tollbrothers 10-q-jan_2007

TRANSCRIPT

UNITED STATES SECURITIES AND EXCHANGE COMMISSIONWashington, D.C. 20549

Form 10-Q

(Mark One)¥ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934For the quarterly period ended January 31, 2007

or

n TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)OF THE SECURITIES EXCHANGE ACT OF 1934For the transition period from to

Commission file number 1-9186

TOLL BROTHERS, INC.(Exact name of registrant as specified in its charter)

Delaware 23-2416878(State or other jurisdiction of (I.R.S. Employerincorporation or organization) Identification No.)

250 Gibraltar Road,Horsham, Pennsylvania 19044

(Address of principal executive offices) (Zip Code)

(215) 938-8000(Registrant’s telephone number, including area code)

Not applicable(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d)of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrantwas required to file such reports), and (2) has been subject to such filing requirements for the past90 days. Yes ¥ No n

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “an accelerated filer and large accelerated filer” in Rule 12b-2 of the ExchangeAct. (Check one):

Large accelerated filer ¥ Accelerated filer n Non-accelerated filer n

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the ExchangeAct) Yes n No ¥

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latestpracticable date:

At March 2, 2007, there were approximately 154,652,000 shares of Common Stock, $.01 par value,outstanding.

TOLL BROTHERS, INC. AND SUBSIDIARIES

TABLE OF CONTENTS

PageNo.

Statement on Forward-Looking Information. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

PART I. FINANCIAL INFORMATIONItem 1. Financial Statements

Condensed Consolidated Balance Sheets at January 31, 2007 (Unaudited) and October 31,2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Condensed Consolidated Statements of Income (Unaudited) For the Three Months EndedJanuary 31, 2007 and 2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Condensed Consolidated Statements of Cash Flows (Unaudited) For the Three MonthsEnded January 31, 2007 and 2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Notes to Condensed Consolidated Financial Statements (Unaudited) . . . . . . . . . . . . . . . . . . . 5

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations . . . 22

Item 3. Quantitative and Qualitative Disclosures About Market Risk . . . . . . . . . . . . . . . . . . . . . . . . . 36

Item 4. Controls and Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

PART II. OTHER INFORMATIONItem 1. Legal Proceedings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Item 1A. Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . 37

Item 3. Defaults upon Senior Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Item 4. Submission of Matters to a Vote of Security Holders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Item 5. Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Item 6. Exhibits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

SIGNATURES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

STATEMENT ON FORWARD-LOOKING INFORMATION

Certain information included herein and in our other reports, SEC filings, verbal or written statements andpresentations is forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995,including, but not limited to, information related to our anticipated operating results, financial resources, changes inrevenues, changes in profitability, changes in margins, changes in accounting treatment, interest expense, landrelated write-downs, effects of home buyer cancellations, growth and expansion, anticipated income to be realizedfrom our investments in unconsolidated entities, the ability to acquire land, the ability to gain governmentalapprovals and to open new communities, the ability to sell homes and properties, the ability to deliver homes frombacklog, the expected average delivered prices of homes, the ability to secure materials and subcontractors, theability to produce the liquidity and capital necessary to expand and take advantage of future opportunities, and stockmarket valuations. In some cases you can identify those so called forward-looking statements by words such as“may,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” “project,”“intend,” “can,” “appear,” “could,” “might,” or “continue” or the negative of those words or other comparablewords. Such forward-looking information involves important risks and uncertainties that could significantly affectactual results and cause them to differ materially from expectations expressed herein and in our other reports, SECfilings, verbal or written statements and presentations. These risks and uncertainties include local, regional andnational economic conditions, the demand for homes, domestic and international political events, uncertaintiescreated by terrorist attacks, the effects of governmental regulation, the competitive environment in which weoperate, fluctuations in interest rates, changes in home prices, the availability and cost of land for future growth,adverse market conditions that could result in substantial inventory write-downs, the availability of capital,uncertainties and fluctuations in capital and securities markets, changes in tax laws and their interpretation, legalproceedings, the availability of adequate insurance at reasonable cost, the ability of customers to finance thepurchase of homes, the availability and cost of labor and materials, and weather conditions. Additional informationconcerning potential factors that we believe could cause our actual results to differ materially from expected andhistorical results is included in Item 1A “Risk Factors” of our Annual Report on Form 10-K for the fiscal year endedOctober 31, 2006. Moreover, the financial guidance contained herein related to our expected results of operationsfor fiscal 2007 reflects our expectations as of February 22, 2007 and is not being reconfirmed or updated by thisQuarterly Report on Form 10-Q.

If one or more of the assumptions underlying our forward-looking statements proves incorrect, then our actualresults, performance or achievements could differ materially from those expressed in, or implied by the forward-looking statements contained in this report. Therefore, we caution you not to place undue reliance on our forward-looking statements. This statement is provided as permitted by the Private Securities Litigation Reform Act of 1995.

When this report uses the words “we,” “us,” and “our,” they refer to Toll Brothers, Inc. and its subsidiaries,unless the context otherwise requires. Reference herein to “fiscal 2007,” “fiscal 2006,” and “fiscal 2005,” refer toour fiscal year ending October 31, 2007, and our fiscal years ended October 31, 2006 and October 31, 2005,respectively.

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

TOLL BROTHERS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

January 31,2007

October 31,2006

(Unaudited)(Amounts in thousands)

ASSETSCash and cash equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 449,249 $ 632,524

Inventory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,182,279 6,095,702

Property, construction and office equipment, net . . . . . . . . . . . . . . . . . . . . . . . . . . 94,299 99,089

Receivables, prepaid expenses and other assets . . . . . . . . . . . . . . . . . . . . . . . . . . . 144,019 160,446

Contracts receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 166,887 170,111

Mortgage loans receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78,345 130,326

Customer deposits held in escrow . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51,008 49,676Investments in and advances to unconsolidated entities . . . . . . . . . . . . . . . . . . . . . 251,035 245,667

$7,417,121 $7,583,541

LIABILITIES AND STOCKHOLDERS’ EQUITYLiabilities:

Loans payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 710,870 $ 736,934

Senior notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,141,452 1,141,167

Senior subordinated notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 350,000 350,000

Mortgage company warehouse loan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65,887 119,705

Customer deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 344,674 360,147

Accounts payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 253,353 292,171

Accrued expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 759,186 825,288

Income taxes payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 286,128 334,500

Total liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,911,550 4,159,912

Minority interest. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,763 7,703

Stockholders’ equity:

Preferred stock, none issued

Common stock, 156,292 shares issued at January 31, 2007 and October 31,2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,563 1,563

Additional paid-in capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 225,359 220,783

Retained earnings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,317,590 3,263,274

Treasury stock, at cost — 1,645 and 2,393 shares at January 31, 2007 andOctober 31, 2006, respectively . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (46,704) (69,694)

Total stockholders’ equity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,497,808 3,415,926

$7,417,121 $7,583,541

See accompanying notes

2

TOLL BROTHERS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME

2007 2006

Three Months EndedJanuary 31,

(Amounts in thousands,except per share data)

(Unaudited)

Revenues:

Traditional home sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,054,136 $1,278,709

Percentage of completion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33,085 57,569

Land sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,390 4,678

1,090,611 1,340,956

Cost of revenues:

Traditional home sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 846,403 884,091

Percentage of completion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25,897 47,346

Land sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,037 3,836

Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22,643 28,754

895,980 964,027

Selling, general and administrative . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134,210 139,178

Goodwill impairment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8,973

Income from operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51,448 237,751

Other:

Equity earnings from unconsolidated entities . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,792 16,569

Interest and other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28,960 11,327

Income before income taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87,200 265,647

Income taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32,884 101,797

Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 54,316 $ 163,850

Earnings per share:

Basic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 0.35 $ 1.06

Diluted . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 0.33 $ 0.98

Weighted average number of shares:

Basic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154,212 155,076Diluted . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164,048 167,027

See accompanying notes

3

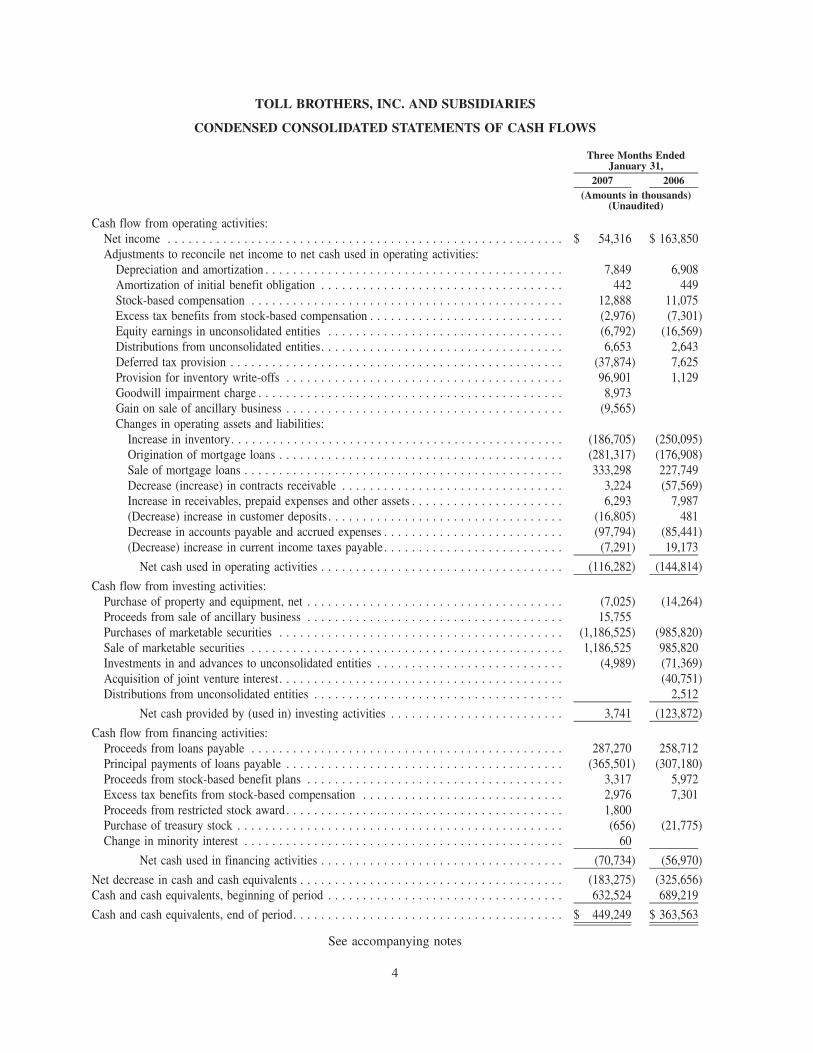

TOLL BROTHERS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

2007 2006

Three Months EndedJanuary 31,

(Amounts in thousands)(Unaudited)

Cash flow from operating activities:Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 54,316 $ 163,850Adjustments to reconcile net income to net cash used in operating activities:

Depreciation and amortization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,849 6,908Amortization of initial benefit obligation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 442 449Stock-based compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12,888 11,075Excess tax benefits from stock-based compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . (2,976) (7,301)Equity earnings in unconsolidated entities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (6,792) (16,569)Distributions from unconsolidated entities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,653 2,643Deferred tax provision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (37,874) 7,625Provision for inventory write-offs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96,901 1,129Goodwill impairment charge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8,973Gain on sale of ancillary business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (9,565)Changes in operating assets and liabilities:

Increase in inventory. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (186,705) (250,095)Origination of mortgage loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (281,317) (176,908)Sale of mortgage loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 333,298 227,749Decrease (increase) in contracts receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,224 (57,569)Increase in receivables, prepaid expenses and other assets . . . . . . . . . . . . . . . . . . . . . . 6,293 7,987(Decrease) increase in customer deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (16,805) 481Decrease in accounts payable and accrued expenses . . . . . . . . . . . . . . . . . . . . . . . . . . (97,794) (85,441)(Decrease) increase in current income taxes payable . . . . . . . . . . . . . . . . . . . . . . . . . . (7,291) 19,173

Net cash used in operating activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (116,282) (144,814)

Cash flow from investing activities:Purchase of property and equipment, net . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (7,025) (14,264)Proceeds from sale of ancillary business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15,755Purchases of marketable securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (1,186,525) (985,820)Sale of marketable securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,186,525 985,820Investments in and advances to unconsolidated entities . . . . . . . . . . . . . . . . . . . . . . . . . . . (4,989) (71,369)Acquisition of joint venture interest. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (40,751)Distributions from unconsolidated entities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,512

Net cash provided by (used in) investing activities . . . . . . . . . . . . . . . . . . . . . . . . . 3,741 (123,872)

Cash flow from financing activities:Proceeds from loans payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 287,270 258,712Principal payments of loans payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (365,501) (307,180)Proceeds from stock-based benefit plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,317 5,972Excess tax benefits from stock-based compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,976 7,301Proceeds from restricted stock award . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,800Purchase of treasury stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (656) (21,775)Change in minority interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

Net cash used in financing activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (70,734) (56,970)

Net decrease in cash and cash equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (183,275) (325,656)Cash and cash equivalents, beginning of period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 632,524 689,219

Cash and cash equivalents, end of period. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 449,249 $ 363,563

See accompanying notes

4

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS(Unaudited)

1. Significant Accounting Policies

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements include the accounts of TollBrothers, Inc. (the “Company”), a Delaware corporation, and its majority-owned subsidiaries. All significantintercompany accounts and transactions have been eliminated. Investments in 50% or less owned partnerships andaffiliates are accounted for using the equity method unless it is determined that the Company has effective control ofthe entity, in which case the entity would be consolidated.

The accompanying unaudited condensed consolidated financial statements have been prepared in accordancewith the rules and regulations of the Securities and Exchange Commission (“SEC”) for interim financialinformation. The October 31, 2006 balance sheet amounts and disclosures included herein have been derivedfrom our October 31, 2006 audited financial statements. Since the accompanying condensed consolidated financialstatements do not include all the information and footnotes required by U.S. generally accepted accountingprinciples for complete financial statements, the Company suggests that they be read in conjunction with theconsolidated financial statements and notes thereto included in its Annual Report on Form 10-K for the fiscal yearended October 31, 2006. In the opinion of management, the accompanying unaudited condensed consolidatedfinancial statements include all adjustments, which are of a normal recurring nature, necessary to present fairly theCompany’s financial position as of January 31, 2007, and the results of its operations and cash flows for the threemonths ended January 31, 2007 and 2006. The results of operations for such interim periods are not necessarilyindicative of the results to be expected for the full year.

Recent Accounting Pronouncements

In June 2006, the Financial Accounting Standards Board (the “FASB”) issued FASB Interpretation No. 48,“Accounting for Uncertainty in Income Taxes” (“FIN 48”). FIN 48 clarifies the accounting for uncertainty inincome taxes recognized in accordance with Statement of Financial Accounting Standards (“SFAS”) No. 109,“Accounting for Income Taxes”, and prescribes a recognition threshold and measurement attribute for the financialstatement recognition and measurement of a tax position taken or expected to be taken in a tax return. FIN 48 will beeffective for the Company’s fiscal year beginning November 1, 2007. The Company is currently reviewing theeffect FIN 48 will have on its financial statements.

In September 2006, the FASB issued SFAS No. 158, “Employers’ Accounting for Defined Benefit Pension andOther Postretirement Plans, an amendment of FASB Statements No. 87, 88, 106, and 132(R)” (“SFAS 158”).SFAS 158 requires the Company to (a) recognize in its statement of financial position the overfunded orunderfunded status of a defined benefit postretirement plan measured as the difference between the fair valueof plan assets and the benefit obligation, (b) recognize as a component of other comprehensive income, net of tax,the actuarial gains and losses and the prior service costs and credits that arise during the period, (c) measure definedbenefit plan assets and defined benefit plan obligations as of the date of the Company’s statement of financialposition, and (d) disclose additional information about certain effects on net periodic benefit costs in the upcomingfiscal year that arise from the delayed recognition of the actuarial gains and losses and the prior service costs andcredits. SFAS 158 is effective for the Company’s fiscal year beginning November 1, 2007. The Company does notexpect that adoption of SFAS 158 will have a material effect on its financial statements.

In September 2006, the Emerging Issues Task Force (the “EITF”) of the FASB issued EITF Issue No. 06-8,“Applicability of the Assessment of a Buyer’s Continuing Investment under SFAS No. 66 for the Sale ofCondominiums” (“EITF 06-8”). EITF 06-8 states that in assessing the collectibility of the sales price pursuantto paragraph 37(d) of SFAS 66, an entity should evaluate the adequacy of the buyer’s initial and continuinginvestment to conclude that the sales price is collectible. If an entity is unable to meet the criteria of paragraph 37,including an assessment of collectibility using the initial and continuing investment tests described in

5

paragraphs 8-12 of SFAS 66, then the entity should apply the deposit method as described in paragraphs 65-67 ofSFAS 66. EITF 06-8 is effective for the Company’s fiscal year beginning November 1, 2007. In November 2006, theFASB ratified the EITF’s recommendation. The application of the continuing investment criteria in evaluating thecollectibility of the sales price will limit the Company’s ability to recognize revenues and costs using the percentageof completion accounting method in the future. The Company does not expect that EITF 06-08 will affect anyrevenues or costs it has reported under percentage of completion accounting in fiscal 2006. The Company does notexpect that the application of EITF 06-08 will have a material effect on its financial statements.

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements” (“SFAS 157”). SFAS 157provides guidance for using fair value to measure assets and liabilities. The standard also responds to investors’request for expanded information about the extent to which a company measures assets and liabilities at fair value,the information used to measure fair value, and the effect of fair value measurements on earnings. SFAS 157 will beeffective for the Company’s fiscal year beginning November 1, 2008. The Company is currently reviewing theeffect SFAS 157 will have on its financial statements.

Reclassification

The presentation of certain prior year amounts have been reclassified to conform to the fiscal 2007presentation.

2. Inventory

Inventory consisted of the following (amounts in thousands):

January 31,2007

October 31,2006

Land and land development costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $2,122,103 $2,193,850

Construction in progress — completed contract . . . . . . . . . . . . . . . . . . . . 3,363,726 3,174,483

Construction in progress — percentage of completion . . . . . . . . . . . . . . . 115,365 153,452

Sample homes and sales offices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 269,258 244,097

Land deposits and costs of future development . . . . . . . . . . . . . . . . . . . . 295,978 315,041

Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15,849 14,779

$6,182,279 $6,095,702

Construction in progress includes the cost of homes under construction, land and land development costs andthe carrying costs of lots that have been substantially improved.

The Company capitalizes certain interest costs to inventory during the development and construction period.Capitalized interest is charged to cost of revenues when the related inventory is delivered for traditional home salesor when the related inventory is charged to cost of revenues under percentage of completion accounting. Interestincurred, capitalized and expensed for the three-month periods ended January 31, 2007 and 2006 is summarized asfollows (amounts in thousands):

2007 2006

Interest capitalized, beginning of period . . . . . . . . . . . . . . . . . . . . . . . . . . . . $181,465 $162,672

Interest incurred . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34,151 32,436

Capitalized interest in inventory acquired . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,679

Interest expensed to cost of revenues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (22,643) (28,754)

Write-off to other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (40) (171)

Interest capitalized, end of period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $192,933 $172,862

6

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Interest included in cost of revenues for the three-month periods ended January 31, 2007 and 2006 was asfollows (amounts in thousands):

2007 2006

Traditional home sales revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $21,737 $26,830

Percentage of completion revenues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 905 1,417

Land sales revenues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 507

$22,643 $28,754

Inventory write-downs and the expensing of costs that the Company believed not to be recoverable for thethree-month periods ended January 31, 2007 and 2006 were as follows (amounts in thousands):

2007 2006

Land controlled for future communities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $13,939 $1,130

Operating communities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82,962

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $96,901 $1,130

The Company has evaluated its land purchase contracts to determine if the selling entity is a variable interestentity (“VIE”) and, if it is, whether the Company is the primary beneficiary of the entity. The Company does notpossess legal title to the land, and its risk is generally limited to deposits paid to the seller. The creditors of the sellergenerally have no recourse against the Company. At January 31, 2007, the Company had determined that it was theprimary beneficiary of one VIE related to its land purchase contracts and had recorded $76.1 million as inventory,$68.6 million as a loan payable and $5.5 million as accrued liabilities.

3. Investments in and Advances to Unconsolidated Entities

The Company has investments in and advances to several joint ventures with unrelated parties to develop land.Some of these joint ventures develop land for the sole use of the venture partners, including the Company, and othersdevelop land for sale to the venture partners and to unrelated builders. The Company recognizes its share of earningsfrom the sale of home sites to other builders. The Company does not recognize earnings from home sites itpurchases from the joint ventures, but instead reduces its cost basis in these home sites by its share of the earnings onthe home sites. At January 31, 2007, the Company had approximately $163.3 million invested in or advanced tothese joint ventures and was committed to contributing additional capital in an aggregate amount of approximately$228.2 million (net of the Company’s $141.0 million of loan guarantees related to two of the joint ventures’ loans) ifrequired by the joint ventures. At January 31, 2007, three of the joint ventures had an aggregate of $1.41 billion ofloan commitments, and had approximately $1.15 billion borrowed against the commitments, of which theCompany’s guarantee of its pro-rata share of the borrowings was $112.7 million.

In October 2004, the Company entered into a joint venture in which it has a 50% interest with an unrelatedparty to convert a 525-unit apartment complex, The Hudson Tea Buildings, located in Hoboken, New Jersey, intoluxury condominium units. At January 31, 2007, the Company had investments in and advances to the joint ventureof $52.8 million, and was committed to making up to $1.5 million of additional investments in and advances to thejoint venture.

The Company has investments in and advances to two joint ventures with unrelated parties to develop luxurycondominium projects, including for-sale residential units and commercial space. At January 31, 2007, theCompany had investments in and advances to the joint ventures of $19.4 million, was committed to making up to$115.5 million of additional investments in and advances to the joint ventures if required by the joint ventures, andguaranteed $13.0 million of joint venture loans. At January 31, 2007, these joint ventures had an aggregate of$292.6 million of loan commitments and had approximately $119.8 million borrowed against the commitments.

7

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

In fiscal 2005, the Company, together with the Pennsylvania State Employees Retirement System (“PASERS”),formed Toll Brothers Realty Trust Group II (“Trust II”) to be in a position to take advantage of commercial real estateopportunities. Trust II is owned 50% by the Company and 50% by PASERS. At January 31, 2007, the Company had aninvestment of $8.9 million in Trust II. In addition, the Company and PASERS each entered into subscriptionagreements that expire in September 2007, whereby each agreed to invest additional capital in an amount not to exceed$11.1 million if required by Trust II. Prior to the formation of Trust II, the Company used Toll Brothers RealtyTrust Group (the “Trust”) to invest in commercial real estate opportunities.

To take advantage of commercial real estate opportunities, the Company formed the Trust in 1998. The Trust iseffectively owned one-third by the Company; one-third by Robert I. Toll, Bruce E. Toll (and members of his family),Zvi Barzilay (and members of his family), Joel H. Rassman and other members of the Company’s current andformer senior management; and one-third by PASERS (collectively, the “Shareholders”). The Shareholders enteredinto subscription agreements whereby each group has agreed to invest additional capital in an amount not to exceed$1.9 million if required by the Trust. The subscription agreements expire in August 2008. At January 31, 2007, theCompany had an investment of $6.6 million in the Trust. The Company provides development, finance andmanagement services to the Trust and received fees under the terms of various agreements in the amounts of$498,000 and $647,000 in the three-month periods ended January 31, 2007 and 2006, respectively. The Companybelieves that the transactions between itself and the Trust were on terms no less favorable than it would have agreedto with unrelated parties.

The Company’s investments in these entities are accounted for using the equity method.

4. Goodwill Impairment

During the three-month period ended January 31, 2007, due to the continued decline of the Detroit market, theCompany re-evaluated the carrying value of goodwill that resulted from a 1999 acquisition in accordance withFASB 142, “Goodwill and Other Intangible Assets”. The Company estimated the fair value of its assets in thismarket including goodwill. Fair value was determined based on the discounted future cash flow expected to begenerated in this market. Based upon this evaluation and the Company’s expectation that this market will notrecover for a number of years, the Company has determined that the related goodwill has been impaired. TheCompany recognized a $9.0 million impairment charge in the three-month period ended January 31, 2007. Afterrecognizing this charge, the Company does not have any goodwill remaining from this acquisition.

5. Accrued Expenses

Accrued expenses at January 31, 2007 and October 31, 2006 consisted of the following (amounts inthousands):

January 31,2007

October 31,2006

Land, land development and construction costs . . . . . . . . . . . . . . . . . . . . . $320,834 $376,114

Compensation and employee benefit costs . . . . . . . . . . . . . . . . . . . . . . . . . 110,671 127,433

Insurance and litigation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129,912 130,244

Warranty costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57,835 57,414Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43,737 43,629

Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96,197 90,454

$759,186 $825,288

The Company accrues for the expected warranty costs at the time each home is closed and title and possessionhave been transferred to the home buyer. Costs are accrued based upon historical experience. Changes in the

8

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

warranty accrual for the three-month periods ended January 31, 2007 and 2006 were as follows (amounts inthousands):

2007 2006

Balance, beginning of period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $57,414 $54,722

Additions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,534 8,531

Charges incurred . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (7,113) (8,604)

Balance, end of period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $57,835 $54,649

6. Employee Retirement Plan

In October 2004, the Company established a defined benefit retirement plan effective as of September 1, 2004,which covers four current or former senior executives and a director of the Company. Effective as of February 1,2006, the Company adopted an additional defined benefit retirement plan for nine other executives. The retirementplans are unfunded and vest when the participant has completed 20 years of service with the Company and reachesnormal retirement age (age 62). Unrecognized prior service costs are being amortized over the period from theeffective date of the plans until the participants are fully vested. The Company used a 5.68% and 5.65% discountrate in its calculation of the present value of its projected benefit obligations for fiscal 2007 and 2006, respectively,which represented the approximate long-term investment rate at October 31 of the preceding fiscal year for whichthe present value was calculated.

For the three-month periods ended January 31, 2007 and 2006, the Company recognized the following costsrelated to these plans (amounts in thousands):

2007 2006

Service cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 83 $ 67

Interest cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 253 205

Amortization of initial benefit obligation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 442 449

Total cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $778 $721

Benefits paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 91 —

7. Stock Based Benefit Plans

The fair value of each option award is estimated on the date of grant using a lattice-based option valuationmodel that uses assumptions noted in the following table. The lattice-based option valuation models incorporateranges of assumptions for inputs; those ranges are disclosed in the table below. Expected volatilities are based onimplied volatilities from traded options on the Company’s stock, historical volatility of the Company’s stock andother factors. The expected life of options granted is derived from the historical exercise patterns and anticipatedfuture patterns and represents the period of time that options granted are expected to be outstanding; the range givenbelow results from certain groups of employees exhibiting different behavior. The risk-free rate for periods withinthe contractual life of the option is based on the U.S. Treasury yield curve in effect at the time of grant.

9

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

The weighted-average assumptions and the fair value used for stock option grants for the three-month periodsended January 31, 2007 and 2006 are as follows:

2007 2006

Expected volatility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36.32% - 38.22% 36.33% - 38.28%

Weighted-average volatility . . . . . . . . . . . . . . . . . . . . . . . . . 37.16% 37.55%

Risk-free interest rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.57% - 4.61% 4.38% - 4.51%

Expected life (years) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.69 - 8.12 4.11 - 9.07

Dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . none noneWeighted-average grant date fair value per share of options

granted . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $11.17 $15.30

In the three-month period ended January 31, 2007, the Company recognized $12.8 million of stock com-pensation expense and $4.8 million of income tax benefit related to stock options awards. In the three-month periodended January 31, 2006, the Company recognized $11.0 million of stock compensation expense and $4.0 million ofincome tax benefit related to stock options awards.

The Company expects to recognize approximately $26.7 million of expense and $9.8 million of income taxbenefit for the full fiscal 2007 year related to stock option awards. The Company recognized approximately$26.8 million of expense and $9.1 million of income tax benefit for the full fiscal 2006 year related to stock optionawards.

The Company’s stock option plans for employees, officers and directors provide for the granting of incentivestock options and non-qualified options with a term of up to ten years at a price not less than the market price of thestock at the date of grant. Options granted generally vest over a four-year period for employees, although for certaingrants vesting is over five years, and grants to non-employee directors which vest over a two-year period. Sharesissued upon the exercise of a stock option are either from shares held in treasury or newly issued shares.

Pursuant to the provisions of the Company’s stock option plans, participants are permitted to use the value of theCompany’s common stock that they own to pay for the exercise of options. The Company received 4,172 shares withan average fair market value per share of $35.43 for the exercise of stock options in the three months ended January 31,2006. No shares were received for the exercise of stock options in the three months ended January 31, 2007.

Stock option activity for the three months ended January 31, 2007 and 2006 was as follows:

Shares(in 000’s)

Weighted-Average

Exercise Price(per share)

Shares(in 000’s)

Weighted-Average

Exercise Price(per share)

2007 2006

Outstanding, beginning of period . . . . . . . . . . . 25,178 $12.70 26,155 $11.04Granted . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,803 $31.82 1,433 $35.97

Exercised . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (460) $ 6.67 (894) $ 6.59

Cancelled . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (39) $31.27 (11) $22.10

Outstanding, end of period . . . . . . . . . . . . . . . . 26,482 $14.08 26,683 $12.52

At January 31, 2007, the exercise price of approximately 5.7 million options was higher than the averageclosing price of the Company’s common stock on the New York Stock Exchange (the “NYSE”) for the three-monthperiod ended January 31, 2007.

The Company realized a tax benefit from the exercise of non-qualified stock options and the exercise anddisqualifying disposition of incentive stock options of approximately $3.5 million and $8.4 million in the threemonths ended January 31, 2007 and 2006, respectively.

10

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

The intrinsic value of options outstanding and exercisable is the difference between the fair market value of theCompany’s common stock on the applicable date (“Measurement Value”) and the exercise price of those optionsthat had an exercise price that was less than the Measurement Value. The intrinsic value of options exercised is thedifference between the fair market value of the Company’s common stock on the date of exercise and the exerciseprice.

The intrinsic value of options outstanding and exercisable at January 31, 2007 and 2006 were as follows(amounts in thousands):

2007 2006

Intrinsic value of options

Outstanding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $526,002 $575,948Exercisable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $513,633 $568,008

The intrinsic value of options exercised and the fair value of options which became vested in the three-monthperiods ended January 31, 2007 and 2006 were as follows (amounts in thousands):

2007 2006

Intrinsic value of options exercised . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $11,234 $26,869Fair value of options vested. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $21,642 $23,551

Stock options outstanding and exercisable at January 31, 2007 were as follows:

Range of Exercise Prices ($)

NumberOutstanding

(in 000’s)

Weighted-Average

RemainingContractual

Life(in years)

Weighted-AverageExercise

Price($)

NumberExercisable(in 000’s)

Weighted-Average

RemainingContractual

Life(in years)

Weighted-AverageExercise

Price($)

Options Outstanding Options Exercisable

4.38 - 6.86 . . . . . . . . . . . . . . . 10,052 2.1 5.34 10,052 2.1 5.346.87 - 9.66 . . . . . . . . . . . . . . . 3,251 3.1 9.03 3,251 3.1 9.03

9.67 - 10.88 . . . . . . . . . . . . . . . 5,235 5.3 10.75 5,235 5.3 10.75

10.89 - 20.14 . . . . . . . . . . . . . . . 2,286 6.9 20.14 1,751 6.9 20.14

20.15 - 35.97 . . . . . . . . . . . . . . . 5,659 8.8 33.14 1,754 8.1 33.27

26,483 4.7 14.08 22,043 3.9 10.56

7. Earnings per Share Information

Information pertaining to the calculation of earnings per share for the three-month periods ended January 31,2007 and 2006 are as follows (amounts in thousands):

2007 2006

Basic weighted-average shares. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154,212 155,076

Common stock equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,836 11,951

Diluted weighted-average shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164,048 167,027

9. Stock Repurchase Program

In March 2003, the Company’s Board of Directors authorized the repurchase of up to 20 million shares of itsCommon Stock, par value $.01, from time to time, in open market transactions or otherwise, for the purpose of

11

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

providing shares for its various employee benefit plans. At January 31, 2007, the Company was authorized torepurchase approximately 12.1 million shares.

10. Commitments and Contingencies

At January 31, 2007, the aggregate purchase price of land parcels under option and purchase agreements,excluding parcels that the Company does not expect to acquire, was approximately $2.68 billion (including$1.22 billion of land to be acquired from joint ventures which the Company has investments in, made advances to ormade loan guarantees on behalf of, in the amount of $162.7 million), of which it had paid or depositedapproximately $161.3 million. The Company’s option agreements to acquire the home sites do not require theCompany to buy the home sites, although the Company may, in some cases, forfeit any deposit balance outstandingif and when it terminates an option contract. Of the $161.3 million the Company had paid or deposited on thesepurchase agreements, $124.0 million was non-refundable at January 31, 2007. Any deposit in the form of a standbyletter of credit is recorded as a liability at the time the standby letter of credit is issued. Included in accrued liabilitiesis $76.8 million representing the Company’s outstanding standby letters of credit issued in connection with optionsto purchase home sites.

At January 31, 2007, the Company had outstanding surety bonds amounting to approximately $742.5 million,related primarily to its obligations to various governmental entities to construct improvements in the Company’svarious communities. The Company estimates that approximately $271.2 million of work remains on theseimprovements. The Company has an additional $132.9 million of surety bonds outstanding that guarantee otherobligations of the Company. The Company does not believe it is likely that any outstanding bonds will be drawnupon.

At January 31, 2007, the Company had agreements of sale outstanding to deliver 5,949 homes with anaggregate sales value of approximately $4.15 billion, of which the Company has recognized $166.9 million ofrevenues using the percentage of completion accounting method.

At January 31, 2007, the Company was committed to providing approximately $942.4 million of mortgageloans to its home buyers and to others. All loans with committed interest rates are covered by take-out commitmentsfrom third-party lenders, which minimize the Company’s interest rate risk.

The Company has a $1.8 billion credit facility consisting of a $1.5 billion unsecured revolving credit facilityand a $300 million term loan facility (collectively, the “Credit Facility”) with 33 banks, which extends to March 17,2011. At January 31, 2007, interest was payable on borrowings under the revolving credit facility at 0.475% (subjectto adjustment based upon the Company’s debt rating and leverage ratios) above the Eurodollar rate or at otherspecified variable rates as selected by the Company from time to time. At January 31, 2007, the Company had nooutstanding borrowings against the revolving credit facility but had letters of credit of approximately $398.5 millionoutstanding under it, of which the Company had recorded $76.8 million as liabilities under land purchaseagreements. Under the term loan facility, interest is payable at 0.50% (subject to adjustment based upon theCompany’s debt rating and leverage ratios) above the Eurodollar rate or at other specified variable rates as selectedby the Company from time to time. At January 31, 2007, interest was payable on the $300 million term loan at5.87%. Under the terms of the Credit Facility, the Company is not permitted to allow its maximum leverage ratio (asdefined in the agreement) to exceed 2.00 to 1.00 and was required to maintain a minimum tangible net worth (asdefined in the agreement) of approximately $2.36 billion at January 31, 2007. At January 31, 2007, the Company’sleverage ratio was approximately 0.56 to 1.00 and its tangible net worth was approximately $3.47 billion. Basedupon the minimum tangible net worth requirement, the Company’s ability to pay dividends and repurchase itscommon stock was limited to an aggregate amount of approximately $1.11 billion at January 31, 2007.

The Company is involved in various claims and litigation arising in the ordinary course of business. TheCompany believes that the disposition of these matters will not have a material effect on the business or on thefinancial condition of the Company.

12

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

In January 2006, the Company received a request for information pursuant to Section 308 of the Clean WaterAct from Region 3 of the Environmental Protection Agency (the “EPA”) requesting information about storm waterdischarge practices in connection with our homebuilding projects in the states that comprise EPA Region 3. To theextent the EPA’s review were to lead the EPA to assert violations of state and/or federal regulatory requirements andrequest injunctive relief and/or civil penalties, the Company would defend and attempt to resolve any such assertedviolations. At this time the Company cannot predict the outcome of the EPA’s review.

11. Business Segments

During the fourth quarter of fiscal 2006, the Company reassessed the aggregation of its operating segments,and as a result, restated its disclosure to include four separate reportable segments. The restatement had no impacton the Company’s financial position, results of operations or cash flows for the three-month period endedJanuary 31, 2006.

Revenue and income before income taxes for each of the Company’s geographic segments for the three monthsended January 31, 2007 and 2006 were as follows (amounts in thousands):

2007 2006

Revenues:

North . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 211,147 $ 311,328

Mid-Atlantic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 331,322 393,954

South . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 247,766 275,830

West . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 300,376 359,844

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,090,611 $1,340,956

Income before income taxes:

North . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 755 $ 71,861

Mid-Atlantic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51,604 118,059

South . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,019 34,462

West . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56,866 84,340

Corporate and other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (26,044) (43,075)

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 87,200 $ 265,647

Corporate and other is comprised principally of general corporate expenses such as the Offices of the ChiefExecutive Officer and President, and the corporate finance, accounting, audit, tax, human resources, risk man-agement, marketing and legal groups, offset in part by interest income and income from our ancillary businesses.

13

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Inventory write-downs and the expensing of costs that it believed not to be recoverable for the three monthsended January 31, 2007 and 2006 were as follows (amounts in thousands):

2007 2006

Land controlled for future communities:

North . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 933 $ 595

Mid-Atlantic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,352

South . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,937 429

West . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,717 106

13,939 1,130

Operating communities:

North . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32,200

Mid-Atlantic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21,500

South . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28,100

West . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,162

82,962 —

$96,901 $1,130

Total assets for each of the Company’s geographic segments at January 31, 2007 and October 31, 2006(amounts in thousands) were as follows:

January 31,2007

October 31,2006

North . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,814,921 $1,776,723

Mid-Atlantic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,699,190 1,729,057

South . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,358,339 1,338,344

West . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,864,115 1,843,395

Corporate and other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 680,556 896,022

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $7,417,121 $7,583,541

Corporate and other is comprised principally of cash and cash equivalents and the assets of the Company’smanufacturing facilities and mortgage subsidiary.

14

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

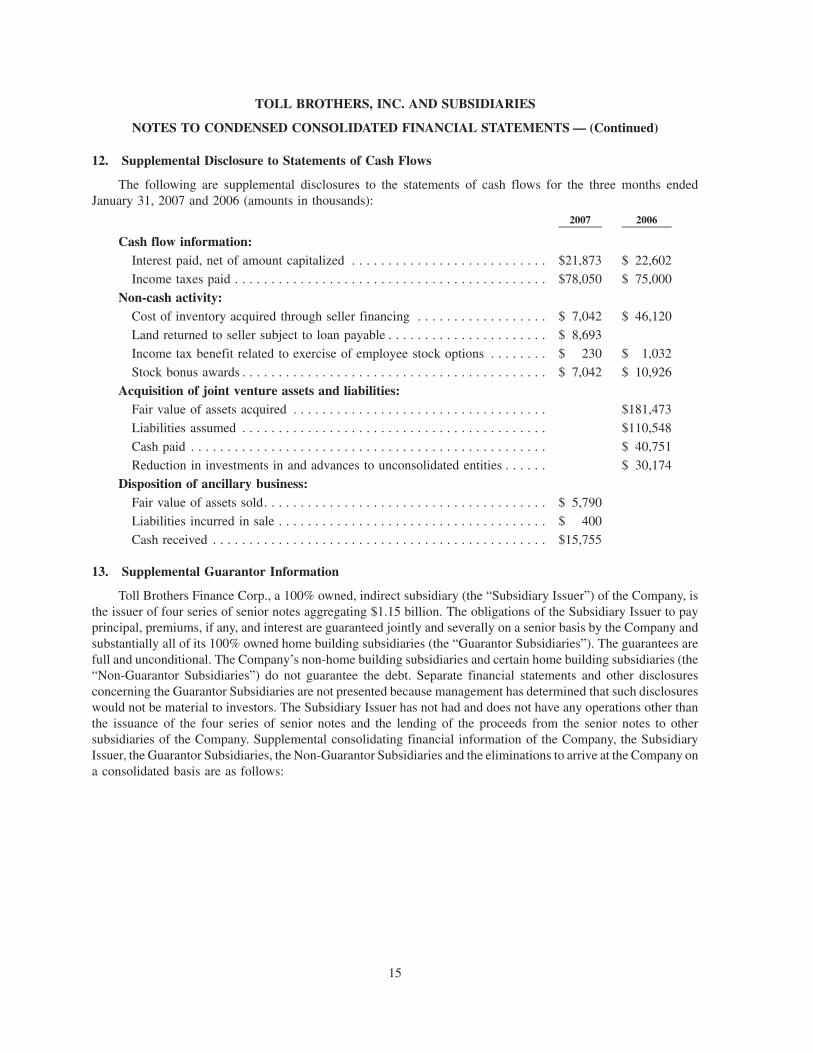

12. Supplemental Disclosure to Statements of Cash Flows

The following are supplemental disclosures to the statements of cash flows for the three months endedJanuary 31, 2007 and 2006 (amounts in thousands):

2007 2006

Cash flow information:Interest paid, net of amount capitalized . . . . . . . . . . . . . . . . . . . . . . . . . . . $21,873 $ 22,602

Income taxes paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $78,050 $ 75,000

Non-cash activity:Cost of inventory acquired through seller financing . . . . . . . . . . . . . . . . . . $ 7,042 $ 46,120

Land returned to seller subject to loan payable . . . . . . . . . . . . . . . . . . . . . . $ 8,693

Income tax benefit related to exercise of employee stock options . . . . . . . . $ 230 $ 1,032

Stock bonus awards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 7,042 $ 10,926

Acquisition of joint venture assets and liabilities:Fair value of assets acquired . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $181,473

Liabilities assumed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $110,548

Cash paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 40,751

Reduction in investments in and advances to unconsolidated entities . . . . . . $ 30,174

Disposition of ancillary business:Fair value of assets sold. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 5,790

Liabilities incurred in sale . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 400

Cash received . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $15,755

13. Supplemental Guarantor Information

Toll Brothers Finance Corp., a 100% owned, indirect subsidiary (the “Subsidiary Issuer”) of the Company, isthe issuer of four series of senior notes aggregating $1.15 billion. The obligations of the Subsidiary Issuer to payprincipal, premiums, if any, and interest are guaranteed jointly and severally on a senior basis by the Company andsubstantially all of its 100% owned home building subsidiaries (the “Guarantor Subsidiaries”). The guarantees arefull and unconditional. The Company’s non-home building subsidiaries and certain home building subsidiaries (the“Non-Guarantor Subsidiaries”) do not guarantee the debt. Separate financial statements and other disclosuresconcerning the Guarantor Subsidiaries are not presented because management has determined that such disclosureswould not be material to investors. The Subsidiary Issuer has not had and does not have any operations other thanthe issuance of the four series of senior notes and the lending of the proceeds from the senior notes to othersubsidiaries of the Company. Supplemental consolidating financial information of the Company, the SubsidiaryIssuer, the Guarantor Subsidiaries, the Non-Guarantor Subsidiaries and the eliminations to arrive at the Company ona consolidated basis are as follows:

15

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Condensed Consolidating Balance Sheet at January 31, 2007 ($ in thousands):Toll

Brothers,Inc.

SubsidiaryIssuer

GuarantorSubsidiaries

Non-Guarantor

Subsidiaries Eliminations Consolidated

ASSETSCash and cash equivalents . . . . . . . . . 380,615 68,634 449,249

Inventory . . . . . . . . . . . . . . . . . . . . . 5,797,982 384,297 6,182,279

Property, construction and officeequipment, net . . . . . . . . . . . . . . . 91,073 3,226 94,299

Receivables, prepaid expenses andother assets . . . . . . . . . . . . . . . . . . 4,759 65,782 72,977 501 144,019

Contracts receivable . . . . . . . . . . . . . 98,602 68,285 166,887

Mortgage loans receivable . . . . . . . . . 78,345 78,345

Customer deposits held in escrow . . . 48,724 2,284 51,008

Investments in and advances to

unconsolidated entities . . . . . . . . . 251,035 251,035

Investments in and advances to

consolidated entities . . . . . . . . . . . 3,785,882 1,156,424 (1,336,009) (134,979) (3,471,318) —

3,785,882 1,161,183 5,397,804 543,069 (3,470,817) 7,417,121

LIABILITIES AND STOCKHOLDERS’ EQUITYLiabilities:

Loans payable . . . . . . . . . . . . . . . . 484,741 226,129 710,870

Senior notes . . . . . . . . . . . . . . . . . 1,141,452 1,141,452

Senior subordinated notes . . . . . . . 350,000 350,000

Mortgage company warehouseloan . . . . . . . . . . . . . . . . . . . . . 65,887 65,887

Customer deposits . . . . . . . . . . . . . 311,443 33,231 344,674

Accounts payable . . . . . . . . . . . . . 243,771 9,582 253,353

Accrued expenses . . . . . . . . . . . . . 19,731 614,680 124,775 759,186

Income taxes payable . . . . . . . . . . 288,074 (1,946) 286,128

Total liabilities . . . . . . . . . . . . . 288,074 1,161,183 2,004,635 457,658 — 3,911,550

Minority interest . . . . . . . . . . . . . . . . 7,763 7,763

Stockholders’ equity:

Common stock . . . . . . . . . . . . . . . 1,563 2,003 (2,003) 1,563

Additional paid-in capital . . . . . . . 225,359 4,420 2,734 (7,154) 225,359

Retained earnings . . . . . . . . . . . . . 3,317,590 3,388,749 72,911 (3,461,660) 3,317,590

Treasury stock, at cost . . . . . . . . . . (46,704) (46,704)

Total stockholders’ equity . . . . . 3,497,808 — 3,393,169 77,648 (3,470,817) 3,497,808

3,785,882 1,161,183 5,397,804 543,069 (3,470,817) 7,417,121

16

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Condensed Consolidating Balance Sheet at October 31, 2006 ($ in thousands):Toll

Brothers,Inc.

SubsidiaryIssuer

GuarantorSubsidiaries

Non-Guarantor

Subsidiaries Eliminations Consolidated

ASSETSCash and cash equivalents . . . . . . . . . 582,465 50,059 632,524

Inventory . . . . . . . . . . . . . . . . . . . . . . 5,719,057 376,645 6,095,702

Property, construction and officeequipment, net . . . . . . . . . . . . . . . . 90,676 8,413 99,089

Receivables, prepaid expenses andother assets . . . . . . . . . . . . . . . . . . 4,932 76,317 78,920 277 160,446

Contracts receivable . . . . . . . . . . . . . . 87,030 83,081 170,111

Mortgage loans receivable . . . . . . . . . 130,326 130,326

Customer deposits held in escrow . . . . 46,198 3,478 49,676

Investments in and advances tounconsolidated entities . . . . . . . . . . 245,667 245,667

Investments in and advances toconsolidated entities . . . . . . . . . . . . 3,752,372 1,157,554 (1,350,097) (151,355) (3,408,474) —

3,752,372 1,162,486 5,497,313 579,567 (3,408,197) 7,583,541

LIABILITIES AND STOCKHOLDERS’ EQUITYLiabilities:

Loans payable . . . . . . . . . . . . . . . . 510,848 226,086 736,934

Senior notes . . . . . . . . . . . . . . . . . . 1,141,167 1,141,167Senior subordinated notes . . . . . . . . 350,000 350,000

Mortgage company warehouseloan . . . . . . . . . . . . . . . . . . . . . . 119,705 119,705

Customer deposits . . . . . . . . . . . . . 325,607 34,540 360,147

Accounts payable . . . . . . . . . . . . . . 282,194 9,977 292,171

Accrued expenses . . . . . . . . . . . . . 21,319 690,651 113,319 (1) 825,288

Income taxes payable . . . . . . . . . . . 336,446 (1,946) 334,500

Total liabilities . . . . . . . . . . . . 336,446 1,162,486 2,159,300 501,681 (1) 4,159,912

Minority interest . . . . . . . . . . . . . . . . 7,703 7,703

Stockholders’ equity:

Common stock. . . . . . . . . . . . . . . . 1,563 2,003 (2,003) 1,563

Additional paid-in capital . . . . . . . . 220,783 4,420 2,734 (7,154) 220,783

Retained earnings. . . . . . . . . . . . . . 3,263,274 3,333,593 65,446 (3,399,039) 3,263,274

Treasury stock, at cost . . . . . . . . . . (69,694) (69,694)

Total stockholders’ equity . . . . 3,415,926 — 3,338,013 70,183 (3,408,196) 3,415,926

3,752,372 1,162,486 5,497,313 579,567 (3,408,197) 7,583,541

17

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Condensed Consolidating Statement of Income for the three months ended January 31, 2007($ in thousands):

TollBrothers,

Inc.Subsidiary

IssuerGuarantor

Subsidiaries

Non-Guarantor

Subsidiaries Eliminations Consolidated

Revenues:

Traditional home sales. . . . . . . . . . 1,054,136 1,054,136Percentage of completion . . . . . . . 14,896 18,189 33,085

Land sales . . . . . . . . . . . . . . . . . . 3,390 3,390

— — 1,072,422 18,189 — 1,090,611

Costs of revenues:

Traditional home sales. . . . . . . . . . 846,177 1,566 (1,340) 846,403

Percentage of completion . . . . . . . 12,473 13,424 25,897

Land sales . . . . . . . . . . . . . . . . . . 1,037 1,037

Interest . . . . . . . . . . . . . . . . . . . . . 16,735 18,989 3,654 (16,735) 22,643

— 16,735 878,676 18,644 (18,075) 895,980

Selling, general and administrative . . 7 180 134,425 8,403 (8,805) 134,210

Goodwill impairment . . . . . . . . . . . . 8,973 8,973

Income from operations . . . . . . . . . . (7) (16,915) 50,348 (8,858) 26,880 51,448

Other:

Equity earnings . . . . . . . . . . . . . . . 6,792 6,792

Interest and other . . . . . . . . . . . . . 16,915 30,067 21,117 (39,139) 28,960

Earnings from subsidiaries. . . . . . . 87,207 (87,207) —

Income before income taxes . . . . . . . 87,200 — 87,207 12,259 (99,466) 87,200

Income taxes . . . . . . . . . . . . . . . . . . 32,884 32,051 4,793 (36,844) 32,884

Net income. . . . . . . . . . . . . . . . . . . . 54,316 — 55,156 7,466 (62,622) 54,316

18

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Condensed Consolidating Statement of Income for the three months ended January 31, 2006($ in thousands):

TollBrothers,

Inc.Subsidiary

IssuerGuarantor

Subsidiaries

Non-Guarantor

Subsidiaries Eliminations Consolidated

Revenues:

Traditional home sales . . . . . 1,278,709 1,278,709Percentage of completion . . . 28,015 29,554 57,569

Land sales . . . . . . . . . . . . . . 4,678 4,678

— — 1,311,402 29,554 — 1,340,956

Costs of revenues:

Traditional home sales . . . . . 883,469 1,271 (649) 884,091

Percentage of completion . . . 21,616 25,730 47,346

Land sales . . . . . . . . . . . . . . 3,836 3,836

Interest . . . . . . . . . . . . . . . . 16,735 28,553 766 (17,300) 28,754

— 16,735 937,474 27,767 (17,949) 964,027

Selling, general andadministrative . . . . . . . . . . . 17 173 139,554 7,421 (7,987) 139,178

Income from operations . . . . . . (17) (16,908) 234,374 (5,634) 25,936 237,751

Other:

Equity earnings . . . . . . . . . . 16,569 16,569

Interest and other . . . . . . . . . 16,908 14,720 11,996 (32,297) 11,327

Earnings from subsidiaries . . 265,664 (265,664) —

Income before income taxes. . . 265,647 — 265,663 6,362 (272,025) 265,647

Income taxes . . . . . . . . . . . . . . 101,797 102,572 2,488 (105,060) 101,797

Net income . . . . . . . . . . . . . . . 163,850 — 163,091 3,874 (166,965) 163,850

19

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Condensed Consolidating Statement of Cash Flows for the three months ended January 31, 2007($ in thousands):

TollBrothers,

Inc.Subsidiary

IssuerGuarantor

Subsidiaries

Non-Guarantor

Subsidiaries Eliminations Consolidated

Cash flow from operating activities:Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54,316 55,156 7,466 (62,622) 54,316Adjustments to reconcile net income to net cash used in

operating activities:Depreciation and amortization . . . . . . . . . . . . . . . . . . . . . 285 7,449 115 7,849Amortization of initial benefit obligation . . . . . . . . . . . . . . 442 442Stock-based compensation . . . . . . . . . . . . . . . . . . . . . . . . 12,888 12,888Excess tax benefit from stock-based compensation . . . . . . . . (2,976) (2,976)Equity earnings in unconsolidated entities . . . . . . . . . . . . . . (6,521) (271) (6,792)Distributions from unconsolidated entities . . . . . . . . . . . . . . 6,660 (7) 6,653Deferred tax provision . . . . . . . . . . . . . . . . . . . . . . . . . . (37,874) (37,874)Provision for inventory write-offs . . . . . . . . . . . . . . . . . . . 96,901 96,901Goodwill impairment . . . . . . . . . . . . . . . . . . . . . . . . . . . 8,973 8,973Gain on sale of business . . . . . . . . . . . . . . . . . . . . . . . . . (9,565) (9,565)Changes in operating assets and liabilities

Increase in inventory . . . . . . . . . . . . . . . . . . . . . . . . . . (179,053) (7,652) (186,705)Origination of mortgage loans . . . . . . . . . . . . . . . . . . . . (281,317) (281,317)Sale of mortgage loans . . . . . . . . . . . . . . . . . . . . . . . . 333,298 333,298Decrease (increase) in contracts receivable . . . . . . . . . . . . (11,572) 14,796 3,224Decrease (increase) in receivables, prepaid expenses and

other assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (33,510) 1,303 (13,566) (10,556) 62,622 6,293Decrease in customer deposits . . . . . . . . . . . . . . . . . . . . (16,690) (115) (16,805)(Decrease) increase in accounts payable and accrued

expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,010 (1,588) (114,277) 11,061 (97,794)Decrease in current income taxes payable . . . . . . . . . . . . (7,291) (7,291)

Net cash (used in) provided by operating activities . . . . . (7,437) — (166,098) 57,253 — (116,282)

Cash flow from investing activities:Purchase of property and equipment, net . . . . . . . . . . . . . . . . (6,307) (718) (7,025)Purchase of marketable securities . . . . . . . . . . . . . . . . . . . . . (1,073,575) (112,950) (1,186,525)Sale of marketable securities . . . . . . . . . . . . . . . . . . . . . . . . 1,073,575 112,950 1,186,525Proceeds from sale of business . . . . . . . . . . . . . . . . . . . . . . 15,755 15,755Investments in and advances to unconsolidated entities . . . . . . . (4,989) (4,989)

Net cash provided by (used in) investing activities . . . . . — — (11,296) 15,037 — 3,741

Cash flow from financing activities:Proceeds from loans payable . . . . . . . . . . . . . . . . . . . . . . . . 506 286,764 287,270Principal payments of loans payable . . . . . . . . . . . . . . . . . . . (24,962) (340,539) (365,501)Proceeds from stock-based benefit plans . . . . . . . . . . . . . . . . 3,317 3,317Excess tax benefit from stock-based compensation . . . . . . . . . . 2,976 2,976Proceeds from restricted stock award . . . . . . . . . . . . . . . . . . 1,800 1,800Change in minority interest . . . . . . . . . . . . . . . . . . . . . . . . . 60 60Purchase of treasury stock . . . . . . . . . . . . . . . . . . . . . . . . . (656) (656)

Net cash (used in) provided by financing activities . . . . . 7,437 — (24,456) (53,715) — (70,734)

Net (decrease) increase in cash and cash equivalents . . . . . . . . . . — — (201,850) 18,575 — (183,275)Cash and cash equivalents, beginning of period . . . . . . . . . . . . . 582,465 50,059 632,524

Cash and cash equivalents, end of period . . . . . . . . . . . . . . . . . — — 380,615 68,634 — 449,249

20

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Condensed Consolidating Statement of Cash Flows for the three months ended January 31, 2006($ in thousands):

TollBrothers,

Inc.Subsidiary

IssuerGuarantor

Subsidiaries

Non-Guarantor

Subsidiaries Eliminations Consolidated

Cash flow from operating activities:Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163,850 163,091 3,874 (166,965) 163,850Adjustments to reconcile net income to net cash used

in operating activities:Depreciation and amortization . . . . . . . . . . . . . . . 285 6,050 573 6,908Amortization of initial benefit obligation . . . . . . . . 449 449Stock-based compensation . . . . . . . . . . . . . . . . . . 11,075 11,075Excess tax benefit from stock-based

compensation . . . . . . . . . . . . . . . . . . . . . . . . . (7,301) (7,301)Equity earnings in unconsolidated entities . . . . . . . (16,569) (16,569)Distributions from unconsolidated entities . . . . . . . 2,643 2,643Deferred tax provision . . . . . . . . . . . . . . . . . . . . . 7,625 7,625Provision for inventory write-offs . . . . . . . . . . . . . 1,129 1,129Changes in operating assets and liabilities:

Increase in inventory . . . . . . . . . . . . . . . . . . . . (215,625) (34,470) (250,095)Origination of mortgage loans . . . . . . . . . . . . . . (176,908) (176,908)Sale of mortgage loans . . . . . . . . . . . . . . . . . . . 227,749 227,749Contracts receivable . . . . . . . . . . . . . . . . . . . . . (28,015) (29,554) (57,569)(Increase) decrease in receivables, prepaid

expenses and other assets . . . . . . . . . . . . . . . (196,846) 573 (7,642) 47,977 163,925 7,987Increase in customer deposits . . . . . . . . . . . . . . 481 481Increase (decrease) in accounts payable and

accrued expenses . . . . . . . . . . . . . . . . . . . . . 10,926 (858) (104,876) 6,327 3,040 (85,441)Increase in current income taxes payable . . . . . . 19,173 19,173

Net cash (used in) provided by operatingactivities . . . . . . . . . . . . . . . . . . . . . . . . . 8,502 — (198,884) 45,568 — (144,814)

Cash flow from investing activities:Purchase of property and equipment, net . . . . . . . . . . (13,469) (795) (14,264)Purchases of marketable securities . . . . . . . . . . . . . . (970,820) (15,000) (985,820)Sales of marketable securities . . . . . . . . . . . . . . . . . 970,820 15,000 985,820Investments in and advances to unconsolidated

entities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (71,369) (71,369)Acquisition of joint venture interest . . . . . . . . . . . . . (40,751) (40,751)Distributions from unconsolidated entities . . . . . . . . . 2,512 2,512

Net cash used in investing activities . . . . . . . . — — (123,077) (795) — (123,872)

Cash flow from financing activities:Proceeds from loans payable . . . . . . . . . . . . . . . . . . 80,870 177,842 258,712Principal payments of loans payable . . . . . . . . . . . . . (93,894) (213,286) (307,180)Proceeds from stock based benefit plans . . . . . . . . . . 5,972 5,972Excess tax benefit from stock-based compensation . . . 7,301 7,301Purchase of treasury stock . . . . . . . . . . . . . . . . . . . . (21,775) (21,775)

Net cash used in financing activities . . . . . . . . (8,502) — (13,024) (35,444) — (56,970)

Net (decrease) increase in cash and cash equivalents . . . — — (334,985) 9,329 — (325,656)Cash and cash equivalents, beginning of period . . . . . . . 664,312 24,907 689,219

Cash and cash equivalents, end of period . . . . . . . . . . . — — 329,327 34,236 — 363,563

21

TOLL BROTHERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

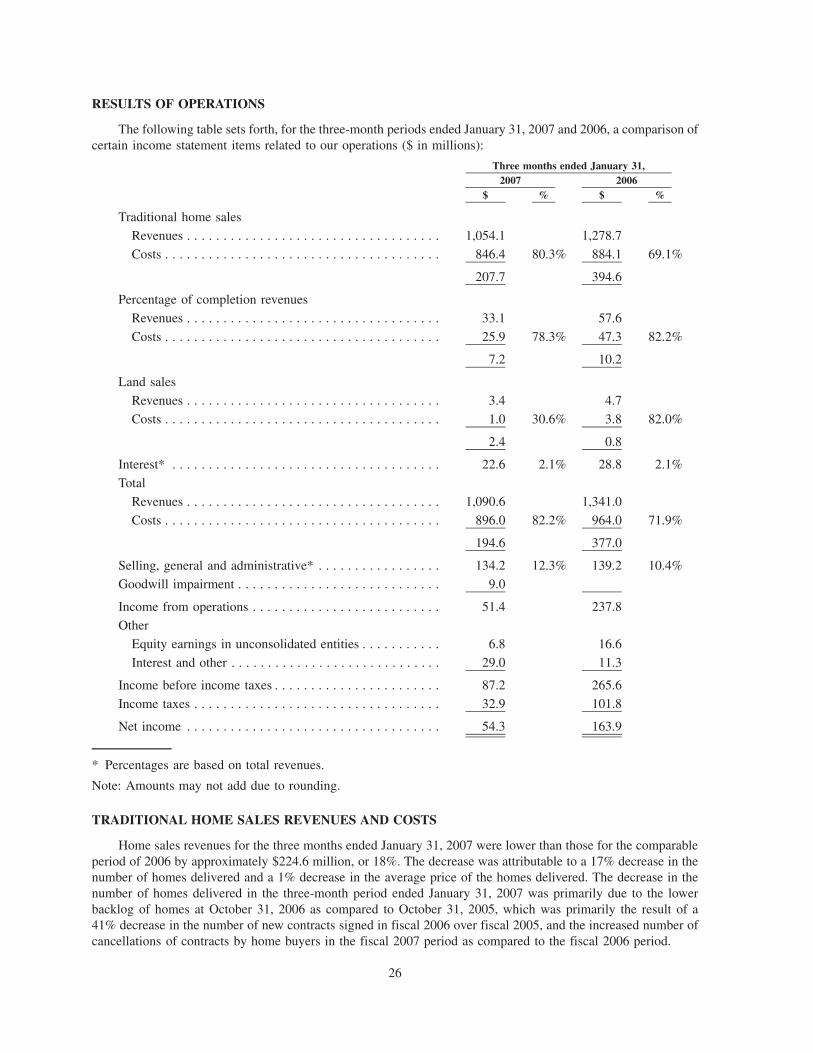

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION ANDRESULTS OF OPERATIONS

OVERVIEW

The financial guidance contained herein related to our expected results of operations for fiscal 2007 reflectsour expectations as of February 22, 2007, is the same guidance given in the Form 8-K that we filed on February 22,2007 and is not being reconfirmed or updated by this Quarterly Report on Form 10-Q.

In our first quarter ended January 31, 2007, we recognized $1.09 billion of revenues and earned $54.3 millionof net income as compared to $1.34 billion of revenue and $163.9 million of net income in the first quarter of fiscal2006. We recognized $105.9 million of inventory write-downs and a goodwill impairment in the first quarter offiscal 2007 as compared to $1.1 million of inventory write-downs in the first quarter of fiscal 2006. In addition, ourbacklog at January 31, 2007 of $4.15 billion decreased 30% as compared to our backlog at January 31, 2006.Backlog consists of homes under contract but not yet delivered to our home buyer for our traditional product and forour non-traditional high- and mid-rise product accounted for using the completed contract method of accounting.Backlog for homes for which we use the percentage of completion accounting method consists of homes undercontract but not yet delivered to our home buyer less the amount of revenues we have recognized related to thosehomes.