tolley tax update

TRANSCRIPT

© Copyright LexisNexis 2017

TOLLEY TAX

UPDATE

Presented by:

Chris Jones &

Rebecca Benneyworth

16th January 2017

Reference

Palette

Copy and paste this palette to

any slide to recall a specified

colour when designing visual

exhibits. Keep off the slide layout

area and it will not display in

slide show mode.

237/28/36 0/0/0 137/137/137

LN Confidential

1

© Copyright LexisNexis 2017

Personal Taxes

© Copyright LexisNexis 2017

Class 2 NIC

• Will be abolished from April 2018

• Just Class 3 (voluntary) and Class 4 for self-employed

• Self-employed people with profits below the Small Profits Limit (so not paying Class 4)

• Access to Contributory Employment and Support Allowance through Class 3 NIC

• Class 3 rate currently £14.10 per week

© Copyright LexisNexis 2017

Trader omitted to pay Class 2

• Applied to pay backdated contributions for the period 1967/68 to 2007/08

• Accepted that failure to pay was due to error and ignorance

• But maintained that he had exercised due care and diligence

• HMRC refused late payments

• Trader had appointed an accountant and was cautious with paperwork

• His behaviour demonstrated that he would have paid class 2 had he known it was due

• Tribunal ruled that late payment was acceptable

© Copyright LexisNexis 2017

Conditions to transfer PAYE to employee

• Three conditions must be met before the PAYE liability transfers to the employee (SI 2003/2682 Reg 72)

• the employer did not deduct PAYE;

• the failure was wilful and deliberate; and

• the employee received remuneration, knowing the employer had wilfully not deducted the tax

• In the case of S. West v HMRC the taxpayer was the director and shareholder of A

• He built up overdrawn DLAs each year

• Extinguished by remuneration and dividends paid at the end of the year

• For the years ending 30 April 2007 to 2010, the accounts showed outstanding loans

• He was advised to liquidate the company by an insolvency practitioner

© Copyright LexisNexis 2017

Conditions to transfer PAYE to employee

• The company could not pay the taxpayer any dividends because there were insufficient profits, so he was advised to draw salary

• The taxpayer gave his accountant instructions to prepare accounts in line with the advice

• The PAYE and National Insurance for the remuneration were shown on the balance sheet as current liabilities

• but not paid to HMRC

• HMRC issued income tax and NIC determinations transferring the liabilities from the company to the taxpayer

• on the assumption that he had knowingly received payments from the company on which it had 'wilfully' failed to deduct tax

• The taxpayer appealed, as he believed the tax had been paid

© Copyright LexisNexis 2017

First Tier Tribunal

• Judge Clark said that the accounts showed deductions for tax and NIC from the payment to the taxpayer

• so the liability could not be shifted to the taxpayer and the appeal would be allowed!

• The decision opens the door for OMBs that are about go into liquidation to make preferential and potentially unfair payments to their owners at the expense of trade or other creditors, like HMRC

• HMRC are likely to appeal as the decision seems very wrong

© Copyright LexisNexis 2017

First Tier Tribunal

• Judge O’Neil disagreed with the decision but Judge Clark had the casting vote

• …but her reasoning seems more sensible

• Judge O’Neill said it was clear from the accounts that the entries for PAYE and NIC deductions were 'entirely notional' and had 'no substance in reality'

• The taxpayer signed off the accounts knowing that

• the sums had not been paid to HMRC, and

• it would be impossible to pay them from the liquidation of the company's assets.

• The taxpayer accepted for practical purposes that he and the company were 'one and the same‘

• By creating obligations which the company knew it could not meet, it had 'wilfully failed to discharge those obligations and has done so, in the knowledge, indeed at the instigation of the taxpayer

© Copyright LexisNexis 2017

Discretionary bonus and SMP

• The FTT found that it was correct to include a discretionary bonus paid to a pregnant employee when determining her 'earnings related rate' of SMP

• The SMP calculation was 'purely arithmetical‘

• You take the earnings in the relevant period (which in this case includes the bonus) and then calculate the weekly equivalent of that amount

• There was no requirement for the pay during the relevant period to be 'normal' in the sense of the usual amount

• The payment of a bonus during the relevant period may have the effect of significantly increasing the amount of SMP due in the first six weeks of maternity leave

© Copyright LexisNexis 2017

Travel expenses – temporary workplace

• Employee will have a permanent workplace when they intend to spend 40% of their time for two years at a certain location

• No employee travel deductions for home to permanent workplace

• Mr Gosset lived in Wales

• 2008/09 employment based in Surrey

• Claimed deduction for travel and subsistence on basis of ‘temporary workplace’

• HMRC refused claim “no evidence of limited duration”

• FTT

• No evidence employer envisaged Mr Gosset working at different sites

• Had been based in Surrey for 2 years without being moved on

• Appeal dismissed

© Copyright LexisNexis 2017

Tax treatment of PILON

• Mr Phillips’ employment with ISG terminated from January 2013

• Paid £15,000 compensation, £47,521 in lieu of notice

• Mr P allocated the £47,521 across 2012/13 and 2013/14 SATRs – covered 6 month period straddling those years

• HMRC – should all be taxed in 2012/13 when received

• FTT decision…

• No contractual right to PILON so £30,000 was tax free

• Balance was taxable when received in 2012/13

© Copyright LexisNexis 2017

Is director’s loan interest annual?

• If a directors loan account is in credit it would be good practice to pay interest on that account

• ….HMRC accepting 6% to 8% as a reasonable rate

• Low salary, high dividend extraction can give access to £6,000 of tax free interest for a base rate taxpayer

• ….£5,500 for a high rate taxpayer

• Should tax be deducted on the interest payments via the CT61 process?

• If it is annual interest tax must be deducted

• If a loan is capable of being outstanding for more than a year it is annual interest and a CT61 is required

• Directors loans are normally shown as repayable on demand in current liabilities on the Balance Sheet

• ….are they legally incapable of being outstanding > 1 year?

© Copyright LexisNexis 2017

Accounting rules

• From an accounting perspective there might well be a rush to charge market rates of interest on director loans to avoid the need for loan remeasurement on initial recognition to NPV and subsequent remeasurement to amortised costs

• The first line of defence against this treatment is accepting that the loan is repayable on demand

• The absence of repayment terms or unclear/unenforceable terms both default to repayable on demand

• This avoids the remeasurement issues and the loan account is shown as a current liability in the Balance Sheet

• Any interest payable will however be yearly interest for tax purposes as it is not incapable of being outstanding for a year or more.

© Copyright LexisNexis 2017

Accounting rules

• Sometimes it is commercially impossible to present creditors in this way because the Balance Sheet suffers liquidity issues so the loan has to be presented as repayable in more than one year

• For this treatment to work then the loan has to be incapable of being recalled within one year

• Loan interest continues be annual interest and this would need to be charged at market value to avoid the remeasurement issues individuals are charging interest on their loans

© Copyright LexisNexis 2017

Lending to the company….

• Max draws salary of £11,000 and dividends of £32,000 from his trading company

• Max also has £75,000 of personal savings in a deposit account bearing interest at < 1%

• Max decides to lend his company £25,000 at 8% over each of the next three years to enable the company to make an annual pension contribution of £25,000

• The company has reasonable levels of retained profit but is not cash rich

• …the loan is required to pay the contribution

© Copyright LexisNexis 2017

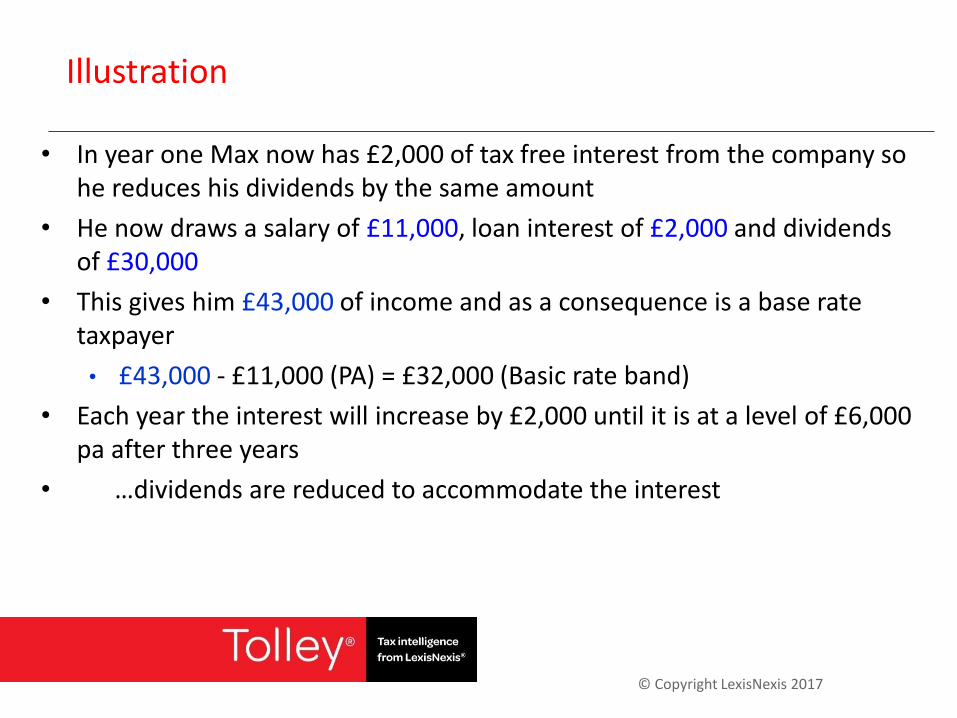

Illustration

• In year one Max now has £2,000 of tax free interest from the company so he reduces his dividends by the same amount

• He now draws a salary of £11,000, loan interest of £2,000 and dividends of £30,000

• This gives him £43,000 of income and as a consequence is a base rate taxpayer

• £43,000 - £11,000 (PA) = £32,000 (Basic rate band)

• Each year the interest will increase by £2,000 until it is at a level of £6,000 pa after three years

• …dividends are reduced to accommodate the interest

© Copyright LexisNexis 2017

Illustration

• Max has restructured his income so as to reduce the effective rate of extraction

• HMRC are unlikely to challenge the remuneration levels..

• Salary of £11,000, pension contributions £25,000

• An employment contract could be drafted to support this

• The £25,000 annual contributions secure CT relief

• After three years he will have £75,000 invested in his pension fund

• ….plus the company owes him the £75,000

• …..accruing £6,000 tax free interest at 8% every year

• ……better return than his current 1% on his £75,000 !

© Copyright LexisNexis 2017

Car benefit?

• Mrs Fowler – fixed term contract

> Choice or

• Car value < allowance so was paid difference

• Car shown on P11D but claimed because only paid balance of car allowance, she had in effect paid the rentals on the car and deducted them

• Also claimed 45p per mile for business mileage

• FTT agreed with HMRC – no contribution from her own resources

• Liable for car benefit, and on excessive mileage payments

© Copyright LexisNexis 2017

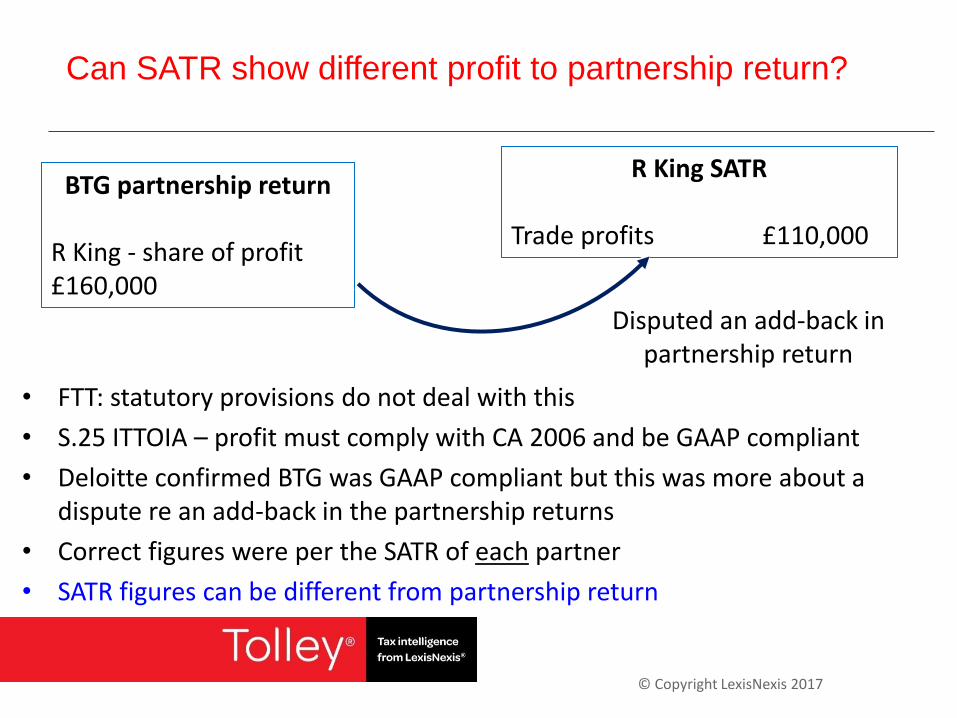

Can SATR show different profit to partnership return?

• FTT: statutory provisions do not deal with this

• S.25 ITTOIA – profit must comply with CA 2006 and be GAAP compliant

• Deloitte confirmed BTG was GAAP compliant but this was more about a dispute re an add-back in the partnership returns

• Correct figures were per the SATR of each partner

• SATR figures can be different from partnership return

BTG partnership return R King - share of profit £160,000

R King SATR Trade profits £110,000

Disputed an add-back in partnership return

© Copyright LexisNexis 2017

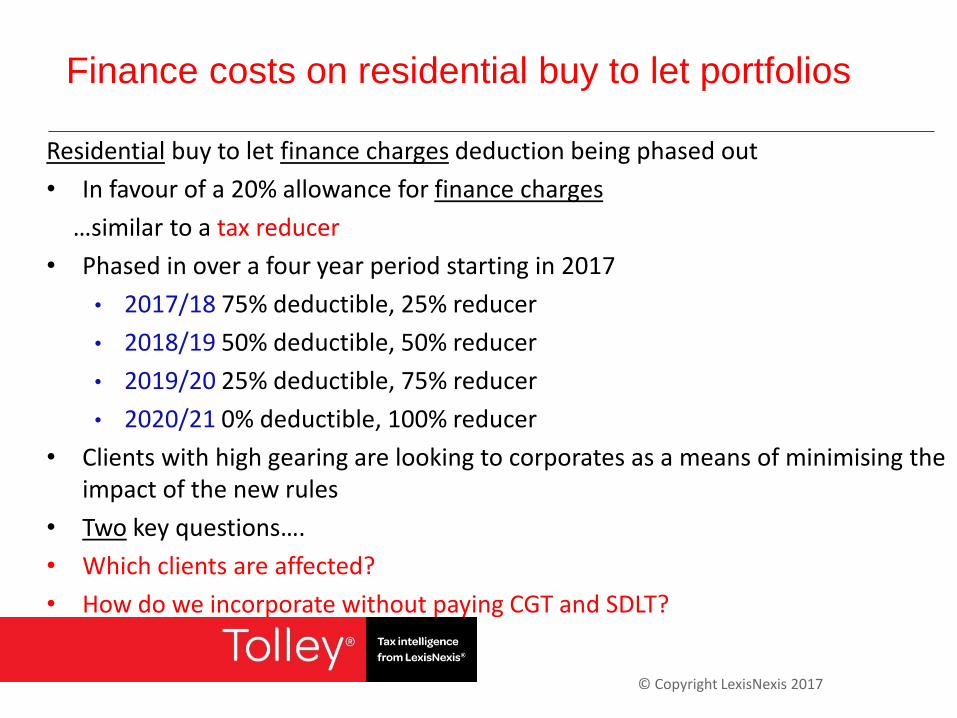

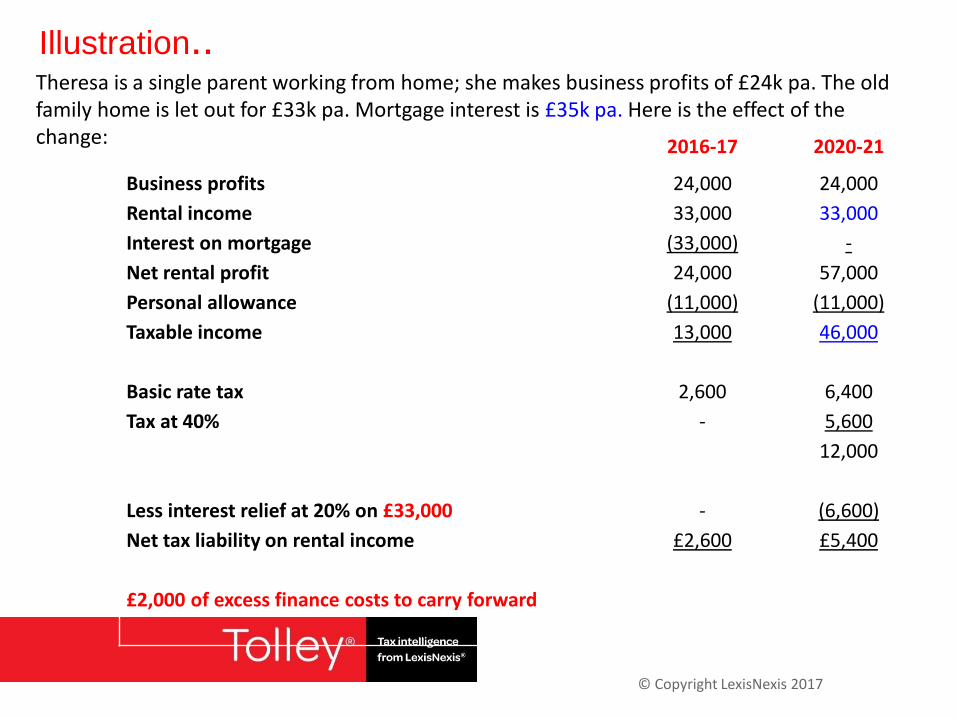

Finance costs on residential buy to let portfolios

Residential buy to let finance charges deduction being phased out

• In favour of a 20% allowance for finance charges

…similar to a tax reducer

• Phased in over a four year period starting in 2017

• 2017/18 75% deductible, 25% reducer

• 2018/19 50% deductible, 50% reducer

• 2019/20 25% deductible, 75% reducer

• 2020/21 0% deductible, 100% reducer

• Clients with high gearing are looking to corporates as a means of minimising the impact of the new rules

• Two key questions….

• Which clients are affected?

• How do we incorporate without paying CGT and SDLT?

© Copyright LexisNexis 2017

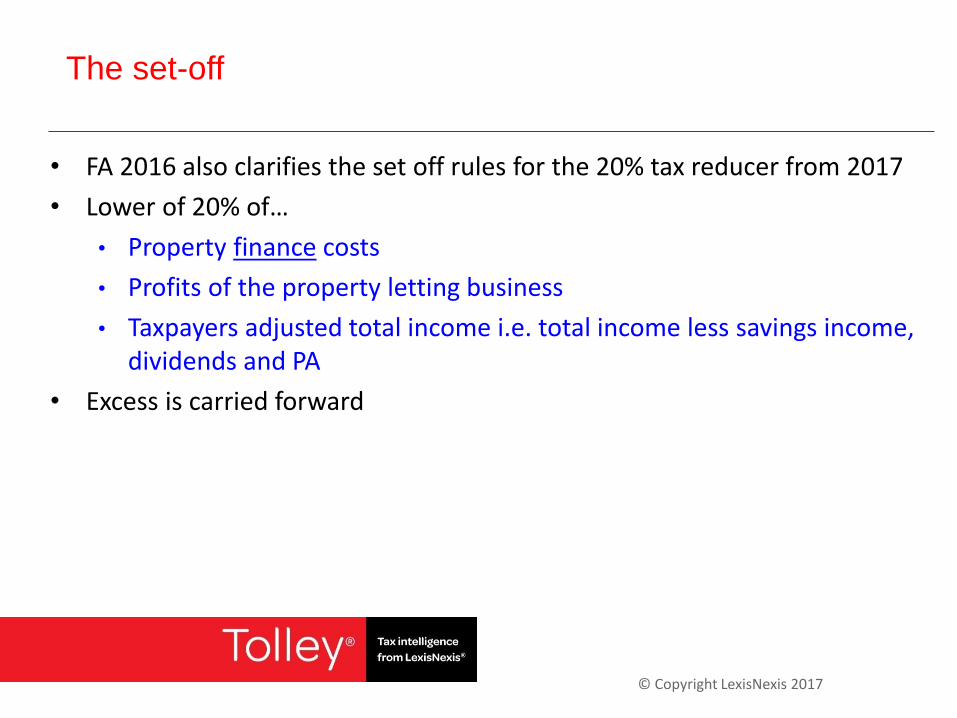

The set-off

• FA 2016 also clarifies the set off rules for the 20% tax reducer from 2017

• Lower of 20% of…

• Property finance costs

• Profits of the property letting business

• Taxpayers adjusted total income i.e. total income less savings income, dividends and PA

• Excess is carried forward

© Copyright LexisNexis 2017

2016-17 2020-21

Business profits 24,000 24,000

Rental income 33,000 33,000

Interest on mortgage (33,000) -

Net rental profit 24,000 57,000

Personal allowance (11,000) (11,000)

Taxable income 13,000 46,000

Basic rate tax 2,600 6,400

Tax at 40% - 5,600

12,000

Less interest relief at 20% on £33,000 - (6,600)

Net tax liability on rental income £2,600 £5,400

£2,000 of excess finance costs to carry forward

Illustration.. Theresa is a single parent working from home; she makes business profits of £24k pa. The old family home is let out for £33k pa. Mortgage interest is £35k pa. Here is the effect of the change:

2

© Copyright LexisNexis 2017

Administration

© Copyright LexisNexis 2017

Too big to miss!

• VAT errors were made when the bookkeeper prepared a manual VAT return from SAGE records!

• Many sales invoices were missed

• HMRC issued assessments to recover the VAT and charged a penalty of 42.5% as the errors were deliberate but not concealed

• Taxpayer appealed against the penalty

• Directors argued that they relied on the bookkeeper to prepare the returns but acknowledged they should have checked them more carefully

• HMRC thought the understated figures were significant and the directors should have noticed

• HMRC thought it strange that the input tax was always correct

• ….whereas the output tax was always understated

• HMRC thought the directors should have insisted on the bookkeeper using SAGE

© Copyright LexisNexis 2017

Too big to miss?

• The key point for deliberate penalties is that HMRC has to prove dishonesty

• Not just a failure to take reasonable care

• FTT thought HMRC had discharged that burden

• The errors were large and the FTT thought the directors could not have failed to spot them

• The inaccuracies were deliberate and the penalty was justified

© Copyright LexisNexis 2017

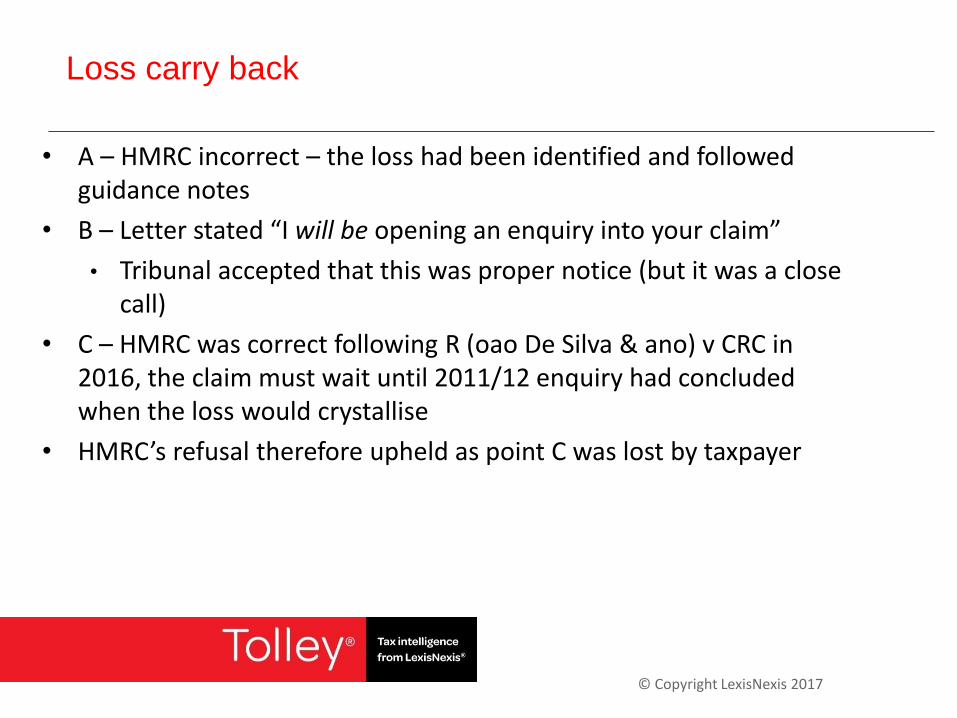

Loss carry back - refusal

• Capital loss incurred in 2011/12 – as a result of a liquidation

• Elect to set against income of 2010/11 and 2011/12

• Liability for 2010/11 reduced to nil – tax already paid was £63,188

• Taxpayer applied to court for a repayment plus interest

• HMRC refused on four grounds:

• A - Claim not properly quantified

• B - Valid enquiry notice into claim had been opened

• C - Claim was premature due to the enquiry into 2011/12

• D - Claim was not for a repayment but was for a credit

© Copyright LexisNexis 2017

Loss carry back

• A – HMRC incorrect – the loss had been identified and followed guidance notes

• B – Letter stated “I will be opening an enquiry into your claim”

• Tribunal accepted that this was proper notice (but it was a close call)

• C – HMRC was correct following R (oao De Silva & ano) v CRC in 2016, the claim must wait until 2011/12 enquiry had concluded when the loss would crystallise

• HMRC’s refusal therefore upheld as point C was lost by taxpayer

© Copyright LexisNexis 2017

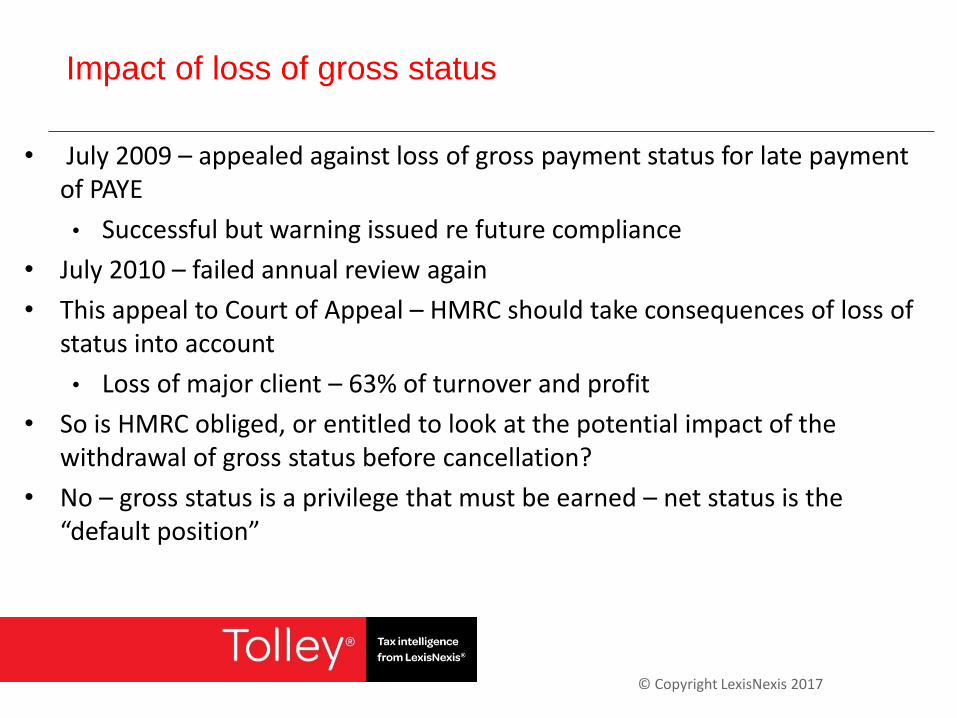

Impact of loss of gross status

• July 2009 – appealed against loss of gross payment status for late payment of PAYE

• Successful but warning issued re future compliance

• July 2010 – failed annual review again

• This appeal to Court of Appeal – HMRC should take consequences of loss of status into account

• Loss of major client – 63% of turnover and profit

• So is HMRC obliged, or entitled to look at the potential impact of the withdrawal of gross status before cancellation?

• No – gross status is a privilege that must be earned – net status is the “default position”

© Copyright LexisNexis 2017

Late appeal

• Trade commenced in April 2003

• Enquiry opened in December 2010 – no clear records of sales

• Large deposit on a property

• HMRC raised assessment, closure notice and penalties

• ADR offered and taken up but trader did not provide information requested

• Trader subsequently appealed – 14 months late

• “Time limits are important for the orderly administration of the tax system” “No good explanation for the delay” “Simple application form for appeal”

© Copyright LexisNexis 2017

Injunction against HMRC to stop enforcement action

• Tax at stake £10.9 million

• Appeals on the matter under dispute

• But HMRC seeking to enforce debt and insolvent liquidation would follow

• Court applied the principles in American Cyanamid

• Claimants case was not “totally without merit”

• A “serious issue to be tried”

• Damages would not be an appropriate remedy should HMRC lose the case

• Should HMRC be successful this delay would be compensated by interest

• Injunction granted

© Copyright LexisNexis 2017

Late VAT registration

• Identified in February 2015 that business should have been VAT registered from 2008

• Had been given bad advice by their accountant

• HMRC had not raised the issue when meeting regarding the construction Industry tax scheme

• BUT – raised the issue with their accountant in 2010 and failed to follow this up

• Reasonable excuse would have ceased at this point

• Penalty upheld

3

© Copyright LexisNexis 2017

CGT Issues for OMBs

© Copyright LexisNexis 2017

Entrepreneurs relief and own share purchase

• The taxpayer declared the share disposal on his tax return and claimed ER

• HMRC concluded that the taxpayer was not entitled to ER because he was not an officer or employee of the company throughout the period of one year ending with the disposal of his shares

• The taxpayer appealed

• He accepted that he had ceased employment with the company and was no longer an office holder from 28 February 2009

• But contended that the completion of the negotiations resulted in a binding contract for sale in February 2009, which was therefore the date of disposal for CGT purposes

© Copyright LexisNexis 2017

FTT decision

• Company law required a contract for a company’s own purchase of shares to be approved in advance by a special resolution

• That resolution was not passed until 29 May 2009

• The company was incapable of entering into a valid contract to purchase the shares until the resolution had been passed.

• Even if there had been a contract, it had to be conditional on approval by special resolution

• The date of disposal under a conditional contract would be the date on which the condition was satisfied

• …29 May 2009

• The taxpayer’s appeal was dismissed

© Copyright LexisNexis 2017

Note

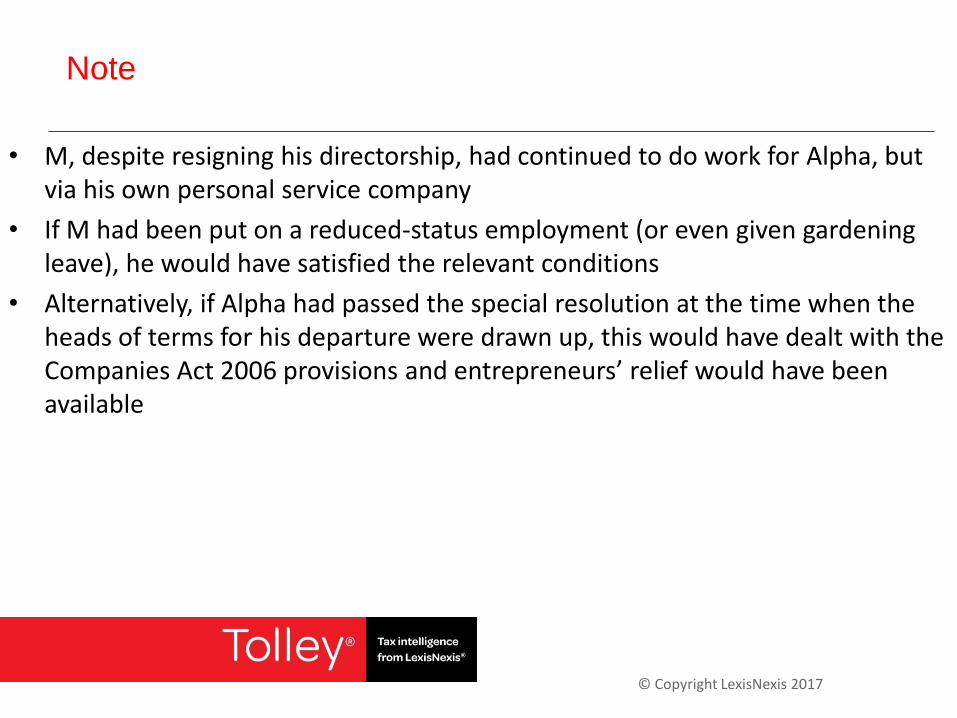

• M, despite resigning his directorship, had continued to do work for Alpha, but via his own personal service company

• If M had been put on a reduced-status employment (or even given gardening leave), he would have satisfied the relevant conditions

• Alternatively, if Alpha had passed the special resolution at the time when the heads of terms for his departure were drawn up, this would have dealt with the Companies Act 2006 provisions and entrepreneurs’ relief would have been available

© Copyright LexisNexis 2017

New challenge on share buy-backs

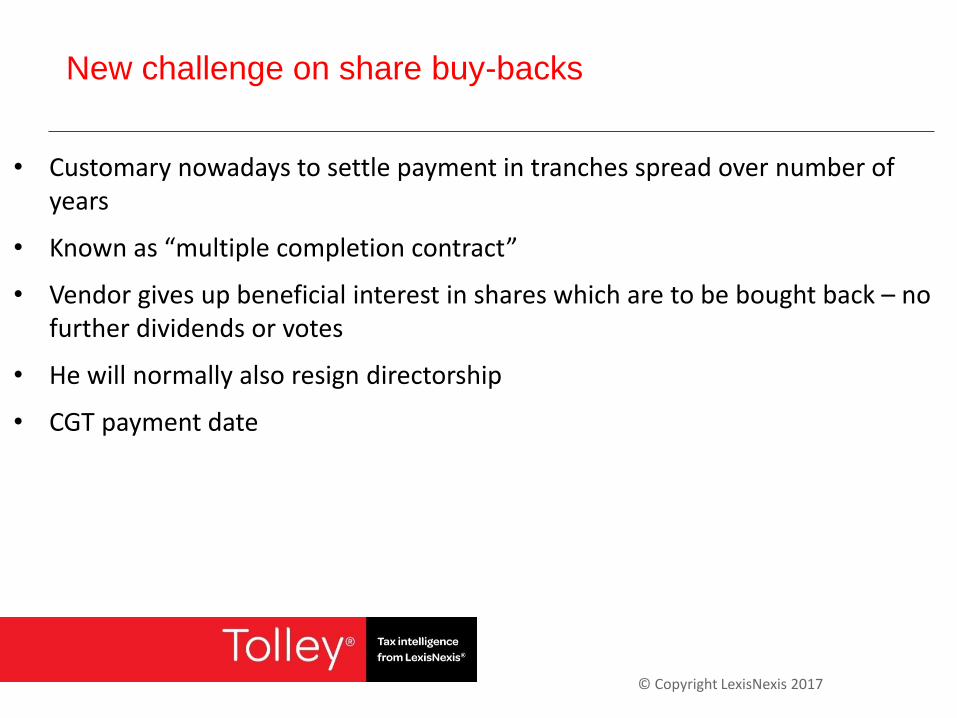

• Customary nowadays to settle payment in tranches spread over number of years

• Known as “multiple completion contract”

• Vendor gives up beneficial interest in shares which are to be bought back – no further dividends or votes

• He will normally also resign directorship

• CGT payment date

© Copyright LexisNexis 2017

New challenge on share buy-backs

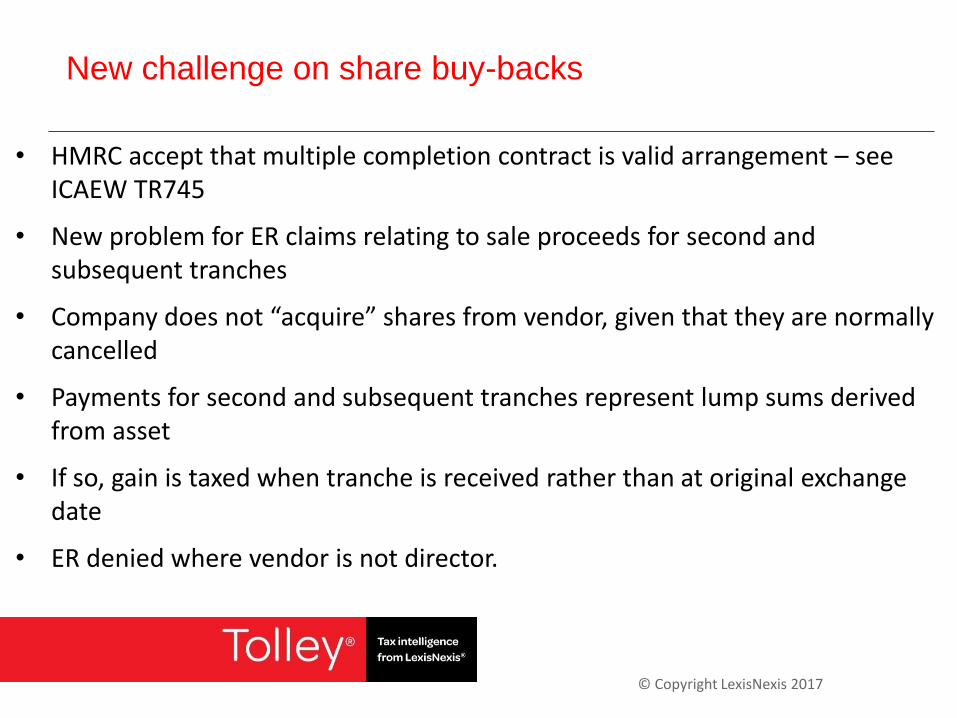

• HMRC accept that multiple completion contract is valid arrangement – see ICAEW TR745

• New problem for ER claims relating to sale proceeds for second and subsequent tranches

• Company does not “acquire” shares from vendor, given that they are normally cancelled

• Payments for second and subsequent tranches represent lump sums derived from asset

• If so, gain is taxed when tranche is received rather than at original exchange date

• ER denied where vendor is not director.

© Copyright LexisNexis 2017

New challenge on share buy-backs

• Note that clearance under S1044 CTA 2010 only confirms that transaction is not treated as income distribution.

• It does not say that ER is available.

• HMRC’s argument goes against all currently accepted technical analyses of multiple completion contracts – they are not tax avoidance schemes.

• Indeed, whole of CGT is paid up front!

• Since ICAEW TR745 has never been retracted, is there possibility of running “legitimate expectation” argument in relation to deals which have already taken place?

• Should shareholders now be looking to retain “sentimental” 5% stake following own share purchases?

• And remaining as part-time employee?

© Copyright LexisNexis 2017

Incorporation of a mixed partnership

• Many mixed partnerships have looked to incorporate in recent times

• Due to FA 2014 anti-avoidance legislation

• In 2014, The CIOT sought guidance from HMRC on the consequences of incorporating a ‘mixed partnership’

• In particular the availability of s.162 CGT relief on incorporation, which allows gains to be rolled over into the cost of the shares

• S.162 relief requires that all the assets of the business (other than cash) are transferred to the company.

• In a response dated 16 May 2014, HMRC stated the following…

© Copyright LexisNexis 2017

HMRC view…

• You have asked about mixed partnerships and incorporation relief in section 162 TCGA 1992

• We would, subject to all the other conditions being satisfied, accept that section 162 can apply to the individual members

• where an LLP transfers its business to the corporate member in exchange for shares in the corporate member.

• Section 59A(1)(b) treats any dealings by the LLP as those of its members

• so the transfer of its business by an LLP will be treated as a transfer by its members.

• Relief would be available to the extent stated in section 162 to any individual member who received shares in exchange for the business

© Copyright LexisNexis 2017

However

• HMRC have recently changed their approach!

• HMRC now state that incorporation relief is unavailable in these circumstances

• as the whole of the business is not transferred (since the corporate partner to which the rest of the business is transferred retains its original interest)

• This change of practice applies to incorporations from 30 April 2016

• CIOT has asked HMRC to consider introducing a specific statutory relief so that the provisions of S162 TCGA 1992 would continue to be in point when mixed partnerships incorporate in the manner described above

• A request that is now being considered

4

© Copyright LexisNexis 2017

VAT

© Copyright LexisNexis 2017

VAT flat rate change

• From 1 April 2017 there is a new 16.5% flat rate scheme percentage for businesses with limited costs

• ….20/120 = 16.67% so advantage removed

• Applies where VAT inclusive spend on goods < 2% of the VAT inclusive turnover

• ….or greater than that but less than £1,000pa

• …..£250 per quarter

• Will affect businesses with limited costs, such as many labour-only businesses

• If your income is £120,000 you need to spend £2,400 on relevant goods (VAT inclusive numbers)

© Copyright LexisNexis 2017

Relevant goods…

• ‘Relevant goods’ excludes vehicles, road fuel and motor parts, as well as food, drink and capital items

• BUT…

• A transport business, using the FRS category for ‘Transport or storage, including couriers, freight, removals and taxis’, would be able to include spending on vehicles, road fuel and motor parts in their calculations

• Only expenses that are wholly business are included in the calculations

© Copyright LexisNexis 2017

Revised Flat rate notice

• Consultants and engineers can use ordinary English language to determine which category they fall into

• Would a tax consultant describe themselves as a management consultant?

• ….no

• ……..use “Business services not listed elsewhere”

• Would mechanical engineers describe themselves as civil engineers?

• ….no

• ……..use “Business services not listed elsewhere”

• Go back four years if you think client has made an error in their categorisation

• ….more clients now fall in the “Other” category

© Copyright LexisNexis 2017

VAT on sale of empty pub

• Pub with first floor flat – 3 rooms plus bathroom

• Opted to tax – charged VAT on rent to tenant (incorrectly!)

• Tenant left without paying

• Property sold for £52,200 treated as VAT exempt as the pub was untenanted and had no commercial value

• Regarded by vendor as a reasonable price for a residential property in that area

• HMRC applied their standard 90% pub 10% domestic proportion and assessed output tax on 90% (standard practice – in use for almost 30 years)

• Held by Tribunal – the 90% rule is not binding; treating as 100% domestic is not reasonable; used floor area to arrive at 2/3 commercial 1/3 residential split