topic 2 (a) demand & supply module 2 topic 1. demand & supply 1. demand 2. supply 3. market...

TRANSCRIPT

Topic 2 (a)Demand & Supply

Module 2 Topic 1

Demand & Supply

1. Demand

2. Supply

3. Market Equilibrium

4. Consumer & Producer Surplus

1.1 What is demand?

No. of units of a good or service that consumers are willing and able to purchase during a period, under a given set of conditions

1.2 Why is the study of demand important for firms?

Determines a firm’s profitability Affect long run planning and

strategic decisions Affects short run decisions

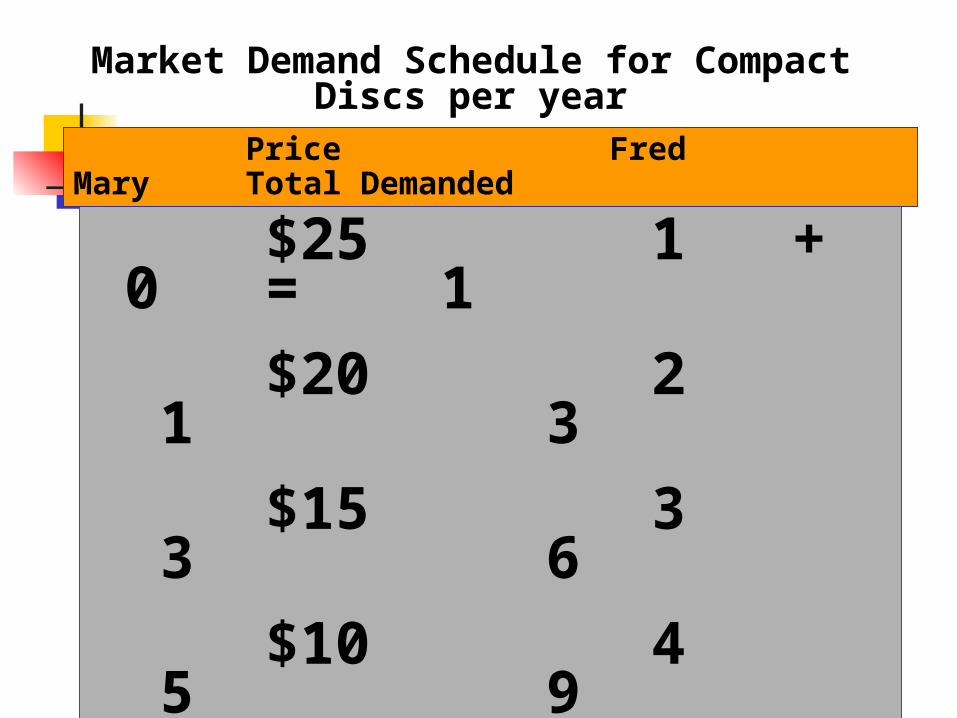

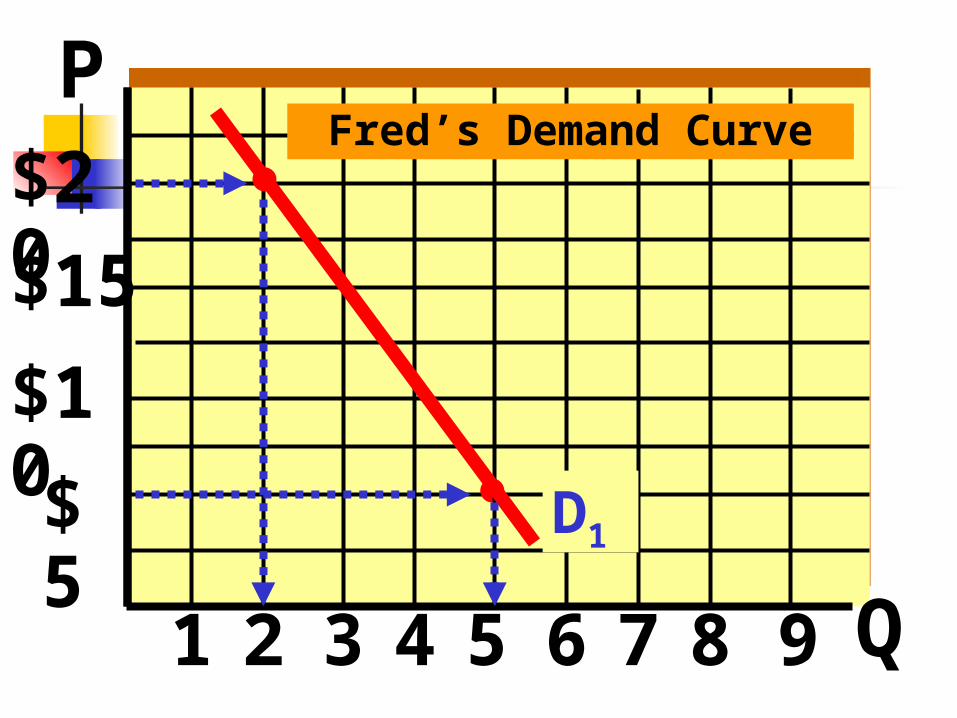

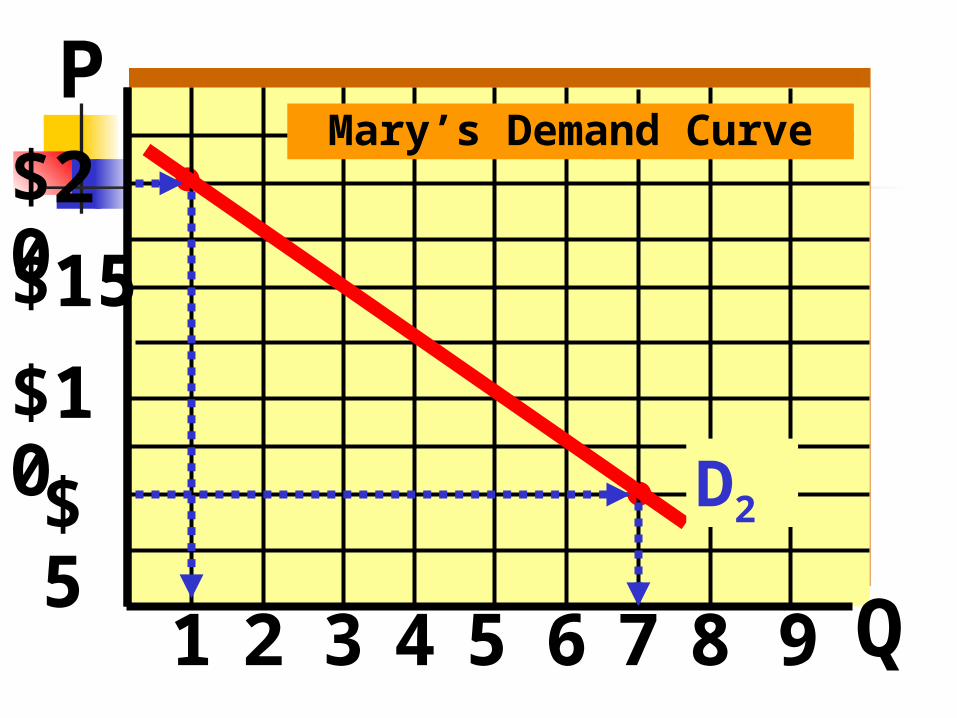

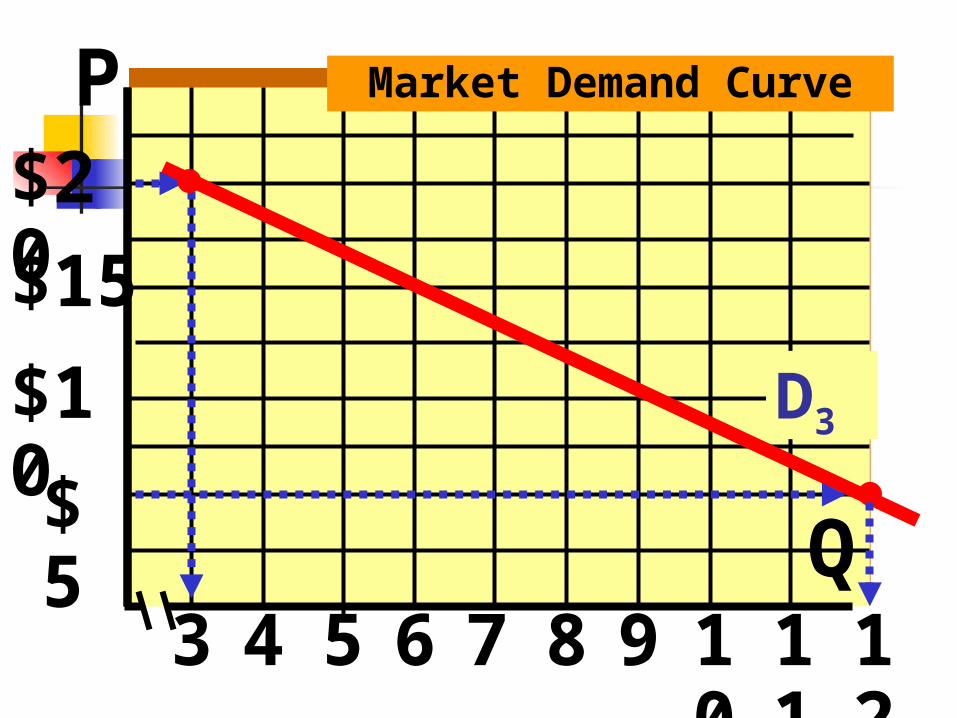

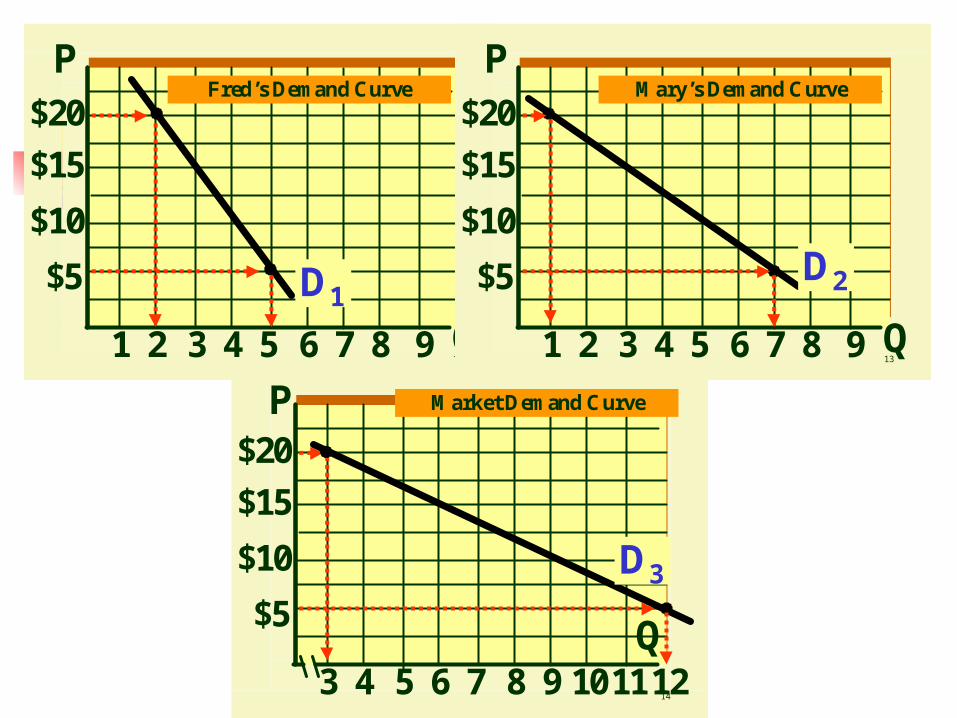

$25 1 + 0 = 1

$20 2 1 3

$15 3 3 6

$10 4 5 9

$5 5 7 12

Price Fred Mary Total Demanded

Market Demand Schedule for Compact Discs per year

$20

$15

$10

$5

1 2 3 4

P

Q5 6 7 8 9

Fred’s Demand Curve

D1

$20

$15

$10

$5

1 2 3 4

P

Q5 6 7 8 9

Mary’s Demand Curve

D2

$20

$15

$10

$5

3 4 5 6

P

Q7 8 9 1011

Market Demand Curve

D3

12

12

$20

$15

$10

$5

1 2 3 4

P

Q5 6 7 8 9

Fred’s Demand Curve

D1

13

$20

$15

$10

$5

1 2 3 4

P

Q5 6 7 8 9

Mary’s Demand Curve

D2

14

$20

$15

$10

$5

3 4 5 6

P

Q7 8 9 1011

Market Demand Curve

D3

12

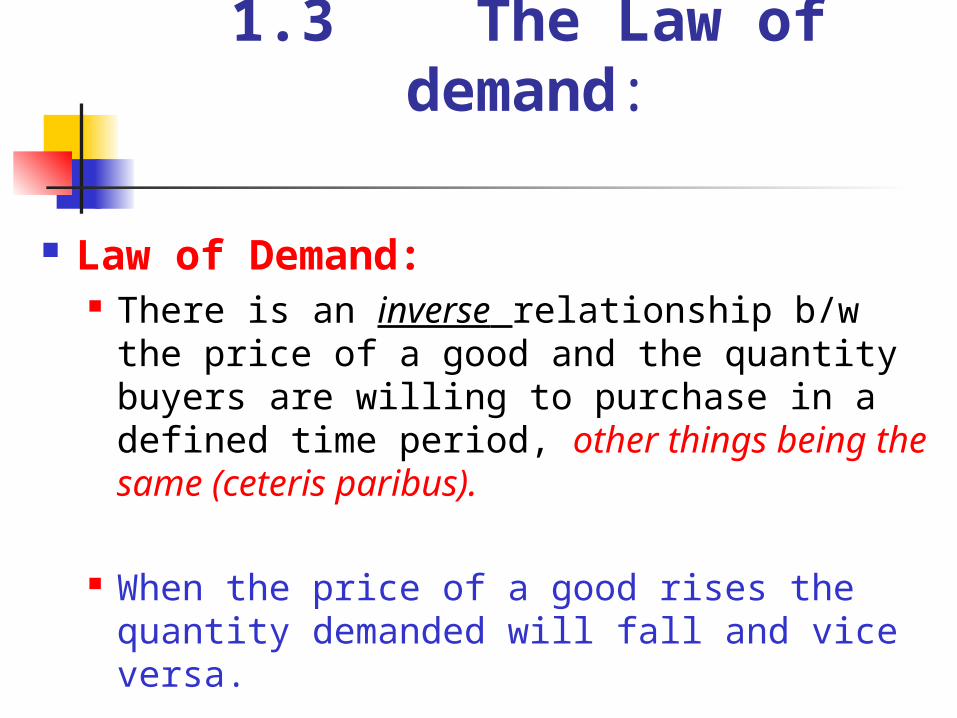

1.3 The Law of demand:

Law of Demand: There is an inverse relationship b/w the

price of a good and the quantity buyers are willing to purchase in a defined time period, other things being the same (ceteris paribus).

When the price of a good rises the quantity demanded will fall and vice versa.

1.3 Law of demand

Reasons for inverse relationship: Income effect: ↑P=> ↓ Real income => ↓ Purchasing power

=> ↓ Qd Substitution effect: ↑P => the good becomes relatively more

expensive => consumers switch to other products => ↓ Qd

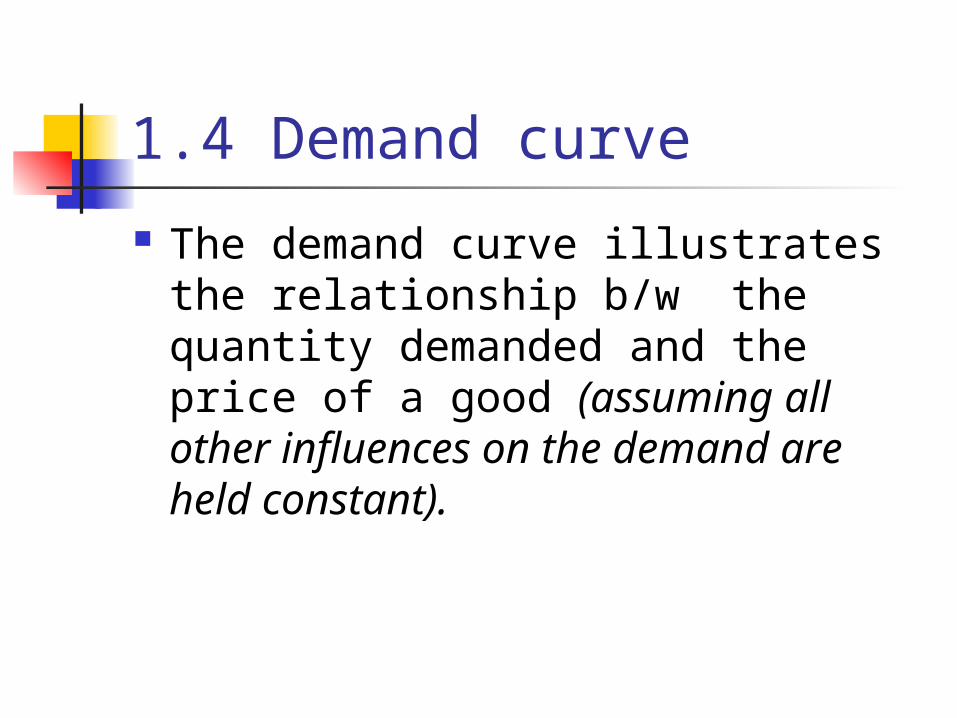

1.4 Demand curve

The demand curve illustrates the relationship b/w the quantity demanded and the price of a good (assuming all other influences on the demand are held constant).

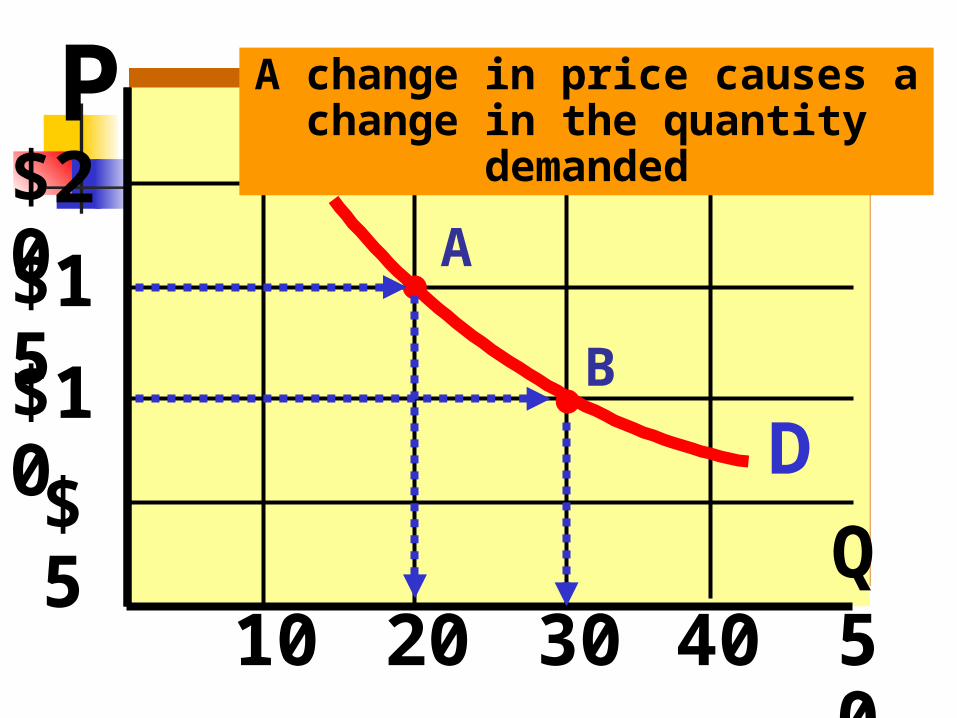

IMPORTANT - KNOW THE DIFFERENCE BETWEEN A CHANGE IN THE QUANTITY DEMANDED AND A CHANGE IN DEMAND

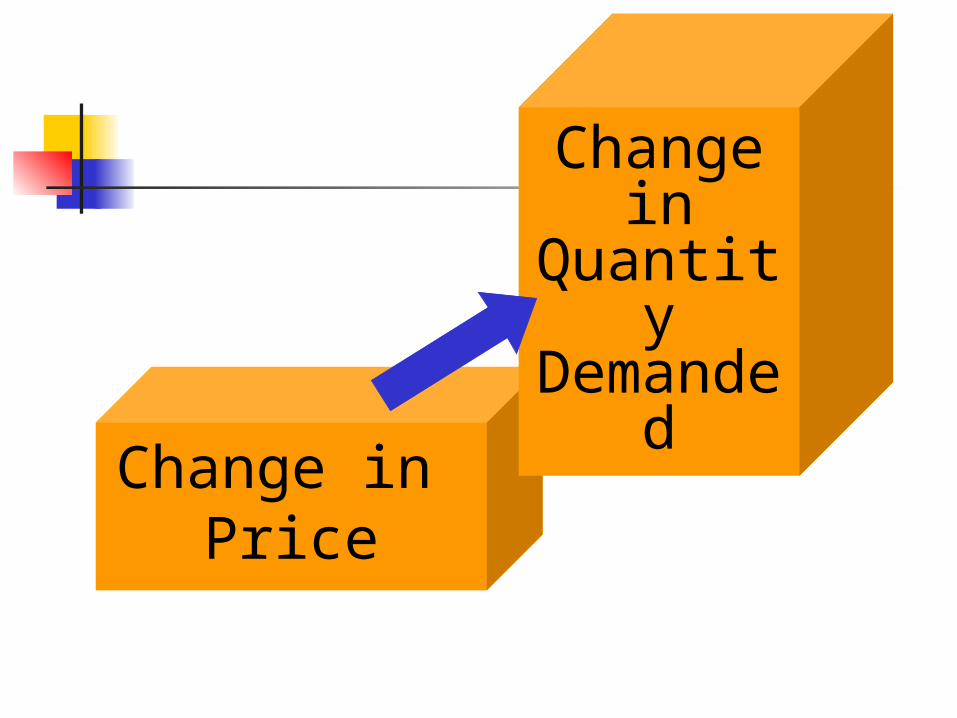

When price changes, what happens?

The curve does not shift - there is a change in the

quantity demanded

Change in Price

Change in Quantity

Demanded

$20

$15

$10

$5

10 20 30 40

A

B

A change in price causes a change in the quantity

demanded

D

P

Q50

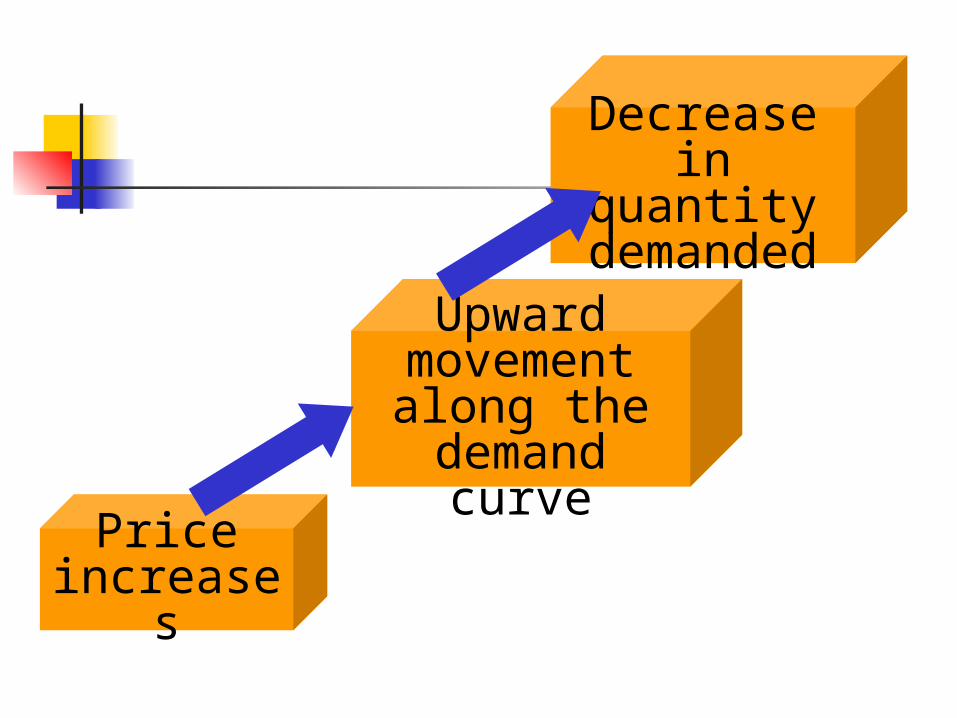

Price increases

Upward movement along the

demand curve

Decrease in quantity

demanded

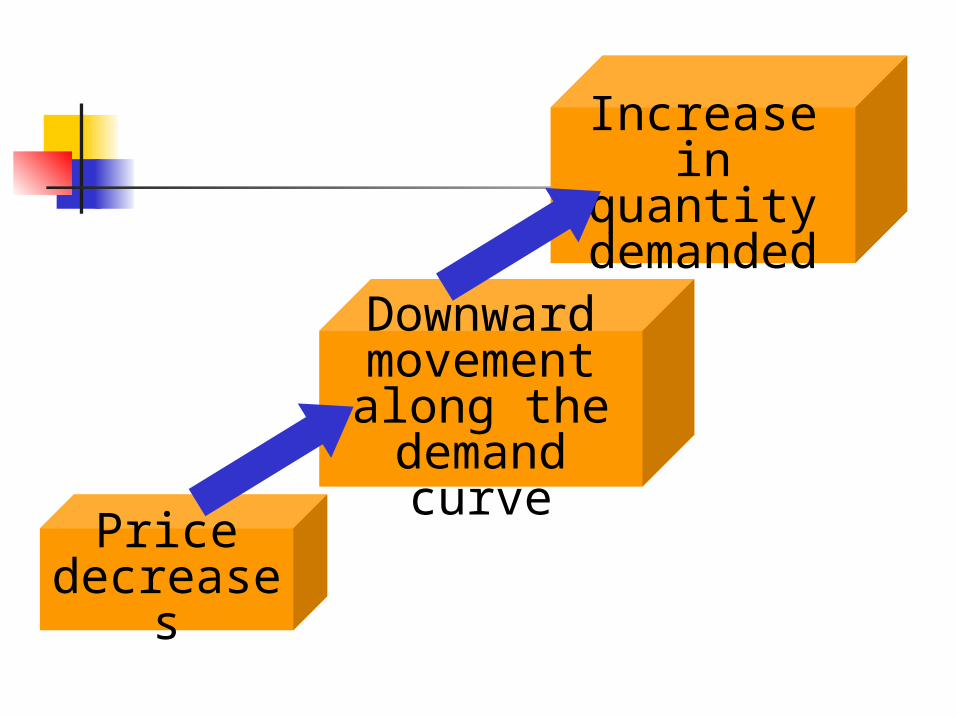

Price decreases

Downward movement along the

demand curve

Increase in quantity

demanded

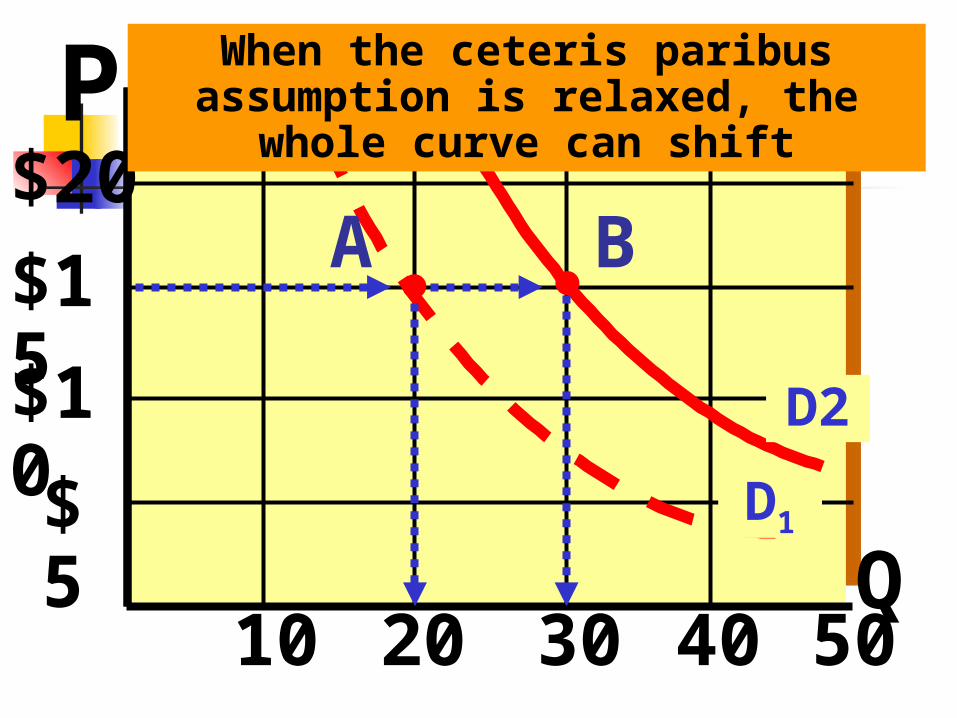

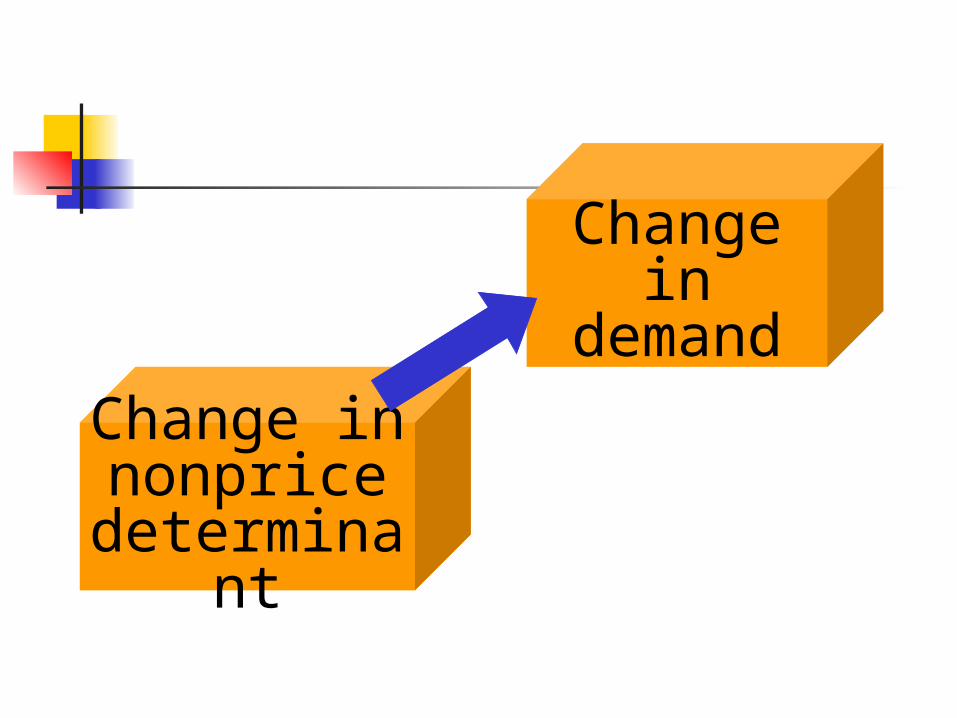

When something changes other than price, what happens?

The whole curve shifts,there is a

change in demand

$20

$15

$10

$5

10 20 30 40

D1

D2

P

50

A

When the ceteris paribus assumption is relaxed, the whole curve can shift

Q

B

Change innonprice

determinant

Change in demand

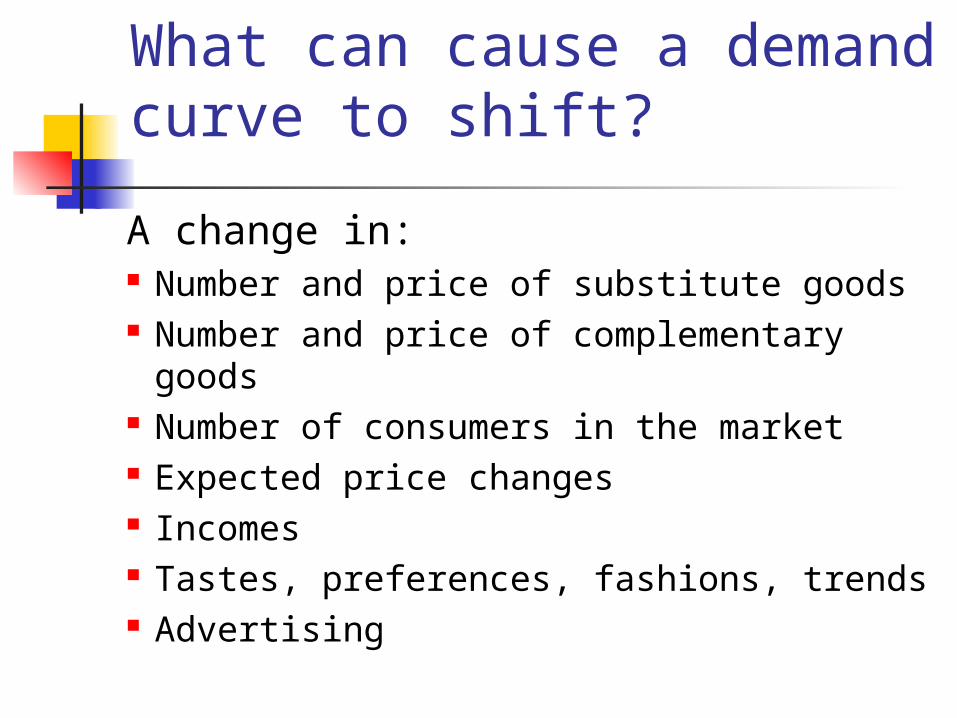

What can cause a demand curve to shift?

A change in: Number and price of substitute goods Number and price of complementary

goods Number of consumers in the market Expected price changes Incomes Tastes, preferences, fashions, trends Advertising

Shift in Demand Curve

P

Price

0 Q0 Q1

D0 D1

QuantityQ2

Decrease Increase

A change in demand results from a change in one or more of determinants of demand, other than the price of the goods.

A change in demand can be represented

by a shift in the position of the demand curve.

Some definitions… Substitute goods are good that can be

used in place of another good (eg. Coke & Pepsi)

Complementary goods are goods that are used in conjunction with each other (eg. Bread and butter)

Normal goods are goods whose demand varies directly with income (also known as superior goods)

Inferior goods are goods whose demand varies inversely with income

1.4 Psychological (or non-functional) factors affecting demand:

Bandwagon effect Everyone is doing it, so will I

Snob effect Not everyone can do it, so I will

Conspicuous consumption Let everyone see how much

money I have

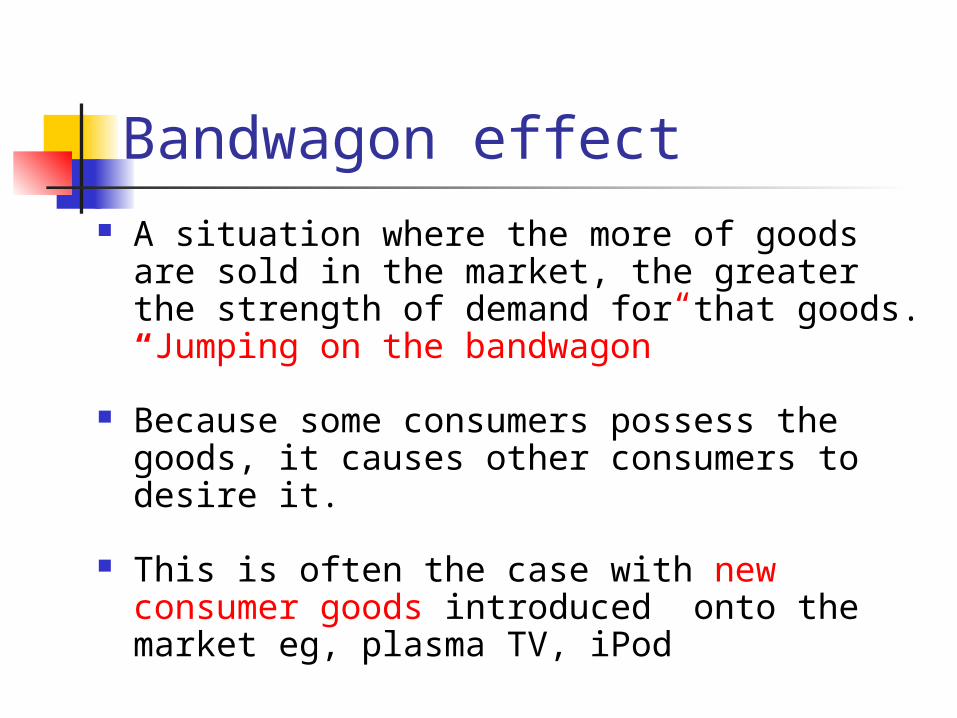

Bandwagon effect A situation where the more of goods are sold

in the market, the greater the strength of demand for that goods. “Jumping on the bandwagon”

Because some consumers possess the goods, it causes other consumers to desire it.

This is often the case with new consumer goods introduced onto the market eg, plasma TV, iPod

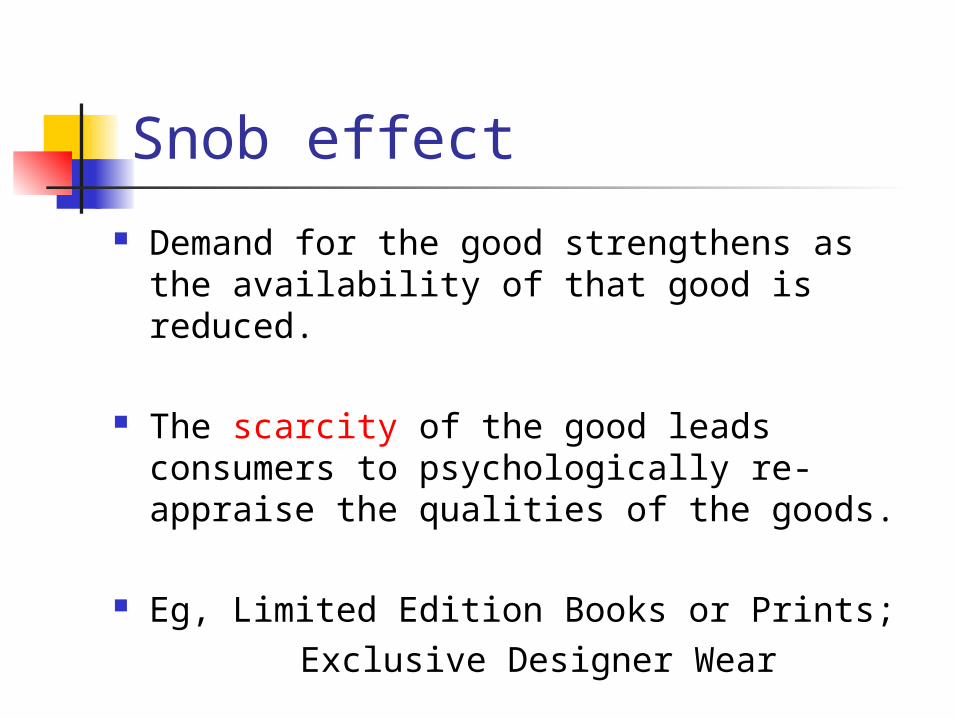

Snob effect

Demand for the good strengthens as the availability of that good is reduced.

The scarcity of the good leads consumers to psychologically re-appraise the qualities of the goods.

Eg, Limited Edition Books or Prints; Exclusive Designer Wear

Conspicuous consumption Where the consumers valuation of the good is

influenced by the price of goods in the market.

Satisfaction is gained not only from the good itself, but also from being seen to be able to afford it.

This may be the case with such prestige items such as paintings, or expensive clothes and cars.

2. What is Supply ?

No. of units of a good or service firms are willing and able to produce during a period, under a given set of conditions

2.2 Law of Supply

There is a direct relationship between the price of a good and the quantity sellers are willing to offer for sale in a defined time period, ceteris paribus

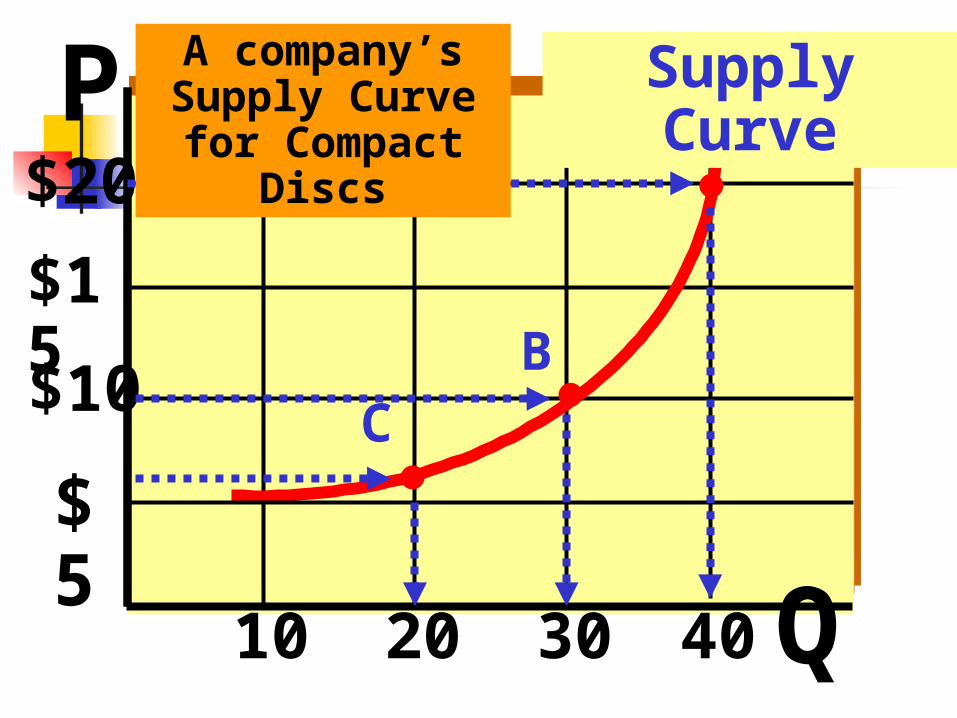

2.1 Supply curve

Supply curve: The supply curve shows the

relationship between quantity supplied & price, other things being the same (citeris paribus)

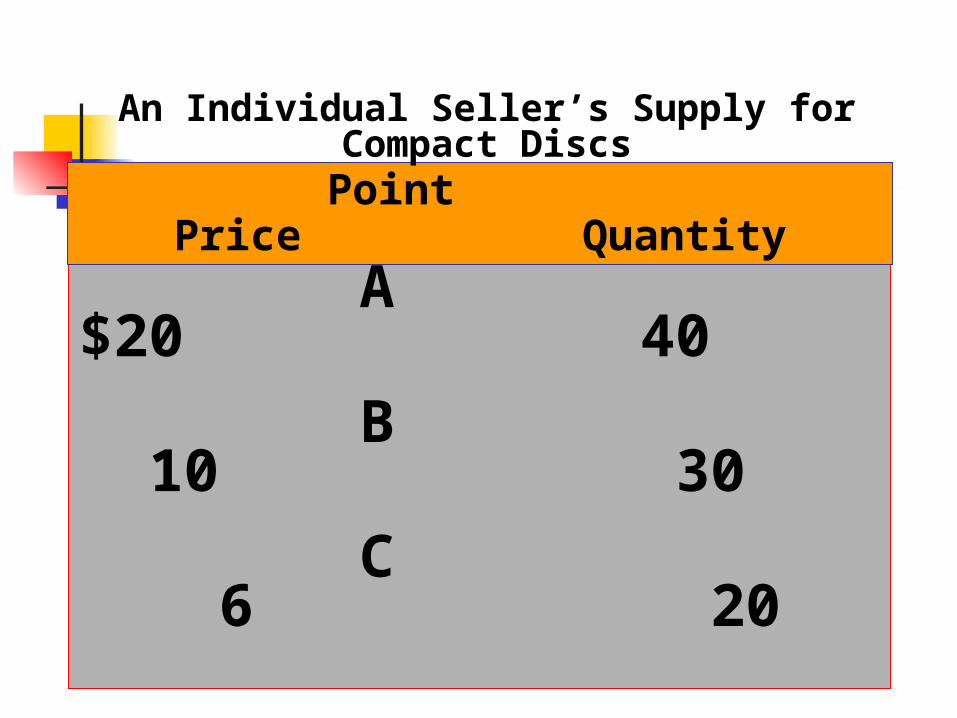

A $20 40

B 10 30

C 6 20

Point Price Quantity

An Individual Seller’s Supply for Compact Discs

$20

$15

$10

$5

10 20 30 40

A

BC

Supply CurveA company’s Supply Curve for Compact Discs

P

Q

Why do supply curves have a positive slope?

A higher price means more profitable to suppliers/sellers.

Therefore, they will supply more of the good or service.

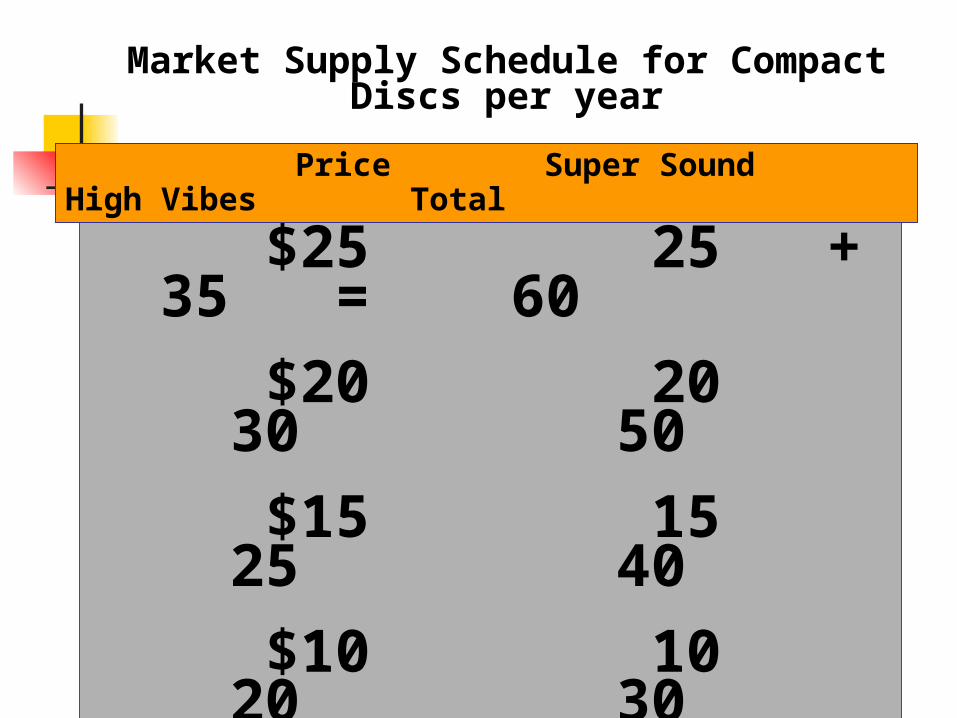

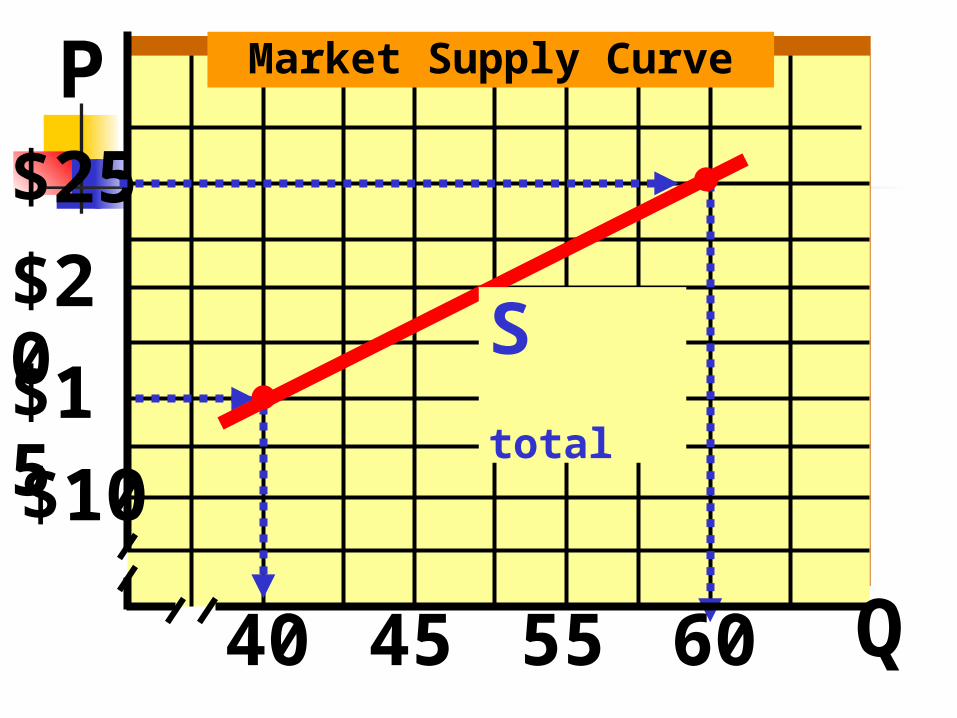

$25 25 + 35 = 60

$20 20 30 50

$15 15 25 40

$10 10 20 30

$5 5 15 20

Price Super Sound High Vibes Total

Market Supply Schedule for Compact Discs per year

$25

$20

$15

$10

10

P

Q15 20

Super Sound Supply Curve

S1

25

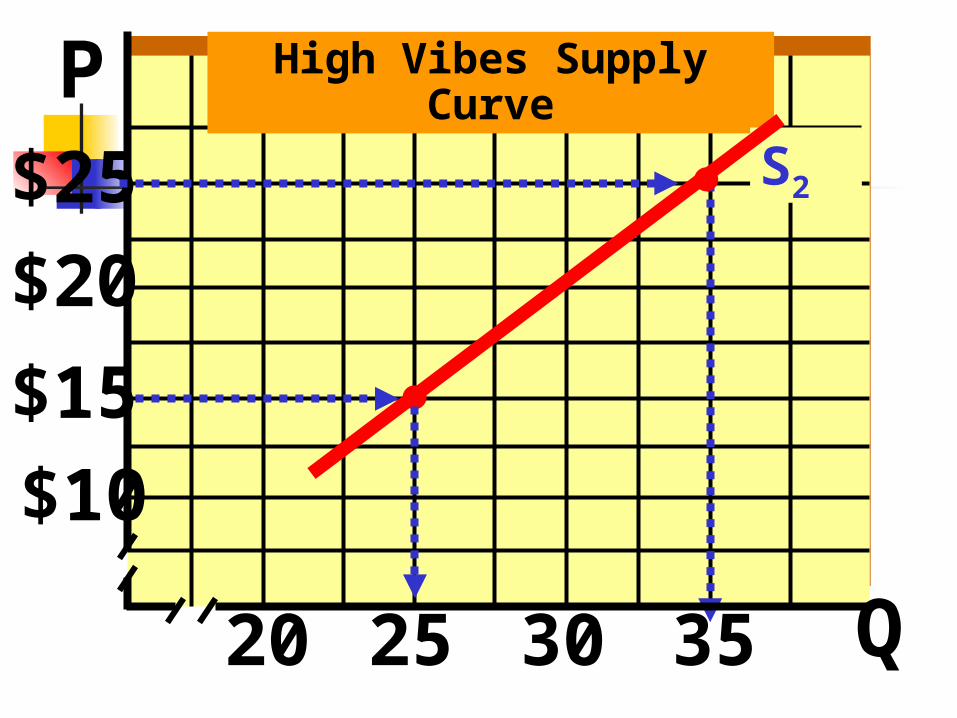

$25

$20

$15

$10

20

P

Q25 30

High Vibes Supply Curve

S2

35

$25

$20

$15

$10

40

P

Q45 55

Market Supply Curve

60

S total

IMPORTANT - KNOW THE DIFFERENCE BETWEEN A CHANGE IN THE QUANTITY SUPPLIED AND A CHANGE IN SUPPLY

When price changes, what happens?

The curve does not shift - there is a change in the

quantity supplied

$20

$15

$10

$5

10 20 30 40

A

B

C

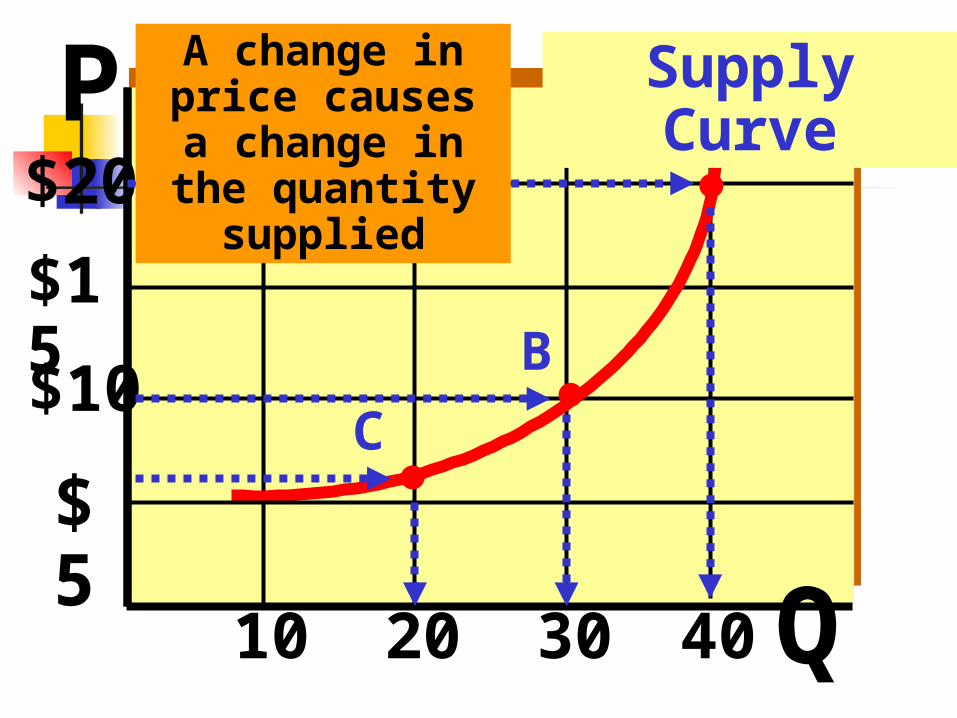

Supply CurveA change in price causes a change

in the quantity supplied

P

Q

Change in Price

Change in Quantity Supplied

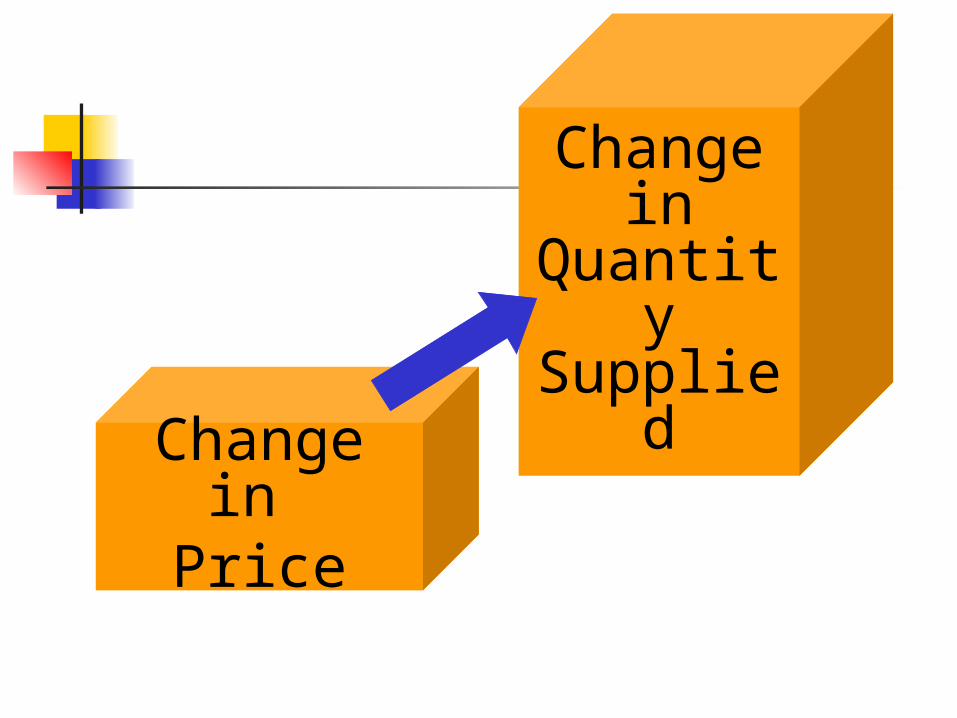

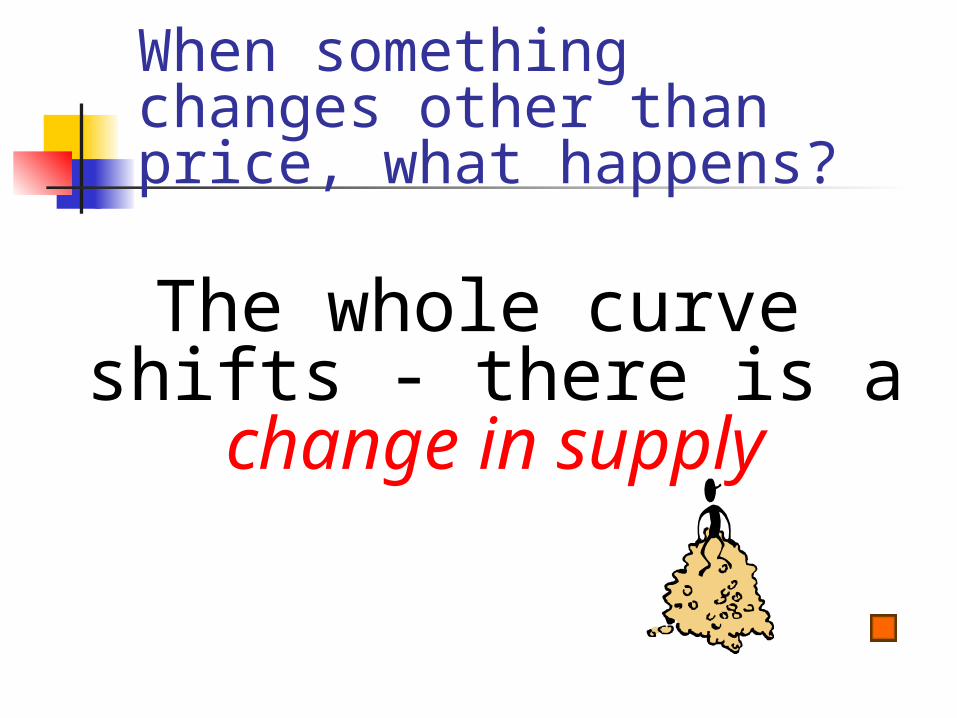

When something changes other than price, what happens?

The whole curve shifts - there is a change in

supply

$20

$15

$10

$5

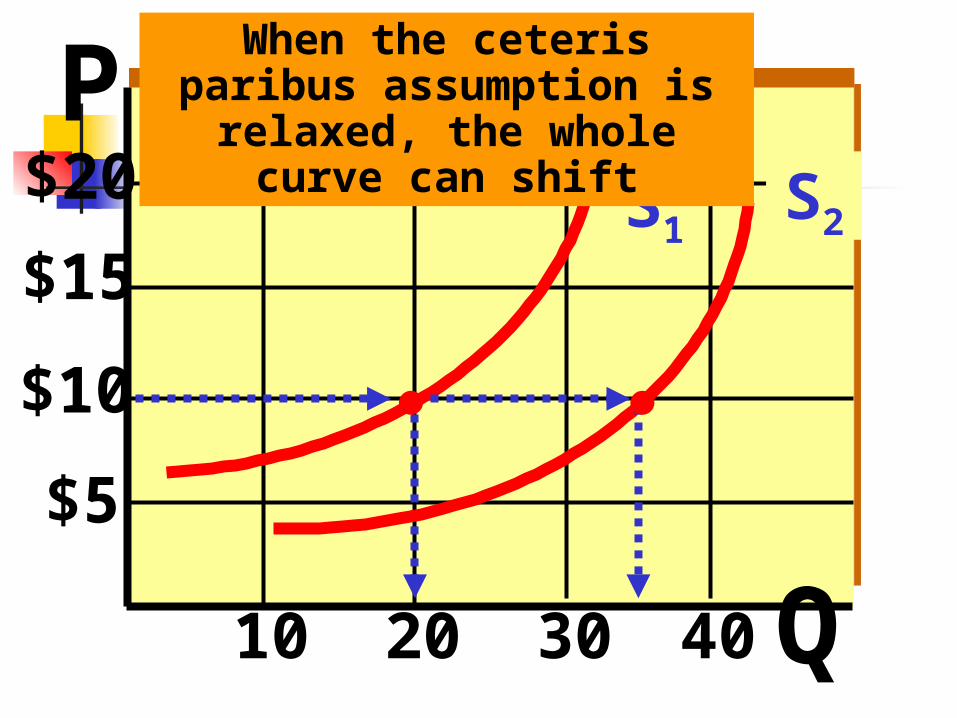

10 20 30 40

S1S2

When the ceteris paribus assumption is relaxed, the

whole curve can shiftP

Q

Change innonprice

determinant

Change in supply

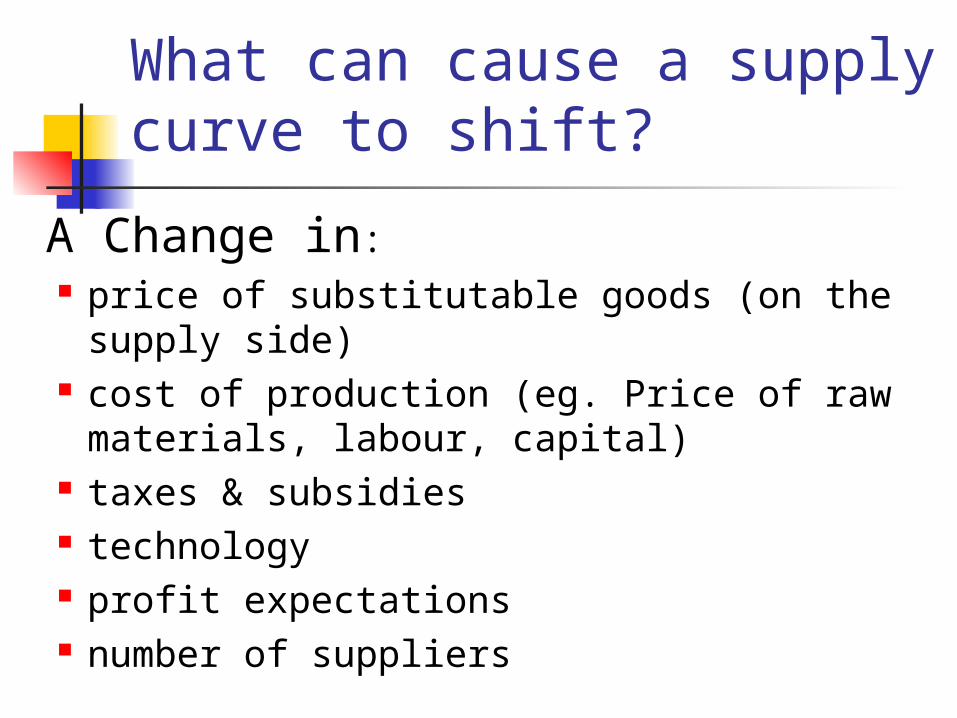

What can cause a supply curve to shift?

A Change in: price of substitutable goods (on the supply

side) cost of production (eg. Price of raw

materials, labour, capital) taxes & subsidies technology profit expectations number of suppliers

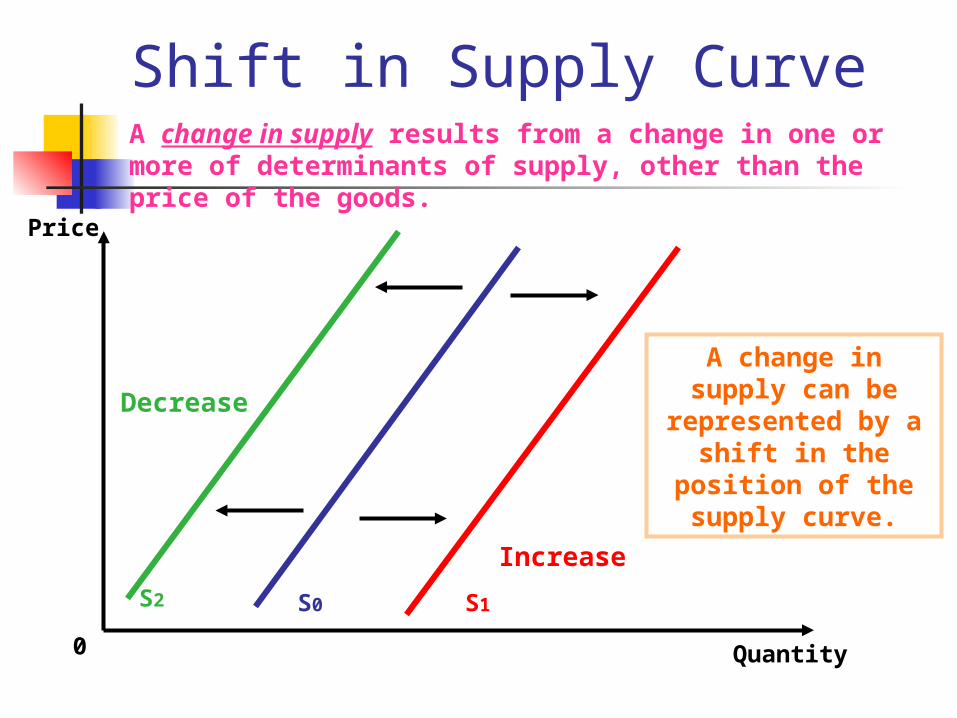

Shift in Supply Curve

Price

0

S0 S1

Quantity

Increase

Decrease

S2

A change in supply results from a change in one or more of determinants of supply, other than the price of the goods.

A change in supply can be

represented by a shift in the

position of the supply curve.

3. Market equilibrium

The point where quantity demanded equals quantity supplied

Market forces keep the price at equilibrium (how?)

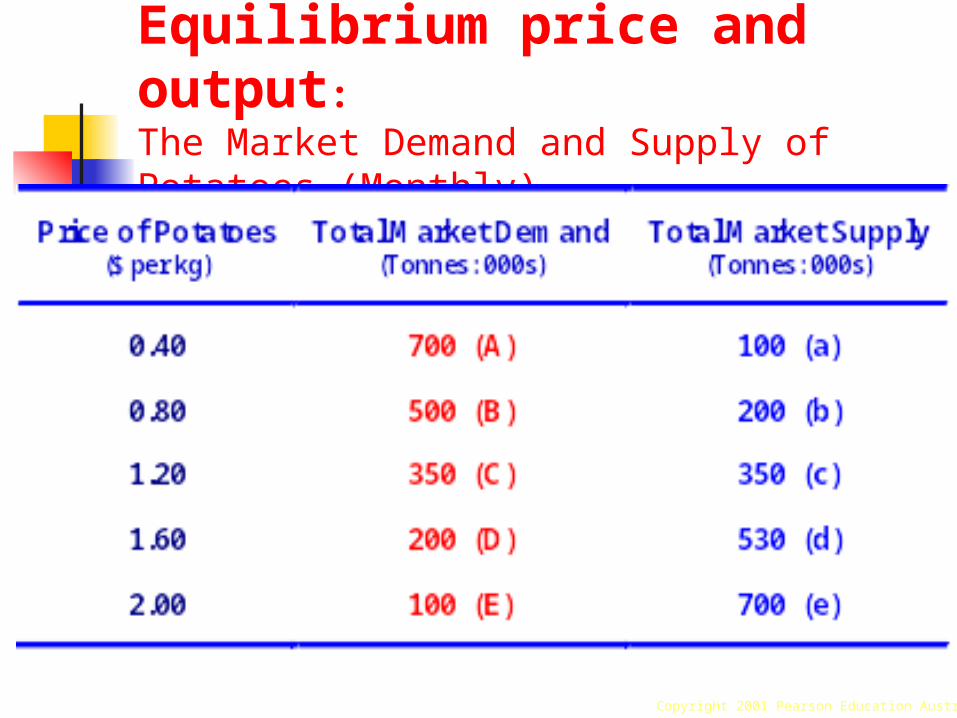

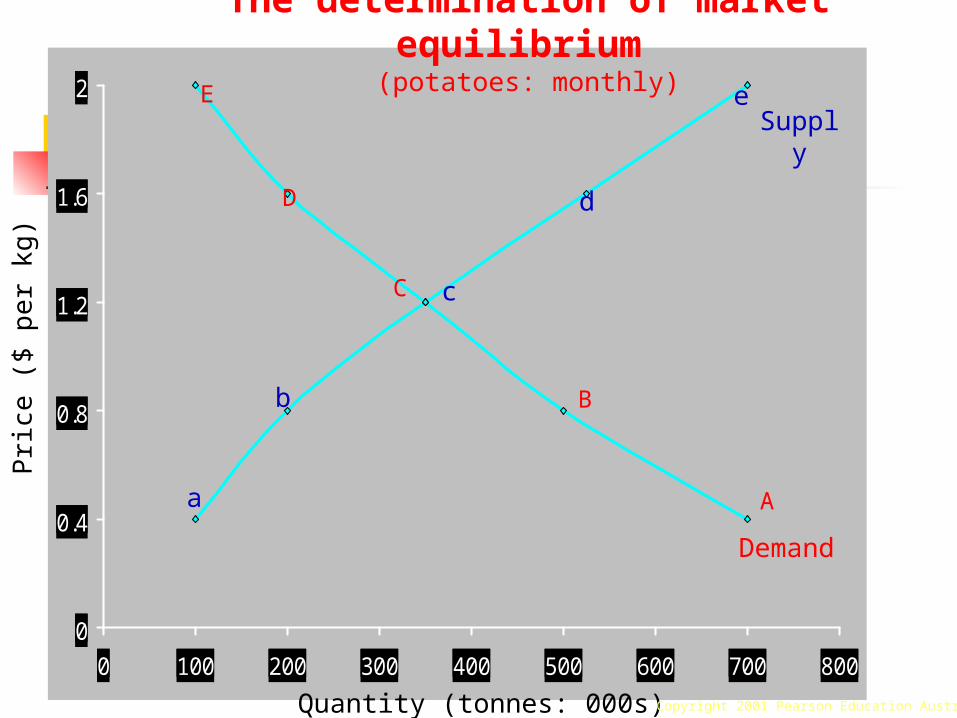

Equilibrium price and output:The Market Demand and Supply of Potatoes (Monthly)

Copyright 2001 Pearson Education Australia

fig

0

0.4

0.8

1.2

1.6

2

0 100 200 300 400 500 600 700 800

The determination of market equilibrium (potatoes: monthly)

Quantity (tonnes: 000s)

Pri

ce (

$ p

er

kg)

E

D

C

B

Aa

b

c

d

eSupply

Demand

Copyright 2001 Pearson Education Australia

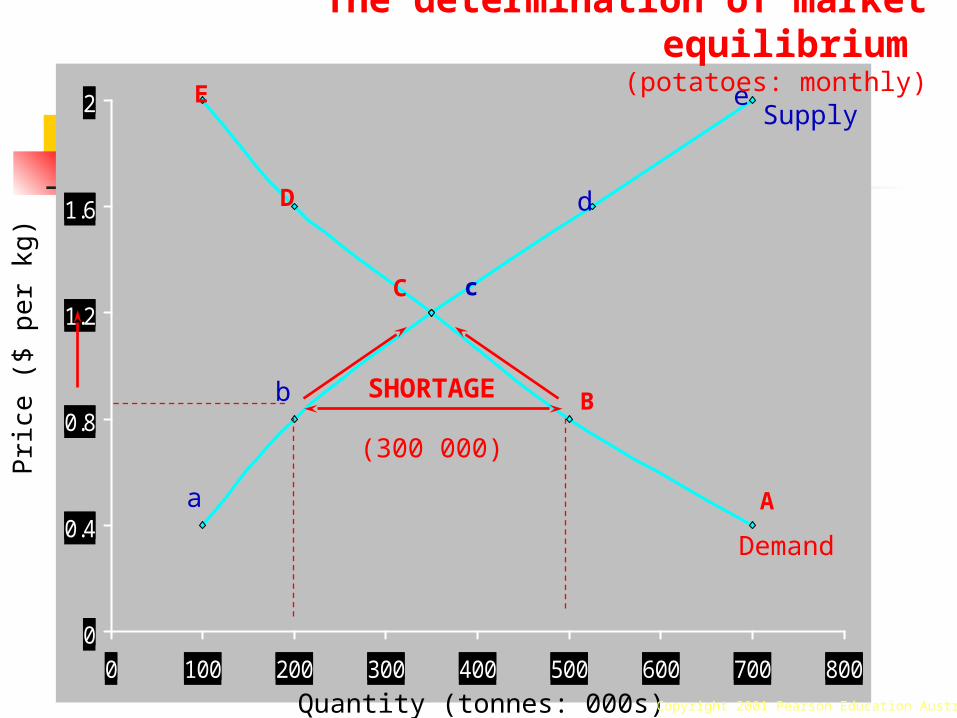

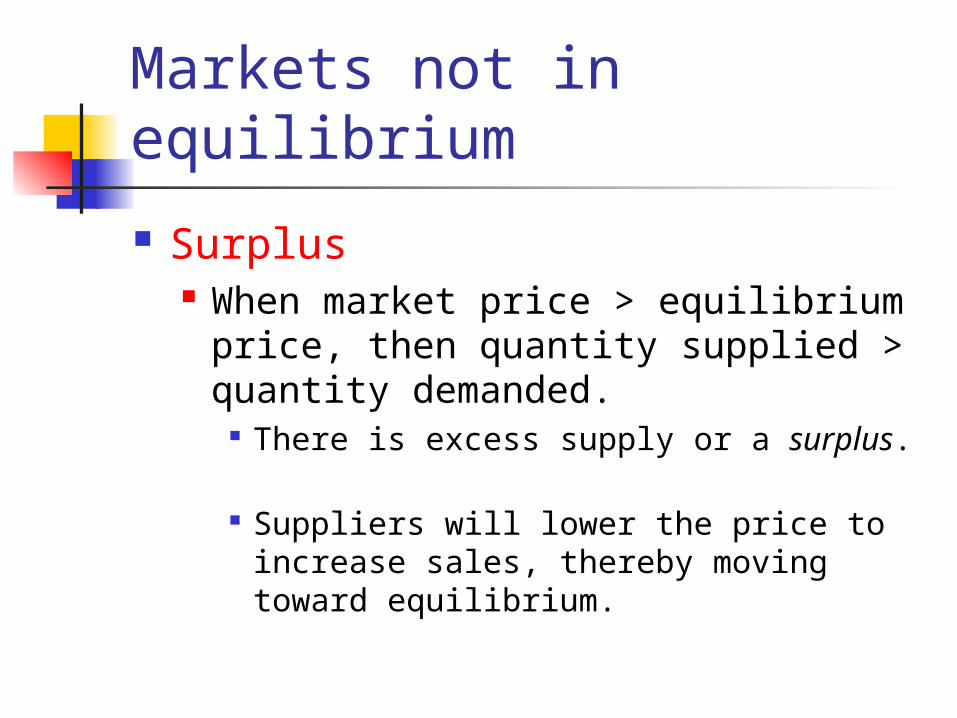

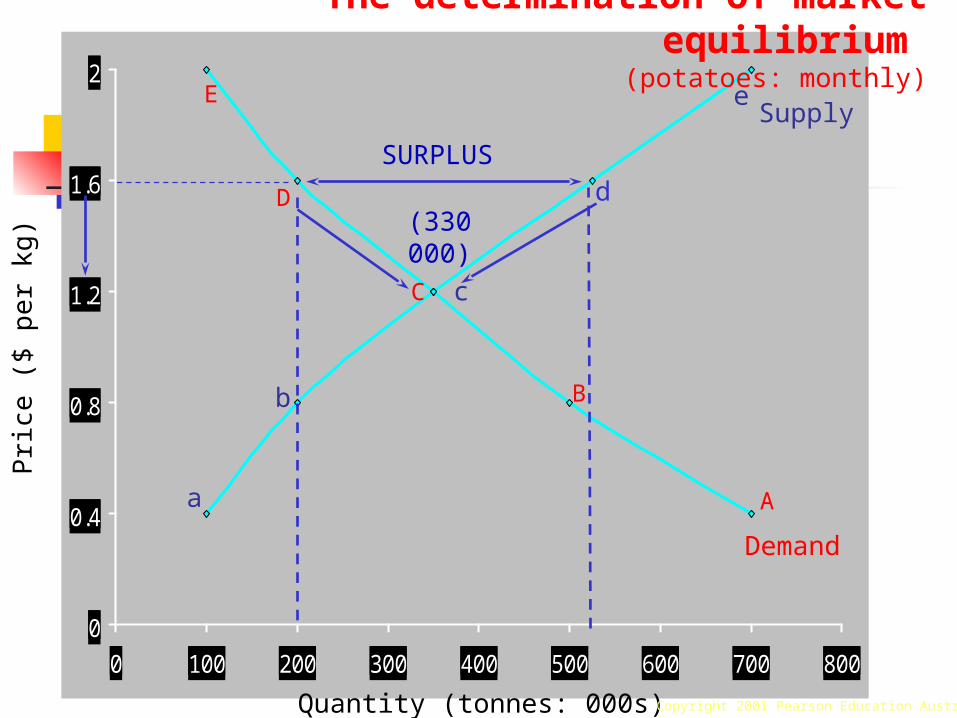

Markets not in equilibrium

Shortage When market price < equilibrium

price, then quantity demanded > the quantity supplied.

There is excess demand or a shortage. Suppliers will raise the price due to too

many buyers chasing too few goods, thereby moving toward equilibrium.

fig

0

0.4

0.8

1.2

1.6

2

0 100 200 300 400 500 600 700 800

Quantity (tonnes: 000s)

Pri

ce (

$ p

er

kg)

E

D

C

B

Aa

b

d

eSupply

Demand

SHORTAGE

(300 000)

The determination of market equilibrium

(potatoes: monthly)

Copyright 2001 Pearson Education Australia

c

Markets not in equilibrium

Surplus When market price > equilibrium

price, then quantity supplied > quantity demanded.

There is excess supply or a surplus. Suppliers will lower the price to increase

sales, thereby moving toward equilibrium.

fig

0

0.4

0.8

1.2

1.6

2

0 100 200 300 400 500 600 700 800

Quantity (tonnes: 000s)

Pri

ce (

$ p

er

kg)

E

D

C

B

Aa

b

c

d

e

SURPLUS

(330 000)

Supply

Demand

The determination of market equilibrium

(potatoes: monthly)

Copyright 2001 Pearson Education Australia

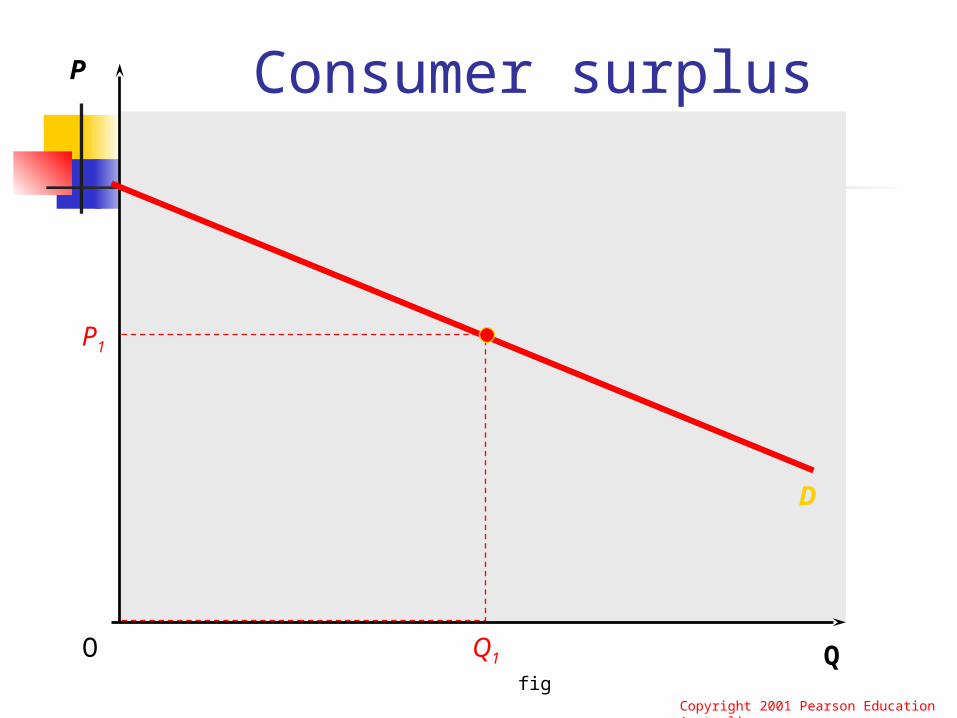

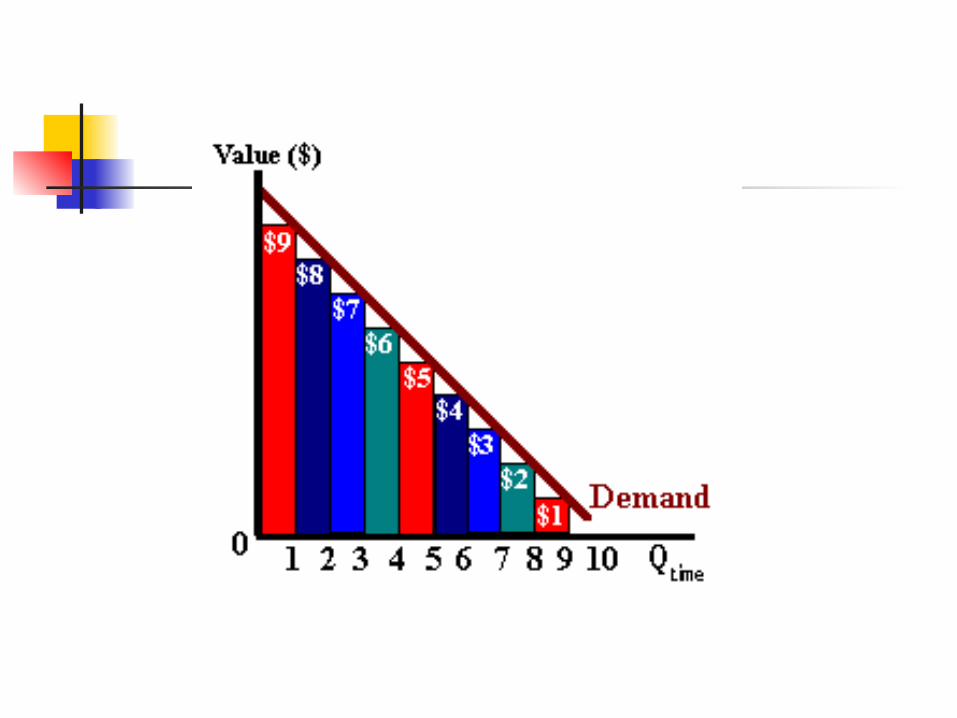

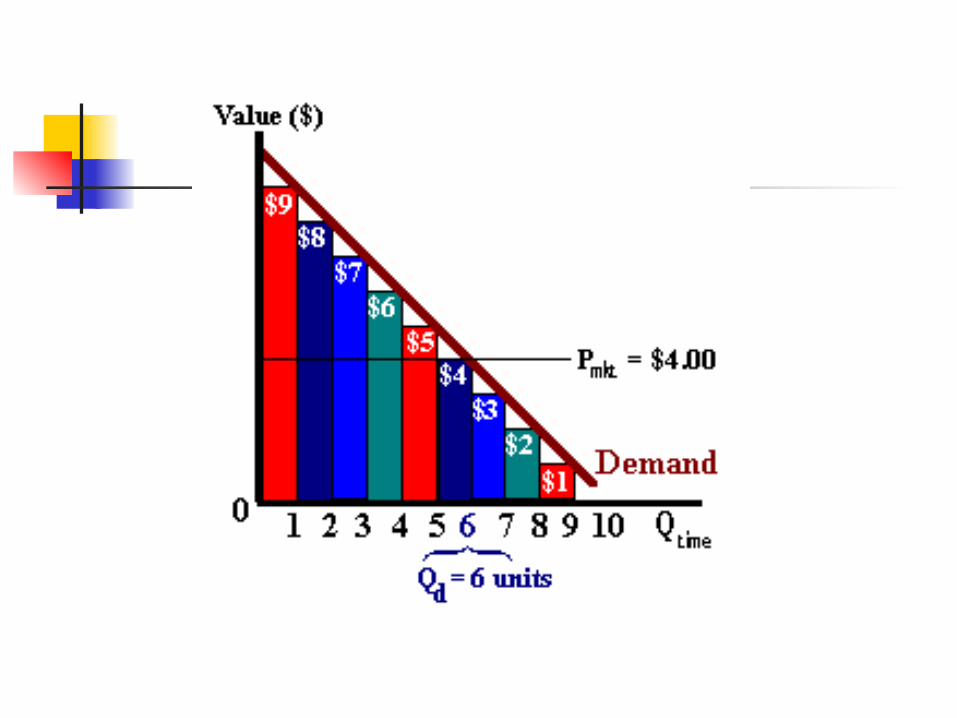

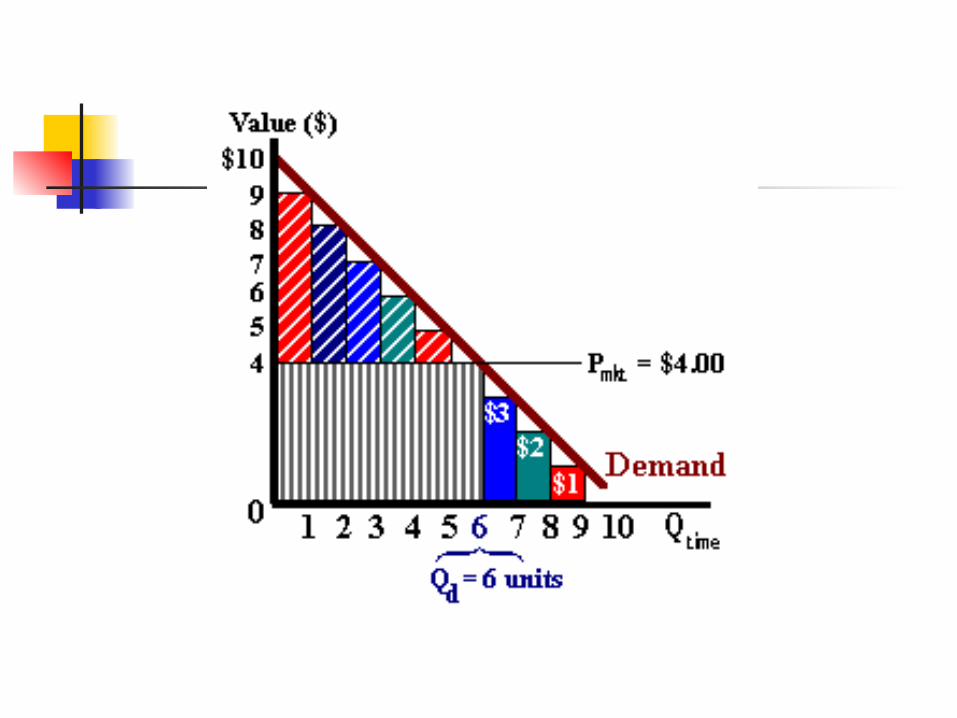

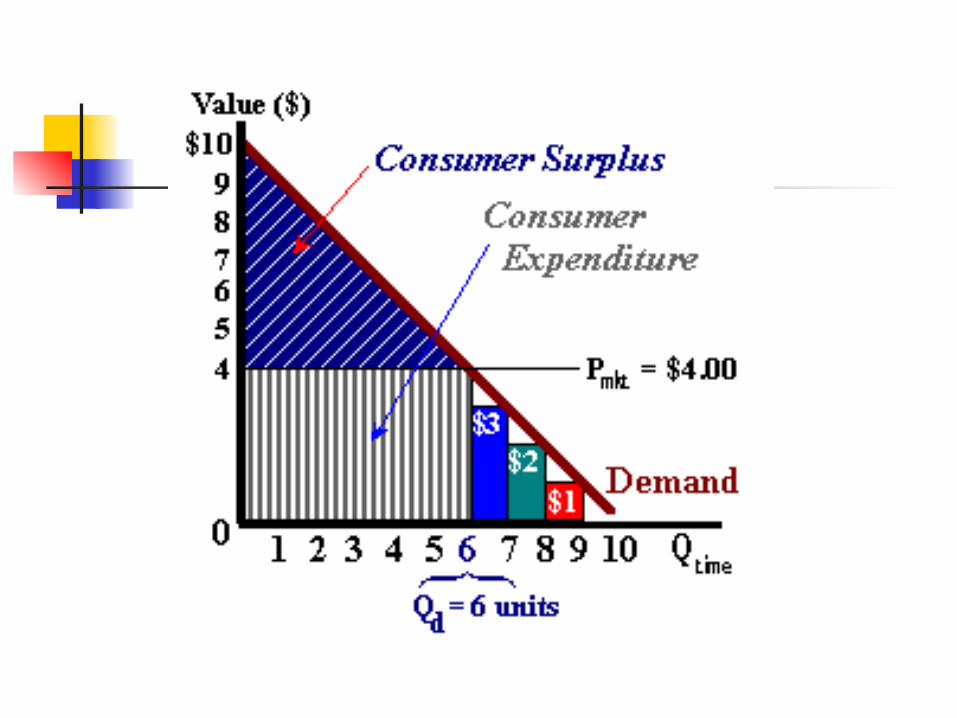

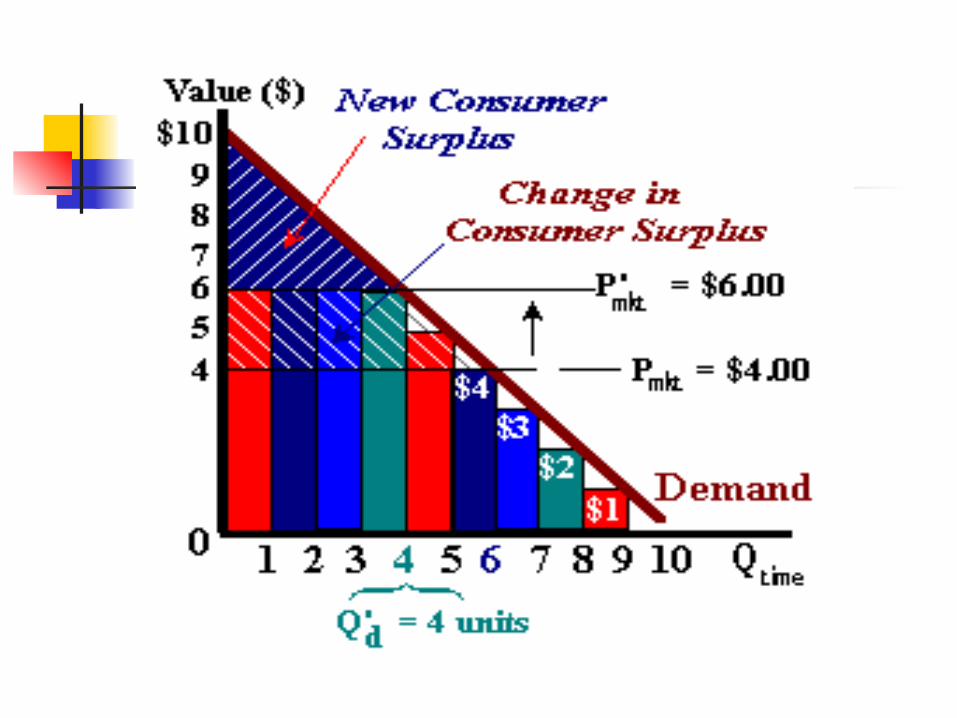

4. 1 Consumer Surplus

the difference between what the consumers are willing to pay (shown on the demand curve)

and what they actually pay (the market price)

In other words, Consumer surplus is the area between the Demand curve and the Price line

fig

Consumer surplus

D

P1

Q1

P

QO

Copyright 2001 Pearson Education Australia

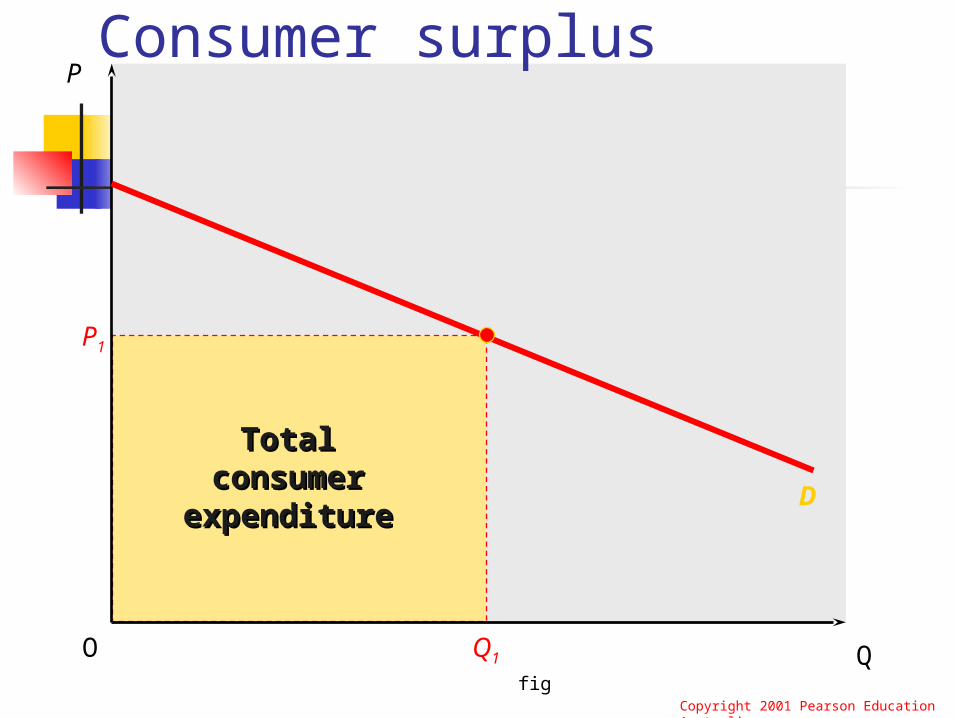

fig

Consumer surplus

D

TotalTotalconsumerconsumer

expenditureexpenditure

P1

Q1

P

QO

Copyright 2001 Pearson Education Australia

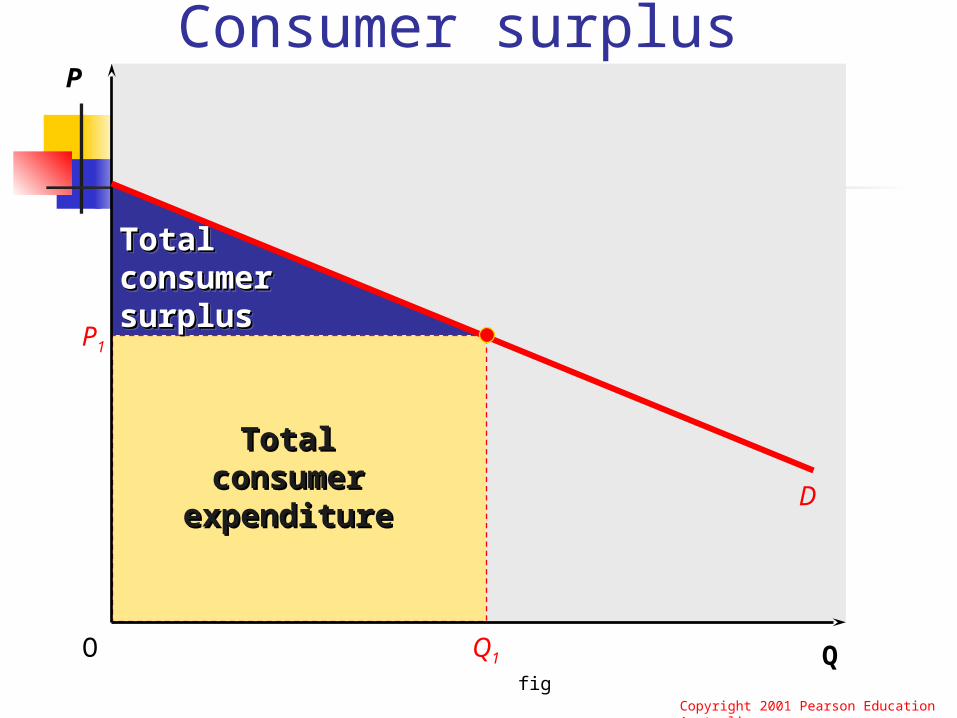

fig

Consumer surplus

D

TotalTotalconsumerconsumer

expenditureexpenditure

TotalTotalconsumerconsumersurplussurplus

TotalTotalconsumerconsumersurplussurplus

P1

Q1

P

QO

Copyright 2001 Pearson Education Australia

Consumer Surplus

CS is the area between the demand curve and the market price line.

It measures how much the consumer gains from buying goods in the market

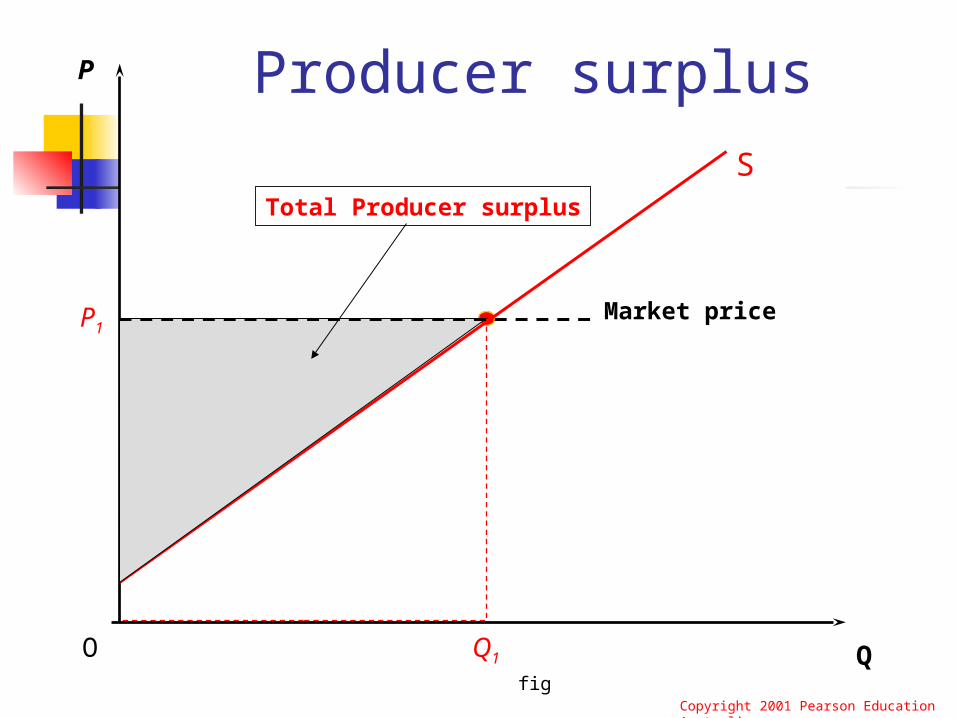

4.2 Producer surplus

the amount producers receive (market price)

above the minimum price required to make them supply the good (shown on the supply curve)

Producer surplus is the area between the Price line and the Supply curve

fig

Producer surplus

P1

Q1

P

QO

Copyright 2001 Pearson Education Australia

S

Producer Surplus

Total Producer surplus

Market price

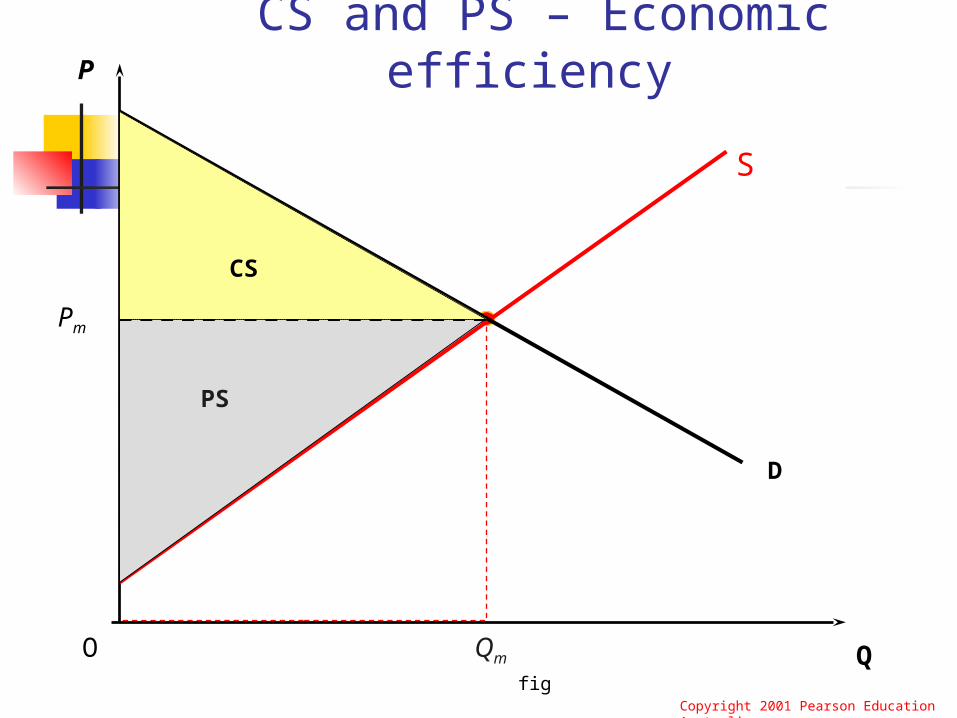

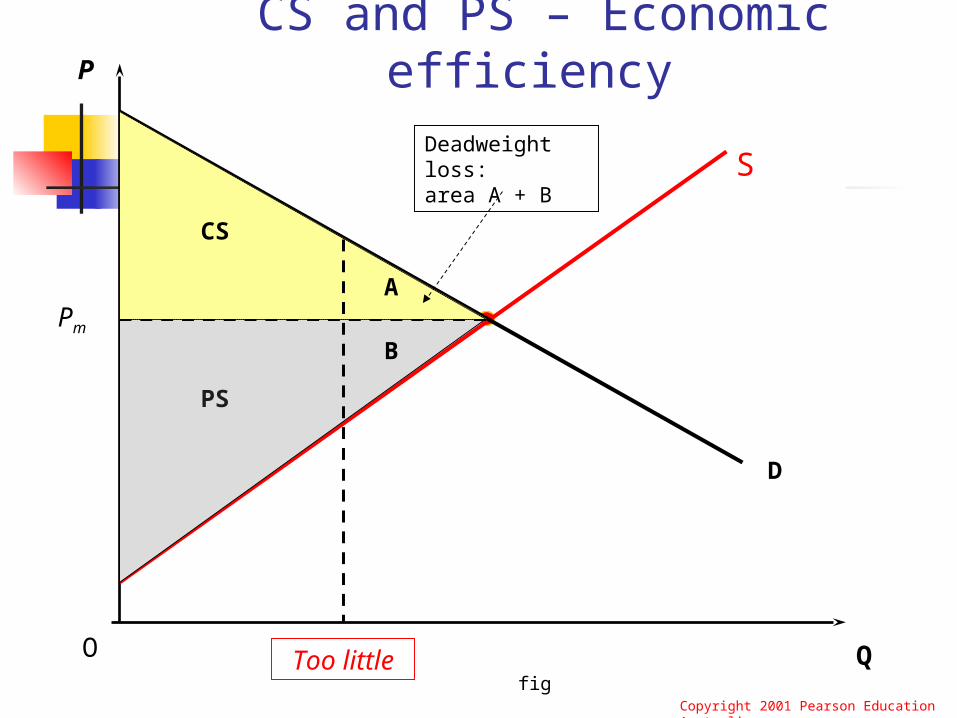

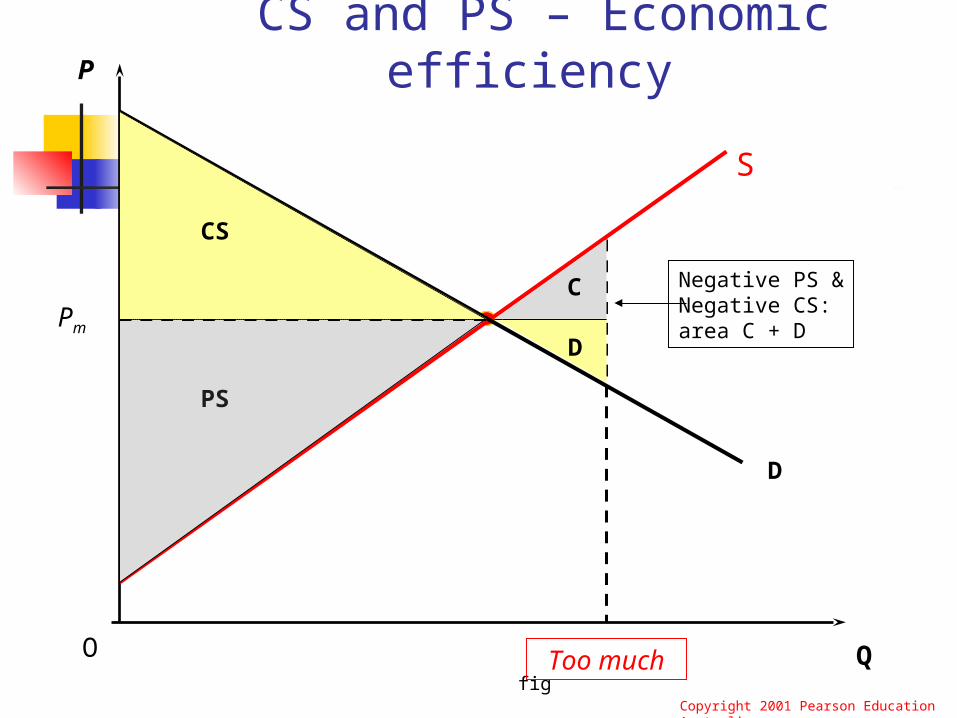

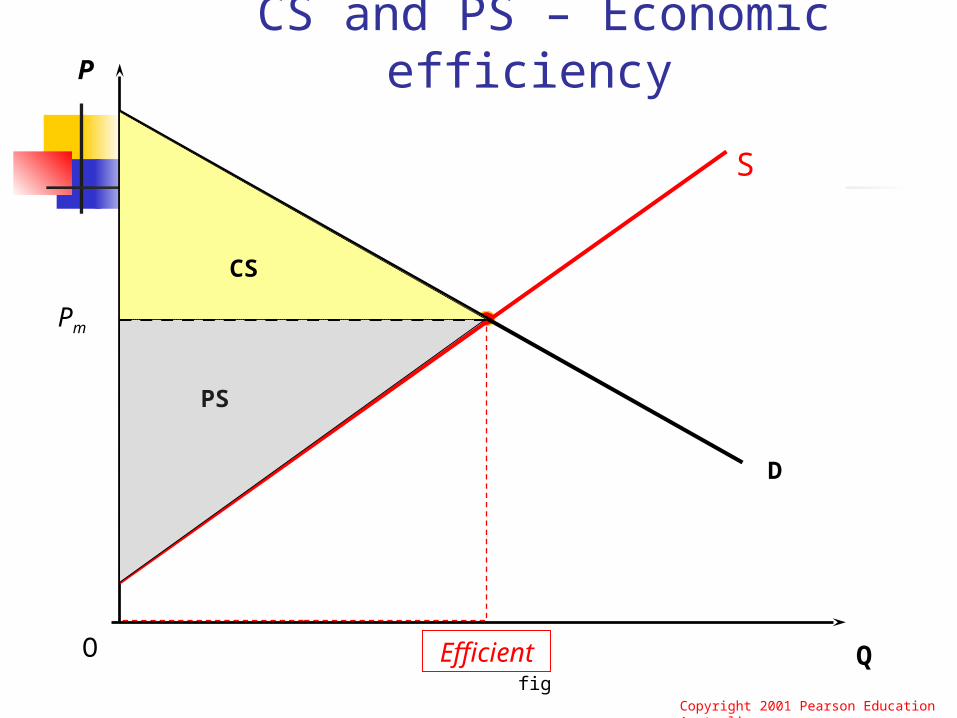

4.3 CS and PS – Economic efficiency

CS and PS are an important tool for measuring the performance of an economic system

or for assessing the impact of alternative government policies in that system.

fig

CS and PS – Economic efficiency

Pm

Qm

P

QO

Copyright 2001 Pearson Education Australia

S

Producer Surplus

PS

CS

D

fig

CS and PS – Economic efficiency

Pm

Too little

P

QO

Copyright 2001 Pearson Education Australia

S

Producer Surplus

PS

D

A

B

Deadweight loss:area A + B

CS

fig

CS and PS – Economic efficiency

Pm

Too much

P

QO

Copyright 2001 Pearson Education Australia

S

Producer Surplus

PS

D

CS

C

D

Negative PS &Negative CS:area C + D

fig

CS and PS – Economic efficiency

Pm

Efficient

P

QO

Copyright 2001 Pearson Education Australia

S

Producer Surplus

PS

CS

D