he

Boa

rd o

f D

irec

tors

NA

ME

OF

DIR

EC

TO

RS

Dat

e of

Dat

e of

Ap

poi

ntm

ent

Ces

sati

on1

23

45

6

31

.05.

0410

.06.

0418

.06.

0424

.09.

0414

.12.

0429

.03.

05

Shri

Su

para

s B

hand

ari

Sinc

e In

corp

orat

ion

N.A

.P

rese

ntP

rese

ntP

rese

ntP

rese

ntP

rese

ntP

rese

nt

Shri

T. K

. Das

Sinc

e In

corp

orat

ion

N.A

.P

rese

ntP

rese

ntP

rese

ntL

eave

Lea

veL

eave

Shri

A. V

. Pu

rush

otha

man

Sinc

e In

corp

orat

ion

N.A

.P

rese

ntP

rese

ntL

eave

Pre

sent

Pre

sent

Pre

sent

Dr.

K.G

. Kar

mak

arSi

nce

Inco

rpor

atio

nN

.A.

Lea

veP

rese

ntP

rese

ntL

eave

Lea

veL

eave

Mr.

M. R

agha

vend

ra13

th J

anu

ary

2003

N.A

.P

rese

ntP

rese

ntL

eave

Lea

veL

eave

Pre

sent

Mr.

K.N

. Bha

ndar

i9t

h M

ay 2

003

N.A

.P

rese

ntP

rese

ntP

rese

ntP

rese

ntP

rese

ntP

rese

nt

Mr.

S.K

. Cha

nana

28th

Ju

ne 2

003

N.A

.P

rese

ntP

rese

ntP

rese

ntP

rese

ntP

rese

ntL

eave

Mr.

G.C

. Cha

turv

edi

28th

Ju

ne 2

003

N.A

.L

eave

Lea

veP

rese

ntP

rese

ntL

eave

Lea

ve

Mr.

T.K

. Roy

29th

Dec

embe

r 20

03N

.A.

Pre

sent

Pre

sent

Lea

veP

rese

ntL

eave

Pre

sent

Mr.

Nav

ed M

asoo

d29

th D

ecem

ber

2003

N.A

.L

eave

Lea

veL

eave

Lea

veP

rese

ntL

eave

Mr.

S.S

. Pra

sad

31st

Mar

ch 2

004

N.A

.P

rese

ntP

rese

ntP

rese

ntL

eave

Pre

sent

Lea

ve

Mr.

Sat

ish

Cha

nder

31st

Mar

ch 2

004

N.A

.L

eave

Pre

sent

Pre

sent

Pre

sent

Lea

veP

rese

nt

2524

CAG Report

COMMENTS OF THE COMPTROLLER AND AUDITOR GENERALOF INDIA UNDER SECTION 619(4) OF THE COMPANIES ACT 1956ON THE ACCOUNTS OF AGRICULTURE INSURANCE COMPANYOF INDIA LIMITED FOR THE PERIOD ENDED 31 MARCH 2005.

A. BALANCE SHEET

Fixed Assets (Schedule 10) - Rs. 4.84 Crore

1. The fixed assets schedule does not indicate gross block and accumulateddepreciation transferred to the Company by the General Insurance Corporation ofIndia. This is noting accordance with the format prescribed by Insurance Regulatoryand Development Authority as well as the Companies Act, 1956, despite beingcommented by the Comptroller & Auditor General of India on the accounts of theCompany for the year ended 31 March 2004.

Current Liabilities

Sundry Creditors (Schedule 13) — Rs. 112.98 Crore

2. A reference is invited to the Comment No. 2 (ii) of the Comptroller & AuditorGeneral of India on the Accounts of the Company for the year 2003-04 wherein it waspointed out that the interest earned on unspent balances had neither been credited tothe Govt. accounts nor the accounting policy in this regard disclosed.Despiteacceptance of the Comment by the Company (Novermber 2004), no policy in thisregard has been disclosed in accounts for the year 2004-05.

3. The balance of Rs. 83.44 crore including interest (Interest for 2004-05 Rs. 3.47 crore)as on 31 March 2005 is not verifiable as the receipts of share of Government towardsindemnity for food crops (which is not meant to be met out of Corpus Fund) had beenaccounted for in the Corpus Fund.

B. REVENUE ACCOUNT

Premium Earned (Net) – Schedule 1 – Rs. 455.37 Crore

4. The above includes an amount of Rs. 60.27 lakh as unearned premium, whichshould have been included in the Current Liabilities of the Company. This has resultedin overstatement of Premium and Profit of the Company by Rs. 60.27 lakh.The factsand figures mentioned above may also please be furnished.

Claims Incurred (Net) – Schedule 2 – Rs. 276.85 Crore

Claims Outstanding at the end of the year Rs. 386.71 Crore

5. The above does not include an amount of Rs. 178.43 crore due to under estimationof claimes Incurred but Not reported (IBNR). This has resulted in the understatementof claimes Outstanding at the end of the year and overstatement of the profit of theCompany by Rs. 178.43 crore.

C. Notes forming Part of Accounts6. The fact that the Company received financial assistance of Rs. 1458.51 crore fromthe Government for meeting out the certain expenses for the year 2004-05, as detailedbelow have not been disclosed in the notes forming part of the Accounts:

Corpus Fund — Rs 139.87 croresA & O Expenses — Rs 0.05 croresPublicity Expenses — Rs 0.49 croresPremium Subsidy Fund — Rs 28.15 croresBank Service Charges — Rs. 23.51 croresOthers — Rs. 1266.44 crores

2726

amounting to Rs.589,566 thousands and Liabilities amounting to Rs. 4,500,329thousands of crop insurance business as given by GIC of India were accounted for bythe Company without any formal agreement/ scheme of arrangement between theCompanies and without obtaining approval from the Government of India. In view ofthe aforesaid, claims paid for the period prior to April 1, 2003 has been debited to theRevenue account and cannot be substantiated. Neither the balance outstanding fromGIC of India as at the year end aggregating to Rs. 138,728 thousands nor the nettransactions entered in the relevant account during the year aggregating to Rs. 1,690,202thousands be verified;

(b) Non compliance of Employees Provident Fund and Miscellaneous Provisions Act, 1952to the extent that deduction has been made at the rate of 10% instead of 12 % as prescribedby the Act and non deposit of the same with relevant authorities, amount whereofcannot be ascertained.

Give a true and fair view:

(i) in the case of the Balance Sheet of the state of affairs of the Company as at 31st March, 2005.

(ii) in the case of the Revenue Account, of the surplus for the year ended on that date.

(iii) in the case of the Profit and Loss Account, of the Profit of the Company for the yearended on that date.

(iv) in the case of Cash flow Statement of the cash flow for the year ended on that date.

4. On the basis of our examination we certify that :

(a) We have reviewed the management report and there is no apparent mistake or materialinconsistency with the financial statements.

(b) The Company has generally complied with the terms and conditions of the registrationstipulated by the Insurance Regulatory and Development Authority.

(c) We have verified the cash and bank balances and investments, by actual inspectionor by production of certificates or other documentary evidence.

(d) No part of the assets of the policyholders’ funds have been directly or indirectlyapplied in contravention of the provisions of the Insurance Act, 1938 relating to theapplication and investments of the policyholder’s funds.

Place : New Delhi For J.P., KAPUR & UBERAIDate : 25.11.2005 CHARTERED ACCOUNTANTS

(VINAY JAIN)PARTNER (M.No.95187)

To,

The Members of Agriculture Insurance Company of India Ltd.

1. We have audited the attached Balance Sheet of AGRICULTURE INSURANCE COMPANYOF INDIA LTD. as at 31st March 2005, and also the Revenue Account of Crops Insuranceand the Profit and Loss Account and the Cash flow statement for the year ended on thatdate annexed thereto. These financial statements are the responsibility of the Company’smanagement. Our responsibility is to express an opinion on these financial statementsbased on our audit

2. We conducted our audit in accordance with auditing standards generally accepted inIndia. Those standards require that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free of material mis-statement. Anaudit includes examining, on a test basis, evidence supporting the amounts and disclosuresin the financial statements. An audit also includes assessing the accounting principlesused and significant estimates made by management, as well as evaluating the overallfinancial statement presentation. We believe that our audit provides a reasonable basisfor our opinion.

3. We report that :

(a) We have obtained all the information and explanations which, to the best of ourknowledge and belief, were necessary for the purpose of our audit and found themsatisfactory.

(b) In our opinion, proper books of accounts as required by law have been maintainedby the Company so far as it appears from our examination of those books.

(c) In our opinion, proper returns, audited, from other regional cells have been receivedand are adequate for the purpose of our audit.

(d) The Balance Sheet, Revenue Account, Profit and Loss Account and Cash flowstatement are in agreement with the books of account and returns.

(e) The actuarial valuation of liabilities is duly certified by the appointed actuary.Assumptions and working papers for such valuation have been provided to us.

(f) As per General Circular No. 8/2002 dated 22/08/2002 of the Department of CompanyAffairs, the nominee directors appointed on the board of the company by publicfinancial institutions, within the meaning of section 4A of the Companies Act, 1956and Central Governments are exempt from the applicability of the provisions ofSection 274 (1) (g) of the Companies Act, 1956.

(g) In our opinion, the Balance Sheet, Revenue Account and Profit & Loss Accountcomply with the Accounting Standards referred to in Section 211 (3C) of theCompanies Act, 1956, to the extent applicable to the Company and are also inconformity with the accounting principles as prescribed in the IRDA Regulations.

(h) In our opinion, the investments have been valued in accordance with the provisionsof the Insurance Act, 1938 and the applicable IRDA Regulations.

(i) In our opinion and to the best of our information and according to the explanationsgiven to us, the said accounts read with the significant accounting policies and notesthereon are prepared and give the information as required by the Insurance Act,1938, the Insurance Regulatory Development Authority Act, 1999 and the CompaniesAct, 1956 to the extent applicable and in the manner so required, subject to:

(a) The Company had been nominated as the Implementing Agency for NationalAgricultural Insurance Scheme by the Ministry of Agriculture from April 1, 2003vide its letter ref. No. 13011/02/2003-Credit II dated October 22, 2003. Assets

Auditors’ Report

2928

Government towards indemnity for food crops(which is not meant to be met out of CorpusFund) had been accounted for in the CorpusFund.

OBSERVATION NO. 4B. Revenue AccountPremimum Earned (Net)-Schedule 1- Rs. 455.37CroreThe above includes an amount of Rs. 60.27 lakhas unearned premium, which should have beenincluded in the Current Liabilities of the Com-pany. This has resulted in overstatement of Pre-mium and Profit of the Company by Rs. 60.27lakh.

OBSERVATION NO. 5B Revenue AccountClaims Incurred (Net)-Schedule 2- Rs. 276.85CroreClaims Outstanding at the end of the year Rs.386.71 CroreThe above does not include an amount of Rs.178.43 crore due to under estimation of claimesIncurred but Not reported (IBNR). This hasresulted in the understatement of claimesOutstanding at the end of the year andoverstatement of the profit of the Company byRs. 178.43 crore.

the opening balance of Corpus Fund as at01.04.2004. In case of Karnataka State, openingbalance of Corpus Fund as on 01.04.2004 wasnegative and hence no interest was payable for theF.Y.2004-05.

In respect of Karnataka, there has been inadvertentcredit of State Govt. funds to Corpus Fund, whichpertains to claims for FC/ OS crops. However, thediscrepancy has been rectified during the year2004-05 and the final closing balance of CorpusFund as on 31.03.2005 represents the actualbalance.

Moreover, in some of the States, funds have beendrawn from the Corpus Fund, with properauthorization from the respective State/UTGovernments and utilized for adjustment ofPremium Subsidy, payment of A&O expenses andBank Service Charges.

Unearned Premium of Rs. 60.27 lakhs is arrived atafter adjusting the excess collection of earlier sea-sons with the short collection of respective seasons,the majority of which is outstanding for more thanthree years. This policy is being uniformly followedfor the Scheme since its inception.

The accounting policy in this regard shall be dis-closed from the next year.

The figure of Claims Incurred But Not Reported(IBNR) includes the claims for current seasons, forwhich the claims are not yet reported as on theBalance Sheet date, due to various reasons, viz.,non-receipt of yield data from the State Govt., etc.

During the last year, outstanding claims (includ-ing IBNR) amounted to Rs. 295.53 crores, out ofwhich actual claims paid amounted to Rs. 185.67crores.As regards the balance claims for seasonspertaining to earlier periods, no IBNR has beenprovided this year, as the Company has alreadyborne the actual claims for earlier seasons and nomore liability in this regard is anticipated. More-over, claims approved but not paid for earlier sea-sons, are included under the head of outstandingclaims.

The figure of IBNR is as certified by the Appointed

MANAGEMENT COMMENT ON AUDITORSOBSERVATIONS

AUDIT OBSERVATION

CAG Observations: Observation No. 1A. Balance Sheet1. Fixed Assets: (Schedule 10) Rs. 4.84 croreThe fixed assets schedule does not indicate grossblock and accumulated depreciation transferredto the Company by the General Insurance Cor-poration of India in the prescribed format as perInsurance Regulatory and Development Author-ity as well as the Companies Act, 1956, despitebeing commented by the Comptroller & AuditorGeneral of India on the accounts of the Companyfor the year ended 31 March 2004.

OBSERVATION NO. 2Current LiabilitiesSundry Creditors: (Schedule 13)-Rs. 112.98 croreA reference is invited to the Comment No. 2 (ii)of the Comptroller & Auditor General of Indiaon the Accounts of the Company for the year2003-04 wherein it was pointed out that theinterest earned on unspent balances had neitherbeen credited to the Govt. accounts nor theaccounting policy in this regard disclosed.Despiteacceptance of the Comment by the Company, nopolicy in this regard has been disclosed inaccounts for the year 2004-05.

OBSERVATION NO. 3Current LiabilitiesSundry Creditors: (Schedule 13) Rs. 112.98 croreThe balance of Rs. 83.44 crore including interest(Interest for 2004-05 Rs. 3.47 crore) as on 31 March2005 is not verifiable as the receipts of share of

MANAGEMENT COMMENTS

The Crop Insurance Business under National Ag-ricultural Insurance Scheme (NAIS) was trans-ferred by the General Insurance Corporation of In-dia (GIC) to Agriculture Insurance Company ofIndia Ltd. (AIC) w.e.f. 01.04.2003, vide its letterdated February 3, 2004. The Assets & Liabilitiestransferred by GIC included Fixed Assets amount-ing to Rs. 76,89,886.00 at various Crop Cells as wellas at Delhi Office.

As in the case of transfer of business, the value ofFixed Assets transferred by GIC to AIC, vide itsabove referred letter, have been taken as the open-ing balance in the books of AIC, which is as per theapplicable laws. Since the amount debited to AICby GIC for these assets is Rs. 76,89,886.00 only,hence the value of these assets has been taken atthe above amount only in the books of AIC.

The original cost as well as the accumulated de-preciation of the above referred assets cannot bereflected in the books of AIC, since AIC has ac-quired these assets at their WDV, & hence theseassets are incorporated in the books of AIC at theirWDV only. Hence, the Preliminary ObservationMemo may kindly be dropped.Our Reply:

As pointed out by C&AG and accepted by us, In-terest earned for the FY 2003-04 has been creditedto the Corpus Fund and disclosed vide Note No.16. Further, we have also credited interest on Cor-pus Fund pertaining to the Current FY 2004-05. Asper the past practice, no interest is credited to Gov-ernment Funds other than Corpus Fund, becausethat's a part of premium ought to have been remit-ted in advance rather than at the nick time of dis-bursement of claims, whereby we loose interest onit, but this is as per flat rate regime under theScheme.

Though the Accounts have been drawn up on theunderlying Policy, the Accounting Policy in thisregard has been inadvertently left out. Noted forfuture compliance. Hence, the Preliminary Obser-vation Memo may kindly be dropped.

Total interest payable on Corpus Fund for the F.Y.2004-05 amounts to Rs. 3.47 crores. This is arrivedat by applying average interest yield i.e. 4.62% on

3130

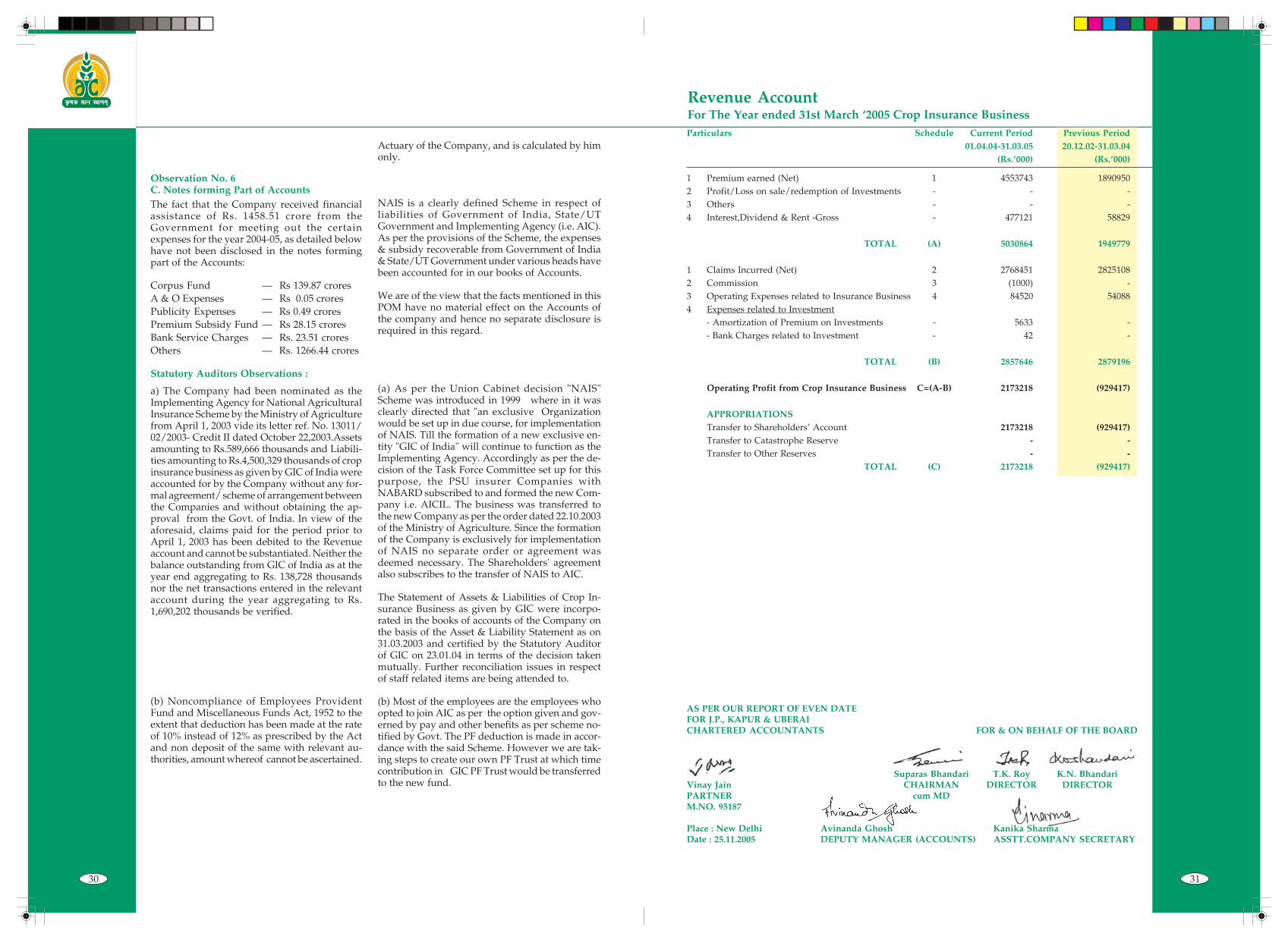

Revenue AccountFor The Year ended 31st March ‘2005 Crop Insurance BusinessParticulars Schedule Current Period Previous Period

01.04.04-31.03.05 20.12.02-31.03.04(Rs.’000) (Rs.’000)

1 Premium earned (Net) 1 4553743 18909502 Profit/Loss on sale/redemption of Investments - - -3 Others - - -4 Interest,Dividend & Rent -Gross - 477121 58829

TOTAL (A) 5030864 1949779

1 Claims Incurred (Net) 2 2768451 28251082 Commission 3 (1000) -3 Operating Expenses related to Insurance Business 4 84520 540884 Expenses related to Investment

- Amortization of Premium on Investments - 5633 -- Bank Charges related to Investment - 42 -

TOTAL (B) 2857646 2879196

Operating Profit from Crop Insurance Business C=(A-B) 2173218 (929417)

APPROPRIATIONSTransfer to Shareholders’ Account 2173218 (929417)Transfer to Catastrophe Reserve - -Transfer to Other Reserves - -

TOTAL (C) 2173218 (929417)

Observation No. 6C. Notes forming Part of AccountsThe fact that the Company received financialassistance of Rs. 1458.51 crore from theGovernment for meeting out the certainexpenses for the year 2004-05, as detailed belowhave not been disclosed in the notes formingpart of the Accounts:

Corpus Fund — Rs 139.87 croresA & O Expenses — Rs 0.05 croresPublicity Expenses — Rs 0.49 croresPremium Subsidy Fund — Rs 28.15 croresBank Service Charges — Rs. 23.51 croresOthers — Rs. 1266.44 crores

Statutory Auditors Observations :

a) The Company had been nominated as theImplementing Agency for National AgriculturalInsurance Scheme by the Ministry of Agriculturefrom April 1, 2003 vide its letter ref. No. 13011/02/2003- Credit II dated October 22,2003.Assetsamounting to Rs.589,666 thousands and Liabili-ties amounting to Rs.4,500,329 thousands of cropinsurance business as given by GIC of India wereaccounted for by the Company without any for-mal agreement/ scheme of arrangement betweenthe Companies and without obtaining the ap-proval from the Govt. of India. In view of theaforesaid, claims paid for the period prior toApril 1, 2003 has been debited to the Revenueaccount and cannot be substantiated. Neither thebalance outstanding from GIC of India as at theyear end aggregating to Rs. 138,728 thousandsnor the net transactions entered in the relevantaccount during the year aggregating to Rs.1,690,202 thousands be verified.

(b) Noncompliance of Employees ProvidentFund and Miscellaneous Funds Act, 1952 to theextent that deduction has been made at the rateof 10% instead of 12% as prescribed by the Actand non deposit of the same with relevant au-thorities, amount whereof cannot be ascertained.

Actuary of the Company, and is calculated by himonly.

NAIS is a clearly defined Scheme in respect ofliabilities of Government of India, State/UTGovernment and Implementing Agency (i.e. AIC).As per the provisions of the Scheme, the expenses& subsidy recoverable from Government of India& State/UT Government under various heads havebeen accounted for in our books of Accounts.

We are of the view that the facts mentioned in thisPOM have no material effect on the Accounts ofthe company and hence no separate disclosure isrequired in this regard.

(a) As per the Union Cabinet decision "NAIS"Scheme was introduced in 1999 where in it wasclearly directed that "an exclusive Organizationwould be set up in due course, for implementationof NAIS. Till the formation of a new exclusive en-tity "GIC of India" will continue to function as theImplementing Agency. Accordingly as per the de-cision of the Task Force Committee set up for thispurpose, the PSU insurer Companies withNABARD subscribed to and formed the new Com-pany i.e. AICIL. The business was transferred tothe new Company as per the order dated 22.10.2003of the Ministry of Agriculture. Since the formationof the Company is exclusively for implementationof NAIS no separate order or agreement wasdeemed necessary. The Shareholders' agreementalso subscribes to the transfer of NAIS to AIC.

The Statement of Assets & Liabilities of Crop In-surance Business as given by GIC were incorpo-rated in the books of accounts of the Company onthe basis of the Asset & Liability Statement as on31.03.2003 and certified by the Statutory Auditorof GIC on 23.01.04 in terms of the decision takenmutually. Further reconciliation issues in respectof staff related items are being attended to.

(b) Most of the employees are the employees whoopted to join AIC as per the option given and gov-erned by pay and other benefits as per scheme no-tified by Govt. The PF deduction is made in accor-dance with the said Scheme. However we are tak-ing steps to create our own PF Trust at which timecontribution in GIC PF Trust would be transferredto the new fund.

AS PER OUR REPORT OF EVEN DATEFOR J.P., KAPUR & UBERAICHARTERED ACCOUNTANTS FOR & ON BEHALF OF THE BOARD

Suparas Bhandari T.K. Roy K.N. BhandariVinay Jain CHAIRMAN DIRECTOR DIRECTORPARTNER cum MDM.NO. 95187

Place : New Delhi Avinanda Ghosh Kanika SharmaDate : 25.11.2005 DEPUTY MANAGER (ACCOUNTS) ASSTT.COMPANY SECRETARY

3332

AS PER OUR REPORT OF EVEN DATEFOR J.P., KAPUR & UBERAICHARTERED ACCOUNTANTS FOR & ON BEHALF OF THE BOARD

Suparas Bhandari T.K. Roy K.N. BhandariVinay Jain CHAIRMAN DIRECTOR DIRECTORPARTNER cum MDM.NO. 95187

Place : New Delhi Avinanda Ghosh Kanika SharmaDate : 25.11.2005 DEPUTY MANAGER (ACCOUNTS) ASSTT.COMPANY SECRETARY

Particulars Schedule Current Period Previous Period01.04.04-31.03.05 20.12.02-31.03.04 (Rs.’000) (Rs.’000)

1. OPERATING PROFIT/(LOSS)Crop Insurance Business 2173218 (929417)

2. INCOME FROM INVESTMENTSa) Interest,Dividend & Rent-Gross 74927 107083b) Profit on Sale of Investments - -

3. OTHER INCOMEMiscellaneous Receipts 457 128

TOTAL (A) 2248603 (822206)

4. PROVISIONS (other than taxation)a) Dimunition in the value of Investments written off - -b) Amortisation of Premium on Investments 2052 502

5. OTHER EXPENSESa) Expenses other than those related to insurance business 277 2b) Loss on sale of Assets(Net) 7 3c) Preliminary Expenses Written off 4527 4527d) Legal expenses - 2000

TOTAL (B) 6862 7034

Profit Before Tax (C=A-B) 2241741 (829240)Provision for Taxation:Current Tax 557142 -Deferred Tax Asset (net) - -

TOTAL (D) 557142 -

Profit after Tax available for appropriation (E=C-D) 1684599 (829240)

APPROPRIATIONS

(a) Interim Dividend paid during the year - -(b) Proposed Final Dividend - -(c) Dividend Distribution Tax - -(d) Transfer to General Reserve 846150 -

TOTAL 846150 -

PROFIT AFTER TAX & APPROPRIATIONS 838448 (829240)Add:Balance of profit/(loss) brought forward from last year (829240)Less: Adj.for Interest on Corpus Fund 9208 (838448)

BALANCE CARRIED FORWARD TO BALANCE SHEET - (829240)Basic & Diluted Earning per share (EPS) 8.38 (4.08)Number of Equity Shares 200000 200000Nominal Value per share Rs.10/- Rs.10/-

Profit And Loss AccountFor The Year Ended 31st March ‘2005

Particulars Schedule Current Period Previous Period01.04.04-31.03.05 20.12.02-31.03.04

(Rs.’000) (Rs.’000)

SOURCES OF FUNDSShare Capital 5 2000000 2000000Reserve & Surplus 6 846150 -Fair Value Change Account - 7265 -Borrowings 7 206071 -

TOTAL 3059486 2000000APPLICATION OF FUNDS

Investments 8 4066613 968824Loans 9 2502 965Fixed Assets 10 48445 39612Current Assets:Cash & Bank Balances 11 6380813 8129365Advances & other Assets 12 628437 449617

SUB-TOTAL (A) 7009250 8578982

Current Liabilities 13 5086059 6633467Provisions 14 2994844 1803086

SUB-TOTAL (B) 8080904 8436553

Net Current Assets (C) =(A-B) (1071654) 142429Miscellaneous Expenditure 15 13580 18930( to the extent not written off or adjusted)DEBIT BALANCE IN PROFIT & LOSS ACCOUNT - 829240

TOTAL 3059486 2000000

Contingent LiabilitiesClaims, other than against policies, notacknowledged as debt by the Company - 1004

SIGNIFICANT ACCOUNTING POLICIES 16 - -& NOTES TO ACCOUNTS

Balance Sheet as at 31st March, 2005

AS PER OUR REPORT OF EVEN DATEFOR J.P., KAPUR & UBERAICHARTERED ACCOUNTANTS FOR & ON BEHALF OF THE BOARD

Suparas Bhandari T.K. Roy K.N. BhandariVinay Jain CHAIRMAN DIRECTOR DIRECTORPARTNER cum MDM.NO. 95187

Place : New Delhi Avinanda Ghosh Kanika SharmaDate : 25.11.2005 DEPUTY MANAGER (ACCOUNTS) ASSTT.COMPANY SECRETARY

3534

Schedule 5SHARE CAPITAL

1 Authorised capital150 crore Equity Shares ofRs.10/- each 15000000 15000000

2 Issued Capital20 crore Equity Shares ofRs.10/- each 2000000 2000000

3 Subscribed Capital20 crore Equity Shares of 2000000Rs.10/- each 2000000

4 Called-up Capital20 crore Equity Shares of 2000000Rs.10/- each 2000000TOTAL 2000000 2000000

Schedule 5APATTERN OF SHAREHOLDING(AS CERTIFIED BY THE MANAGEMENT)Shareholders Number of % of

Shares Holding

PROMOTERS - INDIAN1) General Insurance Corporation of India & its nominee 70000 35.00%2) National Bank for Agriculture & Rural Development & its nominee 60000 30.00%3) National Insurance Company Ltd. & its nominee 17500 8.75%4) Oriental Insurance Company Ltd. & its nominee 17500 8.75%5) United India Insurance Company Ltd. & its nominee 17500 8.75%6) New India Assurance Company Ltd. & its nominee 17500 8.75%

TOTAL 200000 100%

Schedule 6RESERVES & SURPLUS1. Capital Reserve - -2. Capital Redemption Reserve - -3. Share Premium4. General Reserve

Opening Balance -Add: Transfer during the year 846150 846150 -

5. Catastrophe Reserve - -6. Other Reserves - -7. Balance of Profit in Profit & Loss Account - -

TOTAL 846150 -

Schedule 7BORROWINGS

1. Debentures & Bonds - NIL2. Banks(Secured against Deposits) 206071 NIL3. Financial Institutions NIL NIL4. Others NIL NIL

TOTAL 206071 -

Particulars Current Period Previous Period01.04-04-31.03.05 20.12.02-31.03.04

(Rs.’000) (Rs.’000)

Particulars Current Period Previous Period01.04-04-31.03.05 20.12.02-31.03.04

(Rs.’000) (Rs.’000)

Schedule 1PREMIUM EARNED (NET)

Premium from Direct Business written 5497199 3692122Add:Premium on Reinsurance accepted NIL NILLess:Premium on Reinsurance ceded 5000 NILNet Premium 5492199 3692122Adjustment for change in Reserve for Unexpired Risk (938455) (1801172)TOTAL PREMIUM EARNED (NET) 4553743 1890950

Schedule 2CLAIMS INCURRED (NET)Claims paidDirect 1856702 3350662Add:Reinsurance accepted NIL NILLess:Reinsurance ceded NIL NILNet Claims paid 1856702 3350662Add : Claims Outstanding at the end of the year 3867053 2955304Less : Claims Outstanding at the beginning of the year 2955304 3480858TOTAL CLAIMS INCURRED 2768451 2825108

Schedule 3COMMISSIONCommission PaidDirect NIL NILAdd:Reinsurance accepted NIL NILLess:Commission on Reinsurance ceded 1000 NILNET COMMISSION (1000) NIL

Schedule 4OPERATING EXPENSES RELATED TO INSURANCE BUSINESS1 Employees’ remuneration & welfare benefits 39477 224852 Travel,conveyance and vehicle running expenses 4330 35773. Training Expenses 4708 1404 Rents,rates & taxes 10090 61235 Repairs 1918 7666 Printing & Stationery 1558 7767 Communication 2616 15748 Legal & Professional charges 7031 14779 Auditor’s fees,expenses etc.

a) as auditor 443 196b) as advisor or in any other capacity,in respect of

(i) Taxation matters NIL NIL(ii) Insurance matters NIL NIL(iii) Management Services, and NIL NIL

c) in any other capacity NIL NIL10 Advertisement & Publicity 6687 1099211 Interest & Bank Charges 205 145012 Others 2075 351013 Depreciation 3383 1022

TOTAL 84520 54088

Schedules Forming Part of Financial StatementsFor the Year Ended 31st March 2005

3736

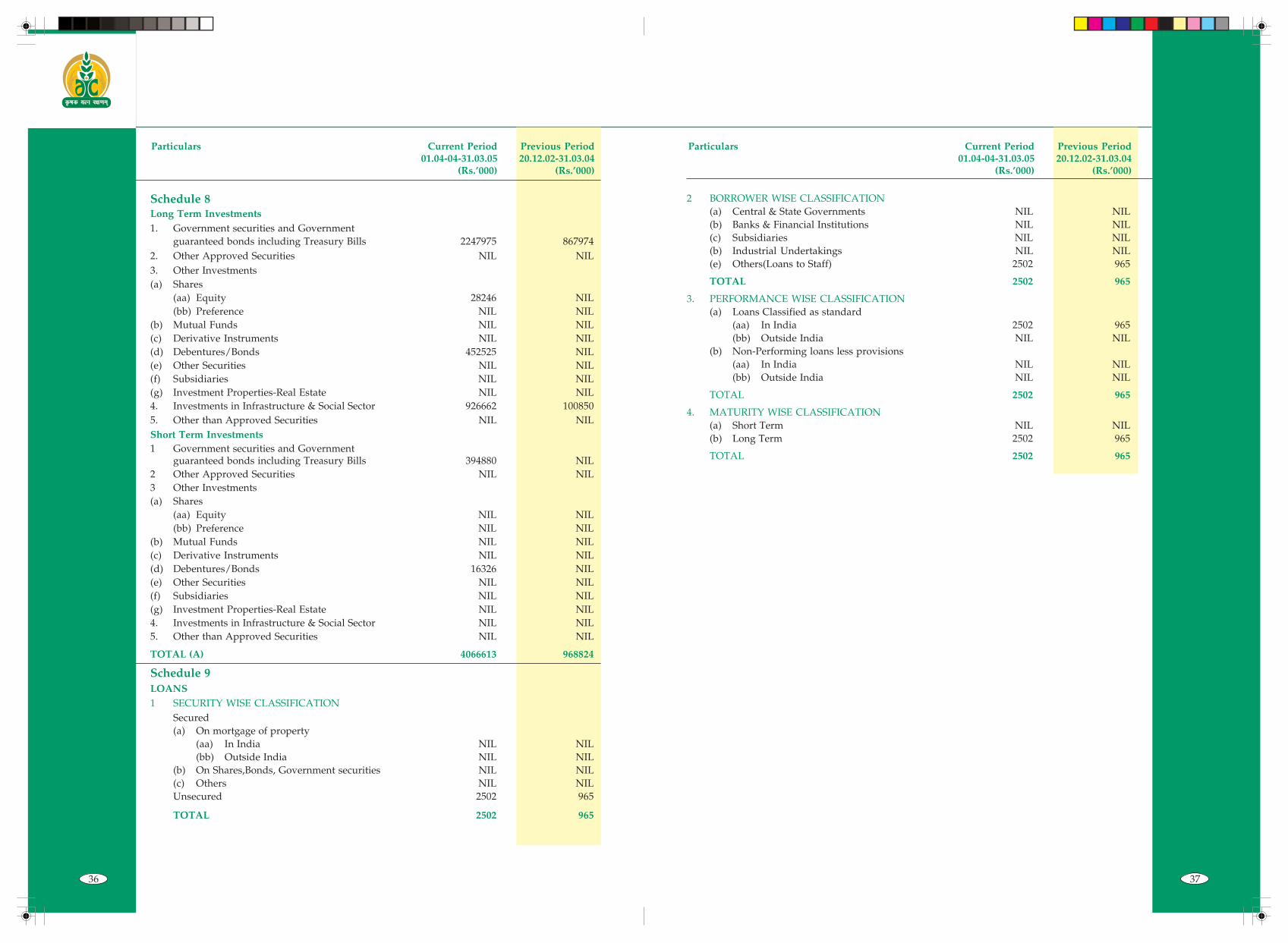

2 BORROWER WISE CLASSIFICATION(a) Central & State Governments NIL NIL(b) Banks & Financial Institutions NIL NIL(c) Subsidiaries NIL NIL(b) Industrial Undertakings NIL NIL(e) Others(Loans to Staff) 2502 965

TOTAL 2502 965

3. PERFORMANCE WISE CLASSIFICATION(a) Loans Classified as standard

(aa) In India 2502 965(bb) Outside India NIL NIL

(b) Non-Performing loans less provisions(aa) In India NIL NIL(bb) Outside India NIL NIL

TOTAL 2502 965

4. MATURITY WISE CLASSIFICATION(a) Short Term NIL NIL(b) Long Term 2502 965

TOTAL 2502 965

Schedule 8Long Term Investments1. Government securities and Government

guaranteed bonds including Treasury Bills 2247975 8679742. Other Approved Securities NIL NIL3. Other Investments(a) Shares

(aa) Equity 28246 NIL(bb) Preference NIL NIL

(b) Mutual Funds NIL NIL(c) Derivative Instruments NIL NIL(d) Debentures/Bonds 452525 NIL(e) Other Securities NIL NIL(f) Subsidiaries NIL NIL(g) Investment Properties-Real Estate NIL NIL4. Investments in Infrastructure & Social Sector 926662 1008505. Other than Approved Securities NIL NILShort Term Investments1 Government securities and Government

guaranteed bonds including Treasury Bills 394880 NIL2 Other Approved Securities NIL NIL3 Other Investments(a) Shares

(aa) Equity NIL NIL(bb) Preference NIL NIL

(b) Mutual Funds NIL NIL(c) Derivative Instruments NIL NIL(d) Debentures/Bonds 16326 NIL(e) Other Securities NIL NIL(f) Subsidiaries NIL NIL(g) Investment Properties-Real Estate NIL NIL4. Investments in Infrastructure & Social Sector NIL NIL5. Other than Approved Securities NIL NIL

TOTAL (A) 4066613 968824

Schedule 9LOANS1 SECURITY WISE CLASSIFICATION

Secured(a) On mortgage of property

(aa) In India NIL NIL(bb) Outside India NIL NIL

(b) On Shares,Bonds, Government securities NIL NIL(c) Others NIL NILUnsecured 2502 965

TOTAL 2502 965

Particulars Current Period Previous Period01.04-04-31.03.05 20.12.02-31.03.04

(Rs.’000) (Rs.’000)

Particulars Current Period Previous Period01.04-04-31.03.05 20.12.02-31.03.04

(Rs.’000) (Rs.’000)

3938

Schedule 11CASH & BANK BALANCES

1 Cash (including Cheques, drafts & Stamps) 5 52 Bank Balances

(a) Deposit Account(aa) Short term (due within 12 months) 6186513 8014015(bb) Others NIL NIL

(b) Current Accounts 193528 101227(c) Others (Remittances in Transit) 767 14118

3. Money at Call and Short Notice(a) With Banks NIL NIL(a) With Other Institutions NIL NIL

4. Others NIL NIL

TOTAL 6380813 8129365

Balances with non-scheduled banks included in 2 & 3 above NIL NIL

Schedule 12ADVANCES AND OTHER ASSETSADVANCES

1. Reserve Deposits with Ceding Companies NIL NIL2. Application Money for Investments NIL 1000003. Prepayments 3814 37674. Advances to Officers & Staff 972 7225. Advance Tax Paid & Taxes Deducted at Source 31402 314026 Others

a) Advance to NSSO 1800 1800b) Advance Rent paid NIL 1359c) Sundry Advances 4658 288

TOTAL (A) 42646 139338

OTHER ASSETS1 Income accured on investments 148733 600542. Outstanding Premiums NIL NIL3. Agents’ Balances NIL NIL4. Foreign Agencies’ Balances NIL NIL5. Due from other entities carrying on Insurance 138728 NIL

Business(including reinsurers)6. Due from subsidiaries/holding company NIL NIL7. Deposit with Reserve Bank of India

(Pursuant to Section 7 of Insurance Act, 1938) 104322 1050098. Others

- Sundry Deposits 3040 1901- Short Collection of Premium 3877 4318- Premium Receivable 186172 138956- Mediclaim Recoverable 915 NIL- Others 4 41

TOTAL (B) 585791 310279

TOTAL (A+B) 628437 449617

Particulars Current Period Previous Period01.04-04-31.03.05 20.12.02-31.03.04

(Rs.’000) (Rs.’000)S

CH

ED

UL

E 1

0

FIX

ED

AS

SE

TS

(Rs.

’000

)

Cos

t/G

ross

Blo

ckD

epre

ciat

ion

Net

Blo

ck

Ad

d:

Les

s:

Ad

dit

ion

sS

ale/

As

atA

s at

For

On

sal

e/U

p t

oA

s at

As

at

As

atd

uri

ng

Ded

uct

ion

/31

.3.2

005

1.4.

2004

the

Per

iod

adju

stm

ent

31.0

3.05

31.0

3.05

31.0

3.04

Par

ticu

lars

01.0

4.04

the

year

Dis

card

ed

Bu

ildin

gs 3

3,72

9.39

2,8

85.0

8 -

36,

614.

47 2

27.5

7 1

,312

.94

- 1

,540

.51

35,

073.

96 3

3,50

1.82

Furn

itu

re &

Fix

ture

s 9

33.0

8 1

,295

.74

- 2

,228

.82

236

.44

590

.02

- 8

26.4

6 1

,402

.36

696

.64

I.T. E

quip

men

ts 2

,054

.79

404

.69

- 2

,459

.48

680

.58

669

.15

- 1

,349

.73

1,1

09.7

5 1

,374

.21

Veh

icle

s 1

,434

.77

2,7

70.9

4 -

4,2

05.7

1 3

25.4

3 6

75.5

9 -

1,0

01.0

3 3

,204

.68

1,1

09.3

4

Off

ice

Equ

ipm

ents

585

.98

928

.02

31.0

1 1

,482

.99

110

.42

170

.57

8.0

0 2

73.0

0 1

,209

.99

475

.56

Ele

c.E

quip

.& F

itti

ngs

488

.09

729

.76

- 1

,217

.84

71.

26 2

32.5

6 -

303

.82

914

.02

416

.83

Lea

seho

ld I

mpr

ovem

ent

- 5

,794

.30

- 5

,794

.30

- 2

64.4

0 -

264

.40

5,5

29.9

0 -

Tot

al 3

9,22

6.10

14,